Errors and Omissions policies often contain exclusions requiring certain conduct or conditions exist “in fact” before the exclusion is operative. For example, an exclu- sion may provide there is no coverage for claims arising out of a wrongful act committed by the insured with the knowledge “in fact” that the act was wrongful as defined in the policy. Thus, when the proscribed conduct is committed “in fact,” the insurer is relieved of its duty to defend, indemnify or provide other coverage contem- plated by the policy. Determining whether the “in fact” requirement is satisfied can be most vexing in at least two instances at either end of the coverage deter- mination spectrum. First, what should the policyholder expect from its insurer when a claim is tendered shortly after the underlying claim is asserted and only the underlying pleadings are available to inform the decision? Second, how should an insurer proceed when a coverage determination must be made after the policyholder settled the under- lying litigation, no factual findings were made on the “in fact” issues, and—because of the settlement—no such findings will ever be made in the underlying litigation to inform the decision? This latter situation may arise when, for example, the insurer issued an excess policy with attaching limits high enough that the insurer chose not to participate in the defense of the underlying litigation and had not gathered facts to satisfy an “in fact” determi- nation before the underlying litiga- tion settled. Under either scenario, however, how must an insurer determine if certain conditions or conduct exists with no factual record? How does an insurer deter- mine whether to exercise any defense right or obligation? This article explores the various ways that courts have interpreted exclusions with “in fact” require- ments when wrestling with the following issues: “IN FACT” EXCLUSIONS IN ERRORS AND OMISSIONS POLICIES Joel R. Mosher,Annie C. Warren, Shook Hardy & Bacon LLP, Kansas City, Missouri 1 Uniting Plaintiff, Defense, Insurance, and Corporate Counsel to Advance the Civil Justice System Insurance Coverage Litigation Committee Spring 2009 Committee News Committee News In This Issue: “In Fact” Exclusions In Errors And Ommissions Policies ...1 Message From The Chairs . . . 4 Note From The Editors ..... 5 Re-evaluating Trigger Of Coverage In Asbestos Bodily Injury Claims Involving Mesothelioma And Brochogenic Carcinoma: A Review Of Recent Case Law ................. 5 A Survey Of Recent Cases Addressing True Excess Carrier Issues: Trigger, Duty To Defend And Drop Down . . 6 2009-2010 TIPS Calendar . . 24 Continued on page 20 1 Mr. Mosher is Of Counsel and Ms. Warren is an Associate with Shook, Hardy & Bacon L.L.P. in Kansas City, Missouri.

CommitteeNews - TurnerPadget · This latter situation may arise when, for example, the insurer issued an excess policy with ... [email protected] Co-Chair JoelRMosher ShookHardy&BaconLLP

May 21, 2018

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Errors and Omissions policiesoften contain exclusions requiringcertain conduct or conditions exist“in fact” before the exclusion isoperative. For example, an exclu-sion may provide there is nocoverage for claims arising out of awrongful act committed by theinsured with the knowledge “infact” that the act was wrongful asdefined in the policy. Thus, whenthe proscribed conduct is committed“in fact,” the insurer is relieved of itsduty to defend, indemnify orprovide other coverage contem-plated by the policy.

Determining whether the “infact” requirement is satisfied can bemost vexing in at least two instancesat either end of the coverage deter-mination spectrum. First, whatshould the policyholder expect fromits insurer when a claim is tenderedshortly after the underlying claim isasserted and only the underlyingpleadings are available to inform the

decision? Second, how should aninsurer proceed when a coveragedetermination must be made afterthe policyholder settled the under-lying litigation, no factual findingswere made on the “in fact” issues,and—because of the settlement—nosuch findings will ever be made inthe underlying litigation to informthe decision?

This latter situation may arisewhen, for example, the insurerissued an excess policy withattaching limits high enough thatthe insurer chose not to participatein the defense of the underlyinglitigation and had not gatheredfacts to satisfy an “in fact” determi-nation before the underlying litiga-tion settled. Under either scenario,however, how must an insurerdetermine if certain conditions orconduct exists with no factualrecord? How does an insurer deter-mine whether to exercise anydefense right or obligation?

This article explores the variousways that courts have interpretedexclusions with “in fact” require-ments when wrestling with thefollowing issues:

“IN FACT” EXCLUSIONS IN ERRORS AND OMISSIONS POLICIESJoel R. Mosher, Annie C. Warren, Shook Hardy & Bacon LLP, Kansas City, Missouri1

Uniting Plaintiff, Defense, Insurance, and Corporate Counsel toAdvance the Civil Justice System

Insurance CoverageLitigation Committee

Spring 2009

CommitteeNewsCommitteeNews

In This Issue:“In Fact” Exclusions In ErrorsAnd Ommissions Policies . . . 1Message From The Chairs . . . 4Note From The Editors . . . . . 5Re-evaluating Trigger OfCoverage In Asbestos BodilyInjury Claims InvolvingMesothelioma AndBrochogenic Carcinoma:A Review Of RecentCase Law . . . . . . . . . . . . . . . . . 5A Survey Of Recent CasesAddressing True ExcessCarrier Issues: Trigger, DutyTo Defend And Drop Down . . 62009-2010 TIPS Calendar . . 24

Continued on page 20

1 Mr. Mosher is Of Counsel and Ms. Warren is an Associate with Shook, Hardy & Bacon L.L.P. in Kansas City,Missouri.

Insurance Coverage Litigation Committee Newsletter Spring 2009

2

ChairJoan M CotkinCotkin & Collins

Fl 24300 S Grand Ave

Los Angeles, CA 90071-3109(213) 688-9350

Fax: (213) [email protected]

Co-ChairJoel R Mosher

Shook Hardy & Bacon LLP2555 Grand Ave

Kansas City, MO 64108-2613(816) 559-2077

Fax: (816) [email protected]

Last Retiring ChairGeorge C RockasWilson Elser et al

Fl 14260 Franklin St

Boston, MA 02110-3112(617) 422-5300

Fax: (617) [email protected]

NewsletterCo-Vice-ChairsJames W Creenan

Creenan Law Offices, PC4154 Old William Penn Highway

Murraysville, PA 15668(724) 733-7832

Elizabeth C SackettResolute Management Inc. -

New England Division2 Central Square

Cambridge, MA 02139Phone: 617-234-3858

Fax: [email protected]

Vice-ChairsDavid H Anderson

Howrey LLPSte 3400

321 N Clark StChicago, IL 60654-4717

(312) 846-5676Fax: (312) 276-4209

Roberta Draper AndersonK&L Gates

Henry W Oliver Bldg535 Smithfield St

Pittsburgh, PA 15222-2393(412) 355-6222

Fax: (412) [email protected]

Richard Lee AngellZupkus & Angell PCMcCourt Mansion

555 E 8th AveDenver, CO 80203-3715

(303) 894-8948Fax: (303) [email protected]

Jill B Berkeley

Howrey LLPSte 3400

321 N Clark StChicago, IL 60654-4717

(312) 846-5675Fax: (312) 275-7780

John B BerringerAnderson Kill & Olick PC

Ste 15101 Gateway Ctr

Newark, NJ 07102-5310(973) 642-5133

Fax: (973) 621-6361

Lyndon F BittleCarrington Coleman

Ste 5500901 Main St

Dallas, TX 75202-3767(214) 855-3353

Fax: (214) [email protected]

John M BjorkmanLarson King LLP

Ste 280030 E 7th St

St Paul, MN 55101-4904(651) 312-6511

Fax: (651) [email protected]

William H Black JrPost & Schell PC

4 Penn Center Fl 131600 John F Kennedy Blvd

Philadelphia, PA 19103-2808(215) 587-1109

Fax: (215) [email protected]

James R BussianMaynard Cooper & Gale PC2400 Regions Harbert Plaza

1901 6th Ave NBirmingham, AL 35203-2618

(205) 254-1074Fax: (205) 254-1999

Tracy A CampbellSchiff Hardin LLP6600 Sears TowerChicago, IL 60606(312) 258-5602

Fax: (312) [email protected]

Greg S ComoLewis Brisbois et al

Ste. 17002929 N. Central Ave.

Phoenix, AZ 850122761(602) 792-1495

Raphael CotkinCotkin & Collins

Fl 24300 S Grand Ave

Los Angeles, CA 90071-3109(213) 688-9350

Fax: (213) [email protected]

E Lynette DentonDenton Law Group LLC

Ste 38247 W Division St

Chicago, IL 60610-2220(312) 794-7822

Fax: (312) [email protected]

Tracy A DuanyMullin Law Group PLLC

Ste 1000315 5th Ave S

Seattle, WA 98104-2682(206) 957-7007

Fax: (206) [email protected]

Madeleine FischerJones Walker et al

Fl 51201 Saint Charles Ave

New Orleans, LA 70170-1000(504) 582-8208

Fax: (504) [email protected]

Gary L GassmanMeckler Bulger & Tilson LLP

Ste 1800123 N Wacker Dr

Chicago, IL 60606-1743(312) 474-7994

Fax: (312) [email protected]

David A GauntlettGauntlett & Assoc

Ste 30018400 Von Karman AveIrvine, CA 92612-0505

(949) 553-1010Fax: (949) 553-2050

Gregory R GiomettiGregory Giometti & Assoc

Ste 50550 S Steele St

Denver, CO 80209-2810(303) 333-1957

Fax: (303) [email protected]

Dawn M GonzalezLitchfield Cavo LLP

Ste 300303 W Madison St

Chicago, IL 60606-3300(312) 781-6667

Fax: (312) [email protected]

Judith F GoodmanGoodman & Jacobs LLP

Fl 3075 Broad St

New York, NY 10004-2415(212) 385-1191

Fax: (212) [email protected]

Stephen P Groves SrNexsen Pruet LLC

Ste 400205 King St

Charleston, SC 29401-3159(843) 720-1725

Fax: [email protected]

Mark J HolzhauerAmerican Family Mutual Ins Co

4802 Mitchell AveSaint Joseph, MO 64507-2500

(816) 364-1541Fax: (866) 737-3459

Andrew T HoughtonSedgwick Detert Moran & Arnold

Fl 39125 Broad St

New York, NY 10004-3211(212) 898-4036

Fax: (212) [email protected]

Timothy W KennaGilbert Kelly Crowley & Jennett

Ste 20001055 W 7th St

Los Angeles, CA 90017-2546(213) 615-7000

Fax: (310) [email protected]

Jeff KichavenProfessional Mediation & Arbitration

Ste 4750707 Wilshire Blvd

Los Angeles, CA 90017-3720(310) 721-5785

Fax: (310) [email protected]

James P KoelzerRobins Kaplan Miller & Ciresi

Ste 34002049 Century Park E

Los Angeles, CA 90067-3208(310) 229-5443

Fax: (310) [email protected]

Seth LamdenHowrey LLP

Ste 3400321 N Clark St

Chicago, IL 60654-4717(312) 846-5677

Fax: (312) [email protected]

John Wesley LemegaHalloran & Sage LLP

1 Goodwin SqHartford, CT 06103-4300

(203) 297-4679Fax: (203) 548-0006

Marc Steven MayersonSpriggs & Hollingsworth

1350 I St NWWashington, DC 20005-3305

(202) 898-5844Fax: (202) 682-1639

Mark Daniel MeseKean Miller Hawthorne et al

PO Box 3513Baton Rouge, LA 70821-3513

(225) 382-3424Fax: (225) 388-9133

Continued on page 3

Insurance Coverage Litigation Committee Newsletter Spring 2009

3

Helen Katherine MichaelHowrey LLP

1299 Pennsylvania Ave NWWashington, DC 20004-2400

(202) 383-7156Fax: (202) 383-6610

Christopher R MosleySherman & Howard

Ste 3000633 17th St

Denver, CO 80202-3622(303) 299-8466

Fax: (303) [email protected]

Bradford S MoyerKelley Casey & Moyer PC

472 Academy StKalamazoo, MI 49007-4680

(586) 563-3500Fax: (269) 384-3200

Lisa Ayn OonkLitchfield Cavo LLP

Ste 4505201 W Kennedy BlvdTampa, FL 33609-1861

(813) 289-0690Fax: (813) 289-0692

Michael Alan OrlandoMeyer Orlando LLC

Ste 11913201 Northwest Fwy

Houston, TX 77040-6012(713) 460-9800

Fax: (713) [email protected]

John G OsbornBernstein Shur

Fl 6100 Middle St

Portland, ME 04101-4100(207) 774-1200

Fax: (207) [email protected]

Charmagne Ann Padua103 Roslyn Ave

Sea Cliff, NY 11579-1553(718) 250-1434

Fax: (201) [email protected]

James D Paskell30455 Cannon Rd

Solon, OH 44139-1608(440) 498-0171

Ginny PetersonKightlinger & Gray LLP

Ste 600151 N Delaware St

Indianapolis, IN 46204-2713(317) 638-4521

Fax: (317) [email protected]

David K PharrBradley Arant Boult Cummings LLP

Ste 450188 E Capitol St

Jackson, MS 39201-2140(601) 948-8000

Fax: (601) [email protected]

Susan M PopikChapman Popik & White LLP

Fl 19650 California St

San Francisco, CA 94108-2736(415) 352-3000

Fax: (415) [email protected]

Jose RamirezHolland & Hart LLP

Ste 4008390 E Crescent Pkwy

Greenwood Village, CO 80111-2822(303) 290-1605

Fax: (303) [email protected]

Ronald L RichmanBullivant Houser Bailey PC

Ste 1800601 California St

San Francisco, CA 94108-2823(415) 352-2700

Fax: (415) [email protected]

Craig E StewartEdwards Angell Palmer & Dodge

111 Huntington AveBoston, MA 02199-7610

(617) 239-0164Fax: (617) 227-4420

Jeffrey E ThomasUniv of Missouri KC Law School

5100 Rockhill RdKansas City, MO 64110-2499

(816) 235-2378Fax: (816) [email protected]

Alan Van EttenKlevansky Piper Van Etten LLP

Pauahi Tower Ste 7701003 Bishop St

Honolulu, HI 96813-6421(808) 237-5545

Fax: (808) [email protected]

Latanishia D WattersHaskell Slaughter et al

Ste 14002001 Park Pl N

Birmingham, AL 35203-2700(205) 251-1000

Fax: (205) [email protected]

Frank James WeissTonkon Torp LLP1600 Pioneer Twr888 SW 5th Ave

Portland, OR 97204-2012(503) 802-2051

Fax: (503) [email protected]

Robert I WesterfieldBowles & Verna

Ste 8752121 N California Blvd

Walnut Creek, CA 94596-7387(925) 935-3300

Fax: (925) [email protected]

Nicole E WilinskiKelley Casey & Moyer PC

19501 E Eight MileSt Clair Shores, MI 48080-1643

(586) 563-3500Fax: (586) 563-3400

Christopher YetkaLindquist & Vennum PLLP

Ste 420080 S 8th St

Minneapolis, MN 55402-2274(612) 371-2416

Fax: (612) [email protected]

Continued from page 2

VISIT OUR WEBSITE AT:HTTP://WWW.ABANET.ORG/TIPS

©2009 American Bar Association, Tort Trial & Insurance Practice Section, 321 N. Clark St., Chicago, Illinois 60610; (312) 988-5607. Allrights reserved.

The opinions herein are the authors’ and do not necessarily represent the views or policies of the ABA, TIPS or the Insurance CoverageLitigation Committee. Articles should not be reproduced without written permission from the Tort Trial & Insurance Practice Section.

Editorial Policy: This Newsletter publishes information of interest to members of the Insurance Coverage Litigation Committee of the TortTrial & Insurance Practice Section of the American Bar Association — including reports, personal opinions, practice news, developing lawand practice tips by the membership, as well as contributions of interest by nonmembers. Neither the ABA, the Section, the Committee, northe Editors endorse the content or accuracy of any specific legal, personal, or other opinion, proposal or authority.

Copies may be requested by contacting the ABA at the address and telephone number listed above.

Insurance Coverage Litigation Committee Newsletter Spring 2009

4

MESSAGE FROM THE CHAIRSAnother ICLC Successful Annual Meeting

We had our 17th Annual Mid-Year meeting in downtown Los Angeles—the real deal— at the Beaux Artsmasterpiece—the Millennium Biltmore Hotel, where the Oscars were first invented.

We had a record turnout for our program and record sponsorship. A special thanks go to the Program ChairmanAlan Van Etten and to all our active committee members whose joint efforts allowed this program to succeed wellbeyond expectations. Our educational program covered a wide spectrum of topics beginning with an introductorysession on the basics of insurance coverage litigation, followed by our Friday in-depth seminars focusing onexcess/primary settlement issues, avoiding bad faith liability in complex insurance cases, the hot topics of climatechange and sub-prime mortgage crises insurance related issues and concluding on Saturday with a seminar onwhich jurisdictions might favor one side or the other in insurance litigation, a lively seminar on stipulated judg-ments and garnishments ending with a program on the ever interesting billing guidelines/auditing issues. As usualour tool box lunch was a rousing success—lively discussions across a large dining room filled with a dozen roundtables at which twelve insurance related topics were debated, sometimes to rotating chairs due to the enthusiasticoverflow attendance.

Our social events included an evening in the mysterious film noir type setting of the hottest nightclub in LosAngeles, the Edison on Friday—so well attended that the waiters had a slow start on the martinis—but eventuallyall were served followed by a lovely buffet dinner where our members, attendees, and their families easily social-ized amidst the exotic furnishings. The Saturday dine around was the usual successful event again allowing addi-tional time to socialize with old friends and make new ones. The Business meeting was well attended and wecovered a long agenda relating to our future events and activities, including the on going publications and plans fornext year’s events, including our 18th Annual Mid-Year.ICLC at the TIPS Spring Meeting

On the last weekend in April, TIPS held its annual Spring Meeting. This year the meeting was at the Broadmoorin Colorado Springs, a magnificent place.

ICLC was represented by four members Jose Ramirez, Joel Mosher, Brad Moyer, and Alan Rutkin. Joseattended a membership development program. Joel participated in the CLE Board. Brad and Alan attended variouscommittee training programs. Training ranged from the tedious to the torturous. TIPS leadership did, however,offer many ideas that the committee will consider. TIPS leadership also reviewed the committee’s various admin-istrative obligations. ICLC is, at this time, up to date in all of its obligations and reports, including various filingsthat were due in the weeks following the spring meeting.

The program also offered very nice social programs, including a golf outing (ICLC participated, without severeembarrassment, in the outing).What’s Next?

We are looking forward to the August 2009 Annual Meeting of the ABA in which ICLC will present a programon the Fairness and Efficiency of Appraisal and Arbitration Clauses lead by our members Chris Yetka and DawnGonzales.

Upcoming TIPS meetings will be at very appealing venues. The Fall 2009 meeting will be at the hotel DelCoronado in San Diego, California. The Spring 2010 meeting will be at the Ritz Carlton in San Juan.

http://www.abanet.org/tips/iclc/home.html

Insurance Coverage Litigation Committee Newsletter Spring 2009

5

NOTE FROM THE EDITORSBetter late than never, that is what everyone says — unless of course, it’s a court deadline. Thankfully, the

publication of the ICLC Newsletter is not tied to court deadlines, so we will apologize for our delay in providingyou with the spring 2009 ICLC Newsletter (my fault, not Jim’s), but it is worth the wait.

We have three great articles on diverse topics, one of which is surely relevant to your practice. Joel Mosherwrites on the timely topic of “in fact” exclusions in E&O policies – exclusions that will likely be invoked in theexpected wave of lawsuits resulting from the current economic downturn. Next, John LaBarbera and BenjaminBlume challenge us to re-examine “trigger of coverage” in asbestos-related coverage litigation in light of updatedmedical science. Finally, Nosizi Ralephata reminds of us when and under what circumstances an excess policy istriggered to indemnify and, in some circumstances, defend the insured.

As this newsletter goes to print we are readying for the summer submissions, thanks to the overwhelmingresponse to the recent listserv request for articles. In fact, the response was so great that we will be publishing four,instead of three, articles for the next two issues to provide everyone with the opportunity to see their words in print.Stay tuned for jam-packed newsletters for the rest of 2009.

Happy spring, well er, early summer!Elizabeth & JimFor questions, comments or article submissions, please contact Elizabeth Sackett at [email protected]

[note new email address] or Jim Creenan at [email protected].

RE-EVALUATING TRIGGER OF COVERAGE IN ASBESTOS BODILYINJURY CLAIMS INVOLVING MESOTHELIOMA AND BROCHOGENICCARCINOMA: A REVIEW OF RECENT CASE LAWBy: John D. LaBarbera and Benjamin A. Blume1

It has been nearly three decades since the earliestcourt decisions addressed the question of when bodilyinjury occurs in determining a liability insurer’s obliga-tions to defend or indemnify underlying asbestosbodily injury claims. Those earliest cases focused theiranalysis almost exclusively on the medical evidencesurrounding asbestosis with limited or no comment onasbestos related malignancies such as mesotheliomaand bronchogenic carcinoma. The medical evidencesupporting these earliest decisions was, in turn, basedon medical studies conducted in the 1940’s, 1950’s and1960’s, decades prior to the courts’s consideration ofthe medical evidence.

Based on these early decisions and premised on thestate of medical knowledge as it existed decades ago,courts in the United States have adopted one of fourdominate views on the issue of trigger of coverage inasbestos bodily injury claims: (1) the exposure theory;

(2) the injury-in-fact theory; (3) the manifestationtheory; and (4) the continuous trigger theory. Whilerecognizing that these decisions were often limited inscope addressing only asbestosis claims, courtsnonetheless have applied the same trigger of coveragerules to asbestos-related malignancies. The jurispru-dence on trigger of coverage has not significantlyevolved over the recent decades; however, manycontend that medical knowledge as to the etiology ofmesothelioma and bronchogenic carcinoma hasadvanced sufficiently such that the courts should beasked to reconsider this issue.

The question of when bodily injury occurs withregard to asbestos related malignancies has been takenup recently by courts in the United States and theUnited Kingdom. Based on the medical evidencepresented in those circumstances, the courts have

Continued on page 12

1 John D. LaBarbera and Benjamin A. Blume are Members of Clark Hill PLC where they co-chair the Insurance and Reinsurance practice group. Their practice focuses on advisinginsurers and reinsurers in a variety of business matters including captive insurer formations, regulatory matters, tax issues, litigation and arbitration. The opinions expressed in thisArticle are those of the Authors and not of Clark Hill PLC or its clients.

Insurance Coverage Litigation Committee Newsletter Spring 2009

6

A SURVEY OF RECENT CASES ADDRESSING TRUE EXCESS CARRIERISSUES: TRIGGER, DUTY TO DEFEND AND DROP DOWN1

This article addresses recent case law construing thecommon issues confronting excess carriers. Indeed, a“true excess” carrier ordinarily has few duties to theinsured so long as the primary insurer fulfills its obli-gation.2 Nonetheless, courts continue to address theissue of when an excess policy is triggered, whetherthere is a duty to defend, and whether the excess carriermust “drop down” and take the place of a primary.These issues remain controlled largely by the precisepolicy language, although other factors tend to creepinto the judicial construction of excess insurancepolicies.

First, it is necessary to identify whether a commer-cial insurance policy is excess or not. A “true excess”policy can be identified from the insuring agreementand other policy language.3 Excess coverage clauses inliability policies can be obtained only when there isother primary coverage available.4 An insurance policyis a “true excess” policy only if it is written undercircumstances where the rates are ascertained aftergiving due consideration to known existing and under-lying basic or primary policies.5 Courts generallyenforce excess coverage language where the excesscarrier has no reasonable expectation of primarycoverage, the rights of the insured are unaffected bythis construction, and particularly where the languageof the excess policy clearly denotes that policy’s excessstatus.6

Trigger Issues

Courts generally look to the policy’s language andhold that excess coverage is not triggered until theunderlying primary limits are exhausted by way ofjudgments or settlements. Courts approach the issue indifferent ways depending on the specific languageemployed by the excess carrier, as illustrated below:

1. Unambiguous Policy Language RequiringPayment of Entire Primary Policy Limits

The following cases required complete exhaustionof the underlying primary limits before the excesspolicy was obligated to respond.

Comerica Inc. v. Zurich Am. Ins. Co.7 The relevantlanguage at issue in that case provided: the excesspolicy “does not provide coverage for any loss notcovered by the Underlying Insurance except and to theextent that such loss is not paid under the UnderlyingInsurance solely be reason of the reduction or exhaus-tion of the available Underlying Insurance throughpayments of loss thereunder.” The court found that thislanguage unambiguously required the primary carrierto either pay limits or be held liable for policy limits asa condition precedent to the excess policy being impli-cated. Therefore, accepting a settlement from theprimary carrier for less than policy limits was insuffi-cient to trigger excess insurance.

Qualcomm v. Certain Underwriters at Lloyd’s,London.8 The relevant policy language provided thatthe excess policy was not implicated until the primarypolicy “ha[s] paid the full amount of [twenty-milliondollars]” where $20M was the primary policy limit. Thecourt held that this language unambiguously requiredthe primary carrier to be liable to pay the $20M policylimit prior to imposing liability on the excess carrier.Thus, when the insured settled with the primary carrierfor below policy limits, the excess carrier was absolvedfrom liability to indemnify the insured.

2. Ambiguous Policy LanguageIn the following cases, the court found the excess

policy language to be ambiguous.Zeig v. Mass. Bonding & Ins. Co.9 The following

language was at issue: “As excess and not contributing1 By Nosizi Ralephata. Ms. Ralephata is an attorney with the law firm Turner Padget Graham & Laney P.A., in Charleston, SC and focuses her practice on business litigation issues.She can be reached at [email protected] Although there are situations whereby a primary policy could be/has been afforded excess status by virtue of certain circumstances, including “other insurance” clauses, the focusof this article is on a “true” excess policy.3 See, Commercial Union Ins. Co. v. Bituminous Cas. Corp., 851 F.2d 98 (3d Cir. 1988); Lexington Ins. Co. v. Virginia Sur. Co., Inc., 486 F. Supp. 2d 173 (D. Mass. 2007); UnitedServices Auto. Ass’n. v. Travelers Indem. Co., 240 Va. 214, 396 S.E.2d 658 (1990).4 Federal Ins. Co., an Indiana corporation v. Hartford Steam Boiler Inspection and Ins. Co., 415 F.3d 487, 2005 FED App. 0291P (6th Cir. 2005).5 Loy v. Bunderson, 107 Wis. 2d 400, 320 N.W.2d 175 (1982).6 Holden v. Connex-Metalna Management Consulting GmbH, 302 F.3d 358 (5th Cir. 2002); Travelers Cas. and Sur. Co. v. American Intern. Surplus Lines Ins. Co., 465 F. Supp. 2d1005 (S.D. Cal. 2006). See also, CJS INSURANCE § 1616.7 498 F. Supp.2d 1019, 1032 (E.D. Mich. 2007).8 73 Cal. Rptr. 3d 770, 777-78 (Cal. Ct. App. 2008).9 23 F.2d 665 (2d Cir. 1928) (opinion by Augustus Hand, J) (pre-Erie decision).

Insurance Coverage Litigation Committee Newsletter Spring 2009

7

insurance, and shall apply and cover only after all otherinsurance herein referred to shall have been exhaustedin the payment of claims to the full amount of theexpressed limits of such other insurance.” The courtfound this language ambiguous, and in often citedlanguage, the court stated:

The defendant argues that it was necessary forthe plaintiff actually to collect the full amount ofthe policies for $15,000, in order to ‘exhaust’that insurance. Such a construction of the policysued on seems unnecessarily stringent. It isdoubtless true that the parties could impose sucha condition precedent to liability upon the policy,if they chose to do so. But the defendant had norational interest in whether the insured collectedthe full amount of the primary policies, so longas it was only called upon to pay such portion ofthe loss as was in excess of the limits of thosepolicies. To require an absolute collection of theprimary insurance to its full limits would inmany, if not most, cases involve delay, promotelitigation, and prevent an adjustment of disputeswhich is both convenient and commendable. Aharmful result to the insured, and of no rationaladvantage to the insurer, ought only be reachedwhen the terms of the contract demand it.

The “harmful result to the insured” and the “norational advantage to the insurer” (sometimes called thewindfall to the excess insurer) bases have been reliedupon by many courts as justification for lookingbeyond policy language, and thereby preclude theexcess carrier from escaping liability due to the exhaus-tion clause’s requirements.

Stargatt v. Fidelity & Cas. Co. of N.Y.10 In this case,the excess policy was liable “only when the primarypolicy … has been exhausted.” The court held thatwhen “exhaustion” is not defined, it is an ambiguousterm. The court found that the plain meaning of‘exhausted’ is ‘entirely used up,’ and the coverage ofthe primary policy has been entirely used up by thesettlement. The court found that the excess insurer hadno rational interest in whether the insured collected thefull amount of the primary policies, so long as it wasonly called upon to pay such portion of the loss as wasin excess of the limits of those policies. To require anabsolute collection of the primary insurance to its fulllimits would in many, if not most, cases involve delay,promote litigation, and prevent an adjustment ofdisputes which is both convenient and commendable.

3. Policy Language Ignored in Favor of OtherFactors

LEGAL TIPSLEGAL TIPS

We're proud to tell you about a special legal podcast series called Legal TIPS

In February, the Government Law and Animal Law Committees began producing a series of internet podcast radio talk shows that air weekly on Legal Talk Network. Join the thousands already tuning in at Legal TIPS on LTN.

CREATIVE APPROACHES TO OLD PROBLEMS

THOUGHT-PROVOKING DISCUSSIONS

CUTTING EDGE ISSUES

Podcasts with global reach concerning...

10 67 F.R.D. 689 (D.Del. 1975), aff’d 578 F.2d 1375 (3d Cir. 1978).

Continued on page 8

Insurance Coverage Litigation Committee Newsletter Spring 2009

8

As may occur from time to time, the following casesdemonstrate a court’s willingness to ignore the actualpolicy language in favor of other considerations.

Periera v. Nat’l Union Fire Ins. Co.11 There, theexcess carrier’s policy provided:

The Company shall provide the Insured withinsurance excess of the Underlying Insurance ...only after all Underlying Insurance has beenexhausted by actual payment of claims or lossesthereunder.

…..In the event of the depletion of the limits ofliability of the Underlying Insurance solely asthe result of actual payment of claims or lossesthereunder by the applicable insurers, this policyshall... apply to claims or losses as excess insur-ance over the amount of insurance remainingunder such Underlying Insurance.

The court refused to require exhaustion as provided inthe policy because of the hardship to the insured (whohas already suffered due to the insolvency of theprimary carrier), and because of the windfall itprovided to the excess carrier. The court expresslydetermined that the language was ambiguous, and alsoprovided that the excess insurer’s construction of theclause was not the only reasonable one.

UMC/Stamford, Inc. v. Allianz Underwriters Ins.Co.12 This holding illustrates the rationale behind thosecourts that hold that as a matter of law, an excess carrieris not going to be absolved from liability by a primarycarrier’s settlement under policy limits:

As long as the underling liability exceeds theprimary limits in a vertical exhaustion, it doesnot matter how much the primary paid plaintiffs.If there is any dollar difference between theprimary layer of coverage and the amount of thesettlement, plaintiffs will have to pay that differ-ence before expecting to obtain any reimburse-ment from excess insurance companies sinceplaintiffs do not contend that these are ‘dropdown’ policies. It is therefore irrelevant what theexact dollar figure was in the settlement.

HLTH Corp. v. Ag. Excess & Surplus Ins. Co.13 Thecourt ignored the exhaustion requirement of the excesspolicy and found that the excess carrier would not bedischarged from liability when the plaintiff settled withthe primary carrier for less than primary policy limits.The court based its opinion on Stargatt and Zieg, sayingthis would help promote settlement.Restatement of Duty to Indemnify

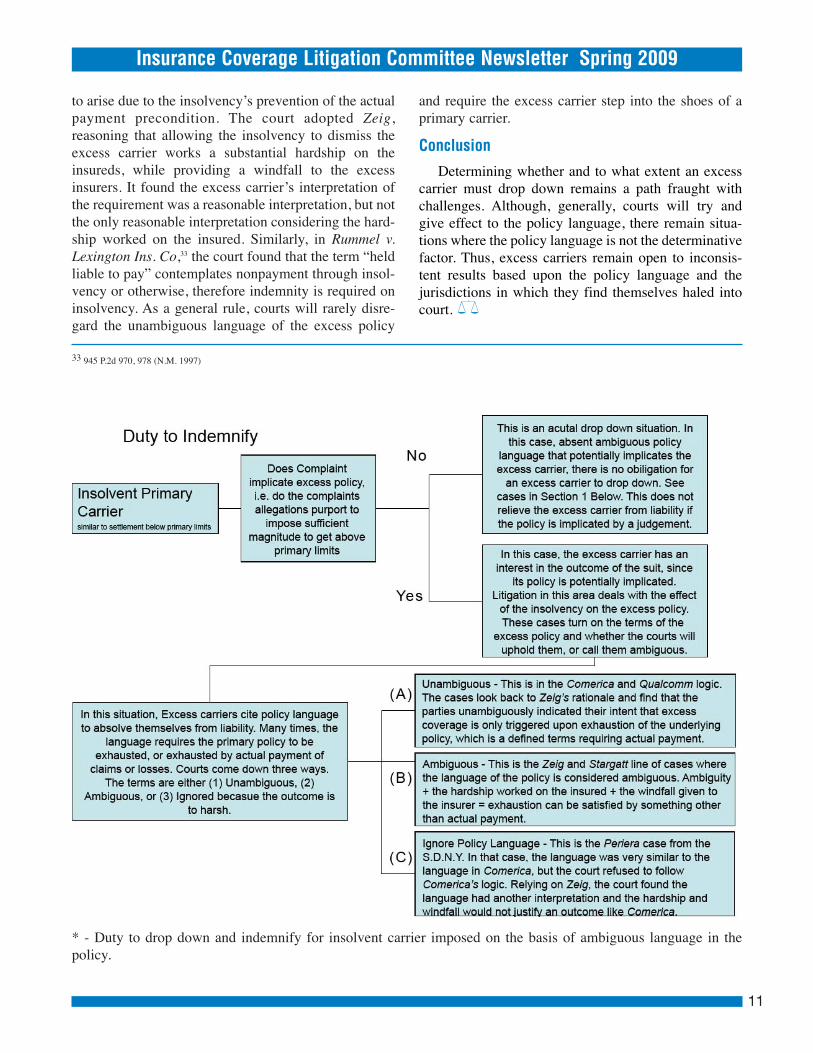

Excess carriers frequently litigate what the policyrequires as a condition precedent to its indemnification.Generally, exhaustion is required; however, whatconstitutes exhaustion is at the core of the controver-sies. In these situations, the excess insurer may seek todeny coverage based on the primary insurers insol-vency or based on a settlement with the primary carrierbelow policy limits that purportedly released the excesscarrier due to the exhaustion requirement. In thosecases where the primary carrier is insolvent, the ques-tion becomes whether the policy language requires theexcess carrier to assume liability or whether thelanguage serves as a release of the excess carrier basedon the primary carrier’s insolvency. The flow chart onpage 11 summarizes the various scenarios.

Continental Marble & Granite v. Canal Ins. Co.14Policy language that stated secondary carrier wasimplicated when primary carrier was “inapplicable” didnot pertain to insolvency of primary carrier. This would“transmogrify the policy into one guaranteeing thesolvency of whatever primary insurer the insured mightchoose.” The court refused to require the excess carrierto indemnify or provide a defense because “inapplic-able” unambiguously meant the liability was notcovered by the primary policy, rather than unable to becovered by the primary carrier due to its insolvency.

Reserve Ins. Co. v. Piciotta.15 Here, the court foundthat the excess carrier must drop down and indemnifywhen it assumed liability for any excess over the“amount recoverable” under the primary policy,because “amount recoverable” was ambiguous andcould mean something substantially less than policylimits in situation where there was an insolvent primarycarrier. This is because the amount recoverable fromthe insolvent primary carrier was obviously going to beless than policy limits. Under those circumstances, theexcess carrier has to drop down and provide coverage.

A SURVEY...Continued from page 7

11 2006 WL 1982789, at *7 (S.D.N.Y. July 12, 2006).12 647 A.2d 182 (N.J. 1994).13 2008 WL 3413327 (Del. Super. Ct. July, 31 2008).14 785 F.2d 1258 (5th Cir. 1986).15 640 P.2d 764 (Cal. 1982).

Insurance Coverage Litigation Committee Newsletter Spring 2009

9

Duty to Defend Issues

A true excess policy usually does not contain adefense obligation. Nevertheless, there are circum-stances when an excess policy has been called upon toprovide a defense, often in “drop down” circumstances.The term “drop-down” refers to an excess carrier’sobligation to assume duties to the insured where theexcess policy’s stated underlying limits have not beenreached.16 Drop down coverage occurs when an insur-ance carrier of a higher level of coverage is obligated toprovide the coverage that the carrier of the immediatelyunderlying level of coverage has agreed to provide.17

By way of example, if a policy that provides$5,000,000 excess of $1,000,000 has a stated attach-ment point of $1,000,000, drop down would occurwhen that excess insurance company is asked to pay aloss that is less than the $1,000,000 stated attachmentpoint.18 If obligated to “drop down”, the excess carrierwould be responsible to fulfill the obligations of setforth in the primary policy.19 Whether the excess policy“drops down” to the level of primary insurer, wherebythe excess insurer assumes the obligations of theprimary insurer, including defense obligations, dependson the provisions of the excess policy.

As illustrated in the flow chart on page 12, an excesscarrier’s obligation to defend becomes the subject oflitigation more often than not, where the primarycarrier becomes insolvent and drop down coverage isrequested from the excess carrier. In these cases, thegeneral rule is there is no duty to drop down where theexcess policy language expressly provides that it willnot drop down in cases of insolvency. Courts havehowever, managed to maneuver around the language incertain cases, as discussed further below.

1. Unambiguous Policy Language Resulting inNo Drop Down

Molina v. U.S. Fire Ins. Co.20 Policy languagerequiring underlying policies to be “in force” and“collectible” was not met by insolvent primary insurer.The duty to defend was not triggered. No duty toadvance defense costs, and defense costs could berecovered after the fact on a pro-rata basis.

Zurich Ins. Co. v. Heil Co.21 Policy languagerequiring underlying policies “be maintained in force ascollectible insurance” during the coverage of the excessinsurer was found to unambiguously require a solventprimary insurer. Thus, the excess insurer has no duty todrop down and provide defense costs. The risk of theprimary carrier’s insolvency stays with the insured.

Premcor USA, Inc. v. American Home AssuranceCo.22 Court determined “amount recoverable”language, which is ambiguous under Illinois law, ismodified by language stating that liability should not beincreased by “the refusal or inability of any underlyinginsurer to pay, whether by reasons of insolvency, bank-ruptcy, or otherwise.” Policy also had language thatsaid excess carrier “shall not be liable for expenses asaforesaid when such are covered by underlying policiesof insurance whether collectible or not.” Court also saiddefense did not argue the fact that the excess carrier’spremium did not reflect the risk of insolvency.

2. Ambiguous Policy Language Resulting inDuty to Drop Down

Donald B. MacNeal, Inc. v. Interstate Fire & Cas.Co.23 In this case, the court found the phrase “amountrecoverable” ambiguous. The excess policy assumedliability in excess of “amount recoverable under under-lying insurance.” The court said this could mean theamount recoverable from an insolvent carrier, ratherthan merely policy limits on the primary carrier, so theexcess carrier had to indemnify the insured for the fullamount of liability. Insured was owed defense costs aswell as full indemnity for the primary limits.

Alabama Ins. Guaranty Assoc. v Magic CityTrucking Service, Inc.24 The court found that thephrase “collectible by the insured” in an excessinsurance policy’s definition of underlying limitmeant that the excess insurer would providecoverage where the primary coverage was notcollectible, and determined that a state guarantyassociation was required to drop down, when boththe primary insurer and excess insurer became insol-vent, to cover the liability of the primary insurer, inthe excess insurer’s stead. The court pointed out that

16 Louisiana Insurance Guaranty Assoc. v. Interstate Fire & Cas. Co., 630 So.2d 759, 761 fn. 1 (1994).17 Id.18 Id.19 Flintkote Co. v. General Acc. Assur. Co. of Canada 2008 WL 3270922, 26 (N.D.Cal.) (N.D.Cal., 2008).20 574 F.2d 1176, 1178 (4th Cir. 1978).21 815 F.2d 1122 (7th Cir. 1987).22 400 F.3d 523 (7th Cir. 2005).23 477 N.E.2d 1322 (1985).24 547 So. 2d 849 (Ala. 1989).

Insurance Coverage Litigation Committee Newsletter Spring 2009

10

when an excess insurer used the term “collectible” orsimilar language in its underlying limit provision,courts had held that the insurer agreed to drop downin the event of the insolvency of the primary insurer,and courts holding that the excess insurer was notrequired to drop down in the event the primaryinsurer became insolvent had relied upon the limitsof liability provisions.

3. Excess Carrier ’s Policy Provides forAdvancement Of Defense Costs

HLTH Corp. v. Ag. Excess & Surplus Ins. Co.25 Theexcess insurers had a provision to advance defensecosts so long as any claims were part of coverage. Thepolicies called for advancement of such costs, andunless all claims could be shown to be out of scope,there was a duty to defend upon exhaustion of lowerclaims.

4. Duty to Provide Defense when Primary Carrierrefuses.

Am. Fam. Life Assurance Co. v. U.S. Fire Co.26 Inthis case, a provision in the policy provided that theexcess insurer had to provide a defense. The courtfound that ordinarily an excess carrier has no duty todefend, unless a primary carrier denies coverage. Sincethe primary policy denied coverage, the excess carrierwas required to drop down and provide it, unless therewas a reason not to provide coverage in good faith.

Hocker v. New Hampshire Ins. Co.27 In interpretingthe pertinent policy language, the court found that theexcess insurer had a duty to drop down and provide adefense even if the primary insurer wrongfully refusedto provide a defense. The excess insurer may recover itscosts if the primary insurer refused to provide a defensein bad faith. Additionally, an excess insurer has a dutyto monitor the primary insurer and ensure it is properlyfulfilling its obligations.

5. Summary of Drop Down Scenarios.The majority rule remains that absent obligatory

policy language, an excess insurer is not required todrop down and cover that portion of a loss once withinan insolvent primary insurer’s coverage, nor must itdrop down to provide the defense that an insolventprimary insurer was obligated to fund.28 Ordinarily, aprimary insurer’s insolvency obligates the state’s guar-anty association to “step into the shoes” of the primaryinsurance carrier and fulfill that carrier’s obligationsbefore the excess insurance carrier is obligated toprovide coverage.29 Accordingly, unless insolvencycoverage is an express exception, most excess coveragepolicies clearly condition the obligation of the excesscarrier to provide coverage only upon the exhaustion ofthe primary carrier’s limits by payment of claimsagainst the primary coverage, and where this conditionis expressed, the courts have ruled that the insolvencyof the primary carrier does not activate excesscoverage.30 As justification for finding that an excesscarrier has no obligation to drop down in the event of aprimary carrier’s insolvency, courts have relied on twoprimary consideration: (1) insolvency of the underlyinginsurer(s) is usually not regarded as an “occurrence” asdefined by most insurance policies; and (2) excessinsurers charge low premiums in exchange for placingthe burden of retaining a financially stable primaryinsurer upon the insured. From this perspective, courtsfind that excess insurers are not the guarantors of thesolvency of underlying insurers.31

However, in spite of policy language and the aboveconsiderations, some courts have found that an excesscarrier is obligated to drop down where the primarycarrier becomes insolvent.32 In Periera, one of theunderlying insurers was insolvent, and the policyrequired actual payment prior to triggering excesscoverage. The excess carrier argued it should bedismissed because it was impossible for its obligation

25 2008 WL 3413327 (Del. Super. Ct. July, 31, 2008).26 885 F.2d 826, 836-37 (11th Cir. 1989).27 922 F.2d 1476, 1484-85 (10th Cir. 1989).28 See, e.g., Hartford Accident & Indem. Co. v. Chicago Hous. Auth., 12 F.3d 92, 95, 97 (7th Cir. 1993); Revco D.S., Inc. v. Gov’t Employees Ins. Co., 791 F. Supp. 1254, 1265(N.D. Ohio 1991), aff’d, 984 F.2d 154 (6th Cir. 1992); Atl. Cargo Operators, Inc. v. First State Ins. Co., 398 S.E.2d 264, 266 (Ga. Ct. App. 1990); Emscor, Inc. v. Alliance Ins. Group,804 S.W.2d 195, 198-99 (Tex. Ct. App. 1991).29 See, e.g., North Carolina Insurance Guaranty Association v. Century Indemnity Company, 115 N.C.App. 175, 444 S.E.2d 464 (1994); Metropolitan Leasing, Inc. v. PacificEmployers Ins. Co., 36 Mass.App.Ct. 536, 633 N.E.2d 434 (1994); Louisiana Ins. Guar. Assn. v. Interstate Fire & Cas. Co., 630 So.2d 759 (La. 1994); Hartford Accident & Indemn.Co. v. Chicago Housing Auth., 12 F.3d 92 (7th Cir. 1993); Playtex FP, Inc. v. Columbia Cas. Co., 622 A.2d 1074 (Del.Sup.Ct. 1992); Morbark Industries, Inc. v. Western EmployersIns. Co., 170 Mich.App. 603, 429 N.W.2d 213 (1988).30 Irvin E. Shermer and William Schermer, 2 Auto Liability Ins. § 18:12 [4th Ed. 2005].31 See, e.g., North Carolina Ins. Guar. Assn. v. Century Indemn. Co., 115 N.C.App. 175, 185-86, 444 S.E.2d 464, 470 (1994) ( “[T]he fundamental purpose of excess insurance isto protect the insured against excess liability claims, not to insure against the underlying insurer’s insolvency[.]”); Wurth v. Ideal Mut. Ins. Co., 34 Ohio App.3d 325, 518 N.E.2d607 (1987) (excess insurance does not drop down when primary insurer is insolvent, because to hold otherwise would “place the risk of loss for securing an insolvent insurer noton the insurance purchaser, who purchased the policy, but on the excess coverage provider, who never contracted to cover such a contingency.”).32 Periera v. Nat’l Union Fire Ins. Co., 2006 WL 1982789, at *7 (S.D.N.Y. July 12, 2006).

Insurance Coverage Litigation Committee Newsletter Spring 2009

11

to arise due to the insolvency’s prevention of the actualpayment precondition. The court adopted Zeig,reasoning that allowing the insolvency to dismiss theexcess carrier works a substantial hardship on theinsureds, while providing a windfall to the excessinsurers. It found the excess carrier’s interpretation ofthe requirement was a reasonable interpretation, but notthe only reasonable interpretation considering the hard-ship worked on the insured. Similarly, in Rummel v.Lexington Ins. Co,33 the court found that the term “heldliable to pay” contemplates nonpayment through insol-vency or otherwise, therefore indemnity is required oninsolvency. As a general rule, courts will rarely disre-gard the unambiguous language of the excess policy

and require the excess carrier step into the shoes of aprimary carrier.Conclusion

Determining whether and to what extent an excesscarrier must drop down remains a path fraught withchallenges. Although, generally, courts will try andgive effect to the policy language, there remain situa-tions where the policy language is not the determinativefactor. Thus, excess carriers remain open to inconsis-tent results based upon the policy language and thejurisdictions in which they find themselves haled intocourt.

33 945 P.2d 970, 978 (N.M. 1997)

* - Duty to drop down and indemnify for insolvent carrier imposed on the basis of ambiguous language in thepolicy.

Insurance Coverage Litigation Committee Newsletter Spring 2009

12

reached conclusions, which cast doubt over theorthodox view that exposure to asbestos constitutes“bodily injury” where the underlying claims involve,mesothelioma or bronchogenic carcinoma. In Durhamv. BAI (Run Off) Ltd. (in scheme of arrangement) andother cases Re Employers’ Liability Policy ‘Trigger’Litigation, EWHC 2692 (2008), Judge Burton of theQueen’s Bench Division in London rejected the ideathat exposure to asbestos containing products consti-tutes bodily injury. A similar result was recentlyreached by the Supreme Court of New York, AppellateDivision, First Department in Continental Casualty Co.v. Employers Insurance Co. of Wausau, 871 N.Y.S.2d48 (N.Y. App. Div. 2008), where the court reversed atrial court ruling that exposure to asbestos triggeredcoverage under comprehensive general liabilitypolicies.

The decisions reached in both Durham andContinental Casualty Co. arose from findings that themedical evidence presented at trial established that inthe context of asbestos related malignancies, exposureto asbestos did not constitute a bodily injury sufficientto trigger an insurer’s obligations. These decisionsstand in stark contrast to the historical approach

employed by courts in addressing the trigger ofcoverage issue as it relates to asbestos related malig-nancies and suggest that perhaps the issue requiresfurther consideration by the courts.

Part I of this paper will review the historical casesaddressing the issue of when “bodily injury” occurs inthe context of asbestos bodily injury claims analyzingthe medical evidence presented at the time of thosedecisions. Part II of this paper will then discuss therecent cases and trends arising from those decisions asthey relate to the issue of whether exposure to asbestosconstitutes bodily injury. Drawing on the analysis ofthe most recent cases addressing the topic, Part III ofthis paper will present a framework for addressing theissues in future cases.I. Timing of Asbestos Bodily Injury - AnHistorical Review

There are a number of decisions that form the basisof the most commonly applied trigger theories in theUnited States. Their genesis and medical basis withregard to asbestos-related disease are each discussedbelow. The one unifying factor presented in eachinstance, is that very little information was known tothe medical community concerning the etiology andprogression of asbestos-related malignancies. Rather ineach of the cases, a detailed recitation of the medical

RE-EVALUATING...Continued from page 5

Insurance Coverage Litigation Committee Newsletter Spring 2009

13

evidence concerning the etiology of asbestosis waspresented.A. The Exposure TheoryThe exposure theory, as its name implies, holds

generally that liability insurance policies are triggeredwhen an underlying asbestos claimant was exposed tothe policyholder’s asbestos containing product. One ofthe earliest decisions addressing the issue of timing ofasbestos related injuries was Insurance Co. of NorthAmerica v. Forty-Eight Insulations, Inc., 451 F. Supp.1230 (E.D. Mich. 1978) aff’d 633 F. 2d 1212 (6th Cir.1980). In that case, the district court was called upon todetermine whether exposure to asbestos productsconstituted a triggering injury for asbestos-caused lungdisease or whether manifestation of disease was theproper trigger of coverage. Id. at 1238. The districtcourt conducted a trial on the issue and heard the testi-mony of three doctors, Dr. Forde A. McIver, Dr. HenryAnderson, and Dr. George Wright each addressingasbestos-caused lung disease. Id. at 1236. The courtfound substantial agreement on all points andrecounted the evidence providing a detailed discussionof asbestosis. Id. at 1236-37.

However, when summarizing the evidenceregarding mesothelioma and bronchogenic carcinoma,the court’s discussion of the evidence was far fromdetailed. The court summarized the medical evidenceoffered with regard to mesothelioma as follows:

The relationship between asbestos and mesothe-lioma is not well understood, and relativelysmall exposures over a period of years have beenassociated with this condition. The growth of atumor generally follows a latent period of over20 years during which there need not be anyadditional exposure. Diagnosis is possible withina short time of the beginning of tumor growth.

Id. at 1237.An even terser summary of the medical evidence

concerning bronchogenic carcinoma was offered by thecourt stating that the cancer was another malignantdisease that “has been associated with asbestos, at leastin persons who smoke cigarettes.” Id. The court alsonoted that bronchogenic carcinoma has a latent periodfollowing inhalation averaging 15 to 20 years and canoften be diagnosed within a few years of its initialappearance. Id. In fairness to the court, it is importantto recall that the Court of Appeals limited the applica-tion of the exposure theory in Forty-Eight Insulations,Inc. to asbestosis claims. 633 F. 2d 1212, 1223 (fn. 21).

B. The Manifestation TheoryThe manifestation theory generally holds that poli-

cies issued at the time that an asbestos claimant knowsor has reason to know they have an asbestos-relateddisease are obligated to respond to the underlyingasbestos claim. Courts applying the manifestationtheory focus on the date on which the claimant’s symp-toms become capable of medical diagnosis, actual diag-nosis, or death. Eagle-Picher Industries, Inc. v. LibertyMutual Insurance Co., 523 F. Supp. 110, 118 (D.C.Mass. 1981) aff’d with modifications 682 F. 2d 12 (1st

Cir. 1982). The First Circuit modified the trial court’sdefinition of manifestation holding that “a disease‘results’ under the policies when it becomes clinicallyevident, that is, when it becomes reasonably capable ofmedical diagnosis.” 682 F. 3d 12, 25.

In reaching this decision, the court received expertmedical testimony from Dr. Bernard Gee, a researchscientist and clinician with experience in the area ofasbestos-related disease and Dr. Edward Burger, whosetestimony was based solely on a review of current liter-ature in the field of asbestos-related disease and char-acterized by the trial court as “not particularly helpful.”523 F. Supp. 110, 115. In rejecting the exposure theorybased on the testimony offered by Dr. Gee, Judge Zobelconcluded:

Along the way, nearly all [asbestos] fibers areremoved, either through expectoration, by meansof the physiological filters of the nose and throat,through being carried back up and out by themucocilliary escalator, or sometimes by beingtaken away by the alveolar macrophage throughthe lymphatic system or the mucocilliary esca-lator. Moreover, even when the [asbestos] fiberhas become embedded in the lung and the scar-ring process has begun, the end result, that is,disabling disease or death, is by no meansinevitable.

Id. In furthering distinguishing the exposure theoryespoused by Forty-Eight Insulations, the trial courtconcluded that “[t]he Forty-Eight decision appears torest primarily on considerations of policy and result.”Id. at 117. Interestingly, it appears that no evidence wasconsidered by the court in Eagle Picher with regard tothe pathogenesis of asbestos related malignancies.C. The Injury-in-Fact TheoryThe injury-in-fact theory generally focuses on when

the injury, sickness, disease, or disability actuallybegan. Continental Casualty Co. v. Rapid America

Insurance Coverage Litigation Committee Newsletter Spring 2009

14

Corp., 593 N.Y.S.2d 966, 971 (N.Y. 1993). One of theleading cases applying the injury-in-fact trigger in thearea of asbestos bodily injury claims is the decision ofthe Supreme Court of Illinois in Zurich Insurance Co.v. Raymark Industries, Inc., 514 N.E.2d 150 (Ill. 1987).In that case, the court concluded that injury occursupon exposure to asbestos, upon sickness, defined as a“disordered, weakened or unsound condition, andmanifestation of disease.” 514 N.E. 2d at 160.Raymark Industries involved one of the more extensivemedical trials presented in the case law. The trial courtconducted a medical trial in the spring of 1983 to deter-mine how the policy terms “bodily injury, sickness ordisease” applies to asbestos related disease. Id. at 155.The medical evidence offered at trial consisted of thetestimony of nine experts who were board certifiedclinicians or pathologists. Again, just as in other cases,substantial medical testimony was offered regardingthe development of asbestosis. With regard to mesothe-lioma, the court concluded:

Although little is known about the disease, it isgenerally believed that it is attributable toasbestos fibers that pierce through the alveoliinto either the pleura or the peritoneum. Shortlyafter, these fibers injure and irritate the lining,causing a pre-malignant disease known asatypia. Then, there follows a long latency periodbefore the actual manifestation of a mesothelialtumor.

Id. at 156. With regard to bronchogenic carcinoma, thecourt concluded:

There was testimony based upon limited experi-mentation, that asbestos alone would not causethis type of cancer. When coupled with cigarettesmoke, however, the two interact synergisticallyto cause cancer. Before it is clinically detectable,bronchogenic carcinoma progresses throughseveral stages. By the time the tumor has grownto a size large enough to detect by an X ray,however, the disease is usually terminal.

Id. The central point of disagreement found among themedical experts testifying at trial was over the point intime when disease occurred. The clinicians generallyconcluded that while disease did not begin upon inhala-tion of asbestos fibers, it was more likely thatasbestosis does not begin until many years after expo-sure, in the years closest to the clinical manifestation ofthe disease. Id. Focusing again on asbestosis, thepathologists, unlike the clinicians, concluded thatasbestos fibers cause physical injury to cells of the lung

at or shortly after inhalation. The most salient pointderived from Raymark Industries is that little evidencewas presented as to the pathogenesis of asbestos-relatedmalignancies.D. The Continuous Trigger TheoryThe continuous trigger theory holds that injury

occurs from the date of exposure to asbestos productsthrough the date of manifestation of disease. Thistheory of coverage was described in Keene Corp. v.Insurance Co. of North America, where the court held“[w]e conclude that each insurer on the risk betweenthe initial exposure and manifestation of disease isliable to Keene for indemnification and defense costs.667 F. 2d 1034, 1041 (D.C. Cir. 1981). Unlike the othercases discussed above with regard to other trigger ofcoverage theories, the decision reached in Keene Corp.was not based upon the evidence presented at a detailedmedical trial. Rather, the decision was reach onmotions for summary judgment filed by the parties. SeeKeene Corp. v. Insurance Co. of North America, 513 F.Supp. 47, 48 (D. D.C. 1981). The trial court in KeeneCorp. did reference the testimony, submitted by theparties, of two medical experts; however, this evidencewas again focused on the pathogenesis of asbestosis.With respect to mesothelioma, the trial court describedthe testimony of Dr. Gaensler, who testified that:

Mesothelioma is a cancer of the mesothelial cellswhich line the chest walls and surround theorgans of the chest cavity. It generally occurs 20years or more after there has been excessiveinhalation of asbestos fibers in those individualswho develop it. While it is easily discovered anddiagnosed shortly after it develops, there is nosatisfactory treatment of the disease and thevictim almost always dies within several years ofthe tumor’s initial development. Dr. Gaenslertestified that the initial injury leading to thedisease occurs when an asbestos fiber travelsdown the lung’s airways, reaches an alveolus onthe edge of the lung, perforates the lung, and,with breathing, irritates the tissue. This processcan occur within several days, but it may take aslong as one to two months.

Id. at 51. With regard to bronchogenic carcinoma, thecourt summarized the testimony of the medical expertas follows:

Bronchogenic carcinoma, a group of tumors thatarise from different parts of the lung, is alsolinked with asbestos inhalation, though it has

Insurance Coverage Litigation Committee Newsletter Spring 2009

15

other known causes. Dr. Gaensler stated thatsignificant asbestos exposure increases asmoker’s chances of developing bronchogeniccarcinoma five to tenfold. He further testifiedthat the irritation caused by the asbestos fibers,which is a factor in the eventually diagnosedbronchogenic carcinoma, begins immediately oninhalation of asbestos.

Id. Interestingly, the trial court noted that “Dr. Gaenslerexplained that the correlation between asbestos inhala-tion and bronchogenic carcinoma in non-smokers is notknown because of its rare occurrence which makescarrying forth statistically significant studies extremelydifficult.” Id. at fn 4. Based on the medical evidence,the trial court found that the proper trigger waspremised on a claimant’s exposure to asbestos. Id.

In reversing the trial court, the Circuit Court foundthat the insurance policy language did not direct thecourt unambiguously to either the exposure or manifes-tation interpretation of the contracts. Rather the courtfocused on the “purpose of the insurance policies.” 667F. 2d at 1043. The court, without citation to medicalevidence, determined that asbestos-related diseases are“single injuries that occur over extended periods oftime.” Id. at 1044. The court, in determining that acontinuous trigger would be applicable found:

. . . in order for Keene’s rights under the policiesto be secure, both inhalation exposure and expo-sure in residence must also trigger coverage.Regardless of whether exposure to asbestoscauses an immediate and discrete injury, the factthat it is part of an injurious process is enoughfor it to constitute “injury” under the policies.

Id. at 1046. With regard to manifestation, the courtconcluded:

A latent injury, unknown and unknowable toKeene at the time it purchased insurance, must,at least, be covered by an insurer on the risk atthe time it manifests itself. Any other resultwould violate very reasonable expectations ofKeene. Therefore we hold that manifestation ofdisease is one trigger of coverage under thepolicies.

Id. at 1044.The court’s holdings with regard to the trigger of

coverage were not specific as to whether the rule artic-ulated applied to underlying claims involvingasbestosis, mesothelioma, or bronchogenic carcinoma.

Furthermore, the result articulated in Keene Corp. wasless reliant on the medical evidence considered by thetrial court as by the results orientated criticism leveledagainst the court in Forty-Eight Insulations. (Seesupra., Section I. B).II. Recent Decisions Addressing Timing ofAsbestos Bodily Injury

Most recently, courts in the United States and theUnited Kingdom have had occasion to revisit the issue oftrigger of coverage with new evidence being presentedon the etiology of asbestos-related malignancies.A. The American CourtsAmerican courts have had occasion to address the

timing of injury with regard to asbestos-related malig-nancies. In National Union Fire Insurance Co. ofPittsburgh, PA v. Porter Hayden Co., 331 B.R. 652(D.C. Md. 2005) the district court in adversaryproceedings was called upon to determine the timing ofinjury with regard to mesothelioma and bronchogeniccarcinoma.

Porter Hayden Company offered the affidavit of Dr.Edward Gabrielson, a pathologist and medical scientist.Dr. Gabrielson offered much more detailed opinionsconcerning the etiology of mesothelioma and bron-chogenic carcinoma than had been found in the earliestcases defining the trigger issue in asbestos coverageactions. His opinions were summarized by the court asfollows:

Most notably, asbestos is a cause of mesothe-lioma and lung cancer. The progenitor cells forthese types of cancer bronchial epithelial cellsfor lung cancer and mesothelial cells formesothelioma-are exposed to asbestos fibersshortly after inhalation.Cancers caused by asbestos present with clinicalsymptoms only after they have grown to aconsiderable size and long after the asbestosfibers initiated the carcinogenic process withcellular and molecular injuries.* * *Asbestos produces critical genetic changesrequired for carcinogenesis by physically andchemically injuring chromosomes. This injuryresults in chromosomal breaks and rearrangements.Asbestos injury also contributes to the carcino-genesis process by functioning as a tumor

Continued on page 17

SAVE THE DATEJoin TIPS at the ABA Annual Meeting July 30-August 4, 2009 - Chicago, IL

The Fairness and E�ciency of the Appraisal and Arbitration ClausesSaturday, August 1, 2009 - 2:00pm - 3:30pm

The Psychology of NegotiationFriday, July 31, 2009 - 8:30am - 10am

Juries: The Wildcard at Issue (Mock Trial)Sunday, August 2, 2009 - 8:30am -10:00am

The Changing Climate of InsuranceSunday, August 2, 2009 - 2:00pm - 3:30pm

Don’t Miss These CLE Programs

Con�ict of Interest and Ethical Considerations in Representing Insured’s and Insurers in Personal Injury LitigationSunday, August 2, 2009 - 2:00pm - 3:30pm

For more information and to register, visit:http://www.abanet.org/tips/market/Annual09/TIPS09Annual.html

Insurance Coverage Litigation Committee Newsletter Spring 2009

17

promoter. Asbestos functions as a tumorpromoter by at least two mechanisms. First,asbestos stimulates cells, including the [**29]genetically altered cells, to replicate. In addition,asbestos injury results in cytotoxicity (cellkilling) to some cells, with a greater cytotoxiceffect on normal cells than on cells with geneticalterations related to cancer.The net result of these two mechanisms — stim-ulation and selective cytotoxicity — is an expan-sion of the cell population that has the cancer-related genetic changes.* * *Many years — typically 20 to 50 — are requiredfor the development and growth of a clinicallyrecognized cancer after the onset of asbestosexposure.* * *Injury to an individual with cancer does notcease when a malignant cell arises from thecarcinogenesis process. In fact, as a cancergrows and invades surrounding normal tissue,additional injuries occur.* * *Lung cancer and mesothelioma are possibleconsequences of injuries to chromosomes and ofinjuries that lead to proliferation of geneticallyaltered cells. These cancers develop well beforeclinical manifestations and over a period ofmany years as a result of multiple and virtuallycontinuous injuries.

Id. at 663-64 (emphasis in the original). Based on thisevidence, the court concluded that exposure to andinhalation of asbestos fibers begins a cumulativeprocess in which the body suffers virtually continuousinjuries. Id. at 664. The court held that “every policy ineffect from the date of exposure until the date of mani-festation is triggered.” Id. What is telling about theresult in Porter Hayden Co. is that the insurerssubmitted no expert medical testimony to rebut thetestimony of Dr. Gabrielson.

Similar events occurred in Continental Casualty Co.v. Employers Insurance Co. of Wausau, 871 N.Y.S.2d48 (N.Y. App. Div. 2008), but with strikingly differentresults. In that case, the CNA companies brought adeclaratory judgment action seeking a declaration that

they had no duty to indemnify the defunct insured,Robert A. Keasbey Co. Id. at 50. In reversing the trialcourt’s ruling that exposure to asbestos triggerscoverage under the liability policies at issue in the case,the appellate division determined that actual injurydoes not occur upon inhalation of asbestos. This deci-sion was based on the expert testimony of CNA’smedical experts, including Dr. Edward Cohen. Withregard to the development of asbestos-related diseases,Dr. Cohen opined that:

Each inhalation of asbestos fibers results in alter-ations that contribute in a significant manner tothe cumulative disease process. I would not usethe word injury […] but certainly the presence ofasbestos fibers indirectly results in damage tocells and alterations of cellular material that overa period of 20-40 years can result in the devel-opment of impairment.

Id. at 61. Testifying about the point where cell mutationbecomes irreversible in malignant asbestos relateddiseases like mesothelioma, Dr. Cohen stated:

to say that cancers develop well before clinicalmanifestations is true but not for [***62]mesothelioma […] once the last mutation occursthe cells take off and grow very, very rapidly andthe evidence from that is the time of death fromthe time symptoms first appear.

Id. at 61-62. As for what causes mesothelioma, hetestified:

mesothelioma is common in individuals whohave been exposed to asbestos however […]many individuals with mesothelioma have nosuch exposure history […] and even in individ-uals who have [it] and have an exposure historydoes not necessarily prove that mesotheliomawas a consequence of the earlier exposure toasbestos and the only way to prove [that] is toexamine the mesothelioma and look for presenceof asbestos bodies.

Id. at 62. As for bronchogenic carcinoma, Dr. Cohentestified that studies have shown “a synergistic increasein the risk of lung cancer is present in individuals whoboth smoked and were exposed to asbestos.” Id.

Based on this testimony, the court concluded that itcan take 20 to 40 years after exposure for actual impair-ment of bodily functions to develop, that it is a progres-sive, cumulative disease that starts with alterations oftissue cells and sub-clinical tissue damage and couldprogress, though not necessarily progress, into full-blown asbestosis, mesothelioma or lung cancer. Id.

RE-EVALUATING...Continued from page 15

Insurance Coverage Litigation Committee Newsletter Spring 2009

18

Further, the court found that medical evidencesubmitted established that while those with asbestos-related diseases can usually track the illness back toasbestos exposure of some type, it is not axiomatic thatexposure results in asbestos-related injury, sickness ordisease. The court concluded, therefore, that factorsother than mere initial or one-time exposure to asbestosfibers are implicated in the development or progressiontowards asbestos-related injury sickness or disease. Id.Just as in Porter Hayden Co., the opposition offered noevidence to rebut the medical evidence presented by theCNA companies.Id. at 63-64.

Conversely, after conducting a medical trial, theCircuit Court of Cook County, Illinois reached theopposite conclusion in John Crane, Inc. v. Admiralinsurance Co., No. 04-CH-08266 (Cir. Ct. Cook Cty.Ill. Dec. 20, 2007), finding that the exposure to asbestoscontaining products constituted bodily injury. UnlikePorter Hayden Co. and Continental Casualty Co., theinsured and insurer presented competing evidence atthe medical trial conducted in the case. Testimony waspresented from three different expert witnesses whoincluded Dr. Gabrielson, presented by John Crane Inc.and Dr. Cohen, presented by CNA. Id. at * 8.Additionally, John Crane Inc. offered the testimony ofDr. Arnold Brody. Id. John Crane Inc. argued that themedical testimony of Dr. Brody and Dr. Gabrielsonrequired the court to find that bodily injury occurscontinuously from the date of exposure to asbestos untildeath. Id. CNA argued that with respect to non-malig-nancy claims, injury should be presumed to occurequally in each year beginning with the first exposureto the insured’s asbestos containing products andcontinuing until diagnosis of disease. Id. In manyrespects the testimony of Dr. Gabrielson was consistentwith his testimony presented in the Porter Hayden Co.case and the testimony of Dr. Cohen was consistent andsimilar to the testimony presented in ContinentalCasualty Co. CNA’s witness, Dr. Cohen opinedhowever, that with respect to asbestos-related malig-nancies injury began, six years before death frommesothelioma and tens years before death for lungcancer. Id. at *9.

While admitting Dr. Cohen’s testimony intoevidence as a general expert on cancer, the trial court,however, determined that he was not an expert withregard to asbestos-related diseases. Id. at *16. The courtnoted that Dr. Cohen’s testimony as to asbestos-relateddiseases was based on a 30-40 hour literature review.

Id. John Crane argued that based on its experts’ opin-ions, that the concept of ‘bodily injury” should beexpanded to encompass the genetic damage and muta-tions to the cells and the surrounding tissue that resultfrom exposure to asbestos fibers. Id. at *19-20.

The court rejected both views as to the etiology ofasbestos-related malignancies noting that Dr. Brodytestified that “no one knows whether cytokines andoxidants are produced with every asbestos fiber or onlyafter some threshold is reached.” Id. at *20. The courtfurther noted:

Even with increased cancer research, all threemedical experts testified that no one can deter-mine whether any given mutation occurred bychance by asbestos, or by another cause.Furthermore, the relation between exposure anda suspected occupational lung disease iscomplex and depends on such facts as cumula-tive exposure, dose, clearance and dissolution,latency, individual susceptibility, and interac-tions with host factor, e.g. smoking and thenature of the asbestos-related job. Moreover,genetic differences in people might progress theasbestos disease and they might not.

Id. Based on the medical evidence presented the courtdetermined that there was no injury during exposure inresidence. Accordingly, the court found that policies ineffect during the time of exposure to a John Craneasbestos containing product, sickness and the years ofmanifestation were triggered.B. The United KingdomCourts in the United Kingdom have reached very

different conclusions thanAmerican courts have histor-ically reached, in part, because they have relied onmore recent medical evidence. Judge Burton of theQueen’s Bench Division in London has recently issueda long and detailed opinion on trigger of coverage,based on, among other things, extensive expert testi-mony on the cause and progression of mesotheliomarejecting the notion that exposure to asbestos consti-tutes “bodily injury.” Durham v. BAI (Run Off) Ltd. (inscheme of arrangement) and other cases ReEmployers’ Liability Policy ‘Trigger’ Litigation,EWHC 2692 (2008).

Judge Burton’s ruling followed a trial that lastedsome eight weeks and included testimony by five“internationally recognized” medical experts. Three ofthe experts were “respiratory consultants.” The courtalso heard testimony from two biochemists, noting that

Insurance Coverage Litigation Committee Newsletter Spring 2009

19

“such biochemistry evidence is, so far as I know, a newfeature in asbestos/mesothelioma litigation.” Durham,¶30.

The court’s opinion contained a detailed discussionof the pathogenesis of mesothelioma, based on experttestimony, which recognized that much of the humanbody’s response to asbestos is no different than itsresponse to numerous foreign bodies that are inhaledevery day. The court stated that it is difficult to track theprogression from inhalation of asbestos to the manifes-tation of symptoms of mesothelioma 40 to 50 yearslater. Id., ¶104. However, one of the respiratory experts,Dr. Rudd, “with the assent of the other experts, gave avery clear diagrammatical overview of at least the startof the slow journey between inhalation and tumor.” Id.,¶105. Most inhaled asbestos fibers are caught in thelayers of mucus lining the airways, and are eliminatedfrom the body. However, some fibers will enter thelungs. Some will move quickly through the lungs andreach the pleura shortly after inhalation, and some maytake years. Many thousands, if not millions of suchfibers will remain in the lungs, where the body’sdefense mechanisms will begin to take care of them. Id.

Some of the fibers in the lung can be coated withprotein and coughed out. Some will attractmacrophages, which disable, destroy or engulf thefibers. If the macrophages are unsuccessful, chemicalsare released that may attract neutrophils by what iscalled an inflammatory response, and the neutrophilscan engulf the fibers. There is a continuous process ofdestruction of fibers and clearance of them from thelungs, but some fibers remain there, even until death.The experts specifically noted that “none of this resultsin or constitutes any symptoms, so far as any effect onthe person is concerned, and all of it involves thenatural reaction of the body on defence to the numerousforeign bodies which we are inhaling.” Id., ¶106.

Once one or more fibers are in the pleura, there maythen be an effect on the mesothilial cells. There can bea variety of effects, including cell death, interferencewith cell division, or impairing the defense againstmalignancy. In particular, they may inhibit a vital partof the body’s defenses, “natural killer cells,” whichidentify and destroy malignant cells. However, this is along process and may never occur. Mesothelial cells areconstantly dividing, like all cells in the body. Mutationsare a normal part of the process. One expert testifiedthat incorrect cell copying can take place 5000 timesper day. The body’s repair mechanisms are quick tocorrect and abort mutations. Even if there are

mutations, the incorrect copy may not be able tosurvive; the mutation may make no difference; it mayimprove the cell; or the mutated cell could survive anditself divide, passing on the alterations, and eventuallyafter many generations and additional mutations,creating a malignant cell.

The experts testified that there are six or sevengenetic alterations, which, when they are all in place,can lead to a malignant cell. Among the necessary alter-ations is the availability of the cells own blood supply,obtained by a process called angiogenesis. Over theyears while this process is occurring, there are manyways in which the fibers or the mutating cells may beameliorated. The experts agreed on several ways inwhich the body’s defenses may protect it from damage.There is also an issue, which the experts included aspart of the body’s defenses, as to whether angiogenesiswill take place or will be prevented.

Once the cell has acquired a “full house” of thenecessary six or seven mutations, and has evaded all ofthe body’s defenses, then it can be described as a malig-nant cell and begins a process of uncontrolled growth.The biochemical experts, however, concluded thatmany of the “full house” cells with malignancies mayfail to grow into tumors. The experts agreed that thecells can still be at risk from natural killer cells. In addi-tion, given the long period of time before diagnos-ability, either the mutation period lasts a very long timeor their are long periods of dormancy, or both.

The court noted that until recently there was noappreciation of the importance of angiogenesis, theprocess by which malignant cells obtain their ownblood supply. This is fundamental to continued growth.Once angiogenesis has occurred, there is no restrictionon continued growth. The experts thought it was prob-able that this occurs somewhere between one millionand one billion cells. The tumor becomes large enoughto cause symptoms at one billion to one trillion cells.