DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION ® Client-Driven Solutions, Insights, and Access 21 January 2015 Asia Pacific/Japan Equity Research Chemical and Consumer Sector: Diaper value chain survey Connections Series Japan’s showpiece product entailing advanced technology from SAP to finished diapers ■ Toiletries and chemicals industries marked by intensifying global competition: Japanese chemical manufacturers expect petrochemicals supply– demand to loosen due to growth in supply as a result of the emergence of shale gas and low-priced gas in the Middle East. In electronics, although Japanese companies are competitive in advanced materials, competition with Chinese and South Korean manufacturers is intensifying, especially in LCDs. Worldwide competition is also heating up in the toiletries segment. Global majors and Asia's new entrants are stepping up local production of cosmetics and daily necessities with an eye to markets in Southeast Asia and China, which are experiencing remarkable economic growth. ■ Expect longer-term growth in diapers: In this environment, while Japan's market for baby diapers is maturing, demand for adult diapers is increasing rapidly due to the growing number of elderly people. Populations are also aging in China and Southeast Asia, and we believe that this, coupled with demand for baby diapers in emerging markets, should drive up global demand in the longer term. Japanese manufacturers of diapers and their component materials should benefit from this demand growth. ■ Focal points: Diapers, which are a general consumer good worldwide, feature Japanese technological innovations, and the barrier to entry into premium products is high. They are a rare differentiated product at a time when daily necessities are easy to commoditize. From a chemical sector perspective, super- absorbent polymer (SAP), which is the focus of this report, is one of three areas in which Japan should be able to retain world-class technological prowess and competitiveness and maintain its technological edge (the other two being silicon wafers and carbon fiber). SAP is made to the unique specifications of each diaper maker and involves joint development by SAP and diaper makers. Only Japanese and major overseas manufacturers possess this technical expertise; Chinese and other manufacturers have been unable to penetrate the global diaper market due to their lack of SAP-related technical expertise. Three Japanese companies (Nippon Shokubai, Sanyo Chemical and Sumitomo Seika) together command nearly half the global market (44%). ■ Stocks to watch: Kao (4452, OUTPERFORM, TP ¥5,500): Kao's diapers are growing more popular as awareness of their high quality spreads, especially among affluent consumers in mainland China. The company is also gaining domestic market share. We intend to focus on the company's sales expansion strategy for as-yet undeveloped Southeast Asian markets. ■ Sanyo Chemical Industries (4471, OUTPERFORM, TP ¥950): An SAP pioneer, Sanyo Chemical has considerable technological prowess. The company should gain the most in earnings from the weaker yen and lower naphtha prices among the stocks in our chemicals and synthetic fiber sector coverage. The Credit Suisse Connections Series leverages our exceptional breadth of macro and micro research to deliver incisive cross-sector and cross-border thematic insights for our clients. Research Analysts Masami Sawato 81 3 4550 9729 [email protected] Masashi Mori 81 3 4550 9695 [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST CERTIFICATIONS, AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit Suisse does and seeks to do

business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

21 January 2015

Asia Pacific/Japan

Equity Research

Chemical and Consumer Sector:

Diaper value chain survey Connections Series

Japan’s showpiece product entailing advanced technology from SAP to finished diapers

■ Toiletries and chemicals industries marked by intensifying global competition: Japanese chemical manufacturers expect petrochemicals supply–

demand to loosen due to growth in supply as a result of the emergence of shale gas and low-priced gas in the Middle East. In electronics, although Japanese

companies are competitive in advanced materials, competition with Chinese and South Korean manufacturers is intensifying, especially in LCDs. Worldwide

competition is also heating up in the toiletries segment. Global majors and Asia's new entrants are stepping up local production of cosmetics and daily necessities

with an eye to markets in Southeast Asia and China, which are experiencing remarkable economic growth.

■ Expect longer-term growth in diapers: In this environment, while Japan's

market for baby diapers is maturing, demand for adult diapers is increasing

rapidly due to the growing number of elderly people. Populations are also aging in China and Southeast Asia, and we believe that this, coupled with demand for

baby diapers in emerging markets, should drive up global demand in the longer term. Japanese manufacturers of diapers and their component materials should

benefit from this demand growth.

■ Focal points: Diapers, which are a general consumer good worldwide, feature

Japanese technological innovations, and the barrier to entry into premium products is high. They are a rare differentiated product at a time when daily

necessities are easy to commoditize. From a chemical sector perspective, super-absorbent polymer (SAP), which is the focus of this report, is one of three areas

in which Japan should be able to retain world-class technological prowess and competitiveness and maintain its technological edge (the other two being silicon

wafers and carbon fiber). SAP is made to the unique specifications of each diaper maker and involves joint development by SAP and diaper makers. Only

Japanese and major overseas manufacturers possess this technical expertise; Chinese and other manufacturers have been unable to penetrate the global

diaper market due to their lack of SAP-related technical expertise. Three Japanese companies (Nippon Shokubai, Sanyo Chemical and Sumitomo Seika)

together command nearly half the global market (44%).

■ Stocks to watch: Kao (4452, OUTPERFORM, TP ¥5,500): Kao's diapers are

growing more popular as awareness of their high quality spreads, especially among affluent consumers in mainland China. The company is also gaining

domestic market share. We intend to focus on the company's sales expansion strategy for as-yet undeveloped Southeast Asian markets.

■ Sanyo Chemical Industries (4471, OUTPERFORM, TP ¥950): An SAP pioneer,

Sanyo Chemical has considerable technological prowess. The company should

gain the most in earnings from the weaker yen and lower naphtha prices among the stocks in our chemicals and synthetic fiber sector coverage.

The Credit Suisse Connections Series

leverages our exceptional breadth of

macro and micro research to deliver

incisive cross-sector and cross-border

thematic insights for our clients.

Research Analysts

Masami Sawato

81 3 4550 9729

Masashi Mori

81 3 4550 9695

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 2

Table of contents Japan's globally competitive diaper industry 3

Reasons for focus on diaper industry 3 Stocks to watch 4

Diaper market overview 5 Asia the largest segment of a ¥6tn market 5 Emerging markets set for higher penetration rate and growth in per capita usage 7 Keywords for the Chinese market: premium diapers, pants-type diapers, and e-

commerce 8 Japanese rivals take on Unicharm’s stronghold in Southeast Asia 13 Growth in baby diaper exports and strong demand for adult diapers in Japan 15

Basic materials 20 Diaper structure and business overview of related chemical makers 20 Japan leads with top class SAP technology and production capacity 23

SAP makers in spotlight 25 Sustained growth in SAP demand 25 Price trends 27 Japanese SAP makers 27

Japanese manufacturers also dominant in nonwoven fabric and other materials 31 Nonwoven fabric 31 Microporous film 33 Hot-melt adhesive 33

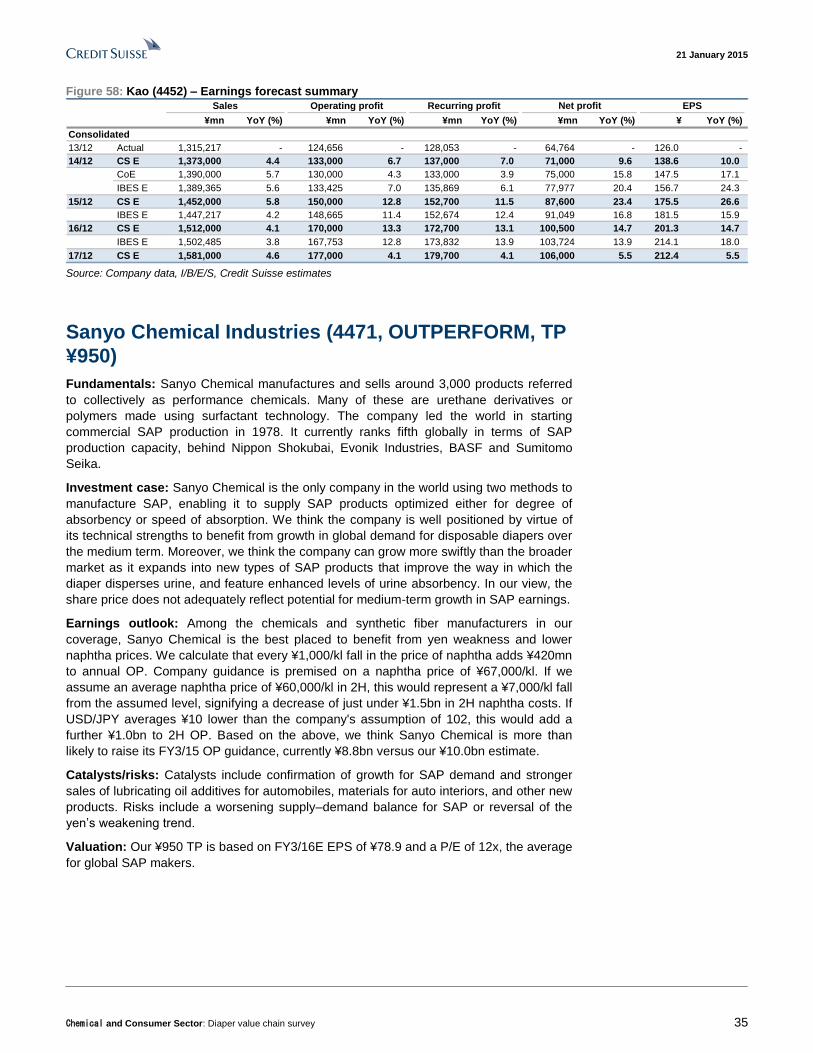

Stocks to watch 34 Kao (4452, OUTPERFORM, TP ¥5,500) 34 Sanyo Chemical Industries (4471, OUTPERFORM, TP ¥950) 35

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 3

Japan's globally competitive diaper industry Reasons for focus on diaper industry

We expect supply–demand of basic chemicals such as ethylene to loosen due to growth in

supply as a result of the emergence of shale gas and low-priced gas in the Middle East. In

electronics, although Japanese companies are competitive in advanced materials,

competition with Chinese and South Korean manufacturers is intensifying, especially in

LCDs.

In contrast, it is easy to draw up projections for diapers—a daily necessity—based on

countries' demographic trends and economic foundations. While Japan's market for baby

diapers is maturing, demand for adult diapers is increasing rapidly due to the growing

number of elderly people. Populations are also aging in China and Southeast Asia, and

this combined with demand for baby diapers in emerging markets should drive up global

demand in the longer term.

Generally speaking, the baby diaper market takes off when per capita GDP breaks

through the $3,000 level, while the disposable adult diaper market does so when per

capita GDP exceeds $10,000. Asian countries' economic strength is growing steadily. Per

capita GDP in 2013 was $10,457 in Malaysia, $6,959 in China, $5,676 in Thailand and

$3,510 in Indonesia, all levels sufficient for diaper use to take off in earnest. The Asian

region (including Japan) is now the largest baby diaper market, accounting for around 30%

of the global total (on a sales volume basis). We see substantial worldwide growth

potential, including in Africa, Latin America and Asia, where we expect populations and

economies to grow.

The leading Japanese diaper makers are Unicharm (8113), Kao, and Daio Paper (3880).

We intend to focus on Kao. The company has been gaining share in China and Japan

since mid-2013, and we believe sales grew strongly in 2014. We think this trend will likely

remain in place from 2015. We intend to focus on the company's sales expansion strategy

for as-yet underdeveloped Southeast Asian markets. With the company having entered

the market late, we expect investor expectations will hinge on how it recovers lost ground.

Among diaper raw materials makers, we intend to focus on Sanyo Chemical. In 1978, it

became the first company in the world to commercially produce super-absorbent polymers

(SAP) used as absorption material in disposable diapers. It currently ranks fifth in the

world in SAP production capacity behind Nippon Shokubai (4114), BASF, Evonik and

Sumitomo Seika (4008). Sanyo Chemical has advanced technology. It is the only

manufacturer in the world employing two SAP production processes. This allows it to offer

two kinds of SAP, one with high absorption capacity and one with fast absorption rate. We

believe the advantage afforded by this favorably positions the company to benefit from

global growth in disposable diaper demand over the medium term. The fact that it is

expanding production capacity for new grades of SAP with superior urine diffusion

capability and increased absorption capacity is also significant, as the launch of these new

products promise to drive growth exceeding that in the market as a whole.

Loosening petrochemical

supply–demand, sustained

competition in electronic

materials

Expectations of longer-term

growth in diapers

Diaper use growing in Asian

countries

Kao is a highly competitive

diaper maker with growth

potential

Focusing on Sanyo

Chemical among raw

materials makers

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 4

Stocks to watch

Kao (4452, OUTPERFORM, TP ¥5,500)

Kao's diapers are growing more popular as awareness of their high quality spreads,

especially among affluent consumers in mainland China. The company is also gradually

gaining share the Russian market. Demand for high-quality, high-price diapers is

increasing in Russia, as it is in China. Kao plans a full-fledged entry into Indonesia at the

start of 2015. The company already has strength in the traditional small retail outlets in

Indonesia known as warung, which are a key distribution channel, via its sanitary products

for women, and we see considerable longer-term growth potential.

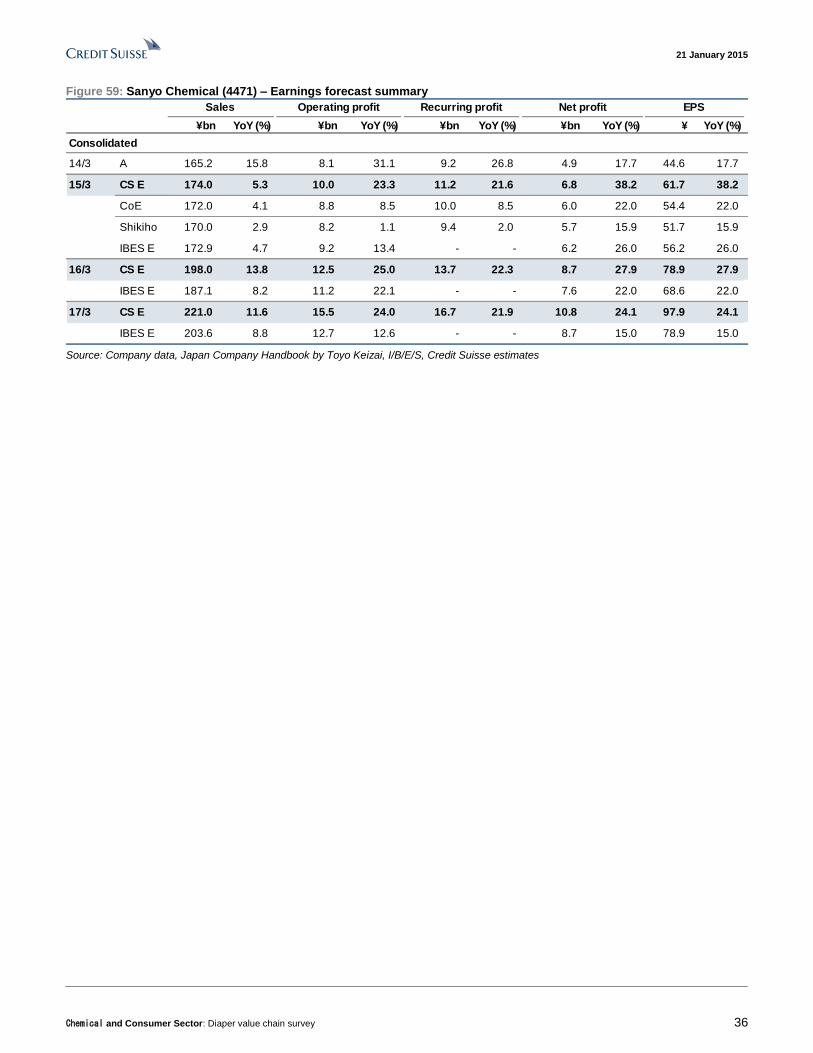

Sanyo Chemical Industries (4471, OUTPERFORM, TP ¥950)

An SAP pioneer, Sanyo Chemical has considerable technological prowess. We think the

company will benefit from increasing demand for diapers over the medium term via the

launch of new-grade products and worldwide development. The share price in our view

does not reflect market growth-beating expansion in earnings. The company should

experience the largest earnings impact from the weaker yen and lower naphtha prices

among the stocks in our chemicals and synthetic fiber sector coverage. We also expect

positive surprises in near-term earnings.

Growth in China, Russia,

focus on Indonesia in 2015

SAP pioneer

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 5

Diaper market overview Asia the largest segment of a ¥6tn market

Expect global demand to grow by a steady 4–5% per year

We estimate global demand was around 160bn diapers in 2013, with baby diapers making

up around 90%, and adult diapers around 10%. As the market is worth around $50bn

(around ¥6tn at roughly ¥120/$), the baby diaper weighting comes to around 85%, the

adult diaper weighting to around 15%. Overall worldwide diaper demand (baby and adult)

rose by a CAGR of 4.4% from 2008 to 2013. Based on global demographic forecasts, we

believe historical levels of growth will continue at least until 2020.

Figure 1: Global diaper market breakdown by type (2013) Figure 2: Global diaper sales volume growth rates (CAGR

over the past five years) by type

Baby85%

Adult15%

4.4%4.1%

7.6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Total Baby Adult

Source: Credit Suisse assumptions (Sales value basis) Source: Company data, Euromonitor, Credit Suisse

Baby diaper market growing most strongly in Asia

The Asian region (including Japan) is now the largest baby diaper market, accounting for

around 30% of the global total (on a sales volume basis). The Chinese and Southeast

Asian markets continue to expand. Whereas the average growth rate over the past five

years worldwide was 4.1%, Asian market growth (excluding Japan) was in double digits.

We expect demand for baby diapers to continue to grow strongly, due in part to rising

birthrates and increasing demand for daily necessities supported by rising per capita GDP,

especially in emerging economies. While we do not expect a surge growth in the diaper

market, we do regard it as stable and steadily growing.

Figure 3: Baby diaper market shares by region (2013) Figure 4: Baby diaper sales volume growth rates by

region

Asia Pacific30%

Australasia1%

Eastern Europe7%

Latin America19%

Middle East and Africa

14%

North America15%

Western Europe

14%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Source: Euromonitor, Credit Suisse (sales volume) Source: Euromonitor, Credit Suisse (CAGR for the past five years)

Steadily growing ¥6tn

market

Baby diapers driving growth

in Asia

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 6

Industrialized nations are the main market for adult diapers; Asia, Latin America

look promising further ahead

North America, Japan, and western Europe account for nearly 80% of worldwide adult

diaper sales (on a volume basis). We think demand in these industrialized nations will

likely continue to increase for now. Long term, we look for the Asian (excluding Japan) and

Latin American markets to expand.

Product development expertise with respect to adult diapers has accumulated early in the

Japanese market, which has experienced a decline in the number of children and an aging

population sooner than many other countries. We believe Japanese companies will

consequently have a strong competitive edge in Asian adult diaper markets. Asian

markets' entry into a phase of full-fledged demand expansion could well drive new growth

for Japanese companies.

Figure 5: Adult diaper market shares by region (2013) Figure 6: Adult diaper sales volume growth rates by

region

Japan25%

Non Japan Asia7%

Australasia2%

Eastern Europe3%

Latin America9%

Middle East and Africa

1%

North America30%

Western Europe

23%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

Source: Euromonitor, Credit Suisse (sales volume) Source: Euromonitor, Credit Suisse (CAGR for the past 5 years)

Demographic trend forecasts imply longer-term diaper demand growth of at least

4% per year

Based on global population, birthrate and other forecasts and certain assumptions

including with regard to frequency of use, we estimate that sales of baby diapers will grow

by 4.4% per year over ten years from 2010 to 2020. We assume that demand for adult

diapers will similarly increase as the number of people aged 65 and over worldwide is

expected to increase by around 3% per year. We conclude that diaper demand as a whole

will grow by 4.3% per year.

Figure 7: Diaper demand forecasts based on demographic trend estimates (growth outlook of 4.3% per year in 2010–20)

Total population (2010) 2010-2020 annual avg 2020 total pop Birthrate (2010-2015 est)

(1,000s) growth est (%) est (1,000s) (per 1,000) 2010 2020

Developed countries 1,240,935 0.3 1,274,929 11.2 13,898 14,279 1,848

Developing countries 5,675,249 1.3 6,441,820 21.3 120,883 137,211 65,270

Global 6,916,184 1.2 7,716,749 19.5 134,781 151,490 67,118

■ Assumptions

・Developed countries: Ave. diaper use 3.5yrs from birth, ave. diaper replacement 4 per day

・Nearly 95% of total infants in developed countries wearing disposable diapers, same level in 2020

・Diaper usage rate in developing countries rising from around 10% in 2010 to nearly 20% in 2020

Total population (2010) 2020 total population Est of average growth in

(1,000s) est (1,000s) 2010 2020 (est) 2010 2020 (est) poulation over 65 (%)

Developed countries 1,240,935 1,274,929 15.9 19.0 197,309 242,237 2.1

Developing countries 5,675,249 6,441,820 5.8 7.5 329,164 483,137 3.9

Global 6,916,184 7,716,749 7.6 9.4 526,473 725,373 3.3

■ Conclusions

・We estimate diaper demand at around 140bn pieces in 2010, c90% for infant-use diapers, c10% for adult-use diapers

・We thus calculate that infant-use diaper demand will rise 4.4% over the next five years

・We estimate that the over 65 population will grow by around 3% annually, with demand for adult-use diapers rising at the same rate (3% annually)

・Based on these assumptions, we forecast that diaper demand will rise 4.3% annually in 2010-2020

Assumptions for infant-use diapers

Births per year (1,000s) Est of aggregated growth in consumption for infants'

diapers 2010-2020 (tons)

Assumptions for adult diapers

Population over 65 (%) Population over 65 (1,000s)

Note 1: Population growth rates, birthrates, and ratios of people aged 65 and over reference United Nations estimates.

Note 2: Population forecasts, etc., are Credit Suisse estimates based on IMF population data.

Source: IMF, UN, Statistics Bureau, Credit Suisse estimates

Industrialized nations

account for 80% of adult

diaper sales

Expecting annual growth of

4.3% through 2020

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 7

Emerging markets set for higher penetration rate and

growth in per capita usage

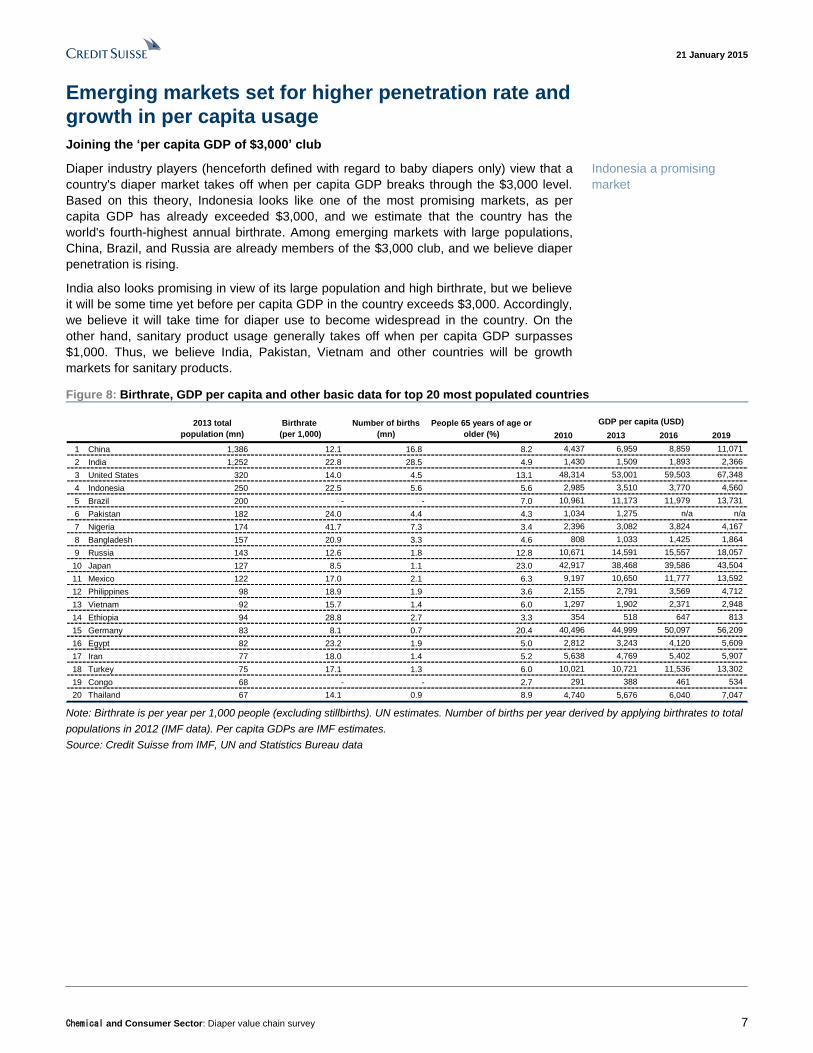

Joining the ‘per capita GDP of $3,000’ club

Diaper industry players (henceforth defined with regard to baby diapers only) view that a

country's diaper market takes off when per capita GDP breaks through the $3,000 level.

Based on this theory, Indonesia looks like one of the most promising markets, as per

capita GDP has already exceeded $3,000, and we estimate that the country has the

world's fourth-highest annual birthrate. Among emerging markets with large populations,

China, Brazil, and Russia are already members of the $3,000 club, and we believe diaper

penetration is rising.

India also looks promising in view of its large population and high birthrate, but we believe

it will be some time yet before per capita GDP in the country exceeds $3,000. Accordingly,

we believe it will take time for diaper use to become widespread in the country. On the

other hand, sanitary product usage generally takes off when per capita GDP surpasses

$1,000. Thus, we believe India, Pakistan, Vietnam and other countries will be growth

markets for sanitary products.

Figure 8: Birthrate, GDP per capita and other basic data for top 20 most populated countries

2010 2013 2016 2019

1 China 1,386 12.1 16.8 8.2 4,437 6,959 8,859 11,071

2 India 1,252 22.8 28.5 4.9 1,430 1,509 1,893 2,366

3 United States 320 14.0 4.5 13.1 48,314 53,001 59,503 67,348

4 Indonesia 250 22.5 5.6 5.6 2,985 3,510 3,770 4,560

5 Brazil 200 - - 7.0 10,961 11,173 11,979 13,731

6 Pakistan 182 24.0 4.4 4.3 1,034 1,275 n/a n/a

7 Nigeria 174 41.7 7.3 3.4 2,396 3,082 3,824 4,167

8 Bangladesh 157 20.9 3.3 4.6 808 1,033 1,425 1,864

9 Russia 143 12.6 1.8 12.8 10,671 14,591 15,557 18,057

10 Japan 127 8.5 1.1 23.0 42,917 38,468 39,586 43,504

11 Mexico 122 17.0 2.1 6.3 9,197 10,650 11,777 13,592

12 Philippines 98 18.9 1.9 3.6 2,155 2,791 3,569 4,712

13 Vietnam 92 15.7 1.4 6.0 1,297 1,902 2,371 2,948

14 Ethiopia 94 28.8 2.7 3.3 354 518 647 813

15 Germany 83 8.1 0.7 20.4 40,496 44,999 50,097 56,209

16 Egypt 82 23.2 1.9 5.0 2,812 3,243 4,120 5,609

17 Iran 77 18.0 1.4 5.2 5,638 4,769 5,402 5,907

18 Turkey 75 17.1 1.3 6.0 10,021 10,721 11,536 13,302

19 Congo 68 - - 2.7 291 388 461 534

20 Thailand 67 14.1 0.9 8.9 4,740 5,676 6,040 7,047

Number of births

(mn)

People 65 years of age or

older (%)

Birthrate

(per 1,000)

2013 total

population (mn)

GDP per capita (USD)

Note: Birthrate is per year per 1,000 people (excluding stillbirths). UN estimates. Number of births per year derived by applying birthrates to total

populations in 2012 (IMF data). Per capita GDPs are IMF estimates.

Source: Credit Suisse from IMF, UN and Statistics Bureau data

Indonesia a promising

market

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 8

Figure 9: Baby diaper and sanitary napkin usage volume

per month

Figure 10: Daily consumption volume and penetration

rates in emerging and industrialized economies

Baby diaper Sanitary napkin

Japan 140 21

China 26 9

Indonesia 25 6

Thailand 48 8

Brazil 160 6

India 10 7

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Indonesia Thailand China Russia Brazil Japan

Daily consumption volume (piece/day, lhs)

Penetration rate (rhs)

Source: Company data, Credit Suisse Note: 100% penetration rate = four diapers per infant per day

Source: Credit Suisse estimates based on Euromonitor data (2013)

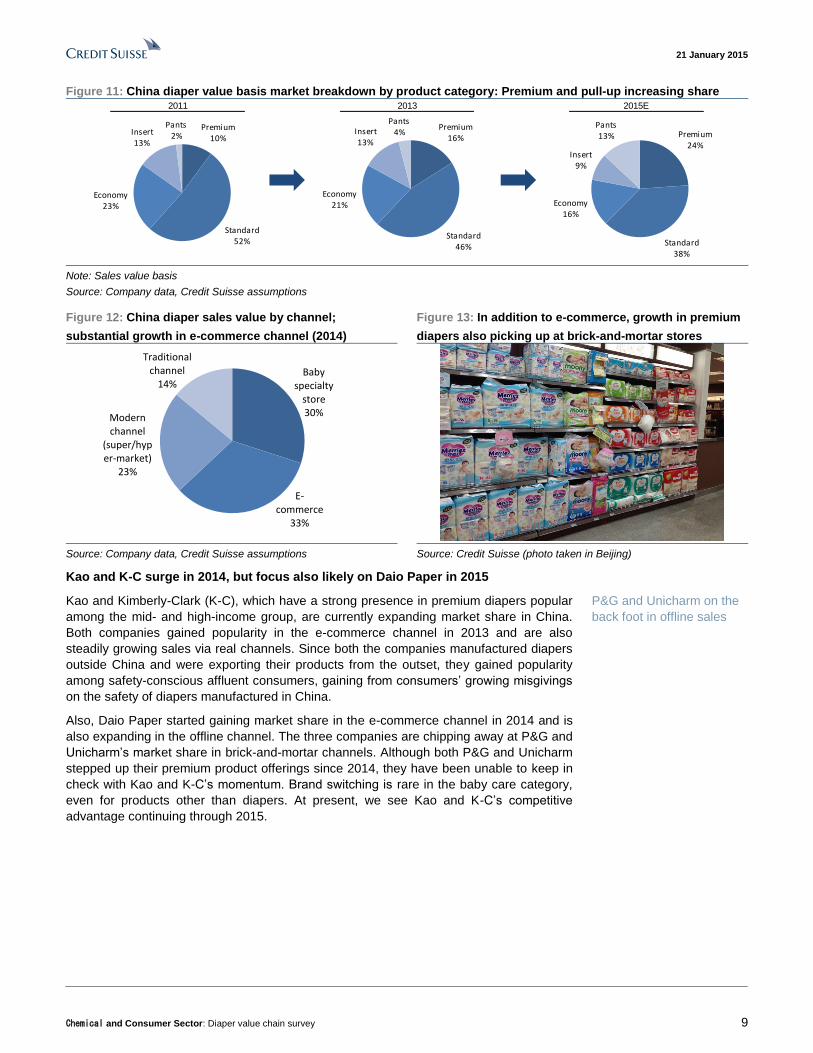

Keywords for the Chinese market: premium diapers,

pull-up diapers, and e-commerce

E-commerce emerging as the most important sales channel; shift to premium

products gains momentum

The year 2014 heralded major changes for the Chinese diaper market, the most significant

of these in our view being rapid growth in the e-commerce channel. Representing more

than 30% of the overall market, e-commerce outpaced specialty baby care stores to

emerge as the largest sales channel. According to Unicharm’s estimates, the weighting of

the e-commerce channel in overall sales is likely to reach 40% by 2017. The main factors

for growth in the Chinese e-commerce channel include greater convenience and lower

prices. We therefore assume the e-commerce channel is likely to remain dominant in the

Chinese diaper market in the near-term.

We note a sustained trend, particularly among affluent consumers, of valuing quality over

price in the coastal areas of China, and we see imported overseas brands remaining

popular. The shift from standard and economy-types to premium diapers is gaining

momentum, and we see no factors that could hinder this trend for 2015 or beyond. It

appears only a question of time before premium diapers outpace standard-type diapers

and emerge as the product category with highest sales weighting in the market by value.

Also, awareness of pull-up (locally known as "pants-type") diapers is steadily rising in

China, where tape-type diapers (disposable diapers with resealable tapes and elasticated

leg cuffs) are the most commonly used.

Based on the trend in 2014, we believe only those companies that have strong premium

products and a pull-up diapers category as well as those adept in e-commerce sales

strategy are likely to emerge as winners going forward.

E-commerce channel grew

rapidly in 2014

Growth in premium diapers

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 9

Figure 11: China diaper value basis market breakdown by product category: Premium and pull-up increasing share 2011 2013 2015E

Premium16%

Standard46%

Economy21%

Insert13%

Pants4%

Premium10%

Standard52%

Economy23%

Insert13%

Pants2% Premium

24%

Standard38%

Economy16%

Insert9%

Pants13%

Note: Sales value basis

Source: Company data, Credit Suisse assumptions

Figure 12: China diaper sales value by channel;

substantial growth in e-commerce channel (2014)

Figure 13: In addition to e-commerce, growth in premium

diapers also picking up at brick-and-mortar stores

Baby

specialty store30%

E-commerce

33%

Modern channel

(super/hyper-market)

23%

Traditional channel

14%

Source: Company data, Credit Suisse assumptions Source: Credit Suisse (photo taken in Beijing)

Kao and K-C surge in 2014, but focus also likely on Daio Paper in 2015

Kao and Kimberly-Clark (K-C), which have a strong presence in premium diapers popular

among the mid- and high-income group, are currently expanding market share in China.

Both companies gained popularity in the e-commerce channel in 2013 and are also

steadily growing sales via real channels. Since both the companies manufactured diapers

outside China and were exporting their products from the outset, they gained popularity

among safety-conscious affluent consumers, gaining from consumers’ growing misgivings

on the safety of diapers manufactured in China.

Also, Daio Paper started gaining market share in the e-commerce channel in 2014 and is

also expanding in the offline channel. The three companies are chipping away at P&G and

Unicharm’s market share in brick-and-mortar channels. Although both P&G and Unicharm

stepped up their premium product offerings since 2014, they have been unable to keep in

check with Kao and K-C’s momentum. Brand switching is rare in the baby care category,

even for products other than diapers. At present, we see Kao and K-C’s competitive

advantage continuing through 2015.

P&G and Unicharm on the

back foot in offline sales

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 10

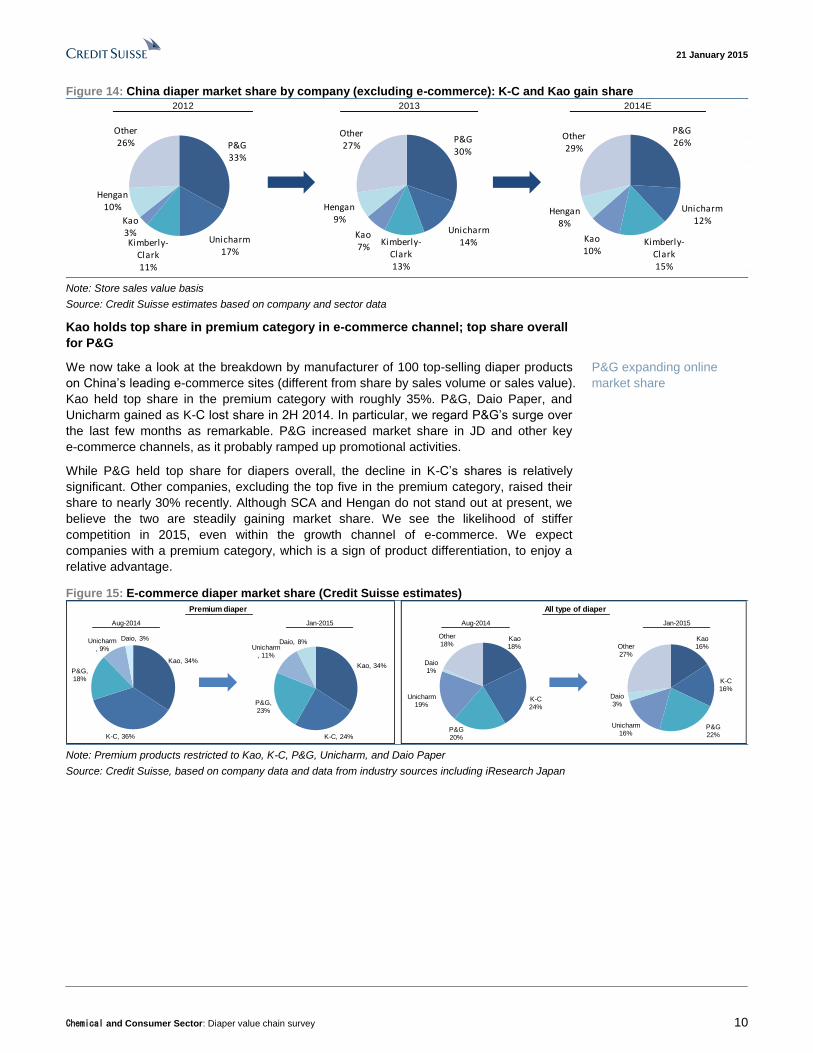

Figure 14: China diaper market share by company (excluding e-commerce): K-C and Kao gain share

2014E2012 2013

P&G33%

Unicharm17%

Kimberly-Clark11%

Kao3%

Hengan10%

Other26% P&G

30%

Unicharm14%Kimberly-

Clark13%

Kao7%

Hengan9%

Other27%

P&G26%

Unicharm12%

Kimberly-Clark15%

Kao10%

Hengan8%

Other29%

Note: Store sales value basis

Source: Credit Suisse estimates based on company and sector data

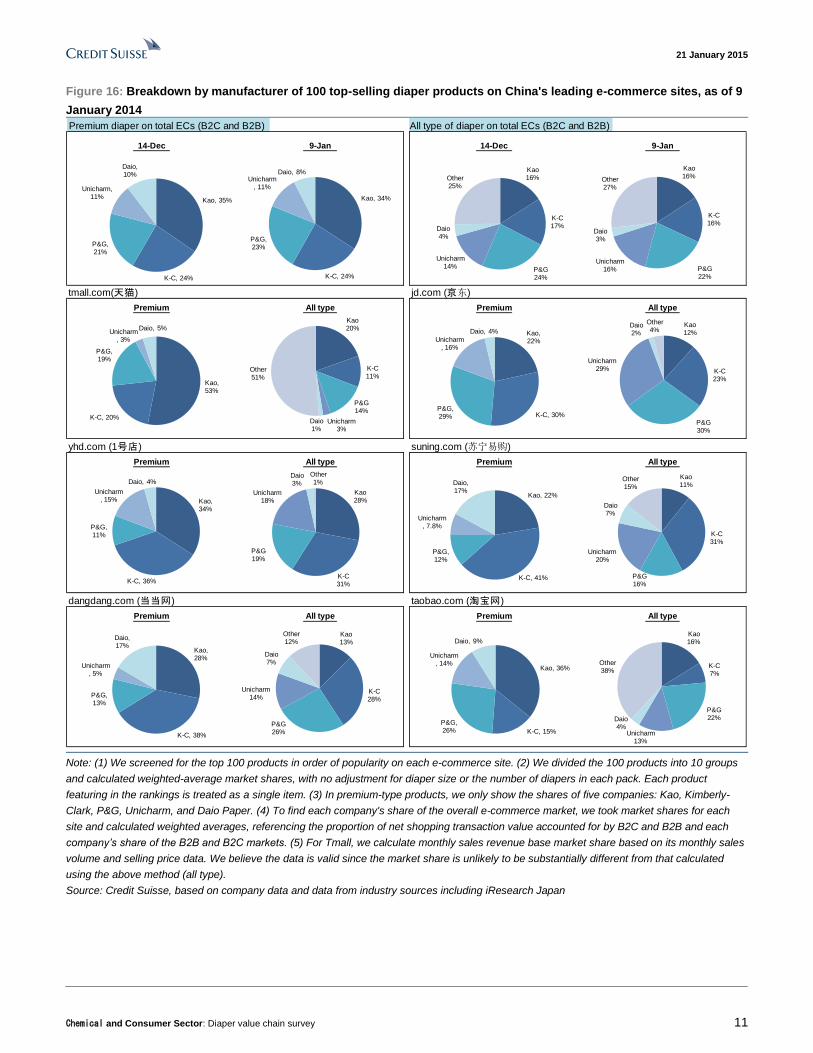

Kao holds top share in premium category in e-commerce channel; top share overall

for P&G

We now take a look at the breakdown by manufacturer of 100 top-selling diaper products

on China’s leading e-commerce sites (different from share by sales volume or sales value).

Kao held top share in the premium category with roughly 35%. P&G, Daio Paper, and

Unicharm gained as K-C lost share in 2H 2014. In particular, we regard P&G’s surge over

the last few months as remarkable. P&G increased market share in JD and other key

e-commerce channels, as it probably ramped up promotional activities.

While P&G held top share for diapers overall, the decline in K-C’s shares is relatively

significant. Other companies, excluding the top five in the premium category, raised their

share to nearly 30% recently. Although SCA and Hengan do not stand out at present, we

believe the two are steadily gaining market share. We see the likelihood of stiffer

competition in 2015, even within the growth channel of e-commerce. We expect

companies with a premium category, which is a sign of product differentiation, to enjoy a

relative advantage.

Figure 15: E-commerce diaper market share (Credit Suisse estimates)

Aug-2014 Jan-2015

Premium diaper All type of diaper

Aug-2014 Jan-2015

Kao16%

K-C16%

P&G22%

Unicharm16%

Daio3%

Other27%

Kao, 34%

K-C, 36%

P&G, 18%

Unicharm, 9%

Daio, 3% Kao18%

K-C24%

P&G20%

Unicharm19%

Daio1%

Other18%

Kao, 34%

K-C, 24%

P&G, 23%

Unicharm, 11%

Daio, 8%

Note: Premium products restricted to Kao, K-C, P&G, Unicharm, and Daio Paper

Source: Credit Suisse, based on company data and data from industry sources including iResearch Japan

P&G expanding online

market share

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 11

Figure 16: Breakdown by manufacturer of 100 top-selling diaper products on China's leading e-commerce sites, as of 9

January 2014

14-Dec 9-Jan 14-Dec 9-Jan

Premium All type Premium All type

Premium All type Premium All type

Premium All type Premium All type

dangdang.com (当当网) taobao.com (淘宝网)

Premium diaper on total ECs (B2C and B2B) All type of diaper on total ECs (B2C and B2B)

tmall.com(天猫) jd.com (京东)

yhd.com (1号店) suning.com (苏宁易购)

Kao, 53%

K-C, 20%

P&G, 19%

Unicharm, 3%

Daio, 5%Kao20%

K-C11%

P&G14%

Unicharm3%

Daio1%

Other51%

Kao, 34%

K-C, 36%

P&G, 11%

Unicharm, 15%

Daio, 4%

Kao28%

K-C31%

P&G19%

Unicharm18%

Daio3%

Other1%

Kao, 28%

K-C, 38%

P&G, 13%

Unicharm, 5%

Daio, 17%

Kao13%

K-C28%

P&G26%

Unicharm14%

Daio7%

Other12%

Kao, 36%

K-C, 15%

P&G, 26%

Unicharm, 14%

Daio, 9%Kao16%

K-C7%

P&G22%

Unicharm13%

Daio4%

Other38%

Kao, 22%

K-C, 30%P&G, 29%

Unicharm, 16%

Daio, 4%Kao12%

K-C23%

P&G30%

Unicharm29%

Daio2%

Other4%

Kao, 22%

K-C, 41%

P&G, 12%

Unicharm, 7.8%

Daio, 17%

Kao11%

K-C31%

P&G16%

Unicharm20%

Daio7%

Other15%

Kao, 34%

K-C, 24%

P&G, 23%

Unicharm, 11%

Daio, 8%Kao16%

K-C16%

P&G22%

Unicharm16%

Daio3%

Other27%

Kao, 35%

K-C, 24%

P&G, 21%

Unicharm, 11%

Daio, 10%

Kao16%

K-C17%

P&G24%

Unicharm14%

Daio4%

Other25%

Note: (1) We screened for the top 100 products in order of popularity on each e-commerce site. (2) We divided the 100 products into 10 groups

and calculated weighted-average market shares, with no adjustment for diaper size or the number of diapers in each pack. Each product

featuring in the rankings is treated as a single item. (3) In premium-type products, we only show the shares of five companies: Kao, Kimberly-

Clark, P&G, Unicharm, and Daio Paper. (4) To find each company's share of the overall e-commerce market, we took market shares for each

site and calculated weighted averages, referencing the proportion of net shopping transaction value accounted for by B2C and B2B and each

company’s share of the B2B and B2C markets. (5) For Tmall, we calculate monthly sales revenue base market share based on its monthly sales

volume and selling price data. We believe the data is valid since the market share is unlikely to be substantially different from that calculated

using the above method (all type).

Source: Credit Suisse, based on company data and data from industry sources including iResearch Japan

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 12

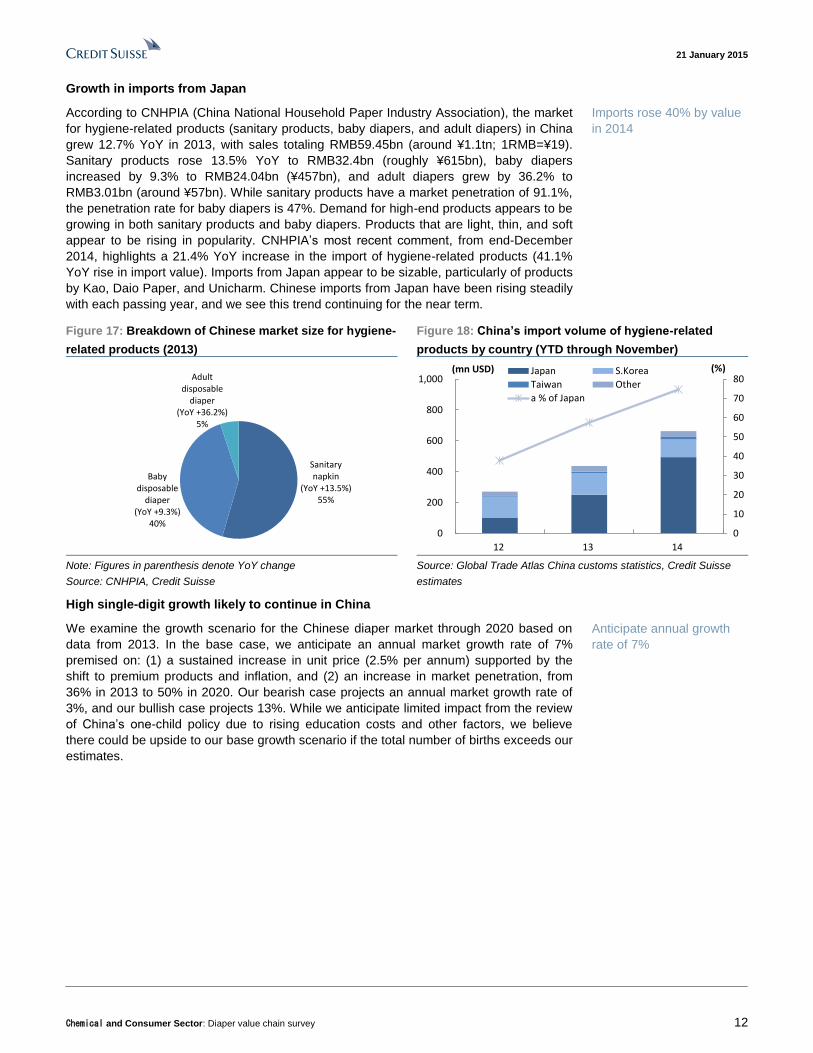

Growth in imports from Japan

According to CNHPIA (China National Household Paper Industry Association), the market

for hygiene-related products (sanitary products, baby diapers, and adult diapers) in China

grew 12.7% YoY in 2013, with sales totaling RMB59.45bn (around ¥1.1tn; 1RMB=¥19).

Sanitary products rose 13.5% YoY to RMB32.4bn (roughly ¥615bn), baby diapers

increased by 9.3% to RMB24.04bn (¥457bn), and adult diapers grew by 36.2% to

RMB3.01bn (around ¥57bn). While sanitary products have a market penetration of 91.1%,

the penetration rate for baby diapers is 47%. Demand for high-end products appears to be

growing in both sanitary products and baby diapers. Products that are light, thin, and soft

appear to be rising in popularity. CNHPIA’s most recent comment, from end-December

2014, highlights a 21.4% YoY increase in the import of hygiene-related products (41.1%

YoY rise in import value). Imports from Japan appear to be sizable, particularly of products

by Kao, Daio Paper, and Unicharm. Chinese imports from Japan have been rising steadily

with each passing year, and we see this trend continuing for the near term.

Figure 17: Breakdown of Chinese market size for hygiene-

related products (2013)

Figure 18: China’s import volume of hygiene-related

products by country (YTD through November)

Sanitary napkin

(YoY +13.5%)55%

Baby disposable

diaper(YoY +9.3%)

40%

Adult disposable

diaper(YoY +36.2%)

5%

0

10

20

30

40

50

60

70

80

0

200

400

600

800

1,000

12 13 14

(%)(mn USD) Japan S.Korea

Taiwan Other

a % of Japan

Note: Figures in parenthesis denote YoY change

Source: CNHPIA, Credit Suisse

Source: Global Trade Atlas China customs statistics, Credit Suisse

estimates

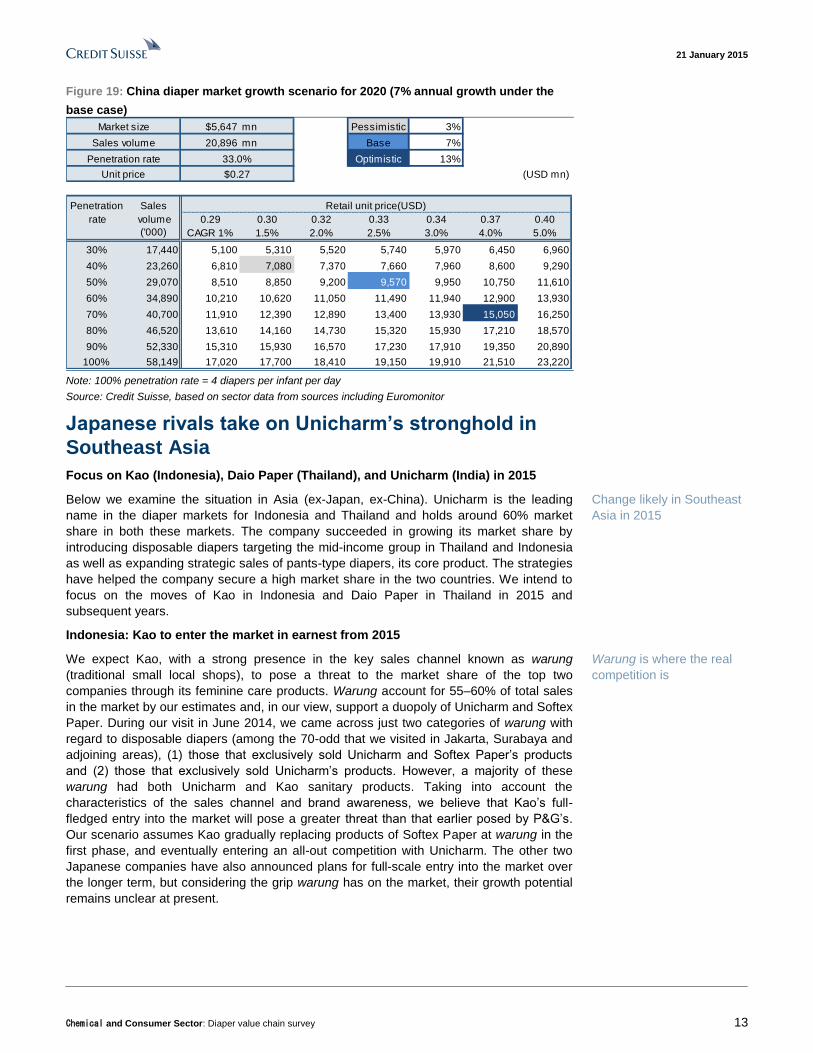

High single-digit growth likely to continue in China

We examine the growth scenario for the Chinese diaper market through 2020 based on

data from 2013. In the base case, we anticipate an annual market growth rate of 7%

premised on: (1) a sustained increase in unit price (2.5% per annum) supported by the

shift to premium products and inflation, and (2) an increase in market penetration, from

36% in 2013 to 50% in 2020. Our bearish case projects an annual market growth rate of

3%, and our bullish case projects 13%. While we anticipate limited impact from the review

of China’s one-child policy due to rising education costs and other factors, we believe

there could be upside to our base growth scenario if the total number of births exceeds our

estimates.

Imports rose 40% by value

in 2014

Anticipate annual growth

rate of 7%

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 13

Figure 19: China diaper market growth scenario for 2020 (7% annual growth under the

base case)

$5,647 mn Pessimistic 3%

20,896 mn Base 7%

Optimistic 13%

(USD mn)

Penetration Sales

rate volume 0.29 0.30 0.32 0.33 0.34 0.37 0.40

('000) CAGR 1% 1.5% 2.0% 2.5% 3.0% 4.0% 5.0%

30% 17,440 5,100 5,310 5,520 5,740 5,970 6,450 6,960

40% 23,260 6,810 7,080 7,370 7,660 7,960 8,600 9,290

50% 29,070 8,510 8,850 9,200 9,570 9,950 10,750 11,610

60% 34,890 10,210 10,620 11,050 11,490 11,940 12,900 13,930

70% 40,700 11,910 12,390 12,890 13,400 13,930 15,050 16,250

80% 46,520 13,610 14,160 14,730 15,320 15,930 17,210 18,570

90% 52,330 15,310 15,930 16,570 17,230 17,910 19,350 20,890

100% 58,149 17,020 17,700 18,410 19,150 19,910 21,510 23,220

Market size

Retail unit price(USD)

Sales volume

Penetration rate 33.0%

Unit price $0.27

Note: 100% penetration rate = 4 diapers per infant per day

Source: Credit Suisse, based on sector data from sources including Euromonitor

Japanese rivals take on Unicharm’s stronghold in

Southeast Asia

Focus on Kao (Indonesia), Daio Paper (Thailand), and Unicharm (India) in 2015

Below we examine the situation in Asia (ex-Japan, ex-China). Unicharm is the leading

name in the diaper markets for Indonesia and Thailand and holds around 60% market

share in both these markets. The company succeeded in growing its market share by

introducing disposable diapers targeting the mid-income group in Thailand and Indonesia

as well as expanding strategic sales of pants-type diapers, its core product. The strategies

have helped the company secure a high market share in the two countries. We intend to

focus on the moves of Kao in Indonesia and Daio Paper in Thailand in 2015 and

subsequent years.

Indonesia: Kao to enter the market in earnest from 2015

We expect Kao, with a strong presence in the key sales channel known as warung

(traditional small local shops), to pose a threat to the market share of the top two

companies through its feminine care products. Warung account for 55–60% of total sales

in the market by our estimates and, in our view, support a duopoly of Unicharm and Softex

Paper. During our visit in June 2014, we came across just two categories of warung with

regard to disposable diapers (among the 70-odd that we visited in Jakarta, Surabaya and

adjoining areas), (1) those that exclusively sold Unicharm and Softex Paper’s products

and (2) those that exclusively sold Unicharm’s products. However, a majority of these

warung had both Unicharm and Kao sanitary products. Taking into account the

characteristics of the sales channel and brand awareness, we believe that Kao’s full-

fledged entry into the market will pose a greater threat than that earlier posed by P&G’s.

Our scenario assumes Kao gradually replacing products of Softex Paper at warung in the

first phase, and eventually entering an all-out competition with Unicharm. The other two

Japanese companies have also announced plans for full-scale entry into the market over

the longer term, but considering the grip warung has on the market, their growth potential

remains unclear at present.

Change likely in Southeast

Asia in 2015

Warung is where the real

competition is

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 14

Figure 20: Market share breakdown of disposable diapers

in Indonesia

Figure 21: Market share breakdown of disposable diapers

in Thailand

Unicharm67%

Softex Paper 17%

P&G8%

Other8%

Unicharm59%

DSG Int'l30%

Daio 5%

SCA 4%

Other2%

Note: Sales value basis, market share for most recent 12 months

Source: Company data, Credit Suisse

Note: Sales value basis, market share for most recent 12 months

Source: Company data, Credit Suisse estimates

Thailand: Daio Paper gradually increasing market share; DSG firm as well

The growth rate in disposable diapers appears to be slowing down in Thailand, affected by

the economic downturn. There has been no major change in the market share of

Unicharm, the market leader. In Thailand, there is no downtrend in the market share of

local makers—unlike what we have seen in other emerging markets—as the share of DSG

International also remains firm. Daio Paper is steadily expanding sales and appears to

have secured a 5% share for the first time in 2014 to come in at third position. Daio Paper

appears to have a relatively strong momentum going for it as it (1) boosted capacity in

September 2014 and (2) kicked off sales in high gear at major convenience stores. We

understand that Daio Paper accounts for 10% market share in certain months. We see the

market gradually shifting to a three-way oligopoly. The weighting of modern channels

appears to be higher in Thailand than in Indonesia. The risks posed by the slowdown in

market growth, stiffer competition particularly for modern channels, and earnings decline

due to higher sales promotion costs are concerns.

Figure 22: Warung (Indonesia’s traditional retail outlet) channel penetration a key factor

Traditional channel (Warung)Modern channel

(convenience store)

Source: Credit Suisse (photos taken in Surabaya, Indonesia)

Three-way monopoly set to

intensify in Thailand

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 15

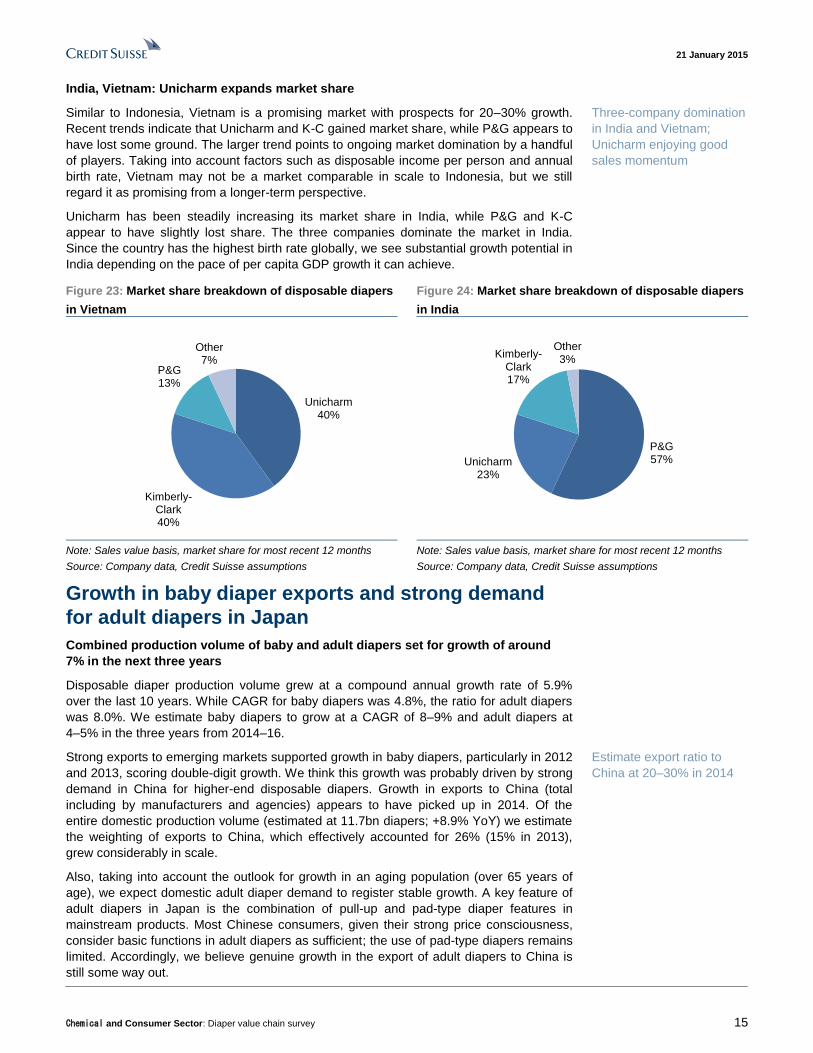

India, Vietnam: Unicharm expands market share

Similar to Indonesia, Vietnam is a promising market with prospects for 20–30% growth.

Recent trends indicate that Unicharm and K-C gained market share, while P&G appears to

have lost some ground. The larger trend points to ongoing market domination by a handful

of players. Taking into account factors such as disposable income per person and annual

birth rate, Vietnam may not be a market comparable in scale to Indonesia, but we still

regard it as promising from a longer-term perspective.

Unicharm has been steadily increasing its market share in India, while P&G and K-C

appear to have slightly lost share. The three companies dominate the market in India.

Since the country has the highest birth rate globally, we see substantial growth potential in

India depending on the pace of per capita GDP growth it can achieve.

Figure 23: Market share breakdown of disposable diapers

in Vietnam

Figure 24: Market share breakdown of disposable diapers

in India

Unicharm40%

Kimberly-Clark 40%

P&G13%

Other7%

P&G57%Unicharm

23%

Kimberly-Clark 17%

Other3%

Note: Sales value basis, market share for most recent 12 months

Source: Company data, Credit Suisse assumptions

Note: Sales value basis, market share for most recent 12 months

Source: Company data, Credit Suisse assumptions

Growth in baby diaper exports and strong demand

for adult diapers in Japan

Combined production volume of baby and adult diapers set for growth of around

7% in the next three years

Disposable diaper production volume grew at a compound annual growth rate of 5.9%

over the last 10 years. While CAGR for baby diapers was 4.8%, the ratio for adult diapers

was 8.0%. We estimate baby diapers to grow at a CAGR of 8–9% and adult diapers at

4–5% in the three years from 2014–16.

Strong exports to emerging markets supported growth in baby diapers, particularly in 2012

and 2013, scoring double-digit growth. We think this growth was probably driven by strong

demand in China for higher-end disposable diapers. Growth in exports to China (total

including by manufacturers and agencies) appears to have picked up in 2014. Of the

entire domestic production volume (estimated at 11.7bn diapers; +8.9% YoY) we estimate

the weighting of exports to China, which effectively accounted for 26% (15% in 2013),

grew considerably in scale.

Also, taking into account the outlook for growth in an aging population (over 65 years of

age), we expect domestic adult diaper demand to register stable growth. A key feature of

adult diapers in Japan is the combination of pull-up and pad-type diaper features in

mainstream products. Most Chinese consumers, given their strong price consciousness,

consider basic functions in adult diapers as sufficient; the use of pad-type diapers remains

limited. Accordingly, we believe genuine growth in the export of adult diapers to China is

still some way out.

Three-company domination

in India and Vietnam;

Unicharm enjoying good

sales momentum

Estimate export ratio to

China at 20–30% in 2014

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 16

Figure 25: Domestic diaper production volume (2003–13

CAGR=+5.9%)

Figure 26: Trends in number of births and aging

population in Japan

0

5

10

15

20

25

03 04 05 06 07 08 09 10 11 12 13 14E 15E 16E

(bn pieces)

Infant-use Adult-use

0

500

1,000

1,500

2,000

2,500

3,000

19

50

19

55

19

60

19

65

19

70

19

75

19

80

19

85

19

90

19

95

20

00

20

05

20

10

20

15

20

20

20

25

20

30

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

('000 ppl) ('000 ppl)Aging population (over 65 year old, RHS)

Number of births (LHS)

Source: JHPIA, Credit Suisse estimates Source: STAT (MIC) estimates, Credit Suisse

Figure 27: Breakdown of diapers manufactured in Japan

by type (volume basis)

Figure 28: Weighting by export region for baby diapers

manufactured in Japan For babies

For adults

diapers with

resealable tapes48%

pants diapers

52% disposable adult diapers

21%

absorbency booster pads

(flat type)3%

incontinence pads and

others76%

0%

10%

20%

30%

40%

50%

60%

70%

12E 13E 14E

Japan China Russia Other

Source: JHPIA, Credit Suisse (2013) Note: Effective domestic demand and effective exports (Other

includes inventory)

Source: Credit Suisse assumptions, based on sector data from

sources including Global Trade Atlas and JHPIA

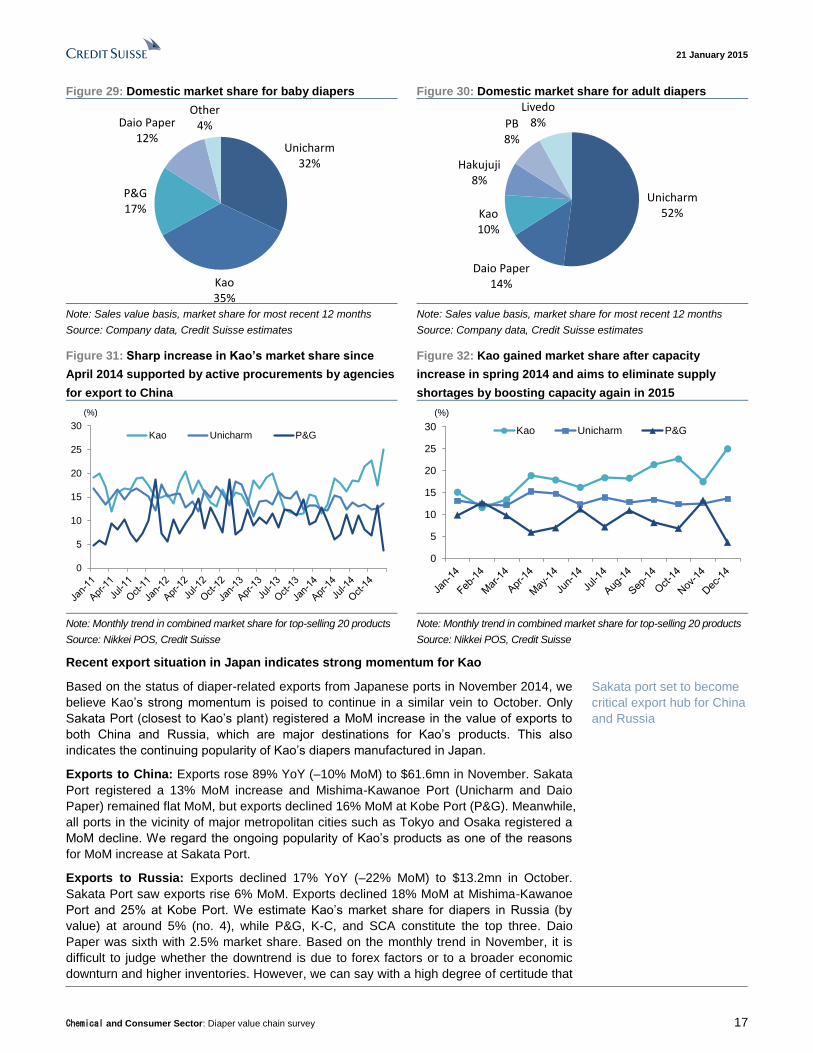

Top share for Kao in baby diapers, Unicharm strong in adult diapers

In the past, Unicharm held top domestic share in baby diapers, but we think a major

change is likely in terms of market share in 2014. We estimate that Kao may have secured

top share in this category. We see a sustained trend of Chinese agencies actively

procuring Kao’s Merries brand diapers at Japanese retail stores, which appears to have

boosted Kao’s domestic market share. Merries brand diapers appear to be constantly out-

of-stock in both urban and rural areas. Our survey shows that the shortage of Merries

brand diapers was a contributing factor in some higher-end products of Daio Paper and

Unicharm going out of stock at some retail stores recently.

We estimate that Unicharm currently holds about 50% domestic market share in adult

diapers. The gap between Unicharm and the company ranked second (with just under

20% market share) is overwhelming. Compared with baby diapers, adult diapers involve

extremely detailed requirement parameters such as size, shape, and absorption capacity

and odor-reduction functions. We believe that Unicharm’s edge in this category stems

from its highly capable marketing (including in both hospital and general retail routes) in

addition to its rich product lineup and product development capability.

Kao reached top share at

end-2014

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 17

Figure 29: Domestic market share for baby diapers Figure 30: Domestic market share for adult diapers

Unicharm32%

Kao35%

P&G17%

Daio Paper12%

Other4%

Unicharm52%

Daio Paper14%

Kao10%

Hakujuji8%

PB8%

Livedo8%

Note: Sales value basis, market share for most recent 12 months

Source: Company data, Credit Suisse estimates

Note: Sales value basis, market share for most recent 12 months

Source: Company data, Credit Suisse estimates

Figure 31: Sharp increase in Kao’s market share since

April 2014 supported by active procurements by agencies

for export to China

Figure 32: Kao gained market share after capacity

increase in spring 2014 and aims to eliminate supply

shortages by boosting capacity again in 2015

0

5

10

15

20

25

30Kao Unicharm P&G

(%)

0

5

10

15

20

25

30 Kao Unicharm P&G

(%)

Note: Monthly trend in combined market share for top-selling 20 products

Source: Nikkei POS, Credit Suisse

Note: Monthly trend in combined market share for top-selling 20 products

Source: Nikkei POS, Credit Suisse

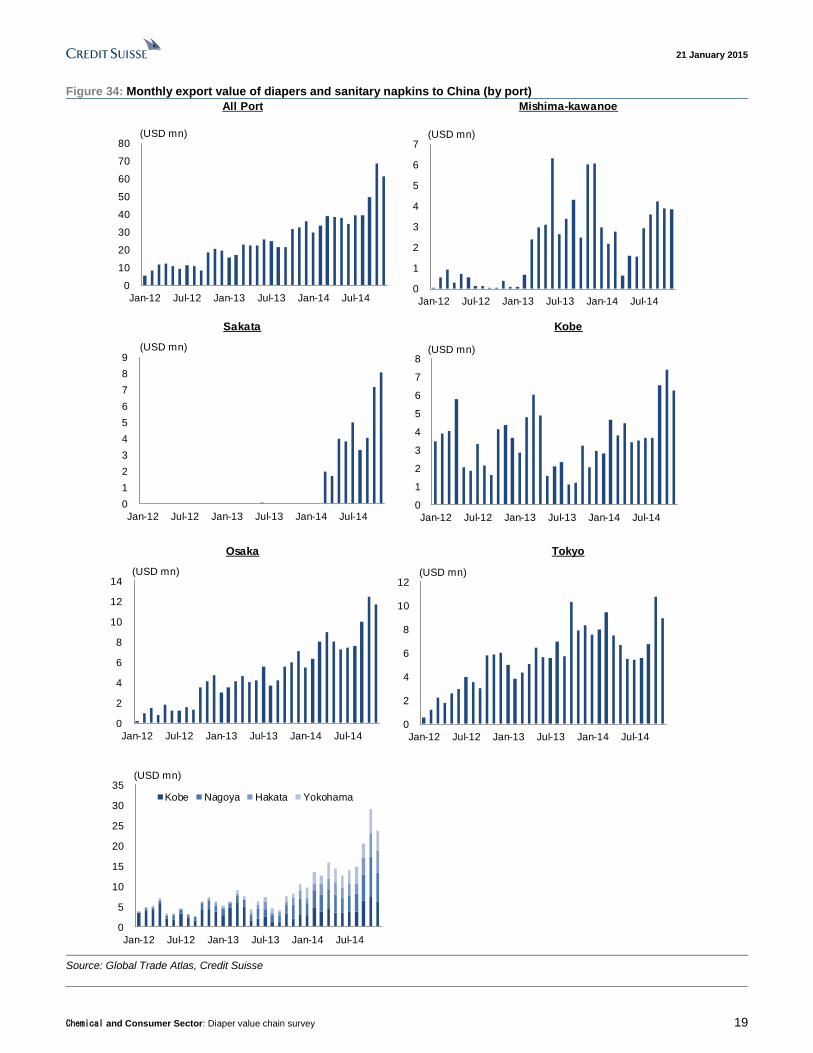

Recent export situation in Japan indicates strong momentum for Kao

Based on the status of diaper-related exports from Japanese ports in November 2014, we

believe Kao’s strong momentum is poised to continue in a similar vein to October. Only

Sakata Port (closest to Kao’s plant) registered a MoM increase in the value of exports to

both China and Russia, which are major destinations for Kao’s products. This also

indicates the continuing popularity of Kao’s diapers manufactured in Japan.

Exports to China: Exports rose 89% YoY (–10% MoM) to $61.6mn in November. Sakata

Port registered a 13% MoM increase and Mishima-Kawanoe Port (Unicharm and Daio

Paper) remained flat MoM, but exports declined 16% MoM at Kobe Port (P&G). Meanwhile,

all ports in the vicinity of major metropolitan cities such as Tokyo and Osaka registered a

MoM decline. We regard the ongoing popularity of Kao’s products as one of the reasons

for MoM increase at Sakata Port.

Exports to Russia: Exports declined 17% YoY (–22% MoM) to $13.2mn in October.

Sakata Port saw exports rise 6% MoM. Exports declined 18% MoM at Mishima-Kawanoe

Port and 25% at Kobe Port. We estimate Kao’s market share for diapers in Russia (by

value) at around 5% (no. 4), while P&G, K-C, and SCA constitute the top three. Daio

Paper was sixth with 2.5% market share. Based on the monthly trend in November, it is

difficult to judge whether the downtrend is due to forex factors or to a broader economic

downturn and higher inventories. However, we can say with a high degree of certitude that

Sakata port set to become

critical export hub for China

and Russia

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 18

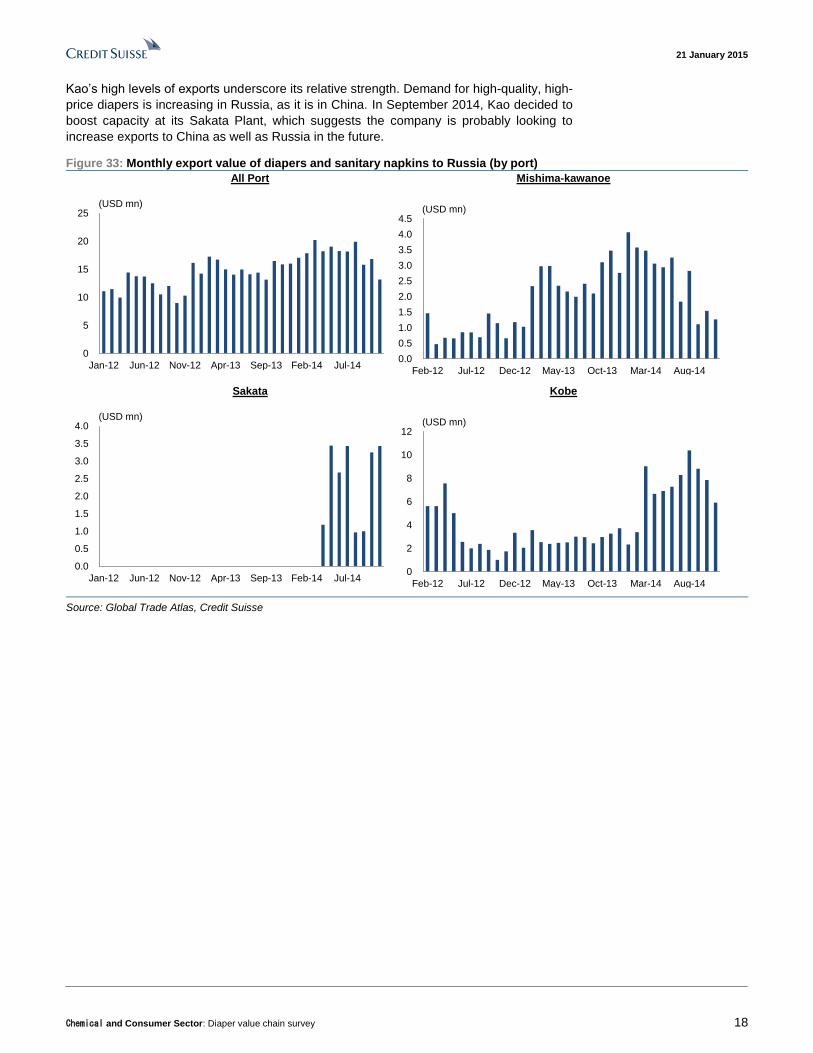

Kao’s high levels of exports underscore its relative strength. Demand for high-quality, high-

price diapers is increasing in Russia, as it is in China. In September 2014, Kao decided to

boost capacity at its Sakata Plant, which suggests the company is probably looking to

increase exports to China as well as Russia in the future.

Figure 33: Monthly export value of diapers and sanitary napkins to Russia (by port)

Mishima-kawanoe

Sakata Kobe

All Port

0

5

10

15

20

25

Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14

(USD mn)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Feb-12 Jul-12 Dec-12 May-13 Oct-13 Mar-14 Aug-14

(USD mn)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14

(USD mn)

0

2

4

6

8

10

12

Feb-12 Jul-12 Dec-12 May-13 Oct-13 Mar-14 Aug-14

(USD mn)

Source: Global Trade Atlas, Credit Suisse

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 19

Figure 34: Monthly export value of diapers and sanitary napkins to China (by port)

Osaka Tokyo

All Port Mishima-kawanoe

Sakata Kobe

0

10

20

30

40

50

60

70

80

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

Th

ou

sa

nd

s

(USD mn)

0

1

2

3

4

5

6

7

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

(USD mn)

0

1

2

3

4

5

6

7

8

9

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

(USD mn)

0

1

2

3

4

5

6

7

8

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

(USD mn)

0

2

4

6

8

10

12

14

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

Th

ou

sa

nd

s

(USD mn)

0

2

4

6

8

10

12

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

Th

ou

sa

nd

s

(USD mn)

0

5

10

15

20

25

30

35

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

Th

ou

sa

nd

s Kobe Nagoya Hakata Yokohama

(USD mn)

Source: Global Trade Atlas, Credit Suisse

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 20

Basic materials Diaper structure and business overview of related

chemical makers

Disposable diapers can be broadly divided into three layers: a surface layer, absorption

layer, and waterproof material layer. The surface layer comes into direct contact with the

skin and catches urine flow. The purpose of this layer is to improve user comfort and is

normally made of nonwoven fabric such as polyester or polypropylene. The use of

nonwoven fabric helps in keeping the diaper surface dry.

Urine passing through the surface layer enters the absorption layer directly under it. This

layer includes SAP, which enables easy absorption and allows urine to be trapped in the

diaper core. SAP can absorb urine up to 50–100 times its weight and retain it even when

pressed.

The outermost layer of a diaper is wrapped in waterproof material that prevents urine

leakage. Some diapers are made with a breathable material that allows for airflow but

prevents moisture from passing pass through.

Figure 35: Disposable diaper structure

Body

Top sheet

Leak guard

Tape

Waterproof fabricAbsorbent paper

Fluff pulp

SAP

Ab

so

rbe

nt

Source: Credit Suisse

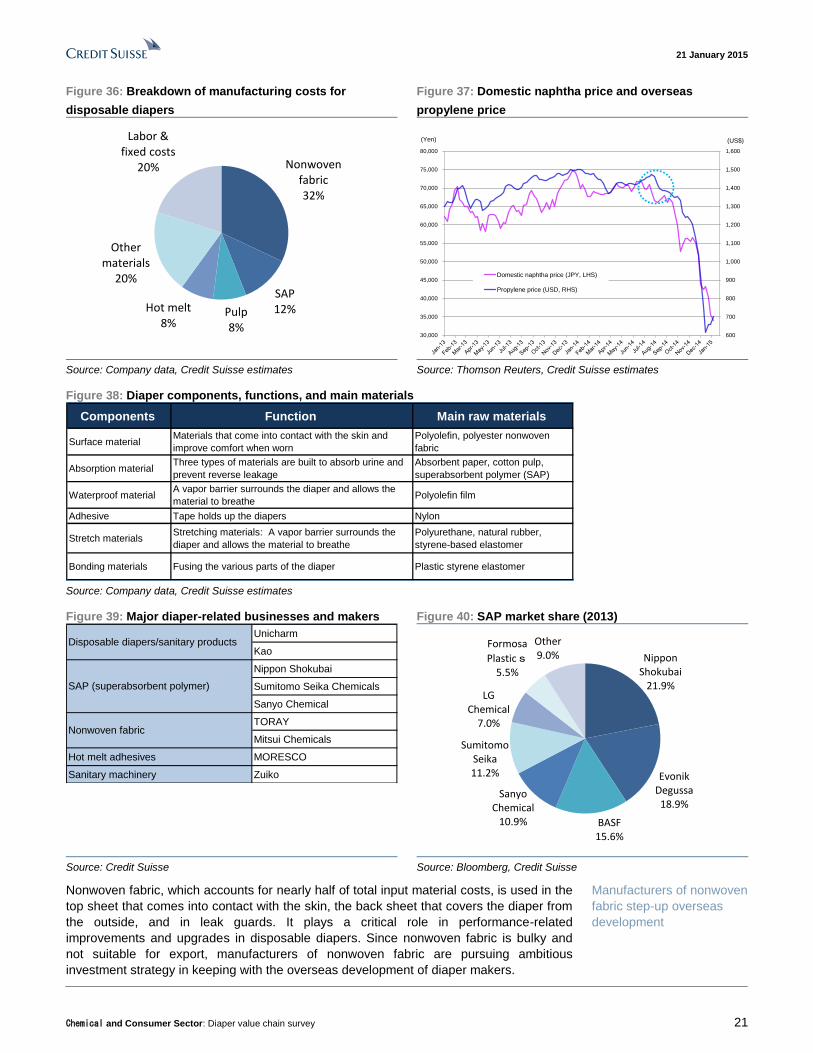

Figure 39 shows a list of diaper materials and related makers. We estimate diaper

manufacturing costs break down as nonwoven fabric 32%, super-absorbent polymers

(SAP) 12%, pulp 8%, hot-melt adhesives 8%, other materials 20%, and labor and other

fixed costs 20%. Since all input materials other than pulp are produced from naphtha, a

crude oil derivative, the trend in naphtha prices impacts the total cost of disposable

diapers.

Diaper structure consists of

three layers

Diaper manufacturing cost

breakdown: nonwoven

fabric 32%, SAP 12%, pulp

8%, and other fixed costs

20%

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 21

Figure 36: Breakdown of manufacturing costs for

disposable diapers

Figure 37: Domestic naphtha price and overseas

propylene price

Nonwoven fabric 32%

SAP12%Pulp

8%

Hot melt8%

Other materials

20%

Labor & fixed costs

20%

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

70,000

75,000

80,000

Domestic naphtha price (JPY, LHS)

Propylene price (USD, RHS)

(Yen) (US$)

Source: Company data, Credit Suisse estimates Source: Thomson Reuters, Credit Suisse estimates

Figure 38: Diaper components, functions, and main materials

Components Function Main raw materials

Surface material Materials that come into contact with the skin and

improve comfort when worn

Polyolefin, polyester nonwoven

fabric

Absorption material Three types of materials are built to absorb urine and

prevent reverse leakage

Absorbent paper, cotton pulp,

superabsorbent polymer (SAP)

Waterproof materialA vapor barrier surrounds the diaper and allows the

material to breathePolyolefin film

Adhesive Tape holds up the diapers Nylon

Stretch materials Stretching materials: A vapor barrier surrounds the

diaper and allows the material to breathe

Polyurethane, natural rubber,

styrene-based elastomer

Bonding materials Fusing the various parts of the diaper Plastic styrene elastomer

Source: Company data, Credit Suisse estimates

Figure 39: Major diaper-related businesses and makers Figure 40: SAP market share (2013)

Unicharm

Kao

Nippon Shokubai

Sumitomo Seika Chemicals

Sanyo Chemical

TORAY

Mitsui Chemicals

Hot melt adhesives MORESCO

Sanitary machinery Zuiko

SAP (superabsorbent polymer)

Nonwoven fabric

Disposable diapers/sanitary products

Nippon Shokubai

21.9%

Evonik Degussa 18.9%

BASF 15.6%

Sanyo Chemical

10.9%

Sumitomo Seika11.2%

LG Chemical

7.0%

Formosa

Plastics5.5%

Other9.0%

Source: Credit Suisse Source: Bloomberg, Credit Suisse

Nonwoven fabric, which accounts for nearly half of total input material costs, is used in the

top sheet that comes into contact with the skin, the back sheet that covers the diaper from

the outside, and in leak guards. It plays a critical role in performance-related

improvements and upgrades in disposable diapers. Since nonwoven fabric is bulky and

not suitable for export, manufacturers of nonwoven fabric are pursuing ambitious

investment strategy in keeping with the overseas development of diaper makers.

Manufacturers of nonwoven

fabric step-up overseas

development

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 22

Figure 41: Top 20 global nonwoven fabric makers (2011 sales basis)

Rank Company Country Rank Company Country

1 Freudenberg Germany 11 Sandler AG Germany

2 DuPont US 12 Hollingswroth & Vose US

3 Kimberly-Clark US 13 Japan Vilene Japan

4 Polymer Group, Inc. US 14 Companhia Providencia Brazil

5 Ahlstrom Finland 15 First Quality Nonwovens US

6 Johns Manville US 16 Asahi Kasei Japan

7 Fitesa US 17 Buckeye Technologies US

8 Glatfelter Canada 18 Fibertex Personal Care Denmark

9 Fiberweb UK 19 Toray Japan

10 Avgol Israel 20 Mitsui Chemicals Japan Source: Nonwovens Industry 2012, Nonwovens Yearbook

Figure 42: Acrylic acid, SAP and disposable diaper value chain (Credit Suisse estimates)

Acrylic acid SAP Disposable diaper

Nippon Shokubai(640kt)

BASF (1,140kt)

A w ide variety of customers

Hengan Intl. (1.1%)

BASF (400kt, 16%)

P&G (30%)

Nippon Shokubai(560kt, 22%)

Mitsubishi Chemical (110kt) Sanyo Chemical

(280kt, 11%)

Sumitomo Seika(287kt,11%)

Unicharm (7%)

Kao (1.5%)

Arkema (600kt)

Dow Chemical(890kt)

Evonik Degussa(485kt, 19%)

Kimberly-Clark (23%)

LG Chem (353kt) LG Chem (180kt, 7%)

Formosa Plastics(320kt)

Formosa Plastics

(140kt, 5%)

A few Chinese makers

A few Chinese makers

SCA (6%)

Note: Figures in parenthesis denote production capacity at end-2013 and global share based on production

capacity

Source: Company data, Credit Suisse estimates

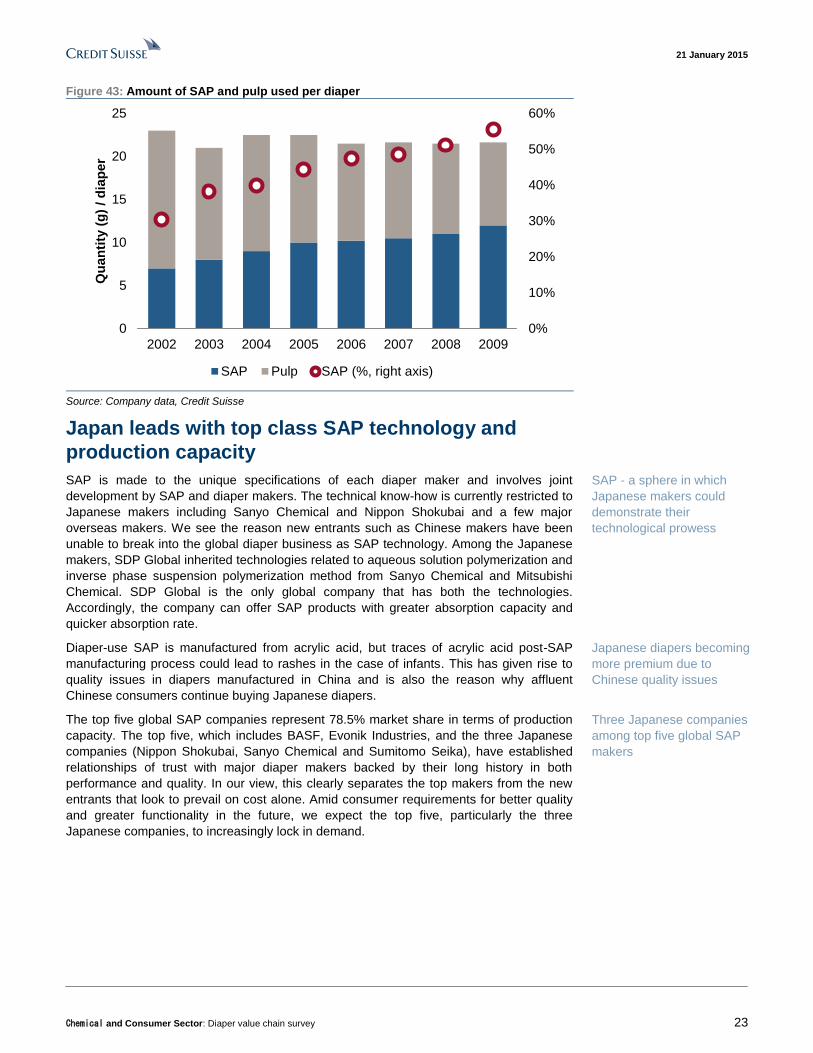

Consumer needs for diapers are becoming increasingly diverse in tandem with higher

market penetration for baby diapers in emerging markets and adult diapers in developed

markets. Some of the key needs are thinner diapers, reduced leakage, and post-

absorption surface dryness. In adult diapers, where quick drying is expected in view of

urine discharge volume, consumers are now seeking greater absorption volume per unit

time, leading to greater SAP usage. Further, the trend toward thinner diapers in raising

user comfort and saving on resources means greater usage of SAP and a reduction pulp

usage.

Increase in SAP usage in

keeping with consumer

needs for thinner diapers

with greater absorption

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 23

Figure 43: Amount of SAP and pulp used per diaper

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

2002 2003 2004 2005 2006 2007 2008 2009

Qu

an

tity

(g

) / d

iap

er

SAP Pulp SAP (%, right axis)

Source: Company data, Credit Suisse

Japan leads with top class SAP technology and

production capacity

SAP is made to the unique specifications of each diaper maker and involves joint

development by SAP and diaper makers. The technical know-how is currently restricted to

Japanese makers including Sanyo Chemical and Nippon Shokubai and a few major

overseas makers. We see the reason new entrants such as Chinese makers have been

unable to break into the global diaper business as SAP technology. Among the Japanese

makers, SDP Global inherited technologies related to aqueous solution polymerization and

inverse phase suspension polymerization method from Sanyo Chemical and Mitsubishi

Chemical. SDP Global is the only global company that has both the technologies.

Accordingly, the company can offer SAP products with greater absorption capacity and

quicker absorption rate.

Diaper-use SAP is manufactured from acrylic acid, but traces of acrylic acid post-SAP

manufacturing process could lead to rashes in the case of infants. This has given rise to

quality issues in diapers manufactured in China and is also the reason why affluent

Chinese consumers continue buying Japanese diapers.

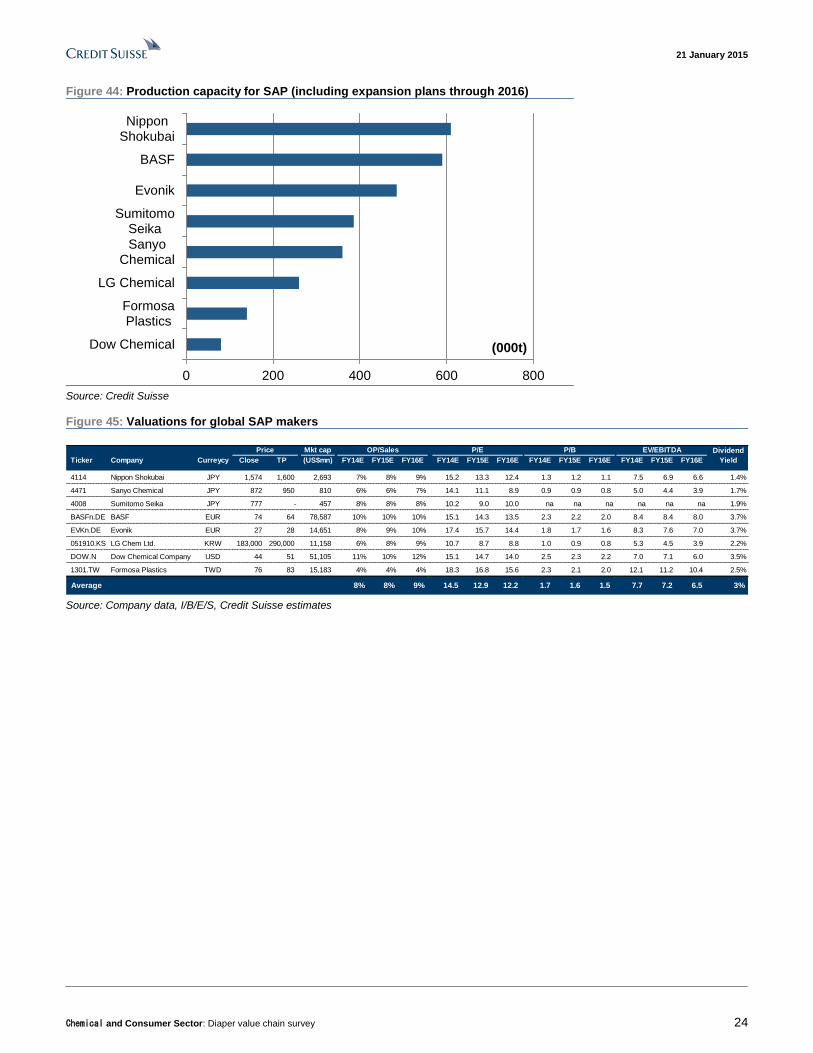

The top five global SAP companies represent 78.5% market share in terms of production

capacity. The top five, which includes BASF, Evonik Industries, and the three Japanese

companies (Nippon Shokubai, Sanyo Chemical and Sumitomo Seika), have established

relationships of trust with major diaper makers backed by their long history in both

performance and quality. In our view, this clearly separates the top makers from the new

entrants that look to prevail on cost alone. Amid consumer requirements for better quality

and greater functionality in the future, we expect the top five, particularly the three

Japanese companies, to increasingly lock in demand.

SAP - a sphere in which

Japanese makers could

demonstrate their

technological prowess

Japanese diapers becoming

more premium due to

Chinese quality issues

Three Japanese companies

among top five global SAP

makers

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 24

Figure 44: Production capacity for SAP (including expansion plans through 2016)

0 200 400 600 800

Dow Chemical

FormosaPlastics

LG Chemical

SanyoChemical

SumitomoSeika

Evonik

BASF

NipponShokubai

(000t)

Source: Credit Suisse

Figure 45: Valuations for global SAP makers

Dividend

Ticker Company Curreycy Close TP (US$mn) FY14E FY15E FY16E FY14E FY15E FY16E FY14E FY15E FY16E FY14E FY15E FY16E Yield

4114 Nippon Shokubai JPY 1,574 1,600 2,693 7% 8% 9% 15.2 13.3 12.4 1.3 1.2 1.1 7.5 6.9 6.6 1.4%

4471 Sanyo Chemical JPY 872 950 810 6% 6% 7% 14.1 11.1 8.9 0.9 0.9 0.8 5.0 4.4 3.9 1.7%

4008 Sumitomo Seika JPY 777 - 457 8% 8% 8% 10.2 9.0 10.0 na na na na na na 1.9%

BASFn.DE BASF EUR 74 64 78,587 10% 10% 10% 15.1 14.3 13.5 2.3 2.2 2.0 8.4 8.4 8.0 3.7%

EVKn.DE Evonik EUR 27 28 14,651 8% 9% 10% 17.4 15.7 14.4 1.8 1.7 1.6 8.3 7.6 7.0 3.7%

051910.KS LG Chem Ltd. KRW 183,000 290,000 11,158 6% 8% 9% 10.7 8.7 8.8 1.0 0.9 0.8 5.3 4.5 3.9 2.2%

DOW.N Dow Chemical Company USD 44 51 51,105 11% 10% 12% 15.1 14.7 14.0 2.5 2.3 2.2 7.0 7.1 6.0 3.5%

1301.TW Formosa Plastics TWD 76 83 15,183 4% 4% 4% 18.3 16.8 15.6 2.3 2.1 2.0 12.1 11.2 10.4 2.5%

Average 8% 8% 9% 14.5 12.9 12.2 1.7 1.6 1.5 7.7 7.2 6.5 3%

P/E P/B EV/EBITDAPrice Mkt cap OP/Sales

Source: Company data, I/B/E/S, Credit Suisse estimates

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 25

SAP makers in spotlight Sustained growth in SAP demand

Among the basic materials used in diapers, we focus on demand growth for SAP, in which

Japanese makers boast top class technology and production capacity. Japanese SAP

makers have stepped up global development in tandem with demand growth for baby and

adult diapers, which account for 90% of SAP demand, and for hygiene-related products.

Nippon Shokubai estimates global SAP demand will grow at an annual rate of 6–7% in the

medium term (from an estimated 2mn t in 2013).

SAP is one of the rare areas registering sustained growth among petroleum-derived

plastics. Initially, the main component of diapers was pulp, but they have become thinner

and easy to use thanks to SAP, which also eliminated leakage and resurfacing of moisture.

Unlike cloth diapers, there is no washing involved in disposable diapers, and since there is

little need for frequent diaper change, disposable diapers have gained widespread support

from parents and care-givers. This has also led to significant growth in demand. The

recent trend in disposable diapers is toward reducing pulp volume to significantly cut

waste. We assume that, unlike repeated washing of cloth diapers, the use of disposable

diapers has almost no environmental impact.

Unicharm has introduced its own theory on disposable diapers. According to this,

disposable diaper sales start rising rapidly once the nation’s per capita GDP exceeds

$3,000. The growth, driven by Asia, is particularly remarkable in China and emerging

markets. The annual growth rate in these regions is over 20%. The use of disposable

diapers is well established in Japan, Europe and the US, but the annual growth rate in

these regions is only around a few percent. The demand is driven by growth in adult

diapers rather than baby diapers in countries such as Japan, which face a declining birth

rate and a growing proportion of elderly people. Also, the recent demand for pet diapers

cannot be overlooked.

According to the Japan Hygiene Products Industry Association (JHPIA), domestic diaper

output rose 8% YoY, up 17.2108bn pieces in 2013 (+6% or 665,435t on a weight basis).

Despite a falling birth rate, baby diapers rose 12% to 107.2005bn pieces, and adult

diapers rose 3% to 6.4902bn pieces in a strong performance. Napkin-type incontinence

pads, which have gained in visibility, also substantially eclipsed year earlier performance.

The overall trend has remained intact in 2014, with Jan–Sep diaper output (by weight)

rising 8% YoY to 523,376t. Baby diapers rose 10% to 291,960t, and adult diapers

increased by 5.6% to 231,416t. Baby diapers continued to register double-digit growth for

the second straight year in Japan, a country facing a declining birth rate and aging

population.

Supply capacity has kept pace with growing demand. Annual production capacity of major

manufacturers in 2013 is as follows: Nippon Shokubai 560,000t, BASF, 400,000t, Evonik

405,000t, Sumitomo Seika 287,000t, SDP Global 280,000t, LG 180,000t. As each

company continued to raise capacity, the combined capacity of the top eight global

companies increased to 2.33mn t.

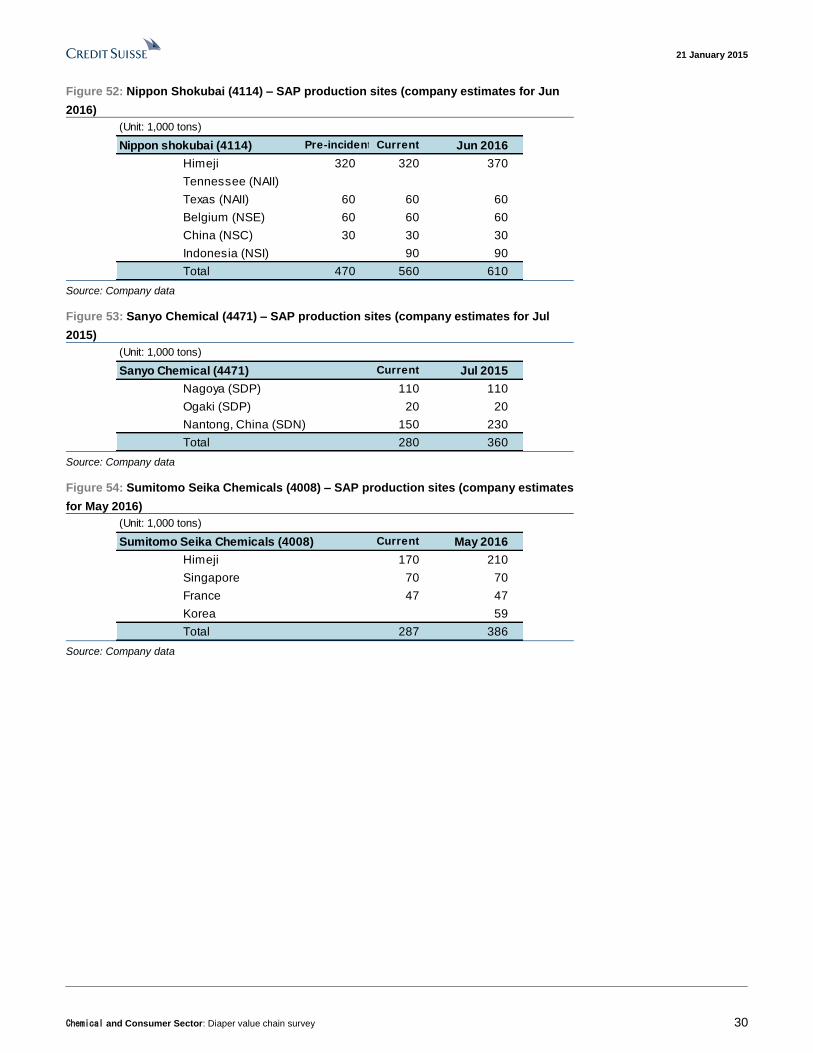

SDP Global is scheduled to raise capacity in China by 80,000t as early as 2015.

Sumitomo Seika plans to bring roughly 40,000t in additional capacity online in April 2015.

As a result, total capacity of the top six global companies is likely to rise to just under

2.71mn t in 2015.

Global demand totaled

2mn t in 2013

SAP – a rare growth area in

plastics

Correlation between

disposable diapers and per

capita GDP of US$3,000

Domestic diaper production

volume rose 8% YoY in

2013

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 26

Figure 46: SAP production capacity global ranking Company Americas Europe Asia Total

1 Nippon Shokubai 60 60 440 560 Jun 2016 Expansion 50 in Japan

2 Evonik Industries *1 135 190 80 405 End of 2013 Expansion 80 in Saudi Arabia

End of 2014 Newly established 60 in Brazil

3 BASF 180 200 20 400 End of 2013 Newly established 80 Saudi Arabia

4 Sumitomo Seika Chemicals *2 47 240 287 Apr 2015 Expansion 40 in Japan

May-16 Expansion 59 in South Korea

5 SDP Global 280 280 Jul-15 Expansion 80 in China

6 LG Chem Ltd. 180 180 Sep 2015 Expansion 80 in South Korea

7 Formosa Plastics Group 140 140

8 The Dow Chemical Company 80 80 Make-to-order for Evonik

Total of top 8 companies 455 497 1,380 2,332

Worldwide total 465 497 1,600 2,562

Unit: 1,000 tons

Note

Note: Additional capacity excluded from total for top eight companies and global total

Source: Chemical goods handbook 2014, The Heavy & Chemical Industries News Agency

The outlook points to a stable supply-demand balance continuing in the foreseeable future.

We calculate SAP demand outlook for diapers based on estimated baby and adult diaper

volumes. The global disposable diaper market in 2012 totaled 138.6590bn pieces in baby

diapers and 14.2850bn pieces in adult diapers. We assume SAP usage at 12 grams for

baby diapers and at 15.6 grams for adult diapers, and applying these to the above diaper

numbers, we arrive at a total SAP volume of 1.8887mn t. Assuming a 5% increase in baby

diapers and an 8% increase in adult diapers from 2012 to 2013, we arrive at a total SAP

demand of 1.9880mn t (close to the 2mn t estimated by Nippon Shokubai).

SAP demand is likely to grow to 2.8710mn t in 2020, assuming the above 5% increase in

baby diapers and 8% increase in adult diapers remains constant throughout the period.

On the other hand, assuming supply grows at an annual rate of 5% beyond 2015, total

supply is likely to rise to 3.7250mn t in 2020, up from 2.5690mn t in 2013.

We forecast the supply–demand balance to remain more or less even, from 78% in 2013

to 77% in 2020. We accordingly expect SAP supply–demand to trend firm over the

medium-term.

Figure 47: Supply–demand of SAP for diapers

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2013 2014 2015 2016 2017 2018 2019 2020

Supply

Adult diaper

Baby diaper

(thousand tons)

Source: Company data, Credit Suisse estimates

Outlook for a strong

supply–demand balance

21 January 2015

Chemical and Consumer Sector: Diaper value chain survey 27

Price trends

SAP export prices were on a downtrend from 2009 following a hike in Chinese supply

capacity. However, after an accident at Nippon Shokubai in September 2012, the supply-

demand situation started to tighten, leading to a sharp increase in export prices. With

outlook emerging for restoration of manufacturing facilities, export prices are trending

somewhat soft recently. We think Japanese SAP makers can ensure margins through the

adoption of a manufacturing process that starts with basic raw materials. Also, we expect

growth in supply of high function SAP used in thinner, premium diapers to drive

improvement in product mix.

Figure 48: SAP export volume from Japan and unit price Figure 49: Acrylic acid export volume from Japan and unit

price

200

300

400

500

600

700

0

1000

2000

3000

4000

5000

6000

7000

8000

Jan

-88

Jul-

89

Jan

-91

Jul-

92

Jan

-94

Jul-

95

Jan

-97

Jul-

98

Jan

-00

Jul-

01

Jan

-03

Jul-

04

Jan

-06

Jul-

07

Jan

-09

Jul-

10

Jan

-12

Jul-

13

Jan

-15

Export volume (LHS,t) Price (RHS, Y000/t)

0

200

400

600

800

1000

1200

0

2000

4000

6000

8000

10000

12000

14000

16000

Jan

-88

Jul-

89

Jan

-91

Jul-

92

Jan

-94

Jul-

95

Jan

-97

Jul-

98

Jan

-00

Jul-

01

Jan

-03

Jul-

04

Jan

-06

Jul-

07

Jan

-09

Jul-

10

Jan

-12

Jul-

13

Jan-1

5

Export volume (LHS,t) Price (RHS, Y000/t)

Source: Trade Statistics of Japan, Ministry of Finance Source: Trade Statistics of Japan, Ministry of Finance

Figure 50: China SAP monthly import volume and unit

price

Figure 51: China acrylic acid monthly import volume and

unit price

2.80

3.00

3.20

3.40

0

10

20

30

40

50

12-3 12-7 12-11 13-3 13-7 13-11 14-3 14-7 14-11

(US$/kg)(000t)

Volume (LHS)

Unit price(RHS)

1.20

1.30

1.40

1.50

1.60

1.70

1.80

1.90

2.00

0

2

4

6

8

10

12

12-3 12-7 12-11 13-3 13-7 13-11 14-3 14-7 14-11

(US$/kg)(000t) Volume (LHS)

Unit price(RHS)

Source: China Customs Information Center Source: China Customs Information Center

Japanese SAP makers

Below, we examine the latest developments at the three Japan-based SAP makers, who

between them account for just under half of the six leading suppliers’ global production

capacity of an estimated 2.4mn tons. Japan’s leading manufacturer, Nippon Shokubai,

produces SAP at its Himeji Plant. In September 2012 the company was ordered to shut

down the entire plant owing to an explosion and fire at the acrylic acid production facility. It

has gradually brought operations back on stream in stages since, recovering to full