Global Trade Review - Commodity Trade Finance Conference Case Study: Hong Kong Monetary Authority (HKMA) September, 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Global Trade Review - Commodity Trade Finance ConferenceCase Study: Hong Kong Monetary Authority (HKMA)September, 2017

Context

3

March

2017

Today

November

2017PoC

Solution visioning

Design and test parameters

Development sprints

DeloitteD Banks

HKMA

• Money laundering

• Limited oversight

• Industry in Hong Kong

Network establishment

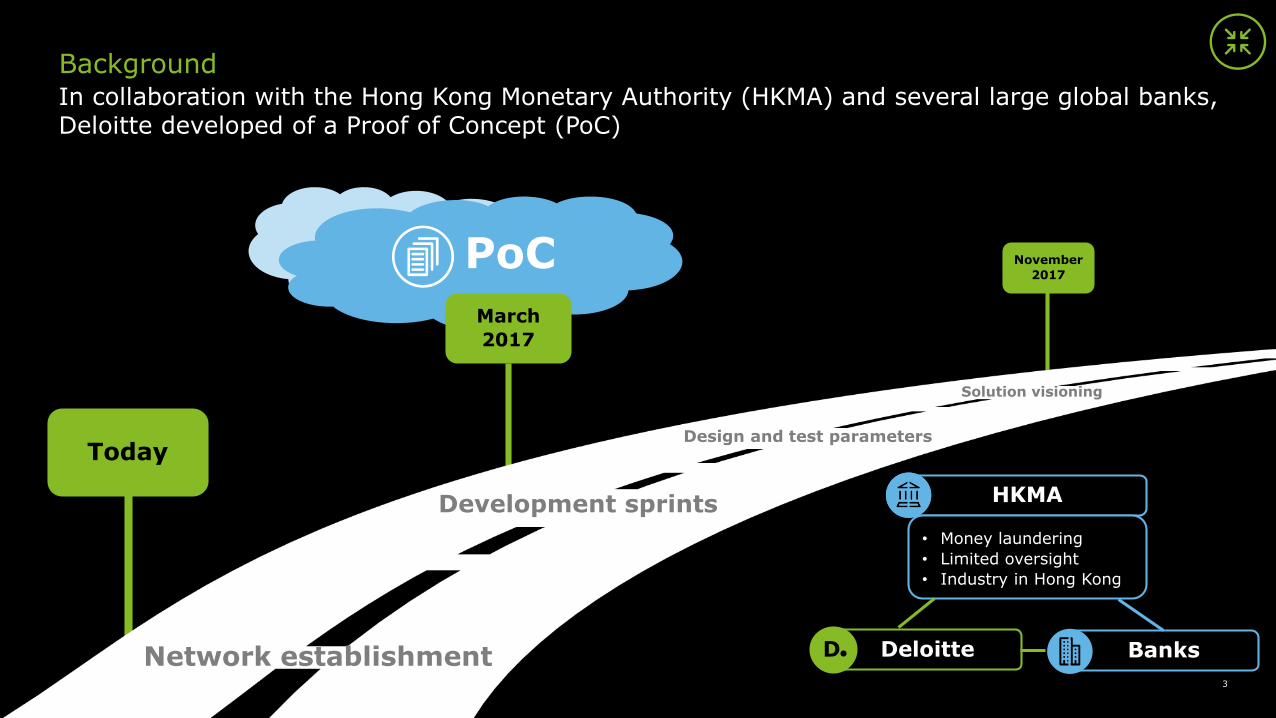

BackgroundIn collaboration with the Hong Kong Monetary Authority (HKMA) and several large global banks, Deloitte developed of a Proof of Concept (PoC)

© 2017 Deloitte 4

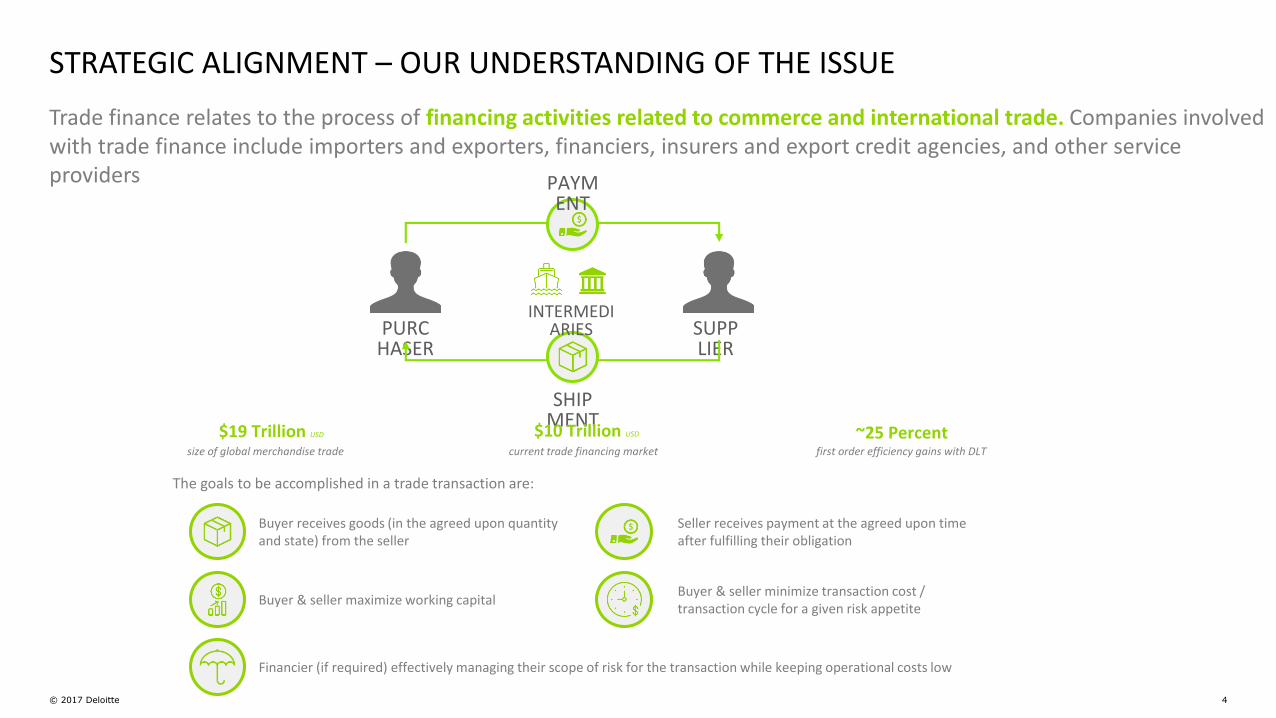

STRATEGIC ALIGNMENT – OUR UNDERSTANDING OF THE ISSUE

Trade finance relates to the process of financing activities related to commerce and international trade. Companies involved with trade finance include importers and exporters, financiers, insurers and export credit agencies, and other service providers

The goals to be accomplished in a trade transaction are:

Buyer receives goods (in the agreed upon quantity and state) from the seller

Buyer & seller maximize working capital

Seller receives payment at the agreed upon time after fulfilling their obligation

SHIPMENT

PURCHASER

SUPPLIER

INTERMEDIARIES

PAYMENT

Financier (if required) effectively managing their scope of risk for the transaction while keeping operational costs low

Buyer & seller minimize transaction cost / transaction cycle for a given risk appetite

$19 Trillion USD ~25 Percent$10 Trillion USD

size of global merchandise trade current trade financing market first order efficiency gains with DLT

© 2017 Deloitte 5

EXPORTERS• Slow, paper based process• Difficulty in asset tracking • Delays in payments• Small, medium exporters face competitive

market conditions and lack adequate access to trade finance credit

IMPORTERS• Slow, paper based process• Difficulty in asset tracking • Competitive market for accessing trade finance

credit due to lack of innovation• High insurance premiums due to difficulties with

asset tracking and fraud

BANKS• Difficulty in asset tracking • High probability of fraud from forged trade

documentation • High pressure from BASEL III regulation to shed

Trade Finance liabilities due to high cost of capital • Lack of innovative trade finance offerings in the

market due to difficulty in asset tracking

FREIGHT FORWARDERS• Paper based process• Manual interaction with all parties • Lack of transparency in the transfer of

assets resulting in low margins and high insurance premiums

REGULATOR AND GOVERNMENT AGENCIES• Oversight is challenging due to paper

based nature of transactions

Trade Based Money Laundering activity

between January 2004 and May 2009, in

aggregate totaled more than US$276

billion3

The WTO contends that access to trade

finance credit is more competitive than ever

due to low margins and an increase in

competition in the global trade market

Source:1. http://www.reuters.com/article/us-asia-trade-blockchain-idUSKCN10L17D2. http://www.europarl.europa.eu/RegData/etudes/note/join/2010/431578/IPOL-TRAN_NT(2010)431578_EN.pdf3. https://www.fincen.gov/resources/advisories/fincen-advisory-fin-2010-a001

The WTO contends that access to trade finance

credit is at its most competitive ever due to low

margins and an increase in competition in the

global trade market

In recent years a number of banks have suffered

great financial loss due to the manual nature of

trade finance leaving them open to forgery of

documents1

A comprehensive report by the European

Parliament into freight forwarding cited

lack of technology leading to incurring of

non essential costs (e.g. premium freight)2

BUSINESS VALUE FOR STAKEHOLDERS – PAIN POINTS IN TRADE FINANCE

Trade Finance

Pain Points and

Real Life Examples

2

3

4

5

1

© 2017 Deloitte 6

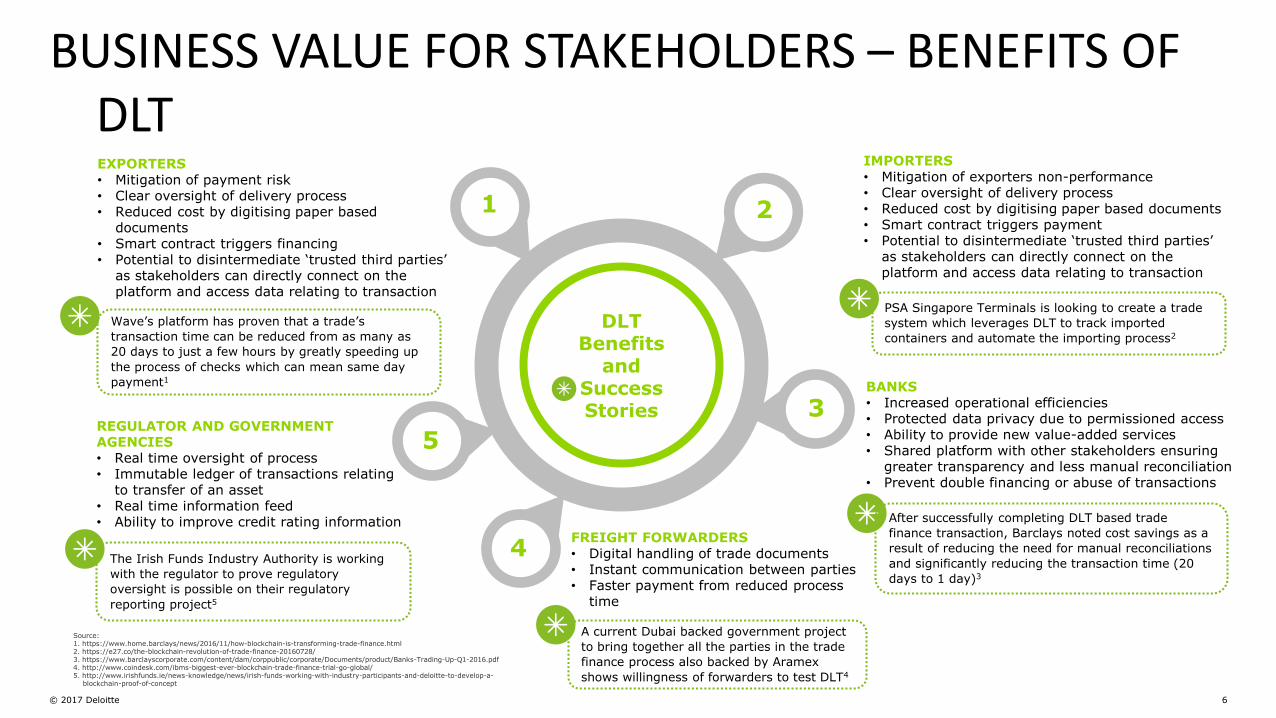

BUSINESS VALUE FOR STAKEHOLDERS – BENEFITS OF DLTEXPORTERS• Mitigation of payment risk• Clear oversight of delivery process• Reduced cost by digitising paper based

documents• Smart contract triggers financing• Potential to disintermediate ‘trusted third parties’

as stakeholders can directly connect on the platform and access data relating to transaction

IMPORTERS• Mitigation of exporters non-performance• Clear oversight of delivery process• Reduced cost by digitising paper based documents• Smart contract triggers payment• Potential to disintermediate ‘trusted third parties’

as stakeholders can directly connect on the platform and access data relating to transaction

BANKS• Increased operational efficiencies• Protected data privacy due to permissioned access• Ability to provide new value-added services• Shared platform with other stakeholders ensuring

greater transparency and less manual reconciliation• Prevent double financing or abuse of transactions

FREIGHT FORWARDERS• Digital handling of trade documents• Instant communication between parties• Faster payment from reduced process

time

REGULATOR AND GOVERNMENT AGENCIES• Real time oversight of process• Immutable ledger of transactions relating

to transfer of an asset• Real time information feed • Ability to improve credit rating information

DLTBenefits

andSuccess Stories

2

3

4

5

The Irish Funds Industry Authority is working

with the regulator to prove regulatory

oversight is possible on their regulatory

reporting project5

1

Wave’s platform has proven that a trade’s

transaction time can be reduced from as many as

20 days to just a few hours by greatly speeding up

the process of checks which can mean same day

payment1

PSA Singapore Terminals is looking to create a trade

system which leverages DLT to track imported

containers and automate the importing process2

After successfully completing DLT based trade

finance transaction, Barclays noted cost savings as a

result of reducing the need for manual reconciliations

and significantly reducing the transaction time (20

days to 1 day)3

A current Dubai backed government project

to bring together all the parties in the trade

finance process also backed by Aramex

shows willingness of forwarders to test DLT4

Source:1. https://www.home.barclays/news/2016/11/how-blockchain-is-transforming-trade-finance.html 2. https://e27.co/the-blockchain-revolution-of-trade-finance-20160728/ 3. https://www.barclayscorporate.com/content/dam/corppublic/corporate/Documents/product/Banks-Trading-Up-Q1-2016.pdf 4. http://www.coindesk.com/ibms-biggest-ever-blockchain-trade-finance-trial-go-global/ 5. http://www.irishfunds.ie/news-knowledge/news/irish-funds-working-with-industry-participants-and-deloitte-to-develop-a-

blockchain-proof-of-concept

© 2017 Deloitte 7

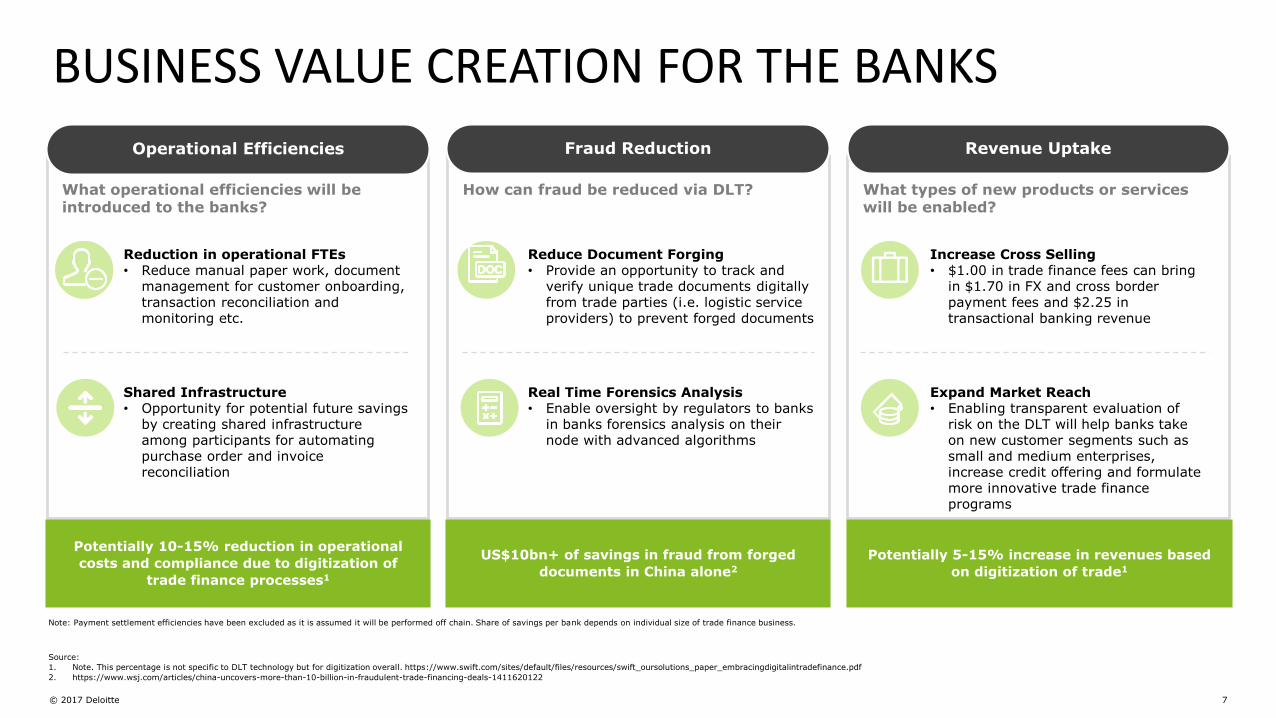

BUSINESS VALUE CREATION FOR THE BANKS

Note: Payment settlement efficiencies have been excluded as it is assumed it will be performed off chain. Share of savings per bank depends on individual size of trade finance business.

Real Time Forensics Analysis• Enable oversight by regulators to banks

in banks forensics analysis on their node with advanced algorithms

What operational efficiencies will be introduced to the banks?

Operational Efficiencies

How can fraud be reduced via DLT?

Fraud Reduction

What types of new products or services will be enabled?

Revenue Uptake

Increase Cross Selling• $1.00 in trade finance fees can bring

in $1.70 in FX and cross border payment fees and $2.25 in transactional banking revenue

Shared Infrastructure • Opportunity for potential future savings

by creating shared infrastructure among participants for automating purchase order and invoice reconciliation

Reduce Document Forging• Provide an opportunity to track and

verify unique trade documents digitally from trade parties (i.e. logistic service providers) to prevent forged documents

Reduction in operational FTEs• Reduce manual paper work, document

management for customer onboarding, transaction reconciliation and monitoring etc.

Expand Market Reach• Enabling transparent evaluation of

risk on the DLT will help banks take on new customer segments such as small and medium enterprises, increase credit offering and formulate more innovative trade finance programs

Potentially 10-15% reduction in operational

costs and compliance due to digitization of

trade finance processes1

Potentially 5-15% increase in revenues based

on digitization of trade1

US$10bn+ of savings in fraud from forged

documents in China alone2

Source:

1. Note. This percentage is not specific to DLT technology but for digitization overall. https://www.swift.com/sites/default/files/resources/swift_oursolutions_paper_embracingdigitalintradefinance.pdf

2. https://www.wsj.com/articles/china-uncovers-more-than-10-billion-in-fraudulent-trade-financing-deals-1411620122

© 2017 Deloitte 8

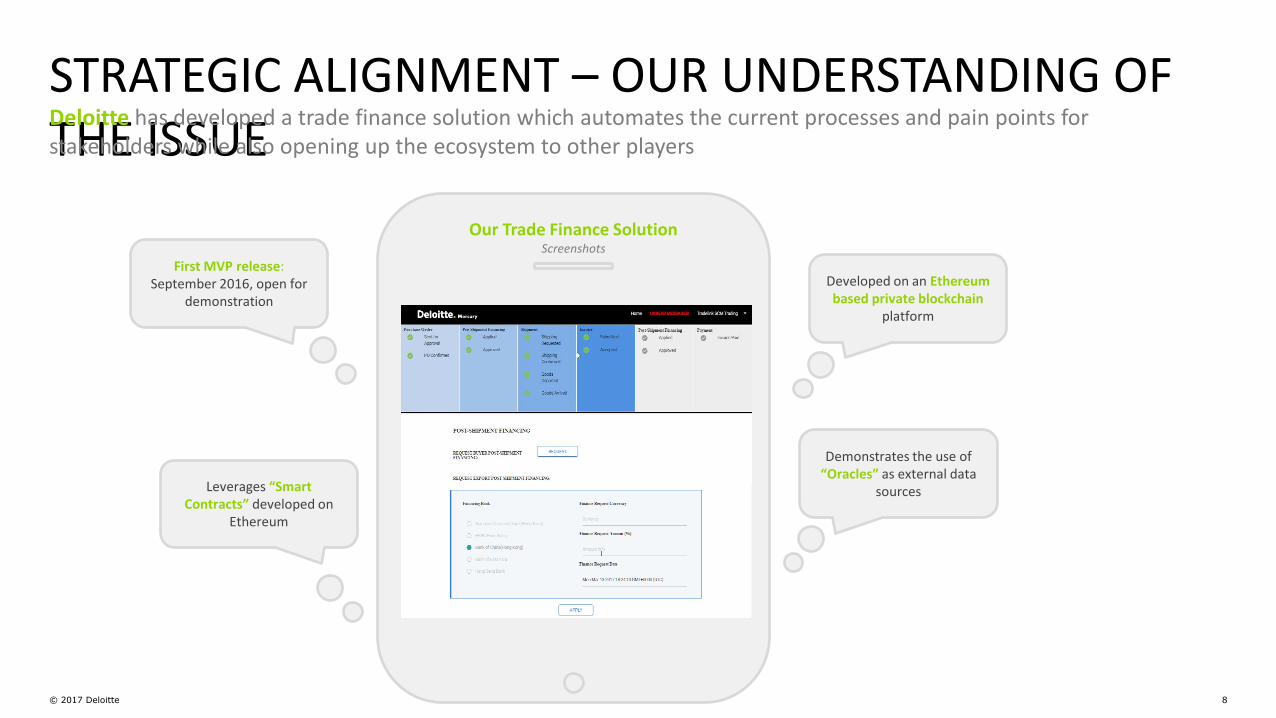

STRATEGIC ALIGNMENT – OUR UNDERSTANDING OF THE ISSUEDeloitte has developed a trade finance solution which automates the current processes and pain points for stakeholders while also opening up the ecosystem to other players

Our Trade Finance SolutionScreenshots

First MVP release: September 2016, open for

demonstration

Developed on an Ethereum based private blockchain

platform

Leverages “Smart Contracts” developed on

Ethereum

Demonstrates the use of“Oracles” as external data

sources

© 2017 Deloitte 9

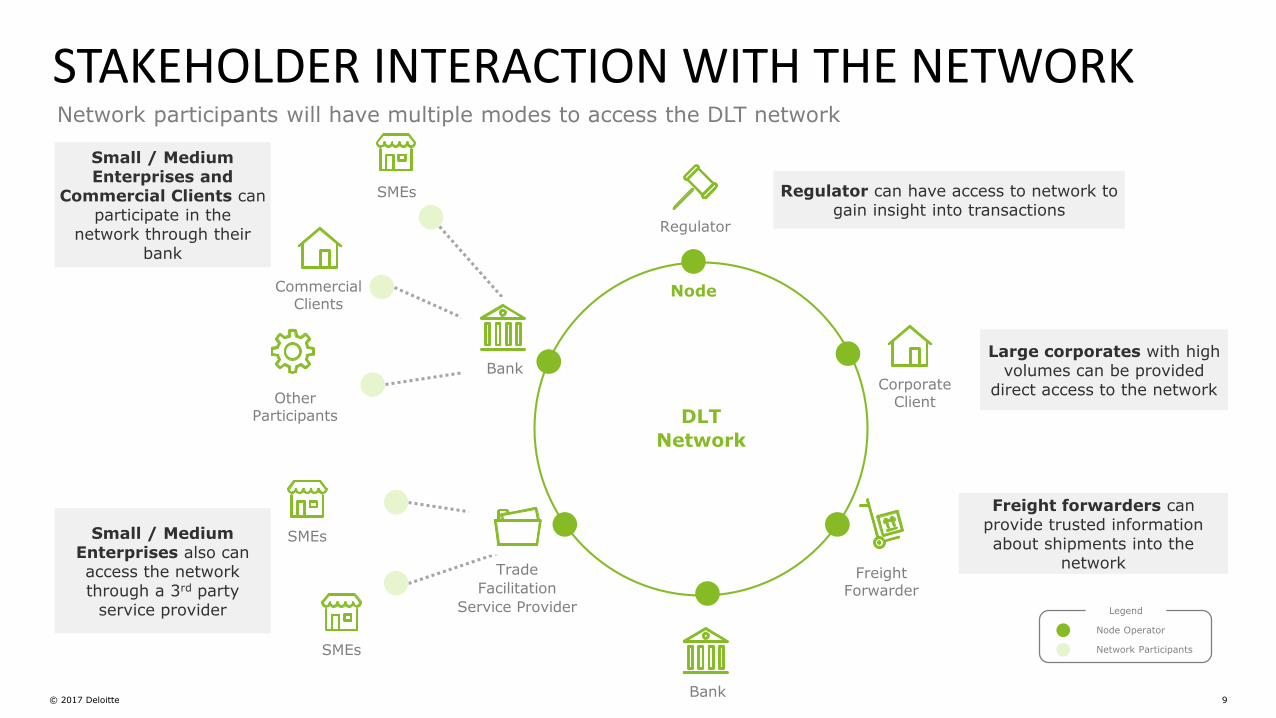

STAKEHOLDER INTERACTION WITH THE NETWORKNetwork participants will have multiple modes to access the DLT network

Node Operator

Network Participants

Legend

Regulator

Other Participants DLT

Network

Node

Freight Forwarder

Commercial Clients

SMEs

SMEs

SMEs

Bank

Trade

Facilitation

Service Provider

Corporate Client

Bank

Regulator can have access to network to gain insight into transactions

Large corporates with high volumes can be provided

direct access to the network

Freight forwarders can provide trusted information about shipments into the

network

Small / Medium Enterprises and

Commercial Clients can participate in the

network through their bank

Small / Medium Enterprises also can access the network through a 3rd party

service provider

10

BLOCKCHAIN BENEFITSBlockchain eases the existing pain points of buyers, sellers and financial institutions while opening the trade finance ecosystem to new non-traditional players

Speed / Real Time Updates

DisintermediationPrivacy &

TransparencyIrreversibility

Capital AccessAccurate / Traceable

InformationFraud Reduction

Eliminate manual processing of paper documents & signatures via uploads to a single interface

and real-time updates

Remove the need for trusted intermediaries to verify

transactions, and allow two parties to transact directly with

each other

Increase security of access, amendments, and exposure,

through the use of key-permissioned access

All transactions are tracked and irreversible, reducing risk of double spending, abuse, and manipulation of transactions

Increase access to third party financiers for improved lending

rates

Improve access to latest sales contracts, single sourced

amendments, and pre-verified documents that are signed by

all parties

Unique tracking and authentic verification of each transaction

and asset will mitigate fraud and associated behaviour

Key Considerations

12© 2016 Deloitte. All rights reserved DLT Trade Finance Business Analysis Report© 2017. For information, contact Deloitte China. 12

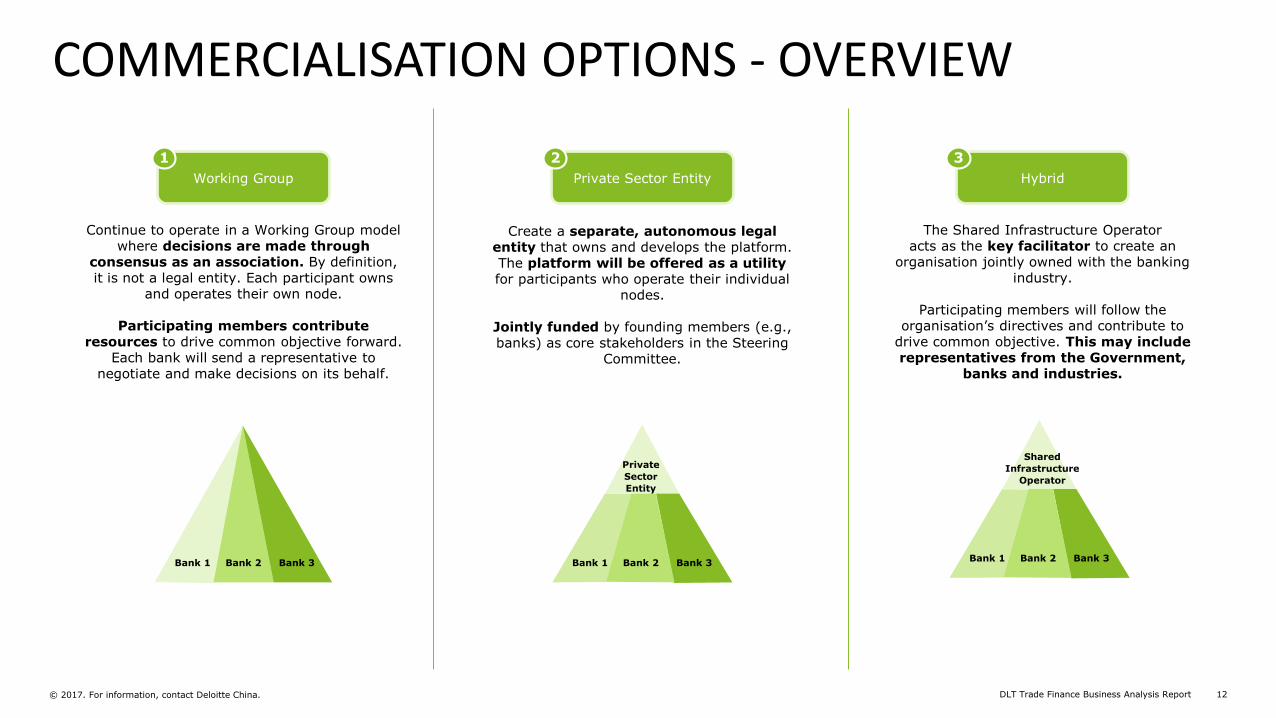

COMMERCIALISATION OPTIONS - OVERVIEW

Create a separate, autonomous legal entity that owns and develops the platform. The platform will be offered as a utility for participants who operate their individual

nodes.

Jointly funded by founding members (e.g., banks) as core stakeholders in the Steering

Committee.

Private Sector Entity

2

Working Group

Continue to operate in a Working Group model where decisions are made through

consensus as an association. By definition, it is not a legal entity. Each participant owns

and operates their own node.

Participating members contribute resources to drive common objective forward.

Each bank will send a representative to negotiate and make decisions on its behalf.

1

Bank 1 Bank 2 Bank 3 Bank 1 Bank 2 Bank 3

Private

Sector

Entity

Hybrid

The Shared Infrastructure Operatoracts as the key facilitator to create an

organisation jointly owned with the banking industry.

Participating members will follow the organisation’s directives and contribute to

drive common objective. This may include representatives from the Government,

banks and industries.

3

Bank 1 Bank 2 Bank 3

Shared

Infrastructure

Operator

13© 2016 Deloitte. All rights reserved DLT Trade Finance Business Analysis Report© 2017. For information, contact Deloitte China. 13

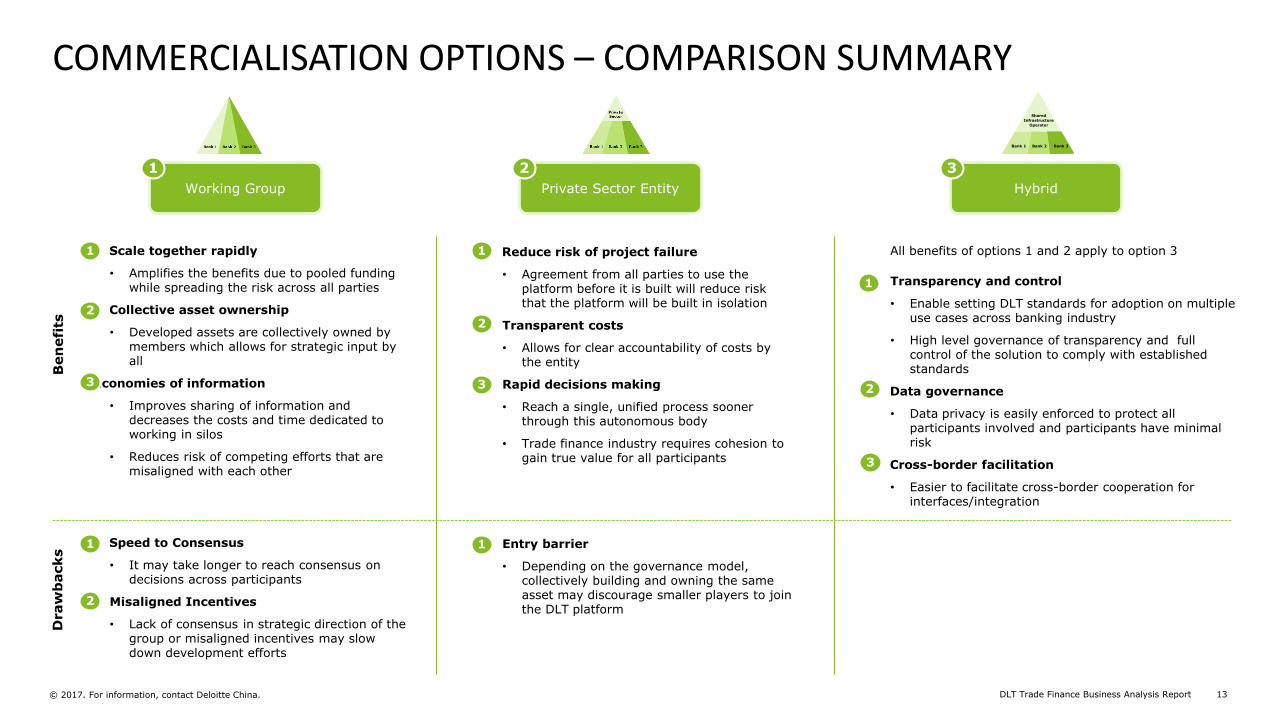

COMMERCIALISATION OPTIONS – COMPARISON SUMMARYB

en

efi

tsD

raw

backs

Working Group

• Scale together rapidly

• Amplifies the benefits due to pooled funding while spreading the risk across all parties

• Collective asset ownership

• Developed assets are collectively owned by members which allows for strategic input by all

Economies of information

• Improves sharing of information and decreases the costs and time dedicated to working in silos

• Reduces risk of competing efforts that are misaligned with each other

• Speed to Consensus

• It may take longer to reach consensus on decisions across participants

• Misaligned Incentives

• Lack of consensus in strategic direction of the group or misaligned incentives may slow down development efforts

1

1

2

3

1

2

• Reduce risk of project failure

• Agreement from all parties to use the platform before it is built will reduce risk that the platform will be built in isolation

• Transparent costs

• Allows for clear accountability of costs by the entity

• Rapid decisions making

• Reach a single, unified process sooner through this autonomous body

• Trade finance industry requires cohesion to gain true value for all participants

Private Sector Entity

Entry barrier

• Depending on the governance model, collectively building and owning the same asset may discourage smaller players to join the DLT platform

2

1

2

3

1

Hybrid

All benefits of options 1 and 2 apply to option 3

• Transparency and control

• Enable setting DLT standards for adoption on multiple use cases across banking industry

• High level governance of transparency and full control of the solution to comply with established standards

• Data governance

• Data privacy is easily enforced to protect all participants involved and participants have minimal risk

• Cross-border facilitation

• Easier to facilitate cross-border cooperation for interfaces/integration

3

1

2

3

Bank 1 Bank 2 Bank 3

Shared

Infrastructure

Operator

14© 2016 Deloitte. All rights reserved© 2017. 14

COMMERCIALISATION AND CRITICAL SUCCESS FACTORS IN DELIVERYGovernance model

Technical• Develop PoC in isolated test environment, pilot would be deployed in ‘test bank’ environments with small client subset• Organisation will be responsible for ensuring timely completion of upgrades by participants, and setting the schedule and guidelines of deployment• Technology solutions group responsible for software development (e.g., development of node software), maintaining node software, providing support for participant deployments• Until the technology further evolves and DLTs are fully interoperable, there should be one single DLT platform• Technology roadmap (including assessment of interoperability) will be created by a technology architecture group

Legal• Working Group - no resolution dispute committee; either need to appoint a party to mediate disputes or have joint responsibility to mediate disputes• Legal entity - form Legal and Regulatory committee (1 member from each bank, 1 from Regulator) to assess legal and regulatory implications)• Establish legal framework (including how liability will be handled)• Establish a clear definition of a smart contract and legal standing to be agreed by platform owner in current form• Engage legal counsel to advise the committee on the impact of potential decisions

Regulations• A digital ID to identify participants and node operators on the network will be critical to address AML/KYC concerns while maintaining data privacy of participants• Work with regulator to shape regulations within the region and how to interoperate with other regions• Re-think how participants will be regulated given regulator has near real-time insight into the ledger• If operating outside the region, define a clear target list of regulators and identify point of contacts in each one• Draft go-to-market plan to target foreign regulators (in conjunction with regulator and local SME resources)

15© 2016 Deloitte. All rights reserved© 2017. 15

Data Protection and IP • Data privacy – data should only be shared on a need to know basis (permissioned)• On chain data should be minimal number of fields – only fields that require data integrity to be preserved and shared with participants• Off chain data should be permissioned• Data resiliency will need to be balanced with data privacy laws (e.g. (Global Data Protection Regulations (GDPR)), particularly when discussing distributed file systems for documents• Personally identifiable information (PII) will require special consideration of all parties (e.g., not maintained on the ledger)• Clear definition of IP and who owns the solution is required (to be decided during negotiations)

Data Retention• Data retention considerations will be factored into the underlying design of the network for nodes to purge ledger information after defined time periods• Legal and Regulatory committee to engage SMEs to assess the potential impact of GDPR on data being stored on and off chain (2018 inception date)

Data Attributes• Work with international bodies to get clear agreement of data attributes relating to trade documents (for example, UCP600 for letter of credit is a common standard/code of

practice relating to letters of credit globally)• Develop common electronic data standards relating to transmittal of trade documents (e.g., purchase order, invoice, transport documents, etc.)

Standard Platforms and Procedures• Form partnerships with international standard bodies (e.g., International Chamber of Commerce) to keep the legal entity at the forefront of standards relating to trade finance and

be the industry leader• Create a standards Working Group from banks and regulator to engage with trade organisations in other identified jurisdictions to establish dialogue around standards• Track International Organisation for Standardisation (ISO) requests by Standards Australia to feed into long term technical roadmap (will help with interoperability)

COMMERCIALISATION AND CRITICAL SUCCESS FACTORS IN DELIVERY (CONT’D)Governance model

Note: Standards apply across all three options

Deloitte Blockchain Capabilities

© 2017 Deloitte 17

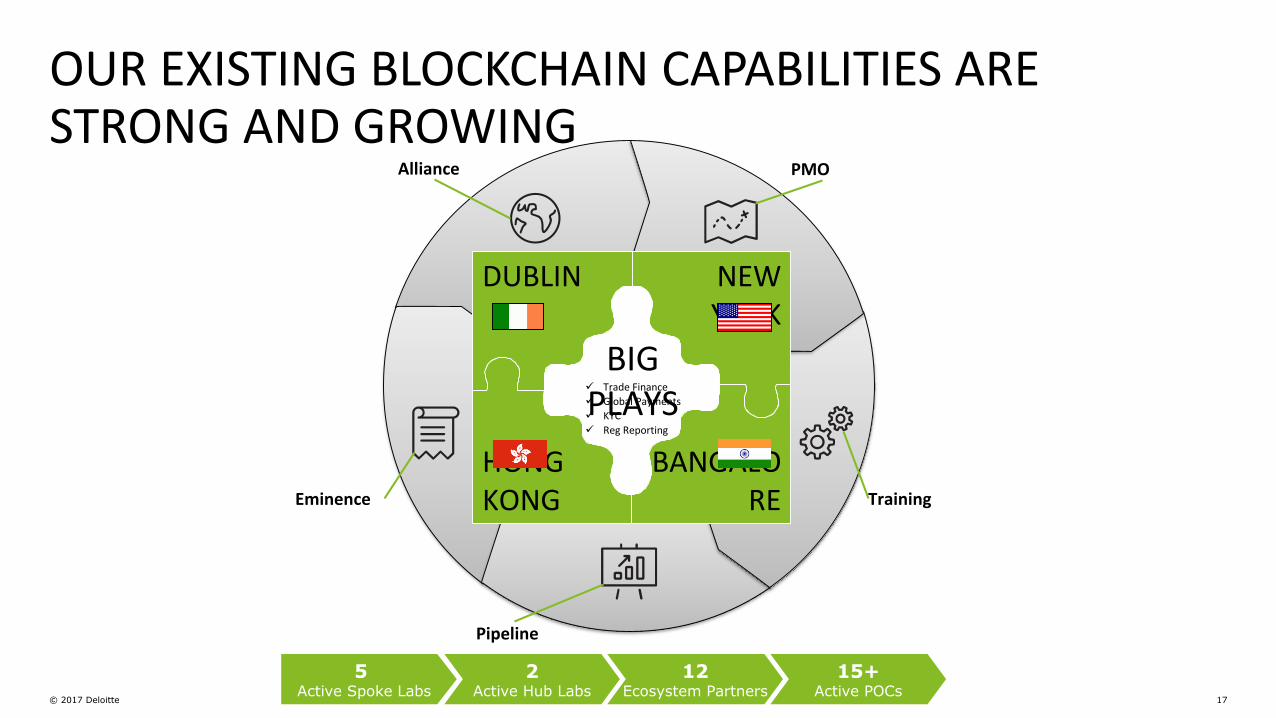

OUR EXISTING BLOCKCHAIN CAPABILITIES ARE STRONG AND GROWING

Eminence

12Ecosystem Partners

15+Active POCs

5 Active Spoke Labs

2Active Hub Labs

✓ Global Payments

✓ KYC

✓ Reg Reporting

✓ Trade Finance

Pipeline

Alliance

Training

PMO

BIG PLAYS✓ Trade Finance

✓ Global Payments

✓ KYC

✓ Reg Reporting

NEW YORK

BANGALORE

HONG KONG

DUBLIN

© 2017 Deloitte 18

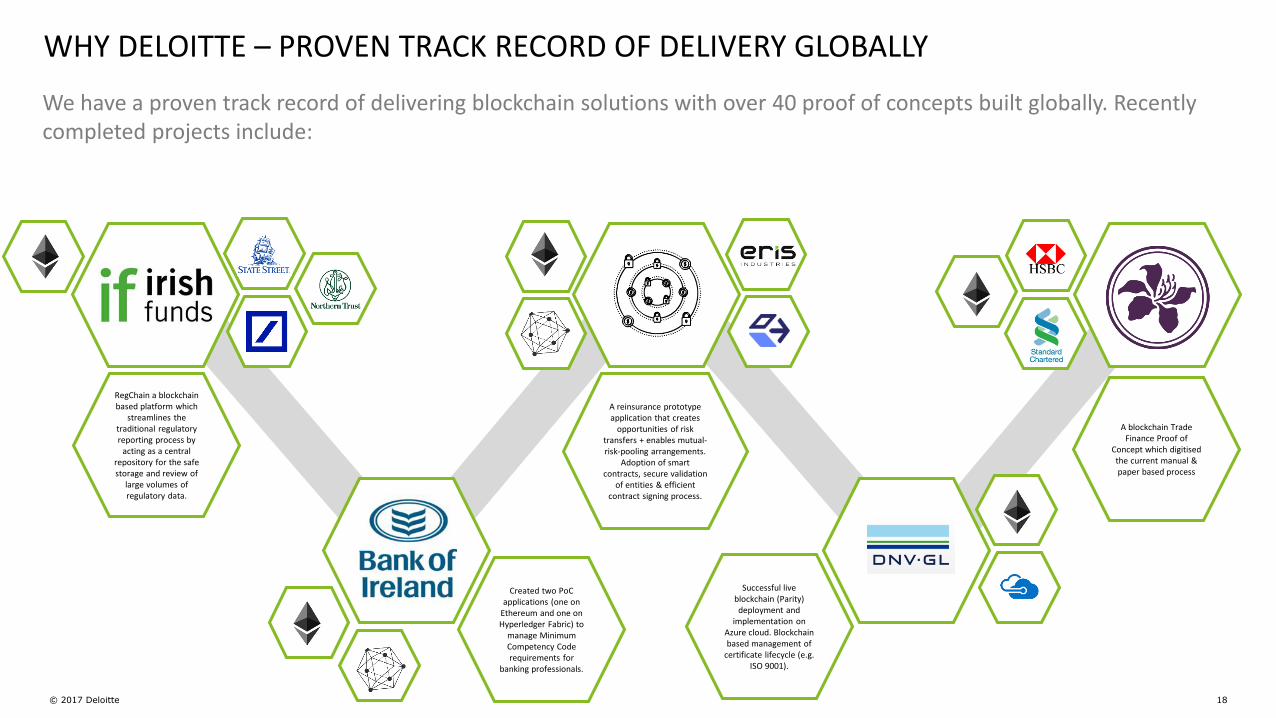

We have a proven track record of delivering blockchain solutions with over 40 proof of concepts built globally. Recently completed projects include:

WHY DELOITTE – PROVEN TRACK RECORD OF DELIVERY GLOBALLY

Created two PoC applications (one on

Ethereum and one on Hyperledger Fabric) to

manage Minimum Competency Code requirements for

banking professionals.

Successful live blockchain (Parity) deployment and

implementation on Azure cloud. Blockchain based management of

certificate lifecycle (e.g. ISO 9001).

RegChain a blockchain based platform which

streamlines the traditional regulatory reporting process by

acting as a central repository for the safe storage and review of

large volumes of regulatory data.

A blockchain Trade Finance Proof of

Concept which digitised the current manual & paper based process

A reinsurance prototype application that creates

opportunities of risk transfers + enables mutual-risk-pooling arrangements.

Adoption of smart contracts, secure validation

of entities & efficient contract signing process.

© 2017 Deloitte 19

DELOITTE SERVICE OFFERING

Code Review

Review code of live blockchain platforms to ensure there are no bugs or weaknesses which can result in manipulation of data

Testing and QA

User acceptance testing, integration testing and unit testing on code and solutions

Integration and Implementation

Implement a blockchain solution as part of an existing incumbent system (rather than replace)

Advise on Initial Coin Offering (ICO)

Disruptive funding model based on blockchain –akin to an IPO

Pilots

Live, secure and robust blockchain solution deployment on the cloud or on-premises

built over a 15 week period

Proof of Concepts

10 week Rapid prototyping phase where a blockchain-based solution is built for your

company

Enterprise and Technical Architecture Design and recommended enterprise solutions

which implement blockchain technologies while complementing business processes.

Big Data and Advance Analysis

Big data meets blockchain – harvesting the large amounts of data which are inherent to blockchain.

20

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legallyseparate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms.

At Deloitte, we make an impact that matters for our clients, our people, our profession, and in the wider society by delivering the solutions and insights they need to address their most complex business challenges. As one ofthe largest global professional services and consulting networks, with over 244,400 professionals in more than 150 countries, we bring world-class capabilities and high-quality services to our clients. In Ireland, Deloitte hasover 2,300 people providing audit, tax, consulting, and corporate finance services to public and private clients spanning multiple industries. Our people have the leadership capabilities, experience, and insight to collaborate withclients so they can move forward with confidence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication,rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Networkshall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2017 Deloitte. All rights reserved

Related Documents