Ross Pfeffer, Director Sales and Marketing, Southern Cross CommsDay Summit, Sydney, April 2013

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Ross Pfeffer, Director Sales and Marketing, Southern Cross

CommsDay Summit, Sydney, April 2013

o Total Design Capacity of .050 Tbps

o Voice, Fax and TV

o Internet Growth from the early 90’s,

o Internet Content centred in the US

o By 1998-2000

o ANZ-US Bottleneck of 0.012 Tbps

o Second Generation of Fibre Cables

Tbps

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

TASMAN 2 0.001

PACRIM EAST 0.001

PACRIM WEST 0.001

JASURAUS 0.005

SE-ME-WE 3 0.040

Protected Ring of 30,500k

Engineered to 2025

> 99.999% availability

Build Cost: US$1.2B Total Design Capacity: 0.25 Tbps or 5

Times Bigger than Gen-1 Cables

Lit Capacity: 0.080Tbps

Bottleneck eradicated!!!!

Pre Sales: US$1.1B, (4 yrs of demand)

o Dot coms and cables crash

o 6 new Trans-Atlantic cables between 2000 and 2003

o Each cable bigger than all that preceded it

o Soon 1 Million kilometres of submarine cable

o Overestimated Demand Growth

o Virtuous Circle became Vicious

o Prices collapsed to less than Operational Cost

o Chapter 11 & Bankruptcies

o Financial Restructuring

o What has been the ANZ Experience?

New Cables Announcements Refinances / Failures

2000 SX1 to USA NAVA-1 to Singapore

SX2 to USA SX Banks Walked, Sponsor Guarantees

AJC to Guam

2002

2003 AJC Bank Rescue

2004 NAVA-1 Initiative Fails

2005

2006

2007

2008 Endeavour to Haw

PPC1 to Guam

AAG SEA-Guam-USA

2010 Pacific Fibre to USA Pipe Incl PPC-1 Sold

AXIN Trans Tasman

ASC to Singapore

ASSC-1 to Singapore

Hawaiiki to USA Pacific Fibre Inititative Fails

APX West to Singapore ASSC-1 and AXIN Gone Quiet

APX East to USA

Tasman Global Access

Freedom extension to Perth

2012

2011

2009

2001

o ANZ International Capacity CAGR

50% since 2002

o Now totals about 2.5 Tbps

o Traffic Capacity + Protection Capacity

o 80% Fully Protected

o 70–80% terminates in the US

o Actual Demand is now 10 times the

initial Design Capability of SX

o So how did the industry do it?

o SX upgraded 8 times

o SX capability increased by 35

o CAGR Price Decline > -23%

o Reflecting:

o Cable Competition

o Resale Competition

o Low MC of Capacity Upgrades

o Retail Broadband Competition

o Price is now < 5c per GB o SX Published 10G-2D/R

o 10 Year Repayment

o 45% Utilisation

o excluding volume discounts and O&M

o Demand Sources

o Applications Changes

o Technology Changes for Access and Transport

o The Dial and DSL waves

drove international capacity

demand

o Entitlement is greater than use

o Unlimited / TB Plans

o More can be consumed for no increase

in retail revenue

o The faster retail demand increases the

faster international capacity price must

fall

o Applications are the real key to future

growth.

o Market Capacity grown at 45% since 2008

o ABS Download Volumes grown at 65%

o Reflects growth of Cache

o Cache accounts for > 30% of D/L today

o Likely to exceed 50% by 2015

o Cache will increasingly subdue demand

o Mobile devices are adding to Fixed Volumes via Wi-Fi

o US evidence suggests the 4G Impact will be strong

o provided mobile quotas expand and mobile data prices fall

o Mobile Substitution of Fixed Line may become much more significant

o 4G Likely to Impact Fibre uptake depending on Pricing

o Will substitute ADSL fixed Line

o The FTTH Wave will take a DECADE

o NBN subs may currently consume twice the volume of ADSL2+

o But DSL Subs are oversubscribed to Data Entitlement

o FTTH has not enabled new applications in other markets

o Most Subscribers unlikely to pay more for more data?

o If FTTH lifts demand Cache will strengthen further

18

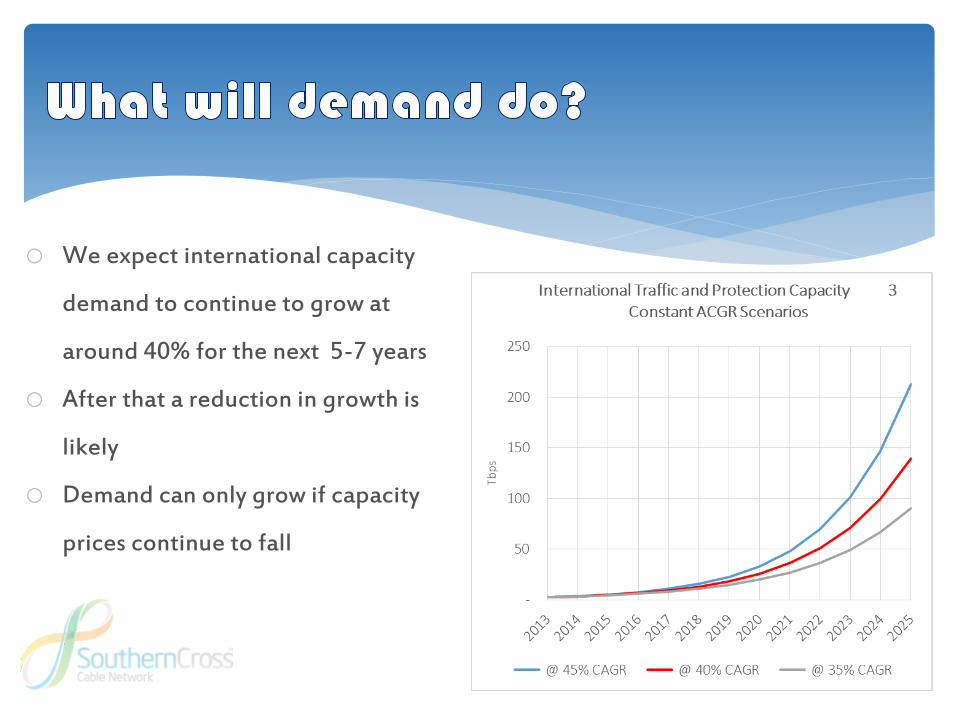

o We expect international capacity

demand to continue to grow at

around 40% for the next 5-7 years

o After that a reduction in growth is

likely

o Demand can only grow if capacity

prices continue to fall

o 5 existing cables from ANZ can all

expand supply at low cost

o Assumes SX1/2 cannot or does not

use 1 Tbps Channels from 2020

o Have not included the construction

of a new SX Cable

o Supply is assuredo International capacity demand likely to remain strong o The impact of Fibre and Mobile remains in doubto Cache Impact will strengthen

o Most Fixed Users have high data entitlements and unlikely to pay moreo so Retail Revenue generation opportunities from more Data have diminished greatly.

o But ISP’s will need to acquire a lot more capacity

o Existing Cables will continue to expand, at low MC and to aggressively compete to meet the evolving needs of ISPs.

o A plethora of new cable proposals will continue to add to price decline pressures

o No imminent need :

o Technical cable performance indicates reliability until at least 2030

o Likely upgrade efficiencies will allow us to easily meet the expected demand

o An early overbuild may have considerable merit i.e Build Cost/Benefit may be more

attractive than Upgrade Economics

o Large installed customer base increasingly looking at LT supply options

o Opportunity to expand route and mesh network options

o Our potential Capacity increases dramatically

o using current100Gbps channels the balanced cable limit of 7 Tbps increases to 24 Tbps!

o The case for an early SX overbuild is under review

o Capacity will continue to be expanded well ahead of demand

o The term of our IRU’s will be extended (again) to 2030

o Construction of more POPS (LA, Sydney No. 2, Auckland)

o Further Price reductions associated with capacity expansions

o Major innovations to de-risk and reward long term customer purchase commitments

Related Documents

![AN v ANZ Banking Group Limited - Home | …...AN v ANZ Banking Group Limited • [2015] AusHRC 93 • 1 Australian Human Rights Commission Level 3, 175 Pitt Street, Sydney NSW 2000](https://static.cupdf.com/doc/110x72/5f04d5317e708231d40feef9/an-v-anz-banking-group-limited-home-an-v-anz-banking-group-limited-a-2015.jpg)