Presentation Theme Innovative models for community healthcare financing Topic Community Health Insurance in Uganda – successes and challenges Dr. Sam O. Orach Executive Secretary Uganda Catholic Medical Bureau Feb 24 th 2015 1 ACHAP BIENNIAL CONFERENCE - NAIROBI

Community health insurance in Uganda by Dr Sam Orach, UCMB

Jul 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Presentation Theme

Innovative models for community healthcare financing

Topic Community Health Insurance in

Uganda – successes and challenges Dr. Sam O. Orach

Executive Secretary Uganda Catholic Medical Bureau

Feb 24th 2015

1

ACHAP BIENNIAL CONFERENCE - NAIROBI

Innovation • Introduction of new ideas / techniques • The application of better solutions that meet new

requirements, unarticulated needs, or existing market needs

• More effective products, processes, services, technologies

• It should be something new and original coming to that market.

• The idea might not be new but being tried in a new context – Therefore the innovation is the new context. – Or the new context considers the idea / proposed

solution an innovation

2

Community Health Financing

• Known by different names:

– Community Health Insurance

– Rural Health Insurance

– Revolving drug funds

– Micro-insurance

– Etc

• Will focus on Community Health Insurance in Uganda

3

Innovation in Community Health Financing should aim at:

• Increasing funding for health care while reducing the burden on the individual or family (Financial protection) – Keeping cost-sharing / user fees low

• Increasing population coverage and reduce social exclusion

• Increasing the service package covered • Enable health providers break even or

have surplus • Increase the population’s voice / control

over health care • Enable sustainability of the financing

scheme

4

Community Health Insurance in Uganda

• Origin:

– Mainly in western and south-western Uganda

– Now a few cases central region and part of eastern region

– Originated among “Burial groups”

• Instead of collecting for burial to collecting to prevent burial (death)

– Among rural poor

– Also joined by some working class in the rural areas.

– Membership is voluntary

5

6

Four main economic zones

Source: GoU; National Development Plan 2010/11 – 2014/2015

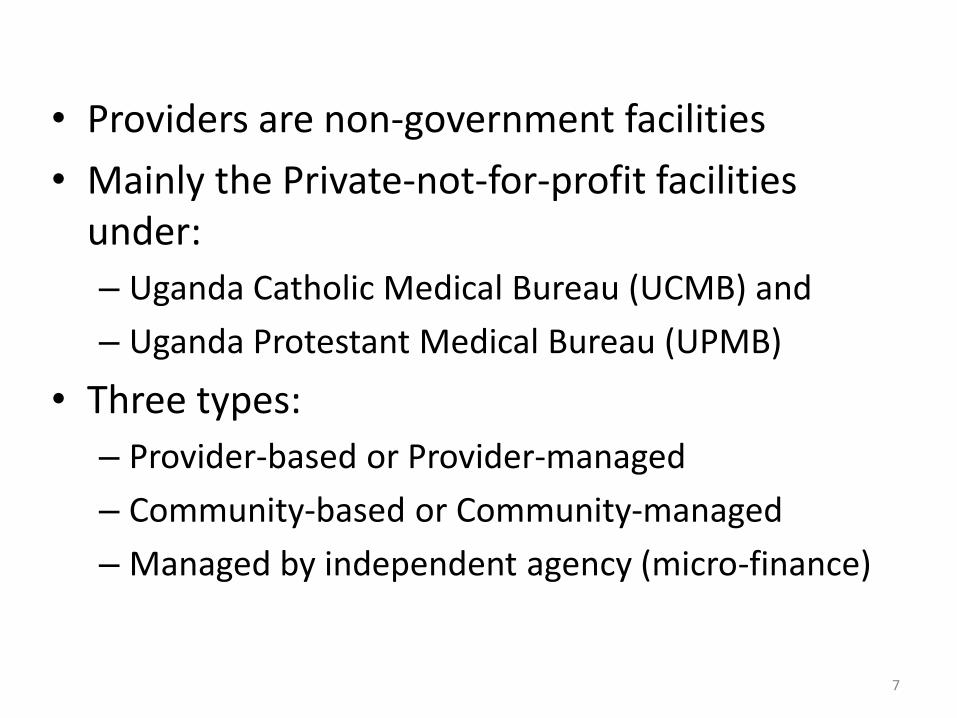

• Providers are non-government facilities

• Mainly the Private-not-for-profit facilities under:

– Uganda Catholic Medical Bureau (UCMB) and

– Uganda Protestant Medical Bureau (UPMB)

• Three types:

– Provider-based or Provider-managed

– Community-based or Community-managed

– Managed by independent agency (micro-finance)

7

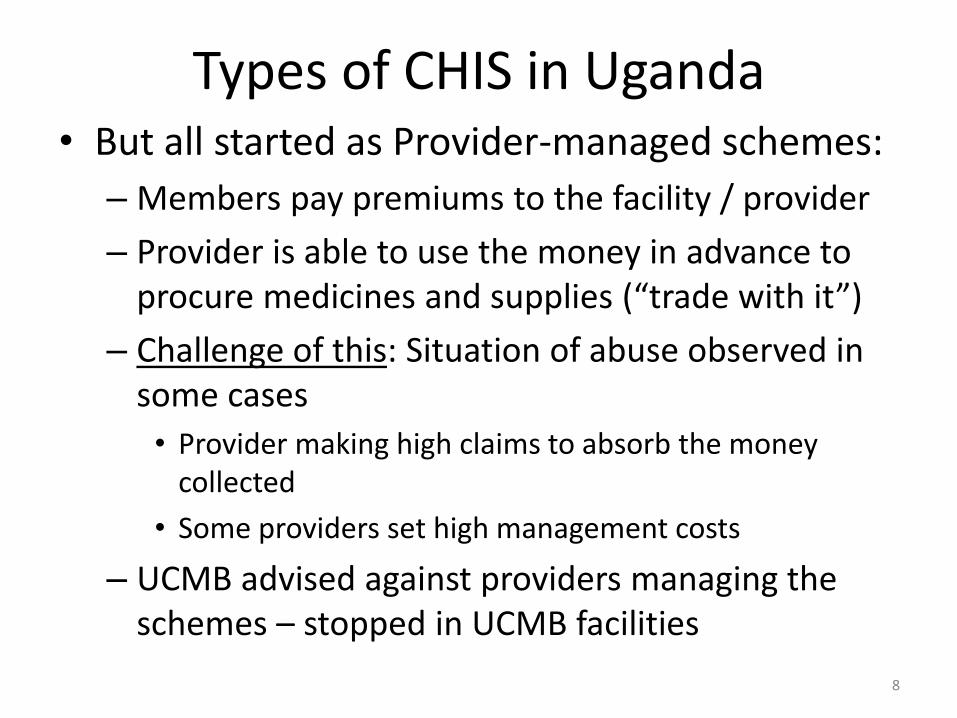

Types of CHIS in Uganda • But all started as Provider-managed schemes:

– Members pay premiums to the facility / provider

– Provider is able to use the money in advance to procure medicines and supplies (“trade with it”)

– Challenge of this: Situation of abuse observed in some cases

• Provider making high claims to absorb the money collected

• Some providers set high management costs

– UCMB advised against providers managing the schemes – stopped in UCMB facilities

8

• Community-managed schemes

– All schemes linked to UCMB facilities

– Challenge of this: Risk of some schemes not paying in time for members treated.

– More cases of health facilities subsiding for scheme members

• Schemes paying less than the poor who could not subscribe to the scheme.

(Study done by Cordaid and UCMB in 2009)

9

Benefits experienced

• Communities report reduction in catastrophic health expenditures in households enrolled in CHIS

• Members do not delay in seeking medical care when sick – better health seeking behaviours among CHIS members

• The relationship between communities and health service providers reported to have significantly improved – more participation in health facility decision making

• Relatively reduced rate of patients escaping from hospitals – better completion of payment for treatment

10

Community Health Insurance • Challenges

– Poor political will leading to:

– Lack of local / in-country support to provide subsidy to the schemes • Donor dependence

– Inability of communities to match premium with increasing costs of services – resist any rise in premium level

• Premiums often do not cover operational and administrative costs e.g.: – Community mobilisation

– Staff salaries

– Office costs • The financial coverage rate (incl. administration cost) is about 73%

• If administration costs were excluded it could reach 97% coverage

11

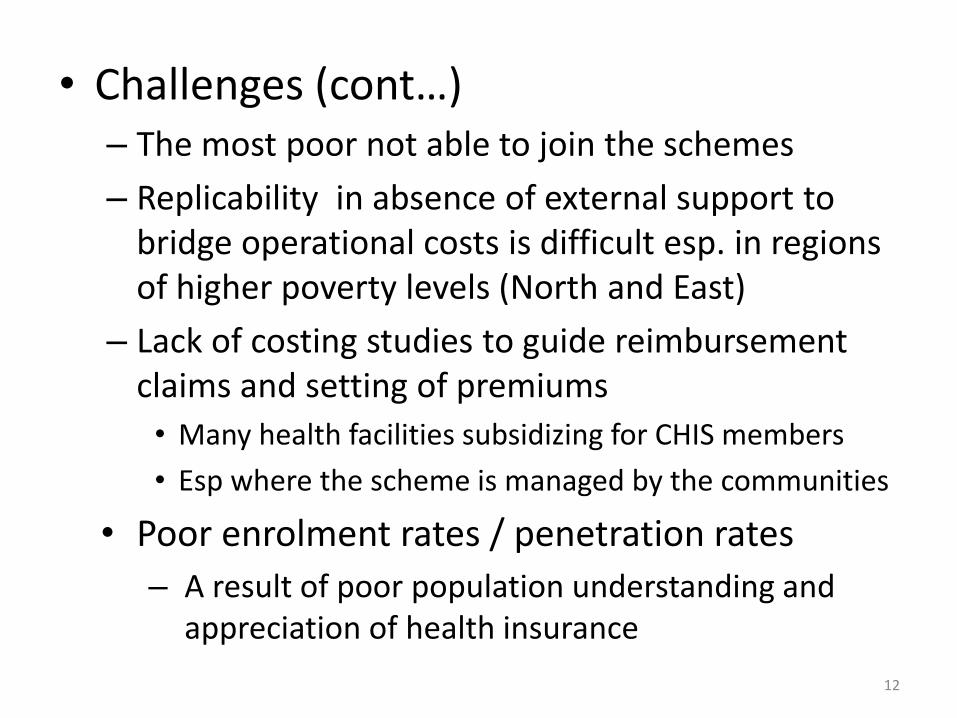

• Challenges (cont…) – The most poor not able to join the schemes

– Replicability in absence of external support to bridge operational costs is difficult esp. in regions of higher poverty levels (North and East)

– Lack of costing studies to guide reimbursement claims and setting of premiums

• Many health facilities subsidizing for CHIS members

• Esp where the scheme is managed by the communities

• Poor enrolment rates / penetration rates

– A result of poor population understanding and appreciation of health insurance

12

• Operating in a “free health care” policy environment – “Free” health services in government facilities

• Leading to Reduced willingness, especially among the rural community to join insurance schemes

• Potential threat from the upcoming National

Health Insurance Scheme (Even though CHIS is part of it) – The formal employed sector will mandatorily

contribute to the Social Health Insurance Scheme – Rural contributors (teachers, nurses etc) may find it

difficult to continue with CHIS (dual subscription) – Leading to lowering of subscriber numbers

13

What innovations? • Community Health Financing is itself an

innovation – Amidst inadequate government funding of health

care

• Possible innovations to improve on it: – Introduce performance-based-financing (PBF) in it

• PBF already successfully tried in Uganda

• Will make it more responsive to priorities agreed between providers and scheme members

– Encourage members to form / join community saving and lending schemes

14

Conclusion

• Community Health Insurance increases involvement in mobilising resources for their health care

• It is easier to scale up in communities with more expendable money

• Its success so far indicates that if supported by national governments it may be more replicable

15

God Bless

16

Related Documents