Comparing US and Canadian Drug Plan Design Trends: The Express Scripts Story Steve Goldberg, MD,MBA Chief of Medical Affairs Value of Generics Symposium October 26, 2011 Montreal, Canada

Comparing US and Canadian Drug Plan Design Trends: The Express Scripts Story Steve Goldberg, MD,MBA Chief of Medical Affairs Value of Generics Symposium.

Dec 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Comparing US and Canadian Drug Plan Design Trends: The Express Scripts Story

Steve Goldberg, MD,MBAChief of Medical Affairs

Value of Generics SymposiumOctober 26, 2011Montreal, Canada

2

Agenda

• Overview: US PBM, Express Scripts

• Generics are a key strategy to maximizing quality and mitigate cost trend

• Our experience with “free” generics and tiered co-

pays• There is significant opportunity in Canada with active management of the pharmacy benefit

3Confidential and Proprietary Information© 2010 Express Scripts, Inc. All Rights Reserved 3

• Emerged in late 1970s to manage increasing prescription costs

• Adjudicate 90% of all prescriptions processed today (approximately four billion annually)

• Top three pharmacy benefit managers (PBMs) handle around 50% of outpatient prescription volume

US Pharmacy Benefit Managers (PBMs)

4

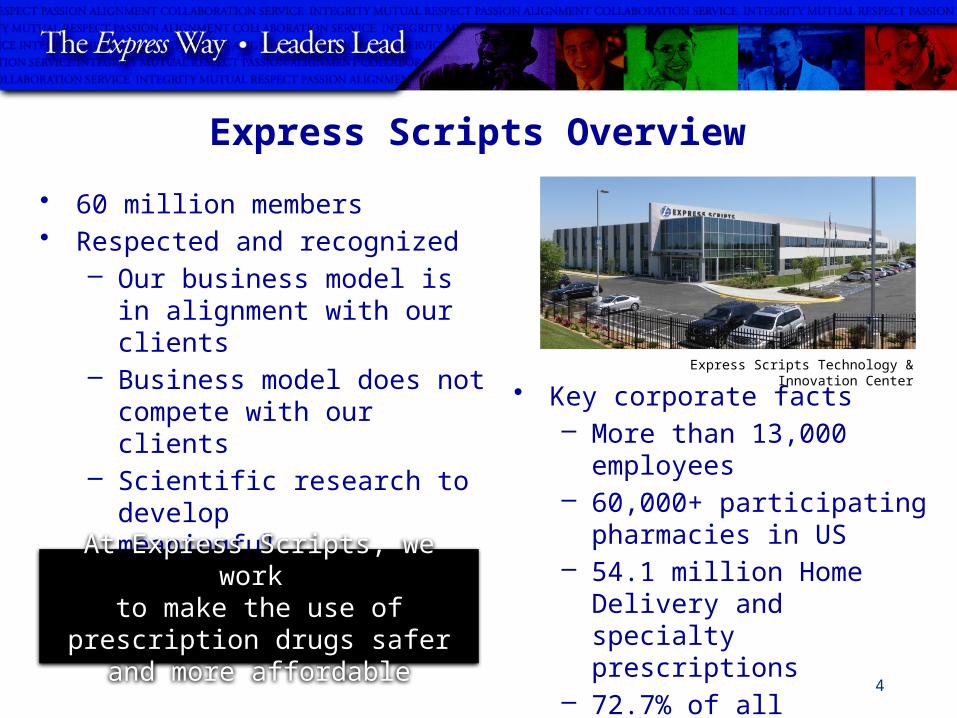

Express Scripts Overview

• 60 million members• Respected and recognized

– Our business model is in alignment with our clients

– Business model does not compete with our clients

– Scientific research to develop meaningful prescription-drug solutions

• Key corporate facts– More than 13,000

employees– 60,000+ participating

pharmacies in US– 54.1 million Home

Delivery and specialty prescriptions

– 72.7% of all prescriptions dispensed are generic drugs

At Express Scripts, we work to make the use of prescription

drugs safer and more affordable

Express Scripts Technology & Innovation Center

5Confidential and Proprietary Information© 2011 Express Scripts, Inc. All Rights Reserved 5

The Research and New Solutions Lab

Data Insights Solutions

6

Key Companies Trust Express Scripts

Confidential & Proprietary © 2011 Express Scripts, Inc. All Rights Reserved

7

Annual US Pharmacy-Related WasteMore than $403 billion

Three steps to drive out pharmacy-related

waste

Step Optimize Channel

Step Optimize Drug Mix

Step Maximize

Adherence

$88.3

$56.7

$258.3

Source: Express Scripts, Inc.

Amounts are in billions of dollars

8Confidential and Proprietary Information© 2010 Express Scripts, Inc. All Rights Reserved 8

– Electronic claims processing

– Benefit design and administration

– Pharmacy networks

– Formulary development and management

– Generic substitution

– Pharma rebates and discounts

– Patient service

– Home Delivery

– Clinical management

– Trend management

– Reporting

Pharmacy Benefit Managers

9

National P&T Committee

Committee composition– 18 physicians and one pharmacist – community- and academic-based practice

settings– No Express Scripts employees– Term of three years

●Allergy and Asthma●Cardiology●Dermatology●Endocrinology●Family Practice●Gastroenterology●Geriatrics (MD and

PharmD)

●Infectious Disease●Internal Medicine●Neurology●Obstetrics and

Gynecology●Oncology●Ophthalmology●Pediatrics

●Psychiatry●Pulmonology●Rheumatology

Specialties

10

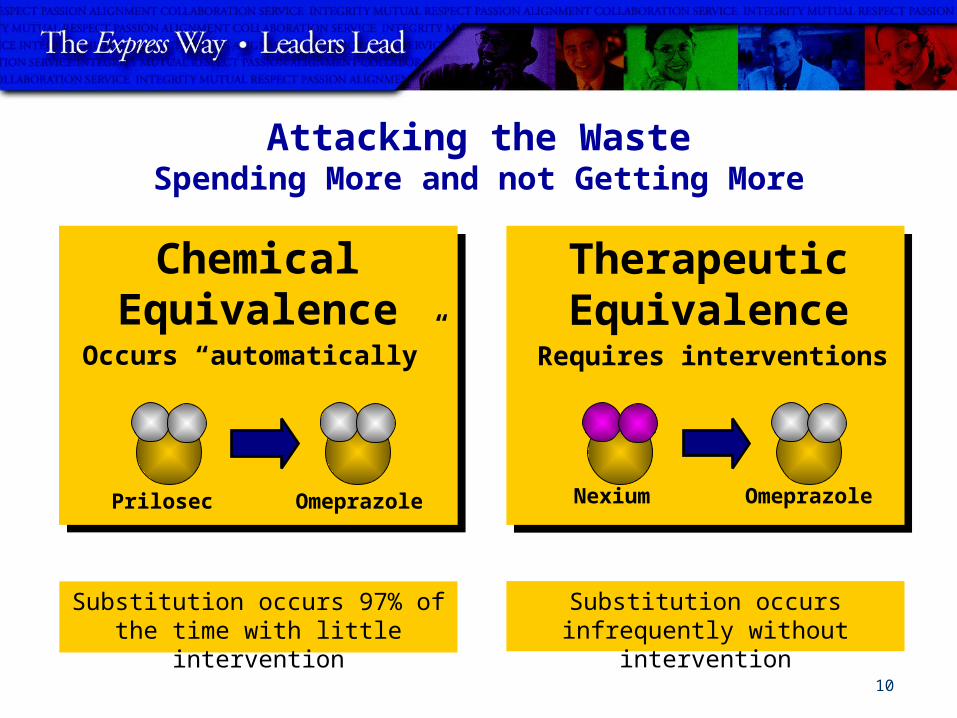

Attacking the WasteSpending More and not Getting More

Chemical Equivalence

Prilosec Omeprazole

Substitution occurs 97% of the time with little intervention

Occurs “automatically”

Therapeutic Equivalence

Nexium Omeprazole

Substitution occurs infrequently without intervention

Requires interventions

11

Attacking the WasteSpending More and not Getting More

30 days of one brand-name drug: $119.51

30 days of the generic

equivalent: $34.34No difference in health

benefitNo difference in health

benefit

12

Express Scripts Average: 72%

The higher the Generic Fill Rate,

the lower the overall drug cost.

Every 1% increase in GFR =

1.5% decrease in Rx spend

Clinical Potential: 86%

Generic Fill Rate (GFR)The “trend management metric”

13

WASTE: Spending

money without

improving health Express Scripts Average:

72%

Clinical Potential: 86%

Generic Fill Rate (GFR)The “trend management metric”

14

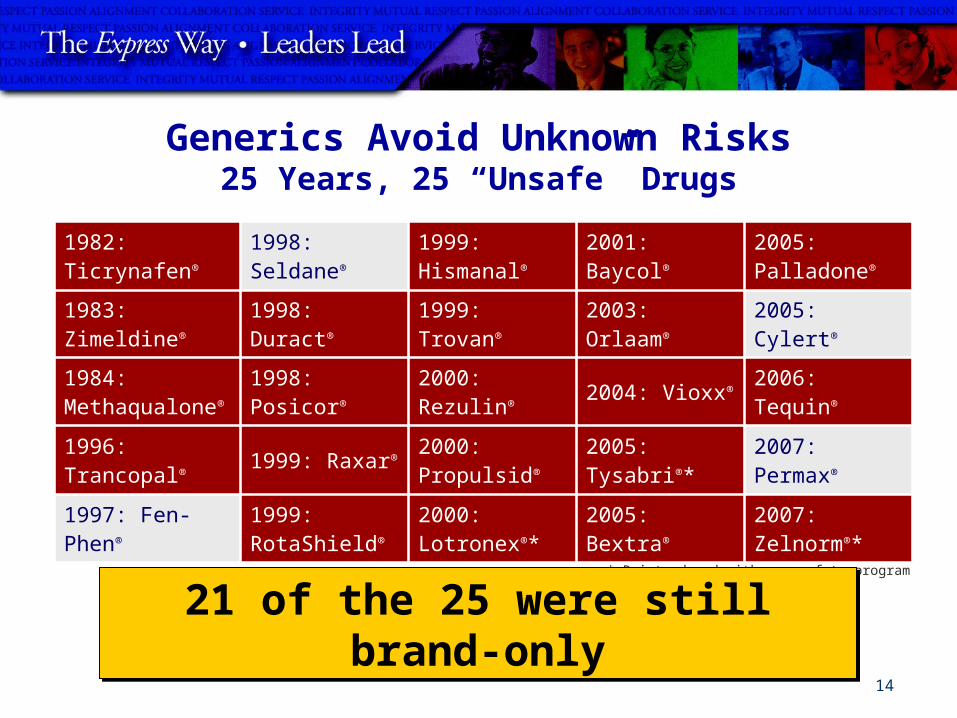

1982: Ticrynafen®

1998: Seldane®

1999: Hismanal®

2001: Baycol®

2005: Palladone®

1983: Zimeldine®

1998: Duract®

1999: Trovan®

2003: Orlaam® 2005: Cylert®

1984: Methaqualone®

1998: Posicor®

2000: Rezulin® 2004: Vioxx® 2006:

Tequin®

1996: Trancopal® 1999: Raxar® 2000:

Propulsid®

2005: Tysabri®*

2007: Permax®

1997: Fen-Phen®

1999: RotaShield®

2000: Lotronex®*

2005: Bextra®

2007: Zelnorm®*

1982: Ticrynafen®

1998: Seldane®

1999: Hismanal®

2001: Baycol®

2005: Palladone®

1983: Zimeldine®

1998: Duract®

1999: Trovan®

2003: Orlaam® 2005: Cylert®

1984: Methaqualone®

1998: Posicor®

2000: Rezulin® 2004: Vioxx® 2006:

Tequin®

1996: Trancopal® 1999: Raxar® 2000:

Propulsid®

2005: Tysabri®*

2007: Permax®

1997: Fen-Phen®

1999: RotaShield®

2000: Lotronex®*

2005: Bextra®

2007: Zelnorm®*

Generics Avoid Unknown Risks25 Years, 25 “Unsafe” Drugs

* Reintroduced with new safety program

21 of the 25 were still brand-only

21 of the 25 were still brand-only

15

Optimize Plan Design, Optimize GFR

16

Optimize Your Copay LevelsTwo employers, two plans

Plan A (7,000 lives) and Plan B (6,300 lives)• Started at same copay levels• Made the same Tier 2 and 3 copay increases• Plan B also lowered Tier 1 copay by $3• No other benefit changes in 2005

17

Optimize Your Copay LevelsTwo employers, two plans

Plan A (7,000 lives) and Plan B (6,300 lives)• Started at same copay levels• Made the same Tier 2 and 3 copay increases• Plan B also lowered Tier 1 copay by $3• No other benefit changes in 2005

Plan A missed a win/win:

$1.69 in additional savings by lowering Tier 1 copay

by $3

Results• Plan A GFR: 1.4% higher than

expected; saved $0.91 pmpm• Plan B GFR: 4% higher than

expected; saved $2.60 pmpm

18

Landscape in Canada

Drug Trend GFR

2003 11.2% 32.1%2004 9.6% 34.7%2005 9.4% 37.5%2006 8.4% 38.8%2007 7.1% 41.4%2008 5.0% 45.0%2009 5.4% 47.0%2010 2.8% 49.0%

19

Generic Fill Rate

2002 2003 2004 2005 2006 2007 2008 2009 20100.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

CanadaU.S.

20

Landscape in Canada

• The vast majority (approx 80%) of plans in Canada are using a single-tier plan that covers all items that require a prescription (vs multiple tiers or step therapy)

• Decline in drug trend due primarily to patent cliff and generic price reform

• Canada GFR rate of 49% vs US 72%

• The clinical potential GFR is much higher through active benefit management (e.g., exchanges of therapeutic equivalents)

21

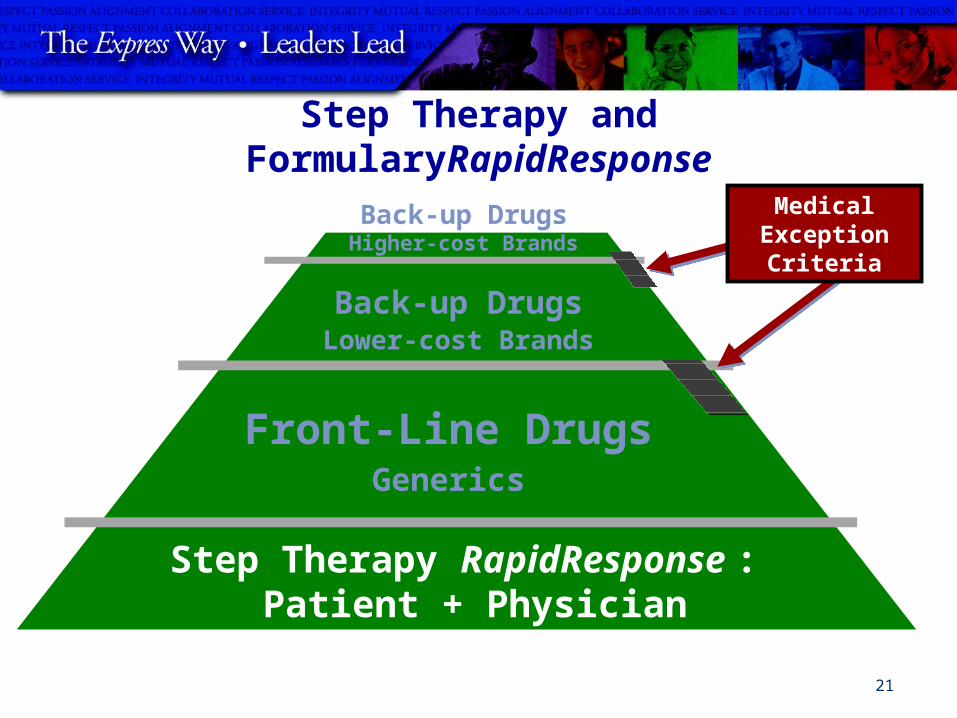

Step Therapy and FormularyRapidResponse

Front-Line DrugsGenerics

Back-up DrugsLower-cost Brands

Back-up DrugsHigher-cost Brands

Step Therapy RapidResponse : Patient + Physician

Medical Exception Criteria

22

Extr

a C

alls

Per

Week

Benefit Changes Have Limited Impact on Calls

10,000 Enrollee Plan, Changed from 2 to 3 Tier Benefit

HR Department

Source: Express Scripts Office of Research and Development based on a 2-tier to 3-tier benefit change

Express Scripts

Call Center

23

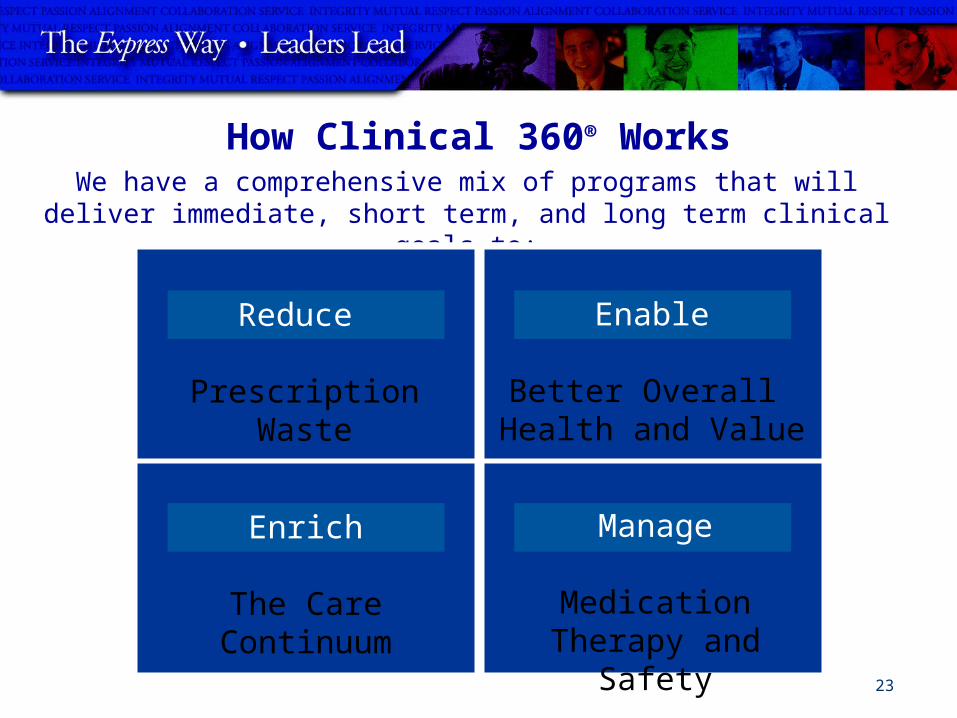

How Clinical 360® WorksWe have a comprehensive mix of programs that will deliver

immediate, short term, and long term clinical goals to:

Reduce

Prescription Waste

Manage

Medication Therapy and

Safety

Enrich

The Care Continuum

Enable

Better Overall Health and Value

Confidential and Proprietary Information© 2011 Express Scripts, Inc. All Rights Reserved 24

Exclusive HD

Preferred HD

Select HD*

Home Delivery Education

Home Delivery

Specialty Pharmacy and Distribution

Specialty Pharmacy Benefit Management• Select

Specialty*Medical Benefit Management

Specialty Benefit

Services

Path to Greater Care and Zero Waste

Drug Utilization Review

Medication Adherence

Fraud, Waste, and Abuse

ExpressAlliance®

Integrated Data Services

MTM

Clinical 360®Health Solutions

Retiree Drug Subsidy

Medicare Part B

2-Tier (open)

3-Tier

Copayment Differential

2-Tier (closed)

High Performanc

e Prime

National Preferred

Prescription-Drug Plan

Medicare Solutions Formulary

Benefit Design

*

Turn2Generics®

Zero $ Generic Copay

Drug Quantity Mgmt

Prior Authorization

Select Step Therapy*

Step Therapy

Clinical 360® Trend

Retail Network

Standard Network (50k)

Select Network*

Preferred Network

Exclusive Network

25

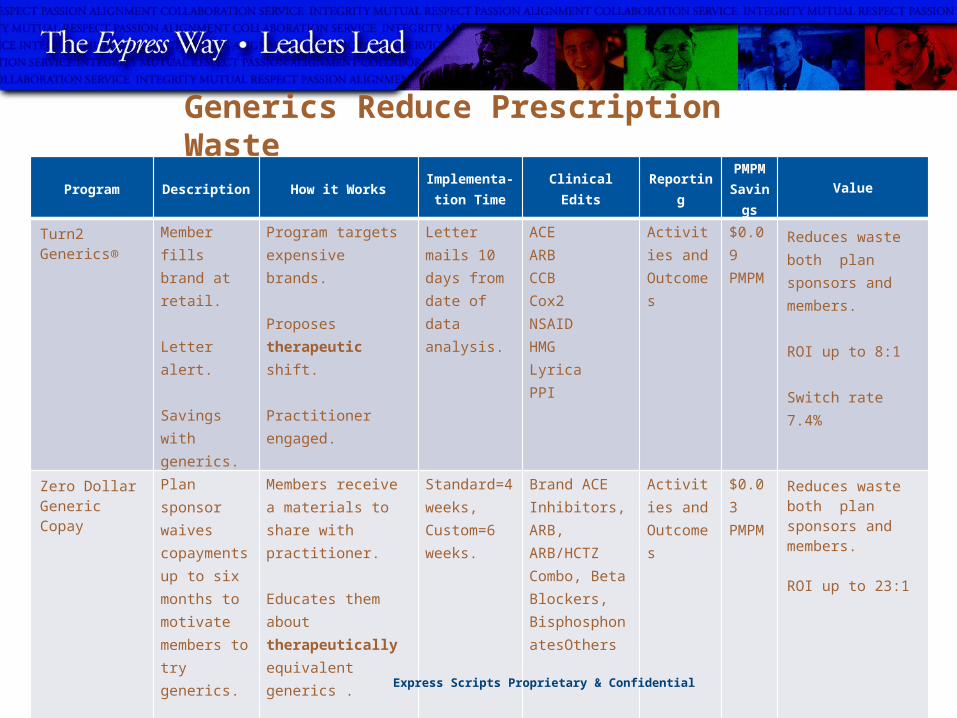

Generics Reduce Prescription Waste

Program Description How it Works Implementa-tion Time Clinical Edits Reporting PMPM

Savings Value

Turn2Generics®

Member fills brand at retail.

Letter alert.

Savings with generics.

Program targets expensive brands.

Proposes therapeutic shift.

Practitioner engaged.

Letter mails 10 days from date of data analysis.

ACEARBCCBCox2NSAIDHMGLyricaPPI

Activities and Outcomes

$0.09PMPM

Reduces waste both plan sponsors and members.

ROI up to 8:1

Switch rate 7.4%

Zero Dollar Generic Copay

Plan sponsor waives copayments up to six months to motivate members to try generics.

Members receive a materials to share with practitioner.

Educates them about therapeutically equivalent generics .

Notes they will have and $0 copayment if their physician provides a new prescription for a generic alternative.

Standard=4 weeks, Custom=6 weeks.

Brand ACE Inhibitors, ARB, ARB/HCTZ Combo, Beta Blockers, BisphosphonatesOthers

Activities and Outcomes

$0.03 PMPM

Reduces waste both plan sponsors and members.

ROI up to 23:1

Express Scripts Proprietary & Confidential

26

Express Scripts National Formularies

National Preferred Prime High PerformanceGeneric Drugs* 99.3% 99.3% 99.3%Brand Drugs* 54.6% 45% 36%

Features

Manages drug trend with a three-tier or open formulary benefit design

Features a broad brand selection and low-cost generic products

Manages drug trend with a three-tier or closed formulary benefit design

Limited number of brands

Aggressively manages drug trend with a closed formulary benefit design

Comprised of generics and the lowest cost brand drug in each therapeutic class

Trend FocusOptional Trend programs Recommended for

use with Enhanced Trend Package

Mandatory Trend Package

Ideal Plan Sponsor Type

Marginally managed$20 Copayment

differential and less

Well-managedGreater than $20

Copayment differential

AggressiveClosed benefit design

27

Summary

• Drug plans in the US that are actively managed by PBM's show significant savings compared to plans that are passively managed

• Much of the savings from actively managed US plans come from maximizing the use of generics

• Most plans in Canada are not actively managed (proven US PBM tools are not used) so generics are underutilized

• Savings opportunity for private plans in Canada with increased use of both interchangeable and therapeutically equivalent generics

28

Thank you

• Questions?

Related Documents