China's Future Structural Policy for the Coal Industry Paper Prepared for the 64 th International Forum on China Reform China’s Reform in the Next Step: Changes and Choices” Haikou, October 2008 Tim Wright White Rose East Asia Centre and School of East Asian Studies, University of Sheffield Introduction China’s immense economic success over the past thirty years has begun to transform a largely traditional into a modern economy. Anyone who has been visiting China at different times since the 1970s cannot fail to be impressed with the massive economic growth and improvement in the people’s livelihood over that period. Nevertheless, China’s economy still faces major challenges. Central to those challenges is the need to move from the previous largely extensive pattern of growth, which made heavy demands on new inputs of labour and other resources, to a more intensive pattern of growth that is much more knowledge- and skill-intensive. 1 The reform period has moved substantially in this direction in comparison with the Mao period, but many scholars still believe that China’s growth since 1978 has been excessively dependent on extensive growth patterns, especially the very high rate of investment. 2 In any case, there is broad agreement that China’s economy needs to move in the direction of intensive growth. 1 Ma Kai, Minister of the NDRC, as cited in “Pattern of growth ‘has to change’”, China Daily, 19 March 2007, available online at http://www.chinadaily.com.cn/china/2007-03/19/content_830589.htm (29 September 2008). 2 Linda Yueh, “China’s Economic Growth with WTO Accession: Is it Sustainable?”, The Royal Institute of International Affairs, Asia Working Paper, no. 1 (May 2003), pp. 6-7.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

China's Future Structural Policy for theCoal Industry

Paper Prepared for the 64th International Forum on ChinaReform

China’s Reform in the Next Step: Changes and Choices”Haikou, October 2008

Tim WrightWhite Rose East Asia Centre and School of East Asian

Studies, University of Sheffield

Introduction

China’s immense economic success over the past thirtyyears has begun to transform a largely traditional into amodern economy. Anyone who has been visiting China atdifferent times since the 1970s cannot fail to beimpressed with the massive economic growth andimprovement in the people’s livelihood over that period.

Nevertheless, China’s economy still faces majorchallenges. Central to those challenges is the need tomove from the previous largely extensive pattern ofgrowth, which made heavy demands on new inputs of labourand other resources, to a more intensive pattern ofgrowth that is much more knowledge- and skill-intensive.1

The reform period has moved substantially in thisdirection in comparison with the Mao period, but manyscholars still believe that China’s growth since 1978 hasbeen excessively dependent on extensive growth patterns,especially the very high rate of investment.2 In anycase, there is broad agreement that China’s economy needsto move in the direction of intensive growth.1 Ma Kai, Minister of the NDRC, as cited in “Pattern of growth ‘has to change’”, China Daily, 19 March 2007, available online at http://www.chinadaily.com.cn/china/2007-03/19/content_830589.htm (29September 2008).2 Linda Yueh, “China’s Economic Growth with WTO Accession: Is it Sustainable?”, The Royal Institute of International Affairs, Asia Working Paper, no. 1 (May 2003), pp. 6-7.

Voracious use of energy has been one of the mainmanifestations of extensive growth, and coal mining is anindustry that particularly illustrates that growthpattern.3 We should certainly acknowledge the massivecontribution that coal mining has made to fuellingChina’s economic growth and to improving living standardsin many mining areas, which have access to few othereconomic opportunities. However, the growth of theindustry over the past thirty, and indeed sixty, yearshas been of a type that is not sustainable in the future.4

Thus, alongside the undoubted benefits it has brought toChina, the coal industry has also caused seriousproblems. In particular, its growth has come atexcessive cost. The cost to coal mining workers is shownby the highest level of mining accidents amongsubstantial coal industries. The cost to the broaderenvironment is evident to anyone visiting coal miningareas – air and water pollution and land degradation.Finally the cost to China’s future development ismanifested in a rate of recovery of resources that wasteswell over half the reserves exploited.

It is such issues that the Chinese government aims totackle through its reforms to the structure of the coalindustry. These reforms have been on-going for asubstantial period and were foreshadowed anew in theEleventh Five Year Plan (2006-2010). The second sectionof the paper shows how these fundamental problems arelinked to the structure of the industry. Section 3 thenoutlines and evaluate some key aims as detailed in thePlan: the concentration of production on large mines, and3 See e.g. Li Renzhi 李李李, “Shuli kexue fazhanguan – cujin meitan jingji zengzhang fangshi de genbenxing zhuanbian” 李李李李李李李 李李李李李李李李李李李李李李李李, Meitan gongcheng 李李李李2004, no. 11: 40-5 (accessed through CNKI).4 The standard and very informative account of the development of thecoal industry since 1949 has been Elspeth Thomson, The Chinese Coal Industry: An Economic History (London: RoutledgeCurzon, 2003). For its history before 1949 see Tim Wright, Coal Mining in China’s Economy and Society, 1895-1937 (Cambridge: Cambridge University Press, 1984), of which the Chinese version, translated by Professor Ding Changqing 李李李 of the Nankai Institute of Economics, is 1895-1937 Zhongguo jingji he shehui zhong de meikuang ye 1895-1937 李李李李李李李李李李李李 (Beijing: Dongfang chuban she, 1991).

2

the elimination of “backward productive forces”;encouragement to large mines to form combines, andcontinued restructuring of small mines; increasedmechanisation and improved safety; and measures toimprove the environmental record of the industry.5

However, the issues involved are far from simplytechnical, and major questions of political economy willconstrain the government’s ability successfully toimplement these policies. The last section of the paperwill discuss some of these questions, specifically themacroeconomic context of restructuring, the question ofuneven regional development, and the issue of rent-seeking and rent capture.

Key problem areas in the current structure of the coalindustry

The structure of the Chinese coal industry is by no meansstatic, and may be changing in the direction in which thegovernment is trying to move. Nevertheless, thegovernment believes with reason that major structuralproblems currently exist in the industry and requireaddressing. Many of these originate in excessivefragmentation and the consequent small average size ofunit of operation. These phenomena then cause the deeperproblems of excessive competition, wasteful use ofresources, poor labour conditions, low technical levelsand serious environmental damage.

The basic problem leading to fragmentation is thatbarriers to entry into the industry have been too low andexit barriers too high. Thus, for whatever reason, localauthorities in China have been unable (or unwilling) toprevent the opening of new small mines in their areas.For decades, large numbers of unlicensed mines have beenopened continuously across China. Nor have theauthorities been able to force existing mines to exit the

5 “‘Shiyiwu’ meitan hangye jiegou tiaozheng de zhuyao mubiao” “李 李一”李李李李李李李李李李李李李, Jingji ribao 李李李李, 9 May 2006, available online at http://www.rz.gov.cn/qysw/swzx/20060509083058.htm (29 September 2008).

3

industry, despite many campaigns to close small ordangerous mines. Social obligations have also made itdifficult even for large mines that are close toexhausting their resources to exit the industry. Thus inrelation to both entry and exit and at varying scales ofoperation, the outcome has been excessive numbers ofenterprises in operation and an excessive fragmentationof the industry.

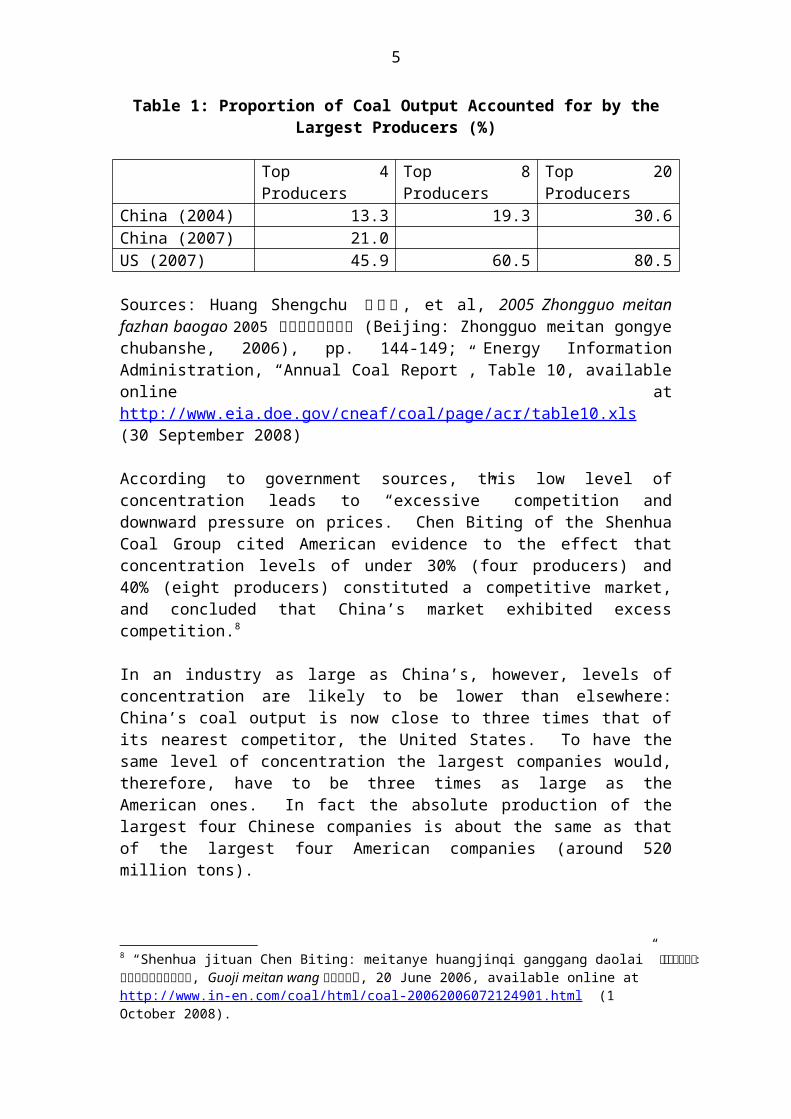

According to official figures, the Chinese coal industryconsists of 15,000 separate units of production, thoughthe real number may be much higher. While this is downfrom over 87,000 a decade ago, the government stillbelieves the number is excessive and the average size toosmall. These 15,000 mines produce about 2.5 billion tonsof coal (suggesting an average size of 167,000 tons). Bycontrast in the United States 1358 mines produced 1.145billion tons in 2007 (average 843,000 tons), and inAustralia 118 mines produced 405 million tons in 2006(average 3.4 million tons).6

At the “top end” of the industry several massiveenterprises each produce over fifty millions of tons ofcoal, though the average physical unit of operation ismuch smaller. By 2007, 34 companies produced over 10million tons of coal each, making up a total of 45% ofthe market.7 These giants, however, account for a smallerpart of the total market than their counterparts in othercountries. Common measures of industry concentration arethe proportion of the market accounted for by the topfour or top eight enterprises, and by these measuresChina’s coal sector is excessively fragmented.

6 Energy Information Administration, “Annual Coal Report”, Table 1, available online at http://www.eia.doe.gov/cneaf/coal/page/acr/table1.xls (8 October 2008); Coal Services Pty Ltd, Annual Report, 2006-2007, p. 14, available online at http://coalservices.com.au/publications/Annual%20Report%202006-2007.pdf (1 October 2008)7 “Zhongguo 2007 nian yuanmei chanliang 25.23 yi dun” 李李 2007 李李李李李 25.23李李, Caijing 李李, 29 February 2008, available online at http://www.caijing.com.cn/2008-02-29/100050210.html (1 October 2008).

4

Table 1: Proportion of Coal Output Accounted for by theLargest Producers (%)

Top 4Producers

Top 8Producers

Top 20Producers

China (2004) 13.3 19.3 30.6China (2007) 21.0US (2007) 45.9 60.5 80.5

Sources: Huang Shengchu 李 李 李 , et al, 2005 Zhongguo meitanfazhan baogao 2005 李李李李李李李李 (Beijing: Zhongguo meitan gongyechubanshe, 2006), pp. 144-149; Energy InformationAdministration, “Annual Coal Report”, Table 10, availableonline athttp://www.eia.doe.gov/cneaf/coal/page/acr/table10.xls(30 September 2008)

According to government sources, this low level ofconcentration leads to “excessive” competition anddownward pressure on prices. Chen Biting of the ShenhuaCoal Group cited American evidence to the effect thatconcentration levels of under 30% (four producers) and40% (eight producers) constituted a competitive market,and concluded that China’s market exhibited excesscompetition.8

In an industry as large as China’s, however, levels ofconcentration are likely to be lower than elsewhere:China’s coal output is now close to three times that ofits nearest competitor, the United States. To have thesame level of concentration the largest companies would,therefore, have to be three times as large as theAmerican ones. In fact the absolute production of thelargest four Chinese companies is about the same as thatof the largest four American companies (around 520million tons).

8 “Shenhua jituan Chen Biting: meitanye huangjinqi ganggang daolai” 李李李李李李李:李李李李李李李李李李, Guoji meitan wang 李李李李李, 20 June 2006, available online at http://www.in-en.com/coal/html/coal-20062006072124901.html (1 October 2008).

5

The lack of concentration of the industry is not,therefore, the main problem. Rather, the problem is thatlarge numbers of mines continue to operate at too small ascale to use the best technology, whether from the pointof view of the quality of the coal, recovery rates,worker safety, or environmental protection.

Thus the still very substantial small mine sector, whicheven now contributes over one third of total output, isthe source of the most serious structural problems.9 Thelow rate of resource recovery, an issue for coal miningas a whole, threatens the industry’s future and leadssome observers to predict a rapid decline in output.10 Inthe United States average recovery rates of undisturbedcoal reserves are just over 80%,11 but those in China aremuch lower: according to one scholar as low as 30%nationally and only 15% for some small mines in difficultcircumstances.12 Nevertheless this comparison is toounfavourable to China: most US mines are open-cast mines,where rates of recovery are much higher than inunderground mines, and even in the US recovery rates fromunderground mines can be as low as 40%, though theaverage is close to 60%.13

Similarly the safety record of small mines isconsistently many times worse than that of large mines.At least up to the early 2000s, the fatality rate evenfor large mines was far higher than that elsewhere, and9 In most statistical; sources, this sector is still known as the Township and Village Coal Mine (TVE) sector, even though since the 1990s many mines have in fact been privately operated.10 See for example “Richard Heinberg's MuseLetter: Coal in China”, which cites an article suggesting that China’s coal output will peak in 2029 and then decline very rapidly. Available online at http://globalpublicmedia.com/museletter_coal_in_china (1 October 2008).11 Table 14 in Energy Information Administration, “Coal Reserves Current and Back Issues”, available online at http://www.eia.doe.gov/cneaf/coal/reserves/table14_06.xls (29 September 2008).12 Huang, 2005 Zhongguo meitan fazhan baogao, p. 55.13 Table 17 in Energy Information Administration, “Coal Reserves Current and Back Issues”, available online at http://www.eia.doe.gov/cneaf/coal/reserves/table17_06.xls (29 September 2008).

6

increasingly constituted an international embarrassmentfor the Chinese leadership. Throughout the 1990s, evenlarge state mines in China were over twice as dangerousas their counterparts in India, and substantially worsethan British mines a quarter of a century earlier.14

Almost by definition the largest disasters take place inlarge mines – and there have been many of them, mostnotably in the horrific year of 2005. However, the day-to-day toll from small mines is much worse than that ofthe large mines. Thus between 1997 and 2007, the averagedeath rate per million tons of production was 0.95 forkey state mines, 3.10 for local state mines, but as highas 7.31 for the small mine (TVE) sector. The TVE ratewas therefore over seven times that of the large statemines.

Again there is a low level of mechanisation in Chinesemines in general, and it is lower the smaller the scaleof the mine. In the United States, Germany and otherdeveloped countries, all coal is cut mechanically, but inChina even in the key mines the proportion was only justunder 75% at the beginning of the 2000s. The smallermines were basically unmechanised, leading to a nationalproportion across the sectors of 30%.15 One implicationof this was that large numbers of miners work undergroundand are therefore vulnerable to safety lapses.

Finally, coal mining everywhere creates problems for theenvironment, whatever the scale of mine. But thedevastation wrought by China’s small mines on their localecologies is increasingly posing a threat both to thehealth of the people and to other aspects of economicdevelopment. This is partly because of discontinuities

14 See for example Tim Wright, "The Political Economy of Coal Mine Disasters in China: Your Rice Bowl or Your Life", China Quarterly, 179 (September 2004): 631-632.15 2006 Zhongguo chanye fazhan baogao – zhizaoye de shichang jiegou, xingwei yu jixiao 2006 李李李李李李李李—李李李李李李李李李李李李李, (Shanghai: Shanghai caijing daxue chubanshe, 2006), p. 111; mechanisation in large mines had increased to 81.5% in 2003, see “Guoyou zhongdian meikuang caijuegong zhuangkuang diaocha” 李李李李李李李李李李李李李, available online at http://www.3ljg.ik8.com/science/coal/caijuegong.htm (8 October 2008).

7

in costs of environmental protection. Many of themeasures necessary to preserve local environments, suchas the cleaning of water used in the mines, are simplynot economic at the scale at which many small minesoperate.16

Restructuring policies

None of these problems are new, and over several decadesthe government has launched a number of policies toaddress them. Recently, the Eleventh Five Year Plan hasspecified a set of targets and policies.17 Thefundamental thrust is to move towards a more intensivegrowth pattern by encouraging large-scale production andeliminating the small-scale mines. This would lead to amore ordered market, higher quality product, moreadvanced average level of technology, better workersafety and less environmental damage.

The key targets include: completing the reform and reorganisation of small

mines; reducing their numbers to 10,000 and theiroutput to 27% of a total of 2.6 billion tons;

raising entry barriers for new mines, limiting theminimum size of new mine to 300,000 tons a year in themain coal producing provinces, 150,000 in the rest ofnorth China and 90,000 tons elsewhere;

95% level of mechanisation of operations for largemines, 80% for medium sized mines and at least 30% forsmall mines.

conservation of coal resources in the long-terminterests of China’s energy security; raising therecovery rate to an average of over 40% in the periodof the Plan;

16 Chen Jiabin 李李李, “Woguo meitan ziyuan huanbao zhengce yu xiangguan chanye fazhan qianjing” 李李李李李李李李李李李李李李李李李李李, Meitan jingji yanjiu 李李李李李李, 2003, no. 4, pp. 13, 21 (accessed through CNKI).17 Unless otherwise indicated the following paragraphs are taken from the abstract of the Plan in relation to coal, “Meitan gongye fazhan ‘shiyi wu’ guihua (zhaoyao)” 李李李李李李“李 李”李李一 (李李), available online at http://www.fdi.gov.cn/pub/FDI/zgjj/hyzk/zzy/mtgy/t20070124_73331.htm (1 October 2008)

8

reduction in the rate of coal mine fatalities by 25% in2010 as compared with 2005;

on the environmental front, a reduction inenvironmental degradation, and the achievement of atleast 75% recycling of coal slurry and gangue, and 50%or above methane drainage and utilisation, as well assuccessful addressing of subsidence.

In pursuit of these aims, the National Development andReform Commission has introduced a series of specificmeasures to strengthen the administration of theindustry: strengthening planning to balance supply and demand,

and controlling the number of mining licences to thatend;

strengthening the administration of mining licences toensure that actual operations are of a scale consistentwith the mining license;

raising entry barriers to ensure sustainabledevelopment, and establishing standards for keyvariables such as recovery rates;

encouraging large-scale coal combines, and eliminatingoutdated production capacity;

planning for and controlling the level of productioncapacity;

strengthening the responsibility of mine managers forworker safety;

strengthening environmental management, insisting thatnew projects must conduct an environmental impact studyand implementing a “polluter pays” principle.

The Eleventh Five Year Plan is over two years fromcompletion, and in any case several of the targets (forexample recovery rates) are long-term and difficult tojudge from short-term statistics (though in the case ofrecovery rates progress towards this aim is being helpedby rising coal prices, which make it more economic toextract the maximum amount of coal from givenresources18). The data allow us, however, to say

18 Xinhua, “Woguo meitan ziyuan huicailű wenti diaocha” 李李李李李李李李李李李李李,Xinhua wang 李李李, 6 November 2007, available online at http://news.xinhuanet.com/newscenter/2007-11/06/content_7019341.htm

9

something about progress in two areas: the scale ofenterprise; and the improvement in work safety.

Scale of enterprise and structure of industry

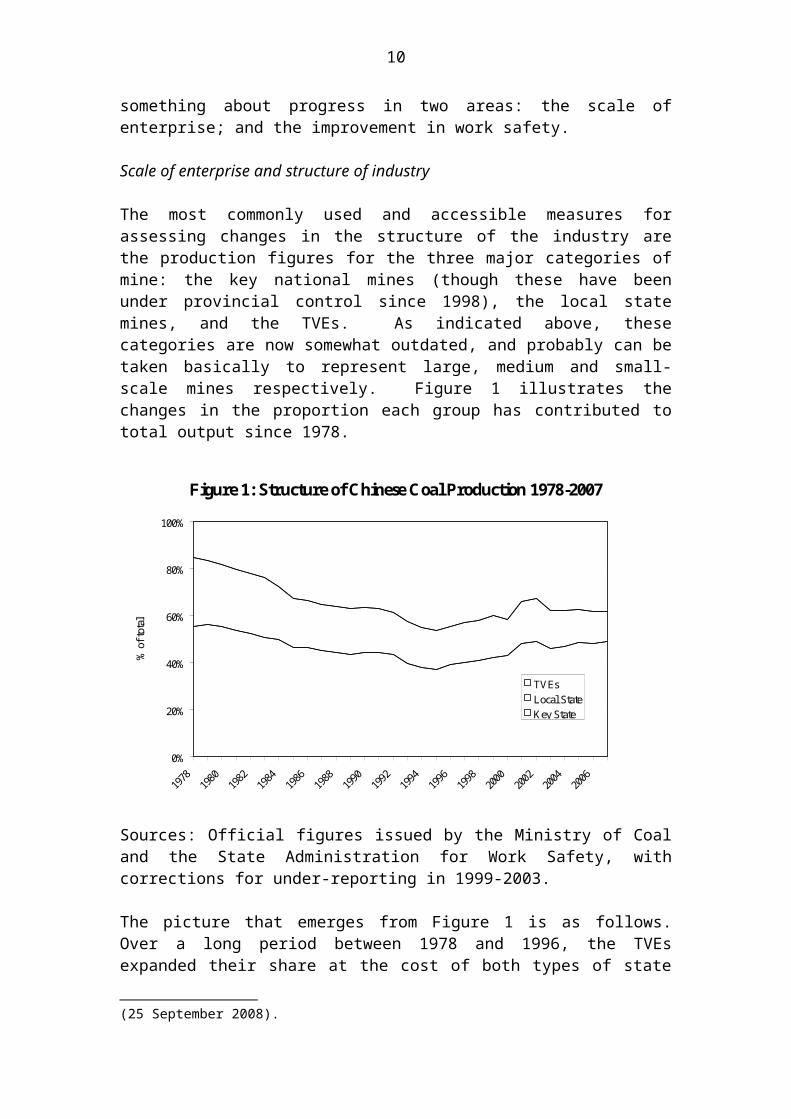

The most commonly used and accessible measures forassessing changes in the structure of the industry arethe production figures for the three major categories ofmine: the key national mines (though these have beenunder provincial control since 1998), the local statemines, and the TVEs. As indicated above, thesecategories are now somewhat outdated, and probably can betaken basically to represent large, medium and small-scale mines respectively. Figure 1 illustrates thechanges in the proportion each group has contributed tototal output since 1978.

Figure 1: Structure of Chinese Coal Production 1978-2007

0%

20%

40%

60%

80%

100%

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

% of total

TVEs Local StateKey State

Sources: Official figures issued by the Ministry of Coaland the State Administration for Work Safety, withcorrections for under-reporting in 1999-2003.

The picture that emerges from Figure 1 is as follows.Over a long period between 1978 and 1996, the TVEsexpanded their share at the cost of both types of state

(25 September 2008).

10

mine. There was then a correction in favour of the keystate mines between 1996 and 2001. Finally, over thelast five years the share of the small mines has beensubstantial (over 35%) and quite stable; the share of thelarge mines is somewhat larger than in the mid 1990s andis still growing slightly, but at the expense of localstate mines.

Of course, this broad picture is quite consistent with anincrease in scale and concentration within any of the majorcategories, and there is strong reason to believe thatthis has happened. There has certainly been a tendencytowards concentration, with an increase in the share ofthe four largest enterprises from 16% to 18% and the topeight from 23% to 25% just between 2005 and 2006.19 Thisconcentration has taken the form of the growth of largecoal mining combines among the largest mines. This ispart of a broader attempt by the Chinese government toencourage the emergence of large companies that arecompetitive on a global scale. The most influentialanalysis of this is by Peter Nolan, whose chapter on coalfocuses on the Shenhua Coal Group, which is now by farthe largest in China. However Shenhua has advantagesdenied to most of its Chinese competitors, in that mostof its mines are both new and open-cast, which enables itto avoid the costs of underground operation and ofdealing with a previous historical legacy of coalmining.20

Perhaps more importantly the government has repeatedlyclaimed that the average size of mines in the small minesector has increased substantially. Official figuressuggest that the proportion of small mine (TVE) outputaccounted for by mines producing less than 30,000 tons ayear fell from over 75% in 1995 to 50% in 2001.21 My

19 Pan Weier, “2006 nian meitan jingji yunxing pingxi” 2006 李李李李李李李李李,Jingji yanjiu cankao 李李李李李李, 2007, no 26, p. 39 (accessed through CNKI).20 Peter Nolan, China and the Global Business Revolution (Houndmills: Palgrave,2001), ch. 10.21 Ye Qing 李李 and Zhang Baoming 李李李, eds, Zhongguo xiangzhen meikuang 李李李李李李 (Beijing: Meitan Gongye Chubanshe, 1998), p. 57; 2004 Zhongguo minying jingji chanye fazhan baogao 2004 李李李李李李李李李李李李 (Beijing: Jixie gongye chubanshe, 2004), p. 193; “Zhongguo yue you 1.6 wanchu meikuang,

11

discussions with coal mine officials in 2004 alsorevealed a consistent picture where they said that thesmallest mines were being closed down, and minimum scalesof between 30,000 tons a year and 100,000 tons a yearwere being enforced. Total numbers of mines declinedfrom around 73,000 in the mid to late 1990s to 24,000 in2004 and 15,000 now.22 Given the increase in coal output,this could only be consistent with an increase in thescale of individual mines.

Certainly the official figures and claims do suggestsuccess, but past experience suggests caution. Repeatedgovernment attempts to close down small mines over thepast ten years have created incentives for localgovernments to conceal their operation. The mostconcerted attempt to control the small mines came withthe “Close the Pits and Reduce Production” campaign in1999-2000. At the time this was claimed to be a greatsuccess, with a very substantial drop both in the numberof mines and in small mine output, which official figuresshowed to have fallen from 615 million to 264 milliontons between 1996 and 2001. The official statistics inThe Statistical Yearbook of China still claim these achievements,but there has long been considerable scepticism as towhether this reflected the actual situation. Because thecareers and salaries of officials depended on thereduction of output, they reported reduction of output.But informed estimates suggest that perhaps 250 milliontons of output per year from small unregistered (andpossibly from some registered) mines went unrecorded inthe statistics in this period.23

xiaomeikuang yue zhan 90%”李李李李 1.6 李李李李 李李李李李 90 %, Xinhua wang 李李李, 9 July 2008, available online at http://www.china5e.com/news/meitan/200807/200807090036.html (3

October 2008); estimates for the number of mines differ substantially (one figure for the 1990s was 87,000), and should not be taken as at all exact, but just as indicating an order of magnitude.22 Wang Shuhe 李李李, “Jinyibu gaizao zhengdun he guifan xiaoxing meikuang” 李 李李李李李李李李李李李李一 , p. 132 in Cujin meitan gongye jiankang fazhan 李李李李李李李李李李 (Beijing: Meitan gongye chubanshe, 2005).23 For a study based on satellite monitoring of emissions, see HajimeAkimoto et al, “Verification of energy consumption in China during

12

Since 2001, although output from the small mine sectorhas increased, there have been continuing reports ofclosures of small inefficient mines, and of declines inthe number of mines operating. Between mid 2005 and mid2006, 5931 mines with a total capacity of 110 milliontons were closed down.24 However, in many case minescontinue operating (often at night), or reopen. Accountsof successful closing of mines and increases in scalemust be looked at sceptically. One example is that ofNayong County (Guizhou). According to the provincialyearbook, Nayong closed almost 400 mines in 1997,reducing the total number to 200. By 2001, only 88 mineswere left, all with a capacity of over the then standardof 30,000 tons.25 However, we then read that 1629unlicensed mines were closed down in the county in 2003.26

It is not clear, therefore, how far reports of reducednumbers of mines reflect reality, and how far they aremerely the result of officials telling the governmentwhat it wants to hear. Probably the number of mines hasfallen but not by as much as the government claims.

Work safety

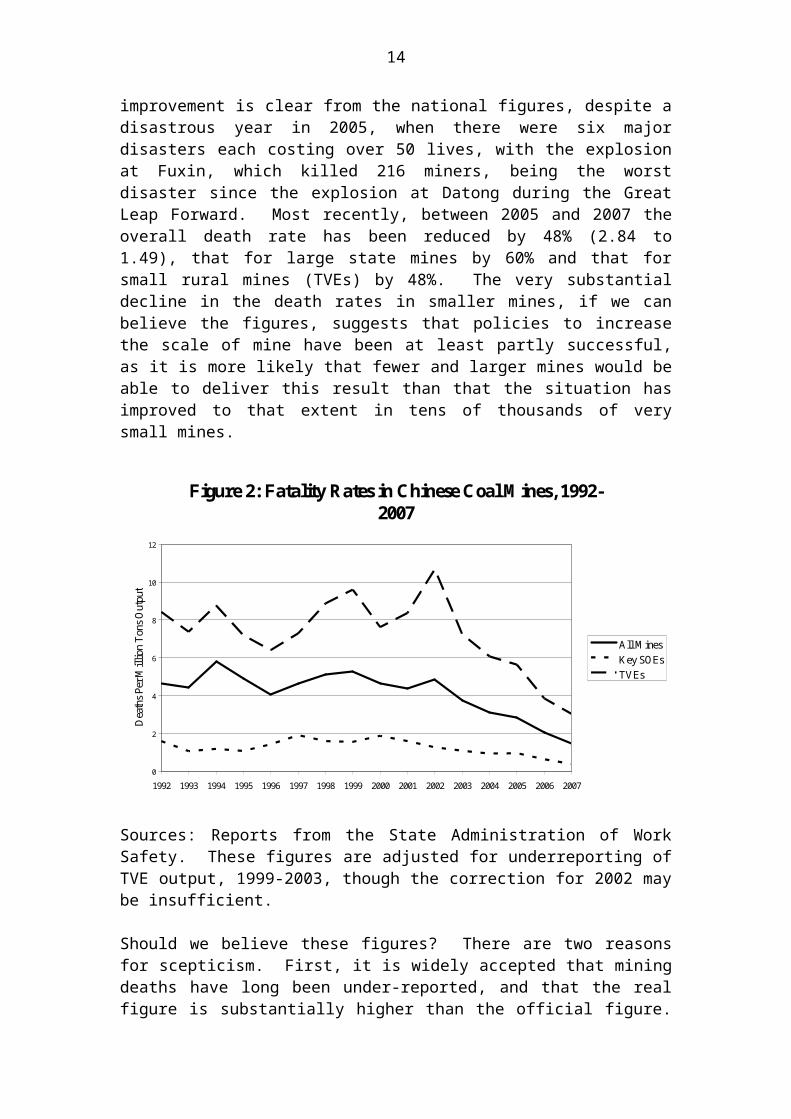

In the area of mine safety, the targets set in the FiveYear Plan have, according to the data summarized inFigure 2, been easily surpassed. A major reduction inthe death rate per million tons began from around 2001-2or possibly earlier. Initially the number of deaths wasstable at around 6000, while output increased rapidly,but total deaths began to fall from 2004. This

1996-2003 by using satellite observational data”, Atmospheric Environment40 (2006): 7663-7667; for a Chinese study see Guo Yuntao 李李李, Shichangyu lixing 李李李李李 (Beijing: Jingji Ribao Chubanshe, 2003), p. 38; see alsoTim Wright, “State Capacity in Contemporary China: ‘Closing the Pitsand Reducing Coal Production’”, Journal of Contemporary China, vol 16, no.51 (May 2007): 173-194.24 Pan, “2006 nian meitan jingji yunxing pingxi”, p. 36.25 Guizhou nianjian 李李李李, 1998, p. 321, 1999, p. 301, and 2002, p. 528.26 ‘Guizhou Nayong guanbi xiao meiyao 1629 ge’ 李李李李李李李李李李李 1629 李, Guizhou ribao 李李李李, 11 March 2004, http://www.china5e.com/news/meitan/200403/200403110083.html (15 November 2004).

13

improvement is clear from the national figures, despite adisastrous year in 2005, when there were six majordisasters each costing over 50 lives, with the explosionat Fuxin, which killed 216 miners, being the worstdisaster since the explosion at Datong during the GreatLeap Forward. Most recently, between 2005 and 2007 theoverall death rate has been reduced by 48% (2.84 to1.49), that for large state mines by 60% and that forsmall rural mines (TVEs) by 48%. The very substantialdecline in the death rates in smaller mines, if we canbelieve the figures, suggests that policies to increasethe scale of mine have been at least partly successful,as it is more likely that fewer and larger mines would beable to deliver this result than that the situation hasimproved to that extent in tens of thousands of verysmall mines.

Figure 2: Fatality Rates in Chinese Coal M ines, 1992-2007

0

2

4

6

8

10

12

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Death

s Per Million

Tons O

utput

All M inesKey SOEsTVEs

Sources: Reports from the State Administration of WorkSafety. These figures are adjusted for underreporting ofTVE output, 1999-2003, though the correction for 2002 maybe insufficient.

Should we believe these figures? There are two reasonsfor scepticism. First, it is widely accepted that miningdeaths have long been under-reported, and that the realfigure is substantially higher than the official figure.

14

However, there is no real evidence for the China LabourBulletin estimate for the early 2000s of 20,000 per year.27

Nevertheless a constant rate of under-reporting would notinvalidate the trend. So, we must examine reasons whyunder-reporting may have increased. Thus the incentivesto conceal accidents do appear to have increased becauseof the regulation raising the amount of compensation tobe paid for a dead miner to 200,000 yuan (this was firstintroduced in Shanxi and later extended to other areas).28

Although this certainly provides an incentive to improvesafety, it also means that, if an accident does happen,there are greater incentives for small mines to avoidreporting it. The leading Chinese observer ofcontemporary coal mining trends stresses the degree towhich under-reporting is still a problem. He evensuggests that more small accidents are concealed than arereported.29 Even major disasters, such as that whichkilled 30 miners in Lijiawa 李李李 in Yuxian 李李 Hebei in July2008, can be concealed at least for a time.30 So it ispossible that the official figures conceal a worsereality.

However, there are countervailing forces. In particular,the increased vigilance of the investigative press maynow make it more difficult to conceal deaths (though thatis probably true mainly in relation to the more serious

27 China Labour Bulletin, “Coal Mining in China, Introduction”, 28 February 2000, available online at http://www.clb.org.hk/en/node/1198(30 September 2008).28 Xinhua, “Shanxi guiding – meikuang shigu siwang peichangjin bu de diyu 20 wan” 李 李李李李李李李李李李李李李李李李西: 20 李, available online at http://www.china5e.com/news/meitan/200412/200412170252.html (30 September 2008); Xinhua wang, “Guojia anjianju zancheng meikuang shigu peichang biaozhun bu di yu 20 wan” 李李李李李李李李李李李李李李李李李李 20 李李, available online at http://www.china5e.com/news/meitan/200504/200504060022.html (30 September 2008).29 Pan Weier 李李李, “2007 nian meikuang anquan zhuangkuang pingxi” 2007 李李李李李李李李李, Meitan jingji yanjiu 李李李李李李 2008, no. 4 (April 2008): 7 (accessed through CNKI).30 Xinhua, “Hebei Yuxian siwang 30duo ren kuangnan bei manbao, 20yu ganbu bei chuli” 李李李李李李 30 李李李李李李李 20 李李李李李李, Xinhua wang, 8 October 2008, available online at http://www.china5e.com/news/meitan/200810/200810080038.html (9 October 2008).

15

disasters). Taking into account the factors tending inboth directions, it remains very difficult to believethat increased under-reporting accounts for the whole ofthe decline in the official death rates. Even if theofficial figures overstate the case, it seems certainthat the industry has registered substantial achievementsin improving safety over the past five years.

Constraints on implementation

The issues addressed by the government’s policies are,however, far from merely technical, but have wide-rangingimplications for the interests of many groups in society.If we wish to understand the likely future success of thepolicies, it is not enough just to look at the policiesthemselves or even the administrative structureresponsible for implementing them. Social forces whoseinterests might be threatened by the policies mightconstrain the ability of the government to implementthem. The issues must therefore be seen in a broadereconomic, geographical and administrative context.

Macroeconomic context

From an economic point of view, booming demand and risingprices create incentives for many areas and most kinds ofmine to expand production beyond the limits set bygovernment policies. At the time of the announcement ofthe Eleventh Five Year Plan policies in 2006, officialsargued that excess capacity and potential oversupply wasthreatening prices and profits.31 The argument was that,because of the structural problems outlined above, theindustry was developing excess capacity, supply wasexceeding demand, and consequently stocks were rising andprices depressed. It is far from clear that events have

31 “Jiakuai meitan hangye jiegou tiaozheng ying dui channeng guosheng de zhidao yijian” 李李李李李李李李李李李李李李李李李李李李李, 10 April 2006, available online at http://www.mep.gov.cn/law/gz/bmhb/gwygf/200604/t20060410_77849.htm# (30 September 2008); “Guojia fazhan gaige wei you guan fuzeren jiu jiakuai meitan hangye jiegou tiaozheng da jizhe wen” 李李李李李李李李李李李李李李李李李李李李李李李李李李李, 28 April 2006, available online at www.ndrc.gov.cn/xwfb/t20060428_67750.htm (24 September 2008).

16

borne out those expectations. In fact there appears tohave been increasing pressure on coal supplies throughout2007 into early 2008. Part of this reflected theinadequacy of the transport system, but neverthelessthere seems to be little doubt that overall coal supplieswere short. As a result the price of coal continued torise. Over the past several years there have beeninnumerable press reports of very steep rises in coalprices.32 More long-term and academic analyses, however,generally give a less dramatic picture. According to oneleading observer average market prices of coal increasedby 7.6% in 2007, after being more or less stable in2006.33 It is, however, clear that prices are not fallingas they were at the very end of the 1990s.

The shortage of coal has caused particular difficultiesfor the electric power industry. For some years thegovernment has attempted to control the price of coalsold for electricity generation, because retailelectricity prices are controlled, and in order to holddown inflation. Consequently this price is around 30%lower than that of coal sold on the open market.34 Butthe mines are reluctant to supply coal to power stationsat such a low price. So lack of fuel has forced powercompanies to implement the sort of power cuts that hadapparently disappeared from Chinese cities after the late1990s.35 These issues came to a head in early spring 2008with the massive problems caused by the storms in southChina.

32 See for example recently “Meitan hangye: guoneiwai meitan jiage chuang xin gao she shouyi” 李李李李 李李李李李李李李李李李李李:, Guoxin zhengquan 李李李李, 19 May 2008, available online in at http://www.china5e.com/news/meitan/200805/200805190038.html (3 October 2008), which reports a 20% rise in coal prices just in the first four months of 2008.33 Pan Weier, “2007 nian meitan jingji yunxing pingxi” 2007 李李李李李李李李李, Zhongguo nengyuan 李李李李2008, no. 4, p. 46 (accessed through CNKI).34 Ibid.35 “Shanxi dianchang: zuo zai meiduishang, wei shenmo ye naoqili ‘meihuang’?”李 李李李 李李李李李西: 李李李李李李李“李李”, Xinhua wang, 18 July 2008, available online at http://www.china5e.com/news/meitan/200807/200807180073.html(3 October 2008).

17

Therefore the urgent need to increase coal supplies hasconflicted with some of the aims of restructuring, inparticular eliminating many of the so-called “backward”small mines. The authorities seem to have adopted anambivalent response to the booming demand in relation tothe small mine sector. On the one hand, official policyhas been to promote the reopening of smaller mines oncethey had been reorganised according to government standards.36 This,they hoped, would help to increase supplies. On theother hand officials repeatedly stated that the crisis inthe electric power industry neither required norjustified the reopening of small mines without suchreorganisation. They denied that the closure of smallmines reduced coal supply, using the somewhat oddargument that the new capacity of reopened small mineswas greater than that of the mines closed down (this maybe true but does not contradict the fact that, in theabsence of closures, total output and capacity would havebeen higher).37 In fact, in a situation of booming demandand high prices, one should expect that coal owners andlocal authorities with access to resources that could beexploited by small mines would take all opportunities,whether legal or not, to open such mines.

Thus the success of future policies of restructuringpartly depends on the overall macroeconomic situation.To some extent, the slowdown in the world economy, whichis likely at least to have some effect on China, mayprovide an opportunity for further restructuring in thecoal industry. Certainly two major earlier reforms wereintroduced in times of economic downturn. In the early1990s most coal prices were successfully deregulated at atime of slower growth of demand. Later, any success

36 See for instance, “Meijia zai chuang xingao, Fagaiwei jiasu xiaomeikuang fuchan yanshou” 李李李李李李 李李李李李李李李李李李李, Shanghai zhengquan bao 李李李李李, 27 May 2008, available online at http://www.china5e.com/news/meitan/200805/200805270140.html (1 October 2008).37 See “Guojia anjian zongju mingque biaoshi dianmei jinzhang yu guanbi xiao meikuang wu guan” 李李李李李李李李李李李李李李李李李李李李李李, Gongren ribao 李李李李, 3 February 2008, available online at http://www.china5e.com/news/meitan/200802/200802030181.html (3 October 2008).

18

achieved by the “close the pits” policy of 2000 wasprobably at least in part the result of the relativelydepressed state of the economy at the time, when coalproduction was barely if at all profitable. As demandand prices recovered in the early 2000s, the incentivesfacing local officials, mine operators and populationsagain fell more on the side of expansion. So long asbreakneck growth continues in a way that increases thedemand for energy, it is unlikely that policies torestructure the small mines will be able to overcome theincentives for operators at the local level to makeprofits from expanded coal production.

Uneven development

That leads to a second major constraint on theimplementation of the restructuring plans: unevenregional development in China. The overall context ofthe restructuring is the move from extensive to intensivegrowth, and it is clear that some areas of the countryare more “ready” for this move than others. Thus broadlythe coastal areas are at a level of per capita income, aswell as a level of development of human capital andinfrastructure, where they are ready to move towards amore advanced stage of economic development. However,these preconditions do not yet exist to the same extentin many areas of central and western China. Coalresources are concentrated in these central and westernareas, and therefore to some extent the restructuringpolicies are being implemented in areas where they arenot fully appropriate.

It is likely (though not entirely or unambiguously true)that the restructuring policies, especially as aimed atthe small mines, will be more successful in the coastalareas where there is more educated public opinion, ahigher level of human capital in the governmentadministration, higher levels of per capita income, and alabour force with better alternatives than to risk theirlives in dangerous mining enterprises.38 On the other

38 Philip Andrews-Speed et al, ‘A Framework for Policy Formulation forSmall-Scale Mines: The Case of Coal in China’, Natural Resources Forum,

19

hand, in many central and western areas increasingincomes and economic diversification have not yet reachedthe stage where the population has better alternativesthan coal as a means of improving their lives. In suchareas threats to small coal mines, however much in thebroader public interest, are perceived, not withoutreason, to be threats to local prosperity and employment.In part, therefore, the struggle over restructuringreflects a struggle by different interests to appropriaterents to themselves at the cost of others. In thebroadest sense, the efforts by the coal bureaucracy toimplement restructuring, in as far as it is aimed at thesmall mines, stands to benefit the large mines and theirworkers (by reducing supply and thence raising – ormaintaining – prices). On the other hand, rural areaswill lose income and employment. Those losing out willinclude not only “black-hearted” coal owners, anddishonest local officials, but also the broaderpopulation in areas of small mine activities who dependfor their livelihoods on employment in the mines or insubsidiary services.

Once again the success of restructuring policies dependson the broader economic and policy context. They aremost likely to be successful in conjunction with policiesof regional development that create alternative sourcesof income for areas that might lose their earnings fromcoal mining.

Regulation and rent seeking

Increased regulation is inevitably required to implementthe restructuring policies. But this carries with itincreased opportunities for “rent seeking” and forcorruption on the part of the officials responsible forimplementation. Regulation creates rents in the form ofhigher profits from coal than would be the case if entryinto the industry was freer. This creates opportunitiesfor the officials in charge – specifically of regulatingentry into the industry – to appropriate part of theprofits of potential (or existing) mines. In the Chinese

26.1 (February 2002): 45-54.

20

press this is known as “rent-seeking” (though it mightbetter be described as “rent capture”).39

“Rent capture” denotes a process whereby individualofficials, particularly but not only in rural areas, arebribed to disregard the requirements for entry into theindustry and to allow mines that do not meet the officialrequirements to continue in operation. The bribes mightbe in the form of cash or of shares in the enterpriseThis creates a nexus of interests between local and coalsector officials on the one hand and coal mine owners onthe other that is known as “guanmei goujie 李 李 李 李 ” (thephenomenon more broadly is known as “guanshang goujie 李李李李”).40

The government faces insoluble problems in this respect.Administrative regulation is necessary and indispensiblefor the control of coal mining in the social interest.It is difficult to imagine the maintenance of appropriatehigh barriers to entry into the industry other than bygovernment regulation through the issue of licences.Indeed this is the pattern in mining industries aroundthe world. It does, however, mean that there is anunavoidable space for rent capture on the part of localand mining officials. Indeed it is a recognised trendfor opportunities for rent capture to increase the morerigorously the government tries to control small mines.41

There is therefore a need to control the officials incharge of the licences. No society has managed to handlethis question entirely successfully, but a strong pressand a strong civil society would contribute to overcomingit, as far as it can be overcome.

39 See Tim Wright, “Rents and Rent Seeking in China’s Coal Industry”, pp. 98-116 in Tak-wing Ngo, ed, Rent Seeking in China (London: Routledge, 2008).40 Yan Yan 李李, “2005 nian fanfu changlian shi da liangdian” 2005 李李李李李李李李李, Juece tansuo 李李李李, no. 1, 2006, p. 31 (accessed through CNKI).41 See Zhongguo meijiao shuzi jiaoyi shichang 李李李李李李李李李李, “Pojie Guizhou guanmei goujie ‘tie sanjiao’” 李李李李李李李李"李李李", 19 July 2007, available online at http://www.china5e.com/news/meitan/200707/200707190132.html (accessed18 December 2007) for Zunyi 李李 in Guizhou.

21

Conclusion

This paper suggests that the Chinese government’s policytowards the restructuring of the coal industry conformsbroadly with the national interest. A move towards alarger scale and more technically advanced sectorpromises to benefit coal miners through the creation of asafer working environment. It will help local populationsby reducing the environmental degradation caused by theproduction and consumption of coal. And it will promotethe future energy security of the nation by reducing thetremendous waste currently involved in the exploitationof China’s coal resources.

Nevertheless, although restructuring conforms in manyways to the national interest, it may still come intoconflict with other valid or sectional interests. It isalso in China’s interest to maintain a high rate ofeconomic growth to provide employment for its stillgrowing population and to continue the dramaticimprovement in the living standards of the Chinesepeople. But in some ways this conflicts with any aim tocontrol the supply of coal – and therefore energy – byeliminating small mine production capacity. Thisconflict is not irresolvable, and in any case China needsto move to a less energy-intensive pattern of growth.But it does suggest that in the short and medium term therestructuring of the coal industry might come up againstother equally or more pressing concerns.

Similarly in this as in many other respects, policiesthat are appropriate for the prosperous and boomingcoastal areas are not necessarily so for the lessdeveloped interior. The Hu Jintao–Wen Jiabao governmenthas to some extent abandoned the faith of itspredecessors in the operation of the “trickle-down”effect and put into effect specific and targeted policiesto develop the interior. At the same time it is alsoshowing greater concern about the social costs of growth,as for example exemplified in coal mining accidents. Butrestructuring the coal industry in the hinterland is muchmore likely to be successful if it is linked to a broader

22

programme of employment and income generation in thoseareas, so that the populations of areas losing coalmining are provided with alternatives.

There are no easy solutions to these problems, but theimplication of this paper is that the process ofrestructuring will be a long one. It would be foolish toexpect quick results or to push the programme too farbeyond what the objective conditions allow. NeverthelessChina already has mines that one informed observer hasdescribed as the cleanest and among the most advanced inthe world. So it is probable that China will surmountthese problems, as it has surmounted so many others inthe past thirty years.

23

Related Documents