Computer Assisted Audit Techniques Pertemuan 21-22 Matakuliah : A0294/Audit SI Lanjutan Tahun : 2009

Computer Assisted Audit Techniques Pertemuan 21-22 Matakuliah: A0294/Audit SI Lanjutan Tahun: 2009.

Dec 31, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Computer Assisted Audit Techniques

Pertemuan 21-22

Matakuliah : A0294/Audit SI Lanjutan Tahun : 2009

Bina Nusantara University 2

Learning Outcomes

Pada akhir pertemuan ini, diharapkan mahasiswa akan mampu :• Menjelaskan berbagai metode audit dengan

berbantuan komputer• Menjelaskan CAATs

Bina Nusantara University 3

Audit Approaches

• Audit around the computer• Audit through the computer• Audit with the computer

Bina Nusantara University 4

IS Auditing Concepts

• Audit around-the-computer approach, the (IS) processing portion is ignored.

• Auditing through the computer is the process of reviewing and evaluating the internal controls in an electronic data processing system.

• Auditing with the computer, is the utilization of the computer by an auditor to perform some audit work that otherwise would have to be done manually.

Bina Nusantara University 5

Auditing Around the Computer

• A system is comprised of input, processing, output.• Source documents supplying the input to the system

are selected and summarized manually so that they can be compared to the output.

• As batches are processed through the system, totals are accumulated for accepted and rejected records.

• Auditors emphasize control over rejected transactions, their correction, and then resubmission.

• The around-the-computer approach is no longer widely used.

Bina Nusantara University 6

Audit around the computer

• Computer is a “black-box.”• Suitable only under the following conditions:

– The audit trail is complete and visible– The processing operations are relatively

straightforward and low volume– Complete documentation are available

Bina Nusantara University 7

Auditing Through the Computer

• Auditing through the computer may be defined as the verification of controls in a computerized system.

• Should be applied to all complex systems– Test Data– Integrated Test Facility– Embedded Audit Module Techniques– Program Code Checking– Parallel Simulation– Controlled Processing

Bina Nusantara University 8

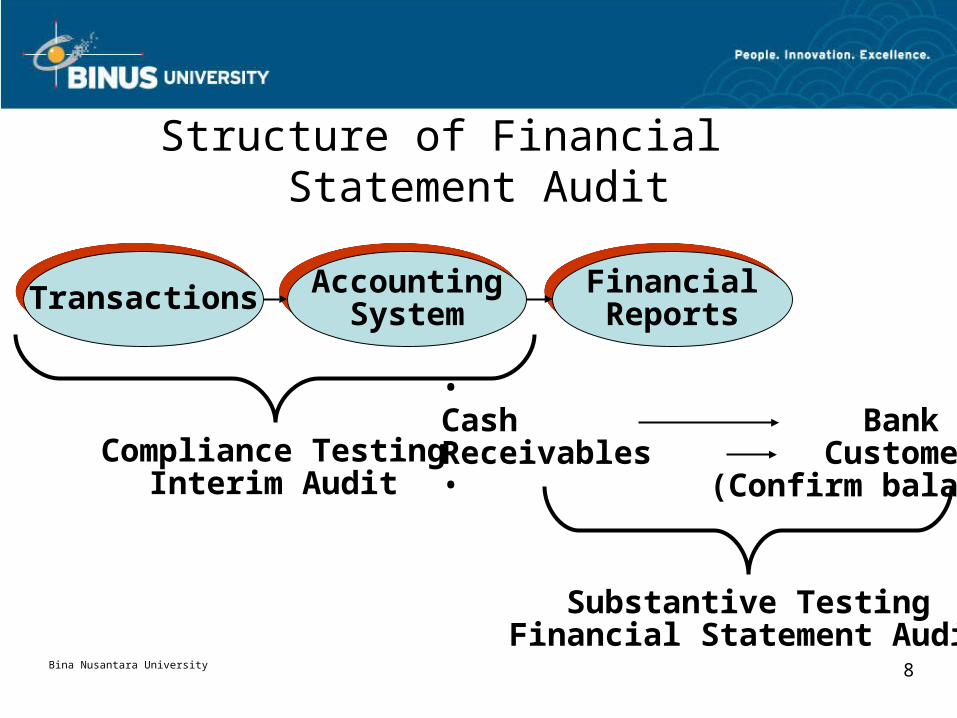

Structure of Financial Statement Audit

AccountingSystem

AccountingSystem

TransactionsTransactionsFinancialReportsFinancialReports

Compliance TestingInterim Audit

Substantive TestingFinancial Statement Audit

• Cash BankReceivables Customers• (Confirm balances)

Bina Nusantara University 9

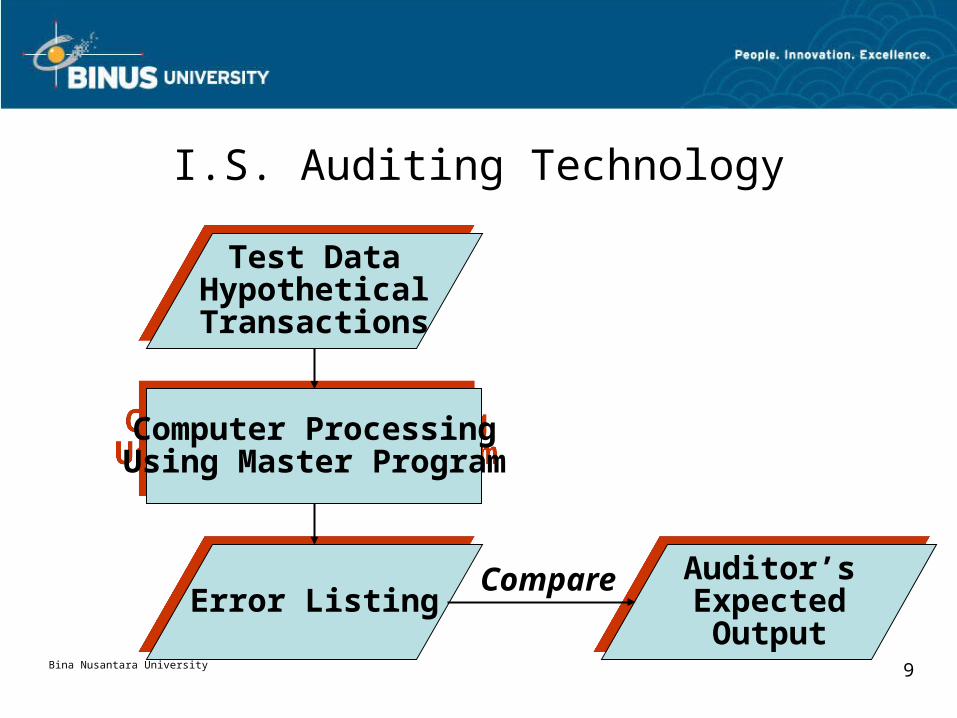

I.S. Auditing Technology

Test DataHypotheticalTransactions

Test DataHypotheticalTransactions

Computer ProcessingUsing Master Program

Computer ProcessingUsing Master Program

Error ListingError ListingAuditor’sExpectedOutput

Auditor’sExpectedOutput

Compare

Bina Nusantara University 10

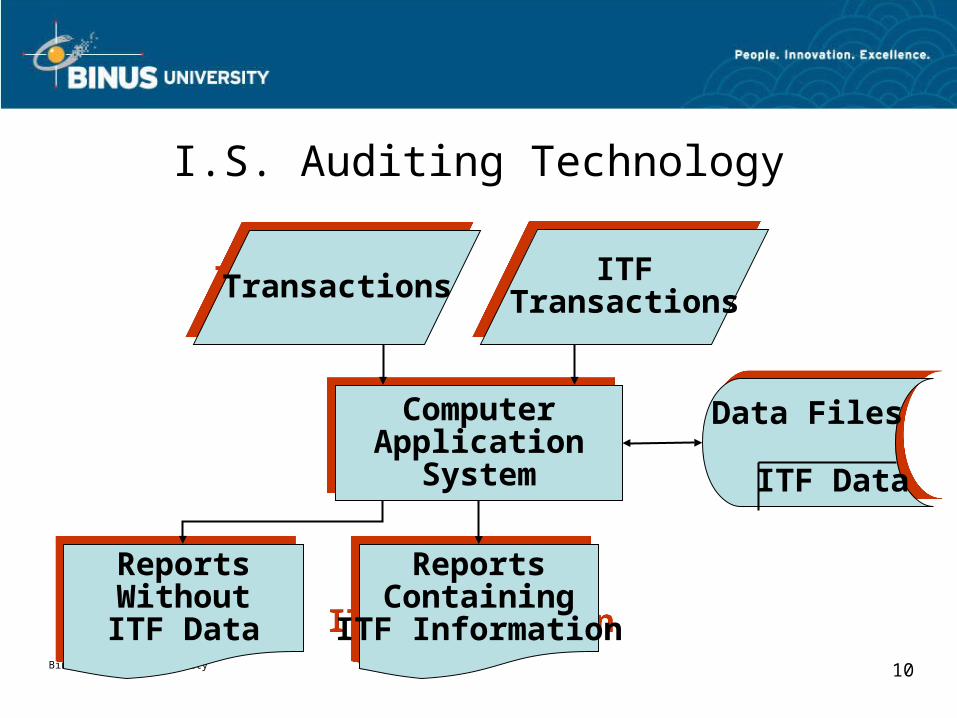

I.S. Auditing Technology

TransactionsTransactionsITF

TransactionsITF

Transactions

ComputerApplication

System

ComputerApplication

System

ReportsWithoutITF Data

ReportsWithoutITF Data

ReportsContaining

ITF Information

ReportsContaining

ITF Information

Data Files

ITF Data

Bina Nusantara University 11

I.S. Auditing Technology

TransactionsTransactions

ParallelSimulationProgram

ParallelSimulationProgram

ReportReportSimulation

ReportSimulation

Report

ComputerApplication

System

Function toBe Verified

Compare

Bina Nusantara University 12

I.S. Auditing Technology

Smart AuditSupport

Smart AuditSupport Access to

InformationAccess to

Information

FileInterrogation

FileInterrogation

WorkPapersWorkPapers

TrialBalance

TrialBalance Multiplication

SupportMultiplication

Support

DocumentManagerDocumentManager

MSWord

MSExcel

MSAccess

Lotuscc:mail ACL

FolioVIEWS

OtherApplications

Bina Nusantara University 13

I.S. Auditing Technology

ProductionTransactions

ProductionTransactions

ProductionReports

ProductionReports

AuditReports

AuditReports

ProductionComputerApplicationSystem

EmbeddedAudit DataCollectionModule

ProductionComputerApplicationSystem

EmbeddedAudit DataCollectionModule

Bina Nusantara University 14

Auditing with the Computer

• Auditing with the computer is the process of using information technology in auditing.

• Most of the data that auditors must evaluate are already in an electronic format.

• The use of information technology is essential to increase the effectiveness and efficiency of auditing.

Bina Nusantara University 15

Auditing with the Computer1. Computer-generated working papers are generally

more legible and consistent.2. Time may be saved by eliminating manual footing,

cross footing, and other routine calculations.3. Calculations, comparisons, and other data

manipulations are more accurately performed.4. Analytical review calculations may be more efficiently

performed.5. Project information may be more easily generated and

analyzed.

Bina Nusantara University 16

Auditing with the Computer

6. Standardized audit correspondence may be stored and easily modified.

7. Morale and productivity may be improved by reducing the time spent on clerical tasks.

8. Increased cost-effectiveness is obtained by reusing and extending existing electronic audit applications to subsequent audits.

9. Increased independence from information systems personnel is obtained.

Bina Nusantara University 17

Audit with the computer

• Generalized Audit Software (GAS)– Prepare trial balances– Statistical Sampling– Data analysis– Evaluate sample results– Histogram (chart) Generation– Record Aging (AR and AP)– File Comparison– Sequence verification

Bina Nusantara University 18

Why use CAATs

• Electronic data• Validate processing• Audit requirement for testing

Bina Nusantara University 19

Usage of CAATs

• Functional• Real time data capture• Data analysis• Confirmation of data

Bina Nusantara University 20

Scope of I.T. audit

• Access• Network• Database• Operating System• Application• Project Management• Business Continuity Plan

Bina Nusantara University 21

AUDIT SOFTWARE

Bina Nusantara University 22

Generalized Audit Software

Off-the-shelf software that provides a means to gain access to and manipulate data maintained on computer storage media.

Reason GAS developmentThe set of problems caused by the diversity of computerized information processing environments that auditors might confront.

Bina Nusantara University 23

GAS in the Market

• ACL by ACL Services• Applaud by Premier International• IDEA

Bina Nusantara University 24

Benefits of using CAATs

• Increases Audit Economy and Efficiency• Improves Audit Effectiveness• Enhances Image of Auditing

Bina Nusantara University 25

Functional of GAS• File access, File reorganization, file Selection• Statistical, Arithmetic• Stratification and frequency analysis• File creation and updating• Reporting• Examine the quality of data• Examine the quality of system processes• Examine the existence of the entities the data purports to

represent• Undertake analytical review• Calculate effects of recommended changes in company policies

(credit limits, interest rates/service charges, commissions, payroll, payment terms, quantity discounts, etc.)

• Continuous monitoring applications

Bina Nusantara University 26

Functional limitations of GAS

• GAS permits auditors to undertake only ex post auditing and not concurrent auditing

• GAS has only limited capabilities for verifying processing logic

• It is difficult for auditors to determine the application system’s propensity for error using GAS

Bina Nusantara University 27

CAATs Planning Considerations

• Understand system and environment• Define the problem or need• Set objectives• Identify files (format and content)• Determine method for obtaining files• Outline processing and output specs.• Estimate cost/benefit of CAATs

Bina Nusantara University 28

Criteria of Selecting GAS• Process various file structures—wk1, xls, rpt, dbf• Review file contents on the screen• Create a data dictionary for all data• Use the modularity approach• Provide audit working papers automatically• Provide the user manual for all modules• Provide data validation feature• Perform statistical sampling • Export files• Provide the on-screen help facilities, tutorial &

toll-free technical assistance

Bina Nusantara University 29

Application in Accounting Industry

• Ernst & Young: Sweden• Application: Improving Audit Efficiency• Benefits

– A standard application make it easier to perform data analysis– Efficiency, audit Sales Process takes only 2-3 hours instead of

12-16– ACL automatically generate audit reports based on most

common factors

Bina Nusantara University 30

Application in Banking Industry

• Investors Group Inc.: HQ in Winnipeg, Manitoba, Canada’s largest mutual fund company

• Application: ensuring regulatory compliance & improving operations

• Benefits– Review client records for cash deposits over CDN$10,000 to

comply with reporting mandated by the Canadian Proceeds of Crime (Money Laundering) and Terrorist Financing Act

– Monitor mutual fund trading activity continuously to ensure ongoing compliance with a wide variety of industry regulations

– Developed a preferred list of suppliers, resulting in overall savings of CDN$600,000

– Develop and implement effective fraud detection controls

Bina Nusantara University 31

Application in Communications Industry

• Ameritech: 73,000 employees & $30 billion in assets

• Application: business process improvements• Benefits

– realized approximately $15 million in value-added recommendations in 9 months

– 100% data analysis (no samples)

Bina Nusantara University 32

Application in Government Accounting

• Louisiana Legislative Auditor: Baton Rouge, LA • Application: Improving Audit Quality and Efficiency• Benefits

– Recover public funds lost due to errors and mismanagement, including an erroneous $173,000 payment uncovered in a five-minute data stratification analysis

– Help auditors pull information from a multitude of agency databases faster, analyze audit risks and conduct data testing with higher accuracy and efficiency

– Obtain a more detailed understanding of agency data during audits, and create standardized reports to analyze monthly agency transactions

Bina Nusantara University 33

Application in Insurance Industry

• Washington National Insurance Company: Phoenix, AZ

• Application: internal audits• Benefits

– Claim checks reconciliation– Significantly reduced the amount of time the Fraud Unit

needed to accomplish their task– Improve policy data analysis– Audit Department is now seen not only as a watchdog but

also as a value-added unit/partner that can increase the productivity and efficiency in all other departments

Bina Nusantara University 34

Application in Manufacturing Industry

• Lockheed Martin Corporation is a large aerospace and defense electronics manufacturing company

• Application: internal audits• Benefits

– perform trend analyses on the labor data (180,000 employees) to determine if people are charging time inappropriately,

– review vendors performance effectively– perform a test in half an hour with ACL; it took 40 hours

before– allow them to conduct a much more thorough analysis

Bina Nusantara University 35

Application in Retail Industry

• Office Depot: the world's largest seller of office products

• Application: how to improve services with meaningful customer data analysis

• Benefits– reduce business risk in A/R– serve customers better– establish clear guidelines service coding & redesign the

customer service coding systems– computer-based training (CBT) program for ACL solutions

Bina Nusantara University 36

Utility Software

Software that performs fairly specific functions that are needed frequently, often by a large number of users, during the operation of computer systems.

Bina Nusantara University 37

Computer-Assisted Audit Techniques

• CAATs - the use of software to perform audit procedures

• Topics– Benefits of CAATs– Examples and success stories– Tools available– Implementation issues

Bina Nusantara University 38

Computer Assisted Audit Techniques

• Testing client’s controls (Assess control risk)– Test data (or test decks) – Parallel simulation– Integrated test facility

• Testing client’s data (Substantive testing)– Data extraction and analysis (e.g., ACL)– Fraud detection (e.g., ACL)– Continuous auditing techniques

Bina Nusantara University 39

Using CAATs Improves Audit Effectiveness

• Join, concantenate and compare different files to quantify findings

• Calculate field statistics (totals, high, low and average value)

• Use multiple indexes to create summary information and highlight possible errors

• Perform detailed analysis– Total file recalculations– Stratification– Gap and duplicate key detection

• Document work performed

Bina Nusantara University 40

Using CAATs Improves Audit Effectiveness

• Example: comparing inventory on hand with subsequent sales enabled auditors to identify slow-moving and obsolete inventory.

Results: better findings/recommendations, and higher assurance on inventory valuations

• Example: analyzing freight charges in a distribution operation identified opportunities for cost savings through relocation of warehouses.

Results: better findings/recommendations, and sales management now requests quarterly analysis of this area

Bina Nusantara University 41

Tools Available for CAATs

• Mainframe/Minicomputers– Report writers – Utilities and Query tools– Conventional programming languages– 4th generation languages– Hardware specific software– Generalized audit software (CA-Panaudit,

FOCAudit, Dyl, SAS, etc.)

Bina Nusantara University 42

Tools Available for CAATs

• Microcomputers– ACL– Applaud– CA-Panaudit Plus– IDEA– PC/FOCAudit– Print report converters (DataImport, Monarch, Link

& Load for use with PC database & spreadsheet packages)

Bina Nusantara University 43

ACL

• Widely used for data extraction and analysis• Allows for virtual 100% testing of client data

Bina Nusantara University 44

IDEA Functionality

• Importing and Exporting Files– Numerous file formats supported, print reports

• Extracting Records – exception testing• Duplicate and gap detection• Statistical Sampling

– sample planning and results analysis– random, stratified, monetary, systematic

Related Documents