Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CONSERVING TROPICAL FORESTS FOR PEOPLE, THE ENVIRONMENT, AND

RESPONSIBLE BUSINESSES

The Benefits TFF Provides

• People who live in or near tropical forests

• The local and global environment

• Businesses that use or produce wood products

Tropical Forests are Disappearing

©earthobservatory.nasa.gov

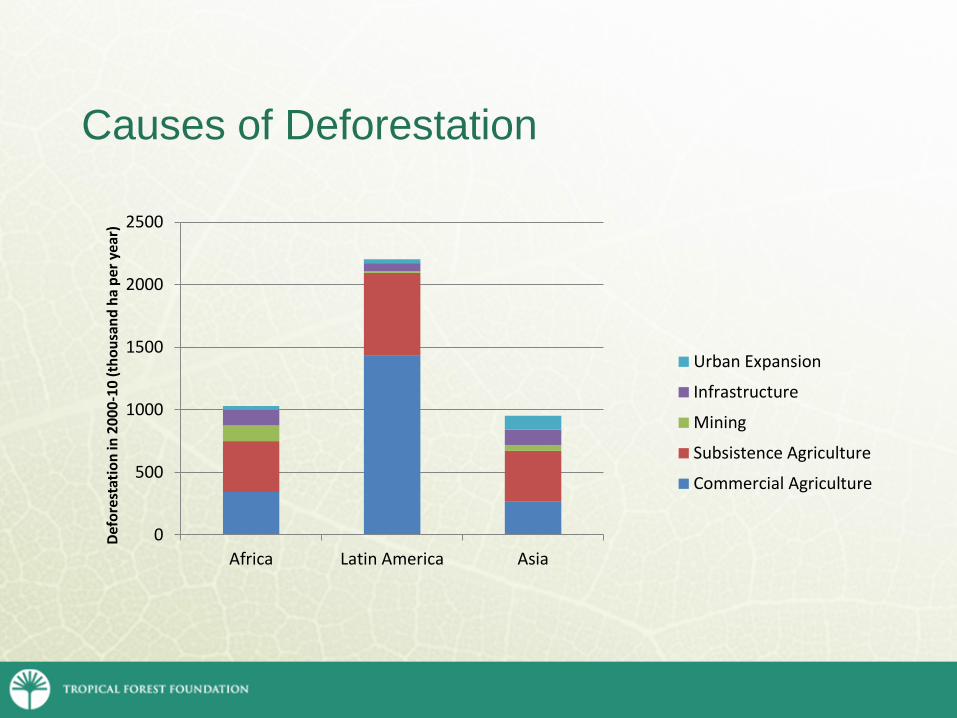

Causes of Deforestation

0

500

1000

1500

2000

2500

Africa Latin America Asia

Defo

rest

atio

n in

200

0-10

(tho

usan

d ha

per

yea

r)

Urban Expansion

Infrastructure

Mining

Subsistence Agriculture

Commercial Agriculture

Worldwide concern was rising in the 1980s regarding the rapid loss of tropical forests

Initiating Change

In 1989, a workshop was organized with experts from industry, conservation, and science. • Smithsonian Institute, Dr. Thomas Lovejoy • World Bank, Dr. Marc Dourojeanni • UNESCO, Dr. Kuswata Kartawinata • Princeton University, Dr. Stephen Hubbell • Government of Nigeria, Dr. Philip R.O. Kio • World Wildlife Fund, Robert Buschbacher • Georgia-Pacific Corporation, Walter Jarck • US Forest Service, Dr. Frank Wadsworth • Rainforest Alliance, Ivan Ussach

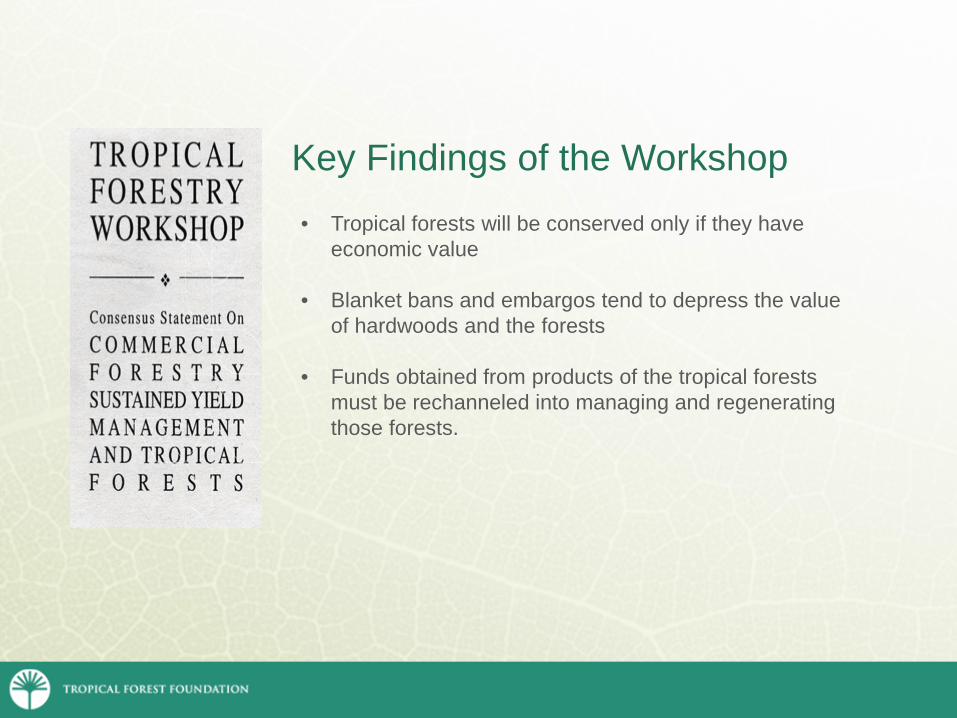

Key Findings of the Workshop

• Tropical forests will be conserved only if they have economic value

• Blanket bans and embargos tend to depress the value of hardwoods and the forests

• Funds obtained from products of the tropical forests must be rechanneled into managing and regenerating those forests.

The Tropical Forest Foundation was formed in 1990

• Continue the discussion and research

• Educate producers and users of tropical woods on these key findings

• Develop relationships among policy-makers, conservation and academic organizations, and industry.

TFF Training Centers

Defining best practices Developed the world’s standard for Reduced Impact Logging in tropical forests.

Conventional Logging Reduced Impact Logging

Improvements Achieved Through Reduced Impact Logging Practices

Measuring the avoided emissions resulting from RIL •Tropical deforestation releases 20% of greenhouse gas emissions worldwide, roughly equivalent to that released by the transportation sector • Reduced Impact Logging is mentioned specifically in the Verified Carbon Standard as a qualifying emissions reduction strategy • Methodology currently in validation to credit RIL practitioners for avoided emissions vs CL

MARKETS ARE SHIFTING

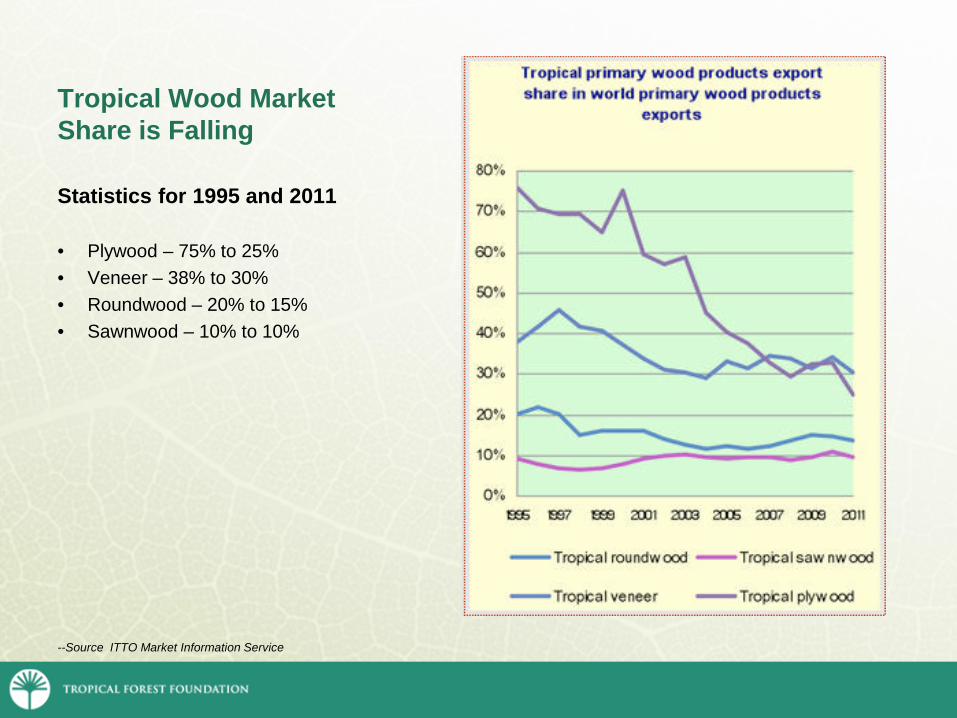

Tropical Wood Market Share is Falling Statistics for 1995 and 2011 • Plywood – 75% to 25% • Veneer – 38% to 30% • Roundwood – 20% to 15% • Sawnwood – 10% to 10% --Source ITTO Market Information Service

Markets are Shifting

“Families in the emergent, established, and affluent segments will make up 37 percent of Brazilian households by 2020, compared with 29 percent in 2010 and just 24 percent in 2000. These households will account for more than 85 percent of incremental spending from 2010 to 2020” -- Boston Consulting Group

“Middle Class” Outside the U.S. Expected to Double By 2020 – Approaching 1 Billion Households Worldwide commodity consumption will be impacted

0

200

400

600

800

1000

1990 1994 1998 2002 2006 2010 2014 2018

Foreign households w/real PPP incomes greater than $20,000 a year (in millions of households)

Developing countries

Developed countries (ex US)

Middle class in developing countries projected to increase 138% by 2020 vs. just 15% in developed countries in 2009

Chart provided by American Hardwood Export Council. Source: Global Insight’s Global Consumer Markets data as analyzed by OGA

“Middle Class” in Developing Countries Could Reach 616 Million Households By 2020, Up 138% From 2009 Levels 25% of households in these countries are middle class. By 2020, this could increase to 49% and the impact on food consumption will be large

23460

129

876

54

33

22

1

0 25 50 75 100 125 150 175 200 225 250 275 300 325 350

ChinaIndia

BrazilIndonesia

RussiaEgypt

ThailandMexicoTurkey

VietnamPhilippines

IranPolandNigeria

Households with real PPP incomes greater than $20,000 (in millions)

levels 2009 Proj gains by 2020

Chart provided by American Hardwood Export Council Source: Global Insight’s Global Consumer Markets data as analyzed by OGA

Developing countries with fastest growing “middle class”

Source: Global Trade Atlas

Chart provided by American Hardwood Export Council Source: Global Trade Atlas

0

100

200

300

400

500

600

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Jan - Nov.2012

Mill

ion

Boar

d Fe

et

US Hardwood Lumber Exports to China

2012

1999 - 2006US Furniture Manufacturing

Shift to China and US Housing Boom

2006 - 2009US Housing

Bust and Worldwide Economic

Turmoil

China's Growing Middle

1999 - 20062009 - 2012

Chart provided by American Hardwood Export Council. Source: Hardwood Market Report 2013

Chart provided by American Hardwood Export Council Source: FII Ltd drawing on BTS Ltd & Eurostat

Markets are Shifting

Substitution of hardwood plywood products “Substitutes are making more inroads into applications previously dominated by hardwood plywood in the European market.” -- ITTO Market Information Service

Markets are Shifting

• Imports are shifting from tropical countries

Markets are Shifting

Fighting trade of illegal timber • Japan “Goho” Wood, 2006 • US Lacey Act amendments,

2008 • EU Trade Regulations, 2013 • Australian law, 2014

Markets are Shifting

Laws are impacting flow of tropical woods • American Hardwood Export Council meeting on

October 4, foreign buyers said they are shifting to more American woods over tropicals because they are certain of the legality of American woods

Markets are Shifting

“Making softwoods more durable could cut demand for unsustainably logged tropical hardwoods.” -- The Economist “Increasing the Durability of Softwoods to Reduce Use of Tropical Hardwoods” -- The Dirt

Markets are Shifting

“…A 2008 pledge by Mayor Michael Bloomberg, Honorary ASLA, to the United Nations General Assembly that he would reduce New York’s tropical hardwood use by 20 percent. Since then, NYC Parks & Recreation has stopped using tropical wood in park benches. San Francisco, Santa Monica, and Baltimore ban the use of tropical hardwoods completely for municipal projects.” -- Landscape Architecture Magazine, 2013

Markets are Shifting

• Market reports at the National Hardwood Lumber Association 2013 Convention show that there is a growing gap between demand and available supply of temperate climate hardwoods

• Hardwood Market Report says that US housing starts will increase by 31% in 2014, 40.6% in 2015. The rapid market growth starting from already thin log inventories in the US will drive demand to imported supplies

Conclusions

• Tropical hardwoods have had a declining share of the world export markets

• Growth of the middle class in China, Brazil, and India is creating rapidly growing markets for wood

Conclusions

• Legal restrictions and inaccurate perceptions are influencing demand in US, EU

• The US housing market offers an opportunity over the next few years for growth in imports due to tight domestic supplies and lack of capacity

Thank You!

• Email:

• Tropical Forest Foundation 2121 Eisenhower Avenue Suite 200 Alexandria, VA 22314

• Phone: 703.518.8834 • Fax: 703.518.8974

• www.tropicalforestfoundation.org

THANK YOU!

Related Documents