Towards A More Liquid and Transparent Gas Market October 2013

Clare Savage, EnergyAustralia:Towards A More Liquid and Transparent Gas Market

Aug 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Towards A More Liquid and Transparent Gas Market October 2013

2

Towards a More Liquid and Transparent Gas Market

Evolution of our gas market

The rise of LNG and impact on demand

The changing face of supply

The challenge in New South Wales

Gas market design for the future

Towards A More Liquid and Transparent Gas Market

3

EnergyAustralia

Towards A More Liquid and Transparent Gas Market

One of Australia’s largest gas and electricity utilities

The largest privately held supplier of generation output to the National Electricity Market (“NEM”)

Australia’s third largest energy retailer with market share of 22% across Eastern Australia by customer accounts

Owns the largest underground gas storage facility in Australia with long-term gas supply contracts

Pipeline of development opportunities in retail, generation and coal seam gas

Experienced management team

Owned by CLP Holdings Limited — listed on the HK Stock Exchange

Rebranded as EnergyAustralia in Q3 2012

Gas assets

Legend

Generation assets

Tallawarra Power Station (420MW) Cathedral

Rocks (66/33MW)

Yallourn Power Station & Coal Mine (1480MW)

Ecogen Hedge (up to 966MW)

Gas Storage Facility

(22PJ Storage; 500TJ/d

Processing)

Brisbane

Melbourne

Adelaide

SA Retail 0.2M

accounts

Queensland Retail

0.1M accounts

VIC Retail 1.2M accounts

NSW /ACT Retail

1.4M accounts

20% interest in Narrabri

Gas Project (500PJ)

Mt Piper and Wallerawang power stations (2,400MW)

Hallett Power

Station (203MW) Sydney

Waterloo (111MW)

4

History of the east coast gas market

1960’s 1970’s 1980’s 1990’s 2000’s 2010’s

-

200

400

600

800

1961-62 1971-72 1981-82 1991-92 2001-02

PJ/a

East Coast Gas Demand

Conventional discoveries brought to market in Brisbane, Adelaide and Melbourne

Cooper basin connects to NSW

Surat basin connects to Gladstone

Surat Basin connects to Mt Isa Market Reform • IC Review • NCP • Open Access • Vic Market

Otway basin connects to VIC / SA NSW and Tasmania connect to Longford Further Reforms • Parer Review • AEMA/NGL Conventional Reserves in decline

Start of STTM’s Rapid growth in CSM production Commitment to East coast LNG Wholesale & Capacity Trading hubs ?

The beginning of a gas industry - Torrens Island and Newport gas power stations built along with open cycle turbines largely in Victoria and South Australia.

Electricity Demand Growth – Tallawarra and OCGTs in Qld, Vic and SA. Emerging CSM industry - Swanbank E, Townsville, Darling Downs and OCGT’s in SW QLD.

BREE 2012, 2012 Australian Energy Statistics, BREE, Canberra, July

Government support to grow industry, e.g. replace declining SA coal

5

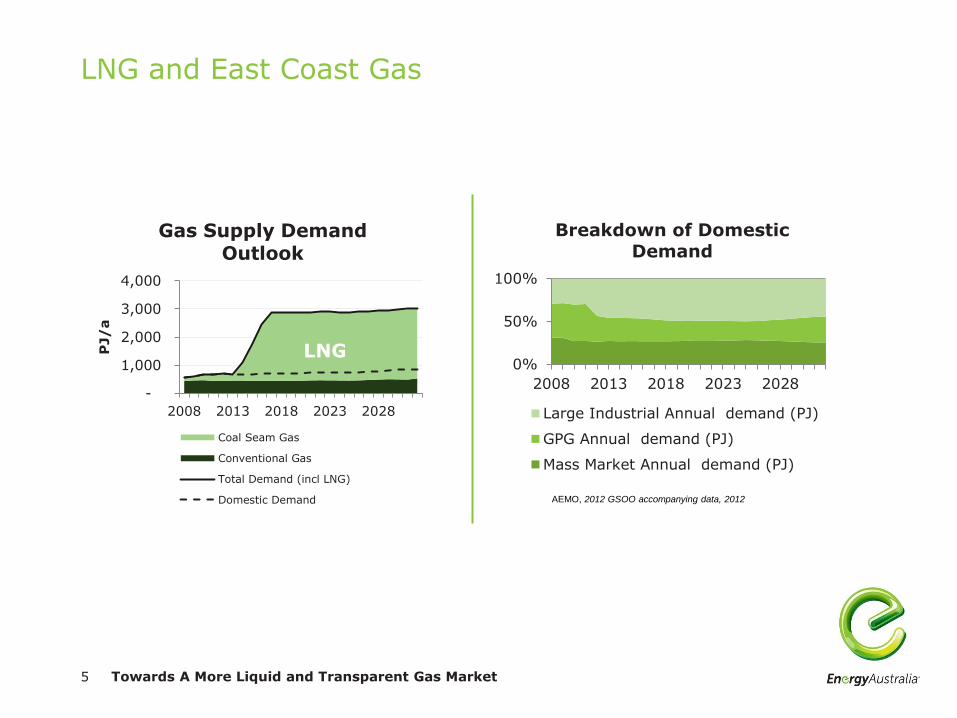

-

1,000

2,000

3,000

4,000

2008 2013 2018 2023 2028

PJ/

a

Gas Supply Demand Outlook

Coal Seam Gas

Conventional Gas

Total Demand (incl LNG)

Domestic Demand

0%

50%

100%

2008 2013 2018 2023 2028

Breakdown of Domestic Demand

Large Industrial Annual demand (PJ)

GPG Annual demand (PJ)

Mass Market Annual demand (PJ)

AEMO, 2012 GSOO accompanying data, 2012

LNG and East Coast Gas

Towards A More Liquid and Transparent Gas Market

LNG

6

Impact of gas price uncertainty

A lack of forward price transparency reduces the willingness of market participants to contract with one another.

Towards A More Liquid and Transparent Gas Market

7

Sources of NSW Gas

Towards A More Liquid and Transparent Gas Market

Gilmore

MurrayBridge

Portland

Warrnambool

Longford

Ballera

Katnook

Wodonga

Geelong

Rockhampton

Gladstone

Wallumbilla

Mt Isa

Townsville

Moomba

Whyalla

PortPirie

Echuca

BendigoHorsham

Ballarat

Newcastle

Wollongong

WaggaWagga

Griff ith

AliceSprings

Barcaldine

McArthurRiver

Young

Mildura

Gold Coast

Orbost

Tennant Creek

Iona

Bell BayPort Latta

Horsley Park

VICTORIA

SOUTHAUSTRALIA

QUEENSLANDNORTHERN TERRITORY

NEW SOUTH WALES

WESTERNAUSTRALIA

TASMANIA

SYDNEY

CANBERRA

MELBOURNE

HOBART

BRISBANE

ADELAIDE

DARWIN

LauncestonBurnie

Mooranbah

8

New sources of supply can emerge - diversifying supply

243.7PJ

94.6PJ

101.9PJ 8.1PJ

244.6PJ

5.7PJ

0.4PJ

202.0PJ

232.0PJ

8.0PJ 0.0PJ

50.0PJ

0.0PJ

0.0PJ

2011/2012Production1999/2000ProductionDemandCentres

Bowen/Surat

Cooper/Eromanga

Otway Basin

Gippsland Basin

Bass Basin

Gunnedah Basin

Sydney Basin South Australia

Victoria

Brisbane

Mt Isa

Gladstone

New South Wales

Legend

Gas Flows

4,123.6PJ

2,485.4PJ

846.5PJ

258.4PJ

40,094.3PJ

731.9PJ

1,426.3PJ

2PReserves

DemandCentres

Bowen/Surat

Cooper/Eromanga

Otway Basin Gippsland Basin

Bass Basin

Gunnedah Basin

Sydney Basin

South Australia

Victoria

Brisbane

Mt Isa

Gladstone

New South Wales

Legend

Gas Flows

Production Reserves

NSW Reserve development crucial to meeting long term demand

Towards A More Liquid and Transparent Gas Market

9

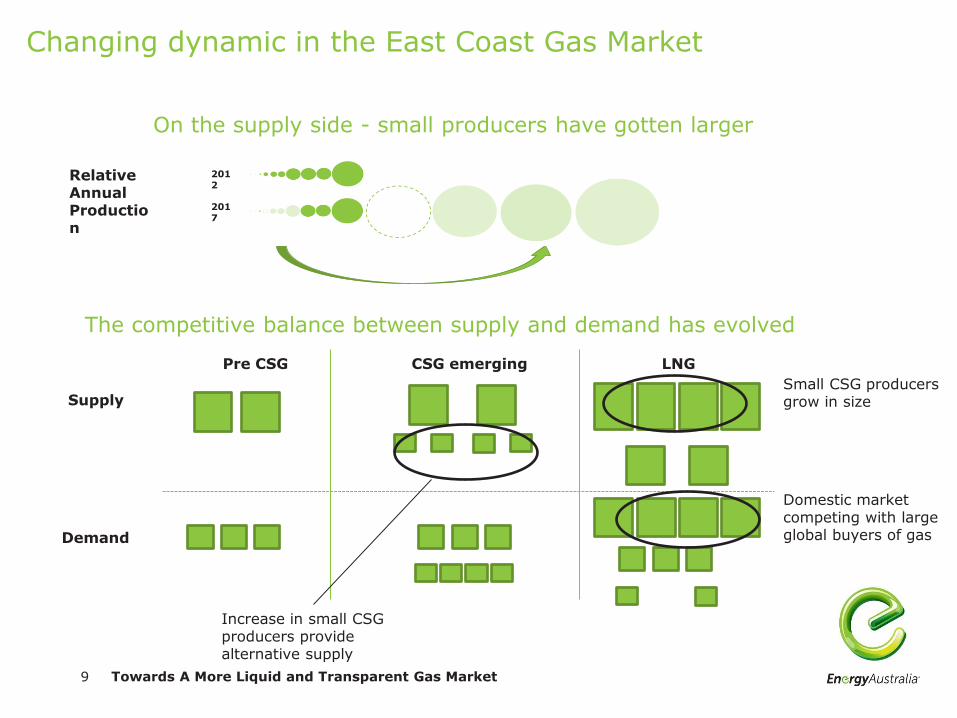

Changing dynamic in the East Coast Gas Market

Towards A More Liquid and Transparent Gas Market

2012

2017

On the supply side - small producers have gotten larger

Relative Annual Production

Pre CSG CSG emerging LNG

The competitive balance between supply and demand has evolved

Supply

Demand

Increase in small CSG producers provide alternative supply

Small CSG producers grow in size

Domestic market competing with large global buyers of gas

10

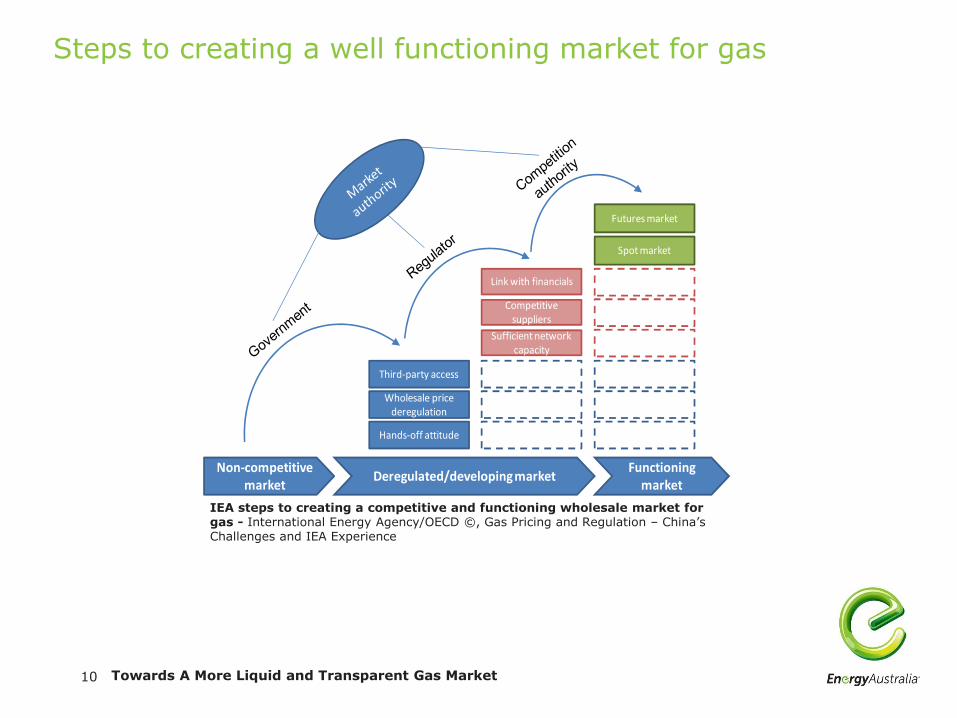

Steps to creating a well functioning market for gas

Towards A More Liquid and Transparent Gas Market

IEA steps to creating a competitive and functioning wholesale market for gas - International Energy Agency/OECD ©, Gas Pricing and Regulation – China’s Challenges and IEA Experience

11

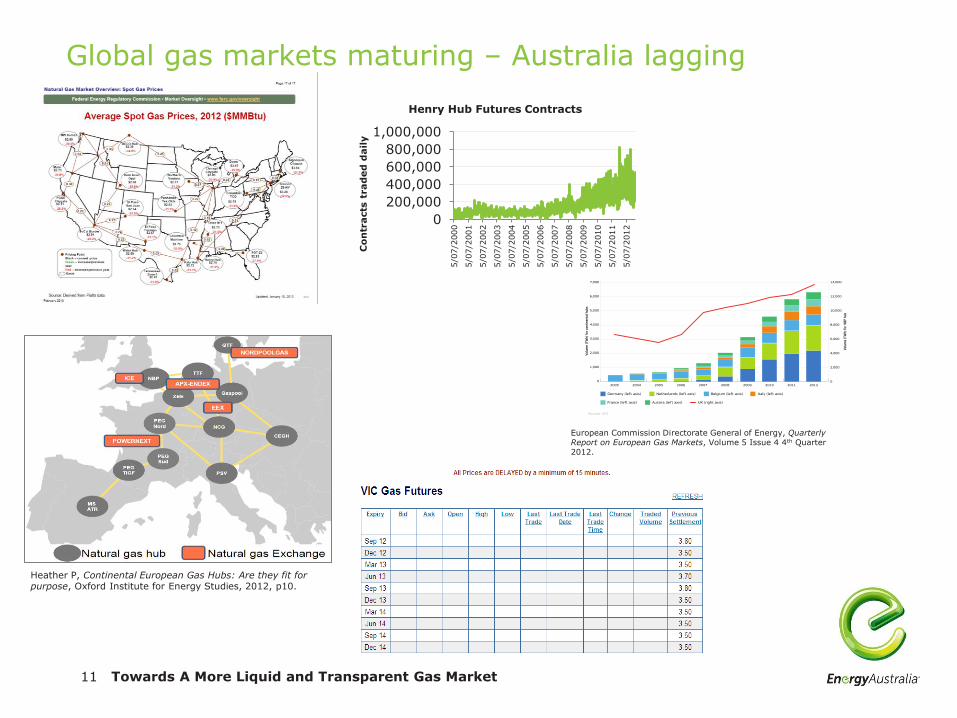

Global gas markets maturing – Australia lagging

Towards A More Liquid and Transparent Gas Market

0

200,000

400,000

600,000

800,000

1,000,000

5/0

7/2

000

5/0

7/2

001

5/0

7/2

002

5/0

7/2

003

5/0

7/2

004

5/0

7/2

005

5/0

7/2

006

5/0

7/2

007

5/0

7/2

008

5/0

7/2

009

5/0

7/2

010

5/0

7/2

011

5/0

7/2

012

Co

ntr

acts

trad

ed

dail

y

Henry Hub Futures Contracts

4

3. Continental European national gas hubs: status and stages of

development

The North West European (NWE) gas markets have seen significant evolutionary change

over the past 10 years both in terms of construct and growth; indeed, in 2002 only two NWE

countries had an operational gas hub, Britain’s NBP (since 1996) and Belgium’s Zeebrugge

(since 2000), and in Germany HubCo9 had just been established. There then followed, one by

one, gas hubs in each of the other NWE countries: the Dutch TTF and the Italian PSV in

2003; the French PEGs in 2004; the Austrian CEGH in 2005; the German EGT10

in 2006; the

German Gaspool and NCG in 2009. Therefore, the current ‘hub landscape’ was complete by

2009 and has shown signs of accelerated development in the last couple of years, especially

since early 2010, through 2011 and the Winter of 2011-12.

Figure 1: European gas hubs and gas exchanges

The situation across all these markets now looks quite different, not only in comparison to a

few years ago, but also to that which presented itself only a year ago in the Spring of 2011.

This is especially true of the Dutch and German markets but there have also been some

9 This gas hub was the forerunner of BEB (2004), which later became Gaspool in 2009.

10 The E.on Gas Transport network’s market was incorporated into the new NCG hub in 2009.

Heather P, Continental European Gas Hubs: Are they fit for purpose, Oxford Institute for Energy Studies, 2012, p10.

European Commission Directorate General of Energy, Quarterly Report on European Gas Markets, Volume 5 Issue 4 4th Quarter 2012.

12

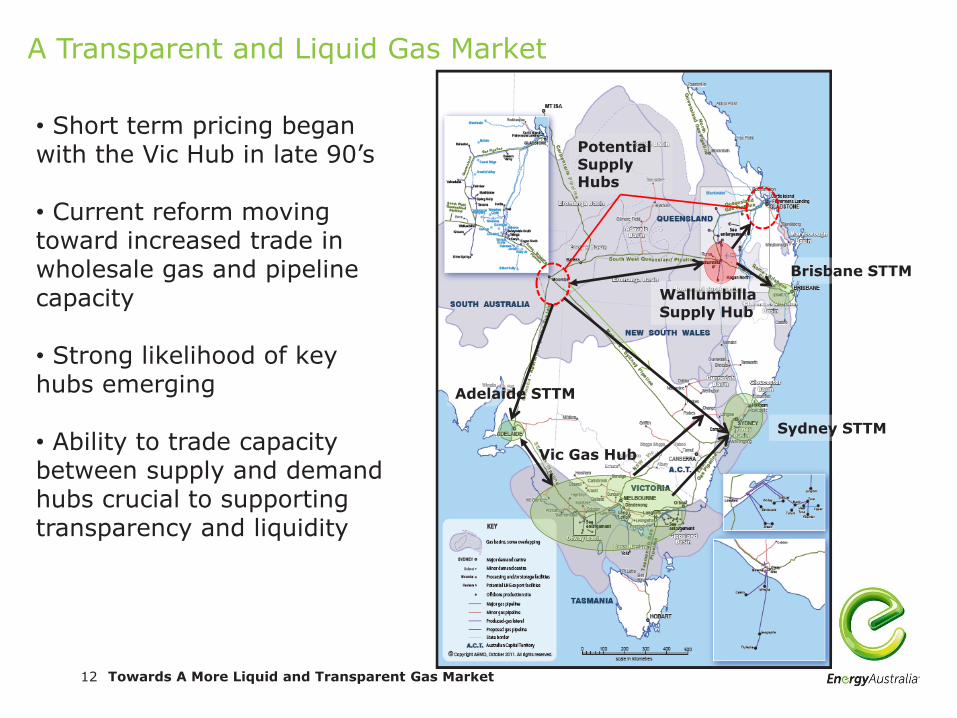

A Transparent and Liquid Gas Market

Towards A More Liquid and Transparent Gas Market

Brisbane STTM

Sydney STTM

Adelaide STTM

Vic Gas Hub

Wallumbilla Supply Hub

Potential Supply Hubs

• Short term pricing began with the Vic Hub in late 90’s • Current reform moving toward increased trade in wholesale gas and pipeline capacity • Strong likelihood of key hubs emerging • Ability to trade capacity between supply and demand hubs crucial to supporting transparency and liquidity

13

A Transparent and Liquid Gas Market

•Enabling guaranteed access to gas by those who value it the most and supporting production by those who can deliver it in the cheapest way.

One

•A more liquid and transparent market for capacity, which encourages more efficient pipeline use and more transparent signals about market demand for investment.

Two

•The role of long term gas and pipeline contracts is diminished. They can still play a role, but are referenced against open and transparent markets.

Three

Towards A More Liquid and Transparent Gas Market

Related Documents