UK AD & BIOGAS TRADESHOW 6-7 JULY 2016 NEC BIRMINGHAM

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

UK AD & BIOGAS

TRADESHOW

6-7 JULY 2016NEC BIRMINGHAM

WELCOME AND

INTRODUCTION

JOINING THE LINKS IN THE FOOD CHAIN

LAUNCHING THE FOOD WASTE

RECYCLING ACTION PLAN

CHARLOTTE MORTON, ADBA CEO

RAY GEORGESON, CHAIRMAN, FOOD WASTE RECYCLING ACTION PLAN STEERING

GROUP

LINDA CRICHTON, HEAD OF RESOURCE MANAGEMENT, WRAP

A Food Waste Recycling Action Plan for England

• 10 million tonnes of ‘post-farm gate’ food waste produced in the UK each

year

• Almost 20% of the food that UK households purchase is thrown away

• The cost to the UK’s hospitality & food services industry is £3 billion a year

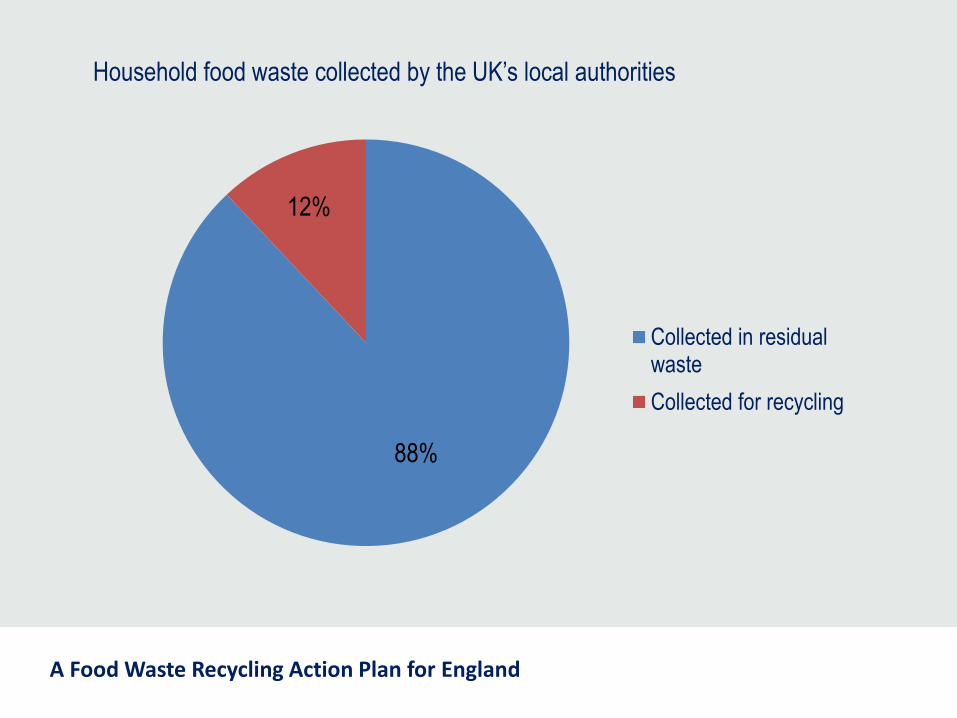

• Of the 4.6 million tonnes of food waste collected each year by local

authorities only 12% is currently recycled.

A Food Waste Recycling Action Plan for England

…but almost 3 million tonnes a year from households is ‘unavoidable’

A Food Waste Recycling Action Plan for England

88%

12%

Collected in residualwaste

Collected for recycling

Household food waste collected by the UK’s local authorities

A Food Waste Recycling Action Plan for England

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Metalpackaging

Glass Paper &Board

Plastic Textiles &Footwear

Gardenwaste

Food waste WEEE &other scrap

metal

Other(including

wood)

Household waste: capture rate by material 2012/13

A Food Waste Recycling Action Plan for England

The Food Waste Recycling Action Plan is the industry’s response to the challenge of

increasing food waste recycling in England.

A Food Waste Recycling Action Plan for England

• Increase the amount of food waste collected

from households and the commercial and

industrial sector.

• Provide long term sustainable feedstocks for

the operators of food waste processing plants,

both anaerobic digestion (AD) and in vessel

composting (IVC).

• Share the costs and benefits of collecting and

recycling food waste across the food waste

supply chain

A Food Waste Recycling Action Plan for England

A Food Waste Recycling Action Plan for England

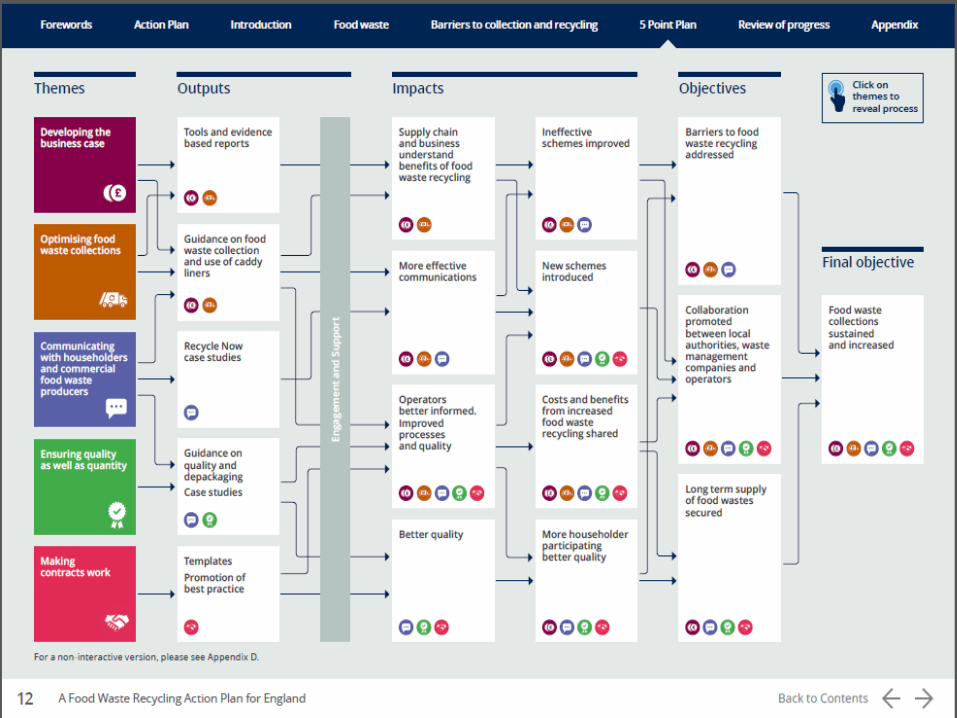

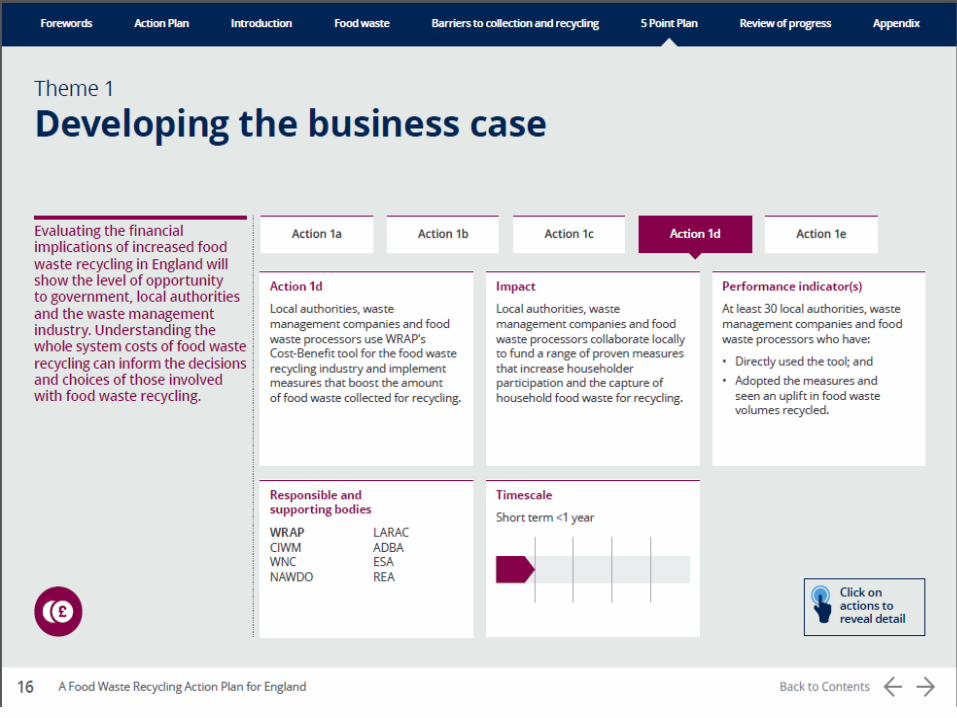

1. Developing the business case

2. Optimising food waste collections

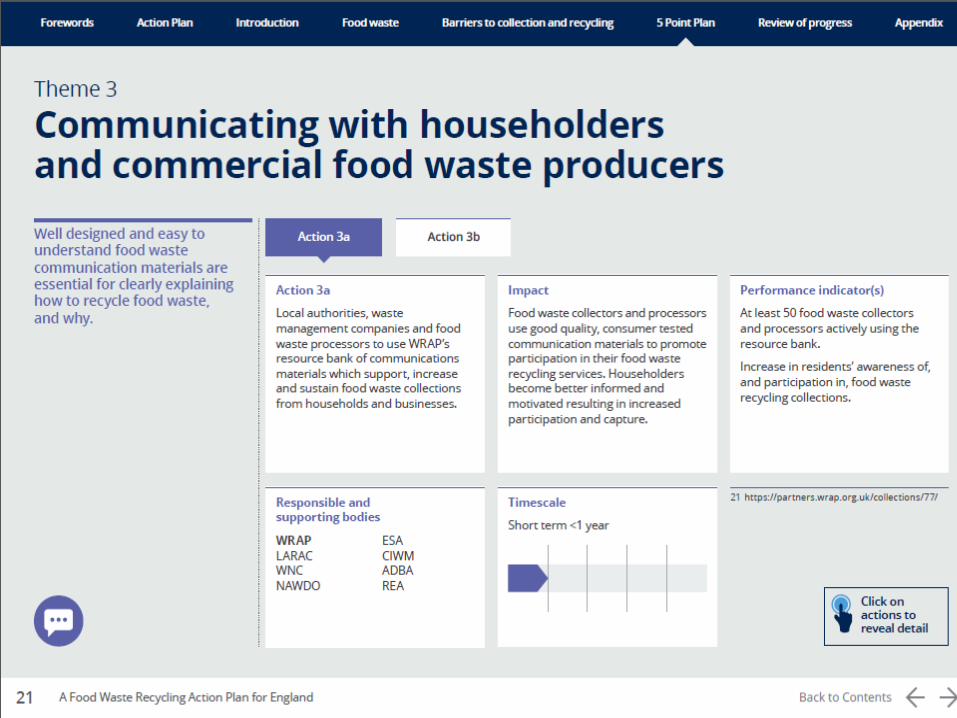

3. Communicating with householders and

commercial food waste producers

4. Ensuring quality as well as quantity

5. Making contracts work

A Food Waste Recycling Action Plan for England

WRAP’s role in the development of the

Food Waste Recycling Action Plan

Enabling & facilitating

the Steering Group

• Coordination

• Administration

• Secretariat

…but we’re also responsible for delivering some of the actions listed in the Plan

A Food Waste Recycling Action Plan for England

Why WRAP supports the Food Waste Recycling Action Plan

• Voluntary industry-led initiative

• Provides a road map for the food waste recycling industry – to help it to realise

it’s full potential

• Establishes a supportive landscape for those already active in food waste

recycling, and for those considering introducing new food waste collections;

• Promotes greater collaboration across the food waste supply chain – essential if

the long term supply of food waste is to be secured

• Will deliver environmental and economic benefits

A Food Waste Recycling Action Plan for England

The Framework for greater consistency in household recycling proposes

the weekly collection of food waste

A Food Waste Recycling Action Plan for England

Communication materials to encourage participation

in food waste collections

A Food Waste Recycling Action Plan for England

A Food Waste Recycling Action Plan for England

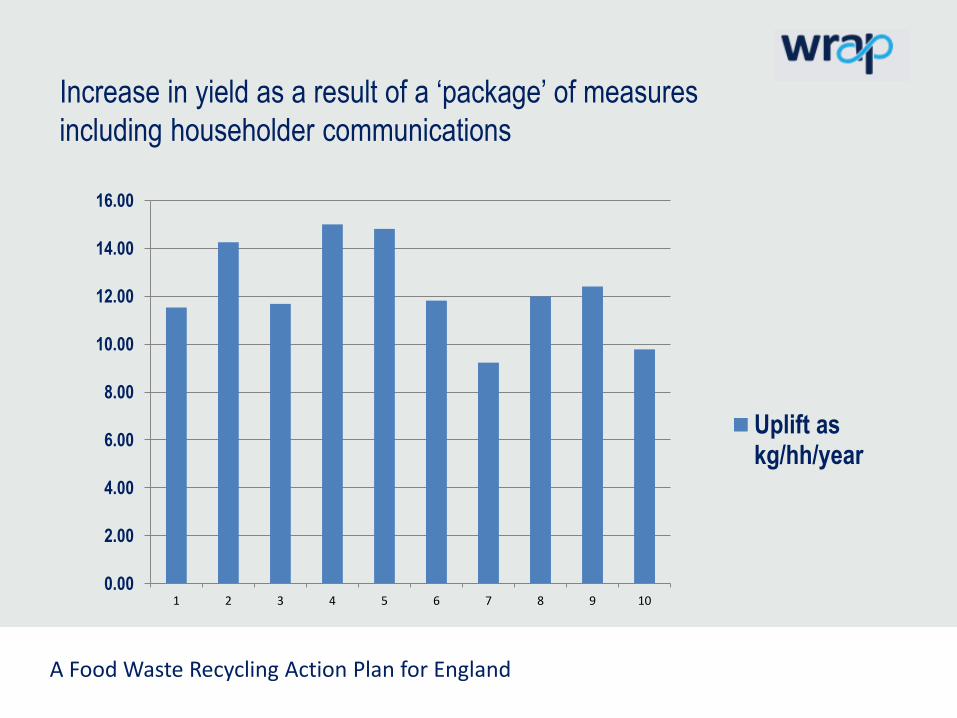

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

1 2 3 4 5 6 7 8 9 10

Uplift askg/hh/year

Increase in yield as a result of a ‘package’ of measures

including householder communications

A Food Waste Recycling Action Plan for England

Results from recent WRAP pilots have shown that a package of

measures including communications increased yields of food waste (by

an average of c12kg/hh/yr);

….but these measures cost;

So need to ensure that the financial benefits that result from adopting

these measures meet, or exceed, the costs of those measures.

A Food Waste Recycling Action Plan for England

What are these ‘financial benefits’?

• Increased capture of food waste…

Benefits to local authorities from avoided residual disposal costs

Benefits to treatment plant operators from increased feedstock

• These benefits taken alone can be insufficient to fund the cost of measures

• But, bringing these benefits together through a contractual arrangement can

mean that it is economic to fund the incentive

A situation where all parties are better off

A Food Waste Recycling Action Plan for England

Cost Benefit Analysis Tool for the

food waste recycling industry

A Food Waste Recycling Action Plan for England

View the plan at:

www.wrap.org.uk/foodwasterecycling

Follow the conversation on twitter #FWRAP

QUESTIONS AND COMMENTS FROM THE FLOOR

THE EU CIRCULAR ECONOMY PACKAGE:

IMPLEMENTATION, REGULATION, AND

IMPACT ON AD

RAY GEORGESON, CHAIRMAN, FOOD WASTE RECYCLING ACTION PLAN STEERING

GROUP

SUSANNA PFLUGER, SECRETARY GENERAL, EUROPEAN BIOGAS ASSOCIATION

ROY HATHAWAY, ESA AND FEAD

LUCIA GURNARI, ECOMONDO FAIR

The EU Circular Economy Package: implementation, regulation, and impact

on AD

UK AD & Biogas 2016: Conference7 July 2016 Birmingham

Susanna PflügerSecretary General

European Biogas Association

• Non-profit association founded in 2009

• Covers biogas and biomethane from anaerobic digesation and biomass gasification

• Well-established network and communication platform for exchanging information and expertise in biogas

• Member of EREF and EUFORES, co-operation with waste, gas and renewable associations

• Based in Brussels, Renewable Energy House (REH)

What is EBA?

www.european-biogas.eu

37 National Associations + 52 Companies = Representing >7,100 Stakeholders in 25 Countries

Domestic, Decentralised, Secure

Versatility of Biogas in Europe

Status – Biogas from FAB Waste

* - waste biogas plants allowed to use FAB industry waste

www.fabbiogas.eu

78 MT of green waste landfilled in the EU in 2012Emitting 110 MT CO2eq1

If digested, these emissions would have been avoided

In addition, 11 million tons of CO2eq from fossil fuel would have been substituted

Digesting this and returning the organic fertiliser would deliver:

400,000t of nitrogen (N)

120,000t of phosphorus (P2O5)

450,000t potassium (K2O)

3 million tonnes of organic carbon (to fight soil erosion)

Feedstock Potential – Biowaste

1 National Reporting Landfill Directive

Every YEAR!

Avoid greenhouse gas emissions (GHG) from landfills; production of renewable energy which replaces fossil fuels; production of organic fertilisers which replace energy intensive mineral fertilisers

Produce renewable energy in the form of biogas and biomethane – In 2014, 63.6 TWh of electricity in Europe from AD - equivalent to the consumption of 14.6 million EU households

Recycle organic material in the form of organic fertiliser

Reap social and economic benefits from producing fertilisers and energy from waste: additional revenue for farmers, municipalities and the food industry from producing renewable energy and fertilisers from their waste; around 70,000 jobs in Europe and potential for many more!

Contribution of AF to the Europe’s Circular Economy

Europe's transition towards a circular economy which will boost global competitiveness, foster sustainable economic growth and generate new jobs

A common EU target for recycling 65% of municipal waste by 2030;

A binding landfill target to reduce landfill to maximum of 10% of municipal waste by 2030;

A ban on landfilling of separately collected waste;

Promotion of economic instruments to discourage landfilling ;

Separate collection of bio-waste where technically, environmentally and economically practicable and appropriate. Member States to encourage the recycling, including composting, and digestion of bio-waste

EU Commission’s Proposal to Close the Loop

Strengthen bio-waste separate collection by removing exemptions – remove words “economically practicable and appropriate”

A progressive incineration ban for organic waste should be included in the amendment of the WFD

Remove manure destined for anaerobic digestion from the scope of the WFD

Clarify and strengthen the provisions for by-products in the WFD

EBA’s Key Messages to Revise the Proposal

First draft report from the European Parliament: stronger EU harmonisation, higher targets and a much better place for biowaste: by 2025, the organic recycling of bio-waste from municipal waste shall be increased to a minimum of 65 % by weight; extend the scope from municipal to industrial waste

Next steps in the EP: committee vote on 7 November, plenary vote likely in December

First Council debate stressing the reduction of food waste; different views on by-products and feasibility of the targets

Next Steps in Legislative Procedure - Parliament and Council

A vast majority of separately collected biowaste directed towards AD

Only synchronised environmental, waste and agricultural policies can ensureeasy access to more feedstock

AD to further expand from rural to urban areas – more jobs, bigger plants

Big plants more difficult to develop (public acceptance, logistics)

Improved performance of wastewater treatment plants through treatment of biowaste (increase the efficiency of the plants)

Increased biogas and biomethane production in Europe

Impact on Europe’s AD Sector

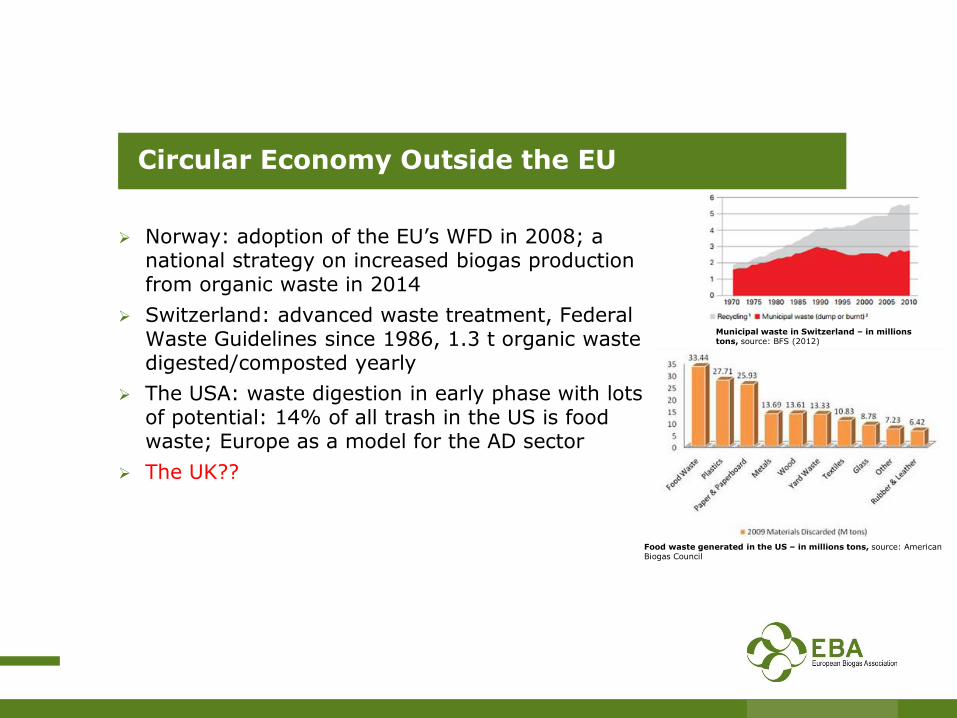

Norway: adoption of the EU’s WFD in 2008; a national strategy on increased biogas production from organic waste in 2014

Switzerland: advanced waste treatment, Federal Waste Guidelines since 1986, 1.3 t organic waste digested/composted yearly

The USA: waste digestion in early phase with lots of potential: 14% of all trash in the US is food waste; Europe as a model for the AD sector

The UK??

Circular Economy Outside the EU

Municipal waste in Switzerland – in millions tons, source: BFS (2012)

Food waste generated in the US – in millions tons, source: American Biogas Council

www.biogasconference.eu

• 3rd biannual Conference on biogas & syngas & biomethane from AD and gasification

• Keynote speakers from the European institutions and the industry – including Commission VP speech on Europe’s Circular Economy!

Thank you

Renewable Energy House

Rue d'Arlon 63-65

B - 1040 Brussels

+32 24.00.10 – [email protected]

European Biogas AssociationSusanna PflügerSecretary [email protected]

The EU Circular Economy Package and its impact on AD

ADBA Conference: 7 July 2016

Roy Hathaway

Europe Policy Adviser

Environmental Services Association

EU Circular Economy package

EU Commission 2015 Proposal - 1

Prevention

“Member States shall take measures…..which shall….reduce the generation of food waste in primary production, in processing and manufacturing, in retail and other distribution of food, in restaurants and food services as well as in households.”

NB no legally binding FW reduction target

EU Commission 2015 Proposal - 2

Separate collection

Replaces first part of WFD Article 22 with:

“ Member States shall ensure the separate collection of bio-waste where technically, environmentally and economically practicableand appropriate to ensure the relevant quality standards and to attain [the MW recycling targets].”

EU Parliament amendments - 1

Prevention

“Member States shall take measures…..which shall….reduce the generation of food waste at the retail and consumer levels and reduce food losses along production and supply chains…..with the aim of achieving a Union food waste reduction target of 50% by 2030”

EU Parliament amendments - 2

Recycling target

“Member States shall take the necessary measures to ensure that by 2025 the organic recycling of bio-waste from municipal waste shall be increased to a minimum of 65% by weight.”

EU Parliament amendments - 3

Separate collection

“Member States shall set up systems for the separate collection at source of bio-waste by 31 December 2020 to ensure the relevant quality standards for compost and digestate and to attain [the MW recycling targets].”

NB the reference to TEEP in the Commission proposal is deleted in the EP amendment

ESA’s Bio-Waste Strategy

Focus on full value chain

Bio-waste hierarchy

AD as recycling

Monitor for quality

Food waste prevention

Bio-waste collections

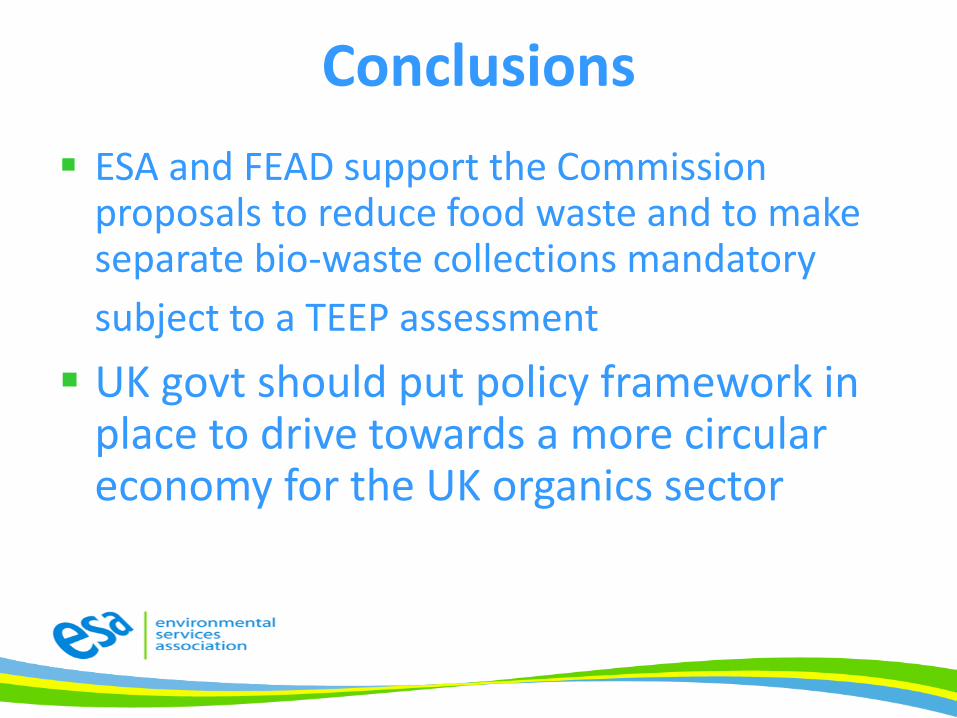

Conclusions

ESA and FEAD support the Commission proposals to reduce food waste and to make separate bio-waste collections mandatory

subject to a TEEP assessment

UK govt should put policy framework in place to drive towards a more circular economy for the UK organics sector

The EU Circular Economy Package and its impact on AD

Thank you for your attention!

Roy HathawayEurope Policy Advisor

Environmental Services [email protected]

Ecomondo and Key Energy have always encouraged interaction between producers, industrial firms, associations andresearchers, evolving awareness of the strategic value of "Biogas Refinery", which has become one of the maindrivers of the event. Ecomondo will provide the optimum setting for all sector stakeholders, with their synergies andtechnological excellence, to compare decision-makers on issues of energy transition and the decarbonisation of theItalian production system. This, according to the position paper signed with SNAM towards a decarbonisationstrategy, that Italian industry players have begun to build up, as well as ENEL, that will increase the efficientmanagement of OFMSW and anaerobic digestion for the production of biomethane.

NEW FOCUS in 2016 edition: “Methane-biomethane. Italian excellence"

Targets involved in the project:• Production (Agriculture: CIB, main partners -CONFAGRICOLTURA, OFMSW: CIC, UTILITALIA)• Industry (FCA, CNH, LANDI, BRC)• Distribution (SNAM; ANIGAS)• Transport (ASSOGASMETANO).• The markets for methane (mobility, cogeneration,heat), traction and methane energy "tradition"• A new process towards the greening of the gasnetwork: from methane to biomethane, their use in theautomotive sector• Placement on the network and extra-networktransport of biomethane: CNG, LNG

For further information, contact: Lucia Gurnari (+39) 0541/744615 [email protected]

QUESTIONS AND COMMENTS FROM THE FLOOR

CASE STUDIES: FOOD WASTE

COLLECTIONS FROM AROUND THE

WORLD

DR DAVID GREENFIELD, MANAGING DIRECTOR, SOENECS

DR PAUL, BIOCOLLECTORS

JULIAN O’NEILL, CEO, BIOGEN

PETER JONES, SENIOR CONSULTANT, EUNOMIA

ALBERTO CONFALONIERI, CHAIR OF THE TECHNOCAL COMMITTEE, ITALIAN

COMPOSTING AND BIOGAS ASSOCIATION

DIARMID JAMEISON, SLR CONSULTING

Food waste operations from around the world

Food Waste Collections

Where to Look for Good Examples

Peter Jones

Principal Consultant

Eunomia Research & Consulting

7th July 2016

Agenda

1. Commercial Food Waste – Japan,

Scotland

2. Household Food Waste – Variations

3. Conclusions

Japan

• Creating a market

• Food Waste Act 2000• Agricultural businesses are required to use recycled

fertilizers and feed

• Driving diversion

• Food Recycling Act• Mandates that businesses take measures to promote the

recycling of food resources

• Mandatory plans, escalating targets

• Claimed 82% recycling rate for food waste across the C&I sector

• Principally driven by manufacturing sector

• Has increased self sufficiency and cut farmers’ costs

Scotland

• Has driven diversion

• Waste (Scotland) Regulations• Mandates that businesses separate food waste for

collection

• This is cutting the cost of collections

• BUT – No mandatory plans or targets, and little enforcement

• Less effective in creating a market

• Shortage of AD facilities

• Regs makes use as animal feed problematic

• Lack of commercial waste stats to assess impact

England

• Mandating commercial food collections would transform the market

• Better logistics

• Cheaper collections

• Food businesses would save

• We already have the AD plants!

• Could achieve much the same effect through waste hierarchy enforcement

• Could also stimulate end markets

• Incentives to use recycled products

Household Collections

• 45% of English councils do not offer

separate food waste collections, or

food/garden

• All authorities in Wales offer them!

• Barriers?

• Huge variation in performance

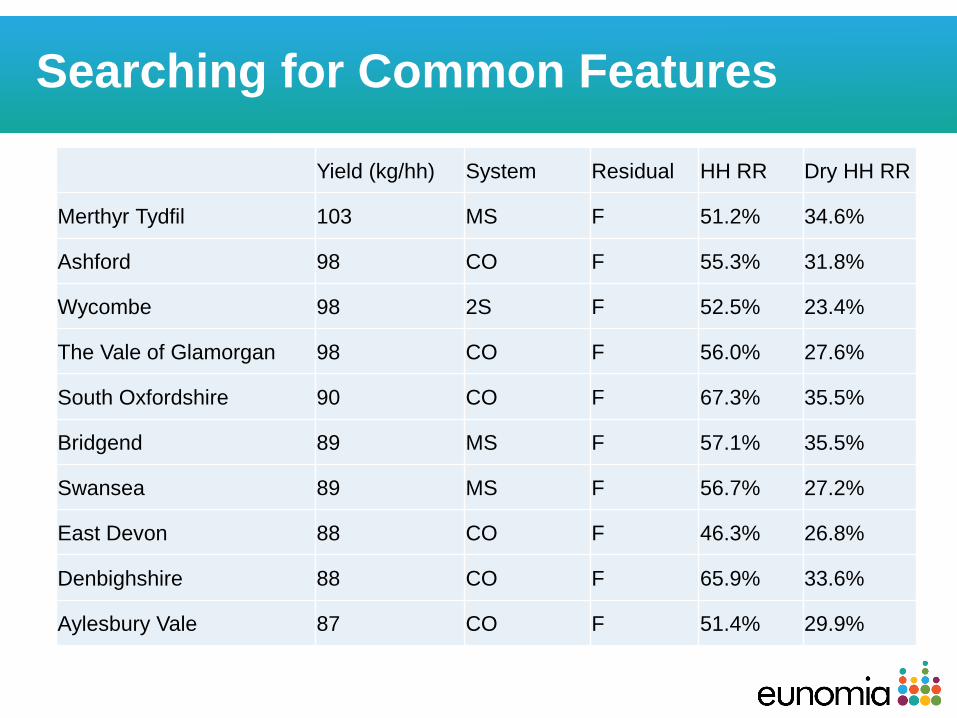

Range of Food Waste Yields (Kg/hh)

Searching for Common Features

Yield (kg/hh) System Residual HH RR Dry HH RR

Merthyr Tydfil 103 MS F 51.2% 34.6%

Ashford 98 CO F 55.3% 31.8%

Wycombe 98 2S F 52.5% 23.4%

The Vale of Glamorgan 98 CO F 56.0% 27.6%

South Oxfordshire 90 CO F 67.3% 35.5%

Bridgend 89 MS F 57.1% 35.5%

Swansea 89 MS F 56.7% 27.2%

East Devon 88 CO F 46.3% 26.8%

Denbighshire 88 CO F 65.9% 33.6%

Aylesbury Vale 87 CO F 51.4% 29.9%

Conclusions

• Japan shows us just how far C&I food

waste recycling can go

• If England adopted the same approach as

Scotland (and NI, and soon Wales), it could

make considerable progress

• For local authorities

• Separating food waste need not be costly

• Yield is key

• We know which authorities are doing well

• Let’s do more to analyse why!

Successful implementation of separate collection

of food waste in urban areas

07/07/2016UK AD&Biogas

Alberto Confalonieri, Marco Ricci-Jürgensen CIC – Italian Composting and Biogas Association- Rome-Italy

www.compost.it

Keywords for a successful implementation

• Large and constant participation

• high capture rates

• Good quality (i.e. low content of impurities)

• Economical sustainability

Keywords for a successful implementation

• Large and constant participation

• high capture rates

• Good quality (i.e. low content of impurities)

• Economical sustainability

The need for kitchen-caddies?

• Limited volume (6 -12 liters):– prevent mixture with MSW

– small and manageable

• Vented caddies:– Allow to collect cooked food too . . .

– reduction of odours, moisture, weight

• Bags/liners should be compostable (complying with CEN standard EN 13432)

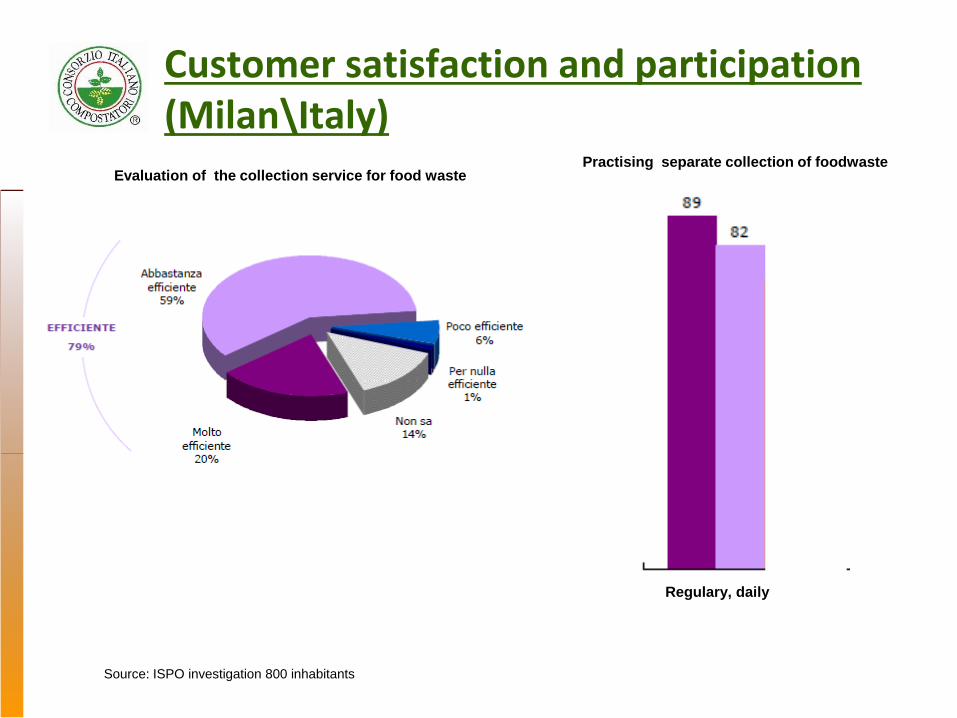

Customer satisfaction and participation (Milan\Italy)

Source: ISPO investigation 800 inhabitants

Evaluation of the collection service for food wastePractising separate collection of foodwaste

Regulary, daily

Keywords for a successful implementation

• Large and constant participation

• high capture rates

• Good quality (i.e. low content of impurities)

• Economical sustainability

www.compost.it

Peculiarities of biowaste separate collection• Focus intensive source separation schemes on food waste only

• Foodwaste (including cooked

food) collected 2-4 times/week

• Garden waste is collected at

bring sites or doorstep at lower

frequency (weekly or

fortnightly)

• Residual waste collection

with lower frequency than

foodwaste (in order to

discourage organic waste

in residual waste)

Milan Metropolitan Area

Population 1.5 M inhab

Density 5-7.000 inhab/km2

Italy’s most vital Economical center

Transient population

Year 2012: food waste collection at Ho.Re.Ca sector only 23kg/inhab/yr

Separate collection 34,5% (2012)

AMSA is the Public company responsible for MSW management in Milan

Milan Metropolitan Area

Year 2014: kerbside collection in the whole city 91kg/inhab/yr

Separate collection 49,9% (2014)

Municipality of Milan

.

Prompt results after the implementation

Recycling of 130,000 t/y of foodwaste (2014/2015)

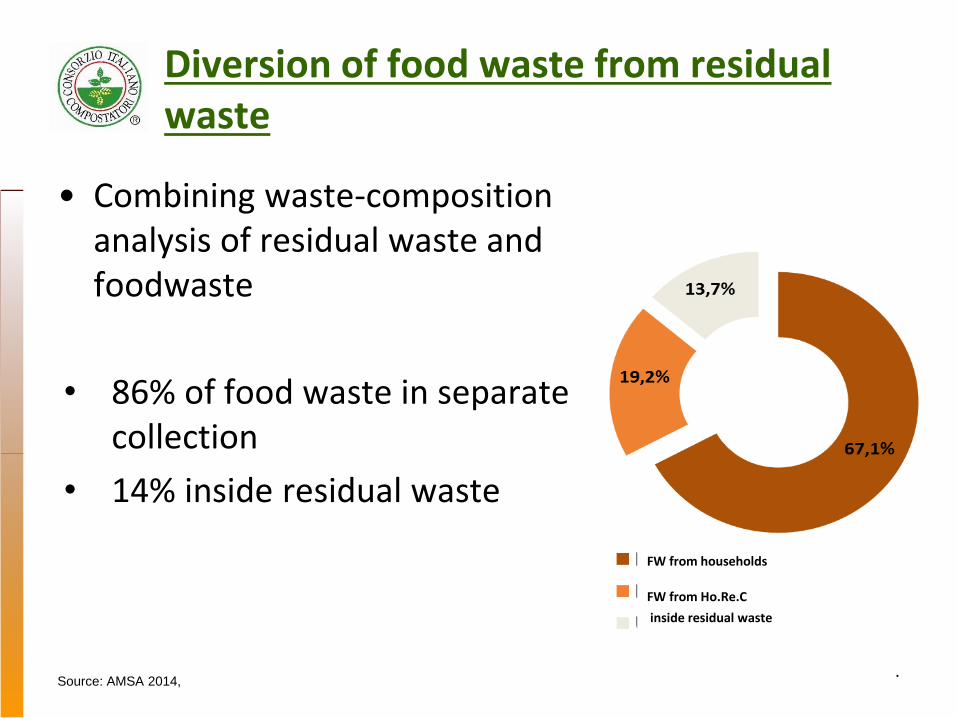

Diversion of food waste from residual waste

• Combining waste-composition analysis of residual waste and foodwaste

• 86% of food waste in separate collection

• 14% inside residual waste

.

FW from households

FW from Ho.Re.C

inside residual waste

Source: AMSA 2014,

Keywords for a successful implementation

• Large and constant participation

• high capture rates

• Good quality (i.e. low content of impurities)

• Economical sustainability

Quality of food waste (non-compostable content)

102Analysis performed by CIC

Average4,27% ± 2,95%

City-center Sub-urbs Social-housing Average

2 months

8 months

14 months

Average

Source: AMSA 2014,

Quality of food waste (non-compostable content)

103impurities inside food waste delivered to CIC’s composting and AD plants - year 2015

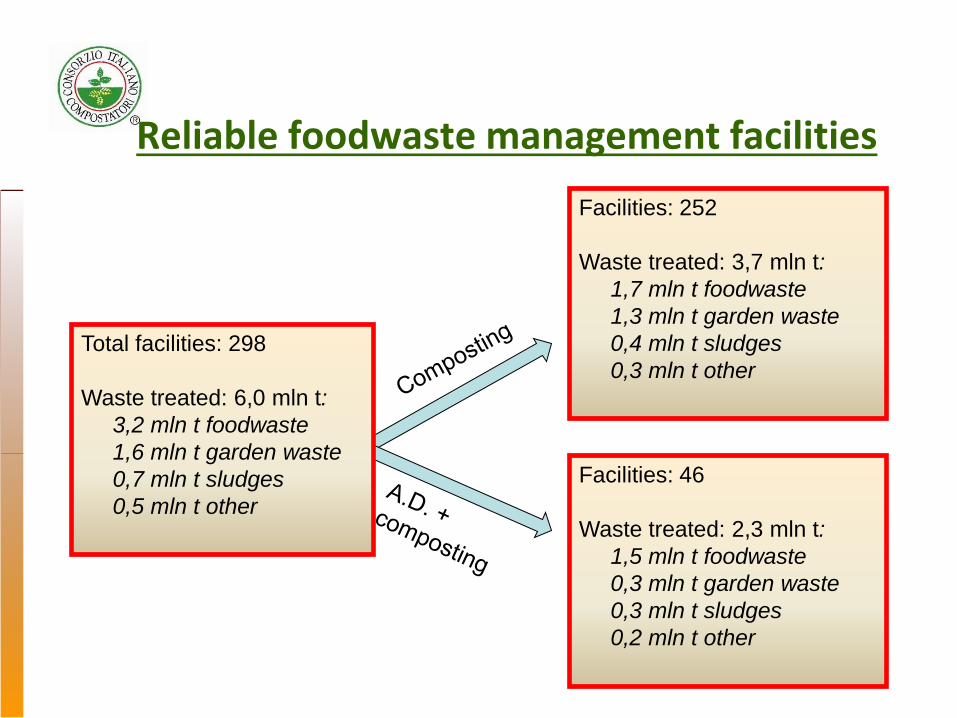

Reliable foodwaste management facilities

Facilities: 252

Waste treated: 3,7 mln t:

1,7 mln t foodwaste

1,3 mln t garden waste

0,4 mln t sludges

0,3 mln t other

Facilities: 46

Waste treated: 2,3 mln t:

1,5 mln t foodwaste

0,3 mln t garden waste

0,3 mln t sludges

0,2 mln t other

Total facilities: 298

Waste treated: 6,0 mln t:

3,2 mln t foodwaste

1,6 mln t garden waste

0,7 mln t sludges

0,5 mln t other

Keywords for a successful implementation

• Large and constant participation

• high capture rates

• Good quality (i.e. low content of impurities)

• Economical sustainability

MSW management costs are stable despite the increasing complexity of MSW management

Region Veneto (Italy); data evaluated by the Author; 2009

Milan waste costs

• The overall scheme for the City of Milan is cost-neutral

• The waste cost (Financial Plan of AMSA) remained substantially unchanged between 2013/2014, compared to the increase of life INDEX in Italy

• Average cost in Lombardy for MSW disposal 95€/ton

• Avarage cost in Milan for Food waste composting 72-74€/ton

Conclusions

• Separate collection of food waste is widespread in Italy, and shown to be possible even in large cities; it reaches outstanding results (Milan: 91 kg/inhab/yr)

• Vented kitchen-caddy & compostable bio-bags (EN13342 certified) increase acceptance and participation

• Low contamination of feedstock is the key-element for producing quality compost and digestate allowing for recycling at AD/C plant

• Total MSW management cost are found to be non-increasing compared to “low-recycling” municipalities, especially in the medium term considering the increase of disposal costs

Thank you

Italian Composting and Biogas Association

Insight into California: – organic waste / AD sector development

Diarmid Jamieson

Technical Director, SLR Consulting Ltd

7th July 2016

Working in Diverse Business Areas

Minerals Infrastructure Energy

Industry Planning and

DevelopmentWaste

Introduction

SLR international presence (Europe, N. America, Southern Africa and

Australasia) and operations include offices and projects on the US and

Canadian Pacific seaboard.

Our Californian operations (Oakland and Irvine) include recent solid waste

projects for public & private sector clients in the state.

Organics Collection:California:• c.40 million population (most populous US

state) and 3rd largest in area;

• 6th largest economy (GDP) in the world;

• State has diverse range of climatic zones and

an extensive arable/orchards agricultural sector;

• CA has some of the most progressive

environmental legislation and renewable energy

targets in the US;

• Includes generating 1/3 of electricity from

renewable sources by 2020.

Waste Organics Sector:• State has well-established green / yard waste

collection system (>20 years) with strong

demand for quality compost from agricultural /

horticultural end-users, orchards etc.

• Collection services fully privatised but contracts

are organised/managed by city/county

authorities;

• Food waste collection started c.10 years ago in

San Francisco but changes in CA state

legislation since 2011 is driving trend for

separate collection of food waste for AD;

• Estimated 6 million tonnes / a of municipal food

waste available.

Key Drivers for Development of

AD:• Energy - security and renewables;

• State policies / legislation;

• Availability of feedstocks & end-users;

• Increasing cost / scarcity of landfill.

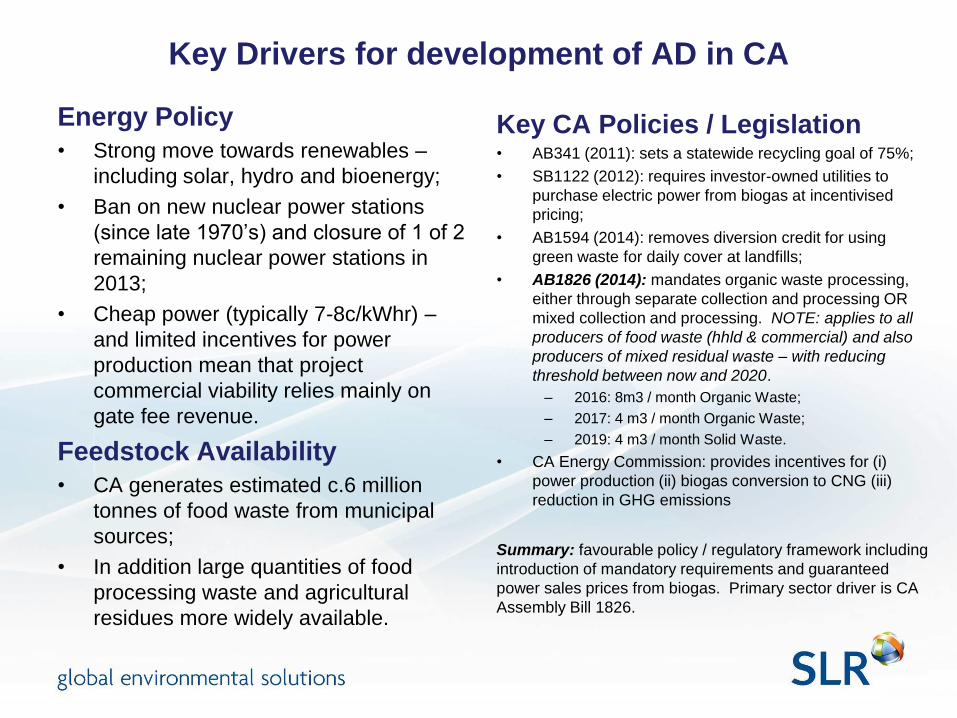

Key Drivers for development of AD in CA

Energy Policy

• Strong move towards renewables –

including solar, hydro and bioenergy;

• Ban on new nuclear power stations

(since late 1970’s) and closure of 1 of 2

remaining nuclear power stations in

2013;

• Cheap power (typically 7-8c/kWhr) –

and limited incentives for power

production mean that project

commercial viability relies mainly on

gate fee revenue.

Feedstock Availability

• CA generates estimated c.6 million

tonnes of food waste from municipal

sources;

• In addition large quantities of food

processing waste and agricultural

residues more widely available.

Key CA Policies / Legislation• AB341 (2011): sets a statewide recycling goal of 75%;

• SB1122 (2012): requires investor-owned utilities to

purchase electric power from biogas at incentivised

pricing;

• AB1594 (2014): removes diversion credit for using

green waste for daily cover at landfills;

• AB1826 (2014): mandates organic waste processing,

either through separate collection and processing OR

mixed collection and processing. NOTE: applies to all

producers of food waste (hhld & commercial) and also

producers of mixed residual waste – with reducing

threshold between now and 2020.

– 2016: 8m3 / month Organic Waste;

– 2017: 4 m3 / month Organic Waste;

– 2019: 4 m3 / month Solid Waste.

• CA Energy Commission: provides incentives for (i)

power production (ii) biogas conversion to CNG (iii)

reduction in GHG emissions

Summary: favourable policy / regulatory framework including

introduction of mandatory requirements and guaranteed

power sales prices from biogas. Primary sector driver is CA

Assembly Bill 1826.

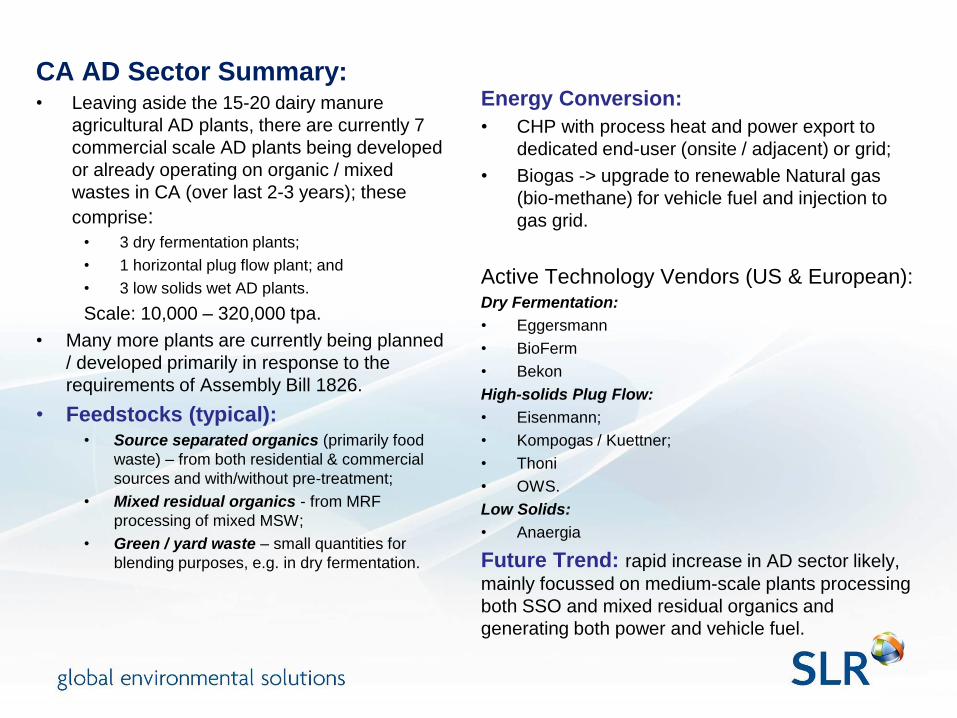

CA AD Sector Summary:• Leaving aside the 15-20 dairy manure

agricultural AD plants, there are currently 7

commercial scale AD plants being developed

or already operating on organic / mixed

wastes in CA (over last 2-3 years); these

comprise:• 3 dry fermentation plants;

• 1 horizontal plug flow plant; and

• 3 low solids wet AD plants.

Scale: 10,000 – 320,000 tpa.

• Many more plants are currently being planned

/ developed primarily in response to the

requirements of Assembly Bill 1826.

• Feedstocks (typical):• Source separated organics (primarily food

waste) – from both residential & commercial

sources and with/without pre-treatment;

• Mixed residual organics - from MRF

processing of mixed MSW;

• Green / yard waste – small quantities for

blending purposes, e.g. in dry fermentation.

Energy Conversion:

• CHP with process heat and power export to

dedicated end-user (onsite / adjacent) or grid;

• Biogas -> upgrade to renewable Natural gas

(bio-methane) for vehicle fuel and injection to

gas grid.

Active Technology Vendors (US & European):Dry Fermentation:

• Eggersmann

• BioFerm

• Bekon

High-solids Plug Flow:

• Eisenmann;

• Kompogas / Kuettner;

• Thoni

• OWS.

Low Solids:

• Anaergia

Future Trend: rapid increase in AD sector likely,

mainly focussed on medium-scale plants processing

both SSO and mixed residual organics and

generating both power and vehicle fuel.

CR&R, Perris ZWEDC, San Jose

Zero Waste Energy Development Company

• Mixed Waste

• 90,000 tpa;

• Eggersmann dry fermentation process;

• Output = power and compost;

• Operational.

CR&R

• Mixed waste & Source Segregated

Organics (SSO);

• 320,000 tpa

• 4 x modules @ 80,000 tpa;

• Eisenmann high-solids horizontal plug flow

digesters;

• Output = biogas -> CNG and compost;

• Phase 1 at commissioning.

Summary

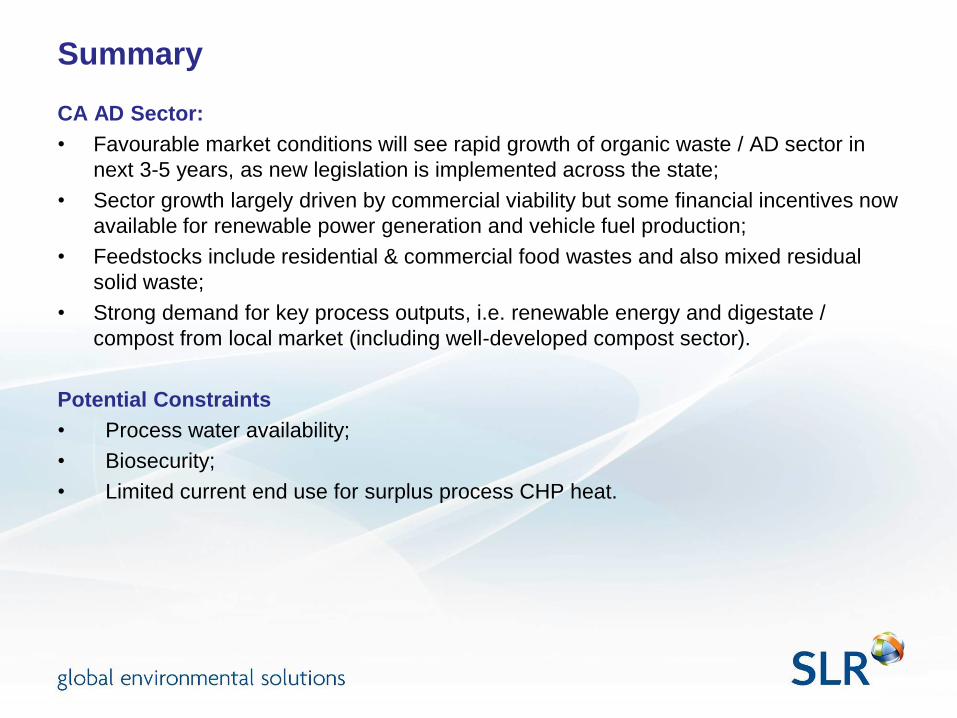

CA AD Sector:

• Favourable market conditions will see rapid growth of organic waste / AD sector in

next 3-5 years, as new legislation is implemented across the state;

• Sector growth largely driven by commercial viability but some financial incentives now

available for renewable power generation and vehicle fuel production;

• Feedstocks include residential & commercial food wastes and also mixed residual

solid waste;

• Strong demand for key process outputs, i.e. renewable energy and digestate /

compost from local market (including well-developed compost sector).

Potential Constraints

• Process water availability;

• Biosecurity;

• Limited current end use for surplus process CHP heat.

Useful Links

• www.biogasassociation.ca

• www.bioenergyca.org

Thank You

Diarmid Jamieson

Technical Director

SLR Consulting Limited

Tel: 0044 131 335 6830

Mob: 0044 7879 814265

Email: [email protected]

Website: www.slrconsulting.com

QUESTIONS AND COMMENTS FROM THE FLOOR

WHAT CHALLENGES AND OPPORTUNITIES

DOES THE DE-REGULATION OF THE

WATER SECTOR HOLD FOR AD?

DR PIERS CLARK, ISLE GROUP

ALISON FERGUSSON, PRINCIPAL ENGINEER – WATER 2020 PROGRAMME, OFWAT

STEVE BUNGAY, CHAIR – WASTEWATER MANAGEMENT PANEL, CIWEM

RICHARD LAIKIN, UK WATER SECTOR LEADER, PWC

Trust in water 122

What challenges and opportunities does the de-regulation of the water sector hold for AD?

Alison Fergusson

July 2016

Trust in water 123

Agenda

Who is Ofwat?

Our role and drivers of change

What’s going on for Ofwat?

What do we mean by “deregulation”?

Why do we think we should introduce markets in sludge?

Key features of Ofwat’s May decision for the way we regulate sludge from 2019:

Publishing information

Transparent market activity

Binding separate price control

Trust in water 124

Ofwat is the economic regulator of the water industry

in England and Wales.

Our key duties:

protect the interests of consumers, wherever

appropriate by promoting effective competition.

secure finance for efficient companies so that they can

properly carry out their functions.

(in relation to English water companies) secure the

long-term resilience of water supply and wastewater

systems so that the needs of customers in the long

term are met.

Ofwat’s role within England and Wales

Government

Defra

Ofgemetc.

Othergroups

NGOs

Europe

Sector Regulators

Environ-ment

Agency

UNECE

EWP

EU

CCWater

Academics

DWI

NaturalEngland

CabinetOffice

Welsh Gov

NaturalResources

Wales

OfwatTrust in water

Other sector

regulators

UKRN

Trust in water 125

Ofwat’s vision and the drivers for change

Trust in water 126

What’s going on for Ofwat?

Trust in water 127

What if we didn’t change our regulation of sludge?

Incremental improvements, saving a few ££?

Optimised

thickness

and

company

transport

costs

More efficient

process

operation and

energy

generation

Optimised in-

company

sludge

movements

Trialling

Innovative

processes

Improved

products for

farmers –

more income

Occasional

exploration

of using third

parties

What do we mean by sludge?

Sludge = activities of sewage sludge transport,

treatment, recycling and disposal. It includes dealing

with liquors generated during treatment.

National Audit Office (October 2015) shows that the impact

on bills of our regulatory approach has fallen over time. This

is partly due to diminishing returns to this form of regulation.

Trust in water 128

There is scope to use markets because…

Potential gains from local market between WaSCs.

Unrealised gains from market with firms in wider

waste markets.

Relatively less stranded asset risk - shorter asset

lives.

1

2

4

Dynamically increasing demand over time - change

in biosolids use and technology.

3

We have analysed the scope for trades between

companies by geography.

We have surveyed potential entrants.

We have examined investment requirements.

We have analysed usage patterns over time.

We know this because…

Why do we think there is scope to use markets in sludge?

What needs to be addressed in order to realise benefits?

Within our influence / control Outside our influence / control

Missing information

Regulatory incentives

Cultural issues

Environmental regulations

Transport costs

Consistent

with 2011

OFT study.

Evidence supports encouraging sludge markets

Trust in water 129

Localised market between WaSCs: rival WaSCs operating STCs within 50km

1

Trust in water 130

Rate of change in sludge treatment and recycling

3

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2010-11 2011-12 2012-13 2013-14 2014-15

Total other including landfill

Through a third party sludge service provider

Phyto-conditioning/composting

Incineration of raw sludge

Raw sludge liming

Incineration of digested sludge

Advanced anaerobic digestion

Conventional anaerobic digestion

UK sludge re-use and disposal routes – tonnes dry solids

Reuse or disposal

routeOthers Sludge reused Sludge disposed Total

Pipelines ShipsSoil and

agricultureOthers Landfill Incineration Others

1992 8,430 273,158 440,137 32,100 129,748 89,800 24,300 997,673

2008 - - 1,241,639 90,857 10,882 185,890 1,523 1,530,779

2010 - - 1,118,159 23,385 8,787 259,642 2,863 1,412,836

England and Wales treatment processes employed

Trust in water 131

Lower risk of stranded assets

4Average asset lives

49

37 36

30

13

0

10

20

30

40

50

60

Waterresources

Watertreatment

Sewagetreatment

Sludgetreatment

Sludgedisposal

Ave

rag

e a

ss

et

live

s (

ye

ars

)

Trust in water 132

Sludge market model: making the best sludge decisions for customers and the environment

Townsville

WwTW, WaSC X

Bigtown STC,

WaSC X

Supertown STC,

WaSC Y.

Novel Tech Co

Commercial

waste co.

Energy

users

Farmers

Energy

users

Farmers

Energy

users

Farmers

??

Trust in water 133

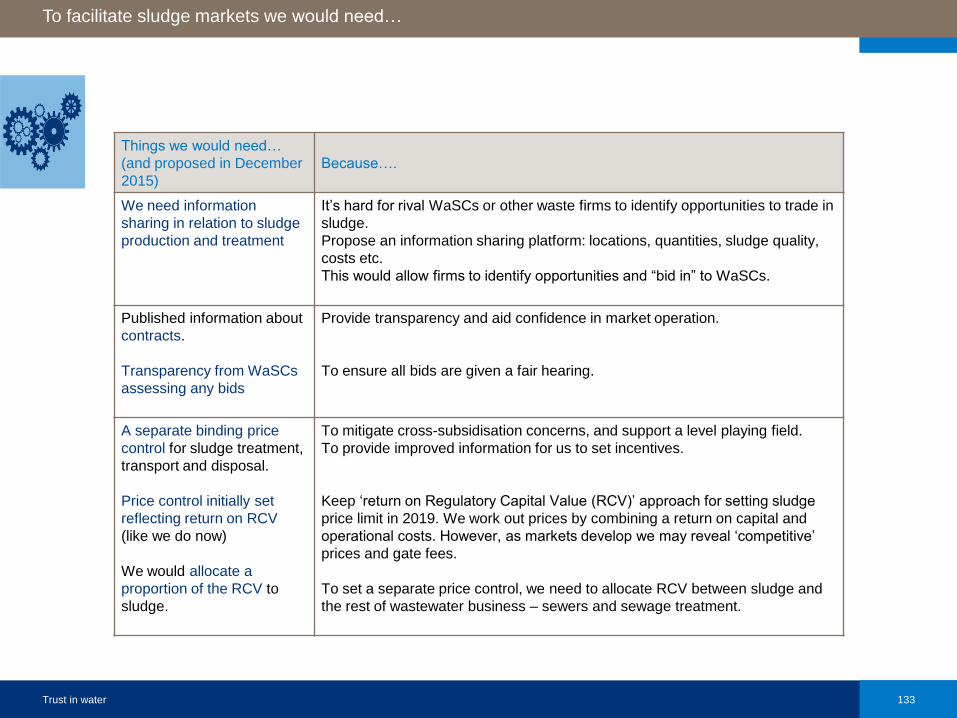

Things we would need…

(and proposed in December

2015)

Because….

We need information

sharing in relation to sludge

production and treatment

It’s hard for rival WaSCs or other waste firms to identify opportunities to trade in

sludge.

Propose an information sharing platform: locations, quantities, sludge quality,

costs etc.

This would allow firms to identify opportunities and “bid in” to WaSCs.

Published information about

contracts.

Transparency from WaSCs

assessing any bids

Provide transparency and aid confidence in market operation.

To ensure all bids are given a fair hearing.

A separate binding price

control for sludge treatment,

transport and disposal.

Price control initially set

reflecting return on RCV

(like we do now)

We would allocate a

proportion of the RCV to

sludge.

To mitigate cross-subsidisation concerns, and support a level playing field.

To provide improved information for us to set incentives.

Keep ‘return on Regulatory Capital Value (RCV)’ approach for setting sludge

price limit in 2019. We work out prices by combining a return on capital and

operational costs. However, as markets develop we may reveal ‘competitive’

prices and gate fees.

To set a separate price control, we need to allocate RCV between sludge and

the rest of wastewater business – sewers and sewage treatment.

To facilitate sludge markets we would need…

Trust in water 134

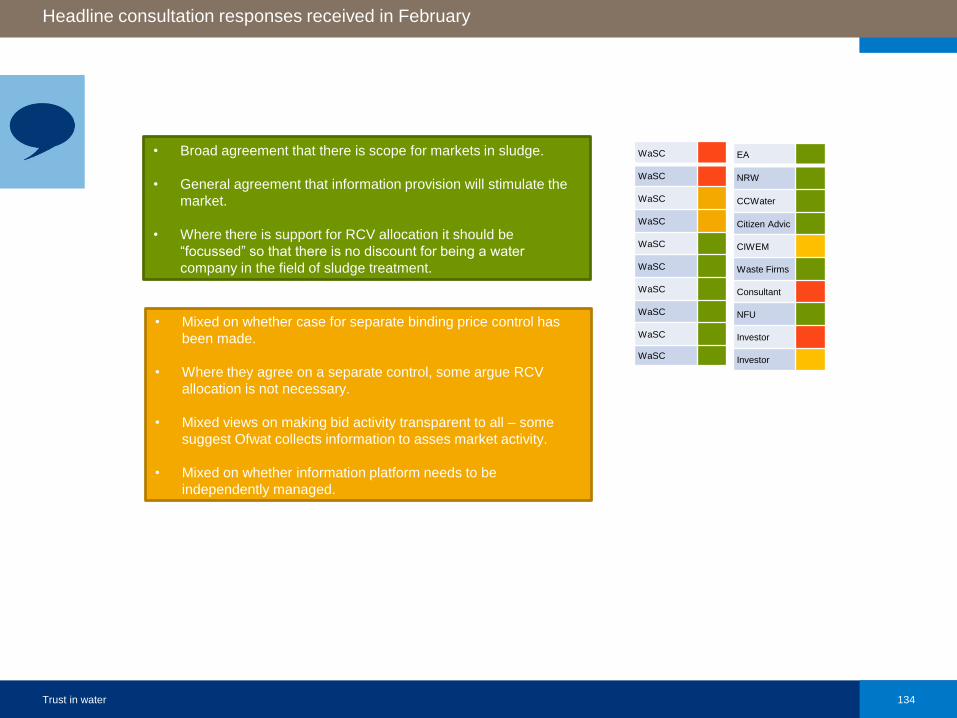

Headline consultation responses received in February

WaSC

WaSC

WaSC

WaSC

WaSC

WaSC

WaSC

WaSC

WaSC

WaSC

EA

NRW

CCWater

Citizen Advic

CIWEM

Waste Firms

Consultant

NFU

Investor

Investor

• Broad agreement that there is scope for markets in sludge.

• General agreement that information provision will stimulate the

market.

• Where there is support for RCV allocation it should be

“focussed” so that there is no discount for being a water

company in the field of sludge treatment.

• Mixed on whether case for separate binding price control has

been made.

• Where they agree on a separate control, some argue RCV

allocation is not necessary.

• Mixed views on making bid activity transparent to all – some

suggest Ofwat collects information to asses market activity.

• Mixed on whether information platform needs to be

independently managed.

Trust in water 135

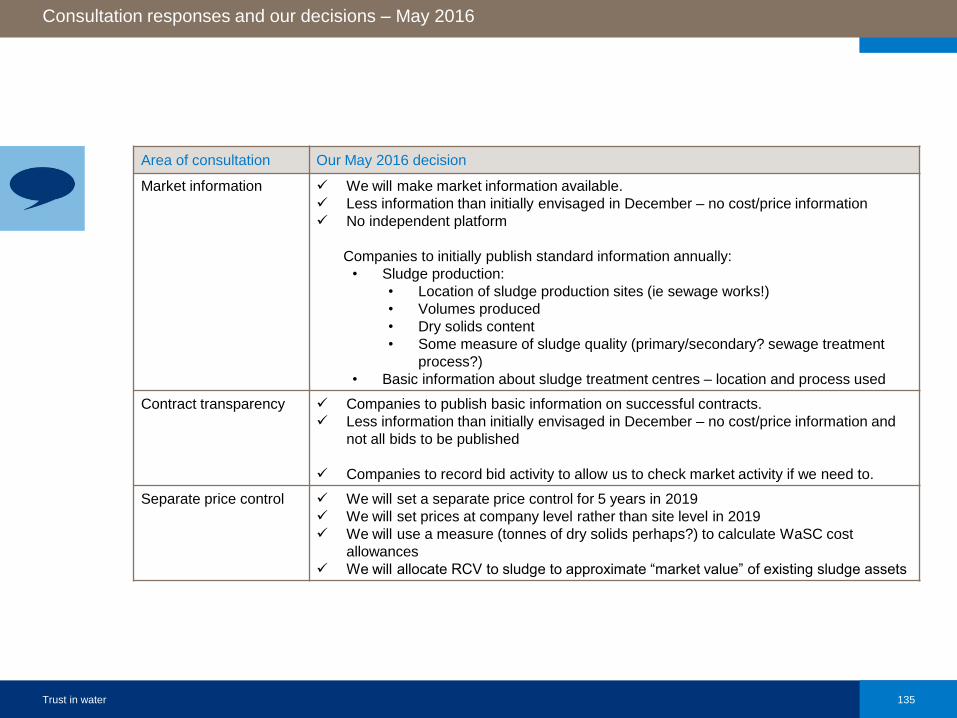

Area of consultation Our May 2016 decision

Market information We will make market information available.

Less information than initially envisaged in December – no cost/price information

No independent platform

Companies to initially publish standard information annually:

• Sludge production:

• Location of sludge production sites (ie sewage works!)

• Volumes produced

• Dry solids content

• Some measure of sludge quality (primary/secondary? sewage treatment

process?)

• Basic information about sludge treatment centres – location and process used

Contract transparency Companies to publish basic information on successful contracts.

Less information than initially envisaged in December – no cost/price information and

not all bids to be published

Companies to record bid activity to allow us to check market activity if we need to.

Separate price control We will set a separate price control for 5 years in 2019

We will set prices at company level rather than site level in 2019

We will use a measure (tonnes of dry solids perhaps?) to calculate WaSC cost

allowances

We will allocate RCV to sludge to approximate “market value” of existing sludge assets

Consultation responses and our decisions – May 2016

Trust in water 136

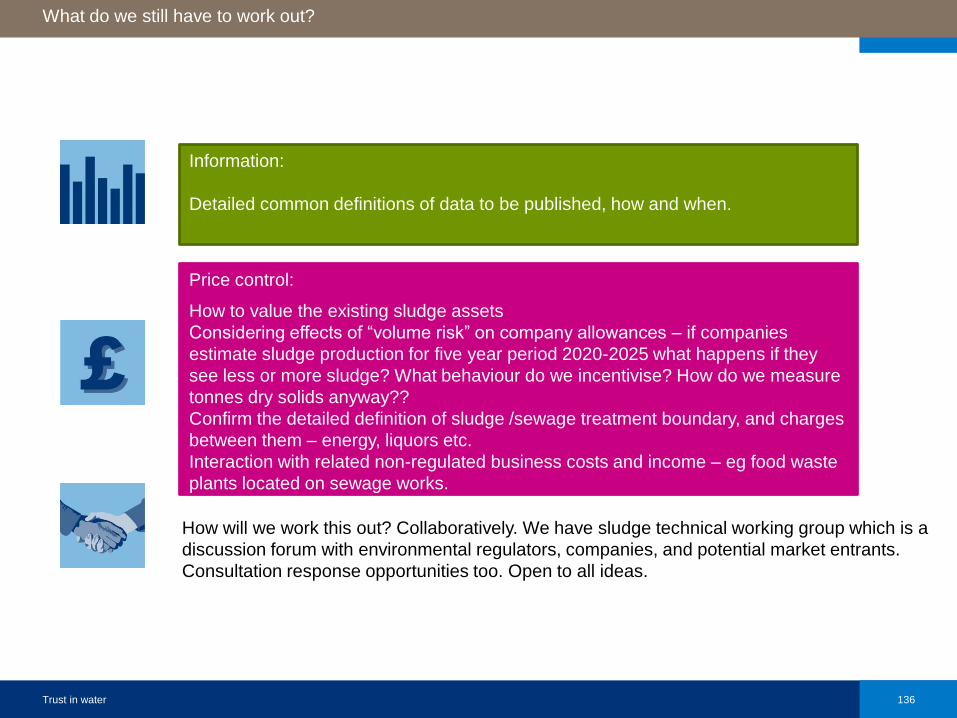

What do we still have to work out?

How will we work this out? Collaboratively. We have sludge technical working group which is a

discussion forum with environmental regulators, companies, and potential market entrants.

Consultation response opportunities too. Open to all ideas.

Information:

Detailed common definitions of data to be published, how and when.

Price control:

How to value the existing sludge assets

Considering effects of “volume risk” on company allowances – if companies

estimate sludge production for five year period 2020-2025 what happens if they

see less or more sludge? What behaviour do we incentivise? How do we measure

tonnes dry solids anyway??

Confirm the detailed definition of sludge /sewage treatment boundary, and charges

between them – energy, liquors etc.

Interaction with related non-regulated business costs and income – eg food waste

plants located on sewage works.

Trust in water 137

www.ofwat.gov.uk

Twitter.com/Ofwat

Thank you and questions

Challenges and Opportunitiesof De-regulation of Sludge

Treatment

Steve Bungay, CIWEM Wastewater Management Panel

Challenges to De-regulation

Disparate Regulation• Sewage Sludge

• Biosolids

• Other Organic Waste

The Final Stakeholder• Protecting Farmers Fields

Regulation

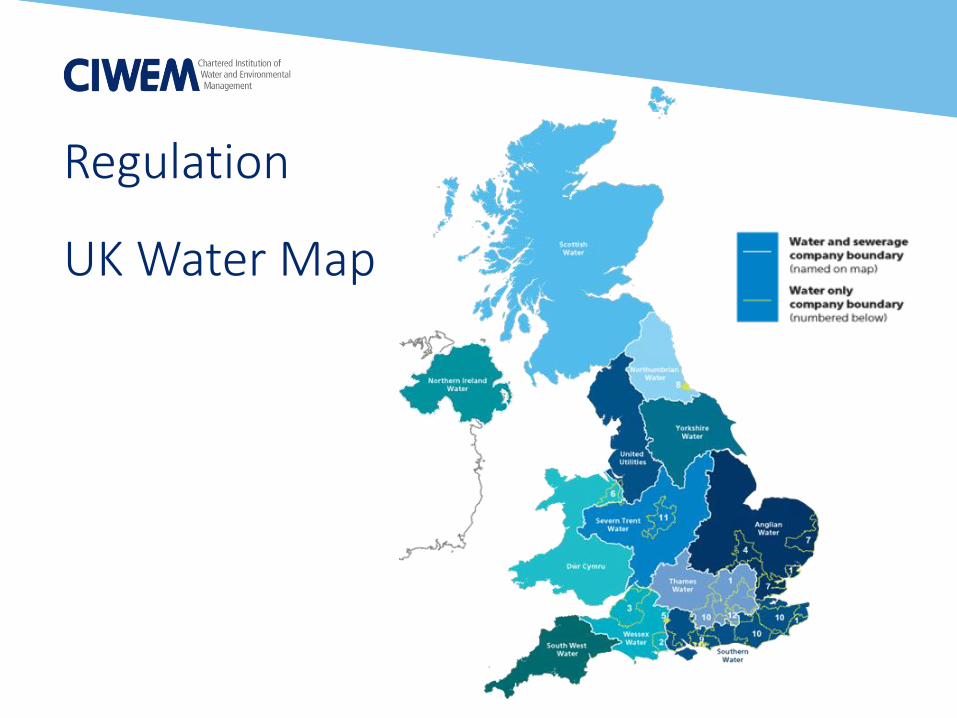

UK Water Map

Regulation

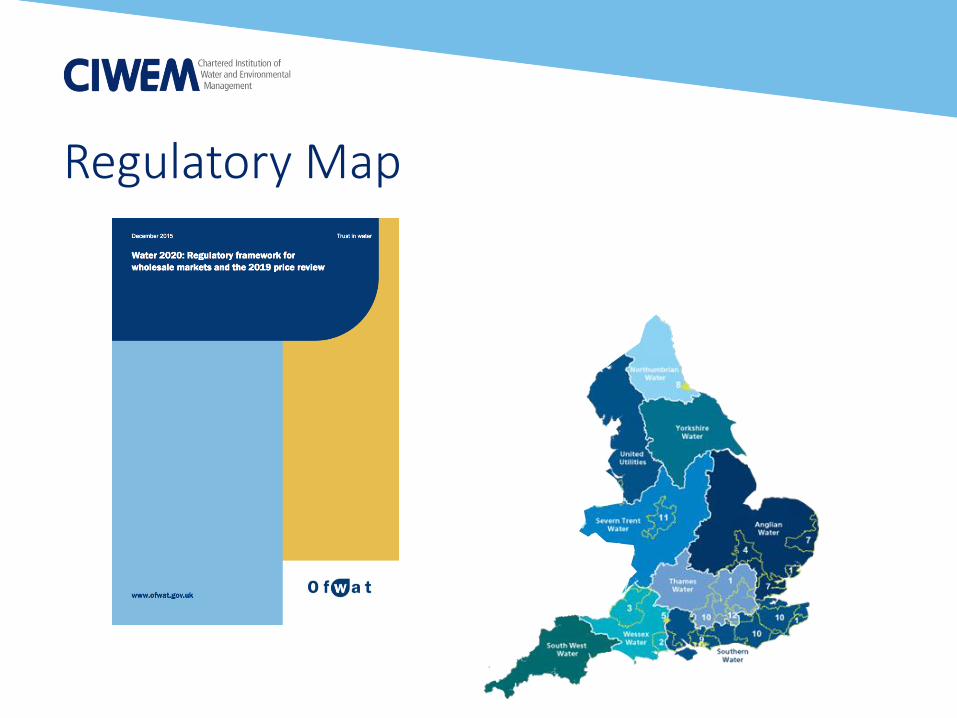

Regulatory Map

Regulatory Map

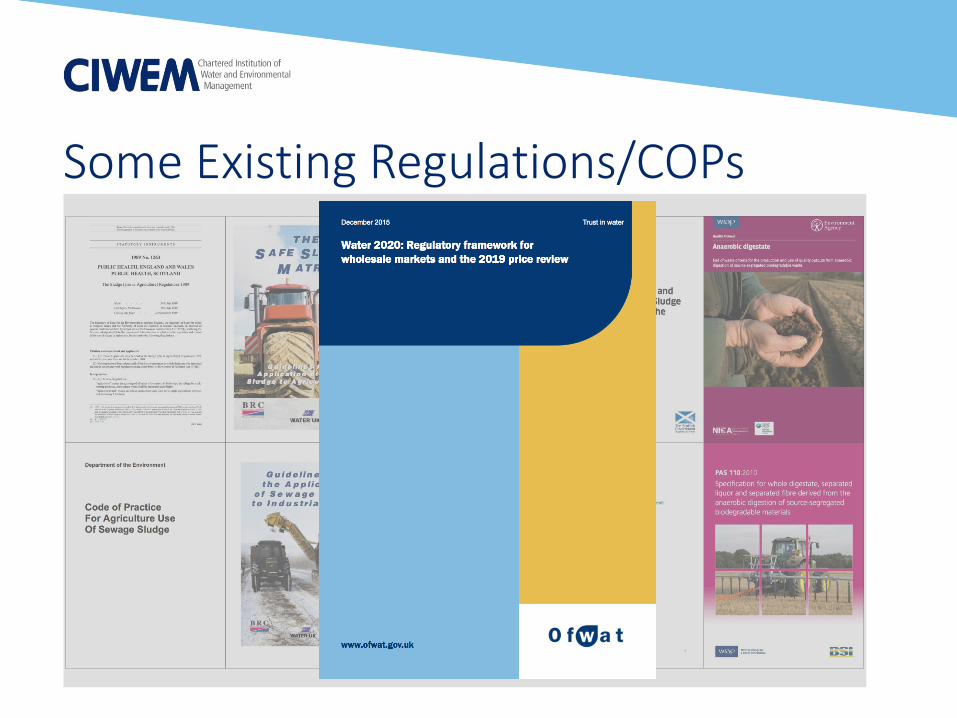

Some Existing Regulations/COPs

Some Existing Regulations/COPs

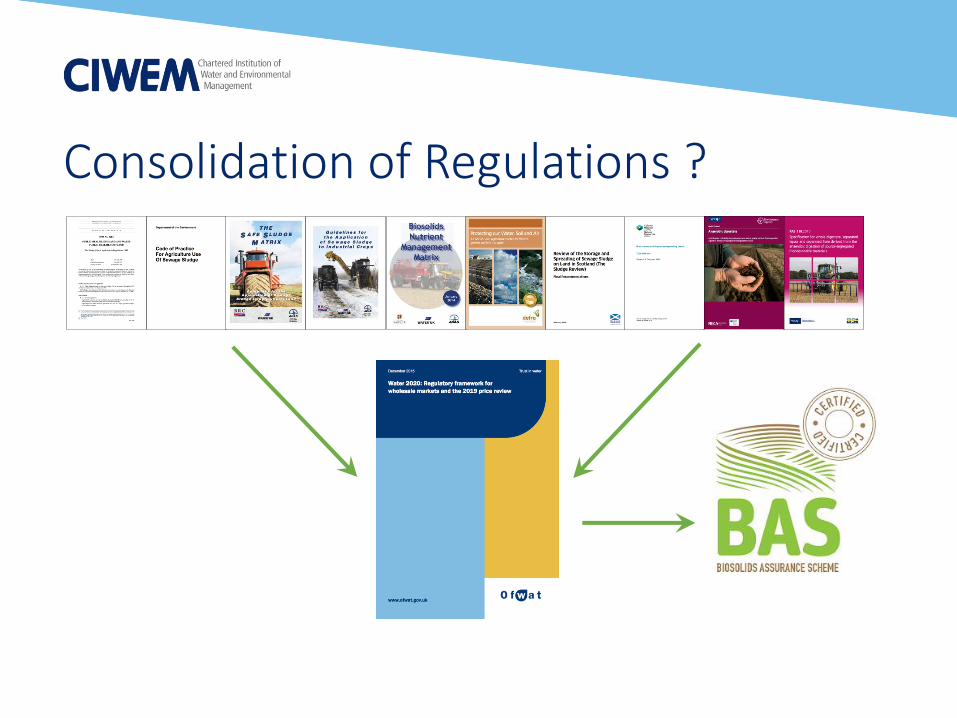

Consolidation of Regulations ?

The Final Stakeholder

Protecting the Farmer’s Fields

Protecting the Farmer’s Fields

Protecting the Farmer’s Fields

Opportunities

Opportunities

Opportunities

Realising the Potential

• De-regulation presents opportunities and challenges to the water industry

• Integrating the skills from the water industry and waste industry, using pragmatic regulation, will realise the greatest potential from the de-regulated sludge market

• Ultimately, we must not lose site that as Regulators, Engineers, Scientists, Business People, Politicians etc…

…we are custodians of the environment

• Working for the public benefit for sustainable future

Thank you

QUESTIONS AND COMMENTS FROM THE FLOOR

MAKING BIOMETHANE FOR TRANSPORT

PROFITABLE – POLICY, SUBSIDIES, AND

INDUSTRY COLLABORATION

THOMAS KOLLER, POLICY OFFICER, ADBA

ROB WOOD, CHIEF EXECUTIVE, GASREC

JONATHAN HOOD, SENIOR POLICY ADVISOR – LOW CARBON FUELS, DFT

OLLIE MORE, MARKET ANALYST, ADBA

JOHN BICKERTON, CHIEF ENGINEER, READING BUSES

Making biomethane for transport profitable - policy, subsidies, and industry collaborationJuly 16

Gasrec is the largest supplier of LNG to road transport in EuropeDIRFT refuelling around 210 vehicles per day from 35 per day in April 2013

The case for methane in road transport

CO2e NOx Cost

15% 35% 70%

Reduction versus Euro 6 diesel

Natural gas

CO2e

90%

Bio-methane

Transports falls-short in subsidy competition

RHI

Bio

-met

han

e p

rod

uce

r

ROC

RTFC

• £0.26 per m3 of raw biogas• Low term certainty• Index linked• Medium capex

• £0.20 per m3 of raw biogas• Predictable market• Low capex

• £0.07 to £0.34 per m3 of raw biogas (5-24p/RTFC)• Market mechanism - un-predicable market price • Certificate price influenced by biofuels production• High capex

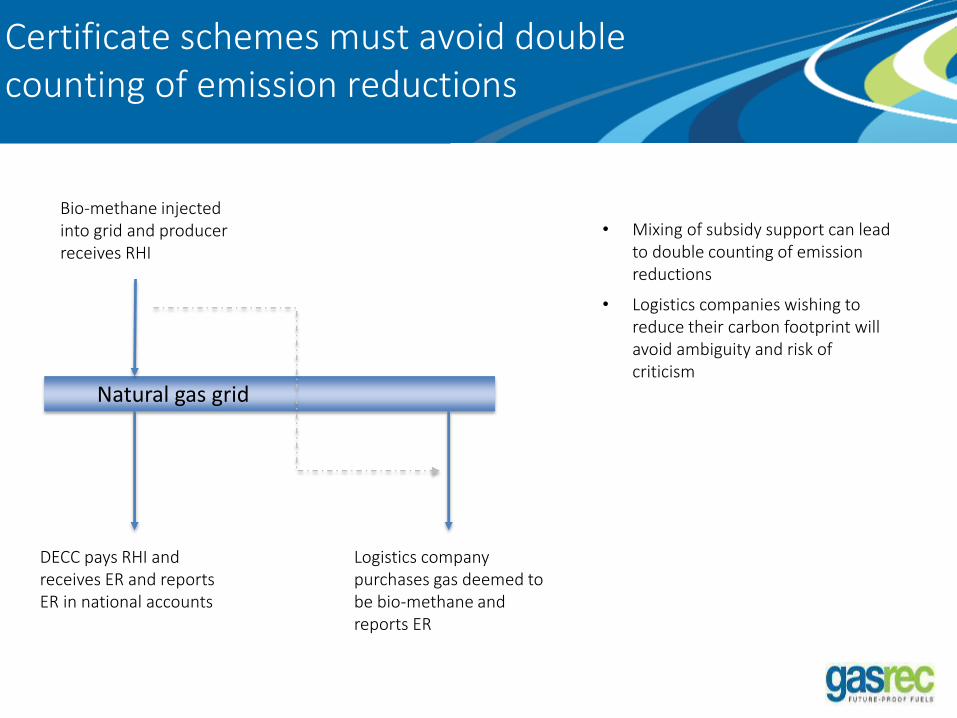

Certificate schemes must avoid double counting of emission reductions

Natural gas grid

Bio-methane injected into grid and producer receives RHI

DECC pays RHI and receives ER and reports ER in national accounts

Logistics company purchases gas deemed to be bio-methane and reports ER

• Mixing of subsidy support can lead to double counting of emission reductions

• Logistics companies wishing to reduce their carbon footprint will avoid ambiguity and risk of criticism

Other policy considerations

How important is the chain of custody and secure supply chain?

• Bio-methane molecules are indistinguishable from methane molecules

• Creating a secure custody chain that delivers bio-methane molecules to transport will be costly

• Mass balancing through the gas network means bio-methane molecules will be mingled with natural gas and not dedicated to transport

• Mass balancing through the gas network should include LNG import terminals otherwise heavy truck operators, the biggest polluters, will be unable to use bio-methane

Can bio-methane attract a price premium to natural gas?

• Road haulage has low barriers to entry and thin margins

• Outside niche operation and philanthropic operators bio-methane will not command a price premium

• Subsidy provides a bridge to carbon pricing and recognition of the carbon impact

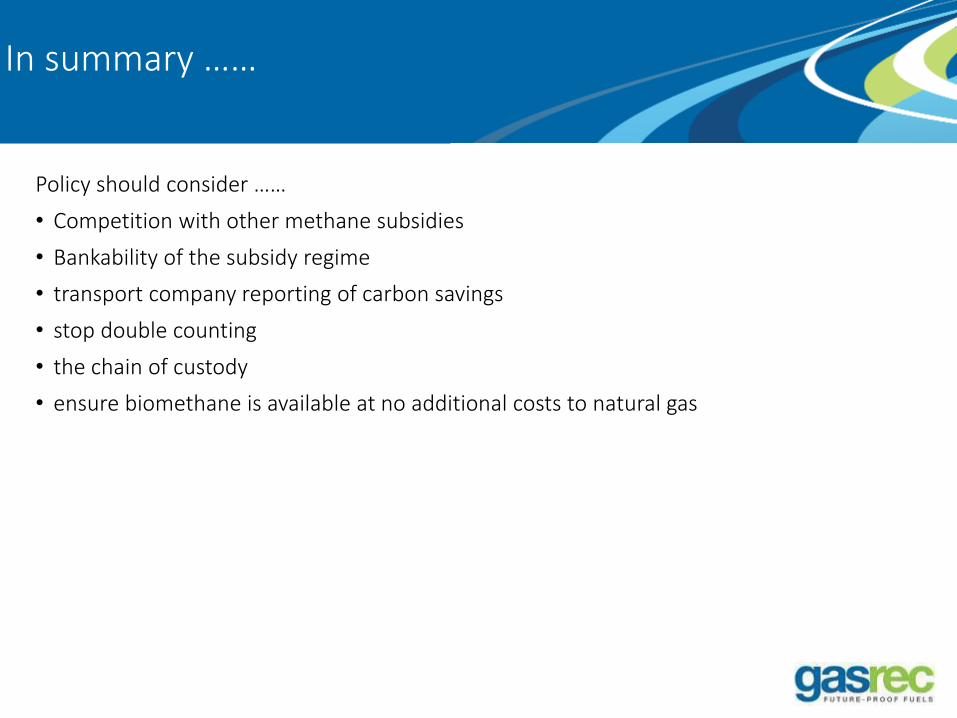

Policy should consider ……

• Competition with other methane subsidies

• Bankability of the subsidy regime

• transport company reporting of carbon savings

• stop double counting

• the chain of custody

• ensure biomethane is available at no additional costs to natural gas

In summary ……

Moving Britain Ahead July 16UK Biomethane Day, Birmingham, Weds 20th April 2016

Biomethane transport fuelUK AD & Biogas 2016

Thurs 7th July, NEC, Birmingham

Jonathan Hood

Low Carbon Fuels, Department for Transport

166

Moving Britain Ahead

Biomethane transport fuel:Strategic case and policy drivers

Heavy road haulage sector difficult to decarbonise: waste

biodiesel and biomethane

2050 strategy

Carbon Budgets

Freight review

July 16

167UK AD & Biogas 2016, Birmingham, Thurs 7th July

Moving Britain Ahead

Biomethane transport fuel:Policies to support

Supported under Renewable

Transport Fuel Obligation (RTFO)

April 2015: 1.9 RTFCs / kg,

doubled to 3.8 for waste

10 yr duty incentive (2013)

£25m advanced biofuel

demonstration competition

Low Carbon Truck Trials

July 16

168UK AD & Biogas 2016, Birmingham, Thurs 7th July

Moving Britain Ahead

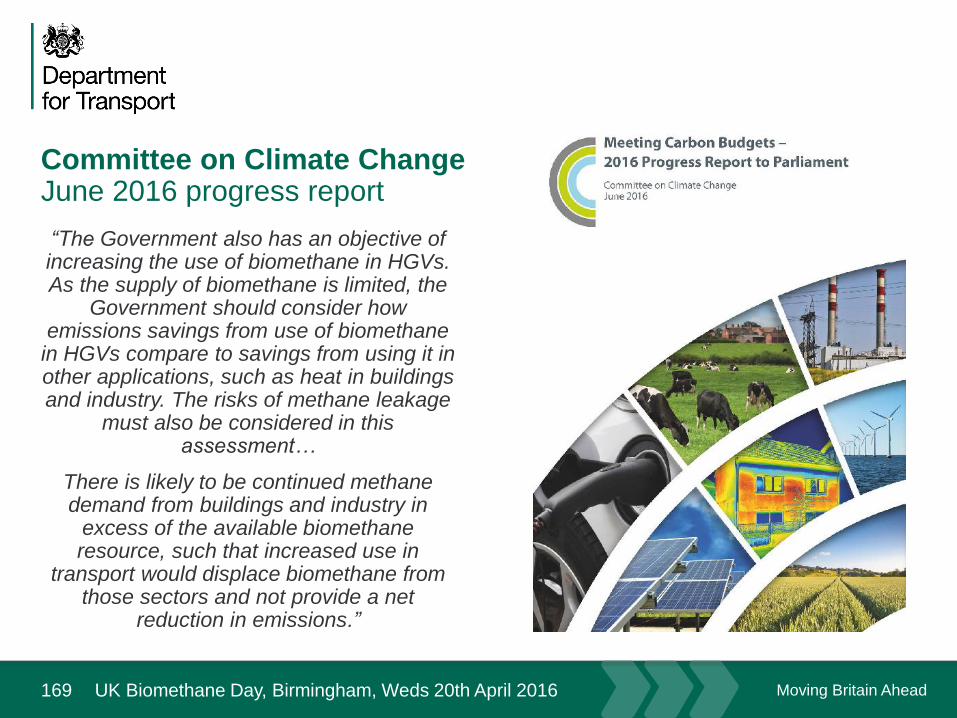

Committee on Climate Change June 2016 progress report

169

“The Government also has an objective of increasing the use of biomethane in HGVs. As the supply of biomethane is limited, the

Government should consider how emissions savings from use of biomethane

in HGVs compare to savings from using it in other applications, such as heat in buildings and industry. The risks of methane leakage

must also be considered in this assessment…

There is likely to be continued methane demand from buildings and industry in

excess of the available biomethane resource, such that increased use in

transport would displace biomethane from those sectors and not provide a net

reduction in emissions.”

July 16

UK Biomethane Day, Birmingham, Weds 20th April 2016

Moving Britain Ahead

Biomethane transport fuel:How to support in future?

2017 legislative amends for Renewable Energy

Directive (RED) and Fuel Quality Directive (FQD)

Options to support biomethane transport fuel

Changes to vehicle fuel duty challenging

Most likely option is an advanced fuels sub-target

within the RTFO

July 16

170UK AD & Biogas 2016, Birmingham, Thurs 7th July

Moving Britain Ahead

“Advanced” sub target

MSs must set a national

target for Annex IX

feedstocks

MSs should introduce

policies that will help achieve

the target

MSs policies ‘shall’ have due

regard to the waste hierarchy

July 16

171UK AD & Biogas 2016, Birmingham, Thurs 7th July

Moving Britain Ahead

0

500

1,000

1,500

2,000

2,500

3,000

Litr

es (

mill

ion

s)

Advanced diesel/gas

1G low blend waste biodiesel 1G low blend crop biodiesel 2G advanced biodiesel

1G low blend crop ethanol 2G advanced ethanol biomethane

biomethanol

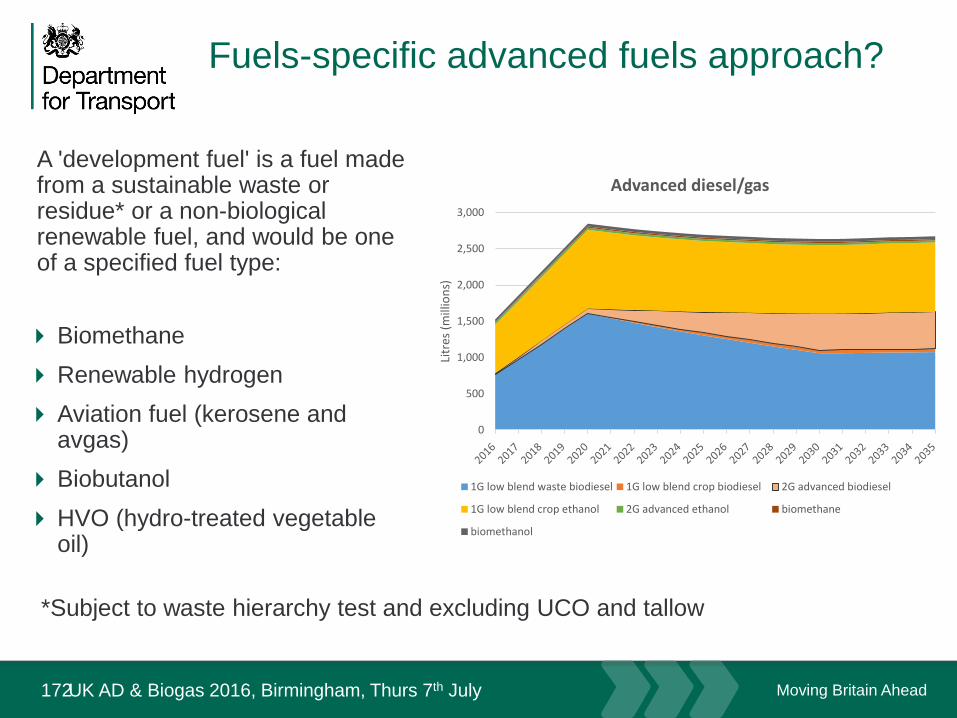

Fuels-specific advanced fuels approach?

A 'development fuel' is a fuel made from a sustainable waste or residue* or a non-biological renewable fuel, and would be one of a specified fuel type:

Biomethane

Renewable hydrogen

Aviation fuel (kerosene and avgas)

Biobutanol

HVO (hydro-treated vegetable oil)

July 16

*Subject to waste hierarchy test and excluding UCO and tallow

172UK AD & Biogas 2016, Birmingham, Thurs 7th July

Moving Britain Ahead

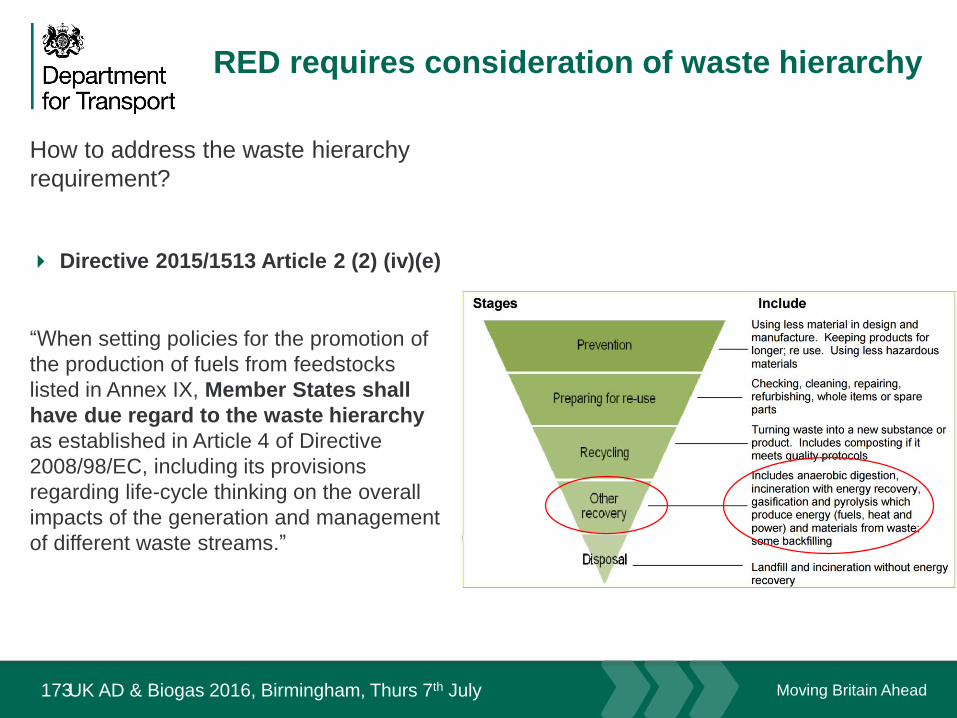

RED requires consideration of waste hierarchy

How to address the waste hierarchy

requirement?

Directive 2015/1513 Article 2 (2) (iv)(e)

“When setting policies for the promotion of

the production of fuels from feedstocks

listed in Annex IX, Member States shall

have due regard to the waste hierarchy

as established in Article 4 of Directive

2008/98/EC, including its provisions

regarding life-cycle thinking on the overall

impacts of the generation and management

of different waste streams.”

July 16

173UK AD & Biogas 2016, Birmingham, Thurs 7th July

Moving Britain Ahead

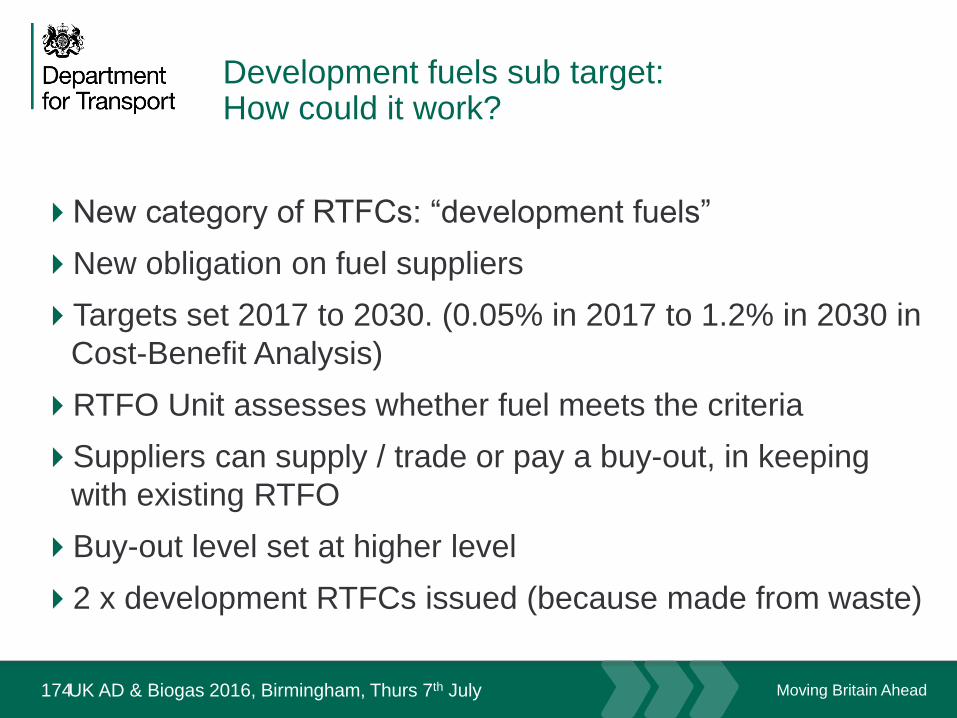

Development fuels sub target: How could it work?

New category of RTFCs: “development fuels”

New obligation on fuel suppliers

Targets set 2017 to 2030. (0.05% in 2017 to 1.2% in 2030 in

Cost-Benefit Analysis)

RTFO Unit assesses whether fuel meets the criteria

Suppliers can supply / trade or pay a buy-out, in keeping

with existing RTFO

Buy-out level set at higher level

2 x development RTFCs issued (because made from waste)

July 16

174UK AD & Biogas 2016, Birmingham, Thurs 7th July

Moving Britain Ahead

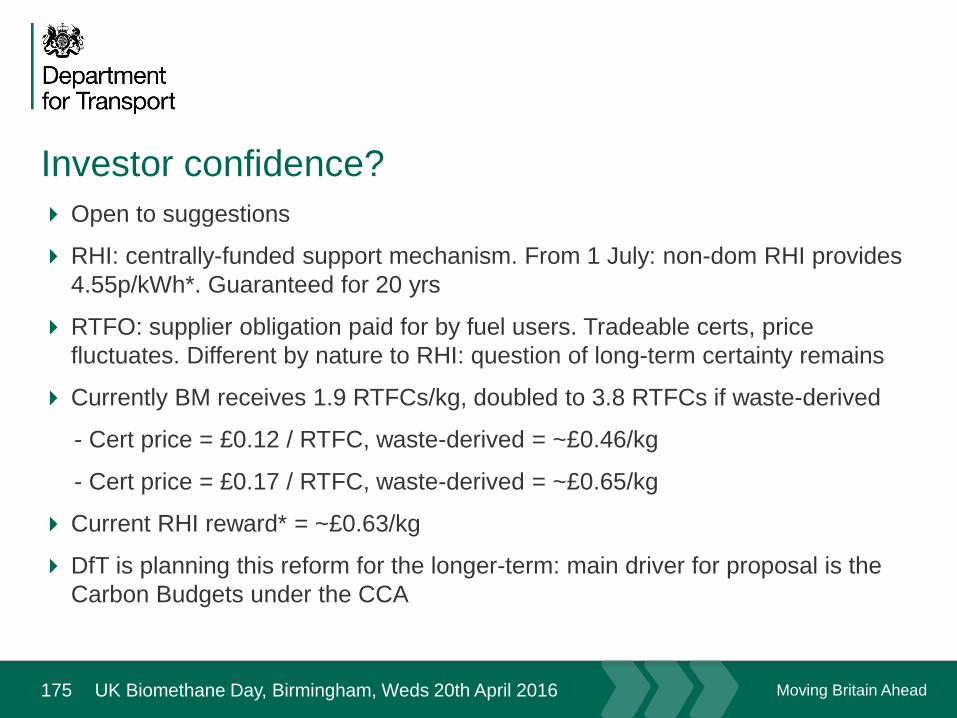

Investor confidence?

175

Open to suggestions

RHI: centrally-funded support mechanism. From 1 July: non-dom RHI provides

4.55p/kWh*. Guaranteed for 20 yrs

RTFO: supplier obligation paid for by fuel users. Tradeable certs, price

fluctuates. Different by nature to RHI: question of long-term certainty remains

Currently BM receives 1.9 RTFCs/kg, doubled to 3.8 RTFCs if waste-derived

- Cert price = £0.12 / RTFC, waste-derived = ~£0.46/kg

- Cert price = £0.17 / RTFC, waste-derived = ~£0.65/kg

Current RHI reward* = ~£0.63/kg

DfT is planning this reform for the longer-term: main driver for proposal is the

Carbon Budgets under the CCA

July 16

UK Biomethane Day, Birmingham, Weds 20th April 2016

Moving Britain Ahead

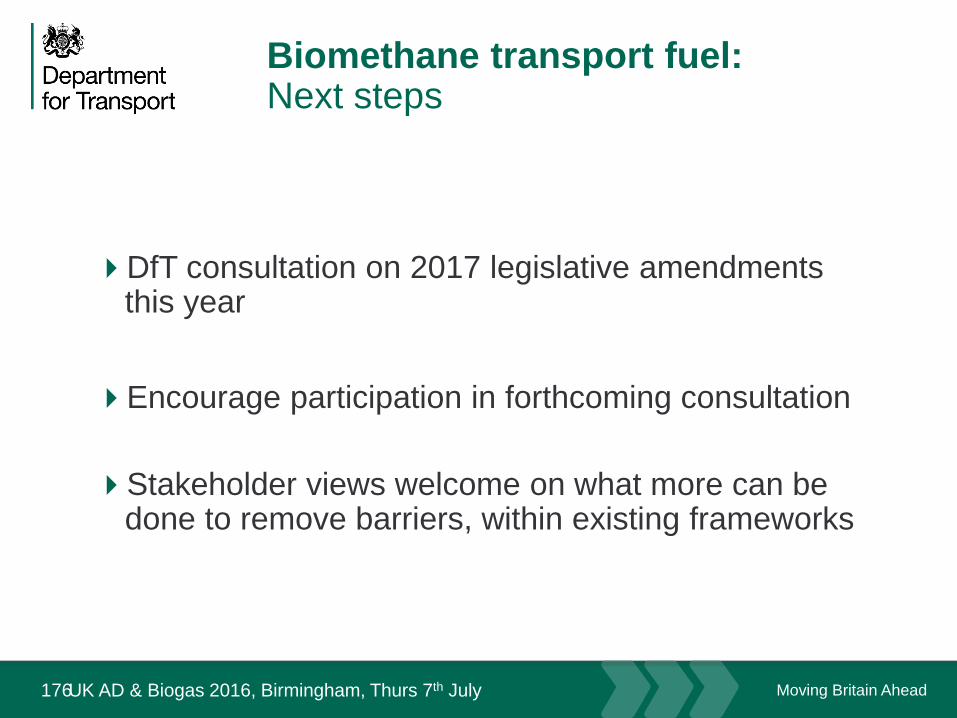

Biomethane transport fuel:Next steps

July 16

DfT consultation on 2017 legislative amendments this year

Encourage participation in forthcoming consultation

Stakeholder views welcome on what more can be done to remove barriers, within existing frameworks

176UK AD & Biogas 2016, Birmingham, Thurs 7th July

Moving Britain Ahead

Thank you

July 16

177UK AD & Biogas 2016, Birmingham, Thurs 7th July

UK biogas: current use and

potential

Ollie More

ADBA

UK biogas use 2016

Biogas 2016

8.9 TWh

Heat-only

Transport (Ludlow, Avonmouth)

<0.1 TWh

Gas grid

2.6 TWh

Electricity generation

6.3 TWh

Electricity

2.5 TWhe

Co-generated heat

(mainly vented)

3.8 TWhth

UK methane potential: 2025-30

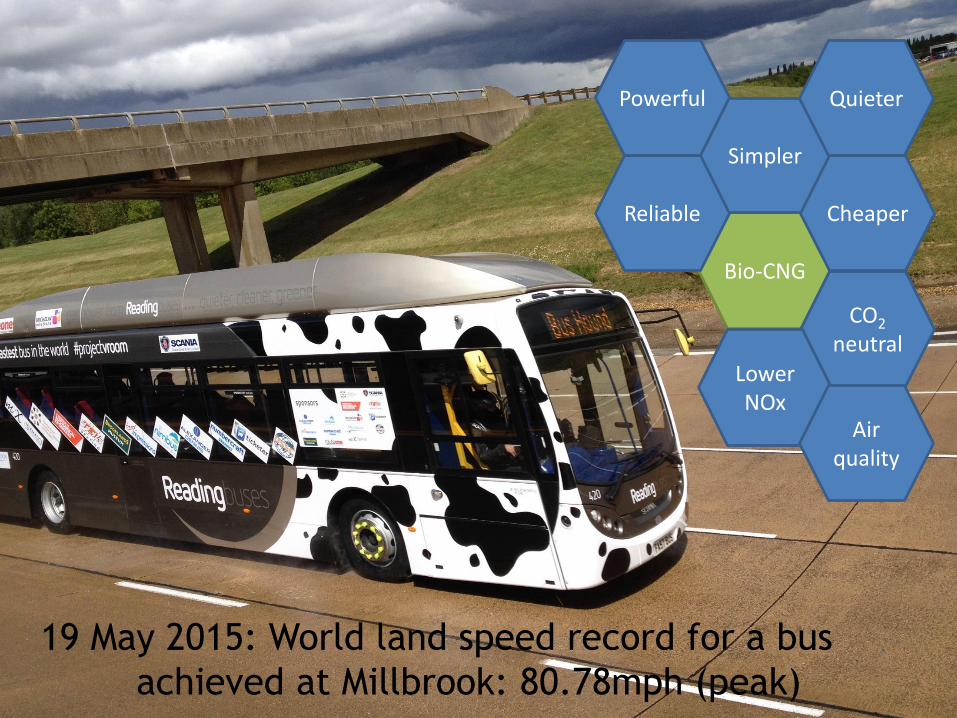

• 180 bus fleet serving Reading and area– Euro IV, Euro V, Euro VI

– Euro V hybrids, Euro V gas

• Early adopters – leaders, innovators

Bio-CNG

Simpler

CO2

neutral

CheaperReliable

Lower NOx

Air quality

QuieterPowerful

19 May 2015: World land speed record for a bus

achieved at Millbrook: 80.78mph (peak)

QUESTIONS AND COMMENTS FROM THE FLOOR

Related Documents