Page 1 of 53 Compliance of the C&AG Inspection Audit Paras up to the year 2018-19 Year and Para Number Details of the Audit Para Compliances Present Status 2015-16 Para 1, Part IIA Irregular fixation of pay of Reader/Lecturer (Selection Grade) and re-designation thereof as Associate Professor leading to excess payment of pay and allowances amounting to Rs. 3.13 crore The MHRD vide its letter no. 1-32/2006-U.II/U. I(i) dated 31 st December 2008 implemented the scheme of revision of pay scales of teachers and equivalent cadres in Central Universities/Colleges following the revision of pay scales of Central Government employees on the recommendation of 6 th CPC. The MHRD/UGC instructed that pay of the Reader and Lecturers (Selection Grade) shall be fixed considering the following: (i) Incumbent Reader and Lecturers (Selection Grade) who had not completed three years in the pay scale of 12000- 18300 on 01.01.2006 shall be placed at the appropriate stage (as indicated in Table-3) in the pay band of 15600-39100 with Academic Grade Pay (AGP) of Rs. 8000 till the complete of three years of service in the grade of Reader/ Lecturers (Selection Grade) and thereafter shall be placed in the higher Corrective measures have already been taken by the University by re- fixing the pay of the concerned incumbents. Recovery from pay of 15 incumbents (out of the total of 23 incumbents) is being made. 08 incumbents have filed a writ petition in the Hon’ble Gauhati High Court challenging the decision of the University to recover the excess pay and the matter is under status quo in the Hon’ble High Court. Audit stated that since the recovery is under process, the para stands.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Page 1 of 53

Compliance of the C&AG Inspection Audit Paras up to the year 2018-19

Year and

Para

Number

Details of the Audit Para Compliances Present Status

2015-16

Para 1,

Part IIA

Irregular fixation of pay of Reader/Lecturer (Selection

Grade) and re-designation thereof as Associate Professor

leading to excess payment of pay and allowances amounting

to Rs. 3.13 crore

The MHRD vide its letter no. 1-32/2006-U.II/U. I(i) dated 31st

December 2008 implemented the scheme of revision of pay

scales of teachers and equivalent cadres in Central

Universities/Colleges following the revision of pay scales of

Central Government employees on the recommendation of 6th

CPC. The MHRD/UGC instructed that pay of the Reader and

Lecturers (Selection Grade) shall be fixed considering the

following:

(i) Incumbent Reader and Lecturers (Selection Grade)

who had not completed three years in the pay scale of 12000-

18300 on 01.01.2006 shall be placed at the appropriate stage

(as indicated in Table-3) in the pay band of 15600-39100 with

Academic Grade Pay (AGP) of Rs. 8000 till the complete of

three years of service in the grade of Reader/ Lecturers

(Selection Grade) and thereafter shall be placed in the higher

Corrective measures have already

been taken by the University by re-

fixing the pay of the concerned

incumbents. Recovery from pay of

15 incumbents (out of the total of 23

incumbents) is being made. 08

incumbents have filed a writ petition

in the Hon’ble Gauhati High Court

challenging the decision of the

University to recover the excess pay

and the matter is under status quo in

the Hon’ble High Court.

Audit stated

that since the

recovery is

under process,

the para stands.

Page 2 of 53

pay band of Rs. 37400-67000 and accordingly re-designated

as Associated Professor.

(ii) Incumbent Readers and Lecturers (Selection Grade) who

have completed three years in current pay scale of 12000-18300

on 01.01.2006 shall be placed in pay band of 37400-67000 with

AGP pay of Rs. 9000 and shall be re-designated as Associate

Professors.

(iii) Readers/ Lecturers (Selection Grade) in service at present

shall continue to be designated as Lecturer (Selection Grade) or

Readers, as the case may be until they are placed in the pay band

of Rs.37400-67000 and re-designated as Associate Professor in

the manner described at Sl No. (i) above.

Records revealed that the University had re-designated all the

Readers as Associated Professors and placed them in pay band-

4 with academic grade pay of Rs. 9000 following the

communication from the Joint Secretary, UGC dated 28.02.2009

and letter dated 31.12.2008 from MHRD. But the University did

not follow the stipulated condition of the said MHRD order dated

31.12.2008 for promotion of Associate Professors with AGP of

Rs. 9000 form Reader/ Lecturers with AGP of Rs.8000 as it was

clearly mentioned in the said order that incumbent Reader and

Page 3 of 53

Lecturers (Selection Grade) who had not completed 3 years in

the pay scale of Rs. 12000-18300 on 01.01.2006 shall not be

placed in the higher pay band of ̀ 37400-67000 with AGP of Rs.

9000 and re-designated as Associate Professor. Finally the

University had fixed Readers in the pay scale of Rs. 37400-

67000 plus AGP of Rs. 9000 (As per table-4) instead of placing

at the appropriate stage (as per table-3) in the pay scale of Rs.

15000-39100 plus AGP of Rs.8000 as the Readers did not

complete 3 years in pay scale of 12000-18300 on 01.01.2006. In

this way the University incurred in excess payment of Rs.

3,12,60,238 in respect of 24 no. of Readers as detailed in the

Annexure-I.

Later on, the UGC had stated in its letter dated on 19.02.2010

that Readers appointed on or after 01.01.2006 are to be placed in

the pay band-4 with AGP of Rs. 9000 only after completion of

three (03) years as Reader. Subsequently the University in its

letter dated on 18.03.2010 had requested to clarify the said matter

in order to avoid any anomaly. Finally, the UGC had stated in its

letter dated on 26th August 2010 and 4th August 2015 stated that

the Readers appointed on or after 01.01.2006 till the issue of

UGC regulation 2010 i.e. 30.06.2010 shall move to pay band-4

with AGP of Rs. 9000 after completing three (3) years of

Page 4 of 53

service. This shall also apply to the Lecturers (Selection Grade)

promoted during the above period.

The University has informed that a high level committee has

already been set up to examine the audit para and make necessary

recommendations wherever required.

Further development is awaited.

2015-16

Para 2

Part IIA

Inadmissible payment of Special Duty Allowances (SDA)

amounting to Rs. 68.28 lakh.

As per FR & SR, Part-I, any Central Government civilian

employees on posting to any station in the North-Eastern Region,

whether the transfer (including initial appointment) was from

outside the region or from another area of the region, was entitled

to get to Special (Duty) Allowance, and SDA was not admissible

during the periods of leave/training beyond 15 days at a time and

beyond 30 days in a year, and during suspension/joining time.

As per the leave calendar of the Tezpur University, all faculties

had enjoyed 30 days of leave during summer recess and they had

not performed their duty during this period. The Head of

Department (HoD), if required, may involve the faculty during

the recess period by issuing an order. Scrutiny of records

revealed that all faculties were being paid Special Duty

Although mention of the

inadmissibility of SDA during the

periods of leave/training beyond 15

days at a time and 30 days in a year

is there in the FR&SR, but the

University could not find reference

of any particular Office

Memorandum issued by the

DoPT/Ministry of Finance, GoI

despite sincere effort. Also, it is not

specifically clear as to whether this

also applies to vacation availed by

teachers. Payment of SDA to the

teachers during vacation has been an

age-old practice in absence of any

clear cut guidelines.

Considering these ambiguities, the

matter has been referred to the University Grants Commission vide

Page 5 of 53

Allowance (SDA) as usual, without considering whether they

had actually performed their duty or not during aforesaid period.

Further scrutiny revealed that an amount of Rs. 68.28 lakh

(Annexure-II) was paid to those faculties who had not

performed their duty during the summer recess.

This action of the University violating the provision stipulated

under the FR & SR resulted in inadmissible payment of Special

(Duty) Allowances to their faculties to the extent of Rs. 68.28

lakh (annexure enclosed) during the period from 01-06-2009 to

31-07-2016.

In reply, the University has informed that the facts and figures in

audit paras were being checked. Action taken in this regard

would be communicated and shown to next audit.

our letter No. TU/Fin/IR/2015-

16/304/3971-A dated 03.1.2017 for

clarification/guidelines. Copy of the

letter is enclosed at Annexure-I.

Subsequent development in the

matter will be produced to next audit

for verification/review of the matter.

2015-16

Para 1.2

Part IIB

Unfruitful expenditure to the tune of Rs. 196.89 lakh.

In August 2012 Tenders for the work, construction of School

Building for KendriyaVidyalay Ground floor & First floor were

called and after opening price bid it was found that the quoted

amount of L-1 (Arunodoy construction) was 0.1 percent below

With reference to the audit paragraph , the following clarifications may be furnished:

1) Height of the stage was

raised by one foot in order

to hold the convocation

Page 6 of 53

the estimated cost of Rs.9,17,69,925 among four bidders. The

work was awarded to the L-4, Hi Tech. Construction at the cost

of Rs. 9.57 crore, which was 4.34% higher than the estimate

cost of Rs. 9, 17, 69,925/- vide W.O. No. F-13-12 (Vol-

XI)/97(EC)/130 dated 03.08.2012 based on preference clause in

the NIT (preference will be given to bidder with experience of

completing a full KendriyaVidyalaya building during the last

five years.

Again the work for construction of second floor of the school

building for K.V. was awarded to the same contractor, M/s. Hi

Tech. Construction vide W.O. No. F.13-12/(Vol-

XI)/97(EC)/185 dated 25.08.13 at the cost of Rs. 551.48 lakh at

the same rate, terms and conditions of the work C/o of School

Building for KV (GF&FF) as an extension.

Rule 181 of G.F.R provides that execution of any work valuing

more than Rs. 25 lakh should be done through inviting open

tender, which has to be well circulated, publish in national daily

and also in web site of the entity. But in this particular case

University did not follow the mandatory provision of GFR and

awarded the work at the cost of Rs. 551.48 lakh to the existing

contractor of their choice without going through tendering

process.

where Hon’ble President of

India , who is also the

Visitor of Tezpur

University, was the Chief

Guest. In convocation ,

sitting arrangement is

required on the stage for the

dignitaries whereas for

school , the stage height was

sufficient as assembly etc.

are carried out on standing

position.

2) The problem of echo as

pointed out by Audit was

there at the beginning but

by opening the top sides of

the dome, it was found that

the problem came down

considerably. Now, it is

within tolerance level and

the space under dome is

fully utilized by KV.

3) No extra expenditure is

made for acoustic treatment

work.

4) Intended purpose for

providing the dome is now

fulfilled. (Certificate from

Principal KV,CUT, Tezpur

is enclosed at Annexure.-

III).

Page 7 of 53

However the above work was completed in all respect on 04.08

2014 and handed over to K.V. authority on 12.08.2014. A site

visit was made by the Hon’ble Vice Chancellor, along-with

Registrar and coordinator on 03.06 2014 for the selection of

forthcoming Convocation to be held on 20.11.2014. It was

pointed out that height of the stage is not sufficient from the point

of view from the back and should be dismantled marble flooring

so that concreting could be done for raising the height of the

stage by one foot. The other serious problem faced in the KV

building was echo and reverberation problem in the court yard.

The problem was so acute that even morning assembly of the

student for prayer could not be held in this designated place and

had to be conducted outside the building.

The construction was carried out adhering to the drawing and

specification provided by the consultant (Harpal Singh

Associates) appointed for this job. The consultant visited the site

and admitted the same. After a few weeks the consultant

proposed another estimate for “Acoustic Treatment work’’ for

corrective measures at the cost of Rs. 32.94 lakh which is under

consideration till date.

At the beginning the purpose of the school building court yard

with full top cover (DOME) at second floor roof level was made

Hence, the construction of the KV

with Dome is found to be justified.

Considering the above, the para

may kindly be reviewed and

dropped.

Page 8 of 53

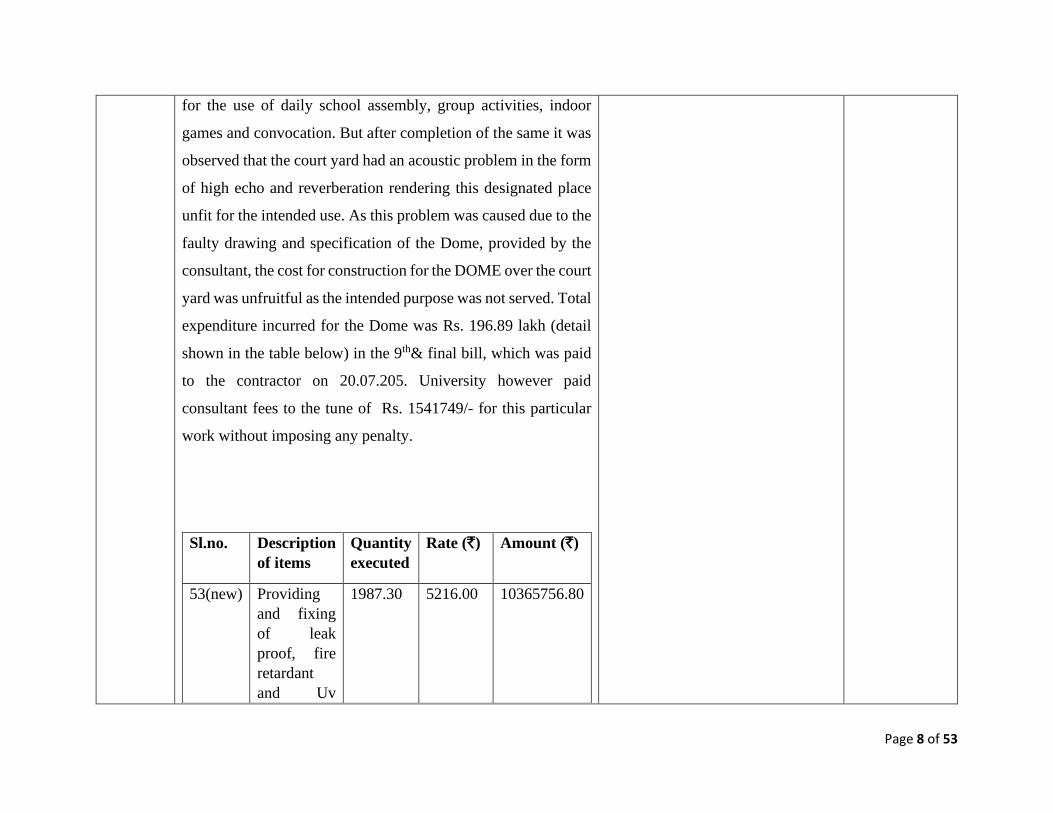

for the use of daily school assembly, group activities, indoor

games and convocation. But after completion of the same it was

observed that the court yard had an acoustic problem in the form

of high echo and reverberation rendering this designated place

unfit for the intended use. As this problem was caused due to the

faulty drawing and specification of the Dome, provided by the

consultant, the cost for construction for the DOME over the court

yard was unfruitful as the intended purpose was not served. Total

expenditure incurred for the Dome was Rs. 196.89 lakh (detail

shown in the table below) in the 9th& final bill, which was paid

to the contractor on 20.07.205. University however paid

consultant fees to the tune of Rs. 1541749/- for this particular

work without imposing any penalty.

Sl.no. Description

of items

Quantity

executed

Rate (`) Amount (`)

53(new) Providing

and fixing

of leak

proof, fire

retardant

and Uv

1987.30 5216.00 10365756.80

Page 9 of 53

resistant sky

lighting

glazing with

Lexan Polly

carbonate

sheet

(multiwall)

10 mm thick

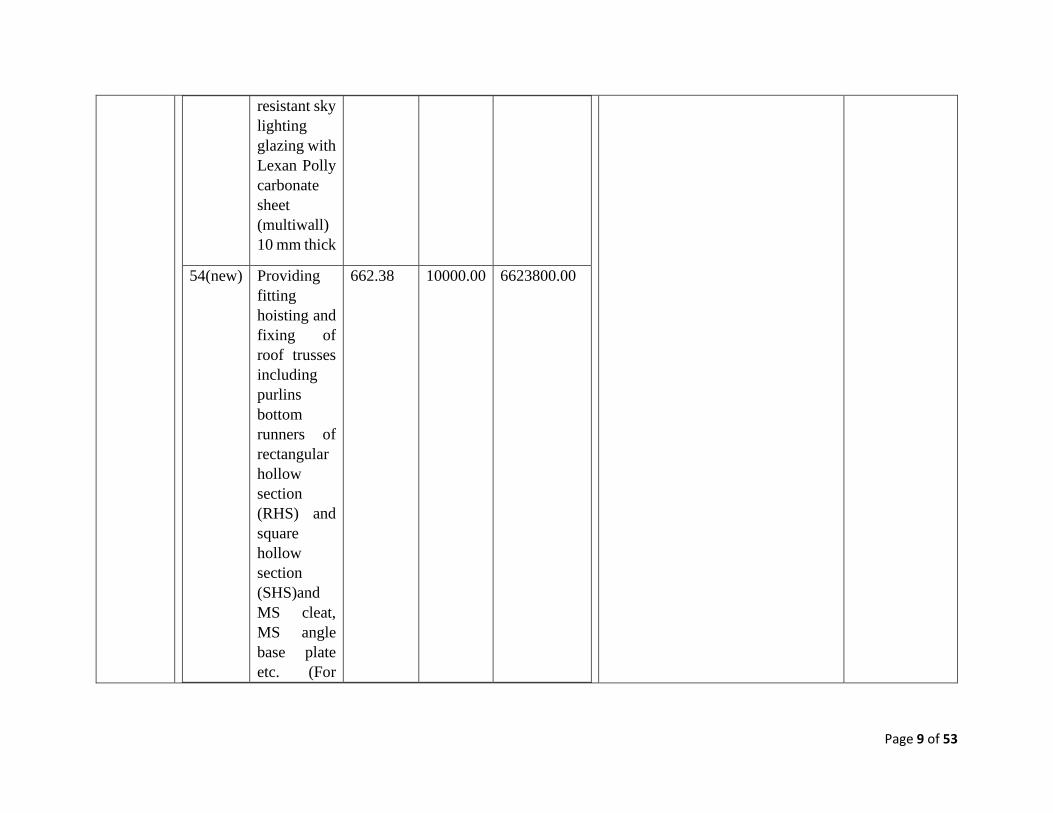

54(new) Providing

fitting

hoisting and

fixing of

roof trusses

including

purlins

bottom

runners of

rectangular

hollow

section

(RHS) and

square

hollow

section

(SHS)and

MS cleat,

MS angle

base plate

etc. (For

662.38 10000.00 6623800.00

Page 10 of 53

Dome

structure)

35(new) Providing

fabrication

and fixing

of structural

glazing

made out of

anodized

aluminum

mother

frame and

5mm

reflective

glass of

approved

shade.(For

Dome side

wall)

248.33 10870.56 2699486.15

TOTAL 19689042.95

Reply was awaited.

2015-16

Para 2.2

Part IIB

Non-payment of EPF amounting to Rs. 51.06 lakh.

In order to provide necessary housekeeping service of personnel

and materials in the University Premises by maintaining neat,

clean and tidy and ensure hygiene and sanitary condition of high

The clarification from the Chief Labour Commissioner, Guwahati is still awaited. The matter is however being referred to them again for necessary clarification.

Page 11 of 53

standard the University entered into a contract on 01.04.2008 and

awarded the work to Sulabh International Social Service

Organization (SISSO) North East (Assam) for a period of one

year and subsequently extended upto July, 2017 with usual terms

and conditions.

(I) The contract was for a period of one year which may be

extended subject to satisfactory performance.

(II) SISSO shall deploy the required number of volunteer to

maintain the specialized service of the premises.

(III) The wages in respect of volunteers and supervisors will

only on daily basis as per GOI Notification from time to time.

Scrutiny of records revealed that the said agency had been

working since 2008 to till date under year wise separate contract

with satisfactory performance.

The casual employees engaged so contractor were entitled to

benefits U/S 16(1)(b) of the Employees Provident Fund and

Miscellaneous Provision (EPF and MP) Act 1952. The

provision of the section 30(3) of the act ibid provided that it

was the responsibility of the principal employer to pay the

contribution payable in respect of the employees employed

by or through a contractor.

Meanwhile, the University drew the attention of SISSO, Assam State Branch, Guwahati on the observation of audit seeking their clarification in the matter, vide letter No. 12-12/98/Vol-II/GA-II/3242 dated 11.11.2016. In response, the Hony. Controller, SISSO vide their letter No. SISSO/ASB/Ghy/2016/222 dated 25.11.2016 has clarified that the volunteers, who are engaged in the cleaning services, are honorary associate members of SISSO. There is no employer-employee relationship between SISSO and the volunteers. As the objective of the volunteers is to render social service and not to attain personal benefits, no wages/salaries are paid to them. However, a token honorarium is given to them by SISSO to sustain their livelihood during the period of their voluntary social service. The copy of the letter is enclosed at Annexure-V. The latest position including the clarification as is being sought from the Chief Labour Commissioner, Guwahati, if received, will be submitted to next audit for further review in the matter.

Page 12 of 53

Further in order to extend and application of EPF and Misc.

Provision act 1952 to any other establishment employee 20 or

more persons of class of such establishment which the

Central Government may by notification in the official

gazette, specify in this behalf.

Checking of records further reveal that the University had

engaged more than 20 volunteers and supervisors for the said

work since beginning i.e. on 2008 but the University did not

remit any EPF contribution for the said workers to the EPF

organization. More over the University did not make any EPF

provision in the agreement. In this way, evasion of the EPF

contribution by the University during the period from

01.04.2008 to 31.07.16 stands Rs. 5105971 (Annexure-IV).

In reply the University stated that the provision of EPF

contribution was not included in the agreement as the SISSO was

exempted being a registered NGO. The University also replied

that it was done on verbal discussion but the university is not

having any such papers/information in regard to Exemption

Certificate.

Further, the University has informed that they have taken up the

matter with the Chief Labour Commissioner, Guwahati

Further , development will be intimated.

Page 13 of 53

2015-16

Para 7.1

Part IIB

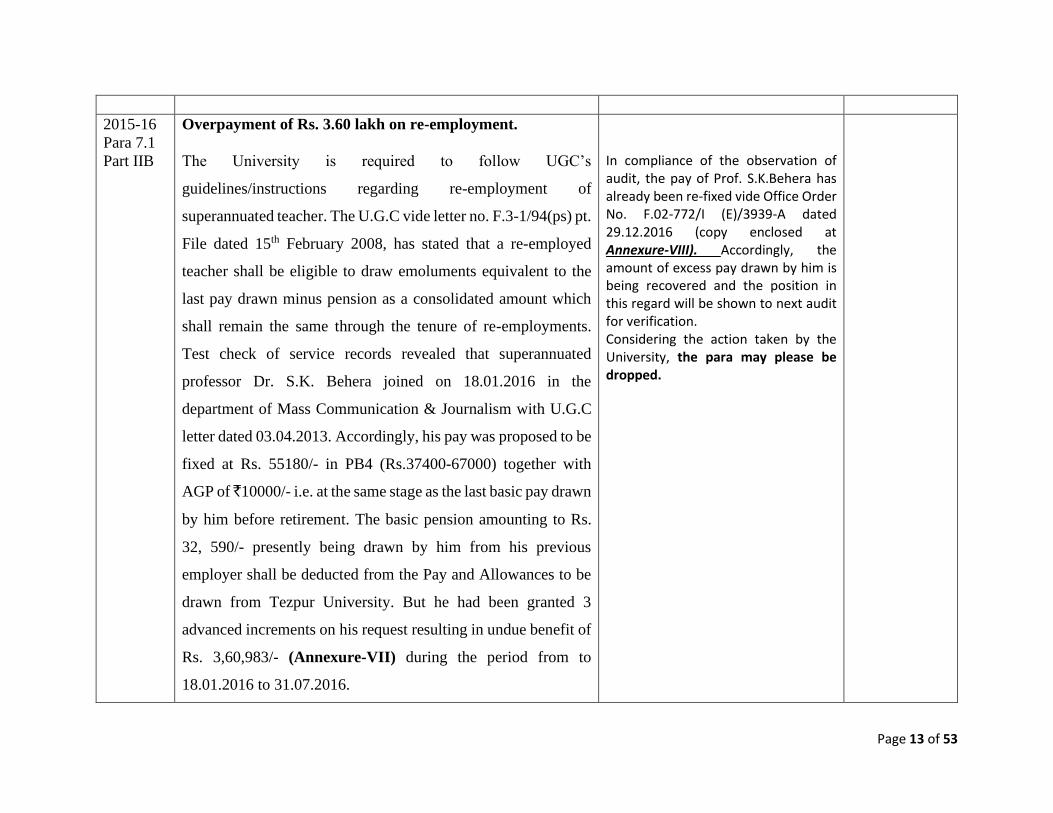

Overpayment of Rs. 3.60 lakh on re-employment.

The University is required to follow UGC’s

guidelines/instructions regarding re-employment of

superannuated teacher. The U.G.C vide letter no. F.3-1/94(ps) pt.

File dated 15th February 2008, has stated that a re-employed

teacher shall be eligible to draw emoluments equivalent to the

last pay drawn minus pension as a consolidated amount which

shall remain the same through the tenure of re-employments.

Test check of service records revealed that superannuated

professor Dr. S.K. Behera joined on 18.01.2016 in the

department of Mass Communication & Journalism with U.G.C

letter dated 03.04.2013. Accordingly, his pay was proposed to be

fixed at Rs. 55180/- in PB4 (Rs.37400-67000) together with

AGP of ̀ 10000/- i.e. at the same stage as the last basic pay drawn

by him before retirement. The basic pension amounting to Rs.

32, 590/- presently being drawn by him from his previous

employer shall be deducted from the Pay and Allowances to be

drawn from Tezpur University. But he had been granted 3

advanced increments on his request resulting in undue benefit of

Rs. 3,60,983/- (Annexure-VII) during the period from to

18.01.2016 to 31.07.2016.

In compliance of the observation of audit, the pay of Prof. S.K.Behera has already been re-fixed vide Office Order No. F.02-772/I (E)/3939-A dated 29.12.2016 (copy enclosed at Annexure-VIII). Accordingly, the amount of excess pay drawn by him is being recovered and the position in this regard will be shown to next audit for verification. Considering the action taken by the University, the para may please be dropped.

Page 14 of 53

Reply was awaited.

2016-17

Para 1

Part IIA

Injudicious investment policy resulted in loss of interest of

Rs. 4.30 crore

Queen’s Academy India (QAI) project, a project between

Government of India and Queen’s University Belfast (QUB) was

aimed at capacity building in 5 partner institutions including

Tezpur University to ensure expansion and quality enhancement

of higher education in the North East Region. The entrants in the

QAI programme were to undergo training embedding quality

and innovation in their research and teaching activities. The

trained persons in turn were to transfer their learning to these

partner institutions in India.

The MHRD was to coordinate the technical institutions namely

IIT-Guwahati and National Institute of Technology-Silchar

whereas funds to remaining three universities including TU were

to be released by UGC.QAI project details were agreed by these

five partner institutions in November 2013 and accordingly TU

submitted its financial proposals to UGC. University Grant

Commission (UGC) released the first year grant on 31st March

2014. Audit noted that the time of release of money by UGC, the

project was yet to be notified/formally approved by MHRD and

remains un-notified till (September 2017) date of audit.

The activities under the scheme could not be started due to non-receipt of any guidelines from UGC about starting of the project. Thus, no expenditure has been incurred till date from the fund made available to the University. The University admits the fact that on certain earlier occasions, internal loans were taken from the fund to the Plan and Non-Plan Account to support the activities under plan and non-plan, particularly when sanctioned UGC grants were not released on time to sustain such activities. The loans were subsequently recouped on immediate basis as and when Plan/Non-Plan grants were made available to the University. These transactions were duly accounted for in the books of account of the university and shown to audit. Audit may kindly take note of the fact that had the University taken any external loan from financial institutions to meet the shortfall in

Page 15 of 53

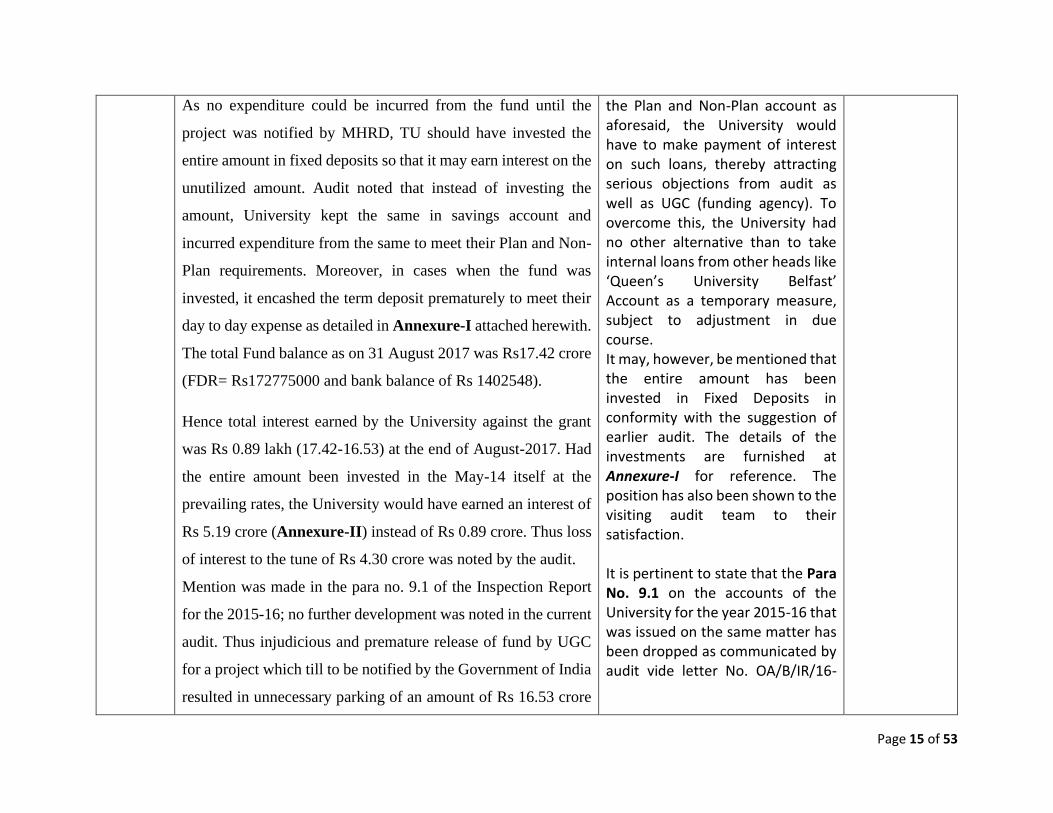

As no expenditure could be incurred from the fund until the

project was notified by MHRD, TU should have invested the

entire amount in fixed deposits so that it may earn interest on the

unutilized amount. Audit noted that instead of investing the

amount, University kept the same in savings account and

incurred expenditure from the same to meet their Plan and Non-

Plan requirements. Moreover, in cases when the fund was

invested, it encashed the term deposit prematurely to meet their

day to day expense as detailed in Annexure-I attached herewith.

The total Fund balance as on 31 August 2017 was Rs17.42 crore

(FDR= Rs172775000 and bank balance of Rs 1402548).

Hence total interest earned by the University against the grant

was Rs 0.89 lakh (17.42-16.53) at the end of August-2017. Had

the entire amount been invested in the May-14 itself at the

prevailing rates, the University would have earned an interest of

Rs 5.19 crore (Annexure-II) instead of Rs 0.89 crore. Thus loss

of interest to the tune of Rs 4.30 crore was noted by the audit.

Mention was made in the para no. 9.1 of the Inspection Report

for the 2015-16; no further development was noted in the current

audit. Thus injudicious and premature release of fund by UGC

for a project which till to be notified by the Government of India

resulted in unnecessary parking of an amount of Rs 16.53 crore

the Plan and Non-Plan account as aforesaid, the University would have to make payment of interest on such loans, thereby attracting serious objections from audit as well as UGC (funding agency). To overcome this, the University had no other alternative than to take internal loans from other heads like ‘Queen’s University Belfast’ Account as a temporary measure, subject to adjustment in due course. It may, however, be mentioned that the entire amount has been invested in Fixed Deposits in conformity with the suggestion of earlier audit. The details of the investments are furnished at Annexure-I for reference. The position has also been shown to the visiting audit team to their satisfaction. It is pertinent to state that the Para No. 9.1 on the accounts of the University for the year 2015-16 that was issued on the same matter has been dropped as communicated by audit vide letter No. OA/B/IR/16-

Page 16 of 53

with University for 41 months. Moreover, due to non investment

of the same in fixed deposits by resulted into loss of interest of

Rs 4.30 Crore. Besides objectives of the project could not be

achieved due to non-notification of the same by MHRD.

Reply of the office is awaited in this regard.

17/Tezpur University/87/312 dated 14.11.2017. Considering the action taken by the university in compliance with the suggestion of audit, the para may please be dropped.

2016-17

Para 1

Part IIB

Excess expenditure of Rs. 21.09 lakh due to irregular

purchase of Rs. 88.21 lakh towards procurement of

computer peripherals

As per Fundamental principles of public buying (Rule137 of

GFR 2005), the offer for public procurement should be invited

following a fair, transparent and reasonable procedure and at

each stage of procurement the concerned procuring authority

must place on record, in precise terms, the considerations which

weighed with it while taking the procurement decision. Further

Rule 160 of GFR 2005, states that criteria for evaluating the bids

on a common platform and subsequent award of the contract to

the lowest responsive bidder should be clearly indicated in the

bidding documents. Bids received should be evaluated in terms

of the conditions already incorporated in the bidding documents;

no new condition which was not incorporated in the bidding

documents should be brought in for evaluation of the bids.

The subject items were procured against a Quotation Notice vide No. TU/11-24/Pur/Qtn/2016-17/1256 dated 04.07.2017, which was floated in our website. As per the term and condition No. 16 of the said notice, it was categorically mentioned that the University could impose any other terms and conditions, which were not originally incorporated, as may be deemed fit and proper while approving the rates. Hence, rejection of the lowest quoted rate(s) on duly recorded genuine ground may be covered by the said condition No. 16. Copy of the Quotation may be seen at Annexture-II. As per the above quotation notice, the quotes of 08 firms, viz. 1)

Page 17 of 53

Scrutiny of records revealed that during the year 2016-17, in

respect of 42 purchase orders (Annexure-III), Tezpur

University purchased computer peripherals, amounting to Rs

82.21 Lakh from supplier other than the lowest bidder. Out of

these 42 cases, in 19 cases (Annexure-IV), Tezpur University

did not approve the lowest bidder stating that the brand (ACER)

offered by lowest bidder has poor service records, and hence was

not considered for purchase. In respect of rest 23 cases

(Annexure-V), no justification was offered for placing the

orders on bidders other than lowest bidders. The purchase of

computer peripherals from other than lowest bidder resulted into

not only irregular purchase of computer peripherals amounting

to Rs 88.21 Lakh but also led to excess expenditure of 21.09

Lakh. The rejection of bids of the lowest bidder on the ground

that this belong to a particular brand was in violation of GFR

provisions which states that bids received should be evaluated in

terms of the conditions already incorporated in the bidding

documents; no new condition which was not incorporated in the

bidding documents should be brought in for evaluation of the

bids.

Further scrutiny of records revealed that out of these 42 purchase

orders, in 14 cases (Annexure-VI), the purchase orders

Sukumar System Service, 2) Eastern Technology Group, 3) BMG Informatics (P) Ltd., 4) B2B Systems and Solutions, 5) Milennium Automation & Systems Ltd., 6) Cineworth Sales & Services, 7) Converge Systems & Services Pvt. Ltd., and 8) Hue Service Ptv. Ltd. were placed to the Central Tender and Purchase Committee for evaluating and approving the rates. After evaluation of the bids, the committee recommended the rates quoted by M/s Converge Systems & Services Pvt. Ltd., which was eventually approved by the competent authority. Although it is the general norm to approve L1 rates, sometimes the L2 or L3 rates are also considered and approved based on the quality of the respective items, specification-matching and durability. Our previous experience of procuring low cost brands was not satisfactory due to their frequent breakdown and lesser durability and therefore, in the instant case, the committee recommended other brands.

Page 18 of 53

amounting to Rs 31.73 Lakh were placed on the suppliers who

had not participated in the tender process. No justification was

found in record for placing order to suppliers who had not

participated in bidding process.

Reply of the office is awaited in this regard.

As regards the observations of audit mentioned in Annexure-III, IV, V and VI of the report, the remarks-wise clarifications are furnished at Annexure-III for kind perusal and consideration. All the purchase orders in question are enclosed at Annexure-IV.

2016-17

Para 3,

Part IIB

Physical verification of equipment costing Rs 5.80 Crore

acquired out of project grants-Observation thereon.

Tezpur University conducts research work under various

projects. The grants are released by various funding agencies to

TU, which keeps the funds in a designated bank account. The

expenditure on the projects (recurring as well as non-recurring)

are sanctioned by TU as per the proposals of respective Principal

Investigator. As per the terms and conditions of the grant

sanctioning letter, provisions of GFR need to be adhered to for

utilizing the grants. Further, TU was required to maintain a

register of assets acquired wholly or substantially out of these

grants. It was further provided that these assets shall not be

disposed or encumbered or utilized for the purpose other than

those for which the grants were given without taking proper

sanction of the funding agency, and should at any time the

university ceased to function, such assets shall revert back to the

funding agency. Rule 215 of GFR also provided that on

completion of the projects or schemes and the receipt of technical

and financial reports, the funding agency shall decide and

communicate to the implementing agency whether the assets

should be returned, sold or retained by the implementing agency.

It is obvious that the implementing agency (TU) is the custodian

of the assets acquired out of these grants until a final decision

regarding their utilization is taken by the funding agency.

University has a decentralized

process of purchase Department

wise, Principal Investigator (PI)

wise for the projects for smooth,

quick and accountable purpose. The

Extra Mural Funding Agencies are

having the ownership of the Fixed

Assets purchased out of the project

grants. Any fixed assets purchased

out of the project grants in the

University are certainly entered into

the Fixed Assets Register of the

Departments/PI’s Office. No

payment is entertained by the

University unless the equipment

purchased from the project grants

are satisfactorily installed and

entered into the Fixed Assets

Register.

The University is making physical

verification of all fixed assets

Para settled

Page 19 of 53

Further, Rule 192 of GFR 2005 stipulates that fixed assets should

be verified at least once in a year and the outcome of the

verification should be recorded in the corresponding register.

Discrepancies, if any, shall be promptly investigated and brought

to account.

Test check of projects closed/completed during last five years

(2012-13 to 2016-17) revealed that neither registers of Assets

(equipments) for the projects have been maintained nor any

physical verification report of the same was produced to audit.

As a result the actual existence assets valuing of Rs 5.80 Crore

cannot be confirmed by audit.

including project fixed assets every

year as per the provision of the Rule

213 of GFRs 2017. The observation

of the audit that “neither registers of

Assets (equipment) for the projects

have been maintained nor any

physical verification report of the

same was produced to audit and as a

result the actual existence assets

valuing of Rs 5.80 Crore cannot be

confirmed by audit” is not correct.

The audit may verify the above in

their next inspection and drop the

para.

2016-17

Para 4,

Part IIB

Blockade of fund of Rs 3.76 crore in addition to loss of

interest of Rs 15.04 lakh towards Campus Wi-Fi project

As per Rule 159 of GFR 2005, payment to supplier should be

released only after the services have been rendered or supplies

made. However, if it becomes necessary to make advance

payments against fabrication contracts, turn-key contracts etc,

the advance payments should not exceed forty percent of the

contract value for contracts placed to government agency or a

Public Sector Undertaking. Ministries or Departments of the

Central Government may relax, in consultation with their

Financial Advisers concerned, the ceilings mentioned above.

Scrutiny of records revealed that Project Approval Board (PAB)

of National Mission on Education through Information and

Communication Technology under MHRD sanctioned Rs 9.40

Crore for establishment of Campus Wi-Fi in Tezpur University

(TU). In August 2016, a Memorandum of Understanding (MOU)

was signed among the Department of Higher Education MHRD,

University Grants Commission

(UGC) in their D.O. No. F.6-2/2016

(CU/DU), dated 16.8.2016 (copy at

Annexure A) intimated that 38

(thirty-eight) Central Universities

under the Campus Connect

Programme of NMEICT have to

sign an agreement among the

MHRD, NICSI, UGC and the

participating Central Universities

for providing Wi-fi facility in the

University campus. Accordingly,

the Tezpur University along with

other 37 Central Universities has

Para settled.

Page 20 of 53

University Grant Commission (UGC), National Informatics

Centre Services Incorporated (NICSI), Ministry of Electronics &

Information Technology and 38 Central Universities including

TU for establishment of Campus Wi-Fi. As per the terms and

condition of the MOU, advance payment of 80% of the project

value was to be released by the concerned university to NICSI.

TU received a sum of Rs 7.52 Crore (80% of Campus Wi-Fi

project) from UGC in September 2016 and it released the entire

amount to NICSI in same month.

Scrutiny of records revealed that despite lapse of one year from

the release of 80 percent of agreed amount, the project is yet to

be completed till (September 2017). It is observed that the MOU

entered into was not in conformity of Rule 159 of GFR 2005, as

it allowed 80% release of fund in advance as against GFR

prescribed maximum ceiling of 40% .Had TU released 40

percent as advance, and kept balance amount in its savings

account, it would earned interest of 15.04 Lakh (3.76*4/100) on

the same. The actions of TU not only led to blockade of fund of

Rs. 3.76 crore for one year, it also led to loss of interest of Rs.

15.04 Lakh.

signed an MoU among four-parties,

viz., MHRD, NICSI, UGC and the

participating Central Universities

including Tezpur University as per

the terms and conditions approved

by the MHRD and UGC. The copy

of the signed MoU is at Annexure B.

The UGC in their D.O. letter No.

F.6-2/2016(CU), dated 24.8.2016

(copy at Annexure C) also intimated

that as UGC has already released

grant, the Tezpur University is

requested to transfer funds to the

NICSI as per the provisions of the

MoU. It is for the information that as

per the Clause No. 10 (Payment

Schedule) of MoU, advance

payment of 80% including Govt.

levies of the NICSI PI value will be

released by the University

concerned as demanded by NICSI.

In case final price is lower than the

estimated price, then NICSI will

refund excess amount paid to it by

the University concerned

immediately on its own. The

remaining amount, if applicable,

based on the actual cost will be paid

after the successful installation and

commissioning.

MHRD sanctioned Rs 9.40 Crore

for establishment of Campus Wi-Fi

in Tezpur University (TU) payable

Page 21 of 53

to NICSI. Accordingly, the UGC in

their release order No. F.57-

15/2016(CU), dated 30.8.2016

(copy at Annexure D) released 80%

of the sanctioned amount, i.e., Rs.

751.66 lakh to the Tezpur

University for releasing the said

fund to NICSI as laid down in MoU.

Accordingly, Tezpur University has

released the amount in advance to

NICSI. As the advance payment was

made in conformity with the orders

of MHRD/UGC and as per the terms

& conditions of the MoU signed by

MHRD, UGC, NICSI and Tezpur

University, the para may kindly be

treated as settled.

2016-17

Para 5,

Part IIB

Irregular Pay protection: Observation thereon.

Sri Chandan Goswami (Assistant Professor) joined Tezpur

University on the post of lecturer on 27.12.1995 in the pay scale

of Rs 2200-75-2800-100-4000 and his pay was fixed at the

minimum of the scale at Rs. 2200. Before joining TU, Sri

Goswami was serving at ANJ Food & Beverages Private Limited

and was drawing Basic pay of Rs 4000 per month and HRA Rs

3000 per month. Based on an application made by Sri Goswami

to protect his basic pay of previous post, Board of Management

(BoM) in September 1996, resolved to protect the pay of Sri

Goswami as per the pay fixation rules of the university.

Accordingly, in terms of further BoM resolution No. B.97/2/35,

Tezpur University refixed the pay of Sri Goswami at Rs 2800 per

month in the pay scale of Rs 2200-75-2800-100-4000 with effect

Based on the observation of audit,

the pay protection provided to Dr.

Chandan Goswami, Department of

Business Administration on the date

of joining as Lecturer was

withdrawn and the pay has been re-

fixed by the University. In this

regard, the revised pay fixation

order without pay protection with

effect from 27.12.1995 till date has

been issued vide Order No. F.02-

97/II(E)/1536-A dated 11.7.2019

(copy of which is enclosed at

Further reply furnished to the Director, Audit vide letter No. TU/FIN/IR/2016-17/2435 ,dated 30 August 2019.

Page 22 of 53

from the date of his joining in the university i.e 27.12.1995.The

basic pay of Sri Goswami was revised in terms of fifth pay

commission recommendation and was refixed at Rs 8550 per

month with effect from January 1996. He has been getting

regular increments thereafter.

As per the (BoM) resolution No. B.96/3/2.2 of September 1996,

the pay of Sri Goswami was to be protected as per the pay

fixation rules of the University. However, TU could not provide

any rules in terms of which the pay drawn by an employee in a

private sector job is to be protected at the time of appointment in

University. Pay fixation rules of Government of India also does

not provide for protection of pay drawn in private sector. It was

observed that the initial pay fixation of Sri Goswami was not as

per the rules, The pay of Sri Goswami need to be revised (Annex

VI A). Due drawn statement need to be prepared and excess

payments made so far need to recovered.

Annexure -A). Based on the above

Office order, a Due-Drawn

Statement has been prepared by the

Finance Department (Annexure-B)

and recovery of the excess payment

of Rs. 1,17,132/- needs to be

recovered in 18 installments.

The recovery will be started

commencing from the month of

August 2019. Therefore, the para

may be treated as settled.

2016-17

Para 8,

Part IIB

Purchase of computer peripherals and equipment of Rs 1.59

Crore made without advertisement in newspaper.

As per Fundamental principles of public buying (Rule137 of

GFR 2005), the offer for public procurement should be invited

following a fair, transparent and reasonable procedure and at

each stage of procurement the concerned procuring authority

must place on record, in precise terms, the considerations which

weighed with it while taking the procurement decision. Further,

Rule 150 prescribes that for purchase of goods having estimated

value of Rs. 25 lakh (Rupees Twenty Five Lakh) and above,

invitation to tenders by advertisement should be used.

Advertisement in such case should be given in the Indian Trade

Journal (ITJ), published by the Director General of Commercial

Intelligence and Statistics, Kolkata and at least in one national

daily having wide circulation.

The University is procuring the

computer peripherals and general

equipment by advertising in one

local daily of wide publicity and

also uploading the advertisement in

the website of the University to

enable the intending parties all over

the world get access to the

advertisement. Specific

advertisements in the National

Dailies are generally not adhered to

considering the longer time and

higher costs involved in such

Para settled.

Page 23 of 53

Scrutiny of records revealed that during the year 2016-17,

Tezpur University purchased computer peripherals amounting to

Rs 88.21 Lakh (Annexure-VIII), by placing orders to approved

suppliers at agreed rates. The agreed rates were arrived at by

inviting open tenders advertised only on university’s website.

It was also noticed that TU purchased equipments amounting to

Rs 76.88 Lakh ( vide supply order no. TU/11-15(Pur)/FPT/2016-

17/6034/6033/6032/ dtd. 31.03.2017) for department of Food

Engineering and Technology by inviting open tenders advertised

only on university’s website

It is evident that tenders for fixing the approved annual rate for

purchase of computer peripherals and for purchase of

equipments were neither advertised in Indian Trade Journal (ITJ)

nor in one national daily having wide circulation. Thus, the

purchases of computer peripherals and equipments worth Rs.

1.59 (0.82+0.77) Crore made by TU during the year 2016-17

were made in violation of GFR norms and hence irregular.

advertisements. The suggestion of

audit is however noted for future

compliance.

It may be stated that the University

has already registered itself with the

Govt. e-Marketing (GeM) portal so

as to enable itself procure necessary

goods and services by using the

facilities provided through the

portal. The position may be verified

by next audit during their

inspection.

Considering the clarification

furnished above and assurance for

compliance, the para may please

be dropped.

2016-17

Para 9,

Part IIB

Non-inclusion of Liquidated Damages (LD) clause in supply

orders led to non levy of LD on defaulting suppliers.

As per General principles for Contract (Rule 204 of GFR 2005)

all contracts shall contain a provision for recovery of Liquidated

damages for defaults on the part of the contractor.

It also provides for levy of liquidated damages for delayed

delivery of goods and further states that where deliveries are

accepted beyond the scheduled delivery date liquidated damages

have to levy on contract price as provided in the Contract.

Scrutiny of records revealed that during the year 2016-17,

Tezpur University purchased computer peripherals and

equipments amounting to Rs 54.53 Lakhs (Annexure-IX) which

were delivered beyond the stipulated date of delivery.

Equipments amounting to Rs 31.89 Lakh (Annexure-IX) are yet

The University is located in a remote

area and therefore, it sometimes

takes longer time for the

companies/firms to supply items to

the University. The University has

however taken note of the

suggestion of audit in this regard

and already ensured compliances of

the same.

In the year 2016-17, any clause of

Liquidity Damages was not

Para settled.

Page 24 of 53

to be delivered despite lapse of stipulated date of delivery.

However, TU could not initiate any action for imposition of LD

against defaulting suppliers as it failed to include the provision

for recovery of LD in the Supply orders.

incorporated in any of the Purchase

Orders issued by the University, as a

result of which University could not

be able to recover any LD from the

defaulting suppliers. However, as

suggested by audit, the University

has already incorporated a specific

clause of LD with the provision of

recovery from the defaulting

suppliers in each and every Purchase

Order issued by the University. This

may be verified by the audit in their

next inspection. As the Rule 225 of

GFRs 2017 is being followed by the

University at present in toto, the

para may be dropped.

2016-17

Para 10,

Part IIB

Excess expenditure of Rs 4.60 lakh towards Security services.

Tezpur University entered into the agreement with M/s North

Eastern Security Service (NESS), for providing round the clock

security service of Tezpur University (TU) Campus with effect

from 01/10/2014 for a period of two years. The contract was

extended for one more year till 31/09/2017. The intial contract

stipulated depoyment of 99 Security Guard which was increased

time to time as per the requirement of TU.

Per man per month salary of a security guard was calculated by

paying for 26 days at the minimum rate of wages prescribed. To

pay for the leave reserve of 4 days, one sixth of the mandays paid

for (26/6) was further added to arrive at the salary per month. As

security services were to be provided round the clock for all days

of a month, security agency deployed additional manpower to

provide security round the clock. As payment towards leave

The University, while

acknowledging the suggestion of

audit in this regard, has already

taken necessary action and has been

making payment of wages for 26

days in a month to all the outsourced

manpower. The compliance of the

University may be verified by audit

during their next inspection.

Also, at present, the University has

engaged security personnel from the

State Home Guards for the purpose

of its campus security and the

Para settled.

Page 25 of 53

salary was already built into the per man per month salary so

arrived, the monthly payment towards deployment of security

guards must match with the actual deployment of security

guards.

Scrutiny of records revealed that the actual deployment of

mandays was less than the mandays paid for. During the period

from April 2016 to March 2017, it was noticed that the deficit in

actual deployment of manpower by 1001 mandays (Annexure-

X). Had TU assessed the actual requirement of manpower before

fixing the manpower to be engaged, the excess payment of Rs

4.60 Lakh towards excess engagement of manpower might have

been avoided.

payment is being made as per the

instructions issued by the State

Government in this regard from time

to time.

As the University at present

discontinued the private security

agency for providing watch and

ward in the campus and engaged

State Home Guards as per the terms

and conditions of the Govt. of

Assam including the Duty

Allowance etc. of the Home Guards,

the para may please be treated as

settled.

2016-17

Para 11,

Part IIB

Excess payment of Rs 1.64 Lakh towards housekeeping

service.

Tezpur University entered into the agreement with Sulabh

International Social Service Organization (SISSO), for providing

housekeeping service at Tezpur University (TU) Campus with

effect from 01/08/2015 for a period of two years. As per the

terms and condition of the agreement, the daily wages of

Volunteers and Supervisors were to be regulated in terms of

relevant Govt. of India notifications (Rate for workers prescribed

by Ministry of Labour and Employment).In terms of Notification

No. 1/13(6)/2016-LS-II dated 31.03.2016 of Ministry of Labour

and Employment, the daily rate of wages for workers involved

in sweeping and cleaning activities in C area cities was fixed at

Rs 246 per day. This rate was applicable for all workers involved

in sweeping and cleaning activities irrespective of their skill

In compliance with the observation

of audit, the excess payment made to

M/s Sulabh International Social

Service Organization (SISSO) up to

August 2019 has been worked out,

which stands at Rs. 4,45,560/-.

The University has already issued

necessary order vide No. TU/15-

10/Estate/House

Keeping/2019/2682 dated

13.9.2019 for recovery of the

aforesaid excess payment in 04

(four) installments. Based on the

administrative order, recovery has

Page 26 of 53

level as sweeping and cleaning activities do not require any

specialized skills.

Test check of vouchers and relevant documents revealed that in

respect of Supervisors and Supervisors In-charge, M/s SISSO

raised bills at higher than the permissible rates by applying the

rates of highly skilled and skilled workers engaged in

construction and maintenance activities of roads and runways,

which was not in order as the worker are engaged in cleaning

activities and not in construction and maintenance activities of

roads and runways. The application of higher rates resulted into

excess payment of Rs.1.64 Lakh (Annexure-XI) towards

housekeeping service.

already been made @ Rs. 1,11,390/-

from the bills of M/s SISSO for the

months of August 2019 and

September 2019, vide Voucher No.

2019-20/9638 dated 23.9.2019 and

Voucher No. 2019-20/10037 dated

03.10.2019, respectively. The

balance amount of Rs. 2,22,780/-

is being recovered from the bills of

M/s SISSO for the month of October

2019 and September 2019.

Taking note of the compliance of the

University in this regard, the para

may be treated as settled.

2016-17

Para 12,

Part IIB

Irregular expenditure of Rs 8.79 Lakh towards purchase of

mobile phones and Desktops and Laptops for establishment

of Centre for Endangered Languages.

As per UNESCO report-Atlas of the World’s Languages in

Danger (2009)-out of the approximately 6000 existing languages

in the world more than 2,500 are under threat of imminent

extinction. As for Indian languages, 196 are currently

endangered according to the report, and most of these languages

are located in North-East India. In the context, Tezpur University

(TU) in May 2013 sent a proposal to University Grants

Commission (UGC) for establishment of a centre for

Endangered Languages of North East as an effective agency for

preserving and promoting the endangered languages of the

region. In the said proposal TU had sent a financial estimate of

Rs 12.07 Crore for five years for establishment of the centre,

against which UGC in April 2014 informed TU that they would

recommend Rs 6 crore for the establishment of the centre and

asked TU to re-work the budget and submit it to the UGC before

As per the revised proposal submitted to UGC, the requirement under Non-Recurring items including Laptops, Desktops and mobile phones were provided on tentative basis based on estimation. But after actual appointments were made in the Centre, the requirement increased. To make it clear, 03 Assistant Professors, 03 Research Scholars, 08 Field Assistants, 01 Technical Assistant and 01 UDC were appointed in

Page 27 of 53

availing the grant. Accordingly, TU sent a revised budget of Rs

6 crore in September 2014 out of which Rs 3 Crore was proposed

under Non-recurring head and subsequently UGC on August

2015 sanctioned Rs 3 crore as first installment towards

establishment of the centre, out of which Rs 1.69 Crore was

sanctioned under Non-recurring head.

During test check of records it was observed that TU had

purchased 15 nos. of mobile phones of Rs 2.38 Lakh under non-

recurring (Equipment) head under the above mentioned project.

However as per Budget proposal of September 2014 which was

sent to UGC, under the non-recurring head there was no proposal

for purchase of mobile phones. Moreover as per budget proposal

there was provision of purchase of 20 nos. of Computer/desktop,

6 nos. of high end laptop for Rs 16 Lakh against which TU

purchased 23 Nos. of Desktop and 16 Nos. of Laptop of Rs 22.41

Lakh. Hence Audit is in opinion that the purchase of mobile

phones of Rs 2.38 Lakh and excess expenditure of Rs 6.41

(22.41-16.00) lakh towards purchase of desktop and laptops

were irregular as it was not as per Sanctioned non-recurring

Budget.

addition to the Coordinator of the Centre. Apart from that, a phonetic lab with 20-seater capacity was in place. Also, there was requirement of Desktops for the office of the Centre. The purchases of the items in question were made based on the actual requirement of the Centre and thus, there was deviation in the number of items incorporated in the revised proposal and the actual number procured. Based on this, audit may consider dropping the para.

2016-17

Para 13,

Part IIB

Irregular reimbursement of airfare to the tune of Rs 7.56

lakh including excess expenditure of Rs 0.36 lakh towards

handling charges.

In terms of Govt. of India, Ministry of Finance O.M.

No.F/19024/1/2009.E.IV dated 16th September 2010, all travel

both domestic and international where the Government of India

bears the cost of air passage, the official concerned may travel

only by Air India. Further, In terms of Govt. of India, Ministry

of Finance O.M. No.19024/1/2009-E.IV dated 7 June 2016

stated that in respect of individual cases of Autonomous bodies,

the financial advisers of the concerned ministry/Department will

accord exemption for air travel by airlines other than Air India.

In compliance with the observation of audit, the University has already issued necessary guidelines making it mandatory for the employees to book air tickets through the authorized travel agents only. The compliance in this regard may be verified during the next audit.

Page 28 of 53

Accordingly, the officials entitled to travel by air were required

to travel only by Air India for official tours. As per the

Guidelines of GOI order No. 19024/1/2009-E.IV dated the 16th

September, 2010 the Air Tickets for official tours may be

purchased directly from Airlines (at Booking counters/Website

of Airlines) or by utilizing the services of Authorized Travel

Agents viz. M/s Balmer Lawrie & Company, M/s Ashok

Travels& Tours.

During test check of voucher it was observed that Tezpur

University did not adhere to the Government orders and

purchased air tickets from the unauthorized travel agent. Further

scrutiny revealed that the University not only paid air fare to

agent but also handling charges (@5%) on the ticket prices. This

resulted in irregular expenditure of Rs 7.56 lakh including excess

expenditure of Rs 0.36 Lakh (Annexure-XII) towards handling

charges. Despite mention of similar observation in the Inspection

Report for the year 2015-16, Tezpur University did not initiate

corrective steps.

Considering the compliance of the suggestion of audit vis-à-vis the standing Govt. of India guidelines, the para may please be dropped.

2016-17

Para 14,

Part IIB

Irregular reimbursement of LTC of Rs. 2.15 lakhs:

Observation thereof.

As per GID (12) below Rule 12 of LTC Rule, Air journey by

non-entitled officers (both national and private airlines) between

places connected by train is allowed. However, as per the O.M.

No.31011/5/2014-Estt (A.IV) dated 19 June 2014 read with even

No. dated 23 September 2015 and dated 11 January 2016 of

Government of India, Ministry of Personnel, Department of

Personnel and Training, in all cases whenever a Government

employees travels by air, he/she is required to book air tickets

either directly through the airlines (booking counters, website of

airlines) or by utilizing the services of Authorized Travel Agents

viz. M/s Balmer Lawrie and Company, M/s. Ashok Travels and

Tours and IRCTC while undertaking LTC journey(s). It further

For the officers who are not entitled by air, their claims have been regulated by making reimbursement of the travel cost restricted to the fare of the entitled class by train. As per the standing Govt. of India guidelines, mandatory travel by Air India as well as booking of air tickets through authorized travel agencies has not been made applicable by

Page 29 of 53

provided that, in no case the booking of tickets through any other

agency, other than specified above, is permitted.

Test check of records (Bill/ vouchers), however, disclosed that

the Tezpur University in contrary to the rule provision ibid, had

reimbursed the LTC concession in full to its employees those are

eligible to travel by air and restricted to the entitled class for the

employees those are not eligible to travel by air even they have

purchased the air tickets from unauthorized agencies such as

Yatra.com, Makemytrip, Indian Air Travel, Cleartrip etc. and

also those who performed air journey by private airlines while

availing LTC thereby resulting in inadmissible payment to that

extant towards LTC as detailed in the Annexure –XIII.

them. As regards travel by the entitled officers are concerned, reply has been furnished against Para 13 ibid. In view of the clarifications furnished above, the para may please be dropped.

2017-18

Para 2.1,

Part-IIA

Penal interest of ₹78.89 Lakh accumulated on unspent grants

refundable to University Grants Commission. During XI Plan (from 2007-08 to 2011-12), Tezpur University

received a total grant of ₹5.50 crore and ₹2.90 crore towards Merged

Scheme and Fellowship to Non-Net M.Phil/Ph.D respectively under

General Development Scheme. The University utilised ₹4.63 crore and

₹2.19 crore against the grants respectively leaving unspent grants

amounting to ₹86.68 lakh and ₹71.10 lakh in respect of Merged

Scheme and Fellowship to Non-NET M.Phil/Ph.D respectively at the

end of March 2013 (2012-13). In Utilisation Certificates prepared by

the university (April 2013), it was also mentioned that the unutilised

balances of ₹1.58 crore would be refundable to University Grants

Commission (UGC).

As per grant sanction letters, the University (grantee institution) shall

ensure the utilisation of grants-in-aid for which it is being

sanctioned/paid. In case of non-utilisation/ part-utilisation, simple

interest of the rate of Six (6) percent per annum as amended from time

to time on unutilised amount from the date of drawl to the date of

refund as per provisions contained in General Financial Rules of Govt.

of India will be charged. The rate was revised to 10 percent p. a. from

2008-09.

However, the University being unable to utilise the grant fully, failed

to refund the unutilised grant amounting to ₹1.58 crore to UGC till date

The University has already submitted the XI Plan (01.4.2007-31.3.2012) accounts to the University Grants Commission (hereinafter referred to as UGC) which is in the process of settlement. It is the usual practice on the part of UGC either to issue orders for refund of the unspent grant or to adjust the same from the grants to be released subsequently. After scrutinizing the XI Plan Utilization Certificates submitted by the University, UGC and communicated to refund the unspent/unutilized funds under Merged Schemes said amount and unutilized fund under Non_NET Ph.D. Fellowship. The refund of the unutilized is in process.

Page 30 of 53

of audit. Despite being pointed out by audit in its audit report of 2013

(Separate Audit Report for the period-2012-13), the University did not

refund the unutilised grant. In July 2018, Utilisation Certificates about

the two schemes, as sought for by UGC (March 2018), were furnished

for finalisation of Accounts of XIth Plan Grant.

The refundable unspent grant of ₹1.58 Crore in respect of the two

schemes (Merged Scheme and Fellowship to Non-NET M.Phil/Ph.D)

under XI Plan Grant lying with the University for 5 years attracted the

penal interest of ₹78.89 lakh (₹1.58 crore x 10% x 5 years).

2017-18

Para 2.2,

Part-IIA

Irregular award of Construction work and undue benefit to

contractor leading to excess expenditure of ₹76.74 lakh.

Tezpur University, in May 2012, decided to construct a ‘3 storied

RCC- Kendriya Vidyalaya Building’ by M/s Hi-tech

Construction (HTC) considering their previous experience of

completion of a similar building for Kendriya Vidyalaya at IIT,

Guwahati. Accordingly the work (G.F & F.F- 6298 Sq. M) was

tendered (July 2012) for an estimated amount of ₹9.18 crore by

incorporating a preference clause of an experience of completion

of a Kendriya Vidyalaya Building (KVB) during last five years

in addition to the main qualification criteria. The criteria fixed

for the work was that a Contractor shall be registered with Class-

I(A) APWD having an experience of completion of at least one

Central Educational Institutional Building valuing ₹10 crore or

more against single work order in any one year during last three

years and having annual turnover not less than ₹25 crore in any

one year during last three years was eligible for the receipt of this

tender documents. After evaluation of the bid documents, M/s

Hi-tech Construction (HTC) who quoted the rate 17.9% above

the tender value (L-IV) was selected as a successful bidder and

awarded the work at the rate of L-II (4.34 % above TV).

On scrutiny, it was noticed that M/s Arunoday Construction Co.

Pvt. Ltd (ACCPL) who was technically sound had quoted the

rates below 0.1 % of the tendered value and was the lowest. M/s

ACCPL had an experience of successful completion of three

The preference clause of having experience of completion of Kendriya Vidyalaya Building (KVB) during last five years was incorporated in the Tender Document of this particular work with a view to ensure that the Contractor, who is awarded the work, is well conversant with the technical specifications of such a project as per the KVS norms so as to safeguard the safely of the pupils. M/s Arunoday Construction Co. Pvt. Ltd (ACCPL), who was the lowest bidder, did not satisfy the aforesaid clause and hence, the work could not be awarded to them as per the terms and conditions of the Tender Document. Since the University was in urgent need of having a designated school building for the KV, it was considered to award the work to M/s Hi Tech Construction (HTC), the only Contractor who fulfilled all the terms

Page 31 of 53

similar works (academic buildings/educational institutional

building valuing ₹10 crore each) and also had a turnover of ₹25

crore. They also had two similar projects valuing ₹65 crore under

execution as on July 2012. ACCPL had also completed many

academic building works in the university by then. Further, the

experience of completion of a KVB shown by M/s HTC was

more than five years old.

The contractor to whom the work was to be awarded was decided

before invitation of the tender. Besides the preference clause as

mentioned in the tender was also not strictly adhered to as

evident from above. The work was however awarded at a higher

cost of ₹9.57 crore (at a price of L-II) to M/s HTC instead of M/s

ACCPL, the lowest tender (₹9.17 crore). It was awarded at a rate

which was 4.30 percent above the estimate/ tender value (4.40%

above L1). This led not only to providing of an undue benefit to

M/s HTC but also to an excess expenditure of ₹40.39 lakh

(₹957.15-₹916.76).

The University had, in October 2013, awarded the construction

of 2nd floor of KVB to M/s HTC with the same terms and

conditions at ₹5.51 crore (7.05% above the estimate- ₹5.15 cr)

without inviting a tender. The KVB (Ground, first and second

floor) was fully completed at a cost of ₹14.91 crore in August

2014. Final bill including the Ground and first floor was paid in

July 2015. Thus the work or construction of second floor of KVB

was awarded on nomination basis in violation of Central

Vigilance Commission’s circular No.18/12/12 dated 11/12/2012

at a cost which was higher than estimated cost by ₹36.35 lakh

(₹551.48-₹515.13).

Awarding the work ‘C/o Ground & 1st floors of KVB’ to a

particular contractor at 4.40 % above lowest tender without

strictly adhering to clauses in the NIT as well as awarding of

another work (2nd floor of KVB) irregularly (without inviting a

and conditions of the TD. Although the firm quoted 17.9% above the Tender Value (TV), the work was awarded at 4.34% above the TV, even below the rate quoted by the L2 bidder, after due negotiation. The University accepts the observation of audit that it deviated from the provisions of GFR-2005 and CVC guidelines by negotiating the rate with L4 bidder, however, such action of the University was in the best interest for smooth functioning of the KV where a dedicated school building was the need of the hour. With regard to awarding the extension work of the KV building to the same contractor without inviting any further tender as stated by audit, it may be clarified that Class XI of the school was to start from the year 2015 apart from starting additional sections of some of the existing classes. As per Kendriya Vidyalaya Sangathan (KVS) norm, KVs offer three sections in all classes, more so in Class XI and XII to offer HS classes in Arts, Science and Commerce. Hence, the Ground Floor and First Floor of the building were not sufficient to accommodate all the classes, labs, etc. Considering these aspects, construction of the Second Floor was awarded to the same contractor as per

Page 32 of 53

tender) as addendum to the earlier work at 7.06% above

estimated cost resulted in excess expenditure of ₹76. 74 lakh.

the already approved rate, and terms and conditions, as the 2nd Floor was an integral part of the complete KV Building. Awarding the additional work to the same contractor resulted in simultaneous progress of the GF, FF and 2nd Floor as well as ensured better coordination and structural integration of the entire building. The University was also apprehensive of the technical and administrative difficulties in executing the 2nd Floor of the same building through a different contractor and at the same time intended to get rid of the hassles and extra time involved in mobilization of the resources had the extension work of the 2nd Floor been awarded to a different contractor. The inherent justifications as stated above may be considered by audit with a pragmatic view and the para may please be dropped.

2017-18

Para 2.2,

Part-IIA

Undue benefit to M/s HTC by irregular award of HSS Building

worth ₹46 crore on Nomination basis at a higher price of ₹2.77

crore, besides, the irregular execution Building Works Committee (BWC) of Tezpur University (TU) in

December 2010, approved a proposal (Sept 2010) of O/o Dean, School

of Humanities and Social Sciences (SHSS) for ‘Construction of RCC

3-Storied Academic Building Complex for SHSS’ covering an area of

18689.70 sq. mt. at an estimated amount of ₹29.56 crore including

furniture, architect fee, contingency etc. (vide resolution

no.60/1013.04). The estimate was based on APWD SoR 2010-11 and

the period considered for completion was 24 months. Layout and

With regard to the observation of audit of not inviting NIT for this particular work, it may be clarified that initially there were uncertainty about the number of wings to be constructed as well as there was lack of clear cut plan

Page 33 of 53

Designs covering an area of about 18689 sq. mt. for the proposed

building was finalised. Subsequently, BWC, in February 2012,

approved a revised estimate (R.E) of ₹55crore for SHSS in an area of

25000 sq. mt. vide no. BC/62/12/3 (Part-I). The R.E of ₹55crore

included an estimate of ₹41.42 crore towards the Building Work

(works of civil, site development, electrical etc.,). Subsequently (28

September 2012), a preliminary work order (PWO) indicating a

scheduled period of completion of twelve months without mentioning

the value of the work was issued to a Contractor (M/s Hi-tech

construction). The work was awarded on a nomination basis (without

inviting a tender) violating Central Vigilance Commission (CVC)

Guidelines. In pursuance of PWO, an agreement was signed between

M/s HTC and TU. The work was awarded as an addendum to work of

“C/o Kendriya Vidyalaya Building” (KVB- G.F & F.F) which was

awarded to MIS HTC at 4.34 % above the Estimate (estimate was

APWD 2010-11). The work construction of (SHSS) was commenced

in October 2012 and was to be completed by October 2013.

Thereafter, a high-level committee constituted by the university took a

decision (November 2012) to allot the work to M/s Hi -tech

Construction (HTC). After a gap of six months from the allotment,

BWC in March 2013 recommended the same that the work would be

allotted at rates of the work of construction of KVB (G.F & F.F) to M/s

HTC on nomination basis. Accordingly, a final work order (July 2013)

was issued to M/s HTC by revising the contract value to ₹45.99 crore

and the time of completion to 24 months. Accordingly, agreement in

pursuance of Formal Work order was again signed.

Despite recommendation of the High-level Committee and BWC, the

work was awarded for ₹.45.99 crore (11 % above the estimate) instead

of ₹43.22 crore (4.34% above the estimates as calculated from

previous award of construction of KVB to the same contractor). Thus,

it was awarded at a price which was higher by ₹2.77 crore (6.40 %

more) than that awardable. The awardable work could have been at

₹43 .22 crore (4.34% above the estimates of ₹41.42 crore) as per the

rates/price of KVB work (G.F & F.F). The work was completed at a

cost of ₹39.61 crore in November 2015 (final bill was paid in April

allocation required for construction of the building. This was precisely the reason as to why the value of the work was not mentioned in the agreement as was signed by the University and the Contractor. Since NIT was not floated, the work was awarded as an addendum to the work of ‘Construction of KV Building’, as both these works were building projects having identical items of work and same rates were considered for determining the estimated value of this work. With regard to the comment of audit that the work was awarded at Rs. 45.99 crore (11 % above the estimate) instead of Rs. 43.22 crore (4.34% above the estimates as calculated from previous award of construction of KVB to the same contractor), it may be stated that a thorough examination of the estimates of both the works would reveal that although the rate of each identical item of work in both the estimates was same, the higher quantities under several items to be executed in case of the HSS building resulted in proportionate increase in the Work Order value in respect of the building in comparison to that of the KV building and thus, the difference in the overall percentage (11% compared

Page 34 of 53

2017) ignoring the work worth ₹17.57 crore and also executing the

excess work worth ₹10.27 crore.

Further, Civil Item work (BOQ) valuing ₹14.73 crore was not executed

whereas the work valuing ₹3.92 crore was executed under extra items.

Reasons for non-execution and excess-execution were not recorded.

Thus, the university had not only awarded the work worth ₹45.99 crore

on nomination basis in violation of CVC guidelines, but also provided

undue benefit to M/s HTC by awarding it at a higher price of ₹2.77

crore (6.40 % above the approved rate).

to 4.34%) as stated by audit was natural and there was no question of awarding the work at a higher price of Rs. 2.77 crore. The facts stated above may be verified by next audit for review and dropping the para.

2017-18

Para 2.4,

Part-IIB

Excess expenditure of ₹12.41 crore over grants received for

construction of Kendriya Vidyalaya. Ministry of Human Resource Development (MHRD), in December

2007 had introduced a scheme for expansion programme of Kendriya

Vidyalaya (KV) under Institutes of higher learning Sectors. KVS, in

October 2010, had advised Tezpur University (TU) to approach the

concerned C.E, CPWD, to assess the cost of construction of school

building and other developmental works for opening a Kendriya

Vidyalaya (KV) based upon the enrolment position of the students.

Accordingly, University Grants Commission sanctioned a (UGC)

grant of ₹1 crore under XI Plan during 2011-12 for opening a new KV

in the campus of the University. KVS, in June 2011 , further accorded

the proposal of opening a new permanent K.V. Building as per

specifications of the KVS under Institute of Higher Learning Sector

with classes I to VI (single section in each class). Subsequently, MoU

was signed between TU and KVS (May 2011) for opening of a project

school. KV was then started in temporary building. UGC had

subsequently released a grant of ₹1.5 crore under XII Plan in February

2015.

Initially (April 2009), the University decided to construct a ‘RCC-3