China Should we fear the red dragon?

China Should we fear the red dragon? China first entered the international stage in the 1800s. There was increasing European demand for tea, silk, and.

Dec 20, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

China

Should we fear the red dragon?

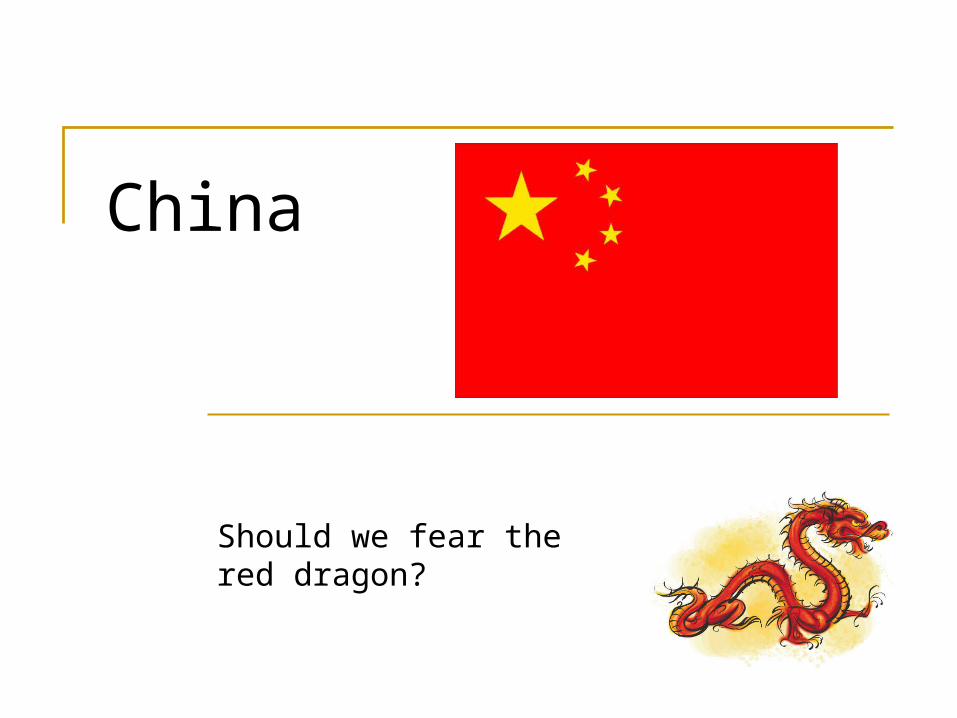

China first entered the international stage in the 1800s. There was increasing European demand for tea, silk, and porcelain from China, but the Chinese didn’t want anything the Europeans had to offer ….the problems was solved by including India

TextilesCotton

Opium

Tea, Silk

The emperor tried to end the opium trade by seizing opium imports. The British responded by crushing the Chinese (the Opium War) – The British were awarded the island of Hong Kong

A left turn

On October 1, 1949, the People's Republic of China was formally established, with its national capital at Beijing. The country was led by the Chinese Communist Party under the Chairmanship of Mao Zedong

China adopted “Five Year Plans” to achieve industrialization and agricultural collectivism. The most noted of these plans was the “Great Leap Forward” which was a disaster!

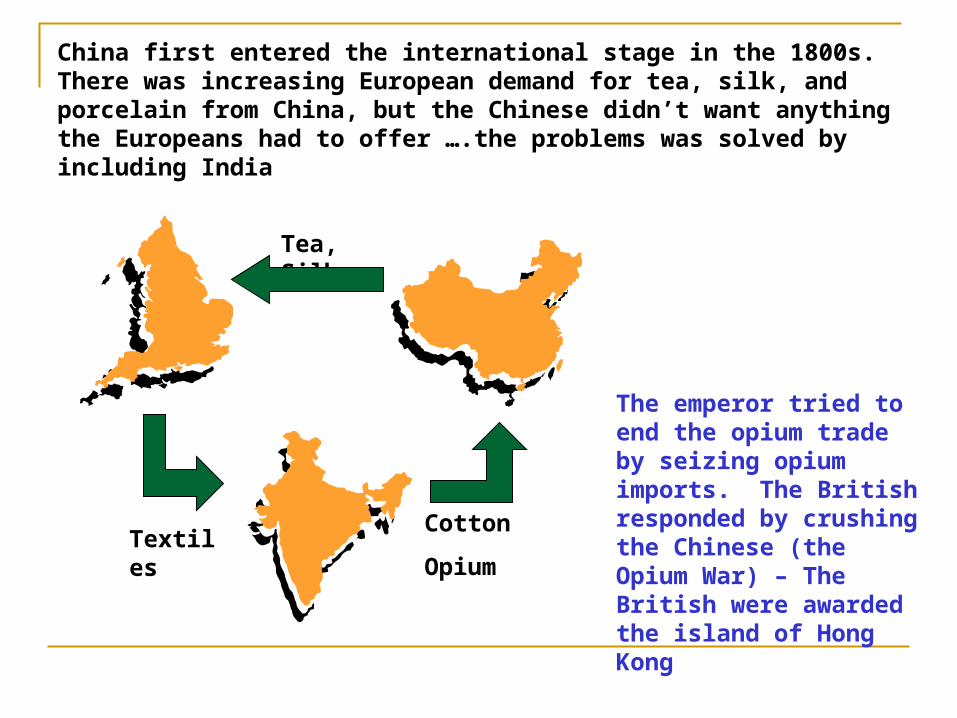

Modern Day China…Hu Jintao became head of China's ruling Communist Party in late 2002

GDP (2005): $8.182T (#4)

Population: 1.314B (#1)

GDP per Capita: $6,300

GDP Growth: 9.7%

Trade Position: $120B Surplus (1.47% of GDP)

Gross Investment: $3.567T (43% of GDP)

0

2

4

6

8

10

12

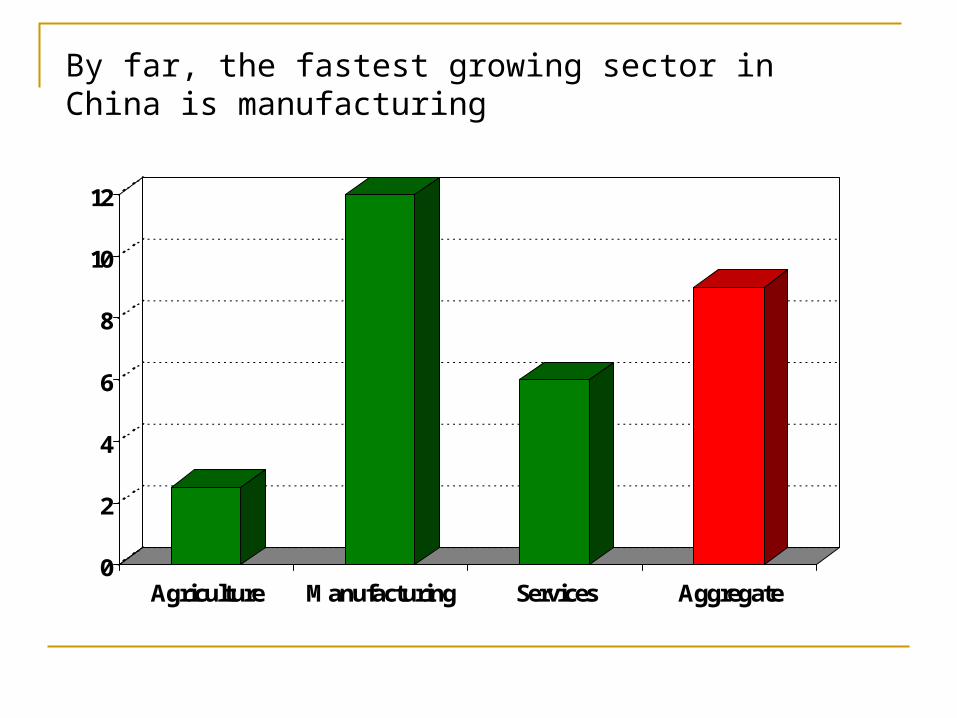

Agriculture Manufacturing Services Aggregate

By far, the fastest growing sector in China is manufacturing

0

5

10

15

20

25

30

Consumption Government Investment Import/Export

The largest growing component of the Chinese economy is its external accounts (import & exports). This is not by accident, but by design.

China has accounted for 25-30% of the growth in total world consumption – most notable raw materials and energy

Oil prices have risen as high as $72 The index of metals prices is up 50% over last year Shipping activity is double what it was last year

In recent years, China outspent the US in virtually every commodity!!

The Chinese are spending like drunken sailors!

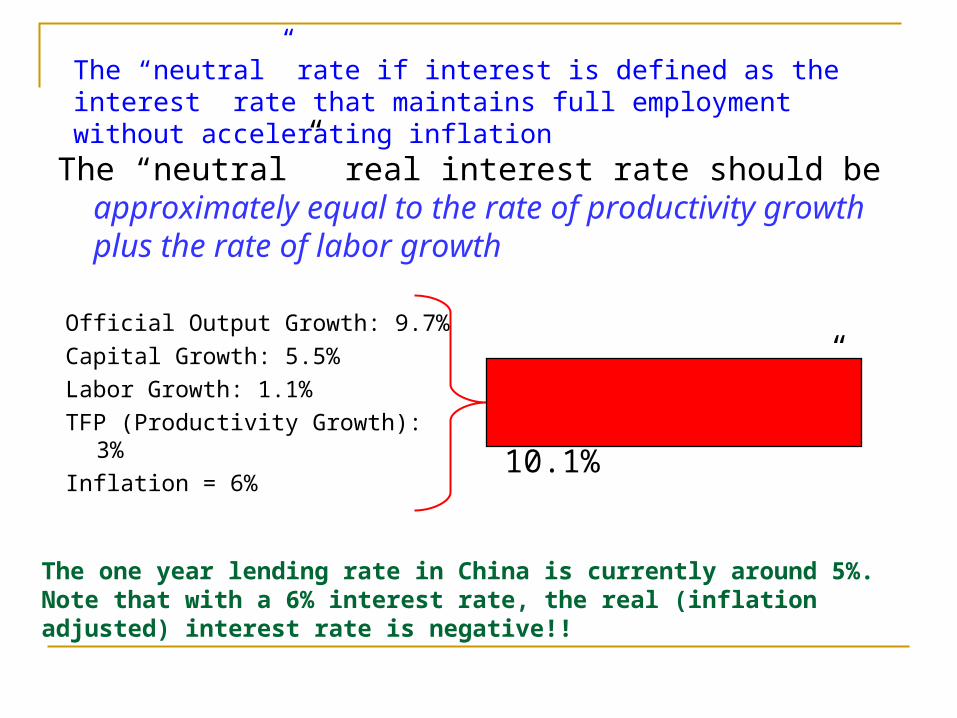

The “neutral” real interest rate should be approximately equal to the rate of productivity growth plus the rate of labor growth

Official Output Growth: 9.7%

Capital Growth: 5.5%

Labor Growth: 1.1%

TFP (Productivity Growth): 3%

Inflation = 6%

Implied “Neutral” Interest Rate: 10.1%

The “neutral” rate if interest is defined as the interest rate that maintains full employment without accelerating inflation

The one year lending rate in China is currently around 5%. Note that with a 6% interest rate, the real (inflation adjusted) interest rate is negative!!

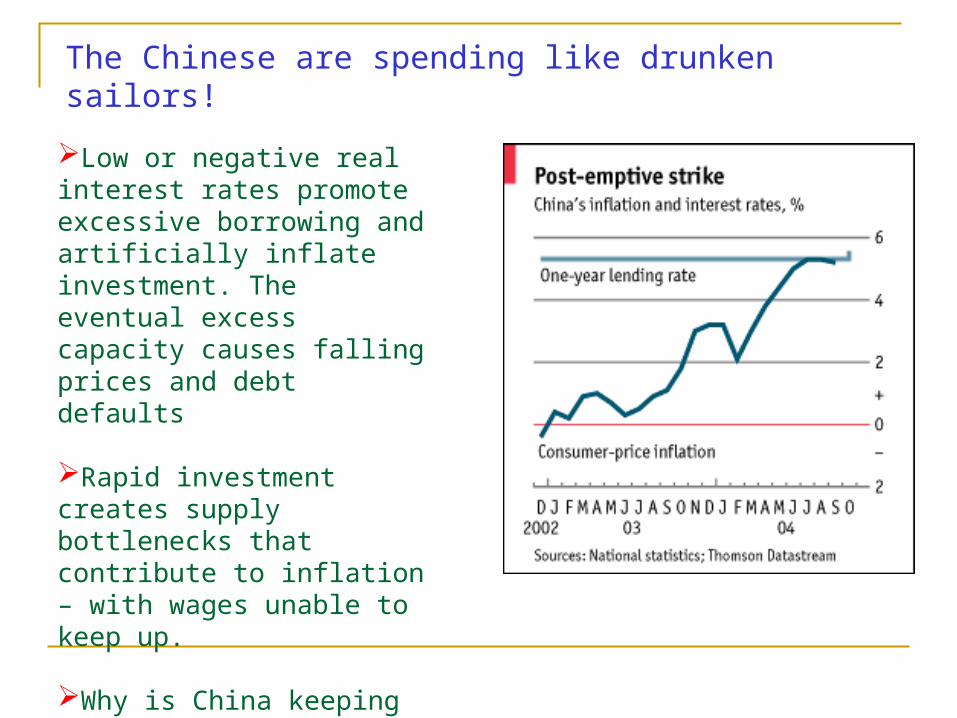

Low or negative real interest rates promote excessive borrowing and artificially inflate investment. The eventual excess capacity causes falling prices and debt defaults

Rapid investment creates supply bottlenecks that contribute to inflation – with wages unable to keep up.

Why is China keeping interest rates so low?

The Chinese are spending like drunken sailors!

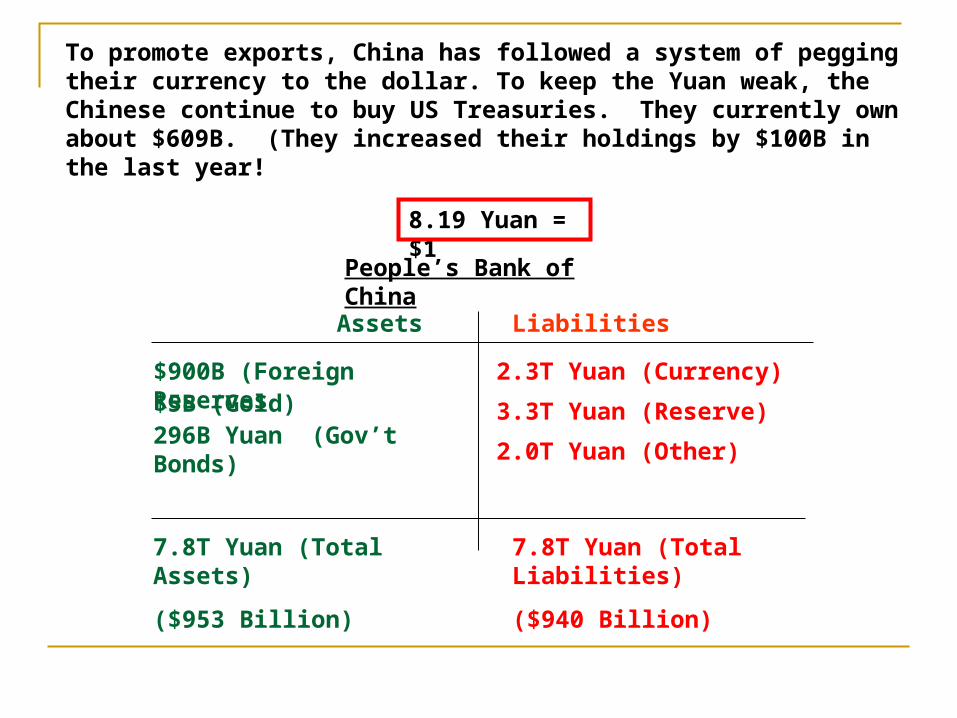

To promote exports, China has followed a system of pegging their currency to the dollar. To keep the Yuan weak, the Chinese continue to buy US Treasuries. They currently own about $609B. (They increased their holdings by $100B in the last year!

Assets Liabilities

$900B (Foreign Reserves 2.3T Yuan (Currency)

People’s Bank of China

3.3T Yuan (Reserve)

2.0T Yuan (Other)

7.8T Yuan (Total Liabilities)

($940 Billion)

8.19 Yuan = $1

$5B (Gold)296B Yuan (Gov’t Bonds)

7.8T Yuan (Total Assets)

($953 Billion)

Is the Red Dragon Heading for Trouble?

Year Total Factor Productivity Growth

1991 Agriculture Industry Construction Transportation Services

1992 -2% 9% 35% -16% 10%

1993 -1% 8% 30% -11% 7%

1994 0% 6% 24% -5% 4%

1995 1% 4% 18% 1% 1%

1996 3% 2% 13% 6% -2%

1997 4% 1% 7% 12% -5%

1998 5% -1% 2% 17% -8%

Recent Productivity gains (with the exception of Telecommunications) is less than stellar!

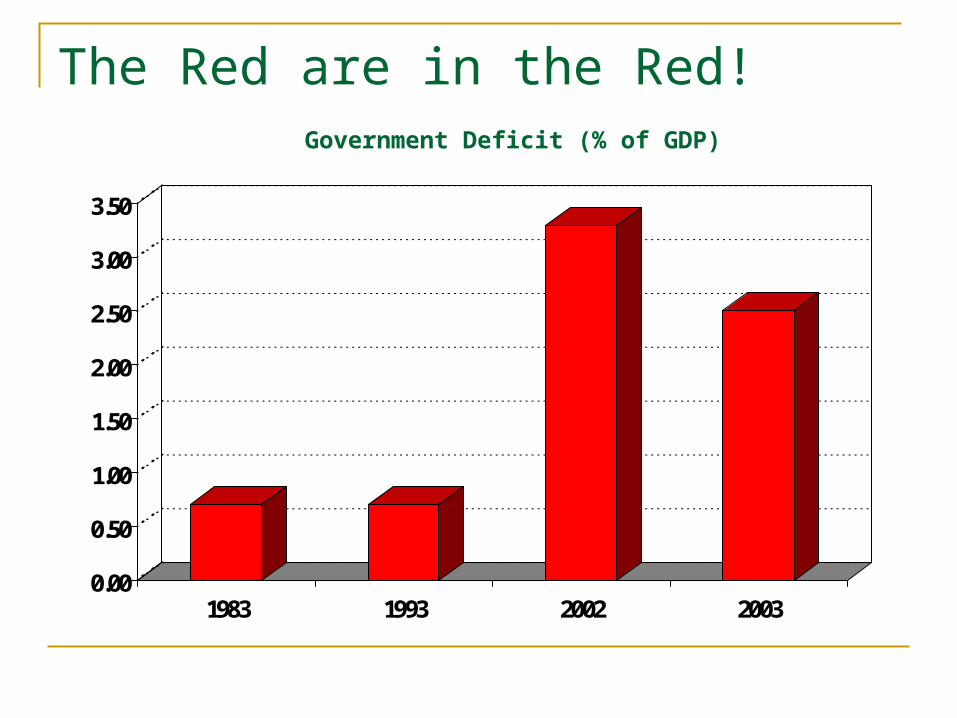

The Red are in the Red!

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

1983 1993 2002 2003

Government Deficit (% of GDP)

China’s Financial System is Extremely Fragile!

The Chinese financial system is dominated by four state run banks

According to Beijing, the NPL (non-performing loans) ratio of the Big Four state banks is 30% of assets

More objective private financial analysts say NPLs represent 50% of the total assets of the Big Four banks

Fitch IBCA and Moody's say the Big Four state banks are technically insolvent.

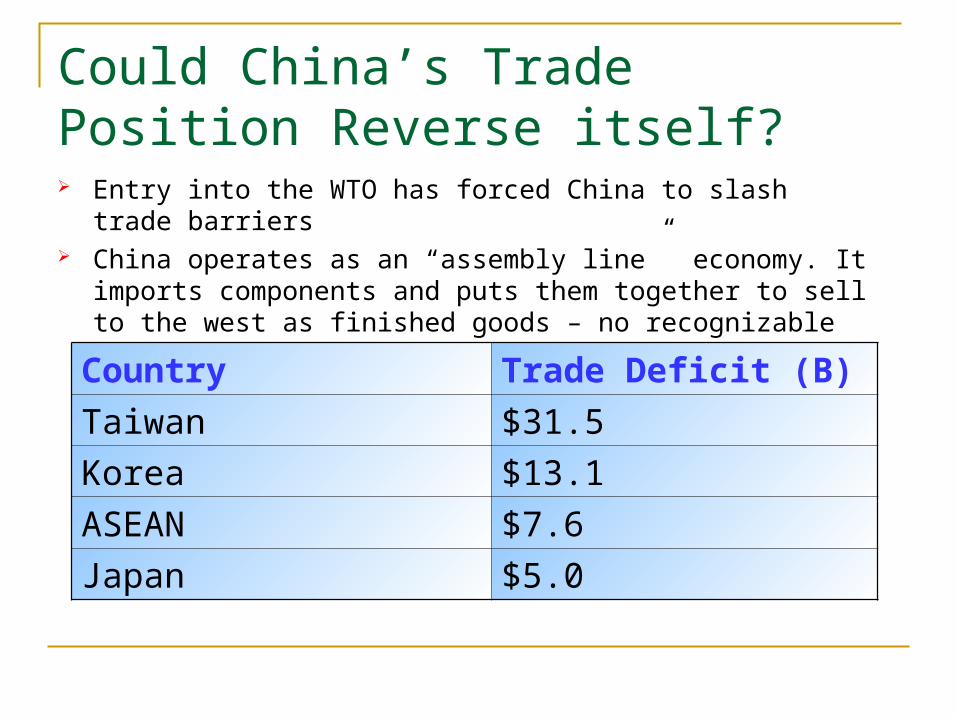

Could China’s Trade Position Reverse itself? Entry into the WTO has forced China to slash trade barriers China operates as an “assembly line” economy. It imports

components and puts them together to sell to the west as finished goods – no recognizable brand names

Country Trade Deficit (B)

Taiwan $31.5

Korea $13.1

ASEAN $7.6

Japan $5.0

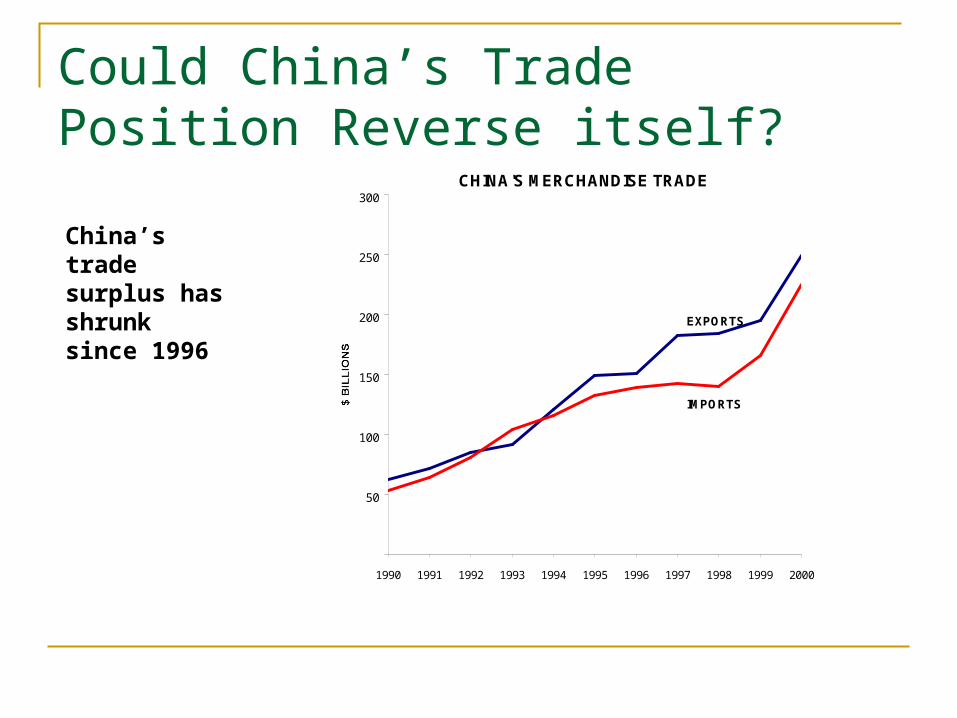

Could China’s Trade Position Reverse itself?

CHINA'S MERCHANDISE TRADE

50

100

150

200

250

300

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000

EXPORTS

IMPORTS

China’s trade surplus has shrunk since 1996

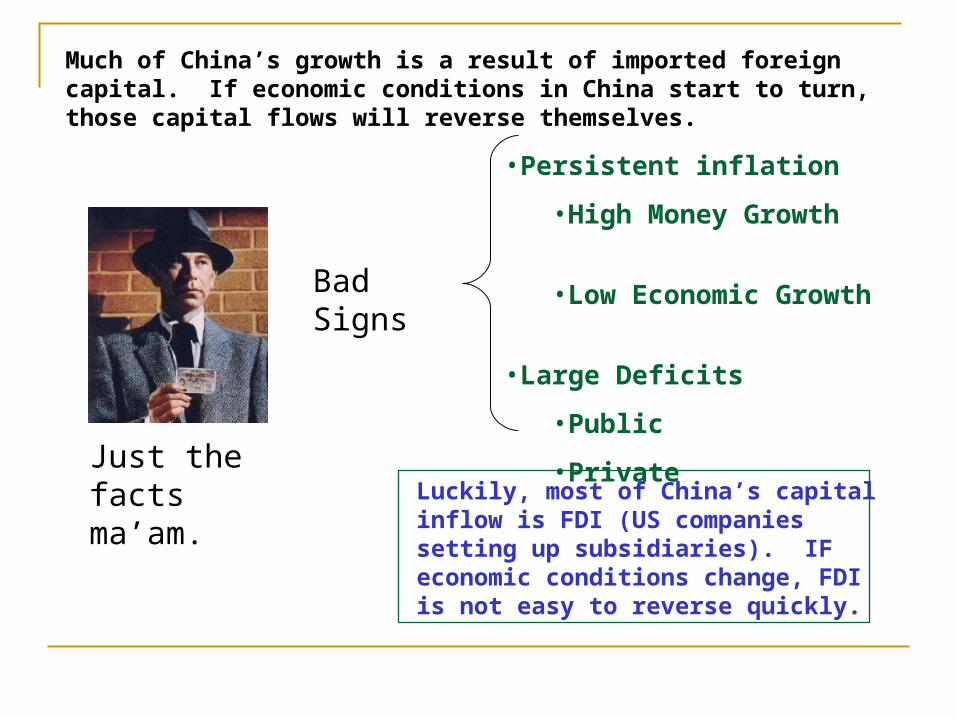

Just the facts ma’am.

•Persistent inflation

•High Money Growth

•Low Economic Growth

•Large Deficits

•Public

•Private

Bad Signs

Luckily, most of China’s capital inflow is FDI (US companies setting up subsidiaries). IF economic conditions change, FDI is not easy to reverse quickly.

Much of China’s growth is a result of imported foreign capital. If economic conditions in China start to turn, those capital flows will reverse themselves.

Related Documents