China’s cosmetics market, 2012 March 2013 Fung Business Intelligence Centre

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

China’s cosmetics market, 2012

March 2013 Fung Business Intelligence Centre

China’s cosmetics market, 2012 2

In this issue:

I. Industry overview p. 3

II. Competitive landscape p. 20

III. Latest developments p. 31

IV. Snapshots of sub-sector performance

p. 50

(1) Market size and market segments

(2) Retail price of cosmetics

(3) Distribution channels

I. Industry Overview

3 China’s cosmetics market, 2012

China’s cosmetics market, 2012

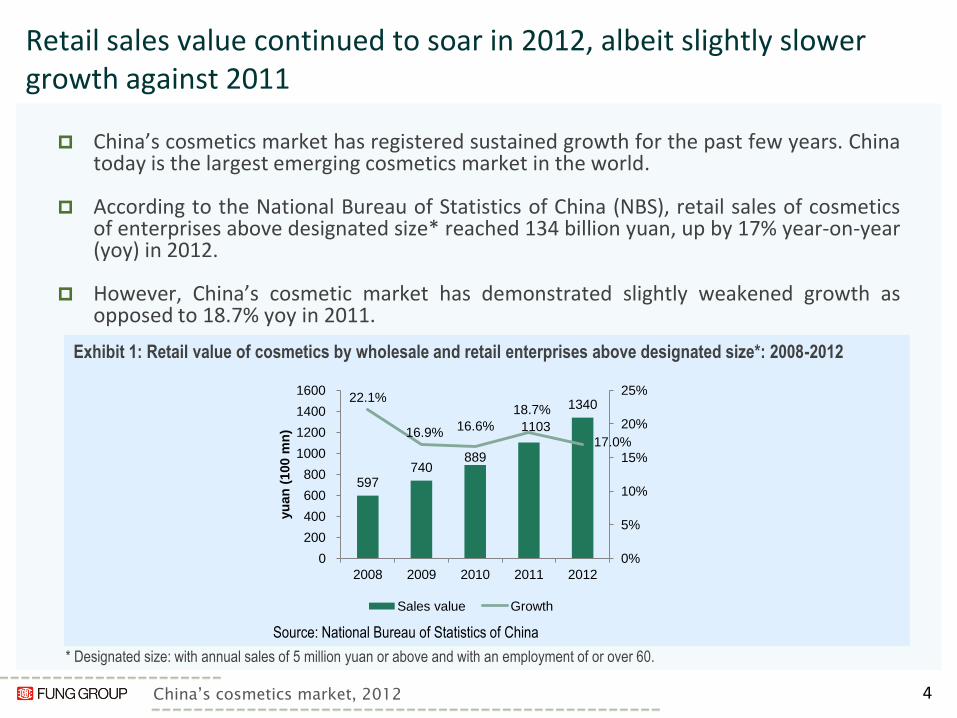

Retail sales value continued to soar in 2012, albeit slightly slower growth against 2011

China’s cosmetics market has registered sustained growth for the past few years. China today is the largest emerging cosmetics market in the world.

According to the National Bureau of Statistics of China (NBS), retail sales of cosmetics of enterprises above designated size* reached 134 billion yuan, up by 17% year-on-year (yoy) in 2012.

However, China’s cosmetic market has demonstrated slightly weakened growth as opposed to 18.7% yoy in 2011.

4 * Designated size: with annual sales of 5 million yuan or above and with an employment of or over 60.

Exhibit 1: Retail value of cosmetics by wholesale and retail enterprises above designated size*: 2008-2012

Source: National Bureau of Statistics of China

597 740

889

1103

1340 22.1%

16.9% 16.6%

18.7%

17.0%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1000

1200

1400

1600

2008 2009 2010 2011 2012

yu

an

(100 m

n)

Sales value Growth

4

China’s cosmetics market, 2012

According to China National Commercial Information Centre (CNCIC), cosmetics sales growth in tier 1 cities was 11.3% yoy in 2011, weaker than those realized in tier 2 cities (18.3% yoy) and tier 3 cities (21.4% yoy).

A report released by Kantar Worldpanel China in May 2012* also indicated that county level cities and counties posted robust growth at above 20% yoy in the first quarter of 2012, while growth in key cities and provincial capitals was less than 15% yoy in the same period.

5

Lower-tier cities posted stronger cosmetics sales growth than key cities in 2011

* Kantar Worldpanel China – “Spotlight on China”, May 2012

China’s cosmetics market, 2012

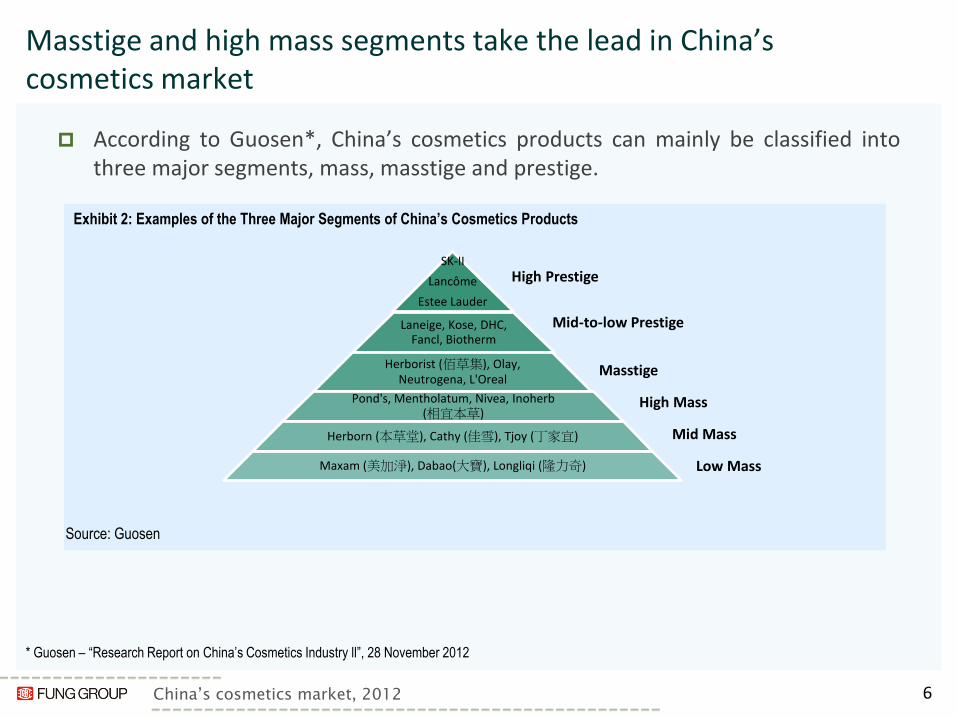

Masstige and high mass segments take the lead in China’s cosmetics market

According to Guosen*, China’s cosmetics products can mainly be classified into three major segments, mass, masstige and prestige.

6

* Guosen – “Research Report on China’s Cosmetics Industry ll”, 28 November 2012

Exhibit 2: Examples of the Three Major Segments of China’s Cosmetics Products

Source: Guosen

SK-II

Lancôme

Estee Lauder

Laneige, Kose, DHC, Fancl, Biotherm

Herborist (佰草集), Olay, Neutrogena, L'Oreal

Pond's, Mentholatum, Nivea, Inoherb (相宜本草)

Herborn (本草堂), Cathy (佳雪), Tjoy (丁家宜)

Maxam (美加淨), Dabao(大寶), Longliqi (隆力奇)

High Prestige

Masstige

High Mass

Mid-to-low Prestige

Mid Mass

Low Mass

China’s cosmetics market, 2012

Masstige and high mass segments take the lead in China’s cosmetics market (cont’d)

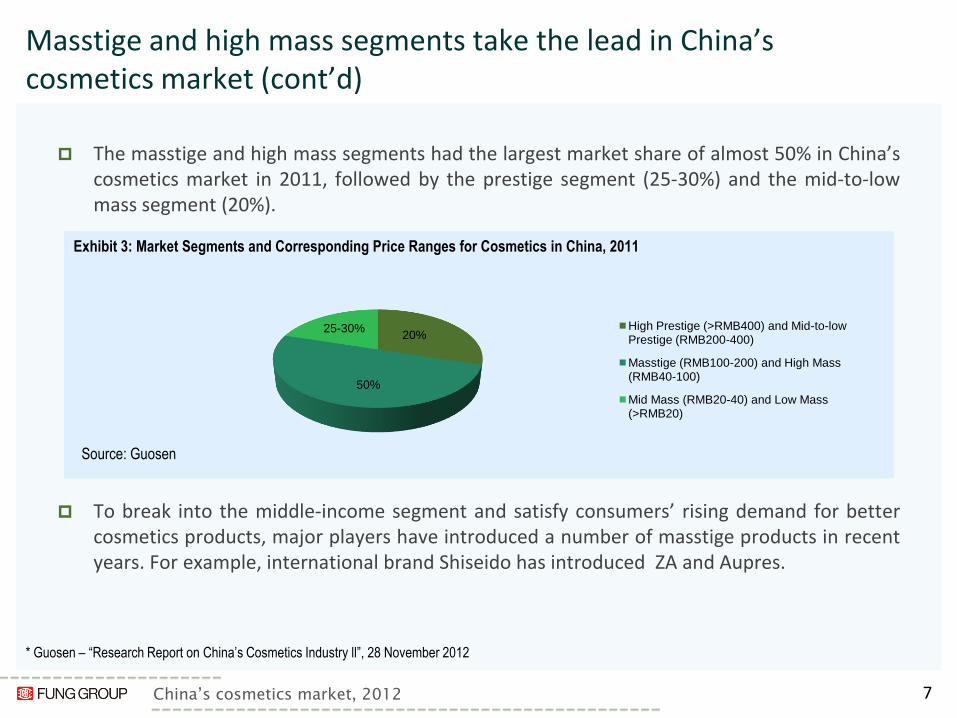

The masstige and high mass segments had the largest market share of almost 50% in China’s cosmetics market in 2011, followed by the prestige segment (25-30%) and the mid-to-low mass segment (20%).

To break into the middle-income segment and satisfy consumers’ rising demand for better cosmetics products, major players have introduced a number of masstige products in recent years. For example, international brand Shiseido has introduced ZA and Aupres.

7

* Guosen – “Research Report on China’s Cosmetics Industry ll”, 28 November 2012

Exhibit 3: Market Segments and Corresponding Price Ranges for Cosmetics in China, 2011

25-30%

50%

20% High Prestige (>RMB400) and Mid-to-low Prestige (RMB200-400)

Masstige (RMB100-200) and High Mass (RMB40-100)

Mid Mass (RMB20-40) and Low Mass (>RMB20)

Source: Guosen

(1) Market size and market segments

(2) Retail price of cosmetics

(3) Distribution channels

I. Industry Overview

8 China’s cosmetics market, 2012

China’s cosmetics market, 2012

Retailers raised retail prices amid higher operating costs

Although China’s cosmetics retail price slid slightly in the second half of 2012, the average retail price in 2012 was still higher than that of 2011.

− According to a report by Euromonitor*, Dior, Chanel, Lancôme and Biotherm lifted their unit prices at the beginning of 2011; retail price for some products may go up by up to 10%.

− Unilever, Procter & Gamble have also hiked their prices for some personal care categories like shower and hair care products.

9

* Euromonitor International – “Beauty and Personal Care in China”, May 2012

China’s cosmetics market, 2012

Escalating cost pressure on cosmetics retailers

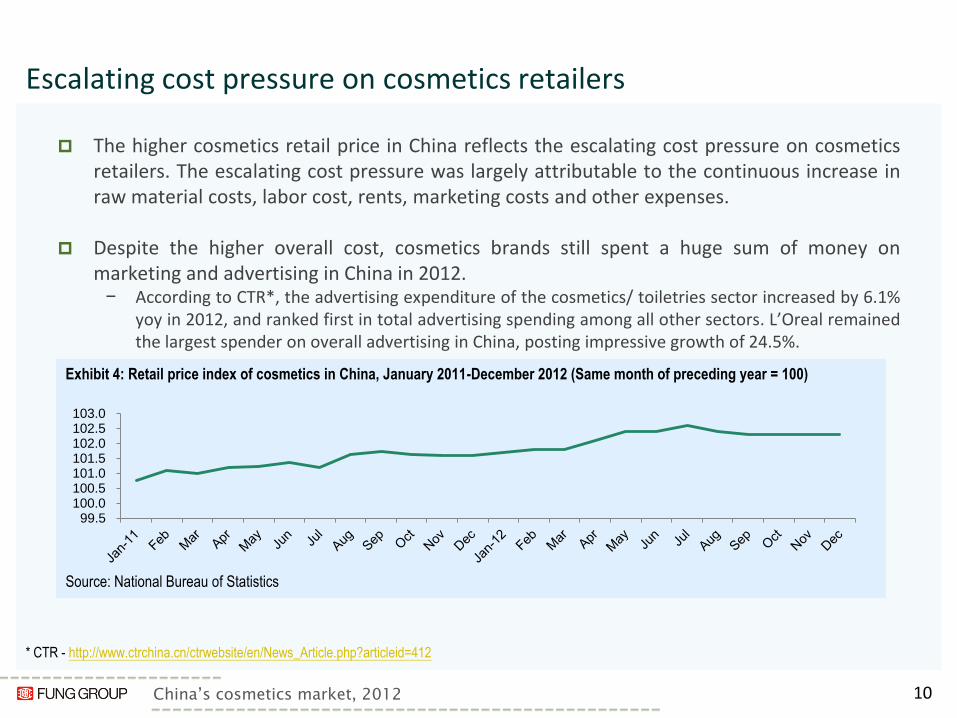

The higher cosmetics retail price in China reflects the escalating cost pressure on cosmetics retailers. The escalating cost pressure was largely attributable to the continuous increase in raw material costs, labor cost, rents, marketing costs and other expenses.

Despite the higher overall cost, cosmetics brands still spent a huge sum of money on marketing and advertising in China in 2012.

− According to CTR*, the advertising expenditure of the cosmetics/ toiletries sector increased by 6.1% yoy in 2012, and ranked first in total advertising spending among all other sectors. L’Oreal remained the largest spender on overall advertising in China, posting impressive growth of 24.5%.

10

* CTR - http://www.ctrchina.cn/ctrwebsite/en/News_Article.php?articleid=412

Exhibit 4: Retail price index of cosmetics in China, January 2011-December 2012 (Same month of preceding year = 100)

99.5 100.0 100.5 101.0 101.5 102.0 102.5 103.0

Source: National Bureau of Statistics

(1) Market size and market segments

(2) Retail price of cosmetics

(3) Distribution channels

I. Industry Overview

11 China’s cosmetics market, 2012

China’s cosmetics market, 2012

Grocery retailers and department stores are signaling decreasing market share; while health and beauty stores and Internet retailing are booming

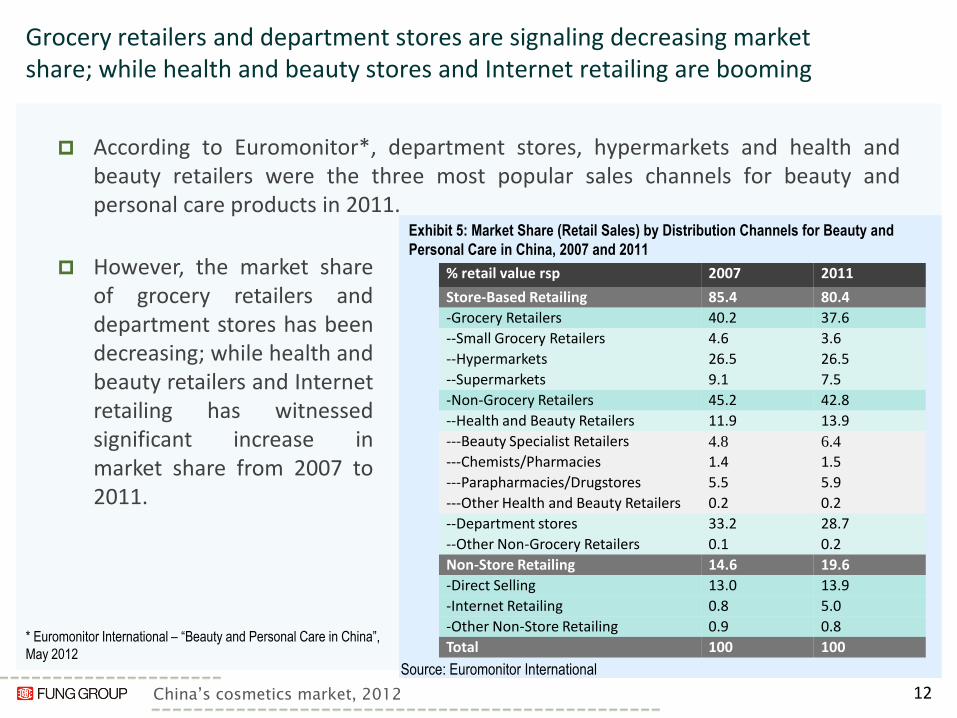

According to Euromonitor*, department stores, hypermarkets and health and beauty retailers were the three most popular sales channels for beauty and personal care products in 2011.

12

* Euromonitor International – “Beauty and Personal Care in China”,

May 2012

% retail value rsp 2007 2011

Store-Based Retailing 85.4 80.4

-Grocery Retailers 40.2 37.6

--Small Grocery Retailers 4.6 3.6

--Hypermarkets 26.5 26.5

--Supermarkets 9.1 7.5

-Non-Grocery Retailers 45.2 42.8

--Health and Beauty Retailers 11.9 13.9

---Beauty Specialist Retailers 4.8 6.4

---Chemists/Pharmacies 1.4 1.5

---Parapharmacies/Drugstores 5.5 5.9

---Other Health and Beauty Retailers 0.2 0.2

--Department stores 33.2 28.7

--Other Non-Grocery Retailers 0.1 0.2

Non-Store Retailing 14.6 19.6

-Direct Selling 13.0 13.9

-Internet Retailing 0.8 5.0

-Other Non-Store Retailing 0.9 0.8

Total 100 100

However, the market share of grocery retailers and department stores has been decreasing; while health and beauty retailers and Internet retailing has witnessed significant increase in market share from 2007 to 2011.

Exhibit 5: Market Share (Retail Sales) by Distribution Channels for Beauty and

Personal Care in China, 2007 and 2011

Source: Euromonitor International

China’s cosmetics market, 2012

Features and characteristics of selected distribution channels

Features and characteristics of selected retail formats are examined:

− Department stores

− Supermarkets/hypermarkets

− Professional stores

− Specialty stores

− Internet retailing

13

China’s cosmetics market, 2012

Characteristics of selected distribution channels – department stores

Department stores Department stores offer a wide range of merchandises and provide one-stop shopping

experiences to consumers.

Department stores play an important role in brand building.

Competition for counter spaces is fierce, many lesser-known brands are forced to phase out.

Department stores may gradually lose appeal to Chinese consumers due to poor differentiation.

14

China’s cosmetics market, 2012

Characteristics of selected distribution channels – supermarkets/hypermarkets

Supermarkets/hypermarkets Supermarkets/ hypermarkets are important channels particularly for low- to mid-range

cosmetics products or products with lower unit prices (e.g. shampoo, facial cleanser).

Brands need to pay a fairly high slotting fees to supermarkets/ hypermarkets for the display and sale of their products; some weaker local brands are facing tough cost challenges.

15

China’s cosmetics market, 2012

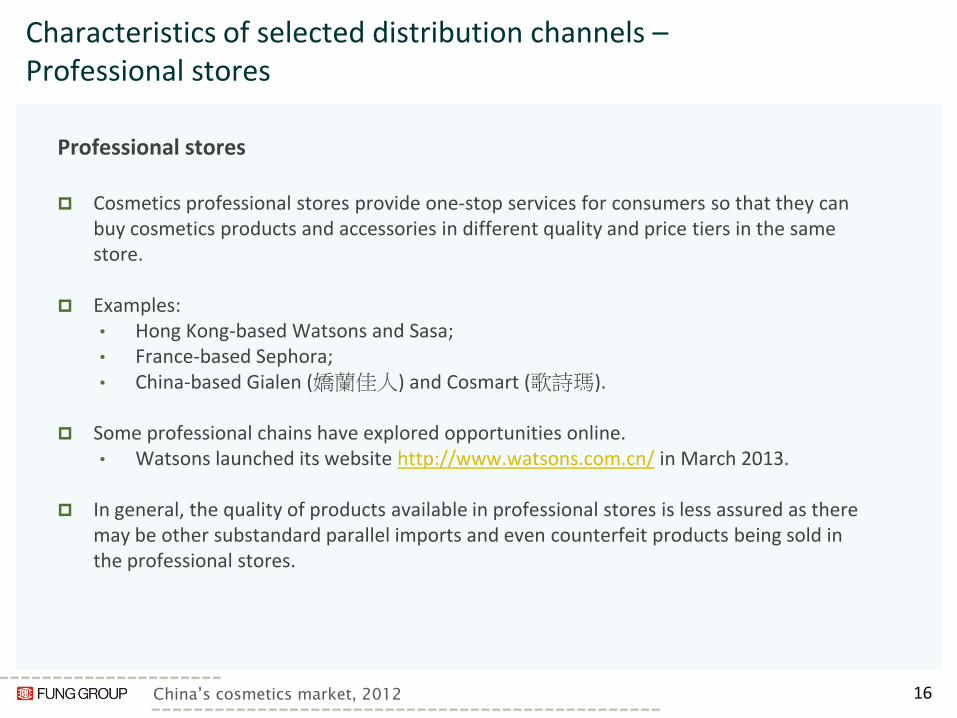

Characteristics of selected distribution channels – Professional stores

Professional stores Cosmetics professional stores provide one-stop services for consumers so that they can

buy cosmetics products and accessories in different quality and price tiers in the same store.

Examples: • Hong Kong-based Watsons and Sasa; • France-based Sephora; • China-based Gialen (嬌蘭佳人) and Cosmart (歌詩瑪).

Some professional chains have explored opportunities online.

• Watsons launched its website http://www.watsons.com.cn/ in March 2013.

In general, the quality of products available in professional stores is less assured as there may be other substandard parallel imports and even counterfeit products being sold in the professional stores.

16

China’s cosmetics market, 2012

Characteristics of selected distribution channels – Specialty stores

Specialty stores Cosmetics brand owners can achieve autonomy over store operation through opening

specialty stores. Specialty stores help promote brand image, ensure standardized prices and services.

In recent years, many Korean cosmetics brands such as Missha and Innisfree are especially interested in distributing their products through specialty stores, in addition to other retail formats.

It is expected that specialty stores will become another key retail channel for cosmetics products.

17

China’s cosmetics market, 2012

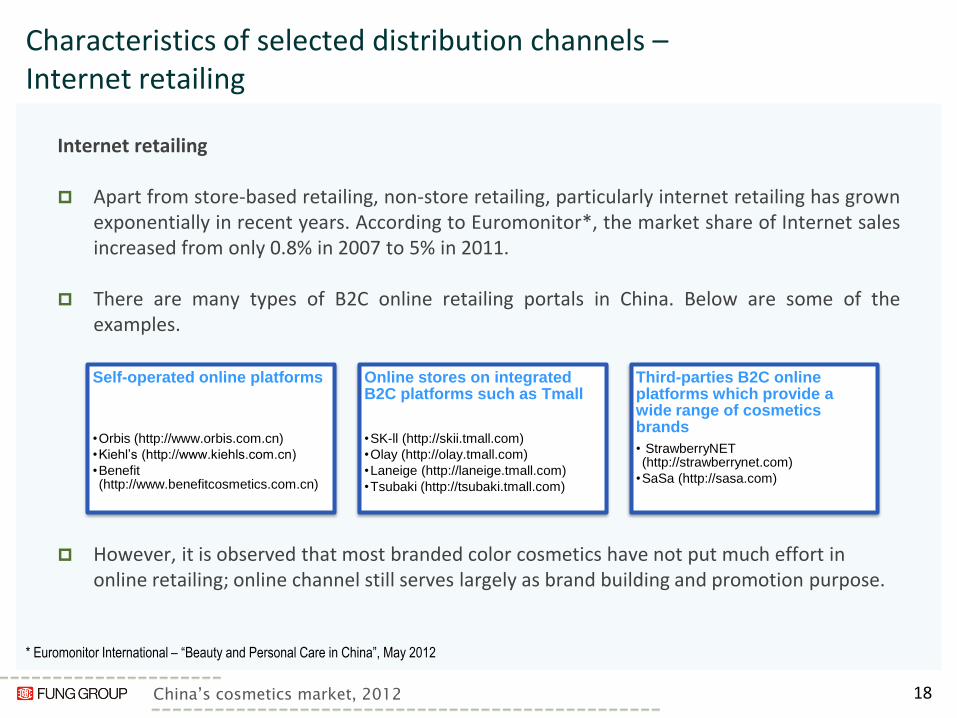

Characteristics of selected distribution channels – Internet retailing

Internet retailing

Apart from store-based retailing, non-store retailing, particularly internet retailing has grown exponentially in recent years. According to Euromonitor*, the market share of Internet sales increased from only 0.8% in 2007 to 5% in 2011.

There are many types of B2C online retailing portals in China. Below are some of the examples.

However, it is observed that most branded color cosmetics have not put much effort in

online retailing; online channel still serves largely as brand building and promotion purpose.

18

* Euromonitor International – “Beauty and Personal Care in China”, May 2012

Self-operated online platforms

•Orbis (http://www.orbis.com.cn)

•Kiehl’s (http://www.kiehls.com.cn)

•Benefit (http://www.benefitcosmetics.com.cn)

Online stores on integrated B2C platforms such as Tmall

•SK-ll (http://skii.tmall.com)

•Olay (http://olay.tmall.com)

•Laneige (http://laneige.tmall.com)

•Tsubaki (http://tsubaki.tmall.com)

Third-parties B2C online platforms which provide a wide range of cosmetics brands

• StrawberryNET (http://strawberrynet.com)

•SaSa (http://sasa.com)

China’s cosmetics market, 2012

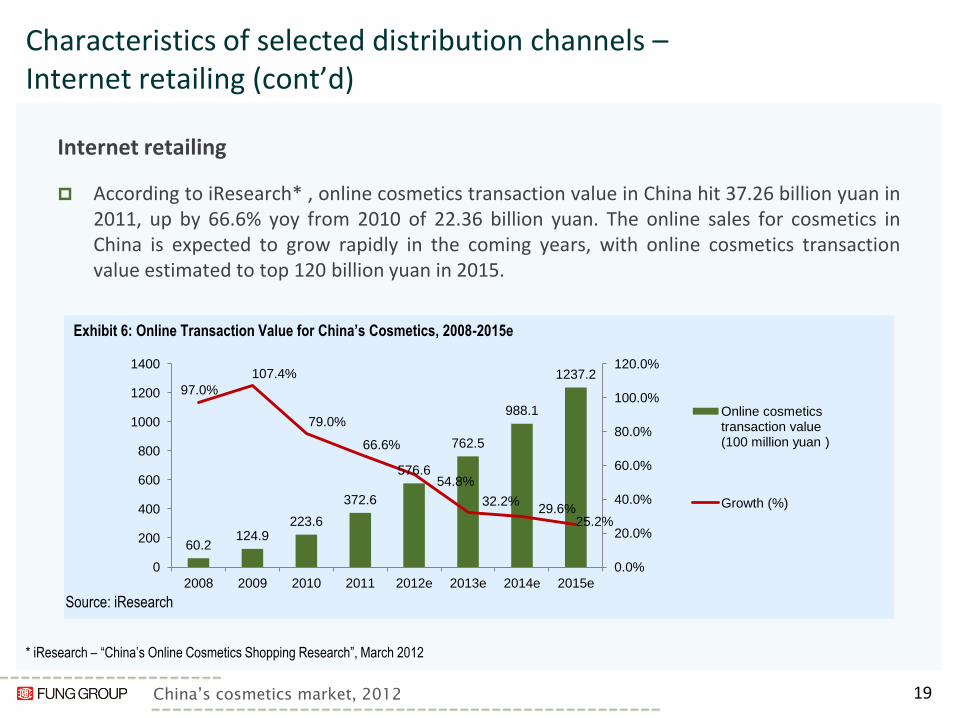

Characteristics of selected distribution channels – Internet retailing (cont’d)

Internet retailing

According to iResearch* , online cosmetics transaction value in China hit 37.26 billion yuan in 2011, up by 66.6% yoy from 2010 of 22.36 billion yuan. The online sales for cosmetics in China is expected to grow rapidly in the coming years, with online cosmetics transaction value estimated to top 120 billion yuan in 2015.

19

* iResearch – “China’s Online Cosmetics Shopping Research”, March 2012

Exhibit 6: Online Transaction Value for China’s Cosmetics, 2008-2015e

Source: iResearch

60.2 124.9

223.6

372.6

576.6

762.5

988.1

1237.2

97.0%

107.4%

79.0%

66.6%

54.8%

32.2% 29.6%

25.2%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

0

200

400

600

800

1000

1200

1400

2008 2009 2010 2011 2012e 2013e 2014e 2015e

Online cosmetics transaction value (100 million yuan )

Growth (%)

II. Competitive landscape

(1) Foreign cosmetics companies

(2) Domestics cosmetics companies

20 China’s cosmetics market, 2012

China’s cosmetics market, 2012

Foreign cosmetics enterprises captured a larger market share in key cities

According to a report by Orient Security (東方証劵), foreign cosmetics brands have been expanding rapidly and captured a larger market share (around 70%-80%) in tier 1 and 2 cities.

Despite the overall slowdown in cosmetics sales in 2012, international premium brands continued to post solid retail sales growth in the market in the third quarter of 2012, with Lancôme and Biotherm achieved retail sales growth of 20% yoy and 15% yoy, respectively.

21

* Orient Security – “Research on China’s Cosmetics Industry”, 30 November 2012

China’s cosmetics market, 2012

Foreign cosmetics enterprises captured a larger market share in key cities (cont’d)

To expedite market penetration, foreign cosmetics enterprises are looking ways to expand their share of the mass market. Some examples include:

− Cosmetics retailer Sephora opened its first outlet in Wuhan in 2011.

− Chained professional store Watsons, which owns 1,000 retail stores across 150 cities of China, has also announced plans to expand its presence in more than 300 cities in China with a total of 3,000 stores by 2016*.

− New Zealand cosmetics brand Jagar** entered Tmall in December 2012 and is planning to set up offline retail stores in China later.

− Upon completion of the acquisition of Dabao (大寶) in 2008, Johnson & Johnson acquired Elsker (嗳呵) in January 2013***, hoping to further extend its influence in the mother and baby care market in China.

22

* China Business News (第一財經日報) http://www.yicai.com/news/2013/03/2565276.html

** Zghzp.com (中國化妝品網) http://www.zghzp.com/news/hyzx/ppdt/48731.html

*** Johnson & Johnson (China) Investment Co., Ltd http://www.jnj.com.cn/news201312617.html

China’s cosmetics market, 2012

Foreign cosmetics groups and their major brands

23

Exhibit 7: Foreign Cosmetics Groups and their Major Brands in China (as of February 2013)

Enterprise Brands

L’Oréal

歐萊雅

L’Oréal Paris 巴黎歐萊雅

Garnier 卡尼爾

Maybelline New York 美寶蓮紐約

L’Oréal Professional 歐萊雅專業美髮

Kérastase 卡詩

Lancôme 蘭蔻

shu uemura 植村秀

Giorgio Armani 喬治 阿瑪尼

LA ROCHE-POSAY理膚泉

Mininurse 小護士

Yue Sai 羽西

Vichy 薇姿

Biotherm 碧歐泉

Helena Rubinstein HR 赫蓮娜

Kiehl’s 科顏氏

Skinceuticals修麗可

Matrix 美奇絲

P&G

寶潔

Head & Shoulders 海飛絲

Rejoice 飄柔

SK-II

Oceana 海肌源

Braun 德國博明

Vidal Sasson 沙宣

Clairol Herbal Essences 伊卡璐

Wella 威娜

Safeguard 舒膚佳

Sebastian 塞巴斯汀

Camay 卡玫爾

Clairol Professional 伊卡璐絲煥專業美髮

Pantene 潘婷

Olay 玉蘭油

Gillette吉列

Shiseido

資生堂

Shiseido 資生堂

Clé de peau beauté 珂麗柏蒂

Aupres 歐珀萊

Urara 悠萊

Elixir White 怡麗絲爾 純肌淨白

Elixir Superieur 怡麗絲爾優悅活顏

Melanreduce 臻白無瑕

IPSA 茵芙莎

UNO 吾諾

DQ 蒂珂

Pure & Mile Soi 泊美舒亞

Dicila 蒂思嵐

Handasui 肌水

Tsubaki 絲蓓綺

Pure & Mild 泊美

Hand Cream 美潤護手霜

Za 姬芮

Aqua Label 水之印

Be 彼嘉

Aquair 水之密語

Perfect 洗顔專科

Kuyura 可悠然

Super Mild 惠潤

PF-COVER 無瑕修顏

Unilever

聯合利華

Vaseline 凡士林

Lux 力士

Dove 多芬

Pond’s 旁氏

Clear 清揚

LYNX 凌仕

Hazeline 夏士蓮

Rexona 舒耐

Source: Respective company websites, compiled by Fung Business Intelligence Centre

Exhibit 7 shows some of the foreign cosmetics groups and their major brands in China.

China’s cosmetics market, 2012

Foreign cosmetics groups and their major brands (cont’d)

24

Exhibit 7: Foreign Cosmetics Groups and their Major Brands in China (cont’d)

Enterprise Brands

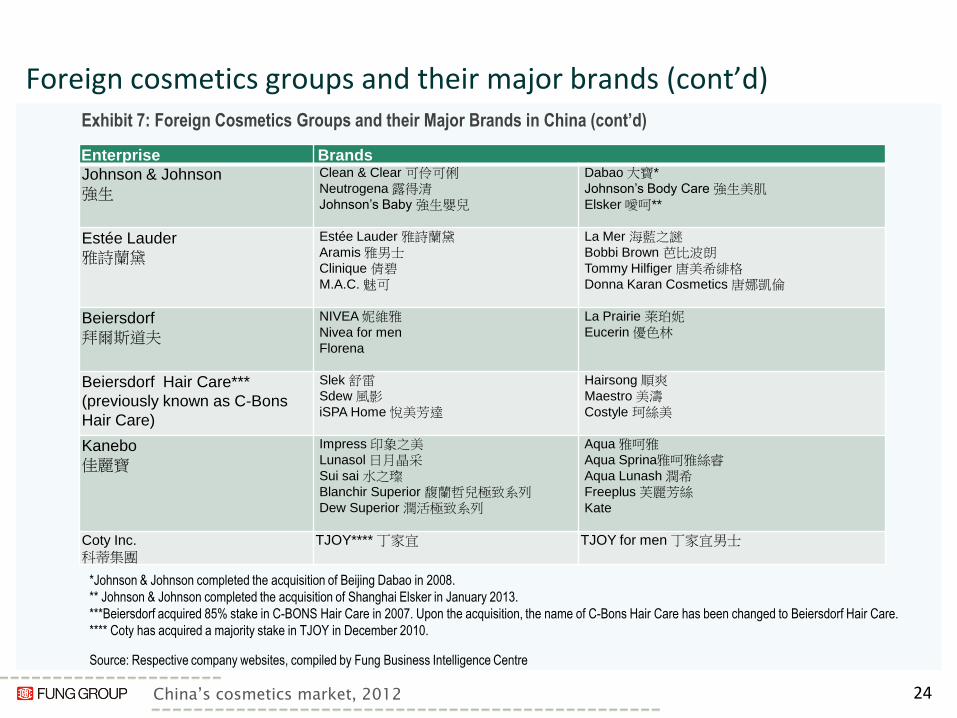

Johnson & Johnson

強生

Clean & Clear 可伶可俐

Neutrogena 露得清

Johnson’s Baby 強生嬰兒

Dabao 大寶*

Johnson’s Body Care 強生美肌

Elsker 噯呵**

Estée Lauder

雅詩蘭黛

Estée Lauder 雅詩蘭黛

Aramis 雅男士

Clinique 倩碧

M.A.C. 魅可

La Mer 海藍之謎

Bobbi Brown 芭比波朗

Tommy Hilfiger 唐美希緋格

Donna Karan Cosmetics 唐娜凱倫

Beiersdorf

拜爾斯道夫

NIVEA 妮維雅

Nivea for men

Florena

La Prairie 莱珀妮

Eucerin 優色林

Beiersdorf Hair Care***

(previously known as C-Bons

Hair Care)

Slek 舒雷

Sdew 風影

iSPA Home 悅美芳達

Hairsong 順爽

Maestro 美濤

Costyle 珂絲美

Kanebo

佳麗寶

Impress 印象之美

Lunasol 日月晶采

Sui sai 水之璨

Blanchir Superior 馥蘭哲兒極致系列

Dew Superior 潤活極致系列

Aqua 雅呵雅

Aqua Sprina雅呵雅絲睿

Aqua Lunash 潤希

Freeplus 芙麗芳絲

Kate

Coty Inc.

科蒂集團 TJOY**** 丁家宜 TJOY for men 丁家宜男士

Source: Respective company websites, compiled by Fung Business Intelligence Centre

*Johnson & Johnson completed the acquisition of Beijing Dabao in 2008.

** Johnson & Johnson completed the acquisition of Shanghai Elsker in January 2013.

***Beiersdorf acquired 85% stake in C-BONS Hair Care in 2007. Upon the acquisition, the name of C-Bons Hair Care has been changed to Beiersdorf Hair Care.

**** Coty has acquired a majority stake in TJOY in December 2010.

China’s cosmetics market, 2012

Enterprise Brands Kao

花王

Kao 花王

Bioré 碧柔

Men’s Bioré 碧柔男士

Sofina 蘇菲娜

Liese 莉婕

Asience 亞羨姿

Sifoné 詩芬

Feather 花王飛逸

Curél珂潤

Kosé

高絲

Kosé 高絲

Beauté de Kosé 美諦高絲

Prédia 貝締雅

Sekkisei 雪肌精

Refine 萊菲

Esprique 綺絲碧

Junkisui 純肌粋

Seikisho 清肌晶

Shirosumi 白澄

Cosme Decorte 黛珂

Avenir 艾文莉

Recipe-O 蘭哲歐

Junkisei 潤肌精

White St妍哲

Nature & Co 娜蔻

Moisture Skin Repair

Astalution

Grandaine 葛倫黛娜

Infinity

Avon Products, Inc.

美國雅芳産品有限公司

Avon 雅芳

Amore Pacific Corp

愛茉莉太平洋集團

Laneige 蘭芝

Mamode 夢妝

Innisfree 悅詩風吟

Amore 愛茉莉

Sulwhasoo 雪花秀

Lirikos 儷瑞恩

Nu Skin Enterprise Inc.

如新集團

Nu Skin 如新

LVMH Group

Guerlain 嬌蘭

Fresh 馥蕾詩 Benefit 貝玲妃

Make Up For Ever

DHC Corp DHC

Fancl Corp Fancl

Foreign cosmetics groups and their major brands (cont’d)

25

Exhibit 7: Foreign Cosmetics Groups and their Major Brands in China (cont’d)

Source: Respective company websites, compiled by Fung Business Intelligence Centre

II. Competitive landscape

(1) Foreign cosmetics companies

(2) Domestics cosmetics companies

26 China’s cosmetics market, 2012

China’s cosmetics market, 2012

Domestic cosmetics enterprises dominated in lower tier cities

Domestic cosmetics brands have made great strides in lower tier cities in recent years.

− As a case in point, Inoherb (相宜本草) has expanded rapidly and shown outstanding performance in lower tier cities for the past three years. It is now the second large domestic brand in the skin care segment, with its market share reaching almost 10%, immediately after Olay*.

To vie for larger market share in the market, some domestic players have cooperated with international players to expand their product portfolios and enhance their competitiveness.

− A typical example is Shanghai Jahwa (上海家化). The company has entered into strategic alliance with Kao in November 2011** on marketing and sales.

27

* Orient Security – “Research on Cosmetics Industry”, 30 November 2012

** Kao - http://www.kao.com/jp/en/corp_news/2011/20111125_001.html

China’s cosmetics market, 2012

Domestic cosmetics groups and their major brands

28

* Ping An Group has acquired 100% of share in Shanghai Jahwa in 2011.

**Shanghai Jahwa has acquired 51% stake in Cortry in 2008.

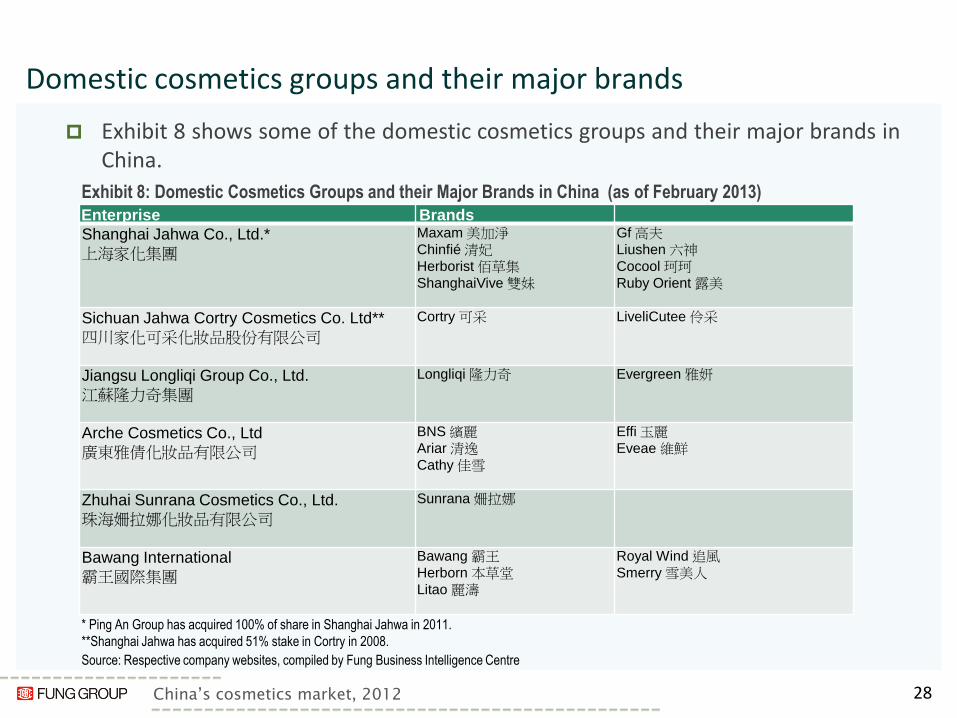

Exhibit 8 shows some of the domestic cosmetics groups and their major brands in China.

Exhibit 8: Domestic Cosmetics Groups and their Major Brands in China (as of February 2013)

Enterprise Brands Shanghai Jahwa Co., Ltd.*

上海家化集團

Maxam 美加淨

Chinfié 清妃

Herborist 佰草集

ShanghaiVive 雙妹

Gf 高夫

Liushen 六神

Cocool 珂珂

Ruby Orient 露美

Sichuan Jahwa Cortry Cosmetics Co. Ltd**

四川家化可采化妝品股份有限公司

Cortry 可采 LiveliCutee 伶采

Jiangsu Longliqi Group Co., Ltd.

江蘇隆力奇集團

Longliqi 隆力奇

Evergreen 雅妍

Arche Cosmetics Co., Ltd

廣東雅倩化妝品有限公司

BNS 繽麗

Ariar 清逸

Cathy 佳雪

Effi 玉麗

Eveae 維鮮

Zhuhai Sunrana Cosmetics Co., Ltd.

珠海姍拉娜化妝品有限公司

Sunrana 姍拉娜

Bawang International

霸王國際集團

Bawang 霸王

Herborn 本草堂

Litao 麗濤

Royal Wind 追風

Smerry 雪美人

Source: Respective company websites, compiled by Fung Business Intelligence Centre

China’s cosmetics market, 2012

Enterprise Brands Shanghai Huayin Commodity Co., Ltd.

上海華銀日用品有限公司 Bee & Flower 蜂花

Guangzhou Houdy Cosmetics Co., Ltd.

廣州市好迪化妝品有限公司

Houdy 好迪 Tongle 童樂

Decolor Cosmetics Co., Ltd.

廣州市迪彩化妝品有限公司 Decolor 迪彩

Luxe-Lotus 蓮尚

Enevous 伊儂華

Crystal 晶彩

Lotuses 千蓮薈

Nenuph 藍蓮花

Lafang Group

拉芳集團 Lafang 拉芳

Raclen 雨潔

Duo Zi 多姿

Bétrue 繽純

Sunfeel 聖峰

Mese 美多絲

Guangzhou Tobaby Cosmetics Co., Ltd.

廣州露純化妝品有限公司

Tobaby 丹芭露

Huaya Group Co., Ltd.

環亞化妝品科技有限公司

Franic 法蘭琳卡

Leila 蕾拉 Meifubao 美膚寶

Jala (Group) Co., Ltd.

伽藍(集團)股份有限公司

Chcedo 自然堂

Aglaia 雅格麗白 Maysu 美素

Insea 醫婷

Domestic cosmetics groups and their major brands (cont’d)

29

Exhibit 8: Domestic Cosmetics Groups and their Major Brands in China (cont’d)

Source: Respective company websites, compiled by Fung Business Intelligence Centre

China’s cosmetics market, 2012

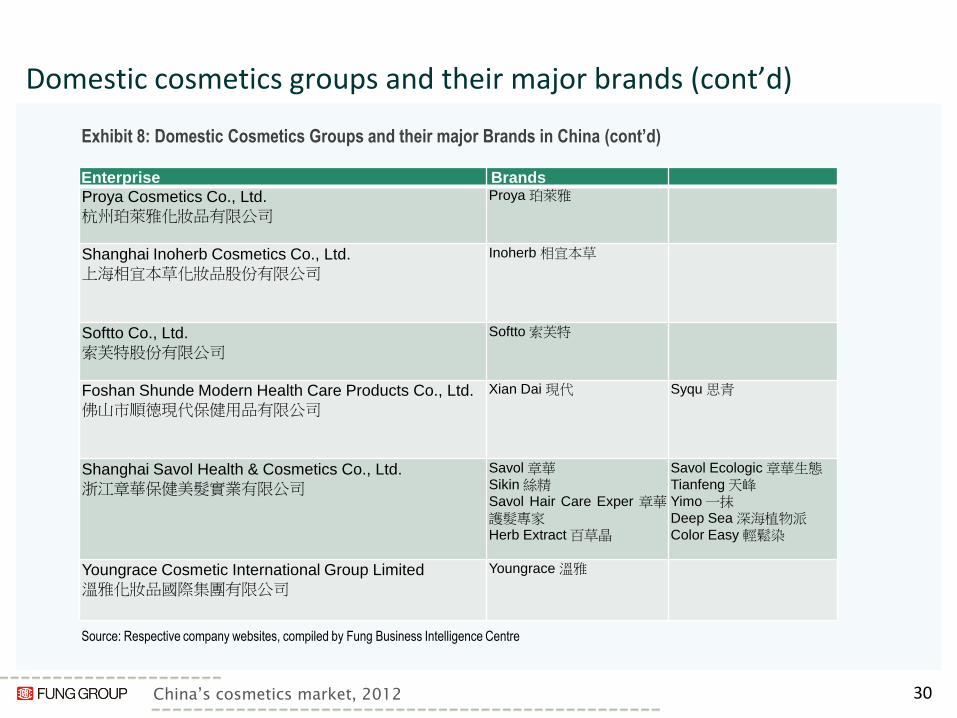

Enterprise Brands Proya Cosmetics Co., Ltd.

杭州珀萊雅化妝品有限公司

Proya 珀萊雅

Shanghai Inoherb Cosmetics Co., Ltd.

上海相宜本草化妝品股份有限公司

Inoherb 相宜本草

Softto Co., Ltd.

索芙特股份有限公司

Softto 索芙特

Foshan Shunde Modern Health Care Products Co., Ltd.

佛山市順德現代保健用品有限公司

Xian Dai 現代 Syqu 思青

Shanghai Savol Health & Cosmetics Co., Ltd.

浙江章華保健美髮實業有限公司

Savol 章華

Sikin 絲精

Savol Hair Care Exper 章華護髮專家

Herb Extract 百草晶

Savol Ecologic 章華生態

Tianfeng 天峰

Yimo 一抹

Deep Sea 深海植物派

Color Easy 輕鬆染

Youngrace Cosmetic International Group Limited

溫雅化妝品國際集團有限公司

Youngrace 溫雅

Domestic cosmetics groups and their major brands (cont’d)

30

Exhibit 8: Domestic Cosmetics Groups and their major Brands in China (cont’d)

Source: Respective company websites, compiled by Fung Business Intelligence Centre

III. Latest developments

31 China’s cosmetics market, 2012

China’s cosmetics market, 2012

Product premiumisation and trading up have become a major development trend

Increasing disposable income led by dynamic economic growth and greater presence of premium brands in lower tier cities subsidize premium cosmetics sales growth.

− According to Euromonitor*, retail sales of premium cosmetics turned higher from 25.89 billion yuan in 2010 to 30.46 billion yuan in 2011, up 17.6% yoy; in particular, sales of premium baby and child-specific products during the same period even jumped more than 20% yoy to 459.3 million yuan.

− Premium cosmetics are expected to post a 14% compound annual growth rate between

2011 and 2016, higher than overall beauty and personal care’s annual average growth of 8%.

* Euromonitor International – “Beauty and Personal Care in China”, May 2012

32

China’s cosmetics market, 2012

Product premiumisation and trading up have become a major development trend (cont’d)

To satisfy the growing demand for higher-end cosmetics, a number of international and domestic brands have expedited their penetration in the high-end segment.

− L’Occitane has introduced hair care products and an upgraded premium lip care product “Shea Butter Lip Balm” in China in recent years.

− Estee Launder has also launched a new premium skin care line “Osiao” which targets the Asian market, especially China.

On the other hand, some domestic brands have launched premium cosmetics to compete with international players.

− Jiangsu Longliqi (隆力奇), one of the most sought-after brands in China, introduced new mid-to-high-end skin care products in 2011.

33

China’s cosmetics market, 2012

Brands are striving to enhance competitiveness

In response to fierce competition and more sophisticated consumers’ needs, key players in the cosmetics market have increased efforts to widen their product portfolios, develop functional products and change the packaging to enhance their competitiveness in the market.

− Unilever has changed the packaging and launched various promotions to reinforce its

hair care brand, Clear for Men, in order to compete with Head & Shoulders for Men, one of the best known hair care brands by P&G in China.

− Shanghai Inoherb introduced an upgraded toner product “Rhodiola Fine Whitening Toner” in 2011, targeting Chinese consumers with a greater desire for whitening function.

− Henkel (China) posted the strongest sales growth in the hair care segment in 2011 after launching its new hair care brand, Syoss, as well as expanding the range of hair care products it offers*.

34

* Euromonitor International – “Beauty and Personal Care in China”, May 2012

China’s cosmetics market, 2012

Business-to-consumer (B2C) online players are tapping into brick and mortar retailing

While many cosmetics brands have been expanding into online retailing in recent years, some brands that originally sold only through business-to-consumer (B2C) model are starting to break into store-based retailing to grab more market share.

− Mask Family (膜法世家) set up offline experience store in Guangzhou in June 2012*.

− Uzise (柚子舍) has revealed its plan to open seven retail stores in Beijing, Shanghai and Chengdu; and Lefeng (樂蜂網) has also planned to tap into the offline market**.

35

* Guangdong E-business Association - http://www.gdeba.org/article/view/id/2993

** iResearch - http://www.iresearch.com.cn/Report/View.aspx?Newsid=176039

China’s cosmetics market, 2012

Cosmeceutical market is growing in prevalence

According to HKTDC*, more than 170 enterprises have tapped into the cosmeceutical market. It is estimated that the cosmeceuticals sector in China would grow by 10% to 20% yoy to reach 20 billion yuan in three to five years. Chinese herbal cosmetics brands are playing an active role in the sector.

In addition, data released by HKTDC** also suggested that China’s cosmeceutical market posted annual sales growth of up to 10% to 20% yoy between 2004 and 2012, with the market share increasing from 20% to 40%. The sales growth of China’s cosmeceutical market was twice as high as that of the European and U.S. markets.

Indeed, many players have entered the cosmeceutical market in recent years. − Dihon Pharmaceutical (滇虹藥業), well-known for its hair care line Health King (康王), launched two

new cosmeceutical lines Freeface (芙芮芬絲) and Beirun (倍潤) in 2012. − Jawha, after successfully launching Herborist, also introduced another cosmeceutial line Dr. Richia (

玉澤) in 2010. − Beijing Tongrentang Cosmetics (同仁堂) announced that it will increase the total number of its retail

stores to 2,000 worldwide by the end of 2015, with total sales estimated to hit 20 billion yuan.

36

* HKTDC - http://china-trade-research.hktdc.com/business-news/article/China-Consumer-Market/China-s-cosmetics-market/ccm/en/1/1X000000/1X002L09.htm

** HKTDC - http://product-industries-research.hktdc.com/business-

news/article/%E5%81%A5%E5%BA%B7%E5%8F%8A%E7%BE%8E%E5%AE%B9%E7%94%A2%E5%93%81/%E8%97%A5%E5%A6%9D%E6%88%90%E4%

B8%AD%E5%9C%8B%E6%97%A5%E5%8C%96%E5%B8%82%E5%A0%B4%E6%96%B0%E5%AF%B5/imn/tc/1/1X3WLQ9L/1X09RYZ7.htm

China’s cosmetics market, 2012

Cosmeceutical market is growing in prevalence (cont’d)

Although the cosmeceutical market in China has long been dominated by foreign brands such as Avene, Vichy, La Roche-Posay, Sulwhasoo and Freeplus, data released by Baidu Data Research Center* showed that domestic cosmeceutical brands Inoherb and Herborist ranked first and second, respectively in terms of popularity in the cosmeceutical market in the third quarter of 2012, outstripping foreign cosmeceutical brand Avene which only ranked the third.

The data also indicated that the dominant position of foreign cosmeceutical brands is being challenged by some outstanding domestic brands.

37

* Baidu Data Research Center – Report on China’s Cosmetics Industry for Q3 2012, November 2012

China’s cosmetics market, 2012

Male grooming market is growing exponentially

According to Euromonitor*, men’s grooming market posted a 20% yoy sales growth to 5.518 billion yuan in 2011; in particular, men’s skin care witnessed the highest sales growth of 34% yoy, while men’s toiletries registered retail sales growth of 26% yoy.

To penetrate the lucrative market, many foreign and domestic brands have

introduced product lines for men. − Examples of foreign brands include Fancl, L’Oreal Men Expert, Mentholatum, Kiehl’s,

SK-ll Men and Orbis. − Examples of domestic brands include Pai Lang (派朗) by Beijing Tongrentang

Cosmetics, GF (高夫) by Jawha, Inoherb Men (相宜本草男士), and Chcedo Men (自然堂男士).

38

* Euromonitor International – “Beauty and Personal Care in China”, May 2012

China’s cosmetics market, 2012

Male grooming market is growing exponentially (cont’d)

Furthermore, some major players have stepped up their efforts to launch more new products to satisfy different consumer needs.

− For instance, following L’Oreal Men Expert introduced an anti-aging line in 2008, Mentholatum also launched Coenzyme Q10 Lifting Face Cream and Power-up Essence in 2009.

− In 2011, Mentholatum (Zhongshan) Pharmaceuticals also widened its product ranges from men’s facial cleansers and facial creams to bath and shower products, and posted remarkable results in key cities.

39

China’s cosmetics market, 2012

Children and baby care market sees propelling growth

According to Euromonitor*, retail sales of China’s children and baby care products continued to register strong growth, posting 17% yoy growth to 4.852 billion yuan in 2011. It is estimated that retail sales of China’s children and baby care products will hit 9.263 billion yuan in 2016.

Major players in the market include Johnson’s Baby, Frog Prince (青蛙王子), Yumeijing (郁美淨), Elsker, Pigeon and Hai Er Mian (孩兒面).

The market has long been dominated by foreign brand, Johnsons’ Baby (with market share of about 50%), however, the brand saw share decline from 2008 onwards. Meanwhile, some domestic brands have experienced strong growth in market share, for instance, the market share of leading domestic brand, Frog Prince increased from 3.3% in 2008 to 6.9% in 2011.

40

* Euromonitor International – “Beauty and Personal Care in China”, May 2012

China’s cosmetics market, 2012

Children and baby care market sees propelling growth (cont’d)

With the increasing demand for children and baby care products, the number of retail stores selling mom and baby products has grown rapidly in recent years. Retailers such as Redbaby (北京紅孩子), Lijiababy (麗家寶貝) and Leyou (樂友) have set up a number of retail stores offering skincare products for expectant mothers and babies.

Some cosmetics brands have also introduced skin care products designed specially for expectant mothers and babies. Examples include Mamale (媽媽樂) by Kong Fengchun (孔鳳春) and Jiabaole (佳寶樂) by Beijing Tongrentang Cosmetics (同仁堂).

41

China’s cosmetics market, 2012

Anti-aging products becomes increasingly popular

Anti-aging products have gained increasing attention among Chinese women, in

particular, in recent years.

− According to Guosen and Euromonitor*, sales of anti-agers has increased 2.4 times over the past five years; in 2011, the total sales of anti-agers increased by 17% yoy to reach almost 20 billion yuan.

− In the past, the main consumers of anti-agers were women over 30 years of age. Nowadays, female consumers are now more conscious about their beauty and youthfulness and many of them start to use anti-ageing products in their early 20s.

42

* Guosen – “Research Report on China’s Cosmetics Industry ll”, 28 November 2012

China’s cosmetics market, 2012

Anti-aging products becomes increasingly popular (cont’d)

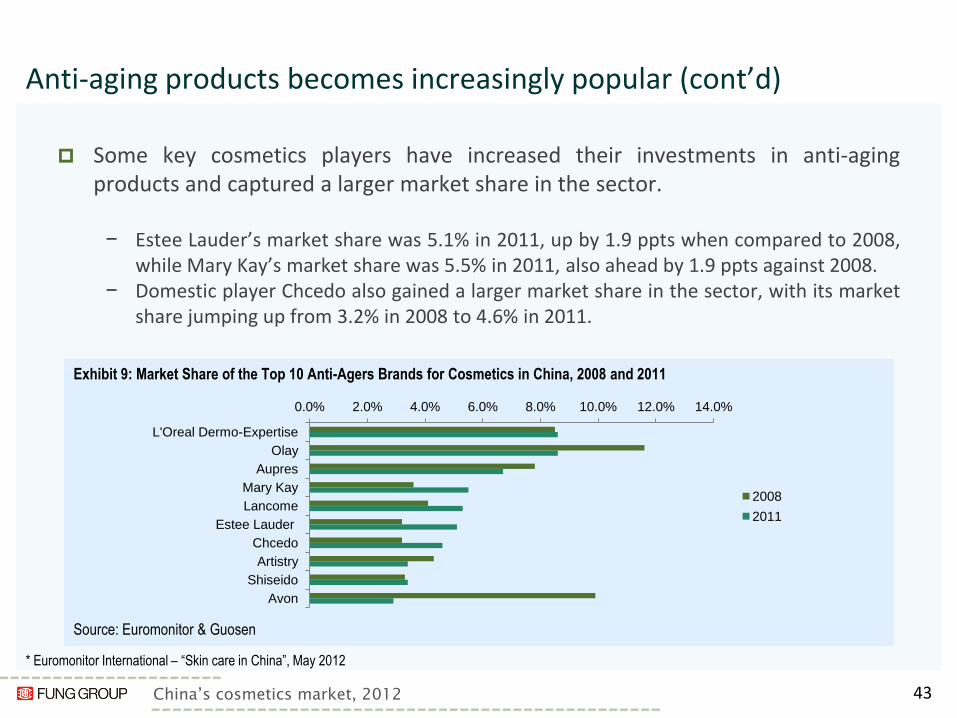

Some key cosmetics players have increased their investments in anti-aging products and captured a larger market share in the sector.

− Estee Lauder’s market share was 5.1% in 2011, up by 1.9 ppts when compared to 2008, while Mary Kay’s market share was 5.5% in 2011, also ahead by 1.9 ppts against 2008.

− Domestic player Chcedo also gained a larger market share in the sector, with its market share jumping up from 3.2% in 2008 to 4.6% in 2011.

43

Exhibit 9: Market Share of the Top 10 Anti-Agers Brands for Cosmetics in China, 2008 and 2011

Source: Euromonitor & Guosen

* Euromonitor International – “Skin care in China”, May 2012

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

L'Oreal Dermo-Expertise

Olay

Aupres

Mary Kay

Lancome

Estee Lauder

Chcedo

Artistry

Shiseido

Avon

2008

2011

China’s cosmetics market, 2012

Anti-aging products becomes increasingly popular (cont’d)

Apart from launching premium anti-aging products, some major players have introduced anti-aging products targeting the mass segment.

− For instance, Olay have launched its anti-aging lines, Regenerist and Pro-X for the mass segment in recent years.

− L’Oreal also introduced its mass anti-aging product, L’Oreal Paris Youth Code Prodigious Rejuvenating Pre-essence in 2011.

44

China’s cosmetics market, 2012

Green cosmetics products are gaining popularity

Green products are products that have less impact on the environment or are less detrimental to human health.

Nowadays, more and more consumers in China are looking for green cosmetics, as cosmetics products are applied directly to the body and excessive chemical substances present in the product may cause skin allergy.

Having identified the huge growth potential, a number of foreign and domestic players have entered the sector.

− Examples of foreign brands include Jurlique, The Body Shop, Origins, Avene, Fancl, and L’Occitane.

− Domestic brands include Longliqi Organic Plus, Inoherb, and Herborist.

45

China’s cosmetics market, 2012

Green cosmetics products are gaining popularity (cont’d)

Chinese consumers’ increasing concerns over product safety has become the major growth driver for green products.

Cosmetics products with natural and chemical-free ingredients benefited remarkably from this trend.

− L’Occitane, an international natural cosmetics brand from France, experienced a 22.7% yoy sales increase in China for the period ended 30 September 2012.

− Japanese natural cosmetics Fancl, which witnessed rapid sales growth in China in recent years, has increased the number of retail stores from 115 in 2010 to 148 in March 2012 in order to cope with Chinese consumers’ strong appetite for green cosmetics products.

46

China’s cosmetics market, 2012

Some old brands have started to rejuvenate

Some time-honored Chinese homegrown brands including Pechoin (百雀羚), Maxam, Shanghai Vive (雙妹), Liushen (六神) and Zhaogui (昭貴) have embarked on brand rejuvenation in recent years. Many of the heritage brands have stepped up their efforts in research and development and introduced new product lines in order to regain lost ground in the market.

A typical example is Shanghai Vive. The homegrown brand, founded in 1898, has caught on again upon its revival in 2010. The brand has changed its product package and formula and introduced a number of new cosmetics products aiming at the mid-to-high end segment in recent years. As at the end of 2012, the brand has successfully set up 15 retail stores in key cities like Shanghai, Beijing and Chengdu.

47

China’s cosmetics market, 2012

Rules and regulations of the cosmetics sector in China

Product safety has long been a major concern in China’s cosmetics market. − In the past years, even famous foreign brands were embroiled in scandal of

defective cosmetics products.

As Chinese consumers are now more discerning, product safety is expected to

gain more attention in the future. More regulations are expected to be launched by the government to better regulate the cosmetics industry.

Exhibit 10 shows some latest rules and regulations related to China’s cosmetics sector.

48

China’s cosmetics market, 2012

Rules and regulations of the cosmetics sector in China (cont’d)

49

Rules and Regulations Publication

Date

Highlights

Guide for Registration and Evaluation of

New Ingredients for Cosmetics *

《化妝品新原料申報與審評指南》

12 May 2011 The Guide aims to strengthen the

administrative licensing of new raw materials

for cosmetics so as to ensure the quality and

safety of cosmetic products.

The CFDA is seeking public opinion on 3T3

Neutral Red Uptake (3T3 NRU) Phototoxicity

Test (Draft) **

國家食品藥品監管局發布《化妝品用化學原料體外3T3中性紅攝取光毒性試驗方法(徵求意見稿)》

10 February

2012

The CFDA proposed an alternative method to

animal testing. The move is considered a very

positive step which could hopefully alter the

requirement for animal test for cosmetics.

Currently, China is the only country in the

world requiring animal testing of cosmetics.

Guide for the Application and Review of

Children's Cosmetics ***

《兒童化妝品申報與審評指南》

22 October

2012

The Guide aims to ensure the quality and

safety of cosmetics for children and further

standardize the application and technical

review of children's cosmetics. It stipulates the

scope of application, principles of formulation,

safety of cosmetics, application requirements

for children's cosmetics and review principles.

Exhibit 10: Selected Rules and Regulations of Cosmetics Sector, 2011-2012

* China Food and Drug Administration - http://www.sda.gov.cn/WS01/CL0846/61608.html

** China Food and Drug Administration - http://www.sda.gov.cn/WS01/CL0781/68975.html

*** China Food and Drug Administration - http://eng.sfda.gov.cn/WS03/CL0757/75588.html

IV. Snapshots of sub-sector performance

50 China’s cosmetics market, 2012

China’s cosmetics market, 2012

Background

The China National Commercial Information Centre (CNCIC) conducts monthly survey to around 200 major department stores* in China to study the performance of different cosmetics sub-sectors.

In this newsletter, performance of 5 sub-sectors is examined: − Shampoos and conditioners − Other hair care products − Skincare products − Color cosmetics − Fragrances

*Note: It is noteworthy that the CNCIC data covers sales in major department stores only.

Retailers of other formats such as professional and specialty stores are growing in popularity. The actual overall market share of cosmetics brands may deviate from the CNCIC data.

51

China’s cosmetics market, 2012

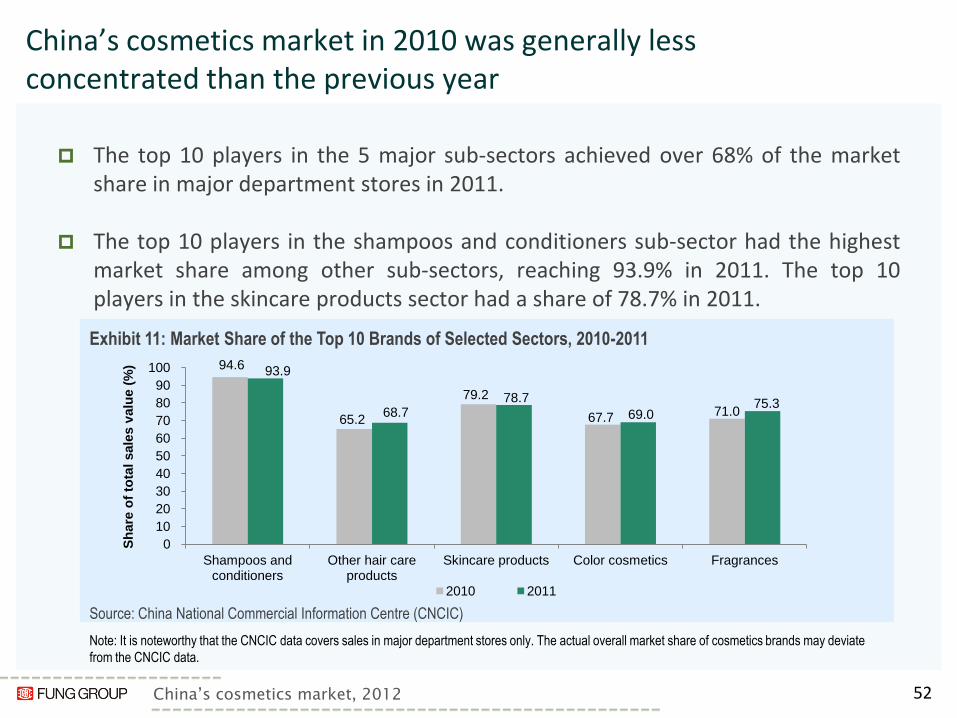

China’s cosmetics market in 2010 was generally less concentrated than the previous year

The top 10 players in the 5 major sub-sectors achieved over 68% of the market share in major department stores in 2011.

The top 10 players in the shampoos and conditioners sub-sector had the highest market share among other sub-sectors, reaching 93.9% in 2011. The top 10 players in the skincare products sector had a share of 78.7% in 2011.

52

94.6

65.2

79.2

67.7 71.0

93.9

68.7 78.7

69.0 75.3

0

10

20

30

40

50

60

70

80

90

100

Shampoos and conditioners

Other hair care products

Skincare products Color cosmetics Fragrances

Sh

are

of

tota

l sale

s v

alu

e (

%)

2010 2011

Source: China National Commercial Information Centre (CNCIC)

Note: It is noteworthy that the CNCIC data covers sales in major department stores only. The actual overall market share of cosmetics brands may deviate

from the CNCIC data.

Exhibit 11: Market Share of the Top 10 Brands of Selected Sectors, 2010-2011

China’s cosmetics market, 2012

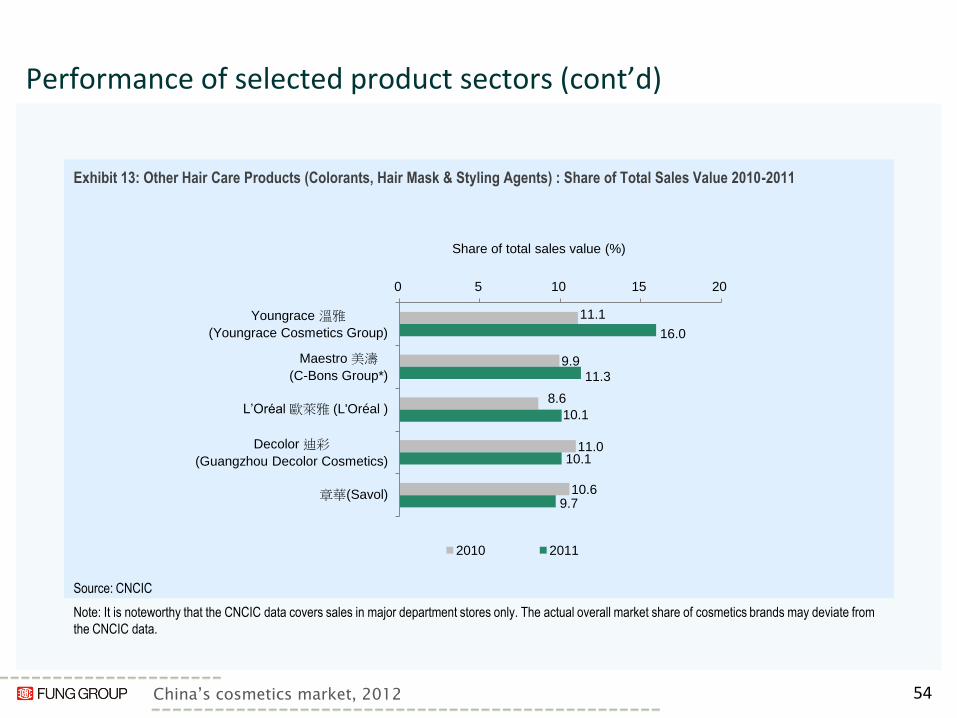

Performance of selected product sectors (cont’d)

53

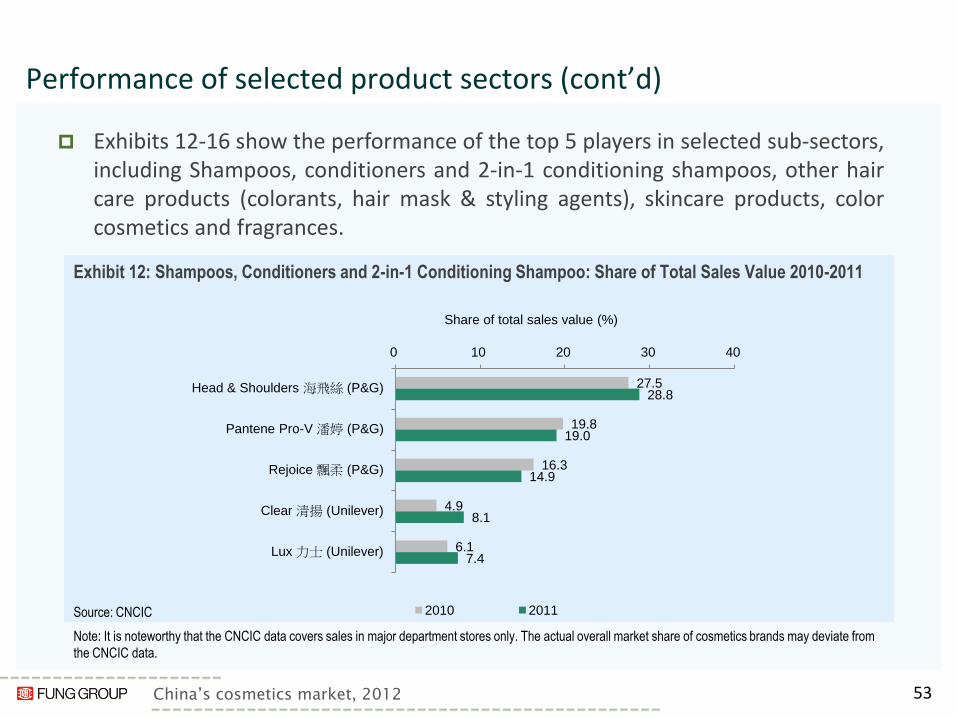

Exhibits 12-16 show the performance of the top 5 players in selected sub-sectors, including Shampoos, conditioners and 2-in-1 conditioning shampoos, other hair care products (colorants, hair mask & styling agents), skincare products, color cosmetics and fragrances.

Note: It is noteworthy that the CNCIC data covers sales in major department stores only. The actual overall market share of cosmetics brands may deviate from

the CNCIC data.

Exhibit 12: Shampoos, Conditioners and 2-in-1 Conditioning Shampoo: Share of Total Sales Value 2010-2011

Source: CNCIC

27.5

19.8

16.3

4.9

6.1

28.8

19.0

14.9

8.1

7.4

0 10 20 30 40

Head & Shoulders 海飛絲 (P&G)

Pantene Pro-V 潘婷 (P&G)

Rejoice 飄柔 (P&G)

Clear 清揚 (Unilever)

Lux 力士 (Unilever)

Share of total sales value (%)

2010 2011

China’s cosmetics market, 2012

Performance of selected product sectors (cont’d)

Exhibit 13: Other Hair Care Products (Colorants, Hair Mask & Styling Agents) : Share of Total Sales Value 2010-2011

54

Source: CNCIC

Note: It is noteworthy that the CNCIC data covers sales in major department stores only. The actual overall market share of cosmetics brands may deviate from

the CNCIC data.

11.1

9.9

8.6

11.0

10.6

16.0

11.3

10.1

10.1

9.7

0 5 10 15 20

Youngrace 溫雅

(Youngrace Cosmetics Group)

Maestro 美濤

(C-Bons Group*)

L’Oréal 歐萊雅 (L'Oréal )

Decolor 迪彩

(Guangzhou Decolor Cosmetics)

章華(Savol)

Share of total sales value (%)

2010 2011

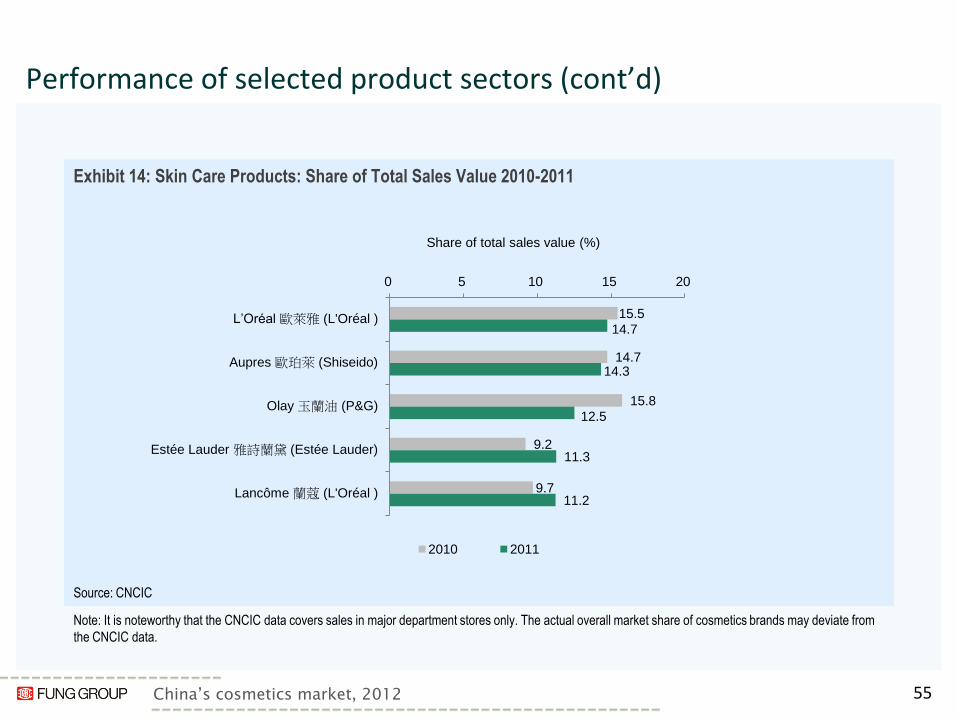

China’s cosmetics market, 2012

Performance of selected product sectors (cont’d)

Exhibit 14: Skin Care Products: Share of Total Sales Value 2010-2011

55

Source: CNCIC

Note: It is noteworthy that the CNCIC data covers sales in major department stores only. The actual overall market share of cosmetics brands may deviate from

the CNCIC data.

15.5

14.7

15.8

9.2

9.7

14.7

14.3

12.5

11.3

11.2

0 5 10 15 20

L’Oréal 歐萊雅 (L'Oréal )

Aupres 歐珀萊 (Shiseido)

Olay 玉蘭油 (P&G)

Estée Lauder 雅詩蘭黛 (Estée Lauder)

Lancôme 蘭蔻 (L'Oréal )

Share of total sales value (%)

2010 2011

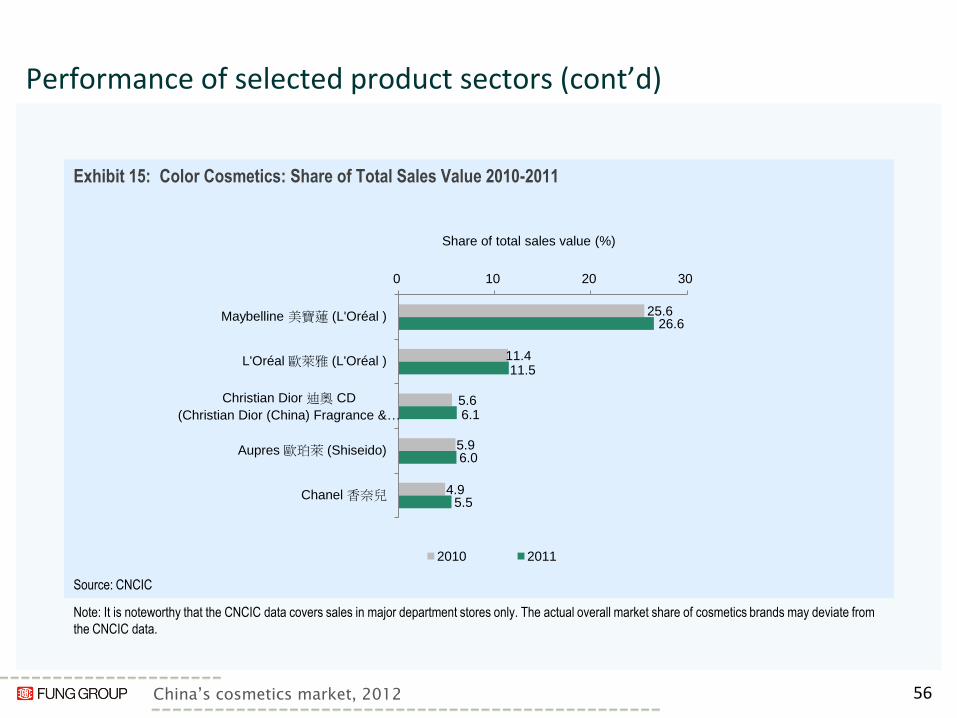

China’s cosmetics market, 2012

Performance of selected product sectors (cont’d)

Exhibit 15: Color Cosmetics: Share of Total Sales Value 2010-2011

56

Source: CNCIC

Note: It is noteworthy that the CNCIC data covers sales in major department stores only. The actual overall market share of cosmetics brands may deviate from

the CNCIC data.

25.6

11.4

5.6

5.9

4.9

26.6

11.5

6.1

6.0

5.5

0 10 20 30

Maybelline 美寶蓮 (L'Oréal )

L'Oréal 歐萊雅 (L'Oréal )

Christian Dior 迪奧 CD

(Christian Dior (China) Fragrance & …

Aupres 歐珀萊 (Shiseido)

Chanel 香奈兒

Share of total sales value (%)

2010 2011

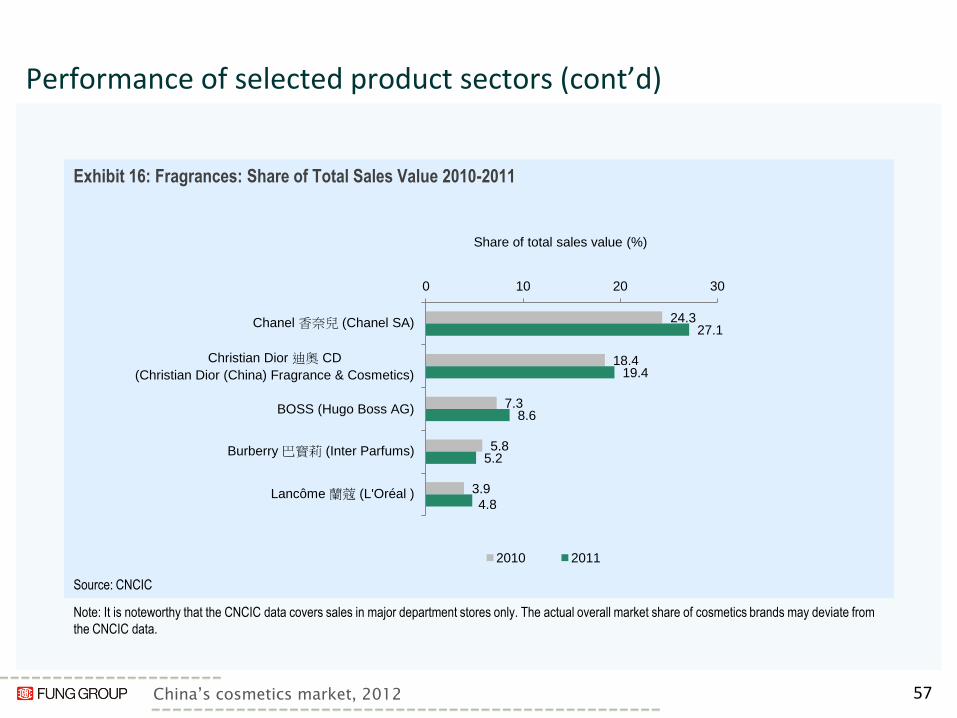

China’s cosmetics market, 2012

24.3

18.4

7.3

5.8

3.9

27.1

19.4

8.6

5.2

4.8

0 10 20 30

Chanel 香奈兒 (Chanel SA)

Christian Dior 迪奧 CD

(Christian Dior (China) Fragrance & Cosmetics)

BOSS (Hugo Boss AG)

Burberry 巴寳莉 (Inter Parfums)

Lancôme 蘭蔻 (L'Oréal )

Share of total sales value (%)

2010 2011

Performance of selected product sectors (cont’d)

Exhibit 16: Fragrances: Share of Total Sales Value 2010-2011

57

Source: CNCIC

Note: It is noteworthy that the CNCIC data covers sales in major department stores only. The actual overall market share of cosmetics brands may deviate from

the CNCIC data.

Fung Business Intelligence Center 10/F, LiFung Tower, 888 Cheung Sha Wan Road, Kowloon, Hong Kong Tel: 2300 2470 Fax: 2635 1598 Email: [email protected] http://www.lifunggroup.com/

For more information

© Copyright 2013 Fung Business Intelligence Center . All rights reserved.

Though the Fung Business Intelligence Center endeavours to have information presented in this document as accurate and updated as possible, it accepts no responsibility for any error, omission or misrepresentation. Fung Business Intelligence Center and/or its associates accept no responsibility for any direct, indirect or consequential loss that may arise from the use of information contained in this document.

China’s cosmetics market, 2012

Related Documents