Competitiveness in the Global Economy: Sweden’s Position Professor Michael E. Porter Dr Christian Ketels Institute for Strategy and Competitiveness Harvard Business School Globalization Council Stockholm, Sweden April 27, 2007 This presentation draws on ideas from Professor Porter’s articles and books, in particular, The Competitive Advantage of Nations (The Free Press, 1990), “Building the Microeconomic Foundations of Competitiveness,” in The Global Competitiveness Report 2006 (World Economic Forum, 2006), “Clusters and the New Competitive Agenda for Companies and Governments” in On Competition (Harvard Business School Press, 1998), and ongoing research on clusters and competitiveness. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means - electronic, mechanical, photocopying, recording, or otherwise - without the permission of Michael E. Porter. Further information on Professor Porter’s work and the Institute for Strategy and Competitiveness is available at www.isc.hbs.edu

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Competitiveness in the Global Economy:Sweden’s Position

Professor Michael E. PorterDr Christian Ketels

Institute for Strategy and Competitiveness Harvard Business School

Globalization CouncilStockholm, Sweden

April 27, 2007

This presentation draws on ideas from Professor Porter’s articles and books, in particular, The Competitive Advantage of Nations (The Free Press, 1990), “Building the Microeconomic Foundations of Competitiveness,” in The Global Competitiveness Report 2006 (World Economic Forum, 2006), “Clusters and the New Competitive Agenda for Companies and Governments” in On Competition (Harvard Business School Press, 1998), and ongoing research on clusters and competitiveness. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means - electronic, mechanical, photocopying, recording, or otherwise - without the permission of Michael E. Porter.Further information on Professor Porter’s work and the Institute for Strategy and Competitiveness is available at www.isc.hbs.edu

2 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

A Changing Global Competitive Environment

• Fewer barriers to trade and investment• Rapidly increasing stock and diffusion of knowledge• Competitiveness upgrading in many countries

• Globalization of markets• Globalization of value chains• Internationalization of capital, especially portfolio investment• Increasing knowledge and skill intensity of competition• Value increasingly in the service component of activities

• Productivity increasingly determines success• Competition among nations need not be zero-sum• Economic success depends on providing unique value, not

just meeting best practice benchmarks

Driver

Marketreaction

Implications

3 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Swedish Competitiveness in 2007

• Sweden is one of the primary beneficiaries of globalization

HOWEVER

• Other countries are catching up, exposing remaining weaknesses in Swedish competitiveness

• Recent policy changes are a move in the right direction but they are not sufficient

4 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Long-Term Trends in Prosperity

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

EU-15

United States

GDP per capita, US-$, PPP-adjusted

Source: Groningen Growth and Development Center, The Conference Board, 2006

Sweden

Countries that have surpassed Swedenin terms of prosperity:

1970s: Canada, Iceland, Norway1980s: Austria, Denmark1990s: Australia, Ireland, UK

5 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

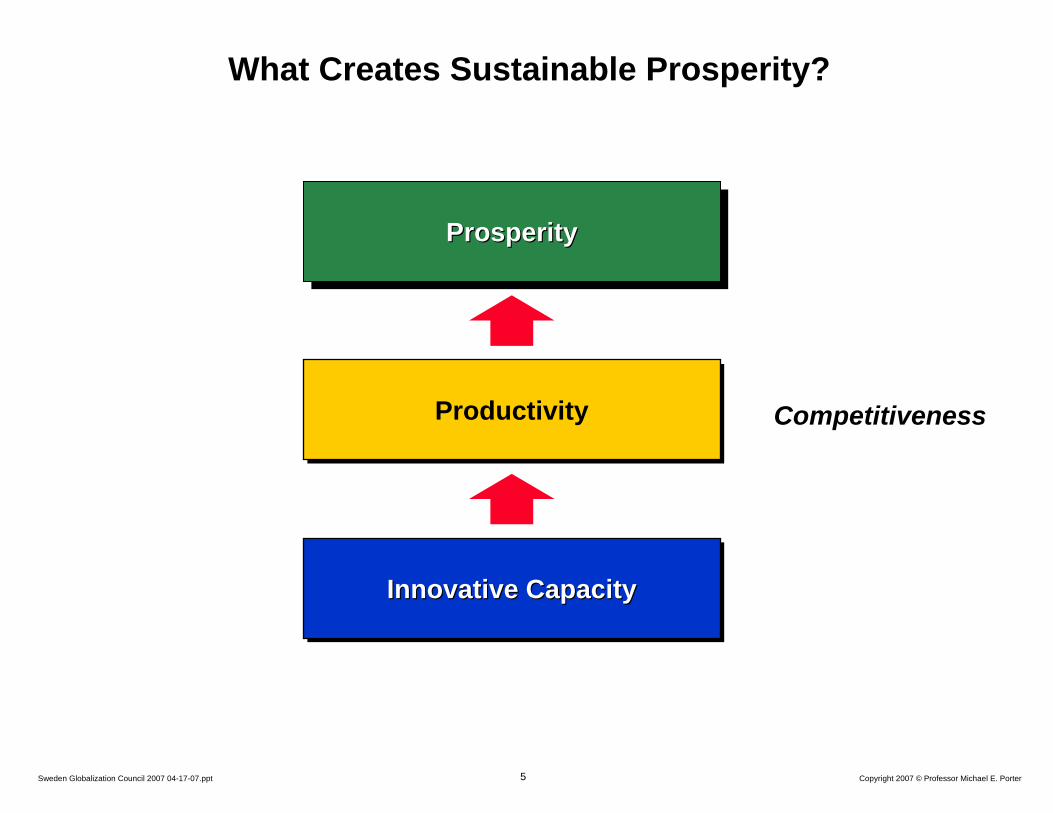

What Creates Sustainable Prosperity?

ProductivityProductivity

Innovative CapacityInnovative CapacityInnovative Capacity

Competitiveness

ProsperityProsperityProsperity

6 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Microeconomic CapabilitiesMicroeconomic Capabilities

Quality of the Business

Environment

Quality of the Quality of the BusinessBusiness

EnvironmentEnvironment

Sophisticationof Company

Operations andStrategy

SophisticationSophisticationof Companyof Company

Operations andOperations andStrategyStrategy

Determinants of Productivity and Productivity Growth

Macroeconomic, Political, Legal, and Social ContextMacroeconomic, Political, Legal, and Social ContextMacroeconomic, Political, Legal, and Social Context

• A sound context creates the potential for competitiveness, but is not sufficient• Competitiveness ultimately depends on improving the microeconomic capability

of the economy and the sophistication of local companies and local competition

7 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Context for Firm

Strategy and Rivalry

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Related and Supporting Industries

Factor(Input)

Conditions

Factor(Input)

ConditionsDemand

ConditionsDemand

Conditions

Improving the Business Environment

• Successful economic development is a process of successive economic upgrading, in which the business environment in a nation evolves to support and encourage increasingly sophisticated ways of competing

Sophisticated and demandinglocal customer(s)Local customer needs that anticipate those elsewhereUnusual local demand in specialized segments that can be served nationally and globally

Presence of high quality, specialized inputs available to firms

–Human resources–Capital resources–Physical infrastructure–Administrative infrastructure–Information infrastructure–Scientific and technological

infrastructure–Natural resources

Access to capable, locally based suppliersand firms in related fieldsPresence of clusters instead of isolated industries

A local context and rules that encourage investment and sustained upgrading

–e.g., Intellectual property protection

Meritocratic incentive systems across all major institutionsOpen and vigorous competition among locally based rivals

8 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

The Boston Life Sciences Cluster

Research OrganizationsResearch OrganizationsResearch Organizations

Biological Products

Biological Biological ProductsProducts

Specialized Risk CapitalVC Firms, Angel Networks

Specialized Risk CapitalVC Firms, Angel Networks

Biopharma-ceutical

Products

BiopharmaBiopharma--ceuticalceutical

ProductsProducts

Specialized BusinessServices

Banking, Accounting, Legal

Specialized BusinessServices

Banking, Accounting, Legal

Specialized ResearchService Providers

Laboratory, Clinical Testing

Specialized ResearchService Providers

Laboratory, Clinical Testing

Dental Instrumentsand Suppliers

Dental Instrumentsand Suppliers

Surgical Instruments and Suppliers

Surgical Instruments and Suppliers

Diagnostic SubstancesDiagnostic Substances

ContainersContainersContainers

Medical EquipmentMedical Equipment

Ophthalmic GoodsOphthalmic Goods

Health and Beauty Products

Health and Beauty Health and Beauty ProductsProducts Teaching and Specialized HospitalsTeaching and Specialized Hospitals

Educational InstitutionsHarvard University, MIT, Tufts University,

Boston University, UMass

Educational InstitutionsHarvard University, MIT, Tufts University,

Boston University, UMass

Cluster OrganizationsMassMedic, MassBio, othersCluster Organizations

MassMedic, MassBio, others

Analytical InstrumentsAnalytical InstrumentsAnalytical Instruments

9 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Institutions for CollaborationSelected Massachusetts Organizations, Life Sciences

Economic Development InitiativesEconomic Development Initiatives

Massachusetts Technology CollaborativeMass Biomedical InitiativesMass DevelopmentMassachusetts Alliance for Economic Development

Massachusetts Technology CollaborativeMass Biomedical InitiativesMass DevelopmentMassachusetts Alliance for Economic Development

Life Sciences Industry AssociationsLife Sciences Industry Associations

Massachusetts Biotechnology CouncilMassachusetts Medical Device Industry CouncilMassachusetts Hospital Association

Massachusetts Biotechnology CouncilMassachusetts Medical Device Industry CouncilMassachusetts Hospital Association

General Industry AssociationsGeneral Industry Associations

Associated Industries of MassachusettsGreater Boston Chamber of CommerceHigh Tech Council of Massachusetts

Associated Industries of MassachusettsGreater Boston Chamber of CommerceHigh Tech Council of Massachusetts

University InitiativesUniversity Initiatives

Harvard Biomedical CommunityMIT Enterprise ForumBiotech Club at Harvard Medical SchoolTechnology Transfer offices

Harvard Biomedical CommunityMIT Enterprise ForumBiotech Club at Harvard Medical SchoolTechnology Transfer offices

Informal networksInformal networks

Company alumni groupsVenture capital communityUniversity alumni groups

Company alumni groupsVenture capital communityUniversity alumni groups

Joint Research InitiativesJoint Research Initiatives

New England Healthcare InstituteWhitehead Institute For Biomedical ResearchCenter for Integration of Medicine and Innovative Technology (CIMIT)

New England Healthcare InstituteWhitehead Institute For Biomedical ResearchCenter for Integration of Medicine and Innovative Technology (CIMIT)

10 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

TradedTraded LocalLocalLocal NaturalResource-Driven

NaturalNaturalResourceResource--DrivenDriven

29.3%0.7%

$49,367137.2%

4.2%

144.1

23.0

590

29.3%0.7%

$49,367137.2%

4.2%

144.1

23.0

590

70.0%2.4%

$30,41684.53.4%

79.3

0.4

241

70.0%70.0%2.4%2.4%

$30,416$30,41684.584.53.4%3.4%

79.379.3

0.40.4

241241

0.7%-1.2%

$35,81599.52.1%

140.1

3.3

48

0.7%0.7%--1.2%1.2%

$35,815$35,81599.599.52.1%2.1%

140.1140.1

3.33.3

4848

Share of EmploymentEmployment Growth Rate,

1990 to 2004

Average WageRelative WageWage Growth

Relative Productivity

Patents per 10,000 Employees

Number of SIC Industries

Note: 2004 data, except relative productivity which uses 1997 data.Source: Prof. Michael E. Porter, Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

The Composition of Regional EconomiesUnited States, 2004

11 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Specialization of Regional EconomiesSelect U.S. Geographic Areas

BostonAnalytical InstrumentsEducation and Knowledge CreationCommunications Equipment

BostonAnalytical InstrumentsEducation and Knowledge CreationCommunications Equipment

Los Angeles AreaApparelBuilding Fixtures,

Equipment and Services

Entertainment

Los Angeles AreaApparelBuilding Fixtures,

Equipment and Services

Entertainment

ChicagoCommunications EquipmentProcessed FoodHeavy Machinery

ChicagoCommunications EquipmentProcessed FoodHeavy Machinery

Denver, COLeather and Sporting GoodsOil and GasAerospace Vehicles and Defense

Denver, COLeather and Sporting GoodsOil and GasAerospace Vehicles and Defense

San DiegoLeather and Sporting GoodsPower GenerationEducation and Knowledge Creation

San DiegoLeather and Sporting GoodsPower GenerationEducation and Knowledge Creation

San Francisco-Oakland-San Jose Bay AreaCommunications EquipmentAgricultural ProductsInformation Technology

San Francisco-Oakland-San Jose Bay AreaCommunications EquipmentAgricultural ProductsInformation Technology

Seattle-Bellevue-Everett, WAAerospace Vehicles and DefenseFishing and Fishing ProductsAnalytical Instruments

Seattle-Bellevue-Everett, WAAerospace Vehicles and DefenseFishing and Fishing ProductsAnalytical Instruments

HoustonHeavy Construction ServicesOil and GasAerospace Vehicles and Defense

HoustonHeavy Construction ServicesOil and GasAerospace Vehicles and Defense

Pittsburgh, PAConstruction MaterialsMetal ManufacturingEducation and Knowledge

Creation

Pittsburgh, PAConstruction MaterialsMetal ManufacturingEducation and Knowledge

Creation

Atlanta, GAConstruction MaterialsTransportation and LogisticsBusiness Services

Atlanta, GAConstruction MaterialsTransportation and LogisticsBusiness Services

Raleigh-Durham, NCCommunications EquipmentInformation TechnologyEducation andKnowledge Creation

Raleigh-Durham, NCCommunications EquipmentInformation TechnologyEducation andKnowledge Creation

Wichita, KSAerospace Vehicles and

DefenseHeavy MachineryOil and Gas

Wichita, KSAerospace Vehicles and

DefenseHeavy MachineryOil and Gas

Note: Clusters listed are the three highest ranking clusters in terms of share of national employmentSource: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

12 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Plastics

Oil and Gas

Chemical Products

Pharma-ceutical

Power Generation

Aerospace Vehicles &

Defense

Lightning & Electrical Equipment

Financial Services

Publishing and Printing

Entertainment

Hospitality and Tourism

Trans-portation

and Logistics

Information Tech.

Communi-cations

Equipment

Medical Devices

Analytical Instruments

Education and

Knowledge Creation

ApparelLeather

and Related Products

Agricultural Products

Processed Food

FurnitureBuilding Fixtures,

Equipment and

Services

Note: Clusters with overlapping borders or identical shading have at least 20% overlap (by number of industries) in both directions. Clusters in which Stockholm has a strong position within Sweden are in bold

Sporting and Recreation

Goods

Business Services

DistributionServices

Fishing & Fishing

Products

Footwear

Forest Products

Heavy Construction

Services

Jewelry & Precious Metals

ConstructionMaterials

Prefabricated Enclosures

Textiles

Tobacco

Heavy Machinery

Aerospace Engines

Automotive

Production Technology

Motor Driven Products

Metal Manufacturing

Related Clusters in the U.S. EconomySchematic Representation

13 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Cross-National Collaboration of Cluster Initiatives

FINLANDCentre of Expertise, Gene Technology

and Molecular BiologyFIVDIC, In Vitro Diagnostics Industry ClusterCulminatum, Medical &Welfare Technologies

Technology Centre Teknia Ltd

FINLANDCentre of Expertise, Gene Technology

and Molecular BiologyFIVDIC, In Vitro Diagnostics Industry ClusterCulminatum, Medical &Welfare Technologies

Technology Centre Teknia Ltd

NORWAYBIOINN

BCNorth

NORWAYBIOINN

BCNorth

SWEDENBiotech UmeåUppsala BIO

Biomedical Development, West SwedenLivets Nya Verktyg

Healthcare Technology AllianceBioMedley

SWEDENBiotech UmeåUppsala BIO

Biomedical Development, West SwedenLivets Nya Verktyg

Healthcare Technology AllianceBioMedley

NORTHERN GERMANYLife Sciences SH & HH

BioCon ValleymedRegio Luebeck

NORTHERN GERMANYLife Sciences SH & HH

BioCon ValleymedRegio Luebeck

DENMARKbioTEAMsouth

BioMedico Forum

DENMARKbioTEAMsouth

BioMedico Forum

ESTONIAEstonian Biotechnology Association

Tartu Biotech Cluster

ESTONIAEstonian Biotechnology Association

Tartu Biotech Cluster

CROSS-BORDER EFFORTSScanBalt

Medicon Valley AcademyMedCoast Scandinavia

CROSS-BORDER EFFORTSScanBalt

Medicon Valley AcademyMedCoast Scandinavia

14 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

The Process of Economic DevelopmentShifting Roles and Responsibilities

Old ModelOld Model

• Government drives economic development through policy decisions and incentives

• Government drives economic development through policy decisions and incentives

New ModelNew Model

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

• Competitiveness must become a bottom-up process in which many individuals, companies, clusters, and institutions take responsibility

• Every region and cluster can take steps to enhance competitiveness

• Successful competitiveness efforts set clear priorities reflecting the specific barriers companies face

15 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Swedish Competitiveness 2007

• Prosperity driven by solid levels of productivity and labor mobilization– Labor productivity still below EU-15 average but closing the gap– Labor mobilization advantage relative to EU-15 stable after

significant drop in 1990s; little job creation in the private sector

• Strong integration into global markets, driven by core of multinationals– Export market share broadly stable, shifting to services– Significant presence of foreign companies– Strong outward investment, especially in the Baltic Sea Region

• Low domestic investment rate

• High but falling patenting rate– Universities leading in the region, but not globally

16 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Productivity versus Working HoursSelected Countries

0

10

20

30

40

50

60

70

500 600 700 800 900 1000 1100 1200

Real GDP per Hour Worked, PPP adjusted, 2005

Hours worked per Capita, 2005

LatviaEstonia

Finland

LithuaniaRussia*

Germany

Poland

Norway*

Note: Affected by oil revenuesSource: Groningen Growth and Development Centre and The Conference Board (2006), authors’ calculations

Denmark SWEDEN

Japan

S Korea

Mexico

United States

Australia

New Zealand

IrelandFrance

Iceland

UK

NL

SwitzerlandItaly

Belgium

Spain

Portugal

Canada

Czech RepublicHungary

Slovakia

Slovenia

Greece

17 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Long-Term Trends in Labor Productivity

0

10

20

30

40

50

60

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

GDP per hour worked US-$, PPP-adjusted

Source: Groningen Growth and Development Center, The Conference Board, 2006

EU-15

United StatesSweden

Catch-Up Stagnation New Growth

18 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Long-Term Trends in Labor MobilizationSweden versus EU-15

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Employees as % of Population

Hours per Employee

Gap in %, Sweden versus EU-15

Unemployment

Source: Groningen Growth and Development Center, The Conference Board, 2006

Net Gap

19 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Entrepreneurship

0%

5%

10%

15%

20%

25%

30%

Greece Ita

lyPort

ugal

Polen

Cypern

Spain

Irelan

d

Czech

Rep

ublic

Lithu

ania

Malta

Hunga

ryBelg

iumSlov

akia UK

Austria

Finlan

dNeth

erlan

dGerm

any

France

Sweden

Latvi

aSlov

enia

Luxe

mbourg

Denmark

Estonia

Norway

Share of Entrepreneurs in the Labor Force, 2005

Source: NUTEK (2007)

20 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

SwedenCluster Export Portfolio, 1997-2005

Change in Sweden’s world export market share, 1997 – 2005Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

Swed

en’s

wor

ld e

xpor

t mar

ket s

hare

, 200

5

0%

1%

2%

3%

4%

5%

6%

7%

8%

-3.5% -2.5% -1.5% -0.5% 0.5% 1.5% 2.5%

Change In Sweden’s Overall World Export Share: -0.05%

Sweden’s Average World Export Share: 1.44%

Exports of US$2 Billion =

Forest Products

Business Services

Communications EquipmentFurniture

Communications Services

ConstructionServices

(1.32%,-4.37%)

Biopharmaceuticals

Power and Power Generation Equipment

Fishing and Fishing ProductsFinancial

Services

Medical Devices

Aerospace Engines

Aerospace Vehicles and Defense

Publishing and Printing

21 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

SwedenCluster Export Portfolio, 1997-2005 (continued)

Change in Sweden’s world export market share, 1997 – 2005Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

Swed

en’s

wor

ld e

xpor

t mar

ket s

hare

, 200

5

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

-0.5% -0.3% -0.1% 0.1% 0.3% 0.5%

Change In Sweden’s Overall World Export Share: -0.05%

Sweden’s Average World Export Share: 1.44%

Publishing and Printing

Automotive

Metal Mining and Manufacturing

Transportation and Logistics

Production Technology

Hospitality and Tourism

Oil and Gas Products

Plastics

Motor Driven Products Heavy Machinery

Chemical Products

Analytical InstrumentsProcessed Food

Information Technology

Building Fixtures and Equipment

Entertainment and Reproduction Equipment

Lighting and Electrical Equipment

Agricultural Products

Prefabricated Enclosures and Structures

Textiles

Apparel

Construction MaterialsMarine Equipment

Jewelry, Precious Metals and Collectibles

Sporting, Recreational and Children's Goods

Leather and Related Products

Footwear

Tobacco

Exports of US$2 Billion =

22 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Foreign Direct InvestmentSelected Countries

0%

20%

40%

60%

80%

100%

120%

140%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50%

Inflows of Foreign Direct Investment, in % of Domestic Capital Formation, 2001 - 2005

Stock of Foreign Direct Investment, in

% of GDP, 2005

SWEDENCzech Republic

Estonia

New Zealand

Chile

UK

US

Australia

Japan

Iceland

Hungary

Italy ChinaIndia

ThailandDenmark

Slovakia

Switzerland

Netherlands

Germany Finland

Ireland

Belgium

Source: World Investment Report (2006), author’s analysis.

23 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Capital Investment IntensitySelected Countries

15%

17%

19%

21%

23%

25%

27%

29%

31%

-4% -2% 0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Source: EIU (2006), author’s analysis.

Denmark

FinlandGermany

Estonia

Latvia

Lithuania

PolandNorway

RussiaSWEDEN

US

Taiwan

S Korea

SingaporeJapan

New Zealand

India

Chile

Ireland

Brazil

Australia

Gross Investment in % of GDP, 2005

Growth Rate of Real Gross Investment, CAGR, 2000 - 2005

Canada

Iceland

24 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

0

50

100

150

200

250

300

-10% -5% 0% 5% 10% 15%

Patents per 1000 Capita, 2005

Growth of Patents per Capita, CAGR, 2000-2005

Innovation PerformancePatenting in the United States

Source: USPTO (2006), author’s analysis.

Denmark

Finland

Germany

Russia

SWEDEN

Norway

United States

Japan

Taiwan

France UK

Canada

Switzerland

Italy

South Korea

Australia

Israel

Singapore

Hong KongIreland

AustriaNL Iceland

New ZealandSpain MalaysiaSouth Africa Hungary

China (.3, +27%)India (.3, +22%)

25 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Sweden in the Business Competitiveness Index Key Observations

• Sweden ranks 7 on the Business Competitiveness Index and has been consistently among the top 10 in most years

Changes over time• Sweden has in the medium-term lost ground on critical competitiveness

factors relative to its peers, despite the positive current results

Wages • Swedish wages are broadly in line with the level of competitiveness but

wage growth has recently been stronger than the speed of competitiveness upgrading

Challenges• Sweden continues to suffer from an imbalance between sound

macroeconomic policies and strong companies on the one hand and a weaker business environment conditions on the other

• Key weaknesses are educational quality, government efficiency, and infrastructure

26 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

BCI Value, 2006

Dynamism Score, 2002 - 2006

India

China Pakistan

Italy

Finland

AustraliaSWEDEN

NorwayHong KongJapan

Portugal

Malaysia

Turkey

El SalvadorPeru

United States Germany

Chad

MaliVietnam

MalawiZimbabwe

High-incomeMiddle-incomeLow-income

EstoniaChile

Switzerland

Iceland

Ireland

Paraguay

Dominican Rep.

EthiopiaBolivia

Mozambique NicaraguaHonduras

Bangladesh

Nigeria

BrazilTrinidad

Slovenia

Russia

Spain

New Zealand

ColombiaJordan

Greece

South Africa

Ukraine

Thailand

Uruguay

Argentina

Mauritius

Slovak RepublicLithuania

High

Low

Below average Above averageAverage

Medium-Term Dynamism in Competitiveness

Source: Global Competitiveness Report (2006)

27 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

$0

$5

$10

$15

$20

$25

$30

$35

$40

Hourly Wage in Manufacturing, 2004

Brazil

Finland

Denmark

Canada

Hungary

Italy

Mexico

Korea

Norway Germany

Hong KongTaiwanSingapore

Source: Global Competitiveness Report 2006, Eurostat, Bureau of Labor Statistics

Business Competitiveness Index 2004 HighLow

Australia

Austria

Belgium

Bulgaria

Cyprus

Czech RepublicEstonia

France

Greece

Iceland

Ireland

Israel

Japan

LithuaniaLatvia

Malta

Netherlands

New Zealand

Portugal

Poland

Romania

Slovenia

Slovakia

Spain

SWEDENSwitzerland

UK

United States

Sri Lanka

Locational Value: Competitiveness and Wages

28 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

University/industry research collaboration 3

Local equity market access 3

Ease of access to loans 5

Efficiency of legal framework 6

Venture capital availability 9

Quality of scientific research institutions 9

Financial market sophistication 10

Availability of scientists and engineers 10

Telephone/fax infrastructure quality 11

Railroad infrastructure development 12

Port infrastructure quality 14

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Quality of math and science education 35

Reliability of police services 26

Quality of public schools 25

Quality of management schools 25

Air transport infrastructure quality 23

Quality of electricity supply 18

Overall infrastructure quality 17

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Factor (Input) ConditionsSweden’s Relative Position 2006

Factor(Input)

Conditions

Factor(Input)

Conditions

Note: Rank versus 121 countries; overall, Sweden ranks 7th in Business Competitiveness and 18th in 2005 PPP adjusted GDP per capita.Source: Global Competitiveness Report 2006-2007.

29 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Context for Firm Strategy and RivalrySweden’s Relative Position 2006

Efficacy of corporate boards 2

Prevalence of trade barriers 4

Intellectual property protection 8

Business costs of corruption 9

Intensity of local competition 11

Favoritism in decisions of government 11 officials

Effectiveness of antitrust policy 14

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Centralization of economic policymaking 65

Decentralization of corporate activity 25

Cooperation in labor-employer relations 18

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Context for Firm Strategy and Rivalry

Context for Firm Strategy and Rivalry

Note: Rank versus 121 countries; overall, Sweden ranks 7th in Business Competitiveness and 18th in 2005 PPP adjusted GDP per capita.Source: Global Competitiveness Report 2006-2007.

30 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Demand ConditionsSweden’s Relative Position 2006

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Stringency of environmental regulations 5

Presence of demanding regulatory 5 standards

Demand ConditionsDemand

Conditions

Laws relating to ICT 18

Government procurement advanced 18technology products

Buyer sophistication 16

Note: Rank versus 121 countries; overall, Sweden ranks 7th in Business Competitiveness and 18th in 2005 PPP adjusted GDP per capita.Source: Global Competitiveness Report 2006-2007.

31 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Related and Supporting IndustriesSweden’s Relative Position 2006

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Related and Supporting Industries

Related and Supporting Industries

Local supplier quality 7

Local availability of specialized research 9 and training services

Local availability of process machinery 10

Local supplier quantity 11

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Note: Rank versus 121 countries; overall, Sweden ranks 7th in Business Competitiveness and 18th in 2005 PPP adjusted GDP per capita.Source: Global Competitiveness Report 2006-2007.

32 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Action Priorities

• Further strengthen physical and communication infrastructure to connect better to the neighborhood and the world

• Educate the public on the benefits of globalization for Sweden

• Sustain focus on education and skill upgrading

• Increase attractiveness for human capital from abroad

• Create a better environment for entrepreneurship

• Achieve world-class in science areas tied to cluster strengths

• Integrate the environmental and competitiveness agendas

• Create a strategy for economic integration of immigrant groups

• Pursue deep integration in the Baltic Sea Region

33 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Moving Towards a New Model for SwedenKey Themes

• Sound macroeconomic policies, solid institutions, and high skills are the basis of competitiveness

• Capital-intensive multinationals drive the economy

• Innovation is based on large company R&D, drawing on university research

• National government defines and executes policy

• Strong microeconomic foundations and regional specialization add critical strengths to competitiveness

• Knowledge-intensive clusters of entrepreneurs drive the economy

• Innovation emerges in open networks of academia and firms of all sizes

• Policy design and execution in triple helix partnership

34 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Finnish Science and Technology

Council

Competitiveness Councils

Internal coordination of government

policies

Public debate of sources of

competitiveness

Encourage collaboration and consensus across public and private

sectors

Danish Globalization

Council

U.S. Council on Competitiveness

35 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Background Data

36 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Comparative Economic PerformanceSelected Countries

Compound annual growth rate of real GDP per capita, 1998-2005

GDP per capita (PPP

adjusted) in US-$,

2005

Iceland

Czech Rep.

EstoniaHungary

LatviaPolandSlovakia

Slovenia

Denmark

FinlandFranceGermany

India

Japan

S Korea

NL

Norway

Australia, Canada,

U.K.

China

U.S.

SWEDENSwitzerland

Ireland

Greece

Source: Groningen Growth and Development Centre and The Conference Board (2006), authors’ calculations

Lithuania

Spain

Mexico

Turkey

Portugal

New ZealandItaly

Austria

37 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Long-Term Trends in Labor Mobilization

0

200

400

600

800

1000

1200

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Annual hours worked per capita

Source: Groningen Growth and Development Center, The Conference Board, 2006

EU-15

United States

Sweden

38 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Domestic Purchasing PowerNormalized Purchasing Power Across Countries

0

1

2

3

4

5

6

India

ChinaRuss

ia

South

KoreaBraz

il

Slovak R

epub

licLa

tvia

ChileHung

aryEsto

niaLit

huania

Mexico

Poland

Czech

Rep

ublic

Taiwan

Slovenia

Greece

Portug

alSpa

in

Hong Kong

SARIta

ly

United Stat

esCana

da

New Zealan

dAus

tralia

Singap

ore

Luxe

mbourg

Irelan

dAus

triaBelg

iumNetherl

ands

German

yFranc

e

United King

domFinl

and

Sweden

Denmark

IcelandJa

pan

Norway

Switzerl

and

Source: IMF (2006), authors’ calculations

Purchasing Power Factor, 2005

39 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Sweden’s Export PerformanceWorld Export Market Shares

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

GoodsServicesTotal

Source: WTO (2006)

World export share in %

40 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Industry Cluster

World Export Share

Change in Share,

1997-2005 Export Value (in US$1,000)

1 Passenger transport vehicles Automotive 1.72% 0.19% $8,122,269

2 Miscellaneous medicaments Biopharmaceuticals 3.18% -2.49% $5,321,590

3 Petroleum Oils Oil and Gas Products 1.58% 0.01% $5,095,941

4 Parts for telecommunication equipment Communications Equipment 4.47% -4.10% $4,693,454

5 TV, radio transmitters Communications Equipment 3.06% -10.94% $4,242,399

6 Flat-rolled products of alloy steel Metal Mining and Manufacturing 8.74% 1.09% $3,532,018

7 Wood of conifer, sawn Furniture 12.63% -0.69% $2,808,103

8 Line telephone or telegraph equipment Communications Equipment 6.21% 3.48% $2,182,022

9 Miscellaneous paper and paperboard, coated Forest Products 10.66% 1.31% $2,051,603

10 Kraft paper and paperboard, uncoated Forest Products 20.19% -0.83% $1,726,457

11 Paper and paperboard, uncoated Forest Products 8.48% 1.08% $1,678,481

12 Chemical wood pulp, soda, bleached Forest Products 9.65% 0.38% $1,580,115

13 Other parts for motor vehicles Automotive 1.32% -1.09% $1,562,860

14 Internal combustion engines for vehicles Automotive 2.81% -0.23% $1,443,783

15 Road tractors, semi-trailers Automotive 6.14% 1.49% $1,240,373

16 Iron Ore and Concentrates Metal Mining and Manufacturing 4.18% -1.68% $1,123,839

17 Iron or steel bars, rods, angles, shapes and sections Metal Mining and Manufacturing 2.24% -0.94% $1,120,379

18 Medicaments containing hormones Biopharmaceuticals 5.57% -1.04% $1,100,424

19 Other parts of vehicle bodies Automotive 2.52% -0.67% $1,085,385

20 Newsprint, rolls, sheets Forest Products 9.99% -1.74% $938,702

21 Motor vehicle bodies Automotive 15.43% -1.00% $868,325

22 Fish, fresh, chilled, or frozen Fishing and Fishing Products 2.77% 1.68% $850,010

23 Polymers of ethylene Plastics 2.19% 2.02% $788,119

24 Work trucks, tractors, and parts Production Technology 6.54% 0.87% $778,778

25 Other plastics in primary forms Plastics 1.26% 0.70% $764,654

SwedenLeading Goods Export Industries, 2005

Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

41 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Industry Cluster

World Export Share

Change in Share,

1997-2005 Export Value (in US$1,000)

26 Insulted wire, cable and conductors Communications Equipment 1.45% -0.51% $752,156

27 Ball or roller bearings Production Technology 3.85% -0.72% $726,793

28 Flat-rolled iron, not clad, plated or coated Metal Mining and Manufacturing 1.17% -0.49% $722,591

29 Electric current Power and Power Generation Equipment 3.35% 3.35% $719,514

30 Miscellaneous goods vehicles Automotive 0.93% 0.65% $716,505

31 Paper and paperboard, coated, other Forest Products 7.51% 2.42% $654,918

32 Other medical instruments Medical Devices 1.61% -0.66% $650,456

33 Industrial washing, bottling machinery Production Technology 3.99% 0.00% $616,407

34 Motor vehicle chassis Automotive 20.92% 7.14% $612,510

35 Spirits Agricultural Products 3.85% 1.87% $592,975

36 Miscellaneous articles of pulp, paper and paperboard Forest Products 4.49% 0.20% $589,734

37 Other recorded media Entertainment and Reproduction Equipment 2.47% 1.26% $584,794

38 Parts of jet, gas turbine engines Aerospace Engines 1.60% -1.11% $568,076

39 Seamless tubes, pipes and hollow profiles of iron or steel Metal Mining and Manufacturing 2.52% -1.46% $521,242

40 Construction, mining machinery Heavy Machinery 11.62% -1.27% $515,621

41 Miscellaneous machinery with individual functions Production Technology 1.40% 0.05% $512,652

42 Builders� joinery and carpentry of wood Furniture 4.51% -2.60% $498,075

43 Gear boxes Automotive 1.99% -0.49% $496,631

44 Artificial aids, disabled Medical Devices 2.10% -2.47% $489,379

45 Color television receivers Entertainment and Reproduction Equipment 0.93% 0.46% $481,866

46 Paints, varnishes Plastics 3.19% 0.52% $481,749

47 Miscellaneous parts of civil engineering machinery Heavy Machinery 1.62% 1.60% $480,504

48 Instruments for analysis, measuring viscosity, expansion Analytical Instruments 2.60% -0.35% $479,735

49 Electric, laser or plasma arc soldering, welding, brazing machines Production Technology 5.86% -0.34% $467,533

50 Miscellaneous articles of iron or steel Metal Mining and Manufacturing 1.61% 0.01% $465,437

SwedenLeading Goods Export Industries, 2005 (continued)

Top 50 Industries as % of Sweden’s total goods exports: 58.3% Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

42 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

FDI Inflows over Time

0%

20%

40%

60%

80%

100%

120%

140%

160%

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

European Union

SWEDEN

Source: UNCTAD (2006), author’s analysis.

FDI Inflows as % of Gross Domestic Investment

WorldU.S.

Inward FDI Stock as % of GDP, 2006

SWEDEN: 47.8%

European Union: 33.5%

World: 22.7%

U.S.: 13.0%

43 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Regional IntegrationForeign Direct Investment Flows

0%

10%

20%

30%

40%

50%

60%

70%

80%

Lithu

ania

Finlan

dEsto

niaNorw

ayDen

markSwed

enN P

oland

NW R

ussia

Icelan

dN G

erman

ySwedenFinlandDenmarkEstoniaN GermanyNorwayLatviaIcelandLithuaniaNW RussiaN Poland

Share of inward FDI from other BSR countries, 1999 - 2004

Source country

Source: UNCTAD, national statistical offices, author’s calculations

BSR average

44 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

ProsperityEuropean Regions

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

GDP per Capita, Euro (PPP adjusted), 2002

Annual Growth Rate of GDP per Capita (PPP adjusted), CAGR, 1995 – 2002

Sweden

Swedish regionsOther EU-15 regionsEU accession country regions

Source: Eurostat, 2005

Sweden

Stockholm

45 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Composition of the Traded EconomyStockholm Cluster Portfolio

0%

10%

20%

30%

40%

50%

60%

-15% -10% -5% 0% 5%Change of Share in National Cluster Employment, 1995-2003

Stockholm Share of National Cluster Employment, 2003: 22.9%

Change in Stockholm’s overall share of National Cluster Employment: -0.5%

Note: Bubble size is proportional to employment levelsSource: Statistics Sweden (2005), author’s calculations

Biopharmaceuticals

Financial Services

Business ServicesCommunication Equipment

Information TechnologyDistribution Services

Education & Knowledge Creation

Heavy Construction Services

TourismPublishing & Printing

Analytical Instruments

Transportation & Logistics

Share in National Cluster Employment,

2003

46 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Global Competitiveness Report 2006-07Sweden

Global Competitiveness Index Business Competitiveness Index

20052006

1

5

10

15

20

Rank

Source: Global Competitiveness Report (2006)

3

77

11

47 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Sweden’s Profile in the Global Competitiveness Report

GCI EfficiencyEnhancers

InnovationDrivers

BasicRequirments

BCI CompanyOperations &Sophistication

BusinessEnvironment

Quality

Rank1

5

10

15

20

3

7

2

57

2

8

Source: Global Competitiveness Report (2006)

Global Competitiveness Index Business Competitiveness Index

48 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Global Competitiveness IndexSweden

Efficien

cy E

nhan

cers

Techn

ology

Higher

Educa

tion

Markets

Innov

ation

Driv

ersBus

iness

Innov

ation

Basic

Requir

ments

Health

, Edu

catio

nInf

rastru

cture

Institu

tions

Macroe

cono

mics

Rank1

5

10

15

20

Source: Global Competitiveness Report (2006)

49 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Country Context

Source: Global Competitiveness Report (2006)

50 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

123456789

10111213141516171819202122232425

123456789

10111213141516171819202122232425

Top 25Top 25 Country

000

+4-1+1+4-30

+7-50

+3+5-1-6+1-5+3+3-6-1-3+3-1

United StatesGermanyFinland

SwitzerlandDenmark

NetherlandsSWEDEN

United KingdomJapan

Hong Kong SARSingapore

AustriaIcelandNorwayCanadaFranceBelgiumAustralia

IsraelMalaysiaTaiwanIreland

New ZealandEstonia

Korea, Rep.

ChangeBusiness Competitiveness Index 2006

Note: Constant sampleof countries

51 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

United States

Switzerland

Italy

DenmarkIceland

Ireland

India

Business Competitiveness Index

2005 GDP per Capita (Purchasing Power Adjusted)

Malaysia

Source: Global Competitiveness Report 2006

SWEDEN

Canada

FinlandGermany

Qatar

Norway

HighLow

UAESpain

Israel

Brazil

Estonia

Chile

Indonesia

Greece

Bahrain

Argentina

Slovenia

SingaporeTaiwan

New Zealand

S Korea

South Africa

Thailand

JordanChina

Trinidad & Tobago

Turkey

Jamaica

Australia

Cyprus

Business Competitiveness Index 2006Relationship with GDP Per Capita

Variation in BCI score explains more than 80% of variation in GDP per capita

52 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

-15000 -10000 -5000 0 5000 10000 15000 20000GAP (Actual – Expected GDP per Capita), 2006

Sustainability in questionUntapped potential

United StatesGermany

India

Malaysia

Qatar

Norway

Italy

Chile

Argentina

Indonesia

EstoniaTunisia

Ireland

Iceland

Greece

U.A.E.Spain

Kenya

Tanzania

High-incomeMiddle-incomeLow-income

BCI Value, 2006

FinlandSWEDEN

Source: Global Competitiveness Report (2006)

Economic Sustainability of Current Prosperity

53 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Business Competitiveness Ranking Over TimeSweden

2001 2002 2003 2004 2005 2006

BCINBECOS

Rank1

5

10

15

Source: Global Competitiveness Report (2006)

54 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

-$20

-$15

-$10

-$5

$0

$5

$10

$15

$20

BelgiumIta

lyNorw

ayDen

markAus

triaIce

land

Netherl

ands

German

yGree

ceFran

ce

Switzerl

and

Finlan

dSpa

inIre

land

Cyprus

Sweden

United

Kingdo

mPola

ndMalt

aSlov

enia

Canad

aBulg

aria

Austra

liaSri L

anka

Roman

ia

Slovak

Rep

ublic

Hunga

ry

Korea,

Rep.

Mexico

Japa

nPort

ugal

United

States

Czech

Rep

ublic

Israe

lLit

huan

iaBraz

il

New Zea

land

Latvi

aEsto

niaSing

apore

Taiwan

Hong K

ong S

AR

Wages higher than justified by competitiveness

Source: Business Competitiveness Index, 2006

Wage advantagegiven competitiveness

Estim

ated

abs

olut

e ga

p in

hou

rly

wag

e in

man

ufac

turin

g, U

S-$,

200

4Wage Differentials by Country

55 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Company Operations and StrategySweden’s Relative Position 2006

Competitive Disadvantages Relative to GDP per Capita

Competitive Advantages Relative to GDP per Capita

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

Note: Rank versus 121 countries; overall, Sweden ranks 7th in Business Competitiveness and 18th in 2005 PPP adjusted GDP per capita.Source: Global Competitiveness Report 2006-2007.

Willingness to delegate authority 1Reliance on professional management 1Capacity for innovation 2Breadth of international markets 3Extent of staff training 3Company spending on research and 5 development Extent of regional sales 5Extent of incentive compensation 5Nature of competitive advantage 7Production process sophistication 7Value chain presence 9Degree of customer orientation 9Control of international distribution 9Extent of marketing 10

Country Ranking, Arrows indicate a change of 5 or more

ranks since 2001

56 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

-20

-15

-10

-5

0

5

10

15

20

-15 -10 -5 0 5 10 15

Wage Gap – EU data

ItalyBelgium

DenmarkAustria

Germany

Finland

NetherlandsFrance

Spain

UK

HungaryPortugal

Czech Republic

Note: Countries in the grey area have changed their sign between 201 and 2004 Source: Global Competitiveness Report 2006 and Eurostat

Wage gap 2004: Actual versus expected wage

Change in wage gap 2001 - 2004

Wages above productivity level indicated by BCI

Wages rising more quickly than productivity growth

indicated by BCI

Iceland

Greece

Poland

SloveniaBulgariaRomania Slovakia

Lithuania

Latvia

Estonia

Malta

Changed sign since 2001

Changed sign since 2001

SWEDEN

57 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Stronger on company sophistication

Stronger on business environment quality

United StatesSwitzerland

Finland

Germany

Australia

Botswana

Brazil

Bulgaria

Chad

Costa Rica

Cyprus

Estonia

FranceHong Kong

IndiaIndonesiaIreland

Japan

Jordan

S Korea

Malta

Mexico

Morocco

New Zealand

NigeriaPhilippines PortugalQatar

Singapore

U.A.E.

Venezuela

Zambia

Algeria

Zimbabwe

Source: Global Competitiveness Report 2006

High-incomeMiddle-incomeLow-income

Business Environment and Company Sophistication

SWEDEN

58 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Patenting Intensity: 1996 – 2005Selected Countries

0

50

100

150

200

250

300

350

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

United StatesJapanTaiwanFinlandIsraelSwitzerlandSwedenGermanyS KoreaCanadaSingaporeIcelandDenmarkNorwayEstoniaRussiaLithuaniaLatviaPolandBrazilIndiaChina

Source: USPTO (2006), author’s analysis.

U.S. Patents per 1000 Capita

59 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

U.S. Patents by Sweden-based InstitutionsPatentor Number of patents, 2000-04

1 TELEFONAKTIEBOLAGET LM ERICSSON 16982 SANDVIK AKTIEBOLAG 2263 ASEA BROWN BOVERI AB 1794 SCA HYGIENE PRODUCTS AB 1645 ASTRAZENECA AB 1426 TETRA LAVAL HOLDINGS & FINANCE S.A. 1217 SIEMENS ELEMA AB 908 AKTIEBOLAGET ASTRA 889 VOLVO LASTVAGNAR AB 7510 AB VOLVO 7411 AKTIEBOLAGET ELECTROLUX 6412 KVAERNER PULPING AKTIEBOLAG 6413 AKZO NOBEL NV 5714 SCANIA CV AKTIEBOLAG 5615 PHARMACIA AKTIEBOLAG 5116 VALMET FIBERTECH AKTIEBOLAG 5016 VOLVO CAR CORPORATION AB 5018 ALLGON AB 4918 VOLVO PERSONVAGNAR AB 4920 DELAVAL HOLDING AB 4821 ALFA-LAVAL AB 4722 AUTOLIV DEVELOPMENT AB 4322 SECO TOOLS AB 4324 PACESETTER AB 3925 ERICSSON, Inc. 38

Source: USPTO (2006), author’s analysis.

60 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Knowledge CreationTop Universities in the Baltic Sea Region

Copyright © 2005 Institute of Higher Education, Shanghai Jiao Tong University

61 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Doing Business 2006 RankingSweden

Source: World Bank – Doing Business (2007), author’s analysis.

Category Rank

Enforcing Contracts 2Registering Property 7Trading Across Borders 9OVERALL 13Closing a Business 17Dealing with Licenses 17Starting a Business 20Getting Credit 33Paying Taxes 39Protecting Investors 46Employing Workers 94

62 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Hong KongSingaporeIrelandIcelandUKEstoniaDenmarkUnited StatesCanadaFinlandChileSwitzerlandGermanySwedenLithuaniaJapanNorwaySpainSlovakiaTaiwanSloveniaLatviaPoland

Free

Index of Economic Freedom1996 - 2006

Source: Index of Economic Freedom (2006), author’s analysis.

63 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Business Competitiveness Effectiveness of Public Spending, Selected Countries

Icelan

dFinl

and

Denmark

Norway

German

yChil

eUnit

ed S

tates

Estonia

Sweden

India

Latvi

aChin

aJa

pan

Lithu

ania

Poland

Russia

n Fed

eratio

nBraz

il

Positive

Negative

34

Note: Number refers to rank among 124 countriesSource: Global Competitiveness Report (2006), author’s analysis.

64 Copyright 2007 © Professor Michael E. PorterSweden Globalization Council 2007 04-17-07.ppt

Business Competitiveness Incentive Effect of Taxation, Selected Countries

Hong K

ong

Icelan

dSing

apore

Irelan

dEsto

nia

United

Stat

esInd

iaTaiw

an

United

King

dom

Chile

Latvi

aNorw

ayGerm

any

Canad

aMex

icoLit

huan

ia

Korea,

Rep.

Poland

Finlan

dRus

siaSwed

enDen

markBraz

il

Positive

Negative

111

Note: Number refers to rank among 124 countriesSource: Global Competitiveness Report (2006), author’s analysis.

Related Documents