Computational Finance Lecture 2 Option Pricing: Binomial Tree Model

Computational Finance Lecture 2 Option Pricing: Binomial Tree Model.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Computational Finance

Lecture 2

Option Pricing: Binomial Tree Model

Is the Stock Market Predictable?

Suppose that Prof. Chen Nan had discovered that stock prices are predictable.

Investors could reap unending profits simply by purchasing stocks that were about to increase and by selling stocks about to fall.

A moment reflection should convince yourself that this is not true.

Is the Stock Market Predictable?

For example, suppose my model predicts that stock XYZ will rise dramatically in three days to $110 from $100.

The prediction must induce a great wave of immediate buy orders.

Huge demands on stock XYZ will push its price to jump to $110 immediately.

Is the Stock Market Predictable?

Any forecast of a future price increase will lead to an immediate price increase.

In other words, any information that could be used to predict stock performance must already be reflected in stock prices.

The genuine driving force behind is new information or unpredictable information.

Efficient Market Hypothesis and Random Walk

Efficient market hypothesis (EMH) : Maurice Kendall (1953), Harry Roberts (1959), Eugene Fama (1965) Weak form:

Stock prices already reflect all information that can be derived by examining market trading data.

Strong form: Stock prices reflect all information relevant

to the firm, even including information available only to the company insiders.

Efficient Market Hypothesis and Random Walk

Under EMH, stock prices should follow a random walk, that is, price changes should be random and unpredictable.

Simplest model of random walk: Flipping a coin Number facing up, then one step

right; Flower facing up, then one step left.

Implication of EMH

Technical analysis: The search for recurrent and predictable patterns in stock prices.

EMH implies that technical analysis is without merit.

Implication of EMH

Fundamental analysis: Attempts to determine “proper”

stock prices using basic information such as earnings and dividend prospects of a firm, expectations of future interest rates, and risk evaluation, etc.

EMH implies that most of such analysis is doomed to failure.

Stock Price as a Random Walk

Imagine that an “invisible hand” is tossing a coin to decide the movement of a stock.

For example, the current stock price is $100. After 1 year, the stock price either goes up to $110 with probability 55%, or goes down to $90 with probability 45%.

Stock Price as a Random Walk

Binomial model: $110, 55%

$100

$90, 45%

Option Pricing on Binomial Model

Suppose that I have a European call option on the stock in the last slide. The maturity is in 1 year and the strike price is $100. How do I evaluate its current value?

$110, 55% Call: $10

$90, 45% Call: 0

Option Pricing on Binomial Model

Idea: Can we construct a portfolio which

consists only of known securities to “duplicate” the behavior of the option?

In other words, if we can duplicate the cash flow of the option by another portfolio using only bank account and the underlying stock, then we can do.

Option Pricing on Binomial Model

Suppose I deposit (or borrow) in a bank account and buy shares of the stock: Up:

Down:

Option Pricing on Binomial Model

Duplicating:

Evaluation: The option price should be equal

to the current value of the portfolio:

Option Pricing on Binomial Model

In general, if we have the following:

Su, p

S Sd, 1-p

Option Pricing on Binomial Model

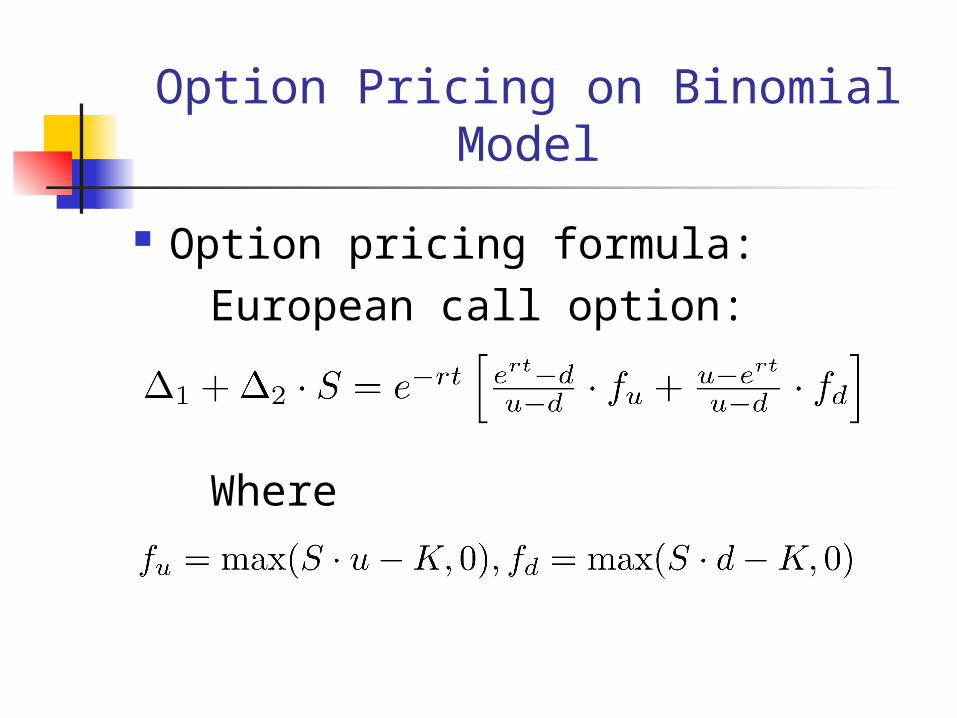

Option pricing formula: European call option:

Where

Option Pricing on Binomial Model

Risk neutral probability:

We can regard the formula in this way:

The value of an option is the present value of the expected cash flow at the maturity, only it is not the “real expectation”.

Risk Neutral Probability

Risk neutral probability: Expected value of the stock at

time t:

Where Did the Real Probability Go?

Real probability plays no role in the option pricing formula.

Why not the following?

Risk and risk premium

Options on Cum Dividend Stocks

Suppose that the dynamic of the underlying stock is :

Su, p

S Sd, 1-p

The time to maturity is t and a dividend amount of D is expected at s.

Options on Cum Dividend Stocks

Duplicating:

Option price:

Options on Foreign Currencies

Suppose that the Australian dollar is currently worth US$0.654. The risk free interest rates are 7% and 5% annually in Australia and the United States, respectively.

A US investor wants to buy a call option on the AUD with strike price of US$0.65. The maturity is in 3 month.

Options on Foreign Currencies

Use a binomial model: $0.677, Call:

0.027

$0.654

$0.632, Call: 0

Options on Foreign Currencies

Duplicating: : USD in a bank account; : AUD Two outcomes:

Up:

Down:

Options on Foreign Currencies

Duplicating:

Option value:

More Realistic Extension:Binomial Tree Model

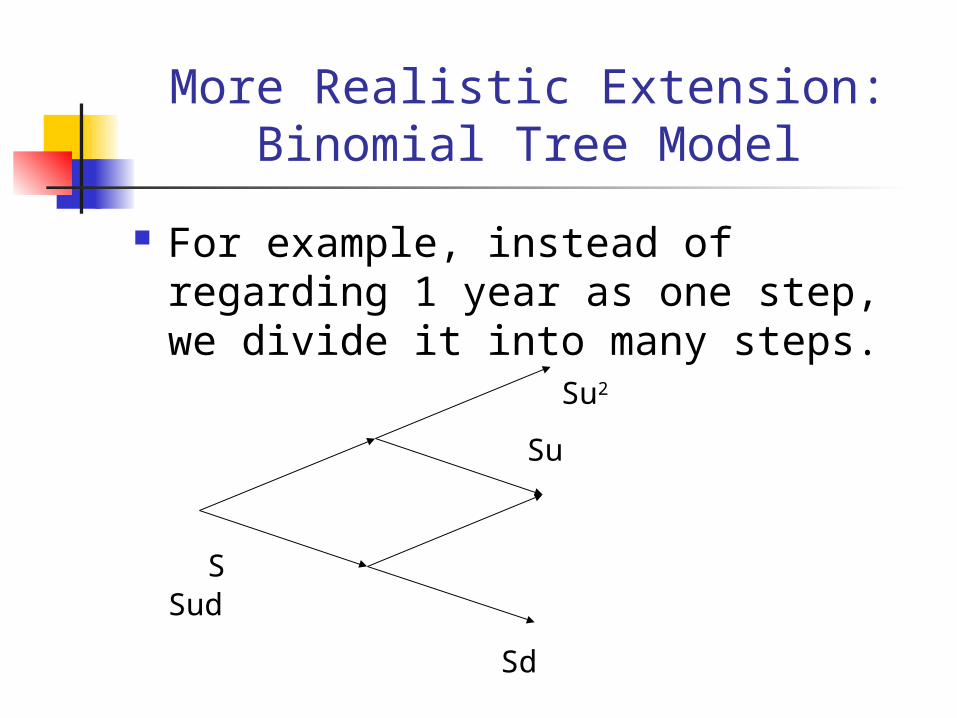

In theory, there should be infinite possible outcomes for the underlying stock price.

One step binomial tree is too simple to be a good approximation to the real world.

Extension: multiple step binomial model.

More Realistic Extension:Binomial Tree Model

For example, instead of regarding 1 year as one step, we divide it into many steps. Su2

Su

S Sud

Sd Sd2

Valuing Back down the Tree

Suppose that we have a stock whose current price is $20 per share. We want to consider a European call option with strike price of $21 and maturity date in 6 month. The risk free interest rate is 12% per annum.

Two step binomial tree: 3 months as a step. In every step the price may go up by 10% or down by 10%.

Valuing Back down the Tree

Work forward to label the stock prices:

$24.2

$22

$20 $19.8

$18 $16.2

Valuing Back down the Tree

Work backward to value the option:

$24.2

$22

$20 $19.8

$18 $16.2

$3.2

$0.0

$0.0

$2.0257

$0.0

$1.2823

American Option Pricing and Early Exercise

Suppose that the previous option is American style, that is, we can exercise it any time before it matures.

How can we evaluate it?

American Option Pricing and Early Exercise

Suppose that we have a stock whose current price is $50 per share.

We want to consider an American put option with strike price of $52 and maturity date in 2 years. The risk free interest rate is 5% per annum.

Two step binomial tree: 1 year as a step. In every step the price may go up by 20% or down by 20%.

American Option Pricing and Early Exercise

Work forward to label the stock prices:

$72

$60

$50 $48

$40 $32

Valuing Back down the Tree

Work backward to value the option:

$72

$60

$50 $48

$40 $32

$0

$4

$20

$1.4147

$9.4636

$5.0894

$0

$12

$2

Matching u and d with Real Data

Two parameters undetermined: u, d

Usually people choose u and d to match the fluctuation of the stock price in the real world, i.e., to match the volatility of the stock price.

Related Documents

![A Skewness-Adjusted Binomial Model for Pricing …file.scirp.org/pdf/JMF20120100011_82298793.pdf · Black-Scholes (B-S) [2] model and the binomial option pricing model (BOPM) with](https://static.cupdf.com/doc/110x72/5b6b45f97f8b9a422e8d3f09/a-skewness-adjusted-binomial-model-for-pricing-filescirporgpdfjmf20120100011.jpg)