Chapter 5 C()NCLUSIONS Sl. No. CHAPTER CONTENTS PAGE 5.1 Conclusions 294 5.2 Recommendations 306 -293-

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 5

C()NCLUSIONS

Sl. No. CHAPTER CONTENTS PAGE

5.1 Conclusions 294

5.2 Recommendations 306

-293-

§5.1 Conclusions..:.

The following inferences can be drawn from the studies in the various chapters:

• DEMOGRAPHIC PROFILES: The demographic profiles differ significantly on

certain issues and are similar in certain issue over the two regions. - Region I

(Burdwan - Asansol in West Bengal ) and Region II (Dhanbad -Bokaro in Jharkhand .

./ AGE: The population are dissimilar in the average age suggesting Region II

people being younger than the region I customers. The average age of the

Region I customers are higher than the Region II customers .

./ EDUCATION: The two regions are similar in the educational level having a

general matriculation level of education .

./ FAMILY STRUCTURE : The populations of the two regiOns are

significantly different , they usually thrive from a joint family in Region II and

a nuclear family in Region I

./ NO. OF GENERATIONS IN TRANSPORT BUSINESS : The two regions

are similar in this perspective mostly belonging to the first generation in

transport business

./ EXPERIENCE IN TRANSPORT BUSINESS: The two regions are similar

in this perspective mostly having less than five years of experience in the

transport business .

./ ANNUAL TURN OVER: The two regions are similar in this perspective

mostly having less 10 lacs of Annual Tum over.

-294-

-/ FORM OF BUSINESS: The two regions are similar in this perspective

usually having a sole-proprietorship form of business.

To sum up, a retail customers of a commercial automobile loan is thus an

individual having an age in the thirties having an education of minimum

matriculation level thriving from a joint family in Region II and a nuclear family

in Region I; having an experience in the Transport business of less than 5 years,

with an annual tum over of around 10 lacs, having a fleet size of less than three

vehicles, and belongs to .a sole proprietorship or family owned form of business

usually in the first generation.

• PSYCHOGRAPHIC PROFILES : The consumer psychographic profile of the

two region are significantly different on certain issues and are similar in certain issues

-/ LOAN DECISION INFLUENCER: A customer of Region I usually

depends on the friends and the opinion leaders for the final decision making of

were to avail the loan from. However a customer of Region II mainly relies on

the dealers' suggestions and previous experience for the final decision

making.

-/ RISK TAKING PROPENSITY: The customers ofboth the regions are low

to moderate risk takers and very very conservative when it comes to there

financial transactions.

-/ OPENNESS TO NE,;v FORMS OF FINANCIAL TRANSACTIONS

LIKE PHONE AND NET BANKING: The populations of two regions are

significantly different in their openness to new forms of Financial

Transactions like phone and net banking. The populations in Region I are

-295-

comparatively are mon;: open to the modem forms of transactions like phone

and net banking.

~ ATTITUDE TOWARDS RELATIONSHIPS AND NETWORKING : The

attitude of the customers over the both the regions towards relationships and

networking are significantly different. The Region I people rely more on the

personal relations where as the Region II people keeping their professional

commitments at the top priority. What ever be the case it is found that both the

regions are similar on the views that relationships and networking are to a

certain extent essential for the success of business.

~ ATTITUDE TOWARDS POLITICS: The search for the reveals that there is

significant difference between the opinions of the customers of the two

regions with respect to their attitude towards politics. The customers of

Region I sustain on their political contacts only on emergency where as those

of Region II bank on their political contacts perpetually.

~ PREFERRED LANGUAGE OF COMMUNICATION: In an effort to

identified the most preferred language of communication it has found that it is

the regional languag<:, Hindi or Bengali, and not English, which is the most

preferred language of communication for these customers over the two

regiOns.

~ PREFERRED MEDIUM OF COMMUNICATION: In an effort to

understand the media habits of the customer populations over the two regions

it was found that th'e modem forms of medium like internet etc. are still to

-296-

make an impact and take the consumer in their stride. They prefer to stick to

the traditional forms of medium like Television and Newspaper.

../ FOOD HABITS: The food habit studies revealed that the customer

population base of Region I are mostly perpetual non-vegetarians and those of

Region II are partial non-vegetarians .

../ ENTERTAINMENT PREFERENCES: A probe into the entertainment

preferences suggest that the consumer bases of both the regions prefer

partying as a regular option for entertainment. They are occasional TV

viewers that too they watch mainly sports programs. Holidaying at religious

places along with the fi1mily once a year is also a preferred mode of taking a

break and enjoying life .

../ BELIEF IN GOD: A study on the populations does reveal that they are

atheists and staunch believers of God irrespective of the region .

../ ATTITUDE TOWARDS AESTHETICS AND THEIR IMPORTANCE

IN BUSINESS: They value aesthetics and feel that aesthetics and physical

ambience do matter a lot and is an indicator of service quality to be delivered

the Financing Institution .

../ SOCIAL CONSERVATIVENESS: They are socially conservative but

education conscious and prefer to have nuclear families rather joint ones.

• TYPE OF FINANCING INSTITUTIONS PREFERRED BY THE

CONSUMERS: The current preference pattern suggest that the majority of the

consumers of both the regions have availed loan from the NBFC in the organized

sector but, they preferred to avail the next loan from the Private Banks due to their

-297-

perception of higher levels of services being delivered by the Private Bank over the

two regions .

./ The Markov analysis suggests that the preference of the population in the next

purchase cycle of a retail commercial automobile loan is gradually shifting

towards the Private Banks from the Public Sectors Banks and the NBFC with

a high market share of around 65% in Region I and 64% in Region II in the

next few years.

• THE CRM FACTORS & ISSUES: The research work thus brings to light a few

very interesting facts. It highlights clearly that there are 1 0 distinct factors that govern

the CRM strategies of the existing Financing Institutions in the aforesaid regions.

These factors also form the basis of the decision making criteria for the choice of a

Financing Institution for availing a Retail Commercial Automobile Loan. They

factors are

1. Flexibility in documentation

2. Flexibility in CREDIT PROFILE JUDGEMENT

3. Flexibility in CHOICE OF MODE OF REPAYMENT

4. Flexibility in INTEREST RATES AND DOWNP A YMENT

5. Transparency in Operations

6. Tum around time (TAT) in Service delivery.

7. Level of augmented services delivered

8. EMI Collection mechanism

9. Default management mechanism

10. Info dissemination &Relational incentives provided to the customers.

-298-

CRM ISSUES : An intense look at the 1 0 factors further reveal that these

factors can be clubbed into 3 specific issues namely:

a) Flexibility Issues

b) Transactional Issues and

c) Relational Issues

The Flexibility Issues include Hexibility in documentations, flexibility in interest rates

and down payment, flexibility in credit profile judgment of the loan applicant,

flexibility in the choice of mode of repayment.

The Transactional Issues includes the transparency aspect in the transaction and day

to operations, the tum around time (TAT) in service delivery, the level of augmented

services delivered.

The Relational Issues incorporated the EMI collection mechanism, default mechanism,

information dissemination mechanism and relational incentive provided to the

customers.

• RELATIVE IMPORTANCE OF THE CRM FACTORS FOR THE

CONSUMER CHOICE OF' THE FINANCING INSTITUTION FOR AVAILING

A RETAIL COMMERCIAL AUTOMOBILE LOAN: The in-depth Analytic

Hierarchy Process study of the 10 factors brought to light that in both the regions the

most important criterion for the choice of an FI for the BIG decision is the Flexibility in

the Negotiation oflnterest rates and down payment.

-299-

AHPwts Region I Region II

Flexibility in Interest Rates and 0.2803 0.2831

Down payment

Flexibility in Documentation 0.135 0.0807

Transparency in Transactions 0.1185 0.1987

EMI Collection Mechanism 0.1101 0.0768

Turn Around Time in Service 0.0777 0.0849

delivery

Default Management 0.0775 0.0749

Information Dissemination and 0.0738 0.0371

Relational Incentives Flexibility in the choice of mode of

0.0615 0.0932 Repayment

Flexibility in Credit Profile 0.0509 0.0329

Judqment

Augmented Services provided ' 0.0147 0.0379

' Consistanc~ Ratio: 0.0987 Consistancy Ratio: 0.0893

It seems that this flexibility to negotiate really gives the consumers something more

than mere monetary benefit. It gives them an immense sense of achievement and makes

them feel special. It has been observed that even a slightest flexibility do work wonders

to the consumer-service provider relationship, and it helps the consumer to move up the

ladder ofloyalty becoming advocates and partners in business.

• CONSUMERS' PERCEPTIONS OF THE FINANCING INSTITUTIONS IN

TERMS OF THE CRM STRATEGIES DEPLOYED :

The research bring to light that the consumers perceptions, regarding the CRM tools

being deployed by the Financial Institutions, over the two regions are significantly

different. In both regions the most preferred service provider for a retail commercial

-300-

automobile loan are the Private Banks. The preference ranking in both the regions are

as follows:

!.Private Banks

2.NBFCs

3.Public Sector Banks.

The regions for the high preference score for The Private Banks could be identified in

the due course of the research work.

• FACTORS INFLUENCING THE CHOICE OF THE CHANNEL

PARTNERS FINANCING INSTITUTIONS FOR TIE-UPS : According to the

channel partners' perception th(: factor influencing the choice of financing institution

for tie-ups could be summed up as follows:

./ The ranking of the factors obtained by the sum of ranks reveal that

relationship of the marketing executive of the financial institutions is the most

important factor over both the regions for all classes of channel partners. Thus

relationship marketing and continuous Internal Customer Relationship

Management (CRM) strategies of the financing institution should be designed

in such a way that it not only gives pecuniary benefits but also relational

exchanges like mutual trust, commitment, cooperation, shared values, keeping

of promises and above all a continuous communication. As suggested by the

literature review HCRM (CRM with a human touch) rather than e CRM

(Electronic CRM) is most effective in this case .

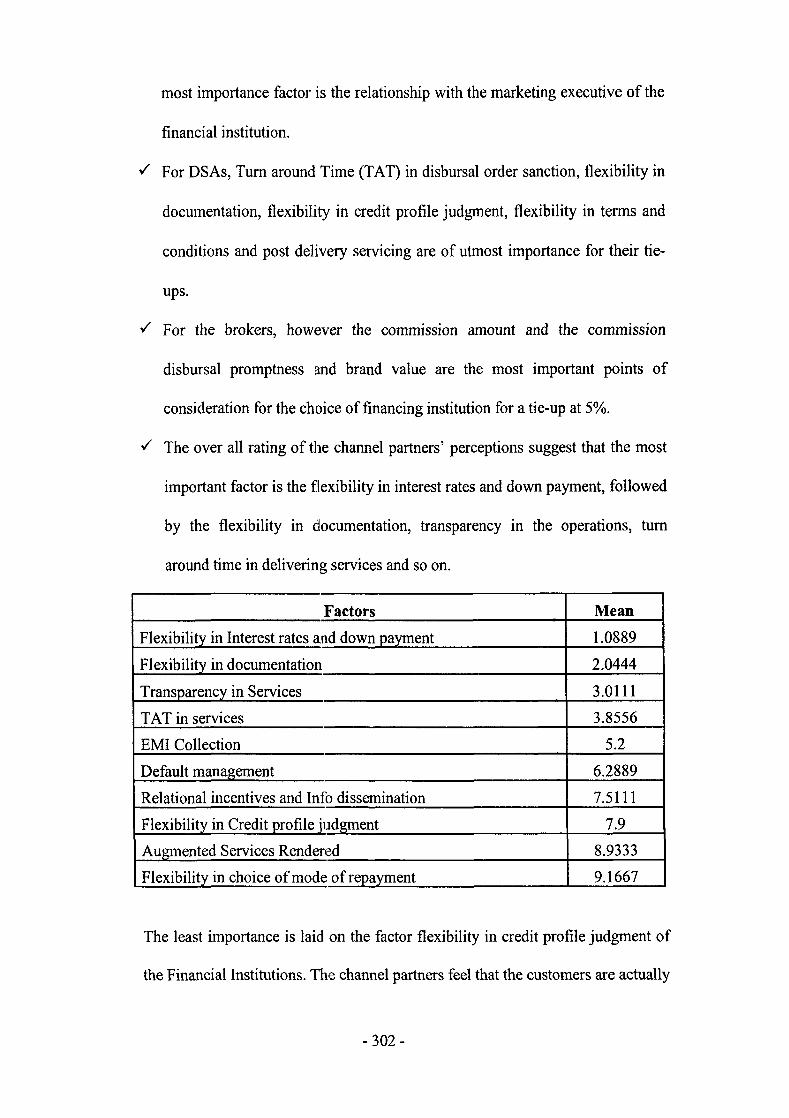

./ Tum around Time (TAT) in disbursal order sanction, flexibility in

documentation is the two least importance factors for the dealers. For them the

- 301 -

most importance factor is the relationship with the marketing executive of the

financial institution .

./ For DSAs, Turn around Time (TAT) in disbursal order sanction, flexibility in

documentation, flexibility in credit profile judgment, flexibility in terms and

conditions and post delivery servicing are of utmost importance for their tie-

ups .

./ For the brokers, however the commissiOn amount and the commissiOn

disbursal promptness and brand value are the most important points of

consideration for the choice of financing institution for a tie-up at 5% .

./ The over all rating of the channel partners' perceptions suggest that the most

important factor is the flexibility in interest rates and down payment, followed

by the flexibility in documentation, transparency in the operations, turn

around time in delivering services and so on.

Factors Mean

Flexibility in Interest rates and down payment 1.0889

Flexibility in documentation 2.0444

Transparency in Services 3.0111

TAT in services 3.8556

EMI Collection 5.2

Default management 6.2889

Relational incentives and Info dissemination 7.5111

Flexibility in Credit profile judgment 7.9

Augmented Services Rendered 8.9333

Flexibility in choice of mode of repayment 9.1667

The least importance is laid on the factor flexibility in credit profile judgment of

the Financial Institutions. The channel partners feel that the customers are actually

-302-

less bothered about the flexibility provided by the financial institutions in credit

profile in the credit profile judgment issue. A lesser emphasis on this particular

CRM tool therefore, may not affect the customers' perceptions'.

• CHANNEL PARTNERS' PERCEPTIONS OF THE FINANCING

INSTITUTIONS IN TERMS OF THE CRM STRATEGIES DEPLOYED BY

THEM:

./ According to the perception of channel partners, the NBFCs score high on the

factors related to the flexibility issues, the tum around Time (TAT) in

disbursal order sanction, collection mechanism and default management

mechanism, and continuous relationship management and communication .

./ The Private Banks score high on post delivery servicing, flexibility m

documentation and flexibility in terms and conditions and transparency issues

their efficient service delivery in issues like PDC swapping and hassle-free

NOC release ;give them competitive age. The public sector banks are lye

behind the private players because of their traditional and reactive mode of

functioning. According to their perception the private players (Private Banks

and NBFCs) are more preferred over .the Public Sectors Bank .

./ Thus it can be concluded that, according to the perception of the channel

partners the private players are more preferred than the public sector banks

by the customers.

-303-

• THE CRM GAPS :

The study to identified the gaps that is the impediments in the process of

implementing the CRM tools by the Financial Institutions reveal that there are

five distinct gaps namely market research gap, design gap, conformance gap,

communication gap which finally get reflected in the consumer gap of the

Financial Institutions laundering retail commercial automobile loan .

./ The market resean=b gap which exists because of a distorted perception of

the consumer expectation by the management. It has been found that their

exists a negative consumer gap for all the three CRM issues namely flexibility

issue, transactional issues and relational issues across the three type of

Financial Institutions with the least gap for NBFCs and highest gap of the

Public Sector Banks.

The NBFCs have the least gap over all the three issues but score exceptionally

well over the flexibility issue. Which means the management of the NBFCs are

able to judge the consumer expectations with accuracy and therefore can deliver

well in the relational perceptive .

./ The design gap also features with a negative score for all the three CRM issue

across the three classes of Financial Institutions. It means that the service

quality design spe(:ifications are far behind what the managers perceive to be

the customers expectations. It is evident from the results the gaps are the

highest for the Public Sector Banks and least for The Private Banks which

conform that the Private Banks have much superior service deli very

specification than the other classes of Financial Institutions.

-304-

../ The conformance gnp which is explained by the difference between the

service quality delivered and service design specification, when studied bring

to light quite and inter•esting picture. The gaps have positive scores in the case

ofNBFCs and Public Sector Banks and negative for the Private Sector Banks.

This means that though the system do not have provisions for meeting

customers expectatiom;, the relationship managers of the Public Sector Banks

and NBFCs go out of the way to personally support the customer by

delivering services which meet the customers expectations. The Private Banks

on the other hand has better service design but less proactive people to

implement the service designs .

../ The communication g:ap which is explained by the difference by between

service delivery and promises made by the Financial Institutions to their

customers when probed in details suggested that there is negative score for all

the Financial Institutions for the three CRM issue, namely - flexibility issues,

transactional issues and relational issues, across the two regions. However the

gaps are the least for The Private Banks and the highest for The Public Sector

Banks. A negative score indicates a situation of over promises and under

delivery which leads to utmost customers' dissatisfaction .

../ Consumers gaps or cu:stomers satisfaction gaps which is explained by the

difference between consumers expectation and perception of service delivery

by the Financial Institutions, when studied in details suggested a high level of

dissatisfaction among th(: Public Sector Banks over all the three issues namely

- flexibility issues, transactional issues and relational issues. The NBFCs

- 305-

however have low to moderate satisfaction level over the three aforesaid

issues and the Private~ Banks emerged as the highest positive scorers

suggesting customers ddight. It means that they are on a continuous research

mode identifying potential offer to be made to the customers which not only

meet their needs but also surpasses them. This leads to customers' pleasant

surprise and binds them in a close relationship.

§5.2 Recommendations

The research study brought to light several interesting facts which requires immediate

attention and implementation.. It is suggested that to gain a competitive edge the

following measures should be implemented. They are

• Customized Services

The customers' needs should be accurately assessed, thus reducing the market

research gap and designing the offers in accordance to the specific customer

needs. Every individual customer is different from the other customers and

therefore requires a special attention and conceptualization of services which are

to be delivered to them. Relationship marketing emphasize on establishing

exclusive relations with t:ach of the customers separately. The 10 CRM factors

identified in the research thesis are the key variables which can either lead to

customer satisfaction or customer dissatisfaction. Some customers prefer

flexibility in interest rates at the cost of transparency in transactions. Some other

customers prefer promptness in service delivery and for that they are even ready

to pay a higher sum. Some customers prefer the Financial Institutions which have

a very effective EMI collection mechanism and yet there are some customers who

-306-

prefer the Financial Institutions which give better relational incentives in the form

of top up funding, refinance or repeat funding. The best practices in the industry

suggest that a top up fund:[ng or a concession in the repeat funding clubbed with

warm relations with the individuals customers do make a lot of impact and ensure

to bind the customers with the Financial Institution for ever, thus enhancing the

Customer Life Cycle.

• Relational Incentives :

"-' Top-Up Funding -· A usual practice with the NBFCs and referred to as

Top-up loans or Overdraft Facility, is a very popular Relational Incentive

for their Excellent Track Record/ Good Track Record holder customers.

Top-up loans in the Retail Commercial Automobile Loan segment has a

slight variation over the other segments. In this, an existing loan account,

at least one-year old, is usually closed down for an ETR /GTR customer

and a new account is created on the same asset, based on the as on date

value of the asset. The loan thus issued acts as a settlement of the previous

outstanding loan amount and also as source of working capital. Thus,

refinancing of the same asset converts the blocked capital to a source of

liquid working capital.

"-' Top up Funding- For purchase of tyres and spares and meeting cost of

repair & maintenance of vehicle to existing borrowers under the scheme

having regular repayment track record of existing loan for at least one

year.

-307-

~ Repeat Financing -- another relational incentive, prevalent mostly with

the private players mainly the NBFCs and the Private Banks. In this form,

the existing ETR/GTR customer is given a special discounted rate of

interest and even a discounted rate on the down payment and Loan-to

value issues.

• Catch the Middlemen and give them something more than mere commission

- The research thesis suggests that the Channel partners look out for something

more than mere pecuniary benefits. And one-to-one relationships with them do

cover up for many a flaw in the system. It is mostly these relationship

management efforts of the marketing executive of the financing institution that

prompts them act as thei:r advocates and partners in business. A one-to-one CRM

and continuous Internal Customer Relationship Management (CRM) strategies of

the financing institution should be designed in such a way that it not only gives

pecuniary benefits but also relational exchanges like mutual trust, commitment,

cooperation, shared values, keeping of promises and above all a continuous

communication. As suggested by the literature review HCRM (CRM with a

human touch) rather thane CRM (Electronic CRM) is most effective in this case.

This may be achieved by entertaining the channel partners with parties, and

special holiday packages etc. to make them feel special. Especially designed trade

promotion tools like Contests, Annual appraisal meetings and acknowledgement

awards for high business generators can be very rewarding.

-308-

• Convert the existing customers I opinion leaders into middlemen - The

research study suggested that the major influencers in the loan decision making

process are usually the friends of the prospective customers who are already

established in the transport business and have availed such a loan . They serve as

the opinion leaders, and 'buzz marketing' or 'word of mouth' is the strongest and

most effective mode of promotion for a service product like a retail commercial

automobile Joan. Efforts thus, should be taken by the Financing Institutions to

create and manage a pos:[tive word of mouth. This can very well be achieved

through superior service quality and customized relational benefits like converting

the existing customers into advocates and partners in business. Most of the

NBFCs like Magma and SREI thrive with this model of business, wherein a

referred customer by an existing client not only gets a benefit but also the

individual customer who refers get a pecuniary benefit of the brokerage which is

entitled for the specific amount of disbursal. This creates a win-win situation for

the existing customer as well as the Financing Institution and hence proves to be

very very effective. The other Banks and the NBFCs who do not implement this

strategy may make an effort to implement this strategy and generate more and

more leads.

• Improve transparency in the transactions - The practices of providing an

amortization schedule with the welcome kit, regular Statement of accounts,

money receipts for every transaction are certain practices which are followed by

the Private Banks like HDFC and ICICI Bank. These efforts are very much

appreciated by the customers and they create a positive word of mouth and

-309-

enhanced image in their perceptual maps. The NBFCs and the Public Sector

Banks are a step behind in this perspective should make efforts to incorporate

these practices for gaining a competitive edge.

• Flexibility in genuine cases (High Profile Customers) - The flexibility issues

include flexibility in documentations, flexibility in interest rates and down

payment, flexibility in credit profile judgment of the loan applicant, flexibility in

the choice of mode of repayment. At times, when the customers are usually High

net worth Individuals a certain degree of flexibility may be allowed which is

normally the practice of the private players. These efforts are very much

appreciated by the customeTs and make them feel very special. As a result, they

create a positive word of mouth and enhanced image in their perceptual maps.

The Public Sector Banks are a step behind in this perspective and should make

efforts to incorporate these practices for gaining a competitive edge.

• Improve on TAT (Turn Around Time)- Promptness or pace in delivery of the

services like Disbursal order sanction, Statement of Account release, No

Objection Certificate (NOC) release, Post Dated Cheque (PDC) swapping or

foreclosure of an account or any sort of grievance handling, has been established

as one of the prime factors of concern for the choice of Financial Institution for

availing a retail commercial automobile loan. The Private players especially the

NBFCs and Private Banks are superior to their Public Sector counter parts. They

take less time to deliver. A proactive effort in this field can contribute manifold

in building a positive image for them.

- 310-

• Regular contact with the cmitomers will help manage default rate- A continuous

touch with the customers not only help the Financing Institutions to keep track of the

whereabouts of the customers but also helps in curbing the default rates. Proactive

practices like-a field investigation prior to loan disbursal, a face to face talk with

customers matching their expectations and delivering accordingly, Pre ca11ing two

days prior to the EMI due date, a thank you call for an on time payment of EMI , a

reminder soft call for one EMI (0 to 30 days) default, a Hard call for 30 to 60 days

default, a Party visit on 60 to 90 days default , Legal notice for 90 + days default,

Repossession of assets for 120 days or more days of default do help keeping the NP A

to minimal levels. The Financing Institutions who do not proactively implement these

strategies should give it a serious consideration and implement them to ensure their

sustainability and enhancement in business.

• Provide your customers with something extra every time: "Delight the

Customers don't mere satisfy them"- Don'tjust meet expectations, surpass

them. That is the main mantra for success in today's business scenario. The

researchers have chalked out a 4-fold Customer -centric FILE approach which

can actually help in achieving the same.

- 311 -

The Customer centric - FILE APPROACH -for delighting the customers

The future of the Financial Institutions in the Retail Commercial Automobile Loan

Segment thus, depends entirely on their actions today. First and foremost they should

have a farsighted vision. The success of a financing business is not only in the disbursal

and accrual of loan amount hut also effective and efficient recovery of the loan plus the

interest. And that definitely calls for a Four-fold approach called the FILE Approach .

FILE is the acronym of the four facets of this approach comprising of Flexibility,

Integrity, Lucidity and Effici,:::ncy that surely spells out success for a financing business in

the present scenario.

Flexibility: refers to the flexibility in terms and conditions that would help the Financing

Institutions to customize their product offerings, the first step towards an effective

Customer Relationship Management.

Integrity: the second step in effective CRM, which deals with the reliability , credibility

and honesty on the part of both the parties (the Fis & the Customers).

Lucidity : in Documentation as well as in communication of terms and conditions should

be a mandatory practice to avoid future litigations in the transaction.

Efficiency: on the part of the FI in terms of loan disbursal and on the part of the customer

in terms of on time EMI payments.

- 312-

BANKS& NBFCS

Far Sighted Vision

requues

makin!!

+ Lucidity in

documentation

'FILE' Approach

To achieve

Overall Efficiency & Effectiveness.

To achieve

• Customer Satisfaction • High Productivity • Profitability

Efficiency in Loan disbursal (for Fls) &

Repayment (for customers)

• Greater Business Volumes

Increased Social Responsibility

Gives rise to

New, Better & Improved Consumer Financing Products coverine: a wide spectrum (Hum Hai Na for all see:ments)

- 313 -

The FILE Approach if practiced diligently would definitely gtve way to Overall

efficiency and effectiveness of the FI & that would spell out success with greater business

volumes, customer satisfaction & :profitability.

This in tum gives way to enhanced Corporate Image and hence more social responsibility

which once again calls for new improved product offerings on the part of the Financial

Institution. And in a process to cater to that requirement shall become a "Financial

Supermarket" offering all sorts of financial products and services under one umbrella.

Saying "Hum Hai Na" to its customer base, just like ICICI Bank Ltd. does today.

In short the Financial Institutions' efforts to attain Customer Delight are the key to

success in today's competition driven market. And would involve a detailed analysis

of the customer information, or data mining to

cr Identify factors that motivate the customers to avail their products and services

cr Understand the customers' p8ychographics.

w Understand the value of consolidating existing relationship.

w Identify the most valuable current and potential clients.

CJF Hence achieve competitive advantage by tendering customized products.

Clearly a customer centric FILE approach can be successful if it is able to successfully

integrate the front and back office to provide real time updates to the strategic business

decision-makers. Further their success lie in the fact that they are implemented in

staggered steps with clearly defined objectives for each customer category.

Implementation may be done through a number of pilot projects, which will allow the

- 314-

Financial Institutions to gauge the efficacy of the solution and make whatever course

corrections, necessary before launching into a full-fledged rollout to all its customers.

§ 5.3 FUTURE SCOPE OF RESEARCH:

Further research studies may thus be concentrated on the issues like

~ Improving on TAT (Turn Around Time) in service delivery by

reducing process losses

~ Enhancing transpa1rency in services

~ Adjudging the individual customer needs

~ Designing better st~rvice products matching the customer

expectations.

§ 5.4 Limitations of the Res•~arch

• Distance (F'or Region II)

• Time

• Funds

- 315-

BIBLIOGRAPHY:

1. Aaker, David A. Managing Brand Equity: Capitalizing on the Value of a Brand

Name. New York:

2. Adelaar, T. (2000). Electronic commerce and the implications for market structure:

The example of the art and antiques trade. Journal of Computer-Mediated

Communication, 5 (3). Retrieved 25 June 2004 from

http://www.ascusc.org(jcmc/vol5/issue3/adelaar.htm.

3. Alderson, W. (1954) Factors Governing the Development of Marketing Channels, in

Clewett, R. (Ed.), Marketing Channels for Manufactured Products, pp. 5-34. Richard

D. Irwin, Inc., Homewood, IL

4. Alderson, W. (1965) Dynamic Marketing Behavior: A Functionalist Theory of

Marketing. Richard D. Irwin, Inc., Homewood, IL.

5. Anderson, J. C. and Narus, J. A. (1990) A Model of Distributor Firm and

Manufacturer Firm Working Partnerships. Journal of Marketing, Vol. 54, January,

pp. 42-58.

6. Anderson, J. C. and Narus, J. A. (1991) Partnering as a Focused Market Strategy.

California Management Review, Spring, pp. 95-113.

7. Anderson, Kristin. Customer Relationship Management. Blacklick, OH, USA:

McGraw-Hill Education Group, 2001. p 2.

8. Angehrn A. A., (1997). The ICDT model: Towards a taxonomy of Internet-related

business strategies. CALT at INSEAD, France.

- 316-

9. Arndt, J. (1979) Toward a Concept of Domesticated Markets. Journal of Marketing,

Vol. 43, Fall, pp. 69-75.

10. Aubert, B., Rivard, S., & Patry, M. (1994). Development of measures to assess

dimensions of IS operation transactions. Proceedings of the International Conference

on Information Systems, Vancouver, 15, 13-26.

11. Avlonitis, J. G., & Karayam1i, A. D. (2000). The impact oflntemet use on business

to-business marketing. Industrial Marketing Management, 29(5), 441-459.

12. Bagozzi, R. P. (1974) Marketing as an Organized Behavioral System of Exchanges,

Journal of Marketing, Vol. 38, October, pp. 77-81.

13. Bagozzi, R. P. (1978) Marketing as Exchange: A Theory of Transactions in the

Market Place, American Behavioral Scientist, Vol. 21, March/April, pp. 535-556.

14. Bagozzi, R. P. (1979) Toward a Formal Theory of Marketing Exchanges, in Ferrell,

O.C.,

15. Bagozzi, R. P. (1994) Interactions In Small Groups: The Social Relations Model, in

Sheth, J.N. and Parvatiyar, A. (Eds); Relationship Marketing: Theory, Methods and

Applications, Center for Relationship Marketing, Emory University, Atlanta.

16. Bakos, Y., & Dellarocas,, C. (2002). Cooperation without enforcement ? A

comparative analysis of litigation and online reputation as quality assurance

mechanisms. Proceedings of the International Conference on Information Systems,

23, 127-142.

17. Bartels, R. (1962) The Development of Marketing Thought. Richard D. Irwin, Inc.

Homewood, IL.

- 317-

18. Bartels, R. (1965) Development of Marketing Thought: A Brief History, in Schwartz,

G. (Ed.), Science in Marketing. pp. 47-69, John Wiley & Sons, Inc., New York.

19. Bartels, R. (1976), The History of Marketing Thought, Second Edition. Grid Inc.,

Columbus, Ohio.

20. Barton, S. G. (1946) The Movement of Branded Goods to the Consumer, in

Blankenship, A.D. (Ed.}, How to Conduct Consumer and Opinion Research. pp. 58-

70, Harper & Bros., New York.

21. Bass, F. M. (1993) The Future of Research in Marketing: Marketing Science, Journal

of Marketing Research, Vol. XXX, February, pp.l-6.

22. Bell, H., & Tang, N. K. (1998). The effectiveness of commercial Internet Web sites:

A user's perspective. Internet Research: Electronic Networking Applications and

Policy, 8(3), 219-228.

23. Bendapudi, N., & Leone, R. (2002). Managing business-to-business customer

relationships following key contact employee turnover in a vendor firm. Journal of

Marketing, 66(2), 83-101.

24. Berry, L. L. (1983) Relationship Marketing, in Berry, L.L., Shostack, G.L., Upah,

G.D. (Eds.) Emerging Perspectives on Service Marketing. pp. 25-38, American

Marketing Association, Chicago, IL.

25. Berry, L. L. (1983). Relationship marketing. In L.L. Berry, G.L. Shostack, & G.D.

Dpah (Eds.), Emerging perspectives on service marketing (pp. 28-38). American

Marketing Association.

26. Berry, L. L., & Parasuraman, A. (1991). Marketing services: Computing through

quality. MA: Free Press/Lexington Books. Lexington.

- 318-

27. Berry, L., and A. Parasuraman. Marketing Services. New York: Free Press, 1991.

28. Berthon, P., Pitt, L. F., & Watson, R. T. (1996). The World Wide Web as an

advertising medium: Toward an understanding of conversion efficiency. Journal of

Advertising Research, 1(1), 43-54.

29. Bitner, J. M. (1995). Building service relationships: It's all about promises. Journal of

Academy of Marketing Science, 23(4), 246-251.

30. Borg, K. (1997). A decision Internet tool for Web marketers. New Technology

Showcase, 14(5), 12-20.

31. Brand Performance: The Role of Brand Loyalty." Journal of Marketing 65 (2001 ):

81-93.

32. Breyer, R. F. (1934) The Marketing Institution. McGraw-Hill Book Co., New York.

Business International Corporation (1987) Competitive Alliances: How to Succeed at

Cross-Regional Collaboration. Business International Corporation, New York.

33. Brown, S.W., and Lamb, Jr., C.W. (Eds), Conceptual and Theoretical Developments

in

34. Butler, R. S. (1923) Marketing and Merchandising. Alexander Hamilton Institute,

New York.

35. Cannie, J. K., and Caplin, D. (1991) Keeping Customers for Life. American

Management Association, New York.

36. Cannon, J. and Sheth, J. (1994) Developing a Curriculum to Enhance the Teaching of

Relationship Marketing, Journal of Marketing Education, Vol. 16, Summer, pp. 3-14.

37. Carratu, V. (1987) Commercial Counterfeiting, in Murphy, J. (Ed.), Branding: A Key

Marketing Tool. The Macmillan Press Ltd., London.

- 319-

38. Chatterjee, D., Grewal, R., & Sambamurthy, V. (2002). Shaping up forE-commerce:

Institutional enablers of the o:rganizational assimilation of Web technologies. MIS

Quarterly, (26)2, 65-89.

39. Chaudhuri, A., and M. Holbrook. "The Chain of Effects from Brand Trust and Brand

Affect to Brand Performance: The Role of Brand Loyalty." Journal of Marketing 65

(2001): 81-93.

40. Chiu, C-M. (2003). Towards integrating hypermedia and information systems on the

Web. Information and Management, 40(3), 165-175.

41. Chow, S., & Holden, R. (1997). Toward an understanding ofloyalty: The moderating

role of trust. Journal of Managerial Issues, 9(3), 275-298.

42. Christopher, M., Payne, A. and Ballantyne, D. (1991) Relationship Marketing.

Butterworth-Heinemann Ltd., Oxford, U.K.

43. Churchill, G. A. (1979). A paradigm for developing better measures of marketing

constructs. Journal of Marketing Research, 16( 1 ), 64-73.

44. Churchill, H.L. (1942), How to Measure Brand Loyalty, Advertising and Selling. Vol.

35, pp. 24ff.

45. Colman A. and Pulford B.," A Crash Course in SPSSfor Windows", 3rd Edition,

Blackwell Publishing, 2006.

46. Compton, Jason. "On Time:, On Target." Destination CRMNov. 2001. 18 Sept. 2002

47. Converse, P. D. and Huegy, H. (1940) The Elements of Marketing. Prentice-Hall,

Inc., New York.

48. Copulsky, J. R., and Wolf, M. J. (1990) Relationship Marketing: Positioning for the

Future, The Journal of Business Strategy. July/August, pp.l6-20.

-320-

49. Coyles, S. and T. C. Gokey. "Customer Retention Is Not Enough." The McKinsey

Quarterly 2

50. Crone, P. (1989) Pre-Industrial Societies. Basil Blackwell, Inc., Cambridge, MA.

51. Crosby, L.A. and Stephens, N. (1987) Effects of Relationship Marketing on

Satisfaction, Retention, and Prices in the Life Insurance Industry, Journal of

Marketing Research. Vol. 24, November, pp. 404-411.

52. Crosby, L. A., Evans, K.R., and Cowles, D. (1990) Relationship Quality in Services

Selling: An Interpersonal In:fluence Perspective, Journal of Marketing. Vol. 52, April,

pp. 21-34.

53. Cundiff, E. W. (1988), The Evolution of Retailing Institutions across Cultures, in

Nevett, T. and Fullerton, R.A. (Eds.), Historical Perspectives in Marketing: Essays in

Honor of Stanley C. Hollander. Lexington Books, Lexington, Massachusetts.

54. Customer Lifetime Value is Reshaping Corporate Strategy. New York: Free Press,

2000.

55. DeVries, J. (1976) Economy of Europe in an Age of Crisis 1600-1700. Cambridge

University Press, Cambridge ..

56. DeYoung, B., & Boldt, W. (1998). Relationship marketing: Putting relationships to

work. Ithaca, NY: Cornell Cooperative Extension Marketing Manual.

57. Dholakia, U. M., & Rego, L. (1998). What makes commercial Web pages popular?

An empirical investigation of Web page effectiveness. European Journal of

Marketing, 32(7 /8), 724-736.

58. Dick, A. S., & Basu, K. (1994). Customer loyalty: Toward an integrated conceptual

framework. Journal of the Academy of Marketing Science, 22(2), 99-113.

- 321 -

59. Dillon, W., et al. "Understanding What's in a Brand Rating: A Model for Assessing

Brand and Document Systems Foundation, 2001.

60. Domingo II, G. E., & Hui, K-L. (2003). The effects of retail format characteristics on

e-loyalty. Ninth Americas Conference on Information Systems, 139-148.

61. Duddy, E. A. and Revzan, D.A. (1947) Marketing: An Institutional Approach.

McGraw- Hill Book Company, Inc., New York.

62. Dufour, J-C., & Maisonnas, S. (1997). Marketing et services: Du transactionnel au

relationnel. Sainte-foy, Quebec: Les presses de l'Universite Laval.

63. Dwyer, F. R., Schurr, P. H., & Oh, S. (1987). Developing buyer-seller relationships.

Journal of Marketing, 51(2), 11-27.

64. Dwyer, F. R., Schurr, P. H., and Oh, S. (1987) Developing Buyer Seller

Relationships, Journal of Marketing, Vol. 51, April, pp. 11-27.

65. Early Hellenistic Greec~~ (500-300 B.C.), in Nevett, T. and Hollander, S. (Eds.),

Marketing in Three Eras: Proceedings of the Third Conference on Marketing

History.pp. 13-22, Michigan State University, East Lansing, MI.

66. Elfrink, J., Bachmann, D., & Robideaux, D. (1997). Internet marketing: Evidence of a

viable medium. The CPA Journal, 1(1), 17-21.

67. Evans, J. R., & Laskin, R. L. (1994). The relationship marketing process: A

conceptualization and application. Industrial Marketing Management, 23(5), 439-

452.

68. Febvre, L. and Martin, H. J. (1976) [1958] The Coming of the Book. (translated by) D.

Gerard, NLB, London.

69. Feltwell, J. (1991) The Story of Silk, St. Martin's Press, NY.

-322-

70. Fomell, C., & Larcker, D. (1981). Structural equation models with unobservable

variables and measurement error. Journal of Marketing Research) 18(1 ), 39-50.

71. Forrester Research. (2001). Business-to-business forecast. Retrieved I September

2001 from http://www.forre:ster.com.

72. Fournier, S. "Delivering on the Relationship in CRM." MSI!Duke Customer

Relationship Management Conference. Durham, NC. Jan. 2002.

73. Fournier, S., & Yao, J. L. (1997). Reviving brand loyalty: A reconceptualization

within the framework of consumer-brand relationships. International Journal of

Research in Marketing, 14(5), 451-472.

74. Fournier, S., Dobscha, S. & Mick, D.G. (1998). Preventing the premature death of

relationship marketing. Harvard Business Review 76(1 ). 42.

75. Frazier, G. L., Spekman, R. E., and O'Neal, C.R. (1988) Just-In-Time Exchange

Relationships in Industrial Markets, Journal of Marketing, Vol. 52, October, pp. 52-

67.

76. Fullerton, R. A. (1988) Modem Western Marketing as an Historical Phenomenon:

Theory and Illustration, in Nevett, T. and Fullerton, R.A. (Eds.), Historical

Perspectives in Marketing: Essays in Honor of Stanley C. Hollander, pp. 71-89,

Lexington Books, Lexington, MA.

77. Gale, B.T., and R.W. Chapman. Managing Customer Value: Creating Quality and

Service ThatCustomers Can See. New York: Free Press, 1994.

78. Ganesan, S. (1994) Determinants of Long Term Orientation in Buyer-Seller

Relationships, Journal of Marketing, Vol. 58, April, pp.l-19.

-323-

79. Gartner Group. (2000). Gartner Group forecasts worldwide business-to-business e

commerce to reach $7.29 trillion in 2004. Press release. Retrieved 17 February 2000

from http:/ I gartner ll.gartnerWeb.com/ public

I static/ aboutgglpressrel/prO 12600c.html.

80. Gefen, D. (2002). Customer loyalty in e-commerce. Journal of the Association for

Information Systems, (3), 27-51.

81. Gerson, Richard. Beyond Customer Service : Keeping Customers for Life. Boston,

MA. USA: Course Technology Crisp, 1998. p 3.

82. Geyskens, I., Gielens, K., & Dekimpe, M. G. (2002). The market valuation oflntemet

channel additions. Journal of Marketing, 66(2), 102-119.

83. Ghosh, S. (1998). Making business sense of the Internet. Harvard Business Review, 2,

126-135.

84. Goldberg, B. (1988) Relationship Marketing, Direct Marketing, Vol. 51, Iss. 6,

October, pp. 103-1 05.

85. Gronroos, C. (1990) Relationship Approach to Marketing In Service Contexts: The

Marketing and Organizational Behavior Interface, Journal of Business Research, Vol.

20, Iss. 1, January, pp. 3-11.

86. Gronroos, C. (1990). Relationship approach to marketing in service contexts: The

marketing and organizational behavior interface. Journal of Business Research, 1 ( 1 ),

3-11.

87. Gronroos, C. (1994) European Perspectives On Relationship Marketing, Paper

presented at the American Marketing Association Fourteenth Faculty Consortium on

Relationship Marketing, Atlanta, Georgia, June 1994.

- 324-

88. Gronroos, C. (1994). From marketing mix to relationship marketing: Towards a

paradigm shift in marketing. Management Decision. 32(2), 4-20.

89. Guion, L.A., Goddard, H. V./., Broadwater, G., Chattaraj, S., & Sullivan-Lytle, S.

(2003). Strengthening programs to reach diverse audiences. Gainesville, FL: Florida

Cooperative Extension, University of Florida.

90. Gummesson, E. (1994). Making relationship marketing operational. International

Journal of Service Industry Management, 5(5), 5-20.

91. Gundlach, G. T., and Murphy, P. E. (1993) Ethical and Legal Foundations of

Relational Marketing Exchanges, Journal of Marketing, Vol. 57, October, pp.35-46.

92. Hakansson, H. (Ed.) (1982) International Marketing and Purchasing of Industrial

Goods: An Interaction Approach. John Wiley & Sons, Inc., Chichester, UK.

93. Hayes, R. H., Wheelright, S.C. and Clarke, K. (1988) Dynamic Manufacturing. The

Free Press, New York.

94. Heide, J. B. (1994). Intero:rganizational governance in marketing channels. Journal of

Marketing, 58(1), 71-85.

95. Heide, J. B. and John, G. (1990) Alliance in Industrial Purchasing: The Determinants

of Joint Action in Buyer-Supplier Relationships, Journal of Marketing Research, Vol.

27, February, pp. 24-36.

96. Heide, J. B. and John, G. (1992) Do Norms Matter in Marketing Relationships?,

Journal of Marketing, Vol. 56, April, pp.32-44.

97. Herzberg, F. (2003). Om: more time: How do you motivate employees? Harvard

Business Review, 81(1), 87-96.

-325-

98. Hofacker, C., & Murphy, J. (1998). World Wide Web banner advertisement copy

testing. European Journal of Marketing, 32(7/8), 703-712.

99. Hoffman, D. L., Novak, T. P. (1996). Marketing in hypermedia computer-mediated

environments: Conceptual foundations. Journal of Marketing, 60(2), 50-66.

100. Hoffman, D. L., Novak, T. P., & Chatterjee, P. (1995). Commercial scenarios for the

Web: Opportunities and challenge:s. Journal of Computer-Mediated Communication, 1 (3).

Retrieved 25 June 2004 from http://www.ascusc.org(jcmc/voll/issue3/hoffinan.html.

101. Hooda R.P, "Statistlcsfor Business and Economics",3rd Edition, Macmillan

India Ltd., 2006.

102. Houston, F. S. (1994) Marketing Exchange Relationships, Transactions, and

Their Media. Quorum Books, Westport, CT.

103. Houston, F. S., Ga5.senheimer, J.B., and Maskulka, J. (1992) Marketing

Exchange Transactions and Relationships. Quorum Books, Westport, CT.

104. Howard, J. A., and Sheth, J. N. (1969) The Theory of Buyer Behavior. John

Wiley & Sons, Inc., New York.

105. http://www.hardmanagement.co.uk/sapproach.htm

106. Hunt, S. D. ( 1983) General Theories and the Fundamental Ex planada of

Marketing, Journal of Marketing, Vol. 4 7, Fall, pp. 9-17.

107. Hunt, S.D., and Goolsby, J. (1988) The Rise and Fall of the Functional

Approach to Marketing: A Paradigm Displacement Perspective, in Nevett, T. and

Fullerton, R.A.(Eds. ), Historical Perspectives in Marketing: Essays in Honor of

Stanley C. Hollander.Le:xington Books, Lexington, Massachusetts.

-326-

108. Iacobucci, D., and J. Hibbard. "Toward an Encompassing Theory of Business

Marketing Relationships and Interpersonal Commercial Relationships: An Empirical

Generalization." Journal of Interactive Marketing 13 (1999): 13-33.

I 09. Jackson, B. B. (I 985). Build customer relationships that last. Harvard

Business Review, 63( 6), 120-128.

110. Jacoby, J., & Kyner, D.B. (1973). Brand loyalty versus repeat purchase

behavior. Journal of Marketing Research, 10(1), 1-9.

111. Jacoby, J., and R. Chestnut. Brand Loyalty: Measurement and Management.

New York: John Wiley,

112. Jarvenpaa, S. L., & Tractinsky, N. (I 999). Consumer trust in an Internet store:

A cross-cultural validation. Journal of Computer-Mediated Communication, 5 (2).

Retrieved 25 June 2004 from http://www.ascusc.org/jcmc/vol5/issue2/jarvenpaa.html.

113. Joachim, David. "CRM Tools Improve Access, Usability." B to B 11 Mar.

2002: 1.

114. Johnston, R. and Lawrence, P.R. (1988) Beyond Vertical Integration- The

Rise of the Value Added Partnership, Harvard Business Review, Vol. 88, No. 4, pp.

94-101.

115. Joseph, V. B., Cook, R. W., & Javalgi, R. G. (2001). Marketing on the Web:

How executives feel, what businesses do. Business Horizons, 44( 4), 32- 40.

116. Journal of Interactive Marketing 13 (1999): 13-33.

117. Kalwani, M. and Narayandas, N. (1995) Long-Term Manufacturer-Supplier

Relationships: Do They Pay Off for Supplier Firms?, Journal of Marketing, Vol. 59,

January, pp.l-16.

-327-

118. Kandampully, Jay(Editor). Relationship marketing in services. Bradford, ,

UK: Emerald Group Publishing Limited, 2002. p 5.

119. Kassarjian, H. H. ( 1977). Content analysis in consumer research. Journal of

Consumer Research, 4(1 ), 8-18.

120. Katz, M. (1988) Understanding Customer Relationships: Marketing CIF, Bank

Systems & Equipment, Vol. 25, Iss. 4, April, pp. 62-65.

121. Keller, K. "Building Customer-Based Brand Equity." Marketing Management

10 (2001): 14-19.

122. Kingson, E. R., Hirshom, B.A., and Commam, J.M. (1986) Ties that Bind:

The Interdependence of Generations. Seven Locks Press, Cabin John, MD.

123. Kleinaltenkamp, Michael. Relationship The01y and Business Markets.

Bradford, , UK: Emerald Group Publishing Limited, 2006. p 73.

124. Kohn, A. (1986) No Contest: The Case Against Competition. Houghton

Mifflin Company, Boston.

125. Kotler, P. (1972), A Generic Concept of Marketing, Journal of Marketing,

Vol. 36 April, pp. 46-54.

126. Kotler, P. (1990), Presentation at the Trustees Meeting of the Marketing

Science Institute in November 1990, Boston.

127. Kotler, P. ( 1994 ),. Marketing Management: Analysis, Planning,

Implementation, and Control. Prentice-Hall, Inc., Englewood Cliffs, New Jersey.

128. Level Explanations for True Variety-Seeking Behavior." Journal of

Marketing Research 33 (1996):

129. Levey, Richard. "Just for You." DIRECT 1 July 2001.

-328-

130. Li, L. M. (1981) Chinais Silk Trade: Traditional Industry in the Modern

World 1842-1937. Harvard University Press, Cambridge, Massachusetts.

131. Little, R. W. ( 1970) The Marketing Channel: Who Should Lead This Extra-

corporate Organization, Journal of Marketing, Vol. 34, January, pp. 31-38.

132. Lombard, M., & Ditton, T. (1997). At the heart of it all: The concept of

presence. Journal of Computer-Mediated Communication, 3 (2). Retrieved 25 June

2004 from http://www.ascusc.org/jcmc/vol3/issue2/lombard.html.

133. Lyons, T. F., Krachenberg, A. R. and Henke, Jr., J. W. (1990) Mixed Motive

Marriages: Whatis Next for Buyer-Supplier Relations?, Sloan Management Review,

Vol.31, Spring, pp.29-36.

134. Macintosh, G., & Lockshin, L. S. ( 1997). Retail relationships and loyalty: A

multi-level perspective. International Journal of Research in Marketing, 14(5), 487-

497.

135. Macklin, T. (1924) Efficient Marketing For Agriculture, Macmillan, New

York.

136. McCammon, B. (1965) The Emergence and Growth of Contractually

Integrated Channels in the American Economy, in Bennett, P. D. (Ed.), Economic

Growth, Competition, and World Markets. pp. 496-515, American Marketing

Association, Chicago.

13 7. McKenna, R. ( 1991) Relationship Marketing: Successful Strategies for the

Age of the Customer. Addison-Wesley Publishing Co., Reading, MA.

138. McMillan, S. J. (1998). Who pays for content? Funding in interactive media.

Journal of Computer-Mediated Communication, 4 (1). Retrieved 25 June 2004 from

http://www .ascusc.orgiicmc/vol4/issue 1 /mcmillan.html. -329-

139. Miller, A. (1949) Dea.th of a Salesman, p. 81, The Viking Press, New York.

140. Milne, G., and A. Rohm. "Consumer Privacy and Name Removal across

Direct Marketing Channels: Exploring Opt-In and Opt-Out Alternatives." Journal of

Public Policy and Marketing 19 (2000): 238-249.

141. Morgan, R. M., & Shelby, D. H. (1994). The commitment-trust theory of

relationship marketing. Journal of Marketing, 58(3), 20-38.

142. Morgan, R., and S. Hunt. "The Commitment-Trust Theory of Relationship

Marketing." Journal of Marketing 58 (1994): 20-38.

143. Muhammad, T. K. (1996). Marketing online. Black Enterprise, 1(5), 85-88.

144. Mwamula-Lubandi, E. D. (1992) Clan Theory in African Development Studies.

University

145. Nargundkar R., "Afarketing Research Text and Cases"Tata Me Graw Hill

Publishing Company Ltd., New Delhi, 2004.

146. Nevett, T., and Nevett, L. (1987) The Origins of Marketing: Evidence from

Classical and

14 7. Nevin, R. J. ( 199:5). Relationships marketing and distribution channels:

Exploring fundamental issues. Journal of Academy of Marketing Science, 23(4), 327-

334.

148. Norusis, M. J. (1993). SPSSfor Windows base system user's guide, release

6.0. Chicago: SPSS Inc ..

149. O'Neal, C. (198.9) JIT Procurement and Relationship Marketing, Industrial

Marketing Management, Vol. 18, February, pp. 55-63.

-330-

150. Oliver, R. L. "Whence Consumer Loyalty." Journal of Marketing 63 (1999):

33-44.

151. Parvatiyar, A. Sheth, J.N., and Whittington, F.B. (1992) Paradigm Shift in

Interfirm Marketing Relationships: Emerging Research Issues, (Working Paper No.

CRM 92-10l),Center for Relationship Marketing, Emory University, Atlanta.

152. Parvatiyar, A., Sheth, J.N. 2002. 'Customer Relationship Management:

emergmg

153. Patrick Marketing Group. "Key Business and Marketing Trends Survey

Analysis." June 2002.

154. Patterson, D. D., and McAnally, A. J. (1947) The Family Panel: A Technique

for Diagnosing Sales Jlls, Sales Management, Vol. 59, October, pp. 134-136.

Peterson, P. G. (1962) Conventional Wisdom and the Sixties, Journal of Marketing,

April, pp. 63-67.

155. Payne, A. (1994). Relationship marketing making the customer count.

Managing Service Quality, 4(6), 29-31.

156. Peltier, J., J. Schibrowsky, and J. Davis. "Using Attitudinal and Descriptive

Database Information to Understand Interactive Buyer-Seller Relationships." Journal

of Interactive Marketing 12.3 (1998): 32-45.

157. Peppers, Don, and Martha Rogers. The One to One Future: Building

Relationships One Customer at a

158. Peterson, A. R. (1995). Relationships marketing and the consumer. Journal of

Academy of Marketing Science, 23(4), 278-281.

- 331-

159. Peterson, A. R., Balasubramanian, S., & Bronnenberg, B. J. (1997). Exploring

the implications of the Internet for consumer marketing. Journal of Academy of

Marketing Science, 25(4), 329-346.

160. Pilzer, P.Z. "The Next Trillion" www.thenextrilllion.com

161. Porter, M. E. (2001). Strategy and the Internet. Harvard Business Review,

79(3), 63-78.

162. Press of America, New York.

163. Pryor, F. L. (1977) The Origins of the Economy. Academic Press, New York.

Room, A. (1987) History of Branding, in Murphy, J. M. (Ed.), Branding: A Key

Marketing Tool. The Macmillan Press Ltd., London.

164. Rafaeli, S., & Sudweeks, F. (997). Networked interactivity. Journal of

Computer-Mediated Communication, 2 (4). Retrieved 25 June 2004 from

http://www .ascusc.org(jcmc/vol2/issue4/rafaeli.sudweeks.html.

165. Reichheld, F. F. (2001) Lead for loyalty. Harvard Business Review, 4, 76-84.

166. Reichheld, Frederick F. The Loyalty Effect. Boston: Harvard Business School

Press, 1996.

167. Reinartz, W. J.. & Kumar, V. (2002). The mismanagement of customer

loyalty. Harvard Business Review, 80(7), 86-94.

168. Reinartz, W. J.. & Kumar, V. (2003). The impact of customer relationship

characteristics on profitable lifetime duration. Journal of Marketing, 67(1), 77-99.

169. Reinartz, Werner, and V. Kumar. "The Mismanagement of Customer

Loyalty." Harvard BusinessReview.

-332-

170. Relationships and Interpersonal Commercial Relationships: An Empirical

Generalization."

171. Robbins, S. S., & Stylianou, A. C. (2003). Global corporate Web sites: An

empirical investigation of content and design. Information and Management, 40(3),

206-212.

172. Rosenberg, L. J. and Cziepiel, J. A. ( 1984) A Marketing Approach to

Customer Retention, Journal of Consumer Marketing, Vol. 1, Spring, pp.45-51.

173. Rothermund, D. (1988) An Economic History of India. Crom Helm, New

York.

174. Rowley, J., & Dawes, J. (2000). Disloyalty: A closer look at non-loyals.

Journal of Consumer A1arketing. 17(6), 538-549.

175. Rust, Roland T., Valarie A. Zeithaml, and Katharine N. Lemon. Driving

Customer Equity: HowCustomer Lifetime Value is Reshaping Corporate Strategy.

New York: Free Press, 2000.

176. Saaty T.L and Vargas L.G, "Models, Methods, Concepts & Applications of

the Analytic Hierarchy Process", Kluwer Academic Publishers, USA, 2001.

177. SaravanaveJ P. and Sumathi S, "Marketing Research and Consumer

Behaviour", Vikas Publishing House Pvt. Ltd., 2006.

178. Savitt, R. ( 1980) Historical Research in Marketing, Journal of Marketing,

Vol. 44, Fall, pp. 52-58.

179. Schubert, P. (2003). Personalizing e-commerce applications in SMEs.

Americas Conference on Information Systems, 9, 737-750.

-333-

180. Sen, S., Padmanabhan., B., Tuzhilin, A., White, N.H., & Stein, R. (1998). The

identification and satisfaction of consumer analysis-driven information needs of

marketers on the WWW. European Journal of Marketing, 32(7 /8), 688-702.

181. Shani, D. and Chalasani, S. (1991) Exploiting Niches Using Relationship

Marketing, The Journal of Consumer Marketing, pp. 33-42.

182. Shapiro, B. P. (1988) Close Encounters of the Four Kinds: Managing

Customers in a Rapidly Changing Environment, (HBS Working Paper No. 9-589-

0 15), Harvard Business School, Boston.

183. Shapiro, B. P., and Moriarty, Jr., R. T. (1980) National Account Management,

Marketing Science Institute, Cambridge, MA.

184. Shapiro, B. P., and Posner, R. S. (1979) Making the Major Sale, Harvard

Business Review, (March-April), pp. 68-79.

185. Shapiro, B. P., and. Wyman, J. (1981) New Ways to Reach Your Customer,

Harvard Business Review, (July-August), pp. 103-110.

186. Shaw, A. ( 1912) Some Problems in Market Distribution, Quarterly Journal of

Economics,

187. Sheth, J. and Parvatiyar, A. (1994) Relationship Marketing: Theory, Methods

and Applications. Center for Relationship Marketing, Emory University, Atlanta.

188. Sheth, J. N. and Sisodia, R. (1995) Improving the Marketing Productivity, in

Encyclopedia of Marketing for the Year 2000. American Marketing Association

NTC, Chicago, (forthcoming).

189. Sheth, J. N., Gardner, D. M. and Garett, D. E. (1988) Marketing Theory:

Evolution and Evaluatlon. John Wiley & Sons, Inc, New York.

-334-

190. Sheth, N. J., & Parvatiyar, A. (1995). Relationships marketing in consumer

markets: Antecedents and consequences. Journal of Academy of Marketing Science,

23(4), 255-271.

191. Shultz, D. H. (1995). Marketing consuling services on line. Journal of

Management Consulting, 8(4), 35-42.

192. Sombart, W. (1951) The Jews and Modern Capitalism, Free Press, Glencoe,

IL.

193. Spekman, R. E. (1988) Strategic Supplier Selection: Understanding Long-

Term Buyer Relationships, Business Horizons, (July/ August), pp. 75-81.

194. Szeinbach, S. L., Barnes, J. H., & Gamer, D. D. (1997). Use of

pharmaceutical manufacturers' value-added services to build customer loyalty.

Journal of Business Research, 40(3), 229-236.

195. Tagliavini, M., Ravarini, A., & Antonelli, A. (2001). An evaluation model for

electronic commerce activities within SMEs. Information Technology and

Management, 2, 211-230.

196. Teo, H. H., Wei, K. K., & Benbasat, I. (2003). Predicting intention to adopt

interorganizationallinkages: An institutional perspective. MIS Quarterly, 27(1), 19-

49.

197. Thomas, J. S. (2001). A methodology for linking customer acquisition to

customer retention. Journal of Marketing Research, 38(2), 262-268.

198. Uncles, M., & Laurent, G. (1997). Editorial. International Journal of

Research in Marketing, I4(5), 399-404.

-335-

199. Van Trijp, Hans C. M.~ Hoyer Wayne D., and Inman Jeffrey J. "Why Switch?

Product Category-Level Explanations for True Variety-Seeking Behavior." Journal of

Marketing Research 33 (1996): 281-292.

200. Vence, Deborah L. "Marketers Expect to See Federal Law on Online Privacy

Soon." Marketing News 24 June 2002: 4.

201. Venkatraman, N. (2000). Five steps to a dot-com strategy: How to find your

footing on the Web. Sloan Management Review, 41(3), 38-67.Vol. 26, (August), pp.

706-765.

202. Viswanathan P .K, "Business Statistics- An Applied Orientation", Pearson

Education (Singapore) Pte Ltd., Delhi, 2005.

203. Walle, A. (1987) Import Wine at a Budget Price: Marketing Strategy and the

Punic Wars, in Nevett, T., and Hollander, S.C. (Eds.), Marketing-Three Eras:

Proceedings of the Third Conference on Marketing History. pp. 13-22, Michigan

State University, East Lansing, Michigan.

204. Webster, F. E., Jr. (1992) The Changing Role of Marketing in the

Corporation, Journal of Marketing, Vol. 56, No.4 (October), pp. 1-17.

205. Weld, L. D. H. (1917) Marketing Functions and Mercantile Organization,

American Economic Review, Vol. 7, (June), pp. 306-318.

206. Williamson, 0. E. (1975) Markets and Hierarchies: Analysis and Antitrust

Implications. The Free Pres.s, New York.

207. Williamson, 0. E. (1985) The Economic Institutions of Capitalism. The Free

Press, New York.

208. Wilson, T. D. (1995). An integrated model ofbuyer-seller. Journal of

Academy of Marketing Science, 23(4), 335-345.

-336-

209. Womer, S. (1944) Some Applications of the Continuous Consumer Panel,

Journal of Marketing, Vol. 9, (October), pp.l32-136.

210. Yuan, Y., Caulkins, J.P., & Roehrig, S. (1998). The relationship between

advertising and content provision on the Internet. European Journal of Marketing,

32(718), 677-687.

211. Zeithaml V.A, Bitner, Gremler Pandit A, "Services Marketing-Integrating

Customer Focus Across the Firm"- Fourth Edition, Tata Me Graw Hill Publishing

Company Ltd., New Delhi, 2008,pp 33-100.

212. Zikrnund W.G, "Business Research Methods", 7th Edition, Thomson Asia

Pte Ltd., Singapore , 2004

-337-

Related Documents