Lease-to-Purchase Housing Finance in Chile: Context, Past Experience, Future Opportunities & Challenges Conference: Expanding Housing Finance to the Lower Income Groups The World Bank, Washington D.C. 17 March, 2006 Presented by: Juan Enrique Montes Gerente General de Securitizadora Security GMAC- RFC S.A.

Conference: Expanding Housing Finance to the Lower Income Groups The World Bank, Washington D.C.

Jan 01, 2016

Lease-to-Purchase Housing Finance in Chile: Context, Past Experience, Future Opportunities & Challenges. Conference: Expanding Housing Finance to the Lower Income Groups The World Bank, Washington D.C. 17 March, 2006 Presented by: Juan Enrique Montes - PowerPoint PPT Presentation

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Lease-to-Purchase Housing Finance in Chile: Context, Past Experience, Future Opportunities & Challenges

Conference:

Expanding Housing Finance to the Lower Income Groups

The World Bank, Washington D.C.

17 March, 2006

Presented by:

Juan Enrique Montes

Gerente General de Securitizadora Security GMAC-RFC S.A.

2

Outline of PresentationContext:

Macroeconomic Scenario

Income Distribution and Housing Needs

Housing activity

Lease-to-Purchase Housing Finance: Past Experience and Current Status

Funding Players in Housing Activity

Leasings versus other Financing Vehicles

Historic Evolution

The Role of Government

MBS: Securitization of Leasings and Mutuos Hipotecarios Endosables (EMC)

ABS Track Record

MBS Track Record

Mortgage Prepayment Impact on MBS

Securitizatio of Lease-to-Purchase Housing Contracts: Future Opportunities and Challenges

Needs, Opportunities & Challenges

Expected Future Outcomes

3

Macroeconomic Scenario: GDP Dynamism

GDP (Growth Rate,%)

6,4%

4,4%

-0,02

0,01

0,04

0,07

0,10

0,13

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

GDP Average

4

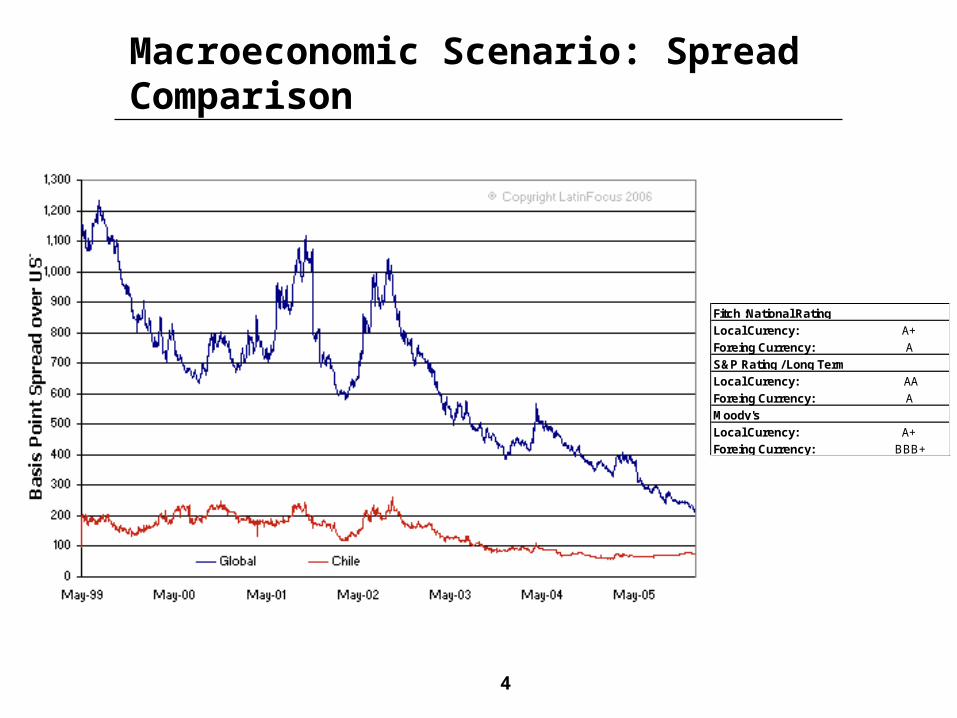

Macroeconomic Scenario: Spread Comparison

Local Curency: A+

Foreing Currency: A

Local Curency: AA

Foreing Currency: A

Local Curency: A+

Foreing Currency: BBB+

Moody's

Fitch :National Rating

S&P Rating / Long Term

5

Macroeconomic Scenario: Unemployment Rate

Unemployment (%)

8,8

7,3

5,5

6,0

6,5

7,0

7,5

8,0

8,5

9,0

9,5

10,0

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

Unemployment % Average

6

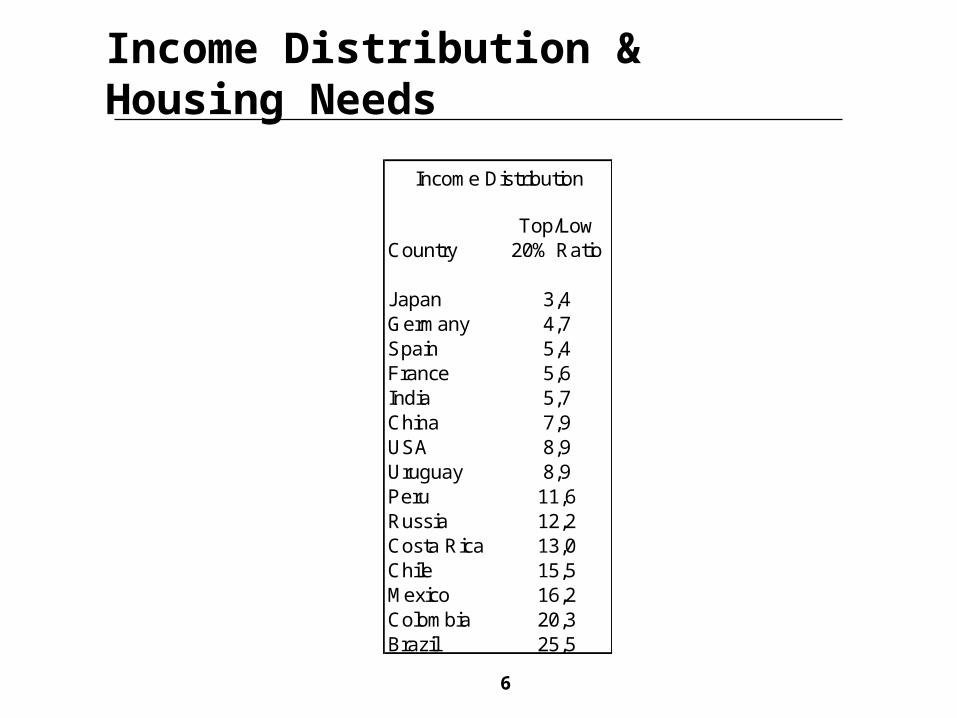

Income Distribution & Housing Needs

CountryTop/Low

20% Ratio

Japan 3,4Germany 4,7Spain 5,4France 5,6India 5,7China 7,9USA 8,9Uruguay 8,9Peru 11,6Russia 12,2Costa Rica 13,0Chile 15,5Mexico 16,2Colombia 20,3Brazil 25,5

Income Distribution

7

Income Distribution & Housing Needs

20% 1990 1994 1996 1998 2000 2003I 4,1 4 3,9 3,7 3,8 3,9II 8,1 8,1 8 8 8,1 8,4III 12,3 11,9 11,7 11,7 12,2 12,1IV 18,1 18,7 19,3 19,3 18,5 19V 57,4 57,3 57,1 57,3 57,5 56,5V/ I 14 14,3 14,6 15,5 15,3 14,3

Home Income Distribution Evolution

8

Income Distribution & Housing Needs

Income Decil Total (%)1 22,42 17,13 16,34 13,2

Subtotal (40% poorest people) 69,0

5 9,16 7,27 6,68 4,19 3

10 1,1

Total 100,0

Housing Deficit Distribution

9

Housing Activity: Sales v/s Housing Deficit

As of 2002, Housing Deficit reaches 543,000 houses or 14% of Total Housing stock

Housing Deficit is explained by 2 basic factors:

387,000 difference between number of Families v/s Number of Houses

155,000 of houses in poor structural conditions

House building pattern (120,000 new houses per year) would take 4,5 years to meet Housing Deficit Needs

However, population growth (1.3%) plus social-economic changes has meant a 2.3% housing need growth

In addition to that, house deterioration also boost housing needs

Considering just home 2.3% growth and 4% house building growth, Chilean housing deficit would disappear in 12 years

This housing deficit is focused in the lowest socio-economic spectrum, thus representing a long-term demand for leasing

10

Housing Activity: Sales v/s Housing Deficit

In 2005, house sales reached US$ 3.2 billion in Santiago. (This data does not include houses provided by the government to poor people)

These sales only represents houses valued at US$ 17,500 (or more)

Leasings typically funds US$ 17,500 to US$ 52,500 houses

33% of total sales (in number) are concentrated in the Leasing niche but, in terms of amounts, sales in this niche represent 13% of the total volume

Thus, this segment reached US$ 420 million sales in 2005

Giving that Santiago represents 40% of Chile housing activity, we may estimate Leasing Market Volume at US$ 1 billion per year

Economic growth (through employment & wages increases) plus Income Distribution improvements may boost this market volume

11

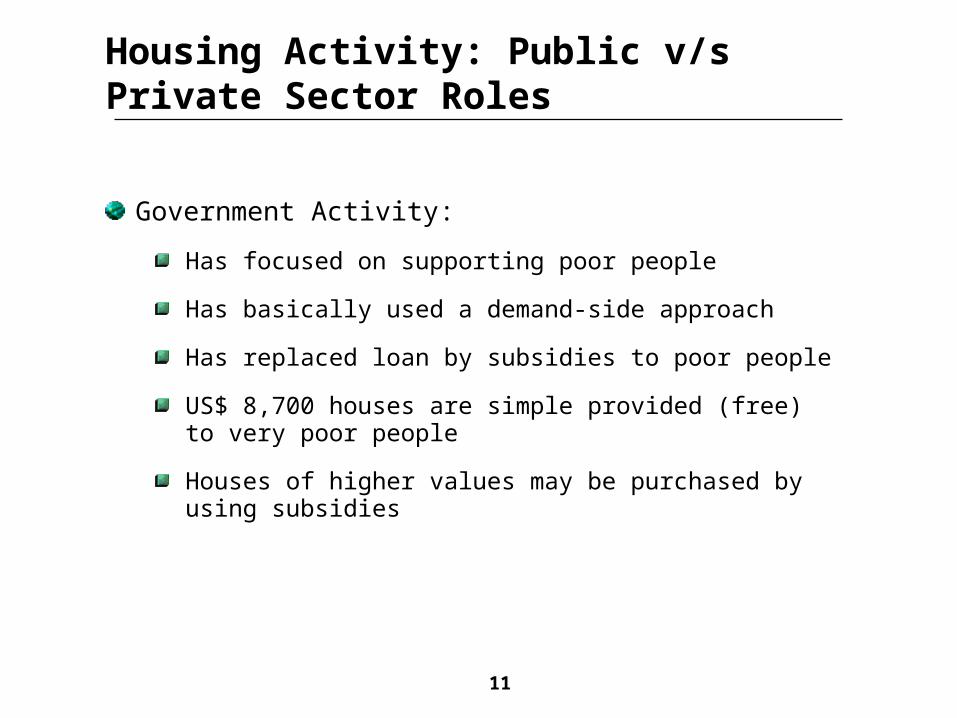

Housing Activity: Public v/s Private Sector Roles

Government Activity:

Has focused on supporting poor people

Has basically used a demand-side approach

Has replaced loan by subsidies to poor people

US$ 8,700 houses are simple provided (free) to very poor people

Houses of higher values may be purchased by using subsidies

12

Leasings : Funding Players in Housing Activity

Real Estate Developers and Constructing companies

Bank Loans

Demand Side Funding:

Government Funding Mechanisms and Banco del Estado (average mortgage of Banco Estado: US$ 9,000).

Commercial Banks Loans (average mortgage: US$ 56,600)

“Mutuos Hipotecarios Endosables” (EMC)

Leasing Habitacional (Lease-to-Purchase Housing Vehicle)

13

Leasings : Pros/Cons v/s Alternative Vehicles

Advantages

No tax applicable (Alternatives: 1,6% of Loan Volume)

No down-payment (Alternatives: non less than 25% of house value)

Houses of US$ 35,000 (or less) are eligible for automatic subsidy (Alternatives: Subsidy uses an “application system”)

Collateral is the house (Alternative: Mortgage over the house)

Legal Framework allows quick “arbitral” legal process (Alternative: Longer legal process)

No tax for investors if house is a “DFL-2” (Alternative: pays 17% corp. tax or personal tax, DFL2 is an “economic house of 140 or less sq. meters)

Disadvantages

Relatively new vehicle (Alternatives: More than 25 years track record provides experience)

Some uncertainty in case leasings are used as collateral and borrower falls into bankruptcy (Alternatives: Pledge over EMC presents no legal uncertainty)

Must be held by a Securitizadora, Lease Originator or Real Estate Fund, only (Alternatives: EMC are eligible for Life Insurance Companies and Banks)

Consequences

Leasings has focused in medium income segments (US$ 17,500 to US$ 52,500 houses)

Leasings have not been fully exploited in terms of volume and rates

14

PeriodNon-bank

EMCsLeasing

ContractsNon-Bank

TotalBank EMCs

Bank Loans

Letters of Credit

Bank Total TOTAL

1996 199 1 200 146 112 924 1.181 1.3811997 243 10 252 236 128 716 1.081 1.3321998 225 24 246 684 32 168 884 1.1311999 208 35 239 600 224 194 1.018 1.2572000 170 41 206 185 214 479 878 1.0842001 259 58 309 -308 157 539 389 6982002 325 79 394 66 243 305 614 1.0082003 493 97 580 -31 697 783 1.450 2.0292004 582 86 668 -103 3.591 -856 2.631 3.2992005 739 81 820 104 3.305 -251 3.157 3.977

Supply Flow Analysis: Residential Mortgages (Figures in USD Millions)

Leasings: Historic Evolution of Funding Vehicles

15

PeriodNon-bank

EMCsLeasing

ContractsNon-Bank

Total Bank EMCs Bank Loans Letters of Credit Bank Total TOTAL

2002 1.786 229 2.014 1.733 1.524 7.411 10.668 12.6822003 1.688 321 2.009 1.702 2.221 8.194 12.117 14.1272004 1.940 410 2.350 1.599 5.811 7.338 14.748 17.0992005 2.114 491 2.605 1.723 8.763 7.077 17.564 20.169

Stock Analysis: Residential Mortgages

(Figures in USD Millions)

Leasings: Historic Evolution of Funding Vehicles

16

Leasing: Historic Evolution of EMC & Leasings

Loan Volume Average Rate Average Loan Loan Volume Average Rate Average Loan Loan to Value

in Th. US$ in UF in Th. US$ in Th. US$ in UF in Th. US$

1996 199 8,5% 52 1 23 86

1997 243 8,5% 45 10 23 90

1998 225 9,4% 44 24 22 90

1999 208 8,6% 52 35 22 91

2000 170 8,7% 50 41 11,9% 24 92

2001 259 7,8% 58 58 11,3% 25 92

2002 325 7,1% 59 79 10,6% 25 93

2003 493 6,5% 63 97 10,6% 26 93

2004 582 5,9% 74 86 11,5% 22 87

2005 738 5,1% 74 81 10,0% 21 79

Average 344 7,6% 57 51 11,0% 23 89

Non-Bank EMC's Leasings

17

Leasings: The role of government

Demand Side Subsidy (Borrower)

Eligibility: House Values of US$ 8,750 to US$ 35,000

Magnitude: 11% of House Value (From 56% to 9%)

Leasing Case: New (Bond) System v/s Old System

Supply Side Subsidy (Originator)

Eligibility: House Values of US$ 21,000 or less

Magnitude: 2.3% of House Value (“Modest” Houses)

Lender Subsidy (SPV or other credit holder)

Eligibility: House Values of US$ 21,000 or less

Loss Limit capped at US$ 7,000 or 75% of loss volume

18

As of December 2005 in US millions

Total Investment ABS Penetration

Pension Funds 74.755 309 0,4%Life Insurance Co. 23.063 614 2,7%P&C Insurance Co. 576 11 1,9%Banks 16.168 N/A N/AMutual Funds 12.628 167 1,3%Others N/A 701 N/A

Total 127.190 1.802 1,4% *

MBS Track Record: Capital Market Penetration

19

Figures in Millions US$MBS Non MBS Total

Total Bond 1.274 1.625 2.899

Number of Total SPV's 37 32 69

Total

Total Bond 44% 56% 100%

Number of Total SPV's 54% 46% 100%

MBS Non MBS

ABS Track Record: Outstanding Bond Volumes

20

Mortgage Prepayment Impact: Risk-Free Rate Trajectory

PRC 20, BCU 10

2,00

3,00

4,00

5,00

6,00

7,00

8,00

9,00

Ene

-95

Jul-9

5

Ene

-96

Jul-9

6

Ene

-97

Jul-9

7

Ene

-98

Jul-9

8

Ene

-99

Jul-9

9

Ene

-00

Jul-0

0

Ene

-01

Jul-0

1

Ene

-02

Jul-0

2

Ene

-03

Jul-0

3

Ene

-04

Jul-0

4

Ene

-05

Jul-0

5

Ene

-06

Date

Rat

e (%

)

21

Mortgage Prepayment Impact: MBS Shock

Note: 2 of the 11 downgrade-liquidated cases were impacted by asset default performance and prepayment, whereas 9 were impacted by prepayment only

Prepayment Impact Over SPV's bond classification

Quantity% Over Senior Bond Amount

% Leasing participation

(Amount)

% EMC participation

(Amount)

Downgraded 5 16,8% 10,9% 89,1%

Liquidated 6 36,8% 18,1% 81,9%

Remain Identical 26 46,3% 45,1% 54,9%

Total 37 100,0% 29,4% 70,6%

22

Mortgage Prepayment Impact: Long-Term Consequences

No (or negligible) negative equity on Senior Bonds

Originators not able to continue making short-run profits

Rating Risk Agencies and Securitizadoras improving structures

Regulator increases control

Institutional investors more able to assess different risks

In sum, a deep change on MBS industrial organization

23

Securitization of Leasings: Opportunities & Challenges

Social and Private Needs:

Housing deficit reduction

Leasing penetration & rates reduction

Higher MBS penetration: Improve volumes, liquidity and risk features

Challenges :

Government: Improve Leasing legal framework, Simplify ABS issuance rules

Rating Risk Agencies: Anticipate potential portfolio changes

Originators: Adaptation to new business environment and improve U/W criteria

Securitizadoras: Boost MBS penetration

Opportunities:

Originators: Focus on originating activities

Banks: Provide long-term funding to warehouse and/or credit enhancement

Securitizadoras: Launch a new business model

24

Securitizations of Leasings: Opportunities & Challenges

Expected Future Outcomes

Housing deficit reduction

Individuals with more funding opportunities

Long term bankers with more loan exposure

Private credit enhancement replaces Government subsidies

Capital Market (MBS) development

Securitizadora and Originators more focused on their core competencies

Related Documents