“Sky’s the limit!”

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

“Sky’s the limit!”

*

*New commercial lead contacts?*New inquiries?*New deals?*Pay attention to “hearing” & “seeing” more opportunities for commercial business?

*

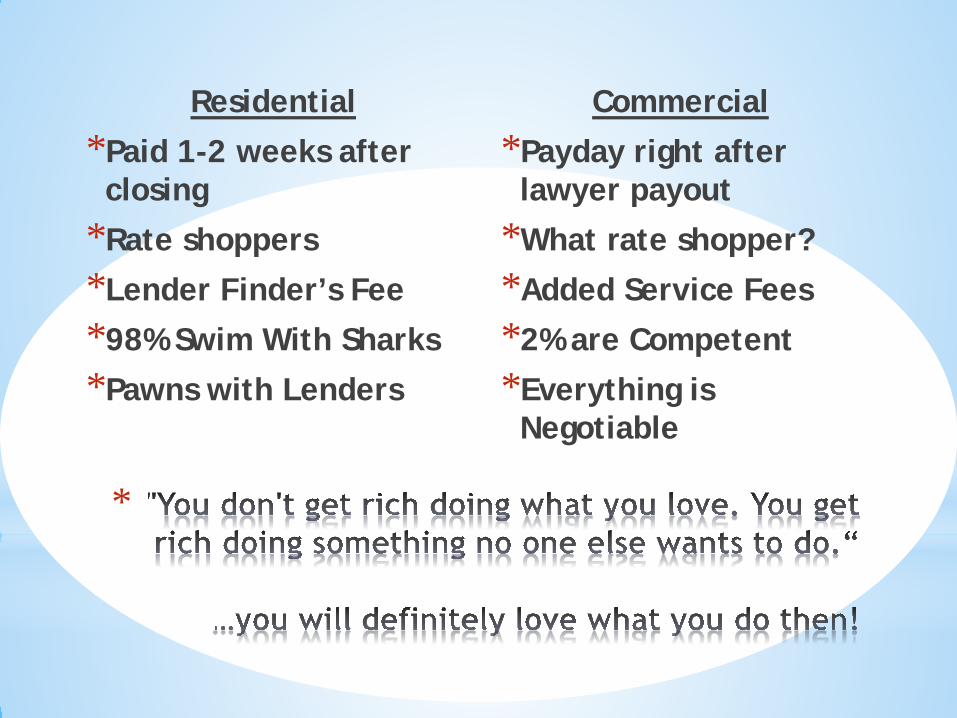

Residential

*Paid 1-2 weeks after closing

*Rate shoppers

*Lender Finder’s Fee

*98% Swim With Sharks

*Pawns with Lenders

Commercial

*Payday right after lawyer payout

*What rate shopper?

*Added Service Fees

*2% are Competent

*Everything is Negotiable

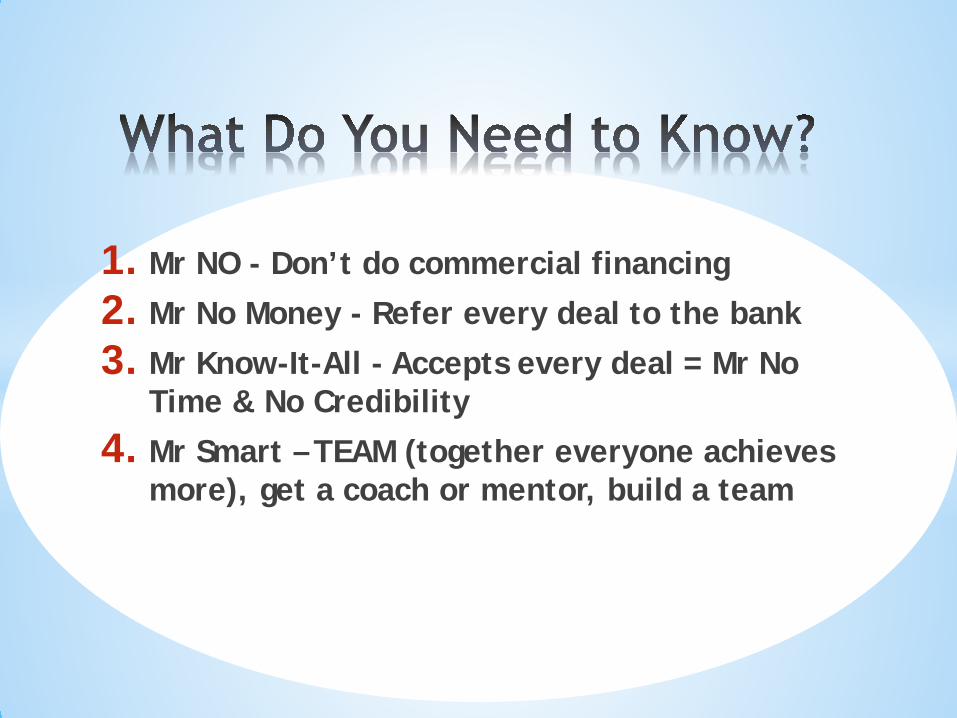

1. Mr NO - Don’t do commercial financing

2. Mr No Money - Refer every deal to the bank

3. Mr Know-It-All - Accepts every deal = Mr No Time & No Credibility

4. Mr Smart – TEAM (together everyone achieves more), get a coach or mentor, build a team

*Future intentions (timeline?)

*Best use of property currently

*Reasonableness of property

*Details of leases compared to rent rolls

*DCR calculations vs class of financing (1,2 or 3)

*Term & amortization client request?

*Future ETO?

*Lithmus test (yay or nay?)

*Resume and background (ALL)*Industry experience, how to mitigate lack of?

*Upfront Expectations – FEES*Needs to Know Basis – Discuss what to the lender?

*Mortgage application versus Personal Net Worth (All Assets)

* Sales price / Cap-Rate* Pay attention to age of property – REL* CMHC Multi-Unit Financing (min $400K+)* Proof of down payment source upfront (reliant on sales of other property?)

* Pursue or Cease & Desist?

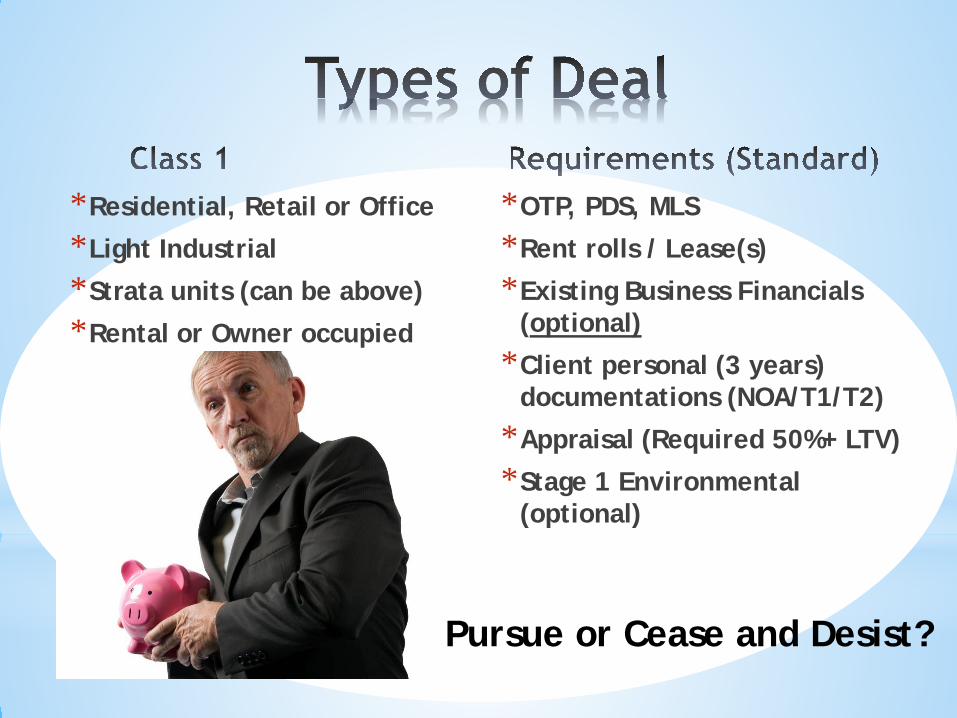

*OTP, PDS, MLS

*Rent rolls / Lease(s)

*Existing Business Financials (optional)

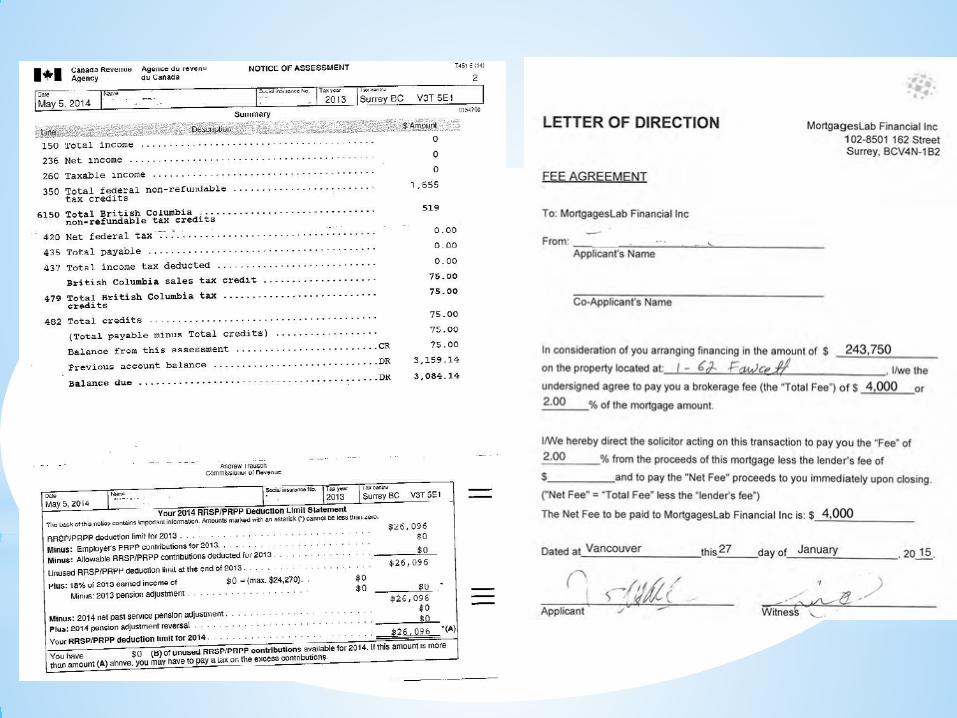

*Client personal (3 years) documentations (NOA/T1/T2)

*Appraisal (Required 50%+ LTV)

*Stage 1 Environmental (optional)

*Residential, Retail or Office

*Light Industrial

*Strata units (can be above)

*Rental or Owner occupied

Pursue or Cease and Desist?

*OTP, PDS, MLS

*Rent rolls / Lease(s)

*3 Years Business Financials

*NTR -> Review Engagement

*Standard client personal documentations (NOA/T1/T2)

*Appraisal (Mandatory)

*Stage 1 Environmental (Mandatory)

*Medium – Heavy Industrial

*Pub / Liquor store

*Non traditional /non conforming

*Farms & Agricultural

Pursue or Cease and Desist?

*OTP & Approved Lease

*3 Years Financials

*Review Engagement

*Standard client personal documentations (NOA/T1/T2)

*Business Plan & Proforma

*25-50% Success Rate

*Business with NO building*Gentleman’s / Drinking Clubs*Gambling establishments*Medicinal or Herbal Farm*Shareholder buyout*Expansion loan*Leasing (Equipment/Vehicle)

Pursue or Cease and Desist?

*Prepare a detailed recommendation to the lender (Executive summary)

*Research most receptive lenders*Collect retainer fee (refundable) or non-refundable commitment fee

*Broker mandate/agreement signed

*Qualify client’s type of required financing –O/O or rental? Type 1, Type 2 (SBL) or Type 3 (BDC/FC/Private)

*Relationship with lender is critical!

*% Sector on books change month to month

*Pricing and fees varies from 3 managers w/ same lender!

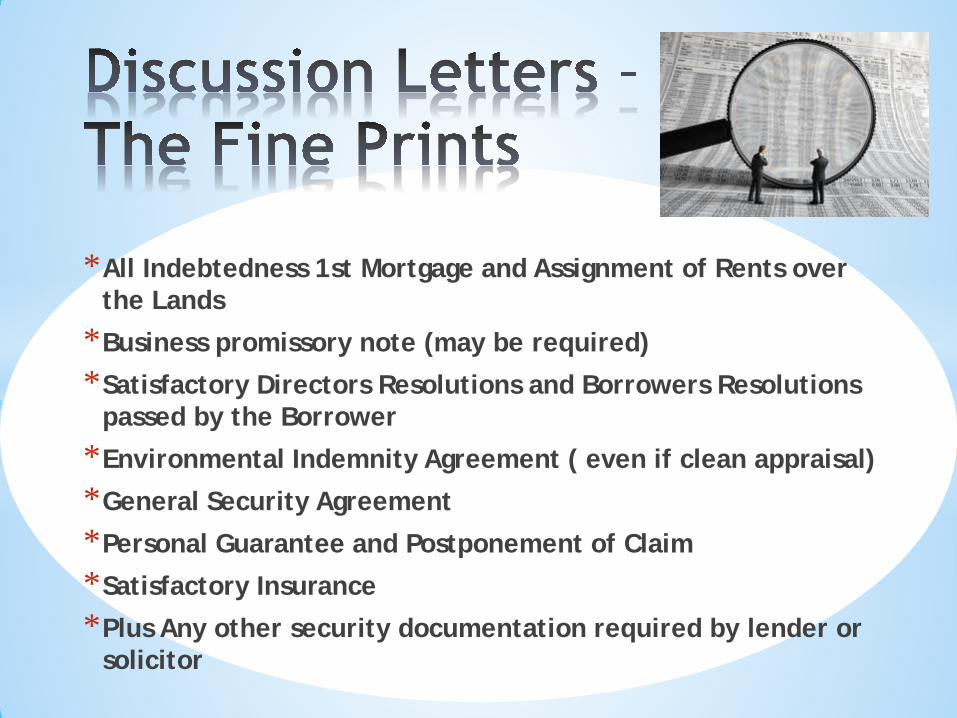

*All Indebtedness 1st Mortgage and Assignment of Rents over the Lands

*Business promissory note (may be required)

*Satisfactory Directors Resolutions and Borrowers Resolutions passed by the Borrower

*Environmental Indemnity Agreement ( even if clean appraisal)

*General Security Agreement

*Personal Guarantee and Postponement of Claim

*Satisfactory Insurance

*Plus Any other security documentation required by lender or solicitor

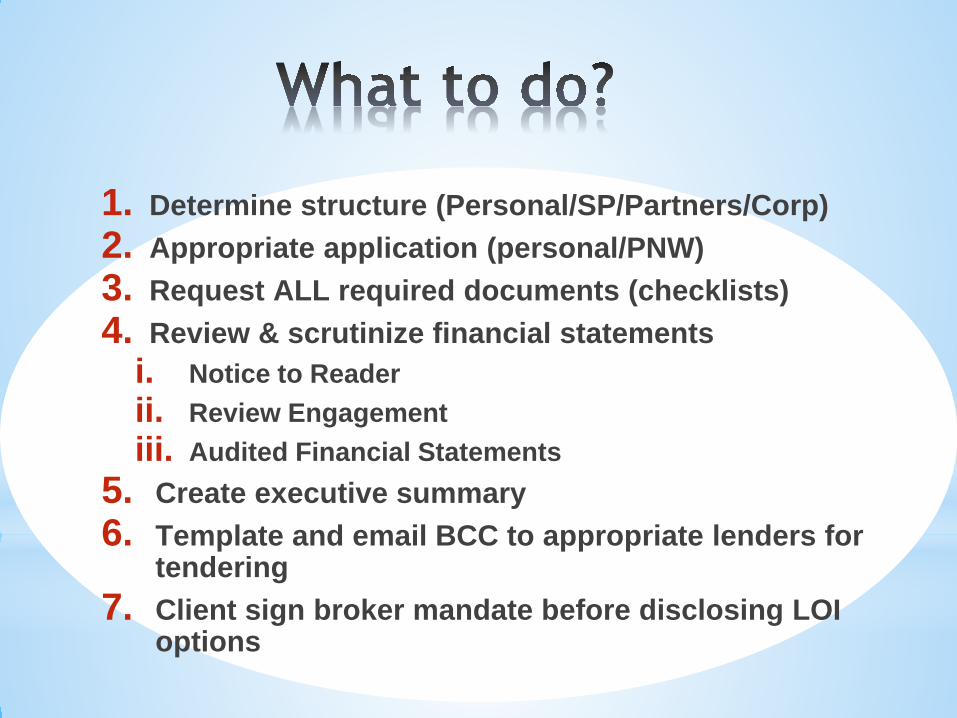

1. Determine structure (Personal/SP/Partners/Corp)2. Appropriate application (personal/PNW)3. Request ALL required documents (checklists)4. Review & scrutinize financial statements

i. Notice to Readerii. Review Engagementiii. Audited Financial Statements

5. Create executive summary6. Template and email BCC to appropriate lenders for

tendering7. Client sign broker mandate before disclosing LOI

options

1. Client Profile:History and experience (resume) of all key applicant(s)SP or Company structure ownershipFinancial history and/or projections

2. Purpose of Loan:Reason for loan makes sense with client profile?Property Details: MLS/PDS/Purchase AgreementRent rolls / Lease agreements / Financials

3. Loan Request:DCR calculations /mitigate shortfallsRequested terms, amortizations Justifications – why 25 years, VRM, Fix

4. Challenges (on this deal):Soil contaminationDerogatory items/issue on credit bureauOffer solutions or suggest remedyCharts, Pro-Forma, Projections

5. Summary / Recommendation:Suggest to waive or make exceptions: appraisal/phase1Client is currently a client at your bankCompetitive situation (client has approach other banks)Client is a sophisticated investor, high net worthClient has large investments consider moving overJustifications for any points that require mitigations

6. Attachments – itemized all attachments

670 & 635 Beacon score$60K & 0K income / $35K RRSPHusband & wife owns residenceProperty valued $1.3M+Owes $761K - $3413 mortgage/monthMatures June 2016 @ RBC 2.99%They also own restaurant (15 years)Owns property restaurant operates in (personal name)Property valued $2.725MOwes $300K – matures June 2017 @ HSBC P+2.25%

Client: 64 years old, semi-retired. Sold his primary residence in 2013 to free up capital to invest in other business and cash flowing properties, has over $100K savings set aside for this purchase.

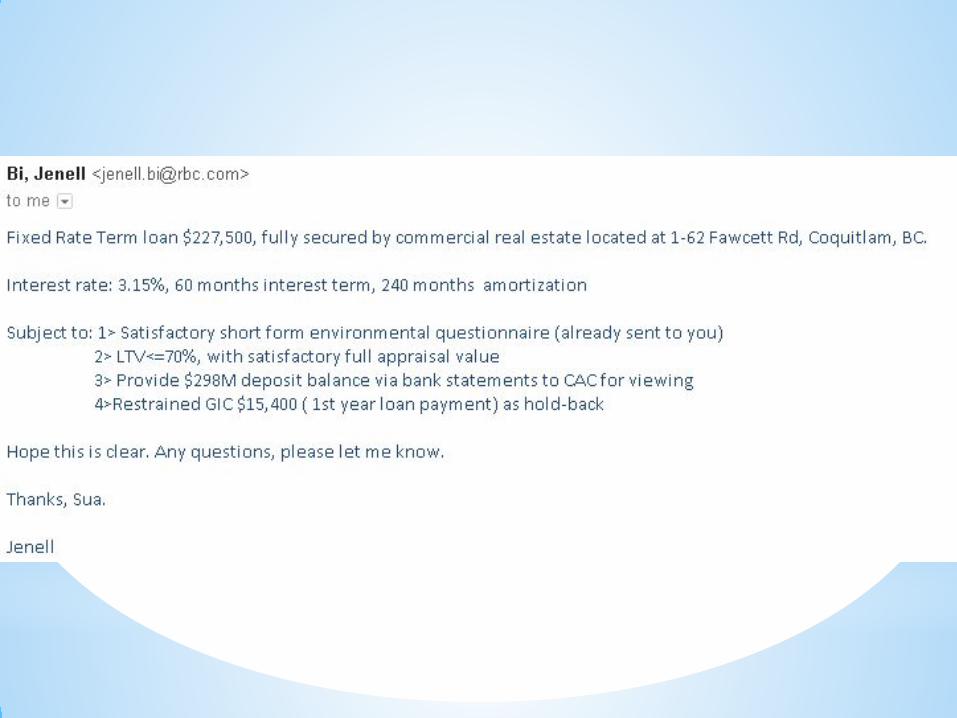

Loan Amount Request: $243,750 @ 75% LTV

He has virtually no debt and only has few late payments due to business challenges he had in his landscaping business in 2013. 2011 late payments were from business trips oversea.

Property: $325,000 agreed purchase price. Industrial with office and retail front in good location. Subject property is currently vacant but has potential parties interested in renting it out after TI's are completed.

Current market rents/gross lease in this strata varies from $1.50 to $1.70 per square foot. Subject unit is 2434 sq.ft. and should easily debt service. Hold-back or reserve can be requested until intent to lease becomes full contract. Estimate rent of $3500 is what client asking from interested parties.2013 depreciation report is also available.

Challenge: 2013 had no income declared, he lives off of his rental income previously and landscaping business that he had sold off at end of 2012 or early 2013.Other than his lack of income from 2013, he is a great potential client for you…

Ingredients Required to Receive What You Ask:

1.Trust2.Value3.Likeability

“Knowing others is wisdom, knowing yourself is enlightment,” Lao Tzu

*Convey who’s “best interest” for the client by “hiring you” rather than go to the bank?

*What difference is there if client walks in himself? (Back and forth trips – require additional docs etc)

*Sell Benefits – save money (re-use appraisals with many lenders), save credit “hits”, integrity

*Can you negotiate the rates or fees? Hidden fees? (ie. I received 3 different quotes from same lender)

*Sell yourself – I save you time & money on lawyers, property appraisers, environmental appraisers

*Sell access your additional network & 7 days a week + outside banking hours, advisory team

*Has process been explained clearly to the client(s)?

*Why are the fees charged? Acceptance?

*What is the timeline? Consistent on OTP?

*Who does what?

*When and how?

Easy as 3.14159…

The Secret to Success isn’t Knowing.

The Secret is DOING!

* Find a mentor* Refer or co-broker to specialized commercial mortgage broker

* Start small and simple* Be prepared to learn a lot more* Be prepared to get paid A LOT more!

Mentorship: The 5 Powerful P’s

• Prospect & Partner Presentations • Persuasive Client Interview• Precondition Client Buy-In • Proficient With Papers (Lease,

Financials, Appraisal, Phase 1-3)• Perfecting Lender Relationship

Enroll in an Ambassador Coaching program today!

Related Documents