Childrens Savings Accounts RE:Conference, Salem OR October 30, 2014 Bruce Abernethy Janet Byrd

Children's Savings Accounts - Neighborhood Partnerships' RE:Conference 2014

Jul 13, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Childrens Savings Accounts

RE:Conference, Salem OROctober 30, 2014Bruce Abernethy

Janet Byrd

Children’s Savings Accounts?

Account typesInitial contributionsIncentives/matchParental/student contributions

Program elements

Pilot: Central Oregon

“Future Accounts”:a College and Training Savings Account

concept for Central Oregon

RE: ConferenceOctober 30, 2014

Vision: "Every child in Central Oregon has started a college/training savings account by the time they leave 3rd grade and has a variety of ways to grow this account over time."

Four Workgroups:1) Early Learning and Wellness2) Supporting Families3) Bridges (critical transition periods)4) Education/Training to Career

Better Together was originally formed to:

“Create a culture of higher education”

Eligible uses of Future Account funds include:

help pay for college credit courses while still in high school

help pay for apprenticeship or work experience while still in high school

help a student attend a 2 or 4-year college (i.e. pay for tuition, books, fees)

help a student pay for vocational/technical school (i.e. pay for tuition, tools, equipment)

Guiding Principles:

Designed to support "40-40-20"

Keep it simple, but not simplistic

Incentives and program activities are always properly aligned

This is a tool, not the solution

Should be available/offered to every student (not means-tested)

Promote ownership by the child/student

This is a long-term initiative

Key Program Design Elements:

An actual savings account that is opened by the student/parent (financial entity/"surrogate bank")

A separate matching account that is tied to this particular savings account (firewall in place)

Incentives for student to make regular deposits of $50-$200 annually and participate in targeted activities to earn $50 bonus match/year

Start with cohort in 3rd grade (~2,400 students) and support going forward

Partners provide resources and information on applying to college, financial aid, scholarships, etc.)

Budget Assumptions:

An investment period of roughly 10 years (3rd -12th grade)

The student contributes the maximum matched amount each year ($50, $100, $200)

The student earns the maximum bonus amount each year ($50)

Upon graduation, each student would have at least $2,650 in their Future Account (comprised of $1,050 in student contributions and $1,600 of community match)

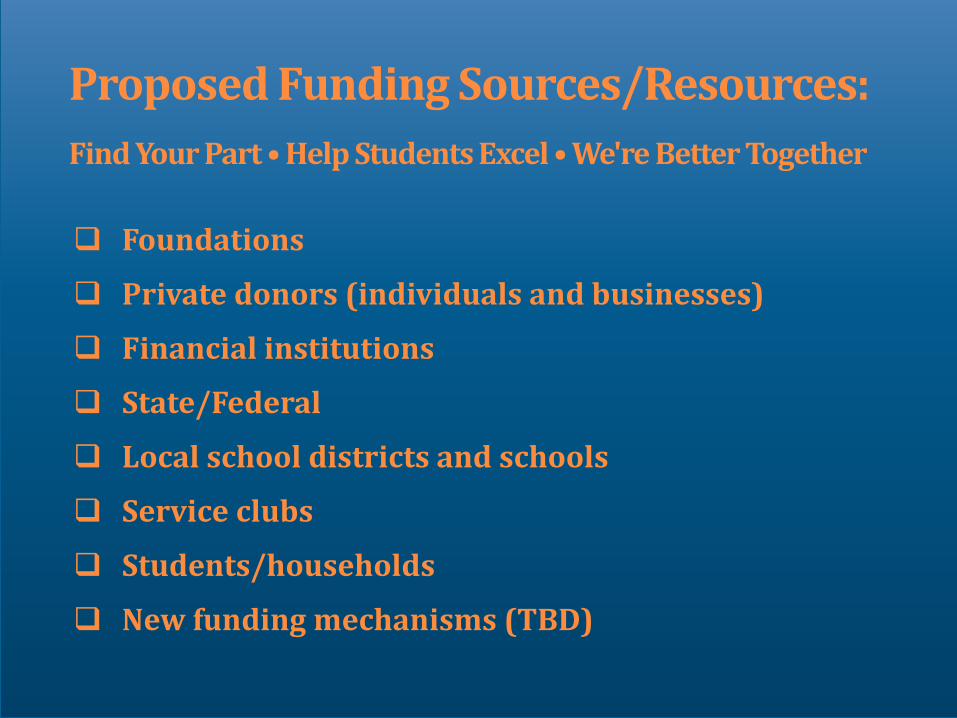

Proposed Funding Sources/Resources:

Find Your Part • Help Students Excel • We're Better Together

Foundations

Private donors (individuals and businesses)

Financial institutions

State/Federal

Local school districts and schools

Service clubs

Students/households

New funding mechanisms (TBD)

Key Operational Partners/Timeline:

Mid Oregon Credit Union - financial entity

High Desert Education Service District - match administrator/disbursement

OSU-Cascades - evaluation

Looking to start pilot program with 8 ES next Spring

Rollout to all of Central Oregon for 2016-17 SY

Questions/Contact info:

Bruce Abernethy

Grantwriter, Bend-La Pine School District

541-355-1024

Anna Higgins

Coordinator of Student Success, Better Together

541-693-5773

State Children’s Savings Policy Overview

• 2004-2009: SEED Initiative drove CSA advocacy

• Incremental wins, but no break-throughs

State Policy Win

AR Authorized & funded pilot project with commitment to expand

TX Authorized (but didn’t fund) matched prepaid tuition program

KY, OK, HI, IL Enacted Study Commissions

OK, TX, CA, ND, HI “Planted a flag” by introducing legislation

• Challenges

Advocates needed to explain, show effectiveness AND build

political support

Coincided with recession: no interest in programs that cost money

1

12

36

0 5 10 15 20 25 30 35 40

State Adoption of Children’s Saving Policy

Universally Available Incentive

Targeted Incentive for LMI Families

Incentive to Noncustodial Parents

Current Policy Landscape

On policy agendas in more than 20 states

Universal

Match3 states

Current Policy Landscape

Of the 36 states with universally available incentives for college

savings …

Tax Credit 3 states

Tax Deduction29 states

Next Steps in Oregon and nationally

Related Documents