Charity Trustee Training and Risk Seminar Tuesday 19 th August 2014

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Charity Trustee Training and Risk Seminar Tuesday 19th August 2014

Charity trustee duties Gavin McEwan Partner

• Common law duties

• Charities and Trustee Investment (Scotland) Act 2005

• Company law duties

• Company law duties technically apply only to companies BUT they can be considered to be good practice generally

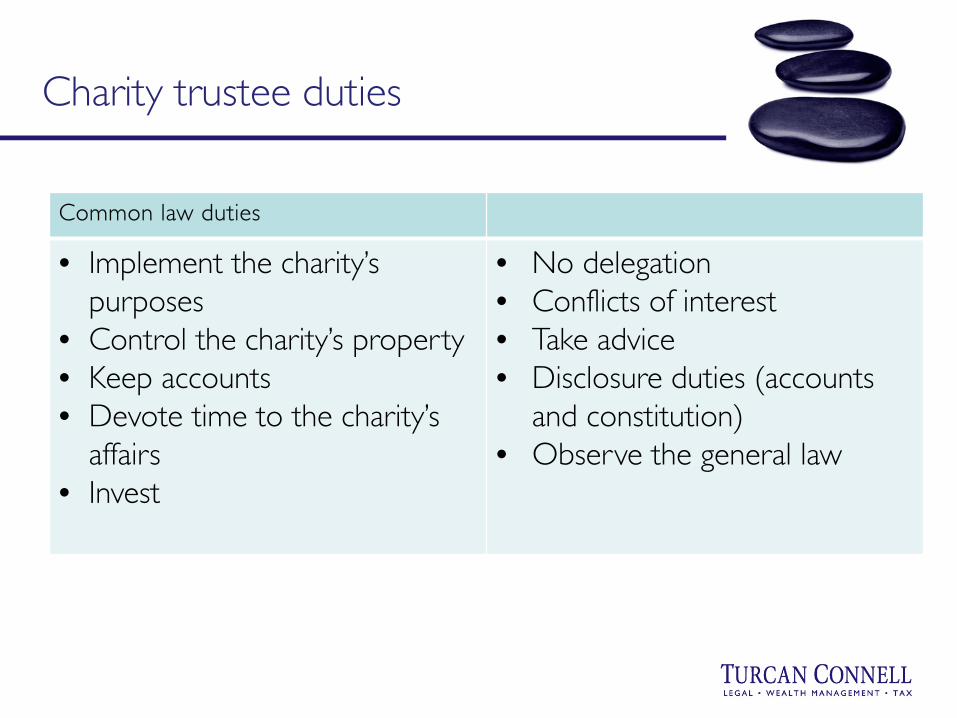

Charity trustee duties

Common law duties

• Implement the charity’s purposes

• Control the charity’s property • Keep accounts • Devote time to the charity’s

affairs • Invest

• No delegation • Conflicts of interest • Take advice • Disclosure duties (accounts

and constitution) • Observe the general law

Charity trustee duties

Charity trustee duties

2005 Act duties

• Seek, in good faith, to ensure that the charity acts in a manner consistent with its purposes

• Act with care and diligence (standard of care)

• Manage conflicts of interest

• Overriding duty: act in best interests of the charity

• Comply with the 2005 Act generally

Charity trustee duties

Company law duties

• Duty to act within powers

• Duty to promote the success of the company*

• Duty to exercise independent judgement

• Duty to exercise reasonable care, skill and diligence

• Duty to avoid conflicts of interest

• Duty not to accept benefits from third parties

• Duty to declare interests

And also: Kirkintilloch, Hamilton, Falkirk and Dumbarton P

Tony Sinclair – Partner Claire McCaffray – VAT Senior Manager

8 French Duncan

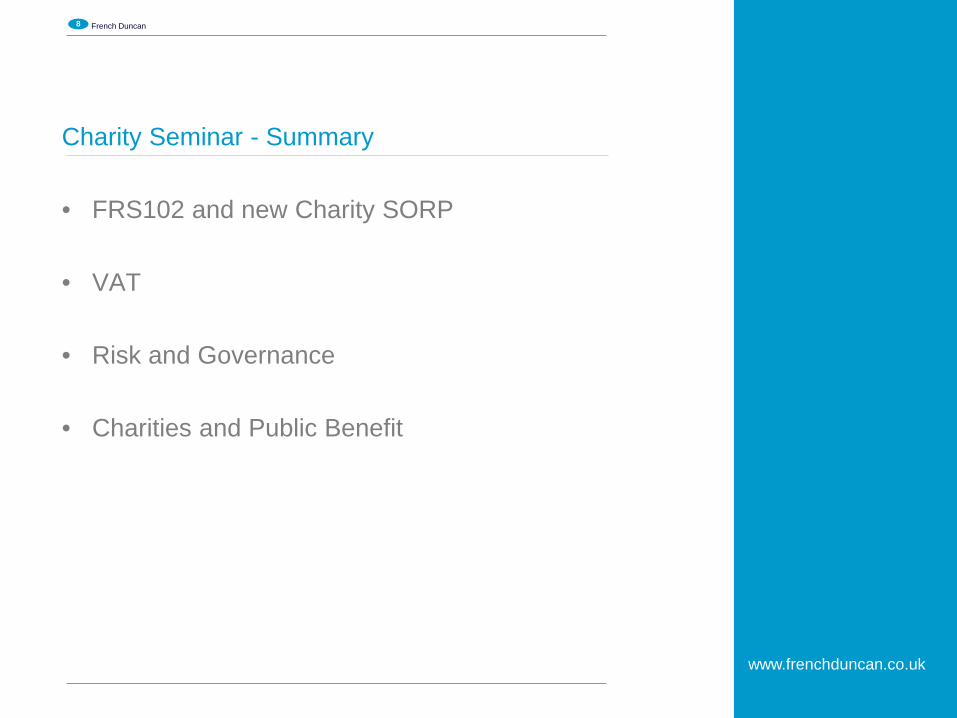

Charity Seminar - Summary

• FRS102 and new Charity SORP

• VAT

• Risk and Governance

• Charities and Public Benefit

www.frenchduncan.co.uk

And also: Kirkintilloch, Hamilton, Falkirk and Dumbarton

FRS102 and the new Charity SORP

Tony Sinclair Partner

10 French Duncan

FRS102 and Charities SORP Overview • New standards coming for accounting periods commencing 1 January

2015 • UK Standards being aligned with international standards

• Charity SORP being updated to reflect changes

www.frenchduncan.co.uk

Full IFRS Listed Groups FRS 102 All other entities FRSSE 2015 Small entities

11 French Duncan

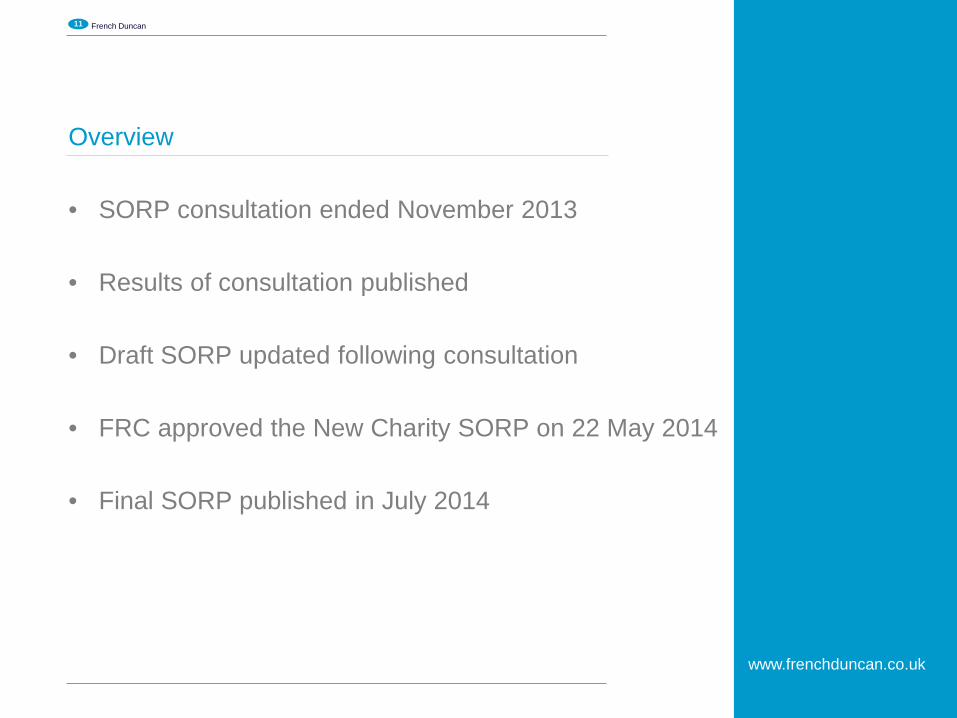

Overview

• SORP consultation ended November 2013 • Results of consultation published

• Draft SORP updated following consultation • FRC approved the New Charity SORP on 22 May 2014 • Final SORP published in July 2014

www.frenchduncan.co.uk

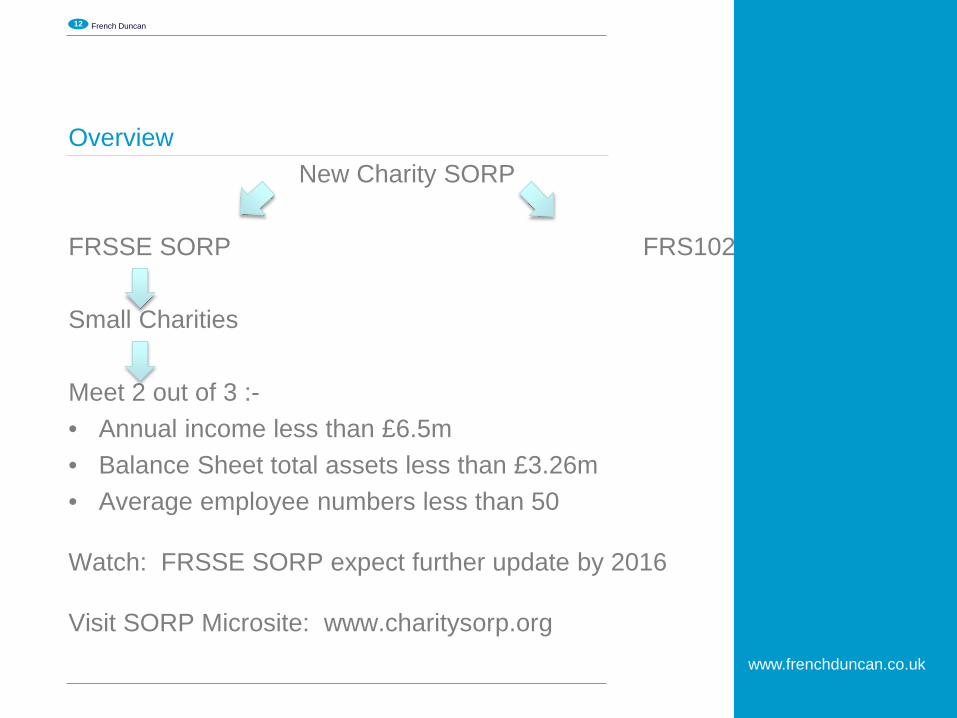

12 French Duncan

Overview New Charity SORP FRSSE SORP FRS102 SORP Small Charities Meet 2 out of 3 :- • Annual income less than £6.5m • Balance Sheet total assets less than £3.26m • Average employee numbers less than 50 Watch: FRSSE SORP expect further update by 2016 Visit SORP Microsite: www.charitysorp.org

www.frenchduncan.co.uk

13 French Duncan

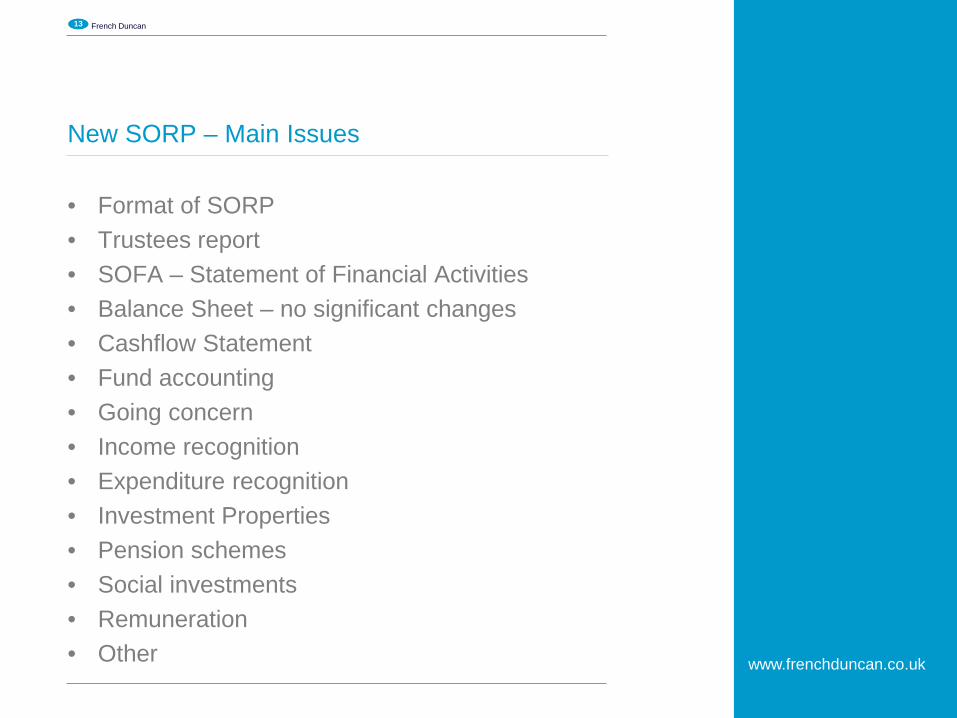

New SORP – Main Issues • Format of SORP • Trustees report • SOFA – Statement of Financial Activities • Balance Sheet – no significant changes • Cashflow Statement • Fund accounting • Going concern • Income recognition • Expenditure recognition • Investment Properties • Pension schemes • Social investments • Remuneration • Other

www.frenchduncan.co.uk

14 French Duncan

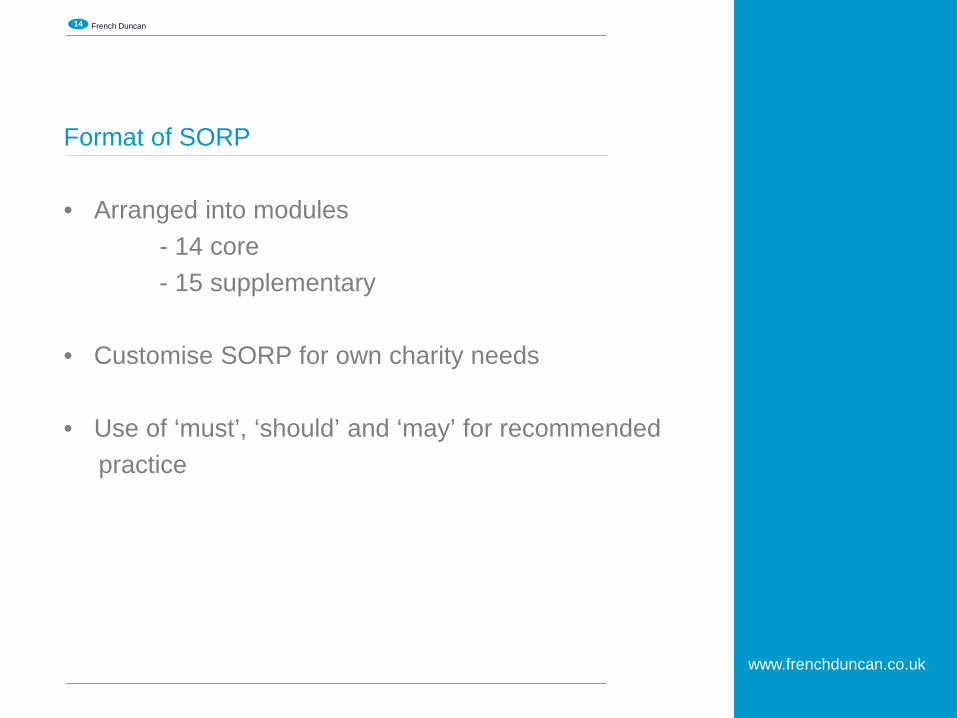

Format of SORP • Arranged into modules - 14 core - 15 supplementary • Customise SORP for own charity needs • Use of ‘must’, ‘should’ and ‘may’ for recommended practice

www.frenchduncan.co.uk

15 French Duncan

Trustees Report

Specific disclosures for larger charities highlighted • Explain social investment policies • Explain financial effect of significant events • Describe principal risks and uncertainty and how managed • Disclose arrangements for setting remuneration of

management personnel

Explain any going concern uncertainties

Explain reasons for reserves policy and also for no reserves policy

All trustees to be listed in accounts

www.frenchduncan.co.uk

16 French Duncan

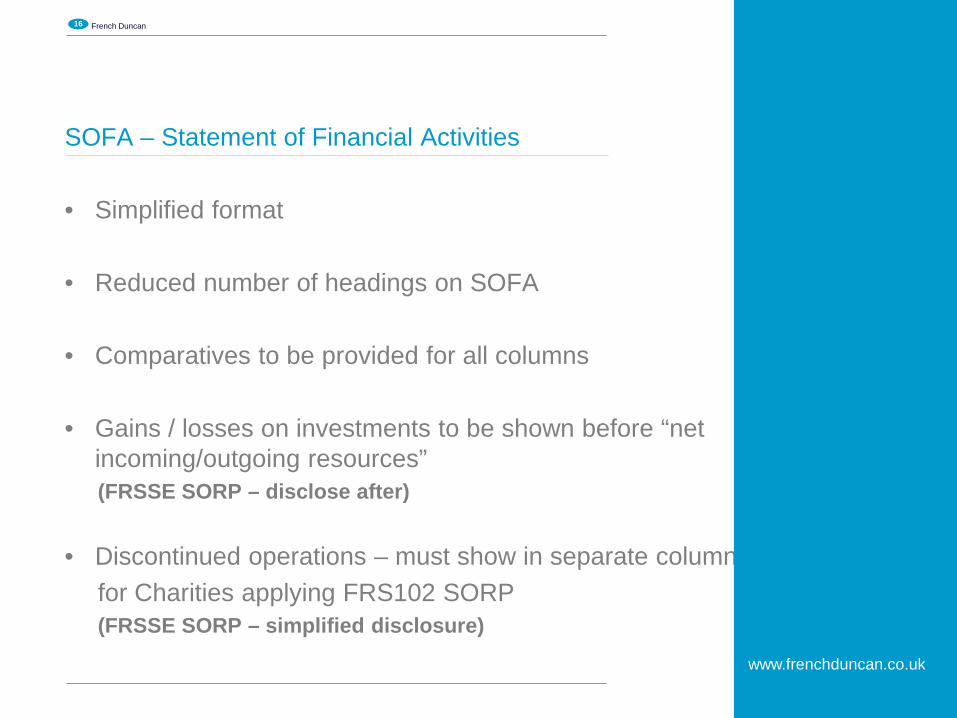

SOFA – Statement of Financial Activities • Simplified format • Reduced number of headings on SOFA • Comparatives to be provided for all columns • Gains / losses on investments to be shown before “net

incoming/outgoing resources” (FRSSE SORP – disclose after)

• Discontinued operations – must show in separate column for Charities applying FRS102 SORP (FRSSE SORP – simplified disclosure)

www.frenchduncan.co.uk

17 French Duncan

SOFA Income OLD SORP NEW SORP Incoming resources Voluntary income Incoming resources from charitable activities Activities for generating funds Investment income Other incoming resources

Income and endowments Donations and legacies Income from charitable activities Other trading activities Income from investments Other income

www.frenchduncan.co.uk

18 French Duncan

SOFA Expenditure

OLD SORP NEW SORP Resources Expended Costs of generating voluntary income Fundraising trading: cost of goods sold and other costs Investment management costs Resources expended on charitable activities Governance Costs Other resources expended

Expenditure Expenditure on raising funds Expenditure on charitable activities Other expenditure

www.frenchduncan.co.uk

19 French Duncan

Balance Sheet Capitalised goodwill – life assumed not to exceed 5 years (FRSSE SORP- life not more than 20 years) More disclosures generally under FRS102 SORP

www.frenchduncan.co.uk

20 French Duncan

Cashflow Statement Charities applying FRS102 must prepare a cashflow

• Mandatory headings: o Operating activities; o Investing activities; o Financing activities

Charities applying FRSSE SORP have option to prepare

a cashflow

www.frenchduncan.co.uk

21 French Duncan

Fund Accounting • Net amount of transfers between funds in any year must

net to zero

• Rules out one sided transfers when accounting for assets acquired/transferred from another charity

www.frenchduncan.co.uk

22 French Duncan

Going Concern • To disclose any material uncertainties casting doubt over its ability to continue as a going concern • If no material uncertainties this should also be stated

• Trustees to consider a period of at least 12 months from

accounts approval (FRSSE SORP does not specify)

www.frenchduncan.co.uk

23 French Duncan

Income Recognition • Income to be recognised when receipt is probable – ‘more likely than not’ • Legacy income – more guidance

• Income from donated goods is recognised when received at its fair value. If impractical then recognise income when goods sold (same as existing SORP)

www.frenchduncan.co.uk

24 French Duncan

Expenditure Recognition • Require accrual for holiday pay and sick pay where

material (FRSSE SORP – not required)

www.frenchduncan.co.uk

25 French Duncan

Investment Properties • Mixed use properties • 2005 SORP requires classification based on main use • New FRS102 SORP requires split between investment

and operations – if impractical, then treat as a tangible fixed asset.

• Investment part of property to be stated at fair value unless can’t be measured without undue cost or effort

www.frenchduncan.co.uk

26 French Duncan

Pension Scheme • Multi-employer defined benefit schemes – if agreed deficit reduction plan in place, this liability must be recognised in accounts

(FRSSE SORP – not required)

www.frenchduncan.co.uk

27 French Duncan

Social Investment • New class of investment including ‘programme related

investments’ and ‘mixed motive investments’

• Defined in SORP – ‘investments undertaken for a financial return and to further the investing charity’s charitable aims and objectives’

• Charities adopting FRS102 SORP use fair value or cost

where reliable FV estimate not available. Charities adopting FRSSE SORP can measure at cost less impairment.

www.frenchduncan.co.uk

28 French Duncan

Remuneration • Charities reporting under FRS102 must disclose total remuneration and benefits of key management personnel • All charities must disclose number of staff paid £60k or

more in bandings of £10k.

www.frenchduncan.co.uk

29 French Duncan

Other • Strategic report required only for charitable companies

qualifying as medium or large

www.frenchduncan.co.uk

30 French Duncan

Summary • Key date: New SORP effective for periods commencing 01/01/2015 • Two Charity SORPS – FRSSE SORP for small charities and FRS102 SORP for all others • Disclosure and accounting changes

• Reference site: www.charitysorp.com

www.frenchduncan.co.uk

And also: Kirkintilloch, Hamilton, Falkirk and Dumbarton

VAT

Claire McCaffray Senior Manager

32 French Duncan

• “We’re a charity, we don’t pay VAT”

• Reliefs

• Exemptions • Pitfalls

www.frenchduncan.co.uk

33 French Duncan

Reliefs

www.frenchduncan.co.uk

• 0% VAT on advertising

• 5% VAT on fuel and power supplied for charitable use

(60% de-minimis)

• 0% VAT on the construction, purchase or long lease of a new building to be used solely for a ‘charitable purpose’ (95% or more)

• 0% VAT on the purchase of specialist goods/equipment for the personal use of the disabled or by a relevant body for medical/scientific/veterinary use

34 French Duncan

Exemptions

www.frenchduncan.co.uk

• Lease of land & property for a non-business use

Not for office use, e.g. for service users If landlord charges VAT, is compulsorily disapplied and exemption applies

• One off fundraising events

• Climate Change Levy: If 5% VAT applies to fuel and

power, will be exempt from CCL

• Certain supplies of education, vocational training and research supplied on a not-for-profit basis

35 French Duncan

Pitfalls

www.frenchduncan.co.uk

• Grant Funding/Service Level Agreements • Business/Non-business

• VAT Registration

36 French Duncan

Is the Charity Making Business Supplies?

www.frenchduncan.co.uk

• Is the activity a serious undertaking earnestly pursued?

• Is the activity an occupation or function which is actively pursued with reasonable or recognisable continuity?

• Does the activity have a certain measure of substance in

terms of the quarterly or annual value of taxable supplies made?

• Is the activity conducted in a regular manner and on sound and recognised business principles?

• Is the activity predominately concerned with the making of taxable supplies for a consideration?

• Are the taxable supplies that are being made of a kind which, subject to differences of detail, are commonly made by those who seek to profit from them?

37 French Duncan

VAT

Questions?…………………….

www.frenchduncan.co.uk

And also: Kirkintilloch, Hamilton, Falkirk and Dumbarton

Contact us Glasgow 133 Finnieston Street, Glasgow, G3 8HB t +141 (0) 221 2984 f +141 (0) 221 2980

www.frenchduncan.co.uk

Edinburgh 56 Palmerston Place, Edinburgh, EH12 5AY t +131 (0) 225 6366 f +131 (0) 220 1041

Stirling Macfarlane Gray House Castlecraig Business Park, Stirling, FK7 7WT t +1786 (0) 451 745 f +1786 (0) 472 528

This proposal is made by French Duncan LLP and is in all respects subject to the negotiation, agreement and signing of a specific contract/letter of engagement.

French Duncan LLP, a limited liability partnership registered in Scotland SO00004. A list of partners is available for inspection at the registered office: 133 Finnieston Street, Glasgow, G3 8HB

And also: Kirkintilloch, Hamilton and Dumbarton

Risk and Governance Kenneth Pinkerton Senior Associate

1. Burden of risk and personal liability

2. Lessons in managing risk: examples

3. Decision making by trustees

Risk and Governance

1. Unincorporated associations

2. Trusts

3. Charitable companies

4. Scottish Charitable Incorporated Organisations (SCIOs)

Burden of Risk and Personal Liability

Burden of Risk and Personal Liability

Unincorporated Associations

• Lack of legal personality

• No clear legal authority on question of risk

• Personal liability:- • All members of the association?

• Committee members / office-bearers?

• Only those who authorised the actings?

• Potential for future developments

Burden of Risk and Personal Liability

Trusts

• Powers contained in trust deed

• Contract in trustee capacity

• Acting outwith powers and loss to trust

• When personal liability may arise

• Immunity clauses

Burden of Risk and Personal Liability

Charitable Companies

• Established position – notion of limited liability

• Dual level of involvement

• Members – equivalent of shareholders

• Limits stated in articles

• Directors – the charity trustees

Burden of Risk and Personal Liability

Scottish Charitable Incorporated Organisations

• SCIO – since April 2011

• Lighter touch regulation

• Separate legal personality

• Growth area

• Similar burden of risk as limited companies

• When personal liability may arise

Potential Areas of Risk

• Governance and management

• Operational and external

• Economic and financial

• Compliance and regulatory

Lessons in Managing Risk

One Plus: One Parent Families

• Turnover in 2005 of £11million

• Lack of liquidity in 2007

• At fault: • Governance of the charity

• Charity’s response to the funding environment

Lessons in Managing Risk

• Ensure they have, collectively, the right mix of skills and experience for the type and scale of the charity for which they are ultimately responsible

• Understand the operating environment faced by their charity and the implications this will have for how the charity is managed

• Maintain overall direction and control of their charity, and be able to actively hold the Chief Executive and Senior Management Team to account as well as providing strategic direction

Lessons in Managing Risk

• Be able to exercise independent judgement when weighing up and considering any plans and proposals from the Chief Executive and Senior Management Team, while at the same time not undermining management authority or de-motivating staff

• Be explicit in defining the respective roles and responsibilities of the Board, Chairperson or Convenor of the Board and Chief Executive, including the extent of delegated authority

• Take ownership of their own Board and implement a programme for board training, building and renewal that includes regular reviews of performance and skills mix

Lessons in Managing Risk

• Make sure they receive full and up-to-date financial information to allow them to fully understand the position of their charity and take informed decisions

• Develop an appropriate risk management strategy that identifies possible risks to the charity and must establish systems or procedures to minimise these risks

• At a time of growth and development Charity Trustees must satisfy themselves that the capacity of the charity’s management and governance structures are appropriate for the planned development

Lessons in Managing Risk

• Charity Trustees and auditors must maintain a direct relationship to obtain an objective and independent view of the charity and to gain assurance and advice on control systems and governance matters

• Large or complex charities must consider establishing an audit committee to ensure that processes and procedures are monitored and are appropriate for the size and scale of the charity

• Charity Trustees must ensure that the organisation seeks external independent professional advice where it faces problems or does not have the required in-house expertise in a particular area

Lessons in Managing Risk

Age Concern England: Heyday

• £22 million Membership Scheme

• Target of 3 million members

• Scheme closed with 40,000 members

• At fault: • Governance of the charity

• Decision making process lacked rigour

Lessons in Managing Risk

Regulators’ Themes

• In One Plus OSCR identified the need to promote to Charity Trustees the importance of risk management.

• In Age Concern England, the Charity Commission emphasised that Charity Trustees should have a robust risk management system in place, because managing risk effectively is essential if the key objectives set by Trustees are to be achieved.

Action points for trustees

• Collective general duty of care – consult with others

• All policies and procedures should address risk

• Adopt and regularly review a Risk Register

• Seek advice when required

• Charity Trustee Indemnity Insurance

• Stay informed: Charity Trustee Induction and Training

Decision making by trustees

• Two recent cases in Scotland

• Rangers Charity Foundation • fundamental conflict of interest

• non-participation by majority of trustees

• failure to take legal advice

• Glasgow East Regeneration Agency • use of local authority comparators in measuring Chief Exec severance

package (incl. one-off payment of £230k)

• non-attending trustees; no external advice

Decision making by trustees

• Charity Commission (England & Wales) guidance (2013)

• Trustees must, amongst other things….. • act within their powers

• act in good faith and only in the interests of the charity

• make sure they are sufficiently well informed

• take account of all relevant factors

• ignore irrelevant factors

• make decisions which are within the range of decisions that a reasonable trustee board could make

Decision making by trustees

• Charity Commission (England & Wales) guidance (2013)

• Trustees must, amongst other things….. • follow requirements in governing documents about decision making

• take decisions collectively

• if delegating, have clear and robust reporting procedures and lines of accountability in place

• record decisions properly so that there is no doubt about what was decided and why

Decision making by trustees

• Governance themes arise for all charities

• Take appropriate advice

• Follow the constitution

• Recognise and manage conflicts of interest

• Bear in mind collective duty of care on trustee body

• Section 66 duties and other legal duties

Risk and Governance Kenneth Pinkerton Senior Associate

Charities and Public Benefit Gavin McEwan Partner

Public Benefit

• A fundamental area of the reformed law of charities in Scotland

• Often misunderstood

• Two areas – schools, equalities

Section 8(2) of the 2005 Act

In determining whether a body provides or intends to provide public benefit, regard must be had to –

a) How any –

i. Benefit gained or likely to be gained by members of the body or any other

persons (other than as members of the public), and

ii Disbenefit incurred or likely to be incurred by the public

In consequence of the body exercising its functions compares with the benefit gained or likely to be gained by the public in that consequence, and

b) Where any benefit is, or likely to be, provided to a section of the public only, whether any condition on obtaining that benefit (including any charge or fee) is unduly restrictive.

Section 8(2) Explained

• No presumption

• Balance • Benefit to public

• Disbenefit to public

• Private benefit

• Have regard to conditions on access to benefit – including fees/charges

• OSCR guidance available

The Schools Project

• All independent/fee-paying schools reviewed

• Most passed first time

• Some directed to change practices to meet test

• Project virtually complete

• Report to come – behaviour has changed

Schools Project

• Fees are a barrier to entry, a restrictive condition

• This must be mitigated in a meaningful, non-token way

• The higher the fee the greater the mitigation required

• Other non-fee benefits, such as free access and contribution to

education sector taken into account

• Refer back to charity constitution

Fee charging charities

• Schools points of wider application

• Focus on affordability and mitigation measures

• It is an “on balance” test

Equality Act – “Unduly Restrictive” Conditions

• Equality Act 2010

• Consolidating anti-discrimination statute

• Applies to all service providers, including charities

• Charity exemption permits discrimination -

• must be a proportionate means of carrying out a legitimate aim; or

• must be designed in itself to tackle discrimination

• must be permitted by the charity’s constitution

Equality law (2)

• OSCR approach: • IF you discriminate & don’t meet the charity exemption

• THEN you are in breach of the Equality Act 2010

• AND you therefore apply an unduly restrictive condition in how benefits are accessed

• The result is that the charity fails the public benefit test and therefore fails the charity test

• “Protected characteristics”

Equality law (3)

• St Margaret’s Children and Family Care Society v OSCR (2014)

• Scottish Charity Appeals Panel

• Voluntary adoption agency connected to the Roman Catholic church

• Charity’s criteria (as published on its website) are to prioritise couples married for minimum of 2 years

• At time of the OSCR inquiry, same sex marriage was not permitted in Scotland – so this amounted to direct discrimination in OSCR’s view

Equality law (4)

• SCAP quashed OSCR’s directions

• The charity and religious exemptions were met

• European Convention on Human Rights, competing articles

• Other factors were taken into account – • -donor impact: charity would have to close

• impact on wider public: 10% of all adoptions in Scotland

• OSCR has not appealed SCAP’s decision

• Of limited effect

• Criticism by Commission on Equality & Human Rights

Public Benefit - Conclusions

• Guidance awaited

• OSCR as assessor of charity law worked well

• OSCR as assessor of equality law not so successful

• Guidance needed from OSCR

Charities and Public Benefit Gavin McEwan Partner

Questions? Follow us @tc_charities

Important Information

We take all reasonable care to ensure information contained within this document is accurate, however, we give no guarantee to the accuracy and completeness of the information or to any errors and omissions that may occur due to circumstances beyond our control. Firm Information Turcan Connell is a Scottish Partnership regulated by The Law Society of Scotland. Registered office Princes Exchange, 1 Earl Grey Street, Edinburgh, EH3 9EE. Risk Warnings Information provided in this document and any opinions expressed are for general use and not personal to your circumstances, nor are they intended to provide specific advice. No information in this document should be viewed as an offer or recommendation to undertake any specific activity. All information provided is based on our understanding of current legislation which is subject to change. It has been produced for information purposes only. Professional advice should always be sought before taking any action. Turcan Connell or any of its associated companies cannot take any responsibility for losses incurred through acting or failing to act on the basis of anything contained in this document. Intellectual Property All rights to use the content of this document belong to the Turcan Connell Group and any unauthorised use, including transmission, extraction, modification and distribution is strictly prohibited. You may not reproduce part or all of the content of this document in any form unless it is for personal use. ©Turcan Connell

Related Documents