June 2014 China Digital TV Holding

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

June 2014

China Digital TV Holding

11

Company Overview Leading Provider of CA Systems to China’s Digital TV Market

2

CA DRM NBP

DVB OTT

CA

Company Overview

Exchange New York Stock Exchange

Ticker STV

Market Cap US$200M

Headquarters Beijing, China

Employee 700+ (including approx. 400 R&D staff)

11

Conditional Access Systems (CAS) & Digital Rights Management (DRM)

3

Core technology for Pay TV market.

Protects the security of signal transmission through signal

encryption in the head end and signal decryption in the terminal

end.

Transmission Channels: Cable, satellite and terrestrial TV.

CAS

Terminal End System Smart Card Head End System

Using the leading security technologies in content encryption,

access control , key replacement, two-way authentication, fingerprint

watermark, clone detection and chromosome tracking to protect

contents.

Can be used in cable TV, IPTV, Internet TV and any other Pay TV

platforms to protect content.

DRM

CA DRM NBP

DVB OTT

11

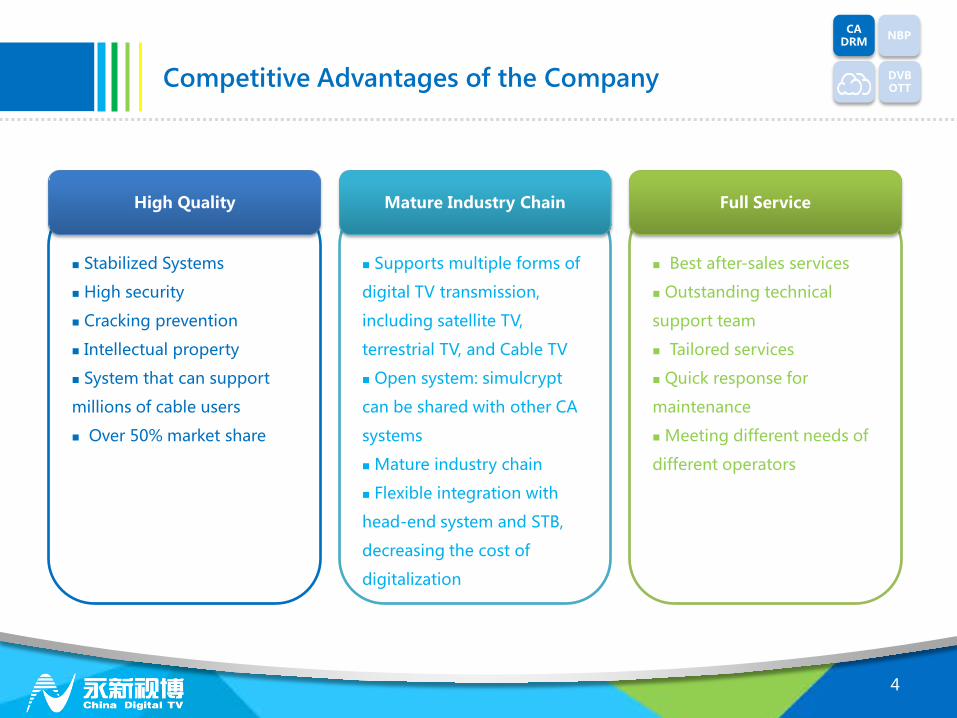

Best after-sales services

Outstanding technical

support team

Tailored services

Quick response for

maintenance

Meeting different needs of

different operators

Supports multiple forms of

digital TV transmission,

including satellite TV,

terrestrial TV, and Cable TV

Open system: simulcrypt

can be shared with other CA

systems

Mature industry chain

Flexible integration with

head-end system and STB,

decreasing the cost of

digitalization

Competitive Advantages of the Company

Stabilized Systems

High security

Cracking prevention

Intellectual property

System that can support

millions of cable users

Over 50% market share

High Quality Mature Industry Chain Full Service

CA DRM NBP

DVB OTT

4

11

China Market Large and Diversified Customer Base

5

China Market

Domestic market

18.2

15.0 15.6

2011 2012 2013

Smart Card Shipment Volume - Domestic Market

(Million)

CA DRM NBP

DVB OTT

*Data Source: Zhongguang Luoda Report and company data

29 provincial operators use STV’s CA systems More than 100million smart cards accumulatively shipped in China market as of Mar 31, 2014 52% market share in year of 2013

CA DRM

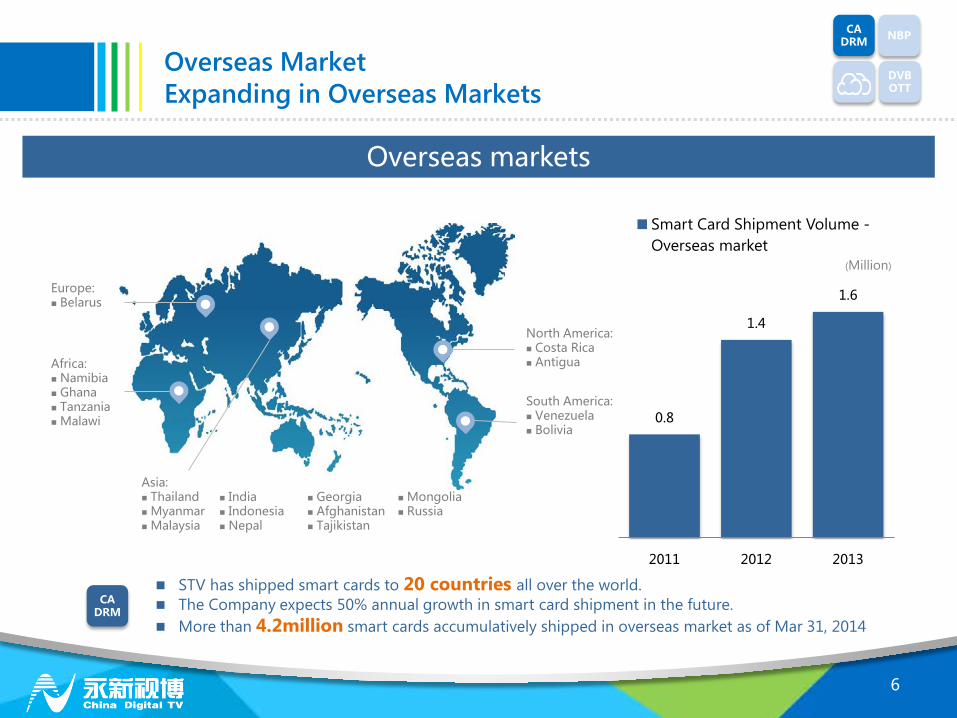

11 0.8

1.4

1.6

2011 2012 2013

Smart Card Shipment Volume - Overseas market

6

North America: Costa Rica Antigua

Overseas markets

South America: Venezuela Bolivia

Africa: Namibia Ghana Tanzania Malawi

Europe: Belarus

Asia: Thailand Myanmar Malaysia

India Indonesia Nepal

Georgia Afghanistan Tajikistan

Mongolia Russia

Overseas Market Expanding in Overseas Markets

CA DRM NBP

DVB OTT

(Million)

STV has shipped smart cards to 20 countries all over the world. The Company expects 50% annual growth in smart card shipment in the future. More than 4.2million smart cards accumulatively shipped in overseas market as of Mar 31, 2014

CA DRM

11

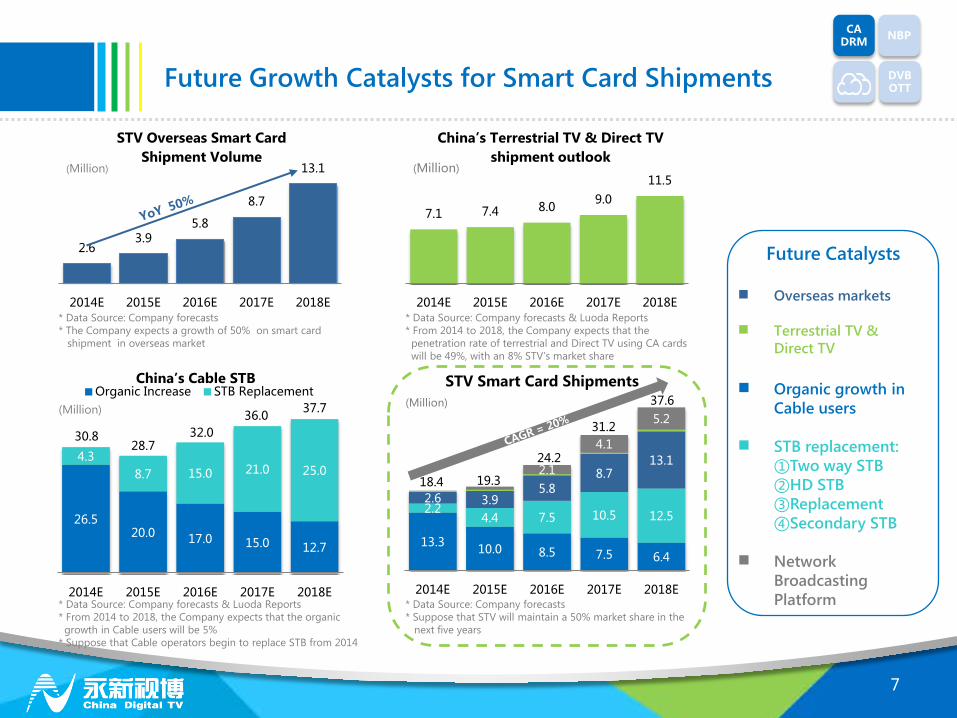

13.3 10.0 8.5 7.5 6.4

2.2 4.4 7.5 10.5 12.5

2.6 3.9 5.8

8.7 13.1

2.1

4.1

5.2

2014E 2015E 2016E 2017E 2018E

STV Smart Card Shipments

18.4 19.3

24.2

31.2

37.6 (Million)

Future Growth Catalysts for Smart Card Shipments

7

7.1 7.4 8.0 9.0 11.5

2014E 2015E 2016E 2017E 2018E

China’s Terrestrial TV & Direct TV shipment outlook

(Million)

CA DRM NBP

DVB OTT

Future Catalysts

Overseas markets

Terrestrial TV & Direct TV

Organic growth in

Cable users

STB replacement: ①Two way STB ②HD STB ③Replacement ④Secondary STB

Network

Broadcasting Platform

26.5 20.0 17.0 15.0 12.7

4.3 8.7 15.0 21.0 25.0

2014E 2015E 2016E 2017E 2018E

China’s Cable STB Organic Increase STB Replacement

30.8 28.7

32.0 36.0 37.7 (Million)

2.6 3.9

5.8

8.7

13.1

2014E 2015E 2016E 2017E 2018E

STV Overseas Smart Card Shipment Volume

(Million)

* Data Source: Company forecasts * The Company expects a growth of 50% on smart card shipment in overseas market

* Data Source: Company forecasts & Luoda Reports * From 2014 to 2018, the Company expects that the penetration rate of terrestrial and Direct TV using CA cards will be 49%, with an 8% STV’s market share

* Data Source: Company forecasts & Luoda Reports * From 2014 to 2018, the Company expects that the organic growth in Cable users will be 5% * Suppose that Cable operators begin to replace STB from 2014

* Data Source: Company forecasts * Suppose that STV will maintain a 50% market share in the next five years

11

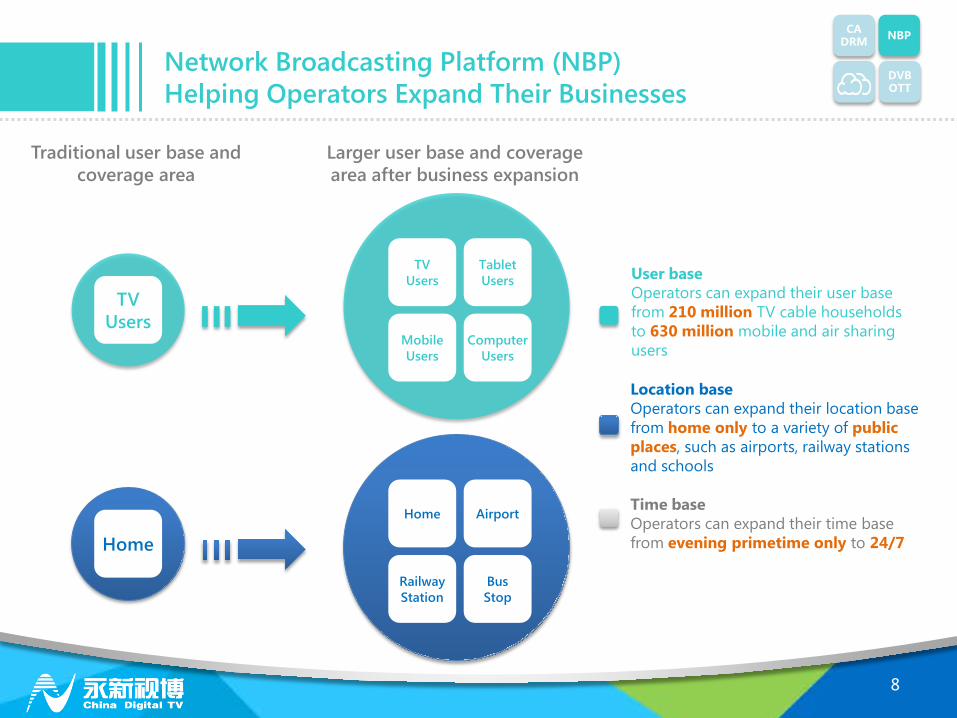

Network Broadcasting Platform (NBP) Helping Operators Expand Their Businesses

8

TV Users

Home

User base Operators can expand their user base from 210 million TV cable households to 630 million mobile and air sharing users Location base Operators can expand their location base from home only to a variety of public places, such as airports, railway stations and schools

Time base Operators can expand their time base from evening primetime only to 24/7

Traditional user base and coverage area

Larger user base and coverage area after business expansion

CA DRM NBP

DVB OTT

TV Users

Tablet Users

Mobile Users

Computer Users

Home

Home Airport

Railway Station

Bus Stop

11

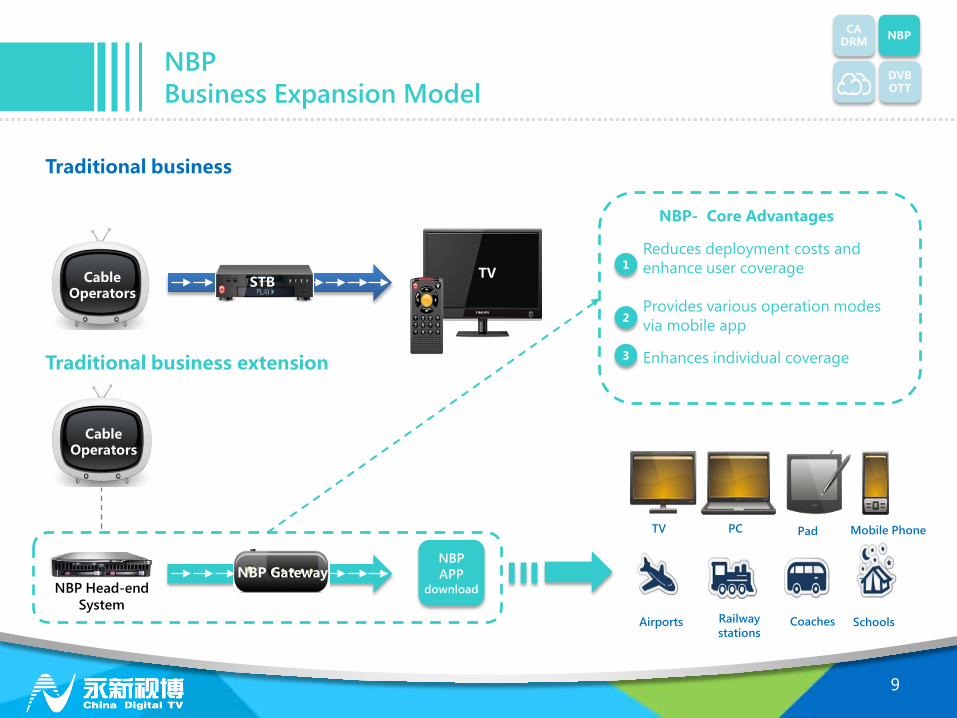

NBP Business Expansion Model

9

STB Cable Operators

TV

Cable Operators

TV PC Pad Mobile Phone

Airports Railway stations

Coaches Schools

NBP APP

download NBP Head-end System

NBP Gateway

Traditional business

Traditional business extension

Reduces deployment costs and enhance user coverage Provides various operation modes via mobile app

Enhances individual coverage

1

2

3

NBP- Core Advantages

CA DRM NBP

DVB OTT

11

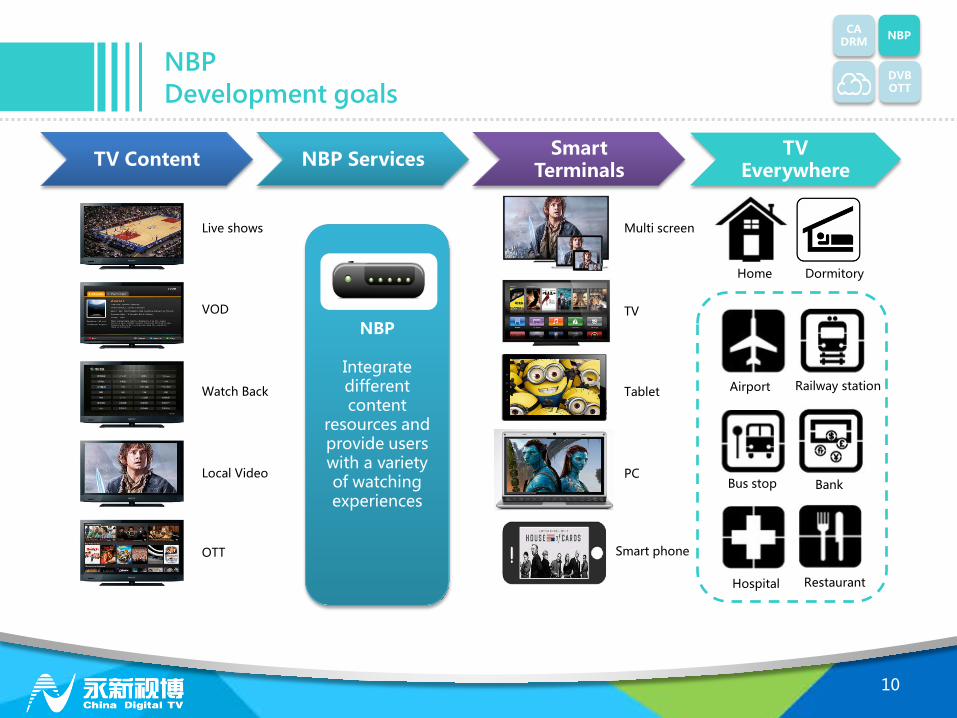

NBP Development goals

10

Live shows

VOD

Watch Back

OTT

Local Video

NBP

Integrate different content

resources and provide users with a variety of watching experiences

TV Content NBP Services Smart Terminals

TV Everywhere

TV

Tablet

PC

Smart phone

Airport Railway station

Bus stop Bank

Hospital Restaurant

Home Dormitory

Multi screen

CA DRM NBP

DVB OTT

11

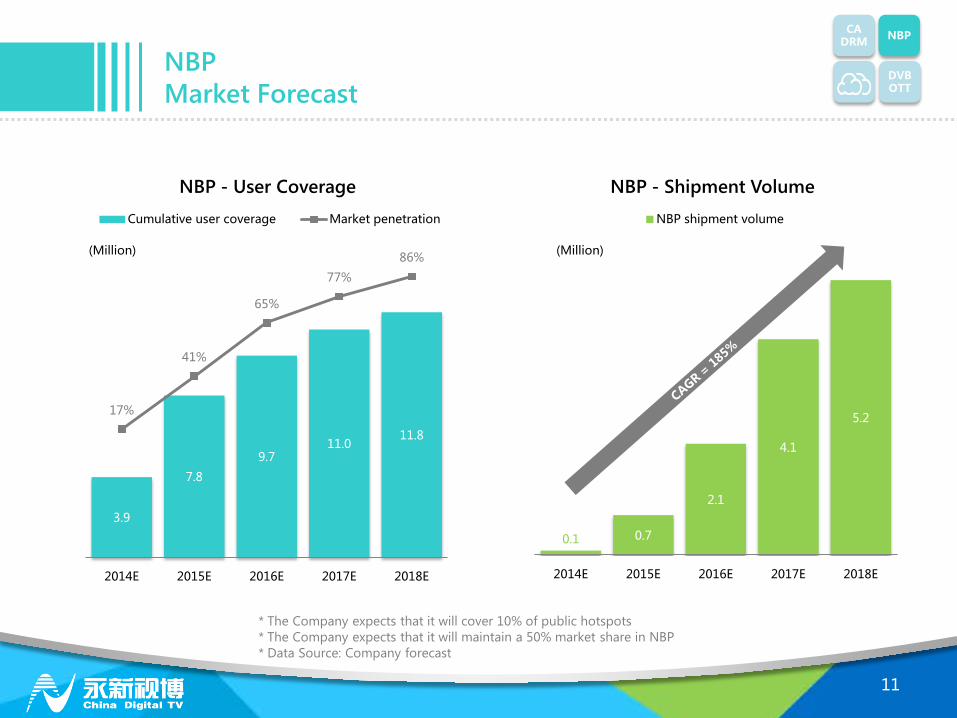

0.1 0.7

2.1

4.1

5.2

-

1

2

3

4

5

6

2014E 2015E 2016E 2017E 2018E

NBP - Shipment Volume NBP shipment volume

3.9

7.8

9.7 11.0

11.8

17%

41%

65%

77%

86%

-50%

0%

50%

100%

-1

1

3

5

7

9

11

13

15

2014E 2015E 2016E 2017E 2018E

NBP - User Coverage Cumulative user coverage Market penetration

NBP Market Forecast

11

(Million) (Million)

CA DRM NBP

DVB OTT

* The Company expects that it will cover 10% of public hotspots * The Company expects that it will maintain a 50% market share in NBP * Data Source: Company forecast

11

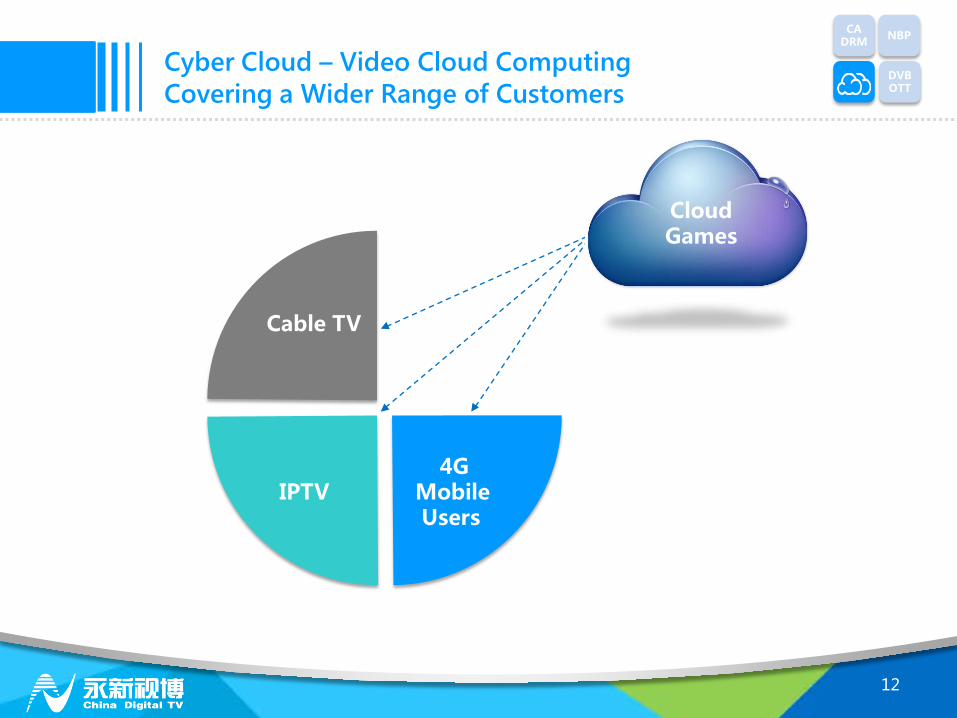

Cyber Cloud – Video Cloud Computing Covering a Wider Range of Customers

12

Cable TV

4G Mobile Users

IPTV

云游戏 Cloud Games

CA DRM NBP

DVB OTT

11

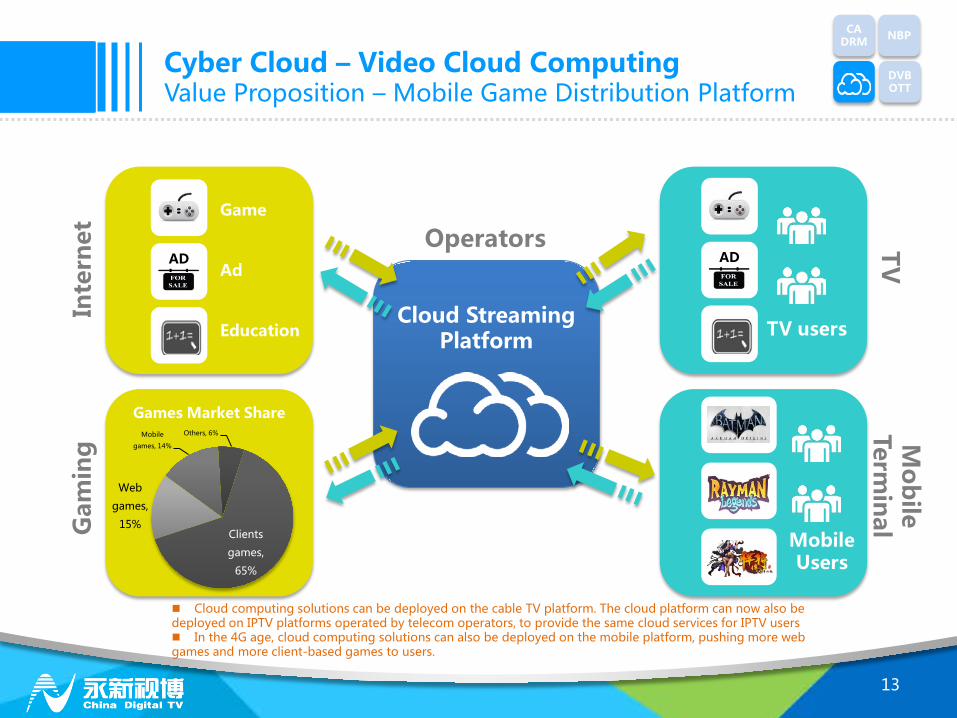

Cyber Cloud – Video Cloud Computing Value Proposition – Mobile Game Distribution Platform

13

Cloud Streaming

Platform

AD

Game

Ad

Education

Games Market Share

TV users

AD

Mobile Users

Inte

rnet

G

amin

g

TV

Mob

ile Term

inal

Operators

Cloud computing solutions can be deployed on the cable TV platform. The cloud platform can now also be deployed on IPTV platforms operated by telecom operators, to provide the same cloud services for IPTV users In the 4G age, cloud computing solutions can also be deployed on the mobile platform, pushing more web games and more client-based games to users.

Clients

games,

65%

Web

games,

15%

Mobile

games, 14%

Others, 6%

CA DRM NBP

DVB OTT

11

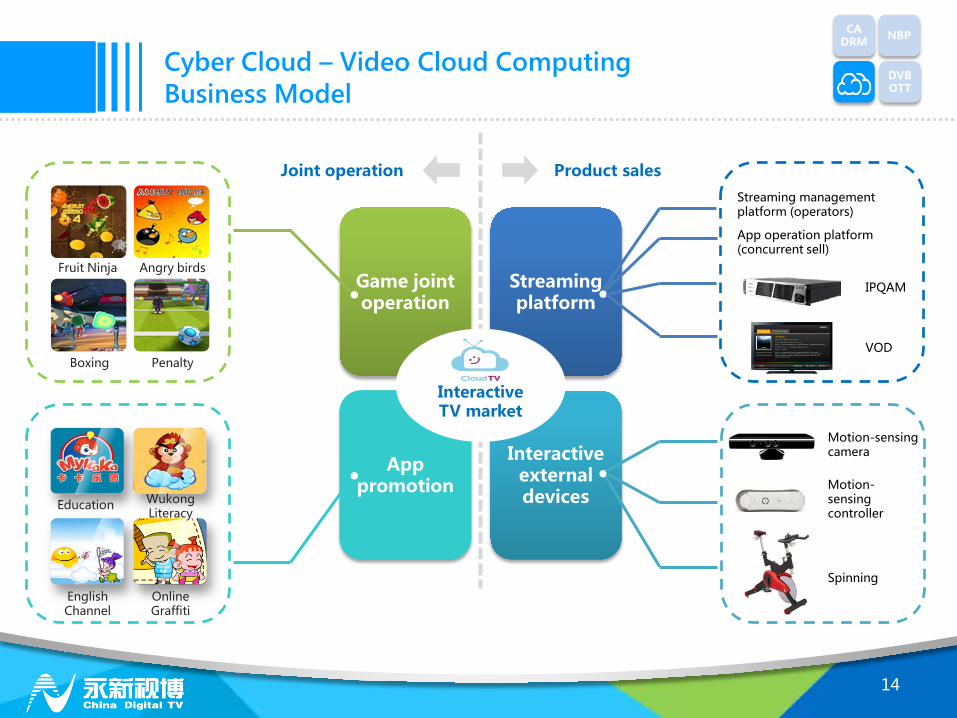

Game joint operation

Interactive external devices

App promotion

Streaming platform

Cyber Cloud – Video Cloud Computing Business Model

14

IPQAM

VOD

Motion-sensing camera

Motion-sensing controller

Spinning

Interactive TV market

Product sales Joint operation

Boxing Penalty

Fruit Ninja Angry birds

English Channel

Online Graffiti

Education Wukong Literacy

Streaming management platform (operators)

App operation platform (concurrent sell)

CA DRM NBP

DVB OTT

11

Cyber Cloud – Video Cloud Computing Product Lines

15

Cloud fitness

Cloud games

Cloud motion sensing Cloud education World-leading motion-sensing games

Fitness at home

Core players, old players

Pre-school, early childhood parent-child interaction

CA DRM NBP

DVB OTT

11

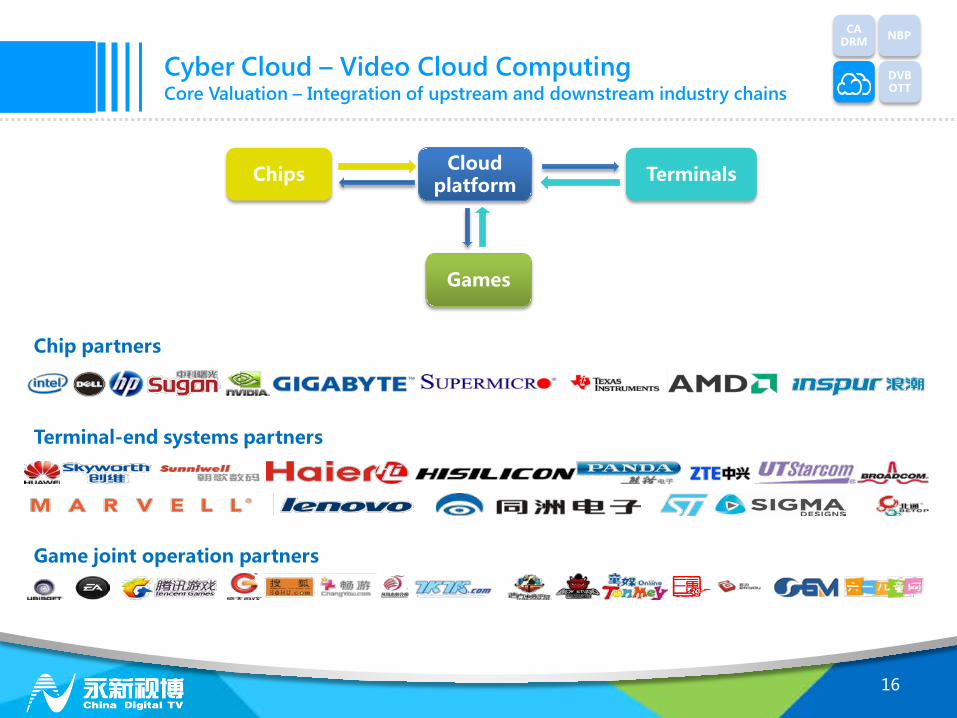

Cyber Cloud – Video Cloud Computing Core Valuation – Integration of upstream and downstream industry chains

Chip partners

Terminal-end systems partners

Game joint operation partners

Chips Cloud platform Terminals

Games

16

CA DRM NBP

DVB OTT

11

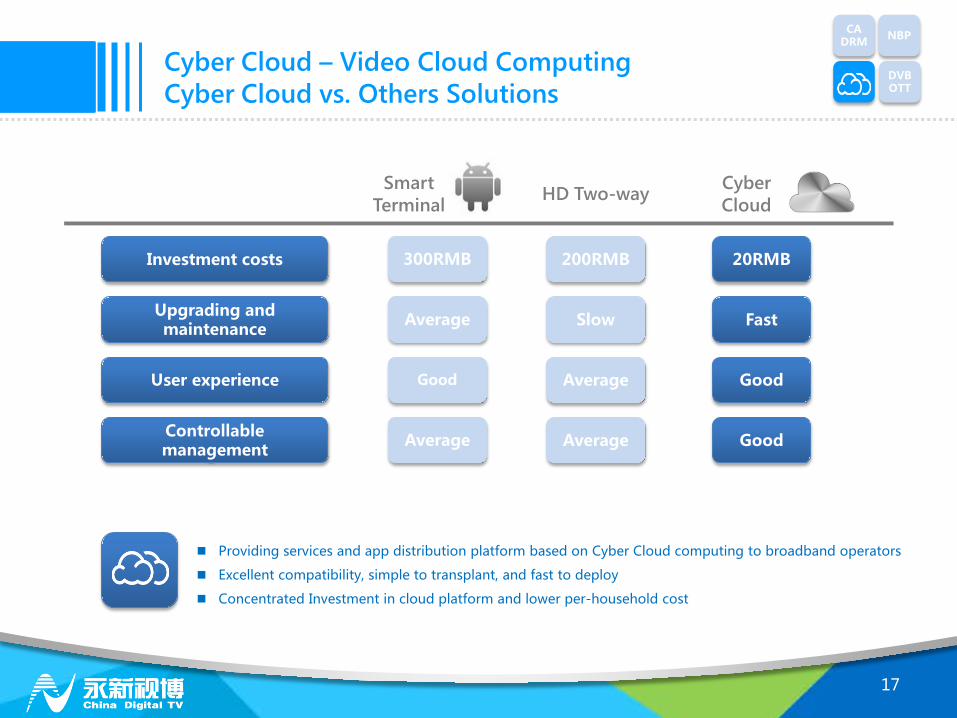

Cyber Cloud – Video Cloud Computing Cyber Cloud vs. Others Solutions

17

Smart Terminal

Cyber Cloud

Investment costs

Upgrading and maintenance

User experience

Controllable management

20RMB

Fast

Good

Good

200RMB

Slow

Average

Average

Providing services and app distribution platform based on Cyber Cloud computing to broadband operators

Excellent compatibility, simple to transplant, and fast to deploy

Concentrated Investment in cloud platform and lower per-household cost

HD Two-way

300RMB

Average

Good

Average

CA DRM NBP

DVB OTT

11

Cyber Cloud – Video Cloud Computing Market Coverage

18

Cable market Gehua Signed

Nanjing Signed

Jiangsu Signed

Dalian Signed

Shijiazhuang Signed

Jishi Signed

Shanxi Signed

Xinjiang Signed

Qingdao Signed

Hunan Signed

Chongqing Signed

Kunshan Signed

Changshu Signed

Anshan Signed

Ningbo Signed

Telecom market Beijing Unicom Signed

Shanghai Telecom Signed

Hebei Unicom Signed

Guangdong telecom Signed

Fujian Telecom Signed

Shandong Unicom

Signed

4G market

China Telecom Signed

Users coverage: Cable: 60 Million; IPTV: 8 Million

CA DRM NBP

DVB OTT

11

Cyber Cloud – Video Cloud Computing Market Coverage

19

CA DRM NBP

DVB OTT

99

139 177

222

274

2014E 2015E 2016E 2017E 2018E

China's total interactive TV subscribers

2 9

19

40

74

2014E 2015E 2016E 2017E 2018E

Cyber Cloud penetration subscribers

(Million)

(Million)

* The Company expects a cloud streaming platform penetration rate of above 50% * The Company expects Cyber Cloud to maintain a 50% market share of the cloud streaming platform market * Data Source: Company forecast

11

JOYsee DVB+OTT Solutions Core Product of Post-STB Age – Product Introduction

20

Directly connected to the TV

Traditional Business

STB Cable Operators

电视 “Live”

Cable Operators

Traditional Business Extension

Dongle + APK

Mini HD STB

“Live”

OTT

1

2

3

Core advantage

Reduces STB investment costs, while retaining traditional users Improves the user experience Enhances Internet access via smart TV; smart terminal manufacturers can provide more forms of TV Internet services.

CA DRM NBP

DVB OTT

11

21

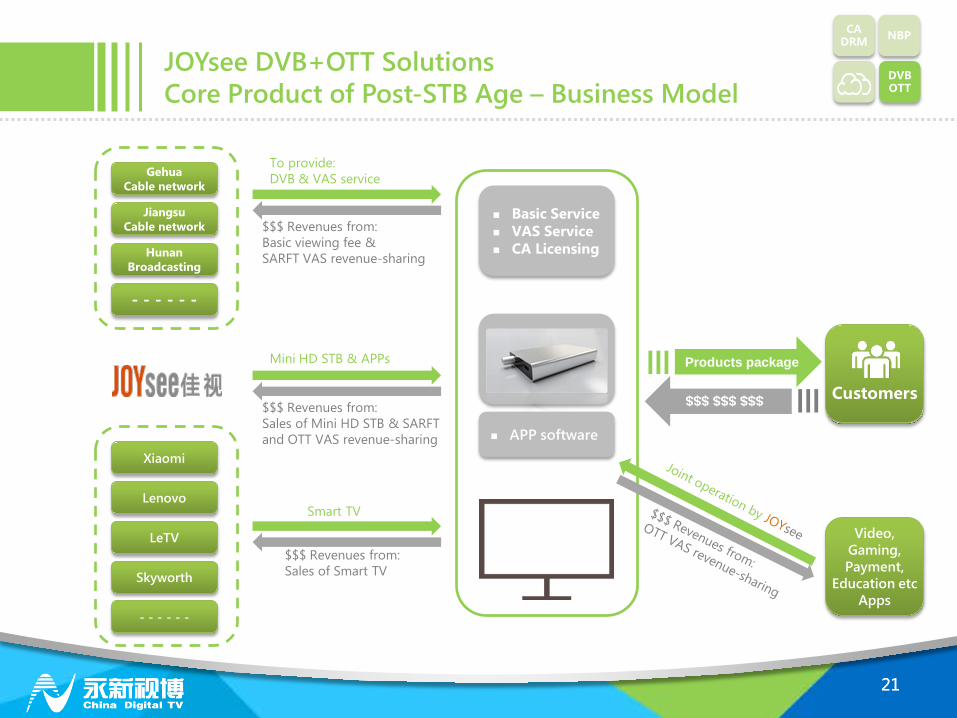

JOYsee DVB+OTT Solutions Core Product of Post-STB Age – Business Model

21

Gehua Cable network

Jiangsu Cable network

Hunan Broadcasting

- - - - - -

Xiaomi

LeTV

Lenovo

- - - - - -

Skyworth

Customers

CA DRM NBP

DVB OTT

Basic Service VAS Service CA Licensing

APP software

Products package

To provide: DVB & VAS service

Mini HD STB & APPs

Smart TV

$$$ Revenues from: Sales of Mini HD STB & SARFT and OTT VAS revenue-sharing

$$$ Revenues from: Basic viewing fee & SARFT VAS revenue-sharing

$$$ Revenues from: Sales of Smart TV

$$$ $$$ $$$

Video, Gaming, Payment,

Education etc Apps

11

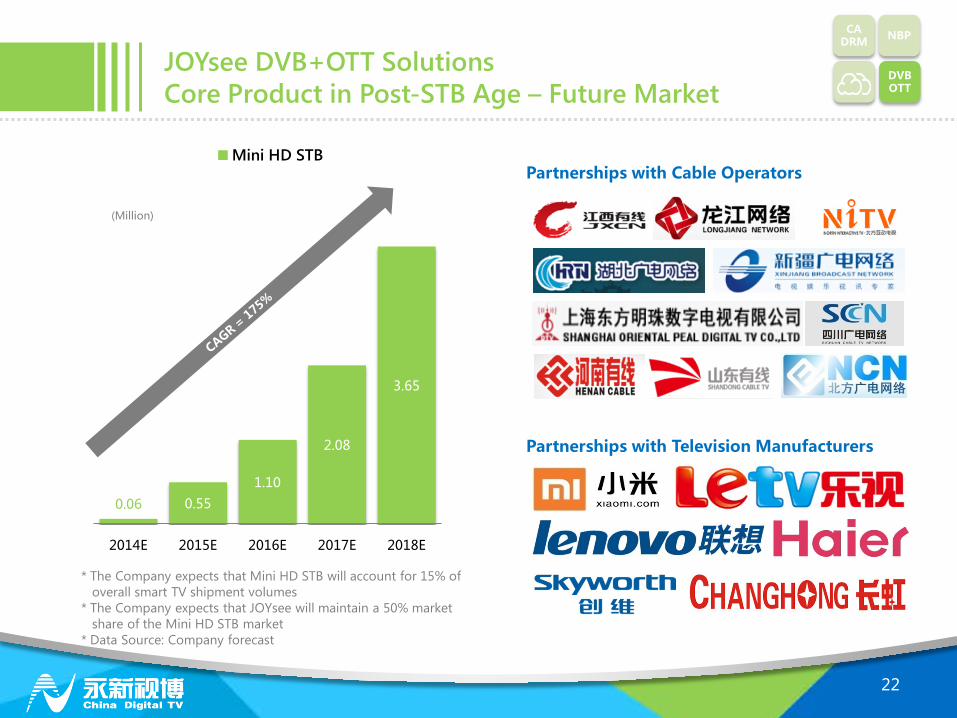

0.06 0.55 1.10

2.08

3.65

2014E 2015E 2016E 2017E 2018E

Mini HD STB

JOYsee DVB+OTT Solutions Core Product in Post-STB Age – Future Market

22

(Million)

Partnerships with Cable Operators

Partnerships with Television Manufacturers

CA DRM NBP

DVB OTT

* The Company expects that Mini HD STB will account for 15% of overall smart TV shipment volumes * The Company expects that JOYsee will maintain a 50% market share of the Mini HD STB market * Data Source: Company forecast

11

23

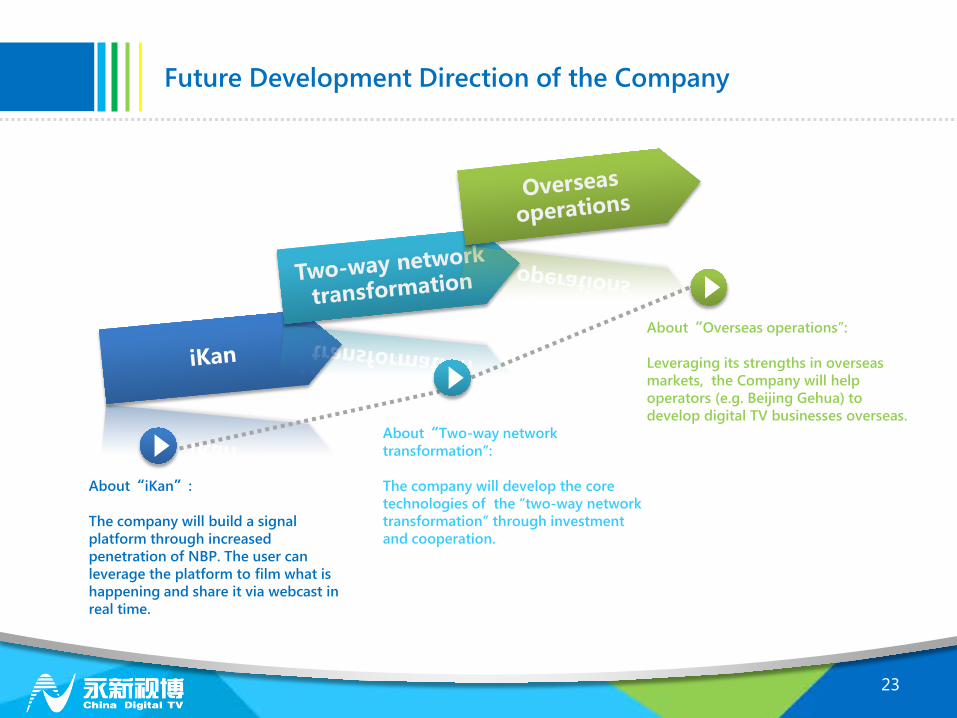

Future Development Direction of the Company

About“iKan”: The company will build a signal platform through increased penetration of NBP. The user can leverage the platform to film what is happening and share it via webcast in real time.

About“Two-way network transformation”: The company will develop the core technologies of the “two-way network transformation” through investment and cooperation.

About“Overseas operations”: Leveraging its strengths in overseas markets, the Company will help operators (e.g. Beijing Gehua) to develop digital TV businesses overseas.

Thank you!

Related Documents