Frances Cheung – Credit Agricole, Senior Strategist, Asia ex-Japan Zhi Ming Zhang – HSBC, Managing Director, Head of China Research Dr Amanda Lee – Deutsche Bank, Asia Head of Index Development Zhiming Yang – Deutsche Bank, Quantitative Trader Michael Chan – Hong Kong Exchange, Assistant Vice President CNH investor showcase 2012 Global Structured Note news, data, analytics and events

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Frances Cheung – Credit Agricole, Senior Strategist, Asia ex-Japan

Zhi Ming Zhang – HSBC, Managing Director, Head of China Research

Dr Amanda Lee – Deutsche Bank, Asia Head of Index Development

Zhiming Yang – Deutsche Bank, Quantitative Trader

Michael Chan – Hong Kong Exchange, Assistant Vice President

CNH investor showcase 2012

Global Structured Note news,data, analytics and events

https://catalystresearch.ca-cib.comCrédit Agricole Corporate and Investment Bank is authorised by the Autorité de Contrôle Prudentiel (ACP) and supervised by the ACP and the Autoritédes Marchés Financiers (AMF) in France and subject to limited regulation by the Financial Services Authority. Details about the extent of our regulation by the Financial Services Authority are available from us on request.

Frances CheungSenior StrategistAsia ex-Japan+852 2826 [email protected]

Offshore RMB market outlookOctober 2012

2Development of the offshore RMB market…

Sources: CBC, FSC, HKMA, PBoC, Credit Agricole CIB

Offshore market development Taiwan-specific

2004 Personal RMB biz in Hong Kong

2005 Personal RMB cash biz in Kinmen and matsu

2007 Offshore RMB bonds (retail) issued in HK 人民幣現鈔買賣於金門馬祖試辦

Jun 2008 Personal RMB cash biz in Taiwan

臺灣民眾可以向已經核准的金融機構及外幣收兌處,進行人民幣2萬元以內的現鈔買賣

2009RMB trade settlement - pilot schemefor HK and Macau initially

Jun 2010 RMB trade settlement scheme extended to the rest of the world

Jul 2010 Emerging of the CNH market RMB cash settlement with PBoC via Bank of China

人民幣在臺灣地區管理及清算辦法

Aug 2010Eligible entities to invest in China's interbank bond market

Jan 2011Non-financial Mainland corporatesto conduct outward FDI in RMB

Mar 2011 Cap on investment iin securities listed on mainland Chinaraised to 30% from 10% of net asset value

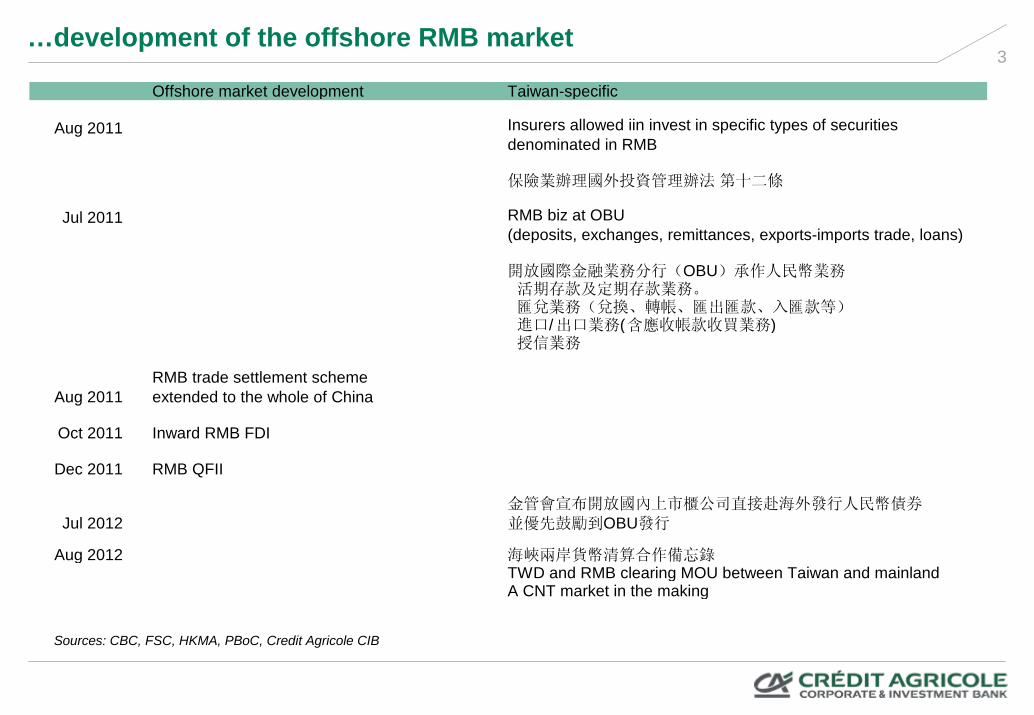

3…development of the offshore RMB market

Sources: CBC, FSC, HKMA, PBoC, Credit Agricole CIB

Offshore market development Taiwan-specific

Aug 2011 Insurers allowed iin invest in specific types of securitiesdenominated in RMB

保險業辦理國外投資管理辦法 第十二條

Jul 2011 RMB biz at OBU(deposits, exchanges, remittances, exports-imports trade, loans)

開放國際金融業務分行(OBU)承作人民幣業務活期存款及定期存款業務。匯兌業務(兌換、轉帳、匯出匯款、入匯款等)進口/出口業務(含應收帳款收買業務)授信業務

Aug 2011RMB trade settlement schemeextended to the whole of China

Oct 2011 Inward RMB FDI

Dec 2011 RMB QFII

Jul 2012金管會宣布開放國內上市櫃公司直接赴海外發行人民幣債券並優先鼓勵到OBU發行

Aug 2012 海峽兩岸貨幣清算合作備忘錄TWD and RMB clearing MOU between Taiwan and mainland A CNT market in the making

4Sources of offshore RMB…

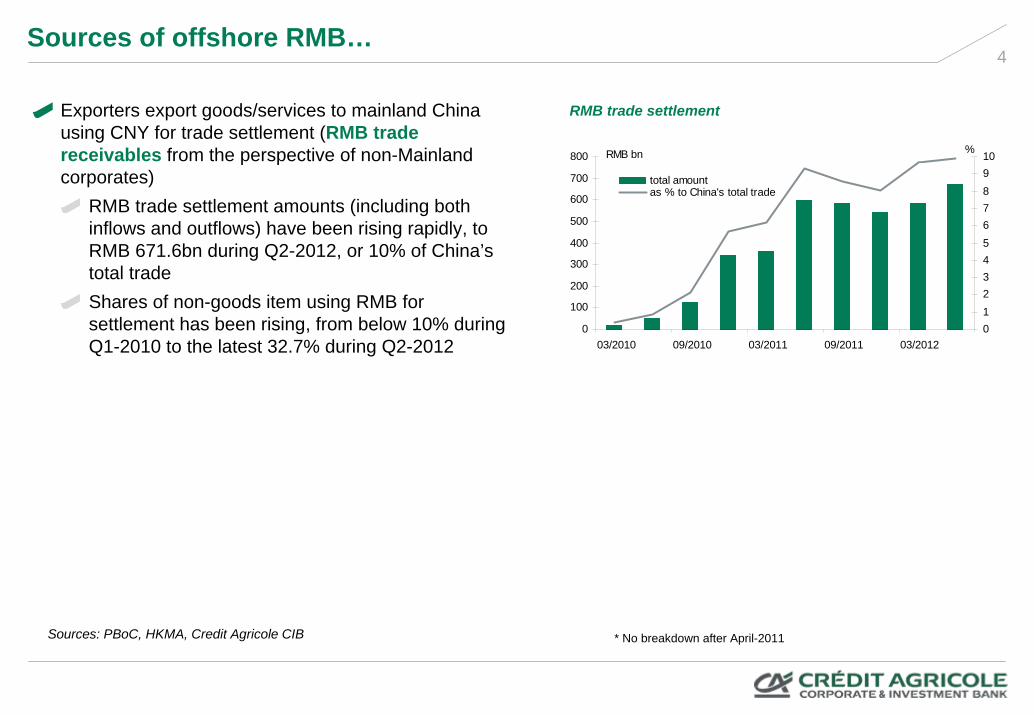

Exporters export goods/services to mainland China using CNY for trade settlement (RMB trade receivables from the perspective of non-Mainland corporates)

RMB trade settlement amounts (including both inflows and outflows) have been rising rapidly, to RMB 671.6bn during Q2-2012, or 10% of China’s total tradeShares of non-goods item using RMB for settlement has been rising, from below 10% during Q1-2010 to the latest 32.7% during Q2-2012

Sources: PBoC, HKMA, Credit Agricole CIB

RMB trade settlement

* No breakdown after April-2011

0

100

200

300

400

500

600

700

800

03/2010 09/2010 03/2011 09/2011 03/2012

RMB bn

012345678910%

total amountas % to China's total trade

5…sources of offshore RMB

Individuals in Hong Kong and Taiwan exchangeforeign currencies for RMBRMB from inbound touristsNon-financial Mainland China companies conduct RMB-settled outward FDIFX swap lines with foreign central banks

Sources: PBoC, HKMA, Credit Agricole CIB

RMB deposits at OBU, Taiwan

RMB deposits in Hong Kong

* No breakdown after April-2011

0

2

4

6

8

10

12

14

16

18

Aug-11 Oct-11 Dec-11 Feb-12 Apr-12 Jun-12

RMB bn

RMB deposits at OBU

Offshore RMB deposit

0

100

200

300

400

500

600

Hong Kong Taiw an Singapore UK

USD bn

0

100

200

300

400

500

600

700

Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

CNY bn

Personal account Corporate account

6Taiwan-China Link - trade

China’s trade deficit is the largest with Taiwan - a source for RMB for TaiwanOf China’s total trade (imports and exports), Taiwan constitutes 4%, Singapore constitutes 2%

Sources: CEIC, Crédit Agricole CIB

China-Taiwan trade

-6

-4

-2

0

2

4

6

8

10

12

14

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

USD bn

Exports to China Imports from China

Share of total trade (exports + imports) with China

Singapore, 2%

Others, 84%

Malaysia, 2%

Taiwan, 4%

Hong Kong, 8%

7Taiwan-China Link - FDI

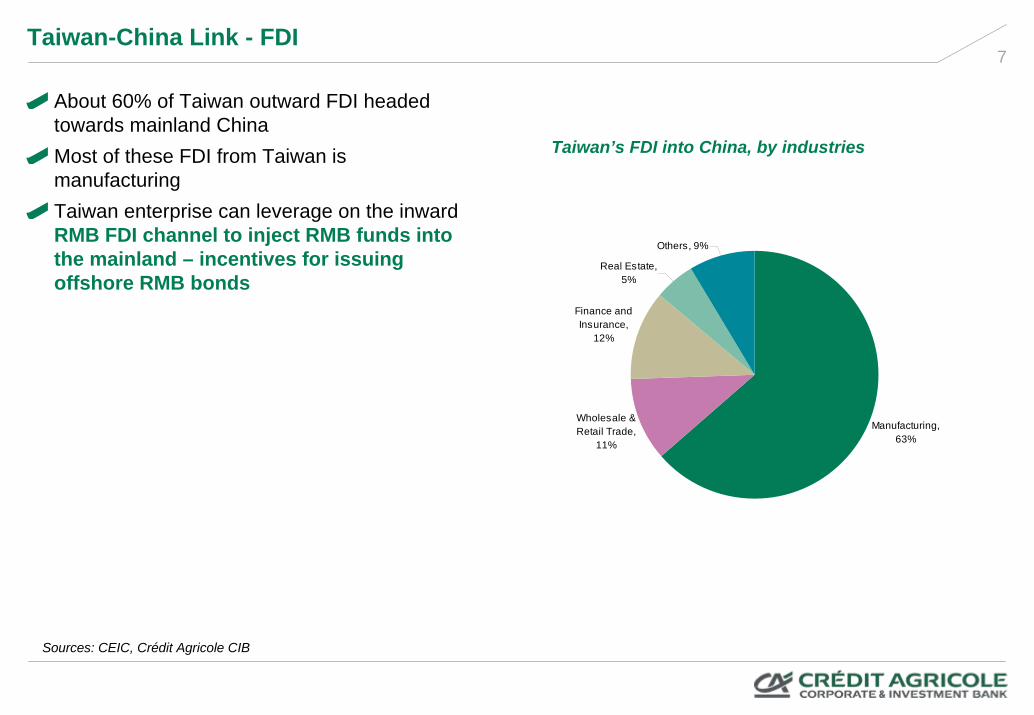

About 60% of Taiwan outward FDI headed towards mainland ChinaMost of these FDI from Taiwan is manufacturingTaiwan enterprise can leverage on the inward RMB FDI channel to inject RMB funds into the mainland – incentives for issuing offshore RMB bonds

Sources: CEIC, Crédit Agricole CIB

Taiwan’s FDI into China, by industries

Manufacturing, 63%

Wholesale & Retail Trade,

11%

Finance and Insurance,

12%

Real Estate, 5%

Others, 9%

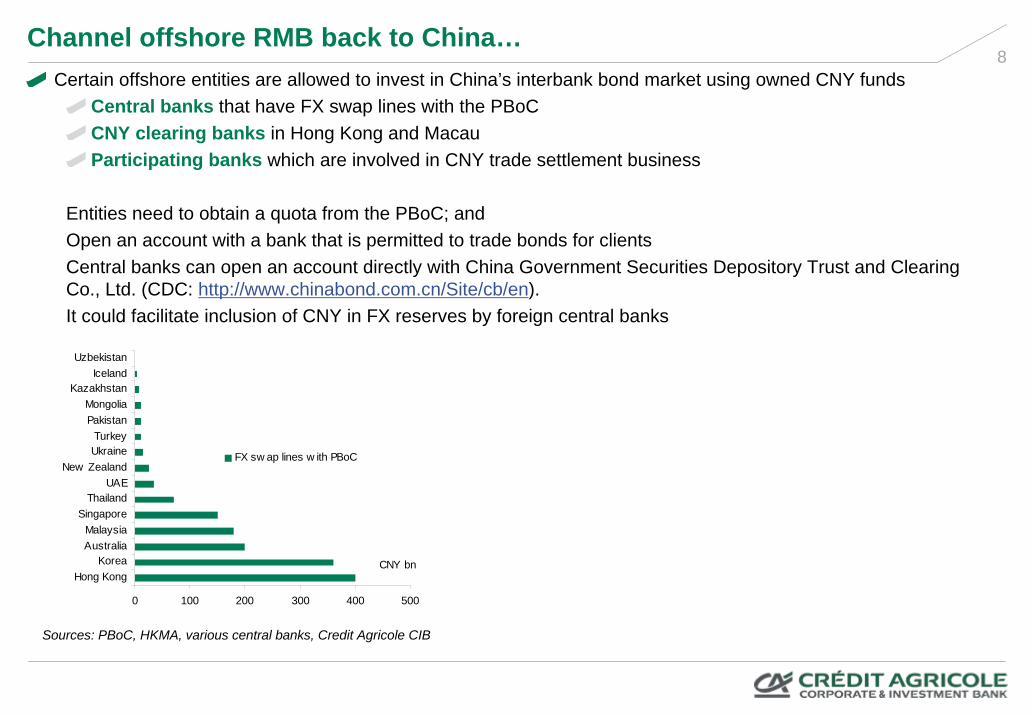

8Channel offshore RMB back to China…

Certain offshore entities are allowed to invest in China’s interbank bond market using owned CNY fundsCentral banks that have FX swap lines with the PBoCCNY clearing banks in Hong Kong and MacauParticipating banks which are involved in CNY trade settlement business

Entities need to obtain a quota from the PBoC; andOpen an account with a bank that is permitted to trade bonds for clientsCentral banks can open an account directly with China Government Securities Depository Trust and Clearing Co., Ltd. (CDC: http://www.chinabond.com.cn/Site/cb/en).It could facilitate inclusion of CNY in FX reserves by foreign central banks

Sources: PBoC, HKMA, various central banks, Credit Agricole CIB

0 100 200 300 400 500

Hong KongKorea

AustraliaMalaysia

SingaporeThailand

UAENew Zealand

UkraineTurkey

PakistanMongolia

KazakhstanIceland

Uzbekistan

CNY bn

FX sw ap lines w ith PBoC

9…channel offshore CNY back to China

RMB-QFIIAllow investment of offshore RMB in onshore securitiesInitial quota: RMB 20bnThis provides investment alternatives for entities holding RMB offshore, which could potentially push up

CNH yields which are lower than onshore CNY yields

RMB inward FDIPBoC notice 145 in Jun 2011: policy direction to allow inward FDI into China using CNYLatest: 13 Oct 2011: PBoC set out procedures for foreign entities to conduct RMB FDI into ChinaThis provides a major channel through which offshore CNY can flow back to China: raise incentive to raise

offshore CNY funds

Promote via the usual trade routeRecently, there were months during which CNH pool accumulation was slow, while overall RMB trade

settlement volume was still large, suggesting RMB-settled trade has become more balanced in terms of shares of exports and imports.

During some months with slow CNH pool growth or drop in CNH pool, HKMA said it was due to the fact that the amount of CNY payments from HK to China exceeded payment from China to HK, regarding trade settlement

Sources: PBoC, HKMA, Credit Agricole CIB

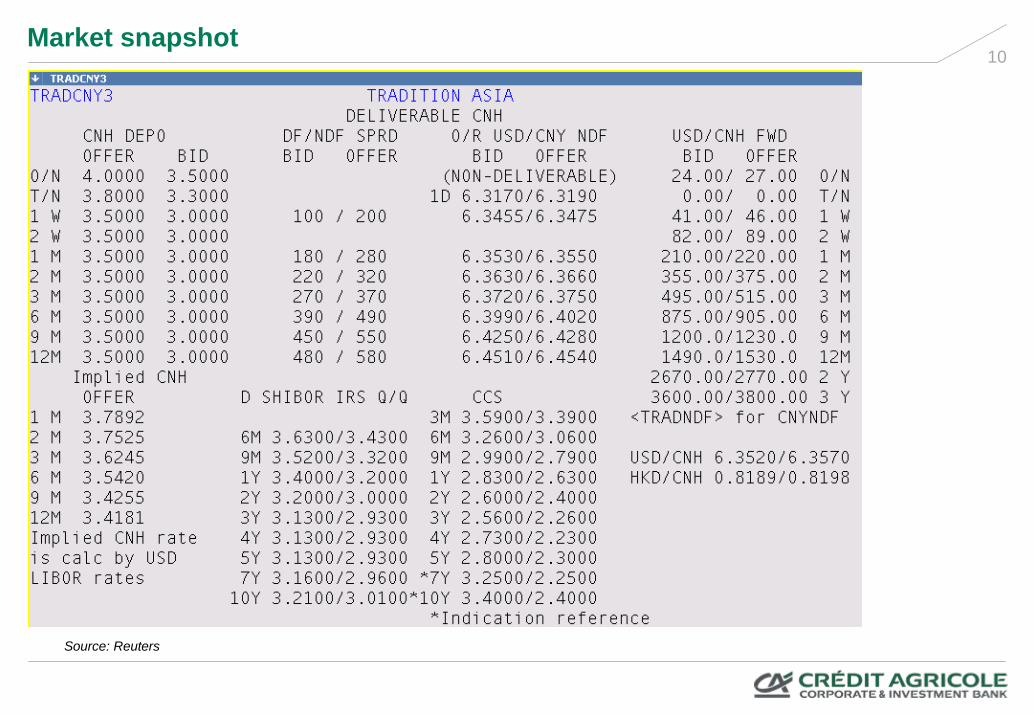

10Market snapshot

Source: Reuters

11CNH spot

Trading volumeUSD 1.5-2.0bn per dayTrade size: USD 5-10mn

Outlook for spot CNH vs CNYCNH initially traded at a premium due to limited supplyDuring risk-off times in late 2011, CNH was traded at a discount to CNYLooking ahead, when market stabilises, CNH may still tend to trade at a premium to CNYWe expect USD/CNH to go down vis-à-vis USD/CNY on tight CNH liquidity

Sources: Bloomberg, Crédit Agricole CIB

6.2

6.3

6.4

6.5

6.6

6.7

6.8

6.9

Aug-10 Nov-10 Feb-11 May-11 Aug-11 Nov-11 Feb-12 May-12 Aug-12-2000

-1500

-1000

-500

0

500

1000

1500

2000pips

spread (RHS)spot USD/CNHspot USD/CNY

12

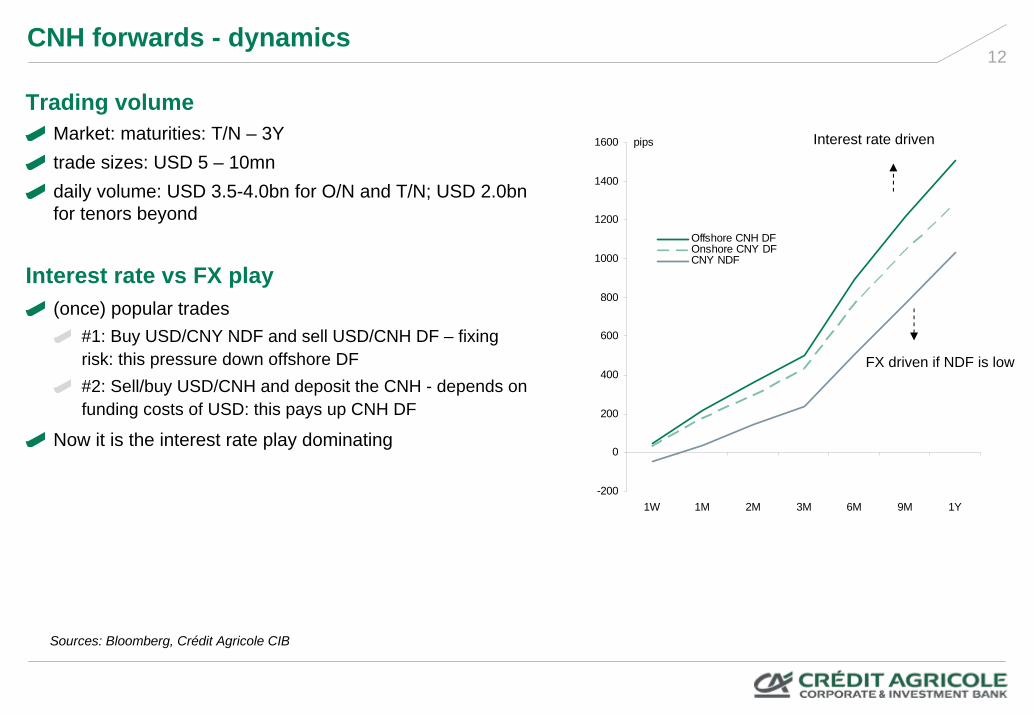

Sources: Bloomberg, Crédit Agricole CIB

Trading volumeMarket: maturities: T/N – 3Ytrade sizes: USD 5 – 10mndaily volume: USD 3.5-4.0bn for O/N and T/N; USD 2.0bn for tenors beyond

Interest rate vs FX play(once) popular trades

#1: Buy USD/CNY NDF and sell USD/CNH DF – fixing risk: this pressure down offshore DF#2: Sell/buy USD/CNH and deposit the CNH - depends on funding costs of USD: this pays up CNH DF

Now it is the interest rate play dominating

CNH forwards - dynamics

-200

0

200

400

600

800

1000

1200

1400

1600

1W 1M 2M 3M 6M 9M 1Y

pips

Offshore CNH DFOnshore CNY DFCNY NDF

Interest rate driven

FX driven if NDF is low

13

Sources: Bloomberg, Crédit Agricole CIB

To be launched on 17 September 2012

Contract size: USD 100,000 Contract months: spot month, the next 3 calendar months, the next 3 calendar quarter monthsSettlement: Delivery of USD by the seller; and payment of the final settlement value in RMB by the buyerFinal settlement price: spot USD/CNY(HK) fixing published by the Hong Kong Treasury Markets Association at 11:15am on the last trading day

CNH futures

14CNH options

Source: Bloomberg, Crédit Agricole CIB

Trading: USD 200-400mn per day

Liquid up to 1Y

Implied 3M vols - USDCNY (offshore) & USDCNH options

0

1

2

3

4

5

5C 20C 35C ATM 35P 20P 5P

USDCNY offshore - 30 Aug 2012USDCNY offshore - 30 Aug 2011USDCNH 30 Aug 2012USDCNH 30 Aug 2011

15

Sources: Bloomberg, TMA, Crédit Agricole CIB

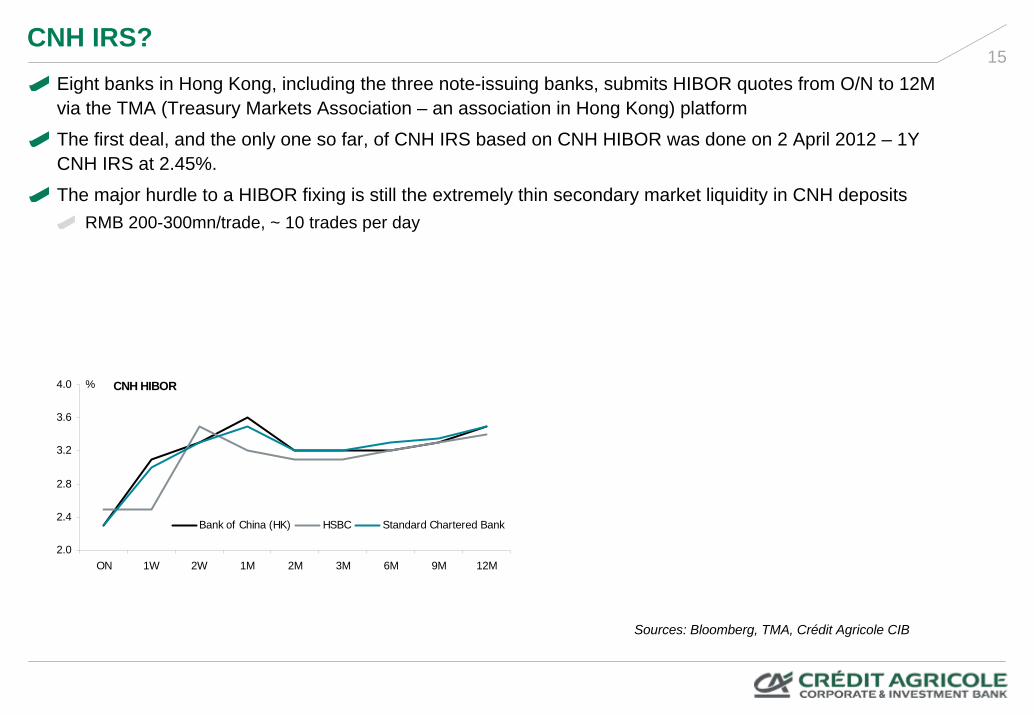

Eight banks in Hong Kong, including the three note-issuing banks, submits HIBOR quotes from O/N to 12M via the TMA (Treasury Markets Association – an association in Hong Kong) platform

The first deal, and the only one so far, of CNH IRS based on CNH HIBOR was done on 2 April 2012 – 1Y CNH IRS at 2.45%.

The major hurdle to a HIBOR fixing is still the extremely thin secondary market liquidity in CNH depositsRMB 200-300mn/trade, ~ 10 trades per day

CNH IRS?

CNH HIBOR

2.0

2.4

2.8

3.2

3.6

4.0

ON 1W 2W 1M 2M 3M 6M 9M 12M

%

Bank of China (HK) HSBC Standard Chartered Bank

16CNH CCS – cross currency swap

Sources: Bloomberg, Crédit Agricole CIB

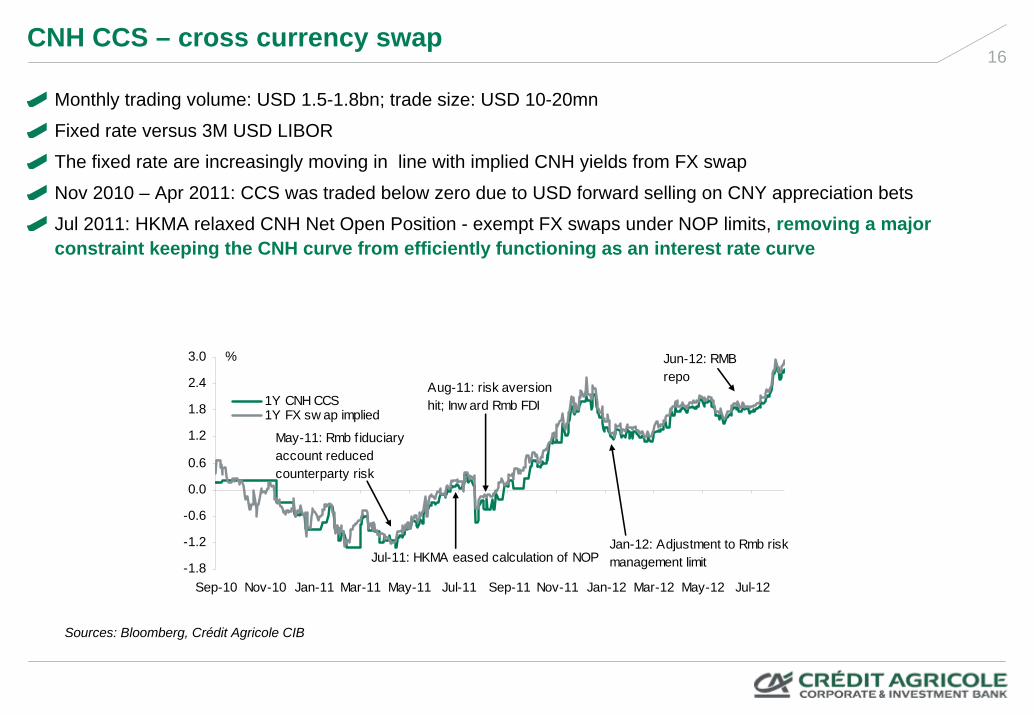

Monthly trading volume: USD 1.5-1.8bn; trade size: USD 10-20mn

Fixed rate versus 3M USD LIBOR

The fixed rate are increasingly moving in line with implied CNH yields from FX swap

Nov 2010 – Apr 2011: CCS was traded below zero due to USD forward selling on CNY appreciation bets

Jul 2011: HKMA relaxed CNH Net Open Position - exempt FX swaps under NOP limits, removing a major constraint keeping the CNH curve from efficiently functioning as an interest rate curve

-1.8

-1.2

-0.6

0.0

0.6

1.2

1.8

2.4

3.0

Sep-10 Nov-10 Jan-11 Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12

%

1Y CNH CCS1Y FX sw ap implied

May-11: Rmb fiduciary account reduced counterparty risk

Jul-11: HKMA eased calculation of NOP

Aug-11: risk aversion hit; Inw ard Rmb FDI

Jan-12: Adjustment to Rmb risk management limit

Jun-12: RMB repo

17CCS: a hedge to dim sum bond positions

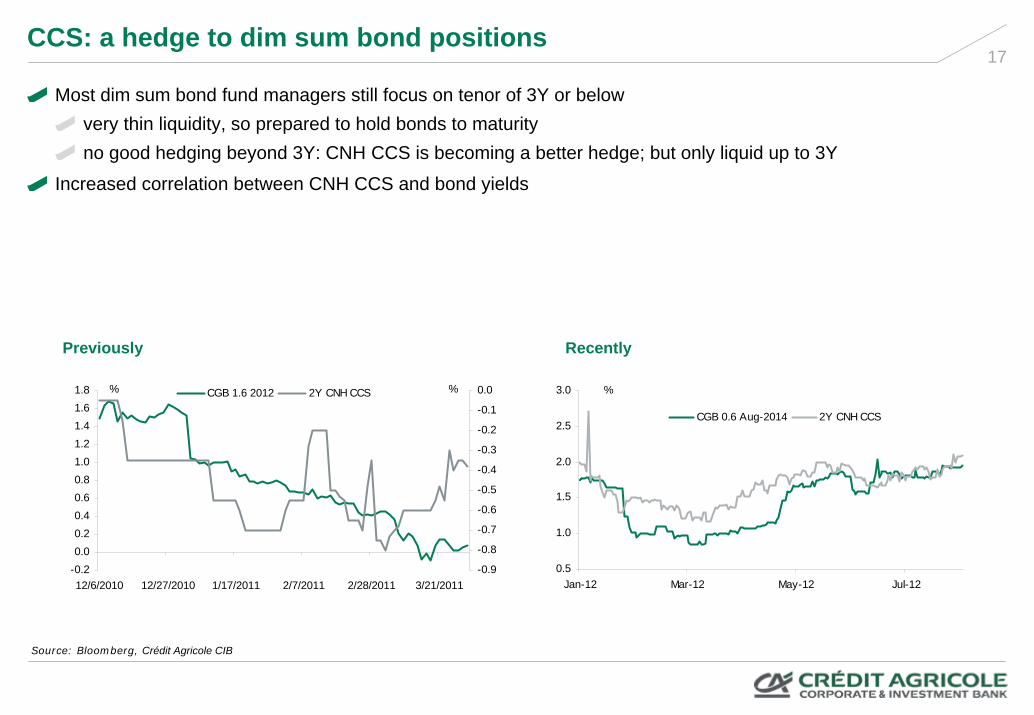

Most dim sum bond fund managers still focus on tenor of 3Y or belowvery thin liquidity, so prepared to hold bonds to maturityno good hedging beyond 3Y: CNH CCS is becoming a better hedge; but only liquid up to 3Y

Increased correlation between CNH CCS and bond yields

Source: Bloomberg, Crédit Agricole CIB

Previously Recently

-0.20.00.20.40.60.81.01.21.41.61.8

12/6/2010 12/27/2010 1/17/2011 2/7/2011 2/28/2011 3/21/2011

%

-0.9

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0.0%CGB 1.6 2012 2Y CNH CCS

0.5

1.0

1.5

2.0

2.5

3.0

Jan-12 Mar-12 May-12 Jul-12

%

CGB 0.6 Aug-2014 2Y CNH CCS

18CNH repo?

RMB facilities provided by the HKMALaunched on 15 June 2012

1-week liquidity

Eligible securitiesEFBN (Exchange Fund Bills and Notes)HKSAR Government Bondsoffshore CGBs (China Government Bonds)

RMB Facilities provided by the RMB Clearing bank in Hong Kong via HKMA’s CMU (Central MoneymarketsUnit)

Launched on 21 February 2011

intra-day liquidity

Eligible securitiesoffshore CGBs (sovereign bonds issued by the MoF)bonds issued by Bank of Chinabonds issued by China’s policy banks

Source: Bloomberg, Crédit Agricole CIB

19

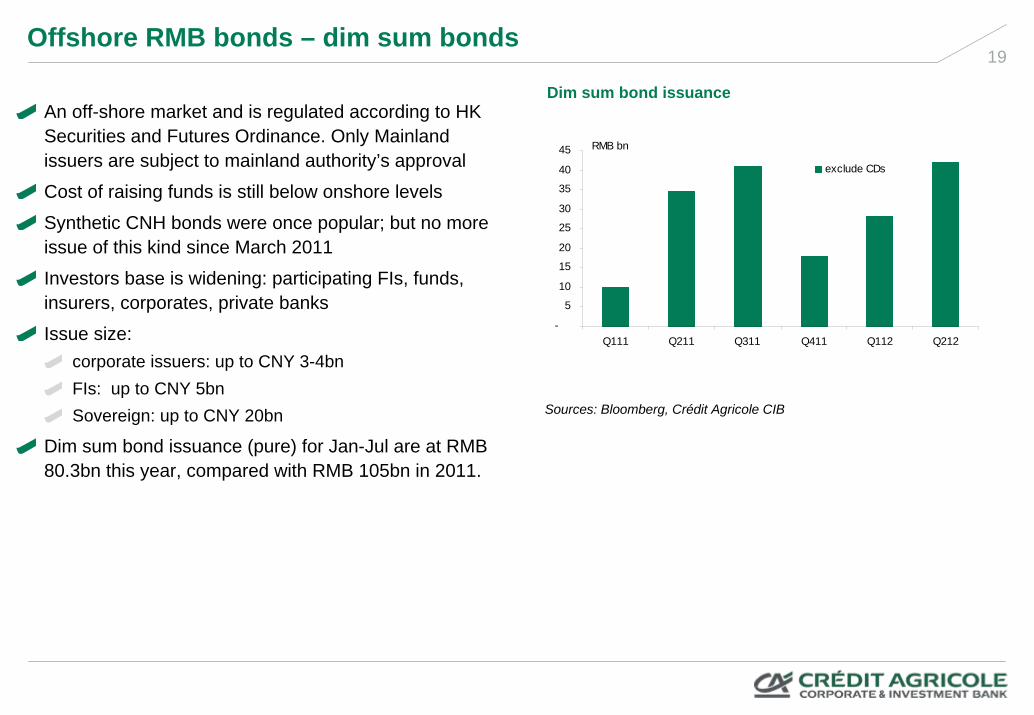

An off-shore market and is regulated according to HK Securities and Futures Ordinance. Only Mainland issuers are subject to mainland authority’s approval

Cost of raising funds is still below onshore levels

Synthetic CNH bonds were once popular; but no more issue of this kind since March 2011

Investors base is widening: participating FIs, funds, insurers, corporates, private banks

Issue size:corporate issuers: up to CNY 3-4bnFIs: up to CNY 5bnSovereign: up to CNY 20bn

Dim sum bond issuance (pure) for Jan-Jul are at RMB 80.3bn this year, compared with RMB 105bn in 2011.

Offshore RMB bonds – dim sum bonds

Sources: Bloomberg, Crédit Agricole CIB

Dim sum bond issuance

-

5

10

15

20

25

30

35

40

45

Q111 Q211 Q311 Q411 Q112 Q212

RMB bn

exclude CDs

20

Onshore-offshore yield spreads have narrowed substantially

We expect consolidation in CNH rates and dim sum bond yields around current levels

Investors: costly to borrow CNH and invest the fundsIssuers: dim sum bonds are not providing the cost-saving by as mush as they did

Dim sum bonds

Sources: Bloomberg, Crédit Agricole CIB

17 August 2011

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

3Y 5Y 7Y 10Y

%

Cut-off at offshore CGB auctionsonshore CGB yields

29 June 2012

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

3Y 5Y 7Y 10Y 15Y

%

Onshore CGBsCut-off at offshore CGB auctions

21Dim sum bonds: market development and landmark issues

Jul 2010

HKMA explains supervisory principles and operational arrangements regarding RMB business in HK

Jun 2009

Feb 2010

Aug 2010

Sep 2010

Sep 2010HKMA and PBoC sign RMB supplementary pact

HKMA publishes circular on RMB business in HK

PBoC published notice on issues concerning RMB investments in the onshore inter-bank bond market

HKEx publishes amendments to operational procedures and clearing rules to facilitate trading and settlement of RMB-denominated products

PBoC issues measures on administration of RMB settlement accounts opened by offshore institutions

Oct 2010PBoC issues interim measures on issuance of bonds in RMB by international development institutions

Hopewell Highway

RMB 1.38bn 2y 2.98%

First Hong Kong enterprise

McDonald’s

RMB 200m 3y 3.00%

First foreign enterprise

ADB

RMB 1.2bn 10y 2.85%

First supranationalFirst long-term issue

Jun 2010

Aug 2010 Oct 2010

Sinotruk HKRMB 2.7bn 3y 2.95%

First HK-listed Chinese SOE

Oct 2010

Nov 2010

China Ministry of FinanceRMB 3bn 2y 1.60% (retails)

RMB 2bn 3y 1.00%RMB 2bn 5y 1.80%

RMB 1bn 10y 2.48%Benchmark launched

Dec 2010Galaxy Entertainment

RMB 1.38bn 3y 4.625%

First High-Yield Bond

Dec 2010

Shui On Land

RMB 3bn 3y 6.875%

First Synthetic Bond

Jan 2011Sinochem

RMB 3.5bn 3y 1.80%

First issuer announced that it will not remit proceeds back to mainland after PBoC started to allow domestic corporate to invest overseas using RMB (announcement on Jan 13, 2011)

Khazanah NasionalRMB 500m 3y 2.9%

First CNH sukukOct 2011

MOFCOM and PBoC publishes notice and administrative measures in relation to cross-border FDI in RMB

Oct 2011

Oct 2011ICBC (Asia)

RMB 1.5bn 10y 6%First subordinated bond issued in HK’s CNH market

Nov 2011

Baosteel GroupRMB 1bn 2y 3.125%

RMB 2.1bn 3y 3.500%RMB 500mn 5y 4.375%

First onshore corporate issued CNH bonds

America MovilRMB 1bn 3y 3.5%First Latin America

issuer and first SEC-registered CNH bond

Feb 2012

NDRC issues new rules on issuance of CNH bonds by onshore-incorporated entities

May 2012

Apr 2012HSBC

RMB 2bn 3y 3%First CNH bond issued outside HK and listed in London

22Market Characteristics - Issuers

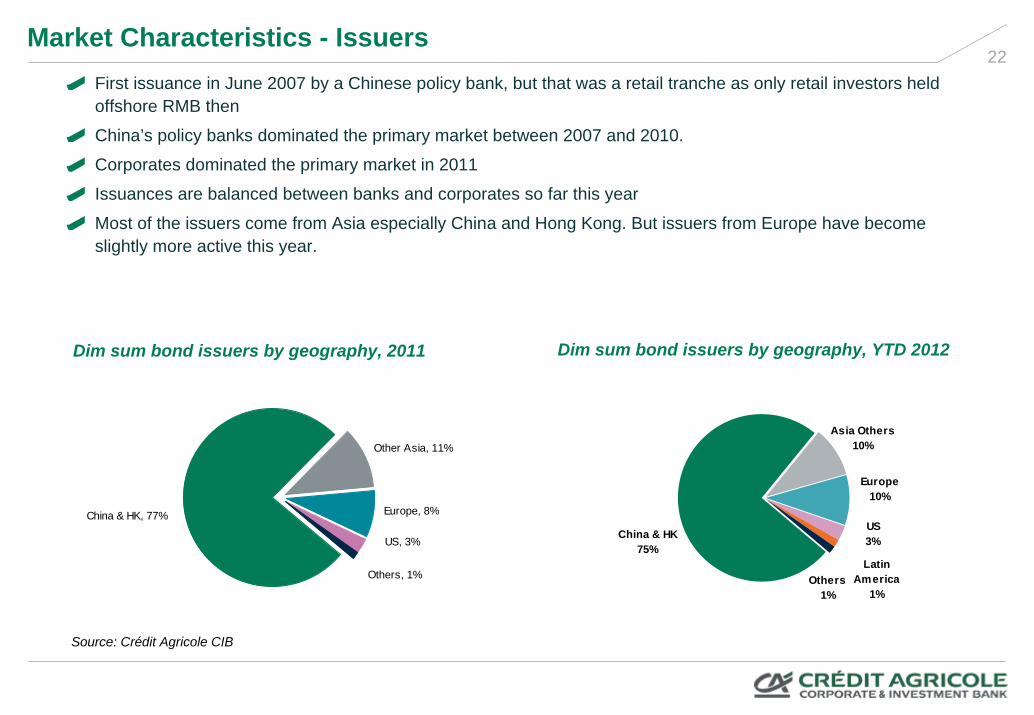

First issuance in June 2007 by a Chinese policy bank, but that was a retail tranche as only retail investors held offshore RMB then

China’s policy banks dominated the primary market between 2007 and 2010.

Corporates dominated the primary market in 2011

Issuances are balanced between banks and corporates so far this year

Most of the issuers come from Asia especially China and Hong Kong. But issuers from Europe have become slightly more active this year.

Dim sum bond issuers by geography, 2011

Source: Crédit Agricole CIB

Other Asia, 11%

Others, 1%

US, 3%

Europe, 8%China & HK, 77%

Dim sum bond issuers by geography, YTD 2012

Others1%

Asia Others10%

Latin America

1%

US3%

Europe10%

China & HK75%

23Market Characteristics – Ratings

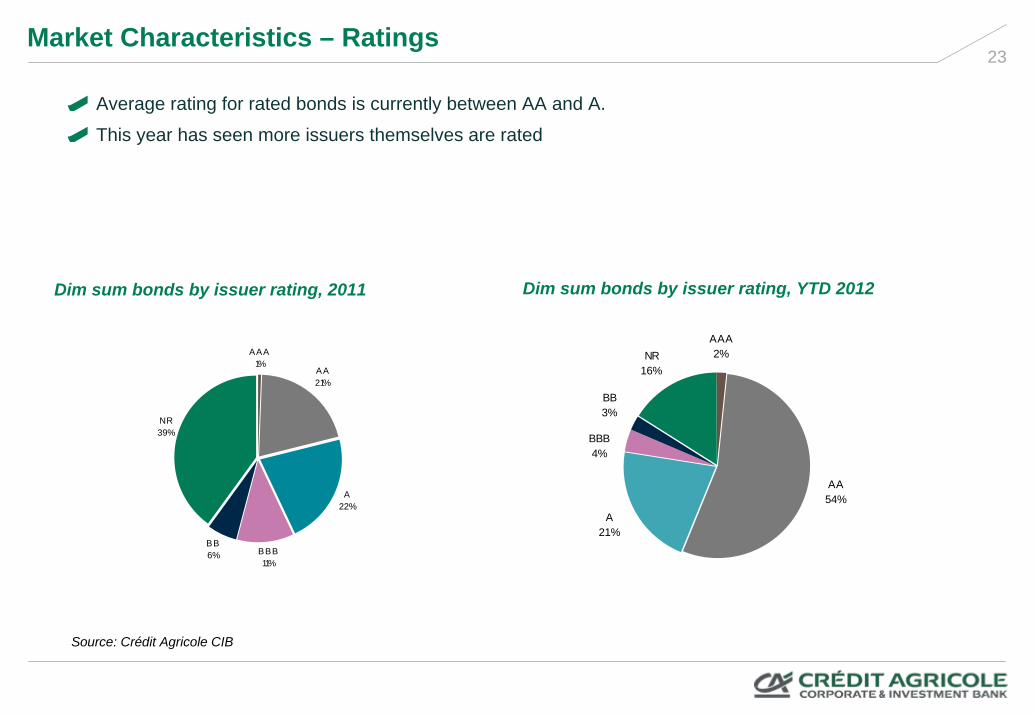

Average rating for rated bonds is currently between AA and A.

This year has seen more issuers themselves are rated

Dim sum bonds by issuer rating, 2011 Dim sum bonds by issuer rating, YTD 2012

Source: Crédit Agricole CIB

AAA1%

AA21%

A22%

BBB11%

BB6%

NR39%

BB3%

AAA2%NR

16%

A21%

BBB4%

AA54%

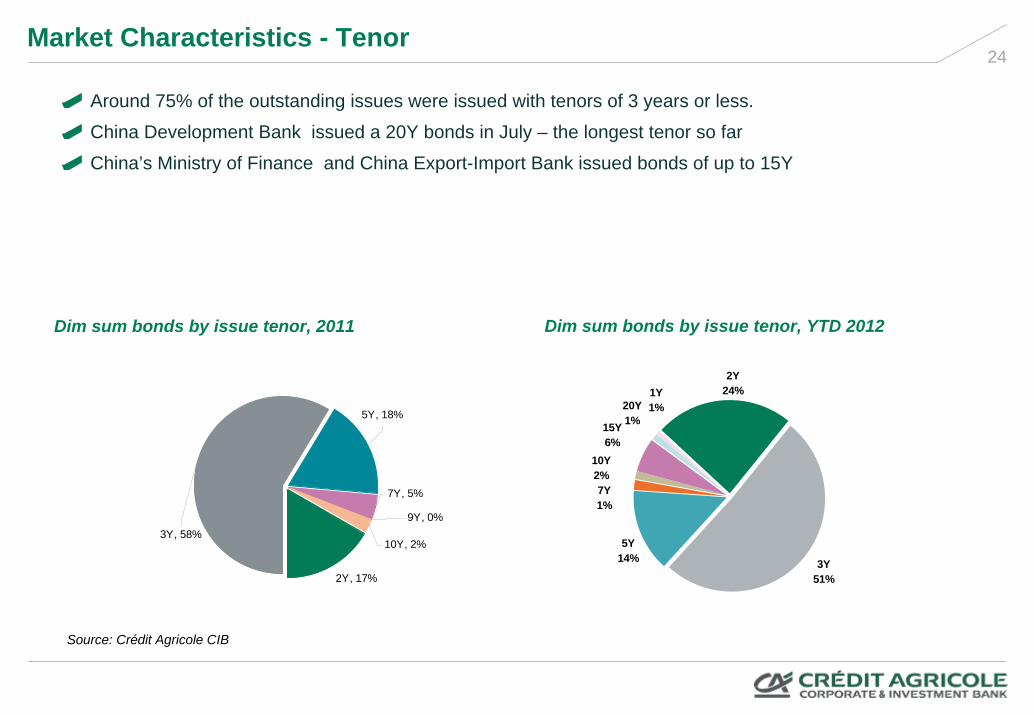

24Market Characteristics - Tenor

Around 75% of the outstanding issues were issued with tenors of 3 years or less.

China Development Bank issued a 20Y bonds in July – the longest tenor so far

China’s Ministry of Finance and China Export-Import Bank issued bonds of up to 15Y

Source: Crédit Agricole CIB

Dim sum bonds by issue tenor, 2011

2Y, 17%

5Y, 18%

9Y, 0%

10Y, 2%

7Y, 5%

3Y, 58%

Dim sum bonds by issue tenor, YTD 2012

20Y1%

1Y1%

2Y24%

10Y2%

5Y14%

7Y1%

3Y51%

15Y6%

25

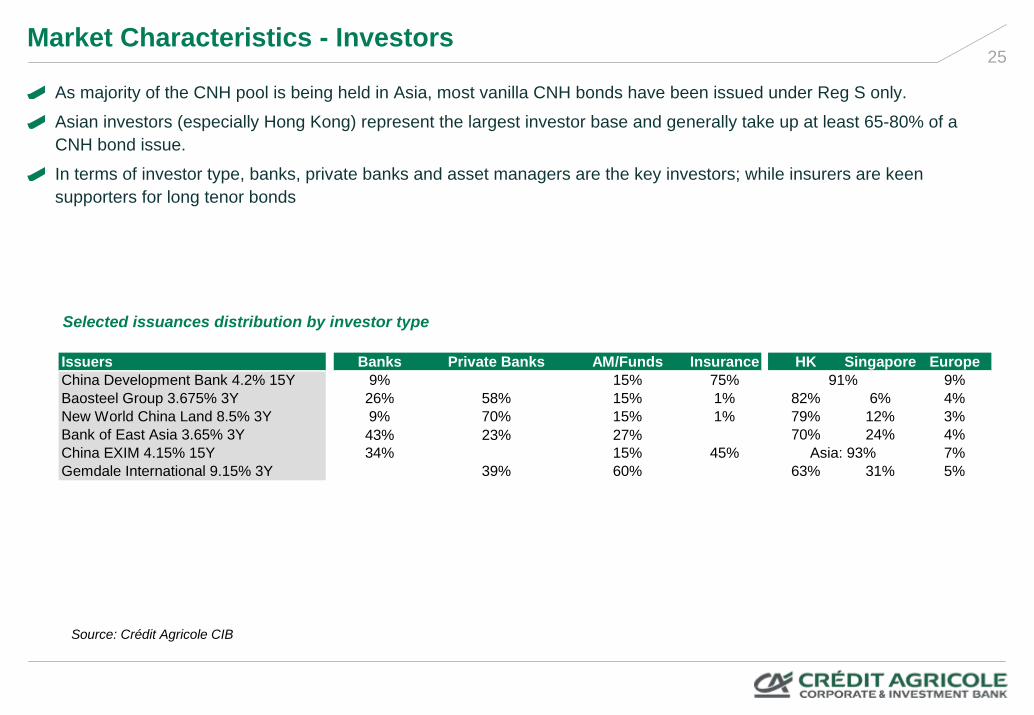

As majority of the CNH pool is being held in Asia, most vanilla CNH bonds have been issued under Reg S only.

Asian investors (especially Hong Kong) represent the largest investor base and generally take up at least 65-80% of a CNH bond issue.

In terms of investor type, banks, private banks and asset managers are the key investors; while insurers are keen supporters for long tenor bonds

Market Characteristics - Investors

Source: Crédit Agricole CIB

Selected issuances distribution by investor type

Issuers Banks Private Banks AM/Funds Insurance HK Singapore EuropeChina Development Bank 4.2% 15Y 9% 15% 75% 9%Baosteel Group 3.675% 3Y 26% 58% 15% 1% 82% 6% 4%New World China Land 8.5% 3Y 9% 70% 15% 1% 79% 12% 3%Bank of East Asia 3.65% 3Y 43% 23% 27% 70% 24% 4%China EXIM 4.15% 15Y 34% 15% 45% 7%Gemdale International 9.15% 3Y 39% 60% 63% 31% 5%

91%

Asia: 93%

Speaker Biography

Frances Cheung

Senior Strategist for Asia ex-Japan Fixed Income Markets Research

Frances Cheung has over 10 years experience as an economist and rates strategist, covering Asian economies and markets. She joined Crédit Agricole CIB in April 2010 as Senior Strategist for Asia ex Japan, with a focus on the rates markets.

She is in charge of formulating rates strategies for markets in Asia ex-Japan. She is involved in relationships with the bank’s clients, presenting her and the Fixed Income Market Research team’s views on a regular basis. She also markets the bank’s economic and market views with the media.

Frances was working with Standard Chartered Bank previously, covering the rates markets in China, Hong Kong and Taiwan, and regional economies. Prior to that, she worked with Primasia (Securities) Asia and the HKSAR government on economic research for Greater China and North East Asia.

She received her Master of Philosophy (Economics) and Bachelor of Social Science (Economics) degree from the Chinese University of Hong Kong. Frances is also a CFA charter holder.

Ranked No. 1 (Best Analyst) in FinanceAsia Fixed Income Research Poll 2011

27

04 October 2012

Disclaimer

CertificationThe views expressed in this report accurately reflect the personal views of the undersigned analyst(s). In addition, the undersigned analyst(s) has not and will not receive any compensation for providing a specific recommendation or view in this report. Frances Cheung

FIM Research contact details

Hervé Goulletquer Global Head of FIM Research +33 1 41 89 88 34

Asia (Hong Kong & Tokyo) Europe (London & Paris) Americas (New York)

Mitul KotechaHead of FIM Research for Asia andHead of Global FX Strategy+852 2826 9821

Sébastien BarbéHead of FIM Research for Europe andHead of EM Research and Strategy+33 1 41 89 15 97

David Keeble Head of FIM Research for the Americas and Global Head of Interest Rates Strategy+1 212 261 3274

Macro Strategy(Facilitator: HervéGoulletquer)

Yoshiro SatoAssociate – Japan+81 3 4580 5337

Frederik DucrozetSenior Economist – Eurozone+33 1 41 89 98 95Slavena NazarovaEconomist – Eurozone/UK+33 1 41 89 99 18Jean-François PerrinSenior Asset Allocation Strategist+33 1 41 89 94 22

Michael P. CareyChief Economist – North America+1 212 261 7134

Interest Rates(Head: David Keeble)

Frances CheungSenior Strategist – Asia ex-Japan+852 2826 1520

Luca JellinekHead of European Interest Rates Strategy+44 20 7214 6244Peter ChatwellSenior Interest Rates Strategist+44 20 7214 5289Orlando GreenSenior Interest Rates Strategist+44 20 7214 7467

David Keeble Global Head of Interest Rates Strategy+1 212 261 3274

Emerging Markets(Head: Sébastien Barbé)

Frances CheungSenior Strategist – Asia ex-Japan+852 2826 1520Dariusz KowalczykSenior Economist/Strategist – Asia ex-Japan+852 2826 1519

Sébastien BarbéHead of EM Research and Strategy+33 1 41 89 15 97Guillaume TrescaSenior Emerging Market Strategist+33 1 41 89 18 47

Foreign Exchange(Head: Mitul Kotecha)

Mitul KotechaHead of Global FX Strategy+852 2826 9821

Stephen GalloFX Strategist+44 20 7214 7469Adam MyersSenior FX Strategist+44 20 7214 7468

Sireen HarajliFX Strategist+1 212 261 7139

Disclaimer© 2012, CRÉDIT AGRICOLE CORPORATE AND INVESTMENT BANK All rights reserved.This research report or summary has been prepared by Crédit Agricole Corporate and Investment Bank or one of its affiliates (collectively “Crédit Agricole CIB”) from information believed to be reliable. Such information has not been independently verified and no guarantee, representation or warranty, express or implied, is made as to its accuracy, completeness or correctness. This report is a “commercial communication” as defined in article 6 of the Directive 2000/31/CE of 8 June 2000. For the avoidance of doubt, it is not a “communication à caractère promotionnel” within the meaning of the Règlement General AMF. It is provided for information purposes only. Nothing in this report should be considered to constitute investment, legal, accounting or taxation advice and you are advised to contact independent advisors in order to evaluate this report. It is not intended, and should not be considered, as an offer, invitation, solicitation or personal recommendation to buy, subscribe for or sell any of the financial instruments described herein, nor is it intended to form the basis for any credit, advice, personal recommendation or other evaluation with respect to such financial instruments and is intended for use only by those professional investors to whom it is made available by Crédit Agricole CIB. Crédit Agricole CIB does not act in a fiduciary capacity to you in respect of this report.Crédit Agricole CIB may at any time stop producing or updating this report. Not all strategies are appropriate at all times. Past performance is not necessarily a guide to future performance. The price, value of and income from any of the financial instruments mentioned in this report can fall as well as rise and you may make losses if you invest in them. Independent advice should be sought. In any case, investors are invited to make their own independent decision as to whether a financial instrument or whether investment in the financial instruments described herein is proper, suitable or appropriate based on their own judgement and upon the advice of any relevant advisors they have consulted. Crédit Agricole CIB has not taken any steps to ensure that any financial instruments referred to in this report are suitable for any investor. Crédit Agricole CIB will not treat recipients of this report as its customers by virtue of their receiving this report.Crédit Agricole CIB, its directors, officers and employees may effect transactions (whether long or short) in the financial instruments described herein for their own accounts or for the account of others, may have positions relating to other financial instruments of the issuer thereof, or any of its affiliates, or may perform or seek to perform securities, investment banking or other services for such issuer or its affiliates. Crédit Agricole CIB may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Crédit Agricole CIB is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. Crédit Agricole CIB has established a “Policy for Managing Conflicts of Interest in relation to Investment Research” which is available upon request. A summary of this Policy is published on the Crédit Agricole CIB website: http://www.ca-cib.com/group-overview/the-markets-in-financial-instruments-directive-mifid.htm. This Policy applies to its investment research activity.None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party without the prior express written permission of Crédit Agricole CIB. To the extent permitted by applicable securities laws and regulations, Crédit Agricole CIB accepts no liability whatsoever for any direct or consequential loss arising from the use of this document or its contents.France: Crédit Agricole Corporate and Investment Bank is authorised by the Autorité de Contrôle Prudentiel (“ACP”) and supervised by the ACP and the Autorité des Marchés Financiers (“AMF”). United Kingdom: Approved and/or distributed by Crédit Agricole Corporate and Investment Bank, London branch. Crédit Agricole Corporate and Investment Bank is authorised by the ACP and supervised by the ACP and the AMF in France and subject to limited regulation by the Financial Services Authority. Details about the extent of our regulation by the Financial Services Authority are available from us on request. United States of America: This research report is distributed solely to persons who qualify as “Major U.S. Institutional Investors” as defined in Rule 15a-6 under the Securities and Exchange Act of 1934 and who deal with Crédit Agricole Corporate and Investment Bank. Recipients of this research in the United States wishing to effect a transaction in any security mentioned herein should do so by contacting Crédit Agricole Securities (USA), Inc. (a broker-dealer registered with the Securities and Exchange Commission). The delivery of this research report to any person in the United States shall not be deemed a recommendation of Crédit Agricole Securities (USA), Inc. to effect any transactions in the securities discussed herein or an endorsement of any opinion expressed herein. Italy: This research report can only be distributed to, and circulated among, professional investors (operatori qualificati), as defined by the relevant Italian securities legislation. Spain: Distributed by Crédit Agricole Corporate and Investment Bank, Madrid branch and may only be distributed to institutional investors (as defined in article 7.1 of Royal Decree 291/1992 on Issues and Public Offers of Securities) and cannot be distributed to other investors that do not fall within the category of institutional investors. Hong Kong: Distributed by Crédit Agricole Corporate and Investment Bank, Hong Kong branch. This research report can only be distributed to professional investors within the meaning of the Securities and Futures Ordinance (Cap.571) and any rule made there under. Japan: Distributed by Crédit Agricole Securities Asia B.V. which is registered for securities business in Japan pursuant to the Law Concerning Foreign Securities Firms (Law n°5 of 1971, as amended), and is not intended, and should not be considered, as an offer, invitation, solicitation or recommendation to buy or sell any of the financial instruments described herein. This report is not intended, and should not be considered, as advice on investments in securities which is subject to the Securities Investment Advisory Business Law (Law n°74 of 1986, as amended). Luxembourg: Distributed by Crédit Agricole Corporate and Investment Bank, Luxembourg branch. It is only intended for circulation and/or distribution to institutional investors and investments mentioned in this report will not be available to the public but only to institutional investors. Singapore: Distributed by Crédit Agricole Corporate and Investment Bank, Singapore branch. It is not intended for distribution to any persons other than accredited investors, as defined in the Securities and Futures Act (Chapter 289 of Singapore), and persons whose business involves the acquisition or disposal of, or the holding of capital markets products (as defined in the Securities and Futures Act (Chapter 289 of Singapore)). Switzerland: Distributed by Crédit Agricole (Suisse) S.A. This report is not subject to the SBA Directive of January 24, 2003 as they are produced by a non-Swiss entity. Germany: Distributed by Crédit Agricole Corporate and Investment Bank, Frankfurt branch and may only be distributed to institutional investors. Australia: Distributed to wholesale investors only. This research, and any access to it, is intended only for “wholesale clients” within the meaning of the Australian Corporations Act. THE DISTRIBUTION OF THIS DOCUMENT IN OTHER JURISDICTIONS MAY BE RESTRICTED BY LAW, AND PERSONS INTO WHOSE POSSESSION THIS DOCUMENT COMES SHOULD INFORM THEMSELVES ABOUT, AND OBSERVE, ANY SUCH RESTRICTIONS. BY ACCEPTING THIS REPORT YOU AGREE TO BE BOUND BY THE FOREGOING.

ABC Global Research

Latest development in offshore RMB market October 2012

View HSBC Global Research at: http://www.research.hsbc.com

Issuer of report: The Hongkong and Shanghai Banking Corporation Limited

Disclosures and Disclaimer This report must be read with the disclosures and the analyst certifications in the Disclosure appendix, and in the Disclaimer, which forms part of it’

ZHANG, Zhi Ming (张之明) MD, Head of China Research The Hongkong and Shanghai Banking Corporation Limited +852 2822 4523 [email protected]

2

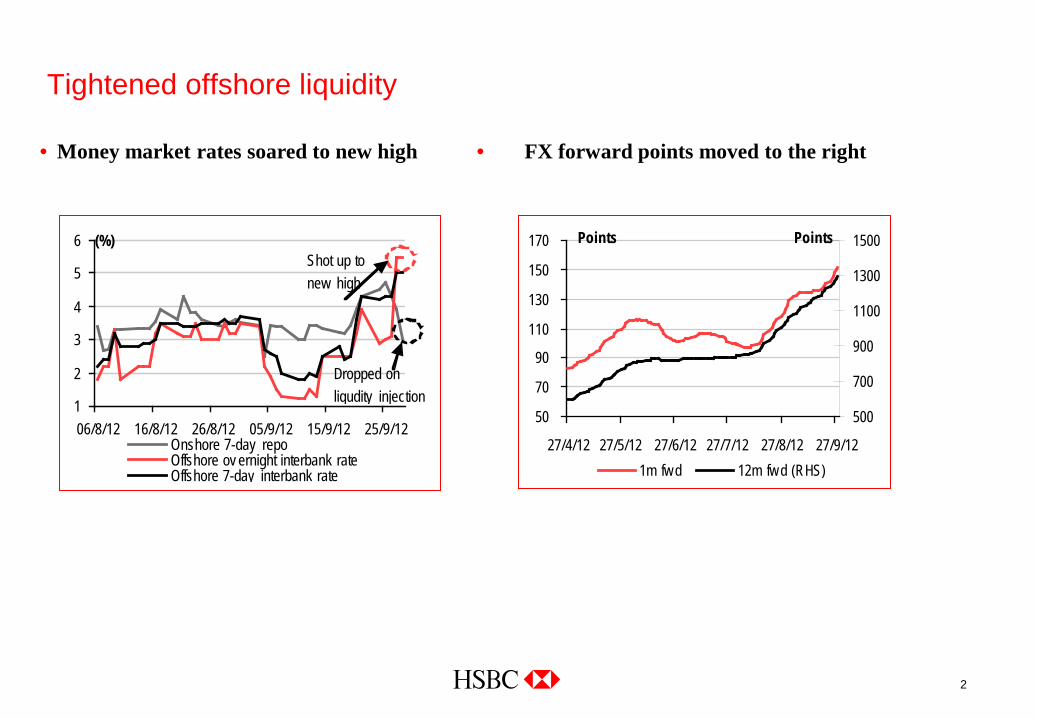

· Money market rates soared to new high

Tightened offshore liquidity

· FX forward points moved to the right

1

2

3

4

5

6

06/8/12 16/8/12 26/8/12 05/9/12 15/9/12 25/9/12

(%)

Onshore 7-day repoOffshore ov ernight interbank rateOffshore 7-day interbank rate

Dropped on liqudity injection

Shot up to new high

50

70

90

110

130

150

170

27/4/12 27/5/12 27/6/12 27/7/12 27/8/12 27/9/12

500

700

900

1100

1300

1500

1m fw d 12m fw d (RHS)

PointsPoints

3

Source: HKMA, City of London commissioned study, Xinhua, www.cens.com, HSBC, Reuters

· Offshore CGB yield surged 60bp-150bp higher along the curve · The gap between on- and offshore CGB yields have narrowed drastically this year

CGB yields continued to rise

1

1.5

2

2.5

3

3.5

4

2 4 6 8 10

Tenor(yrs)

Yield (%)

Jan offshore Sep offshore Jan onshore Sep onshore

0

1

2

3

4

5

12/10 03/11 06/11 09/11 12/11 03/12 06/12 09/12

Yield(%)

Spread Onshore Offshore

4

Source: HKMA, City of London commissioned study, Xinhua, www.cens.com, HSBC, Reuters

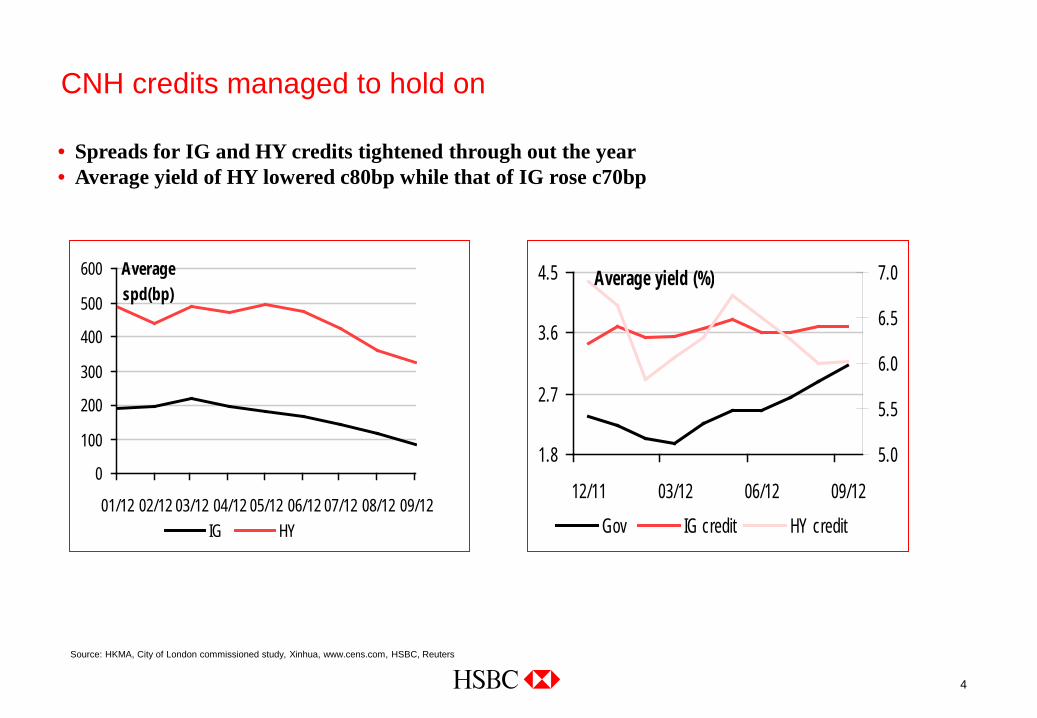

· Spreads for IG and HY credits tightened through out the year · Average yield of HY lowered c80bp while that of IG rose c70bp

CNH credits managed to hold on

0

100

200

300

400

500

600

01/12 02/12 03/12 04/12 05/12 06/12 07/12 08/12 09/12

Average spd(bp)

IG HY

1.8

2.7

3.6

4.5

12/11 03/12 06/12 09/12

5.0

5.5

6.0

6.5

7.0

Gov IG credit HY credit

Average yield (%)

5

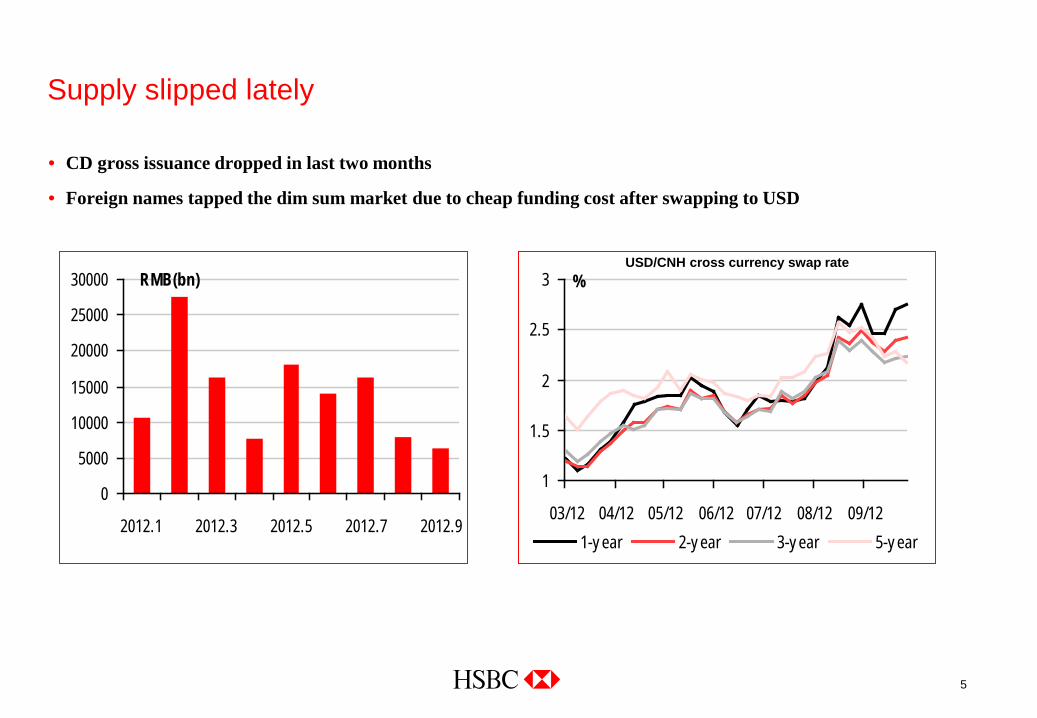

Supply slipped lately

· CD gross issuance dropped in last two months

· Foreign names tapped the dim sum market due to cheap funding cost after swapping to USD

0

5000

10000

15000

20000

25000

30000

2012.1 2012.3 2012.5 2012.7 2012.9

RMB(bn)

1

1.5

2

2.5

3

03/12 04/12 05/12 06/12 07/12 08/12 09/12

%

1-y ear 2-y ear 3-y ear 5-y ear

USD/CNH cross currency swap rate

6

The big picture: on- and offshore integration underway

· 1) Internationalization is not all about offshore development

· Ease of capital in and out flow paves the way for yield convergence…

· …a prerequisite for sustainable RMB internationalization

· 2) Most significant recent initiative: QFII access to interbank bond market

· 3) Market force, not policy support, world eventually dictate the pace RMB offshore development

7

Improved access to onshore market

· Three types of foreign institutions can apply to enter the onshore interbank market: including foreign central banks, clearing banks, and settlement banks

· QFII investors also became eligible to onshore interbank bond market since this July

· R-QFII · Eligibility: Hong Kong subsidiaries of Chinese asset management and security firms (21 approved) · Quota: RMB20bn (utilised) + RMB50bn (increased in April) · Markets: both onshore interbank and stock exchange markets. 80% in fixed income and 20% otherwise

for first batch of RMB20bn quota. 100% can be invested in exchanged-traded fund tracing onshore A-share index for the additional RMB50bn quota.

· QFII

· Quota increased by USD50bn (from USD30bn) in April 2011

· A total of USD31bn approved as of mid-September 2012

8

Proposed changes – lower minimum requirements for applicants

1) Lower minimum requirements of applicants

· For asset management, insurance, pension funds, charity funds, trusts, sovereign wealth funds, and other institutions: minimum years of operation reduced to two years from five years; minimum assets under management (AUM) lowered to USD500m from USD5bn in the most recent financial year;

· For security companies: required minimum years of operation reduced to five years from 30 years; net assets lowered to USD500m from USD1bn, and AUM to USD5bn from USD10bn;

· For commercial banks: current requirement of least 10 years of operation, core capital of no less than USD300m and no less than USD5bn in security assets, changed from total assets ranking in the top 100 globally and at least USD10bn of security assets.

9

Proposed changes – expand onshore access and improve flexibility

· 2) Expand the investment scope to the interbank market, loosen restriction on share holding

· Allow QFIIs to access the interbank bond market, with possibly additional approval by the PBoC

· Combined shareholding of A-shares by all foreign investors proposed to increase to 30% of total shares, up from 20%. The 10% cap by a single foreign investor remains unchanged

· 3) Improve operational flexibility

· Allowing QFII investors to set up separate accounts for their own investment funding and funding from their clients, and allow QFII investors to have more than one broker for transactions

· Others potential changes (reported by onshore media)

· More than one applicant under the same group allowed to apply for QFII

· Applicants used quota for structured products in the past allow to apply for quota increase

10

Disclosure appendix Analyst Certification The following analyst(s), economist(s), and/or strategist(s) who is(are) primarily responsible for this report, certifies(y) that the opinion(s) on the subject security(ies) or issuer(s) and/or any other views or forecasts expressed herein accurately reflect their personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views contained in this research report: Becky Liu

Basis for financial analysis This report is designed for, and should only be utilised by, institutional investors. Furthermore, HSBC believes an investor's decision to make an investment should depend on individual circumstances such as the investor's existing holdings and other considerations.

HSBC believes that investors utilise various disciplines and investment horizons when making investment decisions, which depend largely on individual circumstances such as the investor's existing holdings, risk tolerance and other considerations. Given these differences, HSBC has two principal aims in its credit research: 1) to identify long-term investment opportunities based on particular themes or ideas that may affect the future earnings or cash flows of companies on a six-month time horizon; and 2) from time to time to identify trade ideas on a time horizon of up to three months, relating to specific instruments, which are predominantly derived from relative value considerations or driven by events and which may differ from our long-term credit opinion on an issuer. HSBC has assigned a fundamental recommendation structure only for its long-term investment opportunities, as described below.

HSBC believes an investor's decision to buy or sell a bond should depend on individual circumstances such as the investor's existing holdings and other considerations. Different securities firms use a variety of terms as well as different systems to describe their recommendations. Investors should carefully read the definitions of the recommendations used in each research report. In addition, because research reports contain more complete information concerning the analysts' views, investors should carefully read the entire research report and should not infer its contents from the recommendation. In any case, recommendations should not be used or relied on in isolation as investment advice.

HSBC Global Research is not and does not hold itself out to be a Credit Rating Agency as defined under the Hong Kong Securities and Futures Ordinance.

Definitions for fundamental credit recommendations Overweight: The credits of the issuer are expected to outperform those of other issuers in the sector over the next six months

Neutral: The credits of the issuer are expected to perform in line with those of other issuers in the sector over the next six months

Underweight: The credits of the issuer are expected to underperform those of other issuers in the sector over the next six months

Prior to 1 July 2007, HSBC applied a recommendation structure in Europe that ranked euro- and sterling-denominated bonds and CDS relative to the relevant iBoxx/iTraxx indices over a 3-month horizon.

Distribution of fundamental credit opinions As of 30 November 2011, the distribution of all credit opinions published is as follows:

11

Disclaimer * Legal entities as at 04 March 2011 ‘UAE’ HSBC Bank Middle East Limited, Dubai; ‘HK’ The Hongkong and Shanghai Banking Corporation Limited, Hong Kong; ‘TW’ HSBC Securities (Taiwan) Corporation Limited; ‘CA’ HSBC Securities (Canada) Inc, Toronto; HSBC Bank, Paris Branch; HSBC France; ‘DE’ HSBC Trinkaus & Burkhardt AG, Düsseldorf; 000 HSBC Bank (RR), Moscow; ‘IN’ HSBC Securities and Capital Markets (India) Private Limited, Mumbai; ‘JP’ HSBC Securities (Japan) Limited, Tokyo; ‘EG’ HSBC Securities Egypt SAE, Cairo; ‘CN’ HSBC Investment Bank Asia Limited, Beijing Representative Office; The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch; The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch; HSBC Securities (South Africa) (Pty) Ltd, Johannesburg; ‘GR’ HSBC Securities SA, Athens; HSBC Bank plc, London, Madrid, Milan, Stockholm, Tel Aviv; ‘US’ HSBC Securities (USA) Inc, New York; HSBC Yatirim Menkul Degerler AS, Istanbul; HSBC México, SA, Institución de Banca Múltiple, Grupo Financiero HSBC; HSBC Bank Brasil SA – Banco Múltiplo; HSBC Bank Australia Limited; HSBC Bank Argentina SA; HSBC Saudi Arabia Limited; The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch

Issuer of report The Hongkong and Shanghai Banking Corporation Limited Level 19, 1 Queen's Road Central Hong Kong SAR Telephone: +852 2843 9111 Telex: 75100 CAPEL HX Fax: +852 2801 4138 Website: www.research.hsbc.com

The Hongkong and Shanghai Banking Corporation Limited (“HSBC”) has issued this research material. The Hongkong and Shanghai Banking Corporation Limited is regulated by the Hong Kong Monetary Authority. This material is distributed in the United Kingdom by HSBC Bank plc. In Australia, this publication has been distributed by The Hongkong and Shanghai Banking Corporation Limited (ABN 65 117 925 970, AFSL 301737) for the general information of its “wholesale” customers (as defined in the Corporations Act 2001). Where distributed to retail customers, this research is distributed by HSBC Bank Australia Limited (AFSL No. 232595). These respective entities make no representations that the products or services mentioned in this document are available to persons in Australia or are necessarily suitable for any particular person or appropriate in accordance with local law. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. This publication is distributed in New Zealand by The Hongkong and Shanghai Banking Corporation Limited, New Zealand Branch. This material is distributed in Japan by HSBC Securities (Japan) Limited. HSBC Securities (USA) Inc. accepts responsibility for the content of this research report prepared by its non-US foreign affiliate. All US persons receiving and/or accessing this report and intending to effect transactions in any security discussed herein should do so with HSBC Securities (USA) Inc. in the United States and not with its non-US foreign affiliate, the issuer of this report. In Korea, this publication is distributed by either The Hongkong and Shanghai Banking Corporation Limited, Seoul Securities Branch ("HBAP SLS") or The Hongkong and Shanghai Banking Corporation Limited, Seoul Branch ("HBAP SEL") for the general information of professional investors specified in Article 9 of the Financial Investment Services and Capital Markets Act (“FSCMA”). This publication is not a prospectus as defined in the FSCMA. It may not be further distributed in whole or in part for any purpose. Both HBAP SLS and HBAP SEL are regulated by the Financial Services Commission and the Financial Supervisory Service of Korea. In Singapore, this publication is distributed by The Hongkong and Shanghai Banking Corporation Limited, Singapore Branch for the general information of institutional investors or other persons specified in Sections 274 and 304 of the Securities and Futures Act (Chapter 289) (“SFA”) and accredited investors and other persons in accordance with the conditions specified in Sections 275 and 305 of the SFA. This publication is not a prospectus as defined in the SFA. It may not be further distributed in whole or in part for any purpose. The Hongkong and Shanghai Banking Corporation Limited Singapore Branch is regulated by the Monetary Authority of Singapore. Recipients in Singapore should contact a "Hongkong and Shanghai Banking Corporation Limited, Singapore Branch" representative in respect of any matters arising from, or in connection with this report. In the UK this material may only be distributed to institutional and professional customers and is not intended for private customers. It is not to be distributed or passed on, directly or indirectly, to any other person. HSBC México, S.A., Institución de Banca Múltiple, Grupo Financiero HSBC is authorized and regulated by Secretaría de Hacienda y Crédito Público and Comisión Nacional Bancaria y de Valores (CNBV). HSBC Bank (Panama) S.A. is regulated by Superintendencia de Bancos de Panama. Banco HSBC Honduras S.A. is regulated by Comisión Nacional de Bancos y Seguros (CNBS). Banco HSBC Salvadoreño, S.A. is regulated by Superintendencia del Sistema Financiero (SSF). HSBC Colombia S.A. is regulated by Superintendencia Financiera de Colombia. Banco HSBC Costa Rica S.A. is supervised by Superintendencia General de Entidades Financieras (SUGEF). Banistmo Nicaragua, S.A. is authorized and regulated by Superintendencia de Bancos y de Otras Instituciones Financieras (SIBOIF). Any recommendations contained in it are intended for the professional investors to whom it is distributed. This material is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. HSBC has based this document on information obtained from sources it believes to be reliable but which it has not independently verified; HSBC makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of HSBC only and are subject to change without notice. The decision and responsibility on whether or not to invest must be taken by the reader. HSBC and its affiliates and/or their officers, directors and employees may have positions in any securities mentioned in this document (or in any related investment) and may from time to time add to or dispose of any such securities (or investment). HSBC and its affiliates may act as market maker or have assumed an underwriting commitment in the securities of any companies discussed in this document (or in related investments), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform banking or underwriting services for or relating to those companies. This material may not be further distributed in whole or in part for any purpose. No consideration has been given to the particular investment objectives, financial situation or particular needs of any recipient. (070905) © Copyright. The Hongkong and Shanghai Banking Corporation Limited 2011, ALL RIGHTS RESERVED. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior written permission of The Hongkong and Shanghai Banking Corporation Limited. MICA (P) 208/04/2011 and MICA (P) 040/04/2011

Strictly Private and Confidential

db CNH Plus Index

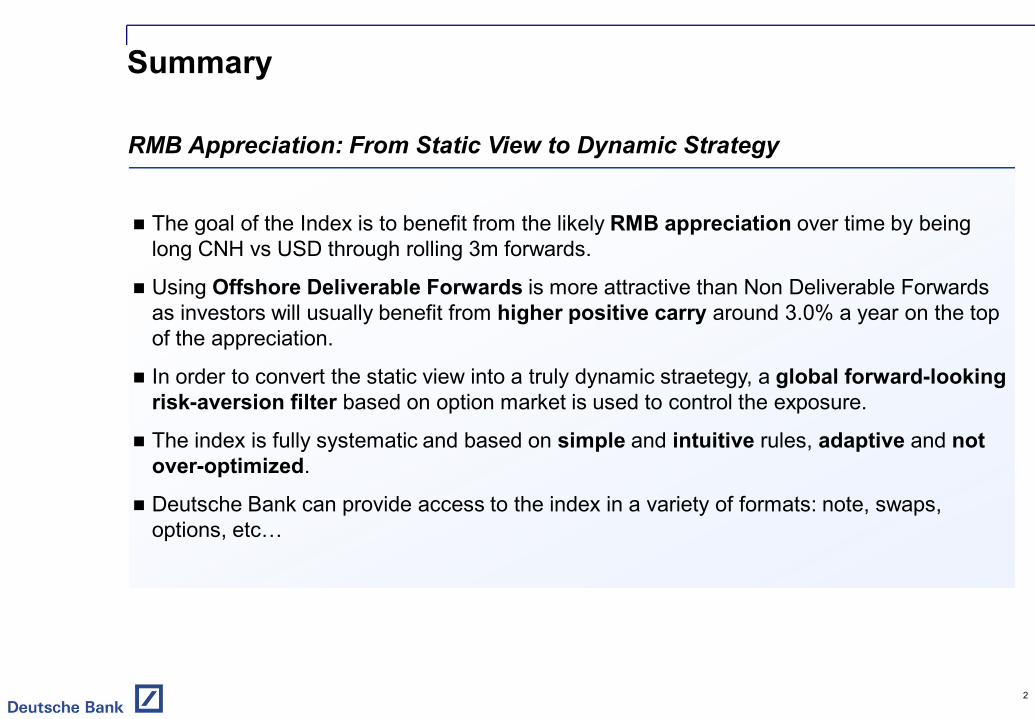

Summary

RMB Appreciation: From Static View to Dynamic Strategy

The goal of the Index is to benefit from the likely RMB appreciation over time by being long CNH vs USD through rolling 3m forwards.

Using Offshore Deliverable Forwards is more attractive than Non Deliverable Forwards as investors will usually benefit from higher positive carry around 3.0% a year on the top of the appreciation.

In order to convert the static view into a truly dynamic straetegy, a global forward-looking risk-aversion filter based on option market is used to control the exposure.

The index is fully systematic and based on simple and intuitive rules, adaptive and not over-optimized.

Deutsche Bank can provide access to the index in a variety of formats: note, swaps, options, etc…

2

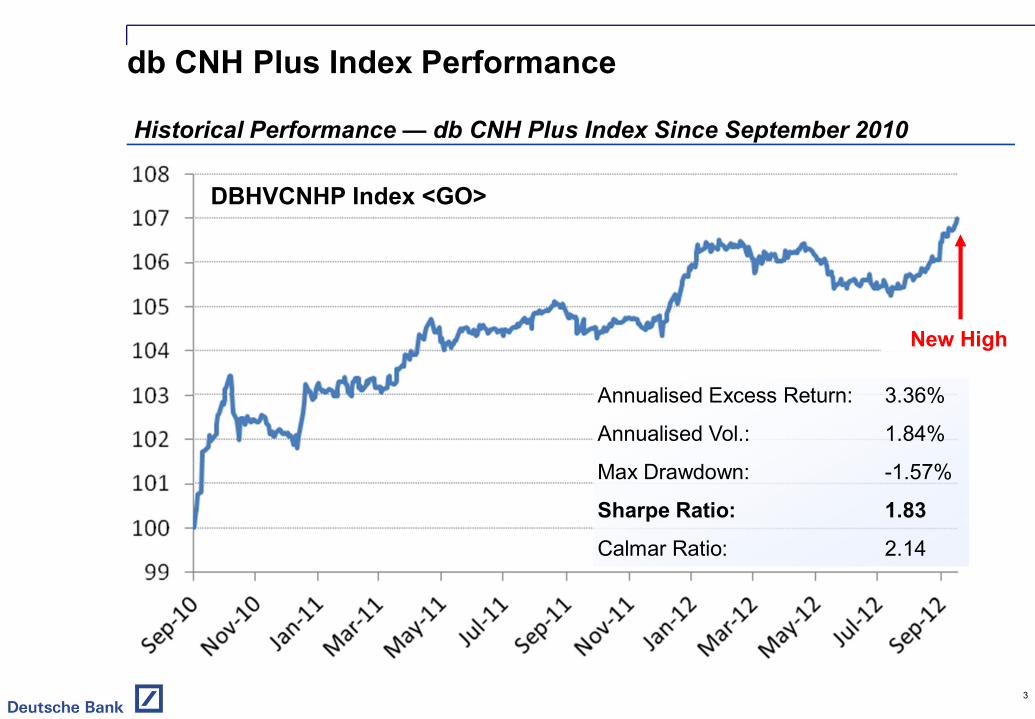

db CNH Plus Index Performance

Historical Performance — db CNH Plus Index Since September 2010

3

New High

Annualised Excess Return: 3.36%

Annualised Vol.: 1.84%

Max Drawdown: -1.57%

Sharpe Ratio: 1.83

Calmar Ratio: 2.14

DBHVCNHP Index <GO>

Appreciation and Positive Carry

44

CNH forward premium is likely to stay positive given its deliverability whereas NDF carry can become negative due to its speculative nature.

Currently, the 3m CNH forward points are much higher than the NDF. As the CNH liquidity tightness has become more systemic, CNH forward premium is expected to hold up at elevated levels.

Appreciation and Positive Carry

Close-up on the Dec11 Roll

6.28

6.30

6.32

6.34

6.36

6.38

6.40

6.42

Dec-11 Jan-12 Feb-12

USDCNH SpotFwds curve as of Dec 11

Profit from CNH appreciation

Profit from 3 month positive carry

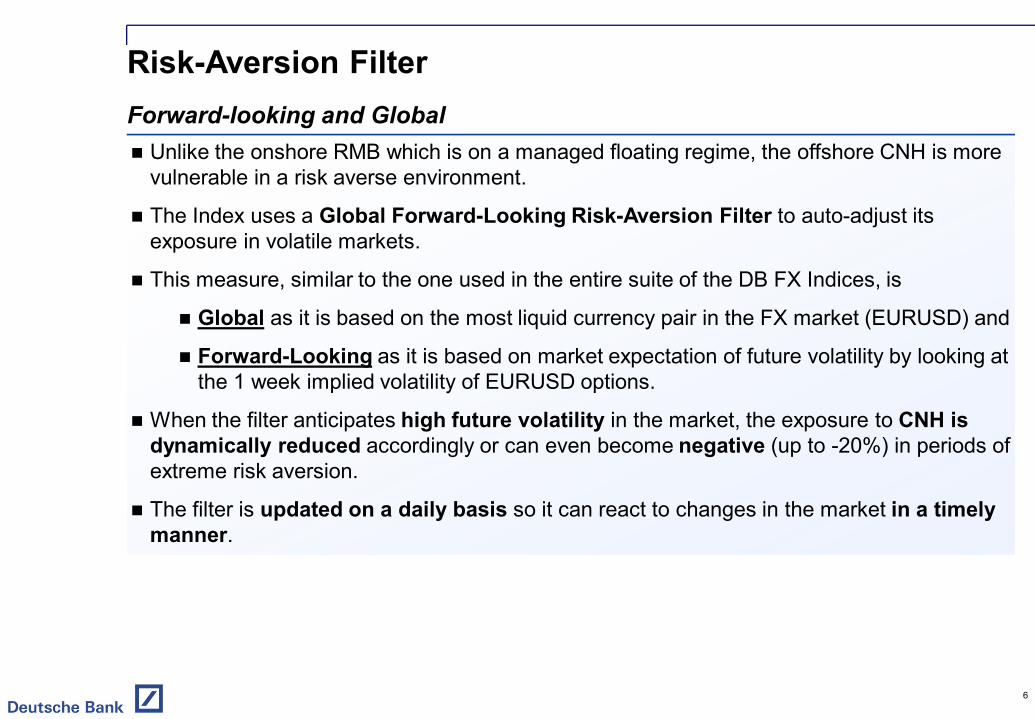

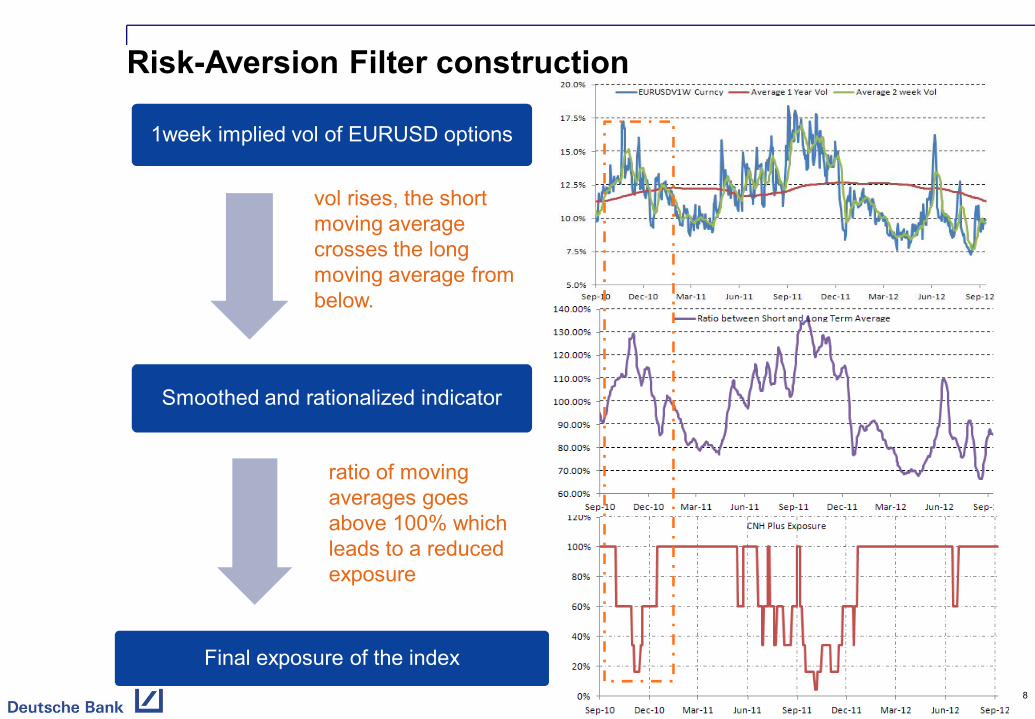

Risk-Aversion FilterForward-looking and Global Unlike the onshore RMB which is on a managed floating regime, the offshore CNH is more

vulnerable in a risk averse environment.

The Index uses a Global Forward-Looking Risk-Aversion Filter to auto-adjust its exposure in volatile markets.

This measure, similar to the one used in the entire suite of the DB FX Indices, is

Global as it is based on the most liquid currency pair in the FX market (EURUSD) and

Forward-Looking as it is based on market expectation of future volatility by looking at the 1 week implied volatility of EURUSD options.

When the filter anticipates high future volatility in the market, the exposure to CNH is dynamically reduced accordingly or can even become negative (up to -20%) in periods of extreme risk aversion.

The filter is updated on a daily basis so it can react to changes in the market in a timely manner.

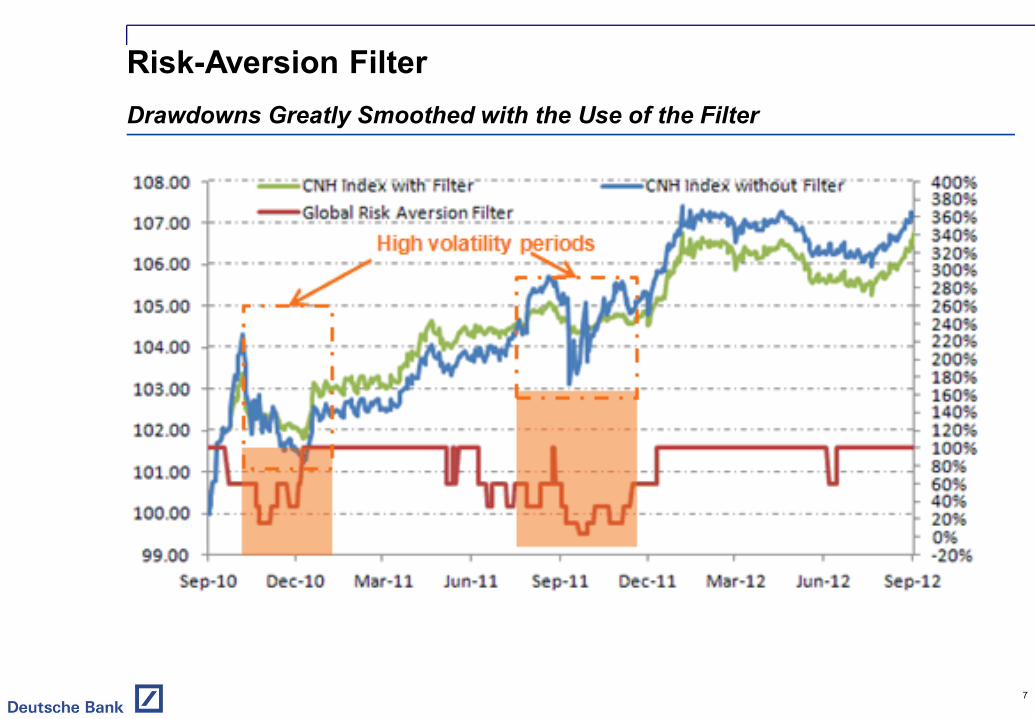

6

Risk-Aversion FilterDrawdowns Greatly Smoothed with the Use of the Filter

7

1week implied vol of EURUSD options

Smoothed and rationalized indicator

Final exposure of the index

Risk-Aversion Filter construction

8

vol rises, the short moving average crosses the long moving average from below.

ratio of moving averages goes above 100% which leads to a reduced exposure

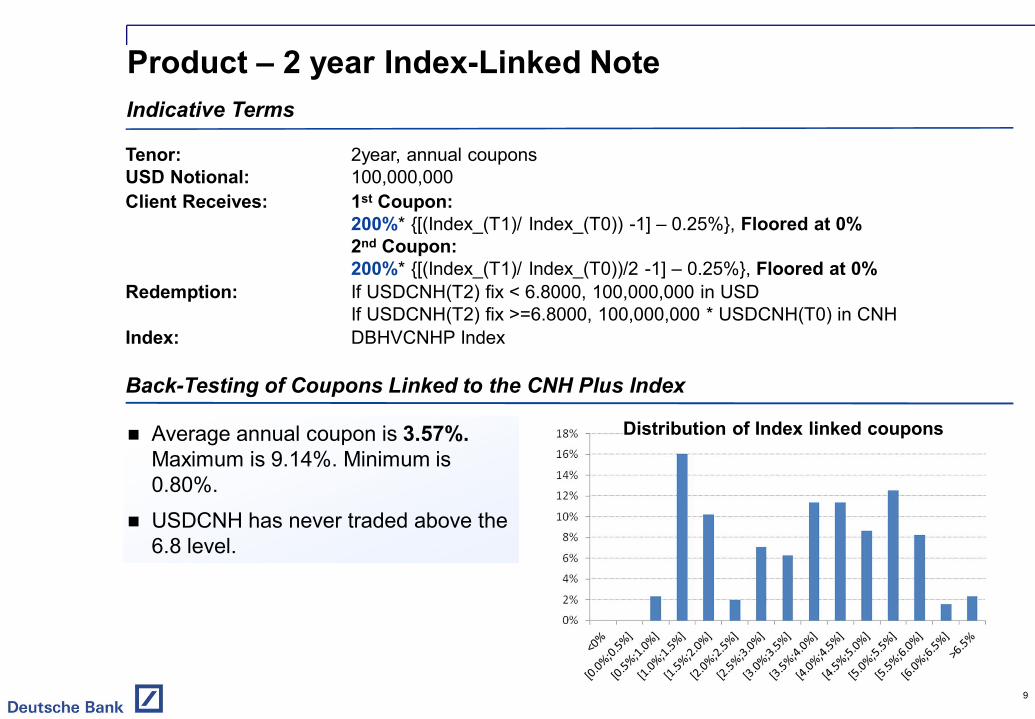

Product – 2 year Index-Linked Note

9

Indicative Terms

Tenor: 2year, annual couponsUSD Notional: 100,000,000Client Receives: 1st Coupon:

200%* {[(Index_(T1)/ Index_(T0)) -1] – 0.25%}, Floored at 0%2nd Coupon: 200%* {[(Index_(T1)/ Index_(T0))/2 -1] – 0.25%}, Floored at 0%

Redemption: If USDCNH(T2) fix < 6.8000, 100,000,000 in USDIf USDCNH(T2) fix >=6.8000, 100,000,000 * USDCNH(T0) in CNH

Index: DBHVCNHP Index

Back-Testing of Coupons Linked to the CNH Plus Index

Average annual coupon is 3.57%. Maximum is 9.14%. Minimum is 0.80%.

USDCNH has never traded above the 6.8 level.

Distribution of Index linked coupons

This document is intended for discussion purposes only and does not create any legally binding obligations on the part of Deutsche Bank AG and/or its affiliates ('DB'). Without limitation, this document does not constitute an offer, an invitation to offer or a recommendation to enter into any transaction. When making an investment decision, you should rely solely on the final documentation relating to the transaction and not the summary contained herein. DB is not acting as your financial adviser or in any other fiduciary capacity with respect to this proposed transaction. The transaction(s) or products(s) mentioned herein may not be appropriate for all investors and before entering into any transaction you should take steps to ensure that you fully understand the transaction and have made an independent assessment of the appropriateness of the transaction in the light of your own objectives and circumstances, including the possible risks and benefits of entering into such transaction. For general information regarding the nature and risks of the proposed transaction and types of financial instruments please go to www.globalmarkets.db.com/riskdisclosures. You should also consider seeking advice from your own advisers in making this assessment. If you decide to enter into a transaction with DB, you do so in reliance on your own judgment. The information contained in this document is based on material we believe to be reliable; however, we do not represent that it is accurate, current, complete, or error free. Assumptions, estimates and opinions contained in this document constitute our judgment as of the date of the document and are subject to change without notice. Any projections are based on a number of assumptions as to market conditions and there can be no guarantee that any projected results will be achieved. Past performance is not a guarantee of future results. This material was prepared by a Sales or Trading function within DB, and was not produced, reviewed or edited by the Research Department. Any opinions expressed herein may differ from the opinions expressed by other DB departments including the Research Department. Sales and Trading functions are subject to additional potential conflicts of interest which the Research Department does not face. DB may engage in transactions in a manner inconsistent with the views discussed herein. DB trades or may trade as principal in the instruments (or related derivatives), and may have proprietary positions in the instruments (or related derivatives) discussed herein. DB may make a market in the instruments (or related derivatives) discussed herein. Sales and Trading personnel are compensated in part based on the volume of transactions effected by them. The distribution of this document and availability of these products and services in certain jurisdictions may be restricted by law. You may not distribute this document, in whole or in part, without our express written permission. DB SPECIFICALLY DISCLAIMS ALL LIABILITY FOR ANY DIRECT, INDIRECT, CONSEQUENTIAL OR OTHER LOSSES OR DAMAGES INCLUDING LOSS OF PROFITS INCURRED BY YOU OR ANY THIRD PARTY THAT MAY ARISE FROM ANY RELIANCE ON THISDOCUMENT OR FOR THE RELIABILITY, ACCURACY, COMPLETENESS OR TIMELINESS THEREOF. DB is authorised under German Banking Law (competent authority: BaFin - Federal Financial Supervising Authority) and regulated by the Financial Services Authority for the conduct of UK business. Copyright© 2007 Deutsche Bank AG 10

Centre Contact Title Phone Email

Global Markets

Hong Kong Michelle-M Xu FX Structuring +852 2203 8726 [email protected]

Singapore Aurelie Dhellemmes FX Structuring +65 6883 1740 [email protected]

Contacts

Disclaimer

Disclaimer

RMB Development in Hong Kong

Michael Chan

Assistant Vice President

4 October 2012

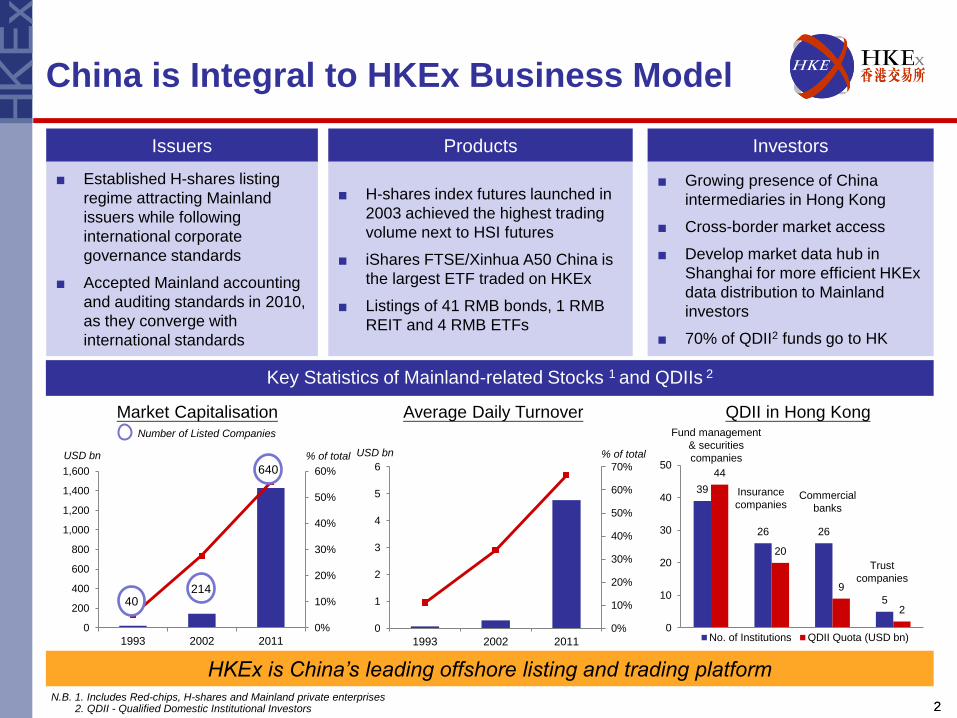

China is Integral to HKEx Business Model

2 2 N.B. 1. Includes Red-chips, H-shares and Mainland private enterprises 2. QDII - Qualified Domestic Institutional Investors

HKEx is China’s leading offshore listing and trading platform

39

26 26

5

44

20

9

2

0

10

20

30

40

50

No. of Institutions QDII Quota (USD bn)

Market Capitalisation Average Daily Turnover

0%

10%

20%

30%

40%

50%

60%

0

200

400

600

800

1,000

1,200

1,400

1,600

1993 2002 2011

USD bn USD bn

Key Statistics of Mainland-related Stocks 1 and QDIIs 2

% of total % of total

40 214

640

Number of Listed Companies

Issuers

■ Established H-shares listing

regime attracting Mainland

issuers while following

international corporate

governance standards

■ Accepted Mainland accounting

and auditing standards in 2010,

as they converge with

international standards

Products

■ H-shares index futures launched in

2003 achieved the highest trading

volume next to HSI futures

■ iShares FTSE/Xinhua A50 China is

the largest ETF traded on HKEx

■ Listings of 41 RMB bonds, 1 RMB

REIT and 4 RMB ETFs

Investors

■ Growing presence of China

intermediaries in Hong Kong

■ Cross-border market access

■ Develop market data hub in

Shanghai for more efficient HKEx

data distribution to Mainland

investors

■ 70% of QDII2 funds go to HK

QDII in Hong Kong

0%

10%

20%

30%

40%

50%

60%

70%

0

1

2

3

4

5

6

1993 2002 2011

Fund management

& securities

companies

Insurance

companies Commercial

banks

Trust

companies

50

150

250

350

450

550

650

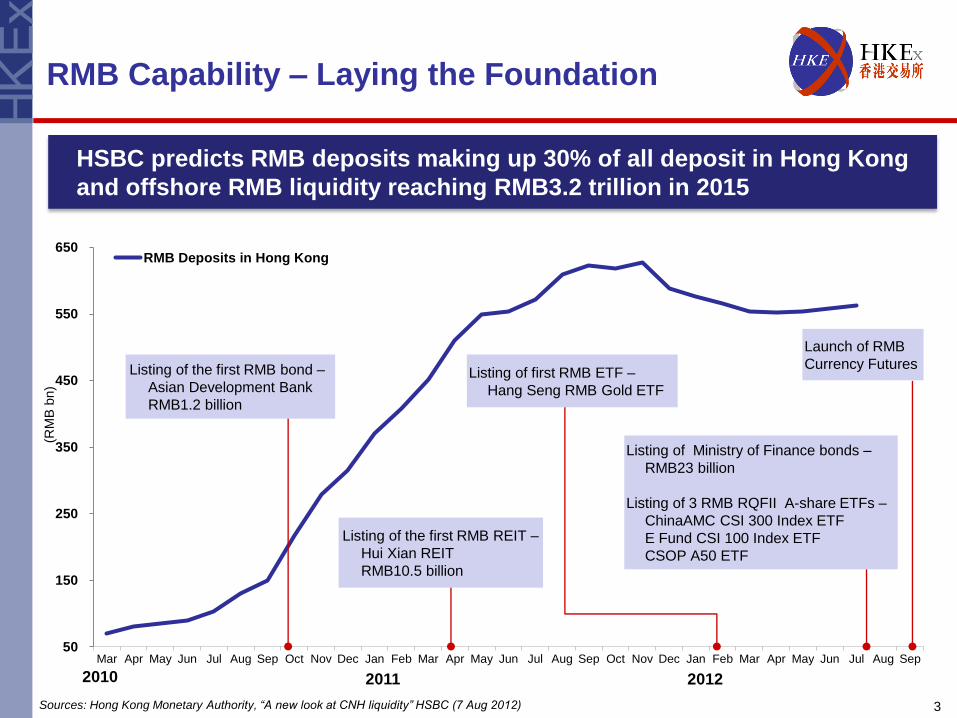

Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep

RMB Deposits in Hong Kong

3

RMB Capability – Laying the Foundation

Listing of the first RMB bond –

Asian Development Bank

RMB1.2 billion

Listing of the first RMB REIT –

Hui Xian REIT

RMB10.5 billion

Listing of first RMB ETF –

Hang Seng RMB Gold ETF

Launch of RMB

Currency Futures

2010 2011 2012

Sources: Hong Kong Monetary Authority, “A new look at CNH liquidity” HSBC (7 Aug 2012)

HSBC predicts RMB deposits making up 30% of all deposit in Hong Kong

and offshore RMB liquidity reaching RMB3.2 trillion in 2015

(RM

B b

n)

Listing of Ministry of Finance bonds –

RMB23 billion

Listing of 3 RMB RQFII A-share ETFs –

ChinaAMC CSI 300 Index ETF

E Fund CSI 100 Index ETF

CSOP A50 ETF

4

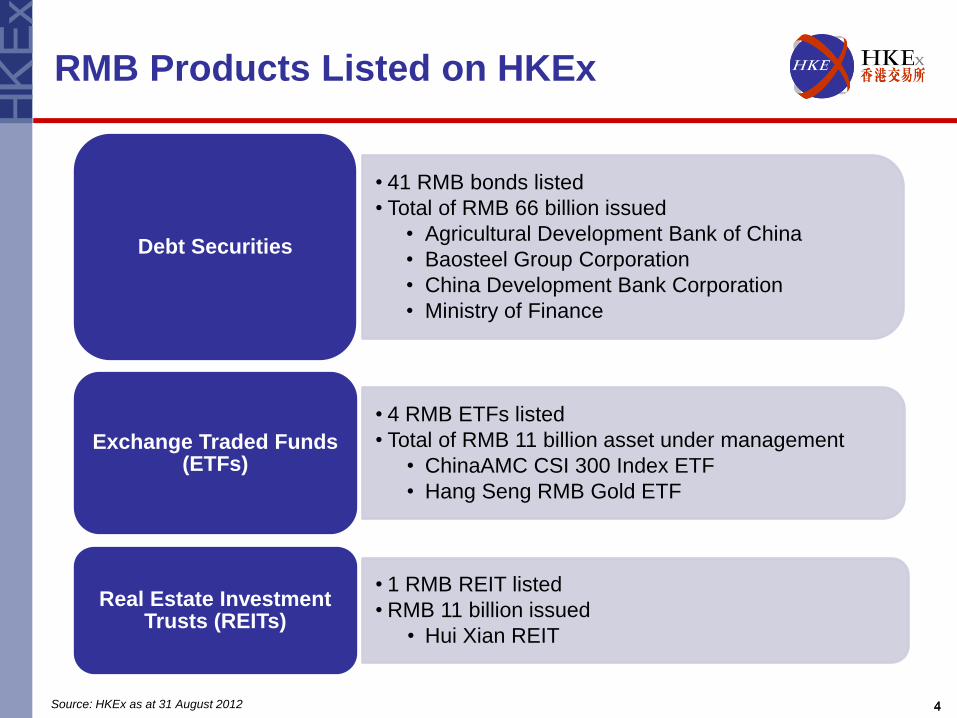

RMB Products Listed on HKEx

4 Source: HKEx as at 31 August 2012

• 41 RMB bonds listed

• Total of RMB 66 billion issued

• Agricultural Development Bank of China

• Baosteel Group Corporation

• China Development Bank Corporation

• Ministry of Finance

Debt Securities

• 4 RMB ETFs listed

• Total of RMB 11 billion asset under management

• ChinaAMC CSI 300 Index ETF

• Hang Seng RMB Gold ETF

Exchange Traded Funds (ETFs)

• 1 RMB REIT listed

• RMB 11 billion issued

• Hui Xian REIT

Real Estate Investment Trusts (REITs)

5 5

Questions and Answers

Related Documents