IN ASSOCIATION WITH COMMERCIAL ENGINES 2011 SPECIAL REPORT CURRENT THINKING, STRATEGIC ANALYSIS & MARKET EVOLUTION

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

IN ASSOCIATION WITH

COMMERCIAL ENGINES2011

SPECIAL REPORT

CURRENT THINKING, STRATEGIC ANALYSIS & MARKET EVOLUTION

To see where a new engine will take you,

look at where it came from.

History alone makes the LEAP engine the right choice for the A320neo. No other engine manufacturer equals the record of CFM* in developing and seamlessly introducing technology and innovation. Or matches its legendary reliability. The LEAP engine is the next generation. Offering 15% lower

fuel consumption and 15% lower CO2 emissions than the engines it will replace. See history repeat itself. Visit www.cfm56.com/leap

*CFM, LEAP and the CFM logo are all trademarks of CFM International, a 50/50 joint company of Snecma and General Electric Co.

LEAP

Commercial Engines 2011 | Flightglobal Insight | 3

FOREWORD

FLIGHTGLOBAL INSIGHTTREVOR MOUNTFORD: MANAGER

ANTOINE FAFARD: ANALYST

AIRLINE BUSINESSMAX KINGSLEY-JONES: EDITOR

FOREWORD2011 promises to be a landmark year for commercial engines across both single-aisle and widebody sectors as market bat-tles play out and development intensifies.

Pratt & Whitney has already gained significant traction on Airbus’s A320neo, with its geared turbofan winning the early engine selection deals and being assigned lead powerplant for the re-engined family. But CFM International – which is market leader in the single-aisle sector – is more than capa-ble of launching a major counter-attack in the sales war as the year progresses.

In the widebody sector, the latest all-new civil engine from General Electric should finally make its service debut on the Boeing 787 and 747-8. While the GEnx is the only engine option on the new 747, it is competing with the Rolls-Royce Trent 1000 on the Dreamliner where it currently has the upper hand in the market share battle (see page 9).

But before the GEnx makes its debut, the 787 should be pow-ered into service by the R-R Trent 1000 as it is the lead pow-erplant on the twinjet programme. Few will need reminding that this first delivery to launch customer All Nippon Airways should have occurred more than three years ago. It is now finally expected to take place before the end of the summer.Over in Toulouse Airbus is preparing to flight-test another new Rolls engine, the Trent XWB for the A350 XWB. Before the engine powers the A350 on its maiden flight next year, it will undertake around 140h of flight-tests on Airbus’s A380 devel-opment hack, beginning later this year.

Meanwhile at the other end of the airliner scale, P&W is about to begin flight-testing the initial PW1500G version of the GTF, which is due to power Bombardier’s 110-145 seat CSeries on its maiden sortie next year ahead of service entry in 2013. In what will be a rapid development programme, the engine maker will quickly evolve the smaller, lower-thrust PW1200G version for the 90-100 seat Mitsubishi MRJ regional jet and the larger, more powerful PW1100G for the A320neo and a similar version, dubbed the PW1400G, for Russia’s MS-21 mainline narrowbody.

CFM International, working to overhaul its rival’s head start on the A320neo, has its own development programme run-ning for the Leap-X advanced turbofan which is the alterna-tive offering on the A320neo and is the sole western engine selected for China’s Comac C919 mainline jet. The Leap-X

is due to begin testing in 2013 on a newly acquired ex-JAL Boeing 747-400 before its debut on the A320neo in around 2016.

Finally, this year has marked the debut for an all-new turbofan developed by CFM partner Snecma in association with Rus-sian engine maker NPO Saturn. The 13,500-17,500lb thrust SaM146 turbofan entered service on the 100-seat Sukhoi Superjet in April 2011 with Armavia, and is also now being deployed by launch operator Aeroflot on its Russian domestic network.

Airb

us

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 5

ENGINE MARKET SHARE

Power players 7

OPERATORS & REGIONS

Share of engines for leading operators & regions 10

NEW ENTRANTS

Bombardier, Comac & Irkut 13

COMMERCIAL ENGINES

CFM International 15

Engine Alliance 17

General Electric 18

International Aero Engines 20

Pratt & Whitney 21

Rolls-Royce 23

AT A GLANCE

Overview of commercial engines currently in operation 25

CONTENTS

TO FIND OUT MORE ABOUT FLIGHTGLOBAL INSIGHT AND REPORT SPONSORSHIP OPPORTUNITIES, CONTACT:

Flightglobal InsightQuadrant House, The Quadrant Sutton, Surrey, SM2 5AS, UKTel: + 44 (20) 8652 8724Email: [email protected]: www.flightglobal.com/insight

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 7

ENGINE MARKET SHAREPower players

ENGINE MANUFACTURER RANKING

2010 deliveries Backlog*

Rank Manufacturer Units Share Units Share1 CFM International 1,162 60.6% 6,038 42.0%2 IAE 336 17.5% 2,002 13.9%3 General Electric 188 9.8% 1,734 12.1%4 Rolls-Royce 154 8.0% 2,392 16.6%5 Engine Alliance 44 2.3% 428 3.0%6 Pratt & Whitney 32 1.7% 146 1.0%

Undecided – – 1,648 11.5%

TOTAL DELIVERIES 1,916 14,388NOTES: *At 31 December 2010. Data for installed engines based on Airbus/Boeing types. Excludes corporate and military operators. Source: Flightglobal Insight analysis using ACAS database.

Data at 31 December 2010 (excludes corporate and military operators and parked aircraft) SOURCE: Flightglobal Insight analysis using ACAS database

Units x1,000

EngineAlliance

GeneralElectric

Pratt &Whitney

InternationalAero Engines

Rolls-RoyceCFMInternational

Airbus Total = 5,730

Boeing Total = 10,045

Total fleet = 15,775

0

1

2

3

4

5

6

7

8

2,636

4,839

441

1,619

382

2,461

491

1,03591

1,761Airbus

19

AIRBUS/BOEING FLEET BY ENGINE MANUFACTURER

Data for installed engines based on Airbus/Boeing types*At 31 December 2010Excludes corporate and military operatorsSOURCE: Flightglobal Insight analysis using ACAS database

Total deliveries = 1,916 engines Total backlog = 14,388 engines

CFM InternationalInternational Aero Engines

General ElectricRolls-Royce

Engine AlliancePratt & Whitney

Undecided

2010 deliveries Backlog*

42%60.6%

17.5% 13.9%12.1%

16.6%

9.8%

8% 2.3% 1.7%

3%

1% 11.5%

ENGINE MANUFACTURER MARKET SHARE

Analysing data from the Flightglobal ACAS database, this section features the market share battles playing out among the engine makers for commercial Airbus and Boeing types. A combined total of 1,916 engines were installed on delivered mainline jet aircraft during 2010 while the engine order backlog stood at 14,388 on 31 December of that year.

CFM International, the 50-50 joint venture between General Electric and Snecma, remains the dominant player in the jet engine market, delivering over 60% of all the powerplants shipped on mainline jet airliners in 2010. CFM is also associated to 42% of the order backlog at the end of 2010, representing more than 6,000 engines.

International Aero Engines (IAE) ranks second in the 2010 commercial deliveries with 336 aircraft (17.5%), with Rolls-Royce placed second in the order backlog overview. The UK engine maker has a strong position on the A330 in market share terms and also benefits from being the only engine currently available on the A350 XWB.

Exclusive widebody powerplant supplier General Electric delivered a total of 188 engines during 2010. Its backlog stood at 1,734 at the end of the year.

The Airbus and Boeing commercial fleet by engine manufacturer chart shows that CFM International stands out in the active fleet comparison. CFM powers a total of 7,475 aircraft (2,636 for Airbus and 4,839 for Boeing).

The CFM56 is the only engine provided on the Boeing 737 and is an engine option on the Airbus A320 family aircraft. The A319, A320 and A321 can also be powered by the IAE V2500 while the A318

COMMERCIAL ENGINES 2011

8 | Flightglobal Insight | Commercial Engines 2011

A330 ENGINE MANUFACTURER SHARE

2010 deliveries Backlog*

Manufacturer Units Share Units ShareGeneral Electric 11 13.1% 17 5.0%Pratt & Whitney 14 16.7% 65 19.0%Rolls-Royce 59 70.2% 224 65.3%Undecided – – 37 10.8%

TOTAL 84 343NOTES: *At 31 December 2010. Excludes corporate and military operators. Source: Flightglobal Insight analysis using ACAS database.

A380 ENGINE MANUFACTURER SHARE

2010 deliveries Backlog*

Manufacturer Units Share Units ShareEngine Alliance 11 61.1% 107 55.7%Rolls-Royce 7 38.9% 67 34.9%Undecided – – 18 9.4%

TOTAL 18 192NOTES: *At 31 December 2010. Excludes corporate and military operators. Source: Flightglobal Insight analysis using ACAS database.

767 ENGINE MANUFACTURER SHARE

2010 deliveries Backlog*

Manufacturer Units Share Units ShareGeneral Electric 11 91.7% 37 74.0%Pratt & Whitney 1 8.3% 6 12.0%Undecided – – 7 14.0%

TOTAL 12 50NOTES: *At 31 December 2010. Excludes corporate and military operators. Source: Flightglobal Insight analysis using ACAS database.

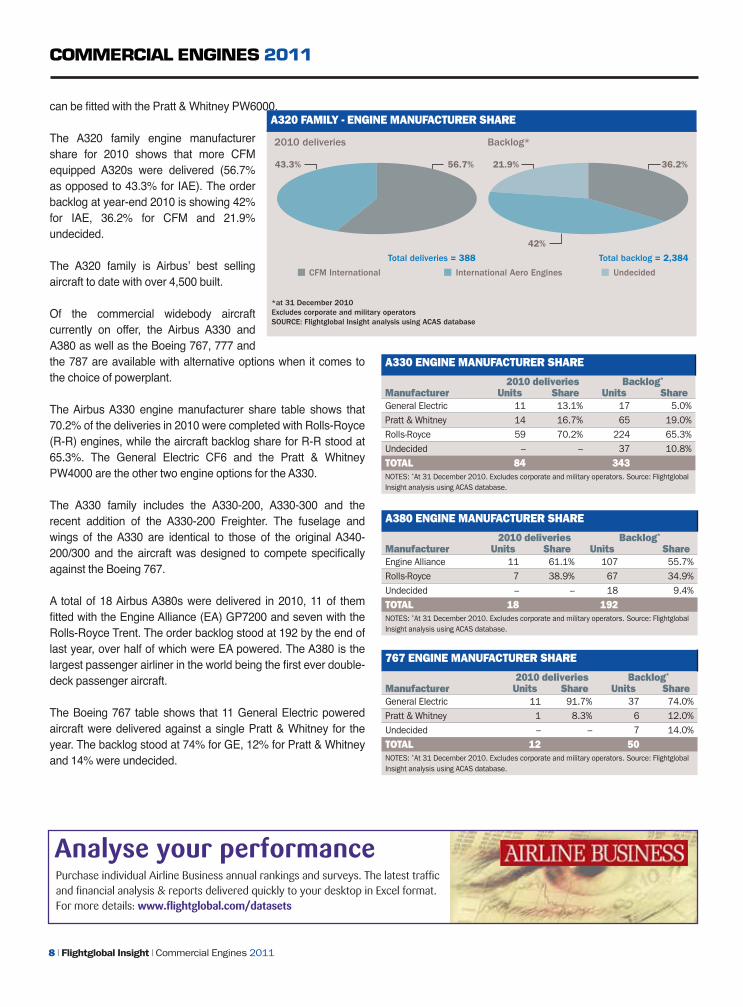

can be fitted with the Pratt & Whitney PW6000.

The A320 family engine manufacturer share for 2010 shows that more CFM equipped A320s were delivered (56.7% as opposed to 43.3% for IAE). The order backlog at year-end 2010 is showing 42% for IAE, 36.2% for CFM and 21.9% undecided.

The A320 family is Airbus’ best selling aircraft to date with over 4,500 built.

Of the commercial widebody aircraft currently on offer, the Airbus A330 and A380 as well as the Boeing 767, 777 and the 787 are available with alternative options when it comes to the choice of powerplant.

The Airbus A330 engine manufacturer share table shows that 70.2% of the deliveries in 2010 were completed with Rolls-Royce (R-R) engines, while the aircraft backlog share for R-R stood at 65.3%. The General Electric CF6 and the Pratt & Whitney PW4000 are the other two engine options for the A330.

The A330 family includes the A330-200, A330-300 and the recent addition of the A330-200 Freighter. The fuselage and wings of the A330 are identical to those of the original A340-200/300 and the aircraft was designed to compete specifically against the Boeing 767.

A total of 18 Airbus A380s were delivered in 2010, 11 of them fitted with the Engine Alliance (EA) GP7200 and seven with the Rolls-Royce Trent. The order backlog stood at 192 by the end of last year, over half of which were EA powered. The A380 is the largest passenger airliner in the world being the first ever double-deck passenger aircraft.

The Boeing 767 table shows that 11 General Electric powered aircraft were delivered against a single Pratt & Whitney for the year. The backlog stood at 74% for GE, 12% for Pratt & Whitney and 14% were undecided.

*at 31 December 2010 Excludes corporate and military operators SOURCE: Flightglobal Insight analysis using ACAS database

Total deliveries = 388 Total backlog = 2,384

CFM International

2010 deliveries Backlog*

International Aero Engines Undecided

36.2%

42%

21.9%56.7%43.3%

A320 FAMILY - ENGINE MANUFACTURER SHARE

Analyse your performancePurchase individual Airline Business annual rankings and surveys. The latest trafficand financial analysis & reports delivered quickly to your desktop in Excel format.For more details: www.flightglobal.com/datasets

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 9

Data at 31 December 2010 (excludes corporate operators)SOURCE: Flightglobal Insight analysis using ACAS database

Total backlog = 846

UndisclosedGeneral ElectricRolls-Royce

44.7%25.8%

29.6%

Market share

= 234 = 1,02243.4%

54% 52.3%

35.1%

2.6% 12.4% 0.2%

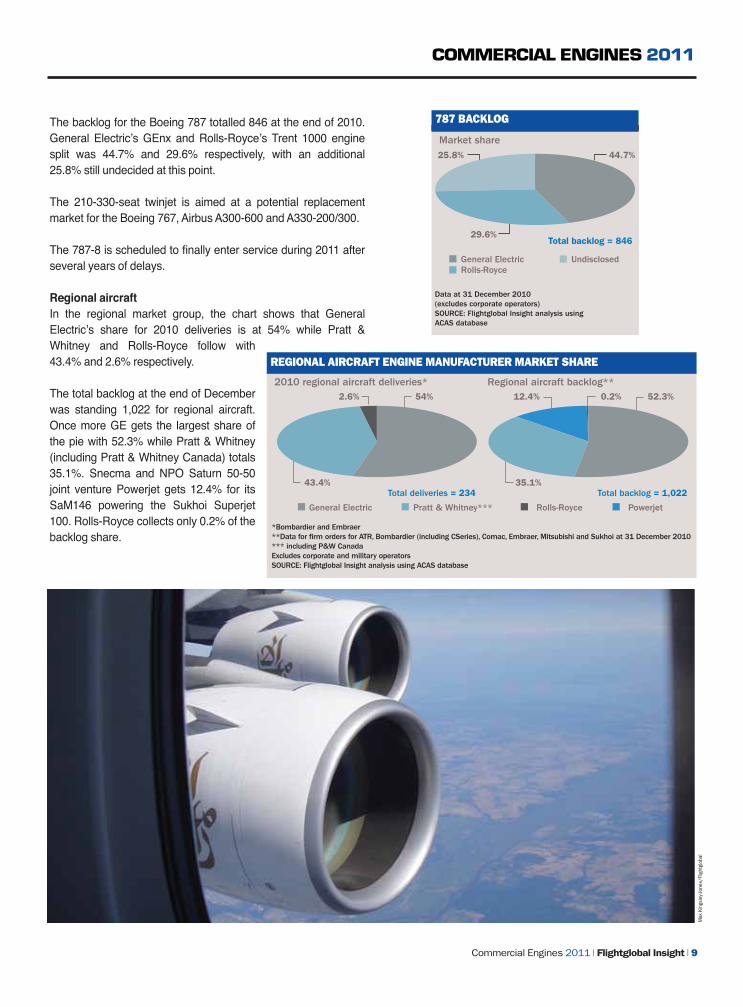

787 BACKLOGThe backlog for the Boeing 787 totalled 846 at the end of 2010. General Electric’s GEnx and Rolls-Royce’s Trent 1000 engine split was 44.7% and 29.6% respectively, with an additional 25.8% still undecided at this point.

The 210-330-seat twinjet is aimed at a potential replacement market for the Boeing 767, Airbus A300-600 and A330-200/300.

The 787-8 is scheduled to finally enter service during 2011 after several years of delays.

Regional aircraftIn the regional market group, the chart shows that General Electric’s share for 2010 deliveries is at 54% while Pratt & Whitney and Rolls-Royce follow with 43.4% and 2.6% respectively.

The total backlog at the end of December was standing 1,022 for regional aircraft. Once more GE gets the largest share of the pie with 52.3% while Pratt & Whitney (including Pratt & Whitney Canada) totals 35.1%. Snecma and NPO Saturn 50-50 joint venture Powerjet gets 12.4% for its SaM146 powering the Sukhoi Superjet 100. Rolls-Royce collects only 0.2% of the backlog share.

Max

Kin

gsle

y-Jon

es/F

light

glob

al

REGIONAL AIRCRAFT ENGINE MANUFACTURER MARKET SHARE

COMMERCIAL ENGINES 2011

10 | Flightglobal Insight | Commercial Engines 2011

OPERATORS & REGIONSShare of engines by leading operators & regions

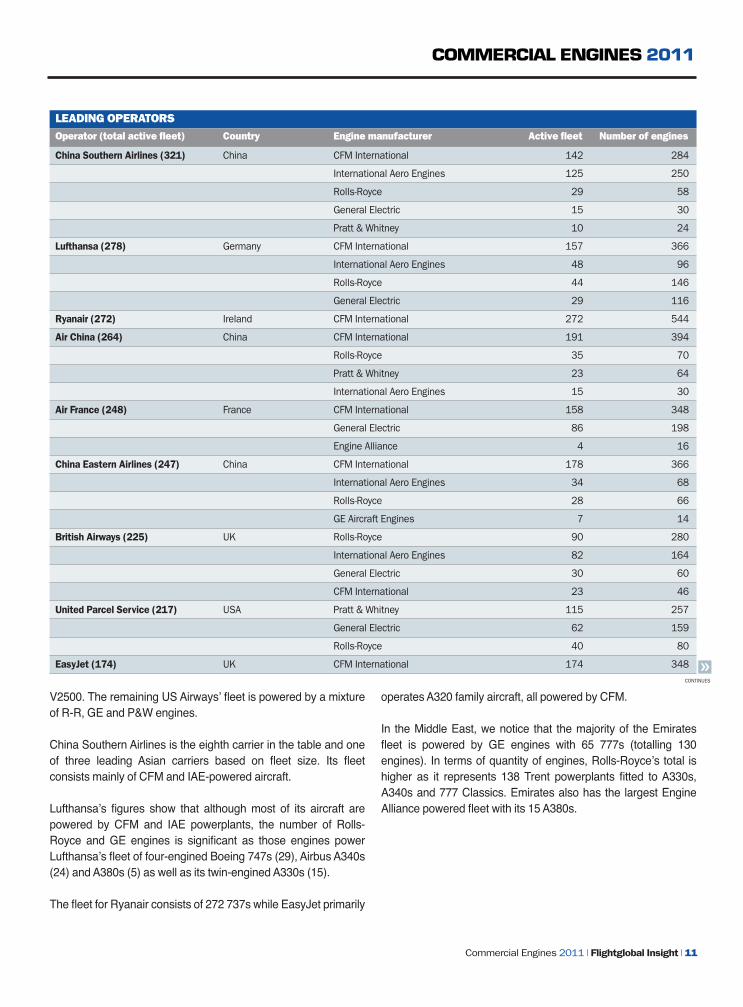

LEADING OPERATORSOperator (total active fleet) Country Engine manufacturer Active fleet Number of engines

Delta Air Lines (730) USA Pratt & Whitney 419 870

CFM International 209 418

General Electric 70 140

International Aero Engines 24 48

Rolls-Royce 8 16

American Airlines (610) USA Pratt & Whitney 214 428

Rolls-Royce 171 342

CFM International 152 304

General Electric 73 146

Southwest Airlines (551) USA CFM International 551 1,102

United Airlines (359) USA Pratt & Whitney 207 462

International Aero Engines 152 304

FedEx Express (356) USA General Electric 190 493

Pratt & Whitney 142 375

Rolls-Royce 24 48

Continental Airlines (338) USA CFM International 229 458

Rolls-Royce 61 122

General Electric 48 96

US Airways (326) USA CFM International 169 338

International Aero Engines 106 212

Rolls-Royce 32 64

General Electric 10 20

Pratt & Whitney 9 18

The leading operators table lists the world’s leading 20 airlines and cargo carriers by fleet size. As a regional breakdown, nine of the 20 carriers are based in North America, five in Europe, four in Asia, a single airline in South America and a further one in the Middle East.

Delta Air Lines appears at the top of the table with a total fleet of 730 in-service aircraft. A total of 419 aircraft are powered by Pratt & Whitney engines which represents 870 engines. CFM-powered aircraft also represent a significant share of the fleet with a combined total of 209 Boeing 737s and Airbus A320 family aircraft.

American Airlines is next in the list with a fleet of 610 active aircraft. Pratt & Whitney is also the leading engine supplier for

their fleet of 214 MD-80s which are all powered by the JT8D.

The Southwest Airlines 737 fleet consists of 551 CFM56-fitted aircraft (prior to the acquisition of AirTran), while the United Airlines mixed fleet of 359 aircraft is powered by either Pratt & Whitney or IAE powerplants.

The majority of cargo operator FedEx Express’s fleet is powered by GE and Pratt & Whitney engines, but the carrier also operates 24 Boeing 757s powered by the Rolls-Royce RB211.

Continental Airlines’ fleet of 229 737s makes up CFM’s majority market share. followed by Rolls-Royce and GE. US Airways’ fleet is also dominated by CFM engines for their 737 and A320 family fleet. But an additional 106 A320s are powered by the IAE

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 11

LEADING OPERATORSOperator (total active fleet) Country Engine manufacturer Active fleet Number of engines

China Southern Airlines (321) China CFM International 142 284

International Aero Engines 125 250

Rolls-Royce 29 58

General Electric 15 30

Pratt & Whitney 10 24

Lufthansa (278) Germany CFM International 157 366

International Aero Engines 48 96

Rolls-Royce 44 146

General Electric 29 116

Ryanair (272) Ireland CFM International 272 544

Air China (264) China CFM International 191 394

Rolls-Royce 35 70

Pratt & Whitney 23 64

International Aero Engines 15 30

Air France (248) France CFM International 158 348

General Electric 86 198

Engine Alliance 4 16

China Eastern Airlines (247) China CFM International 178 366

International Aero Engines 34 68

Rolls-Royce 28 66

GE Aircraft Engines 7 14

British Airways (225) UK Rolls-Royce 90 280

International Aero Engines 82 164

General Electric 30 60

CFM International 23 46

United Parcel Service (217) USA Pratt & Whitney 115 257

General Electric 62 159

Rolls-Royce 40 80

EasyJet (174) UK CFM International 174 348

V2500. The remaining US Airways’ fleet is powered by a mixture of R-R, GE and P&W engines.

China Southern Airlines is the eighth carrier in the table and one of three leading Asian carriers based on fleet size. Its fleet consists mainly of CFM and IAE-powered aircraft.

Lufthansa’s figures show that although most of its aircraft are powered by CFM and IAE powerplants, the number of Rolls-Royce and GE engines is significant as those engines power Lufthansa’s fleet of four-engined Boeing 747s (29), Airbus A340s (24) and A380s (5) as well as its twin-engined A330s (15).

The fleet for Ryanair consists of 272 737s while EasyJet primarily

operates A320 family aircraft, all powered by CFM.

In the Middle East, we notice that the majority of the Emirates fleet is powered by GE engines with 65 777s (totalling 130 engines). In terms of quantity of engines, Rolls-Royce’s total is higher as it represents 138 Trent powerplants fitted to A330s, A340s and 777 Classics. Emirates also has the largest Engine Alliance powered fleet with its 15 A380s.

CONTINUES

COMMERCIAL ENGINES 2011

12 | Flightglobal Insight | Commercial Engines 2011

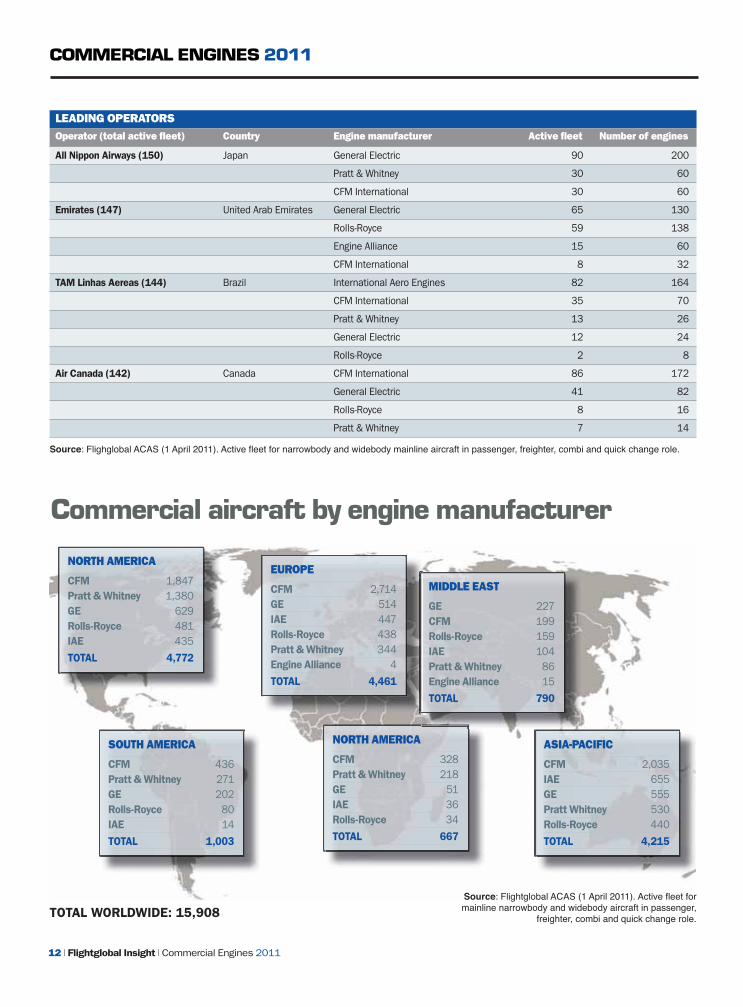

Commercial aircraft by engine manufacturer

EUROPE

CFM 2,714GE 514IAE 447Rolls-Royce 438Pratt & Whitney 344Engine Alliance 4

TOTAL 4,461

Source: Flightglobal ACAS (1 April 2011). Active fleet for mainline narrowbody and widebody aircraft in passenger,

freighter, combi and quick change role.

NORTH AMERICA

CFM 1,847Pratt & Whitney 1,380GE 629Rolls-Royce 481IAE 435

TOTAL 4,772

SOUTH AMERICA

CFM 436Pratt & Whitney 271GE 202Rolls-Royce 80IAE 14

TOTAL 1,003

NORTH AMERICA

CFM 328Pratt & Whitney 218GE 51IAE 36Rolls-Royce 34

TOTAL 667

ASIA-PACIFIC

CFM 2,035IAE 655GE 555Pratt Whitney 530Rolls-Royce 440

TOTAL 4,215

MIDDLE EAST

GE 227CFM 199Rolls-Royce 159IAE 104Pratt & Whitney 86Engine Alliance 15

TOTAL 790

Source: Flighglobal ACAS (1 April 2011). Active fleet for narrowbody and widebody mainline aircraft in passenger, freighter, combi and quick change role.

LEADING OPERATORSOperator (total active fleet) Country Engine manufacturer Active fleet Number of engines

All Nippon Airways (150) Japan General Electric 90 200

Pratt & Whitney 30 60

CFM International 30 60

Emirates (147) United Arab Emirates General Electric 65 130

Rolls-Royce 59 138

Engine Alliance 15 60

CFM International 8 32

TAM Linhas Aereas (144) Brazil International Aero Engines 82 164

CFM International 35 70

Pratt & Whitney 13 26

General Electric 12 24

Rolls-Royce 2 8

Air Canada (142) Canada CFM International 86 172

General Electric 41 82

Rolls-Royce 8 16

Pratt & Whitney 7 14

TOTAL WORLDWIDE: 15,908

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 13

NEW ENTRANTSBombardier, Comac & Irkut

For airlines in the market for a mainline narrowbody jet, things have suddenly become interesting. In the past year, the choice of suppliers has more than doubled.

Since the demise of McDonnell Douglas and its MD-80/90 line a decade ago after the takeover by Boeing, airlines have had only two doors to knock on when seeking a short-haul airliner in the 110 to 180-seat market. While the regional jet sector has constantly created under the weight of too many suppliers, no-one wanted to brave it in the space above.

Until now, that is. Bombardier, along with aircraft manufac-turers in China and Russia, all have new-generation nar-rowbodies targeted at the mainline sector in development, and all of them have signed up customers. If they beat the odds and keep to schedule, these new jets should become realities over the next three to five years.

Bombardier was the first to step up, with its all-new CSeries powered by Pratt & Whitney’s PW1000G geared turbofan, which was launched in 2008. Despite slow sales – and doubts in some quarters about Bombardier’s ability to go up against the big two – the 110 to 145-seater is already mak-ing its presence felt. Airbus, which launched its A320 New Engine Option (Neo) in December, has publicly stated that a desire to stop the CSeries was one of the criteria that drove the move.

The industry is waiting to see what Boeing does in response to Neo, CSeries and the emerging manufacturers. It has been evaluating a possible re-engining of the 737, but has given strong indications that it will concentrate on developing an all-new single-aisle jet.

Serious ThreatBut while the new Canadian twinjet could be an irritant, it is the “national projects”, as one Boeing executive once described them, coming from Russia and, more sig-nificantly, China, that arguably represent the more serious threat to Airbus and Boe-ing’s equilibrium in the long term.

The two countries’ state-run manufacturers

NEW ENTRANTS: SPECIFICATIONS

Bombardier CSeries Comac C919 Irkut MS-21Seats 110-145 150 150-210Powerplant P&W PW1400G CFM Leap-X P&W PW1500GRange (nm) 2,950 3,000 2,700-2,970First delivery Late 2013 2016 2016Orders 90 100* 180*

*Includes options, MoUs, LoIs etc. Source: Flightglobal/manufacturers.

have adopted advanced engines from Western suppliers as the cornerstone of their plans for clean-sheet new genera-tion single-aisles in the 100 to 200-seat category.

For Russia, this represents possibly a last chance to return to the glory days of high-volume airliner manufacturing of the Soviet era, whereas for China the endgame is arguably more feasible. That is: to ensure that its local industry rides the wave of its airline boom in the coming years.

As now planned, the two new airliners – Russia’s MS-21 and China’s Comac C919 – are conventional in profile but will incorporate advanced materials and new generation en-gines. The MS-21, which is being developed by Irkut under the umbrella of United Aircraft (UAC), will be powered by a version of P&W’s GTF closely related to the PW1100G under development for the A320neo. Similarly Comac’s new twinjet will use a version of the Neo’s other engine option, the CFM International Leap-X advanced turbofan.

With Airbus now consistently out-delivering Seattle, it is re-markable to consider that it is only in the past decade or so that its production rose consistently beyond one-third of the overall mainline aircraft shipments. It finally broke the 50% share threshold in 2003 – 29 years after it shipped its first A300.

So like the Airbus evolution, the threat from new entrants may be a slow burn, initially denting the full market potential of the established players before they become fully fledged rivals to-wards the middle of the century.

ChinaBetween them, Airbus and Boeing have delivered almost 1,700 airliners into the Chinese market – indeed the former

COMMERCIAL ENGINES 2011

14 | Flightglobal Insight | Commercial Engines 2011

has a final assembly line in the country, which will be produc-ing at least four A320s a month. The two rivals’ combined backlog from Chinese airlines stands at around 670 units – or 10% of their total orderbook, but the C919 threatens to dent their prospects of cleaning up among the airlines from now on.

Comac signalled its intent to grab a share of the business at the Zuhai air show last year when the first C919 custom-ers were announced. These comprised Air China, China Southern Airlines, China Eastern Airlines, Hainan Airlines, Chinese lessor CDB Leasing Company (CLC) and US les-sor GECAS (sister company to GE Aircraft Engines, which is a partner in Leap-X builder CFM International). Between them they signed for 100 orders and options.

In Flightglobal Insight’s recently published Commercial Fleet Forecast (CFF) 2011-2030, which was produced in associa-tion with Achieving the Difference, it predicts demand from China for 3,700 passenger aircraft in the 121- to 200-seat category, covering both replacement and growth require-ments. Of these, it forecasts that more than 20% – or 700 units – will be of Chinese origin.

Like Airbus four decades ago, the new entrants know they need to break into the overseas markets to really enjoy suc-cess, but as Toulouse found out, achieving this is not simply about creating a competitive product.

Sukhoi successThe Sukhoi Superjet regional jet has had some international success, helped by the fact that its Russian builder has tied up with Italy’s Alenia Aeronautica to boost its credibility – and in-service support capability – on the global stage. The company is pitching its 100-seater at Delta Air Lines’ require-ment for up to 200 new narrowbodies, but most observers see this as a very long shot.

Ryanair recently indicated that not only was it now big enough to break the low-cost carriers’ single-type fleet rule but more controversially that it might be interested in the Chinese and Russian types.

But any lower cost of ownership benefit a deal with Comac or Irkut might bring, must be weighed up against several ba-sic risks.

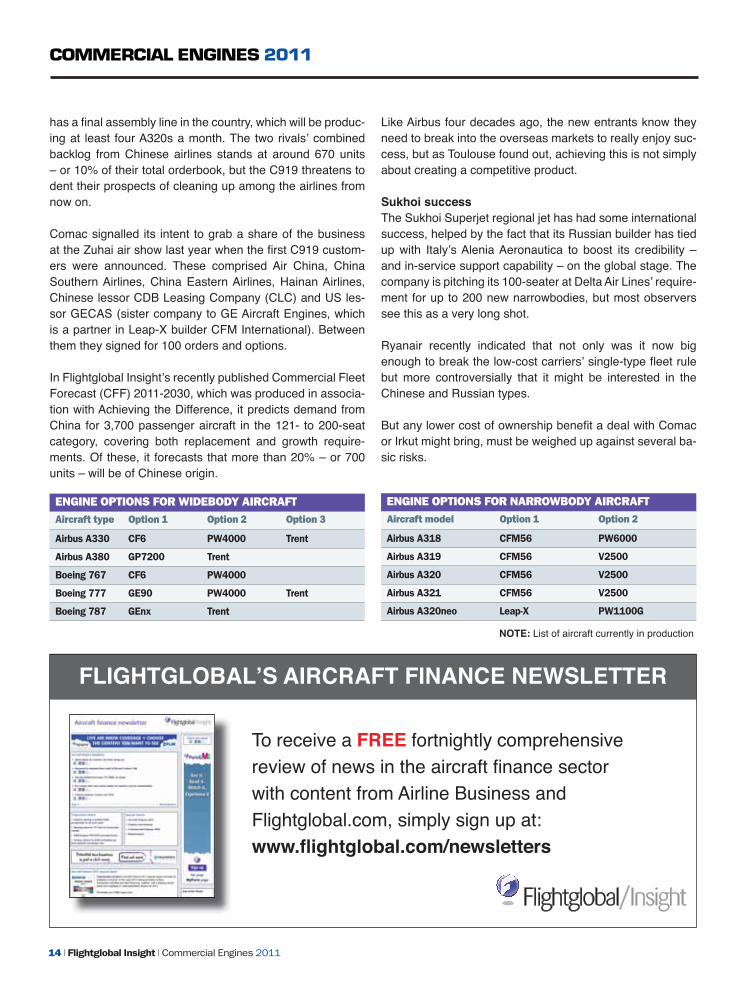

ENGINE OPTIONS FOR WIDEBODY AIRCRAFTAircraft type Option 1 Option 2 Option 3

Airbus A330 CF6 PW4000 Trent

Airbus A380 GP7200 Trent

Boeing 767 CF6 PW4000

Boeing 777 GE90 PW4000 Trent

Boeing 787 GEnx Trent

ENGINE OPTIONS FOR NARROWBODY AIRCRAFTAircraft model Option 1 Option 2

Airbus A318 CFM56 PW6000

Airbus A319 CFM56 V2500

Airbus A320 CFM56 V2500

Airbus A321 CFM56 V2500

Airbus A320neo Leap-X PW1100G

NOTE: List of aircraft currently in production

FLIGHTGLOBAL’S AIRCRAFT FINANCE NEWSLETTER

To receive a FREE fortnightly comprehensive review of news in the aircraft finance sector with content from Airline Business and Flightglobal.com, simply sign up at:www.flightglobal.com/newsletters

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 15

COMMERCIAL ENGINESOverview by manufacturer

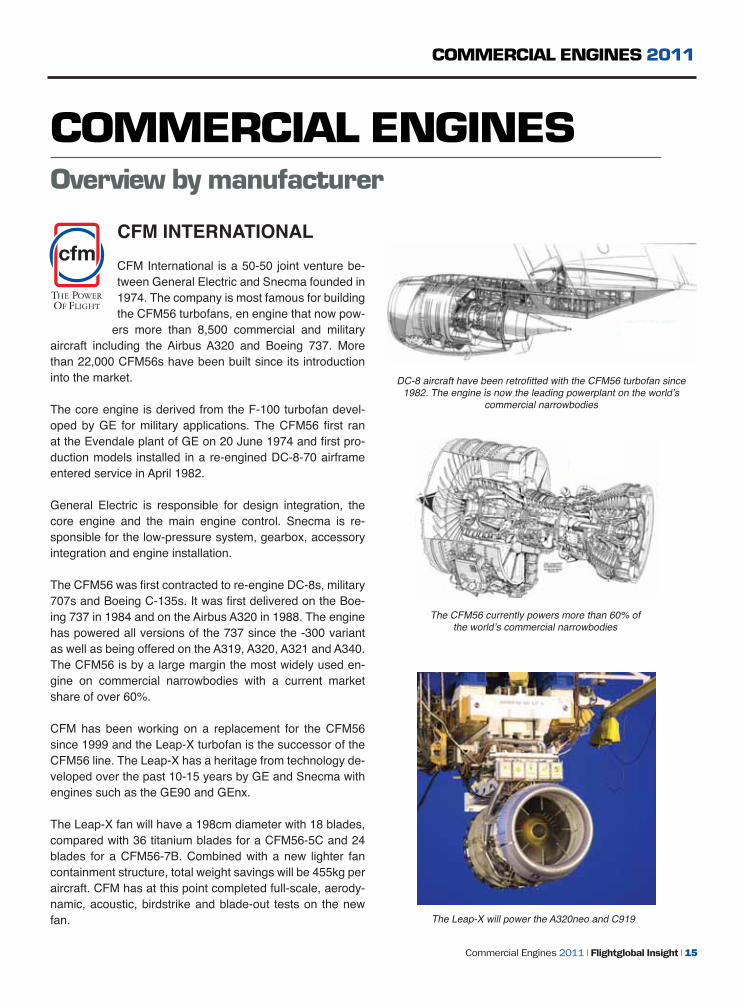

CFM INTERNATIONAL CFM International is a 50-50 joint venture be-tween General Electric and Snecma founded in 1974. The company is most famous for building the CFM56 turbofans, en engine that now pow-

ers more than 8,500 commercial and military aircraft including the Airbus A320 and Boeing 737. More than 22,000 CFM56s have been built since its introduction into the market.

The core engine is derived from the F-100 turbofan devel-oped by GE for military applications. The CFM56 first ran at the Evendale plant of GE on 20 June 1974 and first pro-duction models installed in a re-engined DC-8-70 airframe entered service in April 1982.

General Electric is responsible for design integration, the core engine and the main engine control. Snecma is re-sponsible for the low-pressure system, gearbox, accessory integration and engine installation.

The CFM56 was first contracted to re-engine DC-8s, military 707s and Boeing C-135s. It was first delivered on the Boe-ing 737 in 1984 and on the Airbus A320 in 1988. The engine has powered all versions of the 737 since the -300 variant as well as being offered on the A319, A320, A321 and A340. The CFM56 is by a large margin the most widely used en-gine on commercial narrowbodies with a current market share of over 60%.

CFM has been working on a replacement for the CFM56 since 1999 and the Leap-X turbofan is the successor of the CFM56 line. The Leap-X has a heritage from technology de-veloped over the past 10-15 years by GE and Snecma with engines such as the GE90 and GEnx.

The Leap-X fan will have a 198cm diameter with 18 blades, compared with 36 titanium blades for a CFM56-5C and 24 blades for a CFM56-7B. Combined with a new lighter fan containment structure, total weight savings will be 455kg per aircraft. CFM has at this point completed full-scale, aerody-namic, acoustic, birdstrike and blade-out tests on the new fan.

DC-8 aircraft have been retrofitted with the CFM56 turbofan since 1982. The engine is now the leading powerplant on the world’s

commercial narrowbodies

The Leap-X will power the A320neo and C919

The CFM56 currently powers more than 60% of the world’s commercial narrowbodies

COMMERCIAL ENGINES 2011

16 | Flightglobal Insight | Commercial Engines 2011

FleetWatch newsletterFleetWatch is a FREE weekly e-newsletter which brings together the latest headlines as well as news, data and analysis from across Flightglobal’s portfolio of services.

FleetWatch is an e-newsletter focusing on the latest pipeline information for orders, fleet plans, start-ups and suspended operations.

Subscribe for freewww.flightglobal.com/fleetwatchnews

FleetWatch monthly dataEvery month, Flightglobal Insight provides a FREE fleet order analysis which is a condensed version of the montlhy data available to Flightglobal Pro subscribers.

Our FleetWatch articles provide you with a brief overview of commercial aircraft orders by customer, market group and aircraft type.

Find out morewww.flightglobal.com/fleetwatch

FleetWatch

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 17

ENGINE ALLIANCE Engine Alliance is a 50-50 joint venture be-tween General Electric and Pratt & Whitney which was formed in 1996. The GP7200 en-

gine came into service in 2008 on the Airbus A380 and is one of the two powerplant options for this aircraft.

The main application for Engine Alliance’s first engine was originally the Boeing 747-500/600X projects, before these were cancelled owing to lack of demand from airlines. The GP7200 was designed for the A380.

The GP7000 family is derived from the GE90 and PW4000 families. It is built on the GE90 core and the PW4000 low spool heritage.

The GP7200 is certificated at thrusts of 76,500lb (340kN) and 81,500lb (363kN).

The Leap-X is one of the two engine options on the Airbus A320neo which is due to enter service in 2016. The Leap-X programme remains on schedule and CFM is confident that their next-generation powerplant will be competitive in the battle for engine market share on the A320neo.

The Leap-X has also been selected by China’s Comac for its C919, a 168-190 passenger single-aisle twinjet. It will be the largest commercial airliner ever designed and built in China. Its first flight is expected to take place in 2014, with initial deliveries scheduled for 2016.

Operators can expect double-digit fuel burn improvement compared to current production CFM56 engines. Noise lev-els will also be cut in half and NOx levels will meet CAEP/6 requirements with a 50% margin. These advances will come even as the Leap-X inherits the unsurpassed reliability and

The Leap-X will have 18 blades

World airline rankings on your desktopPurchase the latest Airline Business traffic and financial rankings withdetailed analysis, delivered direct to your desktop. For details:

www.flightglobal.com/datasets

maintenance cost of the CFM56.

Accompanying the Leap-X is an integrated propulsion sys-tem (IPS) built by Nexcelle, a GE and Safran joint venture.

COMMERCIAL ENGINES 2011

18 | Flightglobal Insight | Commercial Engines 2011

GENERAL ELECTRIC General Electric’s aerospace division is called GE Aviation which is part of GE Technology Infrastructure, itself part of the conglomerate

General Electric. GE Aviation previously operated under the name of General Electric Aircraft Engines (GEAE) until Sep-tember 2005.

The General Electric Company built its first turbine engine in 1941 when it began development of Whittle-type turbojets under a technical exchange arrangement between the Brit-ish and American governments.

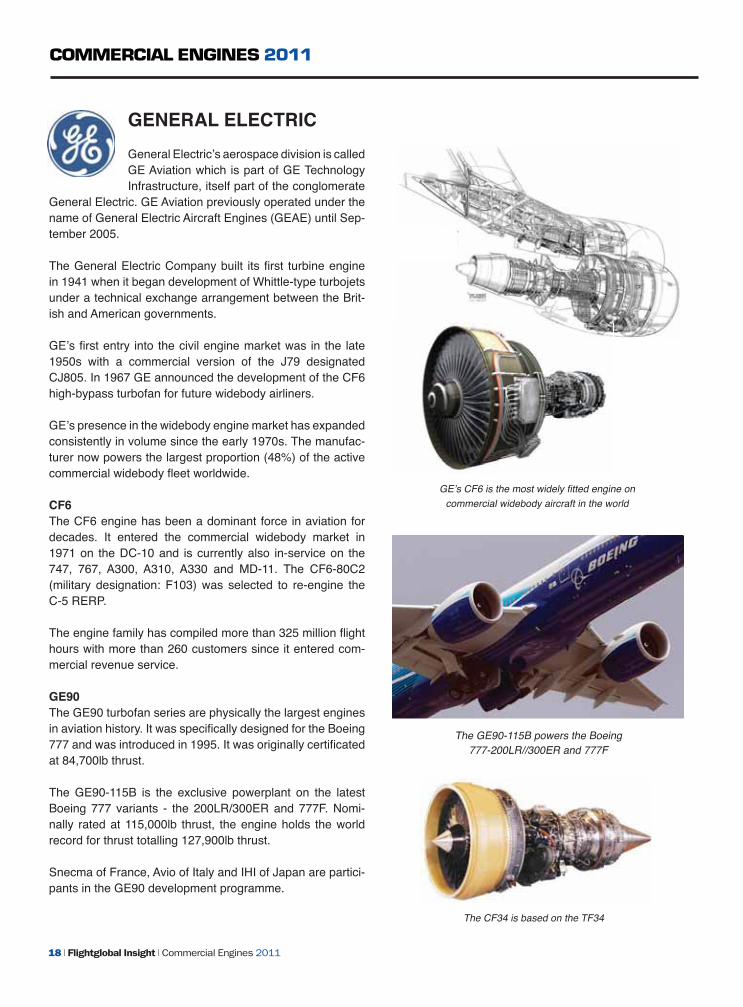

GE’s first entry into the civil engine market was in the late 1950s with a commercial version of the J79 designated CJ805. In 1967 GE announced the development of the CF6 high-bypass turbofan for future widebody airliners.

GE’s presence in the widebody engine market has expanded consistently in volume since the early 1970s. The manufac-turer now powers the largest proportion (48%) of the active commercial widebody fleet worldwide.

CF6The CF6 engine has been a dominant force in aviation for decades. It entered the commercial widebody market in 1971 on the DC-10 and is currently also in-service on the 747, 767, A300, A310, A330 and MD-11. The CF6-80C2 (military designation: F103) was selected to re-engine the C-5 RERP.

The engine family has compiled more than 325 million flight hours with more than 260 customers since it entered com-mercial revenue service.

GE90The GE90 turbofan series are physically the largest engines in aviation history. It was specifically designed for the Boeing 777 and was introduced in 1995. It was originally certificated at 84,700lb thrust.

The GE90-115B is the exclusive powerplant on the latest Boeing 777 variants - the 200LR/300ER and 777F. Nomi-nally rated at 115,000lb thrust, the engine holds the world record for thrust totalling 127,900lb thrust.

Snecma of France, Avio of Italy and IHI of Japan are partici-pants in the GE90 development programme.

GE’s CF6 is the most widely fitted engine on commercial widebody aircraft in the world

The GE90-115B powers the Boeing 777-200LR//300ER and 777F

The CF34 is based on the TF34

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 19

The GEnx is available on both the 787 and 747-8

CF34The CF34 turbofan is a deriative of the GE TF34 which pow-ers the US Air Force A-10 and US Navy S-3A. The CF34 is used on regional jets including the Bombardier CRJ series, the Embraer E-Jets and the Chinese Comac ARJ21 which is currently under development.

GEnxThe GEnx (General Electric Next-generation) is the succes-sor to the CF6 and is based on the GE90’s architecture.

The GEnx will deliver 15% better specific fuel consumption than the engines it replaces. It is designed to stay on wing 30% longer, while using 30% fewer parts, greatly reducing maintenance. The GEnx’s emissions will be as much as 95% below current regulatory limits.

The GEnx is an engine option on the Boeing 787 and is the exclusive powerplant on the 747-8. The GEnx is intended to replace the CF6 in GE’s production line.

GE is in partnership with Pratt & Whitney forging the Engine Alliance, responsible for the GP7200 engine designed for the Airbus A380. GE is also a partner with Snecma in CFM International.

The CF34 powers the majority of the world’s regional jets, including Embraer’s E-Jet family

Download the FREEAircraft Finance 2011 report

Flightglobal Insight’s Aircraft Finance 2011 report provides an analytical overview of the year 2010 looking at airliner orders, transaction activities and deal financing, together with a leasing market study and glimpse of what appraisers expect for 2011.

Find out morewww.flightglobal.com/insight

COMMERCIAL ENGINES 2011

20 | Flightglobal Insight | Commercial Engines 2011

International Aero Engines (IAE) is a Pratt & Whitney, Rolls-Royce, MTU Aero Engines and Japanese Aero Engines joint venture which was formed in 1983. The V2500 powerplant made is debut in 1989 on the Airbus A320. The engine also powers the A319 and A321 variants and the Boeing MD-90.

IAE unveiled the SelectOne performance improvement package for the V2500 in 2005 with launch customer IndiGo, and with an after-market agreement.

The next package of improvements, dubbed SelectTwo, will be introduced in 2013. IAE is offering the SelectTwo pack-age as a sales order option on V2500-A5 SelectOne en-gines, but has not announced a launch customer.

The SelectTwo engine should trim fuel burn costs by 0.58% for an Airbus A320 on a 930km leg. That would translate to roughly $4.3 million savings over a 10-year period for a 10-aircraft fleet of A320s completing 2,300 flights per year.

Although IAE promises smaller fuel burn cuts than next-generation engines (Leap-X and PW1000G), the SelectTwo shows that the joint venture is committed to providing sub-stantial support and continued investment in the V2500.

The core and low-pressure spool of the two-shaft V2500 is left untouched by the upgrade. SelectTwo comprises a soft-ware upgrade for the electronic engine control and a new data entry plug.

The Pratt & Whitney PW1100G geared turbofan was se-lected by Airbus to power the re-engined A320neo after the manufacturer and Rolls-Royce failed to reach an agreement to offer the engine jointly through the IAE venture.

Members of the IAE consortium have agreed to extend their partnerships to 2045 despite philosophical differences on the design of future engines.

IAE’s V2500 entered service with Adria Airways in 1989

Nearly 6,500 V2500 engines are either in service or on order

INTERNATIONAL AERO ENGINES

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 21

PRATT & WHITNEY Pratt & Whitney was established in 1925 by its

founder, Frederick Rentschler, as part of United Aircraft and Transport Corporation (which later became known simply as the United Aircraft Corporation and from 1975 as Unit-ed Technologies). Pratt & Whitney manufactures products widely used in both civil and military aircraft.

Pratt & Whitney began producing commercial jet engines in the late 1950s for the Boeing 707 and the Douglas DC-8 with engines including the JT3 and the JT4A. Later, the JT8D powered the 727, 737 and DC-9.

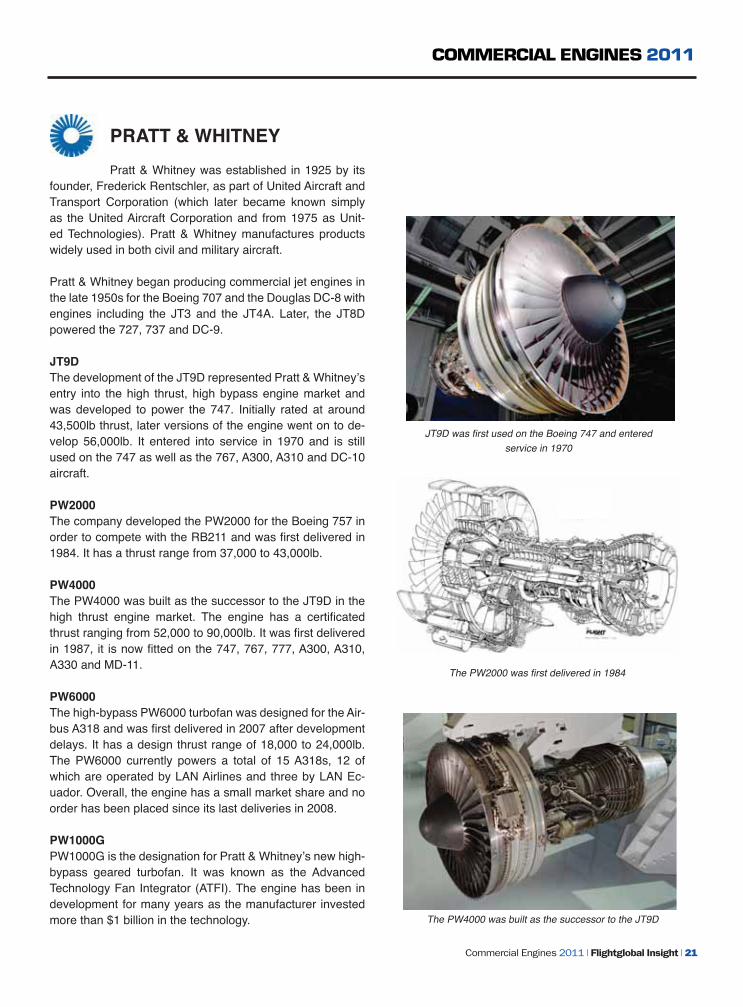

JT9DThe development of the JT9D represented Pratt & Whitney’s entry into the high thrust, high bypass engine market and was developed to power the 747. Initially rated at around 43,500lb thrust, later versions of the engine went on to de-velop 56,000lb. It entered into service in 1970 and is still used on the 747 as well as the 767, A300, A310 and DC-10 aircraft.

PW2000The company developed the PW2000 for the Boeing 757 in order to compete with the RB211 and was first delivered in 1984. It has a thrust range from 37,000 to 43,000lb.

PW4000The PW4000 was built as the successor to the JT9D in the high thrust engine market. The engine has a certificated thrust ranging from 52,000 to 90,000lb. It was first delivered in 1987, it is now fitted on the 747, 767, 777, A300, A310, A330 and MD-11.

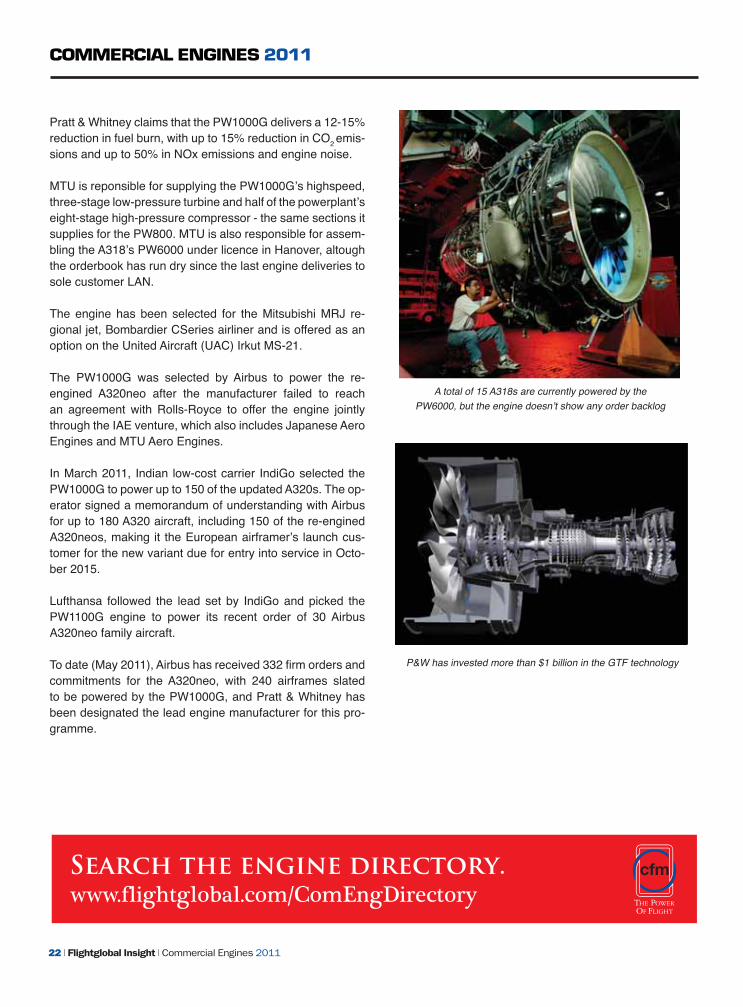

PW6000The high-bypass PW6000 turbofan was designed for the Air-bus A318 and was first delivered in 2007 after development delays. It has a design thrust range of 18,000 to 24,000lb. The PW6000 currently powers a total of 15 A318s, 12 of which are operated by LAN Airlines and three by LAN Ec-uador. Overall, the engine has a small market share and no order has been placed since its last deliveries in 2008.

PW1000GPW1000G is the designation for Pratt & Whitney’s new high-bypass geared turbofan. It was known as the Advanced Technology Fan Integrator (ATFI). The engine has been in development for many years as the manufacturer invested more than $1 billion in the technology.

The PW2000 was first delivered in 1984

JT9D was first used on the Boeing 747 and entered service in 1970

The PW4000 was built as the successor to the JT9D

COMMERCIAL ENGINES 2011

22 | Flightglobal Insight | Commercial Engines 2011

P&W has invested more than $1 billion in the GTF technology

Pratt & Whitney claims that the PW1000G delivers a 12-15% reduction in fuel burn, with up to 15% reduction in CO2 emis-sions and up to 50% in NOx emissions and engine noise.

MTU is reponsible for supplying the PW1000G’s highspeed, three-stage low-pressure turbine and half of the powerplant’s eight-stage high-pressure compressor - the same sections it supplies for the PW800. MTU is also responsible for assem-bling the A318’s PW6000 under licence in Hanover, altough the orderbook has run dry since the last engine deliveries to sole customer LAN.

The engine has been selected for the Mitsubishi MRJ re-gional jet, Bombardier CSeries airliner and is offered as an option on the United Aircraft (UAC) Irkut MS-21.

The PW1000G was selected by Airbus to power the re-engined A320neo after the manufacturer failed to reach an agreement with Rolls-Royce to offer the engine jointly through the IAE venture, which also includes Japanese Aero Engines and MTU Aero Engines.

In March 2011, Indian low-cost carrier IndiGo selected the PW1000G to power up to 150 of the updated A320s. The op-erator signed a memorandum of understanding with Airbus for up to 180 A320 aircraft, including 150 of the re-engined A320neos, making it the European airframer’s launch cus-tomer for the new variant due for entry into service in Octo-ber 2015.

Lufthansa followed the lead set by IndiGo and picked the PW1100G engine to power its recent order of 30 Airbus A320neo family aircraft.

To date (May 2011), Airbus has received 332 firm orders and commitments for the A320neo, with 240 airframes slated to be powered by the PW1000G, and Pratt & Whitney has been designated the lead engine manufacturer for this pro-gramme.

A total of 15 A318s are currently powered by the PW6000, but the engine doesn’t show any order backlog

Search the engine directory.www.flightglobal.com/ComEngDirectory

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 23

ROLLS-ROYCE

Rolls-Royce was founded in 1906 by Henry Royce and Charles Rolls, and produced its first aircraft engine in 1914. Rolls-Royce has produced commercial jet engines since the 1950s with the Avon for the de Havilland Comet and the Sud Aviation Caravelle. The Conway engine came to promi-nence in the early 1960s and was fitted to the 707, DC-8 and the Vickers VC10. The Spey engine was also produced in the 1960s and designed for the BAC One-Eleven and the three-engined Hawker Siddeley Trident.

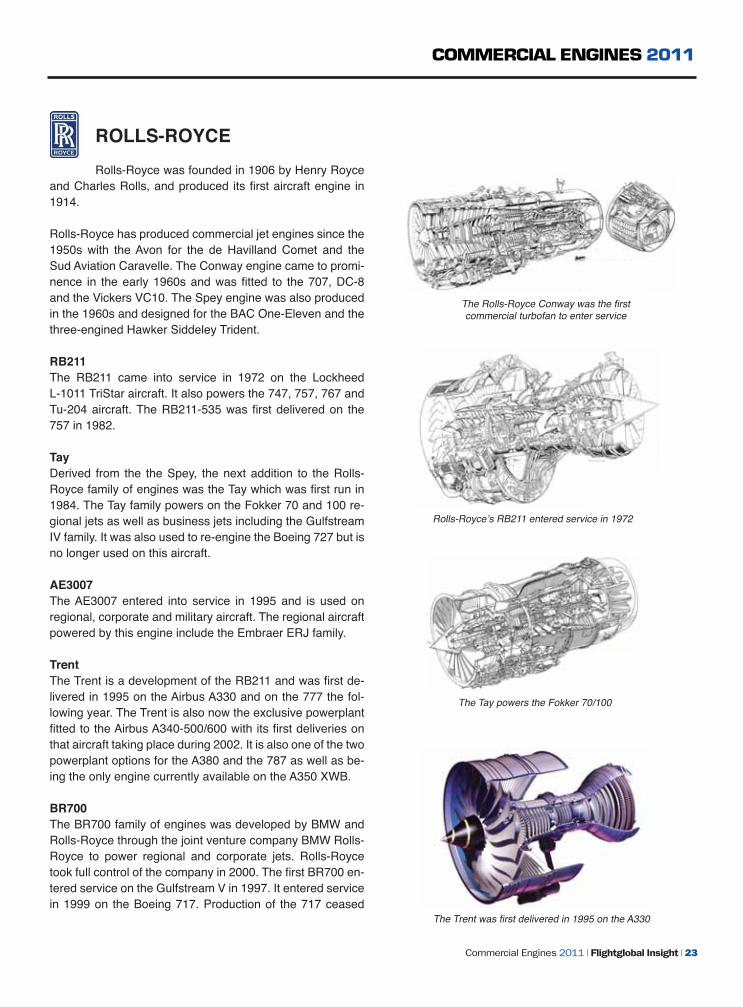

RB211The RB211 came into service in 1972 on the Lockheed L-1011 TriStar aircraft. It also powers the 747, 757, 767 and Tu-204 aircraft. The RB211-535 was first delivered on the 757 in 1982.

TayDerived from the the Spey, the next addition to the Rolls-Royce family of engines was the Tay which was first run in 1984. The Tay family powers on the Fokker 70 and 100 re-gional jets as well as business jets including the Gulfstream IV family. It was also used to re-engine the Boeing 727 but is no longer used on this aircraft.

AE3007The AE3007 entered into service in 1995 and is used on regional, corporate and military aircraft. The regional aircraft powered by this engine include the Embraer ERJ family.

TrentThe Trent is a development of the RB211 and was first de-livered in 1995 on the Airbus A330 and on the 777 the fol-lowing year. The Trent is also now the exclusive powerplant fitted to the Airbus A340-500/600 with its first deliveries on that aircraft taking place during 2002. It is also one of the two powerplant options for the A380 and the 787 as well as be-ing the only engine currently available on the A350 XWB.

BR700The BR700 family of engines was developed by BMW and Rolls-Royce through the joint venture company BMW Rolls-Royce to power regional and corporate jets. Rolls-Royce took full control of the company in 2000. The first BR700 en-tered service on the Gulfstream V in 1997. It entered service in 1999 on the Boeing 717. Production of the 717 ceased

Rolls-Royce’s RB211 entered service in 1972

The Rolls-Royce Conway was the first commercial turbofan to enter service

The Trent was first delivered in 1995 on the A330

The Tay powers the Fokker 70/100

COMMERCIAL ENGINES 2011

24 | Flightglobal Insight | Commercial Engines 2011

The Trent XWB is a new engine designed for the Airbus A350 XWB family

in 2006. A total of 129 BR700-powered 717s are currently in service.

Next generationRolls-Royce has committed to developing a new, more ef-ficient engine core to power the next generation of narrow-bodies, bypassing the near-term option of re-engining im-proved versions of the Boeing 737 and A320.

Although Rolls-Royce and Pratt & Whitney are partners in IAE, the companies have different approaches to engine de-velopment for next generation narrowbodies. R-R has con-sistently rejected the geared turbofan concept, preferring in-stead to research advanced two and three-shaft turbofans, known as the RB282 and RB285, respectively. R-R believes that its design can deliver the same efficiency benefits as the GTF, without the need for a gearbox to decouple the fan.

Although Airbus favoured IAE to offer an engine option for their A320neo, Rolls-Royce and Pratt & Whitney failed to

Delivering critical aircraft market information to your businessACAS 3 has been developed to provide the most timely and detailed aircraft dataavailable anywhere in the market, delivering the accurate reporting and forecasting you rely on for your business.Everyday ACAS helps thousands of air transport professionals at OEMs, MROs,suppliers, operators, lessors, CAAs and governments to better understand the world’s civil and military fleets.Planners, market analysts, product managers, CSMs, sales and marketing teams alike, know that ACAS helps them:

React first – With daily updates on fleetdata, aircraft orders and aircraftretirements, ACAS 3 will ensure you’realways the first to know.

Forecast, analyse and benchmark –With ACAS 3 innovative reporting toolsyou can forecast aircraft retirements anddelivery rates to really discover whereyour next customer is coming from.

To request a free demo [email protected] or call +44 1788 564 800US toll free +1 866 348 4503

*ACAS user survey 2005

Win business and save time – ACAS 3contains all the data you need, in oneconstantly updated service. In fact, 85% ofsubscribers would choose ACAS if theycould only have one source of aviationdata.*

agree. Consequently, Pratt & Whitney is going it alone with the PW1000G which is the alternative to CFM’s Leap-X.

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 25

CFM InternationalCFM56

Thrust 19,500-34,000lb

Length 250cm

Diameter 165cm

Weight 2,360kg

Service entry 1982

Aircraft 737, A320 family, A340, DC-8

Engine AllianceGP7200

Thrust 70,000-77,000lb

Length 475cm

Diameter 316cm

Weight 6,725kg

Service entry 2008

Aircraft A380

General ElectricCF34

Thrust 9,220-20,000lb

Length 260-368cm

Diameter 124-145cm

Service entry 1992

Aircraft ARJ21, CRJ, E-Jet

AT A GLANCEEngine comparison

Leap-X

Thrust ~30,000lb

Diameter 190.5cm

Service entry due in 2015

Aircraft A320neo, C919

CF6

Thrust 40,000-72,000lb

Length 424-477cm

Diameter 266-36cm

Weight 4,067-4,104kg

Service entry 1971

Aircraft A300, A310, 747, 767, DC-10, MD-11

Sipa

Pre

ss/R

ex F

eatu

res

COMMERCIAL ENGINES 2011

26 | Flightglobal Insight | Commercial Engines 2011

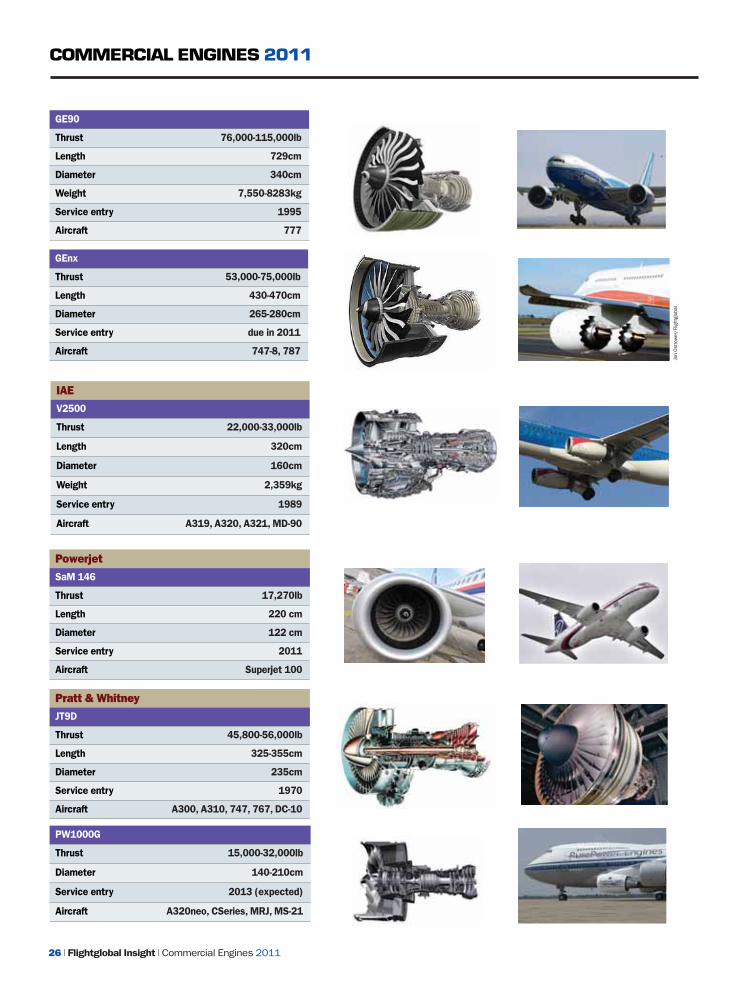

IAEV2500

Thrust 22,000-33,000lb

Length 320cm

Diameter 160cm

Weight 2,359kg

Service entry 1989

Aircraft A319, A320, A321, MD-90

GE90

Thrust 76,000-115,000lb

Length 729cm

Diameter 340cm

Weight 7,550-8283kg

Service entry 1995

Aircraft 777

GEnx

Thrust 53,000-75,000lb

Length 430-470cm

Diameter 265-280cm

Service entry due in 2011

Aircraft 747-8, 787

Pratt & WhitneyJT9D

Thrust 45,800-56,000lb

Length 325-355cm

Diameter 235cm

Service entry 1970

Aircraft A300, A310, 747, 767, DC-10

PowerjetSaM 146

Thrust 17,270lb

Length 220 cm

Diameter 122 cm

Service entry 2011

Aircraft Superjet 100

PW1000G

Thrust 15,000-32,000lb

Diameter 140-210cm

Service entry 2013 (expected)

Aircraft A320neo, CSeries, MRJ, MS-21

Jon

Ost

row

er/F

light

glob

al

COMMERCIAL ENGINES 2011

Commercial Engines 2011 | Flightglobal Insight | 27

Rolls-RoyceAE3007

Thrust 6,495-8,917lb

Length 270cm

Diameter 98cm

Weight 720kg

Service entry 1995

Aircraft ERJ-145 family

PW6000

Thrust 18,000-24,000lb

Length 275cm

Diameter 145cm

Weight 2,245kg

Service entry 2007

Aircraft A318

PW4000

Thrust 52,000-90,000lb

Length 414cm

Diameter 240-255cm

Service entry 1987

Aircraft A300, A310, A330, 747,

767, 777, MD-11

PW2000

Thrust 37,000-43,000lb

Length 360cm

Diameter 200cm

Service entry 1984

Aircraft 757

RB211

Thrust 7,264-9,874lb

Length 300-320cm

Diameter 188-220cm

Weight 3,300-4,490kg

Service entry 1972

Aircraft L-1011, 747 , 757, 767, Tu-204

Trent

Thrust 53,000-115,000lb

Length 390-455cm

Diameter 250-455cm

Weight 4,700-6,550kg

Service entry 1995

Aircraft A330, A340, A350, A380, 777, 787

NOTE: Engines listed are currently in production and or in servicefor commercial narrowbody, widebody and regional aircraft.

Max

Kin

gsle

y-Jon

es/F

light

glob

al

Choosing CFM* to power the A320neo isn’t just playing safe, it’s playing smart. The CFM history of record-breaking reliability is legendary. Now, the LEAP engine with its proven architecture and ground-breaking technology,

delivers 15% lower fuel consumption and 15% lower CO2 emissions than the engines it will replace. Don’t jump into the unknown. Leap into the future.Visit www.cfm56.com/leap

*CFM, LEAP and the CFM logo are all trademarks of CFM International, a 50/50 joint company of Snecma and General Electric Co.

LEAP

There are lots ofrisky options in life.Choosing the LEAP engine isn’t one of them.

Related Documents