Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Submitted to : Sir Aamir

Submitted by : M.Arsalan Qureshi

Roll No :

Cost Accumulation

The use of an accounting system to collect and maintain a database of the expenses incurred by a business in the course of its operation.

The two main forms of cost accumulation are:

A job Order System

A Process Costing System

In process costing, materials, labor, and factory overhead costs are accumulated in the usual accounts, using normal cost accounting procedures. Costs are then analyzed by departments or processes and charged to departments by appropriate journal entries. The details involved in process costing are usually fewer than those in the job order costing, where accumulation of costs for many orders can become unwieldy.

Materials, Labor, and Factory Overhead Costs Accumulations

Procedures for Manufacture Cost Accumulation

The procedure for cost accumulation in job order costing.

Materials costs: In job order costing, materials requisitions are used and changes are made to order.

Labor costs: Time tickets sheet are used in job order costing to accumulate costs by jobs.

Factory overhead: Job cost requires the use of predetermined rates for charging overhead to orders.

Summarizing costs: Job order costs sheet is used to accumulate the cost of an order in job order costing.

Procedures for Manufacture Cost Accumulation

A job order system where direct materials , staffing and over heads are collected under assigned job number.

Job costing involves the calculation of cost involved in construction “job”or the manufacturing of goods done in discrete batches .These costs are recorded in ledger accounts throughout the life of the job or batch and are then summarized in the final trial balance before the preparing of the job cost or batch manufacturing statement.

Job Order System

Job order costingUseful for

Managing the costs of current jobs

Determining inventory costs

Providing data to predict future costs

Identifying likely profitable or unprofitable jobs

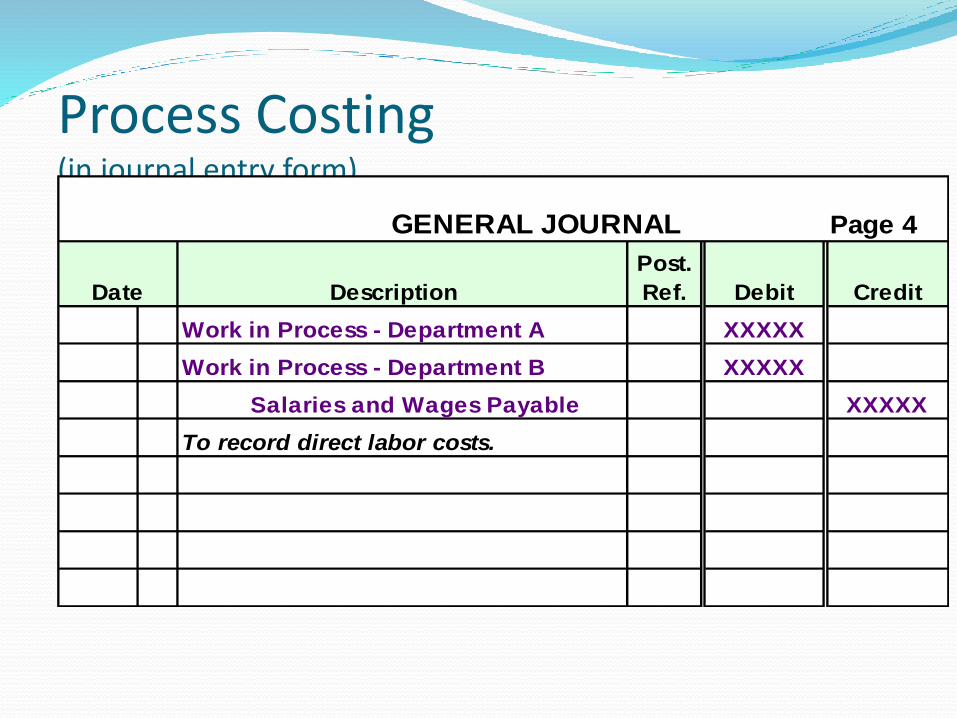

Process Costing(in journal entry form)

GENERAL JOURNAL Page 4

Date Description

Post.

Ref. Debit Credit

Work in Process - Department A XXXXX

Work in Process - Department B XXXXX

Salaries and Wages Payable XXXXX

To record direct labor costs.

Process costing is an accounting methodology that traces and accumulates direct costs, and allocates indirect costs of a manufacturing process. Costs are assigned to products, usually in a large batch, which might include an entire month's production. Eventually, costs have to be allocated to individual units of product.

It assigns average costs to each unit, and is the opposite extreme of Job costing which attempts to measure individual costs of production of each unit.

Process Costing

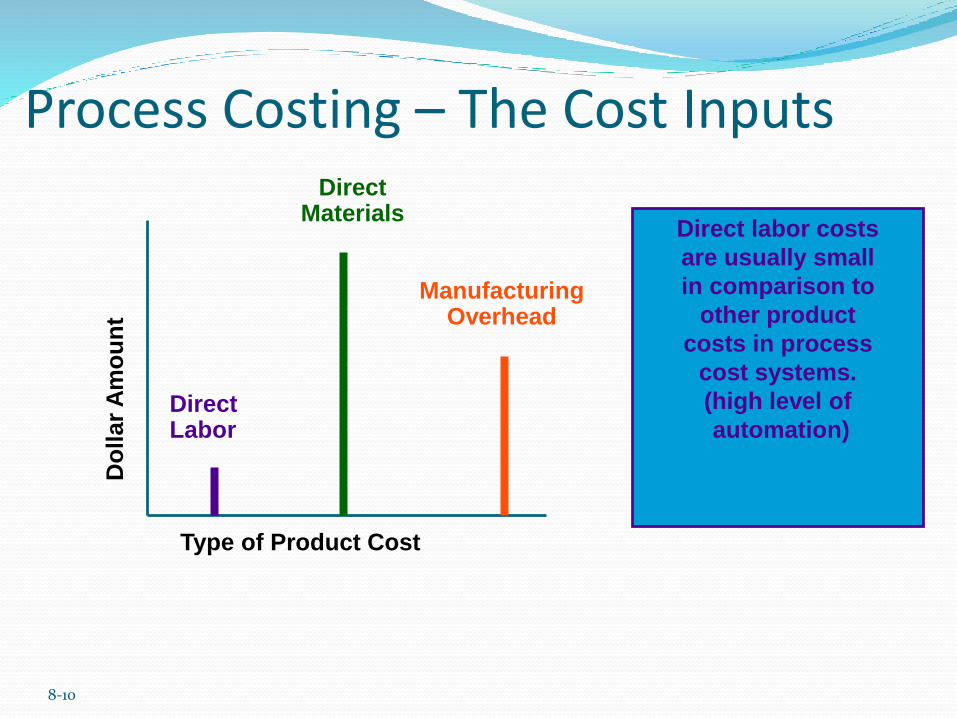

8-10

DirectMaterials

Type of Product Cost

Do

llar

Am

ou

nt

DirectLabor

ManufacturingOverhead

Direct labor costs

are usually small

in comparison to

other product

costs in process

cost systems.

(high level of

automation)

Process Costing – The Cost Inputs

8-11

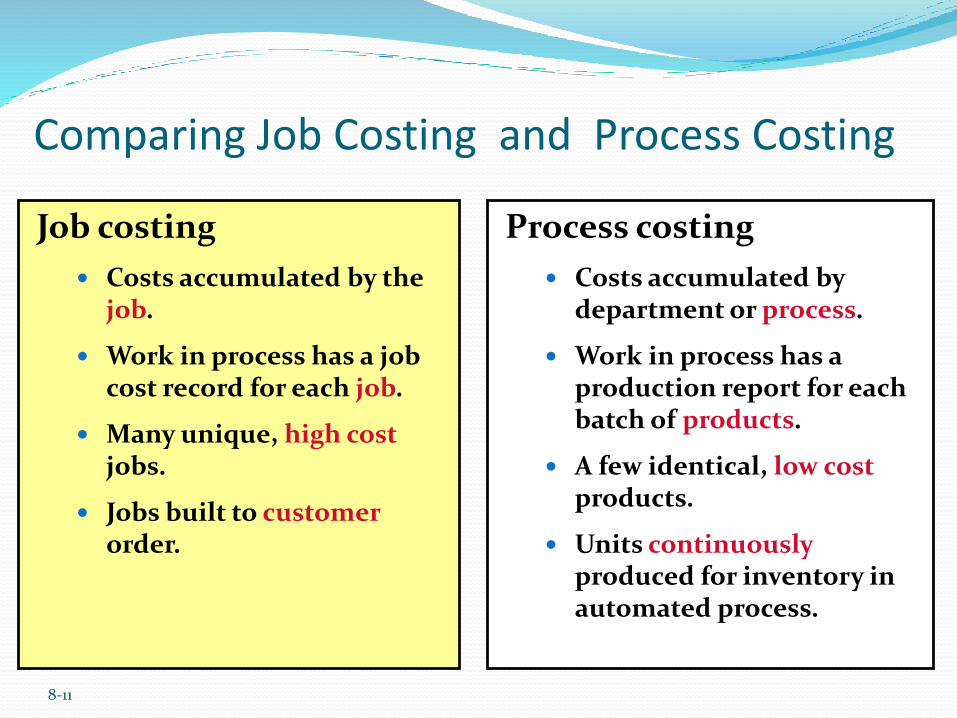

Job costing

Costs accumulated by thejob.

Work in process has a job cost record for each job.

Many unique, high cost jobs.

Jobs built to customerorder.

Process costing

Costs accumulated by department or process.

Work in process has a production report for each batch of products.

A few identical, low cost products.

Units continuouslyproduced for inventory in automated process.

Comparing Job Costing and Process Costing

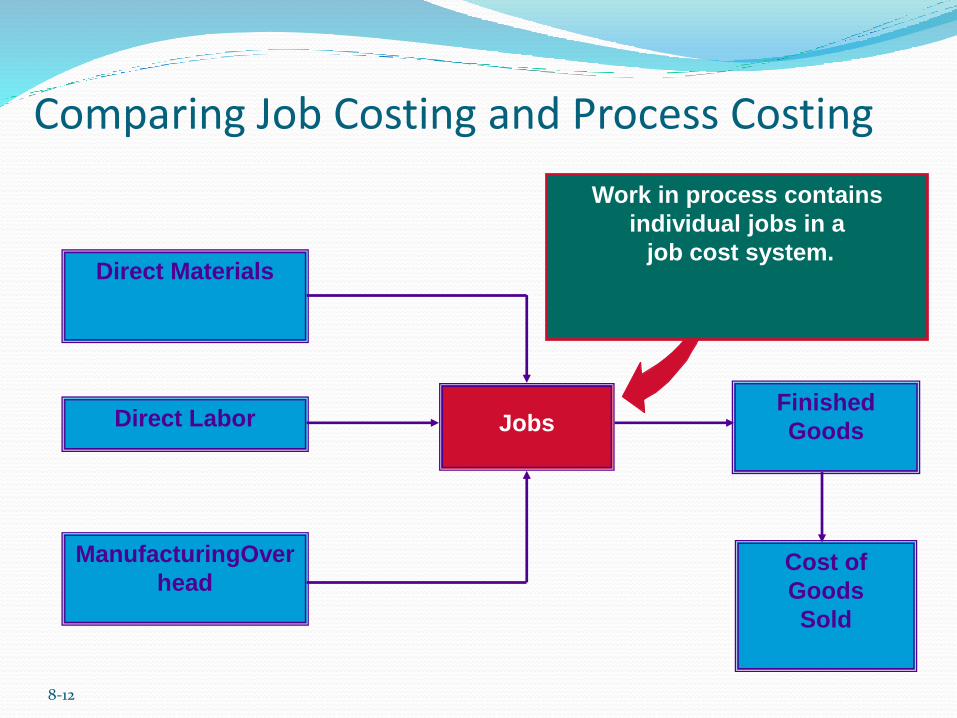

8-12

Work in process contains

individual jobs in a

job cost system.Direct Materials

Finished

Goods

Cost of

Goods

Sold

Direct Labor

ManufacturingOver

head

Jobs

Comparing Job Costing and Process Costing

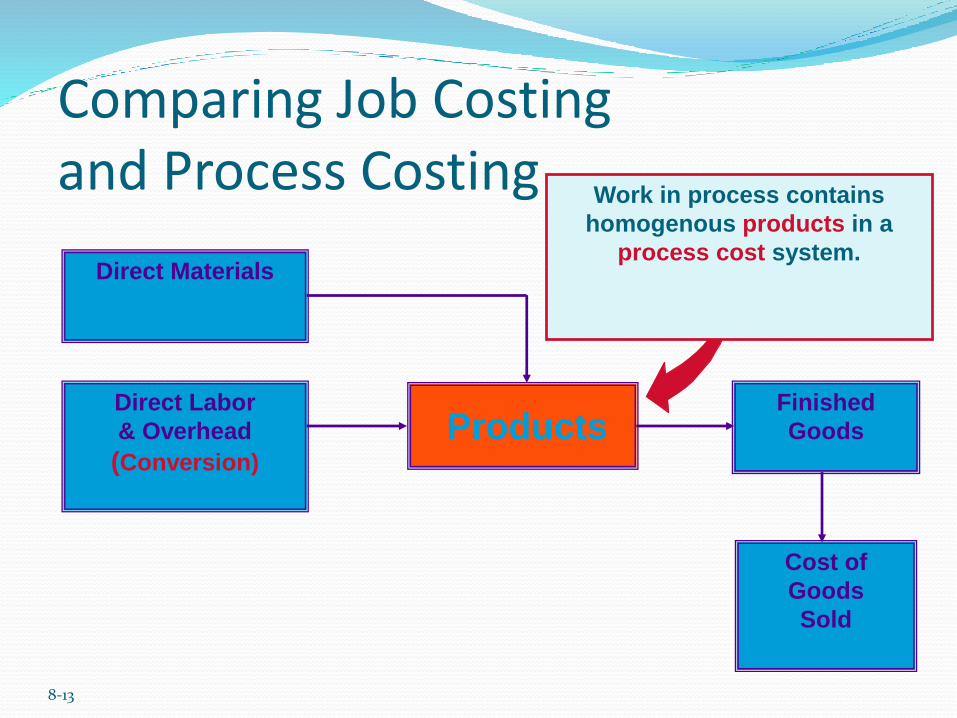

8-13

Finished

Goods

Cost of

Goods

Sold

Products

Work in process contains

homogenous products in a

process cost system.

Direct Labor

& Overhead

(Conversion)

Direct Materials

Comparing Job Costingand Process Costing

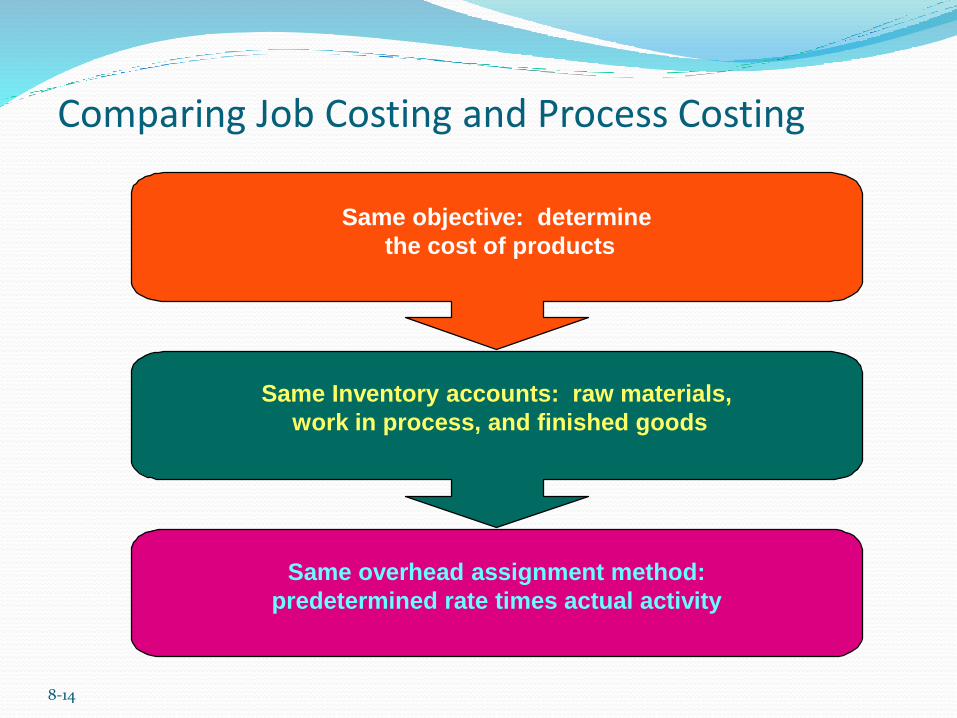

8-14

Same objective: determine

the cost of products

Same Inventory accounts: raw materials,

work in process, and finished goods

Same overhead assignment method:

predetermined rate times actual activity

Same objective: determine

the cost of products

Same Inventory accounts: raw materials,

work in process, and finished goods

Same overhead assignment method:

predetermined rate times actual activity

Comparing Job Costing and Process Costing

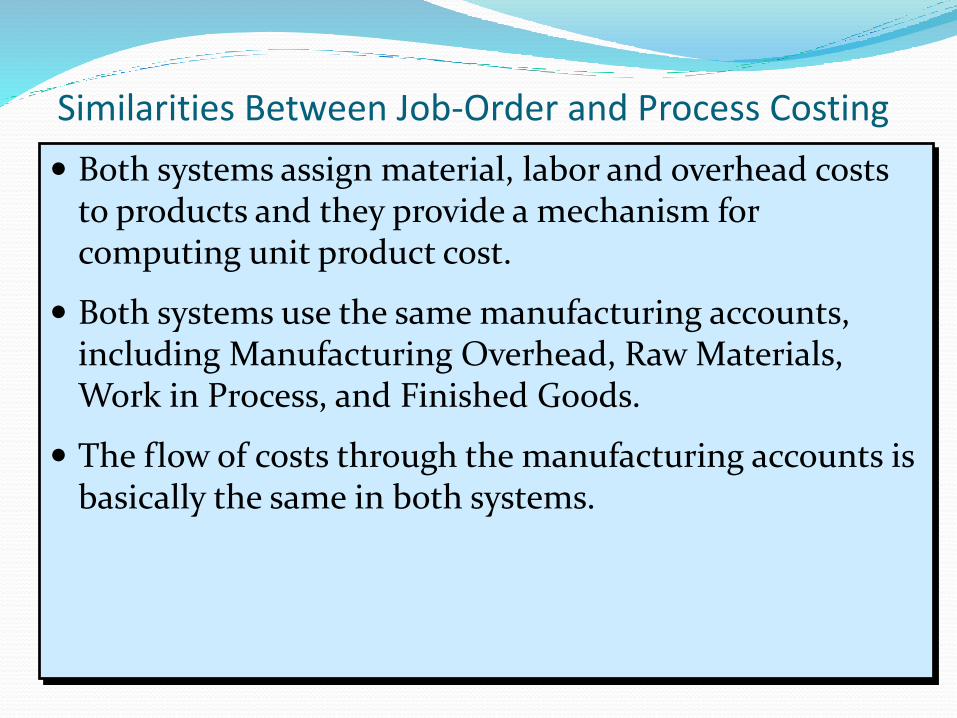

Similarities Between Job-Order and Process Costing

Both systems assign material, labor and overhead costs to products and they provide a mechanism for computing unit product cost.

Both systems use the same manufacturing accounts, including Manufacturing Overhead, Raw Materials, Work in Process, and Finished Goods.

The flow of costs through the manufacturing accounts is basically the same in both systems.

Case Study Organization

Procter & Gamble

Vision

Mission

Nestle origins date back to 1866, when two seperate Swiss enterprises were founded that would later form the core of Nestle.Nestle has been serving this world for over one hundred and thirty years.Nestle started its operations in Pakistan back in 1988

To be recognizededas,thebestconsumerproductsandServicesCompanyintheworld

•Mission:Wewillprovidebrandedproductsandservicesofsuperiorqualityandvaluethatimprovethelivesoftheworld'sconsumers.Asaresult,consumerswillrewarduswithleadershipsales,profit,andvaluecreation,allowingourpeople,ourshareholders,andthecommunitiesinwhichweliveandworktoprosper.KEYPEOPLE•A.GLafley(CurrentCEO,Chairman,President)•RobertA.McDonald(CEOtillMAY2013)BoardOfDirectors(Total11):oNormanAugustineoLynnmmartinoJohnfmartinjroErnestozedillooScottCook

Ambient Diary (Milk Pak) Chilled Diary (Nestle Yougart) Beverages (Fruita vitals) Bottled Water (Pure life) Culinary and food (Maggi noodles) Baby food (Cerelac) Breakfask cereals (Koko crunch) Confectionary (Polo) Juices

Nestle Pakistan

Products

Products

Competitors

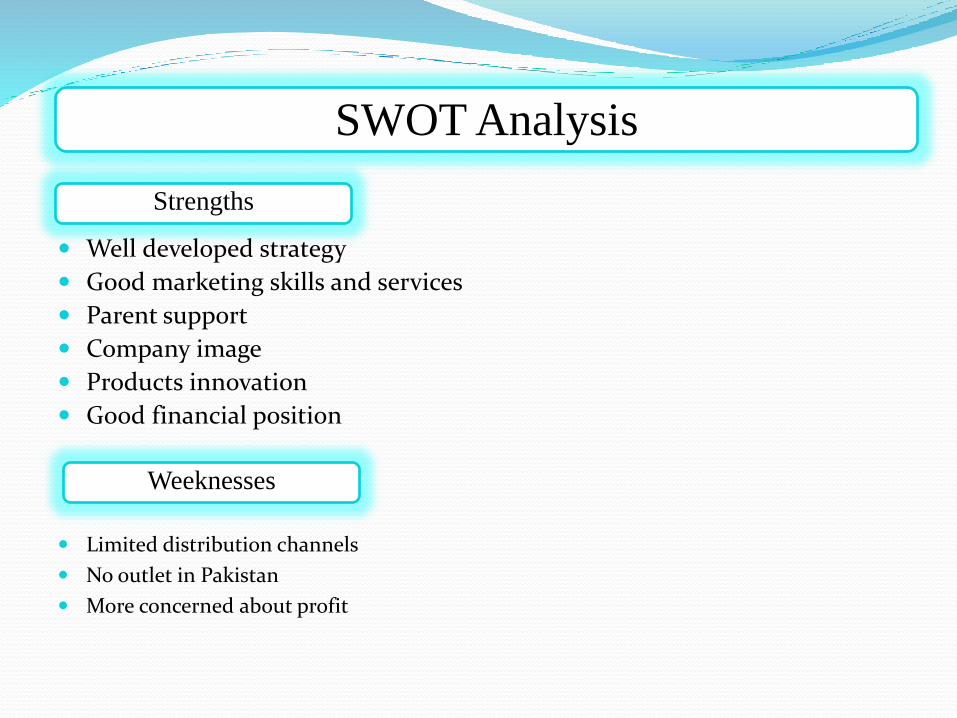

SWOT Analysis

Strengths

Well developed strategy

Good marketing skills and services

Parent support

Company image

Products innovation

Good financial position

Weeknesses

Limited distribution channels

No outlet in Pakistan

More concerned about profit

Support from foreign investors

Enhance distribution channels

Changing social trends

Market growth

Opportunities

Threats

Govt. regulations

Increase in competitions

No Entry barrier

Un favourable changes in customers demand

By analyzing the cash flow chart , for three years of Nestle Pakistan , we come to conclusion that although the organization is improving in terms of increase in sales , but there are also some grey areas which need to be tackaled by method and proper strategy to boost up the sales

Analysis

Overall profit margin showed a slight increase but a slight decline in gross profit margin was witnessed, this was mainly due to cost pressure on some products.

Nestle can be made more profitable by making it more proactive

It is recommended that they should icrease their outlets in Pakistan

Suggestions & Recommendations

Related Documents