CONFIDENTIAL Actively Managing Illiquid Credit Portfolios CONFIDENTIAL Credit Risk 2007 Vienna, June 27-28, 2007 Dr. Christian Bluhm Managing Director Credit Portfolio Management CREDIT SUISSE, Zurich

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CONFIDENTIAL

Produced by: CKR Project OfficeDate: April 11, 2007 Slide 0

Actively ManagingIlliquid Credit Portfolios

CONFIDENTIAL

Credit Risk 2007

Vienna, June 27-28, 2007

Dr. Christian BluhmManaging DirectorCredit Portfolio ManagementCREDIT SUISSE, Zurich

Christian Bluhm, June 2007 CREDIT SUISSE Slide 1

Contents

Credit Risk as an Asset Class - Markets & Challenges

Understanding Credit Portfolio Risk & Evaluation Techniques

Portfolio Analysis & Credit Portfolio Management

Steering of Illiquid Credit Portfolios (Case Study)

Concluding Remarks This presentation represents the opinion of the author

and not necessarily the opinion of Credit Suisse.

Christian Bluhm, June 2007 CREDIT SUISSE Slide 2

Contents

Credit Risk as an Asset Class - Markets & Challenges

Understanding Credit Portfolio Risk & Evaluation Techniques

Portfolio Analysis & Credit Portfolio Management

Steering of Illiquid Credit Portfolios (Case Study)

Concluding Remarks This presentation represents the opinion of the author

and not necessarily the opinion of Credit Suisse.

Christian Bluhm, June 2007 CREDIT SUISSE Slide 3

Credit Risk as an Asset Class

Public Debt

Private Debt

Public information is available, e.g., stock exchange listed clients, bond issuers, clients with capital market access for refinancing, CDO-type products, etc.

Active long/short positions are made easy for market participants, debt tradable via credit derivative market, public structured credit products, etc.

Mature segment of the overall credit market, highly liquid structured products are actively traded, e.g., iTraxx index tranches, bespoke STCDOs, etc.

Data gathering via public information providers like Bloomberg, Reuters, Rating agencies, etc, make risk assessment "easy" ...

Corporate clients where no public information is available, e.g., most clients of the SME segment

Private and retail clients, incl. special private client segments like (U)HNWIs, etc.

Transaction-focussed debt, e.g., income producing real estate and other mortgage products, trade finance, etc.

Credit risk evaluation and risk measurement rely on bank-internal data, agency ratings are most often not available, industry products like MKMV not applicable

Most universal banks have their largest buy & hold book in this category which makes active credit portfolio management a real challenge

Christian Bluhm, June 2007 CREDIT SUISSE Slide 4

Credit Portfolios are Vulnerable to the Credit Cycle

"never again" syndrome

credit consciouslending withshort maturities

heavycreditlosses

decliningspreads

lengtheningmaturities

increasedrisk appetite

lower creditstandards

The

Credit

Cycle

"never again" syndrome

credit consciouslending withshort maturities

heavycreditlosses

decliningspreads

lengtheningmaturities

increasedrisk appetite

lower creditstandards

The

Credit

Cycle

Cycle management is a major challenge in credit risk!

Christian Bluhm, June 2007 CREDIT SUISSE Slide 5

Example: Looser Credit Standards

By Chris Giles and Gillian Tett in London and Richard Beales and Chrystia Freeland in New York

Published: April 26, 2007 (Source: The Financial Times Limited 2007)

"A surge in cheap corporate lending with looser credit standards "has increased the vulnerability of the [global financial] system", the Bank of England will warn today in its strongest comments to date on financial stability.

The Bank also cautions against weakening standards of risk assessment when bank loans are repackaged and resold to new investors, such as pension and hedge funds. [...]

Its concerns relate to the consequences of an unforeseen shock to the global economy, world politics or a large financial institution. It is worried that other big financial institutions could find themselves over-exposed in the event of serious turbulence on global markets.

The Bank's concerns accord with those of Larry Fink, the chief executive of BlackRock, the $1,000bn-plus fund management group, in a Financial Times interview today. He said lendingto highly indebted companies was becoming lax in ways similar to those that have undermined the US subprime mortgage market, making the leveraged loan market "tomorrow's problem".

Christian Bluhm, June 2007 CREDIT SUISSE Slide 6

Example: Looser Credit Standards – continued

By Chris Giles and Gillian Tett in London and Richard Beales, and Chrystia Freeland in New York

Published: April 26, 2007 (Source: The Financial Times Limited 2007)

"If I was the chairman of the Federal Reserve I'd be paying more attention to that because, to me, this is going to be tomorrow's problem," Mr Fink said. "Standards have deteriorated to levels that we never even dreamt we would see."

The biggest reason for weakening lending standards were plentiful liquidity and consequent strong investor demand, Mr Fink said. But he warned many investors were moving into illiquid "alternative" investments such as hedge funds and private equity.

Aggressive lending is also supporting the private equity industry and Mr Fink said that any credit slump would have a knock-on effect on private equity groups such as Blackstone, which is planning a public offering. He said Blackstone, where he once worked, was highly diversified and "uniquely qualified" to go public."

Do we observe a similar trend in our bank/environment? How do we deal with it?

Christian Bluhm, June 2007 CREDIT SUISSE Slide 7

Working on a Healthy Balance ...

FO CRM

FO (Front Office)

Client relationship management

Sales/acquisition focus

Competition driven

Hard performance measured, ...

CRM (Credit Risk Management)

Credit business backbone of the bank, barrier of defense for the bank's P&L

Driven by objective analyses, based on quantitative tools like ratings etc.as well as portfolio models

Independent and separated from sales organization

Respect:

a "no" is a "no"

Bank P&L* view:

business enabling

* Note the P&L difference between a wrongly rejected client and a wrongly approved loan

Christian Bluhm, June 2007 CREDIT SUISSE Slide 8

Contents

Credit Risk as an Asset Class - Markets & Challenges

Understanding Credit Portfolio Risk & Evaluation Techniques

Portfolio Analysis & Credit Portfolio Management

Steering of Illiquid Credit Portfolios (Case Study)

Concluding Remarks This presentation represents the opinion of the author

and not necessarily the opinion of Credit Suisse.

Christian Bluhm, June 2007 CREDIT SUISSE Slide 9

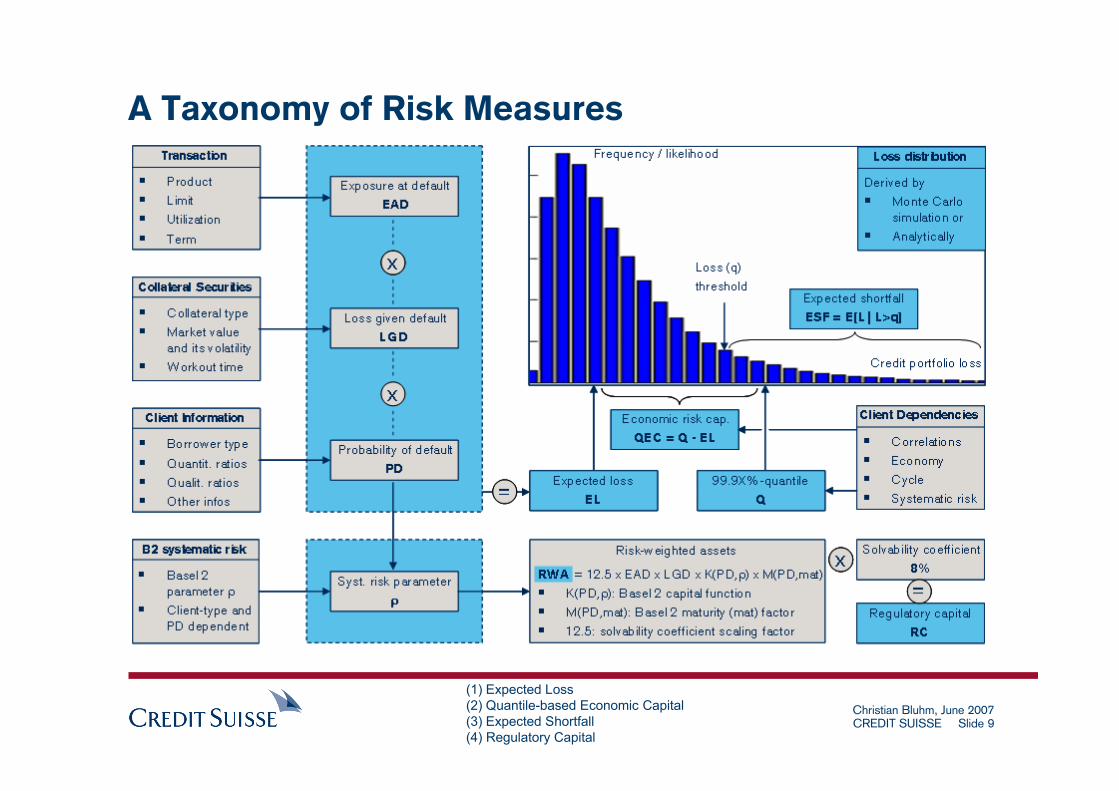

A Taxonomy of Risk Measures

(1) Expected Loss(2) Quantile-based Economic Capital (3) Expected Shortfall (4) Regulatory Capital

Christian Bluhm, June 2007 CREDIT SUISSE Slide 10

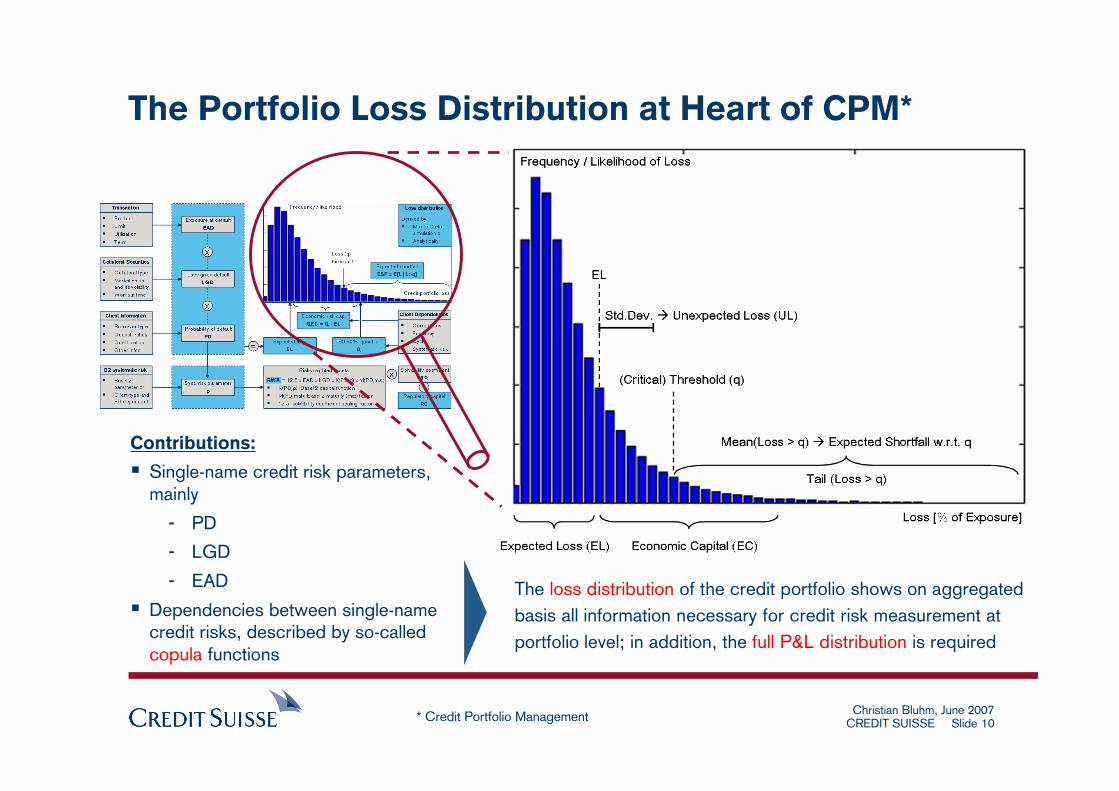

The Portfolio Loss Distribution at Heart of CPM*

Contributions:

Single-name credit risk parameters,mainly

- PD

- LGD

- EAD

Dependencies between single-namecredit risks, described by so-calledcopula functions

The loss distribution of the credit portfolio shows on aggregated basis all information necessary for credit risk measurement at portfolio level; in addition, the full P&L distribution is required

* Credit Portfolio Management

Christian Bluhm, June 2007 CREDIT SUISSE Slide 11

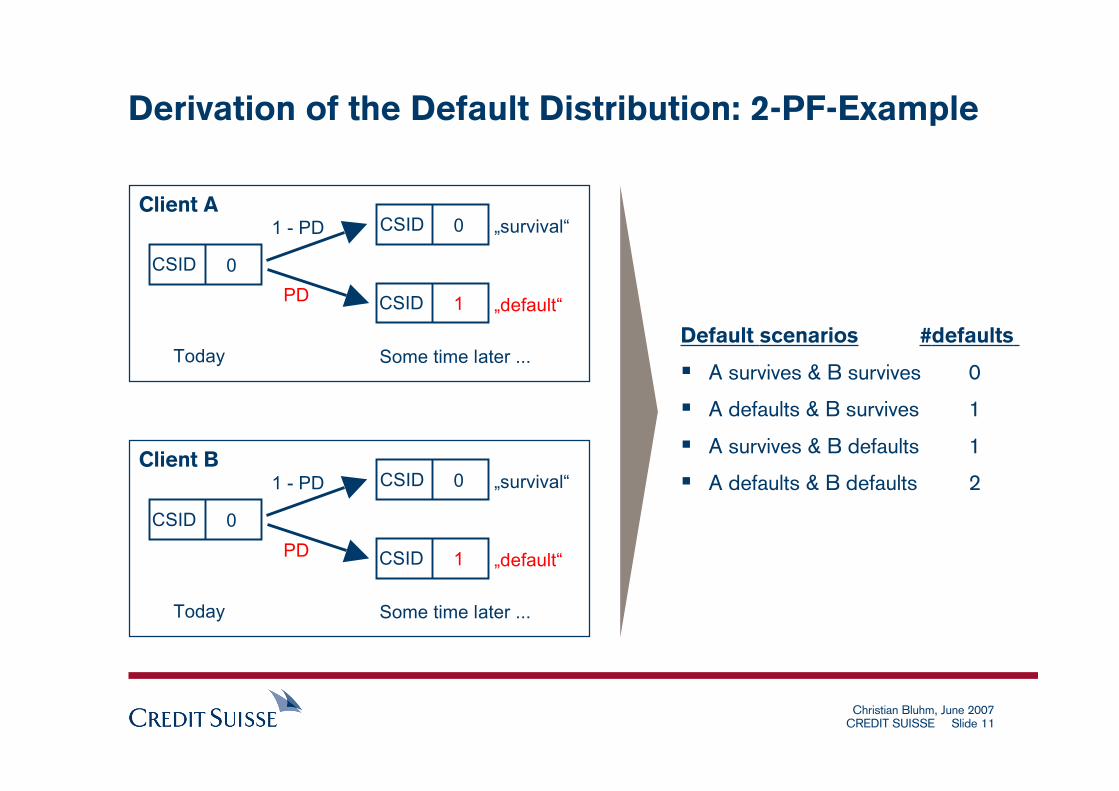

Derivation of the Default Distribution: 2-PF-Example

PD

1 - PD

CSID 0

CSID 0

CSID 1

„survival“

„default“

Today Some time later ...

PD

1 - PD

CSID 0

CSID 0

CSID 1

„survival“

„default“

Today Some time later ...

Client A

Client B

Default scenarios #defaults

A survives & B survives 0

A defaults & B survives 1

A survives & B defaults 1

A defaults & B defaults 2

Christian Bluhm, June 2007 CREDIT SUISSE Slide 12

x EAD LGDx

x EAD LGDx

DDF

CEEF

Loss

Quotes

AGGREGATION

From Default to Loss Distributions: 2-PF-Example

PD

1 - PD

CSID 0

CSID 0

CSID 1

„survival“

„default“

Today Some time later ...

PD

1 - PD

CSID 0

CSID 0

CSID 1

„survival“

„default“

Today Some time later ...

Client A

Client B

Christian Bluhm, June 2007 CREDIT SUISSE Slide 13

Dependence Modeling: What are Copula* Functions?

...

Single-name credit risks

can be compared with

single voices in an

orchestra; risk drivers

are given by various

conditions and the

instrument players

Professionalism of

players as well as

other conditions

drive the performance

of single voices

Single-name level Portfolio level

Portfolio-level credit risks

can be compared with

the score combining

and binding together

the single voices to a

composition of simultan.

sounding voices

Harmony and interplay of

voices can be substantially

different, depending on the

setup of the score

* Copula functions are used in statistics to describe the multivariate

interplay of marginal distributions for any given multidimensional

probability distribution

Christian Bluhm, June 2007 CREDIT SUISSE Slide 14

Case Study: Live Simulation* & Demonstration

Illustration:

Scenario derivation at single-name levelis like a coin flipping game with a biasedcoin

Joint scenario derivation at portfolio level is like a coin flipping game with coins as many as credit risks in the portfolio and coins are biased and interacting

The portfolio default distribution can be derived by repeating scenario generation many times and drawing a histogram

Different copula functions substantially change the shape of loss distributions

* In mathematical statistics, such simulations are called "Monte Carlo Simulations"

Christian Bluhm, June 2007 CREDIT SUISSE Slide 15

Contents

Credit Risk as an Asset Class - Markets & Challenges

Understanding Credit Portfolio Risk & Evaluation Techniques

Portfolio Analysis & Credit Portfolio Management

Steering of Illiquid Credit Portfolios (Case Study)

Concluding Remarks This presentation represents the opinion of the author

and not necessarily the opinion of Credit Suisse.

Christian Bluhm, June 2007 CREDIT SUISSE Slide 16

Credit Portfolio Management: Organizational Options

Source: Mercer Oliver Wyman

Christian Bluhm, June 2007 CREDIT SUISSE Slide 17

Example for a Typical Mandate for ACPM*

Benefits of Active Credit Portfolio Management

Reduce earnings volatility and concentrationsthrough hedging and (secondary) market

transactions

Improve portfolio value and liquidity

Help overcome existing market or policyconstraints

Develop and provide methodology and tool

capabilities for credit portfolio modeling andevaluation

Develop proposals for portfolio strategy, policyand risk appetite

Undertake credit portfolio

analytics and providemanagementinformation

Improveconcentration risks,earnings volatilityand portfolio value

Give input for setting portfolio strategy andrisk appetite

Enable and support business performance

* Active Credit Portfolio Management

Note: there is no "standard fit" for ACPM and its mandate in banks: every institute should

define its individual "best fit" - tailor-made and reflecting the business model of the bank

Christian Bluhm, June 2007 CREDIT SUISSE Slide 18

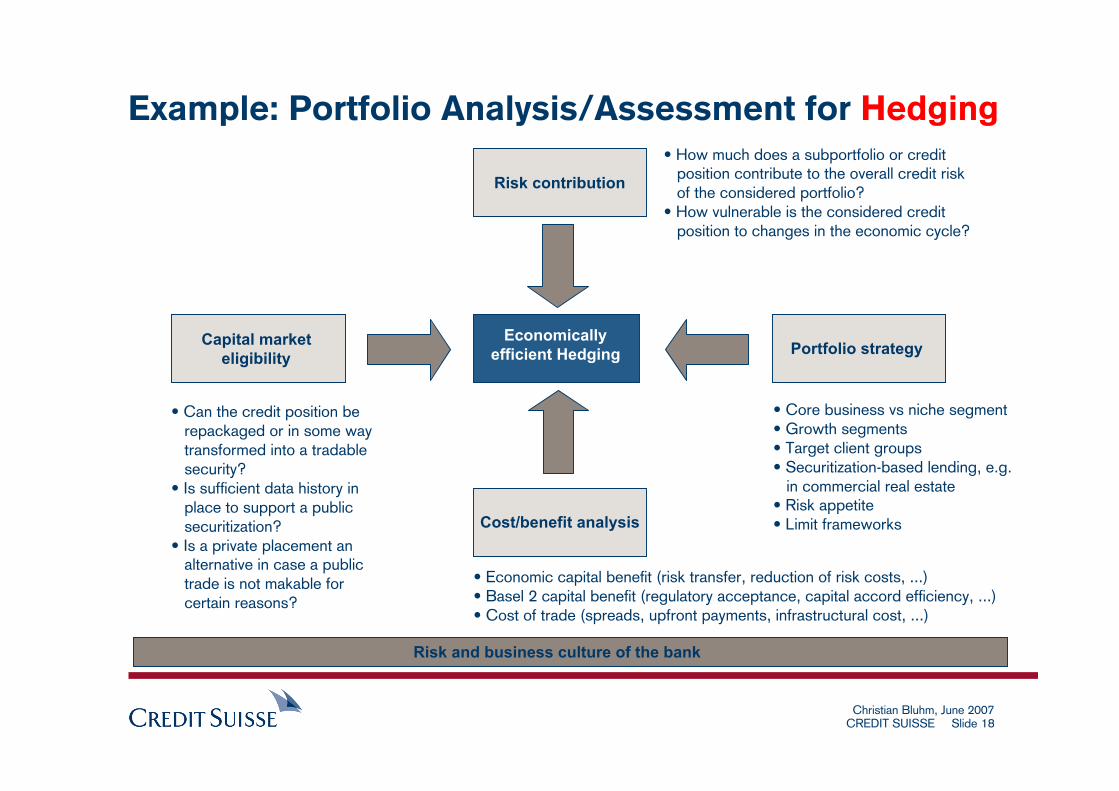

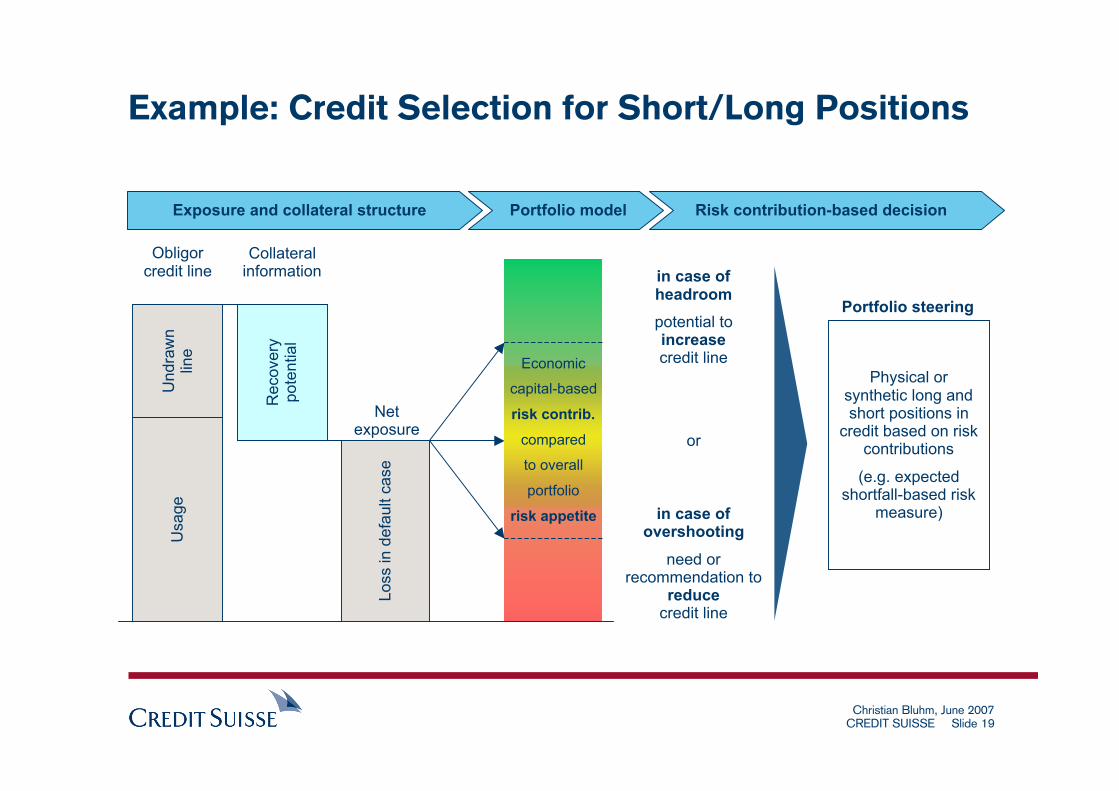

Example: Portfolio Analysis/Assessment for Hedging

Risk and business culture of the bank

• Can the credit position be repackaged or in some way transformed into a tradable security?• Is sufficient data history in place to support a public securitization?• Is a private placement an alternative in case a public trade is not makable for certain reasons?

• Economic capital benefit (risk transfer, reduction of risk costs, ...)• Basel 2 capital benefit (regulatory acceptance, capital accord efficiency, ...)• Cost of trade (spreads, upfront payments, infrastructural cost, ...)

• How much does a subportfolio or credit position contribute to the overall credit risk of the considered portfolio?• How vulnerable is the considered credit position to changes in the economic cycle?

• Core business vs niche segment• Growth segments• Target client groups• Securitization-based lending, e.g. in commercial real estate• Risk appetite• Limit frameworks

Capital market eligibility

Risk contribution

Cost/benefit analysis

Portfolio strategy Economically

efficient Hedging

Christian Bluhm, June 2007 CREDIT SUISSE Slide 19

in case ofheadroompotential toincreasecredit line

or

in case ofovershooting

need orrecommendation to

reducecredit line

Usa

ge

Rec

over

ypo

tent

ial

Und

raw

nlin

e

Loss

in d

efau

lt ca

se

Obligorcredit line

Collateralinformation

Netexposure

Physical orsynthetic long andshort positions in

credit based on riskcontributions

(e.g. expectedshortfall-based risk

measure)

Exposure and collateral structure Portfolio model Risk contribution-based decision

Portfolio steering

Economic

capital-based

risk contrib.

compared

to overall

portfolio

risk appetite

Example: Credit Selection for Short/Long Positions

Christian Bluhm, June 2007 CREDIT SUISSE Slide 20

Contents

Credit Risk as an Asset Class - Markets & Challenges

Understanding Credit Portfolio Risk & Evaluation Techniques

Portfolio Analysis & Credit Portfolio Management

Steering of Illiquid Credit Portfolios (Case Study)

Concluding Remarks This presentation represents the opinion of the author

and not necessarily the opinion of Credit Suisse.

Christian Bluhm, June 2007 CREDIT SUISSE Slide 21

Economic Securitization of Illiquid Credit

In contrast to (Basel 1)-type regulatory arbitrage securitizations, economically efficient

securitizations focus on a transfer of lower tranches to capital market investors but tend

to keep low-risk upper tranches (in partially funded CLOs typically the super senior tranche)

There are market participants who invest in lower tranches, even in equity pieces (so-called

"first loss" position); however, equity needs the most careful evaluation of placement options

Equity placement (if relevant) typically is non-public, e.g., private pre-placement of equity

Basel 2 penalizes kept equity tranches (full capital deduction, 50% Tier 1, 50% Tier 2),

hereby strongly motivating banks to get rid of such positions

Business case for decision making:

Securitization cost vs economic capital and regulatory capital cost

Cost of hedge, cost-to-securitize vs margin situation/pressure (business leverage)

Deployment of capital, re-investment benefit

Marginal economic capital effect on source portfolio

Strategic/tactical portfolio aspects are important to be taken into account

Christian Bluhm, June 2007 CREDIT SUISSE Slide 22

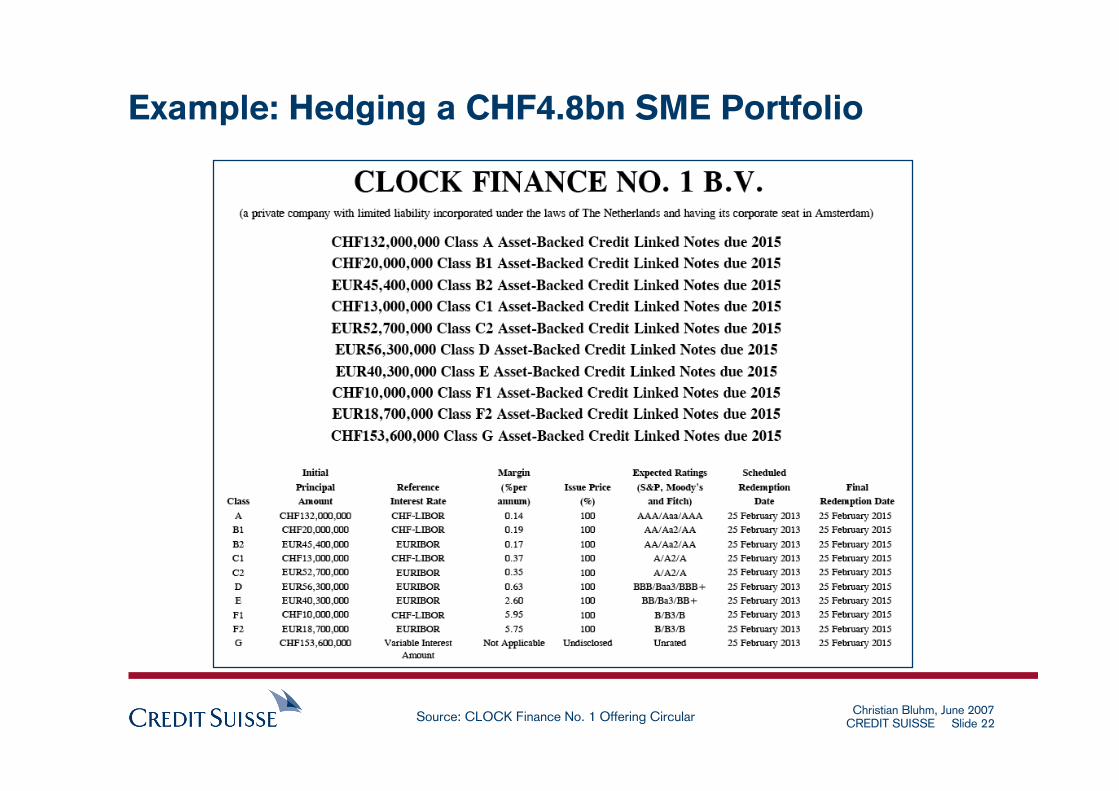

Example: Hedging a CHF4.8bn SME Portfolio

Source: CLOCK Finance No. 1 Offering Circular

Christian Bluhm, June 2007 CREDIT SUISSE Slide 23

Example (contd.): Transaction Structure

Source: CLOCK Finance No. 1 Offering Circular

Christian Bluhm, June 2007 CREDIT SUISSE Slide 24

Example (contd.): Capital Structure Leverage

...

• Losses eat into tranches bottom-up • Deleveraging/ repayments/ interest (Reference Rate + Spread) comes top- down (in order of seniority) • Accordingly, premium payment to note investors decreases with increasing order of seniority • Class G note (equity tranche) is the most risky position • Risk transfer happens in lower tranches

Christian Bluhm, June 2007 CREDIT SUISSE Slide 25

Benefits for the Bank

Economic Risk Transfer

(Credit Risk Hedge)

Economic capital (EC) significantly declines (EC cost reduction)

Hitting probability of kept super senior tranche is negligible such that the total securitized portfolio can be considered to be effectively hedged

Capital Efficiency

(Regulat. Capital Relief)

CLOCK Finance No. 1 is optimized to meet regulatory requirements under the new Basel 2 regime, effective from 01.01.2008 on

As a consequence, CLOCK Finance No. 1 leads to a significant regulatory capital relief (good for the 6-year lifetime of the deal)

Freed-up capital can be reinvested (capital efficiency)

Clients and the credit business itself are not affected by synthetic CLOs

Making Illiquid Assets

Tradable

CLOCK Finance No. 1 makes the attractive asset class of Swiss SME loans available for investment to capital market participants

Credit Suisse offers to investors an attractive participation in the credit risk of the securitized pool of Swiss SME reference entities

Christian Bluhm, June 2007 CREDIT SUISSE Slide 26

Contents

Credit Risk as an Asset Class - Markets & Challenges

Understanding Credit Portfolio Risk & Evaluation Techniques

Portfolio Analysis & Credit Portfolio Management

Steering of Illiquid Credit Portfolios (Case Study)

Concluding Remarks This presentation represents the opinion of the author

and not necessarily the opinion of Credit Suisse.

Christian Bluhm, June 2007 CREDIT SUISSE Slide 27

General Outlook and Expectations

An increasing trend to a more active management of illiquid credit portfolios can be expected

to be seen in the future

Based on observations regarding the cycle and its current state, we see an increasing need to

develop instruments for tailor-made short and long positions in credit risks even in illiquid credit

portfolios, e.g., investments in tailor-made structured credit (long position) or hedges (short) for

certain parts of the capital structure of certain well-selected subportfolios

Banks will more intensively benefit from partnerships with other banks in areas of win-win

situations; examples could include portfolio swaps or pooling, model experience exchange, etc.

Model sophistication will further increase; banks will continue to invest in risk infrastructure and

model expertise; forward looking banks will make sure they are prepared for a potential downturn

of the credit cycle

Product sophistication and complexity will further increase

Related Documents