Company Level Financial Management Accounting

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Company Level

Financial

ManagementAccounting

Accounting

• It's the process of maintaining the Balance implies by the

equation:

• Assets = Liabilities + Owner Equity

• Base of Accounting

Base of Accounting

Cash Base Accrual BaseA business transaction is

recorded for accounting purpose

at the time money is transferred

either paid or received

A business transaction is recorded

for accounting purpose at the time

on obligation for payment incurred

rather than the time of payment

Accrual Methods

• Method of income recognition (Revenue)

• 1.Billing Method:

�Income is recognized by viewing the amount billed as revenue

even it's not collected.

�Billed Amount < Earned Revenue

�(Case of Under Billing)

�Billed Amount > Earned Revenue

�(Case of Over Billing)

�This case occur at the unbalanced bid

•

Accrual Methods2.Percent of completion Method(P.O.C.):

• Revenue is calculated based on the percentage of completion.

• e.g.:

• Tender Price = 2,000,000

• % of Completion = 40%

• Revenue = 2,000,000 × 0.4 = 800,000

• How to Calculate P.O.C.?? :

• Cost to Cost method:

• Man-hours method:

• Unit of Work Performed:

Accrual Methods:2.Percent of completion Method(P.O.C.):

a) Cost to Cost method:

• To solve the problem of over extra cost than the estimated

(real case scenario)

b) Man-hours method:

c) Unit of Work Performed:

Accrual Methods:3. Completed Contract Method(C.C.):

• Revenue and Expenses are delayed to the end of project

• The advantage of this method that we can calculate the

revenue decisively

• The disadvantage of this method the irregularity of accounting

process and tax payments

Example 1:

• A company has 2 projects during 2 years period:

• Calculate the net income (Revenue) in each of the two years

using:

• Billing Method

• P.O.C.

• C.C.

• Tax rate = 20%45

ProjectEstimated

Cost

Tender

Price

Year 20x1 Year 20x2

Amount

Billed

Cost

Incurred

Amount

Billed

Cost

Incurred

P 1 620,000 700,000 340,000 300,000 360,000 320,000

P 2 760,000 840,000 320,000 320,000 450,000 420,000

Example 1: Solution

1. Billing Method

Year 20X1 20X2

Expenses…………. (1)

300,000

+320,000

320,000

+420,000

620,000 740,000

Revenue………..….(2)

340,000

+320,000

360,000

+450,000

660,000 810,000

Profit (2-1)………….(3) 40,000 70,000

Tax 20% =(3)x0.2….(4) 8,000 14,000

Net Profit (3-4) 32,000 56,000

Example 1: Solution

2. P.O.C. MethodYear 20X1 20X2

Expenses…………. (1)

300,000

+320,000

320,000

+420,000

620,000 740,000

Revenue………..….(2)

692,394 825,501

Profit (2-1)………….(3) 72,394 85,501

Tax 20% =(3)x0.2….(4) 14,479 17,100

Net Profit (3-4) 57,915 68,401

3. C.C. Method

• At year 20x1 both projects has not completed

• At year 20x2 only project 1 has been completed

Year 20X1 20X2

Expenses…………. (1)- 300,000+320,000

0 620,000

Revenue………..….(2) 0 700,000

Profit (2-1)………….(3) 0 80,000

Tax 20% =(3)x0.2….(4) 0 16,000

Net Profit (3-4) 0 64,000

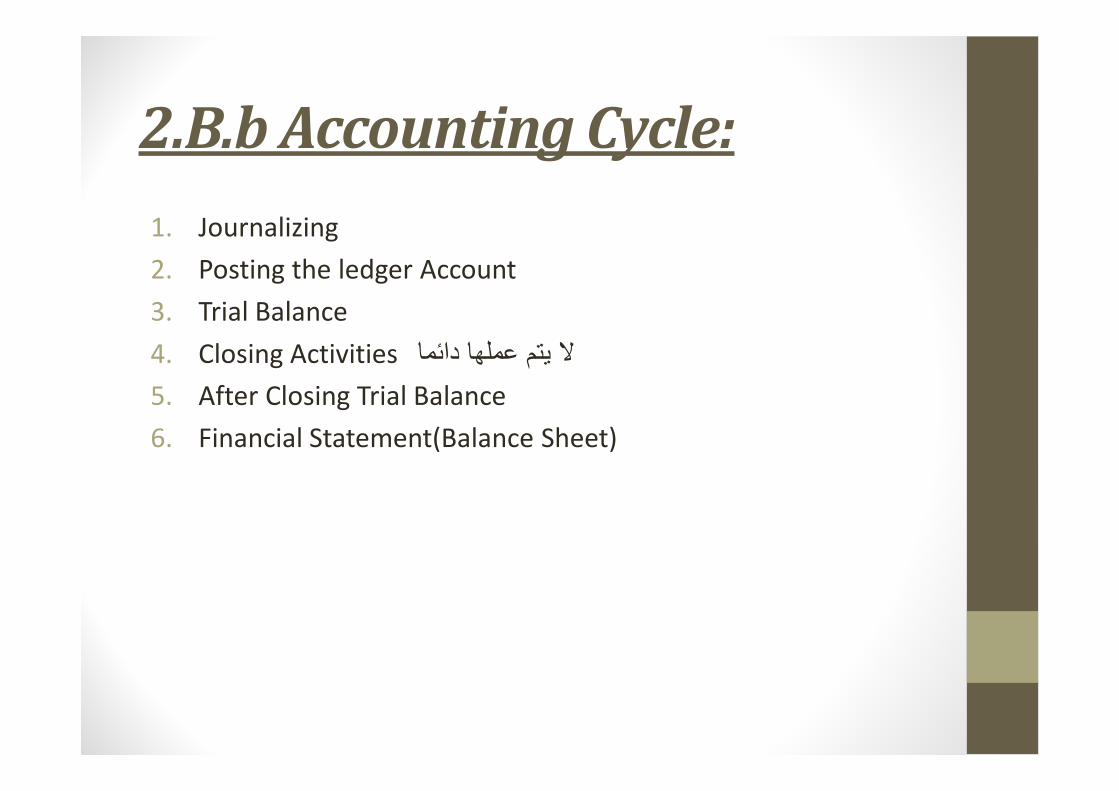

2.B.b Accounting Cycle:

1. Journalizing

2. Posting the ledger Account

3. Trial Balance

4. Closing Activities يتم عملھا دائما

5. After Closing Trial Balance

6. Financial Statement(Balance Sheet)

Journalizing:

No. Date Description Dr Cr

Assets = Liab + O.E. + Revenue - Expenses

Dr Cr Dr Cr Dr Cr Dr Cr Dr Cr

+ - - + - + - + + -

Accounting equation

Table: Journal Form

Journalizing:

• Any transaction has two process, one of them dr and the

other(s) cr.

• If we want to journalize transaction we have to answer the

following question:

1. Which account is affected according to the previous

equation?

2. Which account will increase? And, which account will

decrease?

Journalizing:

• Example.:

• A company purchased equipment 100,000 cash

• The equipment is a fixed asset, and this account have been

increased so it will be recorded as a dr.

• It will be paid in cash (current asset), so this account will be

decreased , so it will be recorded as a cr.

No. Date Description Dr Cr

1 ----------- Equipment(F.A.)

Cash(C.A.)

100,000

100,000

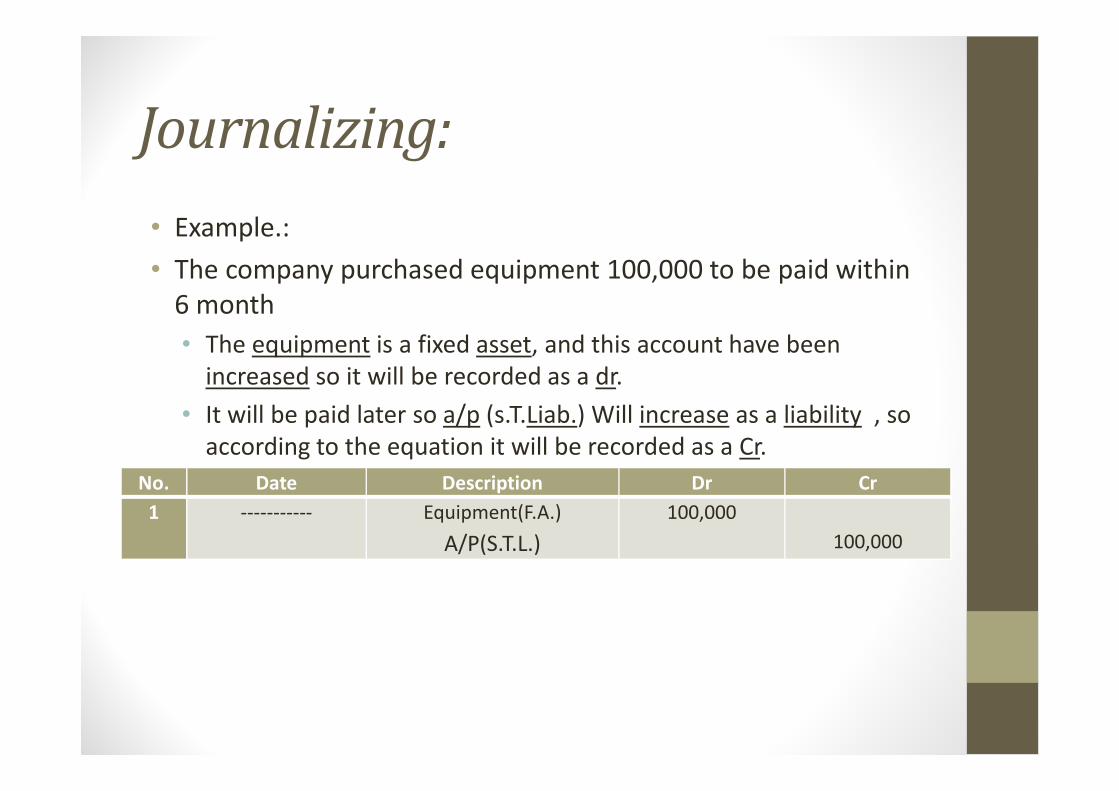

Journalizing:

• Example.:

• The company purchased equipment 100,000 to be paid within

6 month

• The equipment is a fixed asset, and this account have been

increased so it will be recorded as a dr.

• It will be paid later so a/p (s.T.Liab.) Will increase as a liability , so

according to the equation it will be recorded as a Cr.

No. Date Description Dr Cr

1 ----------- Equipment(F.A.)

A/P(S.T.L.)

100,000

100,000

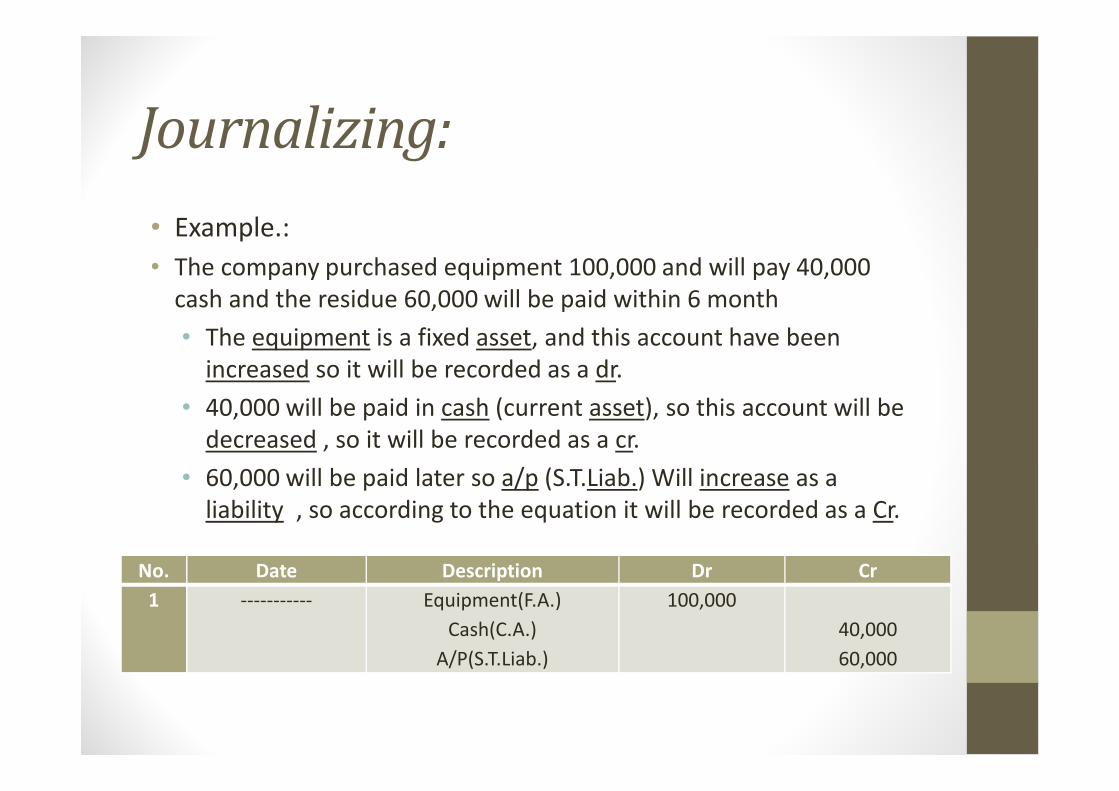

Journalizing:

• Example.:

• The company purchased equipment 100,000 and will pay 40,000

cash and the residue 60,000 will be paid within 6 month

• The equipment is a fixed asset, and this account have been

increased so it will be recorded as a dr.

• 40,000 will be paid in cash (current asset), so this account will be

decreased , so it will be recorded as a cr.

• 60,000 will be paid later so a/p (S.T.Liab.) Will increase as a

liability , so according to the equation it will be recorded as a Cr.

No. Date Description Dr Cr

1 ----------- Equipment(F.A.)

Cash(C.A.)

A/P(S.T.Liab.)

100,000

40,000

60,000

Posting to the ledger Account:Cash A/R

Dr Cr Dr Cr

Posting from

journal

Posting from

journal

Posting from

journal

Posting from

journal

total total total total

difference - difference -

Equipment A/P

Dr Cr Dr Cr

Posting from

journal

Posting from

journal

Posting from

journal

Posting from

journal

total total total total

difference - - difference

Ledger accounts forms

Posting to the ledger Account:

• After finishing the journalizing step we post the records to the ledger accounts as following:• write the record from the previous balance sheet to the related ledger

account and at the related position from the journal (Assets always placed at Dr of the Ledger account, and Liabilities & O.E. always placed at the Cr of the ledger account)

• write the record from journal to the related ledger account and at the same position from the journal (e.g. :if the cash have been recorded as a Cr in the journal so we will put it in Cr Column of the ledger(cash),and the reverse(Dr) is correct)

• Calculate the summation for each column (Dr & Cr) for all of the ledger accounts.

• Calculate the difference between the total Dr and the total Cr

• Place the difference at the related cell (Assets always placed at Dr , and Liabilities & O.E. always placed at the Cr ) as a final result from this step.

Trial Balance:

• List all the ledger account titles (and the remainder accounts

that are not journalized) at the account column of the trial

balance.

• Write the final difference from the ledger account to the

corresponding cell at the trial balance (e.g.: Cash from ledger

will be placed at the Cash/Dr cell in the trial balance……etc.).

• As a final check for all previous steps (journalizing, posting to

the ledger account, trial balance):

• Total Dr of the trial balance = Total Cr of the trial balance

No. Account Dr Cr

1 Cash √ -

2 A/R √ -

3 Equipment √ -

.. ……… …. ….

n A/P - √

Total √ √

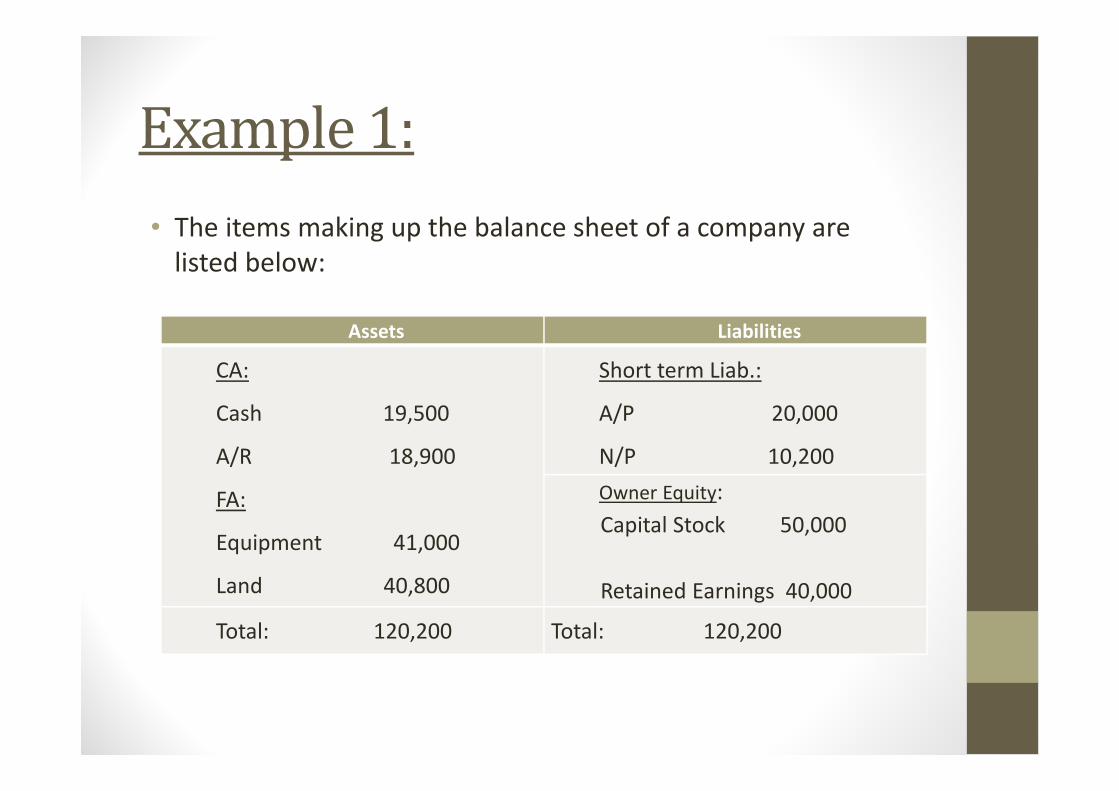

Example 1:

• The items making up the balance sheet of a company are

listed below:

Assets Liabilities

CA:

Cash 19,500

A/R 18,900

FA:

Equipment 41,000

Land 40,800

Short term Liab.:

A/P 20,000

N/P 10,200

Owner Equity:

Capital Stock 50,000

Retained Earnings 40,000

Total: 120,200 Total: 120,200

Example 1:

• During a short time period the company has the following transactions:

1. June 11, the company issued additional stocks of 3,000 at L.E.20 per stock.

2. June 12, the company bought equipment of L.E.20,000 paid cash.

3. June 13, A/P are paid in full.

4. June 14, the company collect A/R of L.E. 15,000

5. June 15, the company bought Land for L.E. 70,000: paid 20,000 in cash and the remainder are due within 4 months.

• Required:

1. Make journal entries

2. Post to the ledger account

3. Make a trial Balance

4. Make a Balance sheet , dated June 15

Example 1: Solution

• 1. Journalizing:

No. Date Description Dr Cr

1 June 11 Cash(C.A.)

Capital stocks(O.E.)

60,000

60,000

2 June 12 Equipment (F.A.)

Cash (C.A.)

20,000

20,000

3 June 13 A/P(S.T.L.)

Cash(C.A.)

20,000

20,000

4 June 14 Cash(C.A.)

A/R(C.A.)

15,000

15,000

5 June 15 Land (F.A.)

Cash(C.A.)

A/P(S.T.L)

70,000

20,000

50,000

Example 1: Solution

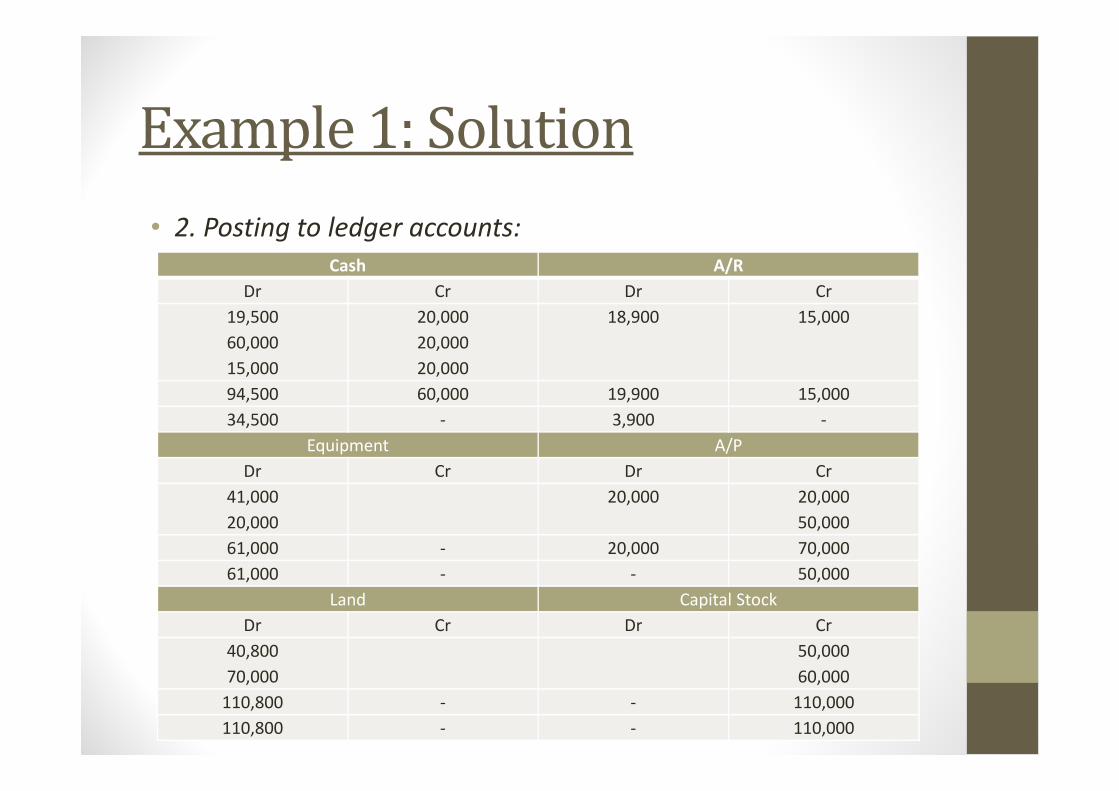

• 2. Posting to ledger accounts:

Cash A/R

Dr Cr Dr Cr

19,500

60,000

15,000

20,000

20,000

20,000

18,900 15,000

94,500 60,000 19,900 15,000

34,500 - 3,900 -

Equipment A/P

Dr Cr Dr Cr

41,000

20,000

20,000 20,000

50,000

61,000 - 20,000 70,000

61,000 - - 50,000

Land Capital Stock

Dr Cr Dr Cr

40,800

70,000

50,000

60,000

110,800 - - 110,000

110,800 - - 110,000

Example 1: Solution

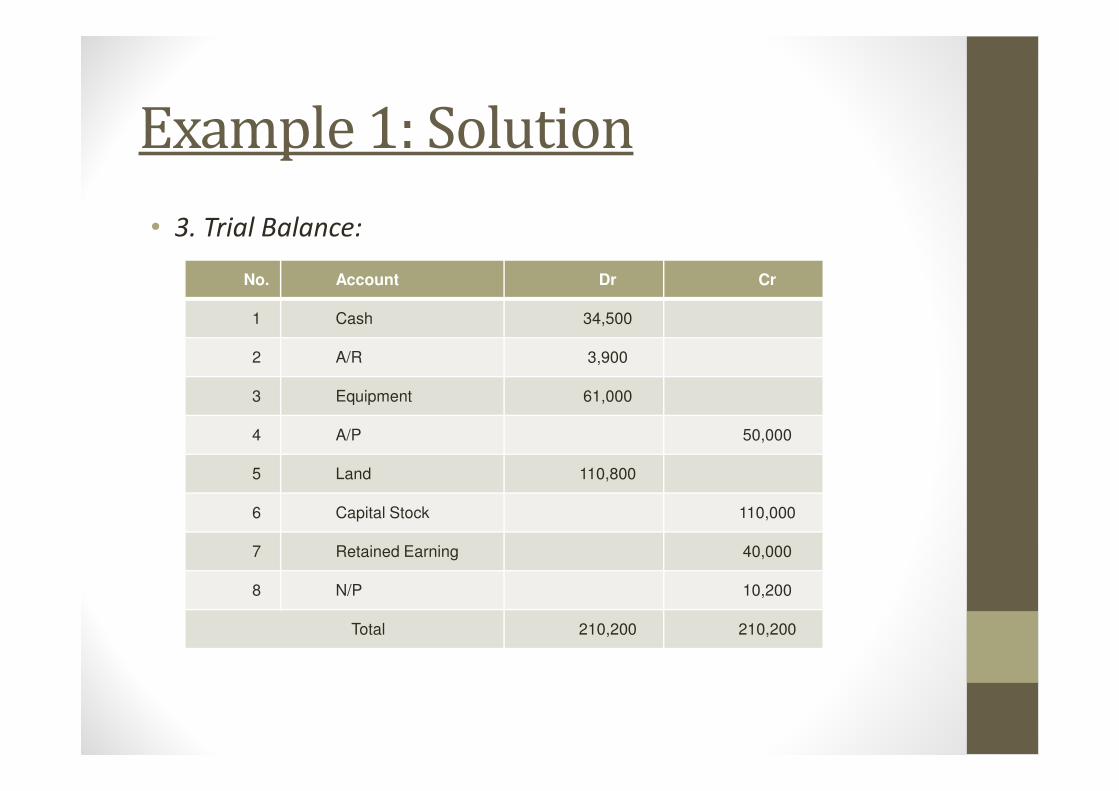

• 3. Trial Balance:

No. Account Dr Cr

1 Cash 34,500

2 A/R 3,900

3 Equipment 61,000

4 A/P 50,000

5 Land 110,800

6 Capital Stock 110,000

7 Retained Earning 40,000

8 N/P 10,200

Total 210,200 210,200

Example 1: Solution

• 4. Balance Sheet at June 15:

Assets Liabilities

CA:

Cash 34,500

A/R 3,900

FA:

Equipment 61,000

Land 110,800

Short term Liab.:

A/P 50,000

N/P 10,200

Owner Equity:

Capital Stock 110,000

Retained Earnings 40,000

Total: 210,200 Total: 210,200

Example 2:

• The balance sheet of a certain construction company of

December 2007 is given below; Assume this company is using

the billing method of income recognition:

Assets Liabilities

C.A.:

Cash 75,000

A/R 110,000

S.T.L.:

A/P 85,000

N/P 50,000

Long.T.L.: 60,000Total C.A. 185,000

F.A.:

Building 300,000

Less accumulated dep. 150,000

Equipment 240,000

Less accumulated dep. 80,000

Total Liab. 195,000

Owner Equity.

Capital Stock 250,000

Retained Earnings 70,000

Total O.E. 320,000

Total F.A. 310,000

Other assets 20,000

Total: 515,000 Total: 515,000

Example 2:• The company has the following transaction:

No. Date Description

1 2/1 The company bought Equipment for L.E. 130,000: paid 15,000 in cash and the

remainder are due within 6 months.

2 4/2 Company was billed 20,000 by material supplier

3 4/3 Company paid 20,000 to material supplier(transaction #2)

4 8/3 Company billed client for L.E. 320,000 (bill #1 on job 101)

5 7/4 Company was billed 60,000 by equipment renting company

6 8/5 Company received 290,000 from client (bill #1)

7 7/6 Company paid 60,000 to equipment renting company (transaction #5)

8 3/7 Company paid 70,000 to cast of labor

9 16/8 Company was billed 45,000 by S/C

10 16/9 Company paid 45,000 to S/C(transaction #9)

11 1/10 Company billed client for L.E. 280,000 (bill #2 on job 101)

12 20/10 A/R of 20,000 were collected

13 15/11 Company received 265,000 from client (bill #2)

14 15/12 A/P of 40,000 are paid

15 25/12 Company paid 145,000 payroll expenses

16 30/12 Building dep. of 30,000 is recognized

17 30/12 Equipment dep. of 65,000 is recognized

18 30/12 20% tax of net profit are paid

19 30/12 Dividends paid in amount of 20,000

Example 2:

• 1-prepare journal entries

• 2-prepare income statement

• 3-Establish relevant posting accounts

• 4-close account at Dec. 31 2008

• 5-prepare trial balance

• 6-prepare balance sheet

Example 2: Solution

1. Journalizing:No. Date Description Dr Cr

1 2/1 Equipment(F.A.)

Cash(C.A.)

A/P(S.T.L.)

130,000

15,000

115,000

2 4/2 W.I.P. (expenses)

A/P(S.T.L.)

20,000

20,000

3 4/3 A/P(S.T.L.)

Cash(C.A.)

20,000

20,000

4 8/3 A/R(C.A.)

Revenue

320,000

320,000

5 7/4 W.I.P. (expenses)

A/P(S.T.L.)

60,000

60,000

6 8/5 Cash(C.A)

A/R(C.A.)

290,000

290,000

7 7/6 A/P(S.T.L.)

Cash(C.A.)

60,000

60,000

8 3/7 W.I.P. (expenses)

Cash(C.A.)

70,000

70,000

9 16/8 W.I.P. (expenses)

A/P(S.T.L.)

45,000

45,000

10 16/9 A/P(S.T.L.)

Cash(C.A.)

45,000

45,000

Example 2: Solution

1. Journalizing:No. Date Description Dr Cr

11 1/10 A/R(C.A.)

Revenue

280,000

280,000

12 20/10 Cash(C.A.)

A/R(C.A.)

20,000

20,000

13 15/11 Cash(C.A)

A/R(C.A.)

265,000

265,000

14 15/12 A/P(S.T.L.)

Cash(C.A.)

40,000

40,000

15 25/12 W.I.P. (expenses)

Cash(C.A.)

145,000

145,000

16 30/12 Dep.(expenses)

Dep. (Contra Assets Building)

30,000

30,000

17 30/12 Dep.(expenses)

Dep. (Contra Assets Equipment)

65,000

65,000

18 30/12 Tax (expenses)

Cash (C.A.)

33,000

33,000

19 30/12 Dividends (expenses)

Cash (C.A.)

20,000

20,000

Example 2: Solution

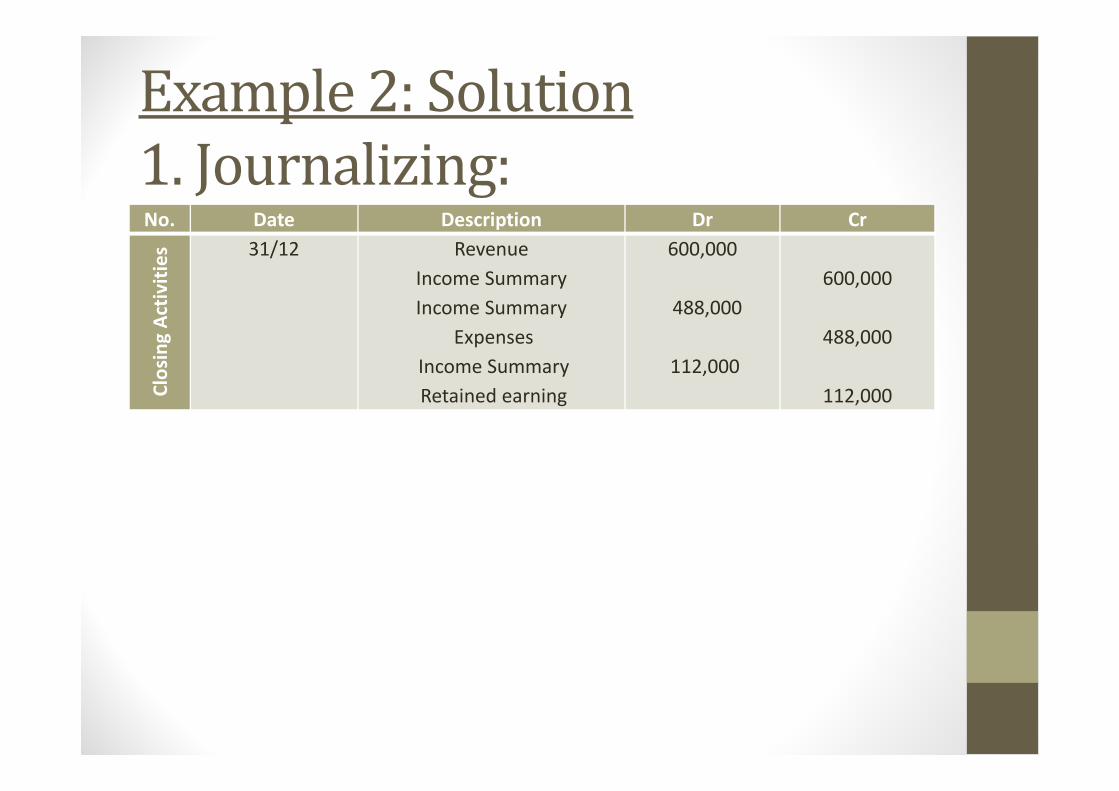

1. Journalizing:No. Date Description Dr Cr

Clo

sin

g A

ctiv

itie

s 31/12 Revenue

Income Summary

Income Summary

Expenses

Income Summary

Retained earning

600,000

488,000

112,000

600,000

488,000

112,000

Example 2: Solution

2. Income Statement:• To journalize transaction # 18 we have to develop the Income Statement:

Total Revenue(1)

(blue Shaded cells at the journal)

320,000 + 280,000 =600,000

WIP(expenses)(2)

(green Shaded cells at the journal)

20,000+60,000+70,000+45,000+145,000 =340,000

Depreciation(3)

(grey Shaded cells at the journal)

30,000+65,000 =95,000

Operating Profit(4)

=1-(2+3)

600,000-(340,000+95,000) =165,000

Tax 20% (5)

=4 x 0.2

165,000 x 0.2 =33,000

Net Profit (6)

=4-5

165,000-33,000 =132,000

Dividends Payment(7) 20,000 =20,000

Retained Earning

=6-7

132,000-20,000 =112,000

Example 2: Solution

3.1 Establishing Relevant Post Accounts:Expenses Revenue

Dr Cr Dr Cr

20,000

60,000

70,000

45,000

145,000

30,000

65,000

33,000

20,000

320,000

280,000

488,000 488,000 600,000 600,000

Closing

Income Summary Retained Earning

Dr

(from exp. ledger)

Cr

(from Rev. ledger)Dr Cr

488,000 600,000 112,000

112,000 112,000

Example 2: Solution

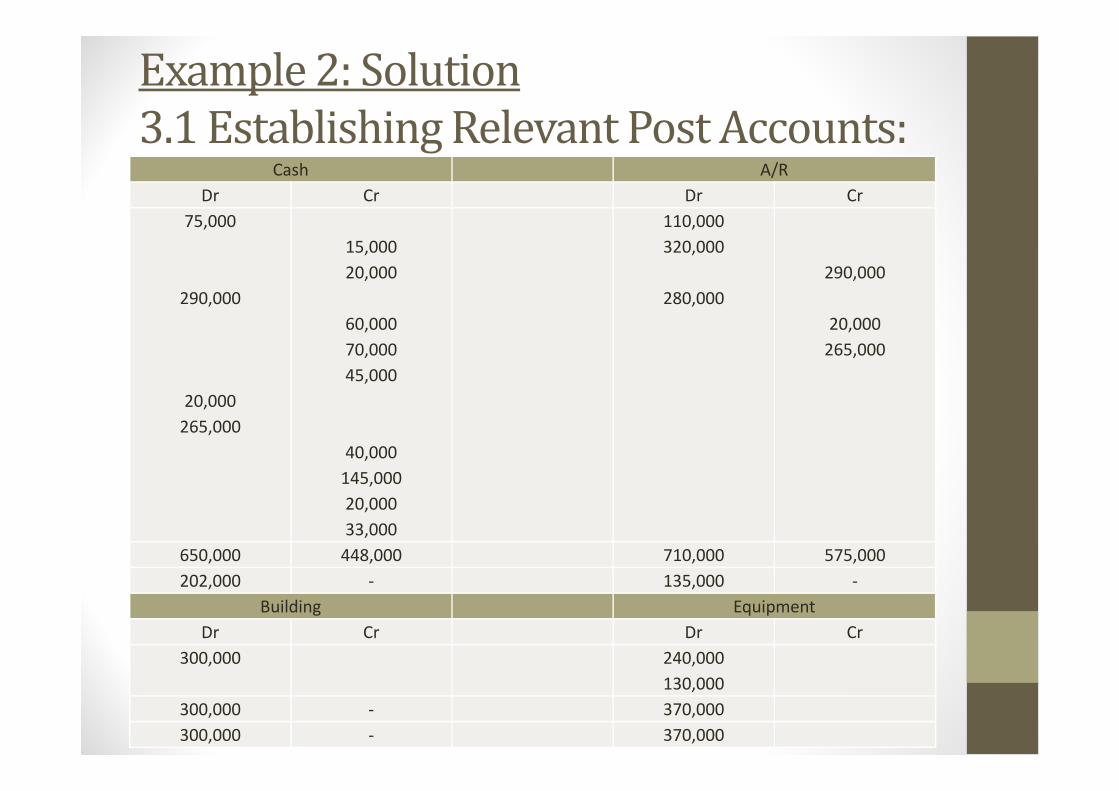

3.1 Establishing Relevant Post Accounts:Cash A/R

Dr Cr Dr Cr

75,000

290,000

20,000

265,000

15,000

20,000

60,000

70,000

45,000

40,000

145,000

20,000

33,000

110,000

320,000

280,000

290,000

20,000

265,000

650,000 448,000 710,000 575,000

202,000 - 135,000 -

Building Equipment

Dr Cr Dr Cr

300,000 240,000

130,000

300,000 - 370,000

300,000 - 370,000

Example 2: Solution

3.1 Establishing Relevant Post Accounts:Other assets Contra assets(Building Dep.)

Dr Cr Dr Cr

20,000 150,000

30,000

20,000 - 180,000

20,000 - 180,000

Contra assets(Equipment Dep.)

Dr Cr

80,000

65,000

145,000

145,000

A/P

Dr Cr

20,000

60,000

45,000

40,000

85,000

115,000

20,000

60,000

45,000

165,000 325,000

160,000

Example 2: Solution

3.1 Establishing Relevant Post Accounts:

N/P Long Term Liab

Dr Cr Dr Cr

50,000 60,000

50,000 60,000

50,000 60,000

Capital Stock R.E.

Dr Cr Dr Cr

250,000 70,000

112,000

250,000 182,000

250,000 182,000

Example 2: Solution

4. Closing account at Dec.31 2008 :

• (as shown in red shaded Row at the journal and Relevant

ledger account)

• To journalize the closing activities we have to develop the

related posting accounts Expenses, Revenue, Income

Summary, Retained Earning (as shown from step 3.1) then

record the closing activities as following:

• A. From Revenue (Dr) to Income Summary (Cr)

• B. From Income Summary (Dr) to Expenses (Cr)

• C. From Income Summary (Dr) to Retained Earnings (Cr)

Example 2: Solution

5. Trial Balance:No. Account Dr Cr

1 Cash 202,000

2 A/R 135,000

3 Building 300,000

4 Equipment 370,000

5 Other Assets 20,000

6 Building Dep. 180,000

7 Equipment Dep. 145,000

8 A/P 160,000

9 N/P 50,000

10 Long term Liab. 60,000

11 Capital Stock 250,000

12 Retained Earning 182,000

Total 1,027,000 1,027,000

Example 2: Solution

6. Balance Sheet:

Assets Liabilities

C.A.:

Cash 202,000

A/R 135,000

S.T.L.:

A/P 160,000

N/P 50,000

Long.T.L.: 60,000Total C.A. 337,000

F.A.:

Building 300,000

Less accumulated dep. 180,000

Equipment 370,000

Less accumulated dep. 145,000

Total Liab. 270,000

Owner Equity.

Capital Stock 250,000

Retained Earnings 182,000

Total O.E. 432,000

Total F.A. 345,000

Other assets 20,000

Total: 702,000 Total: 702,000

QUESTIONS??

Related Documents

![Financial Performance [Company Update]](https://static.cupdf.com/doc/110x72/577ca7bd1a28abea748c88ca/financial-performance-company-update.jpg)