CONFIDENCE, SAVINGS AND CONTROL FROM THE #1 ISSUER 1 Purchasing Card Best Practices : Reduce Costs and Generate Income

CONFIDENCE, SAVINGS AND CONTROL FROM THE #1 ISSUER 0 Purchasing Card Best Practices : Reduce Costs and Generate Income.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

1

Purchasing Card Best Practices :

Reduce Costs and Generate Income

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

2

Agenda

9:00 a.m. Welcome and Introductions

Charlie Pride and John Rogers

9:15 a.m. Purchasing Card Best Practices

Presentation – Brian Rodgers

9:35 a.m. City of Westfield - Efficiencies &

Benefits Recognized through a Card Program

Presentation – John Rogers

9:55 a.m. Q & A

Charlie Pride, John Rogers and Brian Rodgers

10:15 a.m. Adjournment

1

www.westfield.in.gowww.westfield.in.govv

J.P. Morgan Chase◦ Brian Rodgers, Commercial Card Solutions

Manager State Board of Accounts

◦ Charlie Pride, Cities, Towns and Libraries Office Supervisor

City of Westfield, Enterprise Division◦ John Rogers, Director of Enterprise◦ Tammy Havard, Financial Strategist◦ Teresa Evans, Project Manager

City of Westfield, Clerk Treasurers Office◦ Cindy Gossard, Clerk Treasurer◦ Kerri Gagnon, Deputy Clerk Treasurer◦ Micha Farrar, Deputy Clerk Treasurer

2

www.westfield.in.gowww.westfield.in.govv

We evaluated everyday tasks and activities:◦ Are they value-add?◦ Is this the best way to get this task done?◦ Are there best practices?◦ Is Apple going to announce an iClerk to do this

for us?

3

www.westfield.in.gowww.westfield.in.govv

How many invoices were we processing last year?◦How many are we

averaging this year? How much did it

cost us to invoice?

4

www.westfield.in.gowww.westfield.in.govv

When does authorization for spending occur?◦When the budget is approved by the

common council?◦When the claims docket is approved?◦When Charlie says so….

A: When the budget is approved by the common council.

5

www.westfield.in.gowww.westfield.in.govv

What do the State auditors require as proof for all expenses?◦Paper receipts and signed

approval vouchers◦Images of receipts and

electronic approvals◦Let’s ask CHARLIE……

A: Charlie has the answer!

6

www.westfield.in.gowww.westfield.in.govv

7

Agenda

Purchasing Card Best Practices :

Reduce Costs and Generate Income

Presented by: Brian Rodgers, Commercial Card Solutions Manager

8

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

10

This presentation was prepared exclusively for the benefit and internal use of the J.P. Morgan client or potential client to whom it is directly delivered and/or addressed (including subsidiaries and affiliates, the “Company”) in order to assist the Company in evaluating, on a preliminary basis, the

feasibility of a possible transaction or transactions or other business relationship and does not carry any right of publication or disclosure, in whole or in part, to any other party. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in

conjunction with, the oral briefing provided by J.P. Morgan. Neither this presentation nor any of its contents may be disclosed or used for any other purpose without the prior written consent of J.P. Morgan.

To the extent that the information in this presentation is based upon any management forecasts or other information supplied to us by or on behalf of the Company, it reflects such information as well as prevailing conditions and our views as of this date, all of which are accordingly subject to change. J.P. Morgan’s opinions and estimates constitute J.P. Morgan’s judgment and should be regarded as indicative, preliminary and for illustrative purposes

only. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Company or which was otherwise reviewed by us. J.P.

Morgan makes no representations as to the actual value which may be received in connection with a transaction nor the legal, tax or accounting effects of consummating a transaction. Unless expressly contemplated hereby, the information in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control, which may have significant valuation and other

effects.

Notwithstanding anything herein to the contrary, the Company and each of its employees, representatives or other agents may disclose to any and all persons, without limitation of any kind, the U.S. federal and state income tax treatment and the U.S. federal and state income tax structure (if

applicable) of the transactions contemplated hereby and all materials of any kind (including opinions or other tax analyses) that are provided to the Company insofar as such treatment and/or structure relates to a U.S. federal or state income tax strategy provided to the Company by J.P. Morgan.

J.P. Morgan's policies on data privacy can be found at http://www.jpmorgan.com/pages/privacy.

IRS Circular 230 Disclosure: JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters included herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the

promotion, marketing or recommendation by anyone not affiliated with JPMorgan Chase & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties.

Chase, JPMorgan and JPMorgan Chase are marketing names for certain businesses of JPMorgan Chase & Co. and its subsidiaries worldwide (collectively, “JPMC”) and if and as used herein may include as applicable employees or officers of any or all of such entities irrespective of the

marketing name used. Products and services may be provided by commercial bank affiliates, securities affiliates or other JPMC affiliates or entities. In particular, securities brokerage services other than those which can be provided by commercial bank affiliates under applicable law will be provided

by registered broker/dealer affiliates such as J.P. Morgan Securities LLC, J.P. Morgan Institutional Investments Inc. or Chase Investment Services Corporation or by such other affiliates as may be appropriate to provide such services under applicable law. Such securities are not deposits or other

obligations of any such commercial bank, are not guaranteed by any such commercial bank and are not insured by the Federal Deposit Insurance Corporation.

This presentation does not constitute a commitment by any JPMC entity to extend or arrange credit or to provide any other services.

9

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

11

Agenda

What is a Purchasing Card

What Can a Purchasing Card Do For You?

Generate Income

Prevent Fraud and Misuse

Reporting

Implementation and Support

10

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

12

Agenda

What is a Purchasing Card

What Can a Purchasing Card Do For You?

Generate Income

Prevent Fraud and Misuse

Reporting

Implementation and Support

11

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

13

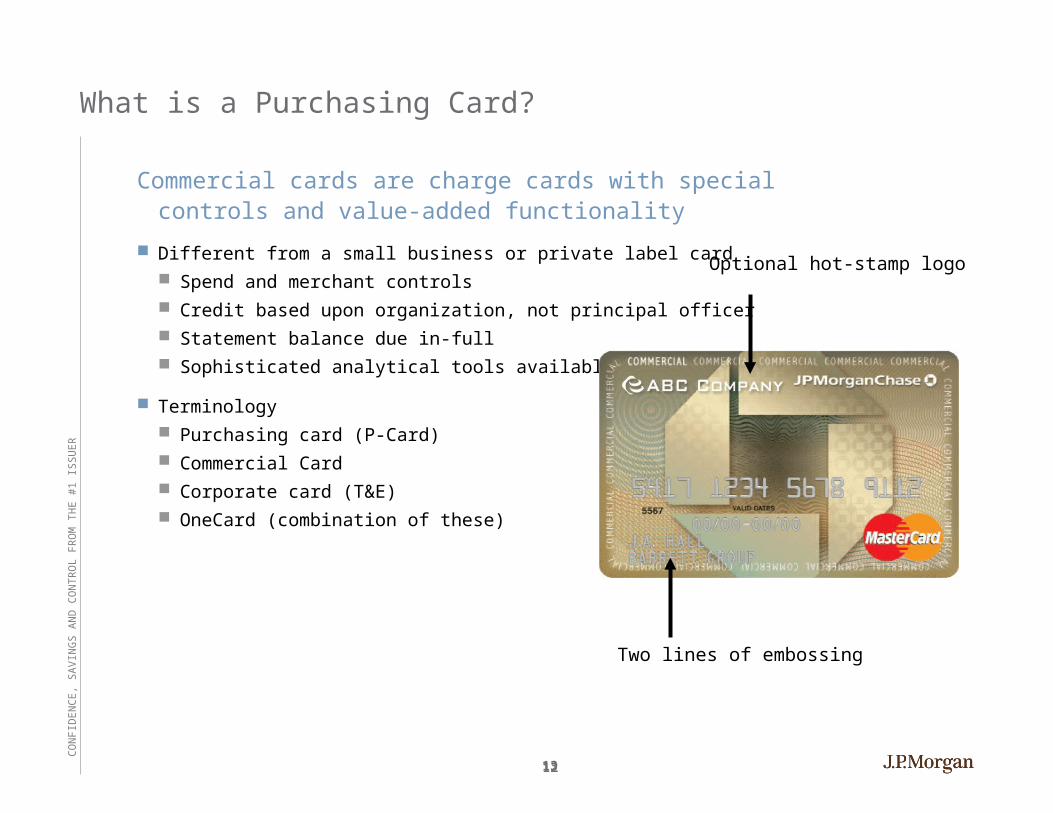

What is a Purchasing Card?

Commercial cards are charge cards with special controls and value-added functionality

Different from a small business or private label card Spend and merchant controls Credit based upon organization, not principal officer Statement balance due in-full Sophisticated analytical tools available

Terminology Purchasing card (P-Card) Commercial Card Corporate card (T&E) OneCard (combination of these)

Optional hot-stamp logo

Two lines of embossing

12

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

14

Agenda

What is a Purchasing Card

What Can a Purchasing Card Do For You?

Generate Income

Prevent Fraud and Misuse

Reporting

Implementation and Support

13

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

15

With a card program you can…

Gain efficiencies

Reduce costs

Optimize cash flow

Earn financial incentives

Improve vendor relations

Empower employees

If 90% of your invoices make up 10% of your dollars ~ does that mean that

accounts payable is spending 90% of their time on 10% of your dollars?

14

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

16

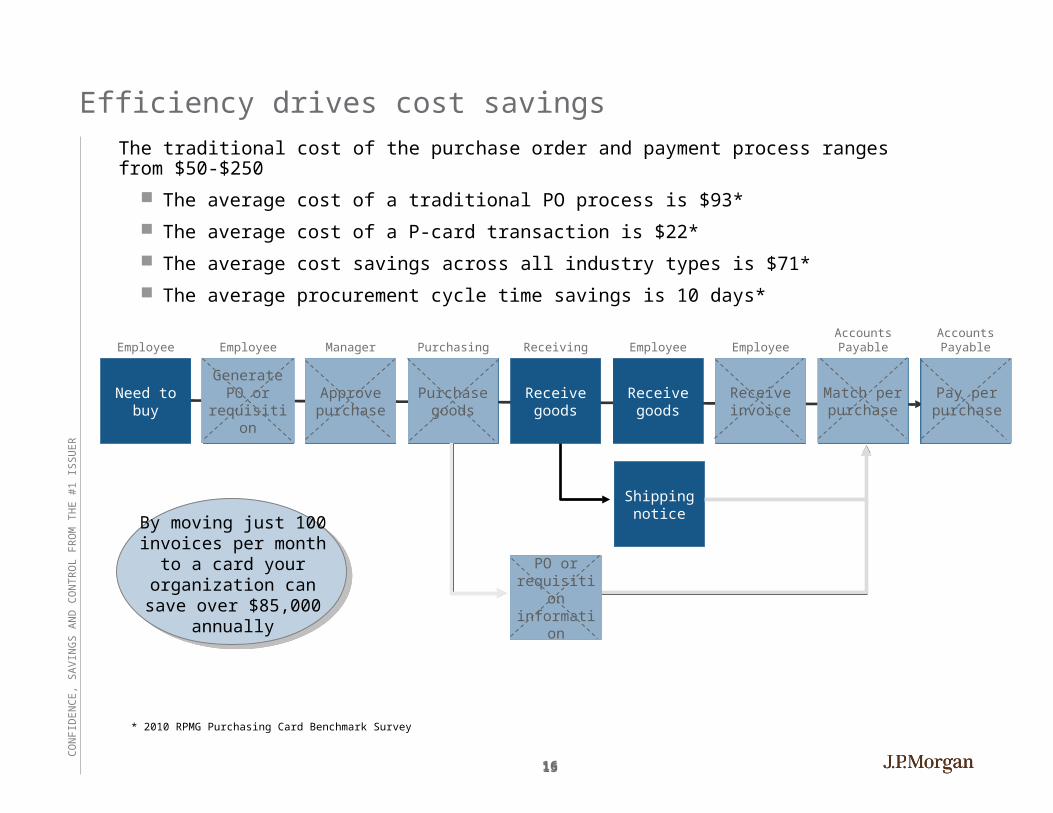

Efficiency drives cost savings

The traditional cost of the purchase order and payment process ranges from $50-$250

The average cost of a traditional PO process is $93*

The average cost of a P-card transaction is $22*

The average cost savings across all industry types is $71*

The average procurement cycle time savings is 10 days*

Need to buyReceive goods

Receive goods

Employee Receiving Employee

Generate PO or

requisition

Approve purchase

Purchase goods

Receive invoice

Match per purchase

Pay per purchase

Employee Manager Purchasing EmployeeAccounts Payable

Accounts Payable

PO or requisition information

Shipping notice

* 2010 RPMG Purchasing Card Benchmark Survey

Generate PO or

requisition

Approve purchase

Purchase goods

Receive invoice

Match per purchase

Pay per purchase

PO or requisition information

By moving just 100 invoices per month to a

card your organization can save over $85,000

annually

15

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

17

The expense category may determine the payment method

ACH/EDI/Wires

ACH/EDI for your top tier suppliers Wires transfers for immediate needs

AP Cards

Use commercial cards in AP to reduce check volume

Checks continue to decline

Commercial Cards and Direct Deposit

Commercial Cards for low dollar procurement and travel

Direct Deposit and Payroll Cards for payroll

16

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

18

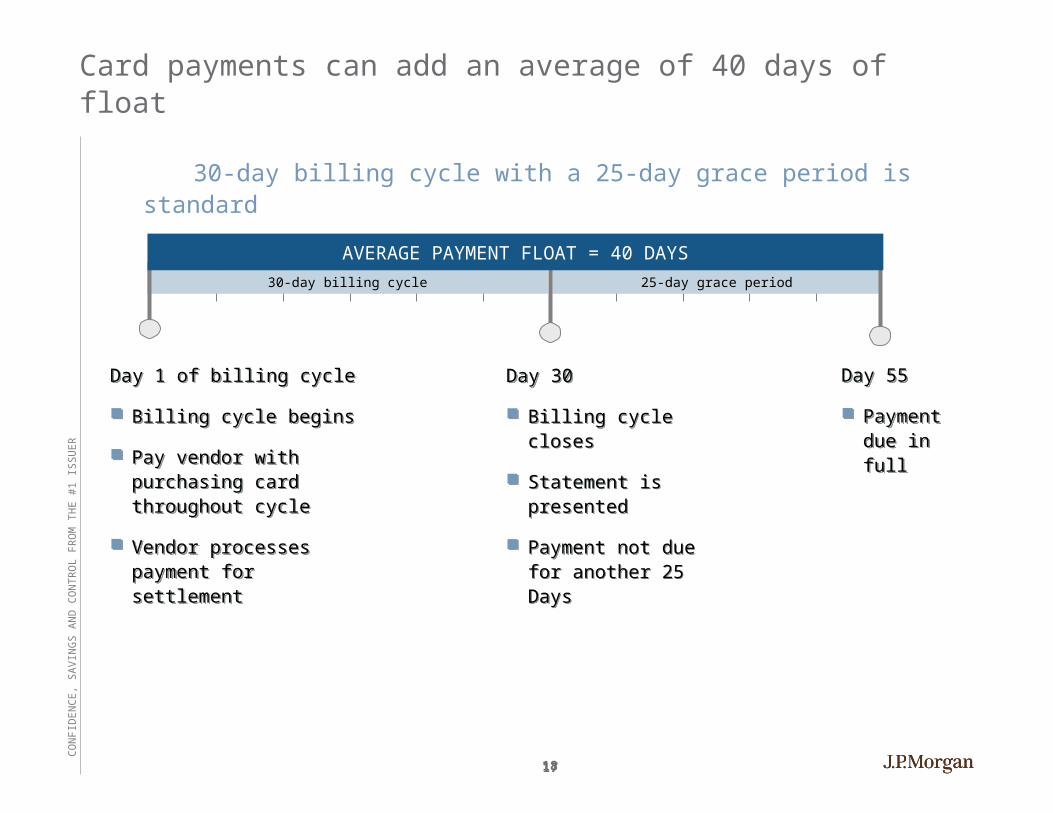

Card payments can add an average of 40 days of float

30-day billing cycle with a 25-day grace period is standard

Day 1 of billing cycle

Billing cycle begins

Pay vendor with purchasing card throughout cycle

Vendor processes payment for settlement

Day 1 of billing cycle

Billing cycle begins

Pay vendor with purchasing card throughout cycle

Vendor processes payment for settlement

30-day billing cycle 25-day grace period

Day 30

Billing cycle closes

Statement is presented

Payment not due for another 25 Days

Day 30

Billing cycle closes

Statement is presented

Payment not due for another 25 Days

Day 55

Payment due in full

Day 55

Payment due in full

AVERAGE PAYMENT FLOAT = 40 DAYS

17

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

19

Empower your employees with controlled purchasing ability

Accounts payable

Central purchasing

Administrative assistants

Maintenance (facilities/transportation)

IT staff members

Office and department managers

Parks and recreation

Fire and police

Courts

Conference and meeting planners

Principals and teachers

Athletics and theater

Travelers

Commercial cards benefit anyone in your organization that needs to make purchases as a regular part of their daily job routine.

18

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

20

Typical card use for best practice organizations

Aberdeen Research

Office Equipment and Supplies

Computer hardware, software and peripherals

Catering

Food/Groceries

Fuel

Media

Print and Duplicating Services

Maintenance, Repair & Operating (MRO) Goods

Clothing/Uniforms

Professional Services

Inventory

Telecommunications

Mail Delivery

Transport/Delivery

Construction Materials

91%

81%

78%

77%

71%

66%

60%

59%

56%

53%

52%

49%

39%

36%

69%

Note: * RPMG 2010Purchasing Card Benchmark Survey Report

Rental Payments 32%

Percentage of Best Practice Organization card uses:Percentage of Best Practice Organization card uses:

19

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

21

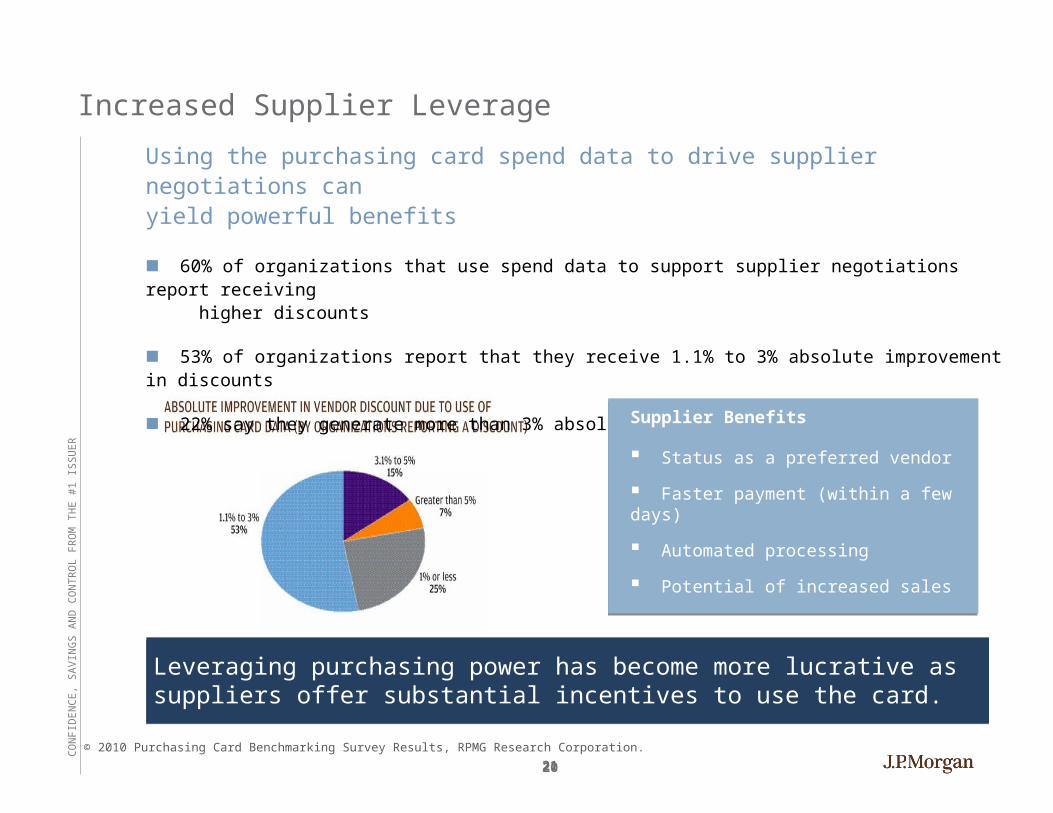

Increased Supplier Leverage

Using the purchasing card spend data to drive supplier negotiations can yield powerful benefits

■ 60% of organizations that use spend data to support supplier negotiations report receiving higher discounts

■ 53% of organizations report that they receive 1.1% to 3% absolute improvement in discounts

■ 22% say they generate more than 3% absolute improvement in supplier deals

Leveraging purchasing power has become more lucrative as suppliers offer substantial incentives to use the card.

Supplier Benefits

Status as a preferred vendor

Faster payment (within a few days)

Automated processing

Potential of increased sales

© 2010 Purchasing Card Benchmarking Survey Results, RPMG Research Corporation.

20

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

22

Agenda

What is a Purchasing Card

What Can a Purchasing Card Do For You?

Generate Income

Prevent Fraud and Misuse

Reporting

Implementation and Support

21

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

23

Rebates have become commonplace for qualified programs

Factors that affect rebate earning potential Annual volume Billing cycle length Speed of pay Program dynamics

While cost/incentive is a large factor, other factors should weigh in:* Technology Experience and expertise Customer and cardholder services

* Source: Best Practices Task Force Report: Optimizing Revenue Sharing, NAPCP, November 2006

22

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

24

Agenda

What is a Purchasing Card

What Can a Purchasing Card Do For You?

Generate Income

Prevent Fraud and Misuse

Reporting

Implementation and Support

23

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

25

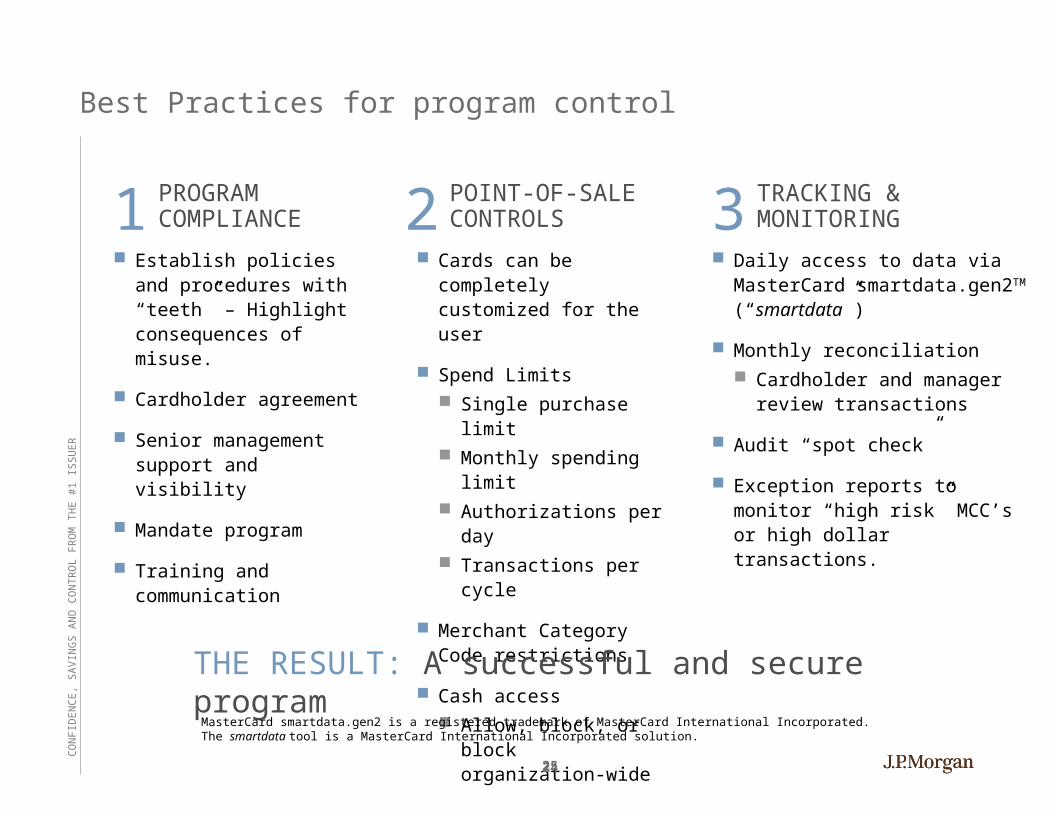

Best Practices for program control

Establish policies and procedures with “teeth” – Highlight consequences of misuse.

Cardholder agreement

Senior management support and visibility

Mandate program

Training and communication

Cards can be completely customized for the user

Spend Limits Single purchase limit Monthly spending limit Authorizations per day Transactions per cycle

Merchant Category Code restrictions

Cash access Allow, block, or block

organization-wide

Daily access to data via MasterCard smartdata.gen2TM

(“smartdata”)

Monthly reconciliation Cardholder and manager review

transactions

Audit “spot check”

Exception reports to monitor “high risk” MCC’s or high dollar transactions.

THE RESULT: A successful and secure program

PROGRAM COMPLIANCE1 POINT-OF-SALE

CONTROLS2 TRACKING & MONITORING3

MasterCard smartdata.gen2 is a registered trademark of MasterCard International Incorporated. The smartdata tool is a MasterCard International Incorporated solution.

24

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

26

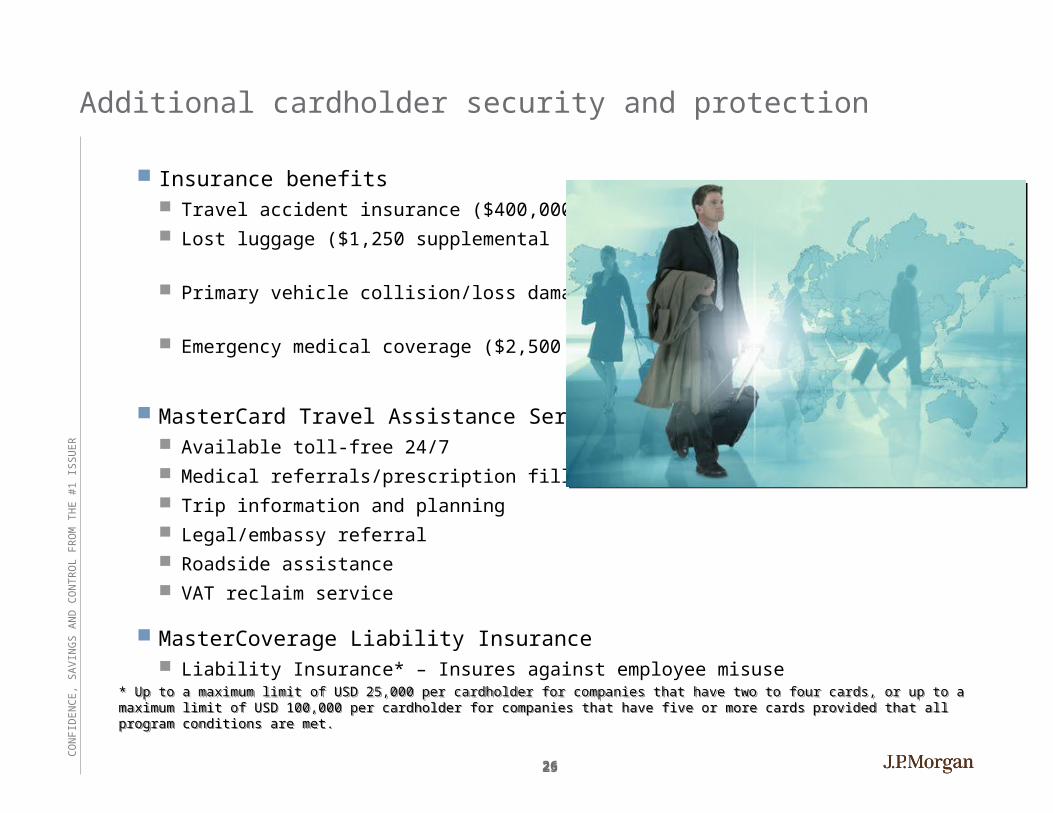

Additional cardholder security and protection

Insurance benefits Travel accident insurance ($400,000) Lost luggage ($1,250 supplemental

coverage) Primary vehicle collision/loss damage

waiver Emergency medical coverage ($2,500

secondary coverage)

MasterCard Travel Assistance Services Available toll-free 24/7 Medical referrals/prescription filling Trip information and planning Legal/embassy referral Roadside assistance VAT reclaim service

MasterCoverage Liability Insurance Liability Insurance* – Insures against employee misuse

* Up to a maximum limit of USD 25,000 per cardholder for companies that have two to four cards, or up to a maximum limit of USD 100,000 per cardholder for companies that have five or more cards provided that all program conditions are met.* Up to a maximum limit of USD 25,000 per cardholder for companies that have two to four cards, or up to a maximum limit of USD 100,000 per cardholder for companies that have five or more cards provided that all program conditions are met.

25

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

27

Agenda

What is a Purchasing Card

What Can a Purchasing Card Do For You?

Generate Income

Prevent Fraud and Misuse

Reporting

Implementation and Support

26

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

28

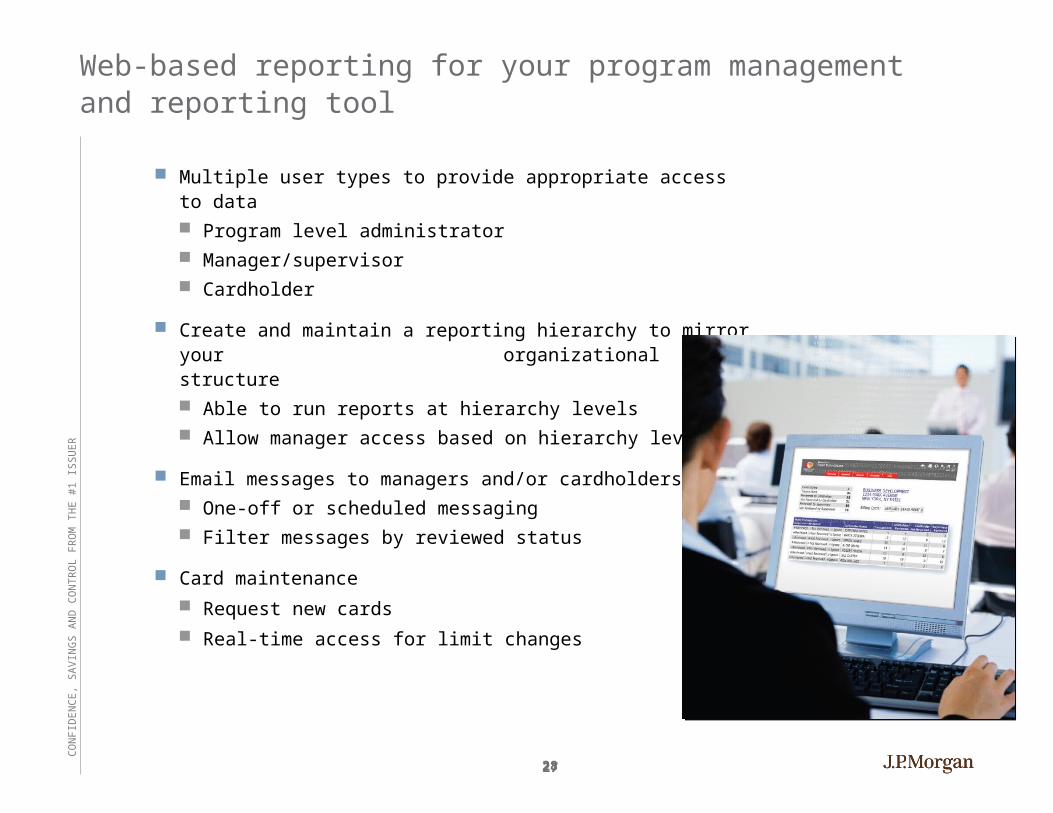

Web-based reporting for your program management and reporting tool

Multiple user types to provide appropriate access to data Program level administrator Manager/supervisor Cardholder

Create and maintain a reporting hierarchy to mirror your organizational structure Able to run reports at hierarchy levels Allow manager access based on hierarchy level

Email messages to managers and/or cardholders One-off or scheduled messaging Filter messages by reviewed status

Card maintenance

Request new cards

Real-time access for limit changes

27

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

29

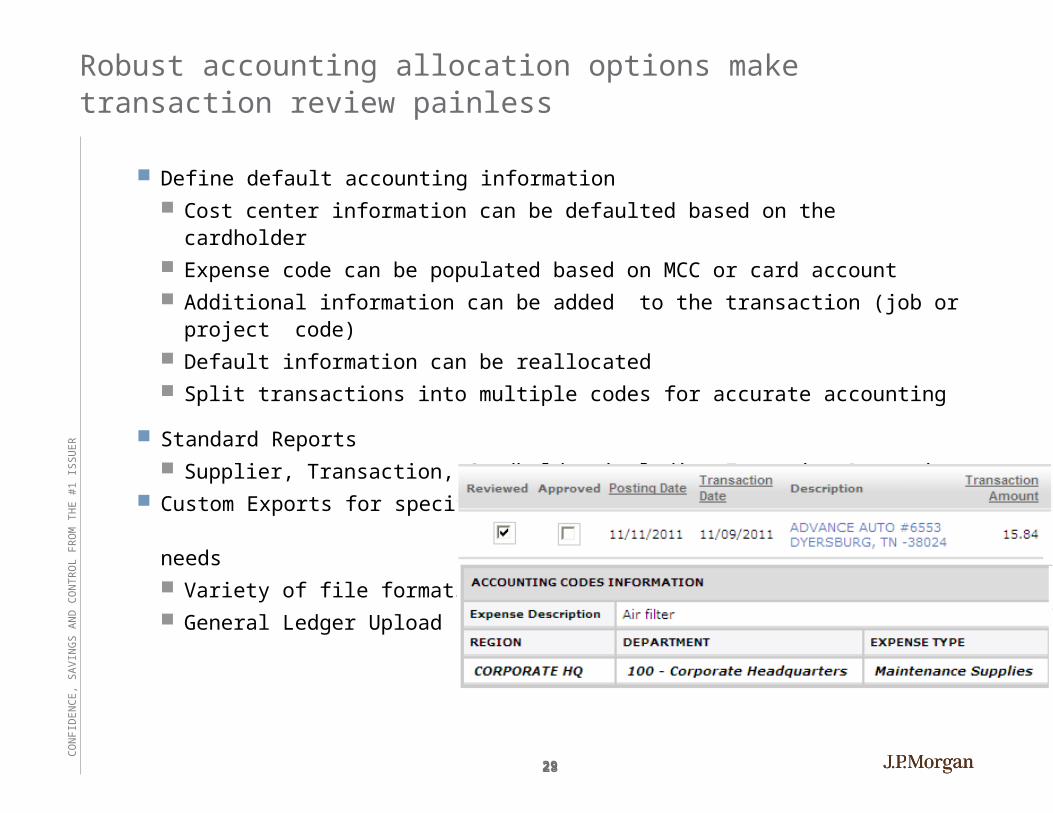

Robust accounting allocation options make transaction review painless

Define default accounting information Cost center information can be defaulted based on the cardholder Expense code can be populated based on MCC or card account Additional information can be added to the transaction (job or project code) Default information can be reallocated Split transactions into multiple codes for accurate accounting

Standard Reports Supplier, Transaction, Cardholder including Exception Reporting

Custom Exports for specific reporting needs Variety of file formats General Ledger Upload

28

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

30

Agenda

What is a Purchasing Card

What Can a Purchasing Card Do For You?

Generate Income

Prevent Fraud and Misuse

Reporting

Implementation and Support

29

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

31

Keys to a successful implementation

30

Clearly define program goals Allows you to benchmark and quantify successes Do a Vendor Match to help estimate the size of your program and rebate potential

Garner senior management and oversight body support and approval Program champion

Involve key areas during the planning process Oversight Body, Accounts Payable, Purchasing and Auditing

Establish and enforce policies and procedures Be sure your policies are ‘enforceable’

Determine program administrator Decision-making abilities and authority

Comprehensive training Cardholders Management

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

32

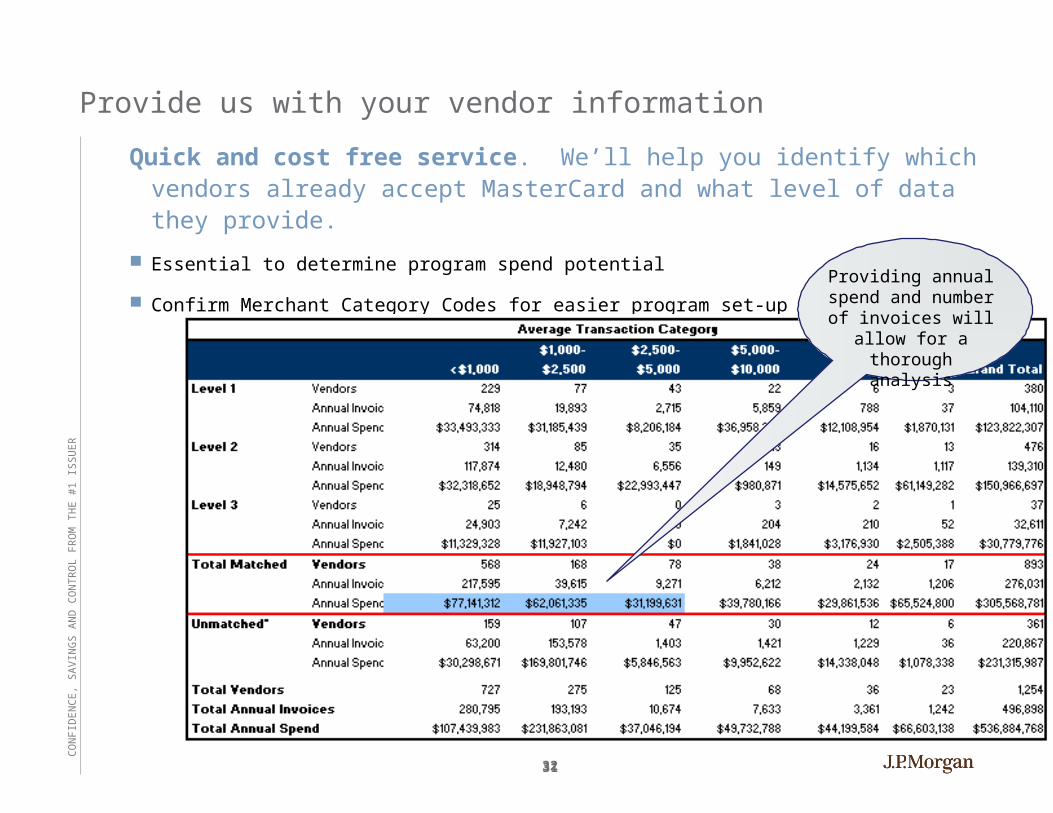

Provide us with your vendor information

Quick and cost free service. We’ll help you identify which vendors already accept MasterCard and what level of data they provide.

Essential to determine program spend potential

Confirm Merchant Category Codes for easier program set-up Providing annual spend and number of invoices will allow for a thorough analysis

31

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

33

Implementation and Support

Dedicated specialists guide and support your program before, during and after implementation

Understand RequirementsUnderstand Requirements Implement and TrainImplement and Train Service & SupportService & Support

Identify project resources

Review technical and reporting requirements

Develop policies

Determine readiness

Identify project resources

Review technical and reporting requirements

Develop policies

Determine readiness

Attend Program Administrator Training

Launch solution within clients needs and parameters

Train Users to provide faster ramp-up

Attend Program Administrator Training

Launch solution within clients needs and parameters

Train Users to provide faster ramp-up

Program Coordinator Team

• Day-to-day servicing and maintenance

• Program Administrator’s main point of contact

Technical Support Team

Cardholder Support Team

Program Coordinator Team

• Day-to-day servicing and maintenance

• Program Administrator’s main point of contact

Technical Support Team

Cardholder Support Team

32

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

34

Training

Successful implementation continues with effective training

Dedicated trainers are responsible for product training and consulting

Program Administrator training

Online through our Learning Website

Telephone consultations

Train-the-trainer sessions

SmartData® “how-to” guide

Quick reference cards

On-demand Webcasts

33

CO

NF

IDE

NC

E,

SA

VIN

GS

AN

D C

ON

TR

OL

FR

OM

TH

E #

1 IS

SU

ER

35

Purchasing Card Best Practices :Reduce Costs, Generate Income and Prevent Fraud

Questions

34

www.westfield.in.gowww.westfield.in.govv

Ask Why◦ Why does the procure-to-

pay process take so long?◦ Why are we paying two

different prices for a similar product or service?

◦ Why are we cutting checks to the bank in lieu of ACH payments?

◦ Why are there interstate highways in Hawaii?

http://www.aaroads.com/shields/show.php?image=HI19790012t100010.jpg&view=135

www.westfield.in.gowww.westfield.in.govv

A pCard program reduces the steps of the procure-to-pay process by:◦ Moving some aspects of the back office support

closer to the transaction◦ Settlement of the transactions (less invoices)◦ Account reconciliation ◦ Reporting

36

www.westfield.in.gowww.westfield.in.govv

The pCard can provide more efficient control of purchasing activity◦ Clerk’s office can adjust or limit spend by sector,

day and time (much more effective than open PO’s at local suppliers

◦ Limit maverick spend by placing tight controls on the pCard

37

www.westfield.in.gowww.westfield.in.govv

Additionally, the pCard data organizes our vendor and spend information for analysis◦Facilitating a review of purchase

activity/inconsistencies enterprise-wide through a single database

◦Allowing for vendor and spend management A vehicle for increasing revenue

◦The annual rebate currently competes with the interest received on short-term investment notes

38

www.westfield.in.gowww.westfield.in.govv

39

www.westfield.in.gowww.westfield.in.govv

Because everything we do affects the quality of life of our citizens.

40

Related Documents