International Financial Reporting Standards The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation. © IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org Classification of assets Joint World Bank and IFRS Foundation ‘train the trainers’ workshop hosted by the ECCB, 30 April to 4 May 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter, not necessarily those of the IASB or IFRS Foundation.

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Classification of assetsJoint World Bank and IFRS Foundation ‘train

the trainers’ workshop hosted by the ECCB,

30 April to 4 May 2012

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter,

not necessarily those of the IASB or IFRS Foundation

Concepts—classification of asset

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

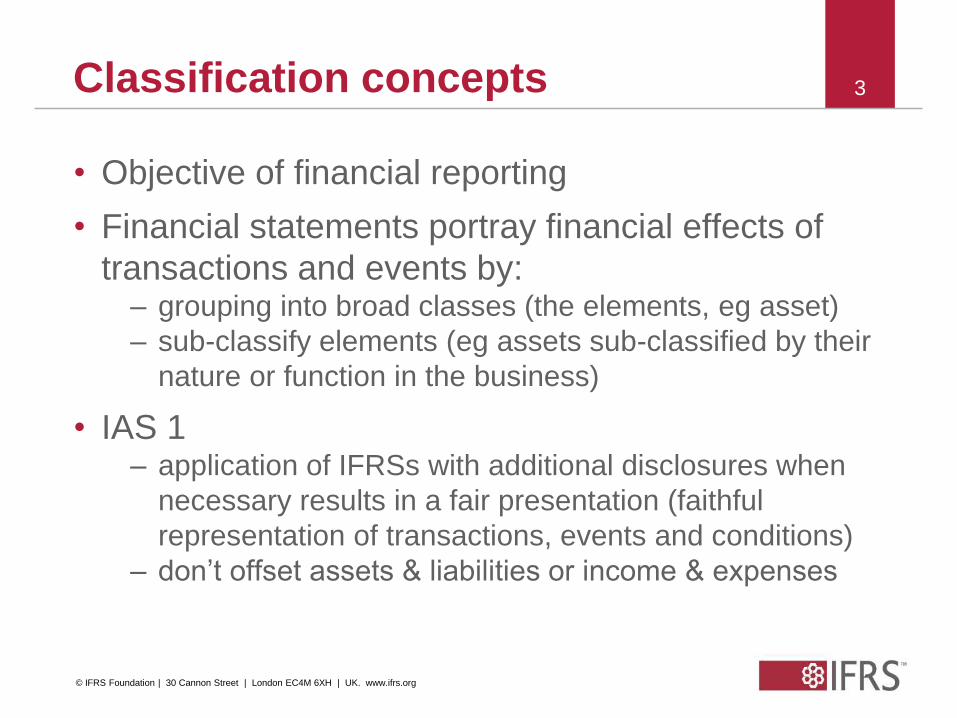

3Classification concepts

• Objective of financial reporting

• Financial statements portray financial effects of

transactions and events by:– grouping into broad classes (the elements, eg asset)

– sub-classify elements (eg assets sub-classified by their

nature or function in the business)

• IAS 1– application of IFRSs with additional disclosures when

necessary results in a fair presentation (faithful

representation of transactions, events and conditions)

– don’t offset assets & liabilities or income & expenses

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

4

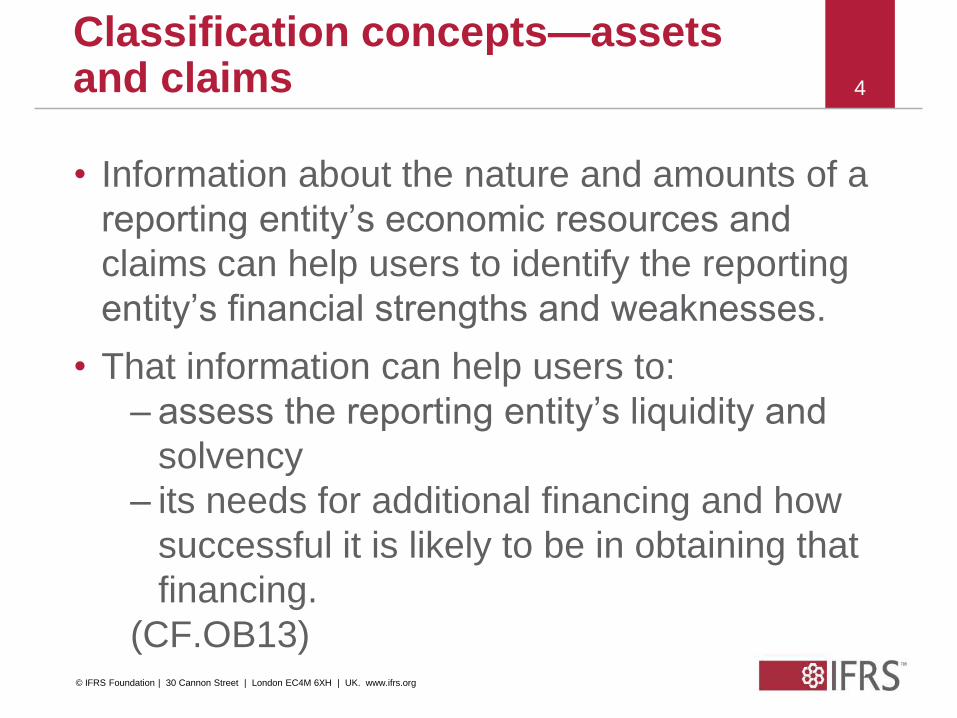

Classification concepts—assets and claims

• Information about the nature and amounts of a

reporting entity’s economic resources and

claims can help users to identify the reporting

entity’s financial strengths and weaknesses.

• That information can help users to:

– assess the reporting entity’s liquidity and

solvency

– its needs for additional financing and how

successful it is likely to be in obtaining that

financing.

(CF.OB13)© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

© 2010 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

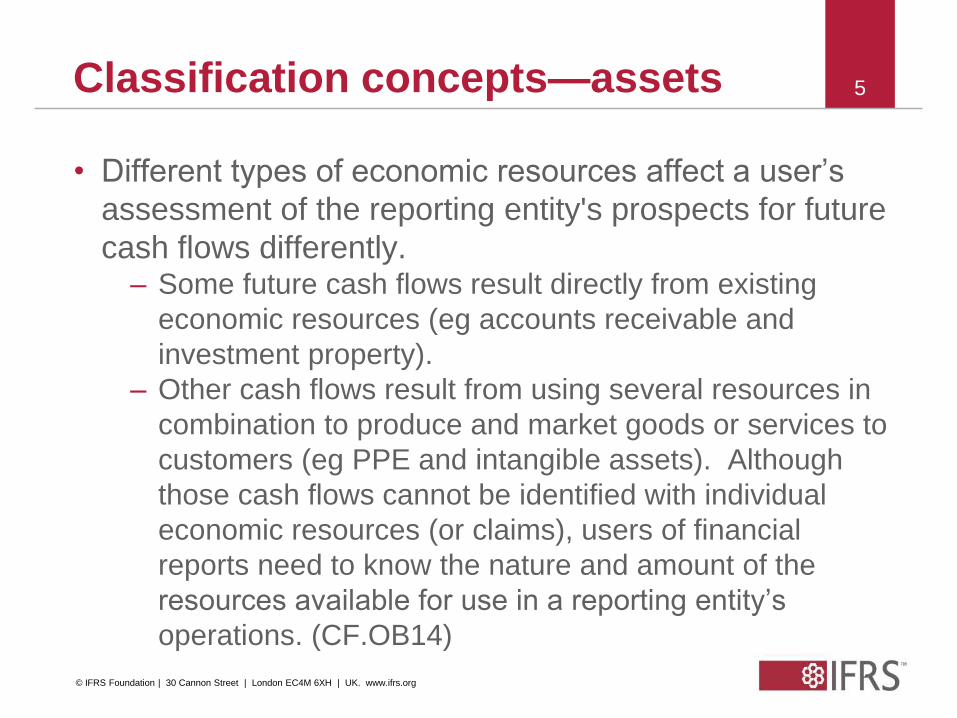

5Classification concepts—assets

• Different types of economic resources affect a user’s

assessment of the reporting entity's prospects for future

cash flows differently. – Some future cash flows result directly from existing

economic resources (eg accounts receivable and

investment property).

– Other cash flows result from using several resources in

combination to produce and market goods or services to

customers (eg PPE and intangible assets). Although

those cash flows cannot be identified with individual

economic resources (or claims), users of financial

reports need to know the nature and amount of the

resources available for use in a reporting entity’s

operations. (CF.OB14)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

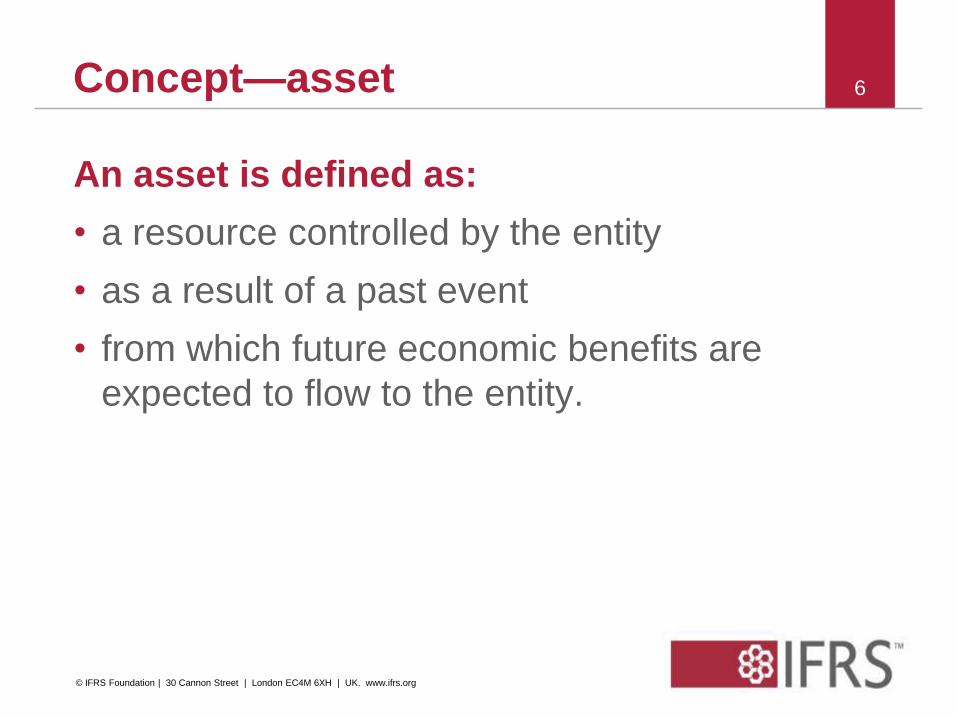

Concept—asset

An asset is defined as:

• a resource controlled by the entity

• as a result of a past event

• from which future economic benefits are

expected to flow to the entity.

6

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Asset recognition concepts

An asset is recognised when:

• it is probable that any future economic benefit

associated with the item will flow to the entity;

and

• the item has a cost or value that can be

measured with reliability.

7

For some items that satisfy the definition of an asset,

significant judgement is required to evaluate whether

such items satisfy the recognition criteria. Individual

IFRSs provide principles and application guidance.

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

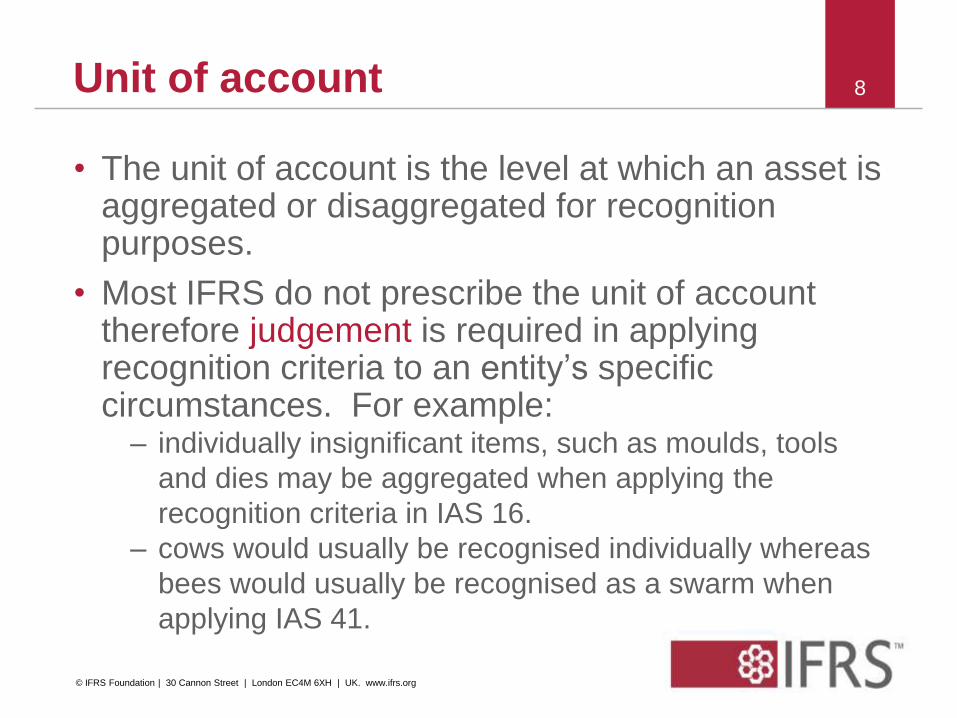

Unit of account

• The unit of account is the level at which an asset is aggregated or disaggregated for recognition purposes.

• Most IFRS do not prescribe the unit of account therefore judgement is required in applying recognition criteria to an entity’s specific circumstances. For example:

– individually insignificant items, such as moulds, tools

and dies may be aggregated when applying the

recognition criteria in IAS 16.

– cows would usually be recognised individually whereas

bees would usually be recognised as a swarm when

applying IAS 41.

8

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

International Financial Reporting Standards

The views expressed in this presentation are those of the

presenter,

not necessarily those of the IASB or IFRS Foundation

Classifying assets

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

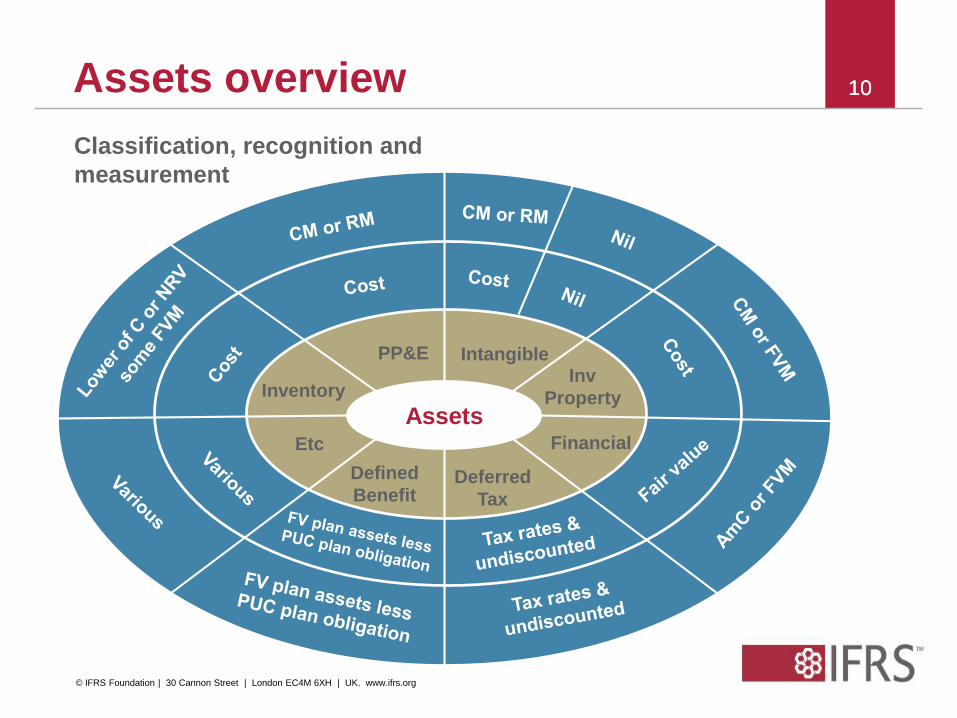

10Assets overview 10

Assets

Intangible

Financial

Inv

Property

PP&E

Inventory

Etc

Defined

BenefitDeferred

Tax

Classification, recognition and

measurement

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Classification of assets

• Different assets exhibit different characteristics (nature)

and can be held for a variety of uses (use) in order to

generate future economic benefits

• Nature and use determine the classification of assets

• IFRSs defines a number of assets

• For some assets significant judgement is required to

determine their classification

11

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

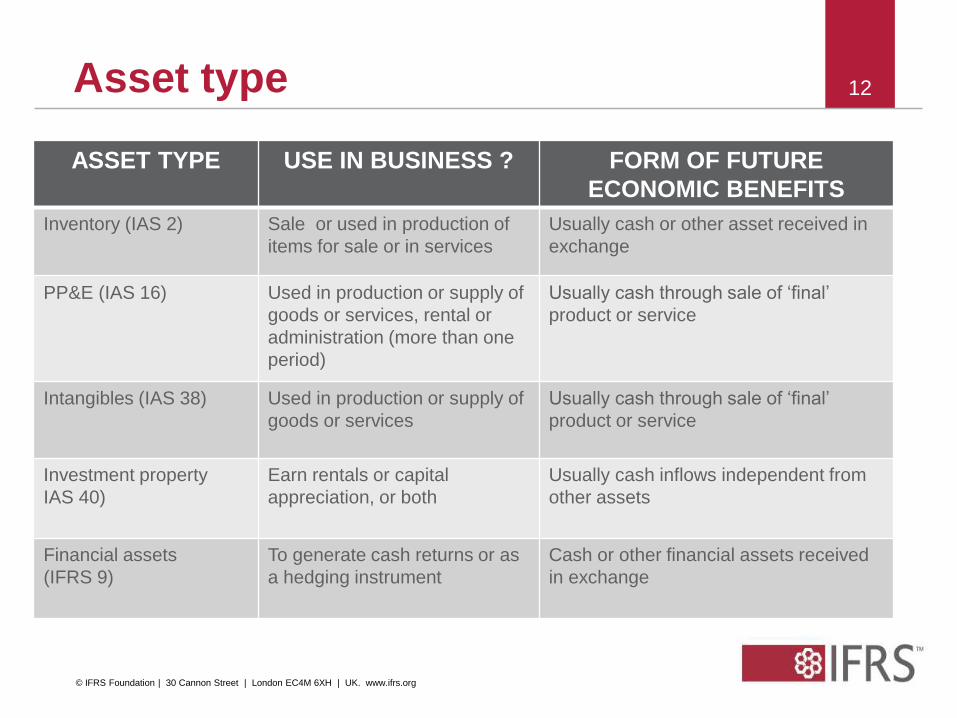

12

ASSET TYPE USE IN BUSINESS ? FORM OF FUTURE

ECONOMIC BENEFITS

Inventory (IAS 2) Sale or used in production of

items for sale or in services

Usually cash or other asset received in

exchange

PP&E (IAS 16) Used in production or supply of

goods or services, rental or

administration (more than one

period)

Usually cash through sale of ‘final’

product or service

Intangibles (IAS 38) Used in production or supply of

goods or services

Usually cash through sale of ‘final’

product or service

Investment property

IAS 40)

Earn rentals or capital

appreciation, or both

Usually cash inflows independent from

other assets

Financial assets

(IFRS 9)

To generate cash returns or as

a hedging instrument

Cash or other financial assets received

in exchange

Asset type

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

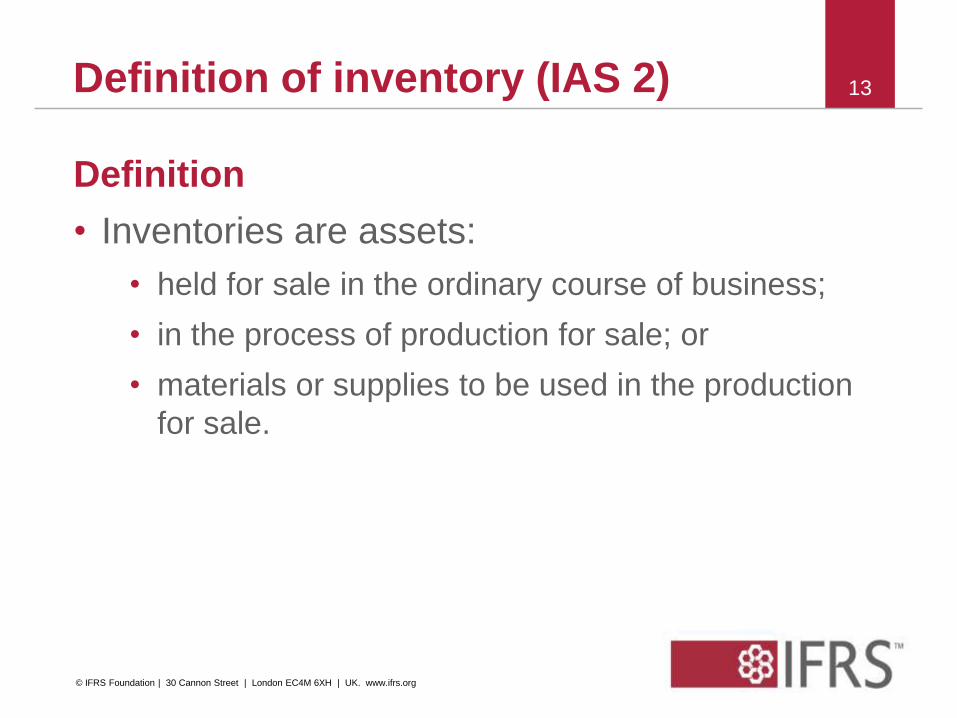

Definition

• Inventories are assets:

• held for sale in the ordinary course of business;

• in the process of production for sale; or

• materials or supplies to be used in the production

for sale.

13Definition of inventory (IAS 2)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

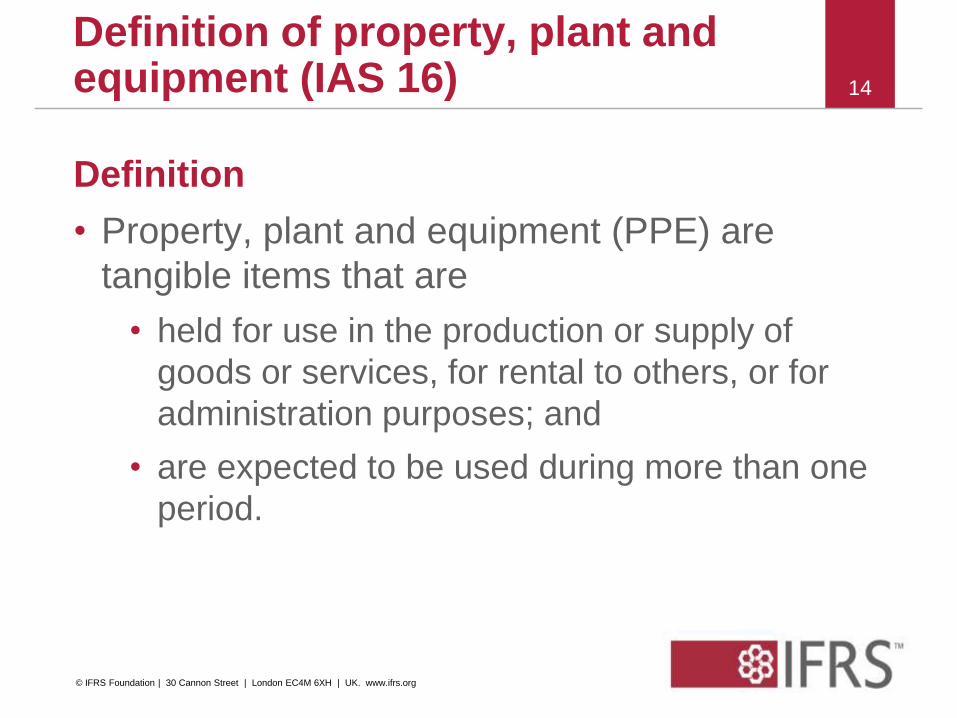

Definition

• Property, plant and equipment (PPE) are

tangible items that are

• held for use in the production or supply of

goods or services, for rental to others, or for

administration purposes; and

• are expected to be used during more than one

period.

14

Definition of property, plant and equipment (IAS 16)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Intangible assets

• The use within the business of intangible assets

is similar to that of property, plant and

equipment.

• An intangible asset is an identifiable non-

monetary asset without physical substance.

Such an asset is identifiable when it is

separable, or when it arises from contractual or

other legal rights.

15

Definition of intangible assets (IAS 38)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• It is sometimes difficult to assess whether an internally generated intangible asset qualifies for recognition because of problems in:

a. identifying whether and when there is an identifiable asset that will generate expected future economic benefits; and

b. determining the cost of the asset reliably. In some cases, the cost of generating an intangible asset internally cannot be distinguished from the cost of maintaining or enhancing the entity's internally generated goodwill or of running day-to-day operations.

• Therefore, special requirements in addition to the general requirements for recognition of an internally generated intangible asset apply.

16

Recognition of internally generatedintangible assets (IAS 38)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Expenditure on particular internally generated

intangible assets must be recognised as an

expense when incurred (eg research

activities—the original and planned

investigation undertaken with the prospect of

gaining new scientific or technical knowledge

and understanding.

17

Recognition of research costs(IAS 38)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

An intangible asset arising from the development phase of an internal project must be recognised if, and only if, an entity can demonstrate all of the following:

a. the technical feasibility of completing the intangible asset so that it will be available for use or sale.

b. its intention to complete the intangible asset and use or sell it.

c. its ability to use or sell the intangible asset.

d. how the intangible asset will generate probable future economic benefits. Among other things, the entity can demonstrate the existence of a market for the output of the intangible asset or the intangible asset itself or, if it is to be used internally, the usefulness of the intangible asset.

e. the availability of adequate technical, financial and other resources to complete the development and to use or sell the intangible asset.

f. its ability to measure reliably the expenditure attributable to the intangible asset during its development.

18

Recognition of development cost(IAS 38)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Definition

• Investment property is land or a building

(including part of a building) or both, held to earn

rentals or for capital appreciation or both.

• It is neither owner-occupied (see IAS 16 Property,

Plant and Equipment) nor held for sale in the

ordinary course of business (see IAS 2

Inventories).

19

Definition of investment property (IAS 40)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Sometimes it is difficult to identify investment

property. In such cases an entity develops

criteria so that it can exercise that judgement

consistently

• eg, owner of a hotel transfers some

responsibilities to third parties under a

management contract (PPE or investment

property?)

20Judgements and estimates (IAS 40)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Introduction

• IFRS 9 prescribes the classification and

measurement of financial assets and completes

the first phase of the project to replace IAS 39

Financial Instruments: Recognition and

Measurement.

21Financial instruments (IFRS 9)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

2011 October | Sao Paulo IFRS Conference

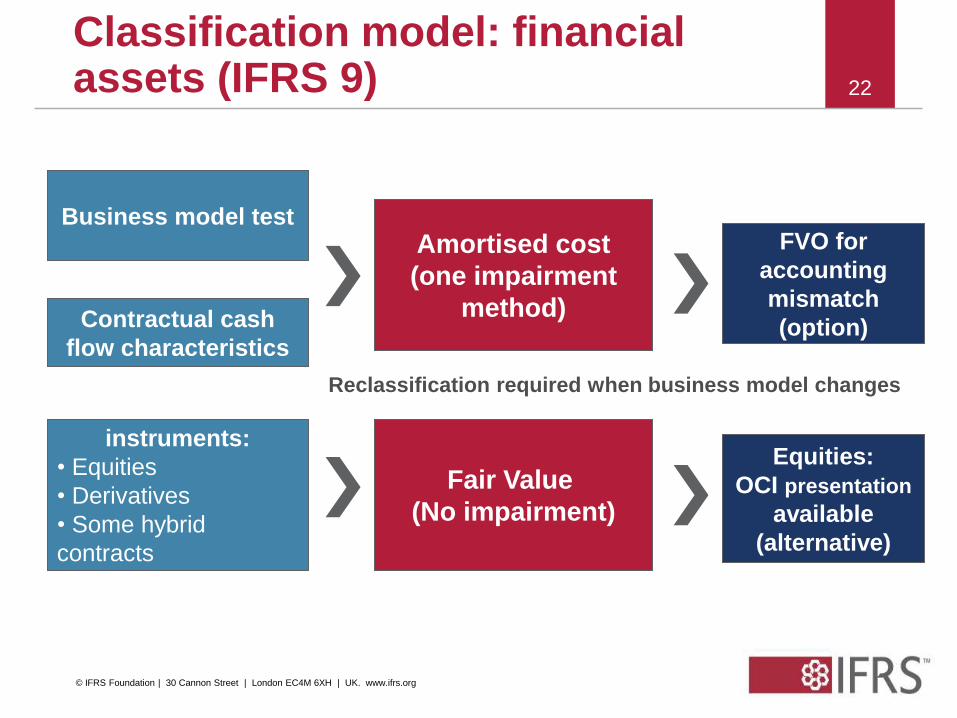

22

Fair Value

(No impairment)

Amortised cost

(one impairment

method)Contractual cash

flow characteristics

Business model testFVO for

accounting

mismatch

(option)

All other

instruments:

• Equities

• Derivatives

• Some hybrid

contracts

• …

Equities:

OCI presentation

available

(alternative)

Reclassification required when business model changes

Classification model: financial assets (IFRS 9)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

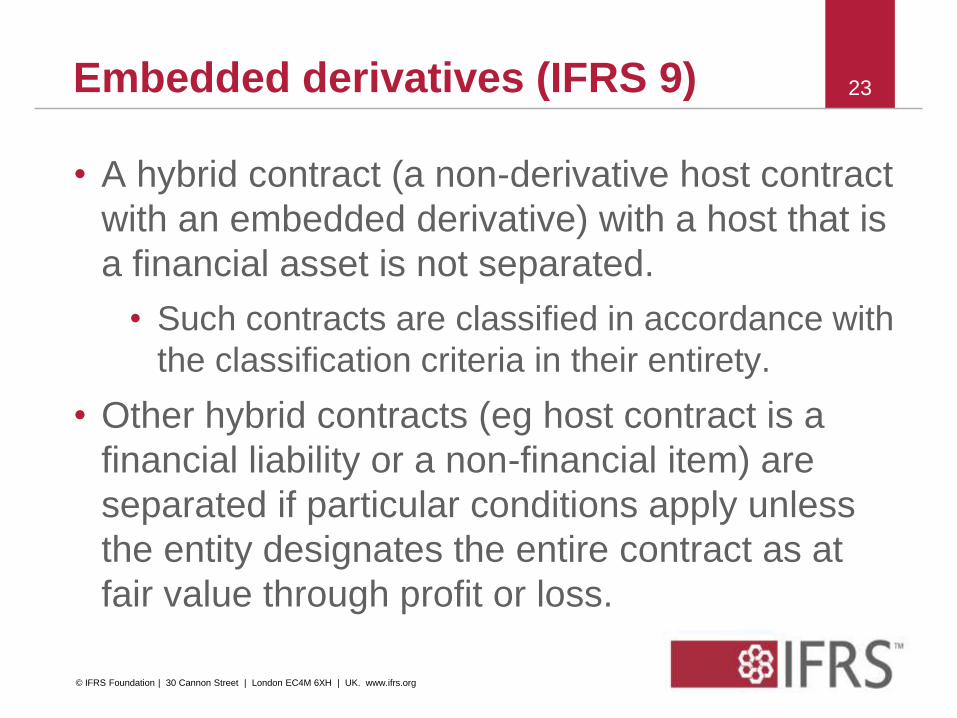

• A hybrid contract (a non-derivative host contract

with an embedded derivative) with a host that is

a financial asset is not separated.

• Such contracts are classified in accordance with

the classification criteria in their entirety.

• Other hybrid contracts (eg host contract is a

financial liability or a non-financial item) are

separated if particular conditions apply unless

the entity designates the entire contract as at

fair value through profit or loss.

23Embedded derivatives (IFRS 9)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

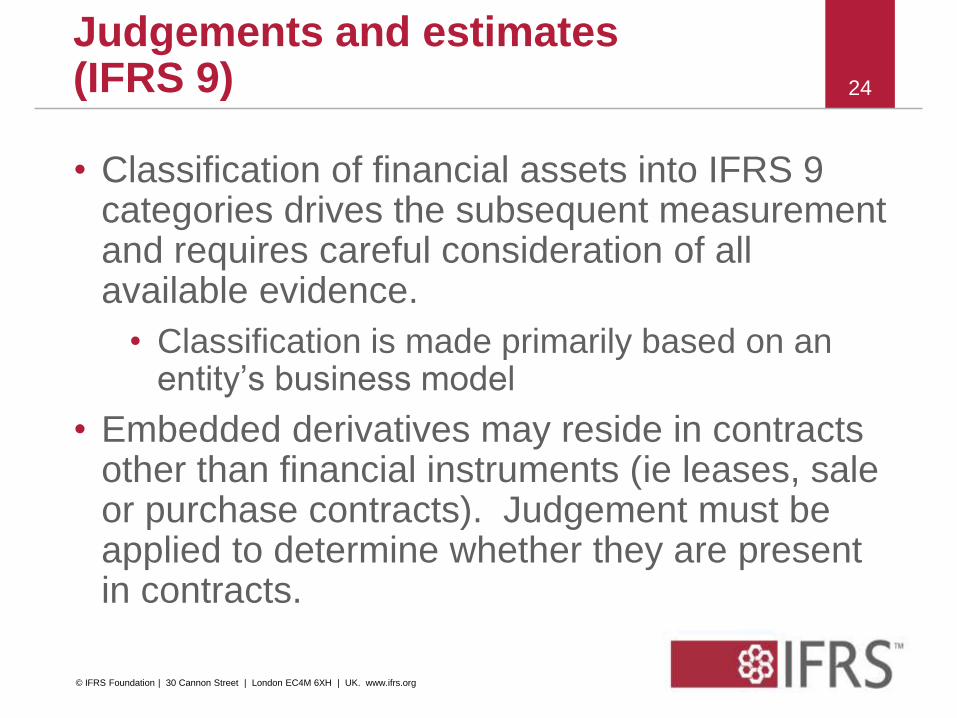

• Classification of financial assets into IFRS 9 categories drives the subsequent measurement and requires careful consideration of all available evidence.

• Classification is made primarily based on an entity’s business model

• Embedded derivatives may reside in contracts other than financial instruments (ie leases, sale or purchase contracts). Judgement must be applied to determine whether they are present in contracts.

24

Judgements and estimates (IFRS 9)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Determining whether the designation at initial recognition at fair value through profit or loss is appropriate.

25

Judgements and estimates (IFRS 9) continued

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• A non-current asset is classified as ‘held for sale’ if its carrying amount will be recovered principally through a sale transaction, rather than through continuing use (paragraph 6).

• To be classified as a non-current asset held for sale:

• The asset must be available for immediate sale in its present condition (subject only to terms that are usual and customary for sales of such assets).

• The sale must be highly probable (appropriate management commitment, actively seeking a buyer, reasonable price, 12 month limit).

26

Non-current Assets Held for Sale (IFRS 5)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

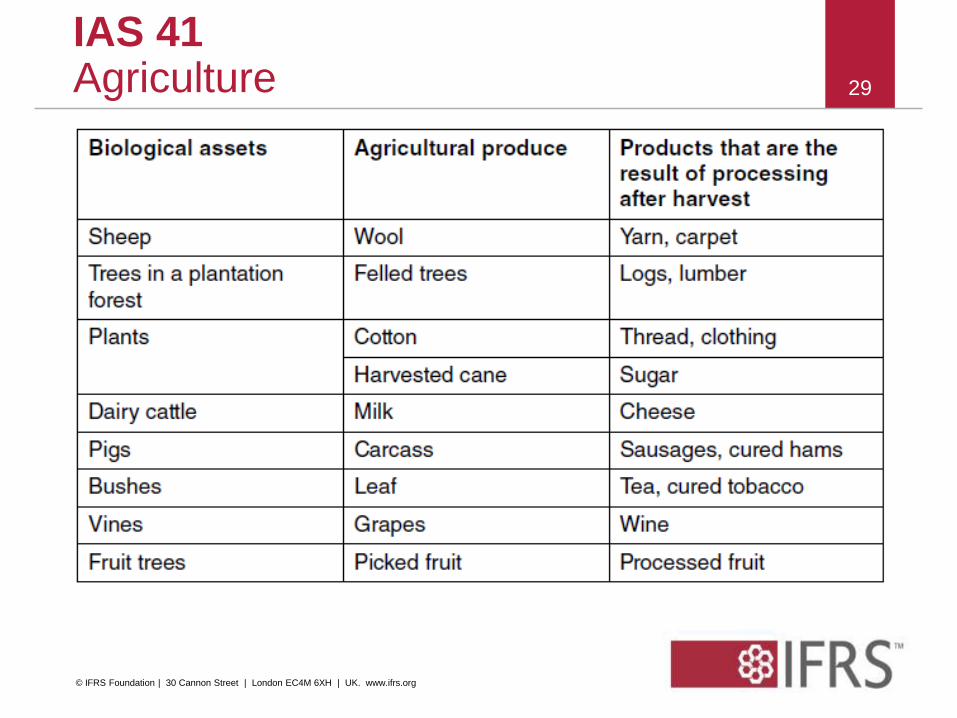

• IAS 41 specifies the accounting for:

• biological assets (living plant or animal) in agricultural activity—whose biological transformation (growth, degeneration, production and procreation) and harvest is managed by an entity for sale or for conversion into agricultural produce or into additional biological assets; and

• agricultural produce up to the point of harvest.

• It does not address the processing of agricultural produce after harvest (eg processing grapes into wine, or wool into yarn).

27Introduction (IAS 41)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• Biological assets that are attached to land

(eg trees in a plantation forest) are classified

separately from the land

• the trees are biological assets in agricultural

activity (IAS 41)

• if owner-occupied, the land is property

accounted for in accordance with IAS 16

28Classification (IAS 41)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

29

IAS 41Agriculture

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

• It can be difficult to determine whether

particular biological assets are engaged in

agricultural activity and therefore in the

scope of IAS 41—eg the animals of some

zoos.

30

Judgements and estimates (IAS 41)

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Assets—classification examples

• Ex 1: A trades in property (ie it buys property

to sell it at a profit near-term)

• Ex 2: B trades in transferable taxi licences

• Ex 3: C produces wine from grapes harvested

from its vineyards in a 3-year production cycle

• Ex 4: D holds lubricants that are consumed

by its machine in producing goods

31

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Assets—classification examples continued

• Ex 5: E maintains its plant using: – a bespoke long-life cleaning machine; & – a set of low-value common tools acquired

from a local hardware store

• Ex 6: F operate a hotel from a building it owns– it rents out hotel rooms for short-stays– guest services included in the room rate =

breakfast and television– services charged for separately = other

meals, room bar, gymnasium facilities & guided tours

32

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Assets—classification examples continued

• Ex 7: G buys a building to earn rentals under an operating lease from its subsidiary. The sub sells its products from the building

• Ex 8: H owns– a herd of cattle—breeding stock of its

agricultural activities – a tractor used to transport feed to the herd

33

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Assets—classification examples continued

• Ex 9: I owns digital films and audio recordings

which it licenses to its customers

• Ex 10: In accounting for the acquisition of the

net assets and operations of a competitor J

recognised future economic benefits arising

from assets that are not individually identified

as an asset (goodwill)

34

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Examples of classification judgements

– when unclear what purpose of acquiring

property is (inventories, IP or PPE?)

– when property owner provide ancillary

services to the occupants of a property (IP or

PPE?)

– mixed use property (IP or PPE?)

– when is undue cost or effort necessary to

measure the fair value of an IP on an

ongoing basis (IP or PPE?)

35

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

© 2012 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

36Questions or comments?

Expressions of individual

views by members of the

IASB and its staff are

encouraged. The views

expressed in this

presentation are those of the

presenter.

Official positions of the IASB

on accounting matters are

determined only after

extensive due process and

deliberation.

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

© 2011 IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK | www.ifrs.org

37

The requirements are set out in International Financial Reporting Standards (IFRSs), as issued by the IASB at 1 January 2012 with an effective date after 1 January 2012 but not the IFRSs they will replace.

The IFRS Foundation, the authors, the presenters and the publishers do not accept responsibility for loss caused to any person who acts or refrains from acting in reliance on the material in this PowerPoint presentation, whether such loss is caused by negligence or otherwise.

37

© IFRS Foundation | 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Related Documents