An Equal Opportunity Employer To help ensure equal access to programs, services and activities, the Office of Management & Finance will reasonably modify policies/procedures and provide auxiliary aids/services to persons with disabilities upon request. CITY OF PORTLAND OFFICE OF MANAGEMENT AND FINANCE Charlie Hales, Mayor Fred Miller, Chief Administrative Officer 1120 SW Fifth Ave., Suite 1250 Portland, Oregon 97204-1912 (503) 823-5288 FAX (503) 823-5384 TTY (503) 823-6868 Date: September 24, 2014 To: Transportation Needs and Funding Advisory Committee + Business Workgroup + Low‐Income and Non‐Profit Workgroup From: Fred Miller + Ruth Adkins RE: Report from Fred Miller and Ruth Adkins to City Council Summarizing Workgroup Recommendations Attached you will find the report that is a compilation of the recommendations and advice you have provided over the last three months. Given the diversity of interest groups and constituencies that you all represent, it is not surprising that several differences of opinion still exist. We feel that we have made considerable progress in identifying the areas of agreement and in moving the process forward. The current approach, outlined in the report, looks very different from the original proposal put in front of Council in May. That is a result of the time you have spent participating in these workgroups deliberating the merits and deficiencies of different funding mechanisms and implementation elements. We want to make sure that you have an opportunity to review the report and provide us with any comments you have by the end of September. We will compile those comments and provide them to City Council. There will be a City Council work session on October 23 rd . At that time, Council will weigh all the items included in the report as well as any additional communications you provide. We will keep you informed of the details of the work session when they become available. Prior to the work session, Council will be briefed on the report and PBOT will continue public outreach. We encourage you to talk with your constituency groups about the content of the report. Additionally, PBOT staff is available to present to your groups. As chairs of the advisory groups, we offer our sincere appreciation to all of you who volunteered your time and expertise throughout this process, as well as to the City staff who worked diligently to provide data, analysis and support to the committees. Please send your comments on the report by September 30 th to Jamie Waltz at [email protected] or call at 503‐823‐7101.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

An Equal Opportunity Employer To help ensure equal access to programs, services and activities, the Office of Management & Finance will reasonably

modify policies/procedures and provide auxiliary aids/services to persons with disabilities upon request.

CITY OF PORTLAND

OFFICE OF MANAGEMENT AND FINANCE

Charlie Hales, Mayor Fred Miller, Chief Administrative Officer

1120 SW Fifth Ave., Suite 1250 Portland, Oregon 97204-1912

(503) 823-5288 FAX (503) 823-5384 TTY (503) 823-6868

Date: September 24, 2014 To: Transportation Needs and Funding Advisory Committee + Business Workgroup + Low‐Income and

Non‐Profit Workgroup

From: Fred Miller + Ruth Adkins RE: Report from Fred Miller and Ruth Adkins to City Council Summarizing Workgroup

Recommendations

Attached you will find the report that is a compilation of the recommendations and advice you have provided over the last three months. Given the diversity of interest groups and constituencies that you all represent, it is not surprising that several differences of opinion still exist. We feel that we have made considerable progress in identifying the areas of agreement and in moving the process forward. The current approach, outlined in the report, looks very different from the original proposal put in front of Council in May. That is a result of the time you have spent participating in these workgroups deliberating the merits and deficiencies of different funding mechanisms and implementation elements. We want to make sure that you have an opportunity to review the report and provide us with any comments you have by the end of September. We will compile those comments and provide them to City Council. There will be a City Council work session on October 23rd. At that time, Council will weigh all the items included in the report as well as any additional communications you provide. We will keep you informed of the details of the work session when they become available. Prior to the work session, Council will be briefed on the report and PBOT will continue public outreach. We encourage you to talk with your constituency groups about the content of the report. Additionally, PBOT staff is available to present to your groups. As chairs of the advisory groups, we offer our sincere appreciation to all of you who volunteered your time and expertise throughout this process, as well as to the City staff who worked diligently to provide data, analysis and support to the committees.

Please send your comments on the report by September 30th to Jamie Waltz at [email protected] or call at 503‐823‐7101.

September 24, 2014

1

Our Streets Transportation FundingReport of Workgroup Recommendations

In May 2014, Mayor Hales and Commissioner Novick presented a proposal to City Council that would

generate new revenue to fund transportation maintenance and safety needs. After considerable input

from the community and interest groups, the proposal at Council was delayed with the intention of

refining it with additional public involvement.

In July 2014, the Portland Bureau of Transportation (PBOT) convened three committees to advise City

Council on a fair and reasonable approach to raising new revenue to fund outstanding transportation

maintenance and safety needs. The committees include the original Transportation Needs and Funding

Advisory Committee, the Business Workgroup and the Nonprofit and Low‐Income Workgroup:

Needs and Funding Advisory Committee

Chair: Fred Miller, Chief Administrative Officer for the City of Portland and Director of the Office of Management and Finance

Purpose: To advise on the residential portion of the fee and refine the project lists to clearly link new revenue with maintenance and safety projects. Additionally, to take recommendations from the Workgroups and propose final recommendations, captured in this report.

Members: Advisory Committee members are made up of business and neighborhood representatives and members of transportation interest groups. See Appendix for the list of members.

Business Workgroup

Chair: Fred Miller, Chief Administrative Officer for the City of Portland and Director of the Office of Management and Finance

Purpose: Businesses stakeholders advise on how to refine the business portion of the Transportation User Fee to minimize negative impacts to the business community.

Members: Working group members include representatives of organizations that represent large business‐related constituency groups across the City of Portland. See Appendix for the list of members.

Nonprofit and Low‐income Workgroup

Chair: Ruth Adkins, Policy Director for Oregon Opportunity Network

Purpose: Nonprofit and government partners advise on how to refine the funding mechanism to minimize the impacts to nonprofits and public institutions. This workgroup also advises on how low‐income discounts for the transportation funding proposal and discounts for existing water and sewer ratepayers can be more easily accessed by low‐income Portlanders.

September 24, 2014

2

Comment: There was significant interest from the workgroup on expanding the low‐income discount

for water and sewer bills to multi‐family properties. After a discussion on the issue, it

was determined that there are many complexities with reaching families in multi‐family

low‐income housing and in order to have a thoughtful and inclusive process, interest

groups will need more time to develop a recommendation. Workgroup members are

interested in continuing to explore the water and sewer discount issue with the City, after

the Our Streets PDX discussion has concluded.

Members: Working group members include representatives of organizations that represent nonprofit groups, institutions and low‐income advocacy groups. See Appendix for the list of members.

Areas of Agreement

The committees each met five times between July and September. As discussions progressed, there were

many points of agreement:

Maintenance and Safety: There is a considerable need for new funds to address the

maintenance needs of existing infrastructure as well as to address the known safety needs. A

three year project list has been discussed with the workgroups and in public forums and once

finalized, it will be included in the final proposal.

PBOT’s Budget: The PBOT budget is not “fat.” More “new” dollars are required to address the

problem. Earlier in the year, there were many questions about how PBOT spends its existing

revenue. PBOT held several budget education sessions with interest groups and there is

agreement that PBOT’s budget is not sufficient to meet the backlog of maintenance and safety

needs identified.

Revenue Generated: The original proposal of $53 million (split equally between business entities

and City of Portland residents) appeared too high to earn business community support. PBOT

provided calculations for a $40 million program that would generate $20 million from the

business sector and $20 million from the residential sector, which was the focus of the

committees.

Taxes on Low‐Income Earners: The groups felt that the proposal presented to City Council in May was too regressive. There is consensus for ensuring that any residential funding mechanism be designed to minimize negative impacts to low‐income residents.

Discount/exemption for nonprofit organizations: There is general support for providing some level of discount or exemption for nonprofit organizations since they provide services that benefit the community and higher payments could reduce these services.

Dedicated Fund: A Street Maintenance and Safety Fund should be created for the new revenues.

Committees stressed the need to ensure that those new revenues are being spent according to

the project lists that will be outlined in the final proposal. There was also a strong desire to

September 24, 2014

3

guarantee that current budget allocations for maintenance programs would continue to be

spent on those programs and new revenue would not supplant existing budgets.

Oversight Committee: An oversight committee should be established and should ensure that

new revenue is spent appropriately and as outlined in the program proposal. This committee

would monitor that:

o PBOT is achieving the project goals.

o The funds are dedicated specifically to the maintenance and safety program allocations

through the establishment of a Street Maintenance and Safety Fund.

o New revenue is not used to supplant expenditures on existing programs.

City Contribution: Committees agreed that support for a proposal depends on the City committing more resources to transportation needs. If fixing streets is important, the City should show its support by allocating more revenues to maintenance and safety. Council will have the opportunity in the fall budget adjustment process as well as in the 2015‐2016 budget process. Additionally, Council should support a package for new revenue at the State level.

Areas of Difference

There are several points on which the committees had different views or where committees raised

specific concerns. The items below capture the different thoughts provided by the three workgroups.

Maintenance and Safety Allocation Split: The Business Workgroup felt that the

“preponderance” of money should be spent on maintenance, especially on pavement

preservation. Although there was no consensus on a specific approach, the percentage split

recommended was a minimum of 2/3 spent on maintenance and 1/3 on safety. Some members

suggested that there are other funding mechanisms available for obtaining revenue to finance

safety projects.

The Nonprofit and Low‐income Workgroup emphasized the high value of safety projects and acknowledged the need for a “balanced” program between maintenance and safety. They also acknowledged that many projects PBOT completes have both maintenance and safety components. They did not want to be overly prescriptive, and emphasized a desire to ensure PBOT staff has flexibility to carry out the projects in a cost‐effective manner. They stated that they trusted the process that led to the development of the 53% maintenance and 47% safety split and felt that a division along those lines was balanced. They affirmed that geographic and racial equity, and the safety needs of the low‐income population, which are at a higher risk of being injured in a crash must be weighed in the project selection process. The Advisory committee was divided on how they felt the allocations should be weighted. Some

members echoed the thoughts from the Business Workgroup. Those that felt maintenance

should receive more funds did not disagree that there are safety needs that should be

September 24, 2014

4

addressed. Transportation safety and modal advocacy groups expressed concern that if there is

not enough money for safety in the proposal, then they cannot support it. They felt the

allocation should remain 50% maintenance and 50% safety. Overall, the Advisory committee did

not recommend a percentage split, but articulated that there should be consideration of the

economic return on investment.

City Contribution: Although the committees agreed that support for a proposal depends on the City committing more resources to transportation needs, there were different suggestions on how that could be accomplished. The Business Workgroup recommended that the proposal be amended from a 50‐50 split between residential and non‐residential to a 1/3‐1/3‐1/3 split between residents, business entities, and the City. The opportunities for funding include:

o City Council could allocate more revenue in the fall budget adjustment process as well as

in the 2015‐2016 budget. Additionally, Council should support a package for new

revenue at the State level.

o Dedicate $4.5 million dollars to PBOT from the General Fund during both

aforementioned budget processes.

o Both the Advisory Committee and the Needs and Funding Advisory Committees

supported the General Fund covering the collection and administrative costs for the

revenue mechanisms. There was also a desire across all committees that administrative

costs be minimized.

o Increase the allocation of the Utility License Fee (ULF) to transportation. Through past City Council actions, the ULF (via the General Fund) was diverted away from transportation and allocated to other City programs and services. While the Advisory Committee felt that public safety and parks are important services, the ULF has a nexus with the use of the transportation system. They would like to see the percentage of ULF over the forecasted amount increased above PBOT’s current $2.2 million cap. They did not specify a dollar amount.

o The Advisory Committee also wants to see a long‐term commitment to transportation

maintenance and safety from the City’s General Fund.

Inflation factor: There was discussion within each group about adding an inflation factor to the

rates. Some felt that if there is a six year sunset, then an inflation factor should not be included

and an increase in the rates could be made if the program is renewed. Others felt that we do not

want to follow the path of the gas tax, which has never been indexed to inflation. That is one of

the reasons why transportation requires additional revenue to meet unfunded safety and

maintenance needs. The Nonprofit and Low‐Income Workgroup recommended if an inflation

factor is included, that it be tied to the increase in average wages (Department of Housing and

Urban Development (HUD) MFI based on five year American Community Survey data) and not

to a Construction Cost Index.

Nonprofit Discounts: The Business Workgroup proposed a sliding scale discount for nonprofit

organizations, ranging from a 40% (smallest entities) to 10% (largest) discount. There was also

September 24, 2014

5

discussion in all groups as to whether the very largest nonprofits (such as hospitals) should not

receive a discount, but there was no clear consensus.

The Nonprofit and Low‐income Workgroup emphasized that nonprofits provide a public benefit

and noted that government has already determined this public benefit merits tax‐exempt

status. That said, there was interest in helping contribute to meet the City’s safety and

maintenance needs. At one point, the group proposed an exemption from the Business Entity

Flat Fee for all non‐profits below $1 million in revenue, but ultimately recommended a 50%

discount on all nonprofit organizations. They acknowledged the complexities of defining

different discounts or exemptions for nonprofits based on number of employees, revenue,

and/or mission. Given the desire to minimize both compliance burden and administrative

complexity, they settled on the 50% discount for all nonprofit organizations.

Progressivity of Taxes: While there was overall agreement that the lowest income earners

should be exempt from paying the residential portion of the fee, the Business Workgroup

expressed a desire that residential funding be fair and reasonable for higher incomes and felt

that the proposal of a $100 or a $200 cap on the highest income earners was too much.

The Nonprofit and Low‐Income Workgroup maintained the core value that the fee should

exempt Portland residents who are struggling to make ends meet. Committee members pointed

out that Increasing housing costs and lack of affordable housing are displacing mid‐ and lower‐

income residents who now must travel farther to work, and the growth in low‐wage jobs has

contributed to rising poverty and income inequality. Their position is that the lowest income

earners should be exempt from paying, that middle income earners should pay a moderate

amount and the highest income earners should pay the most.

They agreed that, for the residential tax, the bracketed capped tax was the preferred method

with the cap being $200. If the bracketed rates change from the approach outlined in the

appendix, the most important value to the group is that the lowest income groups be exempt

from the tax as specified in the proposed residential mechanism.

Sunset Provision: The Business Workgroup favored an approach where PBOT would establish a

six year funding program. After six years, from the point at which PBOT begins collecting

revenue from all new sources, City Council would refer the funding mechanism(s) to the next

election for a public vote. The public would vote on the continuation of the funding program.

The Nonprofit and Low‐income Workgroup does not support a sunset with automatic referral to

voters six years after launch of the program. Instead, this group would support a sunset in which

the oversight committee would be required to review program performance and make

recommendations to Council, at which point the Council would decide whether or not to extend

the program. Some in this workgroup felt that if there was a progressive proposal, there should

not be a sunset. There was also a suggestion for extending a sunset to ten years, if there is to be

a sunset.

September 24, 2014

6

Funding Mechanisms

In May, City Council heard testimony on a transportation funding proposal where $53 million in revenue

would be generated by a Transportation User Fee. This mechanism tied number of trips to a fee that was

to be paid for by both residential and non‐residential properties. After that proposal was delayed,

Transportation held two Town Halls in late June to solicit public input on alternative mechanisms for

generating new revenue. Several weeks later, the Workgroups began their deliberation to refine the

proposal. In addition to considering the Transportation User Fee, the Workgroups weighed the

recommendations from the Town Halls and other funding mechanisms that previous PBOT‐sponsored

committees, such as Transportation’s Financial Task Force, had proposed. Some of those funding

mechanisms considered included: income tax; business gross receipts tax; and general obligation bonds

paid for by property tax.

As a result of all the workgroup meetings, three mechanisms were determined the most viable. Below is

a summary of the details of the residential and business mechanisms.

Residential Mechanisms

Two mechanisms were discussed on the residential side: a Bracketed Capped Tax and a Progressive

Income Tax with a Cap. These two tax mechanisms have the same underlying principles in that they are

based upon a tax filer’s adjusted gross income. The taxes are no longer directly linked to trips or usage of

the system, as defined by the Institute of Traffic Engineers (ITE) Trip Generation manual, but have a

direct connection to an individual’s ability to pay. This methodology addresses the concerns raised in

response to the May proposal and the input from the workgroups that low‐income were adversely

impacted.

There was more support among the committees for the Bracketed Capped Tax, as it is easier and thus

less costly to administer since it is a flat amount per income bracket. The biggest difference among the

groups was how much the highest income earners should be paying. The Nonprofit and Low‐income

Workgroup felt that the higher income earners should be paying a monthly equivalent of $200, or close

to it. The Business Workgroup felt that that rate was too high and they preferred the $20 cap.

All workgroups agreed that the lowest income earners should be exempt from paying. The median family

income (MFI) in Portland‐Vancouver Metro area for a family of two is $55,520, based on data collected

from the 5‐year American Community Survey and adjusted with the Consumer Price Index. Based on

input from housing and social services experts, this approach exempts households from the tax who are

living on income at or less than half of the MFI, which for the purposes of simplification has been

rounded to $30,000 a year for joint tax filers.

Bracketed Capped Tax

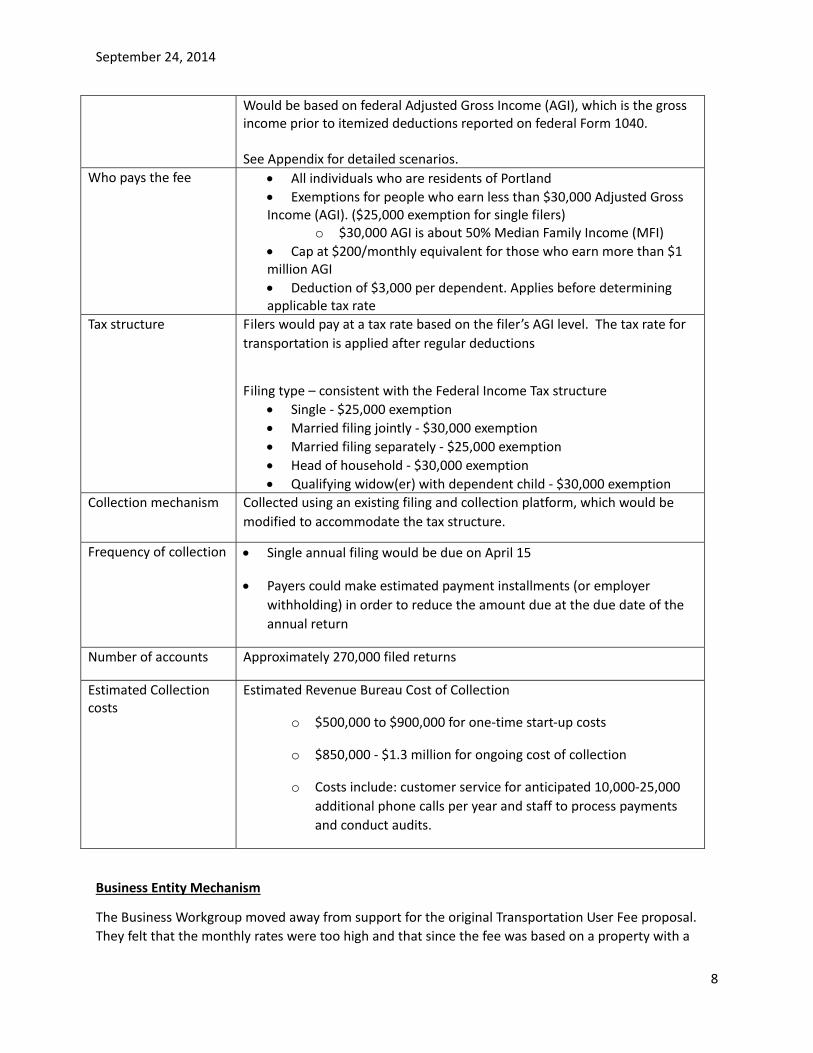

Bracketed Capped Tax A flat amount of revenue collected based upon bracketed Adjusted Gross Income (AGI) levels. Would be based on federal Adjusted Gross Income (AGI), which is the gross

September 24, 2014

7

income prior to itemized deductions reported on federal Form 1040.

See Appendix for detailed scenarios.

Who pays the fee All individuals who are residents of Portland

Exemptions for people who earn less than $30,000 Adjusted Gross Income (AGI). ($25,000 exemption for single filers)

o $30,000 AGI is about 50% Median Family Income (MFI)

Deduction of $3,000 per dependent. Applies before determining applicable tax rate.

There are three alternative monthly caps that have been proposed:

$20, $100, $200.

Tax structure Filers would pay at a tax rate based on the filer’s AGI level. The tax rate for

transportation is applied after regular deductions.

Filing type – consistent with the Federal Income Tax structure

Single ‐ $25,000 exemption

Married filing jointly ‐ $30,000 exemption

Married filing separately ‐ $25,000 exemption

Head of household ‐ $30,000 exemption

Qualifying widow(er) with dependent child ‐ $30,000 exemption

Collection mechanism Collected using an existing filing and collection platform, which would be

modified to accommodate the tax structure.

Frequency of collection Single annual filing would be due on April 15

Payers could make estimated payment installments (or employer

withholding) in order to reduce the amount due at the due date of the

annual return

Number of accounts Approximately 270,000 filed returns

Estimated Collection costs

Estimated Revenue Bureau Cost of Collection

o $500,000 to $900,000 for one‐time start‐up costs

o $850,000 ‐ $1.3 million for ongoing cost of collection

o Costs include: customer service for anticipated 10,000‐25,000

additional phone calls per year and staff to process payments

and conduct audits.

Progressive Income Tax with a Cap

Progressive Income Tax with a Cap

An income tax applied to City of Portland tax filers.

September 24, 2014

8

Would be based on federal Adjusted Gross Income (AGI), which is the gross income prior to itemized deductions reported on federal Form 1040. See Appendix for detailed scenarios.

Who pays the fee All individuals who are residents of Portland

Exemptions for people who earn less than $30,000 Adjusted Gross Income (AGI). ($25,000 exemption for single filers)

o $30,000 AGI is about 50% Median Family Income (MFI)

Cap at $200/monthly equivalent for those who earn more than $1 million AGI

Deduction of $3,000 per dependent. Applies before determining applicable tax rate

Tax structure Filers would pay at a tax rate based on the filer’s AGI level. The tax rate for

transportation is applied after regular deductions

Filing type – consistent with the Federal Income Tax structure

Single ‐ $25,000 exemption

Married filing jointly ‐ $30,000 exemption

Married filing separately ‐ $25,000 exemption

Head of household ‐ $30,000 exemption

Qualifying widow(er) with dependent child ‐ $30,000 exemption

Collection mechanism Collected using an existing filing and collection platform, which would be

modified to accommodate the tax structure.

Frequency of collection Single annual filing would be due on April 15

Payers could make estimated payment installments (or employer

withholding) in order to reduce the amount due at the due date of the

annual return

Number of accounts Approximately 270,000 filed returns

Estimated Collection costs

Estimated Revenue Bureau Cost of Collection

o $500,000 to $900,000 for one‐time start‐up costs

o $850,000 ‐ $1.3 million for ongoing cost of collection

o Costs include: customer service for anticipated 10,000‐25,000

additional phone calls per year and staff to process payments

and conduct audits.

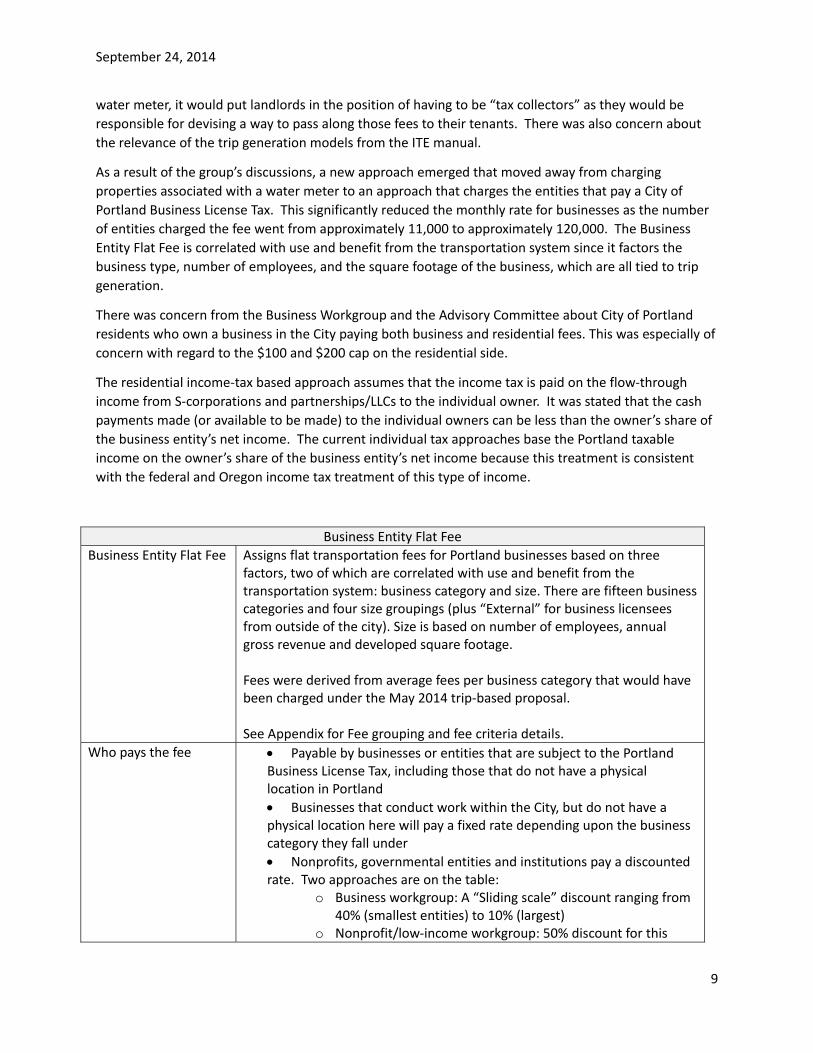

Business Entity Mechanism

The Business Workgroup moved away from support for the original Transportation User Fee proposal.

They felt that the monthly rates were too high and that since the fee was based on a property with a

September 24, 2014

9

water meter, it would put landlords in the position of having to be “tax collectors” as they would be

responsible for devising a way to pass along those fees to their tenants. There was also concern about

the relevance of the trip generation models from the ITE manual.

As a result of the group’s discussions, a new approach emerged that moved away from charging

properties associated with a water meter to an approach that charges the entities that pay a City of

Portland Business License Tax. This significantly reduced the monthly rate for businesses as the number

of entities charged the fee went from approximately 11,000 to approximately 120,000. The Business

Entity Flat Fee is correlated with use and benefit from the transportation system since it factors the

business type, number of employees, and the square footage of the business, which are all tied to trip

generation.

There was concern from the Business Workgroup and the Advisory Committee about City of Portland

residents who own a business in the City paying both business and residential fees. This was especially of

concern with regard to the $100 and $200 cap on the residential side.

The residential income‐tax based approach assumes that the income tax is paid on the flow‐through

income from S‐corporations and partnerships/LLCs to the individual owner. It was stated that the cash

payments made (or available to be made) to the individual owners can be less than the owner’s share of

the business entity’s net income. The current individual tax approaches base the Portland taxable

income on the owner’s share of the business entity’s net income because this treatment is consistent

with the federal and Oregon income tax treatment of this type of income.

Business Entity Flat Fee

Business Entity Flat Fee Assigns flat transportation fees for Portland businesses based on three factors, two of which are correlated with use and benefit from the transportation system: business category and size. There are fifteen business categories and four size groupings (plus “External” for business licensees from outside of the city). Size is based on number of employees, annual gross revenue and developed square footage. Fees were derived from average fees per business category that would have been charged under the May 2014 trip‐based proposal. See Appendix for Fee grouping and fee criteria details.

Who pays the fee Payable by businesses or entities that are subject to the Portland Business License Tax, including those that do not have a physical location in Portland

Businesses that conduct work within the City, but do not have a physical location here will pay a fixed rate depending upon the business category they fall under

Nonprofits, governmental entities and institutions pay a discounted rate. Two approaches are on the table:

o Business workgroup: A “Sliding scale” discount ranging from 40% (smallest entities) to 10% (largest)

o Nonprofit/low‐income workgroup: 50% discount for this

September 24, 2014

10

category

Collection mechanism The fee would be administered using the existing Portland Business License

filing and collection platform, which would be modified to accommodate

the fee structure.

Frequency of collection Single annual filing would be due when the Federal and Oregon tax

returns are due (generally April 15)

Payers could make estimated payment installments in order to reduce

the amount due at the due date of the annual return

How much do businesses pay?

Fees range from $2.50 per monthly equivalent to $120 per monthly equivalent and per location associated with the business, depending upon the business type, annual gross revenue and developed square footage (Since parameters and criteria have not been finalized, fees may change slightly depending upon the final proposal)

Number of accounts Fees would be spread across approximately 120,000 entities, including: o 65,000 businesses with locations in Portland o 30,000 businesses with no locations in Portland o 25,000 non‐profits (including churches, schools and government

entities)

Estimated Collection costs

Estimated Revenue Bureau Collection Costs

o $500,000 to $850,000 for one‐time start‐up costs

o $1.7 ‐ $2.2 million for ongoing cost of collection

o Costs include: creating new schedules for tax returns, customer

service for anticipated 10,000‐15,000 additional phone calls per

year and staff to process payments and conduct audits.

Process from Here

This report contains the thoughts of the three committees, which served to provide advice on how to

refine the original proposal presented in May 2014. Council offices will be briefed on the contents of this

report by City staff in advance of a Council work session scheduled for October 23, 2014. At that time,

Council will discuss the items outlined in this report, specifically focusing on the policy areas that were

not resolved. PBOT staff will be meeting with constituency and interest groups discussing the outcomes

of the workgroups. Additionally, an Open House and public outreach will be conducted. On November

12, 2014, Council will hear the first reading of the final proposal and have the opportunity to hear public

testimony. November 19, 2014 Council is scheduled to vote on the proposal.

1

Appendix: Members of Our Streets Committees and Workgroups

Needs and Funding Advisory Committee Chair: Fred Miller, Chief Administrative Officer, City of Portland Office of Management and Finance

Beebe, Craig City Club of Portland

Collier, Corky Columbia Corridor Association

Dodds, Marie AAA

Dunn, Debra Oregon Trucking Association

Fitzgerald, Marianne SWNI

Fitzpatrick, Maxine Portland Community Reinvestment Initiatives, Inc.

Foren, Leslie Elders in Action

Funk, Deane Portland General Electric

Hagerbaumer, Chris Oregon Environmental Council

Haynes, Marion Portland Business Alliance

Mickelberry, Noel Oregon Walks

Morton, Matt NAYA

Nettekoven, Linda SE Uplift

Ostar, Jonathan OPAL – Environmental Justice Oregon

Rhodes, Vic Rhodes Consulting, Inc.

Sadowsky, Rob Bicycle Transportation Alliance

Tetteh, Mychal Community Cycling Center

Treat, Leah Director, Portland Bureau of Transportation

VanderVeer, Joe Portland Commission on Disability

Zalkow, Dan Portland State University

2

Business Workgroup Chair: Fred Miller, Chief Administrative Officer, City of Portland Office of Management and Finance

Alfano, Brian Unitus Credit Union

Chessar, J. Benjamin NAIOP – Commercial Real Estate Development Association

Coleman, Robert Stewart Sokol and Larkin LLC

Dailey, Melinda Northwest Utility Contractors Association

Dunn, Debra Oregon Trucking Association

Eliason, Mike Associated General Contractors

Ferree, Steve Small Business Advisory Council

Goodman, Greg Downtown Development Group

Haynes, Marion Portland Business Alliance

Hoell, Heather Venture Portland

Micetic, Matthew Red Castle Games

Miller, Sean NW Grocery Association

Oxley, Chris Portland Trail Blazers

Perry, Bill ORLA – Oregon Restaurant and Lodging Assoc.

Polonsky, Jonathon Plaid Pantry

Ross, Kelly NAIOP – Commercial Real Estate Development Association

Sanderson, Ann Odango! Hair Studio

Simpson, Tom Standard Insurance Company

Steward, Susan BOMA – Building Owners and Managers Association

Wax, Ellen M Working Waterfront Coalition

Williams, Terri City of Portland Revenue Bureau

3

Non‐Profit and Low‐Income Workgroup Chair: Ruth Adkins, Policy Director, Oregon Opportunity Network

Blackburn, Ed Central City Concern

Blake, Brad Portland Water Bureau

Castillo, Linda Latino Network

Buri, Justin Community Alliance of Tenants

Herrigel, Joann Elders in Action

Glass, Jenny Rosewood Initiative

Gray, Karen Parkrose School District

Gregg, Bonnie NE Community Center

Hagins, Felisa Service Employees International Union Local 503

Harrison, Michael OHSU

Imse, Deborah Multifamily NW

Jolin, Mark JOIN

Koch, Kathy Portland Water Bureau

Koehler, Anneliese Oregon Food Bank

Komar, Patt David Douglas School District

Lahsene, Susie Port of Portland

Leslie, David Ecumenical Ministries of Oregon

Li, Mary Multnomah County Department of County Human Services

Mena, Javier Portland Housing Bureau

Messinetti, Steve Habitat for Humanity Portland/Metro East

4

Miller, John Oregon ON

Montagriff, Kim NE Community Center

Ostar, Jonathon OPAL Environmental Justice Oregon

Schmanski, Sonia Office of Commissioner Fish

Smith, Jill Home Forward

Friesen‐Strang, Elaine AARP

VanderVeer, Joe Portland Commission on Disability

Williams, David Portland Public Schools

Williams, Terri City of Portland Revenue Bureau

Wynde, David Portland Public Schools

Zalkow, Dan Portland State University

1

(1) Progressive Income Tax Tax Rate

$0 ‐ $30K 0.07%

>$30K‐$72K 0.11%

>$72K‐$146K 0.18%

>$146K‐$223K 0.21%

>$223K‐$398K 0.24%

>$398K‐$450K 0.26%

> $450K 0.29%

Residential Mechanisms

(2) 5 Brackets

Capped Tax≤ $30K exempt,

$20 cap

$0 ‐ $30K $0.0

> $30K‐$50K $6.0

> $50K‐$100K $12.0

> $100K‐$250K $15.0

> $250K $20.0

(3) 8 Brackets Capped Tax

e≤ $30K exempt,

$100 cap≤ $30K exempt,

$200 cap

$0 ‐ $30K $0.0 $0.0

> $30K‐$50K $2.0 $1.5

> $50K‐$75K $4.0 $4.0

> $75K‐$100K $8.0 $8.0

> $100K‐$175K $16.0 $12.0

> $175K‐$250K $32.0 $25.0

> $250K‐$500K $64.0 $85.0

> $500K $100.0 $200.0

9/24/2014

Example Income

Levels≤ $30K exempt,

$200 cap

≤ $30K exempt,

$20 cap

≤ $30K exempt,

$100 cap

≤ $30K exempt,

$200 cap

Adjusted Gross Income (AGI)

b

(1) Progressive Income Tax - All

(Cap)c , d

(2) 5 Brackets Capped Tax

e(3a) 8 Brackets Capped Tax

e(3b) 8 Brackets Capped Tax

e

$15,000 $0.00 $0.00 $0.00 $0.00

$20,000 $0.00 $0.00 $0.00 $0.00

$30,000 $0.00 $0.00 $0.00 $0.00

$40,000 $2.55 $6.00 $2.00 $1.50

$50,000 $3.36 $6.00 $2.00 $1.50

$75,000 $5.58 $12.00 $4.00 $4.00

$87,000 $6.79 $12.00 $8.00 $8.00

$100,000 $8.13 $12.00 $8.00 $8.00

$125,000 $11.87 $15.00 $16.00 $12.00

$150,000 $15.76 $15.00 $16.00 $12.00

$200,000 $23.53 $15.00 $32.00 $25.00

$250,000 $32.18 $15.00 $32.00 $25.00

$400,000 $61.10 $20.00 $64.00 $85.00

$500,000 $81.67 $20.00 $64.00 $85.00

$1,000,000 $200.00 $20.00 $100.00 $200.00a Example based on Married, Filing Jointly with adjusted AGI ≤ $30K exempt from fee; Single filers ≤ $25K exempt

b 50% MFI for a 2‐person HH is about $30,000

c AGI of about $1 million reaches $200/month cap

d Tax schedule per 2013 Federal marginal tax rate schedule for joint filers

e Flat fee structure using the income tax platform

Married, Filing Jointly ‐ 2 Person Householda

Residential $20 Million Gross Revenue Scenario ‐

Example Monthly Equivalent Tax

***DRAFT***

2

Business Entity Mechanism – Sample Rate Sheet

Portland Business Entity Flat Fee (BFF)Sample Rate Table9/24/2014

Must meet 2 of 3 criteria to determine fee

(excluding Group A which requires all 3) Original Proposal

Nonprofit Discount

"Sliding Scale"

Approach

50% Nonprofit

Discount Approach

Category

Non‐

profit? Business Type Square Footage

Employees

(FTE)

Gross Annual

Revenue Size

Monthly

Equivalent

Fee Size

Monthly

Equivalent

Fee Size

Monthly

Equivalent

Fee

Services Small Hair Salon 800 1 95,000 A $2.50 A $2.50 A $2.50

Churches, Charities, Assoc. X Church 6,500 3 195,000 B $2.50 B $3.50 B $2.50

Medical Clinic 5,500 4.5 1,100,000 B $25.00 B $30.00 B $30.00

Office* X Small Foundation 1,500 1.5 750,000 B $7.50 A $4.50 B $7.50

Recreation X Live Local Theater 4,000 5 850,000 B $5.00 A $3.00 B $5.00

Restaurant Café 3,200 4 500,000 B $20.00 B $20.00 B $25.00

Restaurant Shoe Store 3,800 4 1,200,000 B $20.00 B $20.00 B $25.00

Retail Convenience Store 1,016 3.5 1,100,000 B $20.00 B $20.00 B $25.00

Retail Florist 2,500 3 275,000 B $20.00 B $20.00 B $25.00

Retail Vegetable Stand 1,000 2 165,000 B $20.00 A $10.00 B $25.00

Services Consulting Firm 2,000 3 $375,000 B $5.00 B $5.00 B $5.00

Services Credit Union Branch 3,100 8 $1,200,000 B $5.00 B $5.00 B $5.00

Services Day Care 14,000 2.5 225,000 B $5.00 A $2.50 B $5.00

Office Financial Advisor 14,000 20 2,200,000 C $30.00 B $15.00 C $30.00

Recreation 8‐screen movie cinema 50,000 35 2,500,000 C $20.00 C $20.00 C $20.00

Restaurant Pub 4,100 7 2,000,000 C $40.00 C $40.00 C $50.00

Restaurant Sandwich Shop 3,100 7 600,000 C $40.00 B $20.00 C $50.00

Restaurant Sit‐down restaurant 8,500 12 2,500,000 C $40.00 C $40.00 C $50.00

Restaurant Fast‐food restaurant 3,900 7.5 1,600,000 C $40.00 B $20.00 C $50.00

Retail* Neighborhood Grocery 20,000 9 1,100,000 C $40.00 B $20.00 C $50.00

Retail X Thrift Store 25,000 10 1,250,000 C $20.00 B $14.00 C $25.00

Services Large Hair Salon 6,000 12 1,100,000 C $10.00 C $10.00 C $10.00

Office X Large Advocacy Org. 60,000 110 10,500,000 D $30.00 D $54.00 D $30.00

Retail Large Grocery 65,000 75 14,000,000 D $80.00 D $80.00 D $100.00

Retail Retailer ‐ Location 1 35,000 30 5,000,000 D $80.00 D $80.00 D $100.00

Retail Retailer ‐ Location 2 65,000 60 12,000,000 D $80.00 D $80.00 D $100.00

Lodging Hotel 600,000 175 25,000,000 D $100.00 D $120.00 D $120.00

Construction Beaverton‐based contractor N/a 0 275,000 Ext $10.00 Ext $10.00 Ext $10.00

* Highlighted rows will be discussed in detail to i l lustrate rate determination for each scenario

***DRAFT***

3

Business Entity Mechanism– Original Rate Structure ProposalBusiness Category Criteria and Fees Business Entity Fee Approach

Based on fees per business entity Scenario: Approach Presented to Workgroups on August 24th, 2014

9/24/2014 $20 Million Gross Revenue Target (+/‐ $2 M)

A B C D External****Employees 0 ‐ 1 2‐5 6 ‐ 50 > 50

Annual Gross Revenue < $50,000 $50,000 ‐ $1,500,000 $1,500,000 ‐ $8,000,000 > $8,000,000

* Sqft.<

Monthly

Equivalent

Fee** * Sqft.<

Monthly

Equivalent

Fee** * Sqft.

Monthly

Equivalent

Fee** * Sqft. >

Monthly

Equivalent

Fee**

Monthly

Equivalent

Fee**

Group 1Agricultura l 2,500 $2.50 40,000 $5 40,000 - 95,000 $10 95,000 $20 $5

Churche s, Charities, Associa tions 2,500 $2.50 5,000 $5 5,000 - 10,000 $10 10,000 $20 $5

Pa rks a nd Ope n Area s 2,500 $2.50 300,000 $5 300,000 - 675,000 $10 675,000 $20 $5Se rvice s 2,500 $2.50 10,000 $5 10,000 - 30,000 $10 30,000 $20 $5

Other 2,500 $2.50 5,000 $5 5,000 - 5,000 $10 5,000 $20 $5

Group 2Construction 2,500 $5.00 10,000 $10 10,000 - 20,000 $20 20,000 $40 $10

Industria l 2,500 $5.00 20,000 $10 20,000 - 40,000 $20 40,000 $40 $10

Recrea tion 2,500 $5.00 10,000 $10 10,000 - 20,000 $20 20,000 $40 $10

T ransporta tion 2,500 $5.00 20,000 $10 20,000 - 40,000 $20 40,000 $40 $10

Group 3Institutiona l 2,500 $7.50 35,000 $15 35,000 - 80,000 $30 80,000 $60 $15

Office 2,500 $7.50 15,000 $15 15,000 - 35,000 $30 35,000 $60 $15

Group 4Resta ura nt 2,500 $10.00 5,000 $20 5,000 - 10,000 $40 10,000 $80 $20

Reta il 2,500 $10.00 15,000 $20 15,000 - 40,000 $40 40,000 $80 $20

Group 5Lodging 2,500 $12.50 35,000 $25 35,000 - 75,000 $50 75,000 $100 $25

Medica l 2,500 $12.50 18,500 $25 18,500 - 40,000 $50 40,000 $100 $25

*** Non‐Profits receive a 50% discount on their category based fee (Category A nonprofits do not receive discount)

* Square footage based on developed use in buildings, except in Agricultural and Parks / Open Areas, which is based on parcel size.

** Entity pays rates in column "A" if it meets ALL three criteria: 0 or 1 Employees,

Gross Revenue < $50,000, and developed square footage below 2,500.

** Entity pays rates in Group "B" if it meets two of the three criteria: Number of Employees <5,

Gross Revenue between $50,000 ‐ $1,500,000, or square footage below value shown in table.

** Entity pays rates in column "D" if it meets two of the three criteria: Number of Employees > 50,

Gross Revenue > $8,000,000, or square footage below value shown in table.

*** Non‐profit (Permanently exempt) entities classified as per use, then extended a 50% discount

(except for Churches, Charities and Associations; minimum rate = Column A)

**** External ‐ Entities located outside of Portland with City business licenses. Rates are set equal to Column B.

DRAFT fees shown are roughly based on rounded averages of trip‐based fees by category.

Fee table subject to further refinement and validation.

***DRAFT***

4

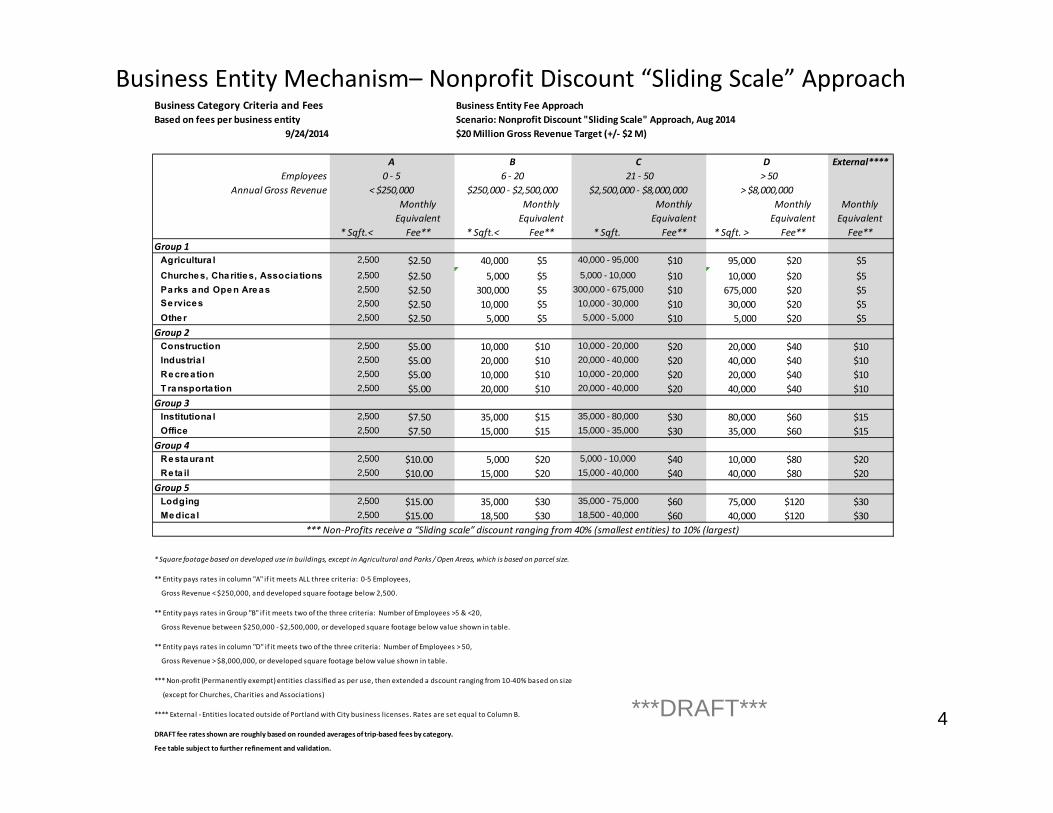

Business Entity Mechanism– Nonprofit Discount “Sliding Scale” Approach

***DRAFT***

Business Category Criteria and Fees Business Entity Fee Approach

Based on fees per business entity Scenario: Nonprofit Discount "Sliding Scale" Approach, Aug 2014

9/24/2014 $20 Million Gross Revenue Target (+/‐ $2 M)

A B C D External****Employees 0 ‐ 5 6 ‐ 20 21 ‐ 50 > 50

Annual Gross Revenue < $250,000 $250,000 ‐ $2,500,000 $2,500,000 ‐ $8,000,000 > $8,000,000

* Sqft.<

Monthly

Equivalent

Fee** * Sqft.<

Monthly

Equivalent

Fee** * Sqft.

Monthly

Equivalent

Fee** * Sqft. >

Monthly

Equivalent

Fee**

Monthly

Equivalent

Fee**

Group 1Agricultura l 2,500 $2.50 40,000 $5 40,000 - 95,000 $10 95,000 $20 $5

Churche s, Charities, Associa tions 2,500 $2.50 5,000 $5 5,000 - 10,000 $10 10,000 $20 $5

Pa rks and Ope n Are as 2,500 $2.50 300,000 $5 300,000 - 675,000 $10 675,000 $20 $5Se rvices 2,500 $2.50 10,000 $5 10,000 - 30,000 $10 30,000 $20 $5

Othe r 2,500 $2.50 5,000 $5 5,000 - 5,000 $10 5,000 $20 $5

Group 2Construction 2,500 $5.00 10,000 $10 10,000 - 20,000 $20 20,000 $40 $10

Industria l 2,500 $5.00 20,000 $10 20,000 - 40,000 $20 40,000 $40 $10

Re crea tion 2,500 $5.00 10,000 $10 10,000 - 20,000 $20 20,000 $40 $10

T ransporta tion 2,500 $5.00 20,000 $10 20,000 - 40,000 $20 40,000 $40 $10

Group 3Institutiona l 2,500 $7.50 35,000 $15 35,000 - 80,000 $30 80,000 $60 $15

Office 2,500 $7.50 15,000 $15 15,000 - 35,000 $30 35,000 $60 $15

Group 4Re staurant 2,500 $10.00 5,000 $20 5,000 - 10,000 $40 10,000 $80 $20

Re ta il 2,500 $10.00 15,000 $20 15,000 - 40,000 $40 40,000 $80 $20

Group 5Lodging 2,500 $15.00 35,000 $30 35,000 - 75,000 $60 75,000 $120 $30

Me dica l 2,500 $15.00 18,500 $30 18,500 - 40,000 $60 40,000 $120 $30

*** Non‐Profits receive a “Sliding scale” discount ranging from 40% (smallest entities) to 10% (largest)

* Square footage based on developed use in buildings, except in Agricultural and Parks / Open Areas, which is based on parcel size.

** Entity pays rates in column "A" if it meets ALL three criteria: 0‐5 Employees,

Gross Revenue < $250,000, and developed square footage below 2,500.

** Entity pays rates in Group "B" if it meets two of the three criteria: Number of Employees >5 & <20,

Gross Revenue between $250,000 ‐ $2,500,000, or developed square footage below value shown in table.

** Entity pays rates in column "D" if it meets two of the three criteria: Number of Employees > 50,

Gross Revenue > $8,000,000, or developed square footage below value shown in table.

*** Non‐profit (Permanently exempt) entities classified as per use, then extended a dscount ranging from 10‐40% based on size

(except for Churches, Charities and Associations)

**** External ‐ Entities located outside of Portland with City business licenses. Rates are set equal to Column B.

DRAFT fee rates shown are roughly based on rounded averages of trip‐based fees by category.

Fee table subject to further refinement and validation.

5

Business Entity Mechanism– 50% Nonprofit Discount Approach

***DRAFT***

Business Category Criteria and Fees Business Entity Fee Approach

Based on fees per business entity Scenario: 50% Nonprofit Discount Approach, Aug 20149/24/2014 $20 Million Gross Revenue Target (+/‐ $2 M)

A B C D External****Employees 0 ‐ 5 6 ‐ 20 21 ‐ 50 > 50

Annual Gross Revenue < $250,000 $250,000 ‐ $2,500,000 $2,500,000 ‐ $8,000,000 > $8,000,000

* Sqft.<

Monthly

Equivalent

Fee** * Sqft.<

Monthly

Equivalent

Fee** * Sqft.

Monthly

Equivalent

Fee** * Sqft. >

Monthly

Equivalent

Fee**

Monthly

Equivalent

Fee**

Group 1Agricultura l 2,500 $2.50 40,000 $5 40,000 - 95,000 $10 95,000 $20 $5

Churches, Charities, Associa tions 2,500 $2.50 5,000 $5 5,000 - 10,000 $10 10,000 $20 $5

Pa rks a nd Open Area s 2,500 $2.50 300,000 $5 300,000 - 675,000 $10 675,000 $20 $5Se rvice s 2,500 $2.50 10,000 $5 10,000 - 30,000 $10 30,000 $20 $5Other 2,500 $2.50 5,000 $5 5,000 - 5,000 $10 5,000 $20 $5

Group 2Construction 2,500 $5.00 10,000 $10 10,000 - 20,000 $20 20,000 $40 $10

Industria l 2,500 $5.00 20,000 $10 20,000 - 40,000 $20 40,000 $40 $10

Recrea tion 2,500 $5.00 10,000 $10 10,000 - 20,000 $20 20,000 $40 $10T ransporta tion 2,500 $5.00 20,000 $10 20,000 - 40,000 $20 40,000 $40 $10

Group 3Office 2,500 $7.50 15,000 $15 15,000 - 35,000 $30 35,000 $60 $15

Institutiona l 2,500 $7.50 35,000 $15 35,000 - 80,000 $30 80,000 $60 $15

Group 4Resta ura nt 2,500 $12.50 5,000 $25 5,000 - 10,000 $50 10,000 $100 $25Reta il 2,500 $12.50 15,000 $25 15,000 - 40,000 $50 40,000 $100 $25

Group 5Lodging 2,500 $15.00 35,000 $30 35,000 - 75,000 $60 75,000 $120 $30

Me dica l 2,500 $15.00 18,500 $30 18,500 - 40,000 $60 40,000 $120 $30

*** Non‐Profits receive a 50% discount across all categories

* Square footage based on developed use in buildings, except in Agricultural and Parks / Open Areas, which is based on parcel size.

** Entity pays rates in column "A" if it meets ALL three criteria: 0‐5 Employees,

Gross Revenue < $250,000, and developed square footage below 2,500.

** Entity pays rates in Group "B" if it meets two of the three criteria: Number of Employees >5 & <20,

Gross Revenue between $250,000 ‐ $2,500,000, or developed square footage below value shown in table.

** Entity pays rates in column "D" if it meets two of the three criteria: Number of Employees > 50,

Gross Revenue > $8,000,000, or developed square footage below value shown in table.

*** Non‐profit entities classified as per use, then extended a 50% discount

(except for Churches, Charities and Associations; minimum rate = Column A)

**** External ‐ Entities located outside of Portland with City business licenses. Rates are set equal to Column B.

DRAFT fee rates shown are roughly based on rounded averages of trip‐based fees by category.

Fee table subject to further refinement and validation.

6

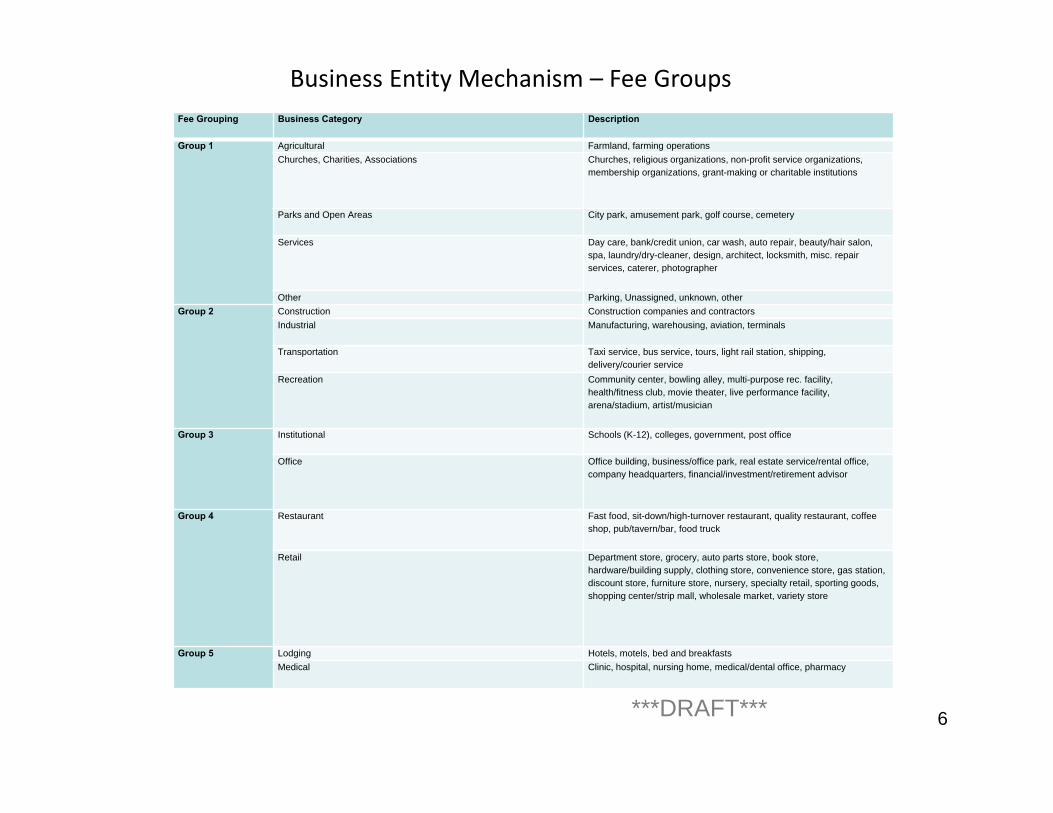

Business Entity Mechanism – Fee Groups

***DRAFT***

Fee Grouping Business Category Description

Group 1 Agricultural Farmland, farming operations

Churches, Charities, Associations Churches, religious organizations, non-profit service organizations, membership organizations, grant-making or charitable institutions

Parks and Open Areas City park, amusement park, golf course, cemetery

Services Day care, bank/credit union, car wash, auto repair, beauty/hair salon, spa, laundry/dry-cleaner, design, architect, locksmith, misc. repair services, caterer, photographer

Other Parking, Unassigned, unknown, other

Group 2 Construction Construction companies and contractors

Industrial Manufacturing, warehousing, aviation, terminals

Transportation Taxi service, bus service, tours, light rail station, shipping, delivery/courier service

Recreation Community center, bowling alley, multi-purpose rec. facility, health/fitness club, movie theater, live performance facility, arena/stadium, artist/musician

Group 3 Institutional Schools (K-12), colleges, government, post office

Office Office building, business/office park, real estate service/rental office, company headquarters, financial/investment/retirement advisor

Group 4 Restaurant Fast food, sit-down/high-turnover restaurant, quality restaurant, coffee shop, pub/tavern/bar, food truck

Retail Department store, grocery, auto parts store, book store, hardware/building supply, clothing store, convenience store, gas station, discount store, furniture store, nursery, specialty retail, sporting goods, shopping center/strip mall, wholesale market, variety store

Group 5 Lodging Hotels, motels, bed and breakfasts

Medical Clinic, hospital, nursing home, medical/dental office, pharmacy

Related Documents