A Work Project, presented as part of the requirements for the Award of a Masters Degree in Finance from the NOVA – School of Business and Economics. Equity Report Adidas AG Ludwig Schwarzmayr (646) A Project carried out on the field lab course, under the supervision of: Prof. Rosario André 07.01.2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A Work Project, presented as part of the requirements for the Award of a Masters Degree in Finance from the NOVA – School of Business and Economics.

Equity Report Adidas AG

Ludwig Schwarzmayr (646)

A Project carried out on the field lab course, under the supervision of:

Prof. Rosario André

07.01.2015

THIS REPORT WAS PREPARED BY LUDWIG SCHWARZMAYR, A MASTERS IN FINANCE STUDENT OF THE NOVA SCHOOL OF BUSINESS

AND ECONOMICS, EXCLUSIVELY FOR ACADEMIC PURPOSES. THIS REPORT WAS SUPERVISED BY ROSÁRIO ANDRÉ WHO REVIEWED THE VALUATION METHODOLOGY AND THE FINANCIAL MODEL. (SEE DISCLOSURES AND DISCLAIMERS AT END OF DOCUMENT)

See more information at WWW.NOVASBE.PT Page 1/27

MASTERS IN FINANCE

EQUITY RESEARCH

! We confirm our previous buy recommendation with a

lower target price for the financial year 2015 of EUR 61.81. The

stock currently trades at a P/E ratio of 16.2x – a 24.3% discount

over its peers’ median. According to our analysis this is

exaggerated given Adidas’ strong cash flows and ability to

generate value to its shareholders.

! Adidas’ profits and cashflows come from the disposable

income of the people in the markets it serves. As a result, regions

with high disposable income, measured by GNI levels, and GDP

growth offer growth opportunities for the company. Adidas’ core

markets suffered strongly from the financial crisis. The company’s

inability to compete with Nike in the US market comes costly. The

slide of the Rubel additionally puts pressure on the revenues.

! Management announced to increase marketing initiatives

especially in the US, to gain much-needed market share. Also it

will lower the investment exposure on the Russian market by

closing more shops than re-opening them. On top a share buy

back program with a volume of EUR 1.5 billion was announced in

the second half of 2014

! Our YE15 target price is based on a DCF analysis. The

target price of EUR 61.81 implies an upside of 9.7% and a total

expected shareholder return of 15.4% on the current stock price.

Company description

Adidas AG is a German manufacturer of sports equipment, comprising the brands adidas, Reebok, TaylorMade, Rockport and CCM. The company was founded in 1949 by Adolf Dassler and has been listed on the Frankfurt Stock Exchange (Frankfurter Wertpapierbörse) since 1995. Adidas is listed in the German stock market index DAX (Deutscher Aktienindex).

ADIDAS AG COMPANY REPORT SPORTS APPAREL 07 JANUARY 2015

STUDENT: LUDWIG SCHWARZMAYR [email protected]

Regaining strength, slowly

Strong player in a weak macro environment

Recommendation: BUY

Vs Previous Recommendation BUY

Price Target FY15: 61.81 €

Vs Previous Price Target 66.64 €

Price (as of 3-Jan-15) 56.36 €

Reuters: ADSGn.DE, Bloomberg: ADS:GR

52-week range (€) 52.94-94.10

Market Cap (€m) 11,789.33

Outstanding Shares (m) 209.22

30-Day average volume 1,632,921

Source: Bloomberg

Source: S&P Capital IQ

(Values in € millions) 2013 2014E 2015F

Revenues 14,492 13,619 13,511

EBITDA 1,542 1,226 1,087

EBITDA growth 6.5% -20.5% -11.3%

Net Profit 790 614 512

EPS 3.76 3.01 2.59

Payout ratio 36% 37% 38%

Dividends per Share 1.35 1.50 1.14

Net Debt / EBITDA 0.07 0.13 0.39

Net Debt to Equity 2.1% 3.2% 8.8%

Source: Adidas AG Annual Report 2013, Analyst’s Estimates

-20% 0% 20% 40% 60% 80% 100%

02.01.12 02.01.13 02.01.14

MSCI World DAX Adidas AG

speralta

Rectangle

ADIDAS AG COMPANY REPORT

PAGE 2/27

Table of Contents

I. INVESTMENT CASE ............................................................................... 3!II. UNDERSTANDING THE BUSINESS ..................................................... 4!

A) BUSINESS OVERVIEW ........................................................................................ 4!B) ECONOMIC OVERVIEW ...................................................................................... 6!

Economic Development ........................................................................ 6!Peer Companies .................................................................................... 8!

C) BRAND OVERVIEW .......................................................................................... 10!adidas .................................................................................................. 11!Reebok ................................................................................................. 11!TaylorMade-adidas Golf .................................................................... 12!Rockport & Reebok-CCM Hockey ...................................................... 12!

D) DISTRIBUTION CHANNELS .............................................................................. 12!Wholesale ............................................................................................ 13!Retail ................................................................................................... 13!

III. FORECASTS ....................................................................................... 15!A) ECONOMIC FORECASTS ................................................................................... 15!B) SEGMENTAL FORECASTS ................................................................................. 16!

Wholesale ............................................................................................ 16!Retail ................................................................................................... 17!Other businesses ................................................................................. 18!

C) BUSINESS FORECASTS ..................................................................................... 18!Strategic Focus ................................................................................... 18!

IV. VALUATION ........................................................................................ 19!A) COMPARABLES ................................................................................................ 19!B) DISCOUNTED CASH FLOW ANALYSIS .............................................................. 20!

WACC ................................................................................................. 20!Perpetual Growth ............................................................................... 21!Sum of Parts ........................................................................................ 21!Sensitivity Analysis ............................................................................. 21!

V. APPENDIX ........................................................................................... 22!APPENDIX 1: FINANCIAL STATEMENT & CF MAP ............................................... 22!APPENDIX 2: VALUATION .................................................................................... 24!APPENDIX 3: SENSITIVITY ANALYSIS .................................................................. 25!APPENDIX 4: APPAREL AND FOOTWEAR INDUSTRY ............................................ 26!

VI.! DISCLOSURES AND DISCLAIMER ................................................ 27!

ADIDAS AG COMPANY REPORT

PAGE 3/27

I. INVESTMENT CASE Adidas is the second largest player in the sports apparel industry with total

revenues of EUR 14.5 billion and operations in Europe, Asia and Americas. Its

product range covers the entire spectrum of apparel goods ranging from sportive

fashion to high-performance apparel for competitive athletes. The goods are sold

through wholesale (63%), retail (24%) and eCommerce.

The company’s biggest competitor is Nike. The US firm leads the industry in

terms of sales. This is mainly due to its dominant market position in the US, the

industry’s most lucrative and important region. Adidas tried to buy market share

in this region by acquiring Reebok in 2006. However, so far, it failed to improve

its market position but lost share to Nike. Only EUR 3.1 billion revenues were

generated in 2013 compared to EUR 10.5 billion US revenues from Nike.

During the financial year 2014 the golfing sector got under strong pressure. Due

to stagnating player numbers in the US and Europe, sales plummeted, leaving

companies in this sector with high amounts of inventories. Revenues are

estimated to decrease double-digit in 2014. Adidas’ CEO announced to reduce

the company’s golfing inventory and to restructure the division in order to align it

to the industry’s lower future growth expectations.

The year 2014 was also affected by the Ukraine crisis and the following sanctions

against Russia. As a high prospect emerging country, Russia is amongst Adidas’

most important growth regions. Therefore the company has a high exposure in

this region. The fall of the Rubel towards the end of 2014 is expected to have a

destructive influence on Adidas’ revenues generated in this region. The total net

profit of 2014 is expected to be about EUR 600 million, in line with the

management’s prediction.

Management had to issue already three profit warnings within the last year. The

weak macroeconomic situation seems to punish Adidas for not having sufficient

market share in the stable US market. Management therefore announced to

increase marketing budgets, trying to gain market share in the US. Also it is

trying to lower the investment exposure to the Russian market by increasing the

retail shop closings and decreasing the openings. Additionally management

announced a share buy back program of about EUR 1.5 billion.

We therefore issue a buy recommendation and a target price of EUR 61.81 for

the shares of Adidas, representing an upside of 9.7% on the current stock price

and a total expected shareholder return of 15.4%.

Second largest player in the sports apparel industry

Biggest competitor is Nike, dominating the US market

Golfing sector sales decrease double-digit

Russian Rubel in free-fall

Management announced share buy back program

BUY recommendation with EUR 61.81 target price

ADIDAS AG COMPANY REPORT

PAGE 4/27

II. UNDERSTANDING THE BUSINESS Adidas AG is a German manufacturer of sports equipment, comprising the

brands adidas, Reebok, TaylorMade, Rockport and CCM. The company was

founded in 1949 by Adolf Dassler and has been listed on the Frankfurt Stock

Exchange (Frankfurter Wertpapierbörse) since 1995. Adidas is listed in the

German stock market index DAX (Deutscher Aktienindex), which is composed of

30 local stocks, whereof Adidas currently constitutes approximately 1.9% of it.

Valued by the market, Adidas has a market cap of about EUR 12 billion. This

makes the company only second biggest globally far behind its competitor Nike

Inc (Market cap of USD 82 billion) and quite ahead of Puma (Market cap of EUR

2.6 billion). In terms of stock performance Nike clearly outperformed Adidas and

Puma in 2014 with +25% over –36% and –26% respectively (see figure 1).

Adidas’ stock however managed to outperform its index, the DAX, steadily from

2009 to 2013. In 2014, due to reasons elaborated later in more detail, the stock

clearly underperformed the index, but still leaving investors, who invested in early

2010, with the same approximate stock performance as the index (see figure 2).

The company’s dividend policy aims to payout a 20%-40% dividend of annual net

income to its shareholders. In the last years Adidas managed to steadily increase

the payout ratio, reaching 36% (EUR 1.35 per share) in 2013 (see figure 3).

No investor in the company is holding a majority of the voting rights of the

company. As biggest single investor Société Générale S.A. can be considered

with a share of 5.09% as per year-end 2014. The global spread of shareholders

shows a strong focus on North America (see figure 4). Current CEO of the

company is Herbert Hainer.

Growth of the company was made through major acquisitions in the past and

through organic growth from thereon. In 2006 Adidas acquired its British rival

Reebok for USD 3.8 billion, giving it direct access to the North American market.

In 2011 the company acquired outdoor specialist Five Ten for USD 25 million.

Through acquisitions of Ashworth in 2009, TaylorMade in 2011 and Adams Golf

in 2012, Adidas gained access to the golfing market.

a) BUSINESS OVERVIEW

Adidas is the largest European sportswear manufacturer and second largest in

the world. It typically outsources manufacturing of its products to Asia and

focuses on innovation and design of products. The company separates its

business by its brands in order to tackle different markets and different clienteles

at the same time. As can be seen from figure 5, the company’s original brand

Figure 2: Adidas vs DAX

Adidas DAX

Source: Yahoo Finance

37%

32%

14%

10% 5% 2%

Figure 4: Shareholder structure

Rest of Europe North America Other

Germany Rest of World Management

Source: Adidas AG

Source: Adidas AG, Annual Reports

17% 18% 15% 30% 29% 34% 36%

0,42 0,50 0,50

0,35

0,80

1,00

1,35

Figure 3: Dividends

% Payout Ratio EUR Dividend

Source: Yahoo Finance

Figure 1: Peer comparison

Adidas Puma SE Nike Inc

ADIDAS AG COMPANY REPORT

PAGE 5/27

adidas adds the most to the group’s revenues. In 2013 it accounted for about

76% (EUR 10,961 million) of total revenues.

The distribution channels used to generate these revenues are either via

wholesale, having one or more intermediates between the producer and the end

customer, or via retail, directly selling its own products. The biggest part of

revenues is generated through wholesale (see figure 6), contributing roughly

63% (EUR 9,100 million) in 2013. The retail channel, which contributed about

24% in 2013, can further be subdivided into concept stores, factory outlets,

eCommerce and concession corners, contributing 46%, 44%, 7% and 3% of

retail sales in 2013 respectively.

As per the regional distribution of the sales, the company generates most of its

sales within its core market Western Europe, the rest mainly within the industry’s

most important market North America and the biggest growth opportunity Asia

(see figure 7). However, Adidas still has only a minor share in the total North

American market compared to Nike, which generates about quadruple of Adidas’

revenues in America (EUR 10.5 billion compared to EUR 3.1 billion in 2013).

On a total sales basis Nike was able to generate about EUR 23.9 billion in 2013.

This is only slightly below double of what Adidas generated (EUR 14.5 billion)

and about eightfold of Puma’s 2013 revenues of about EUR 2.9 billion. The total

apparel, footwear and accessories industry is estimated to have total revenues of

about EUR 260 billion in 2014 according to Bloomberg1. Nike is estimated to

have about 8.5% of market share, while Adidas only has 4.5%.

Vietnam, China and Indonesia account for the majority of the production volume

for footwear, apparel and hardware. The group operates a limited number (10) of

own production and assembly sites in Germany, Finland, USA and Canada. While Vietnam is the most important sourcing country for footwear production

with 35% of the total volume, China dominates the apparel and hardware

production with 33% and 40% respectively (see figure 8).

Through sponsorships of teams and individual athletes, Adidas is trying to

establish a brand awareness and preference for the customer. The marketing

working budget accounts for about 24% of total operating expenses and

therefore is a material component. As an example, Adidas sponsored the 2012

Olympic Games in London and is currently holding the official ball supplier rights

for the FIFA and UEFA tournaments. Recently it acquired the sponsorship rights

for Manchester United for the next ten years for roughly GBP 750 million. The

company hopes to return sales of about GBP 1.5 billion through this deal over the

1 Bloomberg. 2014. “Industry Market Leaders.” Retrieved from: http://www.bloomberg.com/visual-data/industries/detail/apparel,-footwear,-acc-design

7498 8639 9767 11186 10961

2009 2010 2011 2012 2013

Figure 5: Revenue by brand

adidas Reebok adidas Golf

Rockport Reebok-CCM other

Source: Adidas AG, Annual Reports

7174 8181 8949 9533 9100

1906 2389 2793 3373 3446

1283 1420

1580 1977 1946

2009 2010 2011 2012 2013

Figure 6: Revenue by distribution channel

Wholesale Retail Other

Source: Adidas AG, Annual Reports

Nike is the distinct market leader…

Source: Adidas AG, Annual Report 2013

26%

13%

23%

11%

15%

11%

Figure 7: Revenue by region

Europe European EM North america

Greater china Other asia Latin america

ADIDAS AG COMPANY REPORT

PAGE 6/27

next decade2. However, with a gross margin of slightly below 50% for the

company’s total sales and a 50% marketing expenditure on the sales predicted

by this investment we see a high risk of value destruction for the shareholders.

Adidas sees technological innovation as essential for sustainable leadership in

the industry. The R&D focus for its products is on cushioning and energy

solutions, lightweight and digital sports technologies as well as sustainable

product innovation. But also on new means of manufacturing processes and

advanced materials, such as machine knitting and 3-D printing. However, R&D

expenses in 2013 were only 2% of operating expenses.

b) ECONOMIC OVERVIEW

As a proxy for market size we use the Bloomberg estimation for the global

apparel, footwear and accessories industry of about EUR 260 billion, previously

mentioned. In order to estimate the potential growth of the overall sporting goods

market, we use metrics like GDP growth and GNI per capita. While the gross

domestic product growth rate gives us a reasonable estimate of the economic

growth of a region, the gross national income per capita and its performance over

time gives us a reasonable estimate of the disposable income within a region and

whether or not the region might be or become a potential market for the sporting

goods industry. As additional indirect market potential sign we will use the

percentage of people at the age of 15-64 years within a region, since people

within this group are assumed to potentially spend the most money on fitness

products.

ECONOMIC DEVELOPMENT

GDP growth

Over the past 40 years, global markets developed quite differently in terms of

GDP growth. While the Asian markets were able to grow 5% on average, the

Latin American markets grew 4% on average and European and North American

markets grew 3% on average. Against expectations, the difference in volatility

over the same period is only minor for those regions, with only 0.5% higher

standard deviation of Asian markets than European and North American markets

(see figure 9). African markets grew from an average of 3.5% in the sub-

Saharan region to 4.9% in the Middle East and North Africa. Due to the high

political risks in this region the volatility was significantly higher. The German

market in special was only able to grow at an average rate of 2% annually with a

standard deviation of 2%, while the world in total had an average GDP growth of

2 Robinson, D., Ross, A. 2014. “Man Utd seal £750m Adidas tie-up.” Financial Times, 14 July 2014.

78%

14%

7% 1%

Figure 8: Suppliers by region

Asia Americas Europe Africa

Source: Adidas AG, Annual Reports

EUR 260 billion industry revenues in 2014…

Source: World Bank national accounts data, and OECD National Accounts data files

-5,0%

0,0%

5,0%

10,0%

1960 1970 1980 1990 2000 2010

Figure 9: GDP growth

Europe Asia

North America Latin America

ADIDAS AG COMPANY REPORT

PAGE 7/27

3.5% with a standard deviation of 1.7%3. As a result we see real economic

growth on a global basis with emphasis on Asia, Africa and Latin America.

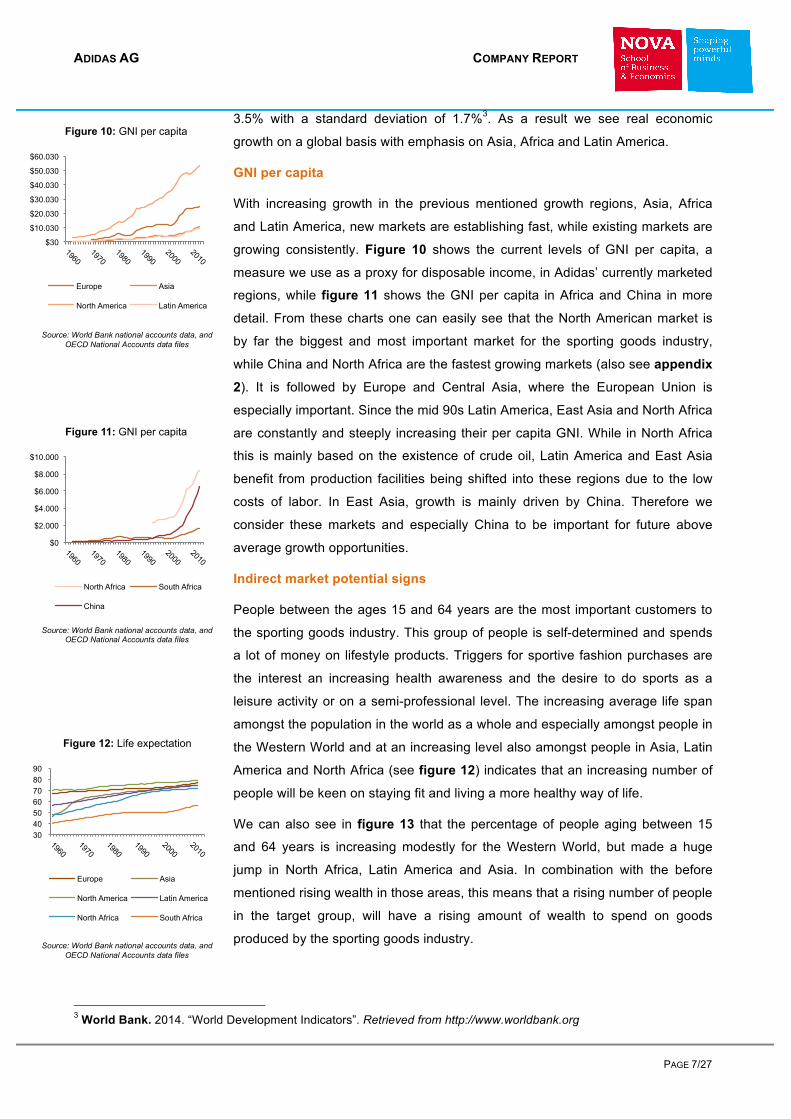

GNI per capita

With increasing growth in the previous mentioned growth regions, Asia, Africa

and Latin America, new markets are establishing fast, while existing markets are

growing consistently. Figure 10 shows the current levels of GNI per capita, a

measure we use as a proxy for disposable income, in Adidas’ currently marketed

regions, while figure 11 shows the GNI per capita in Africa and China in more

detail. From these charts one can easily see that the North American market is

by far the biggest and most important market for the sporting goods industry,

while China and North Africa are the fastest growing markets (also see appendix

2). It is followed by Europe and Central Asia, where the European Union is

especially important. Since the mid 90s Latin America, East Asia and North Africa

are constantly and steeply increasing their per capita GNI. While in North Africa

this is mainly based on the existence of crude oil, Latin America and East Asia

benefit from production facilities being shifted into these regions due to the low

costs of labor. In East Asia, growth is mainly driven by China. Therefore we

consider these markets and especially China to be important for future above

average growth opportunities.

Indirect market potential signs

People between the ages 15 and 64 years are the most important customers to

the sporting goods industry. This group of people is self-determined and spends

a lot of money on lifestyle products. Triggers for sportive fashion purchases are

the interest an increasing health awareness and the desire to do sports as a

leisure activity or on a semi-professional level. The increasing average life span

amongst the population in the world as a whole and especially amongst people in

the Western World and at an increasing level also amongst people in Asia, Latin

America and North Africa (see figure 12) indicates that an increasing number of

people will be keen on staying fit and living a more healthy way of life.

We can also see in figure 13 that the percentage of people aging between 15

and 64 years is increasing modestly for the Western World, but made a huge

jump in North Africa, Latin America and Asia. In combination with the before

mentioned rising wealth in those areas, this means that a rising number of people

in the target group, will have a rising amount of wealth to spend on goods

produced by the sporting goods industry.

3 World Bank. 2014. “World Development Indicators”. Retrieved from http://www.worldbank.org

Source: World Bank national accounts data, and OECD National Accounts data files

$0

$2.000

$4.000

$6.000

$8.000

$10.000

Figure 11: GNI per capita

North Africa South Africa

China

Source: World Bank national accounts data, and OECD National Accounts data files

$30

$10.030

$20.030

$30.030

$40.030

$50.030

$60.030

Figure 10: GNI per capita

Europe Asia

North America Latin America

30 40 50 60 70 80 90

Figure 12: Life expectation

Europe Asia

North America Latin America

North Africa South Africa

Source: World Bank national accounts data, and OECD National Accounts data files

ADIDAS AG COMPANY REPORT

PAGE 8/27

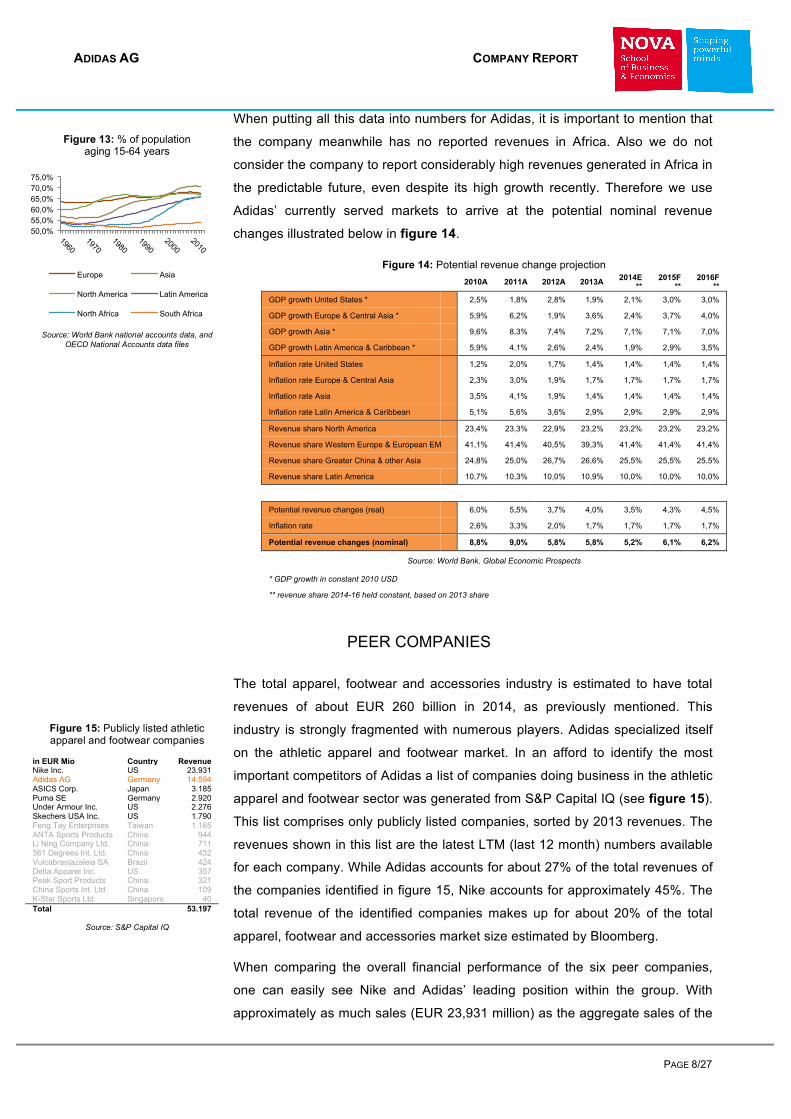

When putting all this data into numbers for Adidas, it is important to mention that

the company meanwhile has no reported revenues in Africa. Also we do not

consider the company to report considerably high revenues generated in Africa in

the predictable future, even despite its high growth recently. Therefore we use

Adidas’ currently served markets to arrive at the potential nominal revenue

changes illustrated below in figure 14.

Figure 14: Potential revenue change projection

2010A 2011A 2012A 2013A 2014E **

2015F **

2016F **

GDP growth United States * 2,5% 1,8% 2,8% 1,9% 2,1% 3,0% 3,0%

GDP growth Europe & Central Asia * 5,9% 6,2% 1,9% 3,6% 2,4% 3,7% 4,0%

GDP growth Asia * 9,6% 8,3% 7,4% 7,2% 7,1% 7,1% 7,0%

GDP growth Latin America & Caribbean * 5,9% 4,1% 2,6% 2,4% 1,9% 2,9% 3,5%

Inflation rate United States 1,2% 2,0% 1,7% 1,4% 1,4% 1,4% 1,4%

Inflation rate Europe & Central Asia 2,3% 3,0% 1,9% 1,7% 1,7% 1,7% 1,7%

Inflation rate Asia 3,5% 4,1% 1,9% 1,4% 1,4% 1,4% 1,4%

Inflation rate Latin America & Caribbean 5,1% 5,6% 3,6% 2,9% 2,9% 2,9% 2,9%

Revenue share North America 23,4% 23,3% 22,9% 23,2% 23,2% 23,2% 23,2%

Revenue share Western Europe & European EM 41,1% 41,4% 40,5% 39,3% 41,4% 41,4% 41,4%

Revenue share Greater China & other Asia 24,8% 25,0% 26,7% 26,6% 25,5% 25,5% 25,5%

Revenue share Latin America 10,7% 10,3% 10,0% 10,9% 10,0% 10,0% 10,0%

Potential revenue changes (real) 6,0% 5,5% 3,7% 4,0% 3,5% 4,3% 4,5%

Inflation rate 2,6% 3,3% 2,0% 1,7% 1,7% 1,7% 1,7%

Potential revenue changes (nominal) 8,8% 9,0% 5,8% 5,8% 5,2% 6,1% 6,2%

Source: World Bank, Global Economic Prospects

* GDP growth in constant 2010 USD

** revenue share 2014-16 held constant, based on 2013 share

PEER COMPANIES

The total apparel, footwear and accessories industry is estimated to have total

revenues of about EUR 260 billion in 2014, as previously mentioned. This

industry is strongly fragmented with numerous players. Adidas specialized itself

on the athletic apparel and footwear market. In an afford to identify the most

important competitors of Adidas a list of companies doing business in the athletic

apparel and footwear sector was generated from S&P Capital IQ (see figure 15).

This list comprises only publicly listed companies, sorted by 2013 revenues. The

revenues shown in this list are the latest LTM (last 12 month) numbers available

for each company. While Adidas accounts for about 27% of the total revenues of

the companies identified in figure 15, Nike accounts for approximately 45%. The

total revenue of the identified companies makes up for about 20% of the total

apparel, footwear and accessories market size estimated by Bloomberg.

When comparing the overall financial performance of the six peer companies,

one can easily see Nike and Adidas’ leading position within the group. With

approximately as much sales (EUR 23,931 million) as the aggregate sales of the

in EUR Mio Country Revenue Nike Inc. US 23.931 Adidas AG Germany 14.594 ASICS Corp. Japan 3.185 Puma SE Germany 2.920 Under Armour Inc. US 2.276 Skechers USA Inc. US 1.790 Feng Tay Enterprises Taiwan 1.165 ANTA Sports Products China 944 Li Ning Company Ltd. China 711 361 Degrees Int. Ltd. China 432 Vulcabras|azaleia SA Brazil 424 Delta Apparel Inc. US 357 Peak Sport Products China 321 China Sports Int. Ltd. China 109 K-Star Sports Ltd. Singapore 40 Total 53.197

50,0% 55,0% 60,0% 65,0% 70,0% 75,0%

Figure 13: % of population aging 15-64 years

Europe Asia

North America Latin America

North Africa South Africa

Source: World Bank national accounts data, and OECD National Accounts data files

Figure 15: Publicly listed athletic apparel and footwear companies

Source: S&P Capital IQ

ADIDAS AG COMPANY REPORT

PAGE 9/27

other companies, Nike is the biggest company in the peer group. Nike is also the

leading company when it comes to EBITDA margin (15%) and income margin

(10%) (see figure 16).

As one can easily see, the most important area for the peer group identified is

North America, accounting for roughly 39% of sales generated, followed by the

European area, in which about 29% of total sales were earned. The biggest

player in North America is without doubt Nike, earning more revenues than the

aggregated other five companies shown (see figure 17). The distinct market

leadership in terms of revenues in the industry’s most important market America

and the stalemate in Europe gives Nike a very strong competitive advantage over

Adidas. Within the American market there are also local players who emerged in

recent years, like Under Armour, which managed to quadruple revenues in the

past 5 years to about EUR 2,275 million currently.

45% 48% 44% 46% 49%

45%

15% 8%

12%

1%

13% 11% 10% 4% 7% 6% 6%

0%

10%

20%

30%

40%

50%

60%

€ 0

€ 5.000

€ 10.000

€ 15.000

€ 20.000

€ 25.000

Nike Inc. Adidas AG ASICS Corp. Puma SE Under Armour Inc. Skechers USA Inc.

Figure 16: Financial performance in Mio EUR and margins in % (2013)

Revenue Gross Profit EBITDA Net Income

% Gross Margin % EBITDA Margin % Income Margin

Nike Inc. Adidas AG ASICS Corp. Puma SE Under Armour Inc.

Skechers USA Inc.

others 1.547 - -13 331 189 543

Japan 613 - 866 - - -

China 2.281 1.733 259 - - -

Emerging Markets 3.238 3.762 152 562 - -

North America 10.548 3.100 997 919 2.086 1.246

Europe 5.705 5.999 924 1.108 - -

€ 0

€ 5.000

€ 10.000

€ 15.000

€ 20.000

€ 25.000

€ 30.000

Figure 17: revenues per region in EUR Mio (2013)

Source: S&P Capital IQ

Source: S&P Capital IQ

Adidas has comparably low EBITDA and income margins but high gross margin…

North America accounts for 39% of sales generated by peer group…

Local players emerged and rose in recent years…

Nike has distinct market leadership in North America…

ADIDAS AG COMPANY REPORT

PAGE 10/27

Adidas stated in its latest Q3 report that regaining share in the North American

market is the top priority, carrying out significant changes in Management and

investing in NBA athletes and the NFL. The marketing working budget

expenditures increased by 8% overall, 11% for adidas and 8% for Reebok. As

can be seen in figure 16, while Nike has about 60% higher revenues, the

marketing budgets for both companies are almost the same (see figure 18). This

affects the EBITDA margin of Adidas negatively and explains why Adidas has a

significantly lower EBITDA margin than Nike (8% vs 15%), despite having a

higher gross margin (48% vs 45%).

Nike

Nike can by far be considered Adidas’ main competitor. The company is currently

holding the market leadership and was leading the market in terms of revenues

for the past 10 years (see figure 19). Although in past years, Adidas was able to

lessen the gap, since 2011 Nike is again starting to increase its lead. Using the

latest numbers, while Adidas was able to be more efficient when it comes to

gross margin, Nike was able to achieve a higher EBITDA and profit margin (see

figure 16). As previously mentioned this is mainly due to the increasing

marketing effort of Adidas.

Nike’s dominant position in the North American market, which is considered the

most important in the sporting goods industry, gives the company a big

advantage. The extent can be seen in figure 17. Nike is able to generate more

than triple the revenues of Adidas in the North American market. These revenues

alone are about 2/3 of Adidas’ total revenues. The equity markets also tend to

value Nike’s earnings with a higher P/E ratio. While one can see from figure 1

that an investment in Adidas and Nike would have approximately yielded the

same returns until 2013, it becomes obvious from figure 20 that the equity

market tends to value revenues generated by Nike at a higher P/E ratio than the

ones generated by Adidas.

Nike faces not only competition by Adidas, its closest competitor, but also from

companies such as Under Armour. This company specialized itself in some niche

markets in North America, like martial arts apparel and thermo underwear.

However, despite its high sales growth (400% within the last 5 years), the

company is not considered as a major threat for Nike or Adidas in the near future.

c) BRAND OVERVIEW

Adidas AG separates its business by its brands. The original brand, adidas, is

separated into adidas Sport Performance, adidas Sport Style and adidas

Originals. All three of them generated EUR 11 billion worth of sales in 2013. As

2.223 1.882

186

978

179 86

11% 13% 8%

33%

11% 6%

0% 5% 10% 15% 20% 25% 30% 35%

€ 0

€ 500

€ 1.000

€ 1.500

€ 2.000

€ 2.500

Figure 18: marketing expenses in Mio EUR and % sales (2013)

Marketing exp. Marketing % sales

Source: S&P Capital IQ

€ 20.416

€ 14.492

€ 0

€ 5.000

€ 10.000

€ 15.000

€ 20.000

€ 25.000

Figure 19: Adidas vs Nike revenue historical EUR Mio

Nike Adidas

Source: Adidas Annual Reports, Nike Annual Reports

16.0

24.9

10 12 14 16 18 20 22 24 26 28

2009 2010 2011 2012 2013

Figure 20: Adidas vs Nike Forward P/E ratio

Adidas Nike

Source: S&P Capital IQ

ADIDAS AG COMPANY REPORT

PAGE 11/27

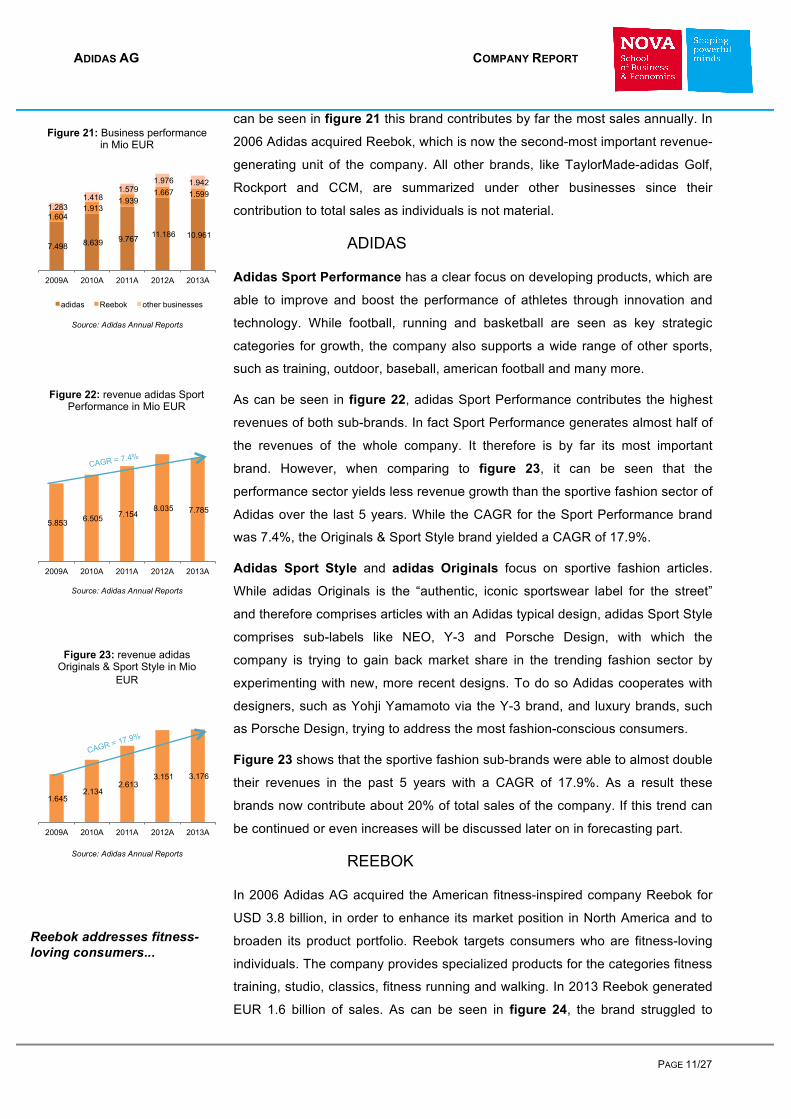

can be seen in figure 21 this brand contributes by far the most sales annually. In

2006 Adidas acquired Reebok, which is now the second-most important revenue-

generating unit of the company. All other brands, like TaylorMade-adidas Golf,

Rockport and CCM, are summarized under other businesses since their

contribution to total sales as individuals is not material.

ADIDAS

Adidas Sport Performance has a clear focus on developing products, which are

able to improve and boost the performance of athletes through innovation and

technology. While football, running and basketball are seen as key strategic

categories for growth, the company also supports a wide range of other sports,

such as training, outdoor, baseball, american football and many more.

As can be seen in figure 22, adidas Sport Performance contributes the highest

revenues of both sub-brands. In fact Sport Performance generates almost half of

the revenues of the whole company. It therefore is by far its most important

brand. However, when comparing to figure 23, it can be seen that the

performance sector yields less revenue growth than the sportive fashion sector of

Adidas over the last 5 years. While the CAGR for the Sport Performance brand

was 7.4%, the Originals & Sport Style brand yielded a CAGR of 17.9%.

Adidas Sport Style and adidas Originals focus on sportive fashion articles.

While adidas Originals is the “authentic, iconic sportswear label for the street”

and therefore comprises articles with an Adidas typical design, adidas Sport Style

comprises sub-labels like NEO, Y-3 and Porsche Design, with which the

company is trying to gain back market share in the trending fashion sector by

experimenting with new, more recent designs. To do so Adidas cooperates with

designers, such as Yohji Yamamoto via the Y-3 brand, and luxury brands, such

as Porsche Design, trying to address the most fashion-conscious consumers.

Figure 23 shows that the sportive fashion sub-brands were able to almost double

their revenues in the past 5 years with a CAGR of 17.9%. As a result these

brands now contribute about 20% of total sales of the company. If this trend can

be continued or even increases will be discussed later on in forecasting part.

REEBOK

In 2006 Adidas AG acquired the American fitness-inspired company Reebok for

USD 3.8 billion, in order to enhance its market position in North America and to

broaden its product portfolio. Reebok targets consumers who are fitness-loving

individuals. The company provides specialized products for the categories fitness

training, studio, classics, fitness running and walking. In 2013 Reebok generated

EUR 1.6 billion of sales. As can be seen in figure 24, the brand struggled to

Reebok addresses fitness-loving consumers...

7.498 8.639 9.767 11.186 10.961

1.604 1.913

1.939 1.667 1.599

1.283 1.418

1.579 1.976 1.942

2009A 2010A 2011A 2012A 2013A

Figure 21: Business performance in Mio EUR

adidas Reebok other businesses

Source: Adidas Annual Reports

5.853 6.505 7.154 8.035 7.785

2009A 2010A 2011A 2012A 2013A

Figure 22: revenue adidas Sport Performance in Mio EUR

Source: Adidas Annual Reports

CAGR = 7.4%

1.645 2.134

2.613 3.151 3.176

2009A 2010A 2011A 2012A 2013A

Figure 23: revenue adidas Originals & Sport Style in Mio

EUR

Source: Adidas Annual Reports

CAGR = 17.9%

ADIDAS AG COMPANY REPORT

PAGE 12/27

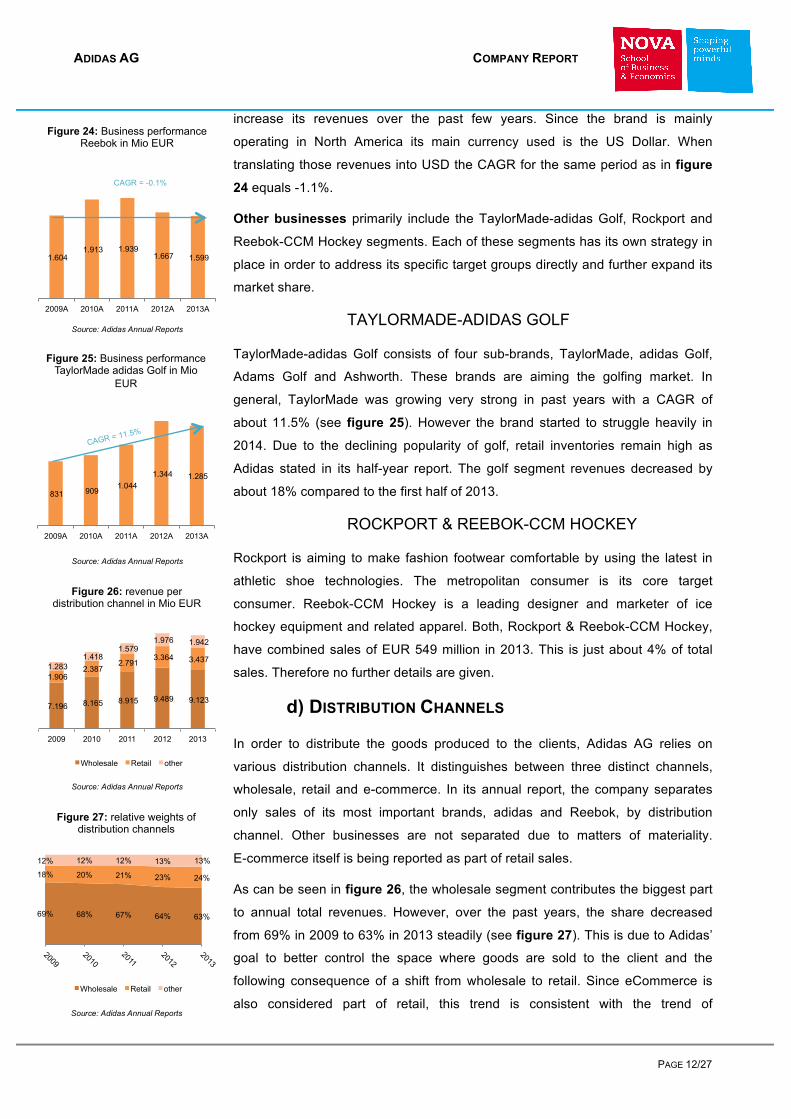

increase its revenues over the past few years. Since the brand is mainly

operating in North America its main currency used is the US Dollar. When

translating those revenues into USD the CAGR for the same period as in figure

24 equals -1.1%.

Other businesses primarily include the TaylorMade-adidas Golf, Rockport and

Reebok-CCM Hockey segments. Each of these segments has its own strategy in

place in order to address its specific target groups directly and further expand its

market share.

TAYLORMADE-ADIDAS GOLF

TaylorMade-adidas Golf consists of four sub-brands, TaylorMade, adidas Golf,

Adams Golf and Ashworth. These brands are aiming the golfing market. In

general, TaylorMade was growing very strong in past years with a CAGR of

about 11.5% (see figure 25). However the brand started to struggle heavily in

2014. Due to the declining popularity of golf, retail inventories remain high as

Adidas stated in its half-year report. The golf segment revenues decreased by

about 18% compared to the first half of 2013.

ROCKPORT & REEBOK-CCM HOCKEY

Rockport is aiming to make fashion footwear comfortable by using the latest in

athletic shoe technologies. The metropolitan consumer is its core target

consumer. Reebok-CCM Hockey is a leading designer and marketer of ice

hockey equipment and related apparel. Both, Rockport & Reebok-CCM Hockey,

have combined sales of EUR 549 million in 2013. This is just about 4% of total

sales. Therefore no further details are given.

d) DISTRIBUTION CHANNELS

In order to distribute the goods produced to the clients, Adidas AG relies on

various distribution channels. It distinguishes between three distinct channels,

wholesale, retail and e-commerce. In its annual report, the company separates

only sales of its most important brands, adidas and Reebok, by distribution

channel. Other businesses are not separated due to matters of materiality.

E-commerce itself is being reported as part of retail sales.

As can be seen in figure 26, the wholesale segment contributes the biggest part

to annual total revenues. However, over the past years, the share decreased

from 69% in 2009 to 63% in 2013 steadily (see figure 27). This is due to Adidas’

goal to better control the space where goods are sold to the client and the

following consequence of a shift from wholesale to retail. Since eCommerce is

also considered part of retail, this trend is consistent with the trend of

1.604 1.913 1.939

1.667 1.599

2009A 2010A 2011A 2012A 2013A

Figure 24: Business performance Reebok in Mio EUR

Source: Adidas Annual Reports

CAGR = -0.1%

831 909 1.044 1.344 1.285

2009A 2010A 2011A 2012A 2013A

Figure 25: Business performance TaylorMade adidas Golf in Mio

EUR

Source: Adidas Annual Reports

CAGR = 11.5%

7.196 8.165 8.915 9.489 9.123

1.906 2.387

2.791 3.364 3.437

1.283 1.418

1.579 1.976 1.942

2009 2010 2011 2012 2013

Figure 26: revenue per distribution channel in Mio EUR

Wholesale Retail other

Source: Adidas Annual Reports

Source: Adidas Annual Reports

69% 68% 67% 64% 63%

18% 20% 21% 23% 24%

12% 12% 12% 13% 13%

Figure 27: relative weights of distribution channels

Wholesale Retail other

ADIDAS AG COMPANY REPORT

PAGE 13/27

Source: Adidas Annual Reports

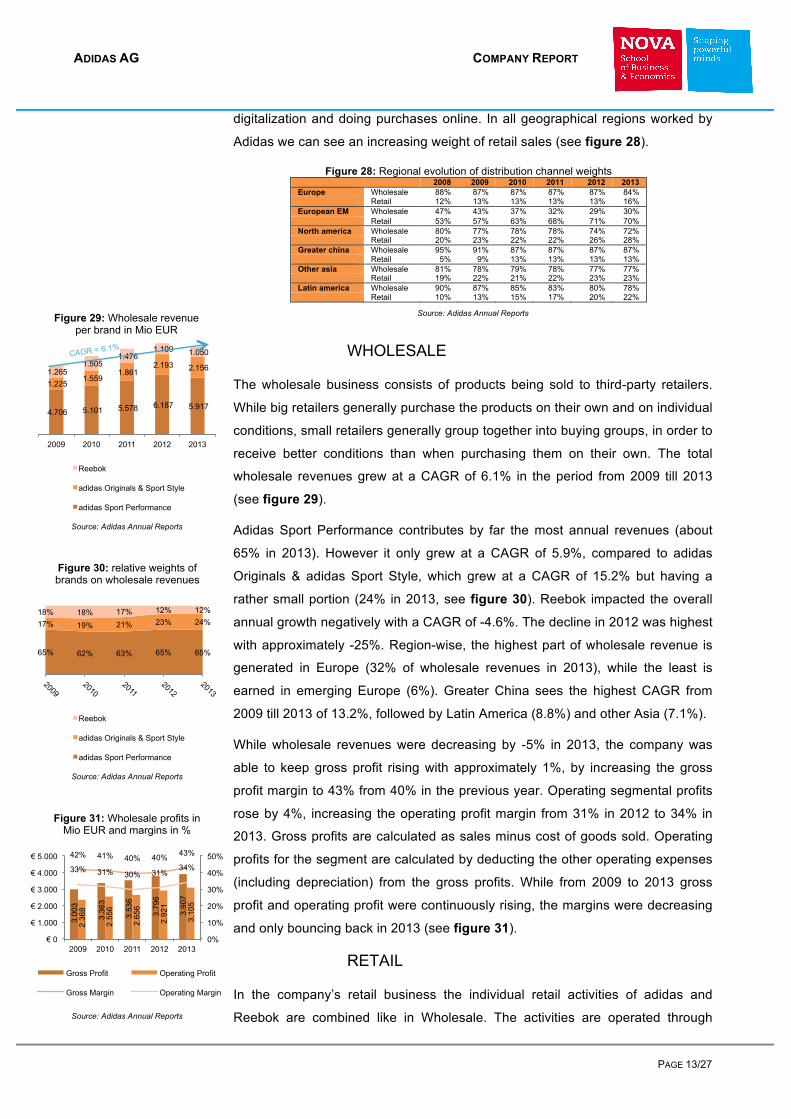

digitalization and doing purchases online. In all geographical regions worked by

Adidas we can see an increasing weight of retail sales (see figure 28).

Figure 28: Regional evolution of distribution channel weights 2008 2009 2010 2011 2012 2013 Europe Wholesale 88% 87% 87% 87% 87% 84% Retail 12% 13% 13% 13% 13% 16% European EM Wholesale 47% 43% 37% 32% 29% 30% Retail 53% 57% 63% 68% 71% 70% North america Wholesale 80% 77% 78% 78% 74% 72% Retail 20% 23% 22% 22% 26% 28% Greater china Wholesale 95% 91% 87% 87% 87% 87% Retail 5% 9% 13% 13% 13% 13% Other asia Wholesale 81% 78% 79% 78% 77% 77% Retail 19% 22% 21% 22% 23% 23% Latin america Wholesale 90% 87% 85% 83% 80% 78% Retail 10% 13% 15% 17% 20% 22%

WHOLESALE

The wholesale business consists of products being sold to third-party retailers.

While big retailers generally purchase the products on their own and on individual

conditions, small retailers generally group together into buying groups, in order to

receive better conditions than when purchasing them on their own. The total

wholesale revenues grew at a CAGR of 6.1% in the period from 2009 till 2013

(see figure 29).

Adidas Sport Performance contributes by far the most annual revenues (about

65% in 2013). However it only grew at a CAGR of 5.9%, compared to adidas

Originals & adidas Sport Style, which grew at a CAGR of 15.2% but having a

rather small portion (24% in 2013, see figure 30). Reebok impacted the overall

annual growth negatively with a CAGR of -4.6%. The decline in 2012 was highest

with approximately -25%. Region-wise, the highest part of wholesale revenue is

generated in Europe (32% of wholesale revenues in 2013), while the least is

earned in emerging Europe (6%). Greater China sees the highest CAGR from

2009 till 2013 of 13.2%, followed by Latin America (8.8%) and other Asia (7.1%).

While wholesale revenues were decreasing by -5% in 2013, the company was

able to keep gross profit rising with approximately 1%, by increasing the gross

profit margin to 43% from 40% in the previous year. Operating segmental profits

rose by 4%, increasing the operating profit margin from 31% in 2012 to 34% in

2013. Gross profits are calculated as sales minus cost of goods sold. Operating

profits for the segment are calculated by deducting the other operating expenses

(including depreciation) from the gross profits. While from 2009 to 2013 gross

profit and operating profit were continuously rising, the margins were decreasing

and only bouncing back in 2013 (see figure 31).

RETAIL

In the company’s retail business the individual retail activities of adidas and

Reebok are combined like in Wholesale. The activities are operated through

65% 62% 63% 65% 65%

17% 19% 21% 23% 24% 18% 18% 17% 12% 12%

Figure 30: relative weights of brands on wholesale revenues

Reebok

adidas Originals & Sport Style

adidas Sport Performance

Source: Adidas Annual Reports

4.706 5.101 5.578 6.187 5.917

1.225 1.559

1.861 2.193 2.156 1.265

1.505 1.476

1.109 1.050

2009 2010 2011 2012 2013

Figure 29: Wholesale revenue per brand in Mio EUR

Reebok

adidas Originals & Sport Style

adidas Sport Performance

Source: Adidas Annual Reports

CAGR = 6.1%

3.0

03

3.3

63

3.5

36

3.7

96

3.9

07

2.3

68

2.5

56

2.6

56

2.9

21

3.1

05

42% 41% 40% 40% 43%

33% 31% 30% 31% 34%

0%

10%

20%

30%

40%

50%

€ 0

€ 1.000

€ 2.000

€ 3.000

€ 4.000

€ 5.000

2009 2010 2011 2012 2013

Figure 31: Wholesale profits in Mio EUR and margins in %

Gross Profit Operating Profit

Gross Margin Operating Margin

Source: Adidas Annual Reports

1.1

16

1.4

74

1.7

47

2.0

46

2.1

34

267

450

591

715

669

59% 62% 63% 61% 62%

14% 19% 21% 21% 19%

0% 10% 20% 30% 40% 50% 60% 70%

€ 0

€ 500

€ 1.000

€ 1.500

€ 2.000

€ 2.500

2009 2010 2011 2012 2013

Figure 34: Retail profits in Mio EUR and margins in %

Gross Profit Operating Profit

Gross Margin Operating Margin

ADIDAS AG COMPANY REPORT

PAGE 14/27

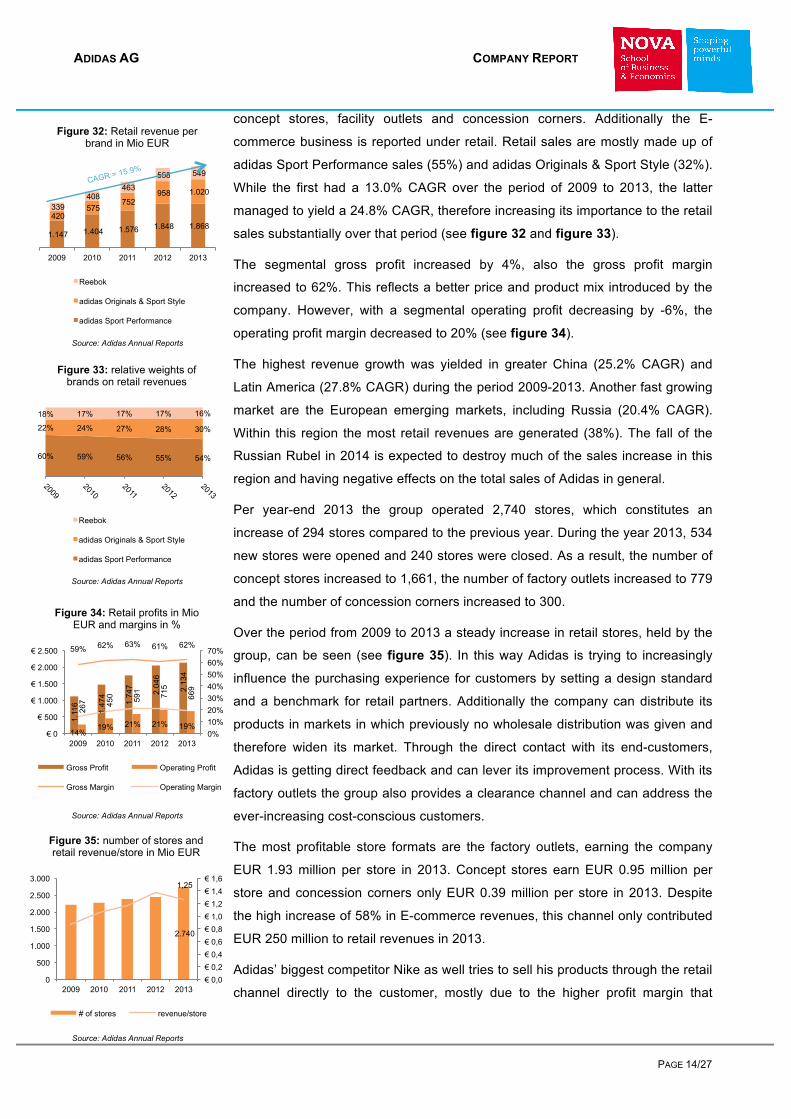

concept stores, facility outlets and concession corners. Additionally the E-

commerce business is reported under retail. Retail sales are mostly made up of

adidas Sport Performance sales (55%) and adidas Originals & Sport Style (32%).

While the first had a 13.0% CAGR over the period of 2009 to 2013, the latter

managed to yield a 24.8% CAGR, therefore increasing its importance to the retail

sales substantially over that period (see figure 32 and figure 33).

The segmental gross profit increased by 4%, also the gross profit margin

increased to 62%. This reflects a better price and product mix introduced by the

company. However, with a segmental operating profit decreasing by -6%, the

operating profit margin decreased to 20% (see figure 34).

The highest revenue growth was yielded in greater China (25.2% CAGR) and

Latin America (27.8% CAGR) during the period 2009-2013. Another fast growing

market are the European emerging markets, including Russia (20.4% CAGR).

Within this region the most retail revenues are generated (38%). The fall of the

Russian Rubel in 2014 is expected to destroy much of the sales increase in this

region and having negative effects on the total sales of Adidas in general.

Per year-end 2013 the group operated 2,740 stores, which constitutes an

increase of 294 stores compared to the previous year. During the year 2013, 534

new stores were opened and 240 stores were closed. As a result, the number of

concept stores increased to 1,661, the number of factory outlets increased to 779

and the number of concession corners increased to 300.

Over the period from 2009 to 2013 a steady increase in retail stores, held by the

group, can be seen (see figure 35). In this way Adidas is trying to increasingly

influence the purchasing experience for customers by setting a design standard

and a benchmark for retail partners. Additionally the company can distribute its

products in markets in which previously no wholesale distribution was given and

therefore widen its market. Through the direct contact with its end-customers,

Adidas is getting direct feedback and can lever its improvement process. With its

factory outlets the group also provides a clearance channel and can address the

ever-increasing cost-conscious customers.

The most profitable store formats are the factory outlets, earning the company

EUR 1.93 million per store in 2013. Concept stores earn EUR 0.95 million per

store and concession corners only EUR 0.39 million per store in 2013. Despite

the high increase of 58% in E-commerce revenues, this channel only contributed

EUR 250 million to retail revenues in 2013.

Adidas’ biggest competitor Nike as well tries to sell his products through the retail

channel directly to the customer, mostly due to the higher profit margin that

1.147 1.404 1.576 1.848 1.868 420

575 752

958 1.020

339 408

463 558 549

2009 2010 2011 2012 2013

Figure 32: Retail revenue per brand in Mio EUR

Reebok

adidas Originals & Sport Style

adidas Sport Performance

Source: Adidas Annual Reports

CAGR = 15.9%

60% 59% 56% 55% 54%

22% 24% 27% 28% 30%

18% 17% 17% 17% 16%

Figure 33: relative weights of brands on retail revenues

Reebok

adidas Originals & Sport Style

adidas Sport Performance

Source: Adidas Annual Reports

1.1

16

1.4

74

1.7

47

2.0

46

2.1

34

267

450

591

715

669

59% 62% 63% 61% 62%

14% 19% 21% 21% 19%

0% 10% 20% 30% 40% 50% 60% 70%

€ 0

€ 500

€ 1.000

€ 1.500

€ 2.000

€ 2.500

2009 2010 2011 2012 2013

Figure 34: Retail profits in Mio EUR and margins in %

Gross Profit Operating Profit

Gross Margin Operating Margin

Source: Adidas Annual Reports

Source: Adidas Annual Reports

2.740

1,25

€ 0,0 € 0,2 € 0,4 € 0,6 € 0,8 € 1,0 € 1,2 € 1,4 € 1,6

0

500

1.000

1.500

2.000

2.500

3.000

2009 2010 2011 2012 2013

Figure 35: number of stores and retail revenue/store in Mio EUR

# of stores revenue/store

ADIDAS AG COMPANY REPORT

PAGE 15/27

comes with it4. However, as the company mentioned in its latest letter to the

shareholders, it does those expansions with a very strong risk aversion, trying to

minimize the direct investments into stores and enforcing investments into online

shopping facilities in which it sees more potential.5 As a result, the number of

stores operated by Nike is only minor when compared to Adidas. However, due

to the stronger eCommerce operated by Nike, its revenues per store are major

compared to Adidas (EUR 5.12 million vs EUR 1.25 million per store).

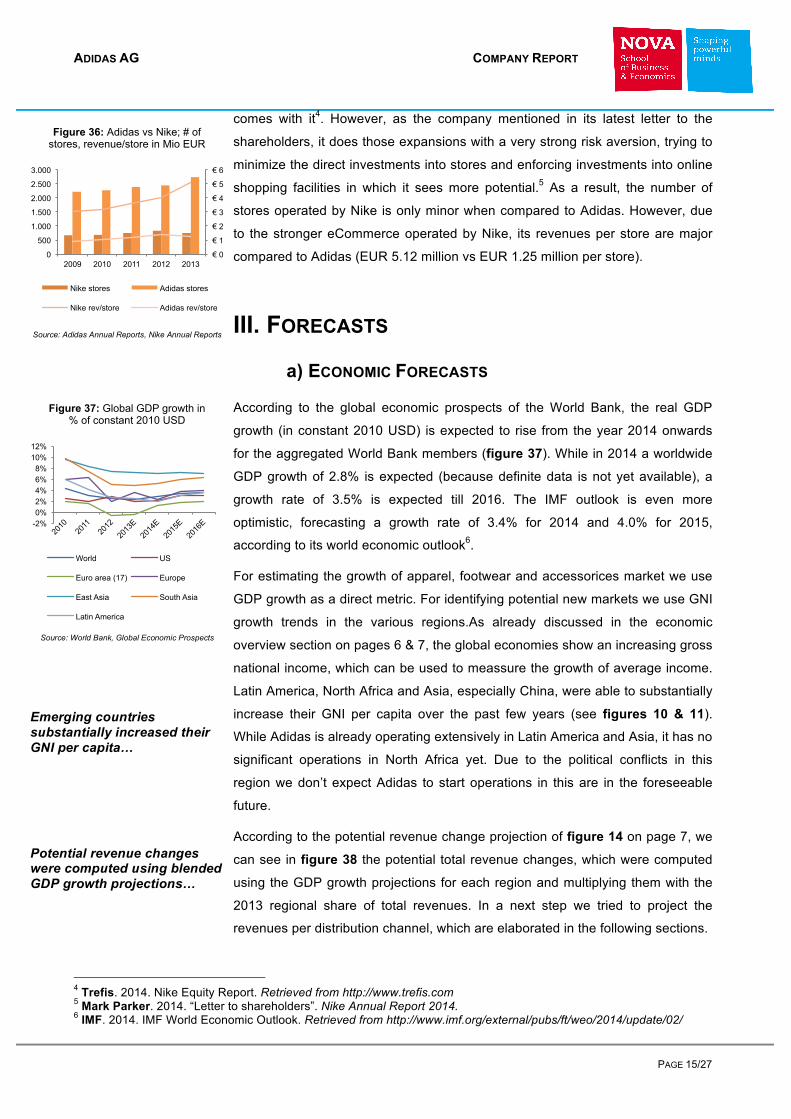

III. FORECASTS

a) ECONOMIC FORECASTS

According to the global economic prospects of the World Bank, the real GDP

growth (in constant 2010 USD) is expected to rise from the year 2014 onwards

for the aggregated World Bank members (figure 37). While in 2014 a worldwide

GDP growth of 2.8% is expected (because definite data is not yet available), a

growth rate of 3.5% is expected till 2016. The IMF outlook is even more

optimistic, forecasting a growth rate of 3.4% for 2014 and 4.0% for 2015,

according to its world economic outlook6.

For estimating the growth of apparel, footwear and accessorices market we use

GDP growth as a direct metric. For identifying potential new markets we use GNI

growth trends in the various regions.As already discussed in the economic

overview section on pages 6 & 7, the global economies show an increasing gross

national income, which can be used to meassure the growth of average income.

Latin America, North Africa and Asia, especially China, were able to substantially

increase their GNI per capita over the past few years (see figures 10 & 11).

While Adidas is already operating extensively in Latin America and Asia, it has no

significant operations in North Africa yet. Due to the political conflicts in this

region we don’t expect Adidas to start operations in this are in the foreseeable

future.

According to the potential revenue change projection of figure 14 on page 7, we

can see in figure 38 the potential total revenue changes, which were computed

using the GDP growth projections for each region and multiplying them with the

2013 regional share of total revenues. In a next step we tried to project the

revenues per distribution channel, which are elaborated in the following sections.

4 Trefis. 2014. Nike Equity Report. Retrieved from http://www.trefis.com 5 Mark Parker. 2014. “Letter to shareholders”. Nike Annual Report 2014. 6 IMF. 2014. IMF World Economic Outlook. Retrieved from http://www.imf.org/external/pubs/ft/weo/2014/update/02/

-2% 0% 2% 4% 6% 8%

10% 12%

Figure 37: Global GDP growth in % of constant 2010 USD

World US

Euro area (17) Europe

East Asia South Asia

Latin America

Source: World Bank, Global Economic Prospects

Emerging countries substantially increased their GNI per capita…

Potential revenue changes were computed using blended GDP growth projections…

Source: Adidas Annual Reports, Nike Annual Reports

€ 0

€ 1

€ 2

€ 3

€ 4

€ 5

€ 6

0

500

1.000

1.500

2.000

2.500

3.000

2009 2010 2011 2012 2013

Figure 36: Adidas vs Nike; # of stores, revenue/store in Mio EUR

Nike stores Adidas stores

Nike rev/store Adidas rev/store

ADIDAS AG COMPANY REPORT

PAGE 16/27

The result is the projected currency neutral revenue changes line in figure 38. In

line with our sentiment, that Adidas will not achieve to grow above the GDP

growth of the areas it is operating in, we can see a lower than potential currency

neutral nominal revenue change.

We see the reason for this in the fact that Adidas still lacks the outstanding

products and technology to get one up on Nike, its most severe competitor. Also

the rise of small niche suppliers in the industry, such as Under Armour is

expected to cost the established market leaders market share. In 2014 we

additionally expect negative forex effects of -7% (-6% in 2013) on total sales,

mostly due to the steep fall of the Russian Rubel and the comparably strong Euro

at the beginning of the year. However these effects are expected to decline

significantly in 2015 (-5%) and 2016 (-2%).

Figure 38: Potential revenue change projection

2010A 2011A 2012A 2013A 2014E **

2015F **

2016F **

Potential revenue changes (real) 6,0% 5,5% 3,7% 4,0% 3,5% 4,3% 4,5%

Inflation rate 2,6% 3,3% 2,0% 1,7% 1,7% 1,7% 1,7%

Potential revenue changes (nominal) 8,8% 9,0% 5,8% 5,8% 5,2% 6,1% 6,2%

Actual / projected currency neutral revenue changes 8,9% 13,1% 7,8% 3,3% 1,5% 4,3% 4,8%

Source: World Bank, Global Economic Prospects, Analysts estimates

* GDP growth in constant 2010 USD

** revenue share 2014-16 held constant, based on 2013 share

b) SEGMENTAL FORECASTS

WHOLESALE

For the wholesale segment we estimate relatively slow growth. Adidas Sport

Performance and adidas Originals & Sport Style are projected by us to rise at an

average currency neutral nominal growth of 2% and 4% respectively over the

upcoming periods due to increasing competition from specialists in the sport

performance industry, as well as slowing growth expectations in Adidas’ most

important wholesale growth markets Latin America and Asia (see figure 37).

Additionally, in our opinion, Adidas still lacks the outstanding products and

technology to get one up on Nike and become market leader in any sector. Even

though CEO Herbert Hainer announced to tackle the issue of a lacking

competitiveness and revitalization of the North American business in the course

of a restructuring, it is estimated that the effects will not have any noticeable

impact in the near future, also due to the homogeneity of the products. The

restructuring process itself aims on stabilizing performance in the weaker

business areas such as golf, enhancing the process flow in the marketing

organization and increasing marketing expenditures in mature markets. Reebok

Source: Analst’s estimates

5.917 5.562 5.395 5.395 5.503 5.613

2.156 2.048 2.028 2.068 2.151 2.237 1.050 982 952 962 991 1.020

2013A 2014E 2015F 2016F 2017F 2018F

Figure 39: Estimated wholesale revenues in Mio EUR

Reebok

adidas Originals & Sport Style

adidas Sport Performance

Source: Analst’s estimates

9.100 8.592 8.375 8.425 8.645 8.871

3.884 3.609 3.518 3.539 3.631 3.726

3.082 2.895 2.806 2.806 2.861 2.927

2013A 2014E 2015F 2016F 2017F 2018F

Figure 40: Estimated wholesale profits in Mio EUR

Sales Operating Profit Gross Profit

Adidas is expected to grow below GDP growth…

Negative forex effects of -7% are expected in 2014…

ADIDAS AG COMPANY REPORT

PAGE 17/27

is expected by us to recover slowly and grow to an average currency neutral

nominal change of 3%, starting in 2017. Our estimations for wholesale revenues

can be seen in figure 39.

We expect the gross margin7 to be constant at an historic average rate of 42%.

This is due to the relative predictability of cost of sales. Because of the

announced marketing initiative and increases in sizeable sponsoring contracts

the operating margin is expected to decrease slightly to its historic average of

33%. From our point of view, incremental cost of restructuring activities will also

put pressure on the operating margin. For the estimated operating and gross

profits see figure 40.

RETAIL

We expect the retail segment to grow the largest among all segments. The

currency neutral annual revenue nominal growth rate for adidas Sport

Performance is expected to rise at a constant rate of 8% from 2015 onwards.

Adidas Originals & Sport Style is expected to rise on average at a nominal 14%

on a currency neutral basis from 2015 onwards (figure 41). We justify this by the

fact that the retail business still gives the company the chance to open up

markets, which are not yet fully covered by the wholesale business. Also the

increasing marketing activities are expected to increase sales mainly in directly

owned retail shops. For the Russian market however, the company plans to

decrease exposure by lowering the number of shops. This will prevent the

potential higher growth to become effective, however at the same time it limits

the risk in this currently volatile region.

The gross margin is expected to stay at approximately 62%. The operating

margin is expected to increase from 20% in 2014 to 22% by 2016 and onwards.

The increasing marketing budget will put pressure on the operating margin,

however we expect this effect to be mainly offset by increased efficiencies on the

management of global brands and global sales. Our estimations for retail gross

and operating profit can be found in figure 42.

Due to the announced adoption of future investments to the current market risks,

especially in Russia, and the also announced enhanced closing of Russian retail

stores, we expect fewer net store openings, i.e. store opening minus store

closings, in 2014 and 2015. However, we expect the openings to rise again to

come up to the expansionary strategy of the company (see figure 43).

7 Gross margin = gross profit / sales ; gross profit = sales – COGS ; operating profit = gross profit – OPEX

Source: Analst’s estimates

1.868 1.868 1.924 2.039 2.203 2.379

1.020 1.051 1.124 1.259 1.448 1.665 549 522 516 537 575 615

2013A 2014E 2015F 2016F 2017F 2018F

Figure 41: Estimated retail revenues in Mio EUR

Reebok

adidas Originals & Sport Style

adidas Sport Performance

Source: Analst’s estimates

3.446 3.440 3.565 3.836 4.225 4.659

2.143 2.133 2.210 2.378 2.620 2.888

678 688 731 805 908 1.025

2013A 2014E 2015F 2016F 2017F 2018F

Figure 42: Estimated retail profits in Mio EUR

Sales Operating Profit Gross Profit

Source: Analst’s estimates

3.068 3.316 3.462 3.587 3.860 4.252

369 124 103 248 365

407 294

103 84

203

296 328

- 50 100 150 200 250 300 350

€ 0

€ 1.000

€ 2.000

€ 3.000

€ 4.000

€ 5.000

Figure 43: Estimated store openings and incremental sales in Mio EUR

Incremental Sales

Like-for-like sales

Store Openings

ADIDAS AG COMPANY REPORT

PAGE 18/27

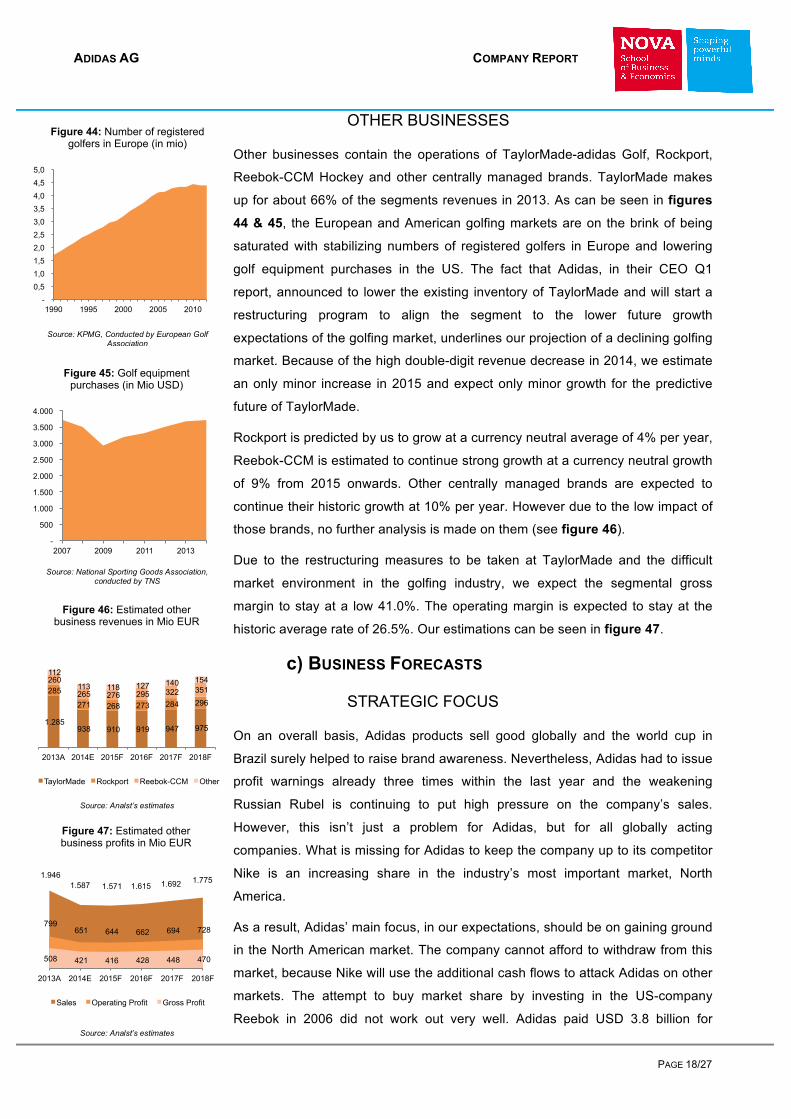

OTHER BUSINESSES

Other businesses contain the operations of TaylorMade-adidas Golf, Rockport,

Reebok-CCM Hockey and other centrally managed brands. TaylorMade makes

up for about 66% of the segments revenues in 2013. As can be seen in figures

44 & 45, the European and American golfing markets are on the brink of being

saturated with stabilizing numbers of registered golfers in Europe and lowering

golf equipment purchases in the US. The fact that Adidas, in their CEO Q1

report, announced to lower the existing inventory of TaylorMade and will start a

restructuring program to align the segment to the lower future growth

expectations of the golfing market, underlines our projection of a declining golfing

market. Because of the high double-digit revenue decrease in 2014, we estimate

an only minor increase in 2015 and expect only minor growth for the predictive

future of TaylorMade.

Rockport is predicted by us to grow at a currency neutral average of 4% per year,

Reebok-CCM is estimated to continue strong growth at a currency neutral growth

of 9% from 2015 onwards. Other centrally managed brands are expected to

continue their historic growth at 10% per year. However due to the low impact of

those brands, no further analysis is made on them (see figure 46).

Due to the restructuring measures to be taken at TaylorMade and the difficult

market environment in the golfing industry, we expect the segmental gross

margin to stay at a low 41.0%. The operating margin is expected to stay at the

historic average rate of 26.5%. Our estimations can be seen in figure 47.

c) BUSINESS FORECASTS

STRATEGIC FOCUS

On an overall basis, Adidas products sell good globally and the world cup in

Brazil surely helped to raise brand awareness. Nevertheless, Adidas had to issue

profit warnings already three times within the last year and the weakening

Russian Rubel is continuing to put high pressure on the company’s sales.

However, this isn’t just a problem for Adidas, but for all globally acting

companies. What is missing for Adidas to keep the company up to its competitor

Nike is an increasing share in the industry’s most important market, North

America.

As a result, Adidas’ main focus, in our expectations, should be on gaining ground

in the North American market. The company cannot afford to withdraw from this

market, because Nike will use the additional cash flows to attack Adidas on other

markets. The attempt to buy market share by investing in the US-company

Reebok in 2006 did not work out very well. Adidas paid USD 3.8 billion for

- 0,5 1,0 1,5 2,0 2,5 3,0 3,5 4,0 4,5 5,0

1990 1995 2000 2005 2010

Figure 44: Number of registered golfers in Europe (in mio)

Source: KPMG, Conducted by European Golf Association

-

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

2007 2009 2011 2013

Figure 45: Golf equipment purchases (in Mio USD)

Source: National Sporting Goods Association, conducted by TNS

Source: Analst’s estimates

1.285 938 910 919 947 975

285

271 268 273 284 296

260

265 276 295 322 351

112

113 118 127 140 154

2013A 2014E 2015F 2016F 2017F 2018F

Figure 46: Estimated other business revenues in Mio EUR

TaylorMade Rockport Reebok-CCM Other

Source: Analst’s estimates

1.946 1.587 1.571 1.615 1.692 1.775

799 651 644 662 694 728

508 421 416 428 448 470

2013A 2014E 2015F 2016F 2017F 2018F

Figure 47: Estimated other business profits in Mio EUR

Sales Operating Profit Gross Profit

ADIDAS AG COMPANY REPORT

PAGE 19/27

Reebok in 2006. Reebok’s revenues decreased from that time on till now with a

CAGR of -2.2%. The new strategy will be to enforce marketing and sponsorships

in order to raise awareness.

In addition TaylorMade-adidas Golf’s business has come under pressure with a

saturated market and high amounts of products still on stock. The strategy will be

to build off these stocks in order to avoid heavy losses. Smaller growth

opportunities should be expected from this sector in the coming years in our

opinion. However, the impact on total results is expected to be small due to the

small share on total revenues of about 8% in the past.

Due to the conflicts in Ukraine and the sanctions imposed on Russia, Adidas will

try to lower its exposure to the Russian market in the foreseeable future. The

sales generated in Russia in 2013 are estimated to exceed EUR 1 billion.8

However, with the Rubel getting under more and more pressure (see figure 48),

sales generated in this region loose their value to the company. The CEO of

Adidas already announced to heavily decrease the number of shop openings and

increase the number of closings in this area. The upcoming years will show,

whether this is the right long-term strategy for growth in this important region. In

order to gain shareholders trust, the company announced a share repurchase

program in 2014. Through it, the company will re-purchase 25 million shares until

the end of 2017. By December 2014 the company already repurchased 4.9

million shares for an average price of EUR 61 per share, therefore a volume of

EUR 300 million. We expect the remaining 20.1 million shares to be repurchased

evenly spread from 2015 to 2017.

IV. VALUATION We used a discounted cash flow model to derive a target price of EUR 61.81,

which is above the market price as per 02.01.2015 and below our initial target

from the Q3 review. All companies in which Adidas has a share are majority held

and therefore consolidated. In the forecast, as mentioned before, the wholesale,

retail and other business sectors were separated in order to increase the

predictability of cash flows in the future. In addition to the scenario predicted by

us we also incorporated a sensitivity analysis.

a) COMPARABLES

As per beginning of January, the Adidas AG stock is trading at a price-earnings

multiple of 16.24, while the median of the identified peer group equals 21.51. This

8 Aaron Ricadela. 2014. “Adidas plunges after reducing forecasts on Russia, Golf”. Bloomberg.com.

72,55

30,00

35,00

40,00

45,00

50,00

55,00

60,00

65,00

70,00

75,00

Figure 48: historical EUR/RUB chart

Source: Investing.com

Using a DCF model we derive a target price of EUR 61.81…

Share re-purchase program announced in 2014…

ADIDAS AG COMPANY REPORT

PAGE 20/27

means a discount of 24.5%. The same is true for the equity value over EBITDA

multiple, which currently equals 9.02, a 13.6% discount over its peer group

median. In our opinion this discount is unjustified because of the company’s

competiveness and ability to generate sustainable cash flows. We expect Adidas’

stock price to increase to the outlined price target over the upcoming year.

b) DISCOUNTED CASH FLOW ANALYSIS

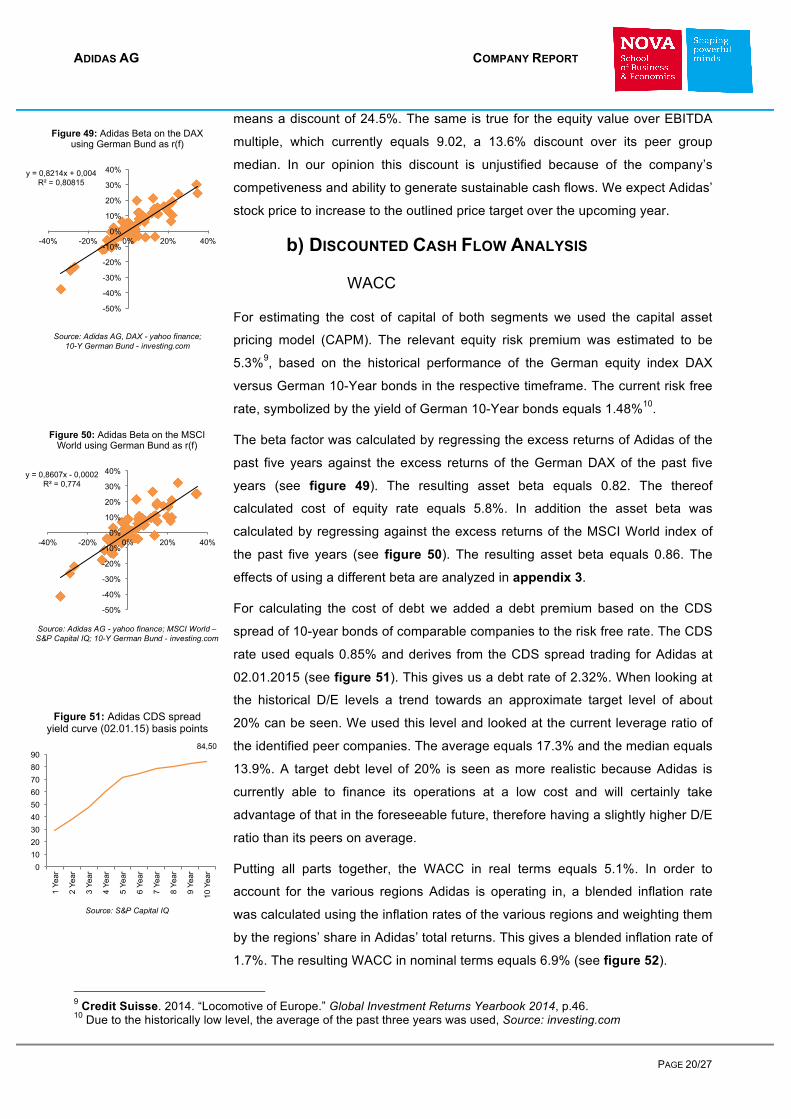

WACC

For estimating the cost of capital of both segments we used the capital asset

pricing model (CAPM). The relevant equity risk premium was estimated to be

5.3%9, based on the historical performance of the German equity index DAX

versus German 10-Year bonds in the respective timeframe. The current risk free

rate, symbolized by the yield of German 10-Year bonds equals 1.48%10.

The beta factor was calculated by regressing the excess returns of Adidas of the

past five years against the excess returns of the German DAX of the past five

years (see figure 49). The resulting asset beta equals 0.82. The thereof

calculated cost of equity rate equals 5.8%. In addition the asset beta was

calculated by regressing against the excess returns of the MSCI World index of

the past five years (see figure 50). The resulting asset beta equals 0.86. The

effects of using a different beta are analyzed in appendix 3.

For calculating the cost of debt we added a debt premium based on the CDS

spread of 10-year bonds of comparable companies to the risk free rate. The CDS

rate used equals 0.85% and derives from the CDS spread trading for Adidas at

02.01.2015 (see figure 51). This gives us a debt rate of 2.32%. When looking at

the historical D/E levels a trend towards an approximate target level of about

20% can be seen. We used this level and looked at the current leverage ratio of

the identified peer companies. The average equals 17.3% and the median equals

13.9%. A target debt level of 20% is seen as more realistic because Adidas is

currently able to finance its operations at a low cost and will certainly take

advantage of that in the foreseeable future, therefore having a slightly higher D/E

ratio than its peers on average.

Putting all parts together, the WACC in real terms equals 5.1%. In order to

account for the various regions Adidas is operating in, a blended inflation rate

was calculated using the inflation rates of the various regions and weighting them

by the regions’ share in Adidas’ total returns. This gives a blended inflation rate of

1.7%. The resulting WACC in nominal terms equals 6.9% (see figure 52).

9 Credit Suisse. 2014. “Locomotive of Europe.” Global Investment Returns Yearbook 2014, p.46. 10 Due to the historically low level, the average of the past three years was used, Source: investing.com

y = 0,8214x + 0,004 R² = 0,80815

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-40% -20% 0% 20% 40%

Figure 49: Adidas Beta on the DAX using German Bund as r(f)

Source: Adidas AG, DAX - yahoo finance; 10-Y German Bund - investing.com

y = 0,8607x - 0,0002 R² = 0,774

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

-40% -20% 0% 20% 40%

Figure 50: Adidas Beta on the MSCI World using German Bund as r(f)

Source: Adidas AG - yahoo finance; MSCI World – S&P Capital IQ; 10-Y German Bund - investing.com

84,50

0 10 20 30 40 50 60 70 80 90

1 Ye

ar

2 Ye

ar

3 Ye

ar

4 Ye

ar

5 Ye

ar

6 Ye

ar

7 Ye

ar

8 Ye

ar

9 Ye

ar

10 Y

ear

Figure 51: Adidas CDS spread yield curve (02.01.15) basis points

Source: S&P Capital IQ

ADIDAS AG COMPANY REPORT

PAGE 21/27

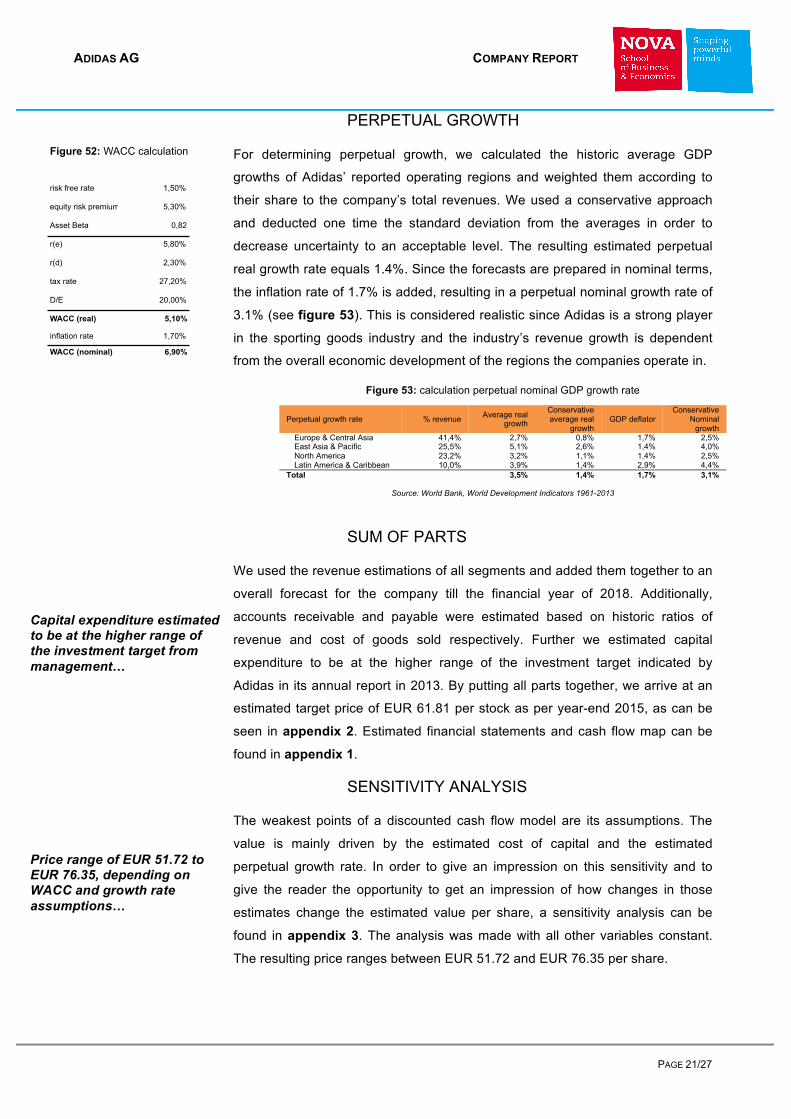

PERPETUAL GROWTH

For determining perpetual growth, we calculated the historic average GDP

growths of Adidas’ reported operating regions and weighted them according to

their share to the company’s total revenues. We used a conservative approach

and deducted one time the standard deviation from the averages in order to

decrease uncertainty to an acceptable level. The resulting estimated perpetual

real growth rate equals 1.4%. Since the forecasts are prepared in nominal terms,

the inflation rate of 1.7% is added, resulting in a perpetual nominal growth rate of

3.1% (see figure 53). This is considered realistic since Adidas is a strong player

in the sporting goods industry and the industry’s revenue growth is dependent

from the overall economic development of the regions the companies operate in.

Figure 53: calculation perpetual nominal GDP growth rate

Perpetual growth rate % revenue Average real growth

Conservative average real

growth GDP deflator

Conservative Nominal

growth Europe & Central Asia 41,4% 2,7% 0,8% 1,7% 2,5% East Asia & Pacific 25,5% 5,1% 2,6% 1,4% 4,0% North America 23,2% 3,2% 1,1% 1,4% 2,5% Latin America & Caribbean 10,0% 3,9% 1,4% 2,9% 4,4%

Total 3,5% 1,4% 1,7% 3,1%

Source: World Bank, World Development Indicators 1961-2013

SUM OF PARTS

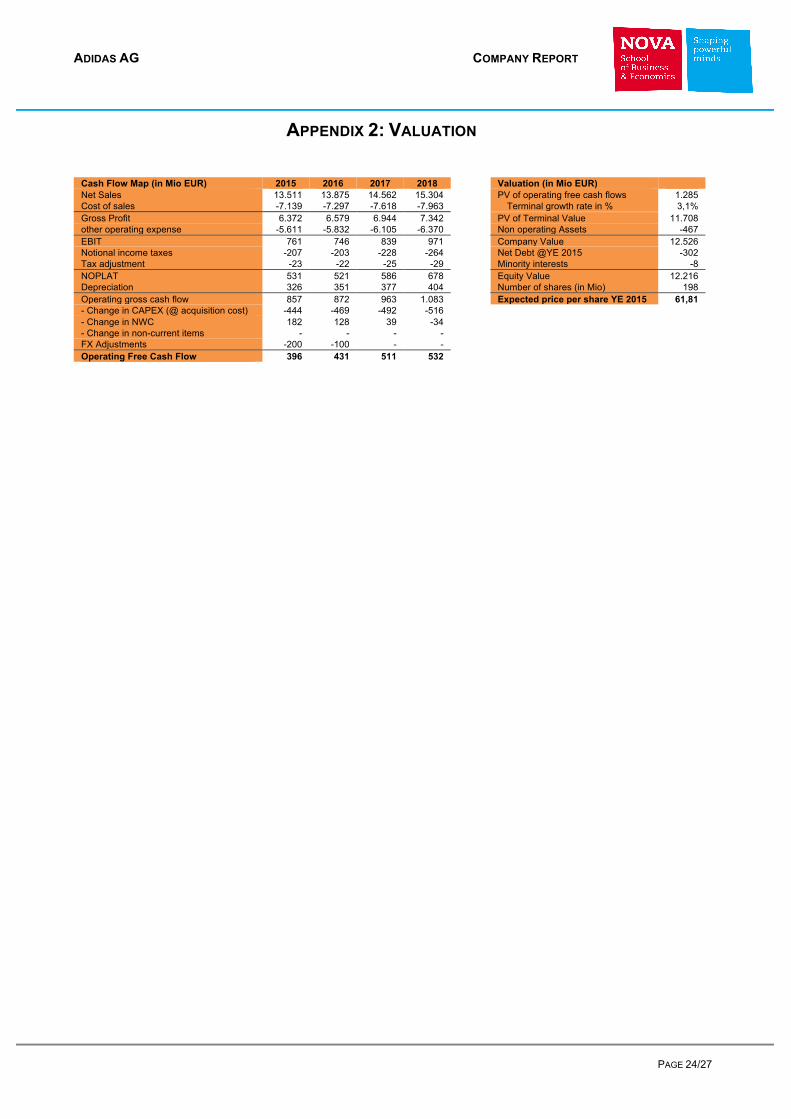

We used the revenue estimations of all segments and added them together to an

overall forecast for the company till the financial year of 2018. Additionally,

accounts receivable and payable were estimated based on historic ratios of

revenue and cost of goods sold respectively. Further we estimated capital

expenditure to be at the higher range of the investment target indicated by

Adidas in its annual report in 2013. By putting all parts together, we arrive at an

estimated target price of EUR 61.81 per stock as per year-end 2015, as can be

seen in appendix 2. Estimated financial statements and cash flow map can be

found in appendix 1.

SENSITIVITY ANALYSIS

The weakest points of a discounted cash flow model are its assumptions. The

value is mainly driven by the estimated cost of capital and the estimated

perpetual growth rate. In order to give an impression on this sensitivity and to

give the reader the opportunity to get an impression of how changes in those

estimates change the estimated value per share, a sensitivity analysis can be

found in appendix 3. The analysis was made with all other variables constant.

The resulting price ranges between EUR 51.72 and EUR 76.35 per share.

Price range of EUR 51.72 to EUR 76.35, depending on WACC and growth rate assumptions…

Capital expenditure estimated to be at the higher range of the investment target from management…

risk free rate 1,50%

equity risk premium 5,30%

Asset Beta 0,82

r(e) 5,80%

r(d) 2,30%

tax rate 27,20%

D/E 20,00%

WACC (real) 5,10%

inflation rate 1,70%

WACC (nominal) 6,90%

Figure 52: WACC calculation

ADIDAS AG COMPANY REPORT

PAGE 22/27

V. APPENDIX

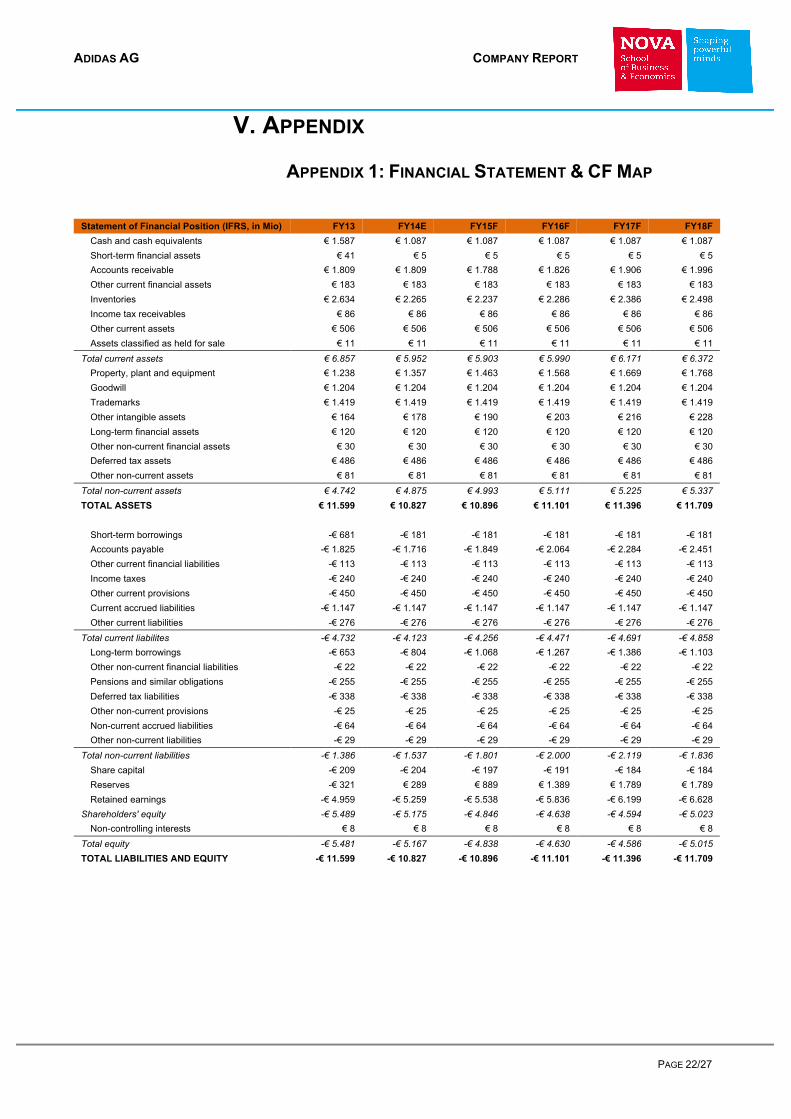

APPENDIX 1: FINANCIAL STATEMENT & CF MAP

Statement of Financial Position (IFRS, in Mio) FY13 FY14E FY15F FY16F FY17F FY18F

Cash and cash equivalents € 1.587 € 1.087 € 1.087 € 1.087 € 1.087 € 1.087 Short-term financial assets € 41 € 5 € 5 € 5 € 5 € 5 Accounts receivable € 1.809 € 1.809 € 1.788 € 1.826 € 1.906 € 1.996 Other current financial assets € 183 € 183 € 183 € 183 € 183 € 183 Inventories € 2.634 € 2.265 € 2.237 € 2.286 € 2.386 € 2.498 Income tax receivables € 86 € 86 € 86 € 86 € 86 € 86 Other current assets € 506 € 506 € 506 € 506 € 506 € 506 Assets classified as held for sale € 11 € 11 € 11 € 11 € 11 € 11

Total current assets € 6.857 € 5.952 € 5.903 € 5.990 € 6.171 € 6.372 Property, plant and equipment € 1.238 € 1.357 € 1.463 € 1.568 € 1.669 € 1.768 Goodwill € 1.204 € 1.204 € 1.204 € 1.204 € 1.204 € 1.204 Trademarks € 1.419 € 1.419 € 1.419 € 1.419 € 1.419 € 1.419 Other intangible assets € 164 € 178 € 190 € 203 € 216 € 228 Long-term financial assets € 120 € 120 € 120 € 120 € 120 € 120 Other non-current financial assets € 30 € 30 € 30 € 30 € 30 € 30 Deferred tax assets € 486 € 486 € 486 € 486 € 486 € 486 Other non-current assets € 81 € 81 € 81 € 81 € 81 € 81

Total non-current assets € 4.742 € 4.875 € 4.993 € 5.111 € 5.225 € 5.337 TOTAL ASSETS € 11.599 € 10.827 € 10.896 € 11.101 € 11.396 € 11.709

Short-term borrowings -€ 681 -€ 181 -€ 181 -€ 181 -€ 181 -€ 181

Accounts payable -€ 1.825 -€ 1.716 -€ 1.849 -€ 2.064 -€ 2.284 -€ 2.451 Other current financial liabilities -€ 113 -€ 113 -€ 113 -€ 113 -€ 113 -€ 113 Income taxes -€ 240 -€ 240 -€ 240 -€ 240 -€ 240 -€ 240 Other current provisions -€ 450 -€ 450 -€ 450 -€ 450 -€ 450 -€ 450 Current accrued liabilities -€ 1.147 -€ 1.147 -€ 1.147 -€ 1.147 -€ 1.147 -€ 1.147 Other current liabilities -€ 276 -€ 276 -€ 276 -€ 276 -€ 276 -€ 276

Total current liabilites -€ 4.732 -€ 4.123 -€ 4.256 -€ 4.471 -€ 4.691 -€ 4.858 Long-term borrowings -€ 653 -€ 804 -€ 1.068 -€ 1.267 -€ 1.386 -€ 1.103 Other non-current financial liabilities -€ 22 -€ 22 -€ 22 -€ 22 -€ 22 -€ 22 Pensions and similar obligations -€ 255 -€ 255 -€ 255 -€ 255 -€ 255 -€ 255 Deferred tax liabilities -€ 338 -€ 338 -€ 338 -€ 338 -€ 338 -€ 338 Other non-current provisions -€ 25 -€ 25 -€ 25 -€ 25 -€ 25 -€ 25 Non-current accrued liabilities -€ 64 -€ 64 -€ 64 -€ 64 -€ 64 -€ 64 Other non-current liabilities -€ 29 -€ 29 -€ 29 -€ 29 -€ 29 -€ 29

Total non-current liabilities -€ 1.386 -€ 1.537 -€ 1.801 -€ 2.000 -€ 2.119 -€ 1.836 Share capital -€ 209 -€ 204 -€ 197 -€ 191 -€ 184 -€ 184 Reserves -€ 321 € 289 € 889 € 1.389 € 1.789 € 1.789 Retained earnings -€ 4.959 -€ 5.259 -€ 5.538 -€ 5.836 -€ 6.199 -€ 6.628

Shareholders' equity -€ 5.489 -€ 5.175 -€ 4.846 -€ 4.638 -€ 4.594 -€ 5.023 Non-controlling interests € 8 € 8 € 8 € 8 € 8 € 8

Total equity -€ 5.481 -€ 5.167 -€ 4.838 -€ 4.630 -€ 4.586 -€ 5.015 TOTAL LIABILITIES AND EQUITY -€ 11.599 -€ 10.827 -€ 10.896 -€ 11.101 -€ 11.396 -€ 11.709

ADIDAS AG COMPANY REPORT

PAGE 23/27