Review of Cloud Asia 2011: A few interesting tidbits from the conference Issue 1 www.alanquayle.com/blog © 2011 Alan Quayle Business and Service Development

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Review of Cloud Asia 2011: A few interesting tidbits from the conference

Issue 1

www.alanquayle.com/blog

© 2011 Alan Quayle Business and Service Development

Asia Pac (ex Japan) anticipating 40% CAGR thru’ to 2014 – its high growth region

Most cloud services today do not have end to end SLAs, yet customers are adopting, and failures are generally DC (Data Center) related (e.g. software patch failure, power failure, etc.) If operator provides a VPN with an

SLA between the customers’ sites and the DC, why is an end to end SLA better than two separate SLAs (transport and DC)? Is it just convenience? How much will a customer pay for such ‘convenience.’

SMB (Small Medium Business) SaaS Store is currently a focus of much attention, but compare most operators’ stores to those of the web service providers, most operators web sites even do a poor job of selling basic communication services. Is an

operator really placed to manage the integration issues of customer data across multiple services from different providers. Hosted Communication Services as rapidly expanding, its just another way of delivering what customers already know, but is a

cloud aggregator even within the core competence of most operators?

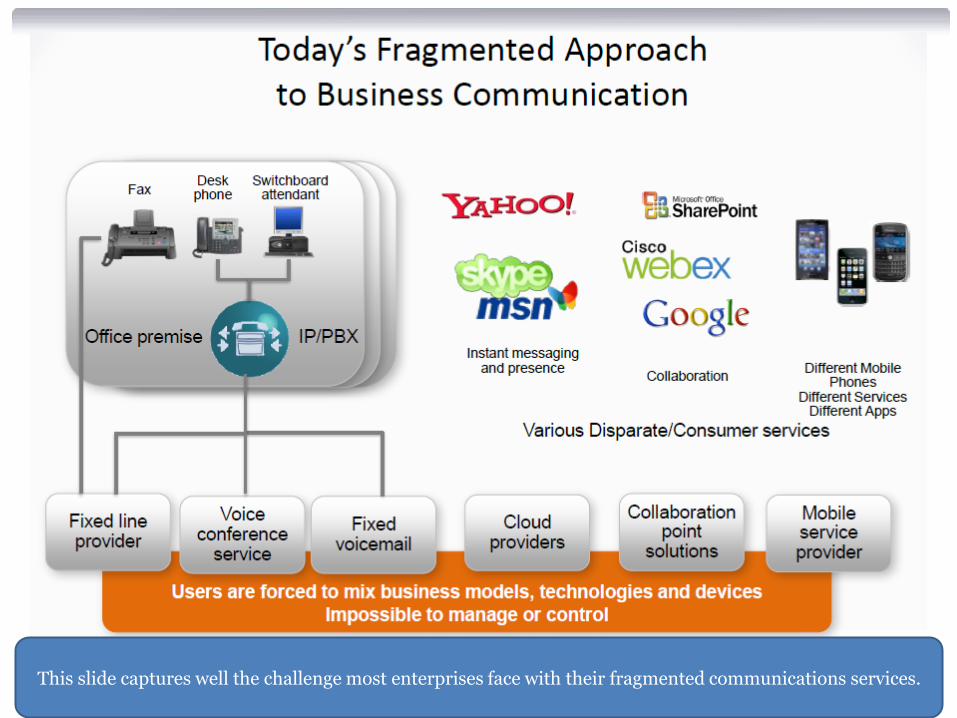

This slide captures well the challenge most enterprises face with their fragmented communications services.

Cisco Hosted Unified Communications Service (HUCS) is starting to gain momentum, its advantage over other approaches is simply costs from the scale of running a multi-tenant, multi-operator cloud-based

service in a large data center. In this model the operator is really more of a reseller, will this become true for most operators and their cloud services?

Example of one of the many slides where the word Revolution was used with Cloud. Given the loose definition of cloud used by many service providers, I’ve been running my business in the cloud for over a decade (email, storage, website, collaboration,

communications). So is cloud really just a technology (automation software) that enables cheaper on-demand hosted services? As adoption ramps up given the fast access most businesses have to the internet, such data center scale (compare to a factory)

enables additional cost savings?

No matter what the hype, cost remains the primary driver: sweating the existing data center asset, or taking advantage of the 5-7 times lower cost of operations of a large public data center. However, the other 2 steps:

reliability given the many recent cloud failures and agility (term used for why an enterprise should implement SOA and business transformation projects) are proving harder for most enterprises to swallow.

There are lots of national industry initiatives across the region – interesting to see if these have much impact given the fact that scale drives cloud economics.

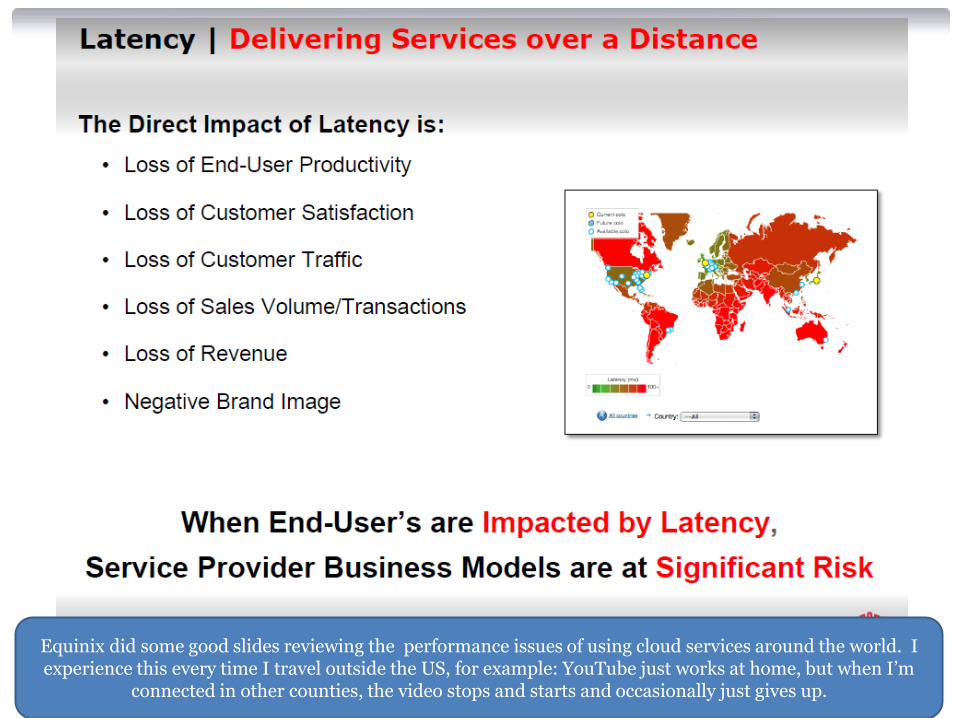

Equinix did some good slides reviewing the performance issues of using cloud services around the world. I experience this every time I travel outside the US, for example: YouTube just works at home, but when I’m

connected in other counties, the video stops and starts and occasionally just gives up.

Good slide on the distances different cloud services can be provided over.

An architecture many operators will be familiar with. Given the importance of global scale, will only the Global Carriers like Verizon, AT&T, Orange, and BT be competitive in the cloud

business?

Equinix view of a cloud exchange – more infrastructure focused than service focused.

Given an operator is a service provider, its challenge is Neutrality. NTTdata’s Biz Integral is an example of an operator building a community, but I caution against using Japan as a case study that can apply to other

markets. Also NTTdata is the IT arm of NTT group, which most operators lack (i.e. a dedicated IT division, like T-Systems for Deutsche Telekom.)

This slide came from Dialog in Sri Lanka, and sets out quite nicely how Cloud can be positioned as ISP 5.0, which backs up the position that Cloud is a technology for even cheaper hosting. But also shows how operators do remain one of the natural cloud service providers given their business history. The gap remains in IT competence to bridge the service to the enterprise. This could be the defining metric, in that most operators win on service that have a relatively low IT competence requirement, e.g.

communications and collaboration.

Another great slide from Dialog in Sri Lanka, which sets out the journey many operators must take in being competitive in Cloud services. Interestingly with many IT companies are targeting this space as well, and in

many cases have worked through this maturity model over the passed couple of decades. Operators are going to need to learn fast, else acquire the necessary competence, like Verizon did in buying Terremark.

This slide from IBM highlights several important aspect of being in the cloud business – for example Industry Solutions. Without a specific focus on a vertical, e.g. banking, and creating specific solutions and

selling though people versed in the business and technical issues of that vertical, its hard to win sales (mid-market, through large to MNCs.) Shows IBM is in competition with the operators’ cloud aspirations.

Public clouds do not interoperate, that’s on purpose, as their business model is about lock-in

Similarly, private clouds do not interoperate as their suppliers have built businesses on not playing nice together.

Vblock is the core offer of VCE (Cisco and EMC) – generally sold into an existing data center (so it lacks scale). Many enterprises were complaining about the cost of Vblock compared to its claimed savings. Also EMC’s automation software appears to have preference in the Vblock sales, which has resulted in the poor

sales of Cisco’s DC automation software, and hence its pull back from VCE.

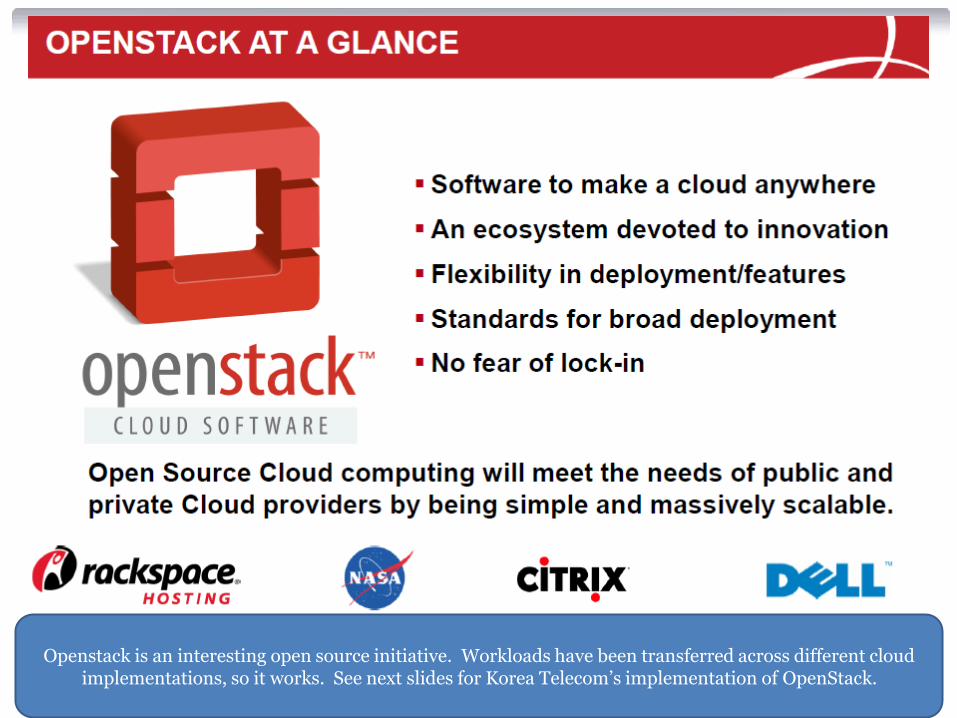

Openstack is an interesting open source initiative. Workloads have been transferred across different cloud implementations, so it works. See next slides for Korea Telecom’s implementation of OpenStack.

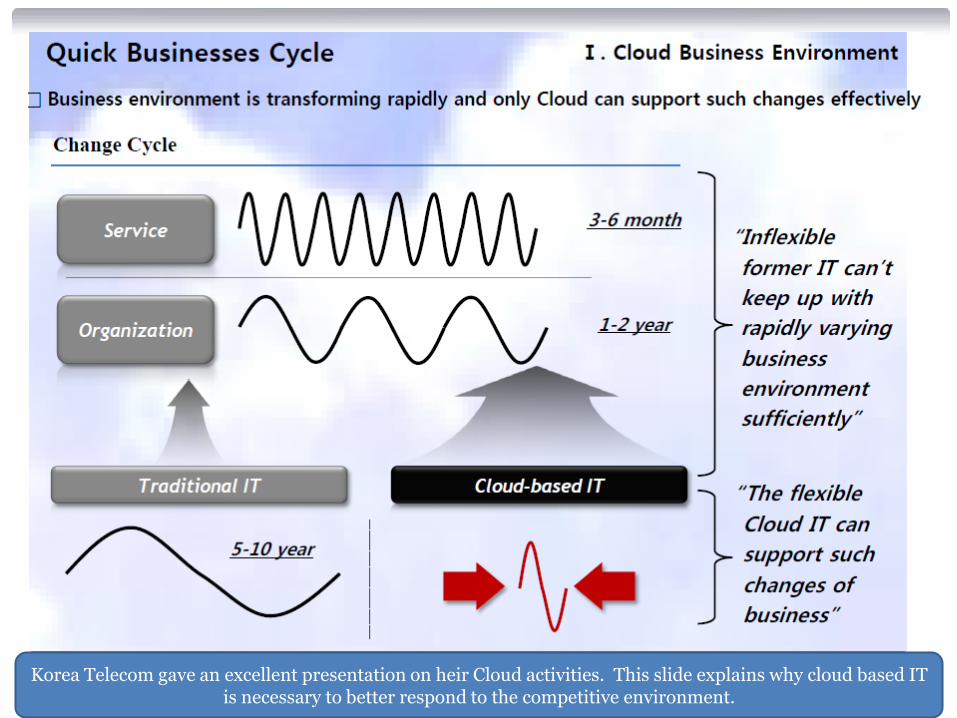

Korea Telecom gave an excellent presentation on heir Cloud activities. This slide explains why cloud based IT is necessary to better respond to the competitive environment.

Nice review of some of the recent Cloud developments, highlighting the web service provider, and IT Solution provider competition and their focus on scale – which drives cloud economics.

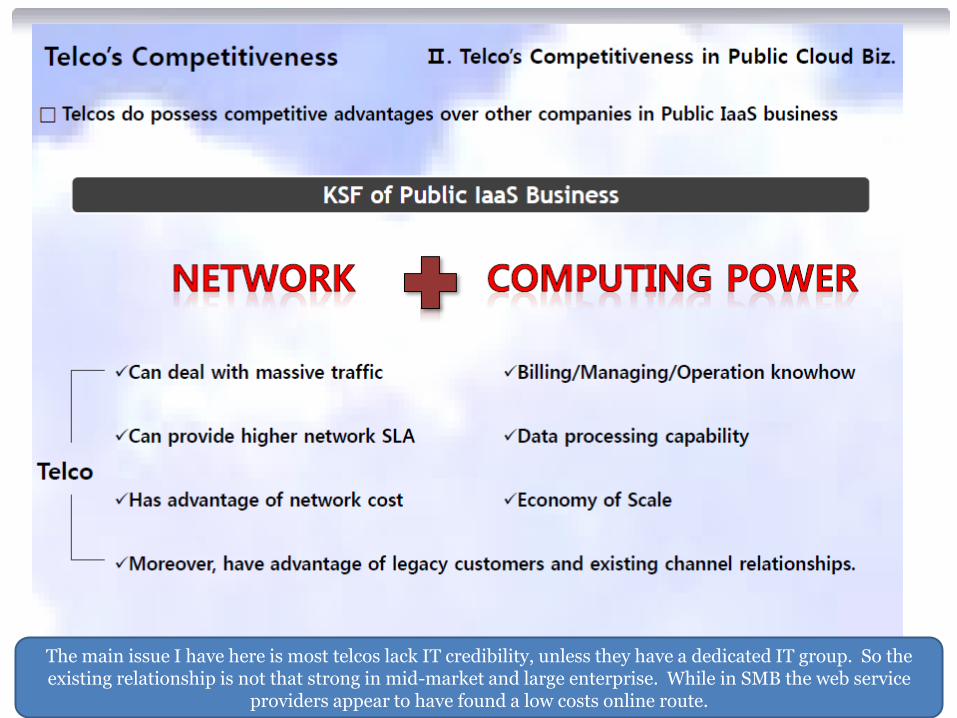

The main issue I have here is most telcos lack IT credibility, unless they have a dedicated IT group. So the existing relationship is not that strong in mid-market and large enterprise. While in SMB the web service

providers appear to have found a low costs online route.

KT have take a very different route to most telcos – they’re not partnering with a competitor to build out their infrastructure, rather they are using open source (see next slide) and using their computing needs to drive

scale in their data centers (eating their own dog food.)

Similar to a Google-like approach in using commodity off the shelf components, though Google has built its own software, e.g. BigTable and MapReduce. KT is using an open source approach to leverage the

community effort behind the software. Then KT focuses upon scale in its national market.

70% of the price of AWS, which is already very cheap, certainly attracts people’s attention and is testament to their approach in building their own data center.

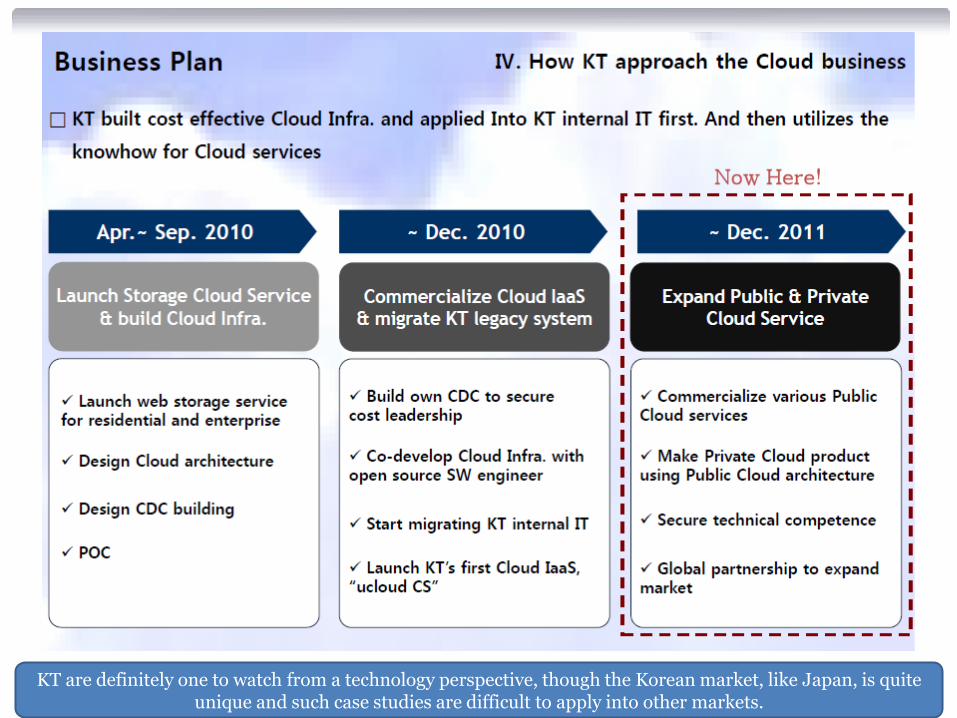

KT are definitely one to watch from a technology perspective, though the Korean market, like Japan, is quite unique and such case studies are difficult to apply into other markets.

KT have built an solid portfolio of services and an interesting roadmap with new services coming on line almost monthly – but how to sell into the enterprises? Perhaps local SI partnerships?

Solid evidence that using open source does not degrade performance.

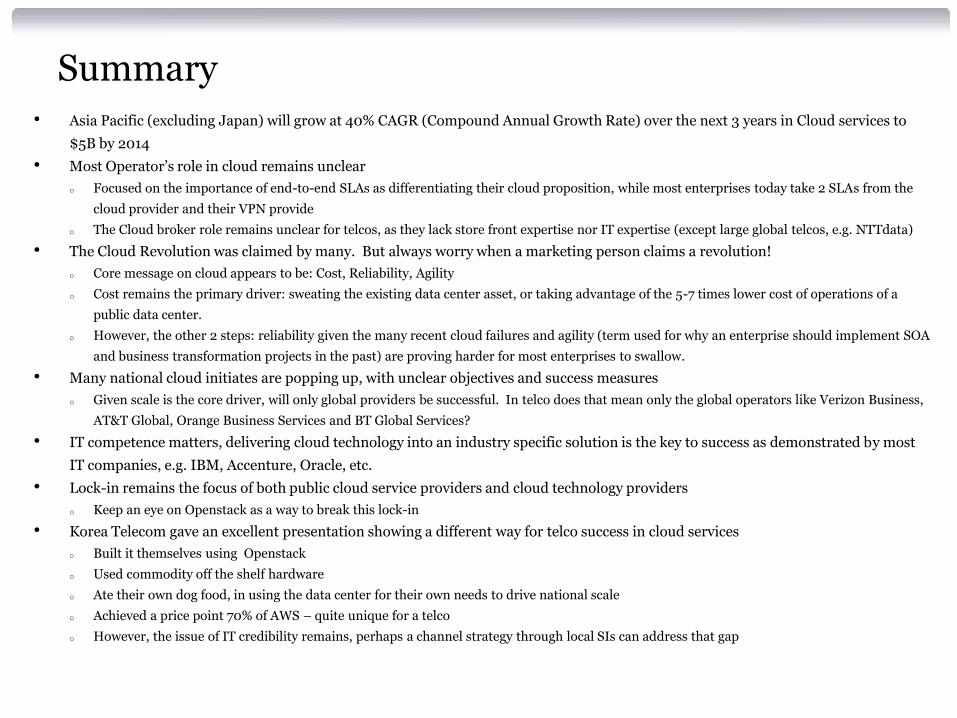

Summary • Asia Pacific (excluding Japan) will grow at 40% CAGR (Compound Annual Growth Rate) over the next 3 years in Cloud services to

$5B by 2014

• Most Operator’s role in cloud remains unclear

o Focused on the importance of end-to-end SLAs as differentiating their cloud proposition, while most enterprises today take 2 SLAs from the

cloud provider and their VPN provide

o The Cloud broker role remains unclear for telcos, as they lack store front expertise nor IT expertise (except large global telcos, e.g. NTTdata)

• The Cloud Revolution was claimed by many. But always worry when a marketing person claims a revolution!

o Core message on cloud appears to be: Cost, Reliability, Agility

o Cost remains the primary driver: sweating the existing data center asset, or taking advantage of the 5-7 times lower cost of operations of a

public data center.

o However, the other 2 steps: reliability given the many recent cloud failures and agility (term used for why an enterprise should implement SOA

and business transformation projects in the past) are proving harder for most enterprises to swallow.

• Many national cloud initiates are popping up, with unclear objectives and success measures

o Given scale is the core driver, will only global providers be successful. In telco does that mean only the global operators like Verizon Business,

AT&T Global, Orange Business Services and BT Global Services?

• IT competence matters, delivering cloud technology into an industry specific solution is the key to success as demonstrated by most

IT companies, e.g. IBM, Accenture, Oracle, etc.

• Lock-in remains the focus of both public cloud service providers and cloud technology providers

o Keep an eye on Openstack as a way to break this lock-in

• Korea Telecom gave an excellent presentation showing a different way for telco success in cloud services

o Built it themselves using Openstack

o Used commodity off the shelf hardware

o Ate their own dog food, in using the data center for their own needs to drive national scale

o Achieved a price point 70% of AWS – quite unique for a telco

o However, the issue of IT credibility remains, perhaps a channel strategy through local SIs can address that gap

Related Documents