Slide 1 © Bobst Group 02/12/2010 Slide 1 © Bobst Group Pack Age 2010 Conference on Packaging Trends Delhi 2 December, 2010

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Slide 1 © Bobst Group02/12/2010 Slide 1 © Bobst Group

Pack Age 2010

Conference onPackaging Trends

Delhi2 December, 2010

Slide 2 © Bobst Group02/12/2010 Slide 2 © Bobst Group

Pack Age 2010

Latest Concepts in Package Converting

World flexible packaging

Packaging Strategy

Flexible Packaging

Indian market & Flexible packaging development

Bobst Group view in the “Latest concepts of package converting”

Slide 3 © Bobst Group02/12/2010 Slide 3 © Bobst Group

Pack Age 2010

Put the FrameworkWorld Flexible Packaging

Slide 4 © Bobst Group02/12/2010 Slide 4 © Bobst Group

Pack Age 2010

World Flexible Packaging

BOPET film price increased 40% to 60%

BOPA film capacity increased by 60%

Flexible Packaging demand in 2010 10% up on 2009Indian and Chinese growth 2x this level

Slide 5 © Bobst Group02/12/2010 Slide 5 © Bobst Group

Pack Age 2010

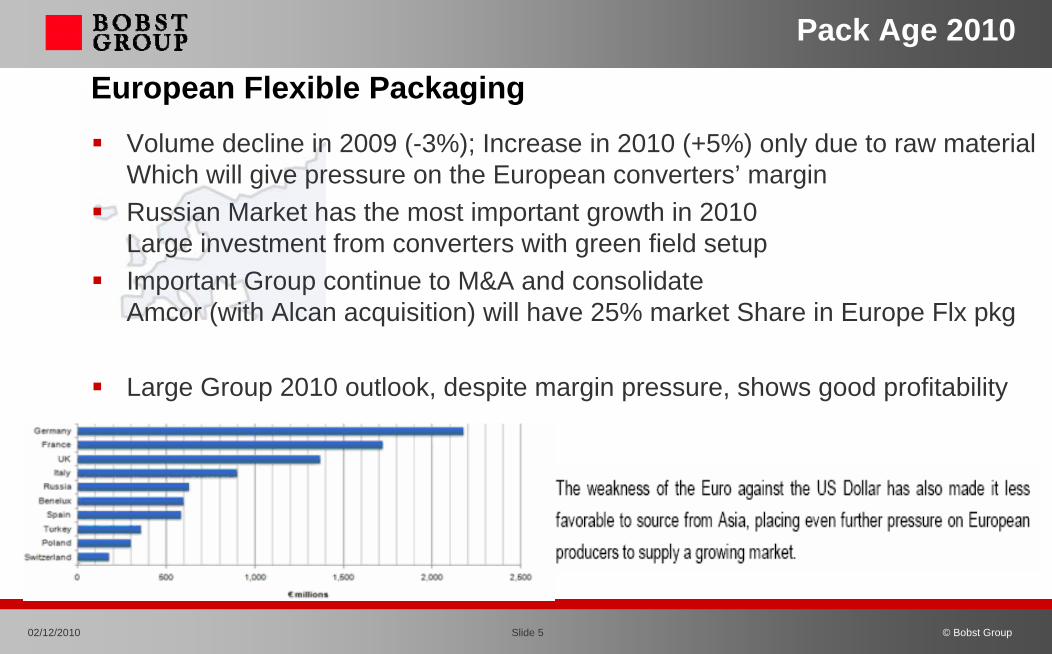

European Flexible PackagingVolume decline in 2009 (-3%); Increase in 2010 (+5%) only due to raw materialWhich will give pressure on the European converters’ marginRussian Market has the most important growth in 2010Large investment from converters with green field setupImportant Group continue to M&A and consolidateAmcor (with Alcan acquisition) will have 25% market Share in Europe Flx pkg

Large Group 2010 outlook, despite margin pressure, shows good profitability

Slide 6 © Bobst Group02/12/2010 Slide 6 © Bobst Group

Pack Age 2010

North American Flexible Packaging Market

08/2010 US Dept. of Commerce announced duties on BOPET film from China(final decision before end of December)

BOPET, BOPP film increase by > 50%Ink or adhesives followed this chemical raw material increase

Despite pressure in margin, converters in US get 8%-10% EBITDA

M&A and market consolidation continue ex: Bemis Sales increase of 53% in 2010 (45% acquisition; 2.5% currency)

Packaging users looking strongly to Biodegradable plastics packaging.

Slide 7 © Bobst Group02/12/2010 Slide 7 © Bobst Group

Pack Age 2010

Middle-East & African Flexible Packaging Market

New film capacity installed in the ME and in AFRICAFilm price up by 30%

Retailers and food MNC invest heavily in new plants

Slide 8 © Bobst Group02/12/2010 Slide 8 © Bobst Group

Pack Age 2010

South & Central American Flexible Packaging Market

New film capacity installed in South America (Peru, ..)BOPET film price up by 35%

Converters become more industrialized with positive outlook in the futureM&A haven’t start yet ; market still very fragmentedBrazil, Peru, Chile and Columbia are the main growing flexible markets

Strong development continue for Retailers and food MNC

Slide 9 © Bobst Group02/12/2010 Slide 9 © Bobst Group

Pack Age 2010

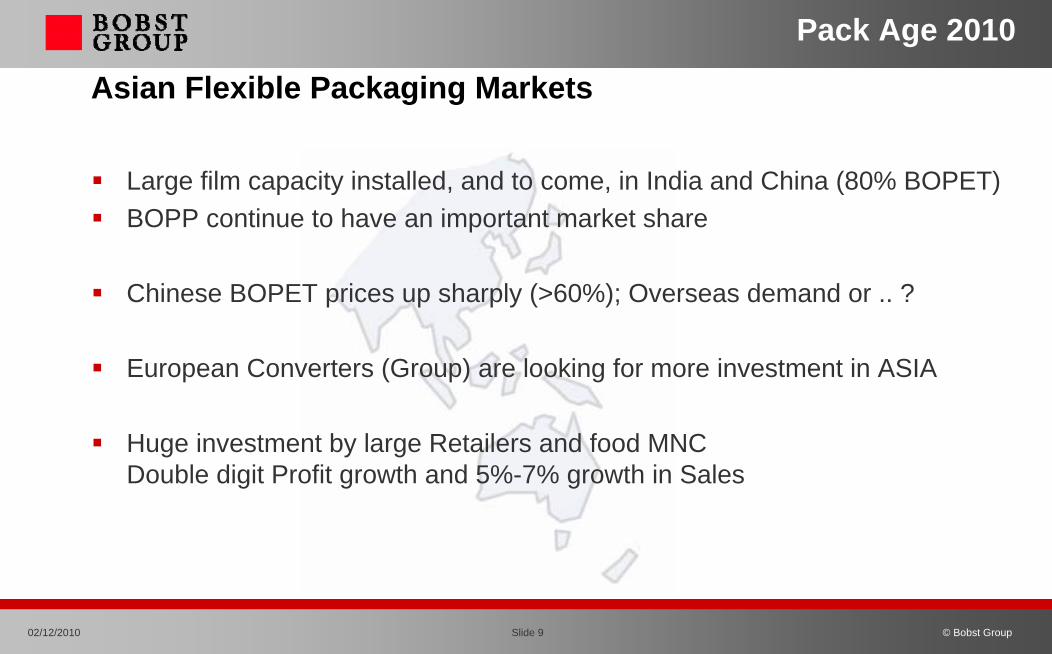

Asian Flexible Packaging Markets

Large film capacity installed, and to come, in India and China (80% BOPET)BOPP continue to have an important market share

Chinese BOPET prices up sharply (>60%); Overseas demand or .. ?

European Converters (Group) are looking for more investment in ASIA

Huge investment by large Retailers and food MNCDouble digit Profit growth and 5%-7% growth in Sales

Slide 10 © Bobst Group02/12/2010 Slide 10 © Bobst Group

Pack Age 2010

World Flexible Packaging Markets

Raw material and Film demand increase > Film prices increaseBiodegradable will take more and more importance

M&A in mature marketModerate Growth in Mature marketsImportant Growth in Emerging markets

Flexible packaging is becoming a “commodities”Our industry landscape will continue to change

Flexible Package growth is bigger than a double digit %

Slide 11 © Bobst Group02/12/2010 Slide 11 © Bobst Group

Pack Age 2010

Global PackagingPackaging Strategy

Slide 12 © Bobst Group02/12/2010 Slide 12 © Bobst Group

Pack Age 2010

Global Drivers for your Strategy

Energy Efficiency– Reduce energy needed for customers’ to transport and

store their products– Reduce energy needed to manufacture products

Carbon Efficiency– Reduce greenhouse gas intensity associated with the

package & contents of the package– Use LCA tools in the development of products

Material Efficiency– Reduce plastic scrap that goes into landfills– Improve performance of shrink films to create thinner

products– Introduce products created from alternative materials

ClimateChange

Use of NaturalResources

WasteManagement

Slide 13 © Bobst Group02/12/2010 Slide 13 © Bobst Group

Pack Age 2010

Global Packaging Location Strategy

Package cost is 10% - 15% of the total productsPackaging is a Global (transportation is 5% of the total costs)As consequence, the Packaging is travelling well !!!

Packaging being transportableSpecialization of setup to one application

BRIC/LCC growth in packaging

Slide 14 © Bobst Group02/12/2010 Slide 14 © Bobst Group

Pack Age 2010

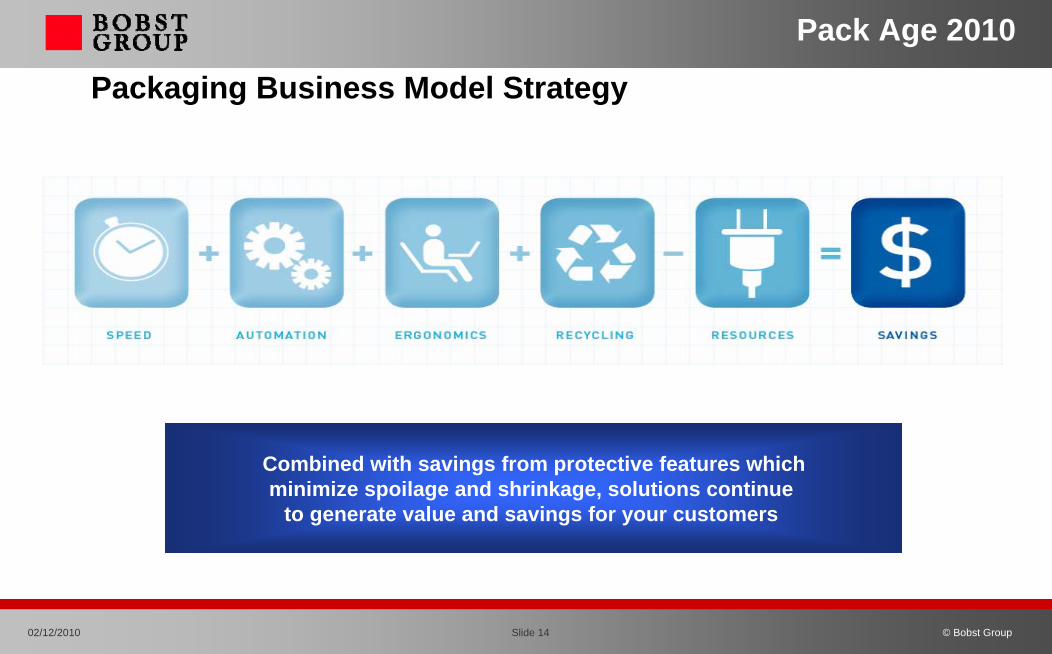

Packaging Business Model Strategy

Combined with savings from protective features whichminimize spoilage and shrinkage, solutions continue

to generate value and savings for your customers

Slide 15 © Bobst Group02/12/2010 Slide 15 © Bobst Group

Pack Age 2010

Innovation & Agile Strategy

Drivers - Innovation Sources - Agile

Exte

rnal

colla

bora

tion

Inte

rnal

colla

bora

tion

ExternalInventors

Technologysuppliers

GovernmentAgencies

ResearchCenters

EquipmentOptions

PackagingMaterials

Invest in the future

Collaborate both inside & outside the Company

Foster an Innovation culture

We are borderless! Regardless of where an innovation is born

Network of Innovation

UniversitiesCustomers

TechnicalSupport

PackageDesign

Slide 16 © Bobst Group02/12/2010 Slide 16 © Bobst Group

Pack Age 2010

Evolution - RevolutionPack, Package, Packaging…

Slide 17 © Bobst Group02/12/2010 Slide 17 © Bobst Group

Pack Age 2010

Pack, Package, Packaging …

Integrating Packaging, Storage & Distribution thru Intelligent Packaging.– Quality Attributes of the Food (Texture, Flavour, Colour, …) – Food Safety (Microbiological Safety, Material Toxicology, …) – Deteriorative Reactions in Food– Moistures – Humidity – Shelf Live…

Potential causes of trouble in packaging in food industry:– Closure of packaging systems, Leakage, Loss of Sterility– Change of temperature, Light, U.V. Radiation– Vibration, Shocks, Compression

Optimizing alternative package types

Slide 18 © Bobst Group02/12/2010 Slide 18 © Bobst Group

Pack Age 2010

Future Trends in Flexible Packaging …

Slide 19 © Bobst Group02/12/2010 Slide 19 © Bobst Group

Pack Age 2010

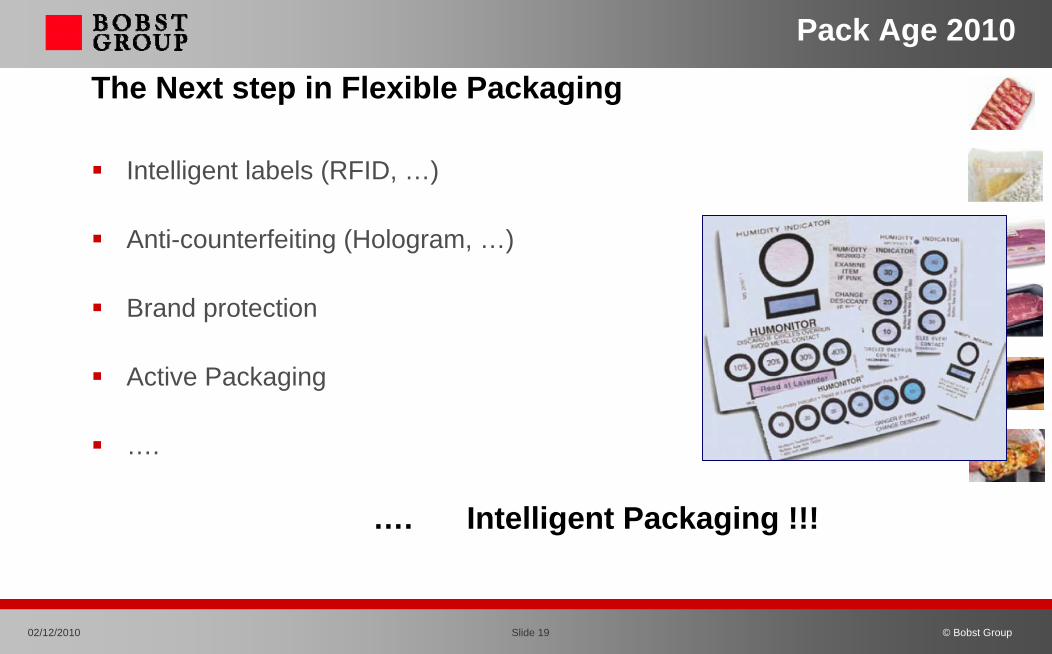

The Next step in Flexible Packaging

Intelligent labels (RFID, …)

Anti-counterfeiting (Hologram, …)

Brand protection

Active Packaging

….

…. Intelligent Packaging !!!

Slide 20 © Bobst Group02/12/2010 Slide 20 © Bobst Group

Pack Age 2010

Indian Flexible Packaging

Slide 21 © Bobst Group02/12/2010 Slide 21 © Bobst Group

Pack Age 2010

INDIA

Government has flagged reforms to land acquisition laws and rules on the use of foreign funds to help finance infrastructure.

India is playing bigger international role (G20; visit of Mr Obama)

PM Singh is pushing for INDIA-ASEAM agreement on trade

Indian real GDP growth of 9.1% in 2010 (inflation adjusted )

Consumer demand rose by 3.2% (inflation-adjusted; nom.20%)

Slide 22 © Bobst Group02/12/2010 Slide 22 © Bobst Group

Pack Age 2010

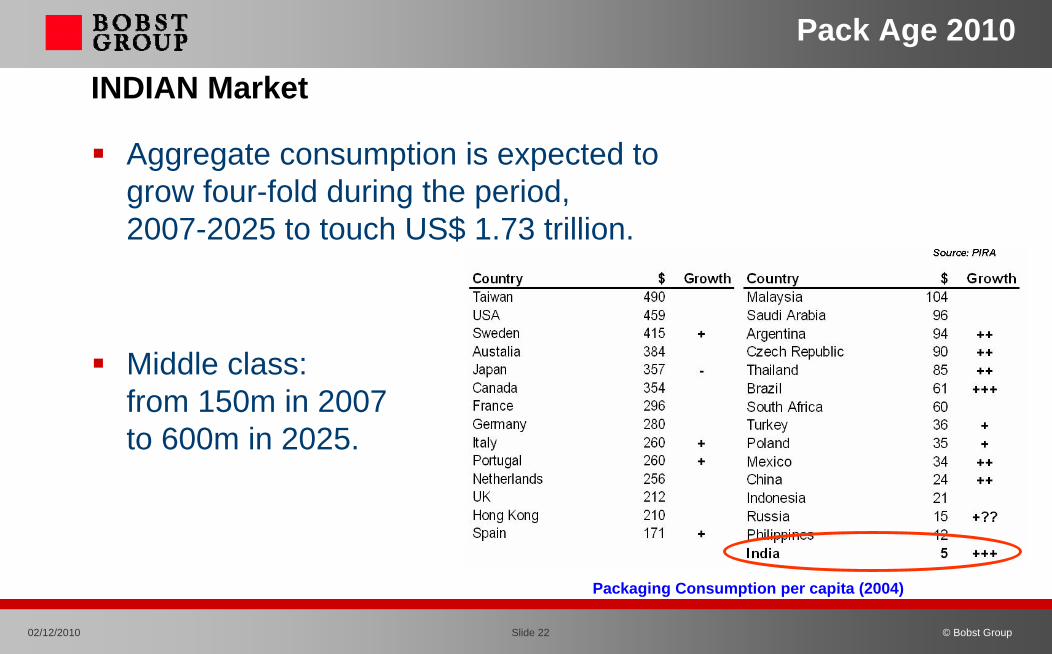

INDIAN Market

Aggregate consumption is expected to grow four-fold during the period, 2007-2025 to touch US$ 1.73 trillion.

Middle class: from 150m in 2007 to 600m in 2025.

Packaging Consumption per capita (2004)

Slide 23 © Bobst Group02/12/2010 Slide 23 © Bobst Group

Pack Age 2010

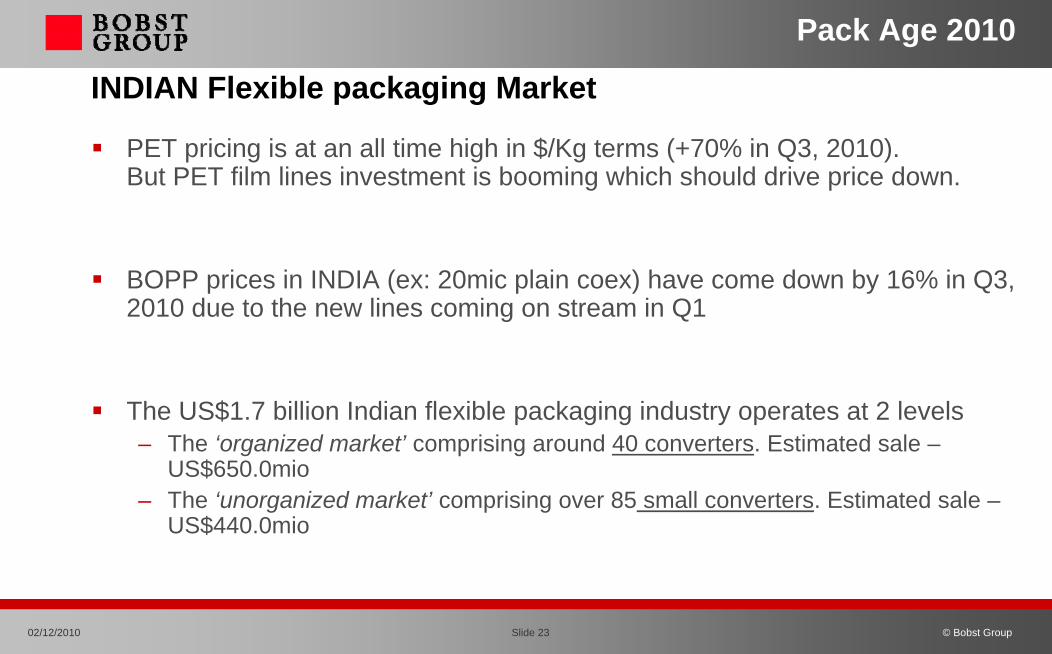

INDIAN Flexible packaging Market

PET pricing is at an all time high in $/Kg terms (+70% in Q3, 2010). But PET film lines investment is booming which should drive price down.

BOPP prices in INDIA (ex: 20mic plain coex) have come down by 16% in Q3, 2010 due to the new lines coming on stream in Q1

The US$1.7 billion Indian flexible packaging industry operates at 2 levels– The ‘organized market’ comprising around 40 converters. Estimated sale –

US$650.0mio– The ‘unorganized market’ comprising over 85 small converters. Estimated sale –

US$440.0mio

Slide 24 © Bobst Group02/12/2010 Slide 24 © Bobst Group

Pack Age 2010

INDIAN Flexible packaging Market

Highly fragmented market – over 900 ConvertersMuch of this industry is small-scale due to:– Prohibition of direct FDI in retail– Prohibition in contract farming– Some of the highest taxes on processed foods in the world– India is unusual in its high usage of flexible packaging in liquid products,

i.e. edible oil, milk.

Rapid growth in grocery & food retailing“Rural” demand growth (10%) leads to incremental volume over 75K tons flexible packaging of capacity additions paFood processing sector growing @ 12%-15%pa.

Slide 25 © Bobst Group02/12/2010 Slide 25 © Bobst Group

Pack Age 2010

Indian Conversion few samples

Glass to Pouch FlexibleThermo formable PouchValue added laminate tubeHolographic laminatesMulti use pack sizesIncrease in varieties of same product / brand

Slide 26 © Bobst Group02/12/2010 Slide 26 © Bobst Group

Pack Age 2010

Indian Retailer trendsContinuous Development of the Retail in India

Modern Retail will put pressure on Marketers toconform to this new format:

– On Visual Applea, Graphics, Shapes– Traceability, Pack sizes, Shelf-Space, JIT– Innovative Differentiation

This segment will sustain >40% growth

Indian

Retail trends

Slide 27 © Bobst Group02/12/2010 Slide 27 © Bobst Group

Pack Age 2010

Indian Converters Key Success FactorsContinuous investment in upgrade, technology, capacity, quality, efficiency, cost, product development

Down gauging remains an ongoing process

Continuous innovation

Supply chain management – fast turn around times

Global market player

Driving growth through value creation. Managing an environment of lower profit and growing volumes

Performances of the Converting M/C with speed, quality, wastage and change over adapted to the industry standard

Slide 28 © Bobst Group02/12/2010 Slide 28 © Bobst Group

Pack Age 2010

Latest concepts of package Converting

Slide 29 © Bobst Group02/12/2010 Slide 29 © Bobst Group

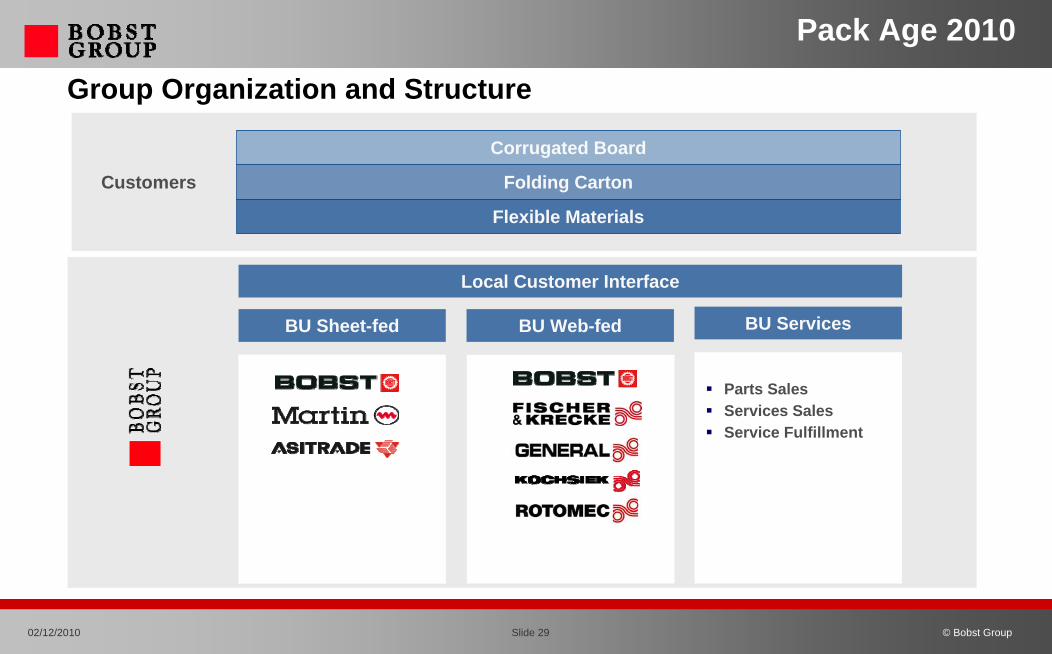

Pack Age 2010

Local Customer Interface

Parts SalesServices SalesService Fulfillment

BU Sheet-fed BU Web-fed BU Services

Group Organization and Structure

Customers Folding Carton

Corrugated Board

Flexible Materials

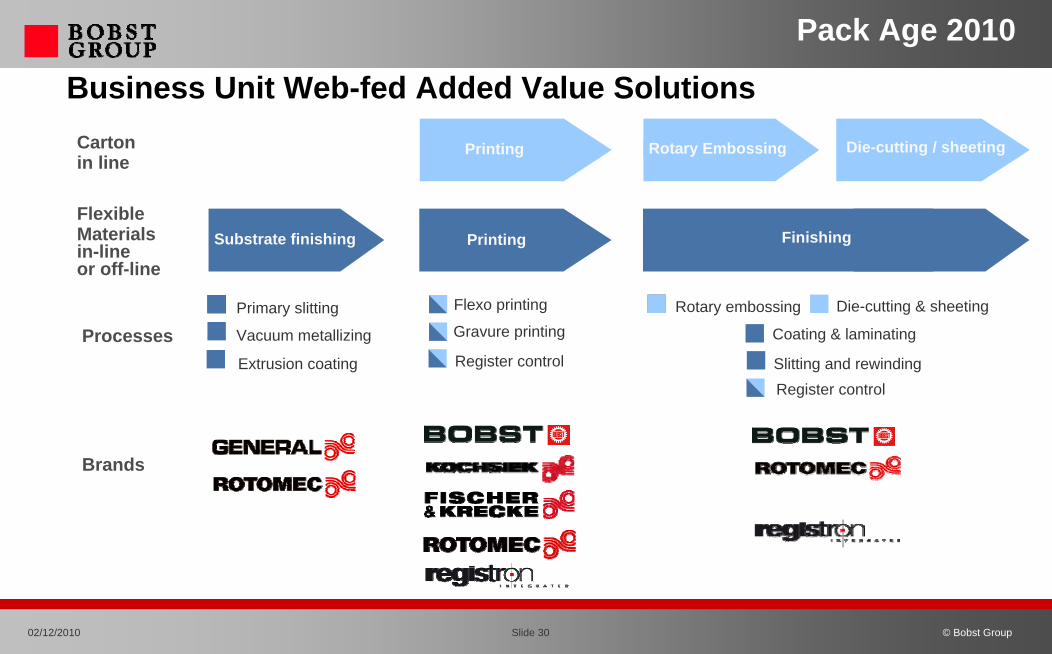

Slide 30 © Bobst Group02/12/2010 Slide 30 © Bobst Group

Pack Age 2010

PrintingCarton in line

Flexible Materials in-line or off-line

Vacuum metallizing

Primary slitting

Extrusion coating

Rotary Embossing Die-cutting / sheeting

Printing FinishingSubstrate finishing

Gravure printing

Flexo printing

Coating & laminating

Slitting and rewinding

Rotary embossing Die-cutting & sheeting

Processes

Brands

Register control

Register control

Business Unit Web-fed Added Value Solutions

Slide 31 © Bobst Group02/12/2010 Slide 31 © Bobst Group

Pack Age 2010Business Unit Web-fed

Films Niches

√

√

√

√

Flexo Printing

Coating Laminating

Film Vacuum Metallizing

Gravure Printing

Gravure Printing

Tobacco

√

√

Labels

√

√

√

Films

√

Flexible

√

√

√

Tapes

√

Process

√

Brand Pre-print

√ √ √ √

Carton

√√

Brands

√

√

Gravure Printing, in-line embossing, die cutting, sheeting √√√

Business Unit Web-fed Added Value Solutions

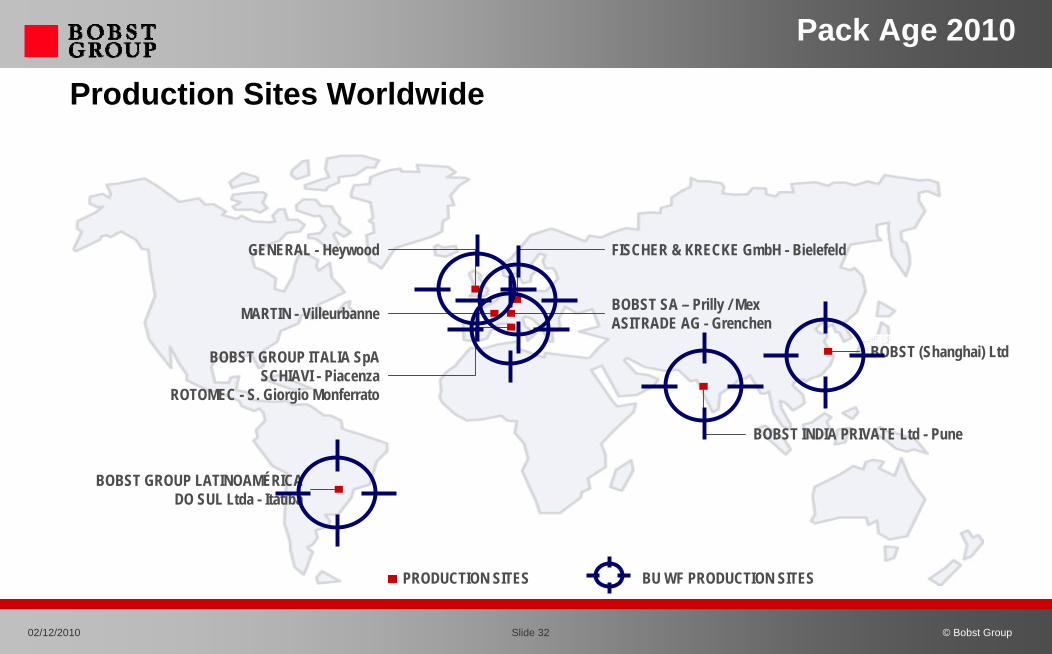

Slide 32 © Bobst Group02/12/2010 Slide 32 © Bobst Group

Pack Age 2010

BU WF PRODUCTION SITES

GENERAL - Heywood

MARTIN - Villeurbanne

FISCHER & KRECKE GmbH - Bielefeld

BOBST SA – Prilly / MexASITRADE AG - Grenchen

BOBST GROUP ITALIA SpASCHIAVI - Piacenza

ROTOMEC - S. Giorgio Monferrato

BOBST GROUP LATINOAMÉRICADO SUL Ltda - Itatiba

BOBST (Shanghai) Ltd

BOBST INDIA PRIVATE Ltd - Pune

Production Sites Worldwide

PRODUCTION SITES

Slide 33 © Bobst Group02/12/2010 Slide 33 © Bobst Group

Pack Age 2010

“Latest concepts of package converting”

Local requirements – Global footprint

Processes Optimization– Wastage– Production optimization– Quality improvement

Value-Added concepts

Slide 34 © Bobst Group02/12/2010 Slide 34 © Bobst Group

Pack Age 2010

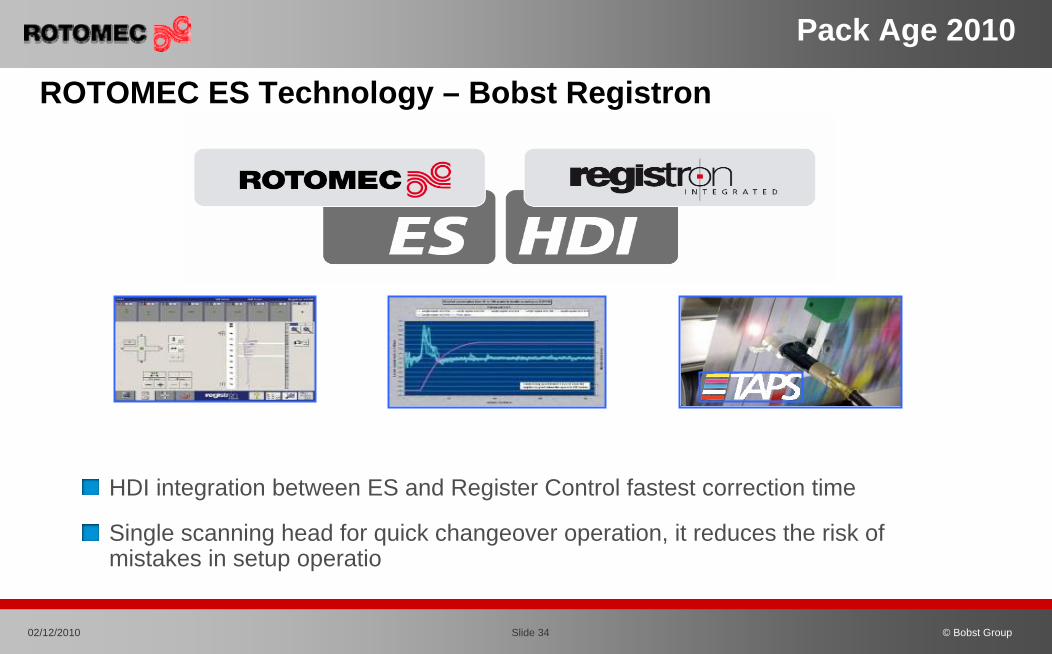

ROTOMEC ES Technology – Bobst Registron

HDI integration between ES and Register Control fastest correction time

Single scanning head for quick changeover operation, it reduces the risk of mistakes in setup operatio

Slide 35 © Bobst Group02/12/2010 Slide 35 © Bobst Group

Pack Age 2010

Wastes and pre-register setting times are affected by:

no need of pre-register devices

Need of pre-register device such as laser pointer, pre-register rings, adhesive tapes or reading sensors for cylinder marksPossible mistakes during the setting phases of rings, laser pointeror adhesive tapes

is not affected by external systems

MachineMachine in in registerregister inin 5 5 minutesminutes onlyonlyminimizingminimizing manualmanual operations/mistakes!operations/mistakes!

Wastage: Pre-register Issues

independant from Operator skill

Slide 36 © Bobst Group02/12/2010 Slide 36 © Bobst Group

Pack Age 2010

ROTOMEC RS 4003

Compact design = 20% reduction of press web lengthSimple and rapid work sequence for fast job changeoverHigh machine flexibility and productivityHigh quality output at high speed and high reliabilityUser-friendliness Competitive cost of investment

Slide 37 © Bobst Group02/12/2010 Slide 37 © Bobst Group

Pack Age 2010

ROTOMEC 888

Consistent speed of productionLocal Need for competitive price/performance solutionLower energy consumptionLower wastage with compact design & integrated Register control

Slide 38 © Bobst Group02/12/2010 Slide 38 © Bobst Group

Pack Age 2010

ROTOMEC CL 850 D

Increase product quality & productivity

Large dryer opening for web handling , cleaning & maintenanceEasy demountable nozzles, rolls and filters

Slide 39 © Bobst Group02/12/2010 Slide 39 © Bobst Group

Pack Age 2010

ROTOMEC CL 850 D

Coating systems: – gravure, – solventless, – semiflexo, flexo, – cold seal, – 1-colour in register

Extremely sensitive web handlingFast job changeover

Synergy with Rotomec gravure printing for parts interchangeabilityImproved ergonomics, accessibility and ease of maintenance

Slide 40 © Bobst Group02/12/2010 Slide 40 © Bobst Group

Pack Age 2010

Far superior optical quality (no orange peel) and low coating weight (2.2-2.8 gr/m² dry at 38-40%) with comparable bond strength due to better adhesive distribution

Reduced thin foil web break

Less solvent retention

Wide coating range from 2 up to 4,5 gr/m² of dry adhesive without changing coating cylinder

ROTOMEC CL 850 D

High quality of laminated material through adhesive coating with flexo system

Slide 41 © Bobst Group02/12/2010 Slide 41 © Bobst Group

Pack Age 2010

Save, Save, Save, Saving !!!

SubstrateInk, SolventEnergy

Hourly press timeLabour

With all kind of flexible materials

CI FLEXO for packaging printing

Slide 42 © Bobst Group02/12/2010 Slide 42 © Bobst Group

Pack Age 2010

TechnologyTechnologyfor fastest set-up and minimum waste

Revolutionary

Slide 43 © Bobst Group02/12/2010 Slide 43 © Bobst Group

Pack Age 2010

36-SeriesFP 36-S: Premium Flexo for Large Volumes

Flexible, Flexibility !!!

Multi-processes in one

Large web width

Large Repeat length

1000 m/min Solution

Slide 44 © Bobst Group02/12/2010 Slide 44 © Bobst Group

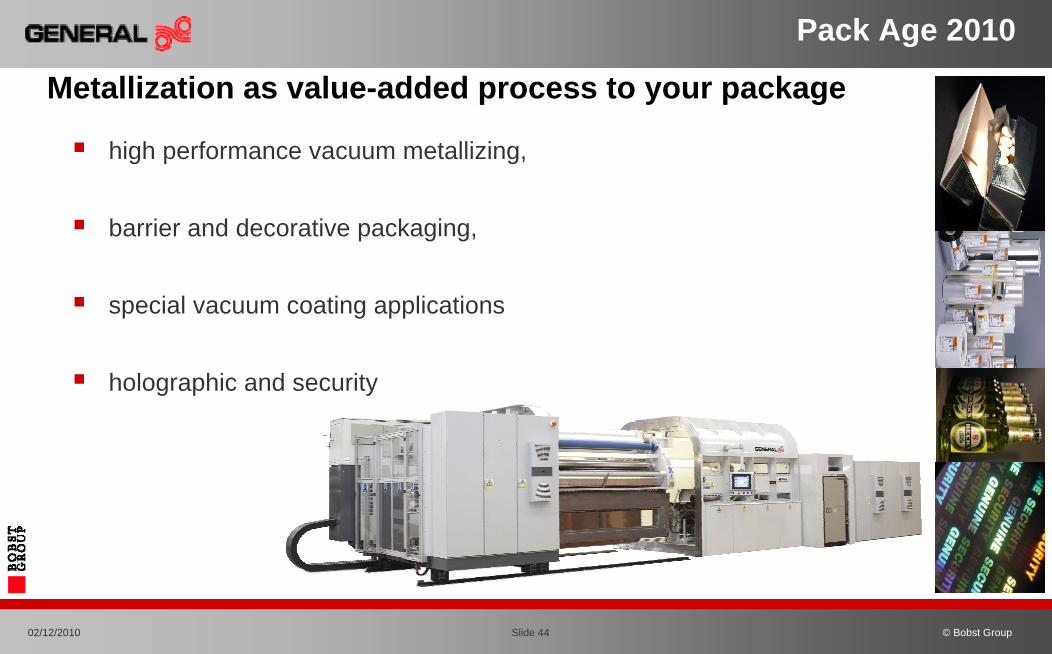

Pack Age 2010

Metallization as value-added process to your package

high performance vacuum metallizing,

barrier and decorative packaging,

special vacuum coating applications

holographic and security

Slide 45 © Bobst Group02/12/2010 Slide 45 © Bobst Group

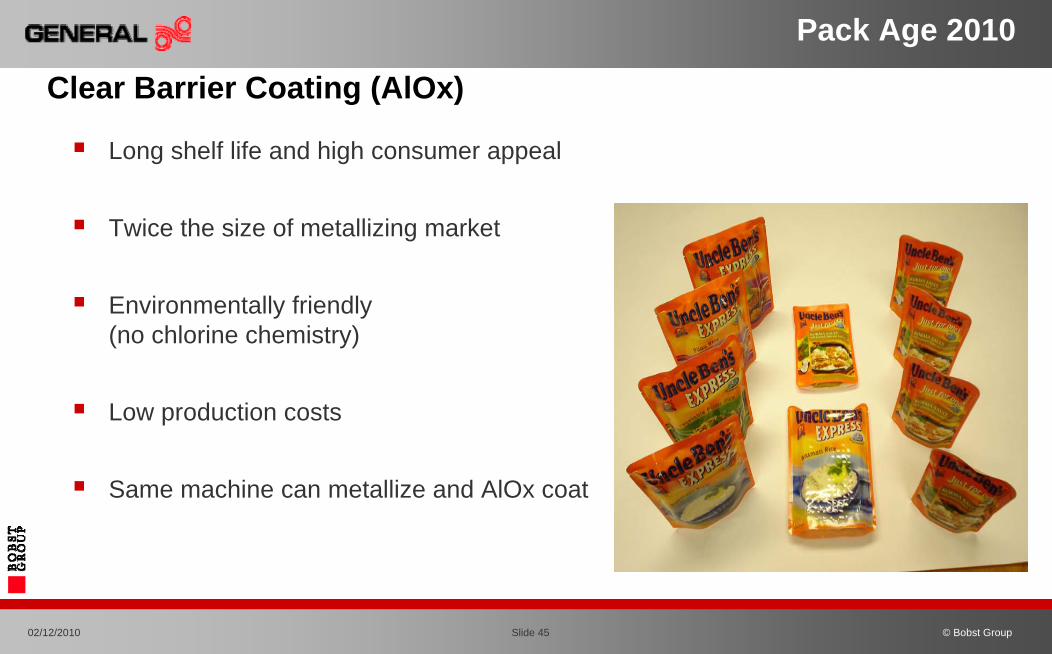

Pack Age 2010

Clear Barrier Coating (AlOx)

Long shelf life and high consumer appeal

Twice the size of metallizing market

Environmentally friendly (no chlorine chemistry)

Low production costs

Same machine can metallize and AlOx coat

Slide 46 © Bobst Group02/12/2010 Slide 46 © Bobst Group

Pack Age 2010

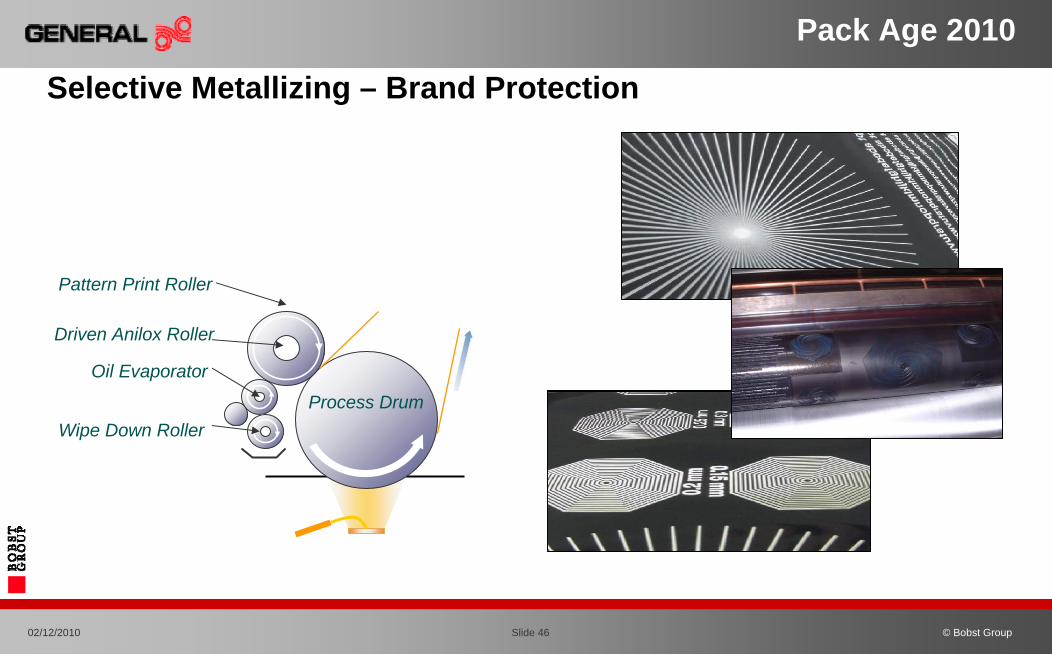

Selective Metallizing – Brand Protection

Pattern Print Roller

Driven Anilox Roller

Oil Evaporator

Wipe Down RollerProcess Drum

Slide 47 © Bobst Group02/12/2010 Slide 47 © Bobst Group

Pack Age 2010

BUWF Business Budget/Objecties (recap)

Slide 48 © Bobst Group02/12/2010 Slide 48 © Bobst Group

Pack Age 2010

Thank You

Related Documents