POA The Professional Trades Union for Prison, Correctional and Secure Psychiatric Workers Headquarters: Cronin House 245 Church Street Edmonton London N9 9HW 0 020 8803 0255 0 020 8803 1761 @ www.poauk.org.uk generaIC3poauk.0rg.uk National Chairman: Colin Moses General Secretary: Brian Caton POA Circular 126/2007 ~ 4th October 2007 Dear Colleagues HEALTHCARE NHS PENSION SCHEME REVIEW The membership will be aware of the Government Review of Public Sector Pensions Scheme. Please find attached a copy of the publication from the NHS Staff Council, which outlines the changes to the Scheme. We ask that this be made available to all members of the POA, who are members of the NHS Pension Scheme. Your help and assistance on this matter is greatly appreciated. Yours sincerely BRIAN CATON General Secretary ENCLOSURE Regional Offices: North: 1 Linden House Sardinia Street Leeds LS10 1BH Northern Ireland: Castell House 116 Ballywalter Road Millisle Co. Down BT22 2HS Scotland: Scottish National Office 21 Calder Road Edinburgh Scotland E H l l 3PF

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

POA The Professional Trades Union for Prison, Correctional and Secure Psychiatric Workers

Headquarters: Cronin House 245 Church Street Edmonton London N9 9HW

0 020 8803 0255 0 020 8803 1761 @ www.poauk.org.uk generaIC3poauk.0rg.uk

National Chairman: Colin Moses General Secretary: Brian Caton

POA Circular 126/2007 ~

4th October 2007

Dear Colleagues

HEALTHCARE

NHS PENSION SCHEME REVIEW

The membership will be aware of the Government Review of Public Sector Pensions Scheme.

Please find attached a copy of the publication from the NHS Staff Council, which outlines the changes to the Scheme.

We ask that this be made available to all members of the POA, who are members of the NHS Pension Scheme.

Your help and assistance on this matter is greatly appreciated.

Yours sincerely

BRIAN CATON General Secretary

ENCLOSURE

Regional Offices: North: 1 Linden House Sardinia Street Leeds LS10 1 BH Northern Ireland: Castell House 116 Ballywalter Road Millisle Co. Down BT22 2HS

Scotland: Scottish National Office 21 Calder Road Edinburgh Scotland EHl l 3PF

I n t roduc t i on

1. This paper sets out the final terms of the agreement reached between NHS Employers and NHS staff side at the Pensions Review Steering Group. Within the overall NHS pension arrangements, the agreement sets out a two scheme structure for active members of the NHS Pension Scheme with new entrants joining the New NHS Pension Scheme and existing members staying in a revised version of the current Pension Scheme, the NHS Pension Scheme (1 April 2008 and after terms) and being given a choice as to whether to remain in this for both past and future service or to transfer to the New NHS Pension Scheme for both past and future service benefits.

2. A separate review is taking place coverirlg ill health retirement. There are a number of clear overlaps between the two reviews. Ill health pensions are an important part of Scheme design and will need to feature in both new and existing Schemes. The cost of the arrangements set out here includes the release of 0.05% of pensionable pay

through changes to the ill health retirement arrangements. This will enable more members to pay the 5% contribution compared with the proposals consulted on in 2006. The Ill Health Retirement arrangements when finally agreed will form part of the overall pension agreement and will be covered by the governance arrangements (paragraphs 65-67).

3. The design of the changes to pension arrangements has taken into account equality issues. As part of the governance arrangements, the impact of these changes on equality issues will be kept under review including benchmarking.

4. This agreement is based on analytical work carried out by the Government Actuary's Department (GAD), independently peer reviewed by the actuarial adviser engaged by the review, Hilary Salt, from First Actuarial. Fuller details of all the agreed changes are set out in separate papers listed in annex B. These and other associated review documents are available at www.nhsempIoyers.org/ pensionagreement.

Membership and choice

Membership of the new NHS pension arrangements

5. Following the Public Services Forum (PSF) agreement on normal pension age and subsequent Scheme negotiations, the overarching NHS pension arrangements will include separate Schemes for existing members of the NHS Pension Scheme and for new entrants. All dates are target dates'for implementation of the changes to these proposals:

members who are active in the Scheme on 31 March and 1 April 2008 or deferred members who return to the IVHS before 1 October 2008 will remain members of the NHS Pension Scheme (1 April 2008 and after terms).

members with service in the NHS Pension Scheme (pre 1 April 2008 terms) who are at that date or later become deferred members, will be able to return to the NHS Pension Scheme (1 April 2008 and after terms), provided that the return is within five years of becoming a deferred member and that they had not previously opted to transfer to the New NHS Pension Scheme. The Business Services Authority Pensions Division (BSA PD) will write to deferred members at their last held address about the five year rule.

Deferred members at 1 April 2008 who do not return to the NHS before taking their pension will remain members of the NHS Pension Scheme (pre 1 April 2008 terms).

6. New entrants to the Pension Scheme on and after 1 April 2008 will become members of the New hlHS Pension Scheme. From 1 October 2008, deferred members with service in the NHS Pension Scheme (pre 1 April 2008 terms) who return to the hlHS more than five years after leaving will join the New NHS Pension Scheme for future service.

Choice exercise

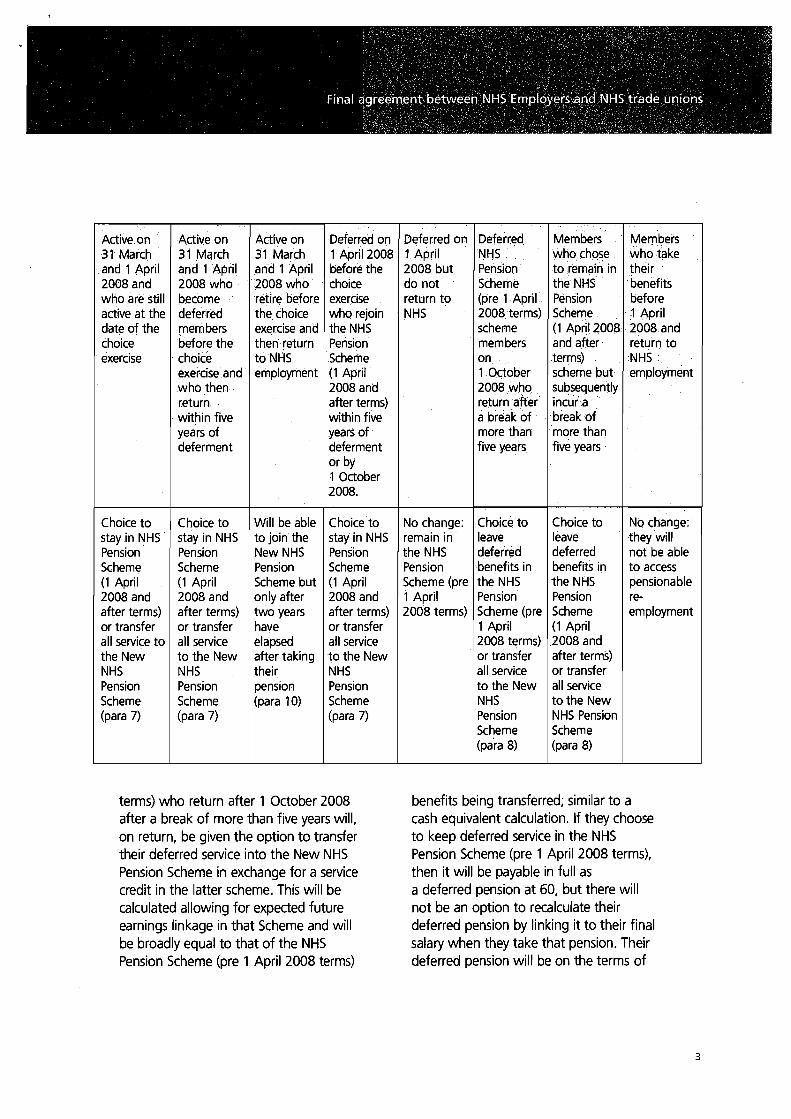

7. There will be a choice exercise in which members will be given a choice to move to the New NHS Pension Scheme. The target date for the choice exercise is 1 July 2009 and it will last until 30 June 201 0, giving members a year to make their choice. This choice will be for past and future pensionable service only (including any prior service not yet aggregated). The basis of the transfer, including the treatment of those with added years contracts, is yet to be agreed but will be determined by the Secretary of State in the light of future negotiations under the governance framework. For those who return within five years of deferment but were in deferment at the time of the choice exercise, choice will be made on return. The BSA PD will take forward the choice exercise with input from the review partners. Those given choice are set out in the table opposite.

Taking 1995 deferred pension a t age 60

8. Deferred members with service in the hlHS Pension Scheme (pre 1 April 2008

terms) who return after 1 October 2008 after a break of more than five years will, on return, be given the option to transfer their deferred service into the New NHS Pension Scheme in exchange for a service credit in the latter scheme. This will be calculated allowing for expected future earnings linkage in that Scheme and will be broadly equal to that of the NHS Pension Scheme (pre 1 April 2008 terms)

benefits being transferred; similar to a cash equivalent calculation. If they choose to keep deferred service in the IVHS Pension Scheme (pre 1 April 2008 terms), then it will be payable in full as a deferred pension at 60, but there will not be an option to recalculate their deferred pension by linking it to their final salary when they take that pension. Their deferred pension will be on the terms of

Deferred NHS Pension Scheme (pre 1 April 2008 terms) scheme members on 1 October 2008 who return after a break of more than five years

Choice to leave deferred benefits in the NHS Pension Scheme (pre 1 April 2008 terms) or transfer all service to the New NHS Pension Scheme (para 8)

Active on 31 March and 1 April 2008 and who are still active at the date of the choice exercise

Choice to stay in NHS Pension Scheme (1 April 2008 and after terms) or transfer all service to the New NHS Pension Scheme (para 7)

Deferred on 1 April 2008 before the choice exercise who rejoin the NHS Pension Scheme (1 April 2008 and after terms) within five years of deferment or by 1 October 2008.

Choice to stay in NHS Pension Scheme (1 April 2008 and after terms) or transfer all service to the New NHS Pension Scheme (para 7)

Members who chose to remain in the NHS Pension Scheme (1 April 2008 and after terms) scheme but subsequently incur a break of more than five years

Choice to leave deferred benefits in the NHS Pension Scheme (1 April 2008 and after terms) or transfer all service to the New NHS Pension Scheme (para 8)

Deferred on 1 April 2008 but do not return to NHS

No change: remain in the NHS Pension Scheme (pre 1 April 2008 terms)

Active on 31 March and 1 April 2008 who become deferred members before the choice exercise and who then return within five years of deferment

Choice to stay in NHS Pension Scheme (1 April 2008 and after terms) or transfer all service to the New NHS Pension Scheme (para 7)

Members who take their benefits before 1 April 2008 and return to NHS employment

No change: they will not be able to access pensionable re- employment

Active on 31 March and 1 April 2008 who retire before the choice exercise and then return to NHS employment

Will be able to join the New NHS Pension Scheme but only after two years have elapsed after taking their pension (para 10)

the NHS Pension Scheme (pre 1 April 2008 terms). They will not have to take benefits from the New NHS Pension Scheme at the same time they take their NHS Pension Scheme (pre 1 April 2008 terms) benefits and can remain active members in the New NHS Pension Scheme.

9. Deferred members and pensioners on 1 April 2008 who do not return to the Scheme and those in receipt of survivor benefits and their dependents at 1 April 2008, will not be affected by any of the changes set out in this document.

IVHS pensioners

10. NHS pensioners who retired before 1 April 2008 will be unaffected by any of the changes. They will not be able to return

to pensionable reemployment. However, those who are active members on 1 April 2008, but retire before being given a choice to move to the New LlHS Pension Scheme, are in a different position as they have participated in the new arrangements which include a later opportunity to move to the new Scheme. They will be able to join the New NHS Pension Scheme if they return to NHS employment. However, there will be a requirement for a two year break in pensionable employment between taking retirement benefits and joining the New hlHS Pension Scheme. It is currently expected that the choice exercise will take place from July 2009 so this arrangement will apply to people who retire between 1 April 2008 and 30 June 2009.

Structure for existing staff who remain in the NHS Pension Scheme (1 April 2008 and after terms)

Building the pension - salaried members

1 1. Existing salaried members will retain the current final salary scheme structure with an accrual rate of eightieths for pension, a half rate survivor's pension and a separate lump sum of three times the initial pension, with a Normal Pension age of 60 (NPA60). Following consideration of the issues by the partners, a normal pension age of 55 will be retained for the closed groups, including Mental Health Officers, who will retain their current rights to doubling of service.

Building the pension - practitioner members

12. Practitioner members will retain their Career Average Revalued Earnings (CARE) Scheme with a pension accrual rate of 1.4% and a lump sum of 4.2%. The method of dynamising practitioner (general medical and dental practitioners) pensionable earnings up to retirement will be changed. All future dynamisation of practitioner pensionable earnings applied after April 2008, will be applied at the rate of Retail Prices Index (RPI) plus 1.5% per annum.

Minimum pension age

13. In line with legislation, active members of the WHS Pension Scheme at 5 April 2006, and deferred members at 5 April 2006 with active service after 30 March 2000, will retain a Minimum Pension Age of 50. Other members of the NHS Pension Scheme will move to an MPA of 55 from 6 April 2010.

Service limits

14. The current service limits of 40 years at 60 and 45 years at 65 will be replaced with a new service limit of 45 years. The lifting of the service limits will take effect for future service from 1 April 2008. The limit of 45 years will include the years credited for any transferred in service.

Earnings limits

15. Currently all members who joined the Pension Scheme after 1 June 1989 or who joined before but have had a break in service of more than 12 months, have their benefits capped. The current earnings cap is f 108,600. From 1 April 2008, this cap will be removed for future service. Service before 1 April 2008 that was subject to the cap will continue to be subject to the cap. The cap will continue to rise in line with RPI rounded up to the nearest f 600 multiple for now. However, the position will be considered at the next valuation as part of the governance arrangements.

16. General dental practitioners are also subject to a separate dental cap, Maximum Allowable Remuneration (MAR). The Department of Health has agreed that

dental MAR will also be removed for future service from 1 April 2008.

Current additional years facility

17. The current facility to purchase added years will be removed when the new arrangements take effect. The transition will take account of the fact that added years contracts can only be taken out from a member's birth date and the intention will be to give members as much notice of the withdrawal of the added years facility as is feasible before the date when the revised Scheme takes effect. Existing added years contracts taken out before the facility is removed will be honoured to buy service in accordance with the current terms. Members will be given notice of these changes in the payslip insert which will be sent by the BSA PD to all active members.

Pension purchase

18. Members will be able to access an additional pension purchase facility of up to f 5,000 of additional pension. Additional pension will be purchased in units of £250. Members in the NHS Pension Scheme (1 April 2008 and after terms) will be able to buy additional pension to be taken without reduction at age 60. Additional pension benefits will be revalued by RPI before and after they come into payment. Members will be able to buy additional pension by lump sum or spread over any period up to 20 years, or their 60th birthday if earlier. Members will be able to choose between buying additional pension for single life

only or with survivor benefits. This is in addition to any Added Years contracts that they may have.

19. Total annual pension contributions will be limited to 100% of pensionable pay. The purchase price of additional pension will be reviewed periodically to take account of changes such as longevity and may change during the period of the purchase.

Money Purchase Additional Voluntary Contributions (MPAVC)

20. Money Purchase Additional Voluntary Contributions (MPAVC) arrangements will be retained to give members an alternative to the in-scheme additional pension purchase facility and to enable members to use the new pension tax regime to increase their pension savings via pay roll, should they wish. In view of the changes to the pension tax regime and the introduction of new arrangements for the NHS, we recommend that the Department of Health re-tenders the AVC contract, including testing whether a single provider would improve the benefits for members of the NIPAVC arrangements.

Taking the pension - salaried and self-employed members

21. At retirement, members of the NHS Pension Scheme (1 April 2008 and after terms) will be able to choose to commute part of their pension to increase the size of their retirement lump sum. Subject to the overriding HM Revenue and Customs (HMRC) limits, pension may be commuted for additional lump at a rate

of f 12 of lump sum for each f 1 per annum of pension given up. This facility will not be available for deferred members on 1 April 2008 who do not subsequently rejoin the Scheme.

Pensionable pay

22. Final pensionable pay for existing members will continue to be based on the best of the last three year's annual pensionable pay.

Pensionable re-employment

23. Members who choose to remain in the hlHS Pension Scheme (post 1 April 2008 terms) will not be able to rejoin either of the Pension Schemes once they have taken their pension benefits. However, deferred members of the NHS Pension Scheme (pre 1 April 2008 terms) who return to the NHS after more than five years will be able to have pensionable re-employment in the New NHS Pension Scheme. For those members of the NHS Pension Scheme (1 April 2008 and after terms), who return to NHS employment within five years and remain in the NHS Pension Scheme (1 April 2008 and after terms) up to retirement, or NHS Pension Scheme (pre 1 April 2008 terms) members who join the new Scheme for future service only, there will continue to be no abatement of those pension benefits after age 60. Those members who take voluntary early retirement with an actuarial reduction will not be subject to abatement as at present. The application of abatement to ill health retirement will be addressed as part of the separate review but will need to be consistent with this.

Early retirement

24. In addition, Agenda for Change (AfC) section 16 (and the parallel agreements for doctors) provide for new arrangements for retirement "in the interests of the service." This provides for early payment of an unenhanced pension as with the new redundancy arrangements but without the possibility of a redundancy payment. This will replace employer agreed voluntary early retirement (which has the same terms).

25. The new NHS redundancy arrangements provide for the alternative of:

a redundancy payment under the collective agreement, or

early payment of an unenhanced retirement pension.

26. The revised AfC agreement also provides for transitional enhanced early retirement arrangements for those over 50 between 2006 and 201 1.

27. From 1 April 2008, a new abatement formula will be introduced for retirements after that date that reduces significantly the impact of abatement. In future, if pensioners return to work for the NHS before the age of 60 for members of the NHS Pension Scheme (1 April 2008 and after terms) and 65 for members of the New NHS Pension Scheme, abatement will take place only on the unearned portion of the pension: that paid for by the employer or the Scheme on top of normal benefits. This is the difference between the pension the member would have received had they taken voluntary early

retirement and what they actually received. This will apply to transitional redundancy and interests of the service retirement, employer agreed voluntary early retirement and new style interests of the service retirement. Ill health retirement arrangements are part of the Ill Health Review but will be consistent.

28. In relation to retirements on redundancy with an unenhanced pension under the new AfC section 16, there will be no abatement of pension for retirements after 1 April 2008. This is the option where the member chooses to use the redundancy payment they are due, to fund early payment of the pension so it is not reduced. Similarly, the redundancy payment only alternative, would not be abated if the member returned to work. It is not therefore appropriate to abate the unenhanced pension in these circumstances.

Voluntary protection in the NHS Pension Scheme (1 April 2008 and after terms)

29. Members of the NHS Pension Scheme (1 April 2008 and after terms) will have access to new, RPI linked, voluntary pay protection arrangements on step down, based on the current pension protection provisions after compulsory step down. This builds on the current protection that exists when members reduce their hours (because final pensionable pay is based on full time equivalent pay).Voluntary protection of final pensionable pay can take effect at any age after the member's MPA. Voluntary

protected pay is intended primarily to operate when a member takes on a less demanding post in the run up to retirement and will be on the following basis:

the reduction in basic pensionable pay will have to be at least 10%

the higher pay level must have lasted for at least one year

the step down pay level will need to be sustained for at least a year after step down

final pensionable pay will be protected for service up to the point of step down

members will only be able to make one step down, although this will be kept under review as part of the governance arrangements in the light of experience

the employer will be asked to certify that a qualifying step down has taken place but not to approve the application by the member for voluntary protection.

31. An eligible non legal partner must have been nominated to receive the pension before the member's death and to have been in a financially interdependent, and cohabiting relationship, for at least two years before the member's death. The member and the nominee must have been free to enter into a marriage or civil partnership at the time of making the nomination and also at the death of the member. The validity of the nomination would be tested at death. The Department of Health may consider cases for ex gratia payment where there is a valid nomination but due to exceptional circumstances, are unable to demonstrate two-year interdependence.

Ending cessation of spouse/civil partner pensions on re-marriage

32. Survivor pensions will be payable for life regardless of the changes in their circumstances.

Short term death in service pensions

33. Short term death-in-service pensions will be standardised at six months.

Death benefits

Survivor benefits 30. In addition to the existing survivor benefits

for legally married and civil partners, eligible non legal partners of all members of the NHS Pension Scheme (1 April 2008 and after terms) or deferred members at 1 April 2008 who return within five years of deferment, will be able to receive survivor pensions for life in respect of service since 1 988.

Child allowance

34. Children's survivor pensions will be provided until the age of 23 in all cases and will be payable indefinitely as long as the child, through physical or mental impairment, remains unable to earn a living and the condition existed at the member's date of death. Existing protections provided in compliance with the Finance Act 2004 will continue.

Multiple nominations

35. In future, scheme members will be able to make multiple nominations for the death in service benefit rather than a single nomination as at present. Either:

evenly to one or more individual parties

or in specific proportions to more than one individual parties.

Survivor and death benefits

36. Death in service benefit will continue to be twice annual pensionable pay. Survivor pensions will continue to be half the member pension as now. The ill health retirement arrangements to be consulted upon as part of the 111 Health Review, will be used for the calculation of survivor pensions on death in service.

The New NHS Pension Scheme for new entrants from 1 April 2008

Building the pension Earnings limits

37. The New NHS Pension Scheme will have a IVPA of 65 and MPA of 55. For salaried members, there will be a final salary structure with an accrual rate of 1160th. For self employed members, the CARE accrual rate will be 1.87% for pension. CARE pension accruals up to the point of taking pension will be dynamised by RPI plus 1.5% per annum.

39. There will not be any earnings limit for service in the New NHS Pension Scheme, except for those who transfer in capped service either from other schemes or via the choice exercise. Capped, transferred service will remain capped on the current basis (see para 15).

Pension purchase

40. Members in the New NHS Pension Scheme Service limits will also have the opportunity to purchase 38. There will be a maximum service limit additional pension on the same terms as

of 45 years. This will include the existing members except that it will be years credited for any transferred structured around a payable age of 65 (and in service. the purchase rates adjusted accordingly).

Taking the pension

Commutation

41. There is not a requirement for members to take any lump sum in the New NHS Pension Scheme. Members will be able to choose how much lump sum they wish to take up to the limits permitted by the Inland Revenue for tax free lump sums. This will be by commutation of pension at the rate of f 12 of tax free cash for every f 1 per annum of pension foregone.

Pensionable pay

42. Final pensionable pay will be calculated using the definition of the average of the best three consecutive annual pensionable pay years, in the last ten years. Before the three best consecutive years' pensionable pay are confirmed, each year's pay (other than the year immediately prior to a pension benefit event) will be revalued in line with RPI. This will support step down in the run up to retirement. For those in the NHS Pension Scheme (1 April 2008 and after terms) who choose to transfer to the New NHS Pension Scheme in the choice exercise, the final pensionable pay calculation period will start from 1 April 2008.

Early retirement

43. Pension taken before the NPA of 65 will be subject to actuarial reduction.

Late retirement

44. Pension accrued before NPA that is taken after NPA will be enhanced by actuarial late retirement factors.

Draw down

45. There will be a range of other flexibilities. After reaching 55, staff will be able to draw down part of their pension, with actuarial reduction before the NPA, whilst continuing to work and build up more pension. Staff will be able to draw down their pension:

in up to three tranches

all remaining pension must be taken in the final tranche

each tranche taken will be subject to a minimum of 20% of years accrued in whole years or one year whichever is greater

the minimum amount of pre-commutation pension that can be drawn down in value after any actuarial reduction will be f 750

rr~inimum pensionable service that can be left in the Scheme after draw down is 20% of total pensionable service before draw down or one year, whichever is greater

will have to be taken in conjunction with a reduction of at least 10% of pensionable pay, for example, as a result from a switch to part-time or a reduction in grade

the employer will be asked to certify that a qualifying reduction in pensionable pay has taken place but not to approve the application by the member for draw down.

Pensionable re-employment

46. Members who have taken their pension in full and left the Scheme will be able to return to pensionable reemployment.

Abatement before NPA65

47. Abatement will apply on the same basis as the new arrangements for existing Scheme members but up to the NPA of 65. Abatement in respect of ill health retirement is being considered in the Ill Health Review.

Survivor benefits

48. Survivor benefits will be based on the 111 60th accrual rate. This will deliver broadly the same level of benefits as for the NHS Pension Scheme. As well as survivor pensions for spouses and civil partners, survivor pensions will be payable to eligible non legal partners. Eligibility criteria are set out in paras 30 and 31.

Death in service (short term pensions)

49. Short term death in service pensions will be standardised at six months.

Death in draw down

50. If a member dies after drawing down pension but before retiring fully, their survivors will receive a combination of death in service and death in retirement benefits. Survivor pensions will be calculated according to the amount of benefits that the member has chosen to

put into payment compared with the amount that they have yet to put into payment (calculated at the last point that drawdown occurred). Lump sum benefits on death after drawdown will consist of two separate lump sums. The first, in respect of benefits not yet put into payment will be twice a member's final pensionable pay but reduced in line with the proportion of benefits already taken. The death after retirement element will be calculated on the current basis (with a cap of twice final pensionable pay less any lump sum already taken) but the member's final pensionable pay used to calculate the cap will be reduced in line with the percentage of benefits already taken.

Ending cessation of spouse/civil partner pensions on re-marriage

51. Members' survivors will receive spouselpartners pensions for life.

Child allowance

52. Children's survivor pensions will be provided until the age of 23 in all cases and will be payable indefinitely as long as the child, through physical or mental impairment, remains unable to earn a living and the condition existed at the member's date of death.

Multiple nominations

53. In future, Scheme members will be able to make multiple nominations for the death in service benefit (para 35).

Funding and governance

Contribution rate structure for al l s ta f f

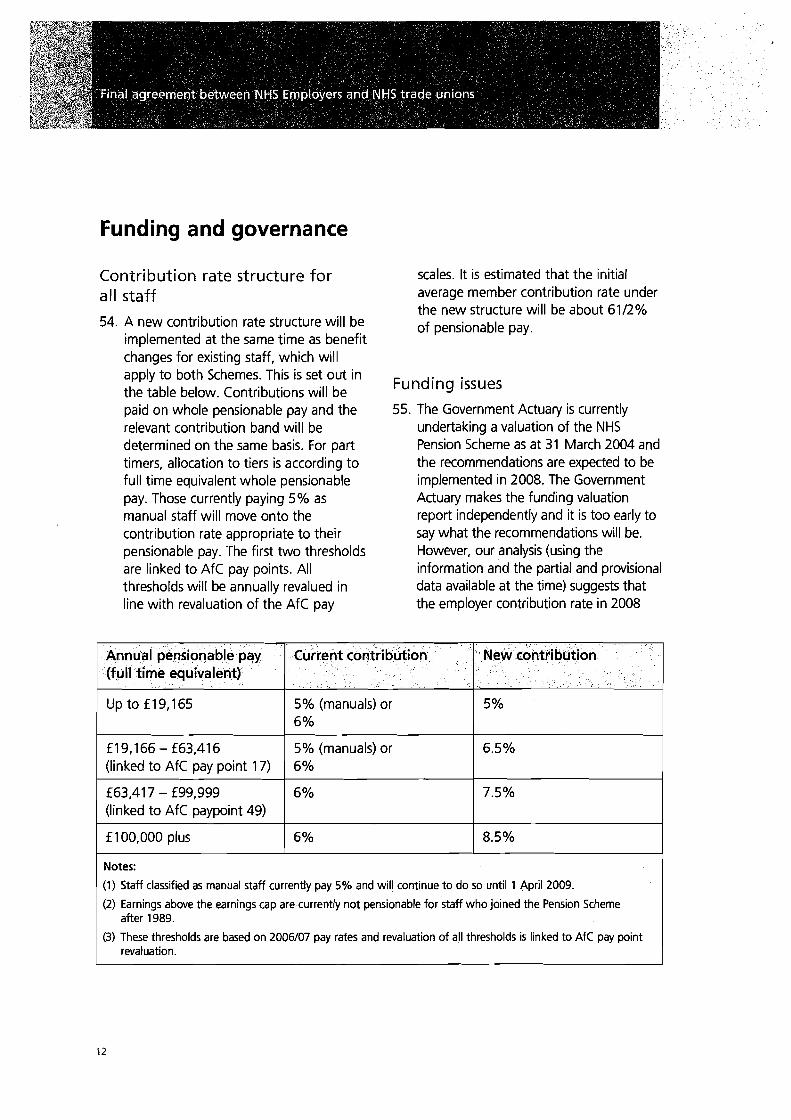

54. A new contribution rate structure will be implemented at the same time as benefit changes for existing staff, which will apply to both Schemes. This is set out in the table below. Contributions will be paid on whole pensionable pay and the relevant contribution band will be determined on the same basis. For part timers, allocation to tiers is according to full time equivalent whole pensionable pay. Those currently paying 5% as manual staff will move onto the contribution rate appropriate to their pensionable pay. The first two thresholds are linked to AfC pay points. All thresholds will be annually revalued in line with revaluation of the AfC pay

scales. It is estimated that the initial average member contribution rate under the new structure will be about 6112% of pensionable pay.

Funding issues

55. The Government Actuary is currently undertaking a valuation of the NHS Pension Scheme as at 31 March 2004 and the recommendations are expected to be implemented in 2008. The Government Actuary makes the funding valuation report independently and it is too early to say what the recommendations will be. However, our analysis (using the information and the partial and provisional data available at the time) suggests that the employer contribution rate in 2008

Up to £19,165 5% (manuals) or 1 6%

£19,166 - £63,416 5% (manuals) or 6.5% (linked to AfC pay point 17) 6%

New contribution Annual pensionable pay (full time equivalent)

Current contribution

Notes:

(1) Staff classified as manual staff currently pay 5% and will continue to do so until 1 April 2009.

(2) Earnings above the earnings cap are currently not pensionable for staff who joined the Pension Scheme after 1989.

(3) These thresholds are based on 2006/07 pay rates and revaluation of all thresholds is linked to AfC pay point revaluation.

(linked to AfC paypoint 49)

£ 1 00,000 plus 6% 8.5%

should not, assuming that the underlying assumptions remain appropriate, vary markedly from 14%.

Employer cap

56. An agreed aim is to maintain employer contributions at or just above the 14% level and employee contributions at the levels tabulated on page 12 until 201 6. Reductions in the employer contribution rate would therefore not take place. Any surplus as a result of this will be used to reduce any upward pressure on the member contribution rate over a 15 year period after 201 6.

57. An overall cap on employer contributions of 14.2% will apply in 2008 and 2012 (when the 2008 valuation is expected to be implemented). This means employers would pick up the first part of any contribution rate increase up to a maximum 14.2% employer contribution. If costs had increased so as to require any further increase, this would fall to employees in the form of contribution increases, benefit changes or some mixture of the two.

58. Employer contributions will be capped at 14% from 2016 (when it is expected that the results of the 2012 valuation will be implemented).

59. The basic principle behind the design and application of cost sharing and capping is that factors that change the expected value of members' benefits, as assessed by the scheme actuary, should be taken into account.

60. Costs in the Scheme, as determined at successive actuarial valuations, are a

function of factors falling into five main categories:

1. Valuation membership data (reflecting 'various elements of actual past experience such as pay increases).

2. Demographic assumptions (set having regard to available data on past experience, including members' past behaviour, and projected where appropriate).

3. Financial assumptions such as gross and net discount rate.

4. The benefit structure (and how benefits are calculated in practice).

5. The actuarial methodology.

61. Examples of the factors in category (2) (which are generally scheme-specific) include pensioner longevity, staff turnover, retirement age, incidence of ill health retirement and pay progression (relative to price inflation).

62. The financial experience of the Scheme is tracked using a system known as the Superannuation Contributions Adjusted for Past Experience (SCAPE) system under which a notional fund of assets is maintained to which income is credited, benefit outgo is debited and to which investment return is credited at a rate equal to actual price inflation plus the assumed net rate of return. The rate of return net of assumed price inflation is set by HM Treasury in consultation with the Government Actuary.

63. The cost sharing and capping arrangements will apply in relation to those factors that change the expected value of members' benefits as assessed by the Scheme actuary, but will generally

not apply in relation to the effects of changes within categories (3) and (5). The cost implications of any changes under (4) that were made to meet external requirements such as over-riding pensions legislation, would need be addressed separately when they arose, but changes under (4) which were made within the governance framework of the Scheme, would be included within the cost sharing and capping arrangements.

64. In the valuation report, the Government Actuary will be required to identify those elements materially contributing to a change in costs, grouped according to the category into which they are assumed to fall.

Governance arrangements

65. A partnership group, involving staff side representatives reporting to the Staff Council, and management representatives, with access to independent actuarial expert advice agreed in partnership, will be set up to advise the health departments. The partnership group will:

initially support implementation of the agreement; for instance advising on the terms and conduct of the choice exercise, other provisions in this agreement and on information that might be desirable for future valuations

also keep under review equality issues including 'red circling' (transitional retention of some provisions for some members) and whether, and to what extent, current arrangements might need to change

at future valuations, consider emerging valuation work in the light of the agreed basis for cost sharing.

66. Subject to the overall employer cap, the group will make recommendations to government (health departments and HM Treasury) on how to implement the valuation results, in terms of any increase (or decrease) to employee contributions or alternatively changes to the benefit structure to reduce (or increase) costs. Initially this will include consideration in the light of increases in final salary in the run up to retirement under the NHS Pension Scheme (1 April 2008 and after terms), whether any additional protective arrangements might avoid increases in costs that would ultimately be met by the rest of the membership.

67. The output of this work would form recommendations to the government who would decide on, and consult on, any regulations needed to implement changes. In some cases, the changes in value may be due to other factors such as legislative changes that might be imposed from outside the Scheme, and the treatment of these would be agreed as and when they arose. Changes in financial assumptions and actuarial methodology generally fall outside the cost sharing and capping arrangements (paras 60-63).

Reduction in pension costs

68. It is possible that in the future, the costs of the Pension Scheme might reduce. If this was to happen any reductions in the costs of the Scheme would go to the member until the overall contribution

rate returned to 20.4%. Any subsequent reductions below 20.4% would be shared on a 50% employee and 50% employer basis, as would any subsequent cost increases back to 20.4% and the employer 14% cap.

Overall scheme costs

69. The effect of this agreement has been modelled by the Government Actuary's Department and the results of its projections are set out in the attached tables (Annex A).

Pension data

70. The current review was hampered by difficulties in accessing information and

the difficulty in comparing pension information with that held by recognised staff groups. The review partners recommend that pension information is in future made available using the same definition for staff groups used by the census. This needs to cover issues such as pensionable service, average retirement rates, average pensions and incidence of ill health retirement. It is also recommended that information be available by ethnicity, sexual orientation, gender, disability and religion, along with any other statutory data that should be collected. This will be important in informing this process of review and allowing benchmarking (establishing baseline data for the key equality areas).

Annex A

NHS Pension Scheme Review: projections of future costs and contribution rates (GAD cost projections)

During the negotiations, the review partners took account of projections of future costs and contribution rates and these tables reflect projected outcomes when the changes in this qgreement are implemented. In the light of NHS pay modernisation and AfC, it was recognised that there could be a long term impact on key factors that affect the cost of the Scheme and the review partners considered a range of different scenarios. In particular, scenarios focused on the explicit aims of pay reform to improve retention of staff and to enable staff to progress their careers through the skills escalator. It was also recognised that both AfC and the consultant contract had increased the potential for incremental progression. The four scenarios considered include the potential impact of a gradual reduction in withdrawal rates so that after about 25 years, they had reduced by 25%. They also cover the potential impact of an increase in career pay progression, as a result of improved incremental progression and the skill escalator considering a phased increase to an improvement of 0.32% or 0.75% per annum salary progression relative to recent experience.

In addition, in each scenario, mortality assumptions (which are derived from standard tables adjusted to reflect recent scheme experience) include projected future improvements to mid-century, in accordance with the standard approach adopted for work underlying the PSF agreement.

In each scenario, the general medical practitioner final dynamisation factors over the five financial years 2003108 are assumed to compound to 48%. No allowance has been made for any potential loss of member contribution yield arising because practitioners may be allocated to a contribution tier on the basis of actual pay rather than notional full time equivalent (FTE) pay.

The tables show the projected costs for both existing members who remain in the current NHS Pension Scheme and new entrants who will join the New NHS Pension Scheme. Given the difference in costs between the two Schemes, as the balance of membership in the two Schemes changes over time, it affects the overall costs of the NHS pension arrangements.

Scenario 1: 25% phased reduction in withdrawal rates & 0.75% pa phased increase in salary progression steepness

Scenario 2: 25% phased reduction in withdrawal rates & 0.32% pa phased increase in salary progression steepness

Year

2008

201 2

201 6

2020

2024

2028

2052

Total existing member cont rate

20.5%

21.1 %

21.4%

21.9%

22.7%

22.7%

22.8%

Year

2008

201 2

201 6

2020

2024

2028

2052

Total new entrant cont rate

18.9%

19.7%

20.2%

20.8%

21.3%

21.7%

22.6%

Total existing member cont rate

20.5%

20.7%

20.8%

21 .O%

21.5%

21.5%

21.6%

Total combined rate paid

20.5%

20.6%

20.8%

21.2%

21.6%

21.9%

22.6%

Total new entrant cont rate

18.9%

19.4%

19.8%

20.1 %

20.4%

20.7%

21.3%

Employers' cont rate paid

14.0%

14.1 %

14.0%

14.0%

14.0%

14.0%

14.0%

Total combined rate paid

20.5%

20.5%

20.2%

20.4%

20.6%

20.7%

21.3%

Members' average cont rate

6.5%

6.5%

6.8%

7.2%

7.6%

7.9%

8.6%

Employers' cont rate paid

14.0%

14.0%

13.8%

13.9%

14.0%

14.0%

14.0%

Members' average cont rate

6.5%

6.5%

6.4%

6.4%

6.6%

6.7%

7.3%

Scenario 3: no reduction in withdrawal rates but 0.32% pa phased increase in salary progression steepness

Scenario 4: no reduction in withdrawal rates & no increase in salary progression steepness - i.e. longevity improvement only

Year

2008

201 2

201 6

2020

2024

2028

2052

Total ex~sting member cont rate

20.5%

20.3%

20.2%

20.2%

20.6%

20.7%

21 .O%

Year

2008

201 2

201 6

2020

2024

2028

2052

Total new entrant cont rate cont rate

Total combined rate paid

20.5%

20.5%

19.1%

19.0%

19.1%

19.1%

19.8%

18.9%

19.1%

19.2%

19.5%

19.7%

19.9%

20.6%

Total existing member cont rate

20.5%

20.1 %

19.8%

19.7%

19.9%

19.9%

20.0%

Employers' cont rate paid

14.0%

14.0%

13.4%

13.3%

13.3%

13.3%

13.5%

Total new entrant cont rate

18.9%

18.9%

19.0%

19.0%

19.1%

19.2%

19.8%

20.5%

20.5%

19.5%

19.5%

19.7%

19.8%

20.6%

Members' average cont rate

6.5%

6.5%

5.7%

5.7%

5.7%

5.7%

6.3%

14.0%

14.0%

13.5%

13.5%

13.6%

13.7%

14.0%

6.5%

6.5%

6.0%

6.0%

6.1 %

6.1 %

6.6%

Annex B

lndex of Technical Advisory Group (TAG) papers These papers are the analytical papers for the Pensions Review produced by the Government Actuary's Department, setting out the costings and implications of the options that we considered. Each one has been peer reviewed by First Actuarial, the independent actuary engaged for the review.

TAG2006 - 01 - NHSPS COST PROJECTIONS

TAG2006 - 02 - SUPPLEMENTARY NOTE ON DEMOGRAPHICS

TAG2006 - 03 - CARE DISTRIBUTION OF OUTCOMES

TAG2006 - 04 - TIERED MEMBER CONTRIBUTION STRUCTURE

TAG2006 - 05 - RANGE OF POSSIBLE COST SHARING FORMULAE

TAG2006 - 06 - OPTIONS ON ABATEMENT IN NEW SCHEME

TAG2006 - 07 - RE-EMPLOYED FORMER MEMBERS OF EXISTING SCHEME

TAG2006 - 08 - EARLY AND LATE RETIREMENT FACTORS

TAG2006 - 08A - EARLY AND LATE RETIREMENT FACTORS APPLICATION

TAG2006 - 09 - COSTINGS FOR 1 JUNE STEERING GROUP

TAG2006 - 10 - EXISTING MEMBERS' OPlION TO SWITCH TO THE NEW SCHEME

TAG2006 - 11 - HIGH EARNERS ISSUES

TAG2006 - 12 - EXTRA DEATH IN SERVICE LUMP SLIM FOR LINPARTNERED MEMBERS

TAG2006 - 13 - SHORT TERM PENSIONS FOR DEPENDANTS

TAG2006 - 14 - MINOR CHANGES FOLLOWING ISSUE OF CONDOC

TAG2006 - 15 - PENSIONABLE RE-EMPLOYMENT

TAG2006 - 16 - DEATH DURING DRAWDOWN AND PENSIONABLE RE-EMPLOYMENT

lndex of Scheme review provision papers These papers set out the rationale and the intention of the changes being made to the NHS Pension Scheme. They set out the rules to be implemented in each area.

These papers are available at www.nhsemployers.org/pensionagreement

SRPl - Funding SRP1.l - Tiered contributions SRP1.2 - Normal Pension Age SRPl .3 - Minimum Pension Age SRP1.4 - Service limits SRP1.5 - Earnings limits

SRP2 - Death benefits SRP2.1 - Survivor pensions SRP2.2 - Initial survivor pensions SRP2.3 - Child allowance SRP2.4 - Lump sum on death

SRP3 - Building the pension SRP3.1 - Accrual rates, dynamising and late

retirement factors SRP3.2 - Additional pension SRP3.3 - Final pensionable pay SRP3.4 - Voluntary protected pay

SRP4 - Taking the pension SRP4.1 - Draw down SRP4.2 - Abatement and suspension SRP4.3 - Lump sum commutation

SRP5 - Scheme membership SRP5.1 - Scheme membership eligibility SRP5.2 - Choice exercise

SRP6 - Governance SRP6.1 - Valuation SRP6.2 - Cost sharing

Contact us

hlHS Employers 29 Bressenden Place 2 Brewery Wharf London Kendell Street SW1 E 5DD Leeds L S l O 1JR

This document is available in pdf format at www.nhsemployers.org/publications Published September 2007 O NHS Employers 2007. This document may not be reproduced in whole or in part without permission. The NHS Confederation (Employers) Company Ltd Registered in England. Company limited by guarantee: number 5252407

NHS Pension Scheme Review Final agreement on changes to the NHS Pension Scheme

The changes t o the NHS Pension Scheme have now been agreed for England and Wales. The agreement concludes four years of partnership working between NHS Employers and the NHS trade unions. It delivers a Scheme that meets the needs of a modern NHS and i t s staff, and is sustainable in the longer term.

This f a d sheet tells you about the main changes for both existing and new members, when the changes arc likely to happen, and what employers will be required t o do t o support implementation.

What is changing in the NHS Pension Scheme?

members, will both be introduced on 1 April 2008. Existing members will have a one-off choice to move to the new Scheme,

An updated Scheme is being introduced for which is planned to run from July 2009 to existing members that keeps most of the 30 June 201 0. current benefits, as well as introducing new ones, alongside a new Scheme for new members. Existing members will have a one-off choice of moving to the new members' Scheme.

When will the changes be introduced?

Changes to the Scheme for existing members and the New NHS Pension Scheme for new

What do employers need to do?

Employers need to communicate the Scheme changes to staff and there is a range of materials at www.nhsernpIoyers.org/ pensionagreement to help you do this. In addition, the Business Services Authori€y (BSA) Pensions Division will be wnding all employers a printed leaflet about the changes for staff, which will be with employers for

distribution with November payslips. Employers will need to ensure that staff who join the NHS between now and 3'1 March 2008, are given a copy of the insert. They will also need to support some staff that have options to think about now (see the More details section on page 6).

New data requirements for employers

Employers will also need to provide new data to support the Scheme changes, including the new contribution rates. The Electronic Staff Records

(ESR) project team and the Department of Health are currently identifying the information required and how best to support all employers, including those who do not have ESR.

Will err~ployer contributions change?

No. We expect that the employer's contribution will continue to be around 14% which is still 2Brds of the overall pension cost. As part of the negotiations, NHS Employers has ensured that in the longer term, employer costs will stay at 14%.

The updated NHS Pension Scheme for existing members - introduced on 1 April 2008

The updated NHS Pension Scheme will New option to take more pension as a continue to offer most of the current benefits tax-free lump sum - staff will be able to that staff and employers said were important take up to 25% of the value of their to them such as final salary, as well as a pension fund in return for a smaller range of new benefits like-the option to take pension, giving up £1 of pension for every more pension as a tax free lump sum. f 12 of lump sum. This will give staff more However, there will also be new contribution flexib~lity on retirement. rates to give a fairer way to fund new benefits and future costs.

Keep final salary pension - this will still be calculated on the highest pensionable pay in the last three years of paying into the pension and still accrued at 1180th of pensionable pay, for every year of paying into the Scheme. Existing members will also continue to get a lump sum of 3180th~ of their pension.

Keep the current Normal Pension Age (NPA) - for most staff this is 60 years, or 55 years for those with special class status. Most staff will still have a minimum pension age of 50.

New option to continue paying into the pension for longer - staff who have not yet retired, can carry on paying into, and building up, their pension for a total of 45 years regardless of their age.

More flexibility in the run-up to retirement - after age 50, staff can step down to a less demanding role on a lower salary, with protection for the pension that they have already built up. However, this only applies if there is a permanent reduction of at least 10% in pensionable pay that is certified (not approved) by the employer.

No earnings cap - for service after 1 April 2008, the current earnings cap of f 1 1 2,800 for 2007/2008 will be removed. However, service before 1 April 2008 will still be subject to the cap of £ 112,800. This will also apply to the earnings cap for dental practitioners called the maximum allowable remuneration (MAR).

A new option for staf f to top up pension, to replace added yesn - staff will be able to purchase up to a total of f 5,000 of additional pension, either as one lump sum or in smaller amounts of £250. any time up to and including age 60, over a total period of 20 yean. Total annual pension contributions will be limited to the total of pensionable pay. Staff will be able to

choose between buying additional pension for single life or with survivor benefits.

This replaces the facility to buy added years but existing contracts will be honoured.

Current money purchase Added Voluntary Comtribrctions (AVO) continues - this gives current members an alternative to the additional purchase facility outlined above.

In future, thou who get suwhror p c n s h follawing the death of an active member, will keep them for Rfe - this will apply even if they re-marry, enter a new civil partnership or co-habit.

Eligibla umrplarriaB prfncrs d l now get nmrivor pelssioms - an eligible partner is anyone who is not married or in a civil partnership, but is nominated to receive a pension and is someone who the member has an exclusive long-term committed relationship with, in which they are financially dependent or inter-dependent.

New contribution rates - individual contributions will be directly linked to earnings. The review partners believe this is a fairer way to fund new benefits and future costs. Individual contribution rates will depend on individuals' pensionable pay or the full time equivalent if they work part time.

The new rates are outlined below and will be introduced on 1 April 2008.

These thresholds are based on 200W7 pay rates and pay thresholds (eg f19.166) will be adjusted in line with Agenda for Change pay awards.

Work is ongoing to confirm detailed next steps for employers, for implementing the new rates.

A range of further improvements - other improvements to the existing Scheme include survivor pensions for children up to age 23; the ability to nominate a number of beneficiaries for the death in service benefit; and going forward, the short term death in service benefit will be standardised at six months.

Ernpbyers continue to contribute around 14% -this is around Znrds of the overall cost of an individual's pension.

-the revised scheme for existing practitioner members (GPs and dentists)

Keep a CARE pension - their Career Average Revalued Earnings (CARE) pension will continue to have an accrual rate of 1.4% and a lump sum of 4.2%.

More stability in annual revaluations - from 1 April 2008, active members' pension will be dynamised annually by the Retail Prices Index (RPI) plus 1.5%, which is broadly in line with the movement in national average earnings.

The New NHS Pension Scheme for new members - introduced on 1 April 2008, with a one-off choice for existing members, planned from 1 July 2009

The New NHS Pension Scheme for new members offers a range of flexibilities to suit different working patterns, particularly in the run-up to retirement. For employers, it gives staff more options such as stepping down to a less demanding role and taking part of their pension, or being able to return to work after they have retired and rejoin the Scheme. Existing members will have a one-off choice to move to this Scheme, which is currently planned for 1 July 2009 to 30 June 201 0.

A final salary pension - this will be based on the average of the best three consecutive years in pensionable pay, in the last ten years' of working, and calculated on a higher accrual rate of 1/60th of pensionable pay and revalued by RPI. This gives staff more options in the run-up to retirement like taking on a lower paid role but knowing that their pension will still be based on their earlier, higher earning years.

pension whilst still working. Whatever they decide to do, they can only take their pension in three portions (no more), so if they have drawn down part of their pension twice before, they must take all their remaining pension when they finally retire.

No age limits on service - they can continue to pay into their pension for as long as they are working, up to a total of 45 years, regardless of their age.

More options om lump sum - they can take up to 25% of their pension as a lump sum or take all their income as a pension, or flex anywhere between the two. They will give up f 1 of pension for every f 12 of lump sum.

Choice of options to t q up their pension - the options are the same as those for existing members (see new option for staff to top up pension on page 3) but payable at 65 years of age.

An NPA of 65 years - this wiH be on ContriMiom rates linked to individual an unreduced pension at 65 years but earnings - exactly the same as those for with more flexibilities for those who want existing members (see the contribution to retire earlier or later. New members rate table on page 4). will be able to retire after 55 years on a reduced pension, or they can continue Further benefits - survivor pensions for working to age 75 to get an enhrKed life; survivor pensions for children aged pension, or start taking part of their up to 23 yean; the ability to nominate

New Scheme for new practitioner members (GPs and dentists)

A CARE pension - wlth an accrual rate of 1.87% and the option to take up to 25% of their pension as a lump sum with a reduced pension.

more than one beneficiary for death in service benefit and getting the Annual revaluations - for active short-term death in service benefit for members, annual dynamisation will be six months. by RPI plus 1.5%.

More details

Who will be supporting employers through implementation?

The BSA Pensions Division is the Scheme administrators and is responsible for implementing the changes. They will be supporting employers throughout the period leading up to and including the implementation, and will be contacting you to ensure that processes to administer the changes are in place in time. You can visit their website at www.pensions.nhsbsa.nhs.uk to register for email alerts to notify you of any new information as it becomes available.

Are there staff who need to make a decision now?

Most staff don't need to do anything in the short term. However, the following staff will need to think about their options now: those who are thinking about retiring in the next three years, those who are leaving the NHS

and deferring their pension, or any staff who want to buy added years before it is replaced by the new option to buy added pension (applications for added years need to be in by 31 March 2008). The Pensions Division has produced a range of factsheets on the changes including ones for specific groups such as those who are planning to retire. This information is available on the Pensions Division's website a t www.nhspensions.nhsbsa.nhs.uk

What about those people who have left the IVHS and deferred their benefits in the Scheme?

Deferred members, who return within rive years of leaving or before 1 April 2008, will return to the updated NHS Pension Scheme and will be given a choice to transfer to the New NHS Pension Scheme for new members. 'Those who return after five years will join the New Scheme for future service but will be given a

c.;<,;y,:<;>,': ;, :.,~.~;,;,~;,,.i.:.:.;!:::\ ,/.. Y,, .=To - .-..,.... .;, ? ' . ~ t .,:.:::. ".- ' ." : ,,>,. ;: .r>; .::,,.: .>.:.. ?,%:..: *a:'.!-.q..;>;,;<>:;:;. ; >,, . ,.., >-, ;,> .yf; %.,.:: ,;c; : :! .2 -!

; 5 2 ~ ~ ~ f i g ~ ~ s ~ d f i . r c a e & & < ~ ~ ~ E 2 6 k ~ : i ! f ; ; ; i ; ; ; ~ how the changes will affect staff and when, , , ; : , ~ - , and how, they will be introduced see :~:anfl~(ng~n~~;~~s~~,,p~~~~~@$~::~;;$$3>;~;', .:- . % . , ,,,,-a pe nsions.n hsbsa. hs. including ,;9i;:.:;?>.$:j,,;; ;);;+;>:;,.,+;;? ;,y: ;<;: sv~::;<;;$~$~;<;3::< ;:tj.>,z;;-;;.. .-. I . . : . . . :--,.- >,. ,. . . . .. . - i ; . . ; ,..- ' . ' . . fad sheets for specific staff groups such as

deferred members and a ready reckoner to choice on whether to transfer their help staff calculate their new contribution deferred service to the New Scheme. rate and options on lump sum. New staff who join the Scheme on or after 1 April 2008, will also join the New Scheme for new members.

The Pensions Division will be contacting deferred members at their last known address to advise them of the changes.

Where can I find out more?

This fact sheet only outlines the key changes to the Scheme for existing and new members. For details on:

all the changes visit www.nhsemployers. orglpensionagreement to see copies of this summary, Q&As, case studies illustrating the changes and a template presentation and editorial to support staff cascades

Contact us

NHS Employers 29 Bressenden Place 2 Brewery Wharf London Kendell Street SW1 E 5DD Leeds LSlO 1 JR

This document is available in pdf format at www.nhsemployers.org/publications Published September 2007 O NHS Employers 2007. This document may not be reproduced in whole or in part without permission. The NHS Confederation (Employers) Company Ltd Registered in England. Company limited by guarantee: number 5252407

Related Documents