Checking Account Simulation Understanding Checking Accounts

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Checking Account

Simulation

Understanding Checking Accounts

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

What is a Checking

Account?

Tool used to transfer funds deposited into the account to make a cash purchase

Could also be named a transaction account

Common financial service used by many consumers

Available at depository institutions Traditionally called banks

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Checking Accounts

continued

Services and fees will vary depending upon the

financial institution

Research the financial institution and type of account

before choosing

Many financial institutions offer telephone and

internet banking services to customers

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Benefits

Can help to manage money

Written record of expenses

Check register

Makes bill paying more convenient

Reduces the need to carry large amounts of cash

Most liquid of cash management tools

Considered cash

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

How Do They Work?

Money is deposited into the account with a deposit

slip

Pay the transaction by:

Writing a check

Using an ATM and/or debit card

Using electronic banking

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Characteristics

Funds are easily accessible through:

A check

Automated teller machine (ATM)

Debit card

Telephone

Internet

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

What is a Check?

Piece of paper pre-printed

with the account holder’s:

Name

Address

Financial institution

Identification numbers

To completed check, fill in the: Amount

Payee

To whom the check was written

Date

Signature

Used at the time of purchase as the form of payment

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Bouncing a Check

Check written for an amount over the current balance held in the account ‘Bounces’ due to insufficient funds

Assessed a substantial fee by both the financial institution and the payee

Can cause harm to credit report Financial institutions report to credit bureaus the account

holder’s failure/success to manage his/her checking account properly

Used as a guide for future inquiries for credit

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Other Checking

Components

Register

Place to immediately record all monetary transactions for

a checking account

Written checks, ATM withdrawals, debit card purchases,

deposits, fees, etc.

Checkbook

Contains the checks and the register to track monetary

transactions

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

What is an ATM?

Automated teller machine (ATM)

Also called cash machines

Electronic computer terminals offering automated, computerized banking

Allows customers to perform transactions just as they would through a teller Deposits, cash withdrawals, account transfers, check

account balances

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

ATMs continued

Transactions at an ATM are automatically posted

to account

Immediately record all transactions into the

checkbook register

Good option for evenings or weekends when

financial institutions are closed

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

ATM Availability

Available most places around the U.S. giving

customers access to money when away from home

Can also be found worldwide

Found in a variety of places including:

Financial institutions

Supermarkets

Convenience stores

Shopping centers

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

ATM Fees

ATMs are owned by different financial institutions

Fees may be charged to the account for ATM use

Fees range from $0.50 to $5.00

Usually free to account holders of the financial

institution

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

ATM Card

Card given to account holder to make financial

transactions at ATMs

In the shape of a credit card, but can only be used in

designated places

Must use personal identification number (PIN) to

access the account

A protected number given or chosen by the account holder

to allow access to the account

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

PINs

Required at ATM as a safety measure so other

people cannot access the account with the only the

ATM card

Choose a PIN which is not easily identified

For example – phone number, birthday

Instead of requiring a PIN, some ATMs may read a

person’s face, fingerprint, or eye’s iris to confirm

identity

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

What is a Debit Card?

Looks like a credit card, but is connected to the

cardholder’s checking account for transactions

Money is automatically withdrawn from account

when transaction occurs

Prevents overdrafts

Transaction cannot be completed without sufficient

funds

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Debit Cards continued

Some are dual function cards

One card performs both functions for

ATMs and debit cards

Clarify whether or not the card is

an ATM card, a debit card, or both

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Using a Debit Card

To make a purchase Debit card is swiped like a credit card

Cardholder signs a printed receipt

Record transactions immediately into check register

Most can be used at retail establishments accepting major credit cards Many have the Visa or MasterCard logo

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Debit Cards continued

Convenient

Small

Can be used like a credit card

Allows a person to carry less cash

Does not allow overspending

Can lose track of balance if

transactions are not immediately

written down

Opens checking account up to

credit card fraud

If lost, anyone can use it

Someone else can gain access to

account if card is found and PIN is

learned

Pros Cons

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Types of Accounts

Available

Financial institutions offer different types of checking accounts All have own characteristics

Research all of the requirements and restrictions before opening the account

Basic types/guidelines include: Regular checking

Free checking

Special checking

Interest-Earning checking

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Regular Checking

No monthly charge if minimum balance is

maintained

No interest is given

Unlimited check writing

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Free Checking

No charges or fees for using the account

No minimum balance required

Unlimited check writing

Usually for a specific group:

Students

Seniors

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Special Checking

Generally for people who write only a few checks

and keep a low balance

Basic account which pays no interest

Monthly service charge or fee for each transaction

May have restrictions on number of transactions

each month

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Interest-Earning

Checking

Pays interest on money in account

Usually the lowest interest rate of all the cash

management tools

Minimum balance required

Unlimited check writing

Called a share draft at credit unions

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Opening a Checking

Account

Most applications are completed on a computer to

process quickly

Customer may have to complete a brief hand-written

application to be entered into the computer by new

accounts personnel

Customer must have:

Picture identification

Name, address, phone number, and social security number

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Opening continued

If customer is approved, he/she completes a signature card Contains account information about the new account and

his/her signature

Used to verify the signature for each signed transaction for the account to prevent fraud

Completion of the signature card means the customer agrees to all terms and conditions of the account

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

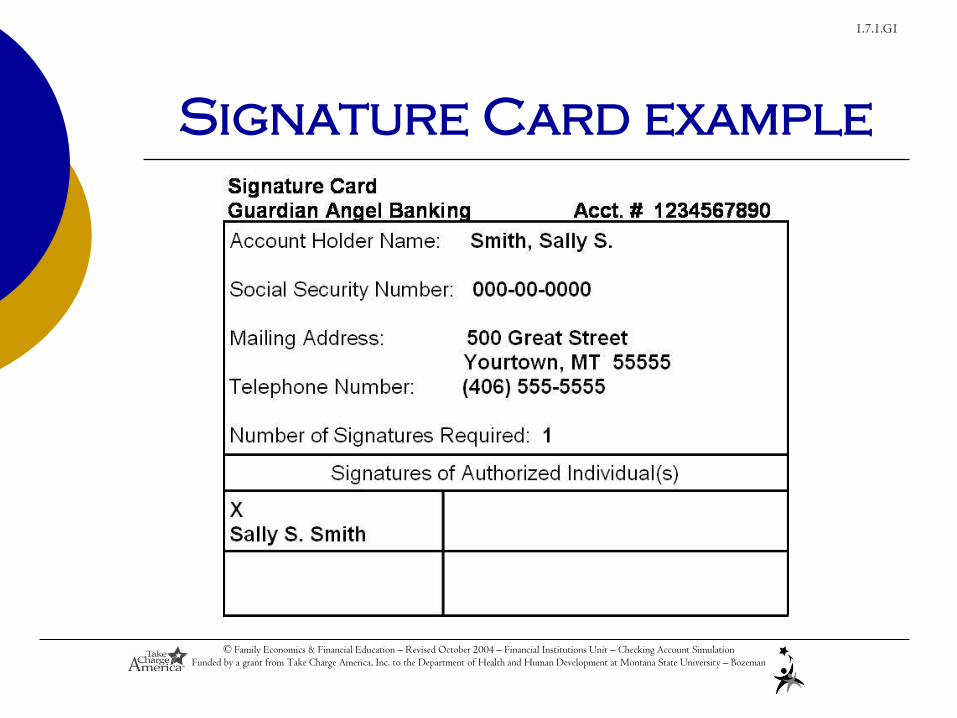

Signature Card example

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Opening continued

If offered, customers may choose to have an ATM

and/or debit card for the account

May be required to complete another form

An initial deposit must be made

Amount will vary among different financial institutions

and type of account

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Ordering Checks

New customers are provided starter checks to use until the ordered checks arrive Generic checks with account number and financial institution pre-

printed

Customer information is hand written

Many businesses do not accept starter checks Take this into consideration before making the initial deposit

Ordered checks may take 5 to 10 business days to arrive

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Ordering continued

Personal information on checks

Name

Address

Optional: phone number, driver’s license number

DO NOT put the account holder’s social security number on

the check for security reasons

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Ordering continued

Design of the check is customer’s choice

Customer pays for checks

Price depends on the style

Style of the check does not change how a check works

Some financial institutions may offer basic checks free of

charge

Single or duplicate checks are available

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

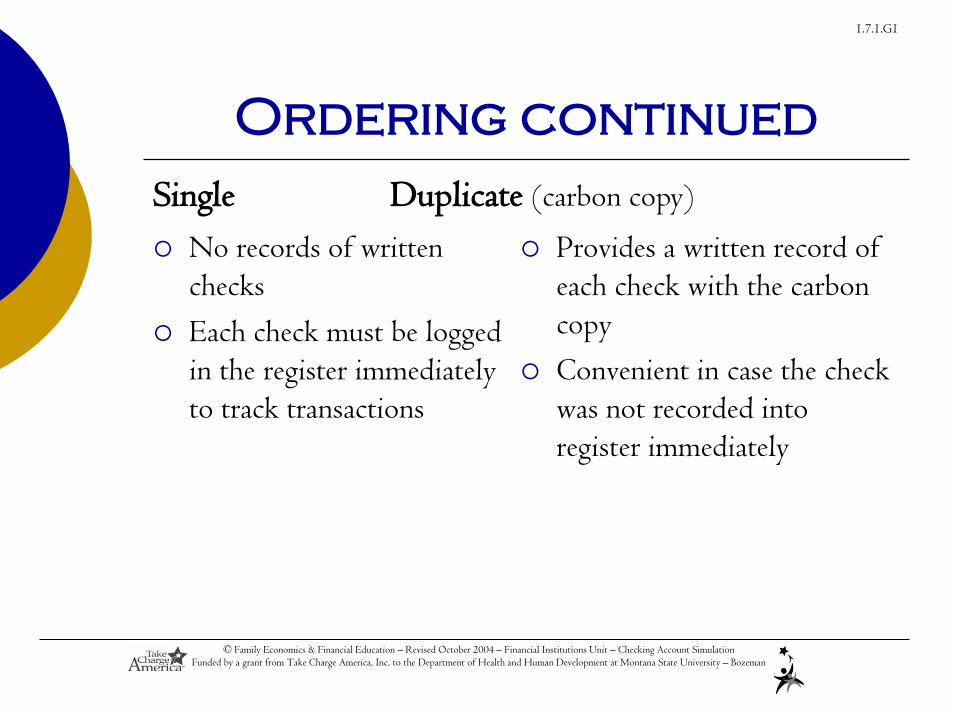

Ordering continued

No records of written

checks

Each check must be logged

in the register immediately

to track transactions

Provides a written record of

each check with the carbon

copy

Convenient in case the check

was not recorded into

register immediately

Single Duplicate (carbon copy)

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Endorsing a Check

Endorsement

Signature on the back of the check from receiving person approving it for

deposit

A check must be endorsed to be deposited

Three types

Blank

Restrictive

Special

Safest way to endorse the check is to wait until going to the

financial institution to deposit or cash the check

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

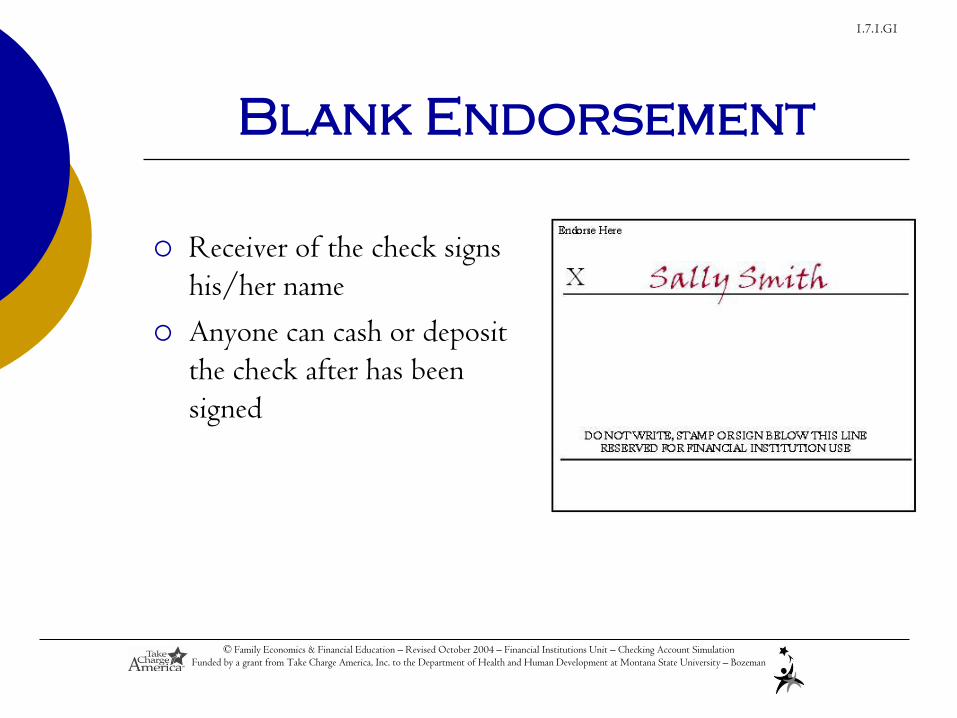

Blank Endorsement

Receiver of the check signs

his/her name

Anyone can cash or deposit

the check after has been

signed

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

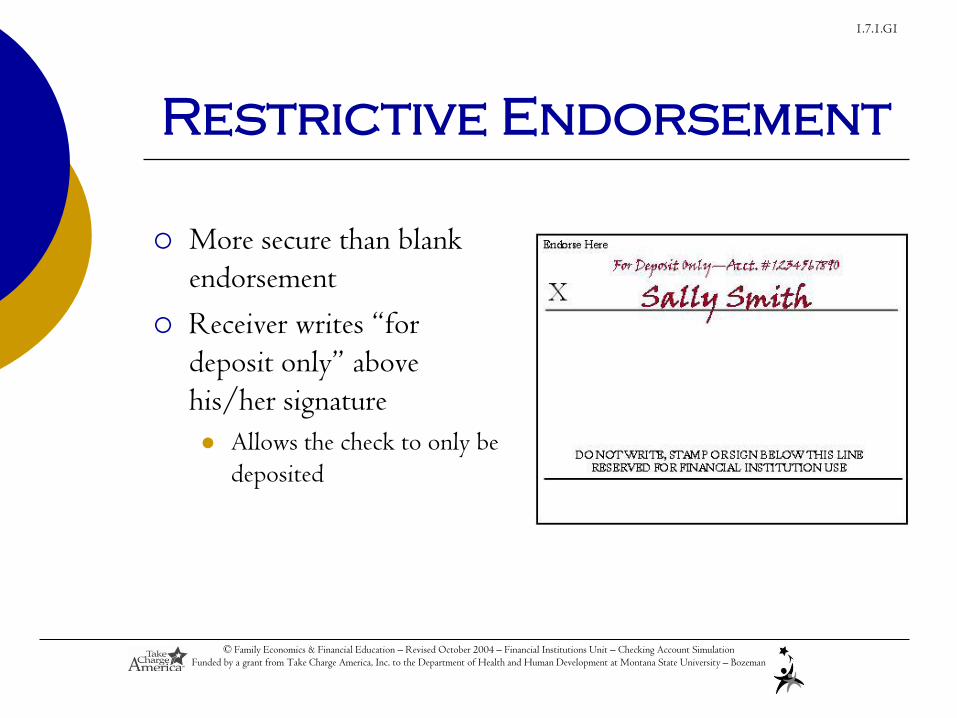

Restrictive Endorsement

More secure than blank

endorsement

Receiver writes “for

deposit only” above

his/her signature

Allows the check to only be

deposited

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Special Endorsement

Receiver signs and writes

“pay to the order of (fill in

person’s name)”

Allows the check to be

transferred to a second

party

Also known as a two-party

check

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Making a Deposit

Deposit slip

Contains the account holder’s account number and allows money

(cash or check) to be deposited into the correct account

Located in the back of the checkbook

Complete a deposit slip to make a deposit

Give to financial institution along with cash and/or check

Checks must be endorsed to be deposited

Deposited amount must be recorded in the check register to

keep the balance current

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

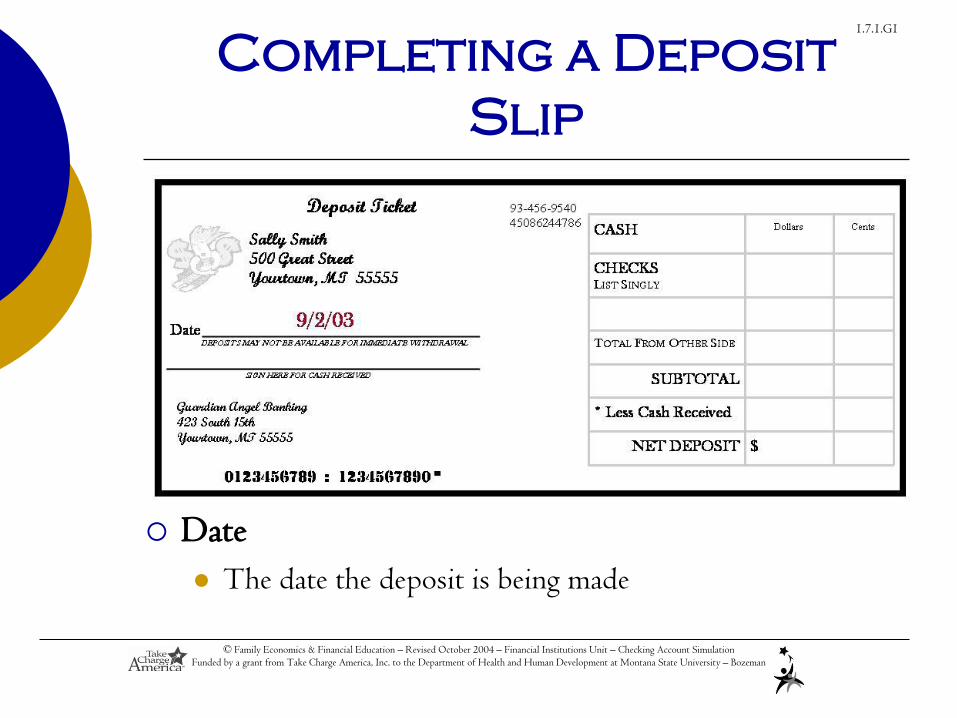

Completing a Deposit

Slip

Date

The date the deposit is being made

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

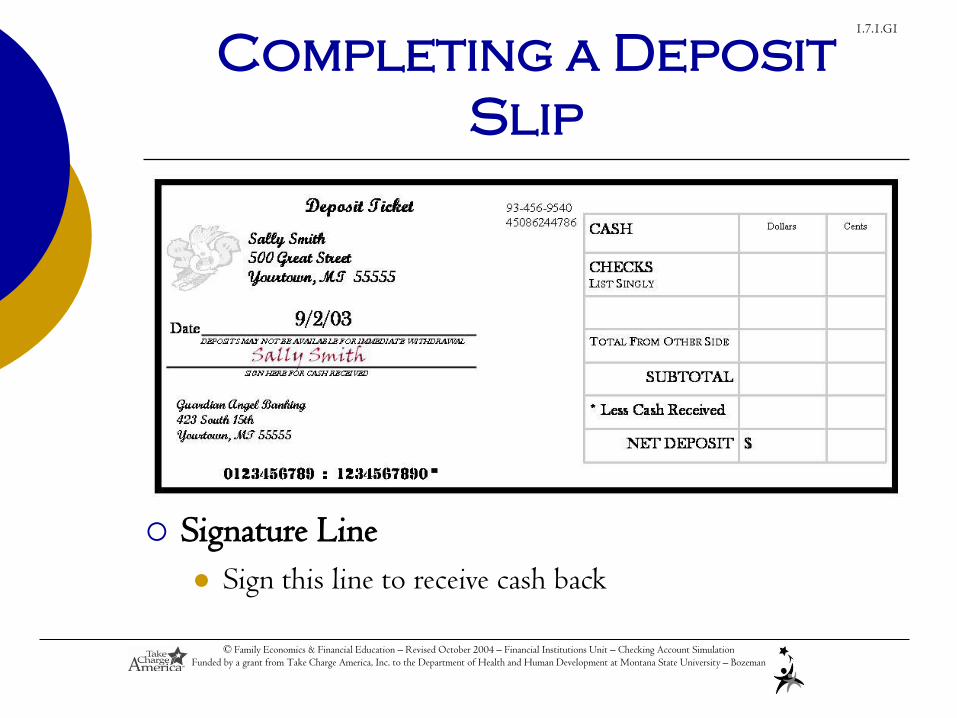

Completing a Deposit

Slip

Signature Line

Sign this line to receive cash back

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

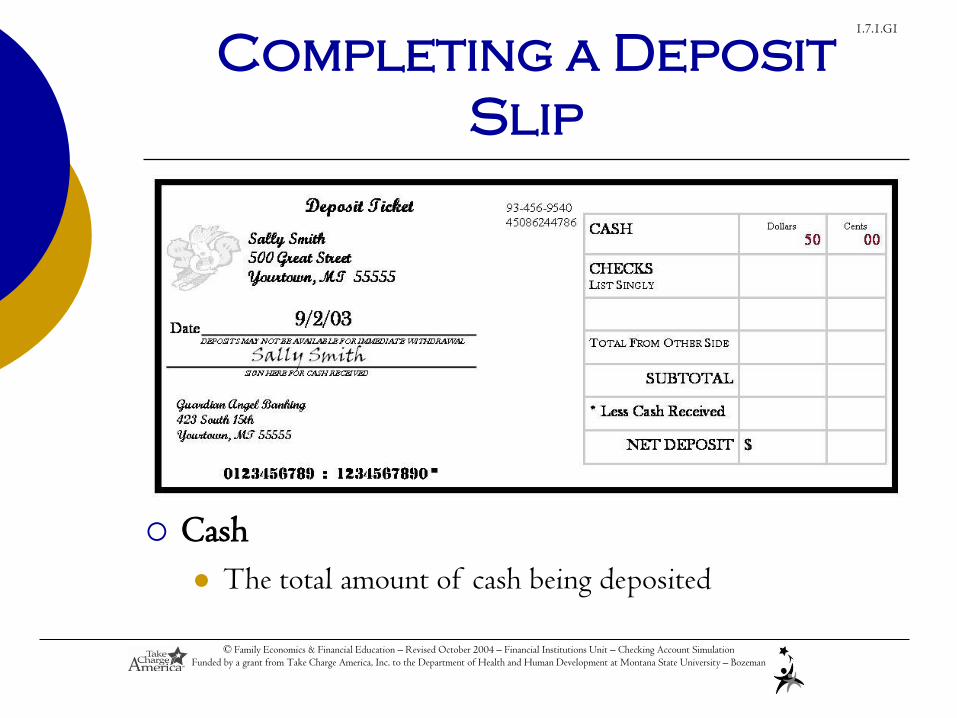

Completing a Deposit

Slip

Cash

The total amount of cash being deposited

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

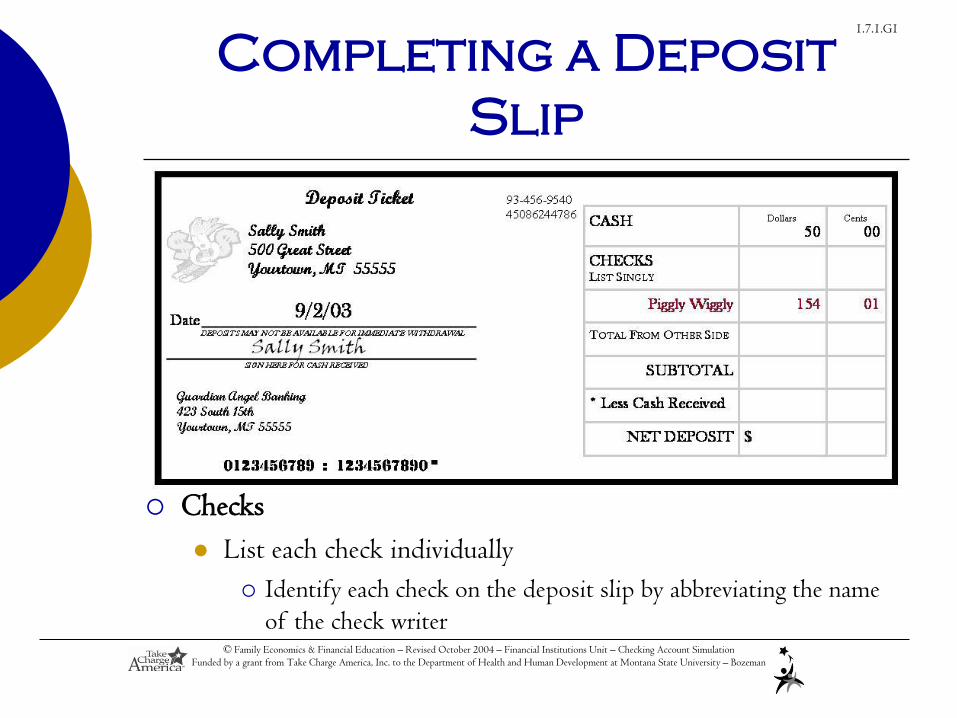

Completing a Deposit

Slip

Checks

List each check individually

Identify each check on the deposit slip by abbreviating the name

of the check writer

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

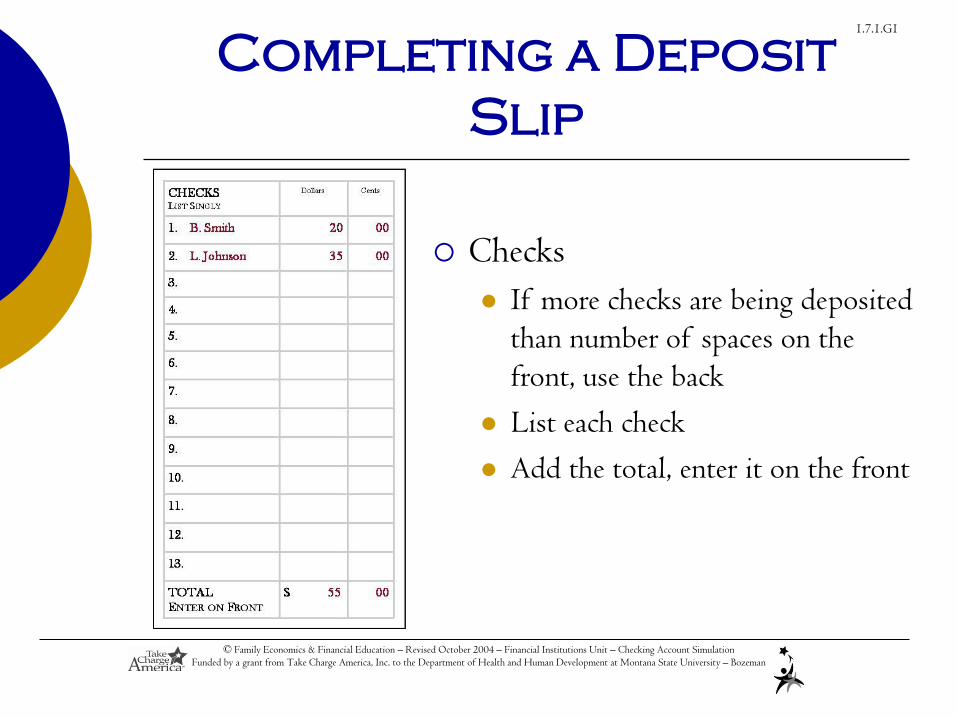

Completing a Deposit

Slip

Checks

If more checks are being deposited

than number of spaces on the

front, use the back

List each check

Add the total, enter it on the front

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

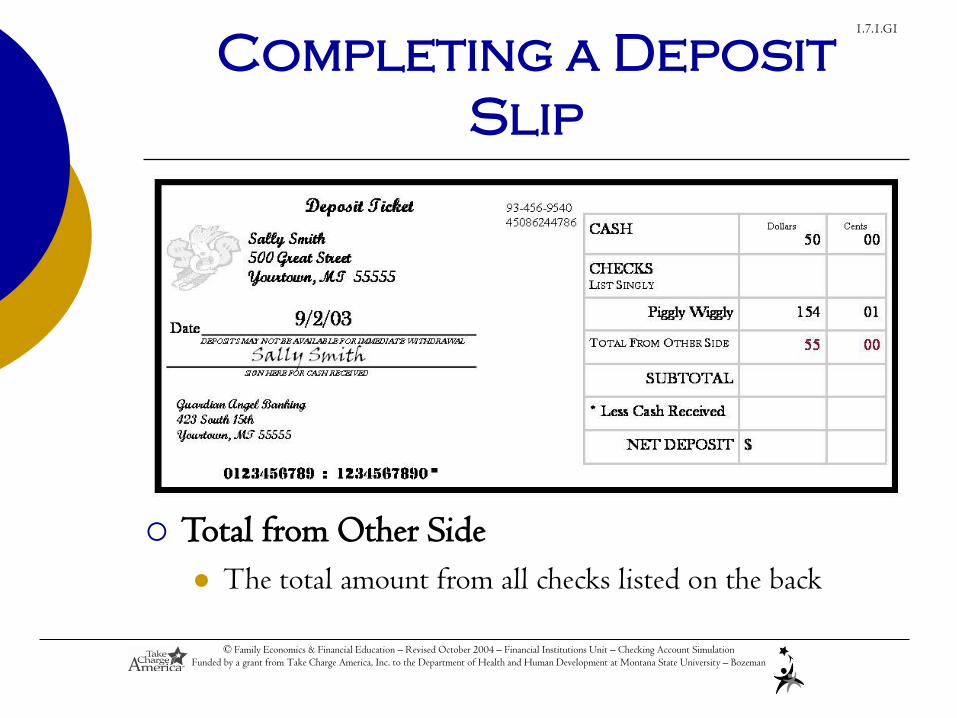

Completing a Deposit

Slip

Total from Other Side

The total amount from all checks listed on the back

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

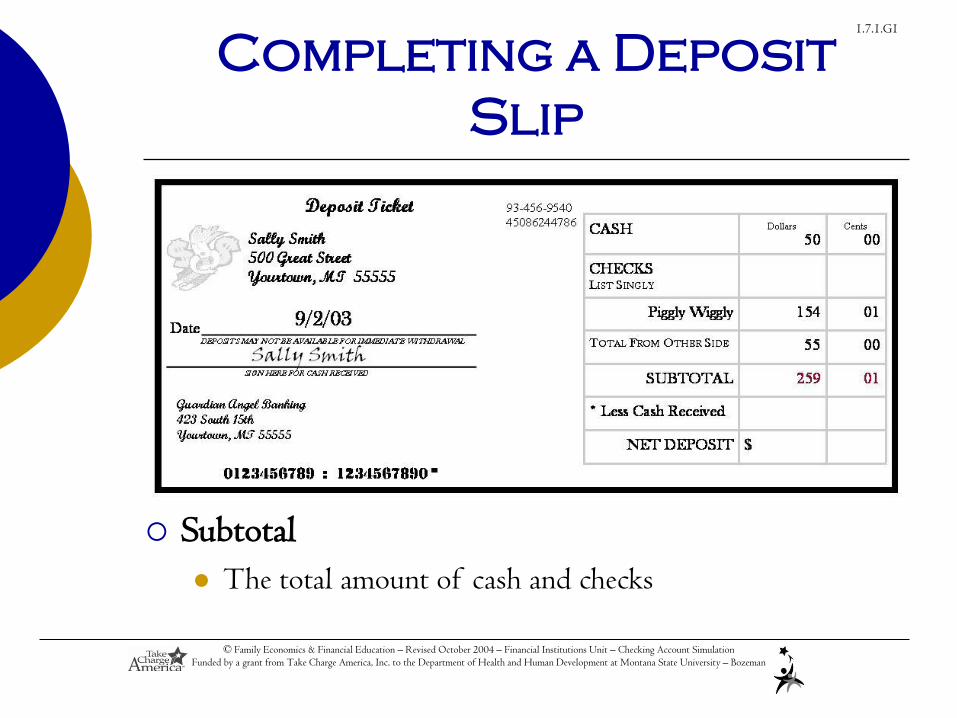

Completing a Deposit

Slip

Subtotal

The total amount of cash and checks

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

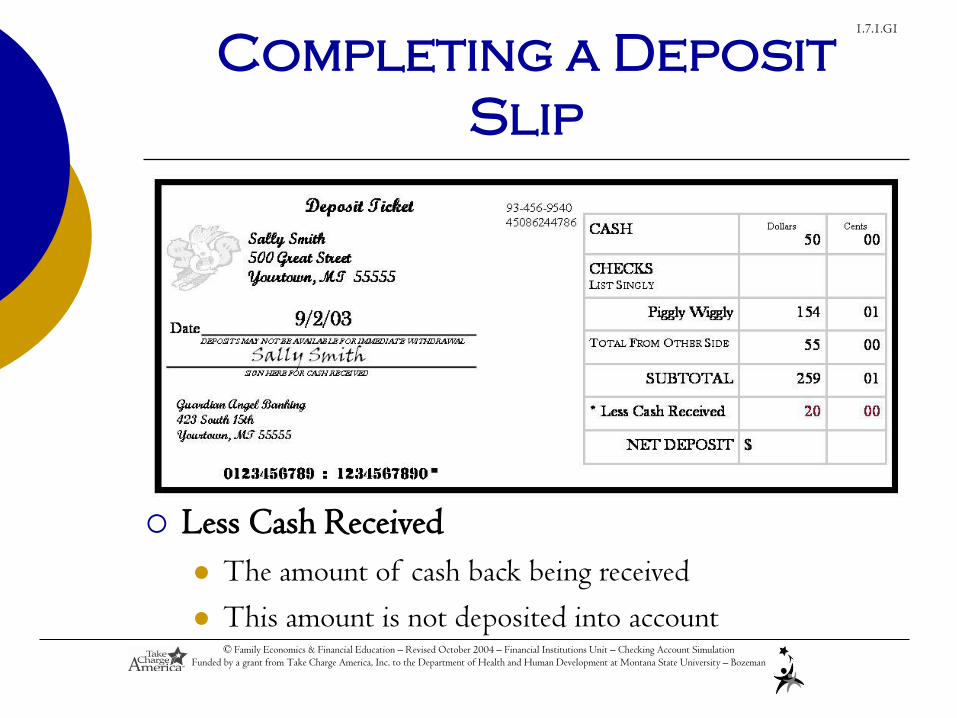

Completing a Deposit

Slip

Less Cash Received

The amount of cash back being received

This amount is not deposited into account

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

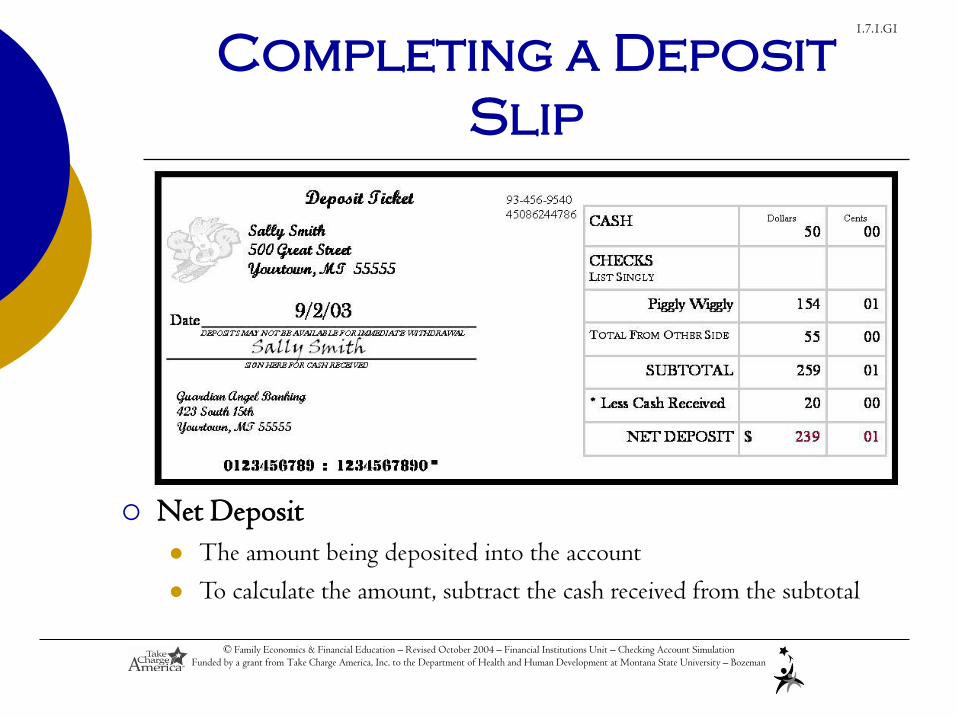

Completing a Deposit

Slip

Net Deposit

The amount being deposited into the account

To calculate the amount, subtract the cash received from the subtotal

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Writing a Check

To pay for items using a checking account A check is given as a form of payment

Must be completed and given to the person or business

Pre-printed items on a check Name and address of account holder

Name and address of financial institution

Check number

Identification numbers (account, routing)

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

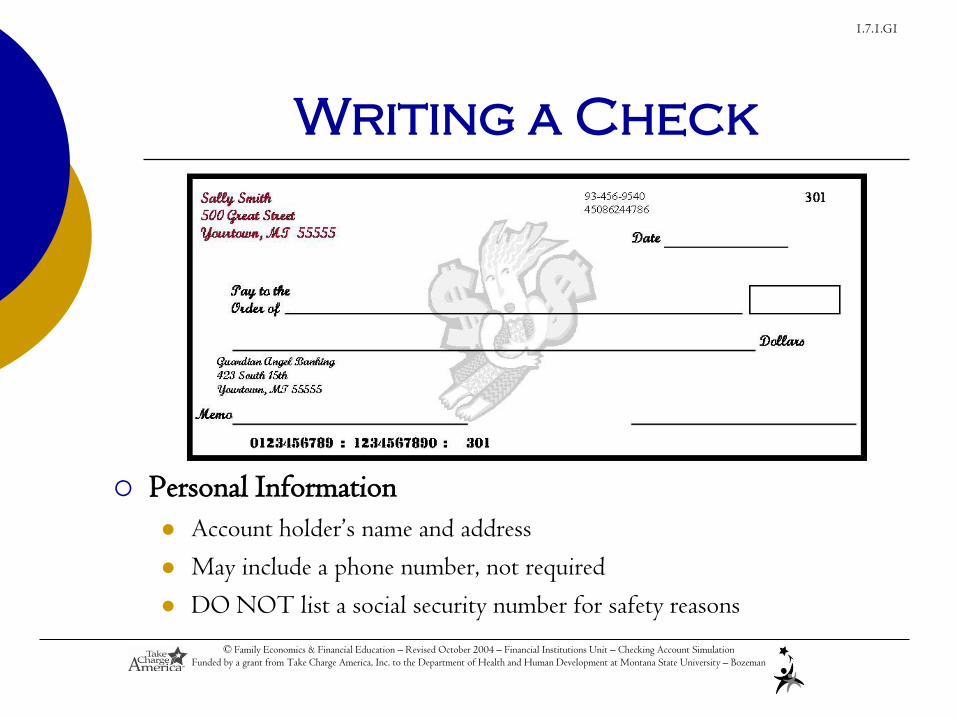

Writing a Check

Personal Information

Account holder’s name and address

May include a phone number, not required

DO NOT list a social security number for safety reasons

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

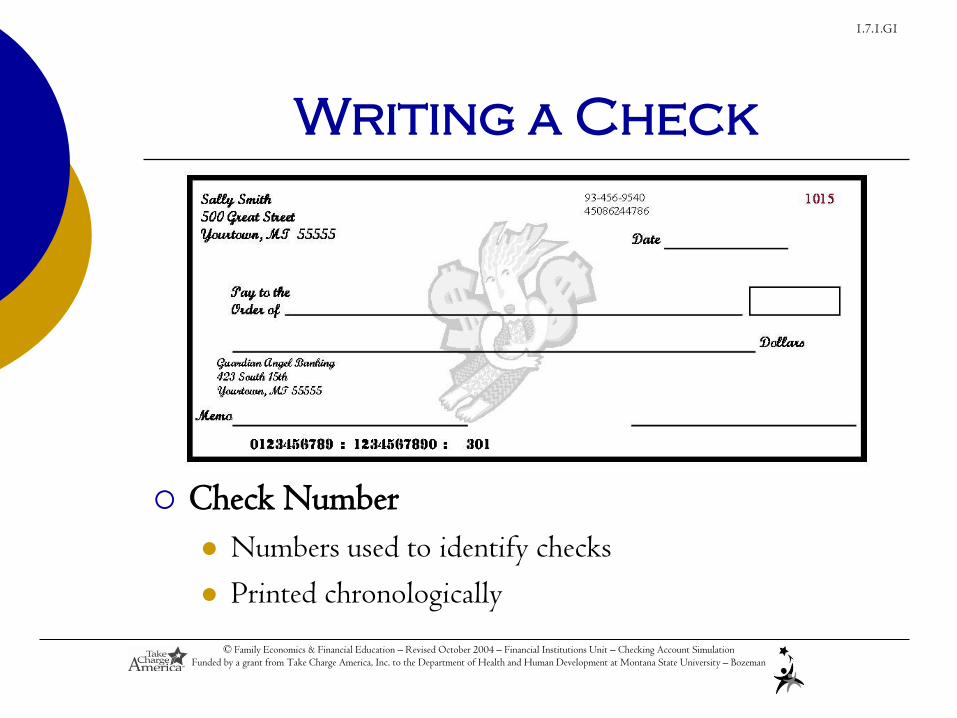

Writing a Check

Check Number

Numbers used to identify checks

Printed chronologically

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

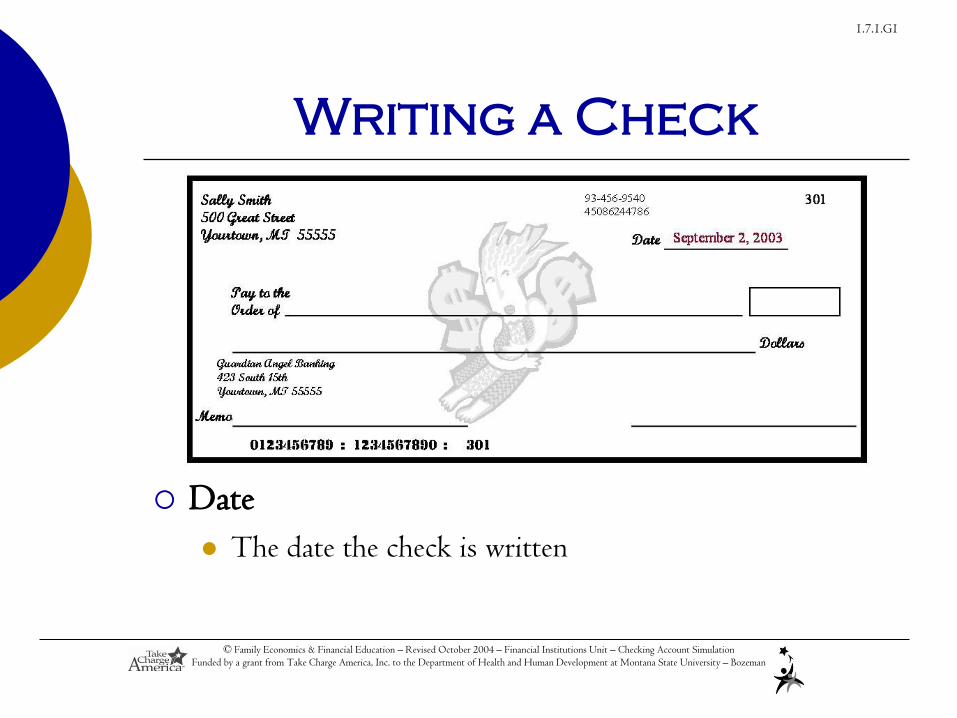

Writing a Check

Date

The date the check is written

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

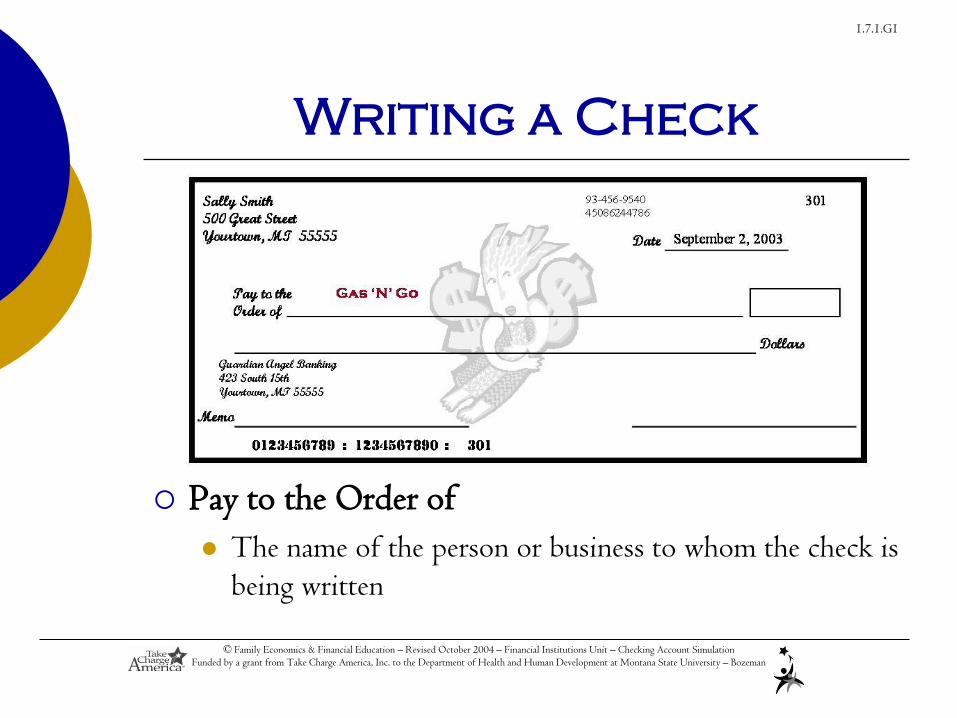

Writing a Check

Pay to the Order of

The name of the person or business to whom the check is

being written

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

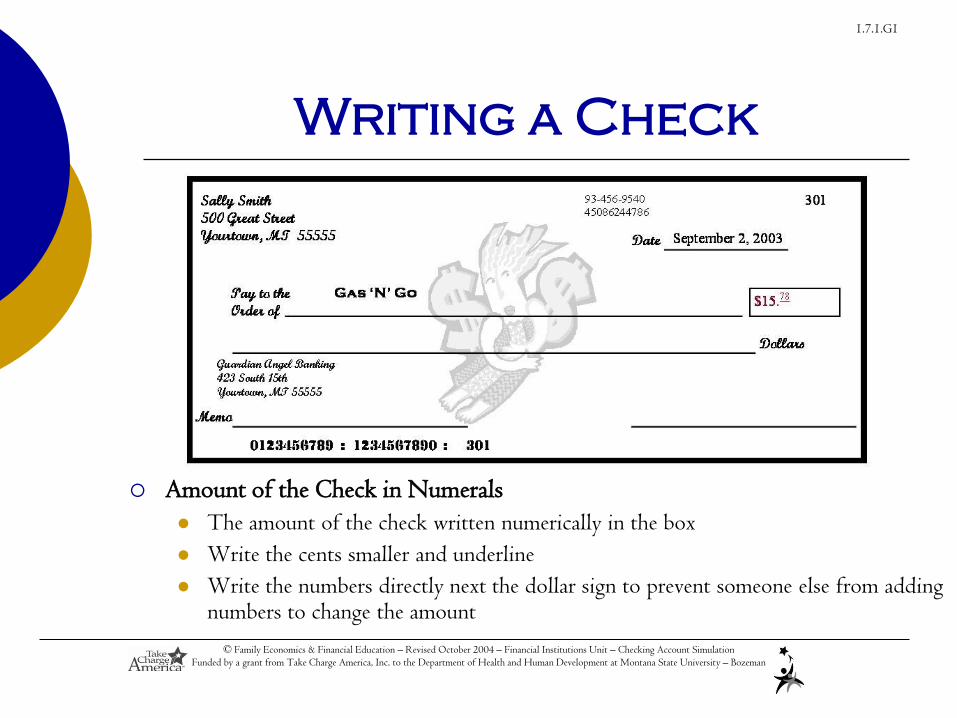

Writing a Check

Amount of the Check in Numerals

The amount of the check written numerically in the box

Write the cents smaller and underline

Write the numbers directly next the dollar sign to prevent someone else from adding numbers to change the amount

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

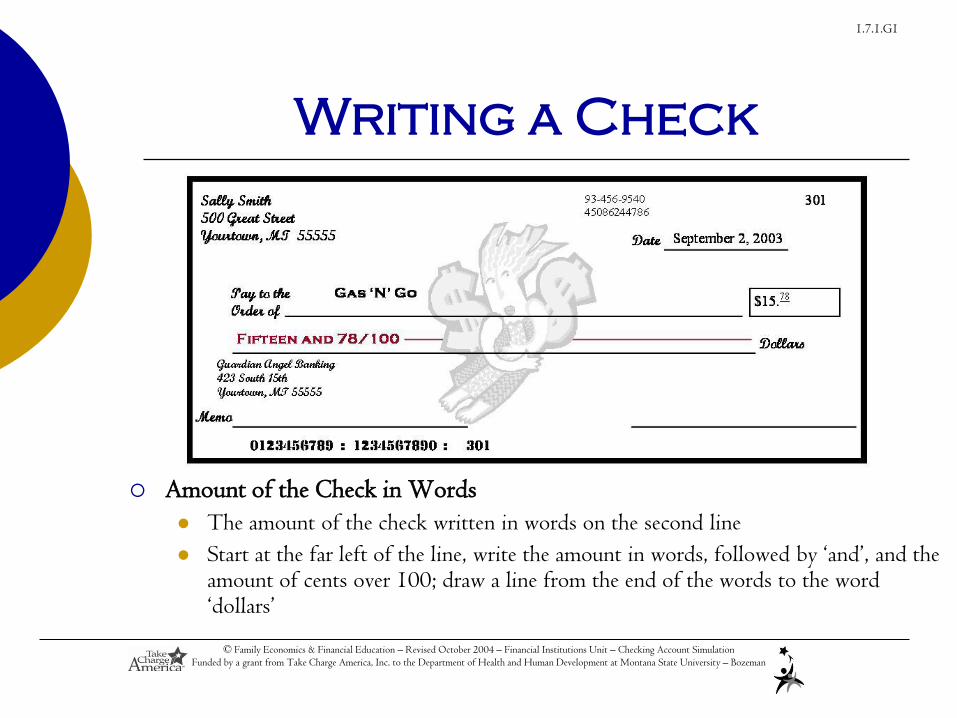

Writing a Check

Amount of the Check in Words

The amount of the check written in words on the second line

Start at the far left of the line, write the amount in words, followed by ‘and’, and the amount of cents over 100; draw a line from the end of the words to the word ‘dollars’

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

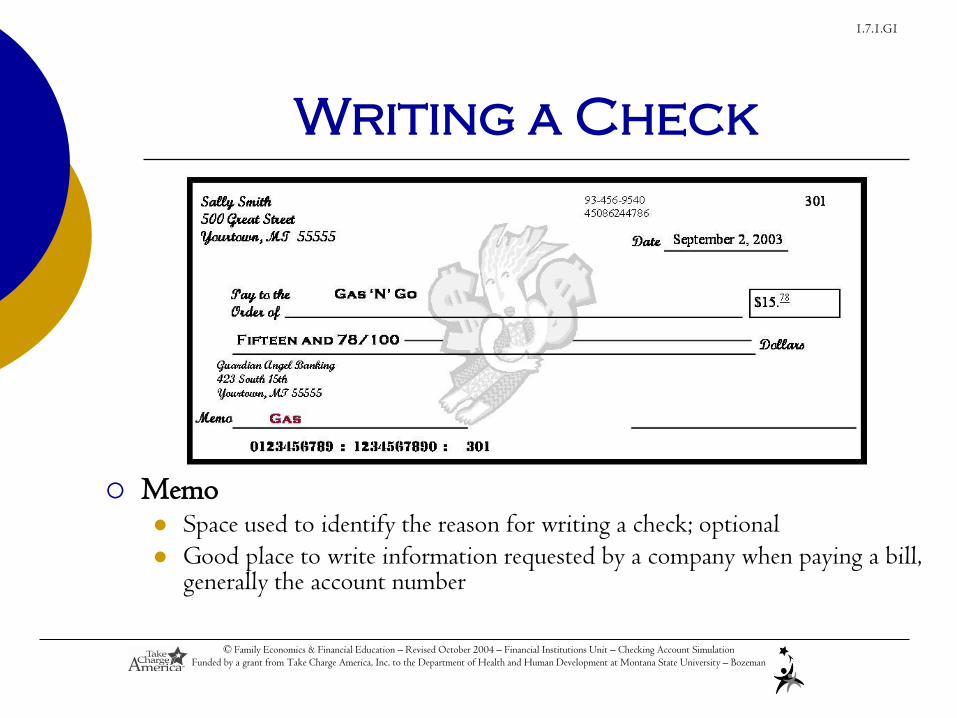

Writing a Check

Memo Space used to identify the reason for writing a check; optional

Good place to write information requested by a company when paying a bill, generally the account number

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

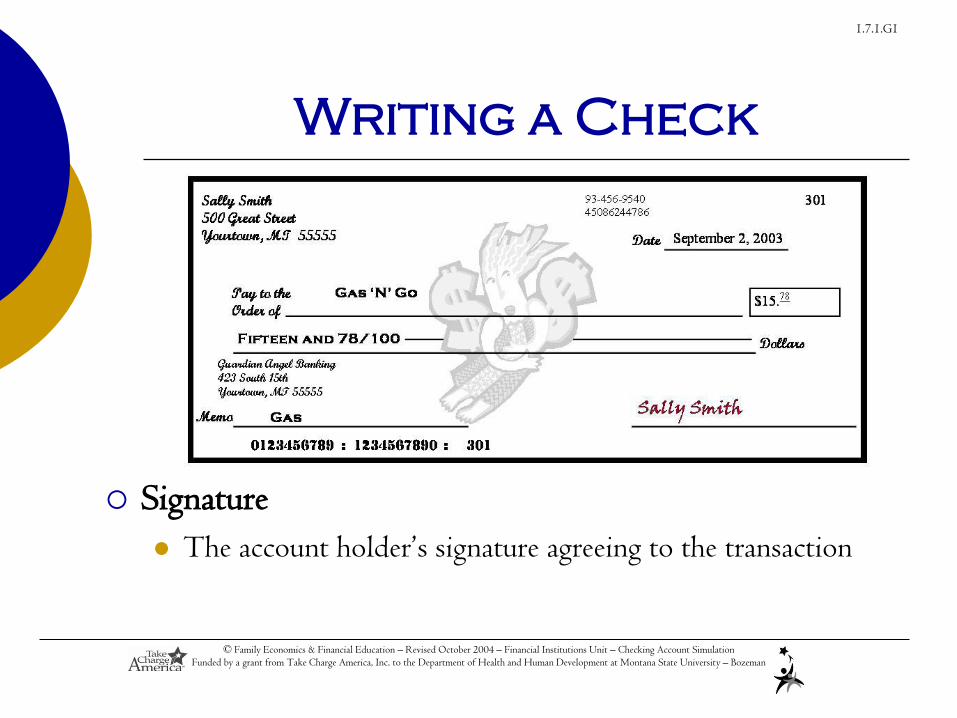

Writing a Check

Signature

The account holder’s signature agreeing to the transaction

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

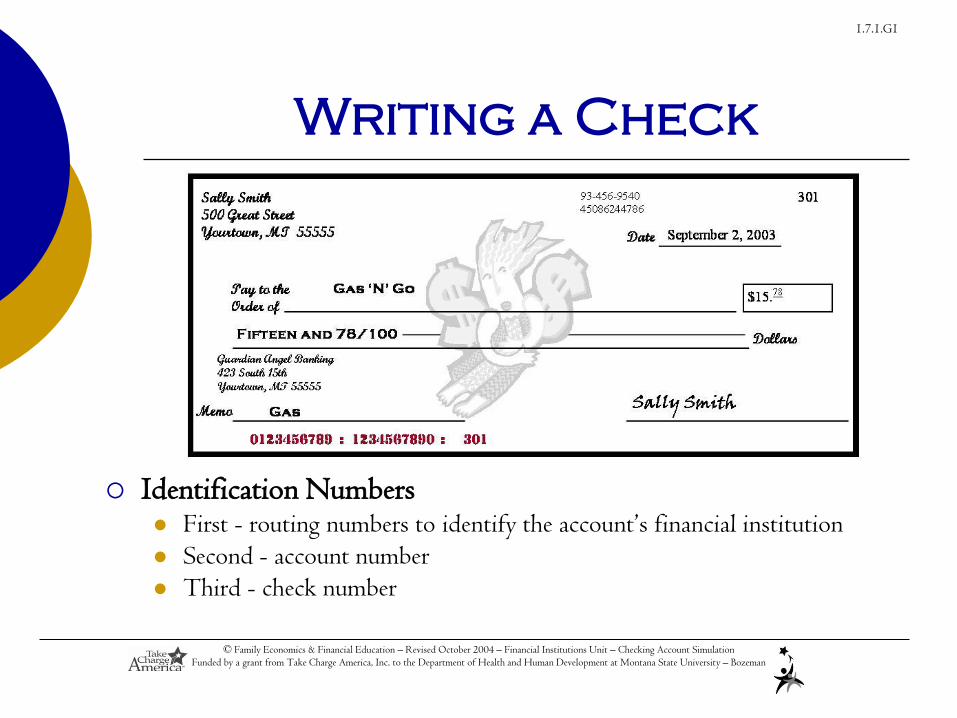

Writing a Check

Identification Numbers First - routing numbers to identify the account’s financial institution

Second - account number

Third - check number

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Check 21

Check Clearing for the 21st Century Act (Check 21)

Current trend that changes how money is withdrawn

from customers account and deposited into businesses

account

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

How Check 21 Works

Prior to Check 21

Paper checks physically moved from customer to business

to various banks and the transfer of money from

customer’s bank to business’ bank took days

After Check 21

Paper checks are scanned into a computer system at the

place of business and immediately returned to the

customer. This electronic copy of the check is called a

substitute check. The substitute check is then transferred

electronically to various banks and the transfer of money

customer’s bank to business’ bank takes hours

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Check Register

Place to immediately record all monetary

transactions for a checking account

Written checks, ATM withdrawals, debit card purchases,

deposits, fees, etc.

Used to keep a running balance of the account

Remember -

Record every transaction!

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

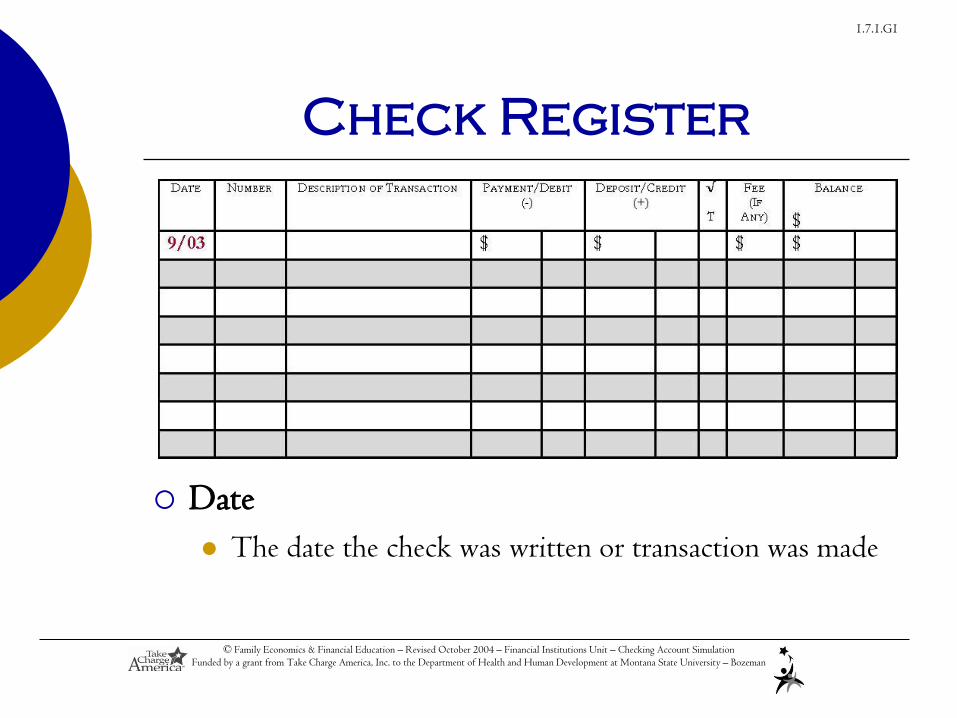

Check Register

Date

The date the check was written or transaction was made

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

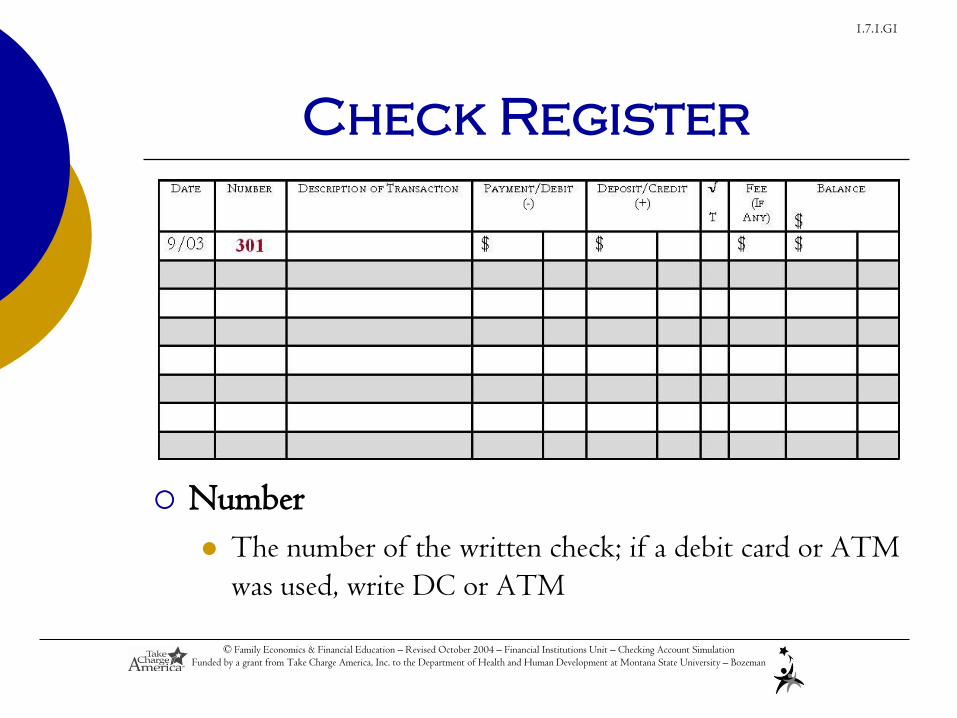

Check Register

Number

The number of the written check; if a debit card or ATM

was used, write DC or ATM

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

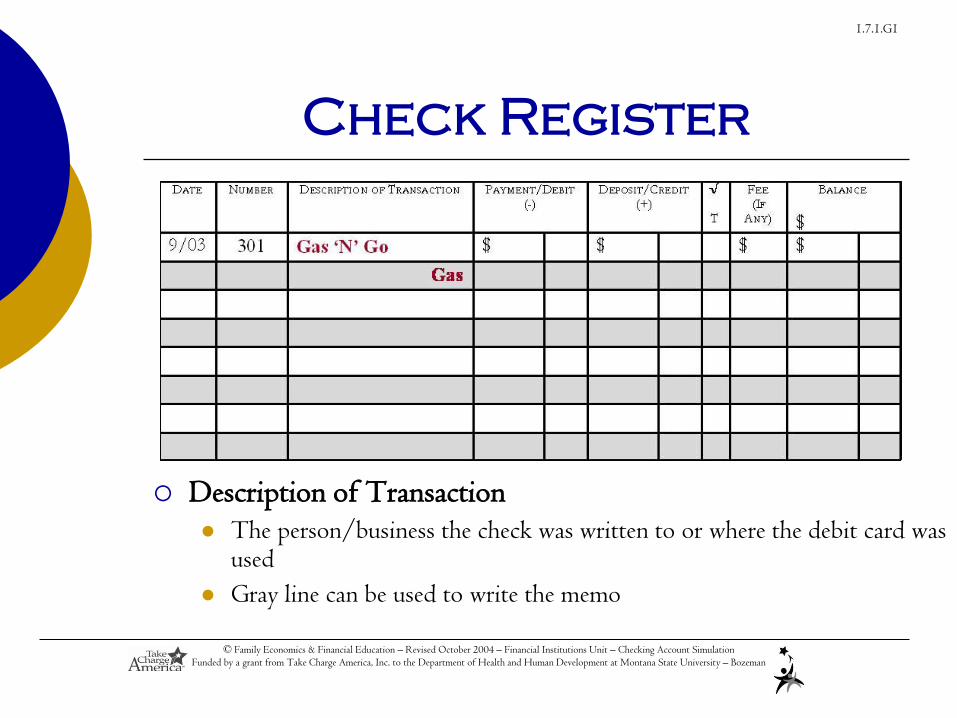

Check Register

Description of Transaction The person/business the check was written to or where the debit card was

used

Gray line can be used to write the memo

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

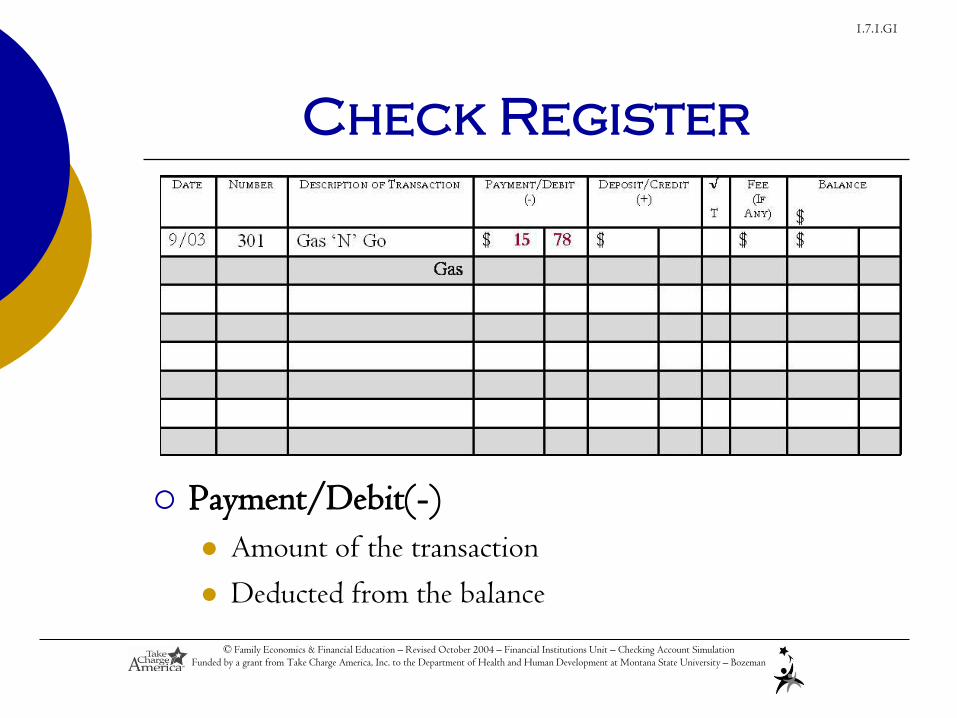

Check Register

Payment/Debit(-)

Amount of the transaction

Deducted from the balance

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

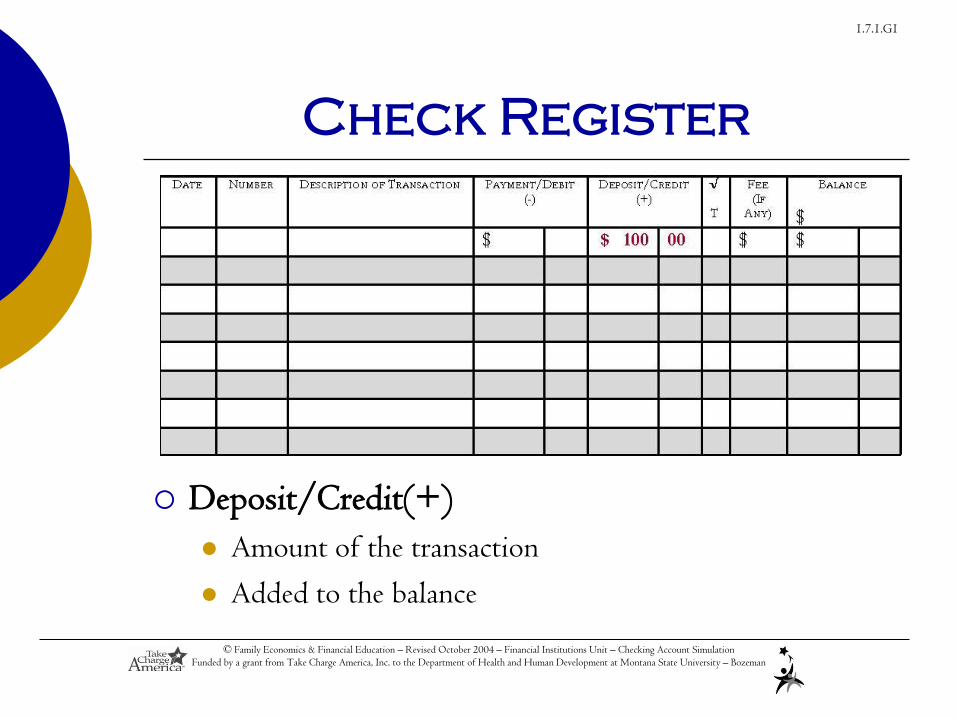

Check Register

Deposit/Credit(+)

Amount of the transaction

Added to the balance

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

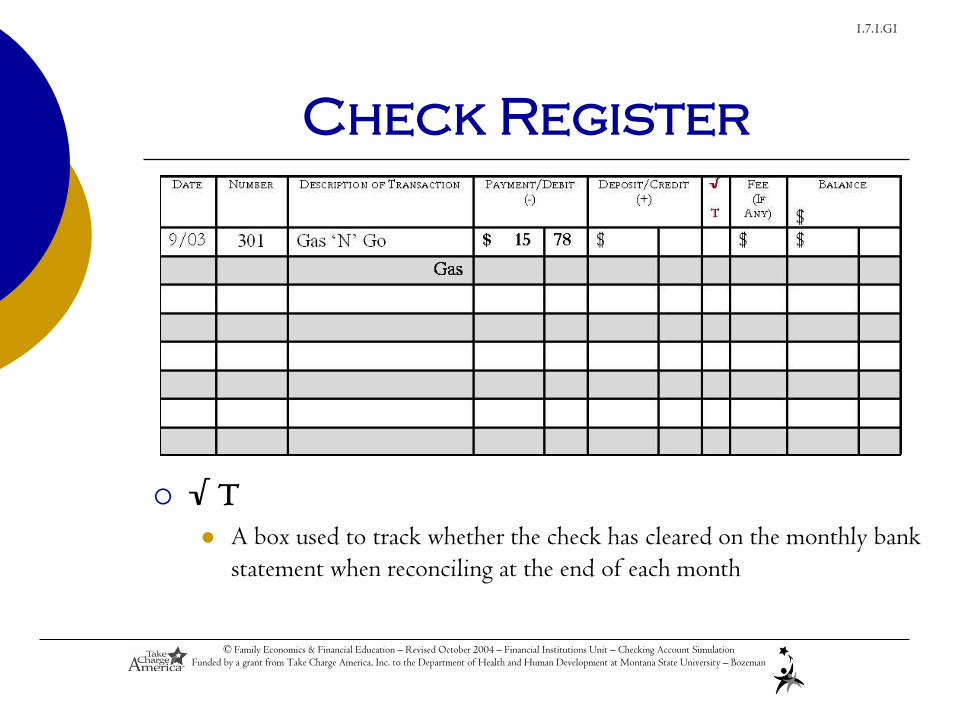

Check Register

√ T

A box used to track whether the check has cleared on the monthly bank

statement when reconciling at the end of each month

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

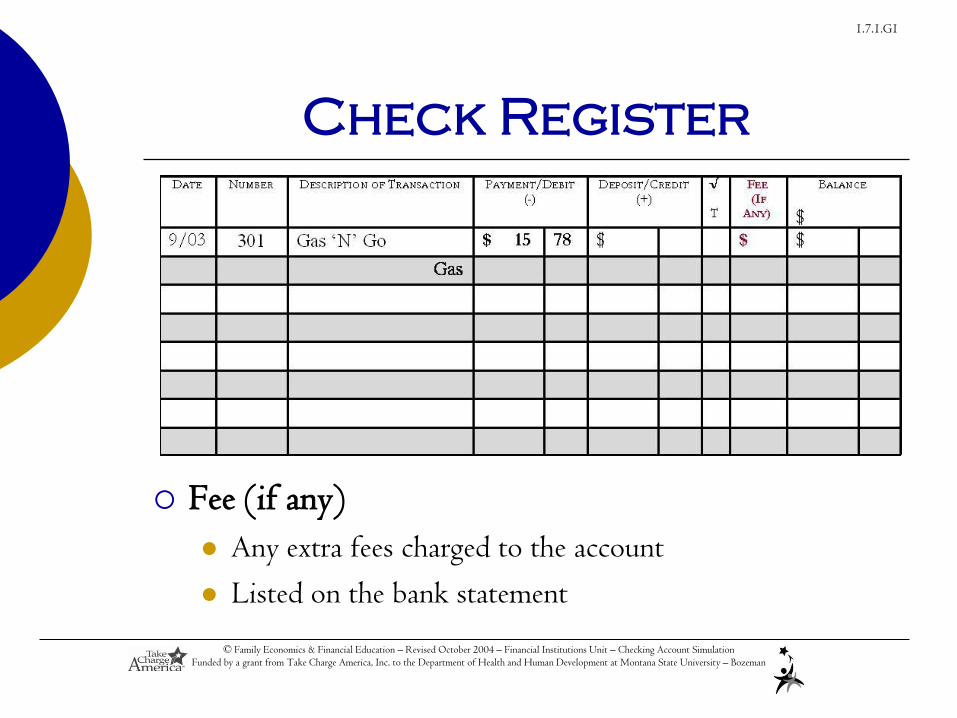

Check Register

Fee (if any)

Any extra fees charged to the account

Listed on the bank statement

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

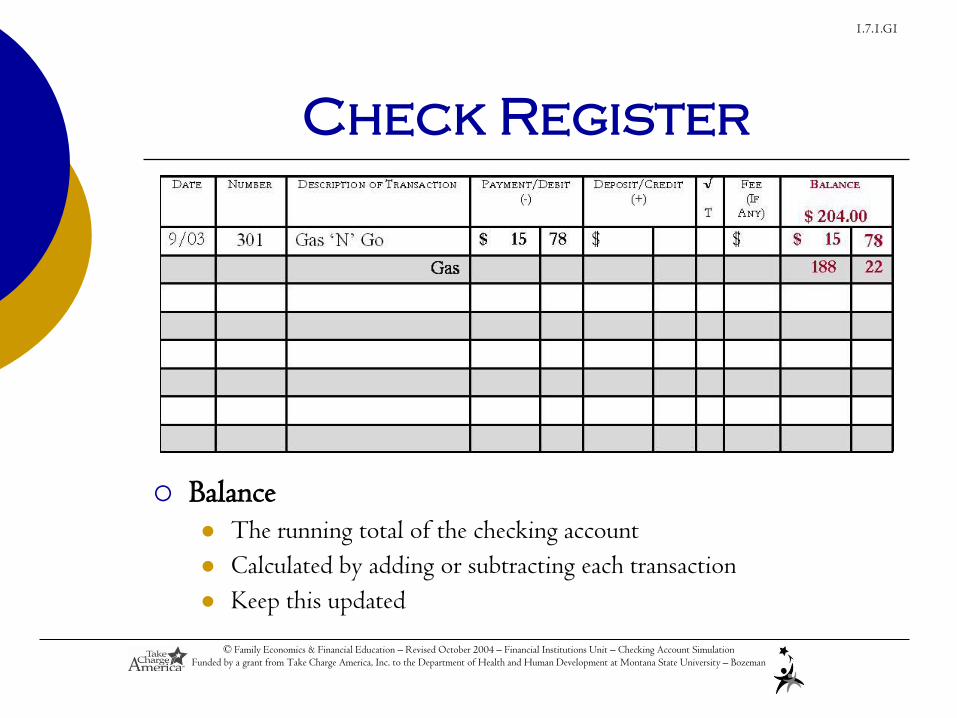

Check Register

Balance The running total of the checking account

Calculated by adding or subtracting each transaction

Keep this updated

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Monthly Statement

Lists each monetary transaction and the current account balance for a specified time period

Includes: Dates

Identification for each transaction (number or type, date, amount)

Transaction amounts for withdrawals and/or deposits

Interest earned (if applicable)

Fees or charges (if applicable)

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Monthly Statement

continued

If customer holds more than one account at the

same financial institution

May receive one statement for both

For example: a checking and a

savings account

May be mailed separately

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Reconciling a Checking

Account

Reconcile

Balance the checkbook register each month to the balance

shown on the statement

Do this every month to ensure the correct balance in

the checkbook

Knowing the correct balance can help to avoid bouncing

checks

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Steps for Reconciling

Make sure every transaction listed on the statement matches

the check register

Place a check next to each item once it has been double-

checked between the statement and register

Do this for both withdrawals and deposits

Identify any outstanding transactions in the check register

Items which have not cleared through the financial institution and

are not listed on the statement

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

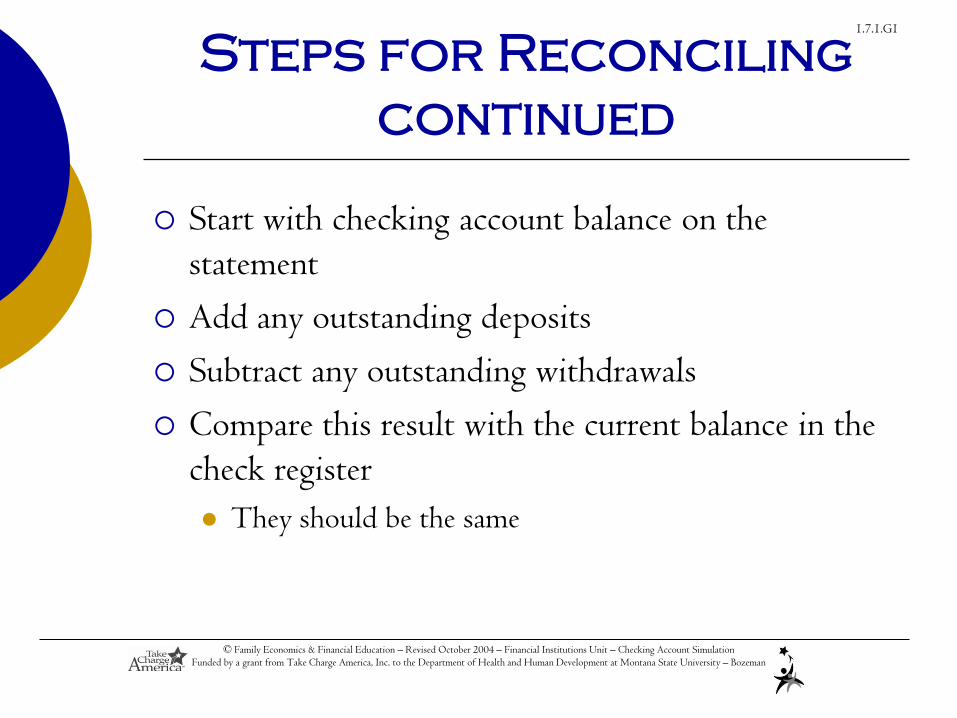

Steps for Reconciling

continued

Start with checking account balance on the

statement

Add any outstanding deposits

Subtract any outstanding withdrawals

Compare this result with the current balance in the

check register

They should be the same

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

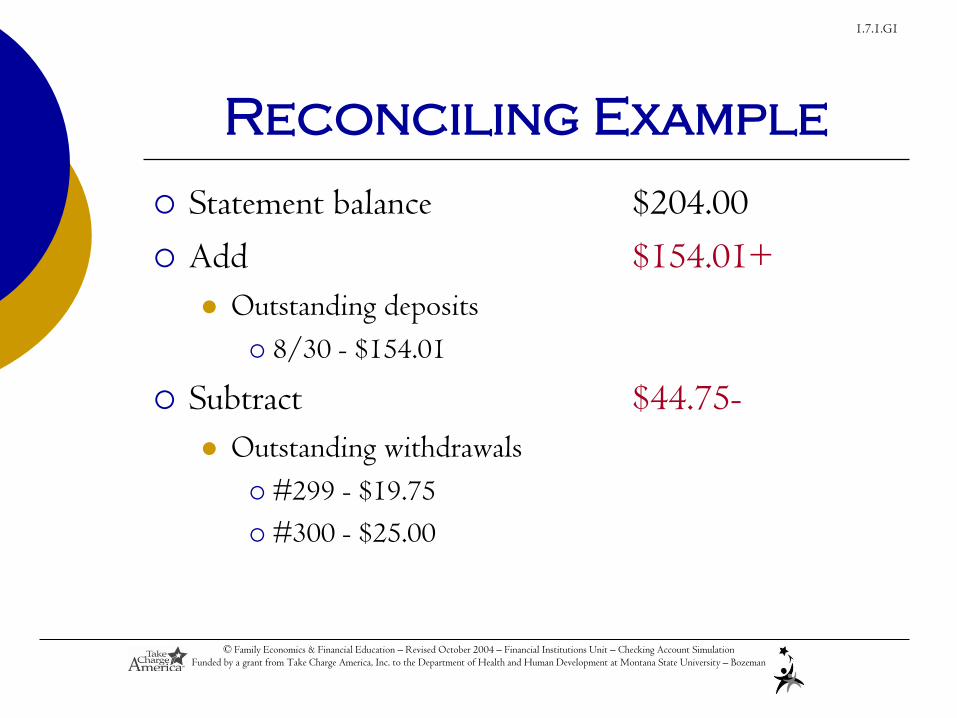

Reconciling Example

Statement balance $204.00

Add $154.01+

Outstanding deposits

8/30 - $154.01

Subtract $44.75-

Outstanding withdrawals

#299 - $19.75

#300 - $25.00

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Reconciling Example

continued

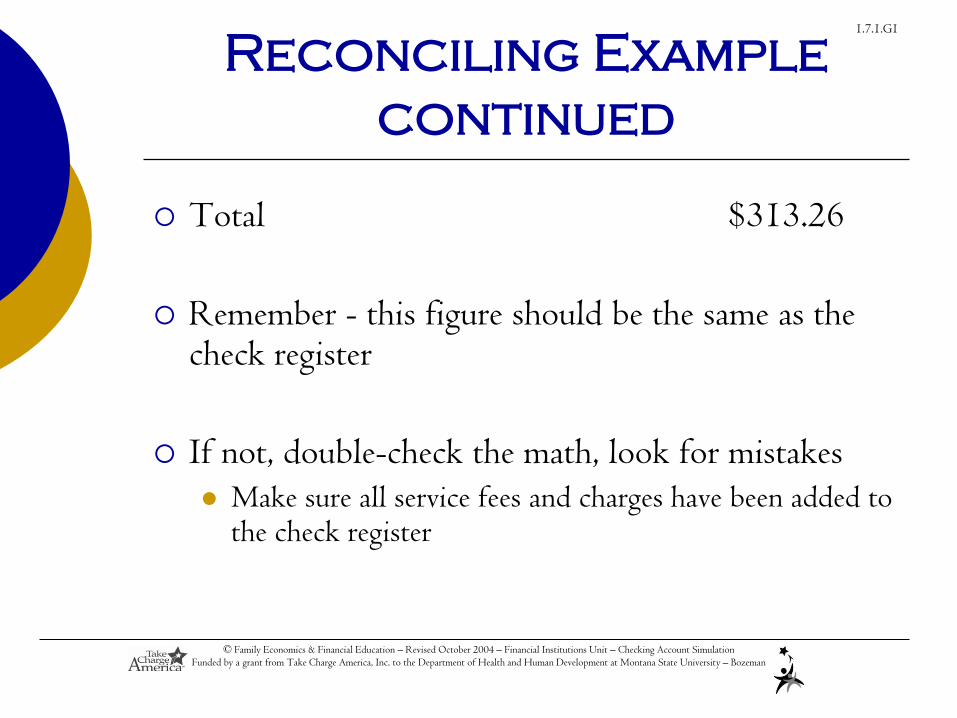

Total $313.26

Remember - this figure should be the same as the check register

If not, double-check the math, look for mistakes Make sure all service fees and charges have been added to

the check register

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Checking Account

Safety

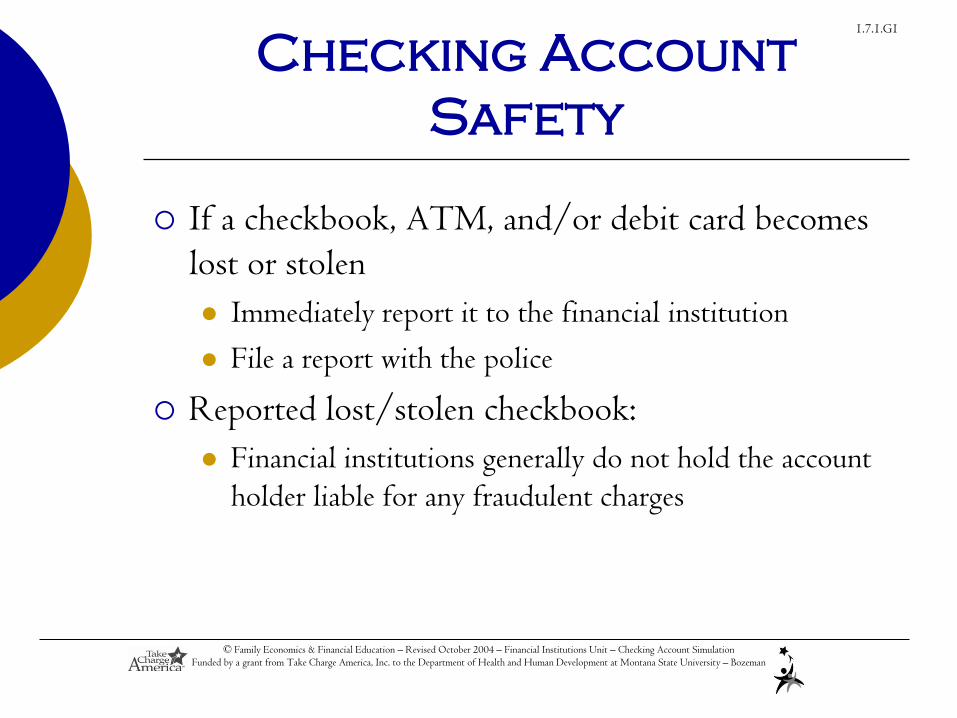

If a checkbook, ATM, and/or debit card becomes

lost or stolen

Immediately report it to the financial institution

File a report with the police

Reported lost/stolen checkbook:

Financial institutions generally do not hold the account

holder liable for any fraudulent charges

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Safety continued

Reported lost/stolen ATM/debit card:

Within 2 business days

Cardholder is only liable for $50.00

Longer than 2 business days

Could be liable for up to $500.00

Varies depending upon the financial institution

May not charge the account holder anything if the correct

steps were taken to report the lost/stolen card

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Conclusion

Research before choosing a financial institution and

checking account!

Follow the precautions to prevent checking account

fraud!

Report a lost/stolen checkbook, ATM, and/or debit

card immediately!

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

CHECKBOOK RECONCILIATION

FORM

The reconciliation form is used for balancing your

check register, or checkbook, and your checking

account.

This form is often found on the back of your

monthly bank statement. .

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

Reconciliation Form

Checks Outstanding Step 2

Check number Amount

Total

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

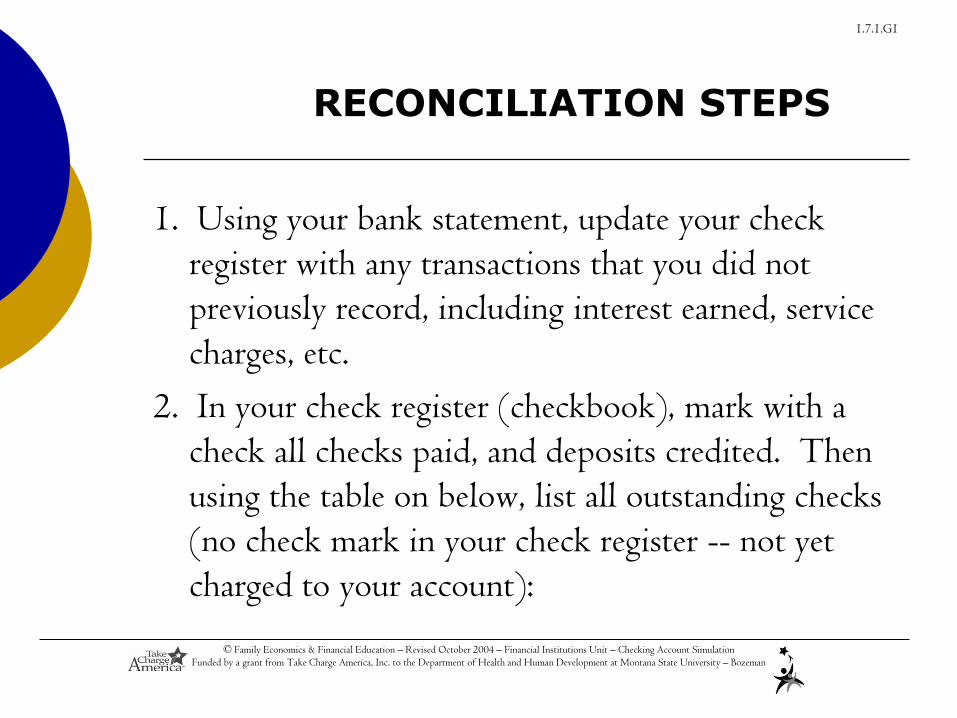

1. Using your bank statement, update your check

register with any transactions that you did not

previously record, including interest earned, service

charges, etc.

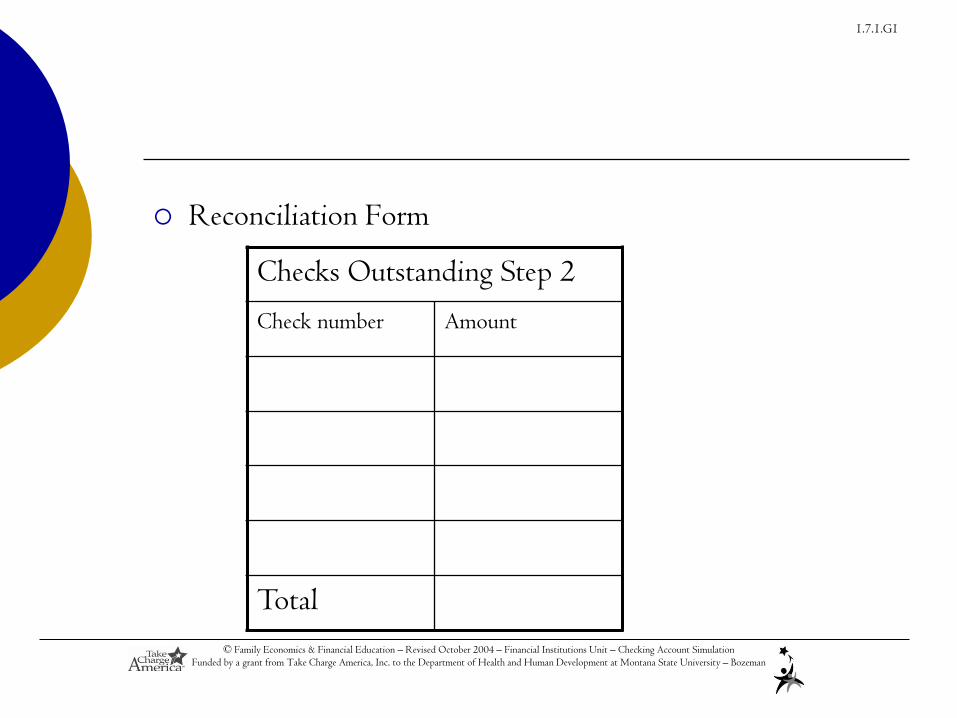

2. In your check register (checkbook), mark with a

check all checks paid, and deposits credited. Then

using the table on below, list all outstanding checks

(no check mark in your check register -- not yet

charged to your account):

RECONCILIATION STEPS

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

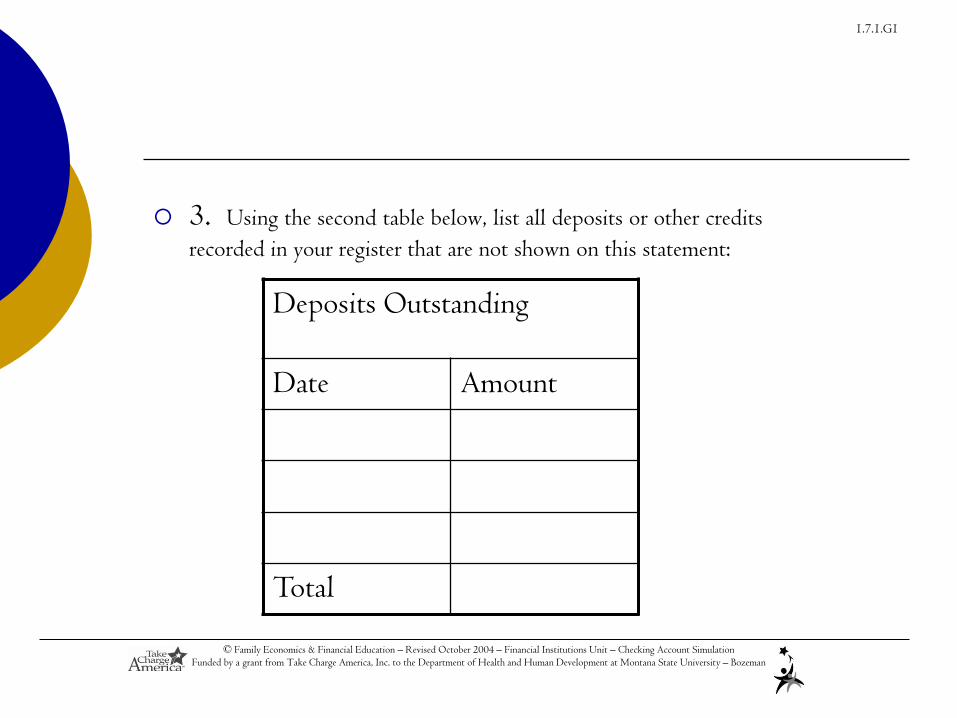

3. Using the second table below, list all deposits or other credits

recorded in your register that are not shown on this statement:

Deposits Outstanding

Date Amount

Total

© Family Economics & Financial Education – Revised October 2004 – Financial Institutions Unit – Checking Account Simulation

Funded by a grant from Take Charge America, Inc. to the Department of Health and Human Development at Montana State University – Bozeman

1.7.1.G1

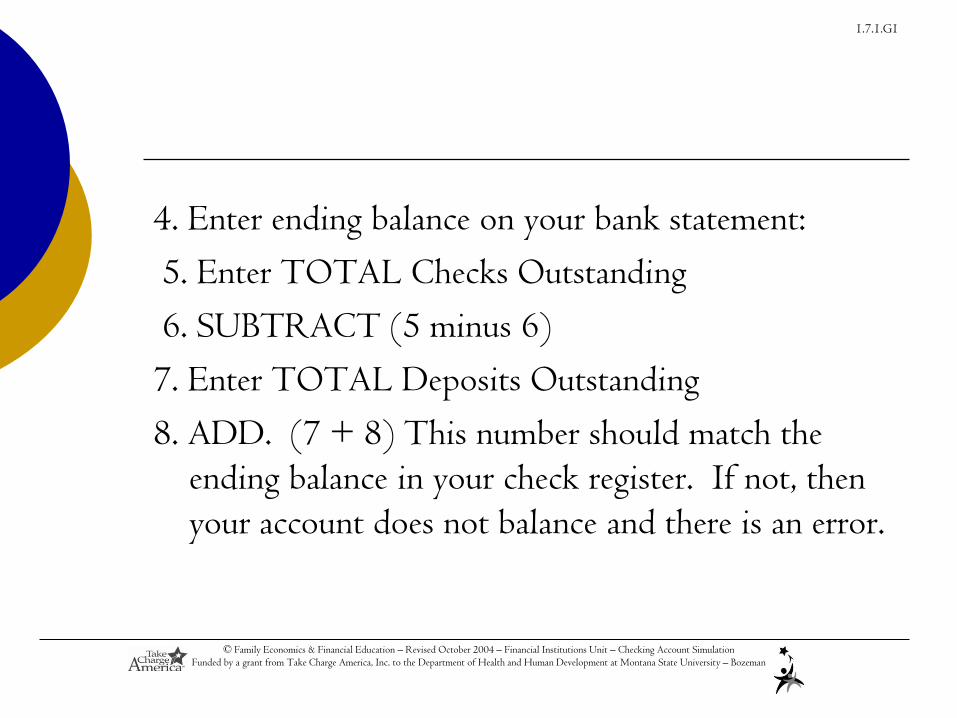

4. Enter ending balance on your bank statement:

5. Enter TOTAL Checks Outstanding

6. SUBTRACT (5 minus 6)

7. Enter TOTAL Deposits Outstanding

8. ADD. (7 + 8) This number should match the

ending balance in your check register. If not, then

your account does not balance and there is an error.

Related Documents