City of North Lauderdale, Florida Comprehensive Annual Financial Report Fiscal Year Ended September 30, 2013 PREPARED BY THE FINANCE DEPARTMENT STEVEN CHAPMAN II, FINANCE DIRECTOR SENDIE RYMER, CONTROLLER

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

City of North Lauderdale, Florida

Comprehensive Annual Financial Report Fiscal Year Ended September 30, 2013

PREPARED BY

THE FINANCE DEPARTMENT STEVEN CHAPMAN II, FINANCE DIRECTOR

SENDIE RYMER, CONTROLLER

City of North Lauderdale, Florida Comprehensive Annual Financial Report Fiscal Year Ended September 30, 2013

Table of Contents

INTRODUCTORY SECTION PAGELetter of transmittal i – iiiCertificate of achievement ivOrganizational chart vList of principal officials vi

FINANCIAL SECTION

Independent auditor’s report 1 – 2Management’s discussion and analysis 3 – 13Basic financial statements: Government-wide financial statements:

Statement of net position 14 Statement of activities 15 –16

Fund financial statements: Governmental funds:

Balance sheet 17 – 18 Reconciliation of governmental funds balance sheet to the statement of net position 19 Statement of revenues, expenditures, and changes in fund balances 20 – 21 Reconciliation of the statement of revenues, expenditures, and changes in fund balances of of governmental funds to the statement of activities 22 Statement of revenues, expenditures, and changes in fund balances – budget to actual – general fund 23 – 24 Statement of revenues, expenditures, and changes in fund balance – budget to actual – special revenue funds – fire/rescue fund 25 Statement of revenues, expenditures, and changes in fund balance – budget to actual – special revenue funds - North Lauderdale Water Control District Fund 26Proprietary funds:

Statement of net position 27 Reconciliation of the statement of net position – proprietary funds to the statement of net position 28 Statement of revenues, expenses, and changes in net position 29 Reconciliation of the statement of revenues, expenses, and changes in net position to the statement of activities 30 Statement of cash flows 31 – 32Fiduciary fund:

Statement of fiduciary net position 33 Notes to financial statements 34 – 55

Required Supplementary Information (unaudited): Schedule of funding progress 56 Schedule of employer contributions 57

Table of Contents

FINANCIAL SECTION (CONTINUED) PAGESupplementary Information: Combining and individual fund statements and schedules: Nonmajor governmental funds: Combining balance sheet 58 Combining statement of revenues, expenditures and changes in fund balances 59 Internal service funds: Combining statement of net position 60 Combining statement of revenues, expenses, and changes in net position 61 Combining statement of cash flows 62-63 Statement of changes in assets and liabilities – agency fund 64 Schedule of revenues, expenditures and changes in fund balance – budget to actual –

65 special revenue funds – parks and recreation fund Schedule of revenues, expenditures and changes in fund balance – budget to actual – debt service fund 66

STATISTICAL SECTION Schedule 1 – Net position by components 67Schedule 2 – Change in net position 68–69Schedule 3 – Governmental activities tax revenues by source 70Schedule 4 – Fund balance of governmental funds 71Schedule 5 – Changes in fund balance of governmental funds 72–73Schedule 6 – Assessed value and estimated actual value of taxable property 74Schedule 7 – Property tax rates – direct and overlapping governments 75Schedule 8 – Principal property taxpayers 76Schedule 9 – Property tax levies and collections 77Schedule 10 – Ratio of outstanding debt by type 78Schedule 11 – Ratio of general bonded debt outstanding 79Schedule 12 – Direct and overlapping governmental activity debt 80Schedule 13 – Legal debt margin information 81Schedule 14 – Pledged revenue coverage 82Schedule 15 – Demographic and economic statistics 83Schedule 16 – Principal employers 84Schedule 17 – Full-time equivalent city government employees by function 85Schedule 18 – Operating indicators by function 86-87Schedule 19 – Capital assets by function 88

COMPLIANCE SECTIONIndependent auditor’s report on internal control over financial reporting and on compliance and other matters based on an audit of financial statements performed in accordance with Government Auditing Standards

89-90

Management letter pursuant to the rules of the Auditor General of the State of Florida 91-92

Independent auditor’s report on compliance for each major program and on internal control over compliance required by OMB Circular A-133 93-94

Schedule of expenditures of federal awards 95Notes to schedule of expenditures of federal awards 96Schedule of findings and questioned costs - federal awards 97

i

701 Southwest 71st Avenue, North Lauderdale, Florida 33068-2395 954-722-0900 • Fax 954-720-2151 • www.nlauderdale.org

March 18, 2014 To the Honorable Mayor, City Commissioners and Citizens of the City of North Lauderdale, Florida The Finance Department is pleased to submit the Comprehensive Annual Financial Report (“CAFR”) of the City of North Lauderdale, Florida (the “City”), for the fiscal year ended September 30, 2013. The report fulfills the state requirements that all general-purpose local governments publish a complete set of audited financial statements. In addition to meeting legal requirements, the report presents full financial disclosure. This philosophy is demonstrated by the informative financial analysis provided herein. Management assumes full responsibility for the completeness and reliability of all of the information contained in this report, based upon a comprehensive internal control framework that is designed for this purpose. Because the cost of internal controls should not outweigh their benefits, the City’s comprehensive framework of internal controls has been designed to provide reasonable rather than absolute assurance that the financial statements are free of any material misstatements. The City’s September 30, 2013 financial statements have been audited by a firm of certified public accountants licensed in the State of Florida. Their independent auditor report contains an unmodified opinion and is presented as the first component of the financial section of this report. The independent audit of the City’s financial statements included the federally mandated “Single Audit” designed to meet the special needs of federal grantor agencies. The standards governing Single Audit engagements require the independent auditor to report not only on the fair presentation of the financial statements, but also on the City’s internal controls and compliance with legal requirements, with special emphasis on internal controls and legal requirements involving the administration of federal awards. These reports are available in the final section of this report. Management’s Discussion and Analysis (“MD&A”) provides a narrative introduction, overview and analysis to accompany the basic financial statements. This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The City’s MD&A can be found immediately following the independent auditor’s report. North Lauderdale at a Glance

The City was incorporated on July 15, 1963 and is located in northwestern Broward County (the “County”), Florida, 8 miles northwest of Fort Lauderdale. The City was developed as a full service municipality serving a largely suburban residential community. Over the past few years, the City has annexed adjacent unincorporated properties into its municipal boundaries, bringing the City’s total land area and population to approximately 5.5 square miles and 41,000 residents, respectively. With the exception of a few remaining undeveloped parcels, the City has essentially reached build-out. Future growth of the City is unlikely due to the City’s geographic location within the County and the reality that there is no remaining unincorporated areas left to annex.

MAYOR VICE MAYOR Jack Brady Jerry Graziose

COMMISSIONER COMMISSIONER Gary Frankel David G. Hilton

COMMISSIONER CITY MANAGER Rich Moyle Ambreen Bhatty

CITY ATTORNEY CITY CLERK Samuel S. Goren Patricia Vancheri

ii

iii

iv

v

CITY OF NORTH LAUDERDALE, FLORIDA

Organizational Chart As of September 30, 2013

vi

CITY OF NORTH LAUDERDALE, FLORIDA

List of Principal Officials As of September 30, 2013 Title Name Mayor (At Large) Jack Brady Vice Mayor (District B) Jerry Graziose Commissioner (District A) Gary Frankel Commissioner (District C) Rich Moyle Commissioner (District D)

David G. Hilton

City Manager Ambreen Bhatty City Attorney Samuel S. Goren City Clerk Patricia Vancheri Assistant City Manager Vacant Community Development Director Tammy Reed-Holguin Finance Director Steven Chapman II Human Resource Manager Jennifer Yarmitzky Fire Chief Rodney Turpel Parks and Recreation Director Michael Sargis Police Chief/Public Safety Director William Jackson Public Works Director Mike Shields

2700 North Military Trail � Suite 350

Boca Raton, Florida 33431 (561) 994-9299 � (800) 299-4728 Fax (561) 994-5823 www.graucpa.com

INDEPENDENT AUDITOR’S REPORT

Honorable Mayor, City Commissioners and City Manager City of North Lauderdale, Florida

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of North Lauderdale, Florida (the “City”) as of and for the fiscal year ended September 30, 2013, and the related notes to the financial statements, which collectively comprise the City’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

OpinionsIn our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City, as of September 30, 2013, and the respective changes in financial position, and, where applicable, cash flows thereof and the respective budgetary comparison for the General Fund, Fire/Rescue and North Lauderdale Water Control District Funds for the fiscal year then ended in accordance with accounting principles generally accepted in the United States of America.

2

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis and the schedules of funding progress and employers contributions be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the City’s basic financial statements. The introductory section, combining and individual nonmajor fund financial statements, budgetary comparison schedules and statistical section, are presented for purposes of additional analysis and are not a required part of the basic financial statements. The schedule of expenditures of federal awards is presented for purposes of additional analysis as required by U.S. Office of Management and Budget Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and is also not a required part of the basic financial statements.

The combining and individual nonmajor fund financial statements, the schedules of revenues, expenditures, and changes in fund balances-budget to actual special revenue funds-parks and recreation and debt service funds, and the schedule of expenditures of federal awards are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining and individual nonmajor fund financial statements, the schedules of revenues, expenditures, and changes in fund balances-budget to actual special revenue funds-parks and recreation and debt service funds, and the schedule of expenditures of federal awards are fairly stated in all material respects in relation to the basic financial statements as a whole.

The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated March 18, 2014, on our consideration of the City’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the City’s internal control over financial reporting and compliance.

March 18, 2014 �

3

Management’s Discussion and Analysis The purpose of financial reporting is to provide financial statements readers with information that will help them make decisions about the entity. The following narrative overview and analysis of the City of North Lauderdale’s (“City”) financial activities for the fiscal year ended September 30, 2013 has been prepared by City management for the readers’ benefit. We encourage readers to consider the information presented herein in conjunction with the Letter of Transmittal, which can be found on pages i through iii of this report.

Financial Highlights

� The assets of the City exceeded its liabilities at the close of the most recent fiscal year by $106,483,510 (net position). Of this amount, $59,057,605 is unrestricted and may be utilized to meet the City’s ongoing obligations to citizens and creditors.

� The City’s total net position increased by $5,634,316. The increase is primarily attributable to

various operational savings resulting from cost containment measures that the City’s Administration has been implementing over the last several years.

� At the close of the most recent fiscal year, the City’s governmental funds reported combined ending

fund balances of $38,771,163. Approximately $27,145,191 is unassigned General Fund balance and is available for spending at the City’s discretion. The City Commission has assigned $2,450,000 for emergencies, $750,000 for future capital projects, and $7,311 for scholarships.

� During the fiscal year the City’s total governmental activity debt (excluding compensated absences) had a net decrease from the prior year of ($508,875) or approximately (11%). This decrease was due to the payment of scheduled debt service for the 2003 Capital Improvement Refunding Bonds.

Overview of the Financial Statements This discussion and analysis are intended to serve as an introduction to the City’s basic financial statements. These financial statements are comprised of three components; 1) government-wide financial statements, 2) fund financial statements and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves. Government-wide Financial Statements The government-wide financial statements are designed to provide readers with a broad overview of the City’s finances in a manner similar to a private-sector business. The statement of net position presents information on all of the City’s assets, liabilities, and deferred inflows/outflows of resources, with the difference reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the City’s financial position is improving or deteriorating. The statement of activities presents information showing how the City’s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement from some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and earned but unused vacation leave).

4

Overview of the Financial Statements (Continued) Both government-wide financial statements distinguish functions of the City that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are intended to recover all or a significant portion of their costs through user fees and charges (business-type activities). The governmental activities of the City include general government, public safety, community development, physical environment, streets, parks and recreation, and interest. The business-type activities of the City include water and sewer utilities and storm-water management operations. The government-wide financial statements include not only the City itself (the primary government), but also the legally separate North Lauderdale Water Control District. Financial information for this component unit is blended with the financial information presented for the primary government itself, since the governing body of the District and that of the City’s are one in the same – the City Commission. The Housing Authority of the City of North Lauderdale, Inc. (“Authority”), a discretely presented component unit, had no balances or activity during the most recent fiscal year. Fund Financial Statements A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City, like other state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. These financial statements report the City’s operations in greater detail than the government-wide financial statements. All of the City’s funds can be divided into three categories: governmental funds, proprietary funds and fiduciary funds.

Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government’s near-term financing requirement. Because the focus of governmental funds is narrower than the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the City’s near-term financing decisions. The governmental fund balance sheet and the governmental fund statement of revenues, expenditures and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. The City maintains several individual governmental funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures and changes in fund balances for the major funds which include the General Fund, the Fire/Rescue Special Revenue Fund, the North Lauderdale Water Control District Special Revenue Fund, the Debt Service Fund and the Capital Projects Fund. Data from the other governmental funds are combined into a single, aggregated presentation. Individual fund data for each of these non-major governmental funds is provided in the form of combining statements presented immediately following the notes to the financial statements. The City prepares and adopts appropriated budgets for all of its governmental and proprietary fund types, except the Police Education Special Revenue Fund, the Law Enforcement Special Revenue Fund, the Grants Special Revenue Fund, and the Capital Projects Fund.

5

Overview of the Financial Statements (Continued) Fund Financial Statements

A budgetary comparison statement has been provided for the General Fund, the Fire/Rescue Special Revenue Fund and the North Lauderdale Water Control District Special Revenue Fund in the Fund Financial Statements section of this report. Additionally, a budgetary comparison schedule has been provided for the Recreation Special Projects Special Revenue Fund and the Debt Service Fund in the Combining and Individual Fund Statements and Schedules section of this report. These are presented to demonstrate compliance with the budget. They compare the actual amount to the budgeted amount as well as the original adopted budget to the final budget.

Proprietary funds provide the same type of information as the government-wide financial statements, only in more detail. The City maintains the following different types of proprietary funds:

� The Enterprise Funds are used to report the same functions presented as business-type activities in the government-wide financial statements. The City uses Enterprise Funds to account for its water and sewer utilities and storm-water management operations. The City’s proprietary fund financial statements provide separate information for the water and sewer utilities operation because it is considered to be a major fund.

� Internal Service Funds are an accounting device used to accumulate and allocate costs internally

among the City’s various functions. The City uses internal service funds to account for its vehicle maintenance, information technology and insurance operations. Because these services benefit both the governmental and business-type functions, they have been included within governmental activities and business-type activities in the government-wide financial statements based on the applicable usage. The three internal services funds are aggregated and combined into a single column for presentation in the proprietary fund financial statements. Individual fund data for the internal service funds is provided in the form of combining statements are presented immediately following the notes to the financial statements.

Fiduciary funds are used to account for resources held in a trust or as an agent by the City for others. Fiduciary funds are not reflected in the government-wide financial statements because the resources of those funds are not available to support the City’s own programs. The accounting used for fiduciary funds is much like that used for proprietary funds. The City only has one agency fund, the Police Explorer Agency Fund. The Notes to the Financial Statements provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements.

In addition to the basic financial statements and accompanying notes, this report also contains Other Information. The information includes certain required supplementary information. In addition, the combining statements referred to above are presented immediately following the required supplementary information.

Government-wide Financial Analysis

Net Position As noted earlier, over time, net position may serve as a useful indicator of a government’s financial position. At the close of the most recent fiscal year the City’s assets exceeded its liabilities by $106,483,510. The following table summarizes the City’s net position at September 30, 2013 and 2012 and is followed by a comparative analysis between the two years.

6

Government-wide Financial Analysis (Continued)

Net Position (Continued)

2013 2012 2013 2012 2013 2012

Current and other assets 46,210,710$ 44,423,893$ 21,993,519$ 18,798,645$ 68,204,229$ 63,222,538$ Capital assets 33,329,872 33,804,457 14,305,201 14,083,183 47,635,073 47,887,640

Total assets 79,540,582 78,228,350 36,298,720 32,881,828 115,839,302 111,110,178

Noncurrent liabilities 6,028,347 6,193,687 113,579 110,469 6,141,926 6,304,156 Other liabilities 1,536,498 1,928,741 1,677,368 2,028,087 3,213,866 3,956,828

Total liabilities 7,564,845 8,122,428 1,790,947 2,138,556 9,355,792 10,260,984

Net position:Net investment in capital assets 29,370,533 29,336,243 14,305,201 14,083,183 43,675,734 43,419,426 Restricted 3,750,171 3,607,006 - - 3,750,171 3,607,006 Unrestricted 38,855,033 37,162,673 20,202,572 16,660,089 59,057,605 53,822,762

Total net position 71,975,737$ 70,105,922$ 34,507,773$ 30,743,272$ 106,483,510$ 100,849,194$

City of North Lauderdale, FloridaNet Position

TotalBusiness-type

ActivitiesGovernmental

Activities

Of the City’s net position, approximately 41% reflects its investment in capital assets (e.g., land, buildings, equipment and infrastructure), net of accumulated depreciation and less any outstanding debt used to construct or acquire those assets. These capital assets are used to provide citizen services and are therefore not available for future spending. Although the City’s investment in its capital assets is reported net of related debt, the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. The restricted portion of the City’s net position, $3,750,171 or approximately 4% represents resources that are subject to external restrictions on how they may be used. The remaining balance of $59,057,605 or approximately 55% is unrestricted and may be used to meet the City’s ongoing obligations to citizens and creditors. As of the end of both the current and prior fiscal year, the City reported an increase in its unrestricted net position, both for the government as a whole, as well as for its separate governmental and business-type activities. For governmental activities, there was an increase in net position of $1,869,815 or approximately 3% from the prior fiscal year resulting primarily from various operational savings resulting from cost containment measures that the City’s Administration has been implementing over the last several years For business-type activities, there was an increase in net position of $3,764,501 or approximately 12% from the prior fiscal year resulting primarily from various operational savings resulting from cost containment measures that the City’s Administration has been implementing over the last several years.

7

Government-wide Financial Analysis (Continued) Net Position (Continued) Changes in Net Position The following table summarizes the City’s changes in net position for the fiscal years ended September 30, 2013 and 2012 and is followed by a comparative analysis between the two years.

Revenues: 2013 2012 2013 2012 2013 2012Program revenues:

Charges for services 12,923,236$ 11,405,275$ 12,056,579$ 12,395,192$ 24,979,815$ 23,800,467$ Operating grants and contributions 2,588,430 686,303 - - 2,588,430 686,303 Capital grants and contributions 62,421 116,124 600,388 - 662,809 116,124

General revenues:Property taxes 6,789,514 7,154,480 - - 6,789,514 7,154,480 Utility taxes 2,421,234 3,546,402 - - 2,421,234 3,546,402 Franchise taxes 2,373,523 2,509,174 - - 2,373,523 2,509,174 Grants and contributions not restricted to specific programs 4,067,481 4,174,950 - - 4,067,481 4,174,950 Interest income 22,325 205,817 2,110 115,816 24,435 321,633 Other 25,759 - - - 25,759 -

Total revenues 31,273,923 29,798,525 12,659,077 12,511,008 43,933,000 42,309,533

Expenses:General government 3,600,906 3,242,231 - - 3,600,906 3,242,231 Public safety 14,084,825 13,442,631 - - 14,084,825 13,442,631 Community development 2,163,929 1,918,200 - - 2,163,929 1,918,200 Physical environment 3,556,925 2,220,793 - - 3,556,925 2,220,793 Streets 1,784,419 1,711,434 - - 1,784,419 1,711,434 Parks and recreation 4,017,915 3,955,195 - - 4,017,915 3,955,195 Interest on debt 195,189 623,976 - - 195,189 623,976 Water and sewer - - 8,146,215 8,522,861 8,146,215 8,522,861 Stormwater - - 748,361 630,768 748,361 630,768

Total expenses 29,404,108 27,114,460 8,894,576 9,153,629 38,298,684 36,268,089 Change in net position 1,869,815 2,684,065 3,764,501 3,357,379 5,634,316 6,041,444 Net position, beginning 70,105,922 67,421,857 30,743,272 27,385,893 100,849,194 94,807,750 Net position, ending 71,975,737$ 70,105,922$ 34,507,773$ 30,743,272$ 106,483,510$ 100,849,194$

City of North Lauderdale, FloridaChanges in Net Position

TotalBusiness-type

ActivitiesGovernmental

Activities

Governmental Activities – Governmental activities increased the City’s net position by $1,869,815 representing approximately 33% of the total increase in the City’s net position. General revenues of the City exceeded program costs as the City continues to experience operational savings resulting from cost containment measures that the City’s Administration has been implementing over the last several years.

8

Government-wide Financial Analysis (Continued)

Changes in Net Position - Governmental Activities (Continued)

Charges for services38%

Operating grants and

contributions2%

Capital grants and

contributions 1%

Property taxes24%

Utility taxes8%

Franchise taxes8%

Grants and contributions not

restricted to specific programs

14%

Interest income and other revenues

1%

Revenues by SourceGovernmental Activities

Charges for services

Operating grants and contributions

Capital grants and contributions

Property taxes

Utility taxes

Franchise taxes

Grants and contributions not restricted tospecific programs

Interest income and other revenues

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

Generalgovernment

Public safety Communitydevelopment

Physicalenvironment

Streets Parks andrecreation

Interest

Expenses and Program RevenuesGovernmental Activities

Expenses Program Revenues

9

Government-wide Financial Analysis (Continued)

Changes in Net Position - (Continued)

Business-type Activities – Business-type activities increased the City’s net position by $3,764,501 representing approximately 67% of the total increase in the City’s net position. The increase resulted from a combination of continuing cost containment measures and an increase in utility service charges.

Charges for services95%

Capital grants and contributions

5%

Interest income and other revenues

0%

Revenues by SourceBusiness-type Activities

Charges for services

Capital grants and contributions

Interest income and other revenues

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

Water and sewer Stormwater

Expenses and Program RevenuesBusiness-type Activities

Expenses Program Revenues

10

Financial Analysis of the Individual Major Funds As noted earlier, the City uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental Funds – The focus of the City’s governmental funds is to provide information on near-term inflows, outflows and balances of spendable resources. Such information is useful in assessing the City’s financing requirements. In particular, unreserved fund balance may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year. At the close of the most recent fiscal year, the City’s governmental funds reported combined ending fund balances of $38,771,163, an increase of $1,858,481 or approximately 5% from prior fiscal year. $27,145,191 of this total amount constitutes unassigned fund balance, which is available for spending at the City’s discretion. The remainder of fund balance is either restricted, committed, or assigned to indicate that it is 1) restricted for particular purposes, 2) committed for particular purposes, or 3) assigned for particulate purposes. The General Fund is the City’s main operating fund. At the end of the current fiscal year, the General Fund’s unassigned fund balance was $27,145,191 while the total fund balance reached $30,352,502. As a measure of the General Fund’s liquidity, it may be useful to compare both unreserved fund balance and total fund balance to total fund expenditures.

The fund balance of the City’s General Fund increased by $2,458,448 from the prior fiscal year resulting primarily from unanticipated revenue streams combined with various operational savings resulting from cost containment measures that the City’s Administration has been implementing over the last several years. The fund balance of the City’s Fire/Rescue Special Revenue Fund, a major fund, decreased by ($50,105) due to the spending of resources for public safety operating expenditures. The fund balance of the North Lauderdale Water Control District Special Revenue Fund, a major fund, increased by $122,303 due to the excess in revenue of special assessments for exempt properties which is funded by the General Fund and the containment of costs. The fund balance of the Debt Service Fund, a major fund, decreased by ($5,433) due to the use of resources for debt costs. The fund balance of the Capital Projects Fund, a major fund, decreased by ($668,452) due to the spending of resources for ongoing capital projects. Proprietary Funds – The City’s proprietary funds provide the same type of information found in the government-wide financial statements, but in more detail. At the close of the most recent fiscal year, unrestricted net position for the Utilities Fund and the Stormwater Fund totaled $17,841,202 (an increase of $3,461,355) and $1,919,653 (an increase of $40,055) respectively. Other factors concerning the finances of both of these funds have already been addressed in the discussion of the City’s business-type activities.

11

General Fund Budgetary Highlights For fiscal year 2013, the general fund budget was amended to increase revenues by $1,350,000 and increase expenditures by $1,350,000, excluding transfers. The budget was amended to provide for the recognition of solid waste assessment and services. The general fund 2013 budget was also amended for interdepartmental re-allocations to decrease general government and increase public safety by $16,000. Actual results were greater than the final amended budget, excluding transfers. These results can be attributed to the following:

� Unanticipated revenue streams including higher than anticipated building permit and code enforcement fines.

� Various operational savings resulting from cost containment measures that the City’s Administration has been implementing over the last several years. These cost containment measures range from freezing vacant positions, consolidating positions, reducing operational hours in various programs, agreeing to lease the school facility, utilizing conservative methods for utilities expenditures, and repairs and maintenance.

Capital Assets and Debt Administration

Capital Assets The City’s investment in capital assets, net of accumulated depreciation, for its governmental and business-type activities as of September 30, 2013 and 2012 amounts to $47,635,073 and $47,887,640, respectively.

The following schedule summarizes the City’s capital assets by category as of September 30, 2013 and 2012.

2013 2012 2013 2012 2013 2012

Land 6,396,615$ 6,396,615$ 86,365$ 86,365$ 6,482,980$ 6,482,980$ Construction in process 692,468 1,037,428 5,204,481 5,052,018 5,896,949 6,089,446 Residual interest in assets held by Broward County Sheriff's Office 489,626 489,626 - - 489,626 489,626 Buildings 12,822,940 12,316,991 - - 12,822,940 12,316,991 Improvements other than buildings 6,130,552 6,178,196 350,242 387,620 6,480,794 6,565,816 Machinery and equipment 2,024,046 2,272,225 44,468 75,236 2,068,514 2,347,461 Infrastructure 4,773,625 5,113,376 8,619,645 8,481,944 13,393,270 13,595,320

Total 33,329,872$ 33,804,457$ 14,305,201$ 14,083,183$ 47,635,073$ 47,887,640$

Governmental Activities

Business-type Activities

City of North Lauderdale, FloridaCapital Assets

(net of depreciation)

Total

The major capital asset activity that occurred during the 2013 fiscal year was comprised of vehicle additions of approximately $206,480, continuing improvements to the City’s park and recreational facilities of approximately $1,138,080, furnishing and equipment additions of approximately $62,230, ongoing water plant renovations of approximately $152,460, and contributed utility infrastructure of approximately $600,390. Additional information can be found in footnote 5 in the notes to the financial statements.

12

Capital Assets and Debt Administration (Continued)

Long-term Debt At September 30, 2013, the City had $3,959,339 in outstanding debt related to the 2003 Capital Improvement Revenue Refunding Bonds secured by specified revenue sources.

2013 2012 2013 2012 2013 2012

Refunding bonds 3,959,339$ 4,468,214$ -$ -$ 3,959,339$ 4,468,214$ Total 3,959,339$ 4,468,214$ -$ -$ 3,959,339$ 4,468,214$

Governmental Activities Total

City of North Lauderdale, FloridaLong-term Liabilities

Business-type Activities

The City’s debt decreased from the prior fiscal year by ($508,875) or approximately (11%). This decrease was due to the payment of scheduled debt service for the 2003 Bonds. Additional information can be found in footnote 8 in the notes to the financial statements. Economic Factors and Next Year’s Budget A large part of the City’s strategic planning and annual budget process involves Commission and staff workshops. During these workshops, the City’s past and current operations are reviewed in detail and discussions are held regarding the City’s future vision for operations including staffing, facilities and public services. In addition to the City’s operations, initiatives for major capital expenditures are discussed at length. Long range goals, economic factors, staffing implications and available financial resources assist the Commission in prioritizing their goals and objectives for the coming fiscal year. In developing the fiscal year 2014 Budget and Capital Improvement Program, the following economic factors were considered:

� Between 2009 and 2012 the City experienced a tremendous reduction in property value, the impact of which will continue to be felt throughout the City for some time. Additionally, due to the unstable financial market and the reduction in consumer spending, intergovernmental revenue (including sales tax allocations and shared revenue) and interest rates on investments have not increased. City Administration will continue its innovative and proactive fiscal practices that have enabled the City to weather the effects of the recession.

� The City’s operating millage rate will be 7.6078 mils and the debt millage rate is 0.000 mils.

� The City’s Solid Waste special assessment rate for residential units remained at $216.02 per year.

� In fiscal year 2011 the City’s Fire/Rescue Special Assessment program had a rate analysis conducted. The study’s resulting rate table is being implemented over a five-year-period beginning in fiscal year 2012 and continuing through fiscal year 2016. The assessment for the fiscal year 2014 is the third year of the five-year plan.

� The City would continue to pay cash (rather than finance) vehicles and certain capital projects

whenever feasible.

� A utility rate study was completed in fiscal year 2007 to ensure that the utility revenue keeps pace with the continually changing needs and costs of essential service. After performing a thorough analysis of the Utility Fund’s operational and capital requirements, the engineers recommended a 5% annual increase. Water and sewer utility rates were revised in March 2011 and have not been increased.

13

Requests for Information These financial statements are designed to provide citizens, taxpayers, customers, investors and creditors with a general overview of the City’s finances and to demonstrate the City’s accountability. If you should have any questions pertaining to the information presented in this report or would like additional information, please contact the Finance Department located at 701 SW 71st Avenue, North Lauderdale, Florida 33068-2395.

This page intentionally left blank.

14

City of North Lauderdale, Florida

Statement of Net Position September 30, 2013

Governmental Business-type Activities Activities Total

AssetsCash and equity in pooled cash 15,902,246$ 6,669,553$ 22,571,799$ Investments 27,005,375 12,865,914 39,871,289 Accounts receivable, net of allowances 3,293,325 1,355,278 4,648,603 Due from other governmental units 9,764 - 9,764 Restricted assets:

Cash, cash equivalents, and investments - 1,102,774 1,102,774 Capital assets not being depreciated:

Land 6,396,615 86,365 6,482,980 Construction in progress 692,468 5,204,481 5,896,949 Residual interest in equipment 489,626 - 489,626

Capital assets, net of accumulated depreciation:Buildings 12,822,940 - 12,822,940 Improvements other than buildings 6,130,552 350,242 6,480,794 Machinery and equipment 2,024,046 44,468 2,068,514 Infrastructure 4,773,625 8,619,645 13,393,270

Total assets 79,540,582 36,298,720 115,839,302

Liabilities and Net PositionLiabilities:

Accounts payable and other liabilities 1,153,459 564,830 1,718,289 Due to other governmental units - 9,764 9,764 Contracts payable 158,252 - 158,252 Accrued interest 86,198 - 86,198 Unearned revenue 138,589 - 138,589 Payable from restricted assets - 1,102,774 1,102,774

Noncurrent liabilities:Due within one year:

Compensated absences 62,360 - 62,360 Bonds payable 533,332 - 533,332

Due in more than one year:Compensated absences 1,212,648 113,579 1,326,227 Net Other Post Employment Benefit obligation 794,000 - 794,000 Bonds payable 3,426,007 - 3,426,007

Total liabilities 7,564,845 1,790,947 9,355,792

Net position:Net investment in capital assets 29,370,533 14,305,201 43,675,734 Restricted for:

Fire rescue 2,396,440 - 2,396,440 Water Control District 892,385 - 892,385 Police education 11,937 - 11,937 Law enforcement 303,063 - 303,063 Grants 146,346 - 146,346

Unrestricted 38,855,033 20,202,572 59,057,605 Total net position 71,975,737$ 34,507,773$ 106,483,510$

Primary Government

See Notes to Financial Statements

15

City of North Lauderdale, Florida

Statement of Activities Fiscal Year Ended September 30, 2013

Charges Operating Capitalfor Grants and Grants and

Function/Program Expenses Services Contributions ContributionsPrimary government: Governmental activities:

General government 3,600,906$ 6,752,084$ -$ -$ Public safety 14,084,825 4,233,652 59,291 - Community development 2,163,929 912,723 424,658 62,421 Physical environment 3,556,925 585,468 143 - Streets 1,784,419 - 2,104,338 - Parks and recreation 4,017,915 439,309 - - Interest 195,189 - - - Total government activities 29,404,108 12,923,236 2,588,430 62,421

Business-type activities:Water and sewer 8,146,215 11,333,236 - 600,388 Stormwater 748,361 723,343 - - Total business-type activities 8,894,576 12,056,579 - 600,388 Total primary government 38,298,684$ 24,979,815$ 2,588,430$ 662,809$

General revenues:Property taxesUtility taxesFranchise taxesGrants and contributions not restricted to specific programsInterest income Miscellaneous revenues

Total general revenues Change in net positionNet position, beginningNet position, ending

Program Revenues

See Notes to Financial Statements

16

Governmental Business-typeActivities Activities Total

3,151,178$ -$ 3,151,178$ (9,791,882) - (9,791,882)

(764,127) - (764,127) (2,971,314) - (2,971,314)

319,919 - 319,919 (3,578,606) - (3,578,606)

(195,189) - (195,189) (13,830,021) - (13,830,021)

- 3,787,409 3,787,409 - (25,018) (25,018) - 3,762,391 3,762,391

(13,830,021) 3,762,391 (10,067,630)

6,789,514 - 6,789,514 2,421,234 - 2,421,234 2,373,523 - 2,373,523

4,067,481 - 4,067,481 22,325 2,110 24,435 25,759 - 25,759

15,699,836 2,110 15,701,946 1,869,815 3,764,501 5,634,316

70,105,922 30,743,272 100,849,194 71,975,737$ 34,507,773$ 106,483,510$

Primary Government

Net (Expense) Revenue and Changes in Net Position

17

City of North Lauderdale, Florida

Balance Sheet Governmental Funds September 30, 2013

North Lauderdale

Water ControlGeneral Fire/Rescue District

Fund Fund FundAssetsCash and equity in pooled cash 10,899,864$ 199,987$ 819,724$ Investments 19,142,151 336,510 72,661Accounts receivable, net of allowances

for uncollectible accounts 1,144,947 1,973,504 - Due from other governmental units 9,764 - -

Total assets 31,196,726$ 2,510,001$ 892,385$

Liabilities and Fund BalancesLiabilities:

Accounts payable and other liabilities 705,635$ 113,561$ -$ Contracts payable - - - Unearned revenue 138,589 - -

Total liabilities 844,224 113,561 -

Fund balances:Restricted for:

Fire rescue - 2,396,440 - Water Control District - - 892,385 Police education - - - Law enforcement - - - Grants - - -

Committed for:Debt service - - -

Assigned to: Future capital projects 750,000 - - Capital projects - - - Contingencies 2,450,000 - - Scholarships 7,311 - -

Unassigned 27,145,191 - - Total fund balances 30,352,502 2,396,440 892,385 Total liabilities and fund balances 31,196,726$ 2,510,001$ 892,385$

Major Funds

See Notes to Financial Statements

18

Debt Capital Other TotalService Projects Nonmajor GovernmentalFund Fund Funds Funds

32,847$ 1,764,982$ 132,622$ 13,850,026$ 55,339 2,973,574 223,438 22,803,673

- - 174,874 3,293,325 - - - 9,764

88,186$ 4,738,556$ 530,934$ 39,956,788$

-$ -$ 69,588$ 888,784$ - 158,252 - 158,252 - - - 138,589 - 158,252 69,588 1,185,625

- - - 2,396,440 - - - 892,385 - - 11,937 11,937 - - 303,063 303,063 - - 146,346 146,346

88,186 - - 88,186

- - - 750,000 - 4,580,304 - 4,580,304 - - - 2,450,000 - - - 7,311 - - - 27,145,191

88,186 4,580,304 461,346 38,771,163 88,186$ 4,738,556$ 530,934$ 39,956,788$

Major Funds

19

City of North Lauderdale, Florida

Reconciliation of Governmental Funds Balance Sheet to the Statement of Net Position September 30, 2013

Total fund balance - governmental fund 38,771,163$

Amounts reported for governmental activities in the statement ofnet position are different because:

The cost of capital assets acquired is reported as an expenditurein the governmental funds. The statement of net position includes those capital assets, net of accumulated depreciation among the assets of the government as a whole.

Cost of capital assets 66,656,313 Accumulated depreciation (33,326,441) 33,329,872

Liabilities not payable from current available resources are notreported as fund liabilities in governmental fund financial statements. All liabilities, both current and long-term, are reported in the government-wide financial statements.

Accrued interest (86,198) Long-term liabilities (3,959,339) Compensated absences (1,250,747) (5,296,284)

Net Other Post Employment Benefit assets/obligations resultingfrom overfunding/underfunding are not reported in the funds as they are not payable from current available resources. (794,000)

Internal service funds are used by management to charge thecost of vehicle maintenance, information technology, andinsurance to individual funds. The assets and liabilities of theInternal Service Fund are included in governmental activitiesin the statement of net position. 5,964,986

Net position of governmental activities 71,975,737$

See Notes to Financial Statements

This page intentionally left blank.

20

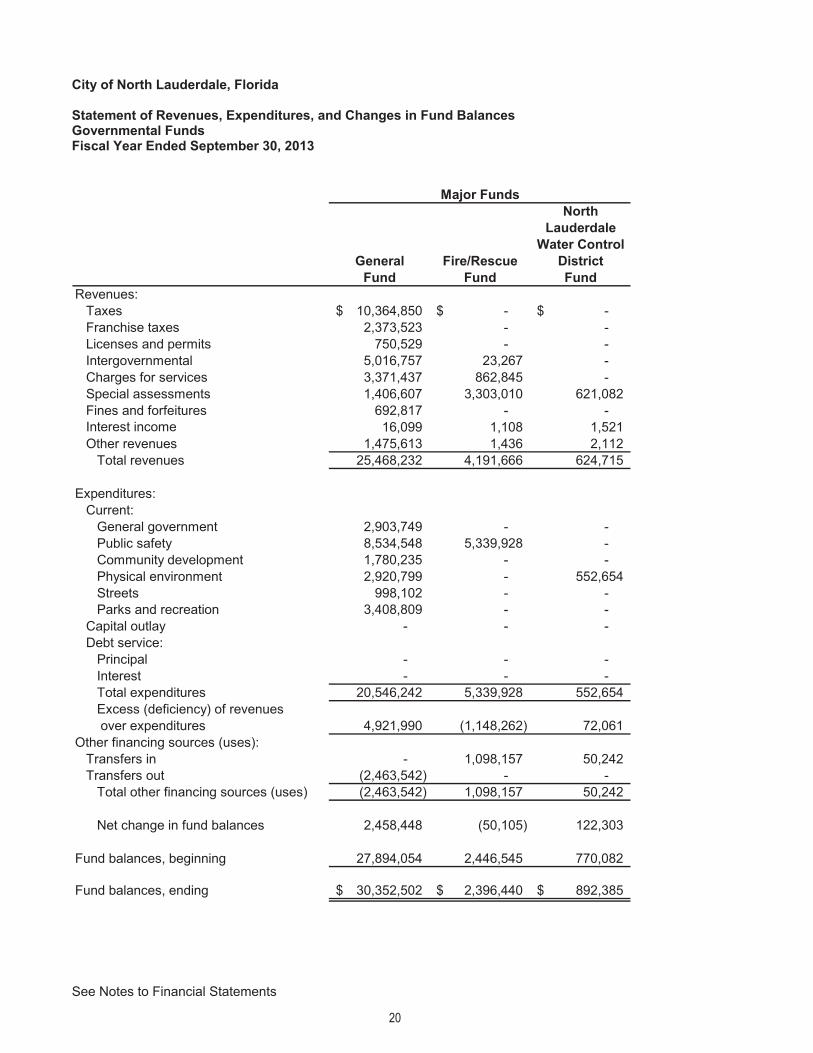

City of North Lauderdale, Florida

Statement of Revenues, Expenditures, and Changes in Fund Balances Governmental Funds Fiscal Year Ended September 30, 2013

NorthLauderdale

Water ControlGeneral Fire/Rescue District

Fund Fund FundRevenues:

Taxes 10,364,850$ -$ -$ Franchise taxes 2,373,523 - - Licenses and permits 750,529 - - Intergovernmental 5,016,757 23,267 - Charges for services 3,371,437 862,845 - Special assessments 1,406,607 3,303,010 621,082 Fines and forfeitures 692,817 - - Interest income 16,099 1,108 1,521 Other revenues 1,475,613 1,436 2,112

Total revenues 25,468,232 4,191,666 624,715

Expenditures:Current:

General government 2,903,749 - - Public safety 8,534,548 5,339,928 - Community development 1,780,235 - - Physical environment 2,920,799 - 552,654Streets 998,102 - - Parks and recreation 3,408,809 - -

Capital outlay - - - Debt service:

Principal - - - Interest - - - Total expenditures 20,546,242 5,339,928 552,654 Excess (deficiency) of revenues over expenditures 4,921,990 (1,148,262) 72,061

Other financing sources (uses):Transfers in - 1,098,157 50,242Transfers out (2,463,542) - -

Total other financing sources (uses) (2,463,542) 1,098,157 50,242 Net change in fund balances 2,458,448 (50,105) 122,303

Fund balances, beginning 27,894,054 2,446,545 770,082

Fund balances, ending 30,352,502$ 2,396,440$ 892,385$

Major Funds

See Notes to Financial Statements

21

Debt Capital Other Total Service Projects Nonmajor GovernmentalFund Fund Funds Funds

960$ -$ -$ 10,365,810$ - - - 2,373,523 - - - 750,529 - - 546,511 5,586,535 - - 378,384 4,612,666 - - - 5,330,699 - - 44,529 737,346 24 1,669 121 20,542

- 15,000 - 1,494,161 984 16,669 969,545 31,271,811

6,417 - - 2,910,166 - - 71,727 13,946,203 - - 377,004 2,157,239 - - - 3,473,453 - - - 998,102 - - 450,178 3,858,987 - 1,285,121 68,916 1,354,037

508,875 - - 508,875 206,268 - - 206,268 721,560 1,285,121 967,825 29,413,330

(720,576) (1,268,452) 1,720 1,858,481

715,143 600,000 - 2,463,542 - - - (2,463,542)

715,143 600,000 - -

(5,433) (668,452) 1,720 1,858,481

93,619 5,248,756 459,626 36,912,682

88,186$ 4,580,304$ 461,346$ 38,771,163$

Major Funds

22

City of North Lauderdale, Florida

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities Fiscal Year Ended September 30, 2013 Net change in fund balances - total governmental funds 1,858,481$

Amounts reported for governmental activities in the statement of activities are differentbecause:

Capital assets are reported in the governmental fund as expenditures. However, in the statement of activities, the cost of certain of those assets is eliminated and capitalized as capital assets. 1,397,022

Repayment of long-term liabilities are reported as expenditures in the governmental funds, but such repayments reduce liabilities in the statement of net position andare eliminated from the statement of activities. 508,875

Internal Service Funds are used by management to charge the costs of VehicleMaintenance, Information Technology, and Insurance to individual funds. The netrevenue of certain activities of Internal Service Funds is reported with governmentalactivities. 223,744

Any net increase or decrease in Internal Service Fund position associated with non-operating items should not be eliminated in the process of consolidation. Theseamounts would be added to the statement of activities. 2,110

Expenses reported in the statement of activities that do not require the use of currentfinancial resources are not reported as expenditures in the governmental funds. The details of the differences are as follows:

Change in accrued interest 11,080 Change in compensated absences (138,356) Change in Other Post Employment Benefit obligation (207,000) Depreciation of capital assets (1,786,141)

Change in net position of governmental activities 1,869,815$

See Notes to Financial Statements

This page intentionally left blank.

23

City of North Lauderdale, Florida

Statement of Revenues, Expenditures, and Changes in Fund Balances – Budget to Actual General Fund Fiscal Year Ended September 30, 2013

Variance withFinal Budget-

Actual PositiveOriginal Final Amounts (Negative)

Revenues:Property taxes 6,737,997$ 6,737,997$ 6,788,554$ 50,557$ Utility taxes 3,588,973 3,588,973 3,576,296 (12,677) Franchise taxes 2,688,478 2,688,478 2,373,523 (314,955) Licenses and permits 567,000 567,000 750,529 183,529 Intergovernmental 4,282,187 4,282,187 5,016,757 734,570 Charges for services 3,306,248 3,306,248 3,371,437 65,189 Special assessments - 1,350,000 1,406,607 56,607 Fines and forfeitures 445,000 445,000 692,817 247,817 Interest income 221,000 221,000 16,099 (204,901) Other revenues 698,048 698,048 1,475,613 777,565

Total revenues 22,534,931 23,884,931 25,468,232 1,583,301

Expenditures:General Government:

City commission 422,283 422,283 357,560 64,723 City manager 427,798 427,798 407,534 20,264 City attorney 278,585 278,585 274,417 4,168 City clerk 354,281 354,281 265,392 88,889 Human resources 419,737 419,737 285,564 134,173 Finance 914,405 914,405 825,421 88,984 Other 575,976 575,976 487,861 88,115 Contingency 267,152 251,152 - 251,152

Total general government 3,660,217 3,644,217 2,903,749 740,468

Public safety:BSO police contract 8,193,667 8,193,667 8,182,204 11,463 Crossing guard contract 325,000 341,000 352,344 (11,344)

Total public safety 8,518,667 8,534,667 8,534,548 119

Community development:Operating 1,291,930 1,291,930 1,270,585 21,345 Code compliance 576,483 576,483 509,650 66,833

Total community development 1,868,413 1,868,413 1,780,235 88,178

Public works:Physical environment:

Building maintenance 956,043 956,043 1,005,937 (49,894) Facility maintenance 10,000 10,000 146,993 (136,993) Canal maintenance 476,361 476,361 422,710 53,651 Solid waste and recycling - 1,350,000 1,345,159 4,841

Total physical environment 1,442,404 2,792,404 2,920,799 (128,395)

Budgeted Amounts

See Notes to Financial Statements

24

City of North Lauderdale, Florida

Statement of Revenues, Expenditures, and Changes in Fund Balances – Budget to Actual General Fund Fiscal Year Ended September 30, 2013 (Continued)

Variance withFinal Budget-

Actual PositiveOriginal Final Amounts (Negative)

Streets:Personnel services 386,184 386,184 397,008 (10,824) Other current expenditures 744,247 744,247 601,094 143,153

Total street maintenance 1,130,431 1,130,431 998,102 132,329 Total public works 2,572,835 3,922,835 3,918,901 3,934

Parks and recreation:Parks 2,202,099 2,202,099 2,231,968 (29,869) Recreation 844,431 844,431 789,061 55,370 Aquatics 404,727 404,727 387,780 16,947

Total parks and recreation 3,451,257 3,451,257 3,408,809 42,448

Total expenditures 20,071,389 21,421,389 20,546,242 875,147

Excess of revenues over expenditures 2,463,542 2,463,542 4,921,990 2,458,448

Other financing sources (uses):Transfers out (2,463,542) (2,463,542) (2,463,542) -

Total other financing sources (uses) (2,463,542) (2,463,542) (2,463,542) -

Net change in fund balance -$ -$ 2,458,448 2,458,448$

Fund balance, beginning 27,894,054

Fund balance, ending 30,352,502$

Budgeted Amounts

See Notes to Financial Statements

25

City of North Lauderdale, Florida

Statement of Revenues, Expenditures and Changes in Fund Balance – Budget to Actual Special Revenue Funds – Fire/Rescue Fund Fiscal Year Ended September 30, 2013

Variance WithFinal Budget-

Actual PositiveOriginal Final Amounts (Negative)

Revenues:Intergovernmental 16,000$ 16,000$ 23,267$ 7,267$ Charges for services 771,819 771,819 862,845 91,026 Special assessments 3,259,105 3,259,105 3,303,010 43,905 Interest income 6,296 6,296 1,108 (5,188) Other revenues - - 1,436 1,436

Total revenues 4,053,220 4,053,220 4,191,666 138,446

Expenditures:Public safety:

Operating division 4,646,126 4,646,126 4,710,438 (64,312) Administration 739,251 739,251 629,490 109,761 Total expenditures 5,385,377 5,385,377 5,339,928 45,449

Excess (deficiency) of revenues over(under) expenditures (1,332,157) (1,332,157) (1,148,262) 183,895

Other financing sources (uses):Transfers in 1,098,157 1,098,157 1,098,157 - Use of fund balance 234,000 234,000 - (234,000)

Total other financing sources (uses) 1,332,157 1,332,157 1,098,157 (234,000)

Net change in fund balance -$ -$ (50,105) (50,105)$

Fund balance, beginning 2,446,545

Fund balance, ending 2,396,440$

Budgeted Amounts

See Notes to Financial Statements

26

City of North Lauderdale, Florida

Statement of Revenues, Expenditures and Changes in Fund Balance – Budget to Actual Special Revenue Funds - North Lauderdale Water Control District Fund Fiscal Year Ended September 30, 2013

Variance withFinal Budget-

Actual PositiveOriginal Final Amounts (Negative)

Revenues:Special assessments 604,505$ 604,505$ 621,082$ 16,577$ Interest income 3,000 3,000 1,521 (1,479) Miscellaneous - - 2,112 2,112

Total revenues 607,505 607,505 624,715 17,210

Expenditures:Physical environment:

Contractual services 553,798 553,798 540,298 13,500 Administration fee - - 12,356 (12,356) Contingency 103,949 103,949 - 103,949

Total expenditures 657,747 657,747 552,654 105,093

Excess (deficiency) of revenues over (under) expenditures (50,242) (50,242) 72,061 122,303

Other financing sources (uses):Transfers in 50,242 50,242 50,242 -

Total other financing sources (uses) 50,242 50,242 50,242 -

Net change in fund balance -$ -$ 122,303 122,303$

Fund balance, beginning 770,082

Fund balance, ending 892,385$

Budgeted Amounts

See Notes to Financial Statements

27

City of North Lauderdale, Florida

Statement of Net Position Proprietary Fund September 30, 2013

Major Fund InternalUtilities Nonmajor Service

Fund Fund Total FundsAssetsCurrent Assets

Cash and equity in pooled cash 5,510,086$ 717,750$ 6,227,836$ 2,493,942$ Investments 11,656,675 1,209,239 12,865,914 4,201,702 Restricted cash, cash equivalents and investments Customer deposits 1,102,774 - 1,102,774 - Accounts receivable, net of allowances for uncollectible accounts 1,307,347 47,931 1,355,278 -

Total current assets 19,576,882 1,974,920 21,551,802 6,695,644 Capital Assets

Land 86,365 - 86,365 - Buildings 296,910 - 296,910 - Improvements 694,899 - 694,899 53,767 Machinery, equipment, furnishings and other 595,987 31,497 627,484 873,961 Infrastructure 19,521,715 2,986,744 22,508,459 - Construction in progress 5,204,481 - 5,204,481 -

Total capital assets 26,400,357 3,018,241 29,418,598 927,728 Less accumulated depreciation (12,854,430) (2,258,967) (15,113,397) (808,751)

Net capital assets 13,545,927 759,274 14,305,201 118,977 Total assets 33,122,809 2,734,194 35,857,003 6,814,621

LiabilitiesCurrent Liabilities Accounts payable and other liabilities 545,386 19,444 564,830 264,675 Due to other governmental units 9,764 - 9,764 - Accrued compensated absences - - - 19,337 Payable from restricted assets 1,102,774 - 1,102,774 -

Total current liabilities 1,657,924 19,444 1,677,368 284,012 Long-Term Liabilities

Accrued compensated absences 77,756 35,823 113,579 4,924 Total long-term liabilities 77,756 35,823 113,579 4,924 Total Liabilities 1,735,680 55,267 1,790,947 288,936

Net PositionNet investment in capital assets 13,545,927 759,274 14,305,201 118,977 Unrestricted 17,841,202 1,919,653 19,760,855 6,406,708

Total net position 31,387,129$ 2,678,927$ 34,066,056$ 6,525,685$

Enterprise FundsBusiness-type Activities -

See Notes to Financial Statements

28

City of North Lauderdale, Florida

Reconciliation of the Statement of Net Position - Proprietary Fund to the Statement of Net Position September 30, 2013

Total net position - Proprietary Fund Financial Statements 34,066,056$

Internal service funds are used by management to charge thecost of Vehicle Maintenance, Information Technology, andInsurance to individual funds. The portion attributable to business-type activities is reflected here and the residualassets and liabilities are included in governmental activitiesin the statement of net position. 441,717

Net position of business-type activities 34,507,773$

See Notes to Financial Statements

29

City of North Lauderdale, Florida

Statement of Revenues, Expenses and Changes in Net Position Proprietary Funds Fiscal Year Ended September 30, 2013

Major Fund InternalUtilities Nonmajor Service

Fund Fund Total FundsOperating revenues:

Charges for services:Water sales 5,434,953$ -$ 5,434,953$ -$ Sewer sales 5,898,283 - 5,898,283 - Other sales and services - 723,343 723,343 1,700,938

Total operating revenues 11,333,236 723,343 12,056,579 1,700,938

Operating expenses:Personnel 718,995 495,098 1,214,093 254,491 Other operating expenses 4,754,788 188,719 4,943,507 1,095,358 General and administrative 2,247,216 - 2,247,216 - Depreciation 463,323 67,510 530,833 86,273

Total operating expenses 8,184,322 751,327 8,935,649 1,436,122

Operating income / (loss) 3,148,914 (27,984) 3,120,930 264,816

Nonoperating revenues (expenses):Interest income 1,580 530 2,110 1,785 Miscellaneous revenue - - - 325

Total nonoperating revenues (expenses) 1,580 530 2,110 2,110

Income before contributions and transfers 3,150,494 (27,454) 3,123,040 266,926

Capital contributions 600,388 - 600,388 -

Change in net position 3,750,882 (27,454) 3,723,428 266,926

Total net position, beginning 27,636,247 2,706,381 30,342,628 6,258,759 Total net position, ending 31,387,129$ 2,678,927$ 34,066,056$ 6,525,685$

Business-type Activities -Enterprise Funds

See Notes to Financial Statements

30

City of North Lauderdale, Florida

Reconciliation of the Statement of Revenues, Expenses and Changes in Net Position Proprietary Funds to the Statement of Activities Fiscal Year Ended September 30, 2013

Change in net position - Proprietary Fund Financial Statements 3,723,428$

Internal Service Funds are used by management to charge the costs of VehicleMaintenance, Information Technology, and Insurance to individual funds. Theportion of the net revenue attributable to business-type activities is reflected here. 41,073

Change in net position of business-type activities 3,764,501$

See Notes to Financial Statements

31

City of North Lauderdale, Florida

Statement of Cash Flows Proprietary Funds Fiscal Year Ended September 30, 2013

Major Fund InternalUtilities Nonmajor Service

Fund Fund Total FundsCash Flows From Operating Activities

Receipts from customers and users 11,192,552$ 723,645$ 11,916,197$ 1,700,938$ Payments to suppliers (7,268,471) (177,764) (7,446,235) (990,872) Payments to employees (715,884) (495,099) (1,210,983) (256,312)

Net cash provided by operating activities 3,208,197 50,782 3,258,979 453,754

Cash Flows From Noncapital Financing ActivitiesMiscellaneous - - - 325

Net cash provided by (used in) noncapitaland related financing activities - - - 325

Cash Flows From Capital and Related FinancingActivities

Purchase of capital assets (152,463) - (152,463) (807) Net cash provided by (used in) capital

and related financing activities (152,463) - (152,463) (807)

Cash Flows From Investing ActivitiesSale of investments (9,715,149) (968,976) (10,684,125) (3,402,319) Purchase of investments 8,492,335 1,050,924 9,543,259 3,496,540 Interest received 1,580 530 2,110 1,785

Net cash provided by (used in) investing activities (1,221,234) 82,478 (1,138,756) 96,006

Net increase in cash and equityin pooled cash 1,834,500 133,260 1,967,760 549,278

Cash and equity in pooled cash, beginning 4,778,360 584,490 5,362,850 1,944,664

Cash and equity in pooled cash, ending 6,612,860$ 717,750$ 7,330,610$ 2,493,942$

Reconciliation to the statement of net position:Cash and equity in pooled cash 5,510,086$ 717,750$ 6,227,836$ 2,493,942$ Restricted assets, cash 1,102,774 - 1,102,774 -

6,612,860$ 717,750$ 7,330,610$ 2,493,942$

Business-type Activities -Enterprise Funds

See Notes to Financial Statements

32

City of North Lauderdale, Florida

Statement of Cash Flows Proprietary Funds Fiscal Year Ended September 30, 2013 (Continued)

Major Fund InternalUtilities Nonmajor Service

Fund Fund Total FundsReconciliation of Operating Income to Net

Cash Provided By Operating ActivitiesOperating income 3,148,914$ (27,984)$ 3,120,930$ 264,816$

Adjustments to reconcile operating income to net cash provided by operating activities: Depreciation 463,323 67,510 530,833 86,273

Changes in assets and liabilities:(Increase)/decrease in accounts receivable (45,483) 302 (45,181) - (Increase)/decrease in prepaid items - - - 135,430 (Decrease)/increase in accounts payable

and other liabilities (230,315) 10,954 (219,361) (30,944) (Decrease)/increase in retainage payable (45,915) - (45,915) - (Decrease)/increase in interfund payable 9,764 - 9,764 - (Decrease)/increase in compensated absences 3,110 - 3,110 (1,821) (Decrease)/increase in payables from

restricted assets (95,201) - (95,201) - Total adjustments 59,283 78,766 138,049 188,938 Net cash provided by (used in) operating activities 3,208,197$ 50,782$ 3,258,979$ 453,754$

Noncash investing, capital or financing items:Contribution of water and sewer improvements 600,388$ -$ -$

Business-type Activities -Enterprise Funds

See Notes to Financial Statements

33

City of North Lauderdale, Florida

Statement of Fiduciary Net Position Fiduciary Funds September 30, 2013

Police ExplorerAgency Fund

AssetsCash and equity in pooled cash 723$ Investments 1,214

Total assets 1,937$

LiabilitiesOther liabilities 1,937

Total liabilities 1,937$

See Notes to Financial Statements

34

CITY OF NORTH LAUDERDALE, FLORIDA NOTES TO FINANCIAL STATEMENTS

Note 1. Summary of Significant Accounting Policies The City of North Lauderdale, Florida (the “City”) was incorporated on July 15, 1963, under the provisions of Chapter 63-1675 Laws of Florida. The City operates under a commission/city manager form of government. The City provides the following full range of municipal services to its residents including: police and fire protection; street construction and maintenance; building, licensing and code compliance; parks and recreation facilities and activities; water, wastewater, canal maintenance, and stormwater services; public records and general administrative services. The Comprehensive Annual Financial Report (the “CAFR”) of the City includes all funds and component units. The financial statements of the City have been prepared to conform with accounting principles generally accepted in the United States of America (“GAAP”) as applicable to state and local governments. The Governmental Accounting Standards Board (“GASB”) is the accepted standard-setting body for establishing governmental accounting and financial reporting principles. Significant accounting and reporting policies and practices used by the City are described below. A. Reporting Entity The accompanying financial statements present the government and its component units, entities for which the government is considered to be financially accountable. Blended component units, although legally separate entities, are, in substance, part of the City’s operation. Each discretely presented component unit is reported in a separate column in the government-wide financial statements (see Note below for description) to emphasize that it is legally separate from the government. Blended component unit: The North Lauderdale Water Control District (the “District”) serves all the citizens of the City and is governed by a board comprised of the City’s elected five-member Commission. The rates for user charges and bond issuance authorizations, when applicable, are approved by the City Commission. The District is reported as a special revenue fund. Discretely presented component unit: The Housing Authority of the City of North Lauderdale, Inc. (the “Authority”) was created by the City in 1994 as a legally separate entity. Members of the Authority’s five member governing body are appointed by the City’s elected five-member Commission. Funding for the Authority is provided solely from the City’s General Fund. The Authority was formed to promote the increase of affordable standard housing within the City for persons of lower income. During fiscal year 2013, the Authority had no balances or activity. Accordingly, no financial statements are included in this document or available in any separate financial statements. B. Government-Wide and Fund Financial Statements

The basic financial statements include both government-wide (based on the City as a whole) and fund financial statements. The government-wide financial statements (i.e., the statement of net position and the statement of changes in net position) report information on all activities of the primary government and its component units, excluding fiduciary funds. For the most part, the effect of interfund activity, with the exception of those that are immaterial, has been eliminated from these statements. Interfund services provided and used are not eliminated in the process of consolidation. Governmental activities, which normally are supported by taxes and intergovernmental revenues, are reported separately from business-type activities, which rely to a significant extent on fees and charges for support. Likewise, the primary government is reported separately from certain legally separate component units for which the primary government is financially accountable.

CITY OF NORTH LAUDERDALE, FLORIDA NOTES TO FINANCIAL STATEMENTS

(Continued)

35

Note 1. Summary of Significant Accounting Policies (Continued) B. Government-Wide and Fund Financial Statements (Continued) The government-wide statement of activities demonstrates the degree to which the direct expenses of a given function or segment is offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function or segment. Program revenues include: 1) charges to customers or applicants who purchase, use or directly benefit from goods, services or privileges provided by a given function or segment 2) grants and contributions that are restricted to meeting the operating requirements of a particular function or segment and 3) grants and contributions that are restricted to meeting capital requirements of a particular function or segment. Taxes and other items not included among program revenues are reported instead as general revenues. The net cost (by function or business-type activity) is normally covered by general revenue (property taxes, sales taxes, franchise taxes, intergovernmental revenues, interest income, etc.). The City applies eligible expenses against available restricted resources before the use of unrestricted resources. Separate fund based financial statements are provided for governmental funds, proprietary funds and fiduciary funds. Major individual governmental funds and major individual enterprise funds are reported as separate columns in the fund financial statements. GASB Statement No. 34 sets forth minimum criteria (percentage of assets, liabilities, revenues or expenditures/expenses of either fund category for the governmental and enterprise combined or funds that management deems major) for the determination of major funds. The nonmajor funds are combined in a column in the fund financial statements. The nonmajor funds are detailed in the combining section of the statements. Internal service funds, which traditionally provide services primarily to other funds of the government, are presented in the summary form as part of the proprietary fund financial statements. Because the principal users of the internal services are the City’s governmental activities, financial statements of internal service funds are consolidated into the governmental activities and business type activities columns when presented at the government-wide level. To the extent possible, the cost of these services is reflected in the appropriate functional activity, (e.g., General Government, Public Safety, etc.). The City’s fiduciary fund is presented in the fund financial statements by type. Since by definition these assets are being held for the benefit of a third party (other local governments, individuals, pension participants, etc.) and cannot be used to address activities or obligations of the government, these funds are not incorporated into the government-wide financial statements. The City has one agency fund. The government-wide focus is more on the sustainability of the City as an entity and the change in aggregate financial position resulting from the activities of the fiscal period. The focus of the fund financial statements is on the major individual funds of the governmental and business-type categories, (by category) and the component units. Each presentation provides valuable information that can be analyzed and compared to enhance the usefulness of the information. The following major governmental funds are used by the City: General Fund – This fund is used to account for all financial transactions, except those required to be accounted for and reported in another fund. Revenue is derived primarily from property taxes, utility taxes, franchise taxes, state and federal distributions and other governmental revenue. Fire/Rescue Fund – This fund is used to account for revenues and expenditures related to the operation of the City’s fire/rescue services. These services are funded primarily through a combination of non-ad valorem special assessment revenue and transfers from the City’s General Fund.

CITY OF NORTH LAUDERDALE, FLORIDA NOTES TO FINANCIAL STATEMENTS

(Continued)

36

Note 1. Summary of Significant Accounting Policies (Continued) B. Government-Wide and Fund Financial Statements (Continued)