Condemning Conservation Easements Protecting the Public Interest & Investment in Conservation Nancy A. McLaughlin Robert W. Swenson Professor of Law University of Utah College of Law www.law.utah.edu [email protected] A’s 55 th Annual International Education Confe June 28 - July 1, 2009 ©2009 by Nancy A. McLaughlin. All rights reserved

Condemning Conservation Easements Protecting the Public Interest & Investment in Conservation Nancy A. McLaughlin Robert W. Swenson Professor of Law University.

Jan 02, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Condemning Conservation Easements Protecting the Public Interest & Investment in Conservation

Nancy A. McLaughlin Robert W. Swenson Professor of Law

University of Utah College of Lawwww.law.utah.edu

IRWA’s 55th Annual International Education ConferenceJune 28 - July 1, 2009

©2009 by Nancy A. McLaughlin. All rights reserved

Who should get what when land encumbered by a conservation easement

is condemned in whole or in part?

Conservation Easement-Encumbered Land

U.S. Constitution

Takings Clause of 5th Amendment

“…nor shall private property be taken for public use without just compensation”

When land encumbered by a conservation easement is taken…

1) Does the conservation easement constitute compensable “property”?

2) How should the conservation easement be valued for purposes of compensating its holder?

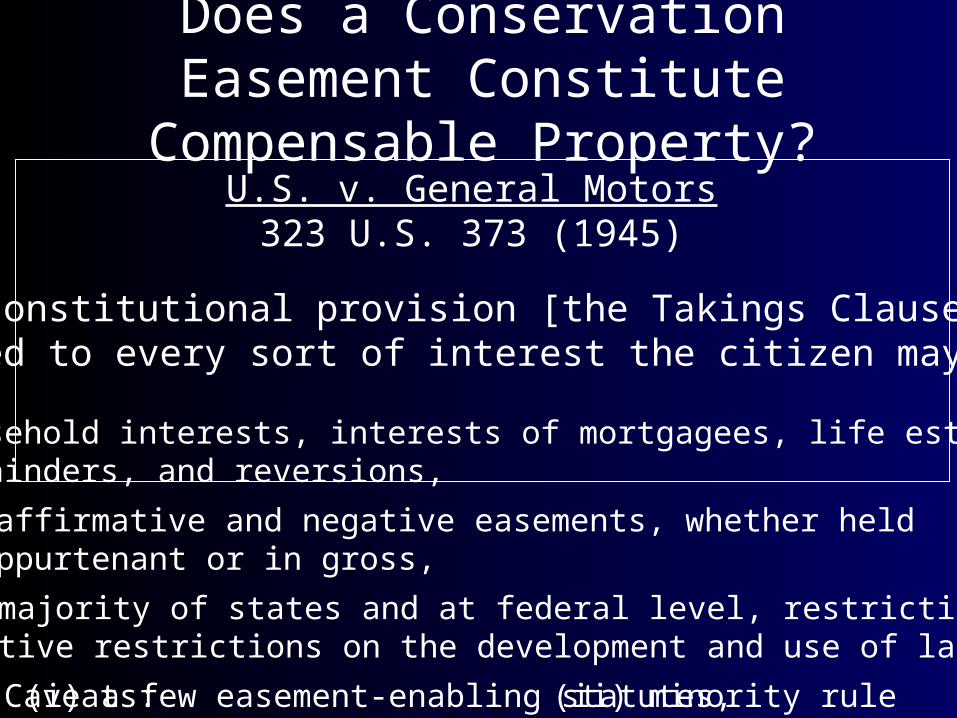

Does a Conservation Easement Constitute Compensable Property?

U.S. v. General Motors 323 U.S. 373 (1945)

“The constitutional provision [the Takings Clause] is addressed to every sort of interest the citizen may possess”

- leasehold interests, interests of mortgagees, life estates, remainders, and reversions,

- affirmative and negative easements, whether held appurtenant or in gross,

- in a majority of states and at federal level, restrictive covenants (negative restrictions on the development and use of land)

(i) a few easement-enabling statutes,Caveats: (ii) minority rule

How should a conservation easement be valued for purposes of

compensating its holder?

First Eminent Domain Valuation PrincipleThe Meaning of “Just Compensation”

Normal Standard: “Fair Market Value”

FMV is not an absolute standard

U.S. v. Commodities Trading 339 U.S. 121 (1950)

Willing Buyer/Willing SellerOpen and Competitive Market

No Open and Competitive MarketOther Valuation Methods are Employed

“Just compensation” must be fair and equitable to all parties involved

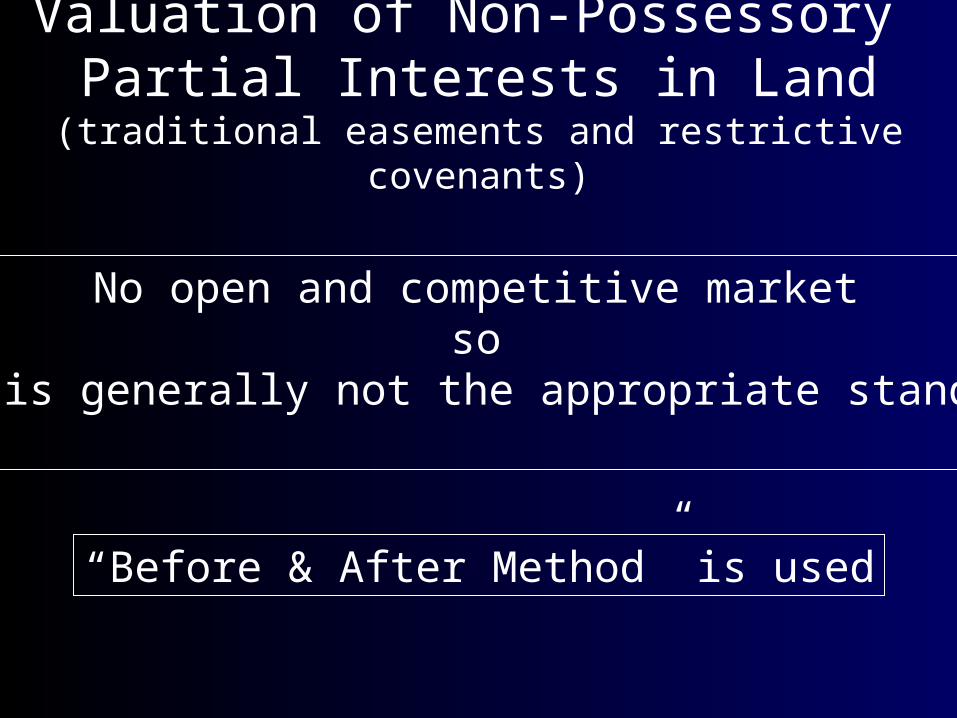

Valuation of Non-Possessory Partial Interests in Land

(traditional easements and restrictive covenants)

“Before & After Method” is used

No open and competitive marketso

FMV is generally not the appropriate standard

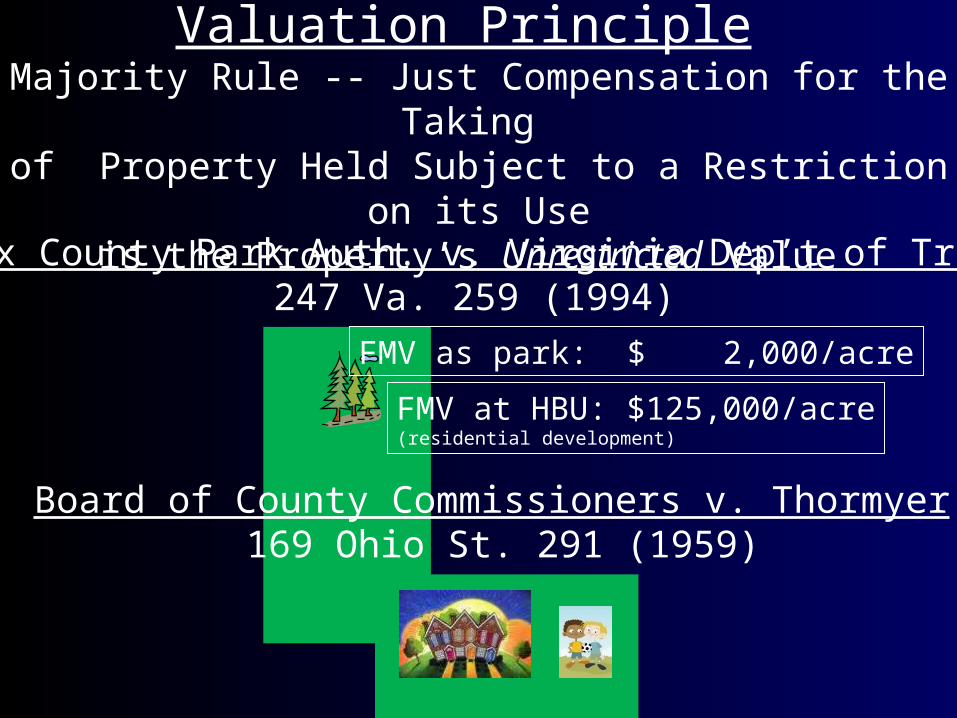

Second Eminent Domain Valuation Principle Majority Rule -- Just Compensation for the Taking of Property Held Subject to a Restriction on its Use

is the Property’s Unrestricted Value

Fairfax County Park Auth. v. Virginia Dep’t of Transp. 247 Va. 259 (1994)

FMV as park: $ 2,000/acre

FMV at HBU: $125,000/acre(residential development)

Board of County Commissioners v. Thormyer 169 Ohio St. 291 (1959)

Second Principle Holder should be entitled to

unrestricted value of CE

First Principle No open and competitive market

FMV is not the appropriate standard

“Before & After Method”

Condemnation of Conservation Easement

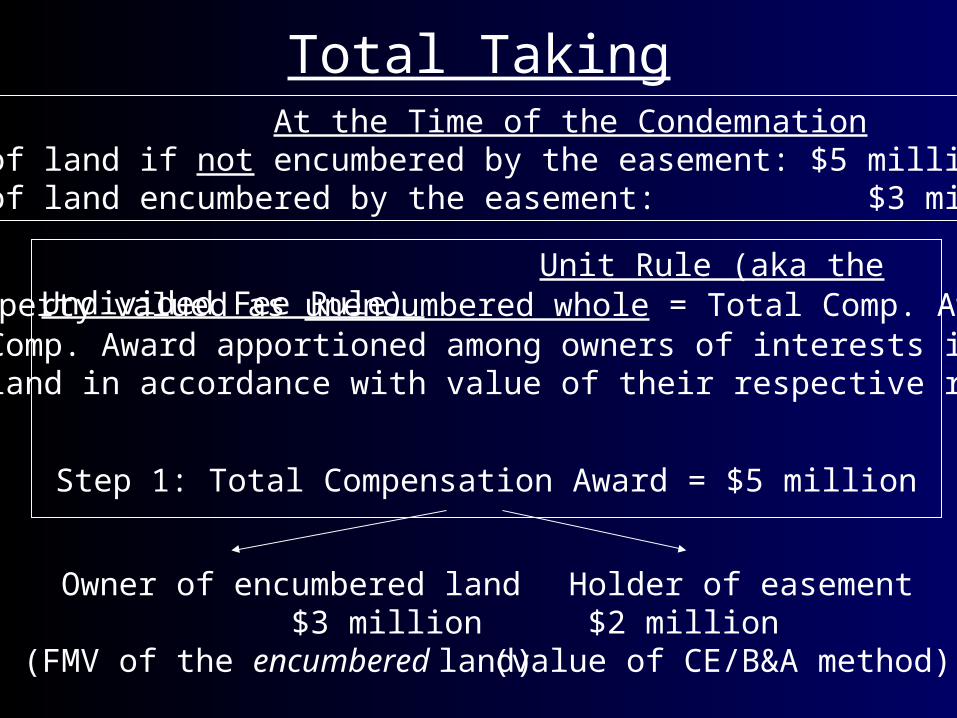

Total Taking

Total Taking At the Time of the CondemnationFMV of land if not encumbered by the easement: $5 millionFMV of land encumbered by the easement: $3 million

Unit Rule (aka the Undivided Fee Rule)

Step 1: Total Compensation Award = $5 million

Owner of encumbered land $3 million (FMV of the encumbered land)

Holder of easement $2 million

(value of CE/B&A method)

1) Property valued as unencumbered whole = Total Comp. Award 2) Total Comp. Award apportioned among owners of interests in the land in accordance with value of their respective rights

Treasury Regulations § 1.170A-14(g)(6)(ii)

“when a change in conditions give rise to the extinguishment of a [conservation easement]…, the donee organization…must be entitled to a portion of the proceeds at least equal to the [Donation %] of the [conservation easement]”

The greater of:1) the Donation % or2) The Extinguishment %

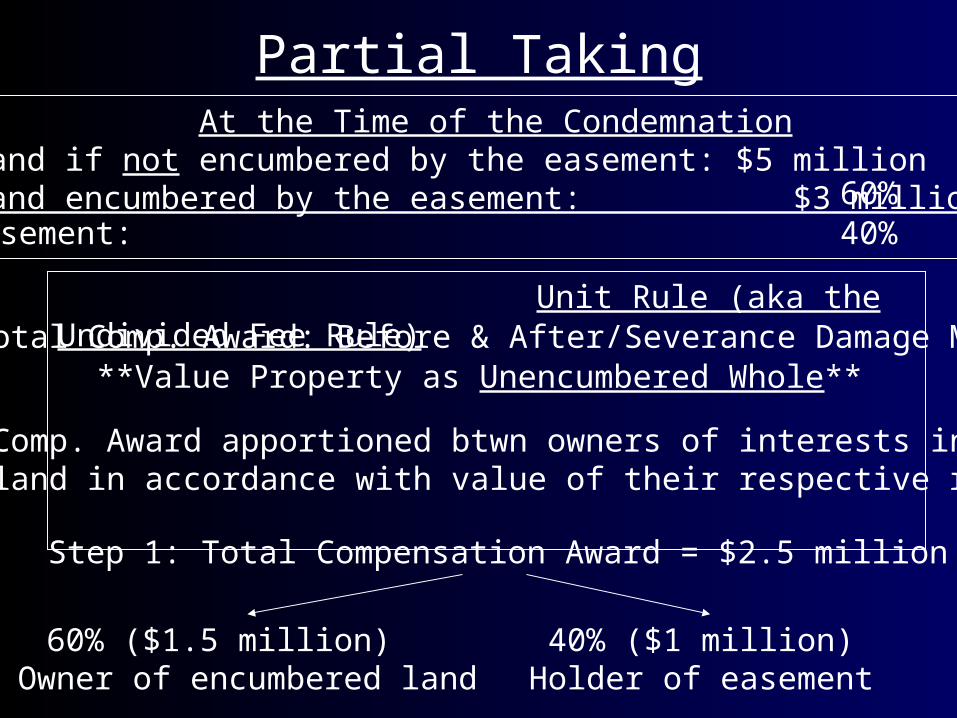

Partial Taking At the Time of the CondemnationFMV of land if not encumbered by the easement: $5 million FMV of land encumbered by the easement: $3 millionValue of the easement: $2 million 40%

60%

Partial Taking At the Time of the CondemnationFMV of land if not encumbered by the easement: $5 million FMV of land encumbered by the easement: $3 million

Step 1: Total Compensation Award = $2.5 million

60% ($1.5 million) Owner of encumbered land

40% ($1 million)Holder of easement

Value of the easement: $2 million

Unit Rule (aka the Undivided Fee Rule)

40%60%

1) Total Comp. Award: Before & After/Severance Damage Method

2) Total Comp. Award apportioned btwn owners of interests in the land in accordance with value of their respective rights

**Value Property as Unencumbered Whole**

Partial Taking

Partial Taking Conservation Purpose Destroyed

Valuation on Front End

Value of deduction = fair market value (FMV)

of conservation easement at time of donation

Prescribed Valuation Methods

Sales Prices of Comparable Easements

But see Browning v. Comm’r, 109 T.C at 312 (1997)

Prescribed Valuation Methods

Before & After Method

Value of Easement = Difference Between:

• FMV of the land immediately before the donation, and

• FMV of the land immediately after the donation

FMV: “the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having a reasonable knowledge of relevant facts.”

Enhancement Rules

Rule #1: Entire Contiguous Parcel Rule

If land contiguous to the land encumbered by the easement is owned by the donor [or] a member of the donor’s family, the value of the easement is equal to the difference between the before-easement and after-easement values of the entire contiguous parcel.

Enhancement Rules

Rule # 2

If the granting of the easement increases the value of any other property owned by the donor or a “related person,” the amount of the deduction must be reduced by the amount of such enhancement, whether or not the property is contiguous.

Incidental Benefit Rule

The donor’s charitable income tax deduction must be reduced by an amount equal to the value of any financial or economic benefit that the donor or a related person receives, or can reasonably expect to receive.

Valuation Abuse

Exaggerating Before-Easement Value

Using

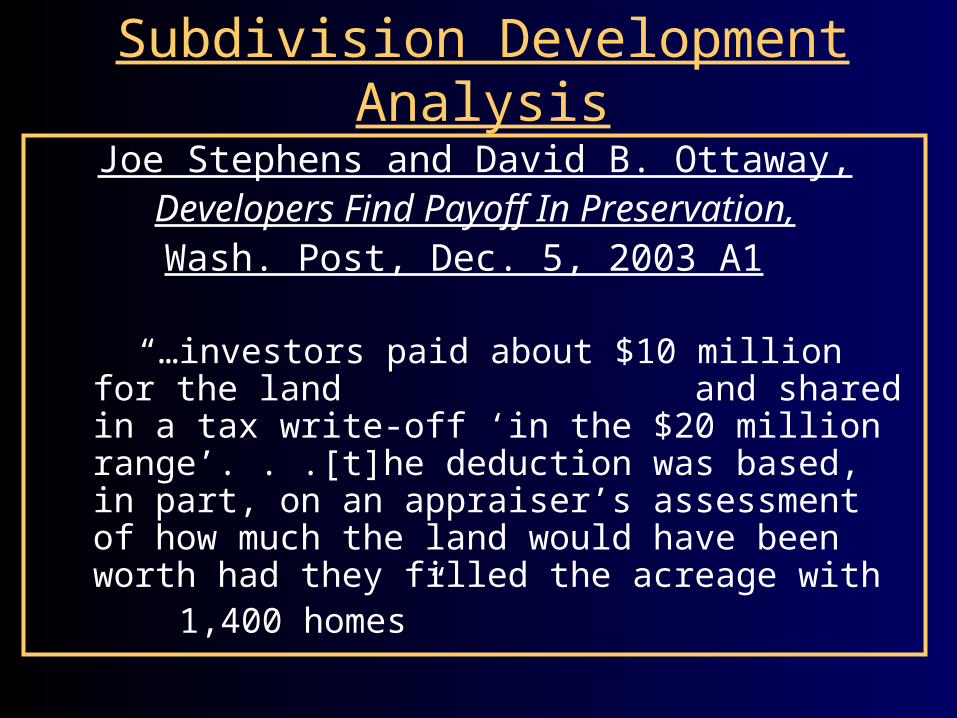

Subdivision Development Analysis

Before & After Method

Value of Easement = difference between:

• FMV of the land immediately before the donation, and

• FMV of the land immediately after the donation

FMV: “the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having a reasonable knowledge of relevant facts.”

Subdivision Development Analysis

• Mimics valuation process employed by prospective purchaser (developer)

• Appraiser determines gross proceeds realizable from imagined development

• Gross proceeds discounted to reflect:- Risks/delays

- Time

- Costs

- Expected profit

Subdivision Development Analysis

• The “highest and best use” of the land is for

subdivision purposes

• The sales comparison approach is not

available

Subdivision Development Analysis

USPAP 2008-2009

“Because [the SDA] is profit oriented and dependent on the analysis of uncertain future events, it is vulnerable to misuse.”

“Because of the compounding effects in the projection of income and expenses, even slight input errors can be magnified and can produce unreasonable results.”

“[The SDA] is best applied in developing value opinions in the context of one or more other approaches.”

Subdivision Development Analysis

U.S. Dept. of Justice, Uniform Appraisal Standards

(“Yellow Book”)

“When comparable sales are available with which to

accurately estimate the property’s market value, the

[SDA] should not be relied upon as the primary

indicator of value, as it is considerably more prone to

error.”

Subdivision Development Analysis

Joe Stephens and David B. Ottaway,Developers Find Payoff In Preservation,

Wash. Post, Dec. 5, 2003 A1

“…investors paid about $10 million for the land and shared in a tax write-off ‘in the $20 million range’. . .[t]he deduction was based, in part, on an appraiser’s assessment of how much the land would have been worth had they filled the acreage with

1,400 homes”

J. D. Eaton, Real Estate Valuation in Litigation (2nd ed.1995)

“If all of the land that has been appraised by the [SDA] were actually subdivided, there would be enough subdivision lots on the market to last hundreds of years and little, if any, farmland left in the United States.”

Subdivision Development Analysis

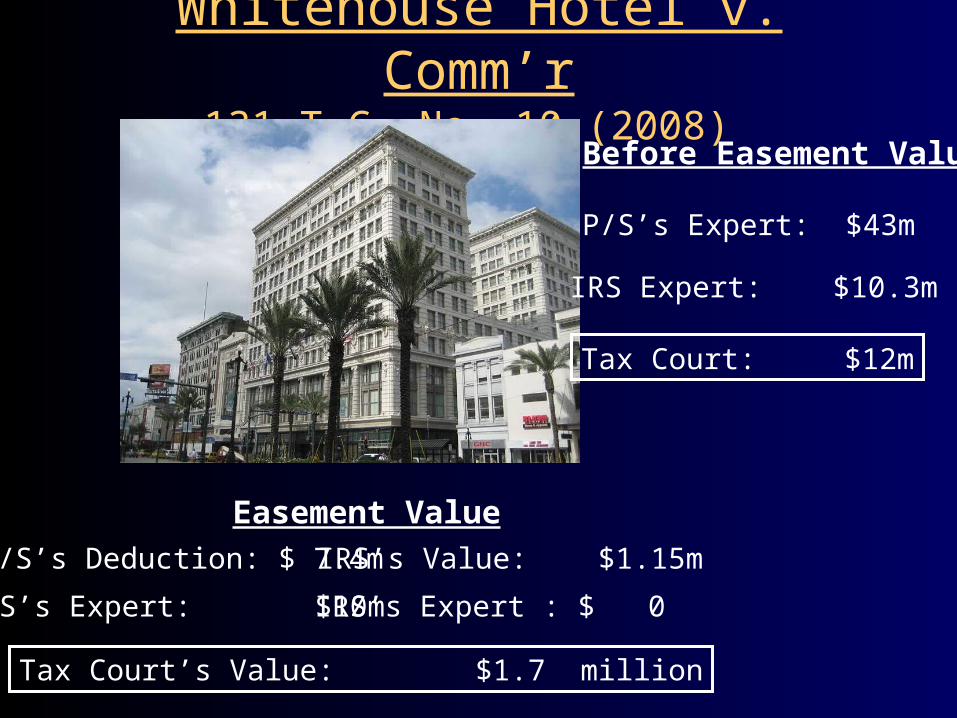

Whitehouse Hotel v. Comm’r131 T.C. No. 10 (2008)

P/S’s Deduction: $ 7.4m IRS’s Value: $1.15m

Tax Court’s Value: $1.7 million

P/S’s Expert: $10m IRS’s Expert : $ 0

Before Easement Value

P/S’s Expert: $43m

IRS Expert: $10.3m

Easement Value

Tax Court: $12m

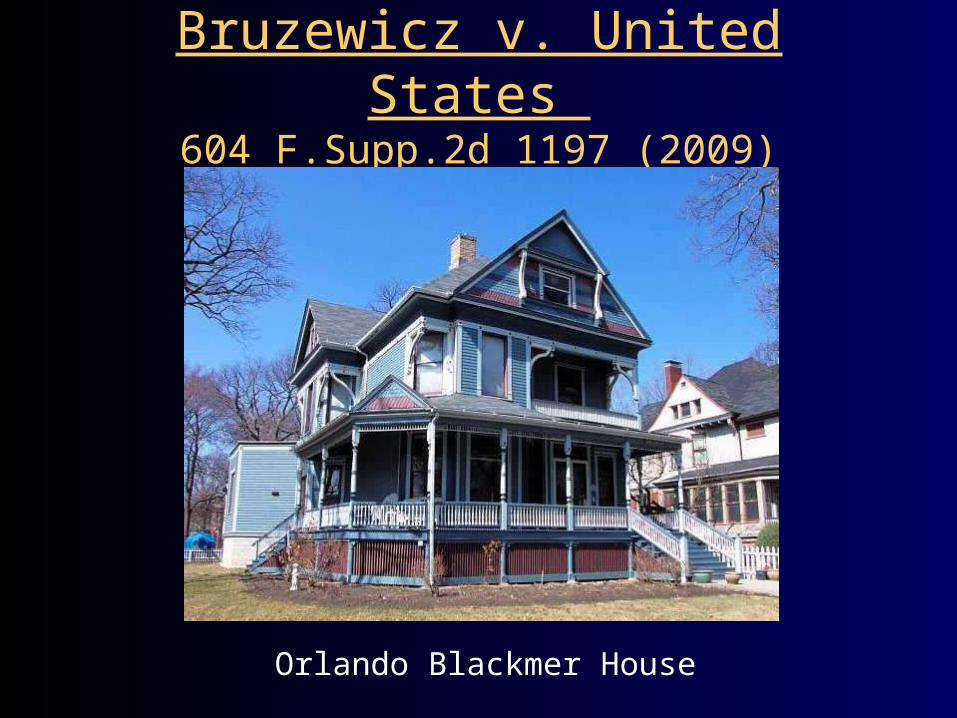

Bruzewicz v. United States 604 F.Supp.2d 1197 (2009)

Orlando Blackmer House

Hughes v. CommissionerT.C. Memo 2009-94

TP’s claimed deduction: $ 3.1mIRS’s value: $ 1.9m

Bull Mountain Parcel

TP purchased for $1.5m in 1999

TP’s expert claims BEV was $3.5m in 2000 (128% appreciation in 14 months)

Court determines BEV was $1.7m 2000

Kiva Dunes v. Comm’r T.C. Memo 2009-145

TP’s Claimed Deduction: $30.5m

Tax Court’s Value: $28.6m

Related Documents