www.jpmorganmarkets.com Asia Pacific Credit Research 04 June 2018 China Local Government Financing Vehicles A rough (and tough) ride ahead given limited transparency, but there are alternatives Asia Corporate Research Varun Ahuja, CFA AC (852) 2800 6038 [email protected] Tiantian Teng AC (852) 2800-7024 [email protected] J.P. Morgan Securities (Asia Pacific) Limited See page 33 for analyst certification and important disclosures. J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. The emergence of LGFVs and their growing representation in the USD bond markets continues to catch investor interest. Major policy shifts have raised questions as to whether all LGFV can be considered provincial debt, and this is further underscored by recent onshore defaults, including some SOEs, leading to more muted supply and wider spreads for the LGFV sector. In this report, we present an update on recent policy changes as well as our views on their impact on the LGFV sector. In an environment where onshore default rates are rising and transparency stays low, we remain cautious on the sector as a whole, preferring to own stronger SOEs rather than LGFVs. That said, we do make exceptions for a few LGFVs that play strong policy roles (willingness) and backed by stronger provincial governments (capacity). We also believe that while one or a few LGFV defaults would be acceptable to the central government, widespread defaults are unlikely given the larger implications for the financial sector. We initiate coverage of Wuhan Metro and its ‘19s with OW, Neutral on BJSTAT and its ‘20s and ‘25s, on Yanzhou Coal and its perps ‘c20s, '22s with OW with the bonds trading wider than even Indika, which we think does not make complete sense. The central government would continue to make LGFVs more market- oriented, as part of the ongoing deleveraging drive. Since the budget law revision in 2014, the government has released a number of documentations around LGFV operations and their funding, which we discuss in this note. Pace of issuance has slowed down in recent times. The issuance of LGFVs USD bonds had increased substantially over 2015-2017 due to onshore issuance policy tightening as well as LGFV’s funding diversification. However, this has slowed drastically in recent months, due to the central government’s tightening policy to address debt overhang problems in the system. In addition, recent onshore defaults have given further apprehension about exposure to the sector, where underlying information flow remains very limited. Staying cautious on sector and preference for LGFVs with clear policy role only. While LGFVs have risen to be a ‘too big to ignore’ sector in JACI, the lack of information flow and opacity in underlying businesses remain key concerns, especially in the current environment. We would stick to LGFVs with clear strategically important roles and ideally with decent standalone credit profiles. Having said that, there are certain LGFVs that are quite wide in the 1-2yr duration bucket, which present investors with the conundrum of missing out on better yields if not invested but having a high ‘jump risk’ if any of these LGFVs widen materially due to financial constraints, which are difficult to monitor given inadequate underlying information flow. Hence, in this note, while we categorize LGFVs based on factors such as policy role, social and economic importance, etc., given that most LGFVs are trading as a ‘group’ in different yield buckets, we would look to take selective exposure in LGFVs through credits in the ‘preferred’ and ‘some comfort’ categories, while for exposure to higher yields, we are more comfortable with the risk-reward and information flow in other China SOEs and HY corporates as presented in this report. Completed 04 Jun 2018 05:55 PM HKT Disseminated 04 Jun 2018 06:08 PM HKT

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

www.jpmorganmarkets.com

Asia Pacific Credit Research04 June 2018

China Local Government Financing VehiclesA rough (and tough) ride ahead given limited transparency, but there are alternatives

Asia Corporate Research

Varun Ahuja, CFA AC

(852) 2800 6038

Tiantian Teng AC

(852) 2800-7024

J.P. Morgan Securities (Asia Pacific) Limited

See page 33 for analyst certification and important disclosures.J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

The emergence of LGFVs and their growing representation in the USD bond markets continues to catch investor interest. Major policy shifts have raised questions as to whether all LGFV can be considered provincial debt, and this is further underscored by recent onshore defaults, including some SOEs, leading to more muted supply and wider spreads for the LGFV sector. In this report, we present an update on recent policy changes as well as our views on their impact on the LGFV sector. In an environment where onshore default rates are rising and transparency stays low, we remain cautious on the sector as a whole, preferring to own stronger SOEs rather than LGFVs. That said, we do make exceptions for a few LGFVs that play strong policy roles (willingness) and backed by stronger provincial governments (capacity). We also believe that while one or a few LGFVdefaults would be acceptable to the central government, widespread defaults are unlikely given the larger implications for the financial sector. We initiate coverage of Wuhan Metro and its ‘19s with OW, Neutral on BJSTAT and its ‘20s and ‘25s, on Yanzhou Coal and its perps ‘c20s, '22s with OW with the bonds trading wider than even Indika, which we think does not make complete sense.

The central government would continue to make LGFVs more market-oriented, as part of the ongoing deleveraging drive. Since the budget law revision in 2014, the government has released a number of documentations around LGFV operations and their funding, which we discuss in this note.

Pace of issuance has slowed down in recent times. The issuance of LGFVs USD bonds had increased substantially over 2015-2017 due to onshore issuance policy tightening as well as LGFV’s funding diversification. However, this has slowed drastically in recent months, due to the central government’s tightening policy to address debt overhang problems in the system. In addition, recent onshore defaults have given further apprehension about exposure to the sector,where underlying information flow remains very limited.

Staying cautious on sector and preference for LGFVs with clear policy role only. While LGFVs have risen to be a ‘too big to ignore’ sector in JACI, the lack of information flow and opacity in underlying businesses remain key concerns,especially in the current environment. We would stick to LGFVs with clear strategically important roles and ideally with decent standalone credit profiles.

Having said that, there are certain LGFVs that are quite wide in the 1-2yr duration bucket, which present investors with the conundrum of missing out on better yields if not invested but having a high ‘jump risk’ if any of these LGFVs widen materially due to financial constraints, which are difficult to monitor given inadequate underlying information flow.

Hence, in this note, while we categorize LGFVs based on factors such as policy role, social and economic importance, etc., given that most LGFVs are trading as a ‘group’ in different yield buckets, we would look to take selective exposure in LGFVs through credits in the ‘preferred’ and ‘some comfort’categories, while for exposure to higher yields, we are more comfortable with the risk-reward and information flow in other China SOEs and HY corporates as presented in this report.

Completed 04 Jun 2018 05:55 PM HKTDisseminated 04 Jun 2018 06:08 PM HKT

2

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Table of ContentsOnshore defaults back in focus ..............................................3

LGFV policy changes in recent years.....................................5

Document No.50 & No.87: weakening the ties between local governments and LGFVs....................................................................................................................5

Relative value............................................................................7

Sector strategy and key recommendations ...........................9

Background of LGFVs ..........................................................................................16

Categorization of LGFVs........................................................18

Technicals: Less negative due to lower supply but investor base still narrow .....................................................................20

Bond supply should slow going forward ................................................................21

Investor base remains narrow as Asia continues to dominate ..................................22

Background of Individual LGFVs..........................................24

3

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Onshore defaults back in focus

Focus is back on onshore defaults, especially from the weaker government-owned entities, after China Energy Reserve and Chemicals Group (CERCG, not covered) defaulted on the principal repayment of its US$350 million offshore bonds,which triggered a cross-default to all of its outstanding debt.

While the company classifies itself as an SOE in the bond prospectus, there remains a question-mark on the company's actual shareholding structure, as per newswires (e.g. Debtwire and other local news). The company was reportedly ~30% owned by the Beijing Municipal Commission of Commerce, 28% by CNPC through its engineering arm; and ~15% by China Economic Cooperation Center, however, its shareholding structure has since changed based on the company’s latest presentation.

Interestingly, just a few months ago, the company was in news (source: SCMP) to buya marquee commercial building in Central, Hong Kong, from CK Assets for ~US$5 billion. CERCG is involved in the oil & gas trading, logistics and distribution, etc. segments. In its disclosure announcement post its principal repayment default, it guided that it is unable to make the payment due to tightening conditions in the PRC over the last two years, which restricted its financing channels, including access to bank funding. As per CERCG, it aims to divest some assets to improve its cash flow situation.

Separately, there has been more news on LGFV defaults. Reuters recently reported that a firm controlled by a city government in Inner Mongolia region hadfailed to pay interest and principals on about RMB4 billion of off balance sheet loans. The article suggested that the firm should be technically in default after missing payments but more information is needed to determine whether it wasactually a missing payment or a delayed payment.

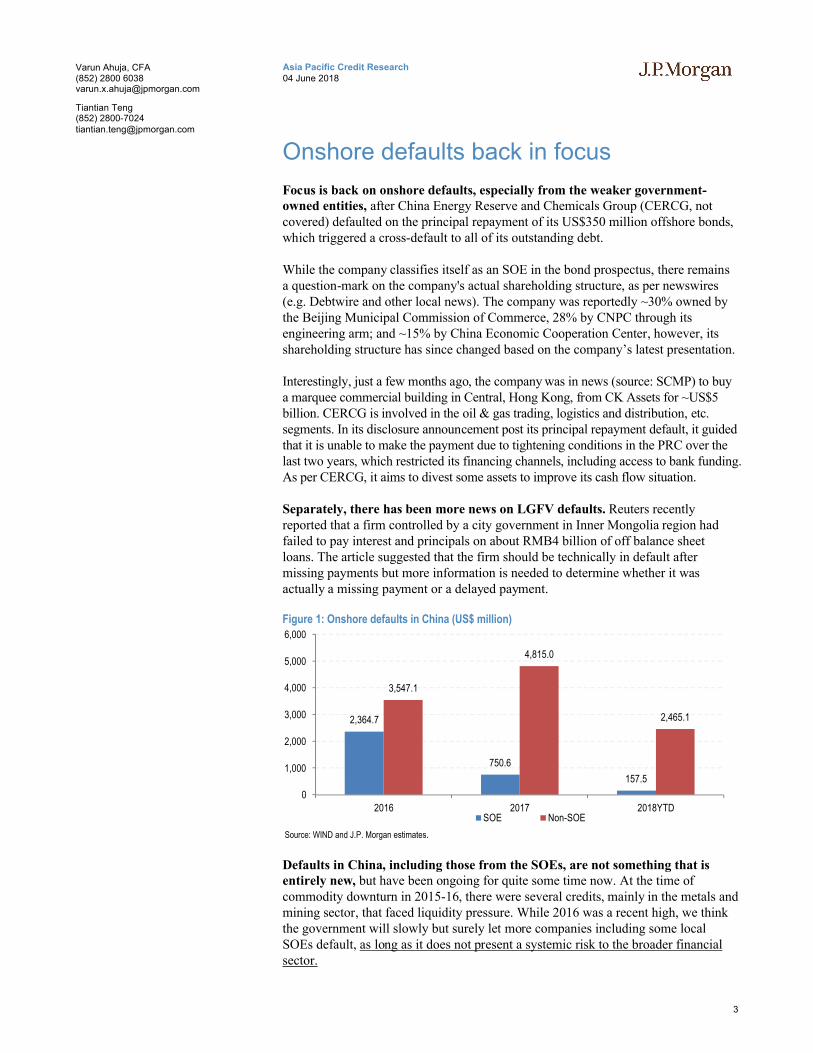

Figure 1: Onshore defaults in China (US$ million)

Source: WIND and J.P. Morgan estimates.

Defaults in China, including those from the SOEs, are not something that is entirely new, but have been ongoing for quite some time now. At the time of commodity downturn in 2015-16, there were several credits, mainly in the metals and mining sector, that faced liquidity pressure. While 2016 was a recent high, we think the government will slowly but surely let more companies including some local SOEs default, as long as it does not present a systemic risk to the broader financial sector.

2,364.7

750.6

157.5

3,547.1

4,815.0

2,465.1

0

1,000

2,000

3,000

4,000

5,000

6,000

2016 2017 2018YTDSOE Non-SOE

4

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

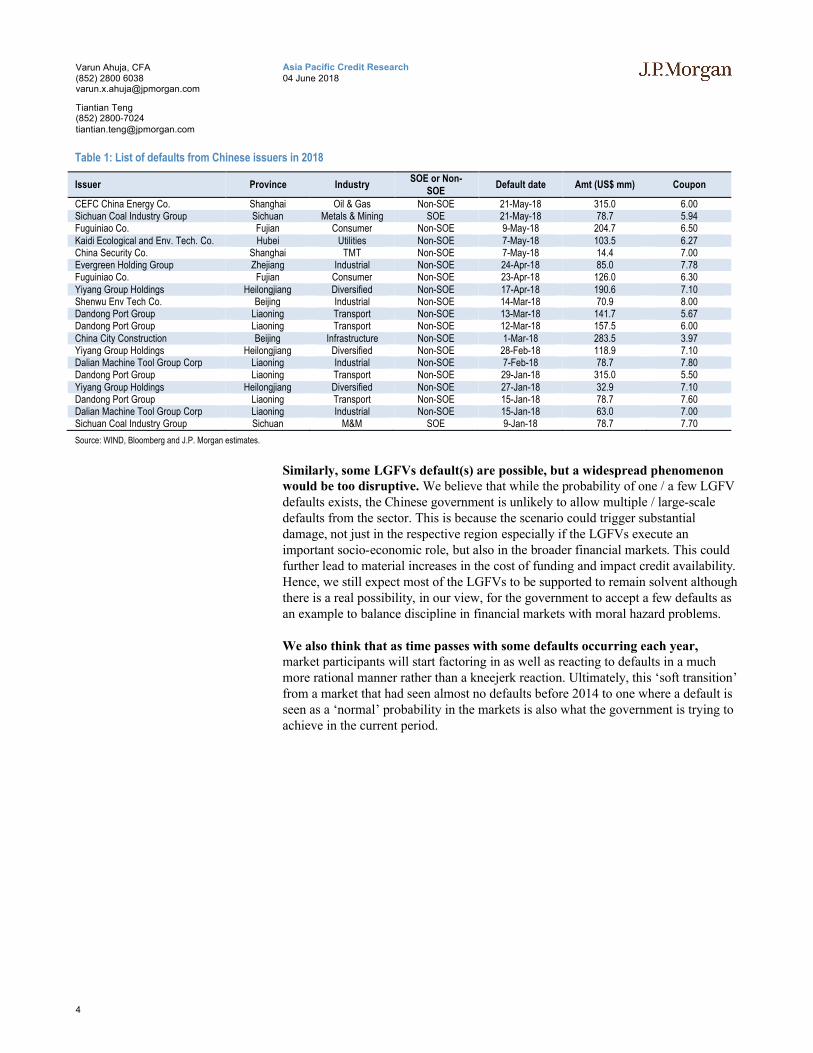

Table 1: List of defaults from Chinese issuers in 2018

Issuer Province IndustrySOE or Non-

SOEDefault date Amt (US$ mm) Coupon

CEFC China Energy Co. Shanghai Oil & Gas Non-SOE 21-May-18 315.0 6.00Sichuan Coal Industry Group Sichuan Metals & Mining SOE 21-May-18 78.7 5.94Fuguiniao Co. Fujian Consumer Non-SOE 9-May-18 204.7 6.50Kaidi Ecological and Env. Tech. Co. Hubei Utilities Non-SOE 7-May-18 103.5 6.27China Security Co. Shanghai TMT Non-SOE 7-May-18 14.4 7.00Evergreen Holding Group Zhejiang Industrial Non-SOE 24-Apr-18 85.0 7.78Fuguiniao Co. Fujian Consumer Non-SOE 23-Apr-18 126.0 6.30Yiyang Group Holdings Heilongjiang Diversified Non-SOE 17-Apr-18 190.6 7.10Shenwu Env Tech Co. Beijing Industrial Non-SOE 14-Mar-18 70.9 8.00Dandong Port Group Liaoning Transport Non-SOE 13-Mar-18 141.7 5.67Dandong Port Group Liaoning Transport Non-SOE 12-Mar-18 157.5 6.00China City Construction Beijing Infrastructure Non-SOE 1-Mar-18 283.5 3.97Yiyang Group Holdings Heilongjiang Diversified Non-SOE 28-Feb-18 118.9 7.10Dalian Machine Tool Group Corp Liaoning Industrial Non-SOE 7-Feb-18 78.7 7.80Dandong Port Group Liaoning Transport Non-SOE 29-Jan-18 315.0 5.50Yiyang Group Holdings Heilongjiang Diversified Non-SOE 27-Jan-18 32.9 7.10Dandong Port Group Liaoning Transport Non-SOE 15-Jan-18 78.7 7.60Dalian Machine Tool Group Corp Liaoning Industrial Non-SOE 15-Jan-18 63.0 7.00Sichuan Coal Industry Group Sichuan M&M SOE 9-Jan-18 78.7 7.70

Source: WIND, Bloomberg and J.P. Morgan estimates.

Similarly, some LGFVs default(s) are possible, but a widespread phenomenon would be too disruptive. We believe that while the probability of one / a few LGFV defaults exists, the Chinese government is unlikely to allow multiple / large-scale defaults from the sector. This is because the scenario could trigger substantial damage, not just in the respective region especially if the LGFVs execute an important socio-economic role, but also in the broader financial markets. This could further lead to material increases in the cost of funding and impact credit availability. Hence, we still expect most of the LGFVs to be supported to remain solvent although there is a real possibility, in our view, for the government to accept a few defaults as an example to balance discipline in financial markets with moral hazard problems.

We also think that as time passes with some defaults occurring each year, market participants will start factoring in as well as reacting to defaults in a much more rational manner rather than a kneejerk reaction. Ultimately, this ‘soft transition’from a market that had seen almost no defaults before 2014 to one where a default is seen as a ‘normal’ probability in the markets is also what the government is trying to achieve in the current period.

5

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

LGFV policy changes in recent years

Since the budget law revision in 2014, the government has taken further steps to tighten policies on local government funding and LGFVs’ borrowing activities. Government authorities released Article No. 43 in 2014 and Article No. 4 in 2016 to separate the financing function of LGFVs from local governments and to prevent LGFVs from using land pledges to obtain financing.

Higher-tier local governments were only allowed to issue bonds directly but not through LGFVs or enterprises. The authorities also introduced the bond swap program to refinance legacy LGFV debts – basically it is a practice to swap LGFV debts into lower-yielding munis so that interest on these products can be effectively reduced.

The government thereafter introduced several more regulatory measures, including:1) Document No. 50 (May-2017), which reinforces the policy goal of Article No. 43 to prohibit local government off-budget borrowing, 2) Document No. 87 (June-2017), which prohibits illegal financing behavior in purchasing certain services of LGFVs by local governments. The most recent development was in April 2018, the Ministry of Finance (MoF) released Notice 23 to regulate state-owned bank lending activities, particularly to LGFVs.

Notice 23: curbing financing sources to LGFVs

Notice 23 was released by the Ministry of Finance in April, mainly towards state-owned bank lending activities and targets, among which LGFVs were included. The Notice guided that banks should not aggressively lend to local governments for new projects, investment funds or PPP projects. It is consistent with the central government’s deleveraging campaign by curbing several expansionaryinfrastructure projects to prevent further leverage build-up in the financial system.

This policy update (Notice 23) also pointed out that when state-owned financial institutions serve as underwriters, they must assess the issuers’ ability to repay and are not allowed to indicate implicit or direct local government support. Stricter underwriting standards should make funding availability somewhat tighter for several LGFVs, from banks or capital markets.

Document No.50 & No.87: weakening the ties between local governments and LGFVs

Document No.50 was jointly issued by the Ministry of Finance, the Development and Reform Commission, the central bank and the Ministry of Justice and Securities and banking regulators. It carries the same policy agenda as of Article No. 43, but stresses more on prohibiting any implicit government guarantee on LGFVfinancing. It prohibits local governments from raising debt via PPP projects, pledging future land sales into LGFVs or executing land sales to repay debt. The document pointed out that local governments should swap their existing debt with more transparent muni-bonds, with the additional purpose of lowering funding costs. Local governments are urged to more thoroughly inspect financing activities and regularlydisclose their government debt information. On the other hand, LGFVs are obliged to declare a lack of local government guarantee in writing if they plan to raise onshore debt. Lastly, a cross-department supervisory mechanism was proposed as well, having both fiscal and financial ministries and commissions to co-operatively supervise and oversee local governments’ financing activities, LGFVs debt and financial institutions’lending activities.

6

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Document No. 87 was released right after Document No. 50 by the Ministry of Finance, for the main purpose of further regulating local government illegal financing activities. The document prohibits local government from financing projects through certain asset and/or service purchase routes, effectively reducing sources of LGFVs revenues that were previously generated directly from local governments.

New regulator appointees signaling deleveraging policy continuity

The central government shuffled several key positions in the country’s top regulatory authorities and expanded the scope of responsibility of such authorities. The 13th National People’s Congress noted that more responsibilities will be carried by the National Audit Office (NAO) and proposed to reform the previously separated national and local taxation system by integrating the offices at and below the provincial level. One of the areas specifically targets local and regional governments through enforcement of stricter investigation of potential LGFV financing using PPP projects.

These policy changes over the last several months, as well as slowly but surely allowing a greater number of onshore defaults or debt-equity restructurings for even some SOEs, aim to adjust the market’s expectations on implicit government support for LGFVs as well as SOEs, in our view.

7

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Relative value

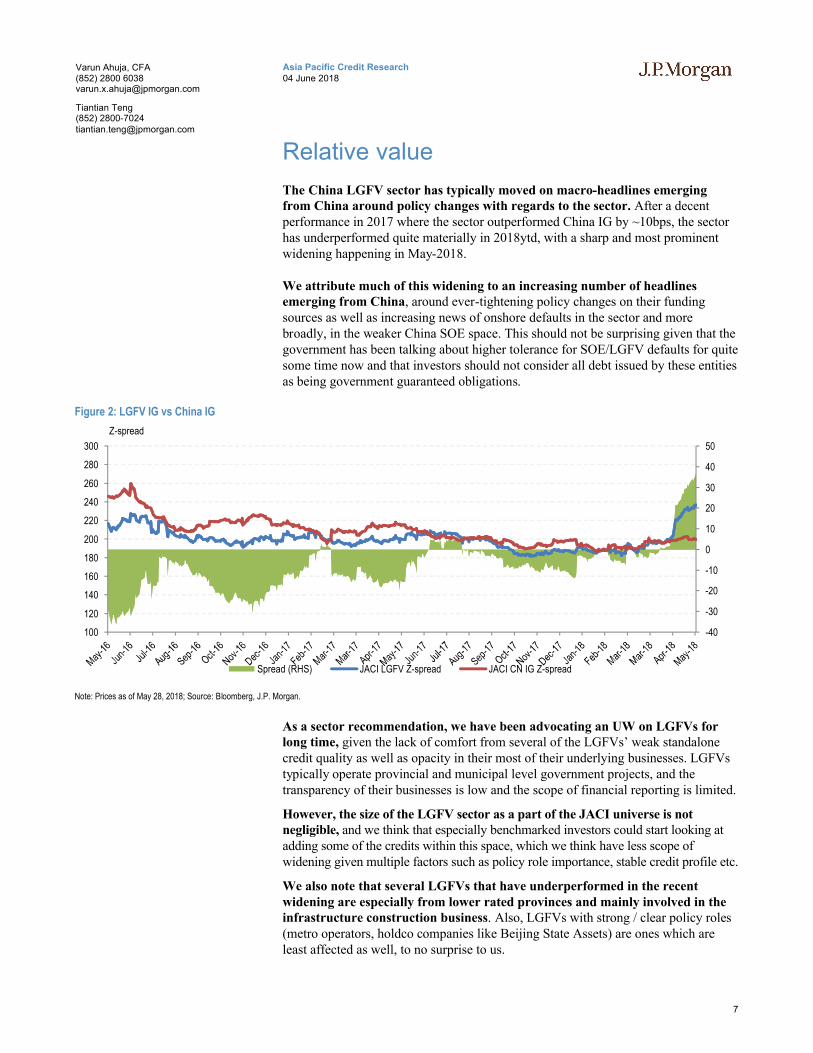

The China LGFV sector has typically moved on macro-headlines emerging from China around policy changes with regards to the sector. After a decent performance in 2017 where the sector outperformed China IG by ~10bps, the sector has underperformed quite materially in 2018ytd, with a sharp and most prominent widening happening in May-2018.

We attribute much of this widening to an increasing number of headlines emerging from China, around ever-tightening policy changes on their funding sources as well as increasing news of onshore defaults in the sector and more broadly, in the weaker China SOE space. This should not be surprising given that the government has been talking about higher tolerance for SOE/LGFV defaults for quite some time now and that investors should not consider all debt issued by these entities as being government guaranteed obligations.

Figure 2: LGFV IG vs China IG

Z-spread

Note: Prices as of May 28, 2018; Source: Bloomberg, J.P. Morgan.

As a sector recommendation, we have been advocating an UW on LGFVs for long time, given the lack of comfort from several of the LGFVs’ weak standalone credit quality as well as opacity in their most of their underlying businesses. LGFVs typically operate provincial and municipal level government projects, and the transparency of their businesses is low and the scope of financial reporting is limited.

However, the size of the LGFV sector as a part of the JACI universe is not negligible, and we think that especially benchmarked investors could start looking at adding some of the credits within this space, which we think have less scope of widening given multiple factors such as policy role importance, stable credit profile etc.

We also note that several LGFVs that have underperformed in the recent widening are especially from lower rated provinces and mainly involved in the infrastructure construction business. Also, LGFVs with strong / clear policy roles(metro operators, holdco companies like Beijing State Assets) are ones which are least affected as well, to no surprise to us.

-40

-30

-20

-10

0

10

20

30

40

50

100

120

140

160

180

200

220

240

260

280

300

Spread (RHS) JACI LGFV Z-spread JACI CN IG Z-spread

8

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

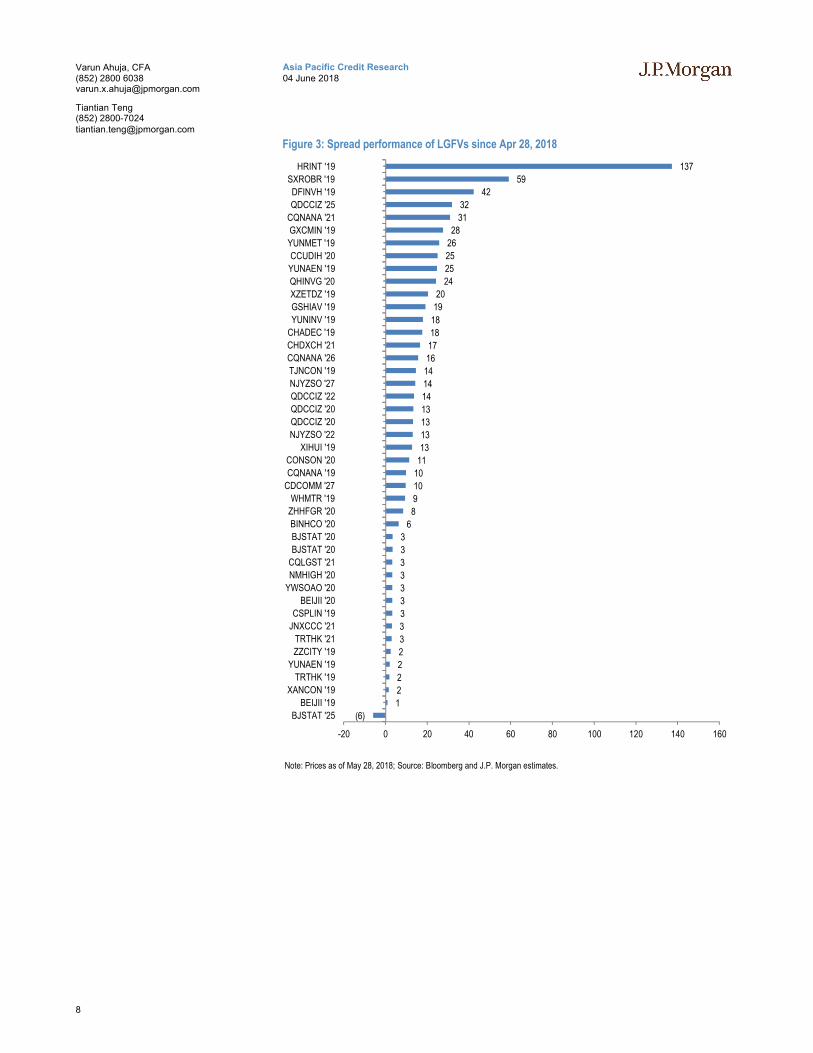

Figure 3: Spread performance of LGFVs since Apr 28, 2018

Note: Prices as of May 28, 2018; Source: Bloomberg and J.P. Morgan estimates.

(6)

1

2

2

2

2

3

3

3

3

3

3

3

3

3

6

8

9

10

10

11

13

13

13

13

14

14

14

16

17

18

18

19

20

24

25

25

26

28

31

32

42

59

137

-20 0 20 40 60 80 100 120 140 160

BJSTAT '25

BEIJII '19

XANCON '19

TRTHK '19

YUNAEN '19

ZZCITY '19

TRTHK '21

JNXCCC '21

CSPLIN '19

BEIJII '20

YWSOAO '20

NMHIGH '20

CQLGST '21

BJSTAT '20

BJSTAT '20

BINHCO '20

ZHHFGR '20

WHMTR '19

CDCOMM '27

CQNANA '19

CONSON '20

XIHUI '19

NJYZSO '22

QDCCIZ '20

QDCCIZ '20

QDCCIZ '22

NJYZSO '27

TJNCON '19

CQNANA '26

CHDXCH '21

CHADEC '19

YUNINV '19

GSHIAV '19

XZETDZ '19

QHINVG '20

YUNAEN '19

CCUDIH '20

YUNMET '19

GXCMIN '19

CQNANA '21

QDCCIZ '25

DFINVH '19

SXROBR '19

HRINT '19

9

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Sector strategy and key recommendations

With LGFVs growing large enough to be a sub-sector in JACI, while too big to ignore, jump-risk stays high, given the lack of information flow. Hence, we think it makes sense to stick to LGFVs with defined/strategically important roles and ideally having decent standalone credit profiles.

Amongst the LGFVs that we screened, given that most LGFVs are trading as a “group” in different yield buckets, we would look to take selective exposure in LGFVs through credits in the first two categories for each yield bucket. For exposure to higher yields, we are more comfortable with the risk-reward and information flow in other China SOEs and HY corporates as presented in this report.

We think those in the regional infra and construction sectors are more at risk compared to say metro operators, public utility services (water treatment etc.) with existing operations or some investment holdco companies that function as a key government arm. While utility and toll-road companies have high earnings visibility, they are also at some risk of reduced uplifts in ratings for them as well as they are more likely to be commercial-like entities (rather than policy) in practice.

Table 2: Summary of recommendations for LGFVs and selected SOEs and corporates

Entity IssueBond

StructureBond rating

Amt (US$ mm) Ratings Z-sprd M. Dur YTW

Guangzhou Metro GUAMET 3.375% '20 Keepwell N 200 Baa1/-/A 106 2.4 3.8%Tianjin Rail Transit TRTHK 2.875% '21 Keepwell N 300 Baa1/-/A 115 2.8 3.9%Tianjin Rail Transit TRTHK 2.5% '19 Keepwell N 200 Baa1/-/A 71 0.9 3.2%Beijing Infrastructure Investment BEIJII 3.625% '19 Keepwell N 300 A2/A/A+ 28 0.8 2.7%Beijing Infrastructure Investment BEIJII 3.25% '20 Keepwell OW 300 A2/A/A+ 76 1.6 3.4%Wuhan Metro Group WHMTR 2.375% '19 sr. unsec OW 290 -/-/A 126 1.4 3.8%Beijing State-Owned Asset Mgmt BJSTAT 3% '20 Keepwell N 300 A3/A-/A 93 1.9 3.6%Beijing State-Owned Asset Mgmt BJSTAT 4.125% '25 Keepwell N 700 A3/A-/A 145 6.0 4.3%Tianjin Binhai New Area Cons & Inv BINHCO 4% '20 sr. unsec UW 500 Baa1/BBB+/A- 167 2.0 4.3%Qingdao City Construction Inv Grp QDCCIZ 5.95% '25 Keepwell UW 300 -/BBB-/BBB+ 243 5.4 5.2%Qingdao City Construction Inv Grp QDCCIZ 4.75% '20 Keepwell N 500 -/BBB-/BBB+ 223 1.6 4.5%Hanrui Overseas Investment Co Ltd HRINT 4.9% '19 Keepwell UW 490 -/-/BB+ 1197 1.0 14.5%Jiangsu NewHeadLine NHLHK 6.25 '19 Keepwell UW 300 -/BB-/BB+ 1327 0.5 15.7%Oriental Capital Co Ltd DFINVH '19 Keepwell NC 300 -/-/BB+ 452 1.4 7.2%ChemChina HAOHUA 4.125% '21s sr. unsec OW 1000 -/BBB/A- 117 2.6 3.9%ChemChina HAOHUA 3.5% '22s sr. unsec OW 1500 -/BBB/A- 146 3.7 4.3%Yanzhou Coal YZCOAL Perp 'c20 sr. unsec OW 500 Ba3/BB/B+ 330 1.7 6.1%Yanzhou Coal YZCOAL 5.73% ‘22 sr. unsec OW 228 Ba3/BB/B+ 407 3.4 7.0%Baoshan Iron & Steel BAORES 3.875% '20s Keepwell OW 500 Baa2/BBB/A 102 1.6 3.7%Sino-Ocean Land SINOCE 4.625% '19s sr. unsec OW 500 Baa3/-/BBB- 124 1.1 3.8%Shanghai Construction SHCONS 3.75% '20s sr. unsec NC 400 Baa2/BBB-/BBB+ 97 2.0 3.7%China Hua Neng Group HUANEN 3.6% c'22s Keepwell OW 500 -/-/- 340 3.7 6.3%Aluminum Corp of China CHALUM 4% '21s Keepwell OW 800 -/-/- 246 2.9 5.3%Central China CENCHI 6.875% '20s sr. unsec OW 386 B1/-/BB- 485 2.1 7.5%Fantasia Holdings FTHDGR 7.25% '19s sr. unsec NC 300 B3/-/- 577 0.6 8.0%ChemChina HAOHUA Perp 'c22 sr. unsec OW 600 Baa2/-/BBB+ 222 3.6 5.3%Power China CHPWCN Perp 'c19 sr. unsec OW 500 Baa1/-/- 128 1.3 4.0%MCC Holding CHMETL Perp 'c21 sr. unsec NC 500 Baa1/-/- 209 2.7 4.9%China Minmetal Corp. MINMET Perp 'c21 sr. unsec OW 400 Baa1/-/- 226 2.7 5.1%China Railway Construction RLCONS Perp 'c19 sr. unsec OW 800 A3/-/- 118 1.1 3.9%Power China CHPWCN Perp 'c22 sr. unsec NC 500 Baa1/-/BBB+ 230 3.6 5.2%Aluminum Corp of China CHALUM Perp 'c21 Keepwell N 500 -/-/BBB 232 3.1 5.2%FWD Ltd FWDINS Perp 'c22 AT1 NC 250 Ba2/-/BB+ 372 3.1 7.0%Nanyang Commercial Bank NANYAN Perp 'c22 AT1 OW 1200 Ba2/-/- 377 3.5 6.0%China Cinda Asset Management CCAMCL Perp 'c21 AT1 OW 3200 B1/-/- 403 2.9 6.1%ICBC ICBCAS Perp 'c21 AT1 OW 1000 Ba1/-/- 315 2.8 5.8%

Note: Prices as of May 28, 2018; Source: J.P. Morgan, Moody’s, S&P, Fitch and Bloomberg.

10

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Clearly, there are certain LGFVs that are quite wide in the 1-2yr duration bucket which presents investors a conundrum of missing out on better yields if not invested but having a high “jump risk” if any of these LGFVs widen materially due to financial constraints, which are difficult to monitor given inadequate underlying information flow. Based on the sector overview, our strategy for LGFVs is as following:

As we have discussed in our prior reports as well, taking exposure in some LGFVs with very definite policy-role and/or with high cash visibility such as metro operators, toll road operators etc. would be better than infrastructure construction companies, especially if the latter have largely under-construction projects. We think tighter financial conditions, limited earnings visibility and overall social impact will likely be lowest for them. Hence, most at risk to underperform in this environment.

In terms of tenor, shorted-dated notes (preferably 1-3 years) remain preferable vs. their longer end notes given LGFV curves are not steep enoughin an already volatile sector with limited information flow. We believe this sector’s bond curve should be steeper as policy environment and regulations are still evolving for the sector and hence uncertainty is relatively higher.

We would also look for similar yielding China SOEs / corps as proxies to this space (especially in 2-3yr duration) as we think this would enable investors to earn similar carry but with better ability to monitor risk. We do note that except for credits where tight liquidity conditions have already started pricing in concerns on the specific credits, most LGFVs are still at least quoted at similar levels to the SOEs whose bonds are more liquid and investor base more diverse, both by investor type and geographically.

11

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

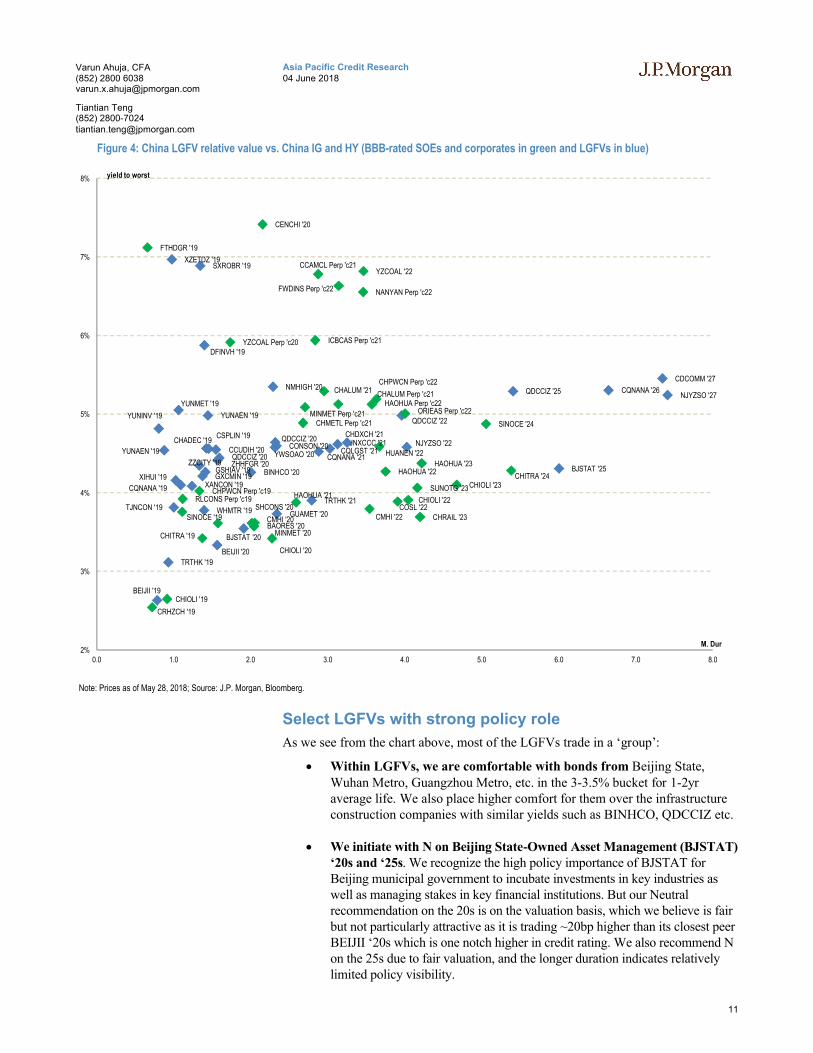

Figure 4: China LGFV relative value vs. China IG and HY (BBB-rated SOEs and corporates in green and LGFVs in blue)

Note: Prices as of May 28, 2018; Source: J.P. Morgan, Bloomberg.

Select LGFVs with strong policy role

As we see from the chart above, most of the LGFVs trade in a ‘group’:

Within LGFVs, we are comfortable with bonds from Beijing State, Wuhan Metro, Guangzhou Metro, etc. in the 3-3.5% bucket for 1-2yr average life. We also place higher comfort for them over the infrastructure construction companies with similar yields such as BINHCO, QDCCIZ etc.

We initiate with N on Beijing State-Owned Asset Management (BJSTAT)‘20s and ‘25s. We recognize the high policy importance of BJSTAT for Beijing municipal government to incubate investments in key industries as well as managing stakes in key financial institutions. But our Neutralrecommendation on the 20s is on the valuation basis, which we believe is fair but not particularly attractive as it is trading ~20bp higher than its closest peer BEIJII ‘20s which is one notch higher in credit rating. We also recommend N on the 25s due to fair valuation, and the longer duration indicates relatively limited policy visibility.

BJSTAT '20

BJSTAT '25

BEIJII '19

BEIJII '20

BINHCO '20

NJYZSO '22

NJYZSO '27

TRTHK '19

CCUDIH '20

GUAMET '20

TRTHK '21

CQNANA '19

CQNANA '21

CQNANA '26

GSHIAV '19

CSPLIN '19

QDCCIZ '20

JNXCCC '21

QDCCIZ '25

XIHUI '19

CONSON '20

ZZCITY '19

GXCMIN '19

YWSOAO '20

SXROBR '19

TJNCON '19

YUNINV '19

YUNAEN '19

XZETDZ '19

YUNMET '19

XANCON '19

WHMTR '19

DFINVH '19

YUNAEN '19

CHADEC '19

ZHHFGR '20

NMHIGH '20

QDCCIZ '20

CQLGST '21

CHDXCH '21

QDCCIZ '22

CDCOMM '27

HAOHUA '21

HAOHUA '22HAOHUA '23

CHRAIL '23

CHIOLI '19

CHIOLI '20

CHIOLI '22

CHIOLI '23

CHITRA '19

CHITRA '24

CMHI '20 CMHI '22

CRHZCH '19

MINMET '20BAORES '20

SINOCE '19

SINOCE '24

SHCONS '20

SUNOTG '23

COSL '22

HUANEN '22

CHALUM '21

HAOHUA Perp 'c22

CHPWCN Perp 'c19

CHMETL Perp 'c21MINMET Perp 'c21

RLCONS Perp 'c19

CHPWCN Perp 'c22

CHALUM Perp 'c21

CENCHI '20

FTHDGR '19

FWDINS Perp 'c22 NANYAN Perp 'c22

ORIEAS Perp 'c22

CCAMCL Perp 'c21

ICBCAS Perp 'c21

YZCOAL '22

YZCOAL Perp 'c20

2%

3%

4%

5%

6%

7%

8%

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

yield to worst

M. Dur

12

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

We initiate with OW on Wuhan Metro (WHMTR) '19s. On a relative basis, we think the bonds look slightly attractive at only marginally inside Tianjin Railway ‘21s (NC), which has the same credit rating but ~2 years shorter duration. Wuhan Metro is also the sole metro operator in a first-tier city in China, with a strategic business positioning that we have bit more comfort with.

Looking at strategic relationships with the provincial government is key when selecting LGFVs. For example, we would have bit more comfort with Tianjin Binhai (BINHCO) over say Xihui Haiwai (NC), Qingdao Conson or Yunnan Metropolitan (YUNMET, NC). While all are in infrastructure construction business, BINHCO is the sole government investment and financing arm for an area which gets regular grants from central government as well. In addition, Tianjin has relatively stronger provincial level local government finances.

We reiterate that these recommendations are for investors looking to invest within LGFVs only as they are nevertheless still trading somewhat close to some of the mid-tier SOEs such as China Merchant Holdings(CMHI), ChemChina, Minmetals, Power China, China Railway Constructions (CRCC), etc. for which we would still have relative preference.

Upside catalysts for Wuhan Metro include higher-than-expected government capital grants and subsidies. Downside risks include weaker economic performance and higher indebtedness of the municipality, which may affect government support for WHMTR.

Upside catalysts for Beijing State-owned Asset Mgmt include diversification of investments and resulting generation of portfolio value. Downside risks include underperformance of investment portfolio and weakening of Beijing municipal government’s willingness to support.

Several SOE alternatives in the 4-5% range

We note that there are several LGFVs with 1-3 year duration that are yielding in the 4-5% range, which should seem attractive for an IG investor, in our view. Typically, investors buy bonds in this tenor for their stability rather than capital appreciation given the short tenor (even 100bp spread compression implies only 1-1.5pts here).

With this in mind, we think investing in strong SOEs even if that means going for the callable part of the capital structure (perpetuals with high step-up), should better qualify for the above yields vs low volatility requirements as mentioned above. We note from the chart above that there are several such alternatives that investors could look at.

For example, we think the following China SOE and corporate bonds are some alternatives we think offer similar yields while information transparency around business and outlook is much clearer and easier to monitor:

13

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

China Railway Construction perps ‘c19s: At 4%ytc for 2019 call date, the bonds are senior unsecured in ranking and issued from A3/A- rated issuer which is one of the largest railway infrastructure construction in China. While the company is ~55% owned by central SASAC and is listed in Shanghai and Hong Kong, we think the partial ownership is more due to bringing financial discipline through listing and management appointment and operations etc. remain closely monitored by central government through the wholly owned China Railway Construction Corp, parent company of CRCC. The perps have 5% step-up if not called, hence a steep incentive to do so given the coupon will reset to ~10%.

ChemChina ‘21s: ChemChina is China’s largest chemical company and third largest globally. As a key company in specialty chemicals, crop protection and agro-chemicals sector, we think the company has a strategic position in a sensitive sector for the government given the importance of food safety and self-sufficiency for the country. In our view, this strategic importance has further increased for the wholly central-SASAC owned entity which also directly guarantees the bonds, post-acquisition of Syngenta and this support is also evidenced from the US$43 billion acquisition which has completed in the middle of an otherwise, “deleveraging focused year” by the Chinese government. The bonds offer ~4%ytm as well, similar to the weaker LGFVs of 2020-21 maturities but in our view, the former has much better earnings visibility, closer government ownership structure and clear and high strategic support.

Minmetals 4.45% perps 'c21s: We also think the perps from China Minmetals Group callable in 2021s (5.2%ytc) are a decent alternative for investors looking to invest in core China SOEs but yielding over 5%, as compared to the weaker LGFVs at similar levels and duration. The SOE is again wholly central-SASAC owned and was designated as the only State-owned Asset Investment Platform in the M&M industry and hence in our view, further increased in its strategic importance. Even from a bottom-up perspective, the credit should be deleveraging especially with commodity prices rebounding and the company’s key project in Peru (Las Bambas) operational. The bonds are rated Baa1, have 400bp step-up if not called and hence in our view, have high likelihood of being called.

The 6-7% club – not without risk but risk-reward wise better, in our view

Clearly, bonds yielding over 6% for 1-2 year average life are not without higher risks or some broad concerns. However, we think the following bonds offer a much better risk-reward vs. some of the lower quality & rated LGFVs in the sense that they can still be more effectively monitored.

Also, these LGFVs are typically from lower rated (weaker credit profile) provinces and typically in infrastructure construction businesses. Consequently, either directly or through the province, these credits are quite dependent on the property sector themselves. Hence, we think it makes some sense to present some HY China property credits as a decent alternative to consider, where we are bit more comfortable with standalone business profile from default-probability perspective.

14

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Yanzhou Coal perp ‘c20s and ‘22s: We initiate coverage on Yanzhou Coal,its 5.75% perps ‘c20s and ‘22s with OW. The perps have a 400bp step-up (to T3+830bp) if not called in Apr-2020 and are senior unsecured in ranking. The outlook for coal prices is relatively better and along with continued cost control in both China and Australian operations, the company has reduced leverage to ~3.4x as of Dec-17 but we expect this number to stay broadly similar on higher capex in next 1-2 years. Yanzhou is 55% owned by Shandong government’s wholly owned Yankuang Group and is the main profit contributor to the SOE. While not a strong standalone credit, we think the company still provides much better earnings visibility, has decent operations at standalone level and being listed, investors would should be able to monitor the company closely. Hence, we think the bonds are a decent alternative to the higher yielding LGFVs in 2-3yr duration bucket. We would also recommend YZCOAL perps ‘c20s over QDCCIZ ‘20s (also Shandong province LGFV) with the former trading ~140-150bps wider to call date. Separately, we think Yanzhou ‘22s look cheap at 7% which is wider than its peers such as Indika ‘22s (also pure coal credit). We also note that in the lows of coal cycle in 2015, Yanzhou was actually buying back its 2022 bonds at around 90cents, even as other commodity credits’ bonds fell to below 50cents.

Key upside catalysts are higher coal prices, reduced capex and asset sales,while key downside risks are a decline in coal prices, higher-than-expected costs of production, aggressive capex etc.

NANYAN and CCAMCL AT1s (covered by Matthew Hughart): We think the AT1s from these financial institutions offer decent yields for the risks and though there is some call risk from them, we think it is still low. For CCAMCL, Matthew writes in his recent note published May 3rd: “Offered at a yield to 2021 call of 6.6%, a variety of comparisons highlight the value, whether it is vs. AT1 peers, vs. senior bonds, or relative to the company's Hong Kong subsidiary: we conclude that the yield supports a more positive view.” Also, while supply remains a concern, it has been quite slow this year, which we believe is either is a reflection of increasing pressure to manage leverage and stick to core businesses, although it may also suggest a pick-up in the rest of the year.

Central China 6.875% ‘20s (covered by Daniel Fan): We would recommend this as an alternative only against the highest yielding LGFVs which are HY rated (by Fitch only) despite getting the uplifts due to provincial government ownership and hence having a very weak standalone profile. Also, as mentioned above, since these LGFVs are, either directly or through the province, quite dependent on the property sector themselves it makes some sense to present some HY China property credits. The company has a good track record in project execution, maintains strong liquidity and conservative financial management. Capitaland is a strategic partner, which should ease some concern over the less transparent JV projects. Key downside risks are concentration in Henan and low transparency at JV level. Further catalyst is the expansion of its asset-light project management business.

15

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Golden Eagle ‘23s: Not an ideal comp but to again exemplify our rationale,the bonds trade about flat to some of the weaker LGFVs of this duration. While the risks would be relatively high in both cases, we draw bit more comfort from holding Golden Eagle at this time, given its likely bottoming out of retail sales cycle, clear asset coverage in multiple of net debt etc. Hence, “jump-risk” of spreads much more mitigated and investors would have better ability to monitor the investment.

Please refer to our last published coverage report for key risks on the above alternatives presented.

16

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

LGFVs: A quick recap

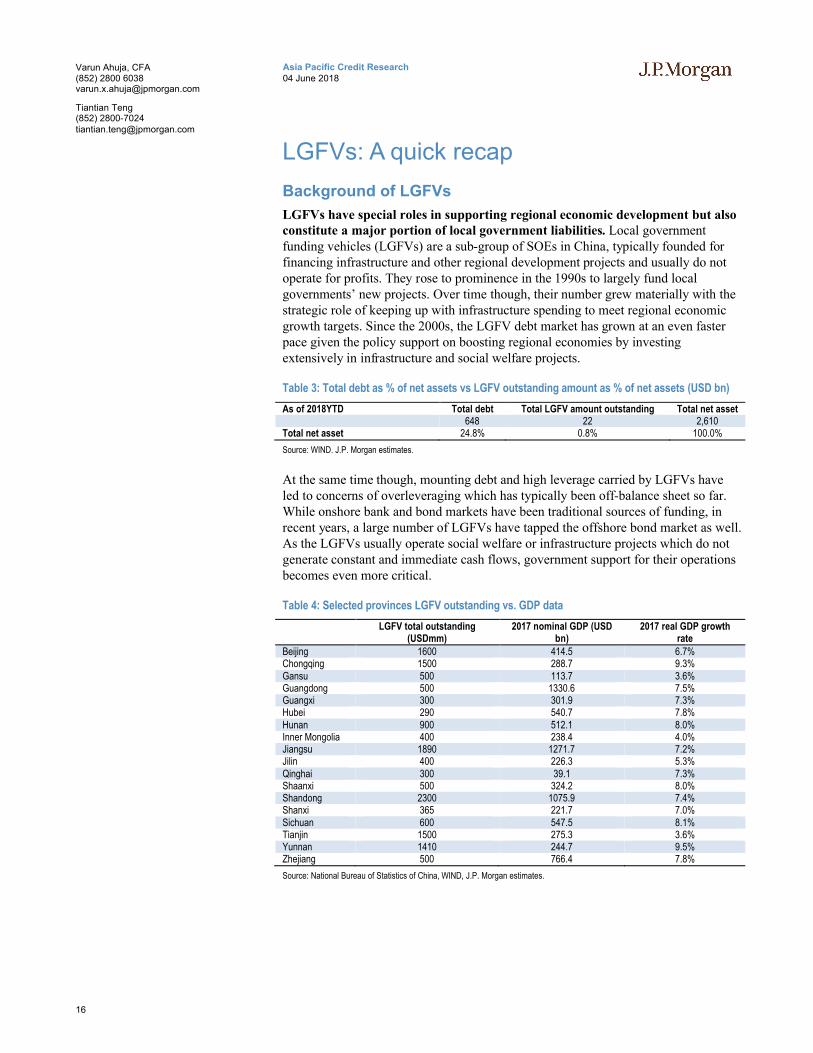

Background of LGFVs

LGFVs have special roles in supporting regional economic development but also constitute a major portion of local government liabilities. Local governmentfunding vehicles (LGFVs) are a sub-group of SOEs in China, typically founded for financing infrastructure and other regional development projects and usually do not operate for profits. They rose to prominence in the 1990s to largely fund local governments’ new projects. Over time though, their number grew materially with the strategic role of keeping up with infrastructure spending to meet regional economic growth targets. Since the 2000s, the LGFV debt market has grown at an even faster pace given the policy support on boosting regional economies by investing extensively in infrastructure and social welfare projects.

Table 3: Total debt as % of net assets vs LGFV outstanding amount as % of net assets (USD bn)

As of 2018YTD Total debt Total LGFV amount outstanding Total net asset648 22 2,610

Total net asset 24.8% 0.8% 100.0%

Source: WIND. J.P. Morgan estimates.

At the same time though, mounting debt and high leverage carried by LGFVs have led to concerns of overleveraging which has typically been off-balance sheet so far.While onshore bank and bond markets have been traditional sources of funding, in recent years, a large number of LGFVs have tapped the offshore bond market as well. As the LGFVs usually operate social welfare or infrastructure projects which do not generate constant and immediate cash flows, government support for their operations becomes even more critical.

Table 4: Selected provinces LGFV outstanding vs. GDP data

LGFV total outstanding (USDmm)

2017 nominal GDP (USD bn)

2017 real GDP growth rate

Beijing 1600 414.5 6.7%Chongqing 1500 288.7 9.3%Gansu 500 113.7 3.6%Guangdong 500 1330.6 7.5%Guangxi 300 301.9 7.3%Hubei 290 540.7 7.8%Hunan 900 512.1 8.0%Inner Mongolia 400 238.4 4.0%Jiangsu 1890 1271.7 7.2%Jilin 400 226.3 5.3%Qinghai 300 39.1 7.3%Shaanxi 500 324.2 8.0%Shandong 2300 1075.9 7.4%Shanxi 365 221.7 7.0%Sichuan 600 547.5 8.1%Tianjin 1500 275.3 3.6%Yunnan 1410 244.7 9.5%Zhejiang 500 766.4 7.8%

Source: National Bureau of Statistics of China, WIND, J.P. Morgan estimates.

17

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Figure 5: Selected provinces LGFV outstanding vs. GDP data

Source: National Bureau of Statistics of China, WIND, J.P. Morgan estimates.

Fundamental analysis framework

We use a top-down approach to assess LGFVs and our selection criterion is therefore more weighted towards its local government strength and its policy role. Standalone credit profile of LGFVs is included as well but with relatively less weight. We take the following listed factors into consideration when we assess individual LGFVs:

1) Strength of the government: We think that how developed and the resulting financial ability of local government is one of the critical factors to be taken into consideration. LGFVs commonly have weak standalone credit profiles, so which provincial or municipal government that is linked to them becomes important. Although the central government has enforced strict rules on the separation of government involvement in LGFV operations and debt financing, we think that the linkage between the two will stay at least for now, but will gradually towards to a much lesser extent. Also, among different levels of governments, we think that provincial governments are usually stronger than municipal or district level governments. In terms of the strength of shareholder structure, we prefer those that are directly owned by central SASACs.

2) Willingness of government support: We would consider lowering weight on this factor eventually given the ongoing reform to eliminate government implicit support for LGFVs. However, in the near term, we still include it as an important part to be considered. Currently, the majority of the existing LGFVs run social and public mandates and projects for their respective local governments and carry policy mandate. In our view, this factor plays a differentiated role for LGFVs that operate on a policy basis versus for commercial purpose, with the former receiving more government support.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

500

1000

1500

2000

2500

3000

3500

4000

Bei

jing

Cho

ngqi

ng

Gan

su

Gua

ngdo

ng

Gua

ngxi

Hub

ei

Hun

an

Inne

r M

ongo

lia

Jian

gsu

Jilin

Qin

ghai

Sha

anxi

Sha

ndon

g

Sha

nxi

Sic

huan

Tia

njin

Yun

nan

Zhe

jiang

LGFV total outstanding (USDmm) Nominal GDP (USD bn) Real GDP growth rate 2017

18

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

3) Standalone credit profile: Given the current trend of policy tightening, we do recognize that LGFVs standalone profiles will become more important for assessment going forward as government guarantee is prohibited. But for now, we think that the above factors will still be dominating in our analysis while the standalone profile plays a relatively smaller role.

For more details on the framework, please see our report dated Aug 3, 2016.

Categorization of LGFVs

We determine categorization of the LGFVs based on the following factors, of which the first two should determine the government’s willingness to support, while the latter two will determine the ability.

Strategic or policy role they play

Economic importance in terms of scale and contribution to provincial economy

Standalone fundamentals (relatively less important, in our view)

Provincial government’s financials (ability to support)

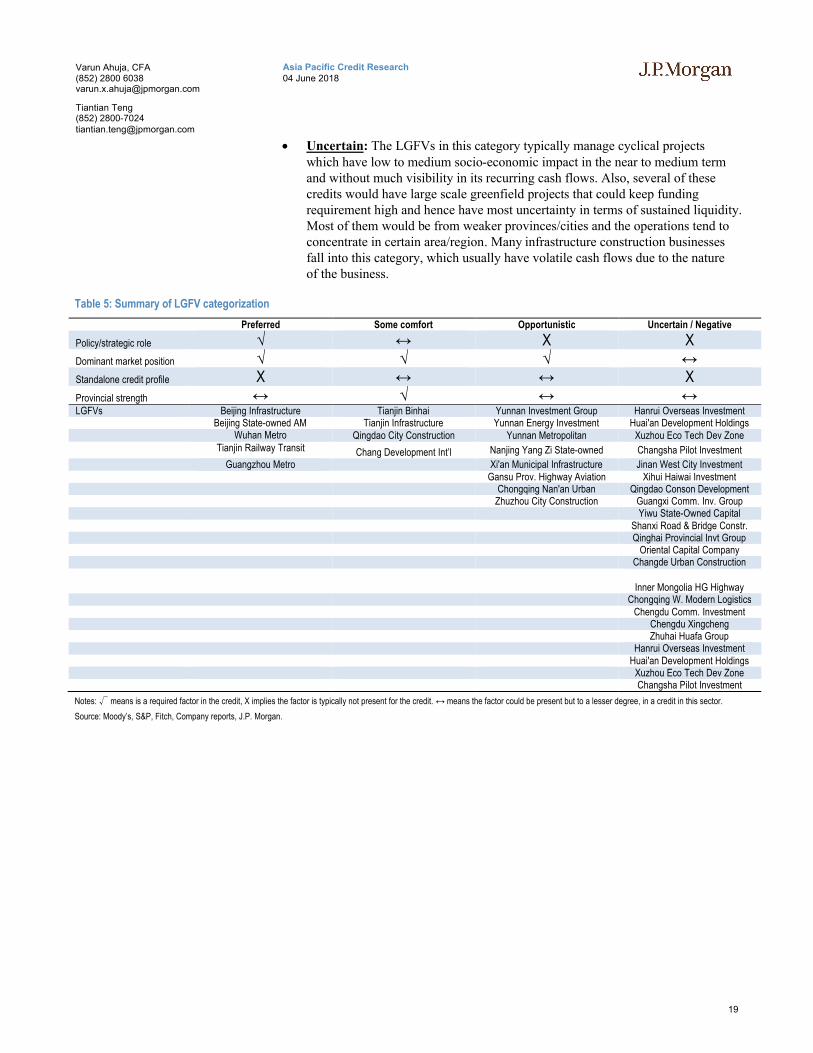

Based on the above four factors, we classify the LGFVs into four broad categories –

Preferred: LGFVs with a clear and defined strategic / policy role within the province that owns the credit. The LGFV should manage socially important projects, are typically sole vehicles to operate in their sector/segment and largely operational. Hence, any liquidity pressure disrupting smooth operations would have large socio-economic impact. Underlying operations would be strong butfinancials may not be, more due to government-mandated reasons (ticket price controls, regulated-tariffs). We believe the above factors would most likely ensure that the government would support through either equity infusion, asset sales or subsidy contribution would remain even in stressed periods. Also, we note that these LGFVs are usually from top-tier provinces/cities in China.

Some comfort: LGFVs with a defined strategic role and again have a dominant, if not a monopolistic position in that sector within the province, even though the operations may be in relatively less strategic sectors. The province should typically be relatively strong as well. If not the above, then they would operateprojects that are typically more profitable, such as highway and toll roads business and hence are generally strong at a standalone level. This also means they are subject to less government support as they operate relatively more commercial projects but being fundamentally strong, the likelihood of requiring parental support would also be limited.

Opportunistic: LGFVs with lesser certain or no material policy role, in a less strategic sector such as mining, infrastructure construction and property development etc. but has a dominant or major market share in the sector / segment it operates in. Also, the province would typically be in the tier 2 or 3 range. The reason this is labeled as opportunistic is while there would be limited social impact in a stressed situation and hence less certain of support in the medium term depending on government’s priority projects. However, since theLGFV would be one of the very few companies implementing the projects for the province, support in near term at least should be there.

19

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Uncertain: The LGFVs in this category typically manage cyclical projects which have low to medium socio-economic impact in the near to medium term and without much visibility in its recurring cash flows. Also, several of these credits would have large scale greenfield projects that could keep funding requirement high and hence have most uncertainty in terms of sustained liquidity. Most of them would be from weaker provinces/cities and the operations tend to concentrate in certain area/region. Many infrastructure construction businesses fall into this category, which usually have volatile cash flows due to the nature of the business.

Table 5: Summary of LGFV categorization

Preferred Some comfort Opportunistic Uncertain / Negative

Policy/strategic role √ ↔ X XDominant market position √ √ √ ↔Standalone credit profile X ↔ ↔ XProvincial strength ↔ √ ↔ ↔LGFVs Beijing Infrastructure Tianjin Binhai Yunnan Investment Group Hanrui Overseas Investment

Beijing State-owned AM Tianjin Infrastructure Yunnan Energy Investment Huai'an Development HoldingsWuhan Metro Qingdao City Construction Yunnan Metropolitan Xuzhou Eco Tech Dev Zone

Tianjin Railway Transit Chang Development Int’l Nanjing Yang Zi State-owned Changsha Pilot Investment

Guangzhou Metro Xi'an Municipal Infrastructure Jinan West City Investment Gansu Prov. Highway Aviation Xihui Haiwai Investment

Chongqing Nan'an Urban Qingdao Conson Development Zhuzhou City Construction Guangxi Comm. Inv. Group

Yiwu State-Owned Capital Shanxi Road & Bridge Constr.Qinghai Provincial Invt Group

Oriental Capital CompanyChangde Urban Construction

Inner Mongolia HG HighwayChongqing W. Modern Logistics

Chengdu Comm. InvestmentChengdu Xingcheng Zhuhai Huafa Group

Hanrui Overseas InvestmentHuai'an Development Holdings

Xuzhou Eco Tech Dev ZoneChangsha Pilot Investment

Notes: √ means is a required factor in the credit, X implies the factor is typically not present for the credit. ↔ means the factor could be present but to a lesser degree, in a credit in this sector.

Source: Moody’s, S&P, Fitch, Company reports, J.P. Morgan.

20

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Technicals: Less negative due to lower supply but investor base still narrow

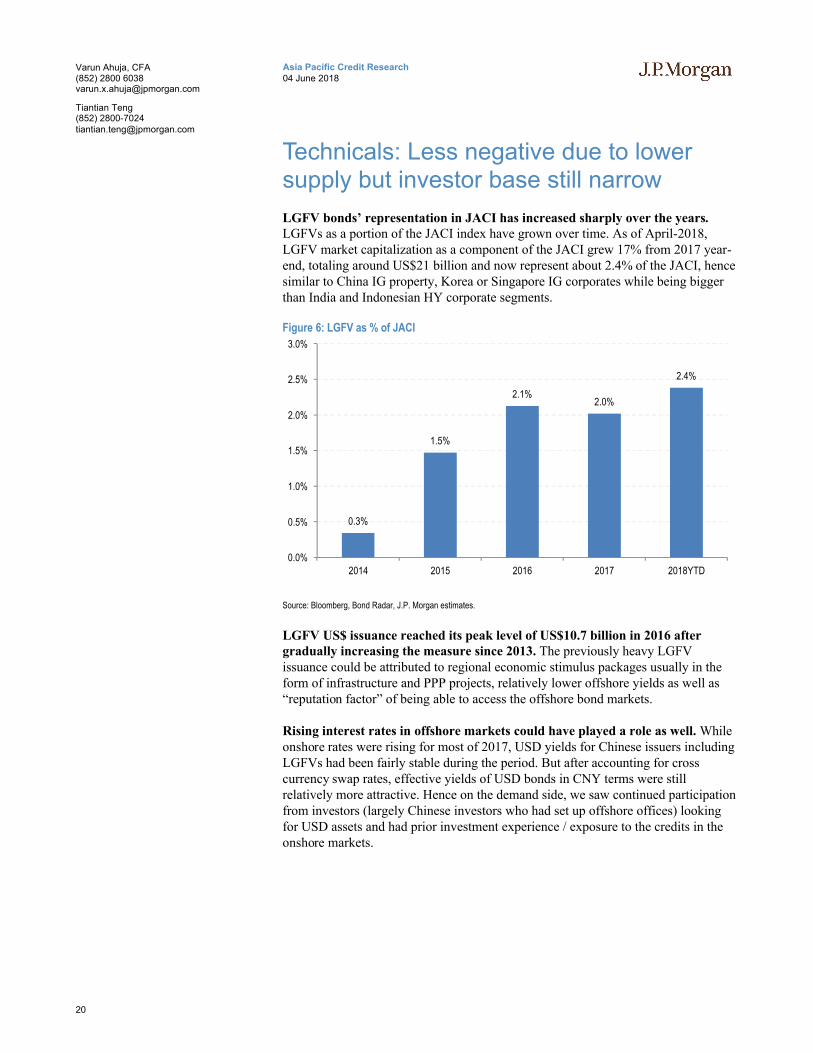

LGFV bonds’ representation in JACI has increased sharply over the years. LGFVs as a portion of the JACI index have grown over time. As of April-2018, LGFV market capitalization as a component of the JACI grew 17% from 2017 year-end, totaling around US$21 billion and now represent about 2.4% of the JACI, hence similar to China IG property, Korea or Singapore IG corporates while being bigger than India and Indonesian HY corporate segments.

Figure 6: LGFV as % of JACI

Source: Bloomberg, Bond Radar, J.P. Morgan estimates.

LGFV US$ issuance reached its peak level of US$10.7 billion in 2016 after gradually increasing the measure since 2013. The previously heavy LGFV issuance could be attributed to regional economic stimulus packages usually in the form of infrastructure and PPP projects, relatively lower offshore yields as well as “reputation factor” of being able to access the offshore bond markets.

Rising interest rates in offshore markets could have played a role as well. While onshore rates were rising for most of 2017, USD yields for Chinese issuers including LGFVs had been fairly stable during the period. But after accounting for cross currency swap rates, effective yields of USD bonds in CNY terms were still relatively more attractive. Hence on the demand side, we saw continued participation from investors (largely Chinese investors who had set up offshore offices) looking for USD assets and had prior investment experience / exposure to the credits in the onshore markets.

0.3%

1.5%

2.1%2.0%

2.4%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2014 2015 2016 2017 2018YTD

21

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Bond supply should slow going forward

Figure 7: Onshore LGFV bond issuances US$ in billions

Source: WIND and J.P. Morgan.

Figure 8: Offshore LGFV issuances US$ in billions

Source: Bloomberg, Bond Radar, J.P. Morgan.

LGFV offshore issuance dropped in 2017 after experiencing consecutive growthsince 2014, as the central government started addressing local indebtedness issues, total amount of LGFV offshore issuance started to decline. This was not surprising and can be partly explained by China’s policy shift to eliminate local governments’ role in both LGFV financing and operations.

Figure 9: Yield basis between China AAA-rated 5yr bonds and JACI China IG corporates

Source: WIND, Bloomberg and J.P. Morgan.

Also, the basis between onshore/offshore yields has narrowed again in recent months in addition to the USD appreciating vs most EM countries including CNY.

Further, Chinese investors who we think has been the dominant buyers of these bonds have been noticeably cautious in adding exposure to the sector in the recent months.

Last but not least, as mentioned in the policy update section above, the government is tightening the underwriting standards whereby state-owned financial institutions should not indicate implicit or direct local government support by reporting local government financials. Implemented in a stringent manner, we believe tighter standards should impose more challenges for LGFVs to tap for more funding going forward and should also imply lower overall supply in the USD bond markets.

153 170

312291

379

290

145

0

100

200

300

400

2012 2013 2014 2015 2016 2017 2018

Onshore LGFV issuance

1.6

3.4

10.7

6.6

1.4

-

2

4

6

8

10

12

2014 2015 2016 2017 Apr-18

Offshore LGFV issuance

0

20

40

60

80

100

120

140

160

2.5

3.5

4.5

5.5

6.5

7.5

May-14 Nov-14 May-15 Nov-15 May-16 Nov-16 May-17 Nov-17 May-18

Basis China corporate bond AAA 5-year ytm JACI China IG ytw

22

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

Investor base remains narrow as Asia continues to dominate

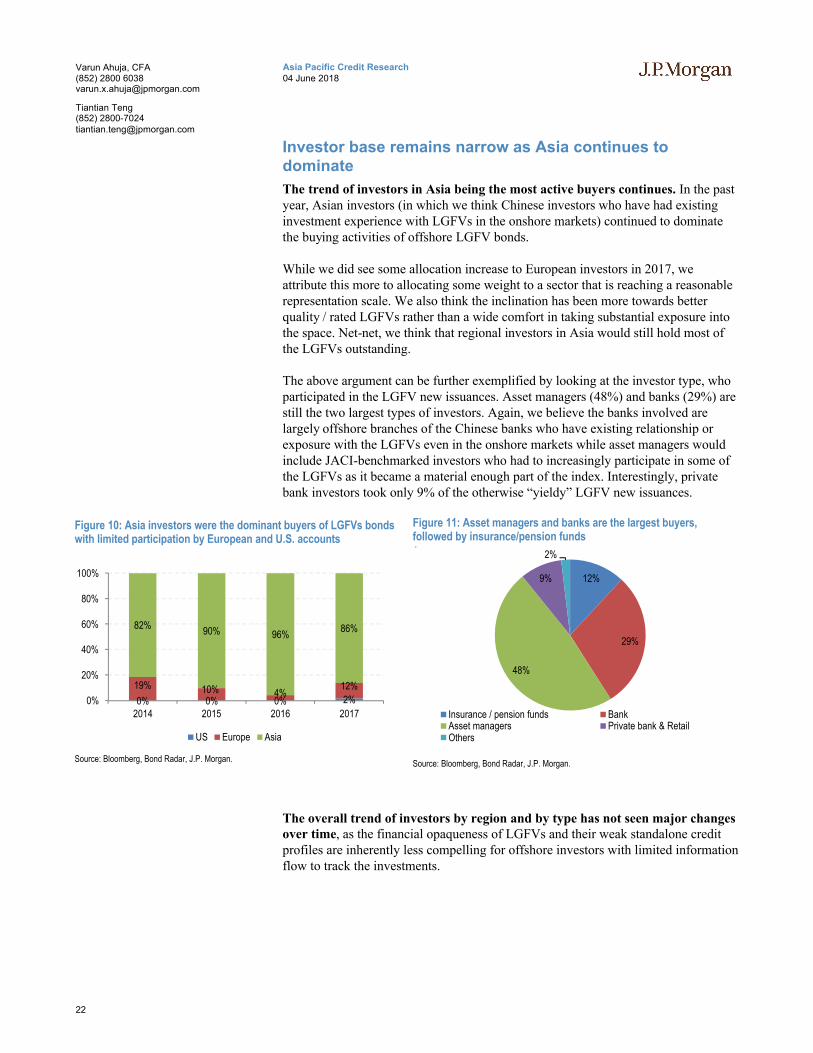

The trend of investors in Asia being the most active buyers continues. In the past year, Asian investors (in which we think Chinese investors who have had existing investment experience with LGFVs in the onshore markets) continued to dominate the buying activities of offshore LGFV bonds.

While we did see some allocation increase to European investors in 2017, we attribute this more to allocating some weight to a sector that is reaching a reasonable representation scale. We also think the inclination has been more towards better quality / rated LGFVs rather than a wide comfort in taking substantial exposure into the space. Net-net, we think that regional investors in Asia would still hold most of the LGFVs outstanding.

The above argument can be further exemplified by looking at the investor type, who participated in the LGFV new issuances. Asset managers (48%) and banks (29%) are still the two largest types of investors. Again, we believe the banks involved are largely offshore branches of the Chinese banks who have existing relationship or exposure with the LGFVs even in the onshore markets while asset managers would include JACI-benchmarked investors who had to increasingly participate in some of the LGFVs as it became a material enough part of the index. Interestingly, private bank investors took only 9% of the otherwise “yieldy” LGFV new issuances.

Figure 10: Asia investors were the dominant buyers of LGFVs bonds with limited participation by European and U.S. accounts

Source: Bloomberg, Bond Radar, J.P. Morgan.

Figure 11: Asset managers and banks are the largest buyers, followed by insurance/pension funds

Source: Bloomberg, Bond Radar, J.P. Morgan.

The overall trend of investors by region and by type has not seen major changes over time, as the financial opaqueness of LGFVs and their weak standalone credit profiles are inherently less compelling for offshore investors with limited information flow to track the investments.

0% 0% 0% 2%

19% 10% 4%12%

82%90% 96%

86%

0%

20%

40%

60%

80%

100%

2014 2015 2016 2017

US Europe Asia

12%

29%

48%

9%

2%

Insurance / pension funds BankAsset managers Private bank & RetailOthers

23

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

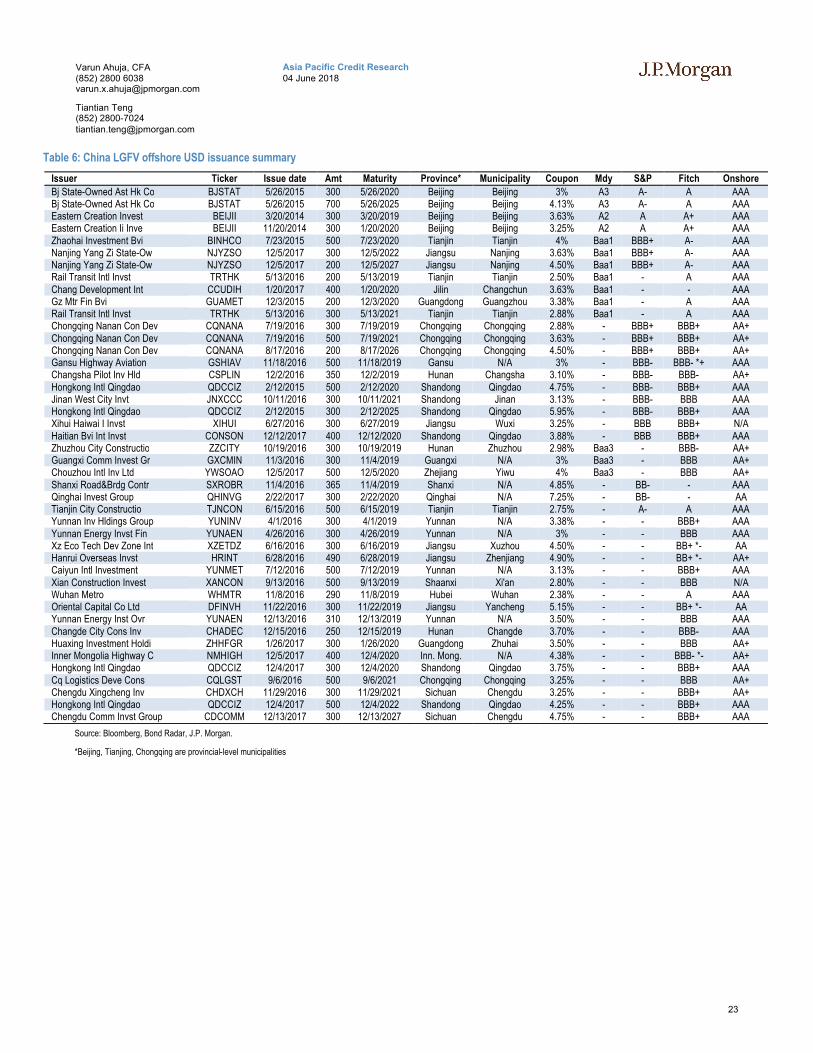

Table 6: China LGFV offshore USD issuance summary

Issuer Ticker Issue date Amt Maturity Province* Municipality Coupon Mdy S&P Fitch Onshore

Bj State-Owned Ast Hk Co BJSTAT 5/26/2015 300 5/26/2020 Beijing Beijing 3% A3 A- A AAABj State-Owned Ast Hk Co BJSTAT 5/26/2015 700 5/26/2025 Beijing Beijing 4.13% A3 A- A AAAEastern Creation Invest BEIJII 3/20/2014 300 3/20/2019 Beijing Beijing 3.63% A2 A A+ AAAEastern Creation Ii Inve BEIJII 11/20/2014 300 1/20/2020 Beijing Beijing 3.25% A2 A A+ AAAZhaohai Investment Bvi BINHCO 7/23/2015 500 7/23/2020 Tianjin Tianjin 4% Baa1 BBB+ A- AAANanjing Yang Zi State-Ow NJYZSO 12/5/2017 300 12/5/2022 Jiangsu Nanjing 3.63% Baa1 BBB+ A- AAANanjing Yang Zi State-Ow NJYZSO 12/5/2017 200 12/5/2027 Jiangsu Nanjing 4.50% Baa1 BBB+ A- AAARail Transit Intl Invst TRTHK 5/13/2016 200 5/13/2019 Tianjin Tianjin 2.50% Baa1 - A AAAChang Development Int CCUDIH 1/20/2017 400 1/20/2020 Jilin Changchun 3.63% Baa1 - - AAAGz Mtr Fin Bvi GUAMET 12/3/2015 200 12/3/2020 Guangdong Guangzhou 3.38% Baa1 - A AAARail Transit Intl Invst TRTHK 5/13/2016 300 5/13/2021 Tianjin Tianjin 2.88% Baa1 - A AAAChongqing Nanan Con Dev CQNANA 7/19/2016 300 7/19/2019 Chongqing Chongqing 2.88% - BBB+ BBB+ AA+Chongqing Nanan Con Dev CQNANA 7/19/2016 500 7/19/2021 Chongqing Chongqing 3.63% - BBB+ BBB+ AA+Chongqing Nanan Con Dev CQNANA 8/17/2016 200 8/17/2026 Chongqing Chongqing 4.50% - BBB+ BBB+ AA+Gansu Highway Aviation GSHIAV 11/18/2016 500 11/18/2019 Gansu N/A 3% - BBB- BBB- *+ AAAChangsha Pilot Inv Hld CSPLIN 12/2/2016 350 12/2/2019 Hunan Changsha 3.10% - BBB- BBB- AA+Hongkong Intl Qingdao QDCCIZ 2/12/2015 500 2/12/2020 Shandong Qingdao 4.75% - BBB- BBB+ AAAJinan West City Invt JNXCCC 10/11/2016 300 10/11/2021 Shandong Jinan 3.13% - BBB- BBB AAAHongkong Intl Qingdao QDCCIZ 2/12/2015 300 2/12/2025 Shandong Qingdao 5.95% - BBB- BBB+ AAAXihui Haiwai I Invst XIHUI 6/27/2016 300 6/27/2019 Jiangsu Wuxi 3.25% - BBB BBB+ N/AHaitian Bvi Int Invst CONSON 12/12/2017 400 12/12/2020 Shandong Qingdao 3.88% - BBB BBB+ AAAZhuzhou City Constructio ZZCITY 10/19/2016 300 10/19/2019 Hunan Zhuzhou 2.98% Baa3 - BBB- AA+Guangxi Comm Invest Gr GXCMIN 11/3/2016 300 11/4/2019 Guangxi N/A 3% Baa3 - BBB AA+Chouzhou Intl Inv Ltd YWSOAO 12/5/2017 500 12/5/2020 Zhejiang Yiwu 4% Baa3 - BBB AA+Shanxi Road&Brdg Contr SXROBR 11/4/2016 365 11/4/2019 Shanxi N/A 4.85% - BB- - AAAQinghai Invest Group QHINVG 2/22/2017 300 2/22/2020 Qinghai N/A 7.25% - BB- - AATianjin City Constructio TJNCON 6/15/2016 500 6/15/2019 Tianjin Tianjin 2.75% - A- A AAAYunnan Inv Hldings Group YUNINV 4/1/2016 300 4/1/2019 Yunnan N/A 3.38% - - BBB+ AAAYunnan Energy Invst Fin YUNAEN 4/26/2016 300 4/26/2019 Yunnan N/A 3% - - BBB AAAXz Eco Tech Dev Zone Int XZETDZ 6/16/2016 300 6/16/2019 Jiangsu Xuzhou 4.50% - - BB+ *- AAHanrui Overseas Invst HRINT 6/28/2016 490 6/28/2019 Jiangsu Zhenjiang 4.90% - - BB+ *- AA+Caiyun Intl Investment YUNMET 7/12/2016 500 7/12/2019 Yunnan N/A 3.13% - - BBB+ AAAXian Construction Invest XANCON 9/13/2016 500 9/13/2019 Shaanxi Xi'an 2.80% - - BBB N/AWuhan Metro WHMTR 11/8/2016 290 11/8/2019 Hubei Wuhan 2.38% - - A AAAOriental Capital Co Ltd DFINVH 11/22/2016 300 11/22/2019 Jiangsu Yancheng 5.15% - - BB+ *- AAYunnan Energy Inst Ovr YUNAEN 12/13/2016 310 12/13/2019 Yunnan N/A 3.50% - - BBB AAAChangde City Cons Inv CHADEC 12/15/2016 250 12/15/2019 Hunan Changde 3.70% - - BBB- AAAHuaxing Investment Holdi ZHHFGR 1/26/2017 300 1/26/2020 Guangdong Zhuhai 3.50% - - BBB AA+Inner Mongolia Highway C NMHIGH 12/5/2017 400 12/4/2020 Inn. Mong. N/A 4.38% - - BBB- *- AA+Hongkong Intl Qingdao QDCCIZ 12/4/2017 300 12/4/2020 Shandong Qingdao 3.75% - - BBB+ AAACq Logistics Deve Cons CQLGST 9/6/2016 500 9/6/2021 Chongqing Chongqing 3.25% - - BBB AA+Chengdu Xingcheng Inv CHDXCH 11/29/2016 300 11/29/2021 Sichuan Chengdu 3.25% - - BBB+ AA+Hongkong Intl Qingdao QDCCIZ 12/4/2017 500 12/4/2022 Shandong Qingdao 4.25% - - BBB+ AAAChengdu Comm Invst Group CDCOMM 12/13/2017 300 12/13/2027 Sichuan Chengdu 4.75% - - BBB+ AAA

Source: Bloomberg, Bond Radar, J.P. Morgan.

*Beijing, Tianjing, Chongqing are provincial-level municipalities

24

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

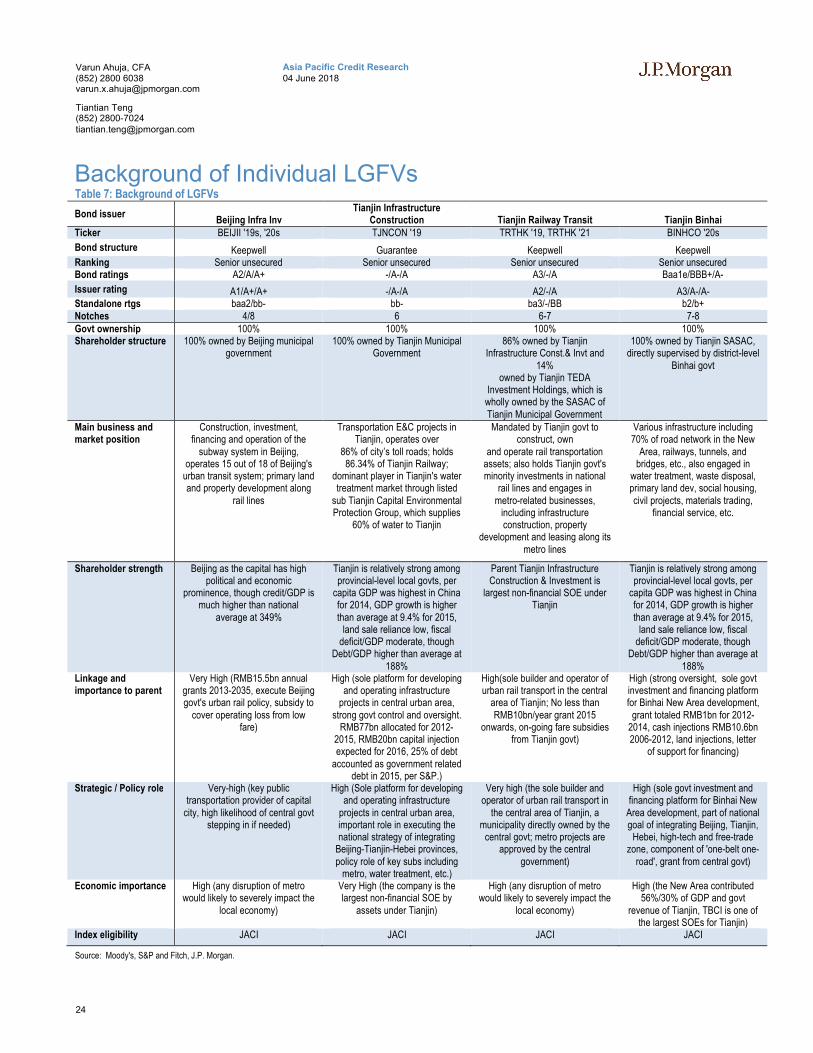

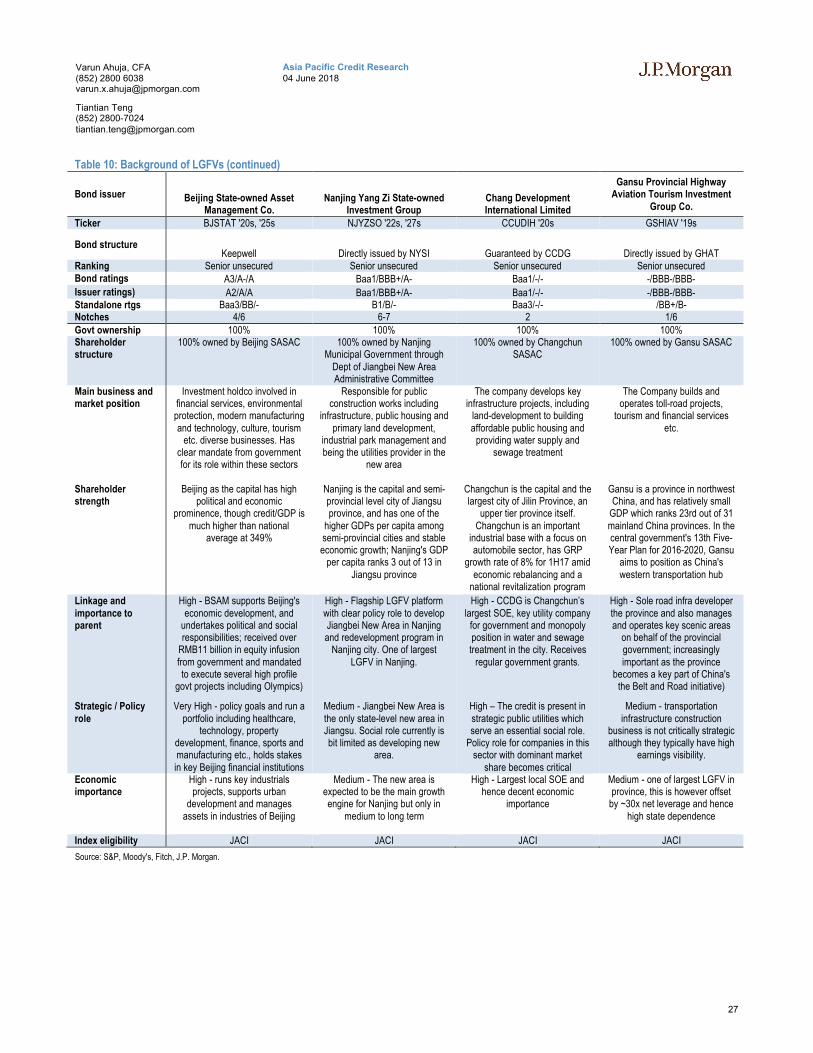

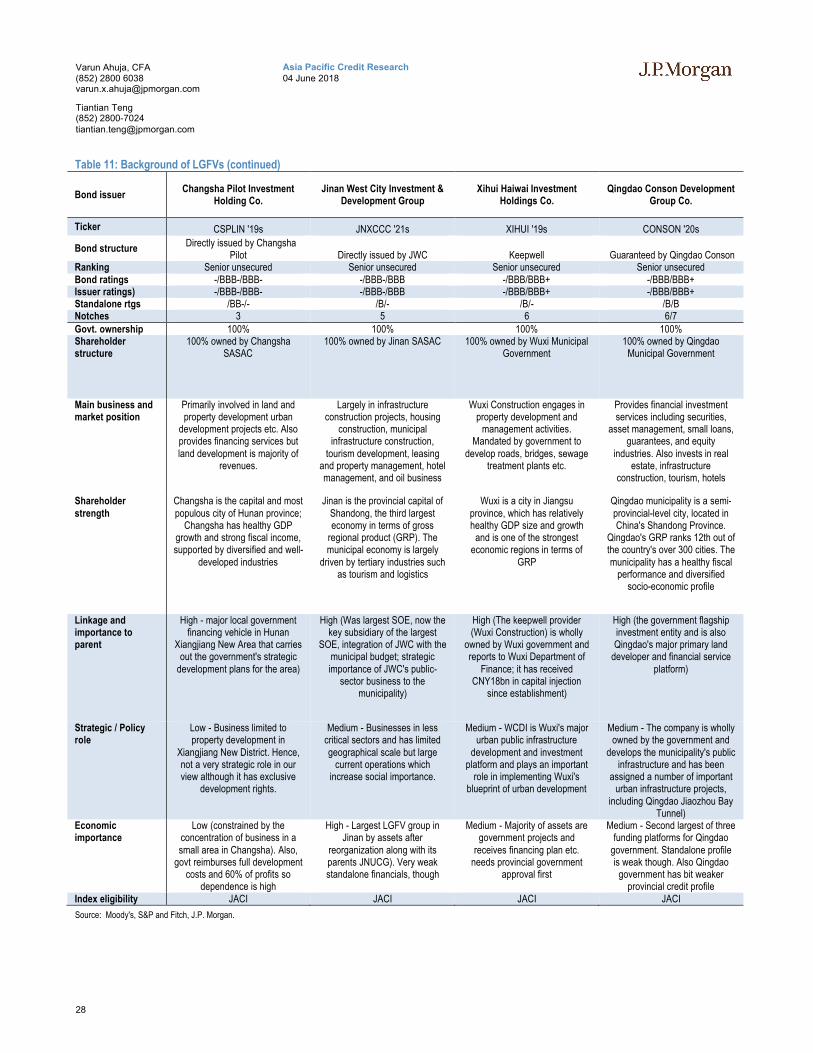

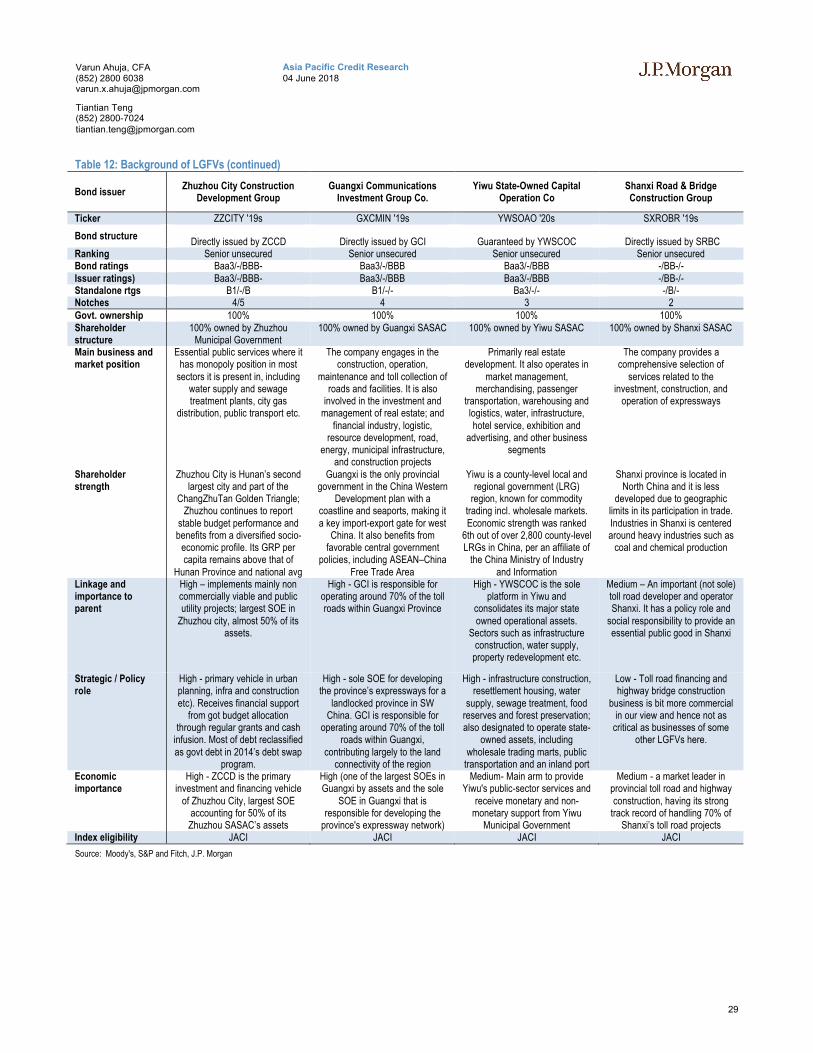

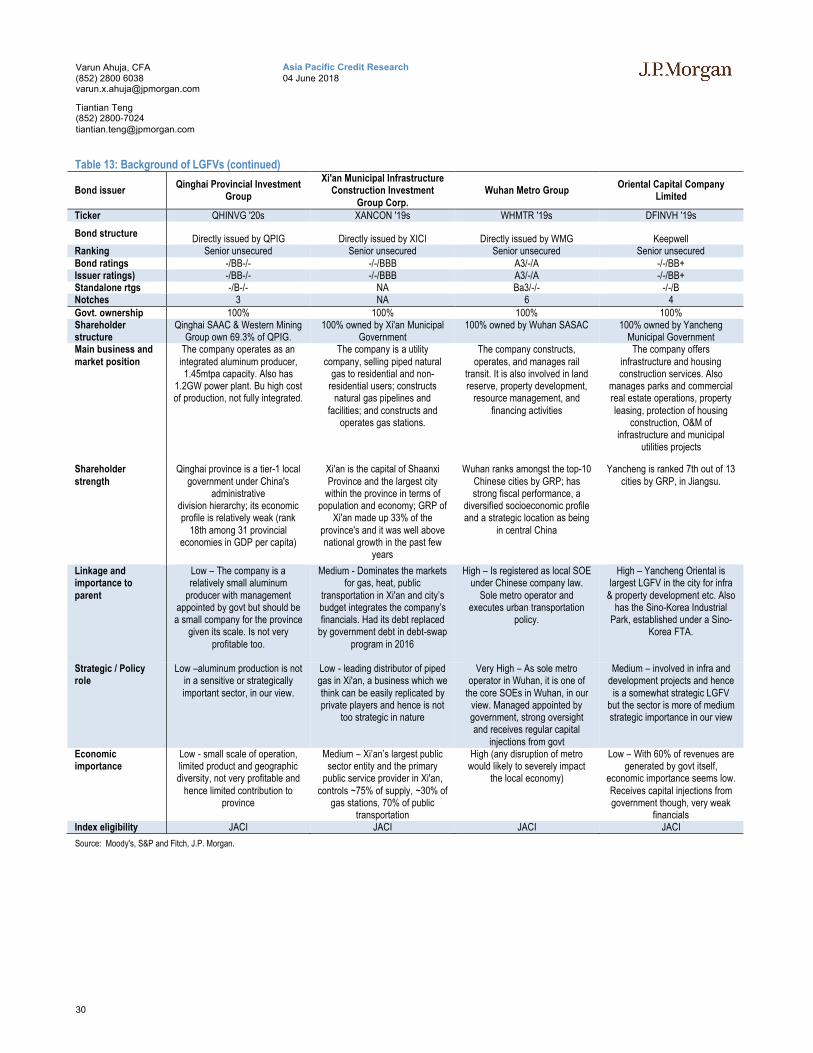

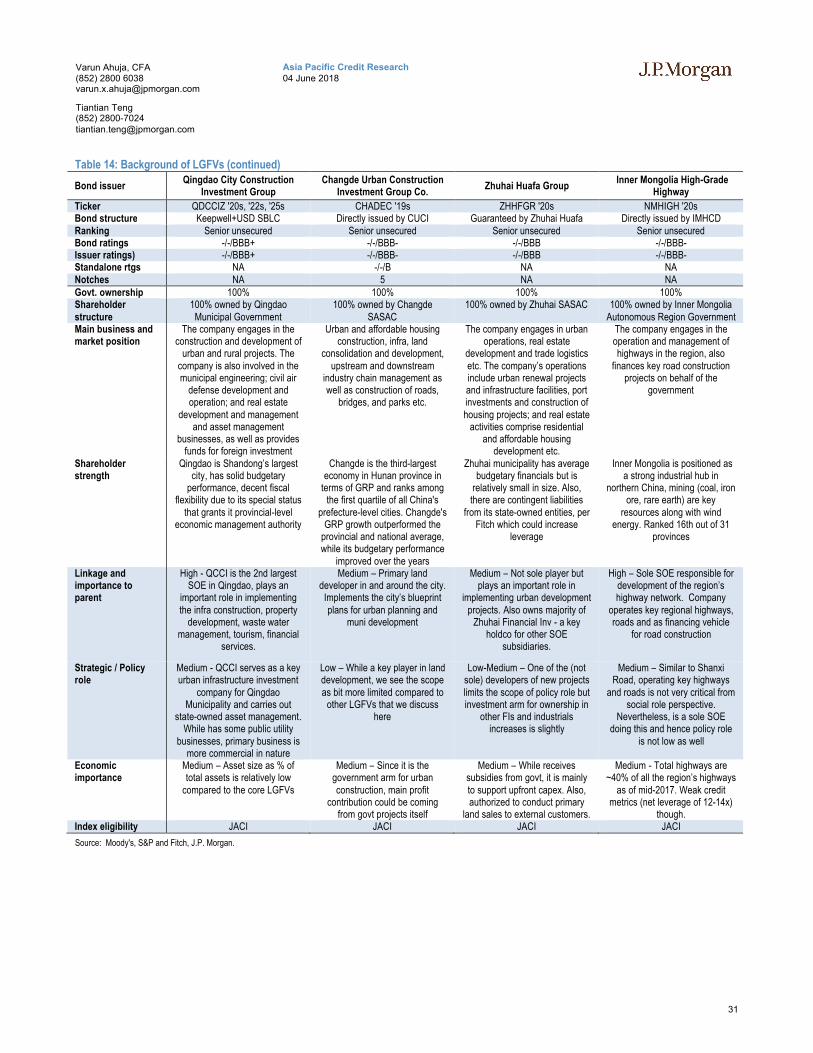

Background of Individual LGFVsTable 7: Background of LGFVs

Bond issuerBeijing Infra Inv

Tianjin Infrastructure Construction Tianjin Railway Transit Tianjin Binhai

Ticker BEIJII '19s, '20s TJNCON '19 TRTHK '19, TRTHK '21 BINHCO '20s

Bond structure Keepwell Guarantee Keepwell KeepwellRanking Senior unsecured Senior unsecured Senior unsecured Senior unsecuredBond ratings A2/A/A+ -/A-/A A3/-/A Baa1e/BBB+/A-

Issuer rating A1/A+/A+ -/A-/A A2/-/A A3/A-/A-Standalone rtgs baa2/bb- bb- ba3/-/BB b2/b+Notches 4/8 6 6-7 7-8Govt ownership 100% 100% 100% 100%Shareholder structure 100% owned by Beijing municipal

government100% owned by Tianjin Municipal

Government86% owned by Tianjin

Infrastructure Const.& Invt and 14%

owned by Tianjin TEDA Investment Holdings, which is

wholly owned by the SASAC of Tianjin Municipal Government

100% owned by Tianjin SASAC, directly supervised by district-level

Binhai govt

Main business and market position

Construction, investment, financing and operation of the

subway system in Beijing, operates 15 out of 18 of Beijing's

urban transit system; primary land and property development along

rail lines

Transportation E&C projects inTianjin, operates over

86% of city’s toll roads; holds 86.34% of Tianjin Railway;

dominant player in Tianjin's water treatment market through listed

sub Tianjin Capital Environmental Protection Group, which supplies

60% of water to Tianjin

Mandated by Tianjin govt to construct, own

and operate rail transportation assets; also holds Tianjin govt's minority investments in national

rail lines and engages inmetro-related businesses,

including infrastructure construction, property

development and leasing along its metro lines

Various infrastructure including 70% of road network in the New

Area, railways, tunnels, and bridges, etc., also engaged in

water treatment, waste disposal, primary land dev, social housing, civil projects, materials trading,

financial service, etc.

Shareholder strength Beijing as the capital has high political and economic

prominence, though credit/GDP is much higher than national

average at 349%

Tianjin is relatively strong among provincial-level local govts, per

capita GDP was highest in China for 2014, GDP growth is higher than average at 9.4% for 2015,

land sale reliance low, fiscal deficit/GDP moderate, though

Debt/GDP higher than average at 188%

Parent Tianjin Infrastructure Construction & Investment is

largest non-financial SOE under Tianjin

Tianjin is relatively strong among provincial-level local govts, per

capita GDP was highest in China for 2014, GDP growth is higher than average at 9.4% for 2015,

land sale reliance low, fiscal deficit/GDP moderate, though

Debt/GDP higher than average at 188%

Linkage and importance to parent

Very High (RMB15.5bn annual grants 2013-2035, execute Beijing govt's urban rail policy, subsidy to

cover operating loss from low fare)

High (sole platform for developing and operating infrastructure

projects in central urban area, strong govt control and oversight.

RMB77bn allocated for 2012-2015, RMB20bn capital injection expected for 2016, 25% of debt

accounted as government related debt in 2015, per S&P.)

High(sole builder and operator of urban rail transport in the central

area of Tianjin; No less than RMB10bn/year grant 2015

onwards, on-going fare subsidies from Tianjin govt)

High (strong oversight, sole govt investment and financing platform for Binhai New Area development,

grant totaled RMB1bn for 2012-2014, cash injections RMB10.6bn 2006-2012, land injections, letter

of support for financing)

Strategic / Policy role Very-high (key public transportation provider of capital

city, high likelihood of central govt stepping in if needed)

High (Sole platform for developing and operating infrastructure

projects in central urban area, important role in executing the national strategy of integrating

Beijing-Tianjin-Hebei provinces, policy role of key subs including

metro, water treatment, etc.)

Very high (the sole builder and operator of urban rail transport in

the central area of Tianjin, a municipality directly owned by the

central govt; metro projects are approved by the central

government)

High (sole govt investment and financing platform for Binhai New

Area development, part of national goal of integrating Beijing, Tianjin,

Hebei, high-tech and free-trade zone, component of 'one-belt one-

road', grant from central govt)

Economic importance High (any disruption of metro would likely to severely impact the

local economy)

Very High (the company is the largest non-financial SOE by

assets under Tianjin)

High (any disruption of metro would likely to severely impact the

local economy)

High (the New Area contributed 56%/30% of GDP and govt

revenue of Tianjin, TBCI is one of the largest SOEs for Tianjin)

Index eligibility JACI JACI JACI JACI

Source: Moody's, S&P and Fitch, J.P. Morgan.

25

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

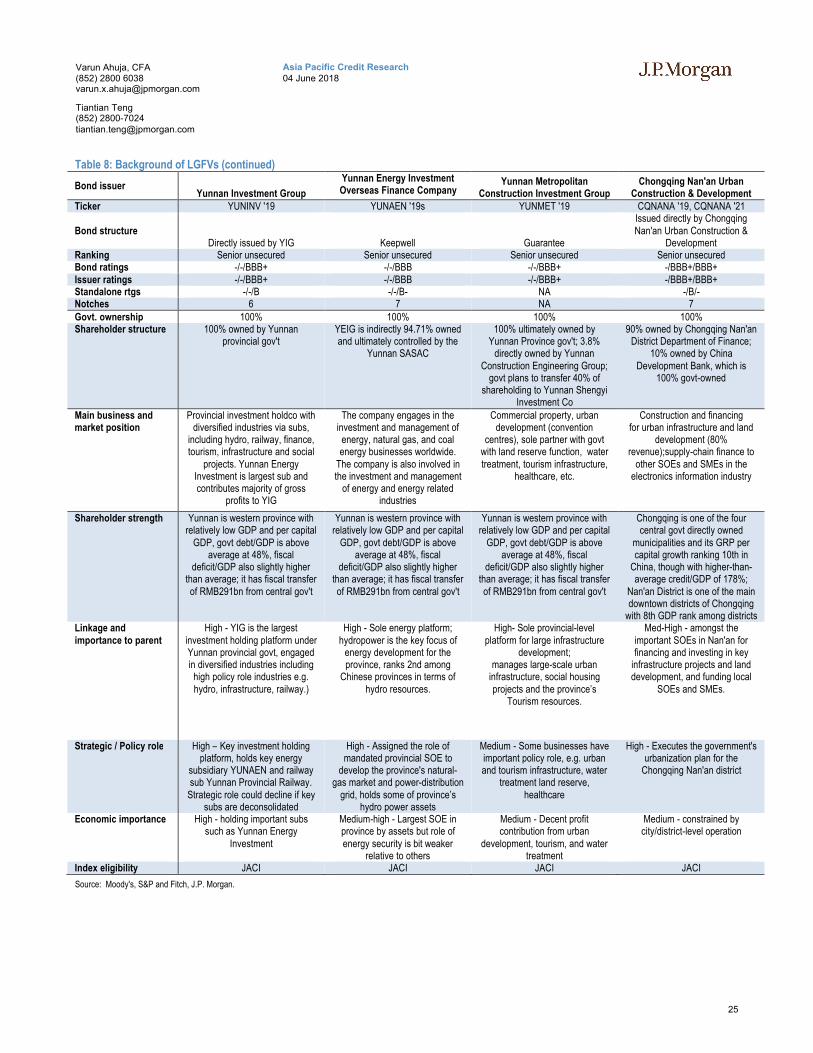

Table 8: Background of LGFVs (continued)

Bond issuerYunnan Investment Group

Yunnan Energy Investment Overseas Finance Company

Yunnan Metropolitan Construction Investment Group

Chongqing Nan'an Urban Construction & Development

Ticker YUNINV '19 YUNAEN '19s YUNMET '19 CQNANA '19, CQNANA '21

Bond structureDirectly issued by YIG Keepwell Guarantee

Issued directly by Chongqing Nan'an Urban Construction &

DevelopmentRanking Senior unsecured Senior unsecured Senior unsecured Senior unsecuredBond ratings -/-/BBB+ -/-/BBB -/-/BBB+ -/BBB+/BBB+Issuer ratings -/-/BBB+ -/-/BBB -/-/BBB+ -/BBB+/BBB+Standalone rtgs -/-/B -/-/B- NA -/B/-Notches 6 7 NA 7Govt. ownership 100% 100% 100% 100%Shareholder structure 100% owned by Yunnan

provincial gov'tYEIG is indirectly 94.71% owned and ultimately controlled by the

Yunnan SASAC

100% ultimately owned by Yunnan Province gov't; 3.8%

directly owned by Yunnan Construction Engineering Group;

govt plans to transfer 40% of shareholding to Yunnan Shengyi

Investment Co

90% owned by Chongqing Nan'anDistrict Department of Finance;

10% owned by China Development Bank, which is

100% govt-owned

Main business and market position

Provincial investment holdco with diversified industries via subs,

including hydro, railway, finance, tourism, infrastructure and social

projects. Yunnan Energy Investment is largest sub and contributes majority of gross

profits to YIG

The company engages in the investment and management of energy, natural gas, and coal energy businesses worldwide.

The company is also involved inthe investment and management

of energy and energy related industries

Commercial property, urban development (convention

centres), sole partner with govt with land reserve function, water treatment, tourism infrastructure,

healthcare, etc.

Construction and financingfor urban infrastructure and land

development (80% revenue);supply-chain finance to

other SOEs and SMEs in the electronics information industry

Shareholder strength Yunnan is western province with relatively low GDP and per capital

GDP, govt debt/GDP is above average at 48%, fiscal

deficit/GDP also slightly higher than average; it has fiscal transfer of RMB291bn from central gov't

Yunnan is western province with relatively low GDP and per capital

GDP, govt debt/GDP is above average at 48%, fiscal

deficit/GDP also slightly higher than average; it has fiscal transfer of RMB291bn from central gov't

Yunnan is western province with relatively low GDP and per capital

GDP, govt debt/GDP is above average at 48%, fiscal

deficit/GDP also slightly higherthan average; it has fiscal transfer of RMB291bn from central gov't

Chongqing is one of the four central govt directly owned

municipalities and its GRP per capital growth ranking 10th in

China, though with higher-than-average credit/GDP of 178%;

Nan'an District is one of the main downtown districts of Chongqing

with 8th GDP rank among districts Linkage and importance to parent

High - YIG is the largest investment holding platform under Yunnan provincial govt, engaged in diversified industries including high policy role industries e.g. hydro, infrastructure, railway.)

High - Sole energy platform; hydropower is the key focus of

energy development for the province, ranks 2nd among

Chinese provinces in terms of hydro resources.

High- Sole provincial-level platform for large infrastructure

development;manages large-scale urban

infrastructure, social housing projects and the province’s

Tourism resources.

Med-High - amongst theimportant SOEs in Nan'an forfinancing and investing in key

infrastructure projects and land development, and funding local

SOEs and SMEs.

Strategic / Policy role High – Key investment holding platform, holds key energy

subsidiary YUNAEN and railway sub Yunnan Provincial Railway.

Strategic role could decline if key subs are deconsolidated

High - Assigned the role of mandated provincial SOE to

develop the province's natural-gas market and power-distribution

grid, holds some of province’shydro power assets

Medium - Some businesses haveimportant policy role, e.g. urban and tourism infrastructure, water

treatment land reserve, healthcare

High - Executes the government's urbanization plan for the

Chongqing Nan'an district

Economic importance High - holding important subs such as Yunnan Energy

Investment

Medium-high - Largest SOE in province by assets but role ofenergy security is bit weaker

relative to others

Medium - Decent profit contribution from urban

development, tourism, and water treatment

Medium - constrained by city/district-level operation

Index eligibility JACI JACI JACI JACI

Source: Moody's, S&P and Fitch, J.P. Morgan.

26

Asia Pacific Credit Research04 June 2018

Varun Ahuja, CFA(852) 2800 [email protected]

Tiantian Teng(852) [email protected]

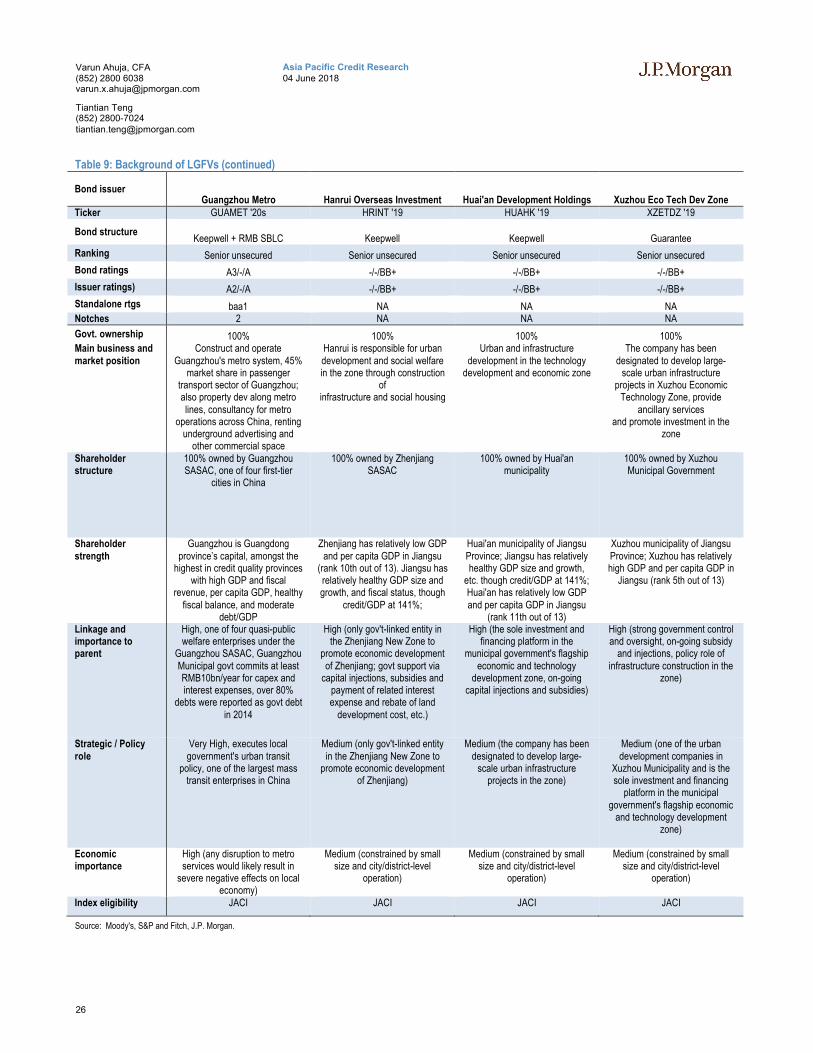

Table 9: Background of LGFVs (continued)

Bond issuerGuangzhou Metro Hanrui Overseas Investment Huai'an Development Holdings Xuzhou Eco Tech Dev Zone

Ticker GUAMET '20s HRINT '19 HUAHK '19 XZETDZ '19

Bond structureKeepwell + RMB SBLC Keepwell Keepwell Guarantee

Ranking Senior unsecured Senior unsecured Senior unsecured Senior unsecured

Bond ratings A3/-/A -/-/BB+ -/-/BB+ -/-/BB+

Issuer ratings) A2/-/A -/-/BB+ -/-/BB+ -/-/BB+

Standalone rtgs baa1 NA NA NA Notches 2 NA NA NA

Govt. ownership 100% 100% 100% 100%Main business and market position

Construct and operate Guangzhou's metro system, 45%

market share in passenger transport sector of Guangzhou; also property dev along metro lines, consultancy for metro

operations across China, renting underground advertising and

other commercial space

Hanrui is responsible for urban development and social welfare in the zone through construction

ofinfrastructure and social housing

Urban and infrastructure development in the technology

development and economic zone

The company has been designated to develop large-

scale urban infrastructure projects in Xuzhou Economic

Technology Zone, provide ancillary services

and promote investment in the zone

Shareholder structure

100% owned by Guangzhou SASAC, one of four first-tier

cities in China

100% owned by Zhenjiang SASAC

100% owned by Huai'an municipality

100% owned by Xuzhou Municipal Government

Shareholder strength

Guangzhou is Guangdong province’s capital, amongst the

highest in credit quality provinces with high GDP and fiscal

revenue, per capita GDP, healthy fiscal balance, and moderate

debt/GDP

Zhenjiang has relatively low GDP and per capita GDP in Jiangsu

(rank 10th out of 13). Jiangsu has relatively healthy GDP size and growth, and fiscal status, though

credit/GDP at 141%;

Huai'an municipality of Jiangsu Province; Jiangsu has relatively healthy GDP size and growth,

etc. though credit/GDP at 141%; Huai'an has relatively low GDP and per capita GDP in Jiangsu

(rank 11th out of 13)

Xuzhou municipality of JiangsuProvince; Xuzhou has relatively high GDP and per capita GDP in

Jiangsu (rank 5th out of 13)

Linkage and importance to parent

High, one of four quasi-public welfare enterprises under the

Guangzhou SASAC, Guangzhou Municipal govt commits at least RMB10bn/year for capex and interest expenses, over 80%

debts were reported as govt debt in 2014