June 2016 Company Profile and Strategic Guidelines

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

June 2016

Company Profile and

Strategic Guidelines

2

Disclaimer

Green Network has included in this document information and methodologies based on our experience and research.

Materials in this document are copyright to Green Network and may not be copied or otherwise distributed to any third party without the written consent of an Officer of Green Network.

This document is not complete without an accompanying oral discussion and presentation by Green Network.

3

• Market Overview and Trends

• Green Network Overview

• Strategic Guidelines

4

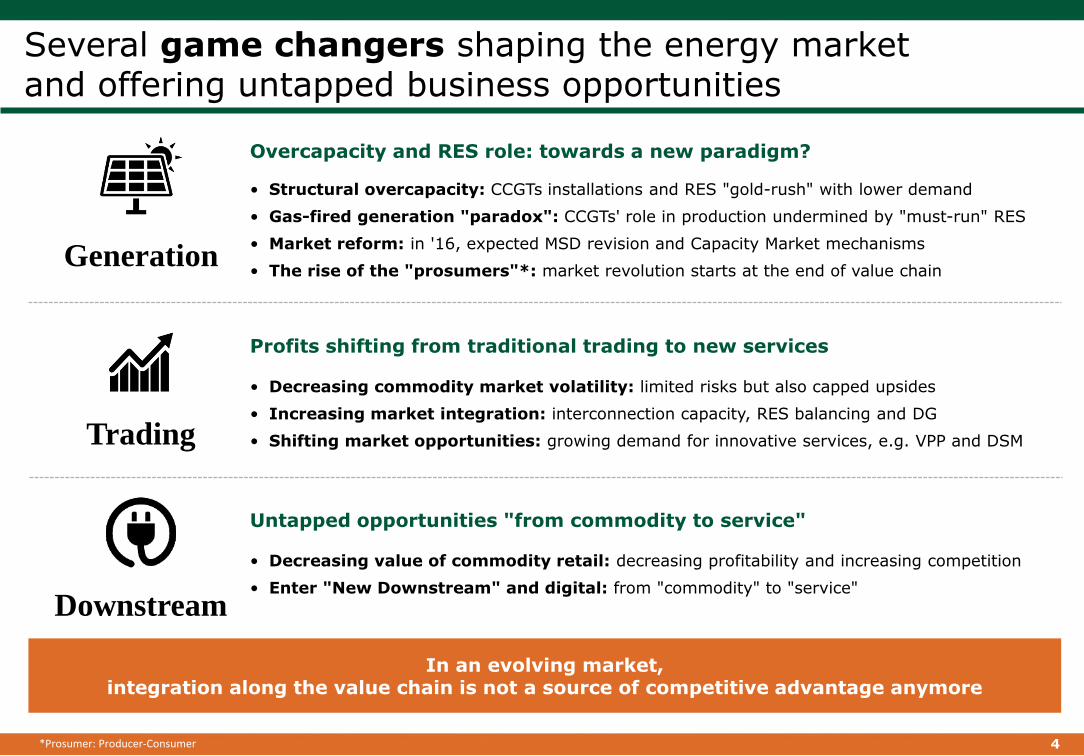

Several game changers shaping the energy marketand offering untapped business opportunities

In an evolving market,integration along the value chain is not a source of competitive advantage anymore

Generation

Trading

Downstream

Overcapacity and RES role: towards a new paradigm?

• Structural overcapacity: CCGTs installations and RES "gold-rush" with lower demand

• Gas-fired generation "paradox": CCGTs' role in production undermined by "must-run" RES

• Market reform: in '16, expected MSD revision and Capacity Market mechanisms

• The rise of the "prosumers"*: market revolution starts at the end of value chain

Profits shifting from traditional trading to new services

• Decreasing commodity market volatility: limited risks but also capped upsides

• Increasing market integration: interconnection capacity, RES balancing and DG

• Shifting market opportunities: growing demand for innovative services, e.g. VPP and DSM

Untapped opportunities "from commodity to service"

• Decreasing value of commodity retail: decreasing profitability and increasing competition

• Enter "New Downstream" and digital: from "commodity" to "service"

*Prosumer: Producer-Consumer

5

Generation: market stress due to overcapacityand RES role – towards a new paradigm?

Today Game changers

Structuralovercapacity

and RES"gold-rush"

Gas-firedgeneration"paradox"

• Lower power demand (~-10TWh vs. pre-crisis) and generation overcapacity(~+40GW combined in the last 10 years)

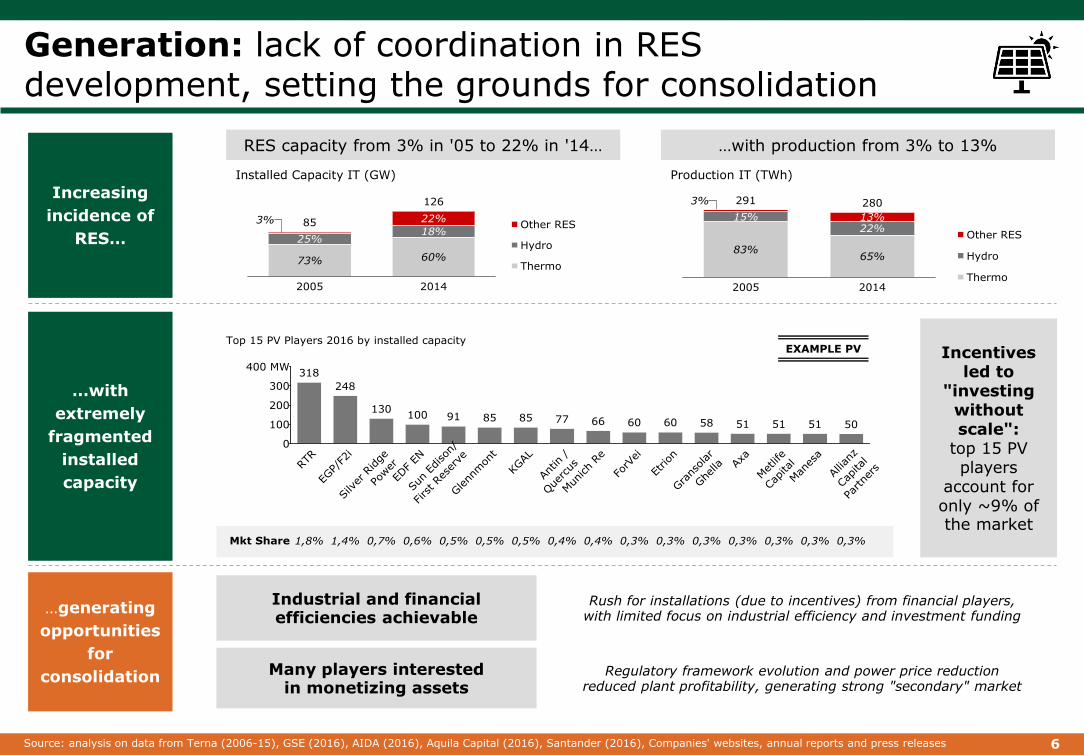

• Lack of coordination and alignment in RES development, building the case for consolidation

• RES share increasing ancillary services needs

• CCGTs' role in production undermined by "must-run" RES

Increasingmarket

integration

• Increasing interconnection capacity

• Shift towards a distributed model

• Need for modulation of "non-programmable" production

Shiftingmarket

paradigm

Smart-grids, energystorage& DSM

• Towards a model based on long-term price signals and stronger planning and coordination

• Development of smartnetworks

• Storage cost reduction

• Implementation of tools and systems to manage demand

6

Increasing

incidence of

RES…

RES capacity from 3% in '05 to 22% in '14…

Installed Capacity IT (GW)

…with production from 3% to 13%

Production IT (TWh)

Incentives led to

"investing without scale":

top 15 PV players

account for only ~9% of the market

…with

extremely

fragmented

installed

capacity

EXAMPLE PV

…generating

opportunities

for

consolidation

Industrial and financial efficiencies achievable

Rush for installations (due to incentives) from financial players,with limited focus on industrial efficiency and investment funding

Many players interested in monetizing assets

Regulatory framework evolution and power price reductionreduced plant profitability, generating strong "secondary" market

Generation: lack of coordination in RESdevelopment, setting the grounds for consolidation

Source: analysis on data from Terna (2006-15), GSE (2016), AIDA (2016), Aquila Capital (2016), Santander (2016), Companies' websites, annual reports and press releases

7

Trading: profits shifting from traditional tradingto the development of new services

Today Game changers

New opportunities

for energymanagers

Generationoptimization

…but the opening of the services marketin Europe unveils new opportunities

• Decreasing volatility, also due to increasing coordination and integration and improved market liquidity and frequency of update of energy markets

• Less discontinuities and asymmetries to leverage in trading activities

Decreasing profitability oftraditional trading activities…

8

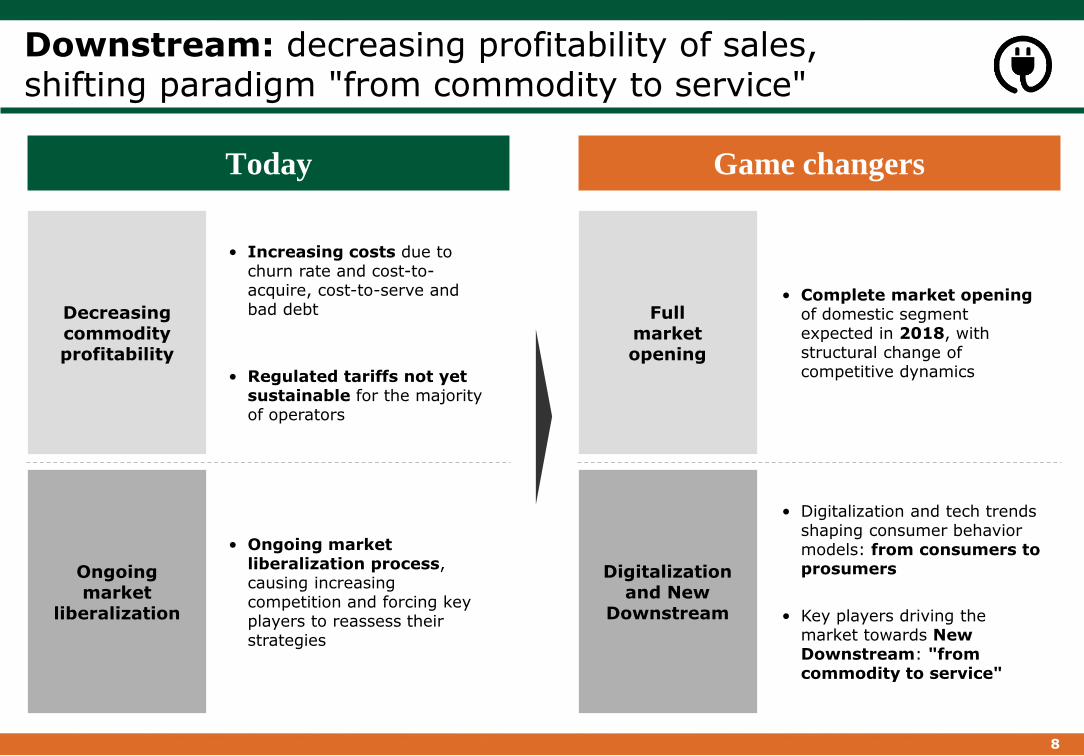

Today Game changers

Decreasing commodityprofitability

Ongoingmarket

liberalization

• Increasing costs due to churn rate and cost-to-acquire, cost-to-serve and bad debt

• Regulated tariffs not yet sustainable for the majority of operators

• Ongoing market liberalization process, causing increasing competition and forcing key players to reassess their strategies

Fullmarketopening

Digitalizationand New

Downstream

• Complete market openingof domestic segment expected in 2018, with structural change of competitive dynamics

• Digitalization and tech trends shaping consumer behavior models: from consumers to prosumers

• Key players driving the market towards New Downstream: "from commodity to service"

Downstream: decreasing profitability of sales, shifting paradigm "from commodity to service"

9

Retail Bad Debt cost (€/customer, 2014)

Bad Debt Cost

Retail CtS 2014 (€/customer, 2014)

Cost-to-Serve

Downstream: profitability affected by few key factors,with huge variations across players and segments

Churn rates Acquisition costs

Gas

Pow

er

Freemarket

Regulated market

Example residential churn rates (2012-14, %) Example acquisition costs (2015, € per gross acquisition)

Italianretail

energymarket

Note: data based on AEEGSI "cliente tipo"; Source: internal analysis on AEEGSI (2014), The World Bank (2015), industry knowledge

10

Downstream: market opening for residential by '18, although transition is still under discussion

Market opening expected for residential customers in 2018: while the transition process is under discussion, key players need to assess their prospects and strategic responses

Options for market liberalization

Mkts

Sta

keh

old

ers

Du

rati

on

As-Is Direct Switch

Voluntary switch Automatic switch

"Tutela"-LikeOption 0 Option 1 Option 2

2A 2B

• As-is "Tutela" services

• Operators procure through AU

• AU manages procurement of "Maggior Tutela" and "Ultima Istanza"

• Switch to "Ultima Istanza" service

• "Tutela"-like service on a voluntary basis

• Switch to "Ultima Istanza" service

• Operators procure through AU

• AU manages the procurement of only "Ultima Istanza"

• "Ultima Istanza" service: current "Maggior Tutela" operator

• "Tutela"-like service: selected free mkt retailers

• AU manages procurement of only "Ultima Istanza"

• Operator instituted by AEEGSI to supervise the market

• Not expected contract expiration

• Until the client findsa service provider in the free mkt

• In "Ultima Istanza" until the client finds another provider

• In "Tutela"-like service for 1 year from the date of the adjudication of the service

• "Ultima Istanza" service

• "Tutela"-like service managed through bids

Solution sponsored by AEEGSI

Source: analysis on AEEGSI data

11

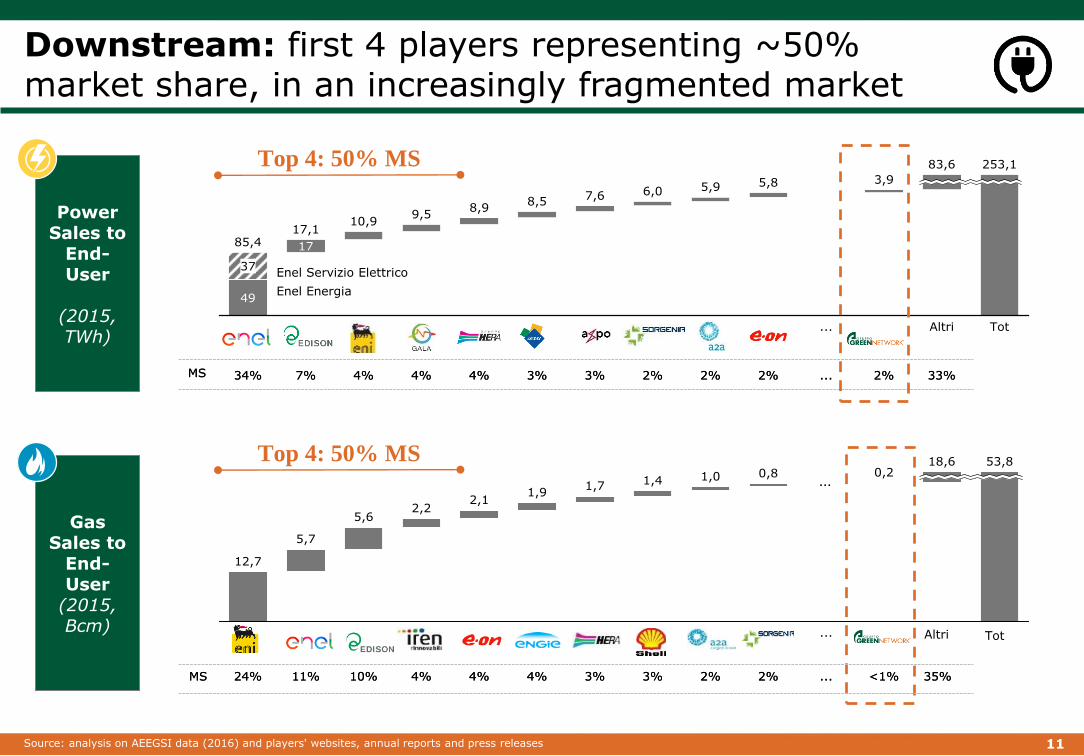

Top 4: 50% MS

Altri Tot

PowerSales to

End-User

(2015, TWh)

GasSales to

End-User

(2015, Bcm)

Enel Servizio Elettrico

Enel Energia

…

Downstream: first 4 players representing ~50%market share, in an increasingly fragmented market

Source: analysis on AEEGSI data (2016) and players' websites, annual reports and press releases

Top 4: 50% MS

12

Downstream: the rise of New Downstream, from a commodity-based to a service-based model

… and tomorrowToday…

Retailer of power & gas

New customers

Equipment retailer

Energy systems management

Provider of TLC services & content

"Smart" system provider

….

Limited customervalue

Limited differentiation

Energy efficiency

Digital trend

…

Commodity ServicesCustomer needs

One business for each retailer One retailer for all businesses

Commodity

Equipment

TLC services & content

Energy systems management

….

"Smart" Systems

13

Several key trends in the UK energy market,with business opportunities mainly in Downstream

Liberalized market with a strong regulatory commitment on transparency and competition

Investment needs and Capacity Market

• Substantial investments in capacity to meet future demand and replace aging plants

• Reduction in RES support, due to conservative Government agenda and economic pressure

• Towards new incentives based on Capacity Market and Contract for Difference

Profits shifting from traditional trading to new services

• Market revision to increase liquidity and regulatory grip over commodities with MiFID/EMIR

• Increasing opportunities in innovative services, e.g. VPP, demand side management

Market opening to new innovative players

• Liberalized market, but still strong positioning of Big 6 players (~87% market share)

• Innovation-based newcomers supported by regulatory incentives and transparency tools

• Further regulatory actions in place (e.g. no caps on # tariffs, settlement system reform)

Generation

Trading

Downstream

14

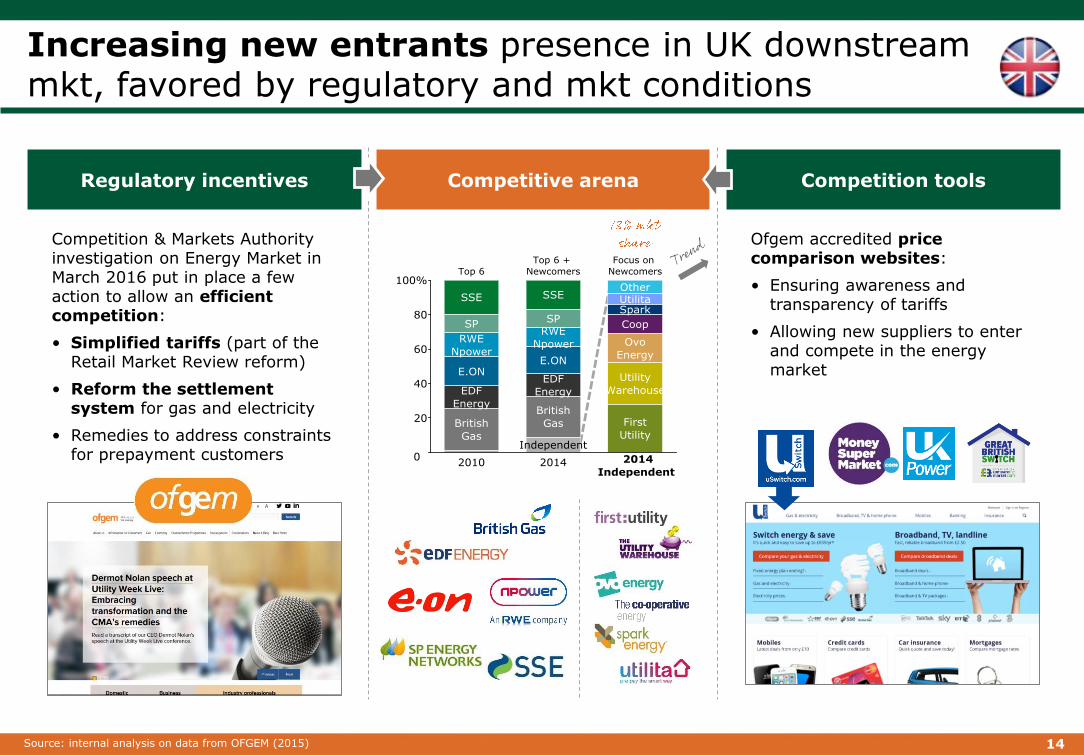

Increasing new entrants presence in UK downstream mkt, favored by regulatory and mkt conditions

Regulatory incentives Competitive arena

Competition & Markets Authority investigation on Energy Market in March 2016 put in place a few action to allow an efficient competition:

• Simplified tariffs (part of the Retail Market Review reform)

• Reform the settlement system for gas and electricity

• Remedies to address constraints for prepayment customers

Ofgem accredited price comparison websites:

• Ensuring awareness and transparency of tariffs

• Allowing new suppliers to enter and compete in the energy market

Competition tools

Source: internal analysis on data from OFGEM (2015)

15

• Market Overview and Trends

• Green Network Overview

• Strategic Guidelines

16

2014

2013

2012

2011

2007

2006

2005

2004

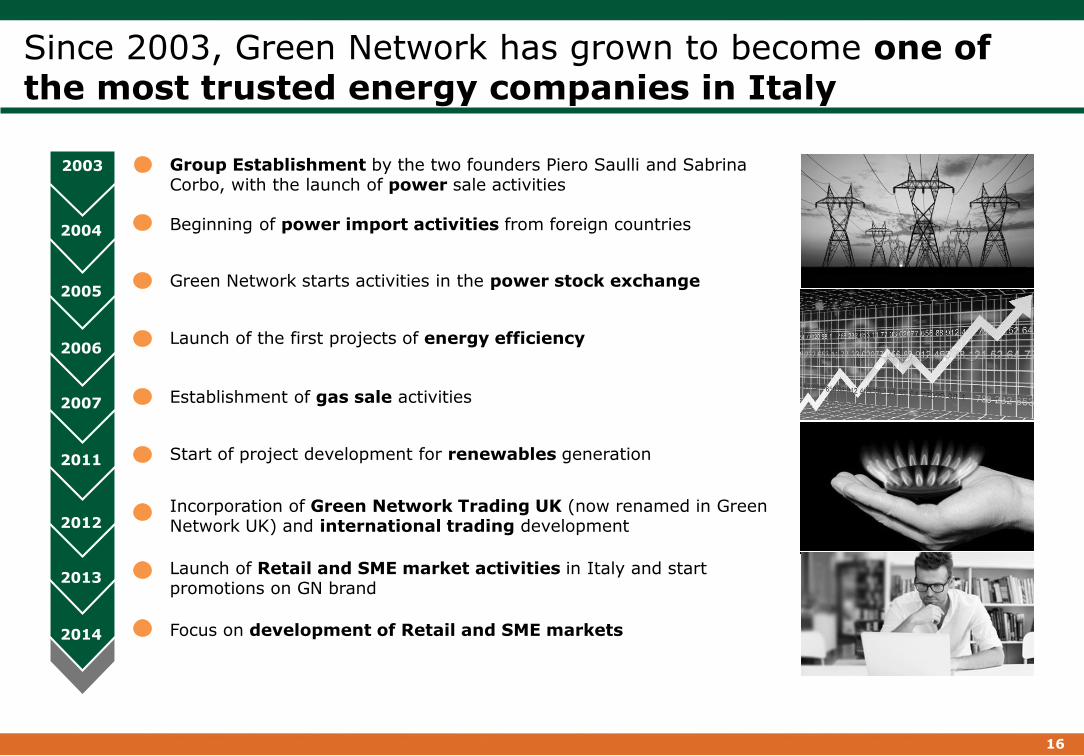

2003 Group Establishment by the two founders Piero Saulli and Sabrina Corbo, with the launch of power sale activities

Beginning of power import activities from foreign countries

Green Network starts activities in the power stock exchange

Launch of the first projects of energy efficiency

Establishment of gas sale activities

Start of project development for renewables generation

Incorporation of Green Network Trading UK (now renamed in Green Network UK) and international trading development

Launch of Retail and SME market activities in Italy and start promotions on GN brand

Focus on development of Retail and SME markets

Since 2003, Green Network has grown to become one of the most trusted energy companies in Italy

17

Green Network today is a primary independent player in the Italian energy market

To consolidate Green Network position as a primary independent player in the energy market, by creating added value for its customers

through consolidated methodologiesMission

Trading

G&P Sales

RES Generation

Holding

Other Businesses

Green Network Holding

Rinnov. S.r.l.

Green Network Energy

SolergysRena

Energia

SolCapGREEN

Green Hydro 1

Green Hydro 2

Green Wind 1

GreenWind 2

83%

100%

100% 55%

49% 51%

51%

51% 51% 51% 87%

74% 55%

ATAEnergia

SpectrumTech S.r.l.

Company structure Leading offices

London officeLeading office for trading and sales activities

Rome officeLeading office for all activities but trading

1 2

100%

Genera Green Energy.

100% 80%

18

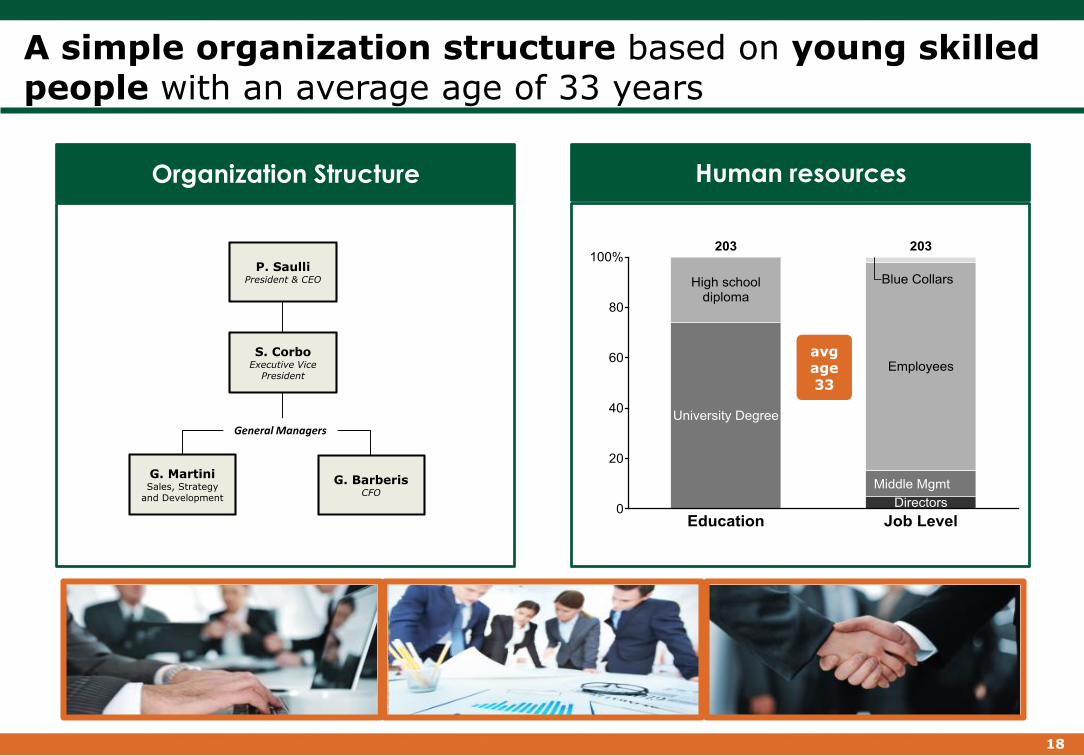

A simple organization structure based on young skilled people with an average age of 33 years

avgage33

Human resourcesOrganization Structure

S. CorboExecutive Vice

President

P. SaulliPresident & CEO

G. MartiniSales, Strategy

and Development

G. BarberisCFO

General Managers

19

Green Network today is lead by a management with deep know-how of energy markets

• Founder of Green Network S.p.A.

• More than 10 year of legal advisory for energy sector players

• Specialization in international business and corporate law

Piero SaulliCEO & Chairman

Sabrina CorboVP

Giovanni BarberisCFO

Giuseppe MartiniCOO

• Founder of Green Network S.p.A.

• Former top manager at Enel S.p.A., where he held various role in definition and development of Italian electricity market

• Former top manager at Enel S.p.A., where he held various role both in technical development and sales department

• Last years at Enel S.p.A. he worked for consolidation of services to large customers

• Since 2016 CFO at Green Network

• Former CFO at d'Amico Compagnia di Navigazione

• Former CFO at ACEA and previously at Hera

• Former CEO at Arena

• Former CFO at CremoniniGroup

• Former CFO at Simint(Giorgio Armani Group)

20

Commercial development lead growth EBITDA of Green Network Spa over last years

EBITDA (M€)

NFP (M€)

EBIT (M€)

EBITDA increased reaching

~24M€ in 2015 driven by an

improvement of profitability

margin (EBITDA %)

21

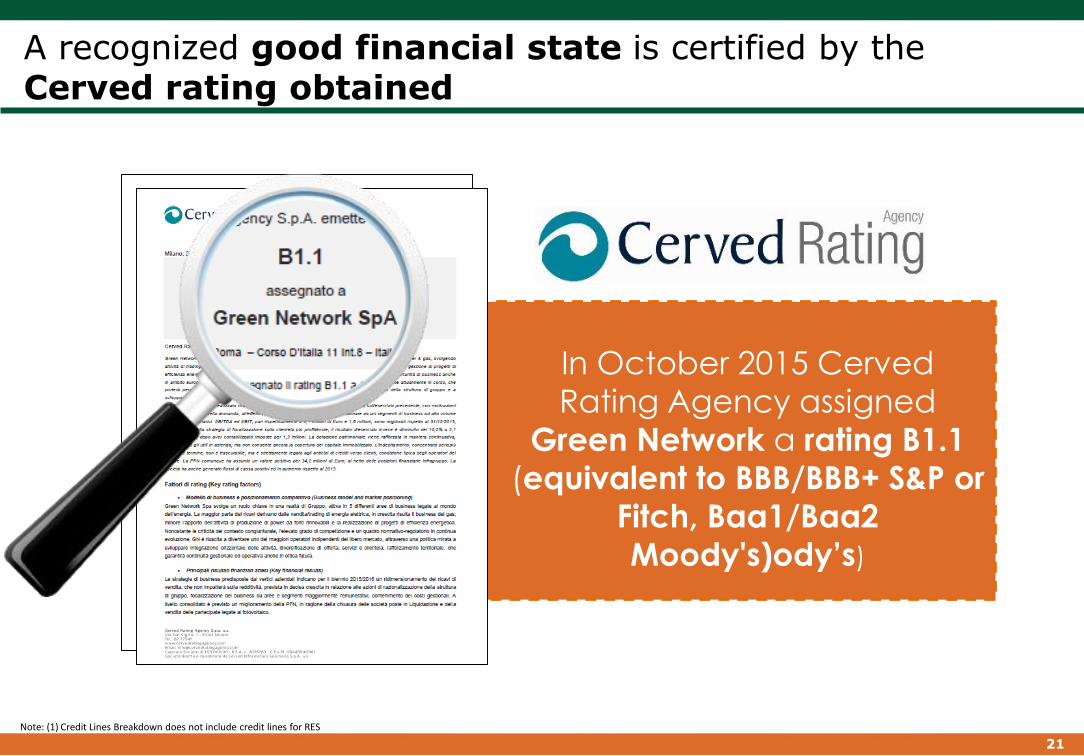

A recognized good financial state is certified by the Cerved rating obtained

In October 2015 Cerved

Rating Agency assigned

Green Network a rating B1.1

(equivalent to BBB/BBB+ S&P or

Fitch, Baa1/Baa2

Moody's)ody’s)

Note: (1) Credit Lines Breakdown does not include credit lines for RES

22

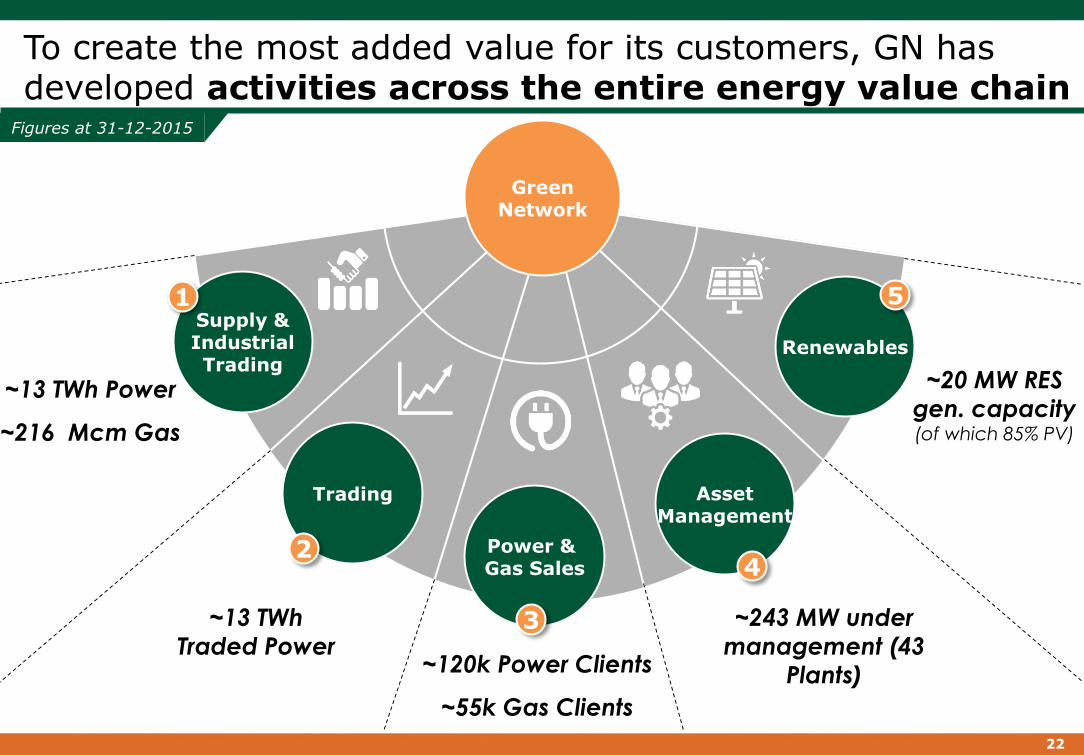

To create the most added value for its customers, GN has developed activities across the entire energy value chain

AssetManagement

Power & Gas Sales

Supply &IndustrialTrading

Trading

Renewables

1 5

4

3

2

GreenNetwork

~13 TWh Power

~216 Mcm Gas

~13 TWh

Traded Power~120k Power Clients

~55k Gas Clients

~243 MW under

management (43

Plants)

~20 MW RES

gen. capacity (of which 85% PV)

Figures at 31-12-2015

23

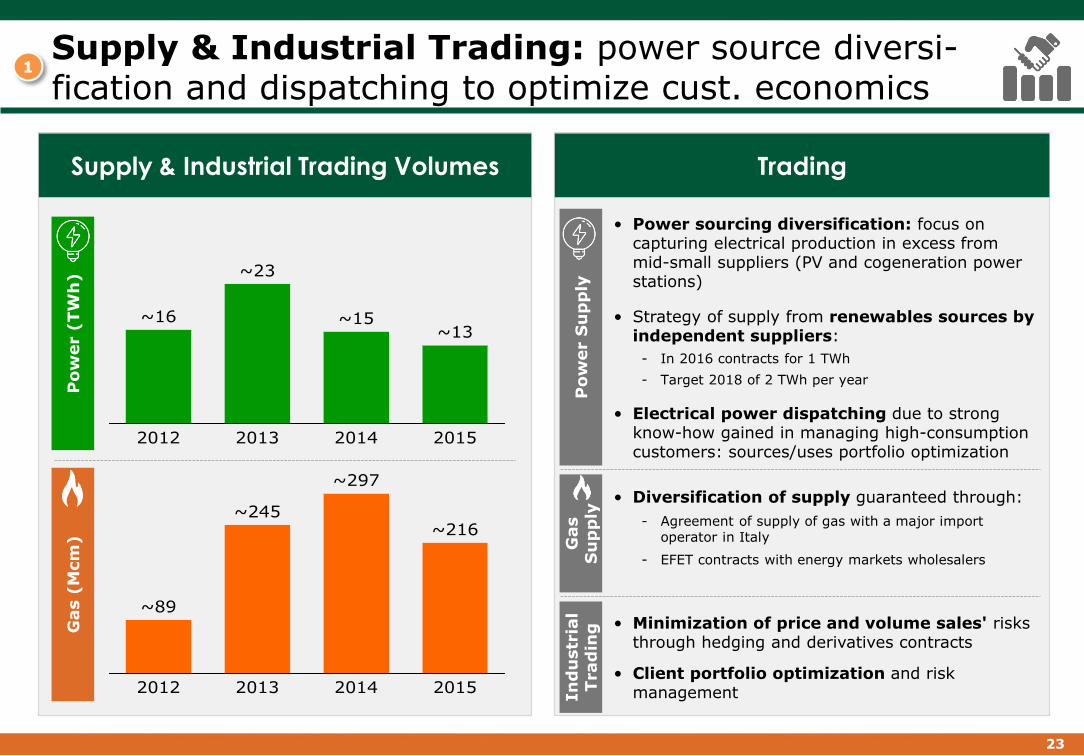

Supply & Industrial Trading: power source diversi-fication and dispatching to optimize cust. economics

1

Supply & Industrial Trading Volumes Trading

• Power sourcing diversification: focus on capturing electrical production in excess from mid-small suppliers (PV and cogeneration power stations)

• Strategy of supply from renewables sources by independent suppliers:

- In 2016 contracts for 1 TWh

- Target 2018 of 2 TWh per year

• Electrical power dispatching due to strong know-how gained in managing high-consumption customers: sources/uses portfolio optimization

Po

wer S

up

ply

• Minimization of price and volume sales' risks through hedging and derivatives contracts

• Client portfolio optimization and risk management

Gas

Su

pp

ly

• Diversification of supply guaranteed through:

- Agreement of supply of gas with a major import operator in Italy

- EFET contracts with energy markets wholesalersIn

du

str

ial

Trad

ing

Po

wer (

TW

h)

Gas (

Mcm

)

24

Trading: Buying and selling, Derivatives and Risk Management within a limited risk profile

2

• Proprietary Trading, established in 2012,operates in main European power trading exchange platforms and OTC

• Currently operating in Italy, Switzerland, UK, France, Austria, and Germany

• Main activities:

- Simply Buying & Selling standard products

- Derivatives contracts on power market

- Risk management

Traded Volumes (TWh) Activity Description

25

Po

wer

Gas

Volume breakdown (2015)

End-user 7.7 TWh

Wholesale

Total

3.6 TWh

11.2 TWh

End-user 183 MScm

Power & Gas Sales: served all customer clusters, with 11 TWh power and 183 MScm gas sales in 2015

3

Clients evolution* (2015)

Domestic (# clients)

Small Bsn (# clients)

Med/Large Bsn (# clients)

Note: (*) Client evolution doesn't include High-Consumption and Wholesaler cluster; Fonte: Management

26

SECOND BEST CUSTOMER SERVICE

in Jan-15 for Altroconsumo

BEST ENERGY OFFER in Feb-15

with "I love Green Network" for

TGCOM24

• TGCOM24 monthly publishes “Il blog del consumatore” (The consumer blog)

identifying best energy offers available on the market

• Green Network Power&Gas was

ranked in first place for energy price thanks to

the offer "I love Green Network"

• In an investigation of

consumer periodical Altroconsumo Jan-2015,

among the top national companies to power supplycustomer service, Green Network Power & Gas is

ranked second for quality

• Main evaluated parameters were info on costs and bills, call center waiting time, …

3Power & Gas Sales: GN has been awarded of several price from consumer studies

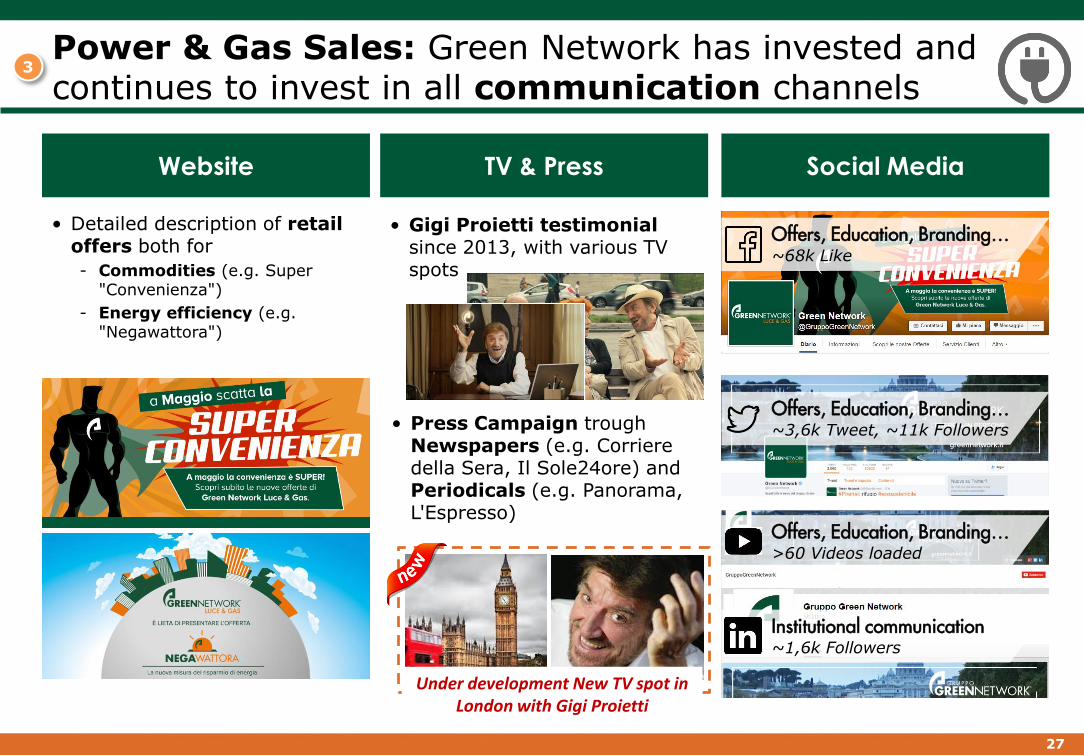

27

Website Social MediaTV & Press

Offers, Education, Branding…~68k Like

Offers, Education, Branding…~3,6k Tweet, ~11k Followers

• Gigi Proietti testimonial since 2013, with various TV spots

• Press Campaign trough Newspapers (e.g. Corrieredella Sera, Il Sole24ore) and Periodicals (e.g. Panorama, L'Espresso)

Institutional communication~1,6k Followers

Offers, Education, Branding…>60 Videos loaded

• Detailed description of retail offers both for

- Commodities (e.g. Super "Convenienza")

- Energy efficiency (e.g. "Negawattora")

3Power & Gas Sales: Green Network has invested and continues to invest in all communication channels

Under development New TV spot in London with Gigi Proietti

28

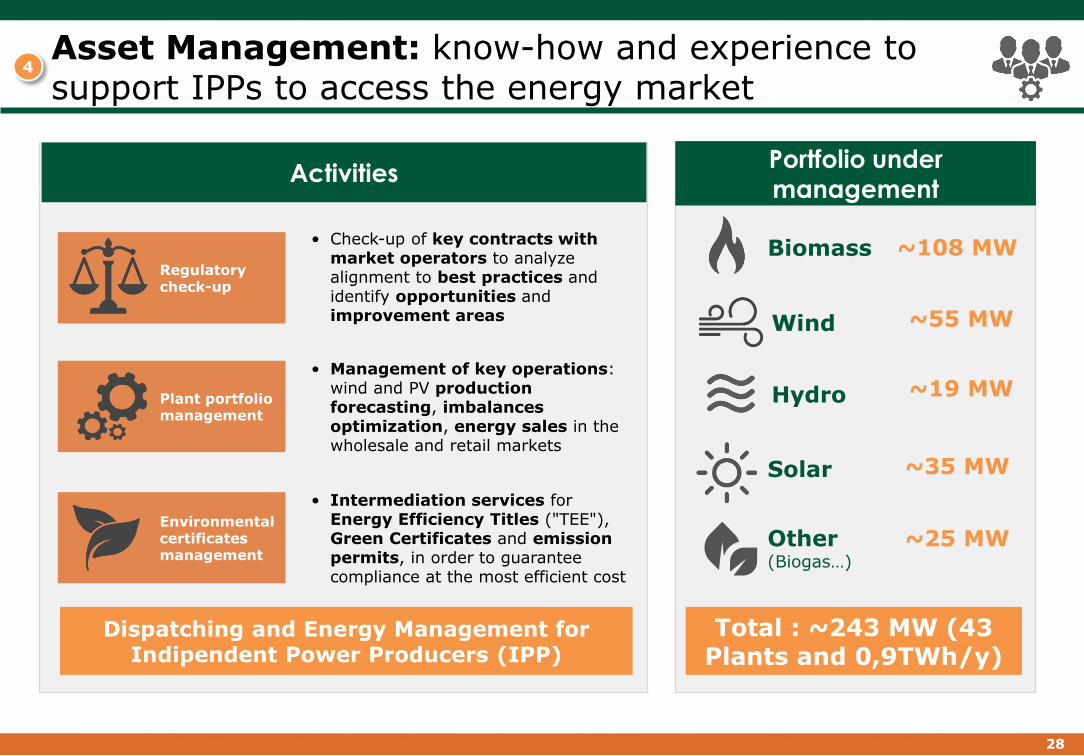

Asset Management: know-how and experience to support IPPs to access the energy market

4

Dispatching and Energy Management for Indipendent Power Producers (IPP)

Activities

Regulatorycheck-up

Plant portfoliomanagement

Environmental certificatesmanagement

• Check-up of key contracts with market operators to analyze alignment to best practices and identify opportunities and improvement areas

• Management of key operations: wind and PV production forecasting, imbalances optimization, energy sales in the wholesale and retail markets

• Intermediation services for Energy Efficiency Titles ("TEE"), Green Certificates and emission permits, in order to guarantee compliance at the most efficient cost

Portfolio under management

Solar

Wind

Hydro

Biomass ~108 MW

Total : ~243 MW (43 Plants and 0,9TWh/y)

Other(Biogas…)

~55 MW

~19 MW

~35 MW

~25 MW

29

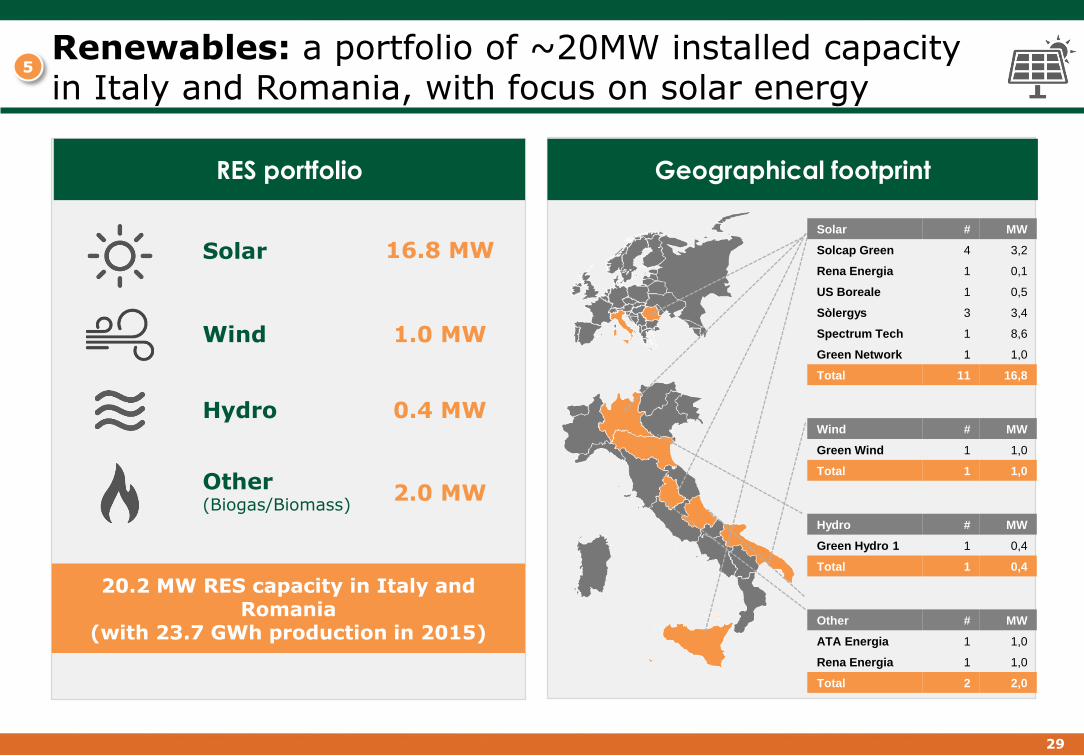

Geographical footprint

Solar

Wind

Hydro

Other(Biogas/Biomass)

16.8 MW

1.0 MW

0.4 MW

2.0 MW

20.2 MW RES capacity in Italy and Romania

(with 23.7 GWh production in 2015)

RES portfolio

Renewables: a portfolio of ~20MW installed capacity in Italy and Romania, with focus on solar energy

5

Solar # MW

Solcap Green 4 3,2

Rena Energia 1 0,1

US Boreale 1 0,5

Sòlergys 3 3,4

Spectrum Tech 1 8,6

Green Network 1 1,0

Total 11 16,8

Wind # MW

Green Wind 1 1,0

Total 1 1,0

Hydro # MW

Green Hydro 1 1 0,4

Total 1 0,4

Other # MW

ATA Energia 1 1,0

Rena Energia 1 1,0

Total 2 2,0

30

• Market Overview and Trends

• Green Network Overview

• Strategic Guidelines

31

New Strategic and Industrial Plan will be based on strong key pillars…

Improve customer loyalty

New channels strategy leveraging on strategic

partnerships

Exploit operational excellence and cost discipline

Strengthen profitability

Control and mitigate risks in trading activities

Widen the offer developing digital technologies

32

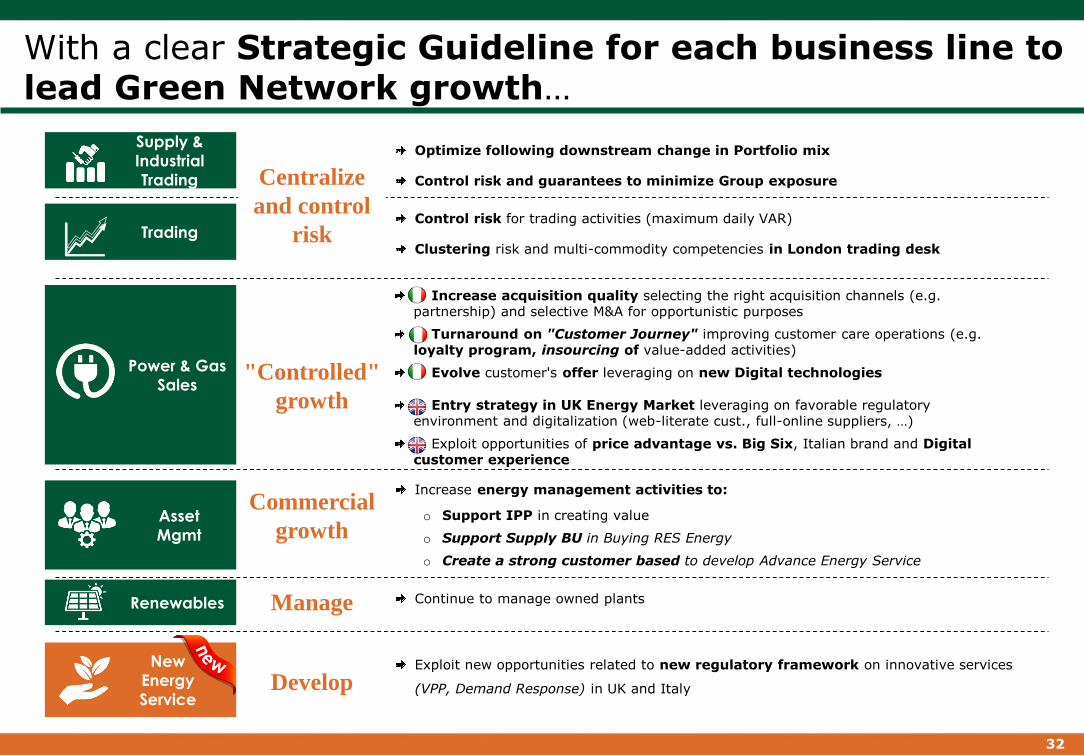

Trading

Power & Gas

Sales

Asset

Mgmt

Renewables

New

Energy

Service

Control risk for trading activities (maximum daily VAR)

Clustering risk and multi-commodity competencies in London trading desk

Increase acquisition quality selecting the right acquisition channels (e.g. partnership) and selective M&A for opportunistic purposes

Turnaround on "Customer Journey" improving customer care operations (e.g. loyalty program, insourcing of value-added activities)

Evolve customer's offer leveraging on new Digital technologies

Entry strategy in UK Energy Market leveraging on favorable regulatory environment and digitalization (web-literate cust., full-online suppliers, …)

Exploit opportunities of price advantage vs. Big Six, Italian brand and Digital customer experience

"Controlled"

growth

Increase energy management activities to:

o Support IPP in creating value

o Support Supply BU in Buying RES Energy

o Create a strong customer based to develop Advance Energy Service

Commercial

growth

Manage

Exploit new opportunities related to new regulatory framework on innovative services

(VPP, Demand Response) in UK and ItalyDevelop

Continue to manage owned plants

Supply &

Industrial

Trading

Optimize following downstream change in Portfolio mix

Control risk and guarantees to minimize Group exposureCentralize

and control

risk

With a clear Strategic Guideline for each business line to lead Green Network growth…

33

OUTLOOK

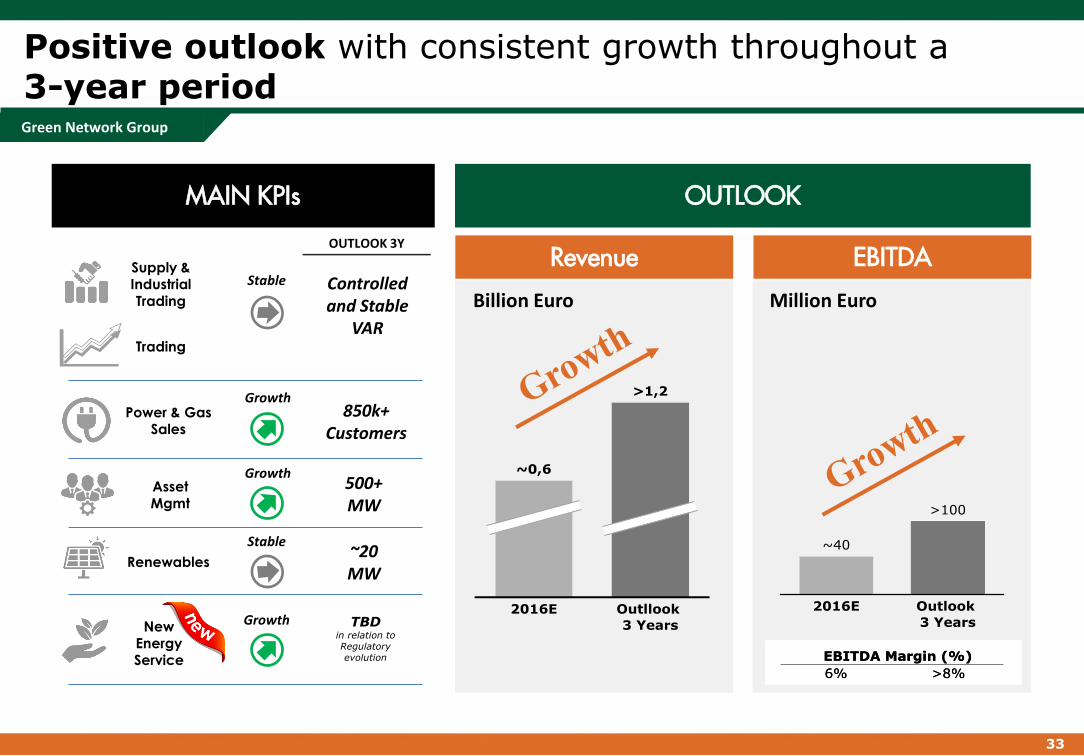

Positive outlook with consistent growth throughout a3-year period

Revenue EBITDA

MAIN KPIs

Trading

Power & GasSales

AssetMgmt

Renewables

New EnergyService

Supply &Industrial Trading

850k+ Customers

Stable

500+ MW

Stable

TBDin relation to Regulatoryevolution

Growth

Growth

Growth

Controlledand Stable

VAR

~20 MW

OUTLOOK 3Y

Billion Euro Million Euro

Green Network Group

34

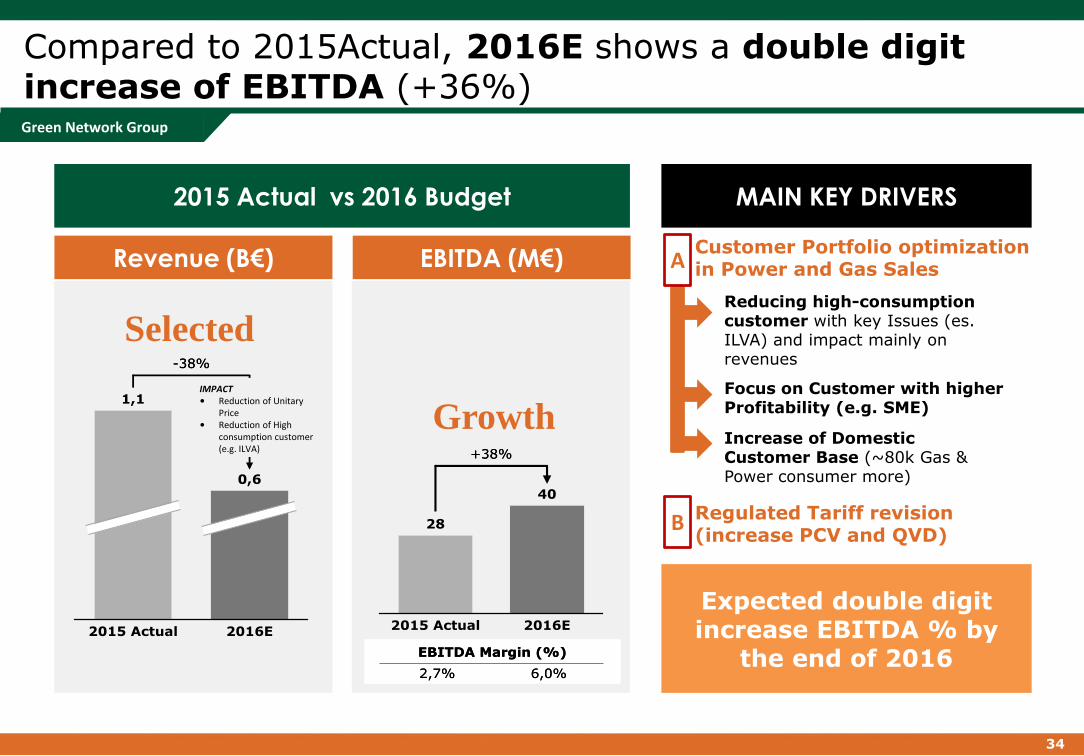

2015 Actual vs 2016 Budget

Compared to 2015Actual, 2016E shows a double digit increase of EBITDA (+36%)

Revenue (B€) EBITDA (M€)Customer Portfolio optimization in Power and Gas Sales

Focus on Customer with higher Profitability (e.g. SME)

Reducing high-consumption customer with key Issues (es. ILVA) and impact mainly on revenues

Increase of Domestic Customer Base (~80k Gas & Power consumer more)

Expected double digit increase EBITDA % by

the end of 2016

MAIN KEY DRIVERS

IMPACT• Reduction of Unitary

Price • Reduction of High

consumption customer(e.g. ILVA)

Regulated Tariff revision (increase PCV and QVD)

A

B

Growth

Selected

Green Network Group

35

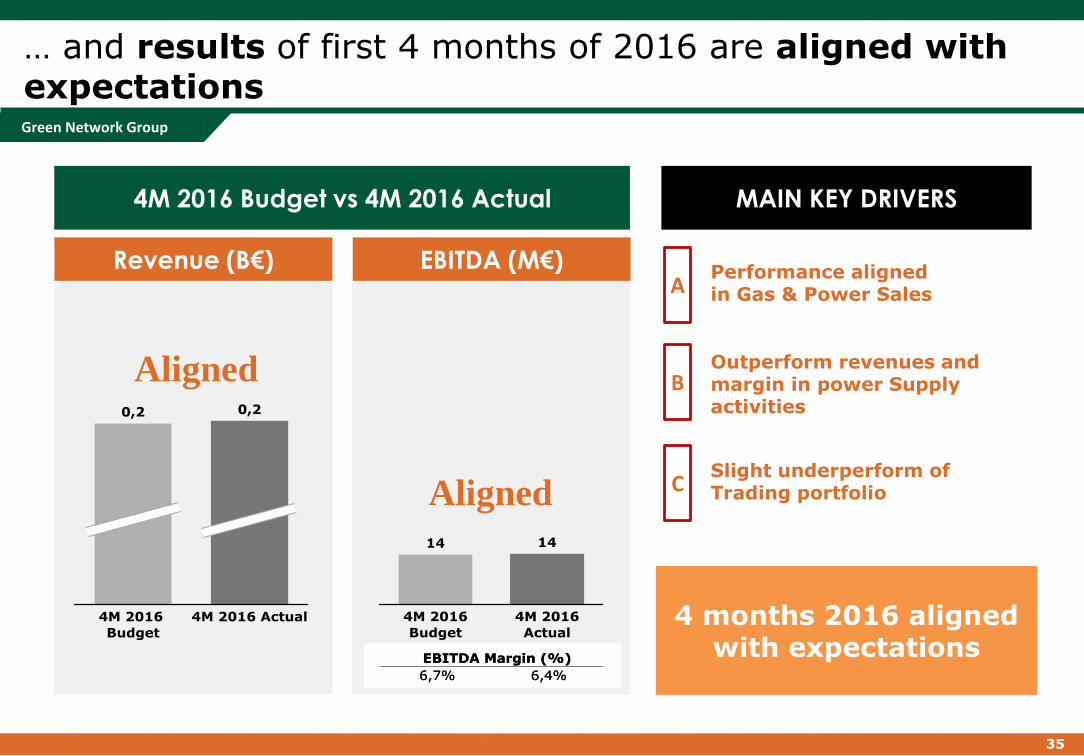

4M 2016 Budget vs 4M 2016 Actual

… and results of first 4 months of 2016 are aligned with expectations

Revenue (B€) EBITDA (M€)

4 months 2016 aligned with expectations

MAIN KEY DRIVERS

Performance aligned in Gas & Power Sales

Slight underperform of Trading portfolio

A

C

Outperform revenues and margin in power Supply activities

B

Aligned

Aligned

Green Network Group

Related Documents