Combining Individual Securities Into Portfolios (Chapter 4) Individual Security Return and Risk Portfolio Expected Rate of Return Portfolio Variance Combination Lines Combination Line Between a Risky Asset and a Risk-Free Asset

Combining Individual Securities Into Portfolios (Chapter 4) Individual Security Return and Risk Portfolio Expected Rate of Return Portfolio Variance Combination.

Dec 21, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Combining Individual SecuritiesInto Portfolios

(Chapter 4)

Combining Individual SecuritiesInto Portfolios

(Chapter 4)

Individual Security Return and Risk Portfolio Expected Rate of Return Portfolio Variance Combination Lines Combination Line Between a

Risky Asset and a Risk-Free Asset

Individual Security Return and Risk

Individual Security Return and Risk

Expected Rate of Return

where:

– E(rA) = Expected rate of return on security (A)

– rA,i = i(th) possible return on security (A)

– hi = probability of getting the i(th) return

Variance and Standard Deviation

n

1iiA,iA rh)E(r

)(rσ)σ(r

)]E(r[rh)(rσ

A2

A

n

1i

2AiA,iA

2

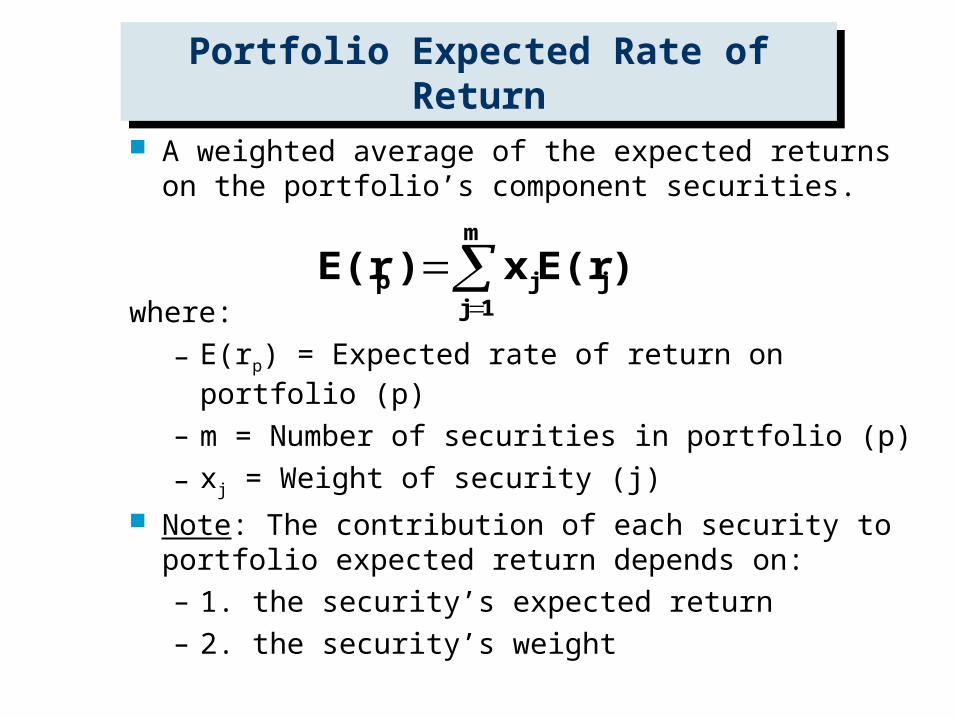

Portfolio Expected Rate of Return

Portfolio Expected Rate of Return

A weighted average of the expected returns on the portfolio’s component securities.

where:

– E(rp) = Expected rate of return on portfolio (p)

– m = Number of securities in portfolio (p)

– xj = Weight of security (j)

Note: The contribution of each security to portfolio expected return depends on:– 1. the security’s expected return– 2. the security’s weight

m

1jjjp )E(rx)E(r

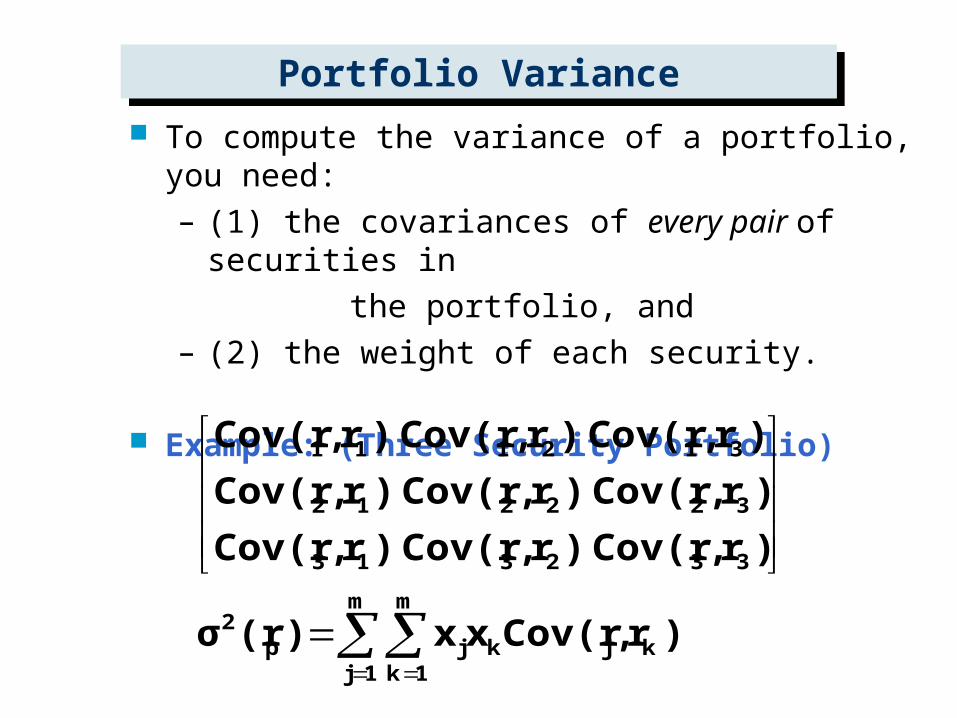

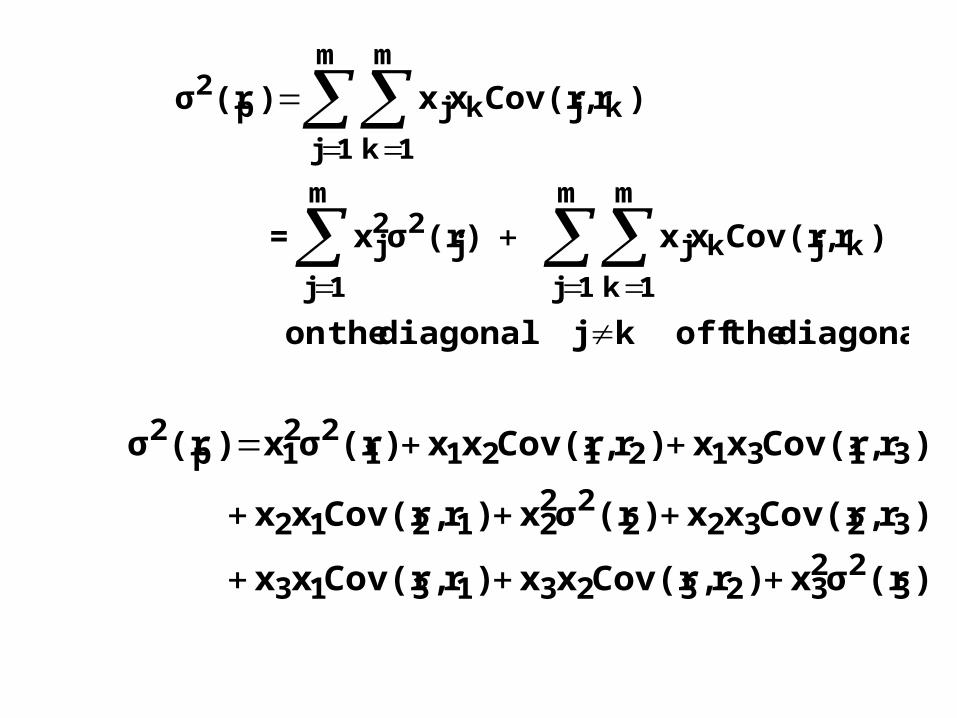

Portfolio VariancePortfolio Variance

To compute the variance of a portfolio, you need:– (1) the covariances of every pair of securities in

the portfolio, and – (2) the weight of each security.

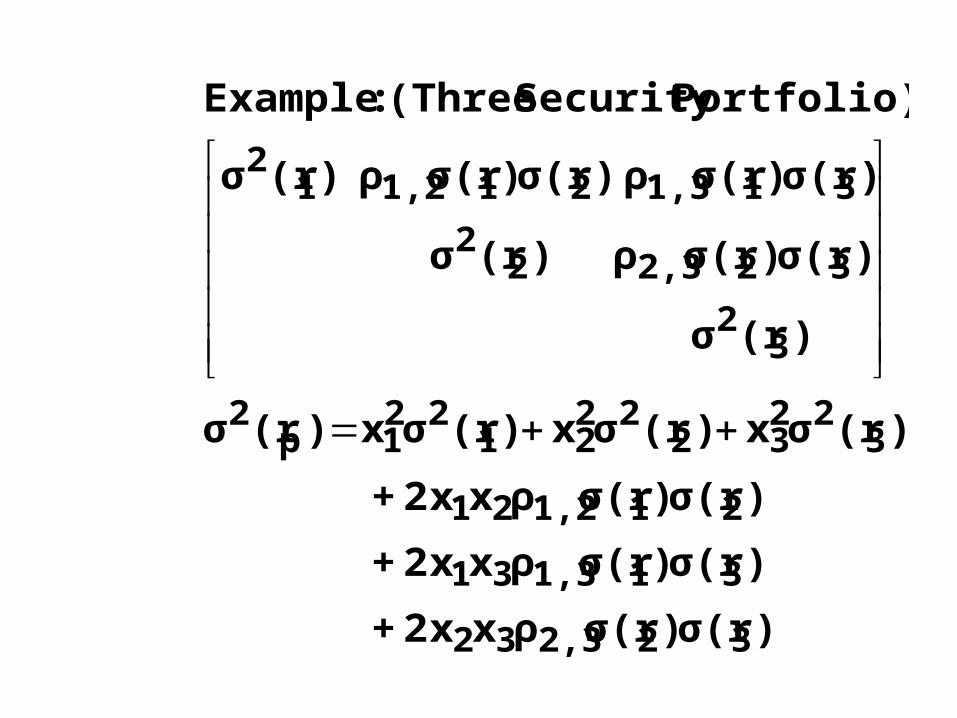

Example: (Three Security Portfolio)

m

1j

m

1kkjkjp

2

332313

322212

312111

)r,Cov(rxx)(rσ

)r,Cov(r )r,Cov(r )r,Cov(r

)r,Cov(r )r,Cov(r )r,Cov(r

)r,Cov(r )r,Cov(r )r,Cov(r

Take each of the covariances in the matrix and multiply it by the weight of the security identified on the row (security j) and then again by the weight of the security identified on the column (security k). Then, add up all of the products.

)r,Cov(rxx)r,Cov(rxx)r,Cov(rxx

)r,Cov(rxx)r,Cov(rxx)r,Cov(rxx

)r,Cov(rxx)r,Cov(rxx)r,Cov(rxx)(rσ

333323231313

323222221212

313121211111p2

The Covariance Between a Security and Itself is Simply Its

Own Variance

The Covariance Between a Security and Itself is Simply Its

Own Variance

)1

(r2σ =

)]1

E(ri1,

[ri

h =

)]1

E(ri1,

[r)]1

E(ri1,

[ri

h)1

r,1

Cov(r

n

1i

2

n

1i

)(rσ )r,Cov(r )r,Cov(r

)r,Cov(r )(rσ )r,Cov(r

)r,Cov(r )r,Cov(r )(rσ

Portfolio) Security (Three :Example

32

2313

3222

12

312112

diagonal the off kj diagonal the on

)r,Cov(rxx )(rσx =

)r,Cov(rxx)(rσ

m

1j

m

1k

kjkj

m

1j

j22

j

m

1j

m

1k

kjkjp2

)(rσx)r,Cov(rxx)r,Cov(rxx

)r,Cov(rxx)(rσx)r,Cov(rxx

)r,Cov(rxx)r,Cov(rxx)(rσx)(rσ

322

323231313

3232222

21212

31312121122

1p2

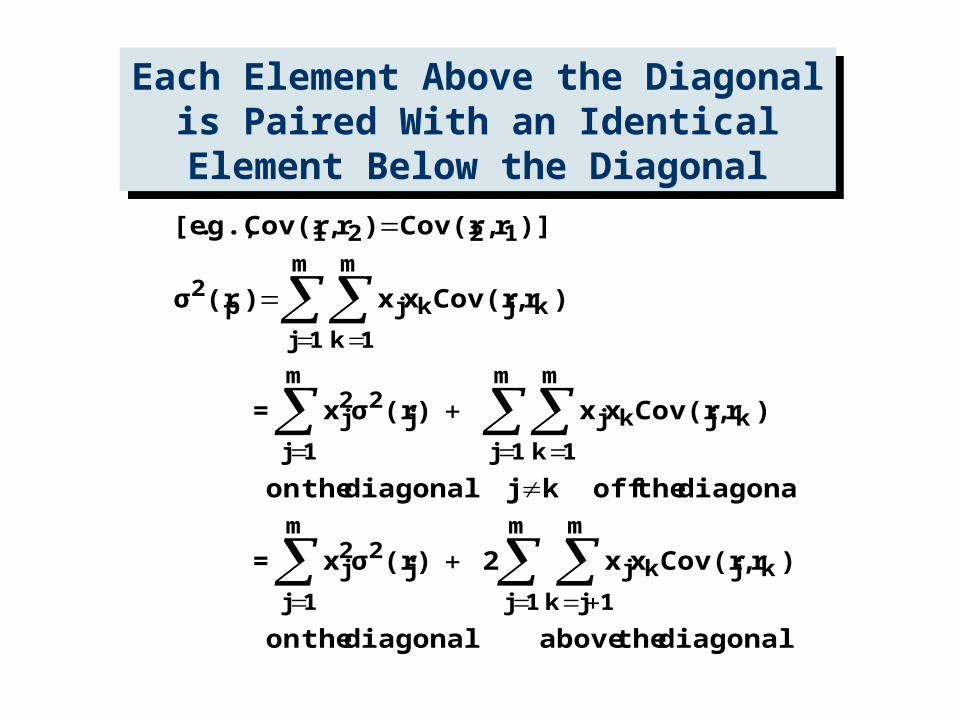

Each Element Above the Diagonal is Paired With an

Identical Element Below the Diagonal

Each Element Above the Diagonal is Paired With an

Identical Element Below the Diagonal

diagonal the above diagonal the on

)r,Cov(rxx2 )(rσx =

diagonal the off kj diagonal the on

)r,Cov(rxx )(rσx =

)r,Cov(rxx)(rσ

)]r,Cov(r)r,Cov(r .,g.[e

m

1j

m

1jk

kjkj

m

1j

j22

j

m

1j

m

1k

kjkj

m

1j

j22

j

m

1j

m

1k

kjkjp2

1221

)r,Cov(rxx2+

)r,Cov(rxx2+

)r,Cov(rxx2+

)(rσx)(rσx)(rσx)(rσ

)(rσ

)r,Cov(r )(rσ

)r,Cov(r )r,Cov(r )(rσ

Portfolio) Security (Three :Example

3232

3131

2121

322

3222

2122

1p2

32

3222

312112

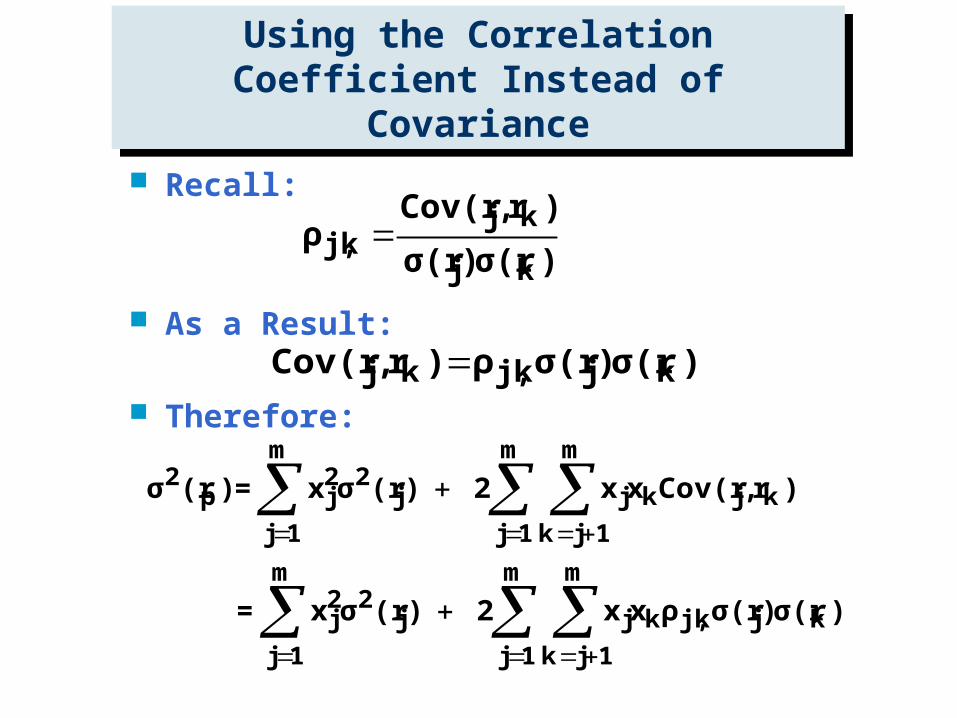

Using the Correlation Coefficient Instead of Covariance

Using the Correlation Coefficient Instead of Covariance

Recall:

As a Result:

Therefore:

)σ(r)σ(r

)r,Cov(rρ

kj

kjkj,

)σ(r)σ(rρ)r,Cov(r kjkj,kj

m

1j

m

1jk

kjkj,kj

m

1j

j22

j

m

1j

m

1jk

kjkj

m

1j

j22

jp2

)σ(r)σ(rρxx2 )(rσx=

)r,Cov(rxx2 )(rσx = )(rσ

)σ(r)σ(rρxx2+

)σ(r)σ(rρxx2+

)σ(r)σ(rρxx2+

)(rσx)(rσx)(rσx)(rσ

)(rσ

)σ(r)σ(rρ )(rσ

)σ(r)σ(rρ )σ(r)σ(rρ )(rσ

Portfolio) Security (Three :Example

322,332

311,331

211,221

322

3222

2122

1p2

32

322,322

311,3211,212

COMBINATION LINESCOMBINATION LINES

A curve that shows what happens to the risk and expected return of a portfolio of two stocks as the portfolio weights are varied.

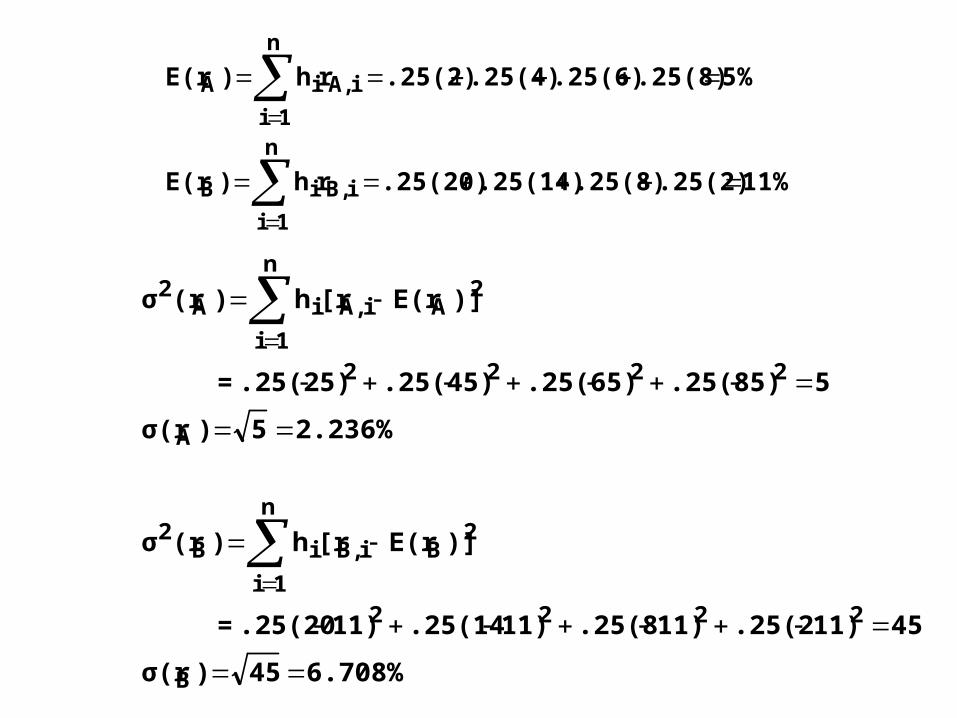

Example 1 (Perfect Negative Correlation)

hi

.25 .25 .25 .25

rA,i

2% 4% 6% 8%

rB,i

20% 14% 8% 2%

11%.25(2).25(8).25(14).25(20)rh)E(r

5%.25(8).25(6).25(4).25(2)rh)E(r

n

1i

iB,iB

n

1i

iA,iA

6.708%45)σ(r

4511).25(211).25(811).25(1411).25(20=

)]E(r[rh)(rσ

2.236%5)σ(r

55).25(85).25(65).25(45).25(2=

)]E(r[rh)(rσ

B

2222

n

1i

2BiB,iB

2

A

2222

n

1i

2AiA,iA

2

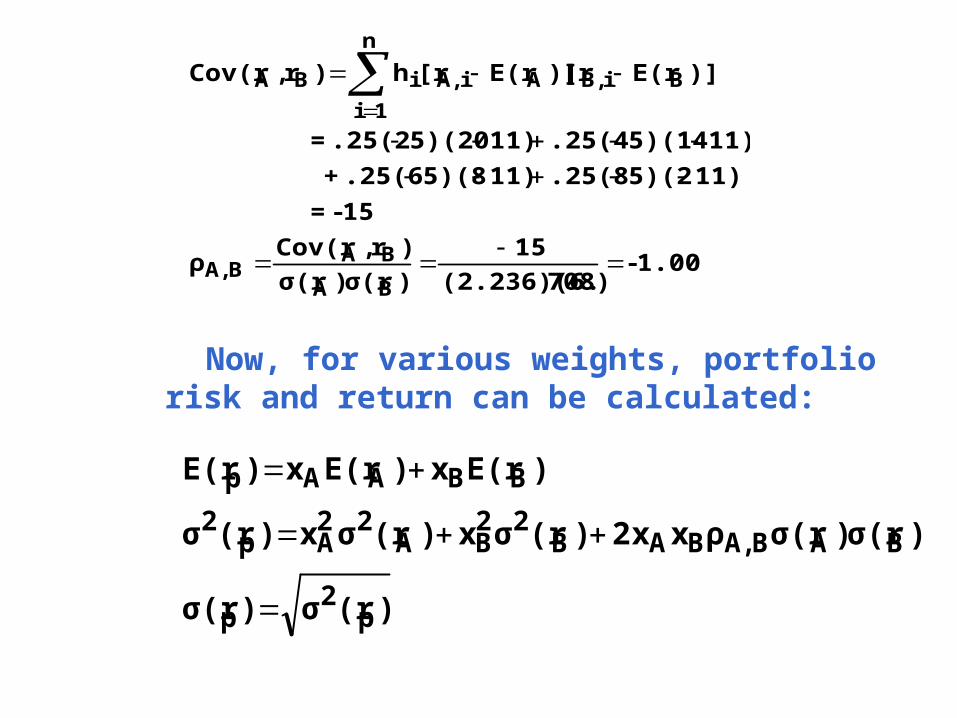

Now, for various weights, portfolio risk and return can be calculated:

1.00- 708)(2.236)(6.

15

)σ(r)σ(r

)r,Cov(rρ

15- =

11)5)(2.25(811)5)(8.25(6 +

11)5)(14.25(411)5)(20.25(2 =

)]E(r[r)]E(r[rh)r,Cov(r

BA

BABA,

BiB,

n

1i

AiA,iBA

)(rσ)σ(r

)σ(r)σ(rρxx2)(rσx)(rσx)(rσ

)E(rx)E(rx)E(r

p2

p

BABA,BAB22

BA22

Ap2

BBAAp

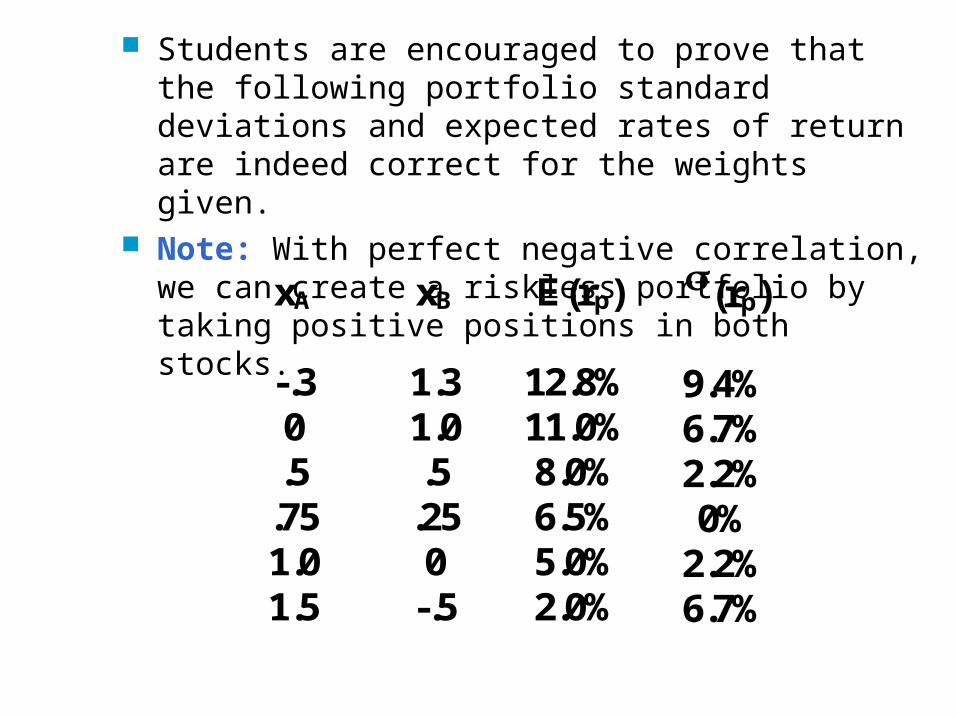

Students are encouraged to prove that the following portfolio standard deviations and expected rates of return are indeed correct for the weights given.

Note: With perfect negative correlation, we can create a riskless portfolio by taking positive positions in both stocks.

xA

-.3 0 .5

.75 1.0 1.5

xB

1.3 1.0 .5 .25 0

-.5

E(rp)

12.8% 11.0% 8.0% 6.5% 5.0% 2.0%

(rp)

9.4% 6.7% 2.2% 0%

2.2% 6.7%

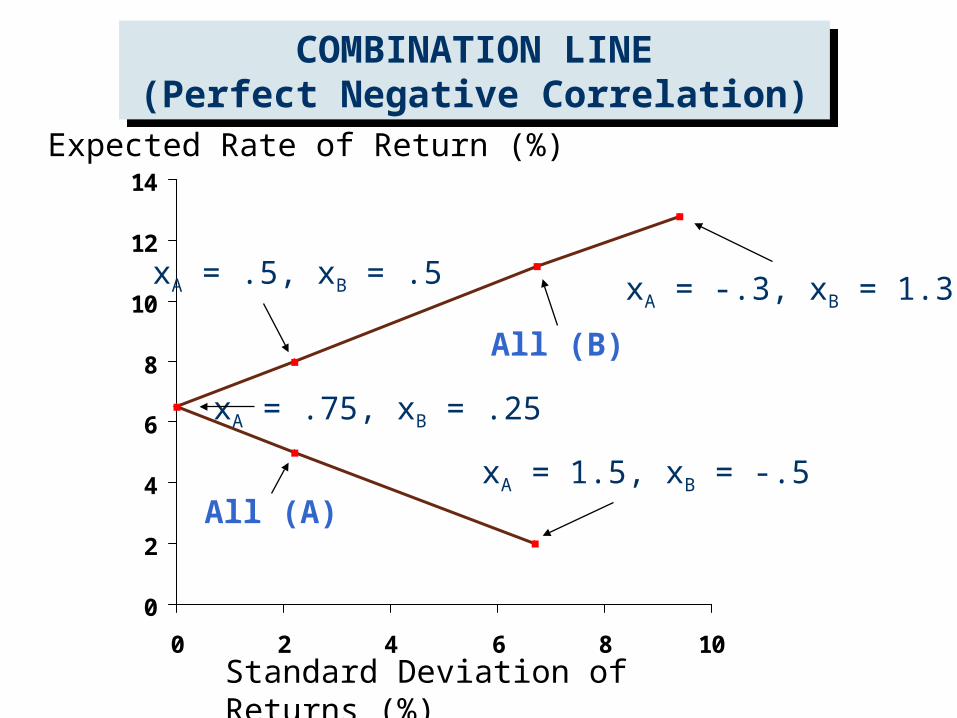

COMBINATION LINE(Perfect Negative Correlation)

COMBINATION LINE(Perfect Negative Correlation)

0

2

4

6

8

10

12

14

0 2 4 6 8 10

Expected Rate of Return (%)

Standard Deviation of Returns (%)

All (B)

All (A)

xA = .75, xB = .25

xA = .5, xB = .5 xA = -.3, xB = 1.3

xA = 1.5, xB = -.5

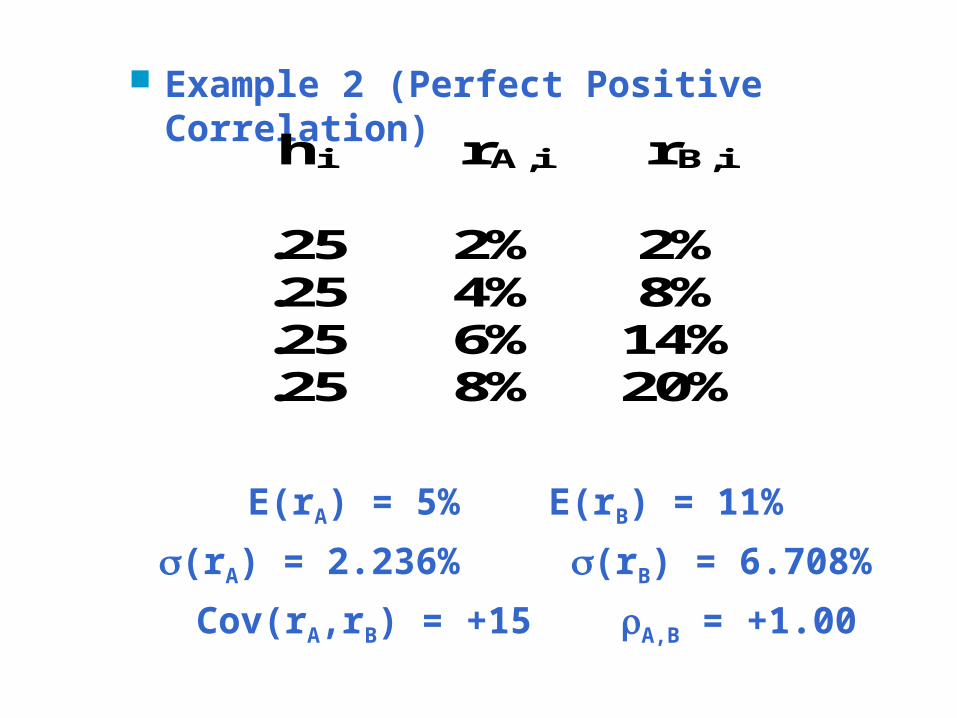

Example 2 (Perfect Positive Correlation)

E(rA) = 5% E(rB) = 11%

(rA) = 2.236% (rB) = 6.708%

Cov(rA,rB) = +15 A,B = +1.00

hi

.25

.25

.25

.25

rA,i

2% 4% 6% 8%

rB,i

2% 8%

14% 20%

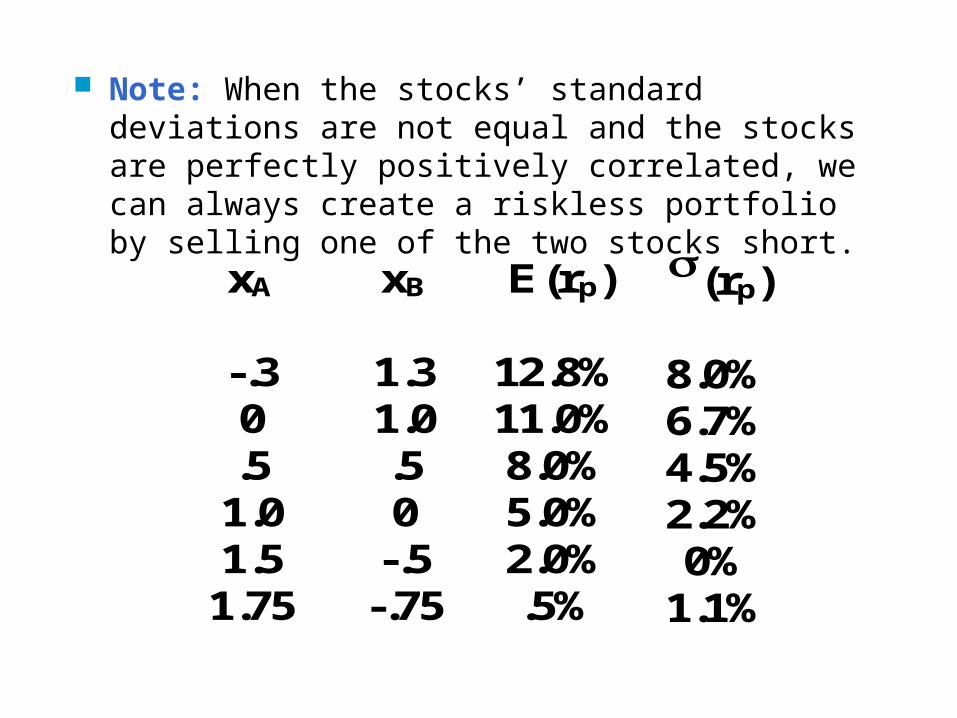

Note: When the stocks’ standard deviations are not equal and the stocks are perfectly positively correlated, we can always create a riskless portfolio by selling one of the two stocks short.

xA

-.3 0 .5 1.0 1.5

1.75

xB

1.3 1.0 .5 0

-.5 -.75

E(rp)

12.8% 11.0% 8.0% 5.0% 2.0% .5%

(rp)

8.0% 6.7% 4.5% 2.2% 0%

1.1%

COMBINATION LINE(Perfect Positive Correlation)

COMBINATION LINE(Perfect Positive Correlation)

0

2

4

6

8

10

12

14

0 2 4 6 8 10

Expected Rate of Return (%)

Standard Deviation of Returns (%)

All (B)

All (A)

xA = -.3, xB = 1.3

xA = .5, xB = .5

xA = 1.5, xB = -.5

xA = 1.75, xB = -.75

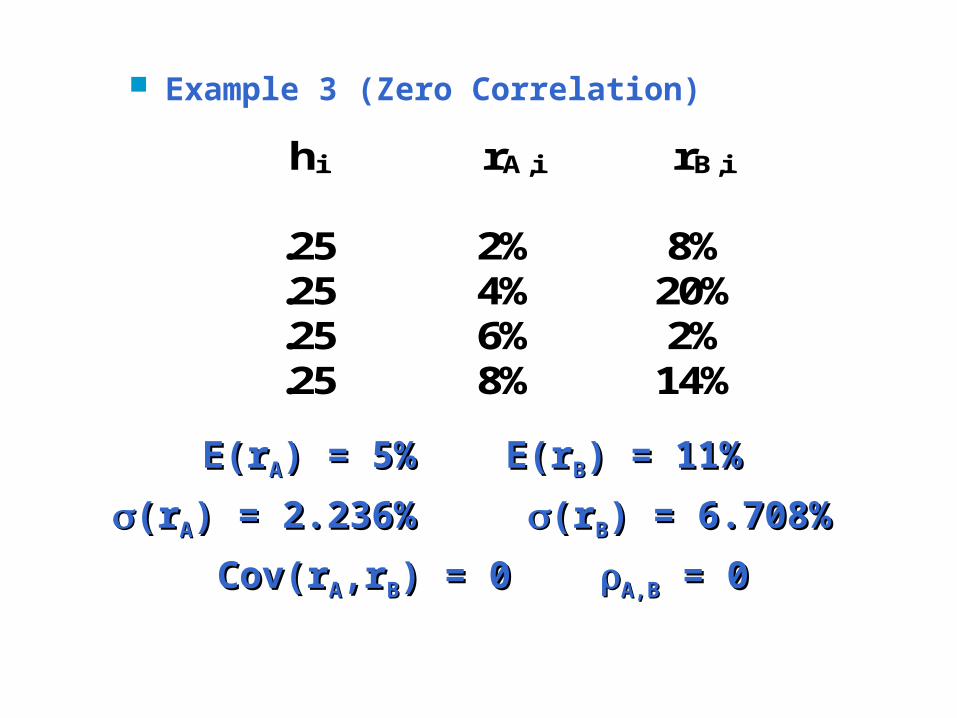

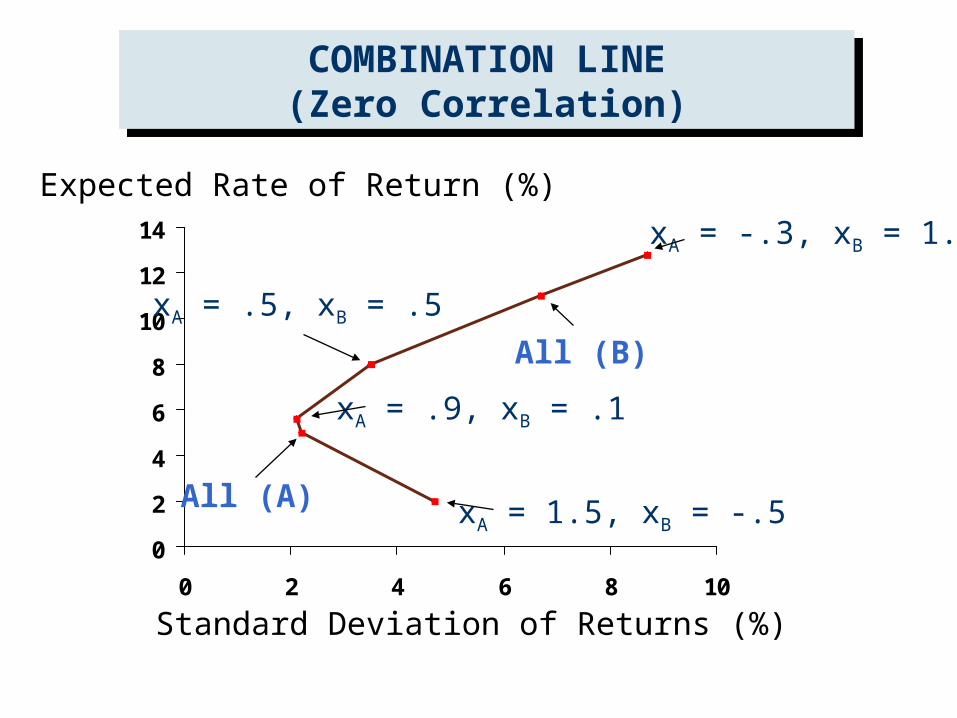

Example 3 (Zero Correlation)

hi

.25

.25

.25

.25

rA,i

2% 4% 6% 8%

rB,i

8% 20% 2%

14%

E(rE(rAA) = 5% E(r) = 5% E(rBB) = 11% ) = 11%

(r(rAA) = 2.236% ) = 2.236% (r(rBB) = 6.708% ) = 6.708%

Cov(rCov(rAA,r,rBB) = 0 ) = 0 A,BA,B = 0 = 0

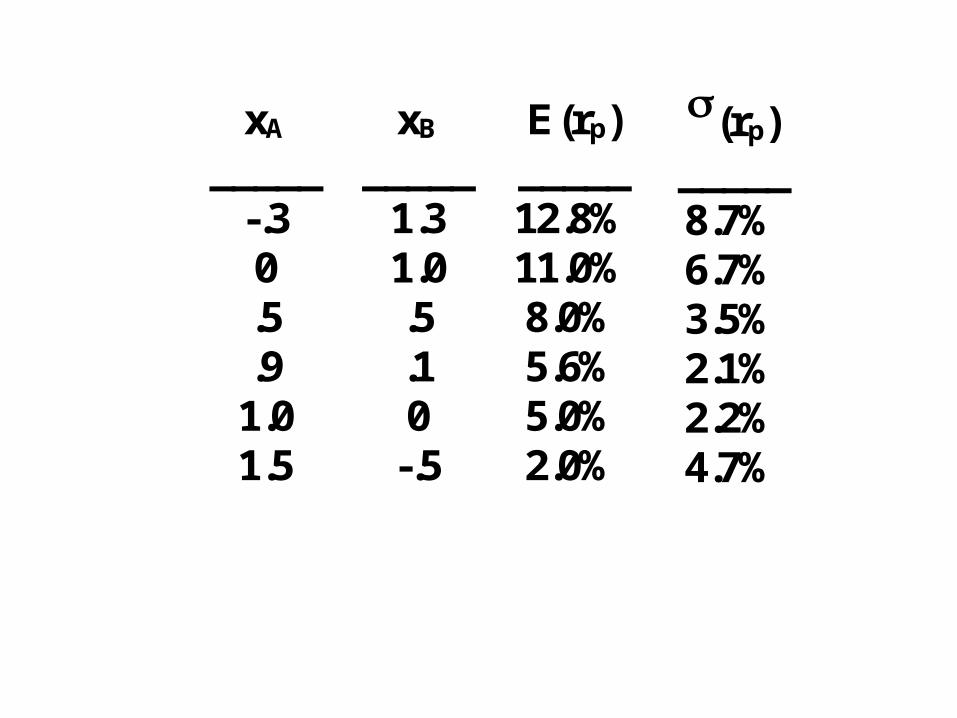

xA

_____ -.3 0 .5 .9

1.0 1.5

xB

_____ 1.3 1.0 .5 .1 0

-.5

E(rp) _____ 12.8% 11.0% 8.0% 5.6% 5.0% 2.0%

(rp) _____ 8.7% 6.7% 3.5% 2.1% 2.2% 4.7%

COMBINATION LINE(Zero Correlation)

COMBINATION LINE(Zero Correlation)

0

2

4

6

8

10

12

14

0 2 4 6 8 10

Expected Rate of Return (%)

Standard Deviation of Returns (%)

All (B)

All (A)

xA = .5, xB = .5

xA = .9, xB = .1

xA = 1.5, xB = -.5

xA = -.3, xB = 1.3

PATHS OF COMBINATION LINESPATHS OF COMBINATION LINES

E(rp) is influenced by E(rj) and xj

(rp) is influenced by (rj), j,k, and xj

j,k determines the path between two securities

Moving along the path occurs by varying the weights.

COMBINATION LINESCOMBINATION LINES

0

2

4

6

8

10

12

14

0 2 4 6 8 10

Stock (B)

Stock (A)

= -1.00

= +1.00

= 0

Expected Rate of Return (%)

Standard Deviation of Returns (%)

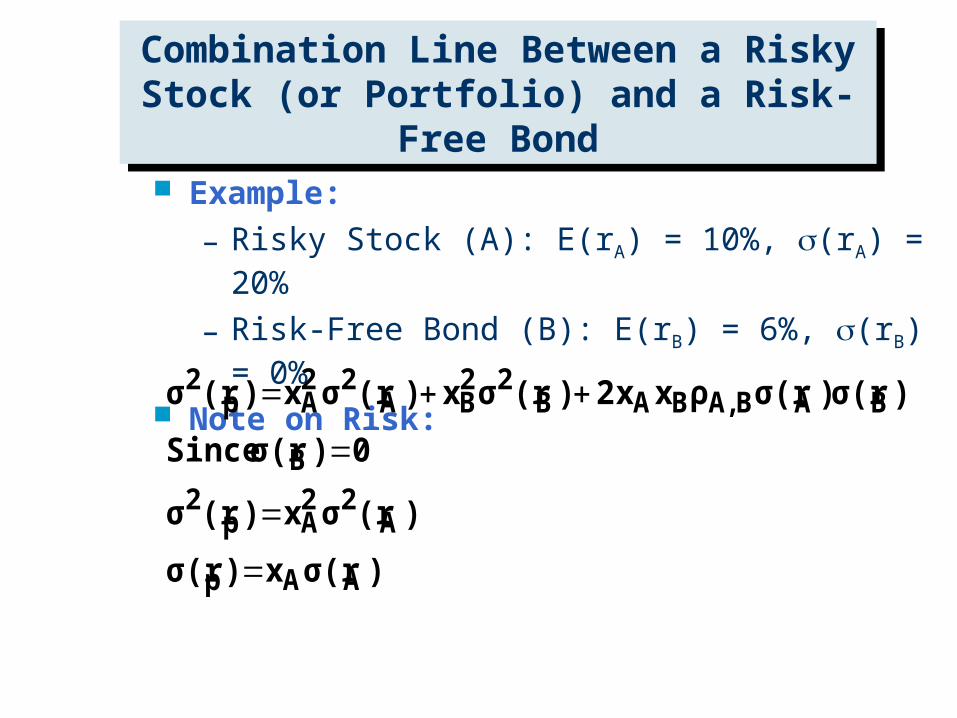

Combination Line Between a Risky Stock (or Portfolio) and a Risk-

Free Bond

Combination Line Between a Risky Stock (or Portfolio) and a Risk-

Free Bond Example:

– Risky Stock (A): E(rA) = 10%, (rA) = 20%

– Risk-Free Bond (B): E(rB) = 6%, (rB) = 0%

Note on Risk:

)σ(rx)σ(r

)(rσx)(rσ

0)σ(r Since

)σ(r)σ(rρxx2)(rσx)(rσx)(rσ

AAp

A22

Ap2

B

BABA,BAB22

BA22

Ap2

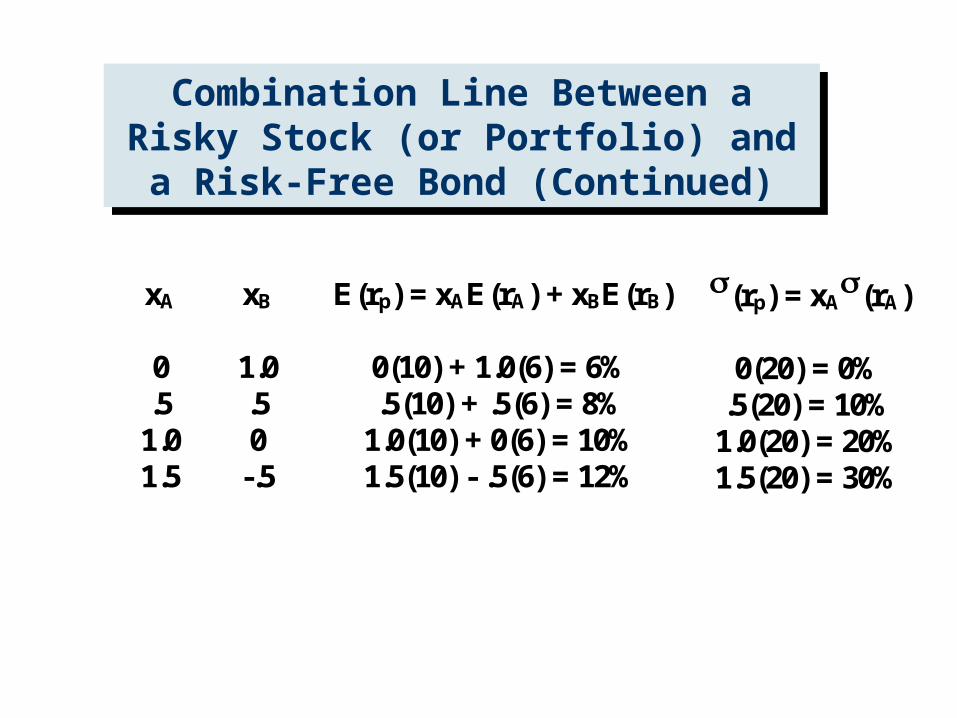

Combination Line Between a Risky Stock (or Portfolio) and a

Risk-Free Bond (Continued)

Combination Line Between a Risky Stock (or Portfolio) and a

Risk-Free Bond (Continued)

xA

0 .5 1.0 1.5

xB

1.0 .5 0

-.5

E(rp) = xAE(rA) + xBE(rB)

0(10) + 1.0(6) = 6% .5(10) + .5(6) = 8%

1.0(10) + 0(6) = 10% 1.5(10) - .5(6) = 12%

(rp) = xA(rA)

0(20) = 0%

.5(20) = 10% 1.0(20) = 20% 1.5(20) = 30%

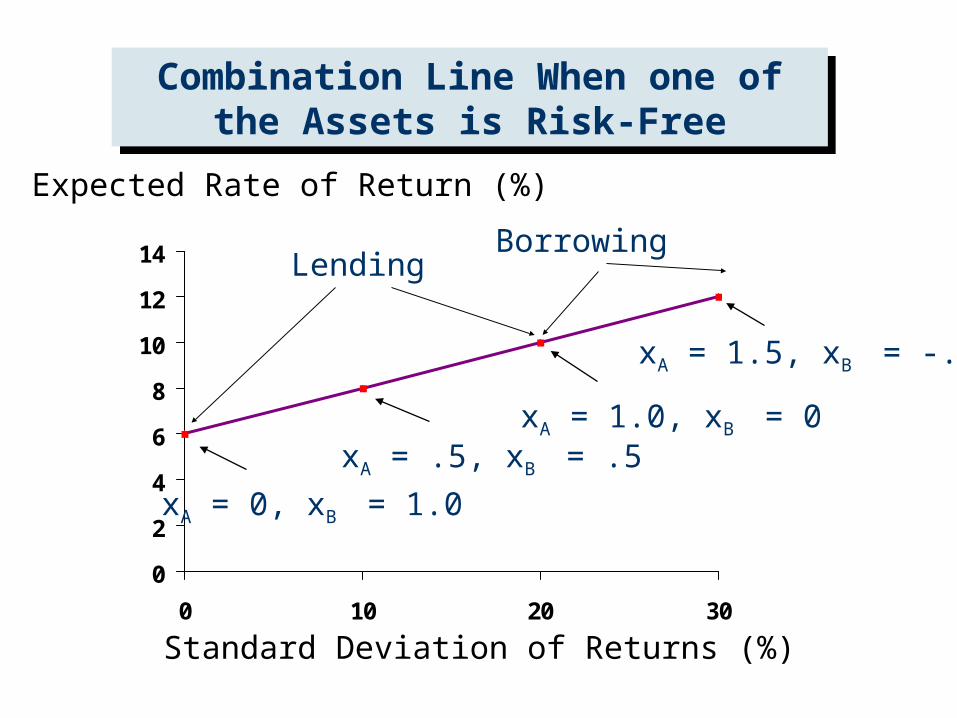

Combination Line When one of the Assets is Risk-Free

Combination Line When one of the Assets is Risk-Free

0

2

4

6

8

10

12

14

0 10 20 30

Expected Rate of Return (%)

Standard Deviation of Returns (%)

xA = 1.5, xB = -.5

xA = 1.0, xB = 0xA = .5, xB = .5

xA = 0, xB = 1.0

LendingBorrowing

Combination Line Between a Risky Stock (or Portfolio) and a Risk-Free

Bond (Continued)

Combination Line Between a Risky Stock (or Portfolio) and a Risk-Free

Bond (Continued)

Note: When one of the two investments is risk-free, the combination line is always a straight line.

Lending: When you buy a bond, you are lending money to the issuer.

Borrowing: Here, we assume that investors can borrow money at the risk-free rate, and add to their investment in the risky asset.

Related Documents