Journal of Econometrics 98 (2000) 129 }161 Conditionally independent private information in OCS wildcat auctions Tong Li!, Isabelle Perrigne",*, Quang Vuong",# !Indiana University, Los Angeles, USA "Department of Economics, University of Southern California, Los Angeles 90089-0253, USA #INRA, France Received 1 May 1998; received in revised form 1 October 1999; accepted 1 October 1999 Abstract In this paper, we consider the conditionally independent private information (CIPI) model which includes the conditionally independent private value (CIPV) model and the pure common value (CV) model as polar cases. Speci"cally, we model each bidder's private information as the product of two unobserved independent components, one speci"c to the auctioned object and common to all bidders, the other speci"c to each bidder. The structural elements of the model include the distributions of the common component and the idiosyncratic component. Noting that the above decomposition is related to a measurement error problem with multiple indicators, we show that both distributions are identi"ed from observed bids in the CIPV case. On the other hand, identi"cation of the pure CV model is achieved under additional restrictions. We then propose a computationally simple two-step nonparametric estimation procedure using kernel estimators in the "rst step and empirical characteristic functions in the second step. The consistency of the two density estimators is established. An application to the OCS wildcat auctions shows that the distribution of the common component is much more concentrated than the distribution of the idiosyncratic component. This suggests that idiosyncratic components are more likely to explain the variability of private information and hence of bids than the common component. ( 2000 Elsevier Science S.A. All rights reserved. JEL classixcation: D44; C14; L70 * Corresponding author. Tel.: (213) 740 3528; fax: (213) 740 8543. E-mail address: perrigne@usc.edu (I. Perrigne). 0304-4076/00/$ - see front matter ( 2000 Elsevier Science S.A. All rights reserved. PII: S 0 3 0 4 - 4 0 7 6 ( 9 9 ) 0 0 0 8 1 - 0

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Journal of Econometrics 98 (2000) 129}161

Conditionally independent private informationin OCS wildcat auctions

Tong Li!, Isabelle Perrigne",*, Quang Vuong",#

!Indiana University, Los Angeles, USA"Department of Economics, University of Southern California, Los Angeles 90089-0253, USA

#INRA, France

Received 1 May 1998; received in revised form 1 October 1999; accepted 1 October 1999

Abstract

In this paper, we consider the conditionally independent private information (CIPI)model which includes the conditionally independent private value (CIPV) model and thepure common value (CV) model as polar cases. Speci"cally, we model each bidder'sprivate information as the product of two unobserved independent components, onespeci"c to the auctioned object and common to all bidders, the other speci"c to eachbidder. The structural elements of the model include the distributions of the commoncomponent and the idiosyncratic component. Noting that the above decomposition isrelated to a measurement error problem with multiple indicators, we show that bothdistributions are identi"ed from observed bids in the CIPV case. On the other hand,identi"cation of the pure CV model is achieved under additional restrictions. We thenpropose a computationally simple two-step nonparametric estimation procedure usingkernel estimators in the "rst step and empirical characteristic functions in the secondstep. The consistency of the two density estimators is established. An application to theOCS wildcat auctions shows that the distribution of the common component is muchmore concentrated than the distribution of the idiosyncratic component. This suggeststhat idiosyncratic components are more likely to explain the variability of privateinformation and hence of bids than the common component. ( 2000 Elsevier ScienceS.A. All rights reserved.

JEL classixcation: D44; C14; L70

*Corresponding author. Tel.: (213) 740 3528; fax: (213) 740 8543.E-mail address: [email protected] (I. Perrigne).

0304-4076/00/$ - see front matter ( 2000 Elsevier Science S.A. All rights reserved.PII: S 0 3 0 4 - 4 0 7 6 ( 9 9 ) 0 0 0 8 1 - 0

Keywords: Conditionally independent private information; Common value model; Non-parametric estimation; Measurement error model; OCS wildcat auctions

1. Introduction

Over the last ten years, the analysis of auction data has attracted muchinterest through the development of the structural approach. This approachrelies on econometric models closely derived from game-theoretic auctionmodels that emphasize strategic behavior and asymmetric information amongparticipants. The structural econometrics of auction models then consists in theidenti"cation and estimation of the structural elements of the theoretical modelfrom available data. The structural elements usually include the latent distribu-tion of private information while observations are usually bids. Previous studieshave mainly adopted the independent private values (IPV) paradigm, whereeach bidder knows his own private value for the auctioned object but does notknow others' valuations which are independent from his.1 An alternative para-digm is the pure common value (CV) paradigm, where the value of the auctionedobject is assumed to be common ex post but unknown ex ante to all bidders whohave private signals about this value. It has been used in Paarsch (1992). Morerecently, Li et al. (1999) have extended the structural approach to the moregeneral a$liated private value (APV) model where bidders' private values area$liated in the sense of Milgrom and Weber (1982).

In this paper, we consider a model where a$liation among private informa-tion arises through an unknown common component. Speci"cally, we assumethat each private information (either private values or signals) can be decom-posed as the product of two unknown independent random components, onecommon to all bidders and the other speci"c to each bidder. Because privateinformation are independent conditionally upon the common component, theresulting model is called the conditionally independent private information(CIPI) model. As we shall see, the CIPI model is quite general and includes asspecial cases the conditionally independent private value (CIPV) model and thepure common value (CV) model.

The structural elements of the CIPI model include the distributions of thecommon and idiosyncratic components of private information. Consideringa quite general model and decomposing private information render the identi-"cation and estimation of the structural elements from observed bids more

1Donald and Paarsch (1996), Paarsch (1992) and La!ont et al. (1995) have proposed someparametric estimation methods while Guerre et al. (2000) and Elyakime et al. (1994, 1997) havedeveloped some nonparametric ones.

130 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

complicated than in previous studies such as Guerre et al. (2000) for the IPVmodel and Li et al. (1999) for the APV model. It turns out that identi"cation andestimation of the CIPI model is related to the measurement error model whenmany indicators are available as studied by Li and Vuong (1998). We show thatthe CIPV model is fully identi"ed nonparametrically. On the other hand, theidenti"cation of the CV model requires some restrictions as the CV model is notidenti"able in general from observed bids, see La!ont and Vuong (1996). Ineither case, combining Li et al. (1999) and Li and Vuong (1998) we proposea two-step nonparametric procedure for estimating the density of the idiosyn-cratic component and the density of the common component. In particular, ourprocedure uses kernel estimators in the "rst step and empirical characteristicfunctions in the second step. We then establish the consistency of our estimators.

As an application, we study the Outer Continental Shelf (OCS) wildcatauctions. These auctions present some speci"c features which render the CIPImodel relevant. On one hand, the common component can be viewed as theunknown expost value. On the other hand, the idiosyncratic component can beconsidered as arising from a "rm's speci"c drilling, prospecting and develop-ment strategies, capital and "nancial constraints, opportunity costs as well asthe precision of its own estimate of the value of the tract derived from geologicalsurveys.

The structure of the CIPI model enables us to assess the roles played by boththe common and idiosyncratic components in "rms' bidding strategies. Conse-quently, our approach complements previous studies done by Hendricks andPorter (see Porter, 1995 for a survey) who adopted the pure common valueparadigm within a reduced form approach. In particular, comparisons of thedistributions of the common and idiosyncratic components indicate that theidiosyncratic component explains a large part of the variability of bidders'signals, and hence of bids.

Our paper is original for several reasons. First, it contributes to the structuralanalysis of auction data as it shows that the structural approach can be extendedto the CIPV and pure CV models. Second, from an econometric point of view,we propose an original method for estimating nonparametrically the latentdistributions of each model that combines kernel methods and empirical charac-teristic functions. To our knowledge, the latter have been seldom used inempirical work. Third, we provide a new analysis of OCS wildcat auctionsthrough a speci"ed structure of a$liation among valuations.

The paper is organized as follows. Section 2 presents the CIPI model and itsspecial cases, the CIPV and pure CV models. We consider identi"cation of bothmodels and propose a two-step nonparametric procedure to estimate the under-lying structural elements, namely the density of the idiosyncratic componentand the density of the common component. Moreover, we show that ourestimators are consistent. In Section 3, after a brief description of the OCSwildcat auctions and the corresponding data, we illustrate our procedure to

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 131

auctions with two bidders and present our empirical "ndings. Section 4 con-cludes the paper. Proofs are contained in an appendix.

2. The CIPI model and the structural approach

In this section, we "rst present the CIPI model as well as the related CIPVand pure CV models. We then address their identi"cation from observed bids.Finally, we propose a two-step nonparametric procedure for estimating theunderlying structural elements.

2.1. The CIPI, CIPV and CV models

We begin with the general a$liated value (AV) model introduced by Wilson(1977) and Milgrom and Weber (1982).

A single and indivisible object is auctioned to n*2 bidders. The utility ofeach potential bidder i, i"1,2, n, for the object is ;

i";(p

i, v) where ;( ) ) is

a nonnegative function strictly increasing in both arguments, pidenotes the ith

player's private signal or information and v represents a common component orvalue a!ecting all utilities. The vector (p

1,2,p

n, v) is viewed as a realization of

a random vector whose (n#1)-dimensional cumulative distribution functionF( ) ) is a$liated and exchangeable in its "rst n arguments.2 The distribution F( ) )is assumed to have a support [p

6, p6 ]n][v

6,v6 ] with p

6*0 and v

6*0 and a density

f ( ) ) with respect to Lebesgue measure. Each player i knows the value of hissignal p

ias well as F( ) ). However, he does not know the other bidders' private

signals and the common component v.In the CIPI model, it is assumed that bidders' private signals p

iare condi-

tionally independent given the common component v. Let Fv( ) ) and Fp@v( ) D ) )

denote the cumulative distribution functions of v and p given v, respectively,with corresponding densities f

v( ) ) and fp@v( ) D ) ) and nonnegative supports [v

6, v6 ]

and [p6, p6 ]. Hence in the CIPI model, the joint distribution F( ) ) of (p

1,2,p

n, v)

is entirely determined by the pair [Fv( ) ),Fp@v( ) D ) )] as

f (p1,2,p

n, v)"f

v(v)Pn

i/1fp@v (pi

Dv). (1)

It can be easily shown from (1) that F( ) ) is symmetric or exchangeable in its "rstn arguments and a$liated. Consequently, the CIPI model is a special case of thegeneral a$liated value model introduced by Wilson (1977) and Milgrom andWeber (1982).

2See Milgrom and Weber (1982) for a de"nition of a$liation. Intuitively, a$liation implies thata bidder who evaluates the object highly will expect others to evaluate the object highly too.

132 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

We focus on the "rst-price sealed-bid auction, which is the mechanism used inthe OCS wildcat auctions analyzed in this paper. As usual, we restrict ourattention to strictly increasing di!erentiable symmetric Bayesian Nash equilib-rium strategies. At such an equilibrium, player i chooses his bid b

iby maximiz-

ing E[(;i!b

i)1(B

i)b

i)Dp

i] where B

i"s(y

i), y

i"max

jEipj, s( ) ) is the

equilibrium strategy, and E[ ) Dpi] denotes the expectation with respect to all

random elements conditional on pi. As is well-known, the equilibrium strategy

satis"es the "rst-order di!erential equation

s@(pi)"[<(p

i, p

i)!s(p

i)] f

y1 @p1(p

iDp

i)/F

y1 @v1(p

iDp

i), (2)

for all pi3[p

6, p6 ] subject to the boundary condition s(p

6)"<(p

6, p

6), where

<(pi, y

i)"E[;(p

i, v)Dp

i, y

i], F

y1 @p1( ) D ) ) denotes the conditional distribution of

y1

given p1, and f

y1 @p1( ) D ) ) is its density. The index &1' refers to any bidder among

the n bidders because the game is symmetric. The distribution Fy1 @p1

( ) D ) ) is theone corresponding to the probability structure de"ned in (1). As shown byMilgrom and Weber (1982), when the reservation price is nonbinding, thesolution is

bi"s(p

i)"<(p

i, p

i)!P

pi

p6¸(aDp

i) d<(a, a), (3)

where ¸(aDpi)"exp[!:pi

a fy1 @p1

(uDu)/Fy1 @p1

(uDu) du]. It is easy to verify thatbi"s(p

i) is strictly increasing in p

ion [p

6, p6 ].

Two important models are derived from the CIPI model. These are the CIPVmodel and the pure CV model.

2.1.1. The CIPV modelIn this model, it is assumed that ;(p

i, v)"p

iso that each bidder's private

information is his own utility, which he knows fully at the time of the auction.We are thus in the private value paradigm and <(p

i, y

i)"p

i.

An economic interpretation of the CIPV model is as follows. Bidders' valu-ations are independently drawn from a common distribution Fp@v ( ) Dv) thatdepends on an unknown parameter v. Thus F

v( ) ) can be interpreted as bidders'

common prior distribution on v. In particular, v can be interpreted as the ex postvalue of the auctioned object for the average bidder while the discrepancybetween p

iand v results from bidder's speci"c characteristics such as his

productive e$ciency, opportunity costs, idiosyncratic preferences, etc. TheCIPV model extends the IPV model by allowing for a$liation among bidders'private values through the unknown common component v. Because it speci"esa special structure on a$liation, it is a special case of the APV model.3

3 In fact, if one assumes that (p1,2,p

n) are exchangeable for every n, then (p

1,2,p

n) are

necessarily conditionally independent by de Finetti's Theorem. See, e.g. Kingman (1978). Conse-quently, any APV model is a CIPV model under such an assumption.

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 133

The CIPV model formalizes the idea that a bidder who evaluates the objecthighly will expect others to evaluate it highly too. It is well suited to auctionsituations, where there is some &prestige' value in owning the auctioned objectwhich is admired by other bidders and there is a possibility of resale at somecurrently undetermined price. These include auction of works of art, memor-abilia, collectibles, etc. In the case of OCS auctions, the auctioned tract adds tothe capital of the winning oil company while the mineral content of the tract isuncertain to the "rm.

2.1.2. The pure CV modelIn this model, it is assumed that ;(p

i, v)"v so that each bidder derives the

same but unknown utility from the auctioned object while piis bidder i's private

estimate of the common value. In this case, <(pi, y

i)"E[vDp

i, y

i"p

i].

The economic interpretation of the pure CV model is well known. Di!erencesin bidders' preferences are neglected. On the other hand, bidders di!er throughtheir private information about the value of the auctioned object. This modelhas been frequently used to analyze auctions of drilling rights as the mineralcontent of the tract is subject to important uncertainty (see, e.g. Rothkopf, 1969,Wilson, 1977). As a result the model is sometimes called the mineral rights model(see Milgrom and Weber, 1982). In particular, oil companies are assumed tohave di!erent estimates of the value of the tract, which are derived fromgeological surveys, but are assumed to have identical productive e$ciency,opportunity costs, etc.

2.2. Nonparametric identixcation

The structural approach relies on the hypothesis that the observed bids arethe equilibrium bids of the auction model under consideration. Hence, thestructural econometric model associated with the CIPI model is de"ned as

bi"s(p

i, ;, F

v, Fp@v) for i"1,2, n, n*2, (4)

where s( ) ) is the equilibrium strategy (3). In particular, because private signalsare random and unobserved, bids are naturally random with an n-dimensionaljoint distribution G( ) ) determined by the structural elements of the model[;( ) ), F

v( ) ), Fp@v( ) D ) )].

To implement the structural approach, a fundamental issue is whether thestructural elements of the economic model are identi"ed from available observa-tions. In general, all "rms' private information as well as the common compon-ent are unknown to the econometrician, while only bids are observed. Therefore,the identi"cation of the CIPI model reduces to whether the utility function;( ) )and the two underlying structural distributions F

v( ) ) and Fp@v ( ) D ) ) can be

determined uniquely from observed bids. An important feature of (4) is that thejoint equilibrium bid distribution G( ) ) depends on the underlying distributions

134 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

Fv( ) ) and Fp@v ( ) D ) ) in two ways: (i) through the unobserved p

i, which is drawn

from Fp@v ( ) Dv) while v is drawn from Fv( ) ), and (ii) through the equilibrium

strategy, which is a complex function of F( ) ) and therefore of Fv( ) ) and Fp@v( ) D ) )

through (1) (see(3)). This feature complicates the analysis of identi"cation.Following a similar argument as in Li et al. (1999), denote the conditional

distribution of B1

given b1

by GB1 @b1

( ) D ) ) and its density by gB1 @b1

( ) D ) ). Then

GB1 @b1

(X1Dx

1)"Pr(B

1)X

1Db

1"x

1)

"Pr(y1)s~1(X

1)Dp

1"s~1(x

1))

"Fy1 @p1

(s~1(X1)Ds~1(x

1)).

It follows that

gB1 @b1

(X1Dx

1)"

fy1 @p1

(s~1(X1)Ds~1(x

1))

s@(s~1(X1))

.

Using the last two equations and p"s~1(b), the "rst-order di!erential equation(2) can be written as

<(p, p)"b#G

B1 @b1(bDb)

gB1 @b1

(bDb),m(b,G). (5)

Recall that <(p, p)"E[;(p1, v)Dp

1"p, y

1"p]. Thus a distinguishing feature

of (5) is that it expresses such an expected value as an explicit function of thecorresponding observed bid, the distribution G

B1 @b1( ) D ) ) and density g

B1 @b1( ) D ) )

of bids without solving the di!erential equation (2). The above equation formsthe basis upon which the identi"ability of the CIPI, CIPV and CV models canbe studied.4

The next proposition relates the identi"ability of these three models. Here-after, we use the standard notion of observational equivalence of competingmodels from observables, which are here the observed bids. See La!ont andVuong (1996) for a formal de"nition.

Proposition 1. Any CIPI model is observationally equivalent to a CIPV model.Hence, any pure CV model is observationally equivalent to a CIPV model.

The "rst part of Proposition 1 says that when explaining bids with condi-tionally independent signals, one can restrict oneself to a CIPV model withoutloss of explanatory power. The second part says that any interpretation in termsof the pure CV model can be equally given in terms of a CIPV model. This

4Because the conditional independence of signals was not used, (5) actually holds for the generalAV model. It also forms the basis upon which the identi"cation of the AV model can be studied.

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 135

proposition parallels Proposition 1 in La!ont and Vuong (1996), which relatesAV to APV models. The di!erence here is that private signals are now assumedto be conditionally independent, which leads naturally to the CIPI and CIPVmodels. Intuitively, to establish that any CIPI model is observationally equiva-lent to a CIPV model, the argument is that ;(p

i, v) can be replaced by ;I

i"p8

i,

where p8i"<(p

i, p

i) are conditionally independent given v. In other words,;( ) )

is not identi"ed. Thus, we focus below on the CIPV and pure CV models where;(p, v)"p and ;(p, v)"v, respectively.5

As noted by La!ont and Vuong (1996, Proposition 4), however, the pure CVmodel is not identi"ed. Similarly, it can be shown that the CIPV model is notidenti"ed either. Intuitively, the conditioning variable v in a CIPV model can bereplaced by any strictly increasing transformation of v while retaining the sameprobabilistic structure on the utilities (p

1,2,p

n). This implies that additional

restrictions are needed for identi"cation. Assuming that signals are unbiased isnot su$cient by itself. In this paper, we assume the multiplicative decompositionpi"vg

i, where v is the common component and g

iis speci"c to the ith bidder.

Moreover, the following assumptions are made.

A1: The gi's are identically distributed with a mean equal to one.

A2: v and the gi's are mutually independent.

The mean requirement in Assumption A1 is a natural normalization andensures that the signals are unbiased estimates of the common component as inWilson (1977). Together Assumptions A1 and A2 imply that private signals p

i's

are independent and identically distributed conditionally upon v. The structuralelements of either model are now the pair [F

v( ) ), Fg( ) )], where Fg( ) ) is the

cumulative distribution of g with support [g6, g6 ] so that [p

6, p6 ]"[vg, v6 g6 ].6

2.2.1. Identixcation of the CIPV modelAs noted earlier, the CIPV model is a special case of the APV model. From

the nonparametric identi"cation of the APV model (see Li et al., 1999, Proposi-tion 2.1), it follows that the joint distribution of private values in the CIPVmodel is identi"ed from observed bids. The remaining question is whether thestructural elements [F

v( ) ), Fg( ) )] of the CIPV model are uniquely determined

5Given the similar probabilistic structure of the CIPV and pure CV models, an interestingquestion is whether any CIPI model is observationally equivalent to a pure CV model. A positiveanswer would imply the converse of the second part of Proposition 1. At this stage, however, it is notknown whether such a conjecture is true.

6See also Wilson (1998). An alternative decomposition for private signals is pi"v#g

iwith the

same Assumptions A1 and A2 with the exception that the gis have a zero mean. We have chosen the

multiplicative decomposition instead because it is more natural with nonnegative variables. Below,we indicate how to adapt our results under the additive decomposition.

136 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

by such a joint distribution. To address this question, we note that the multipli-cative decomposition leads to logp

i"log c#log e

i, where

log c,[log v#E(log g)], log ei,[log g

i!E(log g)], (6)

i"1,2, n*2, and log ei

has zero mean. Hence, under Assumptions A1}A2,this problem is related to an error-in-variable model with multiple indicators.Indeed, log e

ican be considered as the error term in the classical measurement

error model where log c is unobserved. Because the pis can be recovered from

observed bids through (5) where <(p, p)"p, their logs can be viewed asindicators for log c.

When the densities for log c and log e are both unknown, the error-in-variablemodel with multiple indicators is nonparametrically identi"ed under a mildadditional condition (see Li and Vuong, 1998, Lemma 2.1). In our context, sucha condition is satis"ed under the following assumption.

A3: The characteristic functions /v( ) ) and /g( ) ) of log v and log g are nonvan-

ishing everywhere.

Such an assumption is standard in the related deconvolution problem with/g( ) ) known and only one indicator (see, e.g. Fan, 1991; Diggle and Hall, 1993for recent contributions).7 From Li and Vuong's (1998) identi"cation result,which relies upon Kotlarski's result (see Rao, 1992, p. 21), we have immediatelythe following lemma, which will be also useful in the estimation part. Through-out, we use h

x( ) ) to denote the density of logx, keeping f

x( ) ) for the density of x.

Lemma 1. Given A1}A3, the densities hc( ) ) and he( ) ) are uniquely determined by

the joint distribution of an arbitrary pair (logp1, logp

2). Their characteristic

functions are

/c(t)"expP

t

0

Lt(0, u2)/Lu

1t(0, u

2)

du2, (7)

/e(t)"t(0, t)

/c(t)

"

t(t, 0)

/c(t)

, (8)

where t(t1, t

2) is the characteristic function of (logp

1, logp

2).

The identi"cation result in Lemma 1 is useful because not only are thedensities h

c( ) ) and he ( ) ) of log c and log e identi"ed by the joint distribution of

7To our knowledge, the mutual independence of c and e and hence of v and g in A2 is crucial forthe nonparametric identi"cation of the measurement error model with multiple indicators. A stron-ger assumption than A1 is that the density of log g is symmetric about its mean, i.e. that the density oflog e is symmetric about zero. For a recent contribution using the latter assumption within a paneldata framework, see Horowitz and Markatou (1996).

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 137

(logp1, logp

2), but explicit formulae for the characteristic functions of these

densities are also available.8The next proposition establishes the identi"cation of the CIPV model and

characterizes the restrictions on the distribution of observed bids that areimposed by the CIPV model. In particular, it uses Lemma 1 and the equalityE(log g)"!logE(e), which results from the normalization condition E(g)"1.

Proposition 2. Given A1}A3, the CIPV model is identixed. Moreover, a distributionof observed bids can be rationalized by a CIPV model if and only if (i) bids aresymmetric and conditionally independent, and (ii) the function m( ) ,G) is strictlyincreasing on [b

M, bM ].

2.2.2. Identixcation of the pure CV modelThe next proposition establishes the partial identi"cation of the pure CV

model under the following assumption.

A4. <(p, p) is loglinear in log p, i.e. logE[vDp1"p, y

1"p]"C#D logp,

where (C, D)3R]RH̀ .9

The usefulness of A4 under the multiplicative decomposition can be seen bynoting that logE[vDp

i, y

i"p

i]"log c#log e

i, where log c and log e

iare now

de"ned as

log c"C#DE(log g)#D log v, log ei"D[logg

i!E(log g)], (9)

where E(log g)"!logE(e1@D) using the normalization E(g)"1.

Proposition 3. Given A1}A4, the distributions of v and g are given by

log v"logE[e1@D]!C

D#

1

Dlog c, log g"!logE[e1@D]#

1

Dlog e,

where the distributions of c and e are identixed from observed bids throughLemma 1 with t(t

1, t

2) being now the characteristic function of

(log<(p1, p

1), log<(p

2, p

2)) (say).

Proposition 3 says that, up to (C, D) which determine the location and scale,the distributions of log v and log g are uniquely determined from observed bids.Moreover, because the scale is common, the ratio Var(logg)/Var(log v) is inde-pendent of (C, D) and equal to the ratio Var(log e)/Var(log c). Since the latter is

8As indicated in Li and Vuong (1998), an alternative way to establish the identi"ability of(h

c( ) ), he( ) )) consists in showing that all moments of log c and log e are identi"ed from the moments

of the joint density of logp1, logp

2. For instance, E[log c]"E[logp

1]"E[logp

2],

E[log2 c]"E[logp1logp

2], E[log2 e]"E[log2p

1]!E[logp

1logp

2], etc.

9Because of a$liation, E[vDp1"p, y

1"p] is strictly increasing in p. Hence D'0.

138 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

identi"ed, it can be used to assess the relative variability of bidders' idiosyncraticcomponent and the common value.

It remains to discuss when A4 is satis"ed, which will provide additionalinformation on (C, D). A leading case when A4 holds is when the prior on thecommon value is inversely proportional to vc, i.e. f

v(v)J1/vc, c3R. In this case,

it can be shown (see Appendix) that

logE[vDp1"p, y

1"p]"logA

E[gc~11

Dg1"max

jE1gj]

E[gc1Dg

1"max

jE1gj] B#log p, (10)

so that D"1. When c"2 and a homogeneity assumption on the distribution ofsignals holds, which is satis"ed here by the multiplicative decomposition, Smiley(1979) has shown that the bidding strategy is proportional to the signal. UsingSmiley's result, Paarsch (1992) proposes a parametric estimation of the pure CVmodel. Assumption A4 is much more general and allows for nonlinear biddingstrategies.

Another case when A4 holds occurs with two bidders (n"2) when (v, g1, g

2)

is jointly log-normally distributed with parameters (kv, p2

v, kg , p2g ) and

exp(kg#p2g/2)"1 because of the normalization E(g)"1. It can be shown (seeAppendix) that

logE[vDp1"p, p

2"p]"

(kv#p2

v/2)p2g!2p2

vkg

p2g#2p2v

#

2p2v

p2g#2p2v

logp. (11)

Moreover, from (9) the distributions of c and e are log-normal with parameters(k

c, p2

c, p2e ) and ke"0, and we can identify all the structural parameters

(kv, p2

v, kg , p2g ) using

kv"k

c!

p2e8 A

p2ep2c

#2B, p2v"

p2c4 A

p2ep2c

#2B2, p2g"

p2e4 A

p2ep2c

#2B2, (12)

and kg"!p2g /2.10The preceding results are important for several reasons. First, for the CIPV

model, we have achieved full nonparametric identi"cation result of the underly-ing structural distributions. Second, for the pure CV model, we have proposedpartial nonparametric identi"cation results, which are the most general to date.Third, in both cases, we can assess the relative variability of the common

10Under the additive decomposition pi"v#g

i, A4 is replaced by the linearity in p of

E[vDp1"p, y

1"p]. By a similar argument used for establishing (10), it can be easily shown

that such an assumption A4@ is satis"ed with a #at prior on v in which caseE[vDp

1"p, y

1"p]"!E[g

1Dg

1"max

jE1gj]#p. Alternatively, when n"2, A4@ is satis"ed if

E[vDp1, p

2] is linear in p

1and p

2, in which case the posterior mean is a weighted average of the prior

mean and the average of the signals. For instance, this is the case when (v,g1,g

2) is multivariate

normal.

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 139

component and the idiosyncratic component in bidders' private information.Fourth, it is interesting to note that provided one knows G, one has neither tosolve the di!erential equation (2) nor to apply numerical integration in (3) so asto determine <(p, p). For knowledge of G( ) ) and hence of m( ) , G) determineseither the private value p in the CIPV model or E(vDp

1"p, y

1"p) in the pure

CV model for any given bid through (5) and, hence the distributions of thecommon and private components, respectively. Eqs. (5), (7) and (8) formthe basis upon which the nonparametric procedure proposed in the next sub-section rests.

2.3. Nonparametric structural estimation

We now propose a two-step nonparametric procedure for estimating thedensities h

c( ) ) and he ( ) ). Note that these determine uniquely the structural

densities hv( ) ) and hg ( ) ) in the CIPV model through (6) since

E(log g)"!logE(e) from the normalization E(g)"1. On the other hand, up toC and D which determine the location and common scale, the structuraldensities h

v( ) ) and hg ( ) ) in the pure CV model can be recovered from Proposi-

tion 3. Also, because we do not impose any parametric restriction on theunderlying densities, our nonparametric estimation procedure is equivalent toestimating them separately for each number of bidders. 11

The basic idea of our two-step estimation procedure is to use (5) followed byLemma 1. Speci"cally, if one knew G

B1 @b1( ) D ) ) and g

B1 @b1( ) D ) ), then one could use

(5) to recover <i,<(p

i, p

i) for bidder i, i"1,2, n, which is the private value

piin the CIPV model and the expectation E[vDp

i, y

i"p

i] in the pure CV model.

These can be used to estimate the joint characteristic function of (log<1, log<

2)

(say). Hence nonparametric estimates of densities of interest can be obtainedfrom Lemma 1 through (7)}(8). Hence, our estimation procedure is as follows:

Step 1: Construct a sample based on (5) using nonparametric estimates ofG

B1 @b1( ) D ) ) and g

B1 @b1( ) D ) ) from observed bids.

Step 2: Use the pseudo sample in logarithm constructed in Step 1 to estimatenonparametrically h

c( ) ) and he ( ) ) via their estimated characteristic

functions. These are then used to estimate hv( ) ) and hg ( ) ) for either

model.

To be more speci"c, let n be a given number of bidders. Let ¸ be the number ofauctions corresponding to the chosen n, and let l index the lth auction,

11That is, our procedure estimates hv@n

( ) Dn) and hg@n ( ) Dn) for each value of n. In practice, auctionedobjects may display some observed heterogeneity captured by some exogenous variables X. If this isthe case, then Steps 1 and 2 below need to be modi"ed accordingly through some smoothing over X.Though we exclude observed heterogeneity across auctions here and in Section 3, note that we doallow for unobserved heterogeneity across these auctions through the common component.

140 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

l"1,2,¸. In Step 1, using the observed bids Mbil; i"1,2, n; l"1,2,¸N,

we estimate nonparametrically the ratio GB1 @b1

( ) D ) )/gB1 @b1

( ) D ) ) byGK

B1 ,b1( ) , ) )/g(

B1 ,b1( ) , ) ), where

GKB1 ,b1

(B, b)"1

¸h1

L+l

1

n

n+i/1

1(Bil)B)K

GAb!b

il

hGB, (13)

g(B1,b1

(B, b)"1

¸h22

L+l/1

1

n

n+i/1

KgA

B!Bil

hg

,b!b

il

hgB, (14)

for any value (B, b) where hG

and hg

are some bandwidths, and KG

and Kg

arekernels. Using (5) we obtain estimates of the unobserved <

ilas

<Kil"mK (b

il),b

il#

GKB1,b1

(bil, b

il)

g(B1 ,b1

(bil, b

il). (15)

Step 1 is similar to the "rst step in the two-step nonparametric estimationprocedure of the APV model proposed in Li et al. (1999). As mentioned byGuerre et al. (1999), some trimming is necessary in order to correct for theboundary e!ects caused by the density estimate in the denominator of (15). Sucha trimming is presented in Section 3.2 A consequence of the trimming is that itreduces the number of estimates and hence the number of auctions that can beused in Step 2. Let ¸

Tbe the number of auctions after trimming.

We now turn to Step 2, which is composed of three substeps.

f Substep 1. Estimate the joint characteristic function of any two bidders'log<

ilamong n bidders by12

tK (u1, u

2)"

1

n(n!1)+

1xiEjxn

1

¸T

LT

+l/1

exp(iu1

log<Kil#iu

2log<K

jl). (16)

f Substep 2. Estimate hc( ) ) and he( ) ) by

hKc(x)"

1

2pPT

~T

e~*tx/Kc(t) dt (17)

hK e(y)"1

2pPT

~T

e~*ty/K e(t) dt (18)

for x3[log c6, log c6 ] and y3[log e

6, log e6 ], where ¹ is some smoothing para-

meter, and

/Kc(t)"expP

t

0

LtK (0, u2)/Lu

1tK (0, u

2)

du2, (19)

/K e(t)"tK (t,0)//Kc(t). (20)

12Note that, as required by the theoretical model, symmetry is imposed to improve e$ciency.

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 141

f Substep 3. Estimates of the structural densities are obtained in the CIPVmodel by

hKv(x)"hK

c[x#EK (log g)], hK g(y)"hK e[y!EK (log g)],

where EK (log g)"!log EK (e). In the pure CV model, they are obtained as

hKv(x)"DhK

c[D(x#(C/D)!logEK (e1@D))],

hK g(y)"DhK e[D(y#logEK (e1@D))],

given (C,D).

In Li and Vuong (1998), the uniform consistency of the nonparametricestimators proposed in Step 2 is established when the &indicators' <

ilare

observed. This is done by assuming that the densities of interest are eitherordinary or super-smooth through the tail behavior of their characteristicfunctions. Following Fan (1991), we have

Dexnition 1. The distribution of a random variable Z is ordinary smooth oforder b if its characteristic function /

Z(t) satis"es

d0DtD~b)D/

Z(t)D)d

1DtD~b

as tPR for some positive constants d0, d

1, b.

On the other hand, it is super-smooth of order b if /Z(t) satis"es

d0DtDb0 exp(!DtDb/c))D/

Z(t)D)d

1DtDb1 exp(!DtDb/c)

as tPR for some positive constants d0, d

1, b, c and constants b

0and b

1.

Speci"cally, we make the following assumption.

A5. The characteristic functions /v( ) ) and /g( ) ) are ordinary smooth with

b'1 or super-smooth.

Note that the characteristic functions /v( ) ) and /g( ) ) are necessarily both

integrable. In addition, Li and Vuong (1998) make the next assumption, whichwe maintain here.

A6. The supports of hv( ) ) and hg ( ) ) are bounded intervals of R.

Unlike in Li and Vuong (1998), the indicators<il

are unobserved. Instead, weuse their estimates <K

ilobtained in Step 1. Moreover, the pseudo values used in

Step 2 are trimmed to correct for boundary e!ects. Nonetheless, we can stillestablish the following result.

Theorem 1. Under A1}A6, hKc( ) ) and hK e( ) ) are uniformly consistent estimators for

hc( ) ) and he( ) ) on their respective supports, provided T diverges appropriately to

142 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

inxnity as ¸PR. Hence, if C and D are known, hKv( ) ) and hK g( ) ) are uniformly

consistent estimators for hv( ) ) and hg( ) ) in either the CIPV or pure CV model. 13

The proof of Theorem 1 is given in Appendix. It relies on an important lemma,which establishes the uniform convergence of the estimator (19) on [!¹, ¹].This is proved using the log-log law and von Mises di!erentials.

3. Application to the OCS wildcat auctions

In this section, we illustrate our estimation results on OCS wildcat auctionswith two bidders.14 A "rst subsection brie#y discusses the data. A secondsubsection deals with some practical issues for implementing our structuralestimation procedure. Our empirical "ndings within either the CIPV or the pureCV model are discussed in a third subsection.

3.1. Data

The U.S. federal government began auctioning its mineral rights on oil andgas on o!shore lands o! the coasts of Texas and Lousiana in the gulf of Mexicoin 1954. In this application, we focus on wildcat tracts sold through sales heldbetween 1954 and 1969. This gives us a total of 217 auctioned wildcat tracts withtwo bidders.

Before each sale, the government announces to oil companies that an area isavailable for exploration. This area is divided into a number of tracts, each ofwhich is usually a block of 5000 or 5760 acres. Firms are allowed to get limitedinformation about tracts using seismic surveys and o!-site drilling. However, nodrilling is allowed on each tract before the auction. Because bidders have equalaccess to the same information about the tract, they can be considered asidentical ex ante so the game is symmetric (see McAfee and Vincent, 1992 formore details).

13 In the CIPV model, Assumption A4 is automatically satis"ed with C and D known (and equalto zero and one, respectively) since log<(p, p)"log p. In the pure CV model, the assumption thatC and D are known is restrictive. If C and D are unknown, however, h

v( ) ) and hg ( ) ) are estimated

consistently up to location and common scale by hKc( ) ) and hK e( ) ), as mentioned earlier. The

appropriate divergence rate of ¹ is given in the appendix, Lemma A.1.14Recall that our procedure can provide estimates of h

v@n( ) Dn) and hg@n( ) Dn) for each value of

n"2, 3,2. Thus, in this case we estimate hv@n

( ) D2) and hg@n( ) D2) as auctions with two bidders provideus with the largest number of bids. Because the "rst step involves estimating a bivariate density (see(14)), the curse of dimensionality and data availability prevent us to consider n'3. If one is willingto accept the hypothesis that n is exogenous so that h

v@n( ) Dn) and hg@n( ) Dn) are independent of n, one

can pool all the data. Our previous work, however, indicates that this is not the case (see Li et al.,1999).

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 143

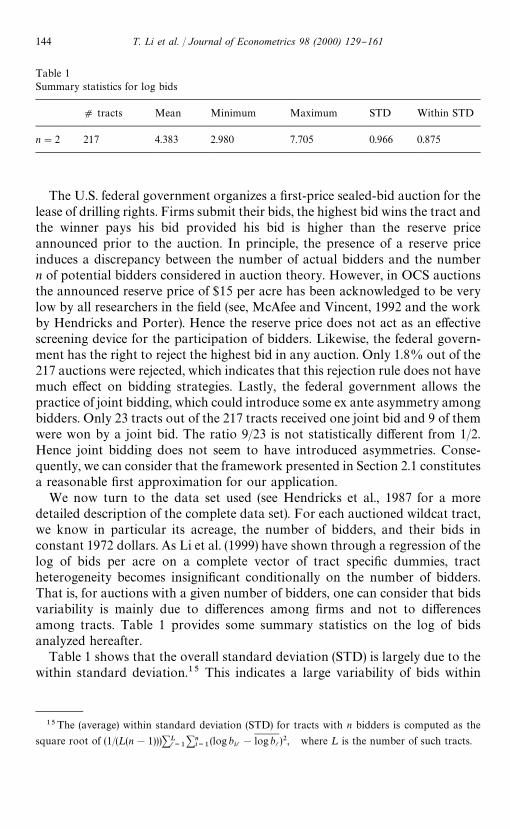

Table 1Summary statistics for log bids

d tracts Mean Minimum Maximum STD Within STD

n"2 217 4.383 2.980 7.705 0.966 0.875

The U.S. federal government organizes a "rst-price sealed-bid auction for thelease of drilling rights. Firms submit their bids, the highest bid wins the tract andthe winner pays his bid provided his bid is higher than the reserve priceannounced prior to the auction. In principle, the presence of a reserve priceinduces a discrepancy between the number of actual bidders and the numbern of potential bidders considered in auction theory. However, in OCS auctionsthe announced reserve price of $15 per acre has been acknowledged to be verylow by all researchers in the "eld (see, McAfee and Vincent, 1992 and the workby Hendricks and Porter). Hence the reserve price does not act as an e!ectivescreening device for the participation of bidders. Likewise, the federal govern-ment has the right to reject the highest bid in any auction. Only 1.8% out of the217 auctions were rejected, which indicates that this rejection rule does not havemuch e!ect on bidding strategies. Lastly, the federal government allows thepractice of joint bidding, which could introduce some ex ante asymmetry amongbidders. Only 23 tracts out of the 217 tracts received one joint bid and 9 of themwere won by a joint bid. The ratio 9/23 is not statistically di!erent from 1/2.Hence joint bidding does not seem to have introduced asymmetries. Conse-quently, we can consider that the framework presented in Section 2.1 constitutesa reasonable "rst approximation for our application.

We now turn to the data set used (see Hendricks et al., 1987 for a moredetailed description of the complete data set). For each auctioned wildcat tract,we know in particular its acreage, the number of bidders, and their bids inconstant 1972 dollars. As Li et al. (1999) have shown through a regression of thelog of bids per acre on a complete vector of tract speci"c dummies, tractheterogeneity becomes insigni"cant conditionally on the number of bidders.That is, for auctions with a given number of bidders, one can consider that bidsvariability is mainly due to di!erences among "rms and not to di!erencesamong tracts. Table 1 provides some summary statistics on the log of bidsanalyzed hereafter.

Table 1 shows that the overall standard deviation (STD) is largely due to thewithin standard deviation.15 This indicates a large variability of bids within

15The (average) within standard deviation (STD) for tracts with n bidders is computed as the

square root of (1/(¸(n!1)))+Ll/1+n

i/1(log b

il!log bl)2, where ¸ is the number of such tracts.

144 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

Fig. 1. Pairs (b1, b

2) with b

1*b

2.

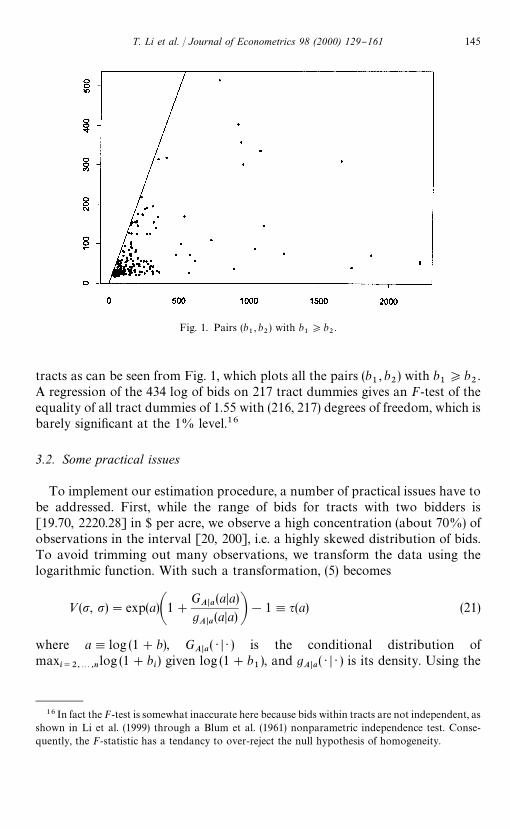

tracts as can be seen from Fig. 1, which plots all the pairs (b1, b

2) with b

1*b

2.

A regression of the 434 log of bids on 217 tract dummies gives an F-test of theequality of all tract dummies of 1.55 with (216, 217) degrees of freedom, which isbarely signi"cant at the 1% level.16

3.2. Some practical issues

To implement our estimation procedure, a number of practical issues have tobe addressed. First, while the range of bids for tracts with two bidders is[19.70, 2220.28] in $ per acre, we observe a high concentration (about 70%) ofobservations in the interval [20, 200], i.e. a highly skewed distribution of bids.To avoid trimming out many observations, we transform the data using thelogarithmic function. With such a transformation, (5) becomes

<(p, p)"exp(a)A1#G

A@a(aDa)

gA@a

(aDa) B!1,q(a) (21)

where a,log (1#b), GA@a

( ) D ) ) is the conditional distribution ofmax

i/2,2,nlog (1#b

i) given log (1#b

1), and g

A@a( ) D ) ) is its density. Using the

16 In fact the F-test is somewhat inaccurate here because bids within tracts are not independent, asshown in Li et al. (1999) through a Blum et al. (1961) nonparametric independence test. Conse-quently, the F-statistic has a tendancy to over-reject the null hypothesis of homogeneity.

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 145

trimming introduced in Guerre et al. (1999), the pseudo values <Kil

are de"nedas

<Kil"G

exp(ail)A1#

GKA,a

(ail, a

il)

g(A,a

(ail, a

il) B!1 if 2maxMh

G, h

gN)a

il

)a.!9

!2maxMhG, h

gN

#R otherwise

(22)

for i"1,2, n and l"1,2,¸. Here, a.!9

is the maximum value of all log-bids,i.e. a

.!9"max

i,lail. This trimming is necessary in view of boundary e!ects in

kernel estimation.17 As in Section 2.3, the nonparametric estimates GKA,a

( ) , ) )and g(

A,a( ) , ) ) are obtained from (13) and (14), with the exception that all bids are

now in log (1#b). The second step of our estimation procedure only uses thepseudo values that are "nite as de"ned in (22). We now discuss the pratical issuesspeci"c to the "rst and second steps.

In the "rst step, we need to address the choice of the kernel functions KG

andK

gand their corresponding bandwidths h

Gand h

g. Though the choice of kernels

does not have much e!ect in practice, we choose a kernel with compact supportthat is continuously di!erentiable on its support including the boundaries so asto satisfy the assumptions in Guerre et al. (1999). Numerous kernel functionssatisfy these properties (see Hardle, 1991). This is the case for the triweight kernelde"ned as

K(u)"35

32(1!u2)31(DuD)1). (23)

Thus Kg

is de"ned as the product of two univariate triweight kernels.In contrast, the choice of the bandwidths requires more attention. From the

rates given in Li et al. (1999), we use bandwidths of the form hG"c

G(n¸)~1@5

and hg"c

g(n¸)~1@6. Note that these rates correspond to the usual ones so that

cG

and cg

can be obtained by the so-called rule of thumb. Speci"cally, we usehG"2.978]1.06p(

a(n¸)~1@5 and h

g"2.978]1.06p(

a(n¸)~1@6, where p(

ais the

standard deviation of the logarithm of (1#bids), and the factor 2.978 followsfrom the use of the triweight kernel instead of the Gaussian kernel (see Hardle,1991). Thus h

Gand h

gare equal to 0.9049 and 1.1079, respectively. After

performing the "rst step estimation and the trimming on the pseudo values <Kil,

we "nd that the trimmed values have a mean equal to $253.41 per acre, while the

17We assume that p6"0. Hence, b

M"0 in view of (3) and A4. The transformation log (1# ) ) then

ensures that a6"0 and that the support [a

6,a6 ] is compact as soon as bM (R, i.e. as soon as p6 (R

because bM "s(p6 ). Thus we do not need to estimate the lower bound a6. Moreover, despite the log

transformation, observations remain relatively sparse in the right tail. Thus, it is more cautious touse a larger trimming (such as twice the bandwidth as in (22)) than the one used in the asymptotictheory of Guerre et al. (1999).

146 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

minimum and maximum are 19.73 and 1181.38, respectively. After trimming,174 auctioned tracts remain out of 217.

In the second step, some new practical problems are encountered. First, theuse of empirical characteristic functions for estimating their correspondingdensities typically produces many oscillations because of the large range ofvalues estimated in Step 1. To mitigate this problem, we divide the logarithm ofall pseudo values<K

ilby 7 so as to get an interval close to [0, 1]. Second, as noted

by Diggle and Hall (1993), the estimators (17) and (18), which are obtained bytruncated inverse Fourier transformation, may have some sharp #uctuatingtails. Such an unattractive feature can be alleviated by adding a damping factorto the integrals in (17) and (18). Following Diggle and Hall (1993), we introducea damping factor de"ned as

d(t)"G1!DtD/¹ if DtD)¹,

0 otherwise.(24)

Thus, estimators (17)}(18) are generalized to

hKc(x)"

1

2pPT

~T

d(t)e~*tx/Kc(t) dt, (25)

hK e (y)"1

2pPT

~T

d(t)e~*ty/K e(t) dt. (26)

In practice, this damping factor will &smooth' the tails of our density estimators.Third, though the smoothing parameter ¹ can be chosen to diverge slowly as

¸PR so as to ensure the uniform consistency of our estimators, the actualchoice of ¹ in "nite samples has not yet been addressed in the literature. Indeed,¹ plays here the role of a smoothing parameter, as large (small) ¹ will produceundersmoothing (oversmoothing) of the density estimate. In our case, ¹ ischosen through some empirical or data-driven criterion. As mentioned infootnote 8, we can obtain estimates for all moments of log c and log e from themoments of (log<

1, log<

2). Hence, using the trimmed pseudo sample of values

obtained in Step 1, we can obtain estimates of the means and variances of log cand log e as k(

c"4.937, k( e,0, p( 2

c"0.00222 and p( 2e"0.02195. These two

estimates can then be used to choose a value of ¹. Speci"cally, we try di!erent¹'s and obtain corresponding estimates of h

c( ) ) and he( ) ) through (25)}(26).

From each estimated density, we compute the corresponding means and vari-ances k8

c, k8 e , p8 2

cand p8 2e , respectively. This gives the goodness-of-"t criterion

Dp8 2c!p( 2

cD#(k8

c!k(

c)2 for c, and similarly for e. The value of ¹ we choose

minimizes the sum of these errors in percentage of p( 2c

and p( 2e . This gives ¹ equalto 50.

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 147

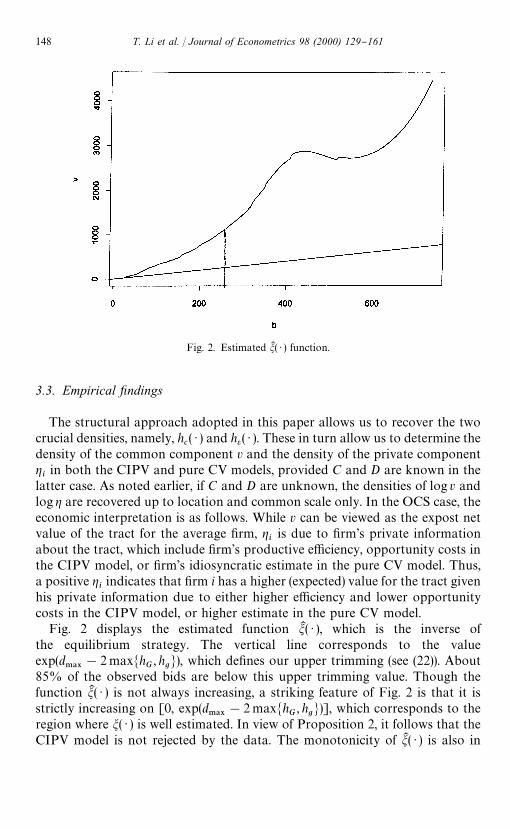

Fig. 2. Estimated mK ( ) ) function.

3.3. Empirical xndings

The structural approach adopted in this paper allows us to recover the twocrucial densities, namely, h

c( ) ) and he ( ) ). These in turn allow us to determine the

density of the common component v and the density of the private componentgiin both the CIPV and pure CV models, provided C and D are known in the

latter case. As noted earlier, if C and D are unknown, the densities of log v andlog g are recovered up to location and common scale only. In the OCS case, theeconomic interpretation is as follows. While v can be viewed as the expost netvalue of the tract for the average "rm, g

iis due to "rm's private information

about the tract, which include "rm's productive e$ciency, opportunity costs inthe CIPV model, or "rm's idiosyncratic estimate in the pure CV model. Thus,a positive g

iindicates that "rm i has a higher (expected) value for the tract given

his private information due to either higher e$ciency and lower opportunitycosts in the CIPV model, or higher estimate in the pure CV model.

Fig. 2 displays the estimated function mK ( ) ), which is the inverse ofthe equilibrium strategy. The vertical line corresponds to the valueexp(d

.!9!2 maxMh

G, h

gN), which de"nes our upper trimming (see (22)). About

85% of the observed bids are below this upper trimming value. Though thefunction mK ( ) ) is not always increasing, a striking feature of Fig. 2 is that it isstrictly increasing on [0, exp(d

.!9!2 maxMh

G, h

gN)], which corresponds to the

region where m( ) ) is well estimated. In view of Proposition 2, it follows that theCIPV model is not rejected by the data. The monotonicity of mK ( ) ) is also in

148 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

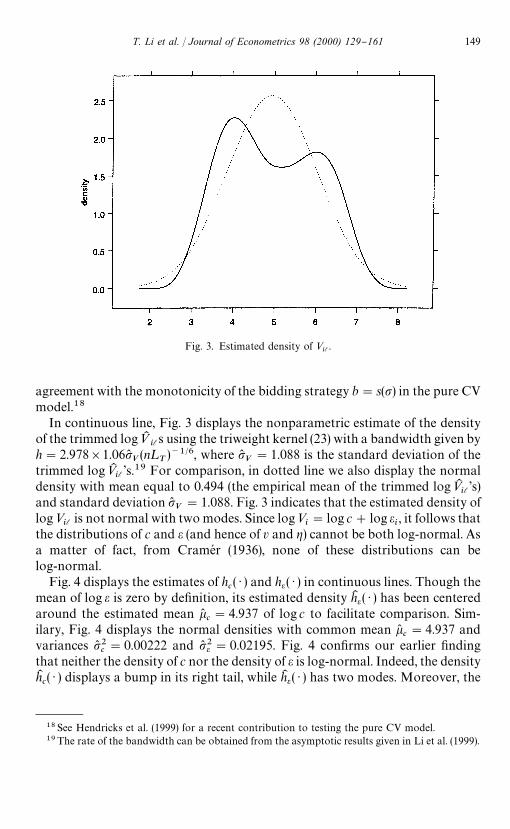

Fig. 3. Estimated density of <il.

agreement with the monotonicity of the bidding strategy b"s(p) in the pure CVmodel.18

In continuous line, Fig. 3 displays the nonparametric estimate of the densityof the trimmed log<K

ils using the triweight kernel (23) with a bandwidth given by

h"2.978]1.06p(V(n¸

T)~1@6, where p(

V"1.088 is the standard deviation of the

trimmed log<Kil's.19 For comparison, in dotted line we also display the normal

density with mean equal to 0.494 (the empirical mean of the trimmed log<Kil's)

and standard deviation p(V"1.088. Fig. 3 indicates that the estimated density of

log<il

is not normal with two modes. Since log<i"log c#log e

i, it follows that

the distributions of c and e (and hence of v and g) cannot be both log-normal. Asa matter of fact, from CrameH r (1936), none of these distributions can belog-normal.

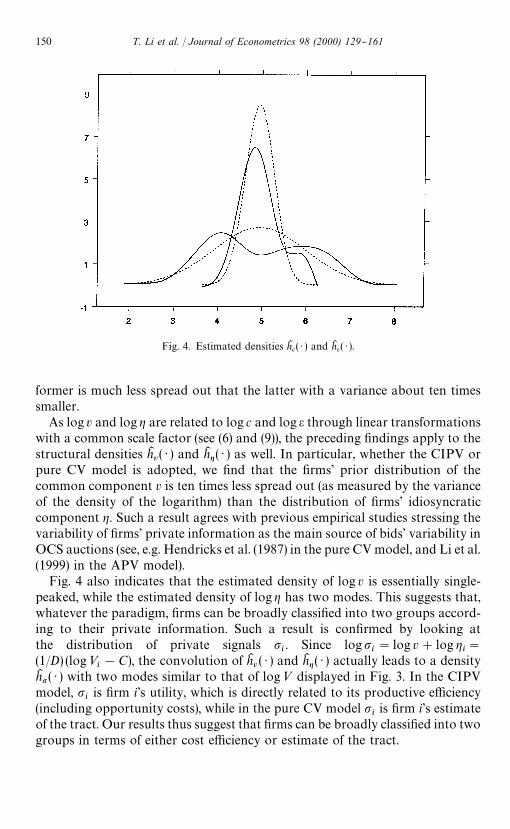

Fig. 4 displays the estimates of hc( ) ) and he ( ) ) in continuous lines. Though the

mean of log e is zero by de"nition, its estimated density hK e ( ) ) has been centeredaround the estimated mean k(

c"4.937 of log c to facilitate comparison. Sim-

ilary, Fig. 4 displays the normal densities with common mean k(c"4.937 and

variances p( 2c"0.00222 and p( 2e"0.02195. Fig. 4 con"rms our earlier "nding

that neither the density of c nor the density of e is log-normal. Indeed, the densityhKc( ) ) displays a bump in its right tail, while hK e( ) ) has two modes. Moreover, the

18See Hendricks et al. (1999) for a recent contribution to testing the pure CV model.19The rate of the bandwidth can be obtained from the asymptotic results given in Li et al. (1999).

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 149

Fig. 4. Estimated densities hKc( ) ) and hK e( ) ).

former is much less spread out that the latter with a variance about ten timessmaller.

As log v and log g are related to log c and log e through linear transformationswith a common scale factor (see (6) and (9)), the preceding "ndings apply to thestructural densities hK

v( ) ) and hK g( ) ) as well. In particular, whether the CIPV or

pure CV model is adopted, we "nd that the "rms' prior distribution of thecommon component v is ten times less spread out (as measured by the varianceof the density of the logarithm) than the distribution of "rms' idiosyncraticcomponent g. Such a result agrees with previous empirical studies stressing thevariability of "rms' private information as the main source of bids' variability inOCS auctions (see, e.g. Hendricks et al. (1987) in the pure CV model, and Li et al.(1999) in the APV model).

Fig. 4 also indicates that the estimated density of log v is essentially single-peaked, while the estimated density of log g has two modes. This suggests that,whatever the paradigm, "rms can be broadly classi"ed into two groups accord-ing to their private information. Such a result is con"rmed by looking atthe distribution of private signals p

i. Since logp

i"log v#log g

i"

(1/D) (log<i!C), the convolution of hK

v( ) ) and hK g( ) ) actually leads to a density

hK p( ) ) with two modes similar to that of log< displayed in Fig. 3. In the CIPVmodel, p

iis "rm i's utility, which is directly related to its productive e$ciency

(including opportunity costs), while in the pure CV model piis "rm i's estimate

of the tract. Our results thus suggest that "rms can be broadly classi"ed into twogroups in terms of either cost e$ciency or estimate of the tract.

150 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

Without information about the constants C and D, nothing further can besaid in the pure CV model. On the other hand, C"0 and D"1 in the CIPVmodel so that the densities of v and g are completely identi"ed as indicated inProposition 2. Speci"cally, from (6) the densities of log v and log g are shiftedversions of the densities of log c and log e, respectively. An estimate of E(log g)can be obtained from E(log g)"!logE(e) with E(e) computed numericallyfrom the density estimate hK e( ) ). We obtain EK (log g)"!1.816. In particular, we"nd that the estimated mean of log v is k(

v"6.753. The variances of log v and

log g are equal to the variances of log c and log e, and thus their estimates arep( 2v"0.00222 and p( 2g"0.02195, respectively. Hence, as noted earlier, the density

of the "rm's idiosyncratic component gi

is much more spread out than thedensity of the common component v.

It is interesting to assess the estimated densities hKv( ) ) and hK g( ) ) in the

framework of the CIPV model. As "rm i's private value pican be decomposed as

logpi"log v#log g

iwith v and g

iindependent, the variance of logp

iis equal

to the sum of the variances of log v and log g. The ratio Var(v)/Var(p) gives thepercentage of variability of logp

iexplained by the variability of log v. This ratio

is 9.16%, which means that only 9.16% of the variability of private values (inlogarithm) is explained by the variability of the common component v. Alterna-tively, we can conclude that the variability of private values can be attributed for90.84% to the variability of "rms' speci"c factors. The ratio 9.16% is also thelinear correlation coe$cient between any two private values in logarithm sincelogp

i"log v#log g

i. Hence linear correlation is low though a$liation is not

negligeable, as shown by Li et al. (1999) through a Blum et al. (1961) non-parametric test of independence.

4. Conclusion

In this paper, we consider the CIPI model, which is derived from the generala$liated value model by assuming that bidders' private information are condi-tionally independent given some unknown common component. The CIPImodel is interesting as it nests two important polar cases, which are the CIPVmodel and the pure CV model. We show that the CIPI model is unidenti"edfrom observed bids without additional restrictions. This leads us to assume thateach bidder's private information p

ican be decomposed as the product of

a common component v and a bidder's idiosyncratic component gi

that aremutually independent.

Under this additional assumption and some regularity conditions, we showthat the CIPV model is fully identi"ed. We also establish that under log-linearityof E[vDp

1"p, y

1"p] in logp, the pure CV model is essentially identi"ed up to

location and scale. We then propose a computationally convenient two-stepnonparametric procedure for estimating the underlying densities of the common

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 151

component v and the idiosyncratic component gi. Our estimation procedure

uses kernel estimators in a "rst step and empirical characteristic functions ina second step. Consistency of the resulting estimators is established by extendingLi and Vuong (1998) results on the nonparametric identi"cation and estimationof the measurement error problem with multiple indicators to the case where theindicators are estimated.

We illustrate our method by analyzing OCS wildcat auctions. Whether theCIPV model or the pure CV model is adopted, our empirical "ndings indicatethat "rms' private information play a major role in explaining the variability ofobserved bids. In particular, we "nd that the "rms' prior distribution of thecommon component v is much less spread out than the distribution of "rms'idiosyncratic component g. We also "nd that, whatever the paradigm, thedistribution of "rms's private information is not normal with two modes. Thissuggests that "rms can be broadly classi"ed into two groups according to eithercost e$ciencies and opportunity costs in the CIPV model or estimates of thetract in the pure CV model.

Lastly, our paper has provided the "rst step towards the nonparametricidenti"cation and estimation of the pure CV model. An important line ofresearch is to expand these results through other restrictions or/and underadditional information. A more general goal will be to develop a completetheory of identi"cation and estimation of the general AV models. This wouldallow us to discriminate among competing models such as the CIPV versus thepure CV model from auction data.

Acknowledgements

The authors are grateful to K. Hendricks and R. Porter for providing the dataanalyzed in this paper. We thank J. Hahn, P. Haile, A. Pakes, four referees andthe editor for helpful comments as well as M. David and L. Deleris foroutstanding research assistance. Preliminary versions of this paper were pre-sented at the North American Meetings of the Econometric Society, Januaryand June 1998, and at Stanford, UC Riverside, and USC econometric seminars.Financial support was provided by the National Science Foundation underGrant SBR-9631212.

Appendix

Proof of Proposition 1. Let M be an arbitrary CIPI model de"ned by thestructure [;( ) ), F

v( ) ), Fp@v ( ) D ) )] for the utility function, the common compon-

ent v, and signals pi, i"1,2, n. De"ne a new utility function ;I ( ) ), a new

common component v8 , and new signals p8i, i"1,2, n such that

152 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

;I (p8i, v)"p8

i, v8 "v, and p8

i"E[;(v, p

i) Dp

i, y

i"p

i],j(p

i), which is strictly

increasing in pi. Note that the p8

i's are conditionally independent given v8 . Hence

the new model MI with structure [;I ( ) ), FIv8( ) ), FI p8 @v8 ( ) D ) )] for the utility function,

the common component v8 , and signals p8i, i"1,2, n is a CIPV model. More-

over, it can be veri"ed that

fIy8 1 @p8 1 ( ) D ) )

FIy8 1 @p8 1 ( ) D ) )

"

1

j@[j~1( ) )]

fy1 @p1

[j~1( ) )Dj~1( ) )]

Fy1 @p1

[j~1( ) )Dj~1( ) )]. (A.1)

Therefore, comparing the di!erential equations (2) for the CIPI model M andthe CIPV model MI subject to their respective boundary conditions, and using<(p, p)"j(p), it follows that the equilibrium strategies in M and MI are relatedby s8 ( ) )"s[j~1( ) )]. Hence bI "s8 (p8 )"s(p). Thus the equilibium bid distributionin M is equal to that in MI , i.e. M is observationally equivalent to MI . h

Proof of Lemma 1. The characteristic functions /c( ) ) and /e ( ) ) of log c and log e

are related to those of log v and log g by

/c(t)"/

v(t)e*tE*-0' g+, /e (t)"/g(t)e~*tE*-0' g+. (A.2)

Hence A3 implies that /c( ) ) and /e ( ) ) are also nonvanishing everywhere. Thus,

given A1}A3, log c and log e satisfy the assumptions of Lemma 2.1 in Li andVuong (1998). The desired result follows. h

Proof of Proposition 2. The identi"cation of [Fv( ) ),Fg ( ) )] in the CIPV model

follows from (i) the identi"cation of the joint distribution of (p1,2,p

n) from

observed bids because a CIPV model is an APV model, which is identi"ed by Liet al. (1999, Proposition 2.1), (ii) the identi"cation of the distributions of log cand log e from the joint distribution of (logp

1,2,logp

n) by Lemma 1, and (iii)

the equalities log v"log c!E[log g] and log g"log e#E[logg], whereE[logg]"!logE[e] from the normalization E[g]"1.

The proof of the second part is similar to the second part of the proof ofProposition 2.1 in Li et al. (1999) with the exception that the utilities p

iare now

conditionally independent. Note that variables that are conditionally indepen-dent given some other variable are necessarily a$liated. h

Proof of Proposition 3. The proof is similar to the "rst part of the proof ofProposition 2. Speci"cally, in (i) the joint distribution of observed bids nowdetermines uniquely the joint distribution of (<(p

1, p

1),2,<(p

n, p

n)) from (5),

(ii) stays the same with pireplaced by <(p

i, p

i) and (A.2) replaced by

/c(t)"/

v(Dt)e*t*C`DE(-0' g)+, /e (t)"/g(Dt)e~itDE(-0' g), (A.3)

while (iii) now uses (9). In particular, solving (9) for log v and log g, and usingE(log g)"!logE(e1@D) from the normalization E(g)"1 give the desired re-sult. h

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 153

Proof of Eq. (10). Under the multiplicative decomposition, we have p1"vg

1and y

1"vmax

jE1gj. Hence, using the Jacobian of the transformation, the joint

density of (v, p1, y

1) is

f (v, p1, y

1)"[(n!1)/v2] fg (p1

/v) fg(y1/v)Fn~2g (y

1/v) f

v(v).

Hence

E[vDp1"p, y

1"p]"

:=0(1/v) f 2g (p/v)Fn~2g (p/v) f

v(v) dv

:=0

(1/v2) f 2g (p/v)Fn~2g (p/v) fv(v) dv

. (A.4)

Suppose now that fv(v)J1/vc. Thus we obtain

E[vDp1"p, y

1"p]"

:=0

(1/vc`1) f 2g (p/v)Fn~2g (p/v) fv(v) dv

:=0

(1/vc`2) f 2g (p/v)Fn~2g (p/v) fv(v) dv

"p:=0uc~1 f 2g (u)Fn~2g (u) du

:=0uc f 2g (u)Fn~2g (u) du

,

where the second equality follows from the change of variable u"p/v. Thedesired Eq. (10) follows from interpreting the proportionality factor of p andtaking the logarithm. h

Proof of Eq. (11). Given A1}A2, the multiplicative decomposition, and thelog-normality of (v, g

1, g

2), we have

Alog v

logp1

logp2B&N AA

kv

kv#kg

kv#kgB; A

p2v

p2v

p2v

* p2v#p2g p2

v

* * p2v#p2gBB.

Hence, vDp1, p

2&LN(k

V, p2

V), where

kV"k

v#(p2

v, p2

v)R~1A

logp1!k

v!kg

logp1!k

v!kgB

;

p2V"p2

vA1!(p2v, p2

v)R~1A

1

1BB,with R being the covariance matrix of (logp

1, logp

2). Using logE[<Dp

1,

p2]"k

V#p2

V/2 and p

1"p

2"p gives (11) after some elementary algebra. h

Proof of Eq. (12). From (9) and (11), we have p2c"D2p2

vand p2e"D2p2g with

D"2p2v/(p2g#2p2

v). Elementary algebra gives (12), which expresses p2

vand p2g as

function of p2c

and p2e . Using (9) and (11) again, we havekc"k

v#[p2

vp2g/2(p2g#2p2

v)]. By replacing p2g and p2

vby their expressions in

154 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

(12), some algebra gives kv

as a function of log c, p2c

and p2e . Lastly,kv#p2g/2"0 because of the normalization E[g]"1. h

Proof of Theorem 1. We need to prove the "rst part only as the second part isstraightforward. We note that

log<il"log cl#log e

il, i"1,2, n, l"1,2,¸,

where<il"p

ilin the CIPV model and<

il"E[vl Dpil

, yil"p

il] in the pure CV

model. If the <il's were observed, one would have a measurement model with

n indicators. Moreover, given A1}A6, log c and log e satisfy all the assumptionsin Li and Vuong (1998) in view of (6), (9), (A.2) and (A.3). Hence Theorem1 would directly follow from Li and Vuong (1998) results.

The <il's are, however, unobserved but they can be estimated by <K

ils from

(15). Now, in Li and Vuong (1998), the crucial result upon which the uniformconvergence of the density estimators (17) and (18) is established is given byLemma 4.1 in that paper. Here, we prove the following Lemma A.1 which playsan analogous role. The di!erence between Lemma A.1 and Lemma 4.1 in Li andVuong (1998) is that here we deal with indicators that are (trimmed) estimates<K

ilwhile Li and Vuong (1998) deal with indicators <

ilthat are observed. Once

Lemma A.1 is established, Theorem 1 can be proved by following the proofs ofTheorems 3.1}3.4 in Li and Vuong (1998).

Hereafter, we let vil,log<

iland v(

il,log<K

il. Let d

L"

supi,l

1(v(ilO#R)Dv(

il!v

ilD and c

LT"supDF(2)

LT!F(2)D, where F(2) is the joint

distribution of any two bidders' vil

and F(2)LT

is its (infeasible) empirical counter-part obtained by using the true but unobserved v

ilof any two bidders. Note that

dL

converges to zero from Li et al. (1999, Proposition A2) as ¸PR, whilecLT

converges to zero from the log}log Law (see Ser#ing, 1980) as ¸TPR.

Lemma A.1. Assume A1}A6. Let eL,maxMc

LT, d

LN.

(i) Suppose Dt(0, t)D*d1DtD~b as tPR for some positive constants d

1and b.

Then

supt|*~T,T+

D/Kc(t)!/

c(t)D"e1~a

L,

where 0(a(1 and ¹"e~a@(2(1`b))L

.(ii) Suppose Dt(0, t)D*d

0DtDb0 exp(!DtDb/c) as tPR for some positive constants

d0, b, c and constant b

0. Then

supt|*~T,T+

D/Kc(t)!/

c(t)D"e1~a

L Alog1

eLB

2(1~b0)@b,

where 0(a(1, and ¹"[!(ac/2)log eL]1@b.

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 155

Proof. From (16) we only need to prove that this lemma holds when

tK (u1, u

2)"

1

¸T

LT

+l/1

exp(iu1v(1l#iu

2v(2l

), (A.5)

where v(1l

and v(2l

, l"1,2,¸T

are estimated vil

for any two bidders, say bidder1 and bidder 2. Thus the result for tK ( ) , ) ) de"ned by (16) can be readily obtainedas it is an average of (A.5) among n bidders imposing symmetry. Hereafter, werede"ne (19) in terms of tK ( ) , ) ) given by (A.5) instead of (16).

Using (7) and (19), a Taylor series expansion gives

/Kc(t)!/

c(t)"

=+p/1

/c(t)

p! APt

0

LtK (0, u2)/Lu

1tK (0, u

2)

du2!P

t

0

Lt(0, u2)/Lu

1t(0, u

2)

du2B

p.

Let DL(t) denote the term in parentheses. The fact that D/

c(t)D)1 gives

D/Kc(t)!/

c(t)D)

=+p/1

DDL(t)Dp. (A.6)

Using von Mises di!erentials (see Ser#ing, 1980), we have

DL(t)"

=+k/1

1

k!dk¹(t; tK !t), (A.7)

where

dk¹(t; tK !t),

dk

djkPt

0

L[t(0, u2)#j(tK (0, u

2)!t(0, u

2))]/Lu

1t(0, u

2)#j(tK (0, u

2)!t(0, u

2))

du2 Kj/0

.

Take k"1. Direct computation then yields

d

djPt

0

L[t(0,u2)#j(tK (0, u

2)!t(0, u

2))]/Lu

1t(0, u

2)#j(tK (0, u

2)!t(0, u

2)

du2

"Pt

0

A(u2)

[t(0,u2)#j(tK (0, u

2)!t(0, u

2))]2

du2, (A.8)

where

A(u2)"

L[tK (0, u2)!t(0, u

2)]

Lu1

t(0, u2)!

Lt(0, u2)

Lu1

[tK (0, u2)!t(0, u

2)].

Note that A(u2) does not depend on j. Moreover, the derivative with respect to

j of the term in brackets in the denominator of (A.8) is

B(u2)"tK (0, u

2)!t(0, u

2),

156 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

which is independent of j. Thus successive di!erentiation of (A.8) gives for anyk*1

dk¹(t; tK !t)"(!1)k~1k!P

t

0

A(u2)B(u

2)k~1

t(0, u2)k`1

du2. (A.9)

Now let us consider A(u2) and B(u

2), respectively. De"ne

tI (u1, u

2)"

1

¸T

LT

+l/1

exp(iu1v1l#iu

2v2l

), (A.10)

where v1l

and v2l

, l"1,2,¸T, are true but unobserved v

ilfor any two

bidders, say bidder 1 and bidder 2. Thus

B(u2)"tK (0, u

2)!tI (0, u

2)#tI (0, u

2)!t(0, u

2)

"

1

¸T

LT

+l/1

(e*u2v( 2l!e*u2v2l)#Pe*u2v2 d(F(2)LT

!F(2)), (A.11)

where F(2) is the joint distribution of v1

and v2

while F(2)LT

is its (infeasible)empirical counterpart obtained by using (v

1l, v

2l), l"1,2,¸

T.

Now for the "rst summand of the last equality, we have

K1

¸T

LT

+l/1

(e*u2v( 2l!e*u2v2l )K)1

¸T

LT

+l/1

De*u2v( 2l!e*u2v2l D

)

1

¸T

LT

+l/1

=+q/1

uq2Dv(2l!v

2lDq

q!

)

=+q/1

uq2dqL

q!.

On the other hand, in view of A6, (6) and (9), DvilD)M, where M'0. Let

cLT

"supDF(2)LT

!F(2)D. We use the inequality

K PMf (y1, y

2) dg(y

1, y

2)K

)K PMg(y1, y

2)L2f (y

1, y

2)

Ly1Ly

2

dy1

dy2 K#8M sup

(y1 ,y2)|MDg(y

1, y

2)D

]A sup(y1 ,y2 )|M

D f (y1, y

2)D# sup

(y1 ,y2)|MKLf (y

1, y

2)

Ly1

K# sup(y1 ,y2)|M

KLf (y

1, y

2)

Ly2

KB,where M"[!M,#M]][!M,#M] (see CsoK rgoK , 1980). Applying thisinequality to the second summand of (A.11) gives

DtI (0, u2)!t(0, u

2)D"K Pe*u2vd(F(2)

LT!F(2))K)8M(1#u

2)c

LT. (A.12)

T. Li et al. / Journal of Econometrics 98 (2000) 129}161 157

Hence, we obtain

DB(u2)D)

=+q/1

uq2dqL

q!#8M(1#u

2)C

LT,b

L(u

2). (A.13)

For A(u2), we have

LtK (0, u2)

Lu1

!

Lt(0, u2)

Lu1

"

LtK (0, u2)

Lu1

!

LtI (0, u2)

Lu1

#

LtI (0, u2)

Lu1

!

Lt(0, u2)

Lu1

"

1

¸T

LT

+l/1

(iv(1l

e*u2v( 2l!iv1l

e*u2v2l)#Piv1e*u2v2 d(F(2)LT

!F(2)). (A.14)

Similarly to B(u2), we can show that the "rst summand of the last equality

satis"es

K1

¸T

LT

+l/1

(iv(1l

e*u2v( 2l!iv1l

e*u2v2l )K"K

1

¸T

LT

+l/1

(i(v(1l!v

il)e*u2v( 2l#iv

1l(e*u2v( 2l!e*u2v2l )K

)

1

¸T

LT

+l/1AdL#M

=+q/1

uq2dqL

q! B"d

L#M

=+q/1

uq2dqL

q!.

Following (A.8) the second summand of (A.11) satis"es

K Piv1e*u2v2 d(F(2)LT

!F(2))K)4M2u2cLT

#8M(M#1#Mu2)c

LT.

Therefore, from the de"nition of A(u2), (A.13), and DLt(0, u

2)/Lu

1D(M, we

obtain

DA(u2)D)d

L#2M

=+q/1

uq2dqL

q!#20M2(1#u

2)c

LT

#8McLT

,aL(u

2). (A.15)

Hence, from (A.7) and (A.9) we obtain

DDL(t)D)

=+k/1

Pt

0

aL(u

2)b

L(u

2)k~1

Dt(0, u2)Dk`1

du2. (A.16)

158 T. Li et al. / Journal of Econometrics 98 (2000) 129}161

(i) Under the assumption that Dt(0, t)D*d1DtD~b as tPR, then there exists

a'0 such that Dt(0, t)D*d1DtD~b for DtD*a. Let b"min

@t@xaDt(0, t)D. Choosing

¹ large enough such that ¹'a, we have Dt(0, t)D*d1DtD~b*d

1D¹D~b for

t3[!¹,¹]C[!a, a]. Also for ¹ large enough, then for t3[!a, a] we haveDt(0, t)D*b*d

1D¹D~b. Therefore, for t3[!¹,¹] where ¹ is large enough, we

obtain

Dt(0, t)D*d1D¹D~b.

On the other hand, by the log}log law (see Chung, 1949; Ser#ing, 1980),

cLT

,sup DF(2)LT

!F(2)D"OA¸

Tlog log¸

TB

~1@2. (A.17)

Let eL"maxMc

LT, d

LN. Then we may choose ¹ appropriately such that

¹(1`b)eL(1 as ¸PR. Hence for t3[!¹,¹] where ¹ is large enough, (A.16)

gives after some algebra

DDL(t)D)

=+k/1

PT

0

Ak(¹k#¹k~1n

)ekL

¹~b(k`1)du

2

"

A¹2(1`b)eL

1!A¹1`beL

#

A¹1`2beL

1!A¹1`beL

,

for some constant A. Let ¹"e~a@(2(1`b))L

where 0(a(1, then for t3[!¹,¹],

DDL(t)D"O(e1~a

L).

It follows that for ¸ large enough and for t3[!¹,¹], DDL(t)D is smaller than

one. Hence, from (A.6)

supt|*~T,T+

D/Kc(t)!/

c(t)D)

supt|*~T,T+

DDL(t)D

1!supt|*~T,T+

DDL(t)D

"OA supt|*~T,T+

DDL(t)DB.

The desired result follows.(ii) Now assume that Dt(0, t)D*d

0DtDb0 exp(!DtDb/c). By using the same argu-

ment as in (i), we can show that for DtD)¹, where ¹ is large enough,

Dt(0, t)D*d0¹b0 exp(!¹b/c).

Therefore, (A.16) gives after some algebra for DtD)¹,

DDL(t)D)

=+k/1