Character Merchandising and Brand Valuation Dr. Guriqbal Singh Jaiya Director Small and Medium-Sized Enterprises Division World Intellectual Property Organization www.wipo.int/sme

Character Merchandising and Brand Valuation Dr. Guriqbal Singh Jaiya Director Small and Medium-Sized Enterprises Division World Intellectual Property Organization.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Character Merchandising and Brand Valuation

Dr. Guriqbal Singh JaiyaDirector

Small and Medium-Sized Enterprises DivisionWorld Intellectual Property Organization

www.wipo.int/sme

Character Merchandising 1The commercial exploitation of the names and images of both, famous personalities and fictional characters has become a highly lucrative practice in the 1990s.

Character merchandising refers to a marketing technique by which products are associated with well-known characters, since such association effectively enhances the commercial value of the products. Modern society is "celebrity-driven," which means that famous personalities can greatly influence the public.

Two distinct forms of activities are usually encompassed by the term “character merchandising”.

Firstly, there is merchandising, where the name or more usually the image of a person or character is applied to goods to make those goods more attractive to consumers.

Secondly, there is endorsement, where the name or likeness of a well-known personality or character is associated with a product or business, usually in its advertising. The endorsement value of superstars appears to be on the increase. If they endorse it, consumers will generally buy it.

Character Merchandising 2• Character merchandising is defined as the use

of popular children’s characters to promote the sale of consumer goods.

• Characters themselves typically derive from television, film, toys, books, comics, and computer games.

• Children (especially the “under tens”) are the key audience for character merchandising, although adults are the principal purchasers.

• Thus, character merchandising is used by manufacturers to trigger a response among children, who then implore their parents to buy on their behalf.

Character Merchandising 3It is becoming recognized by the law that someone well known has a ‘persona’ that is marketable in its own right, regardless of the original reason for the fame.

This has an economic worth to the well known individual, such as a famous movie-star or sports-person, so the individual should be able to use it as he or she pleases, and prevent others from using it without permission and payment to promote their own interests.

The marketing of name or image for monetary gain in this manner is known as ‘character merchandising’.

Two Basic Models 1In practice, one can distinguish between two basic models in the use of advertising symbols.

a) Popular and famous characters derived from mass media (cinema, television and literature, including comic books), such as Mickey Mouse, Asterix, Superman, James Bond, Playboy, E.T., Bee Maja, Smurfs.Here sales appeal is due to identification with the character used in the advertising, or its global image, and partially the general attraction of the media event behind it, of which one is reminded at the point of purchase (Star Wars). In an individual case the concrete motive to purchase appears to be that one likes to be reminded of the character or event, as well as the consideration that because the works behind them were "well done," the products marketed under the respective names must also be or are of good quality.

Two Basic Models 2b) At first glance, the second group of "product patronage" appears to be of a more objective nature, because the person used in the advertising or his name conjures up a particular image of quality. The names of great fashion designers, actors, etc., belong in this category, under whose names a variety of luxury products are marketed, whereby the qualitative prominence of the fashion creation or cinematic flair is supposed to be or is transferred to the product designated as such. But a certain (subjective) "snob appeal" may also play a role here.

Appropriation of Personality

The problem of appropriation of personality is commonly discussed as an aspect of ‘character merchandising’, with a distinction usually being drawn between real persons and fictitious characters, although the problem is also commonly referred to as ‘personality merchandising’, or endorsement.

Interests in PersonalityA broad division may be made between first, economic or pecuniary interests in personality, and second, non-pecuniary or dignitary interests.(1) Economic interests:

(i) existing trading or licensing interests(ii) other intangible recognition values

(2) Dignitary interests:(i) interests in reputation(ii) interests in personal privacy(iii) interests in freedom from mental distress

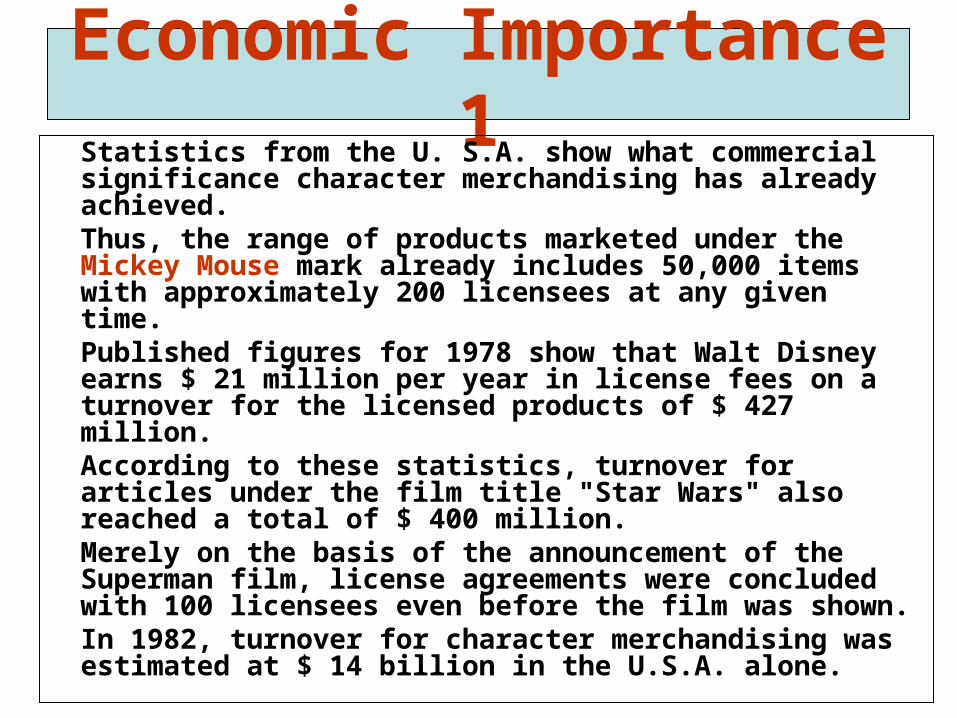

Economic Importance 1Statistics from the U. S.A. show what commercial significance character merchandising has already achieved. Thus, the range of products marketed under the Mickey Mouse mark already includes 50,000 items with approximately 200 licensees at any given time. Published figures for 1978 show that Walt Disney earns $ 21 million per year in license fees on a turnover for the licensed products of $ 427 million. According to these statistics, turnover for articles under the film title "Star Wars" also reached a total of $ 400 million. Merely on the basis of the announcement of the Superman film, license agreements were concluded with 100 licensees even before the film was shown. In 1982, turnover for character merchandising was estimated at $ 14 billion in the U.S.A. alone.

Economic Importance 2• Licensed toys represent one of the most

important segments of the character licensing industry. In fact, licensed toys typically represent about 25%-35% of all annual toy sales. Sales are significantly driven by movies, with the two biggest licensing properties in 2004 being Spider-Man 2 and Shrek 2.

• Food tie-ins are another lucrative channel for character merchandising license holders. Two examples of agreements include Burger King’s promotions using Spider-Man 2 merchandise, and Baskin Robbins offering Shrek’s Swirl Sherbet.

Tort of “Passing Off” Passing off protects the proprietary right of the plaintiff in the

goodwill or reputation of a business likely to be injured by the defendant’s misrepresentation. However, the action of passing off requires proof of a reputation within the jurisdiction. Passing off action not only protects the goodwill in a trade, but also protects promotional exploitation of a name, personality or reputation. Traditionally passing off cases required a representation that the defendant’s goods were those of the plaintiff. However, it would appear that the action of passing off now extends to enjoin any deceptive connection or association between the defendant’s business and the plaintiffs or their business induced by the defendant’s misrepresentation. It protects the plaintiff’s relationship with lines of business other than those actually engaged in by the plaintiff at the time. The defendant does not necessarily, therefore, have to represent his goods as being those of plaintiff, it suffices that he makes a representation, which links him with the plaintiff or his goods. The public may well be aware that the goods in question are the defendant’s, but they are deceived into thinking that the plaintiff is associated with them.

Anne of Green Gables: literary description of the character

“Matthew was not looking at her and would not have seen what she was really like if he had been, but an ordinary observer would have seen this: A child of about eleven, garbed in a very short, very tight, very ugly dress of yellowish-gray wincey. She wore a faded brown sailor hat and beneath the hat, extending down her back, were two braids of very thick, decidedly red hair. Her face was small, white and thin, also much freckled; her mouth was large and so were her eyes, which looked green in some lights and moods and gray in others.

So far, the ordinary observer; an extraordinary observer might have seen that the chin was very pointed and pronounced; that the big eyes were full of spirit and vivacity; that the mouth was sweet-lipped and expressive; that the forehead was broad and full; in short, our discerning extraordinary observer might have concluded that no commonplace soul inhabited the body of this stray woman-child of whom shy Matthew Cuthbert was so ludicrously afraid.”

Background Legal Issues

• Unsettled law regarding:

–IP protection afforded to fictional literary characters

–Overlap between copyright and trademark

–Reach of official marks

IP protection afforded to fictional literary characters

• Not settled re copyright protection for fictional characters independent of the work

• Not settled whether trade-mark is appropriate protection re merchandise

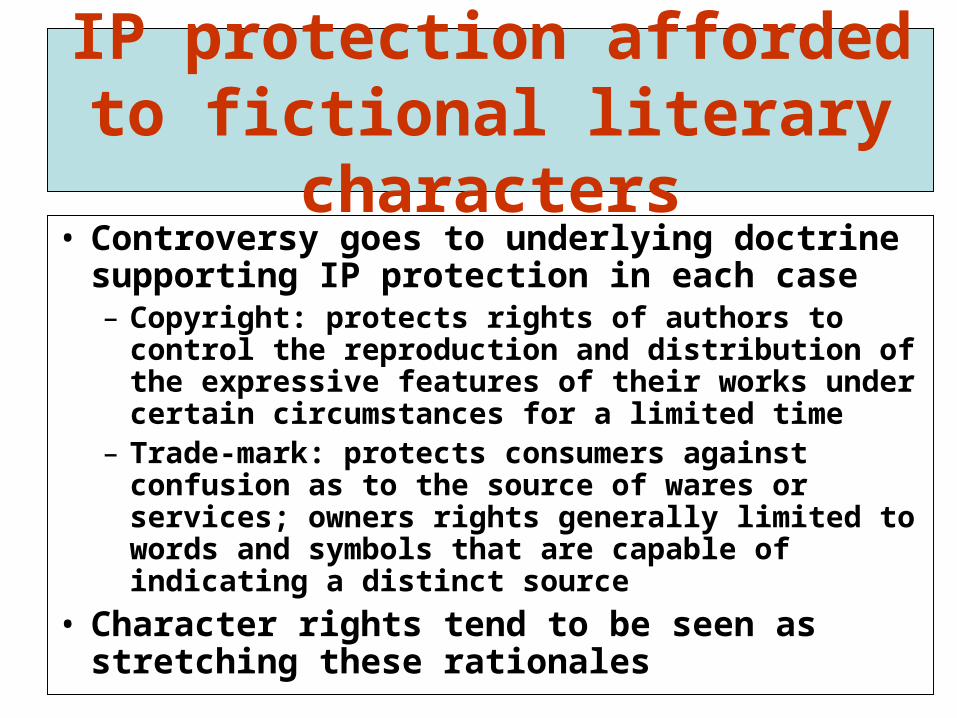

IP protection afforded to fictional literary characters

• Controversy goes to underlying doctrine supporting IP protection in each case– Copyright: protects rights of authors to control the

reproduction and distribution of the expressive features of their works under certain circumstances for a limited time

– Trade-mark: protects consumers against confusion as to the source of wares or services; owners rights generally limited to words and symbols that are capable of indicating a distinct source

• Character rights tend to be seen as stretching these rationales

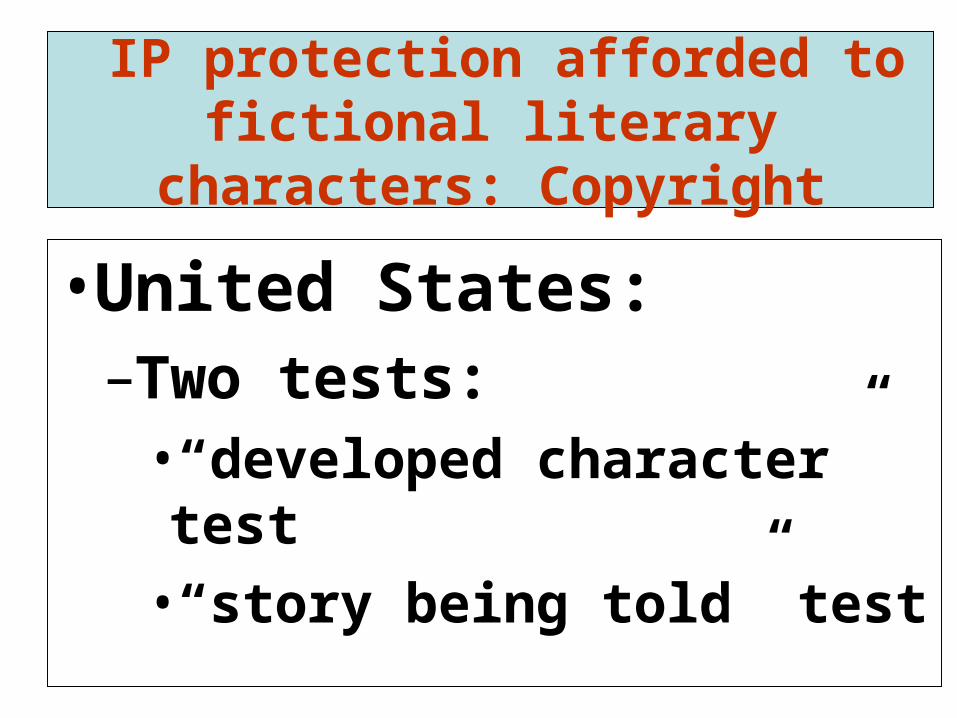

IP protection afforded to fictional literary characters: Copyright

• Courts in the US have dealt with this issue extensively, and have developed two tests for whether a character deserves copyright protection apart from the story

• Canada has very limited case law on the subject

IP protection afforded to fictional literary characters: Copyright

• United States:–Two tests:

•“developed character” test

•“story being told” test

IP protection afforded to fictional literary characters: Copyright

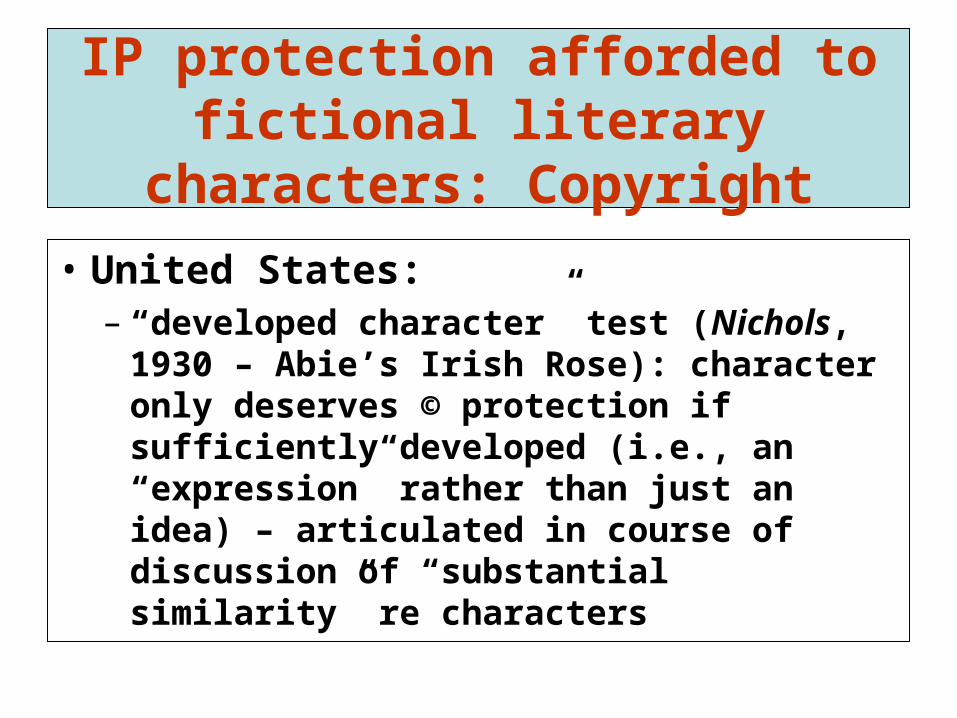

• United States:– “developed character” test (Nichols, 1930

– Abie’s Irish Rose): character only deserves © protection if sufficiently developed (i.e., an “expression” rather than just an idea) – articulated in course of discussion of “substantial similarity” re characters

IP protection afforded to fictional literary characters: Copyright

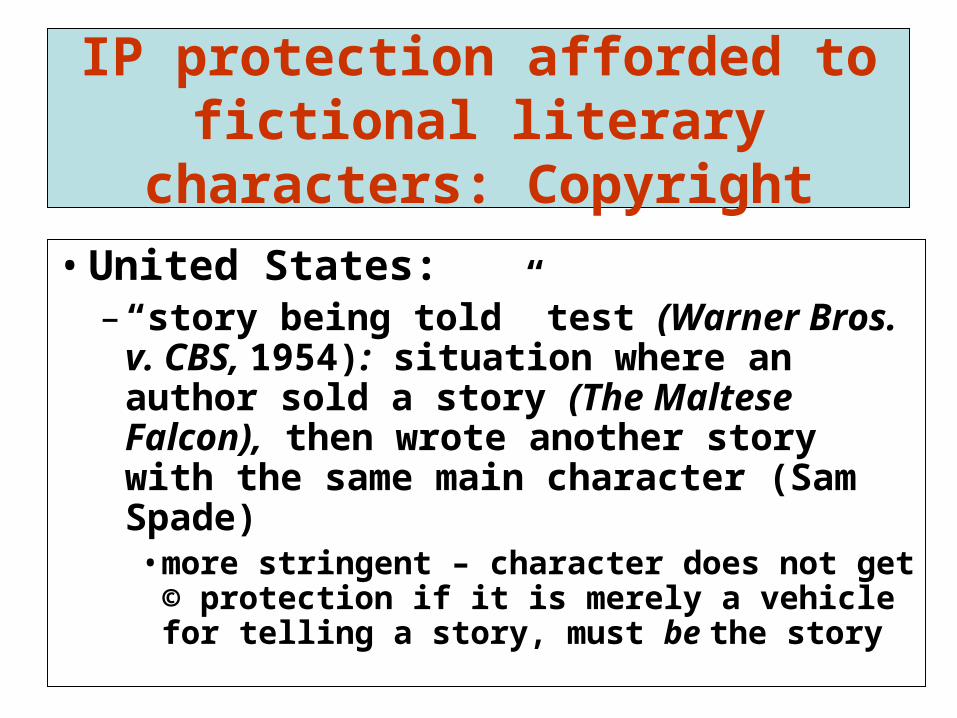

• United States:– “story being told” test (Warner Bros.

v. CBS, 1954): situation where an author sold a story (The Maltese Falcon), then wrote another story with the same main character (Sam Spade)• more stringent – character does not get

© protection if it is merely a vehicle for telling a story, must be the story

IP protection afforded to fictional literary characters: Copyright

• United States:– Tests used by different circuits– So scope of protection of literary

characters independent of plot is unclear– Turns on problems with drawing the line in

idea/expression dichotomy (i.e., when does a character become an expression rather than a mere idea)

IP protection afforded to fictional literary characters: Copyright

• Canada:– Preston v. 20th Century Fox Canada Ltd. (1990,

affirmed 1993) – “Ewoks” case• To deserve © protection, character must be

sufficiently clearly delineated in the work subject to copyright that it has become widely known and recognized

• Draws on Nichols• Problematic because extent to which known is not a

factor in copyright infringement – slips over into passing off

Anne of Green Gables Trade-Mar

IP protection afforded to fictional characters: Trade-mark

• Protection of literary characters in trade-mark in Canada:– Name (I’ll focus on this)– Pictorial representation– Distinguishing guise

• Trade-marks are perpetual, provided they are used continuously (and the registration is regularly renewed)

• Common law trade-mark rights (i.e. protection against passing-off) extends only as far as it is known/the owner has a reputation to protect

• All linked to consumer protection from confusion as to source

IP protection afforded to fictional characters: Trade-mark

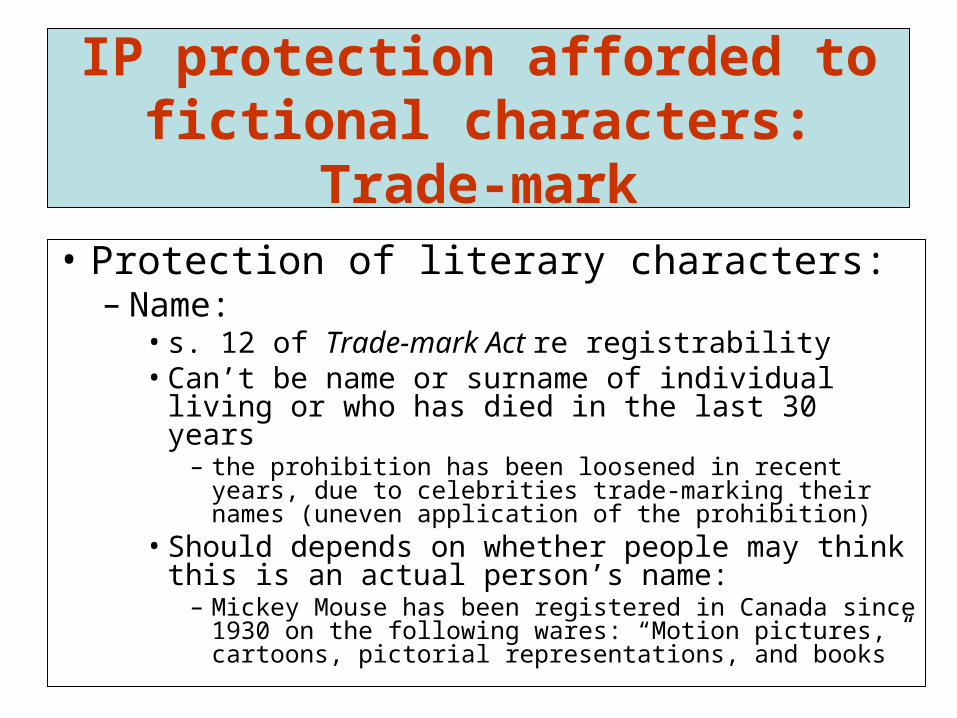

• Protection of literary characters:– Name:

• s. 12 of Trade-mark Act re registrability• Can’t be name or surname of individual living or

who has died in the last 30 years– the prohibition has been loosened in recent years, due to

celebrities trade-marking their names (uneven application of the prohibition)

• Should depends on whether people may think this is an actual person’s name:

– Mickey Mouse has been registered in Canada since 1930 on the following wares: “Motion pictures, cartoons, pictorial representations, and books”

IP protection afforded to fictional characters: Trade-mark

• Protection of literary characters:– Name:

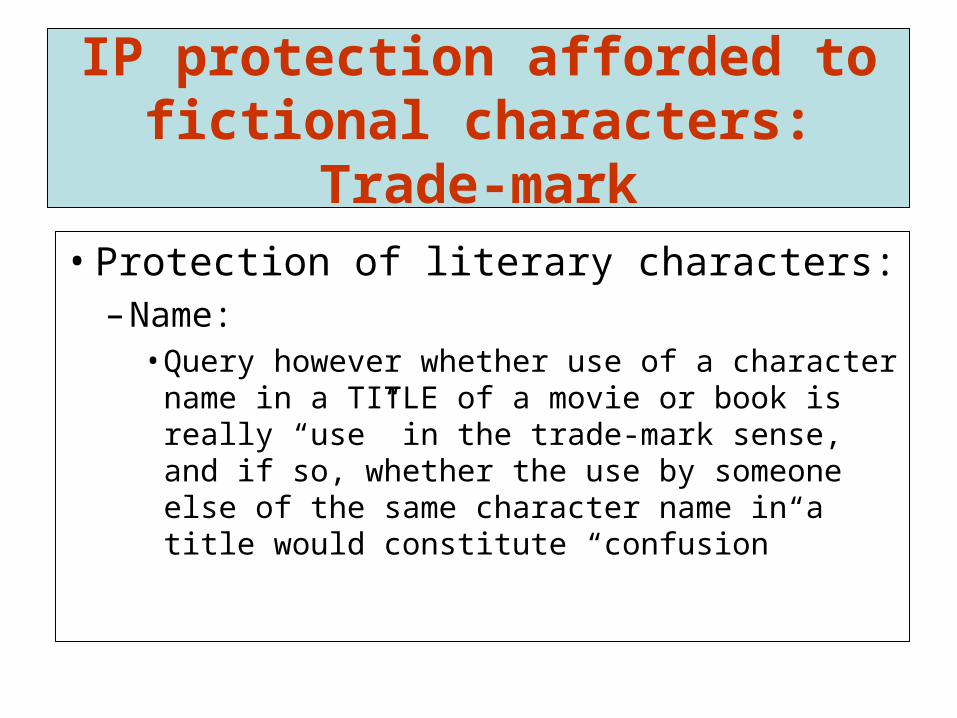

• Query however whether use of a character name in a TITLE of a movie or book is really “use” in the trade-mark sense, and if so, whether the use by someone else of the same character name in a title would constitute “confusion”

IP protection afforded to fictional characters: Trade-mark

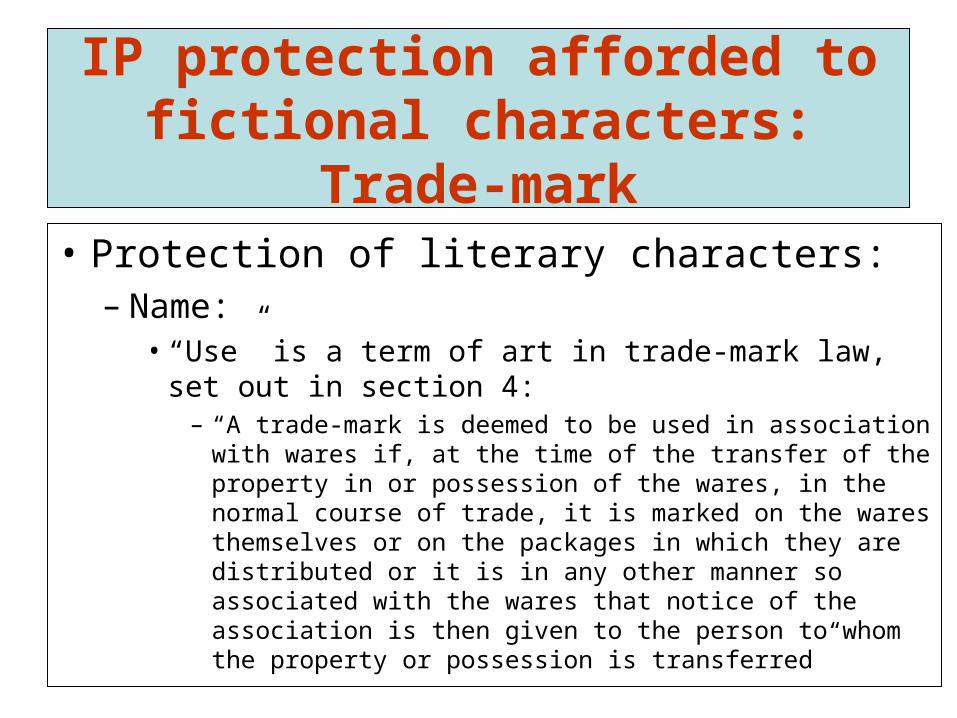

• Protection of literary characters:– Name:

• “Use” is a term of art in trade-mark law, set out in section 4:

– “A trade-mark is deemed to be used in association with wares if, at the time of the transfer of the property in or possession of the wares, in the normal course of trade, it is marked on the wares themselves or on the packages in which they are distributed or it is in any other manner so associated with the wares that notice of the association is then given to the person to whom the property or possession is transferred”

IP protection afforded to fictional characters: Trade-mark

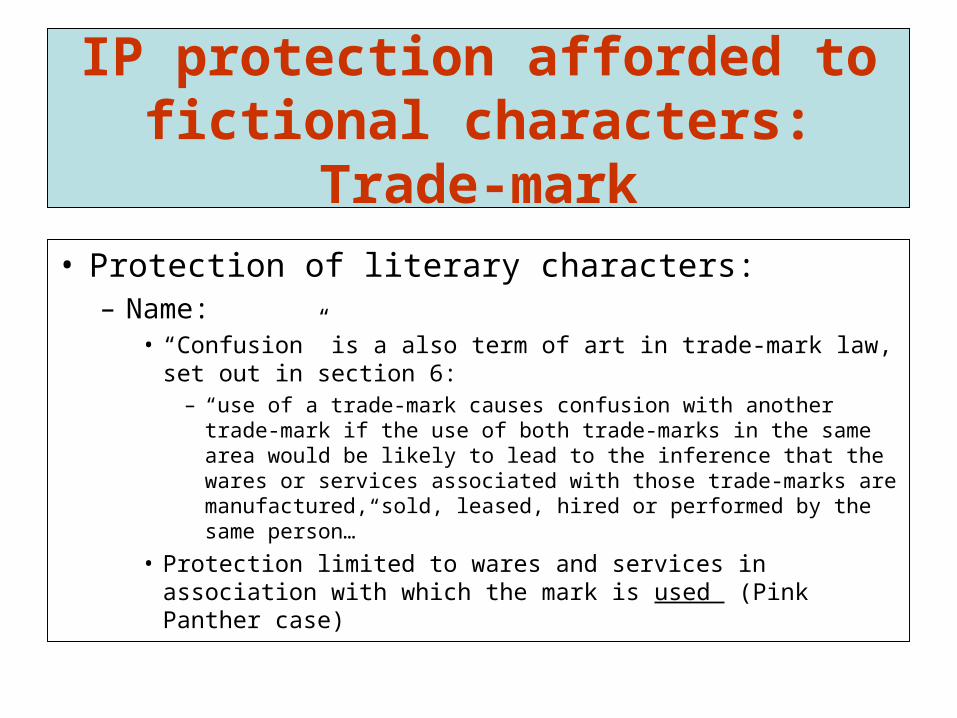

• Protection of literary characters:– Name:

• “Confusion” is a also term of art in trade-mark law, set out in section 6:

– “use of a trade-mark causes confusion with another trade-mark if the use of both trade-marks in the same area would be likely to lead to the inference that the wares or services associated with those trade-marks are manufactured, sold, leased, hired or performed by the same person…”

• Protection limited to wares and services in association with which the mark is used (Pink Panther case)

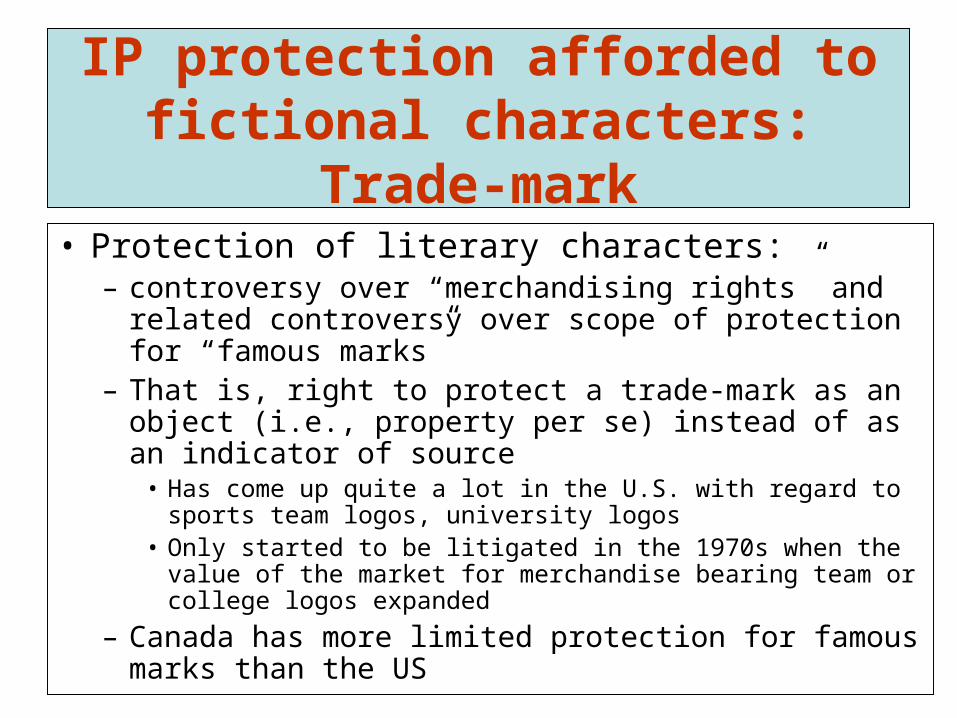

IP protection afforded to fictional characters: Trade-mark

• Protection of literary characters:– controversy over “merchandising rights” and related

controversy over scope of protection for “famous marks”

– That is, right to protect a trade-mark as an object (i.e., property per se) instead of as an indicator of source

• Has come up quite a lot in the U.S. with regard to sports team logos, university logos

• Only started to be litigated in the 1970s when the value of the market for merchandise bearing team or college logos expanded

– Canada has more limited protection for famous marks than the US

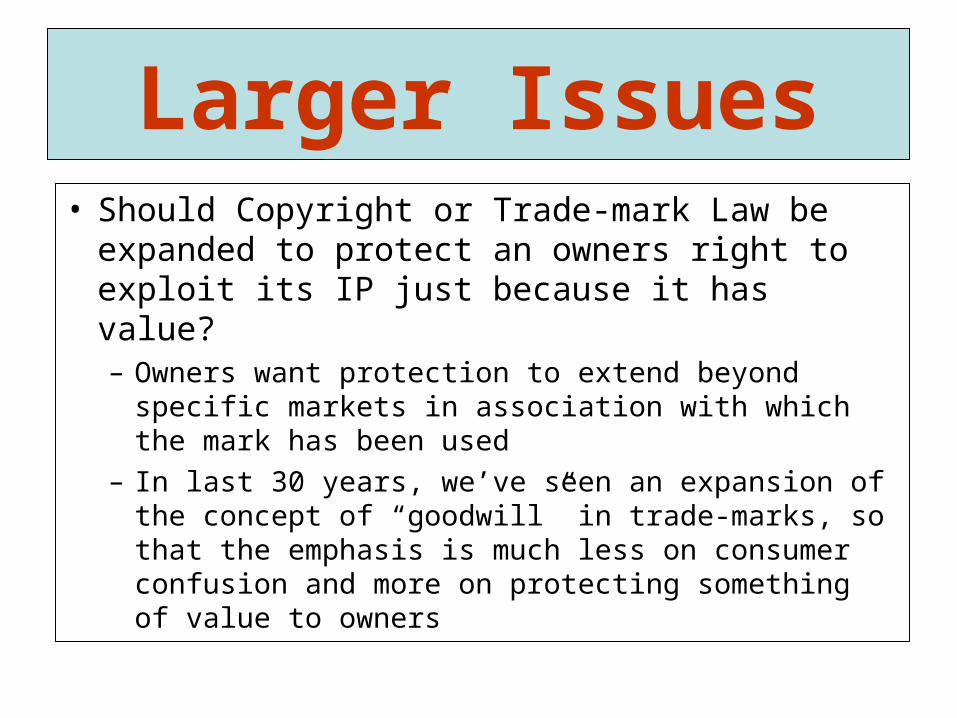

Larger Issues• Should Copyright or Trade-mark Law be

expanded to protect an owners right to exploit its IP just because it has value?– Owners want protection to extend beyond specific

markets in association with which the mark has been used

– In last 30 years, we’ve seen an expansion of the concept of “goodwill” in trade-marks, so that the emphasis is much less on consumer confusion and more on protecting something of value to owners

Larger Issues• Should Copyright or Trade-mark Law be

expanded to protect an owners right to exploit its IP just because it has value?– Value increasingly seen as potential to make money,

rather than something which has established meaning (i.e., as indicator of quality, source)

– Litman: too strong TM protection “arrogates to the producer the entire value of cultural icons that we should more appropriately treat as collectively owned”

• Is this especially true for TMs based on cultural products?

Overlap between copyright and trademark

• Back to IP protection for literary characters:– The above noted controversies in the

expansion of trade-mark protection become particularly acute when a literary work enters the public domain

– Entrance of work into public domain may be thwarted by expanded trade-mark protection, which may be perpetually extended

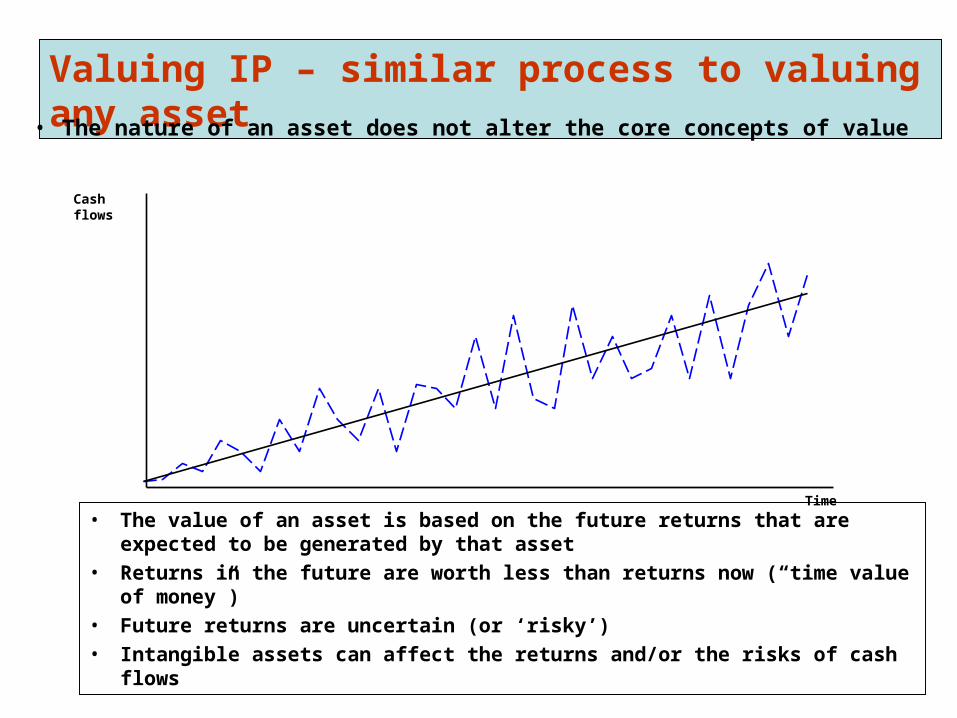

Valuing IP – similar process to valuing any asset• The nature of an asset does not alter the core concepts of value

• The value of an asset is based on the future returns that are expected to be generated by that asset

• Returns in the future are worth less than returns now (“time value of money”)

• Future returns are uncertain (or ‘risky’)

• Intangible assets can affect the returns and/or the risks of cash flows

Cash flows

Time

Valuing IP – similar process to valuing any asset

Open market value

Value in use

Fair value

Liquidation value

Book value

Determine basis/context of

valuation

Select and apply appropriate valuation

methodologies

Copyright

Database

Trade mark / passing off

Patent

Know-how / trade-secrets

Design right

Identify asset(s) / understand rights

Calculate the incremental value added by the IP

Valuing IP – similar process to valuing any asset, only harder

• Intangibles are often composite assets. Value is realised in combination with other assets (tangible and intangible)e.g. brand – value in combination of

– trade marks (registered; rights in passing off)– trade dress– copyright– logo– get-up– recipes/formulaen.b. trade mark licence v. brand v. branded business

• Value may depend on form and scope of legal rights protecting the asset

• Values can vary hugely depending on circumstances– between uses– between users– over time

• Availability of information/incomplete data

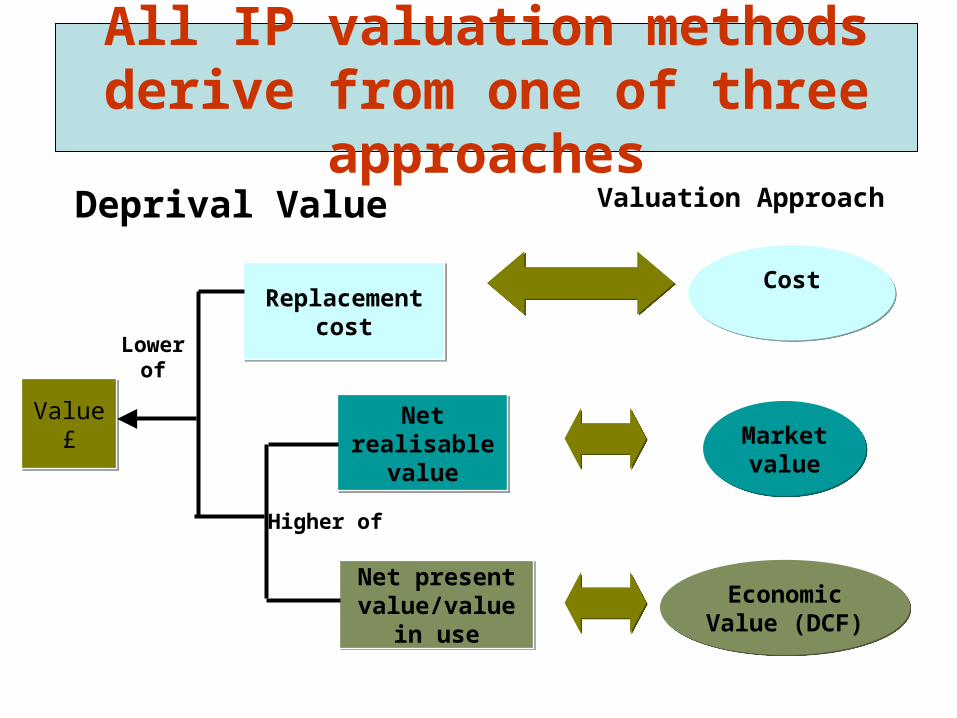

Approach to Value

• Cost Approach

• Market Approach

• Income Approach

All IP valuation methods derive from one of three approaches

Deprival Value

Value£

Value£

Replacementcost

Replacementcost

Net realisable

value

Net realisable

value

Net present value/value in

use

Net present value/value in

use

Lower of

Higher of

Valuation Approach

Marketvalue

Marketvalue

CostCost

EconomicValue (DCF)Economic

Value (DCF)

Market Approach Cost ApproachIncome Approach

Excess Earnings Method

Relief from Royalty Method

Incremental Cash Flow Method

Most recent comparable transactions / Multiples

Current price on active market

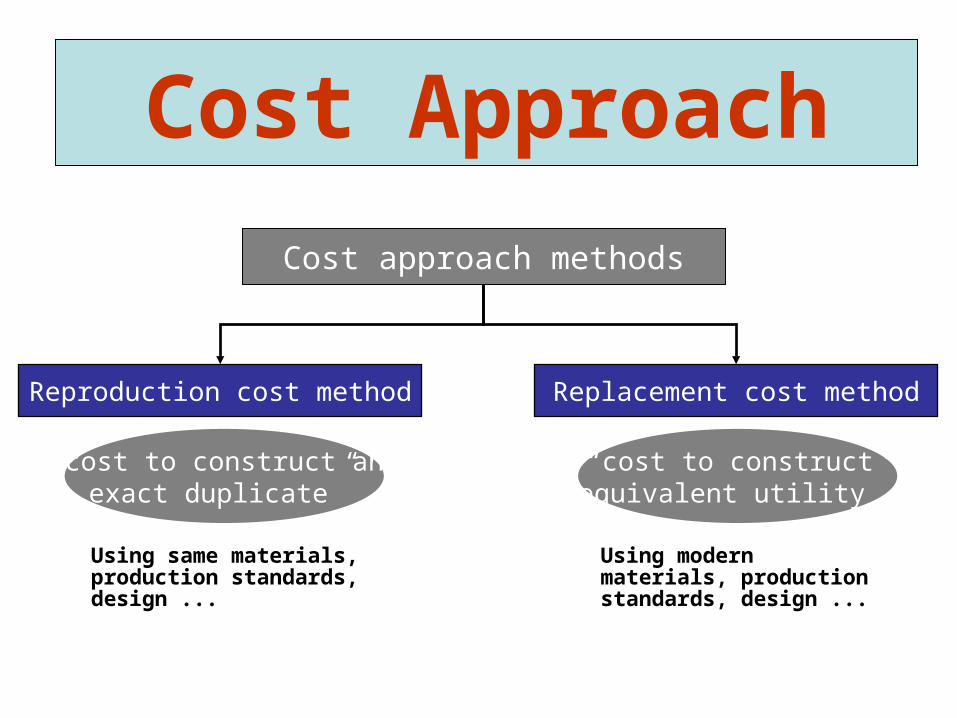

Replacement Cost Method

Reproduction Cost Method

Intangible Asset Valuation Valuation techniques for Financial Reporting

- Overview

Valuation Techniques

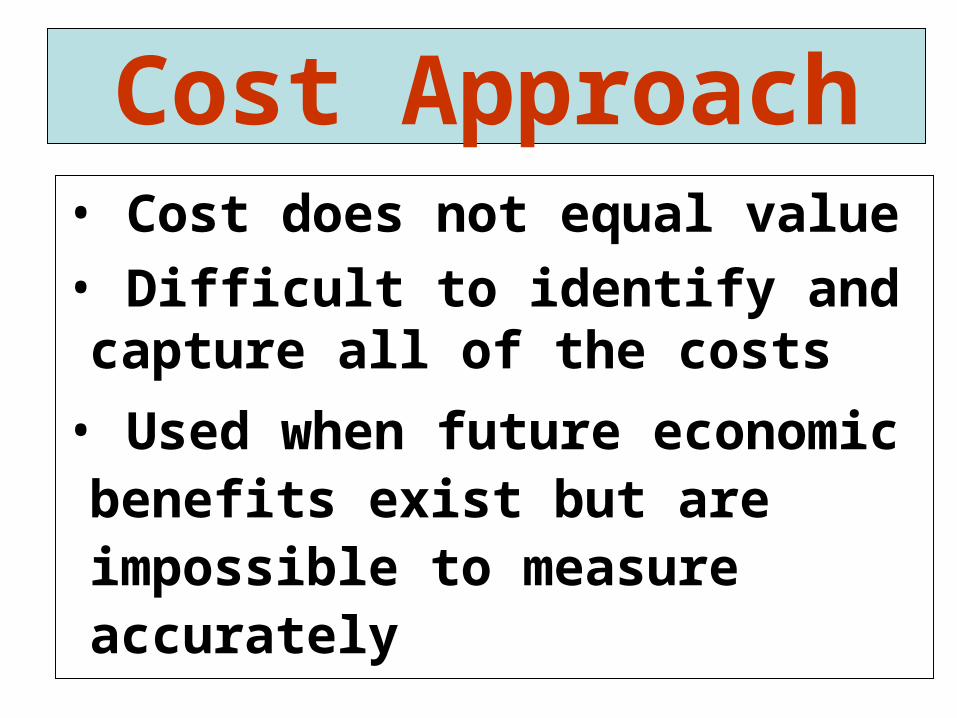

“An investor will pay no more for an asset than the cost to purchase or construct an asset of equal utility!”

Cost ApproachPremise of Value

Cost Approach• Cost does not equal value

• Difficult to identify and capture all of the costs

• Used when future economic benefits exist but are impossible to measure accurately

Cost approach methods

Replacement cost methodReproduction cost method

Using same materials, production standards, design ...

Using modern materials, production standards, design ...

“cost to construct an exact duplicate”

“cost to construct equivalent utility”

Cost Approach

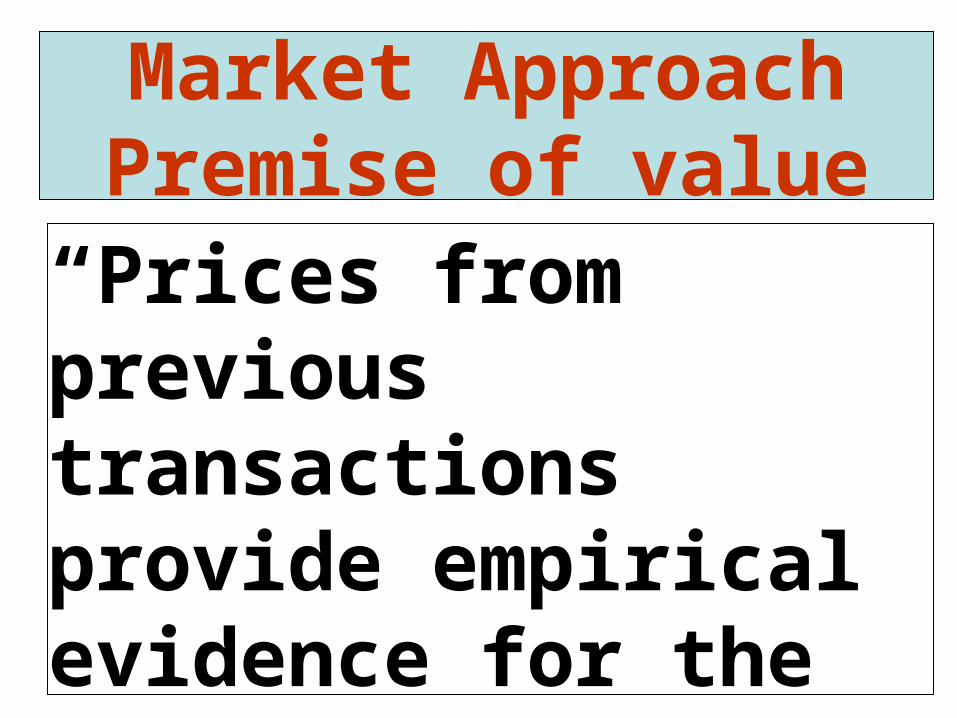

“Prices from previous transactions provide empirical evidence for the value of an intangible asset”

Market ApproachPremise of value

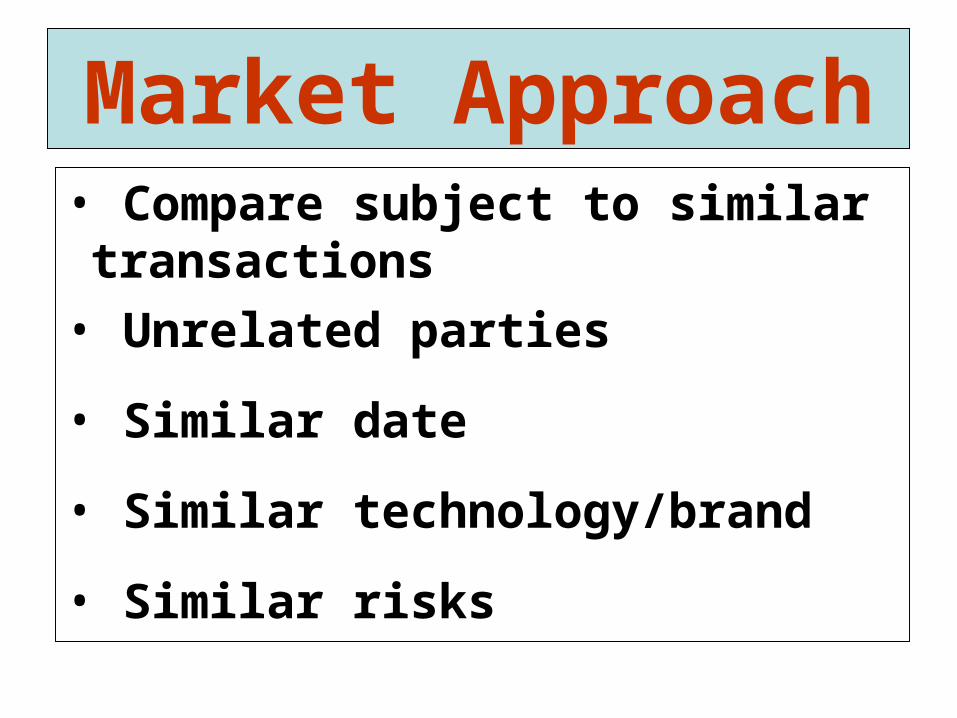

Market Approach• Compare subject to similar transactions

• Unrelated parties

• Similar date

• Similar technology/brand

• Similar risks

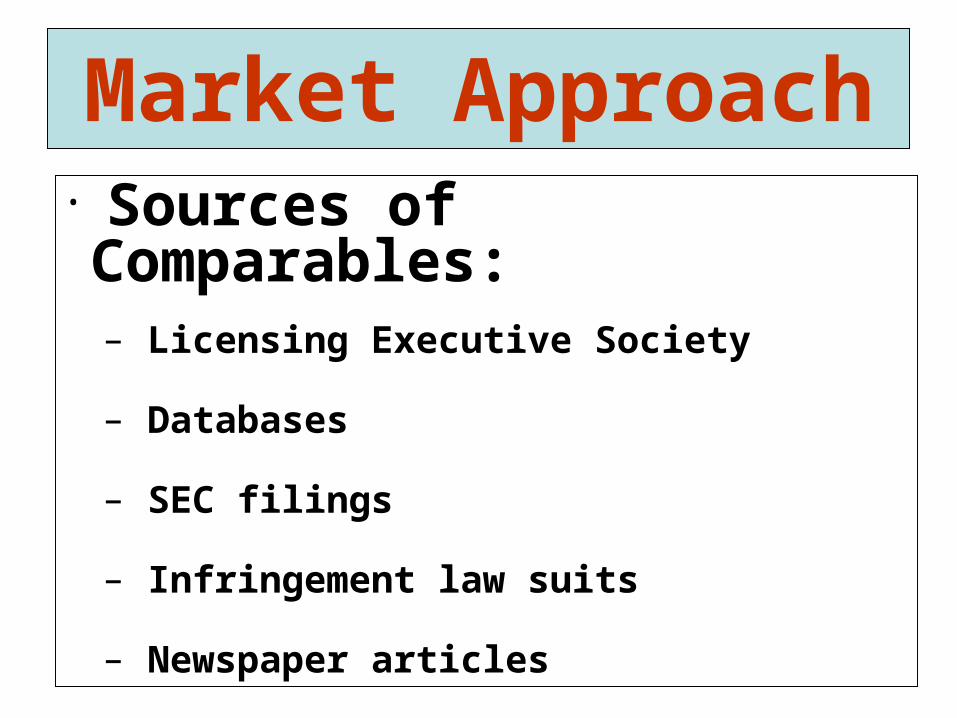

• Sources of Comparables:

– Licensing Executive Society

– Databases

– SEC filings

– Infringement law suits

– Newspaper articles

Market ApproachMarket Approach

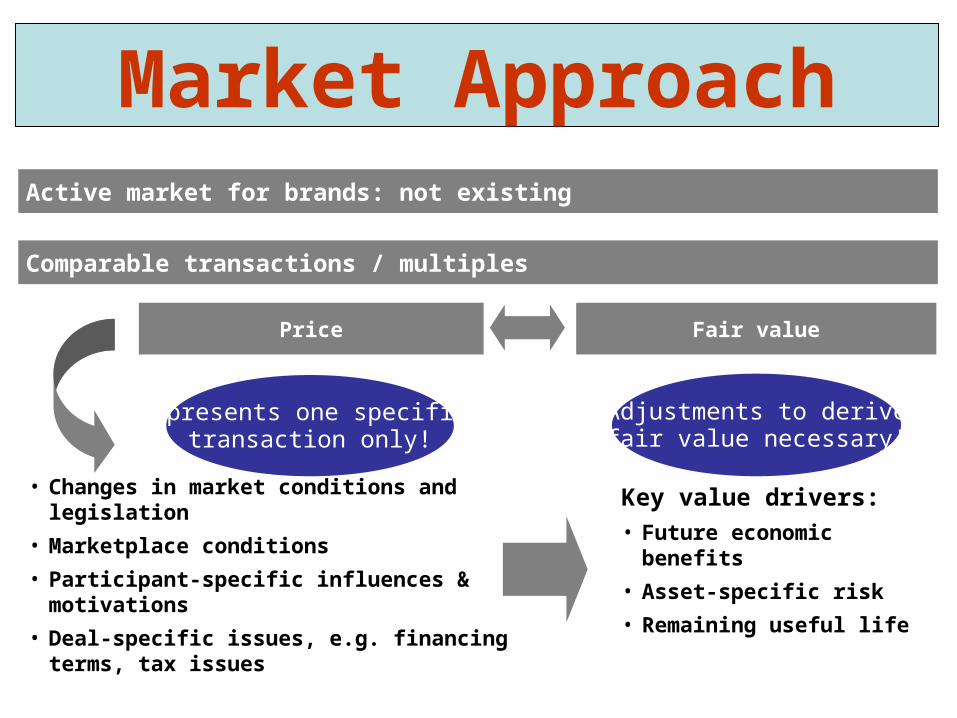

Represents one specific transaction only!

Adjustments to derivefair value necessary!

Price Fair value

• Changes in market conditions and legislation

• Marketplace conditions

• Participant-specific influences & motivations

• Deal-specific issues, e.g. financing terms, tax issues

Market ApproachActive market for brands: not existing

Comparable transactions / multiples

Key value drivers:• Future economic benefits

• Asset-specific risk

• Remaining useful life

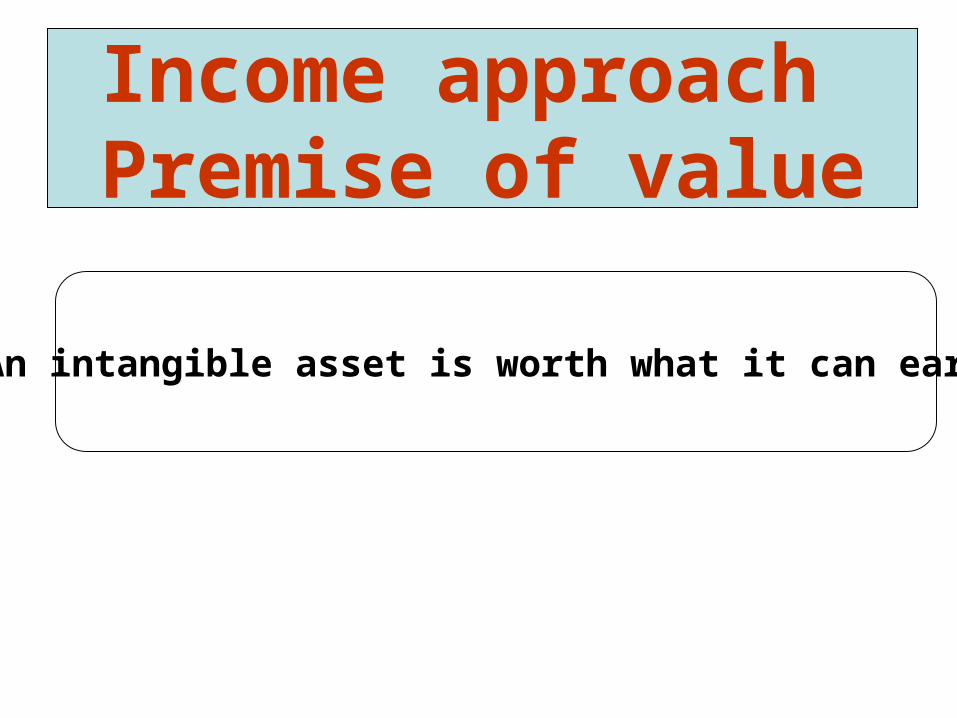

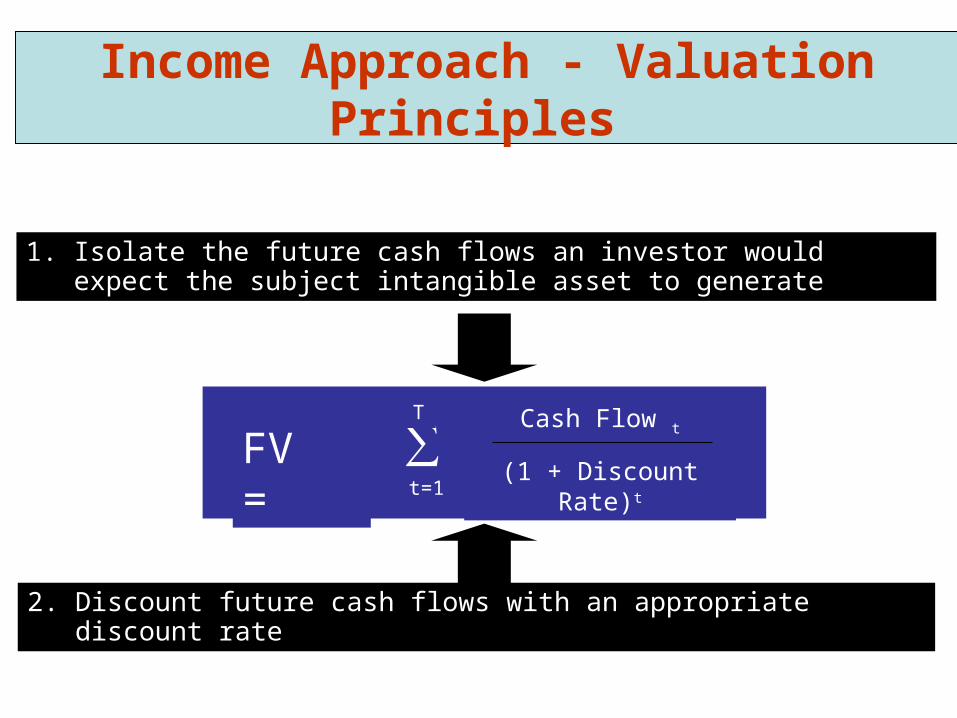

“An intangible asset is worth what it can earn!”

Income approach Premise of value

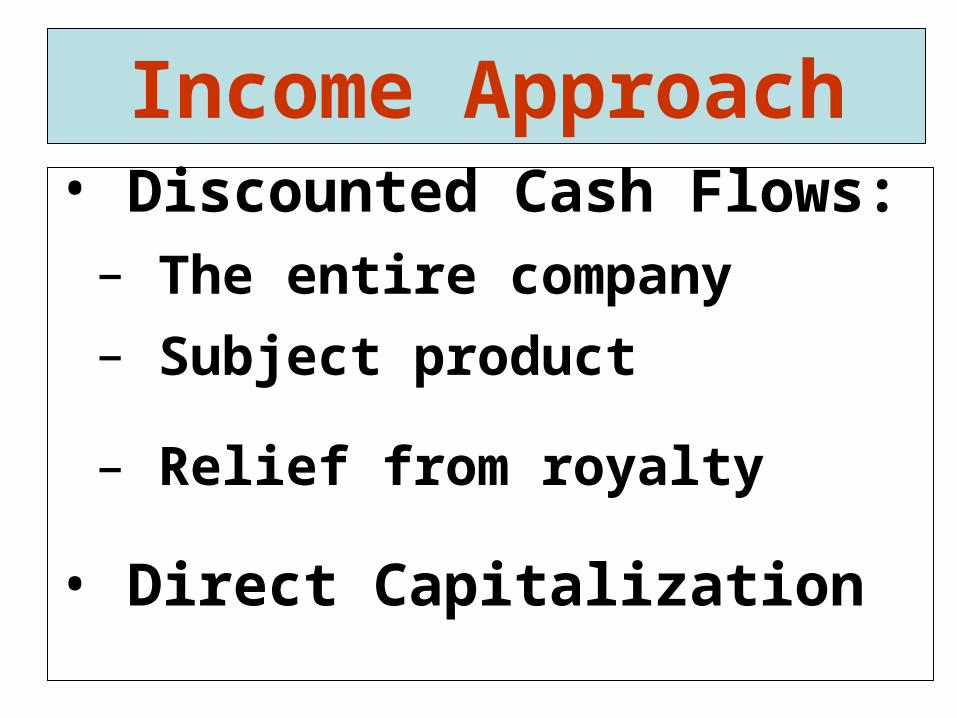

Income Approach• Discounted Cash Flows:

– The entire company

– Subject product

– Relief from royalty

• Direct Capitalization

Income Approach - Valuation Principles

1. Isolate the future cash flows an investor would expect the subject intangible asset to generate

2. Discount future cash flows with an appropriate discount rate

FV =Cash Flow t

(1 + Discount Rate)t∑ t=1

T

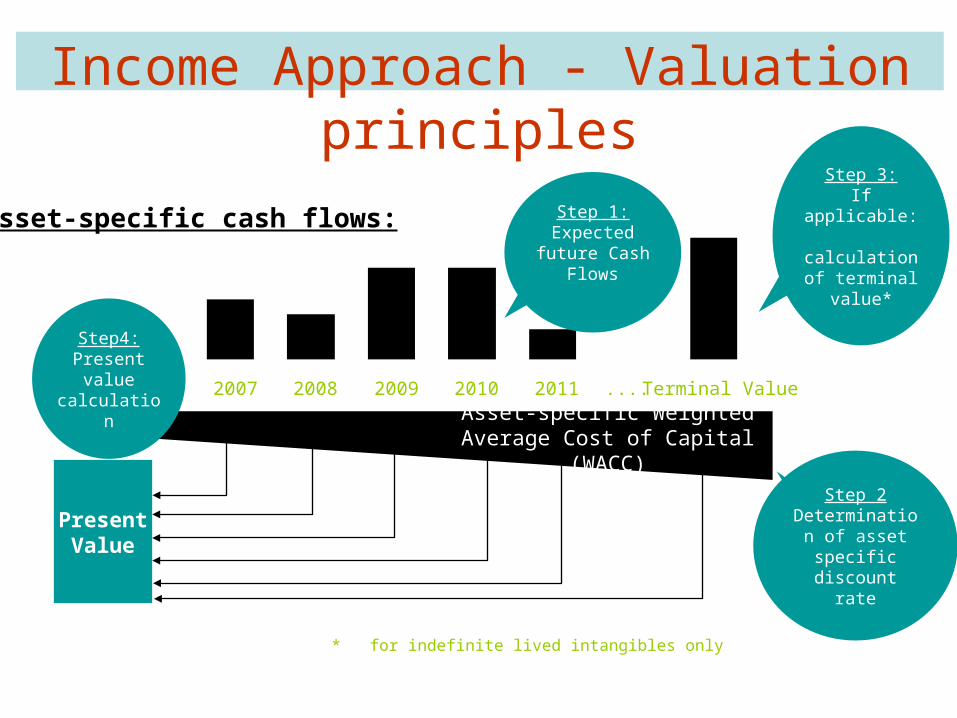

2007 2008 2009 2010 2011 .... Terminal Value

Asset-specific cash flows:

Step 2Determination

of asset specific discount rate

Step 1:Expected future

Cash Flows

Asset-specific Weighted Average Cost of Capital (WACC)

PresentValue

Step 3:If applicable: calculation of

terminal value*

Step4:Present value

calculation

Income Approach - Valuation principles

* for indefinite lived intangibles only

Relief-from-royalty method Concept

relieves owner

The royalty savings are the expected cash flows for the subject intangible asset!

from paying royalty rateOwnership of the asset

e.g. trademark

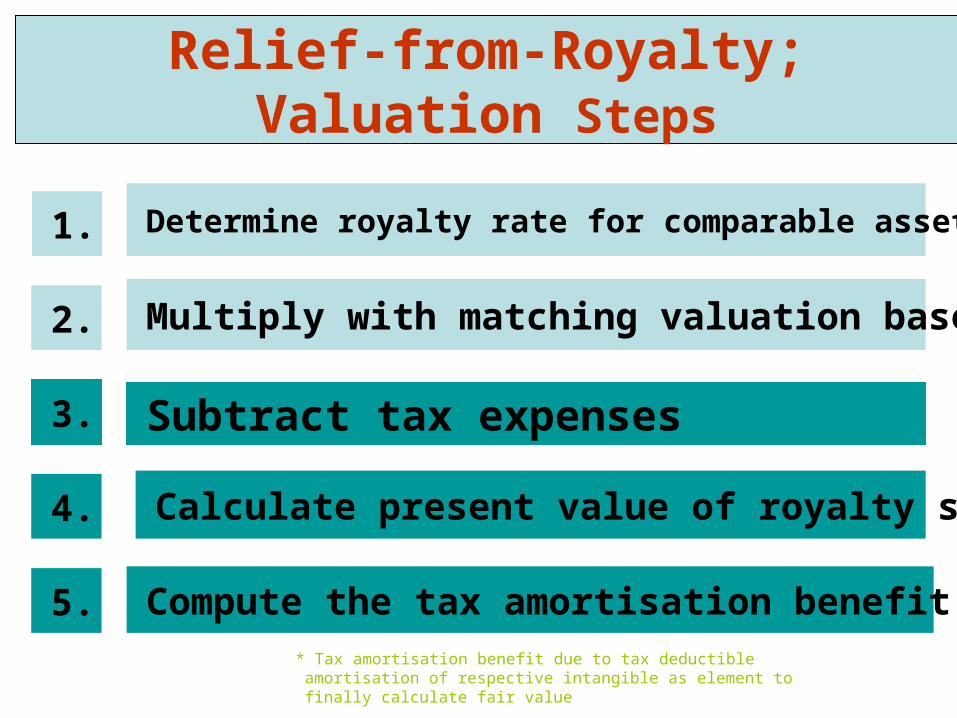

Relief-from-Royalty; Valuation Steps

Determine royalty rate for comparable asset1.

Subtract tax expenses3.

Multiply with matching valuation base2.

Calculate present value of royalty savings4.

Compute the tax amortisation benefit (TAB*)5.* Tax amortisation benefit due to tax deductible amortisation of respective

intangible as element to finally calculate fair value

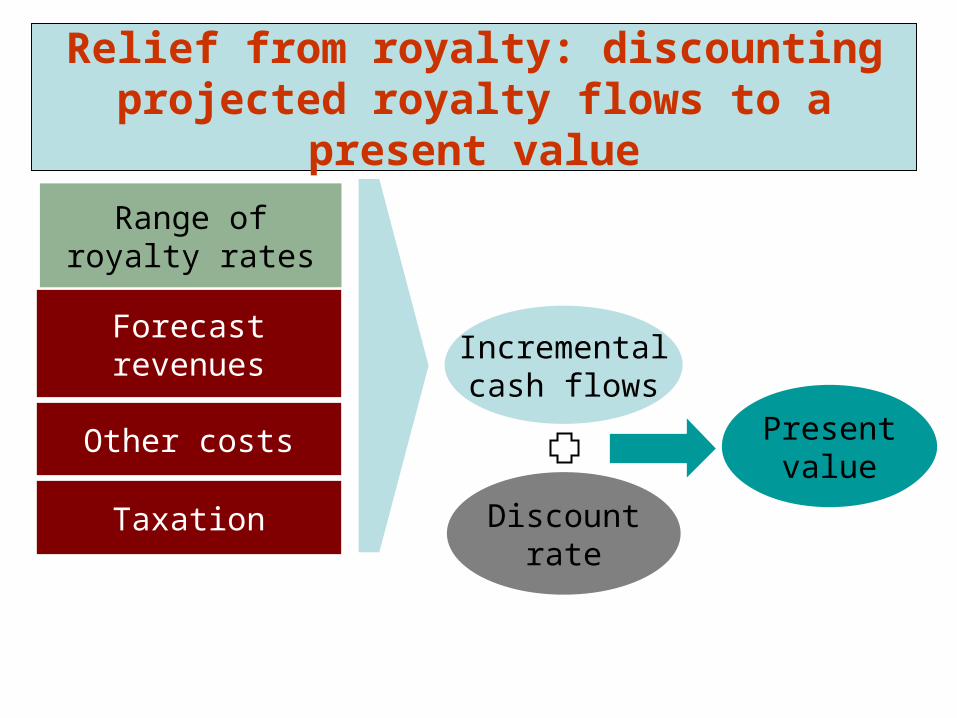

Relief from royalty: discounting projected royalty flows to a present value

Range ofroyalty rates

Taxation

Incrementalcash flows

Discountrate

Presentvalue

Forecast revenues

Other costs

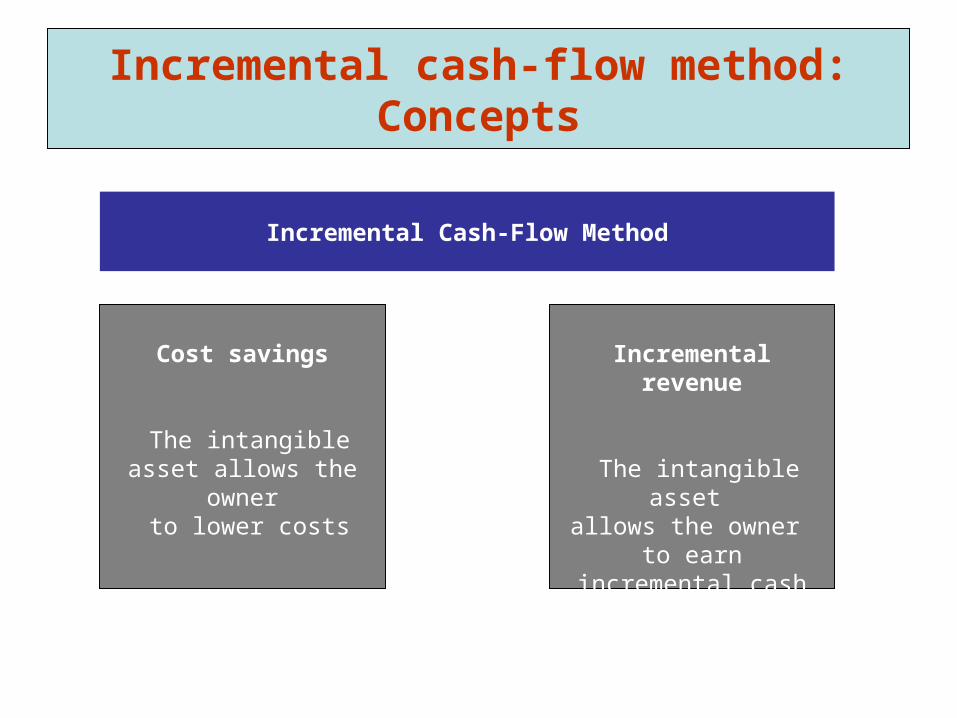

Incremental cash-flow method: Concepts

Cost savings

The intangible asset allows the owner to lower costs

Incremental Cash-Flow Method

Incremental revenue

The intangible asset allows the owner

to earn incremental cash flows, e.g. to charge a

price-premium

Incremental cash-flow methodValuation steps

Derive pre-tax incremental cash flows of subject intangible1.

Consider incremental contributory asset charges (CAC)3.

Subtract tax expenses2.

Calculate present value of incremental cash flows4.

Compute the tax amortisation benefit (TAB*)5.

* Tax amortisation benefit due to tax deductible amortisation of respective intangible as element to finally calculate fair value

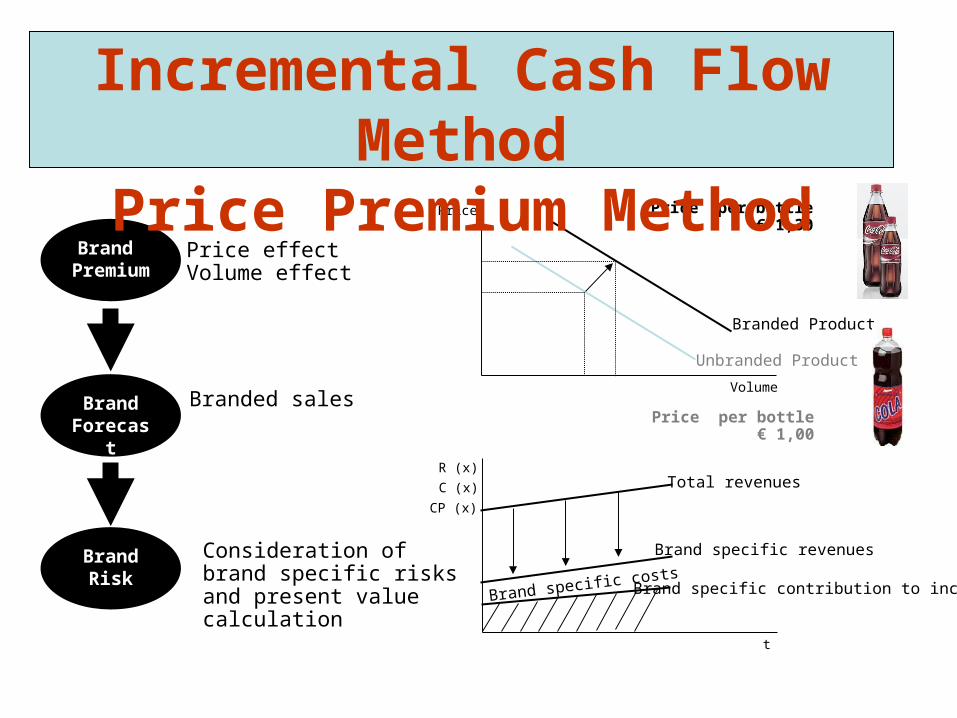

Brand Premium

Brand Forecast

BrandRisk

Branded sales

Price effectVolume effect

Consideration of brand specific risks and present value calculation

Volume

Price

Branded Product

Unbranded Product

Price per bottle€ 1,30

Price per bottle€ 1,00

t

R (x)Total revenues

Brand specific revenues

Brand specific contribution to incomeBrand specific costs

C (x)

CP (x)

Incremental Cash Flow MethodPrice Premium Method

Incremental Cash Flow Method Example

fromFair value 2007

mill. EUR

Price effect 0.15 x 300,000 45.000

Quantity effect 1.65 x 50,000 82.500EBITDA-margin (after CAC) @ 55% 45.375

Pre-tax incremental cash flows 90.375Corporate taxes @ 35% 31.631After-tax incremental cash flows 58.744Discount Rate @ 10% 0,9Present value after-tax incremental cash flows 53.403Tax amortisation benefit 16.021Fair value 69.424

Step-up Factor TAB 1,3

Company xyzValuation of brand

Valuation Date: January 1, 2007Incremental cash flows

Economic value methods – illustrative brand valuation

•Consumer•Business•Consumer•Business

•Premium services•Premium services

•Mix of services•Mix of services

Brand extension•products / services•channels•sector / geography

Brand extension•products / services•channels•sector / geography

Brand loyalty•certainty of demandBrand loyalty•certainty of demand

Demand side factors

Incremental cash flows

Supply side factors

Volumes x Prices x Margins – Capex / Working capital Risk and return

Customer acquisition / retention

Customer acquisition / retention

Staff acquisition / retentionStaff acquisition / retention

Brand supportBrand support

Brand extension costsBrand extension costs

Supply termsSupply terms Financial CapitalFinancial Capital

Economies of scale

Growth Value

Economic value methods – illustrative brand valuation

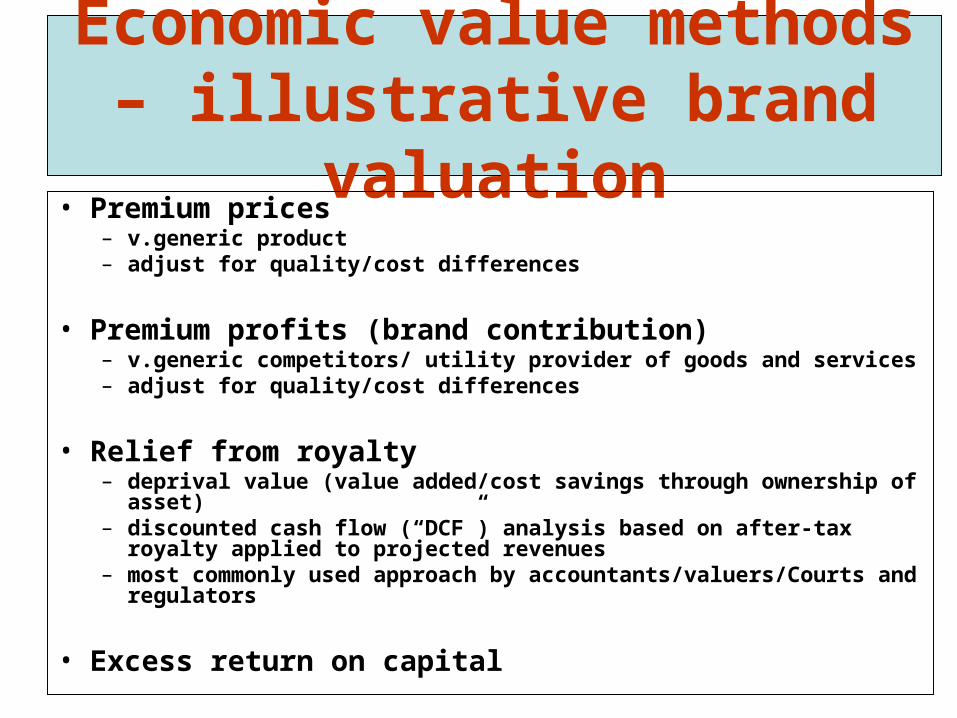

• Premium prices– v.generic product– adjust for quality/cost differences

• Premium profits (brand contribution)– v.generic competitors/ utility provider of goods and services– adjust for quality/cost differences

• Relief from royalty– deprival value (value added/cost savings through ownership of asset)– discounted cash flow (“DCF”) analysis based on after-tax royalty

applied to projected revenues– most commonly used approach by accountants/valuers/Courts and

regulators

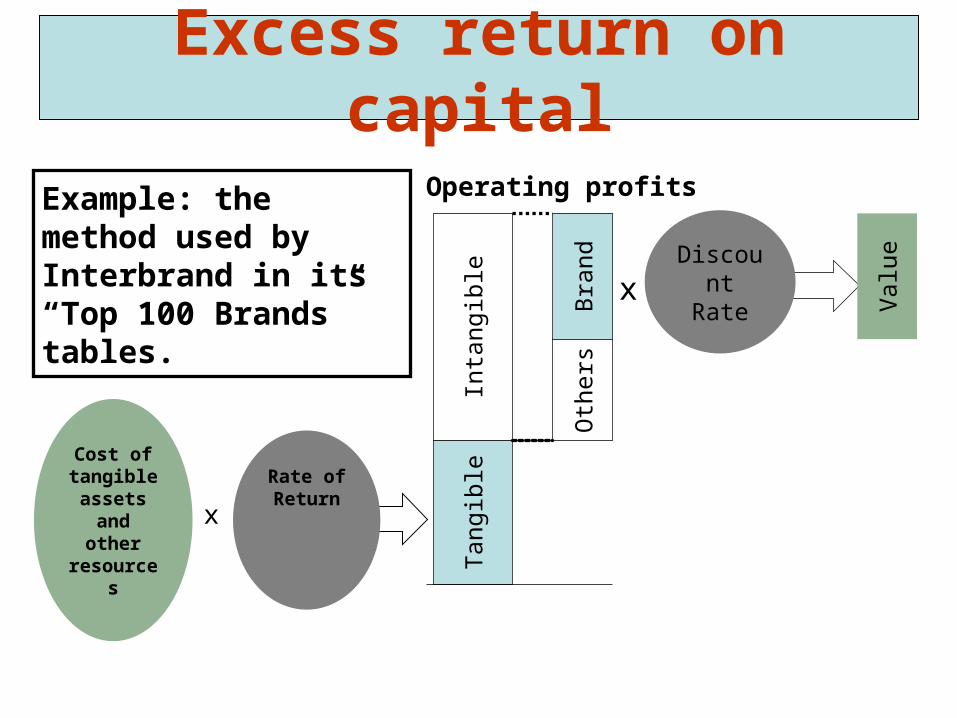

• Excess return on capital

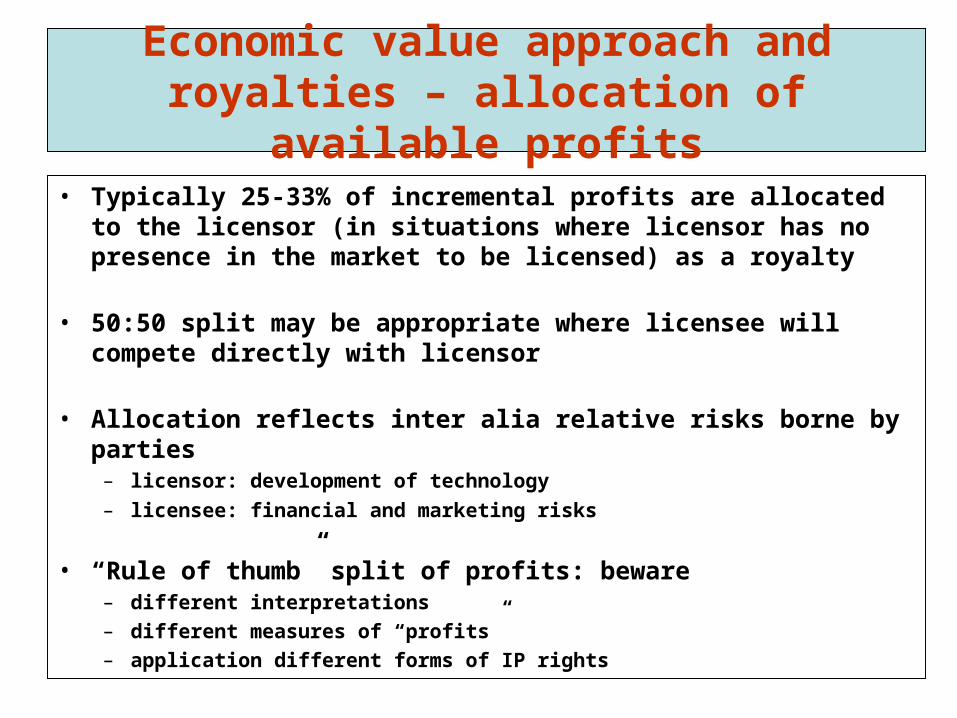

Economic value approach and royalties – allocation of available profits

• Typically 25-33% of incremental profits are allocated to the licensor (in situations where licensor has no presence in the market to be licensed) as a royalty

• 50:50 split may be appropriate where licensee will compete directly with licensor

• Allocation reflects inter alia relative risks borne by parties – licensor: development of technology

– licensee: financial and marketing risks

• “Rule of thumb” split of profits: beware– different interpretations– different measures of “profits”– application different forms of IP rights

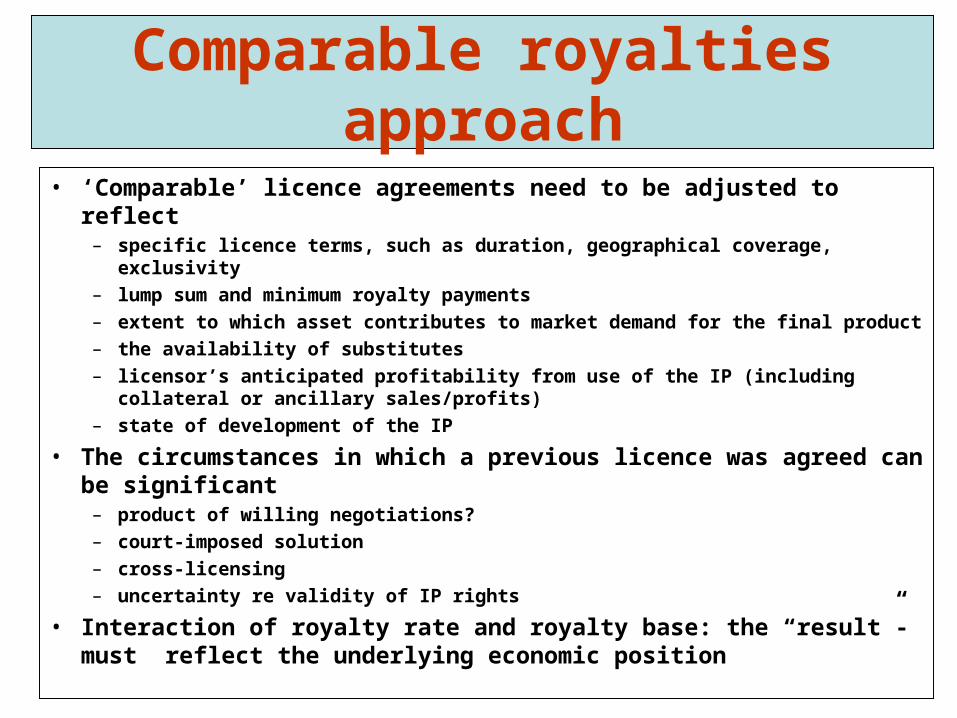

Comparable royalties approach

• ‘Comparable’ licence agreements need to be adjusted to reflect– specific licence terms, such as duration, geographical coverage, exclusivity– lump sum and minimum royalty payments– extent to which asset contributes to market demand for the final product– the availability of substitutes– licensor’s anticipated profitability from use of the IP (including collateral or

ancillary sales/profits)– state of development of the IP

• The circumstances in which a previous licence was agreed can be significant

– product of willing negotiations?– court-imposed solution– cross-licensing– uncertainty re validity of IP rights

• Interaction of royalty rate and royalty base: the “result”- must reflect the underlying economic position

Excess return on capital

Tan

gibl

eIn

tang

ible

Operating profits

Cost oftangible

assets and other

resources

Rate ofReturn

x

Bra

ndO

ther

s

Discount

Rate

Val

ue

x

Example: the method used by Interbrand in its “Top 100 Brands” tables.

Valuation Concepts and MethodsRemaining Useful Lifetime and Nature

of Analysis (IAS 38.90)• Expected usage of the asset

• Typical product life cycle for the asset

• Technical, technological, commercial or other types of obsolescence

• Changes in the market demand for the outputs from the asset

• Expected actions by competitors

• Level of maintenance expenditure required to obtain expected future economic benefits from the asset

• Legal factors (limitations)

• Period of control over the asset

• Dependence on the useful lifetime of other assets

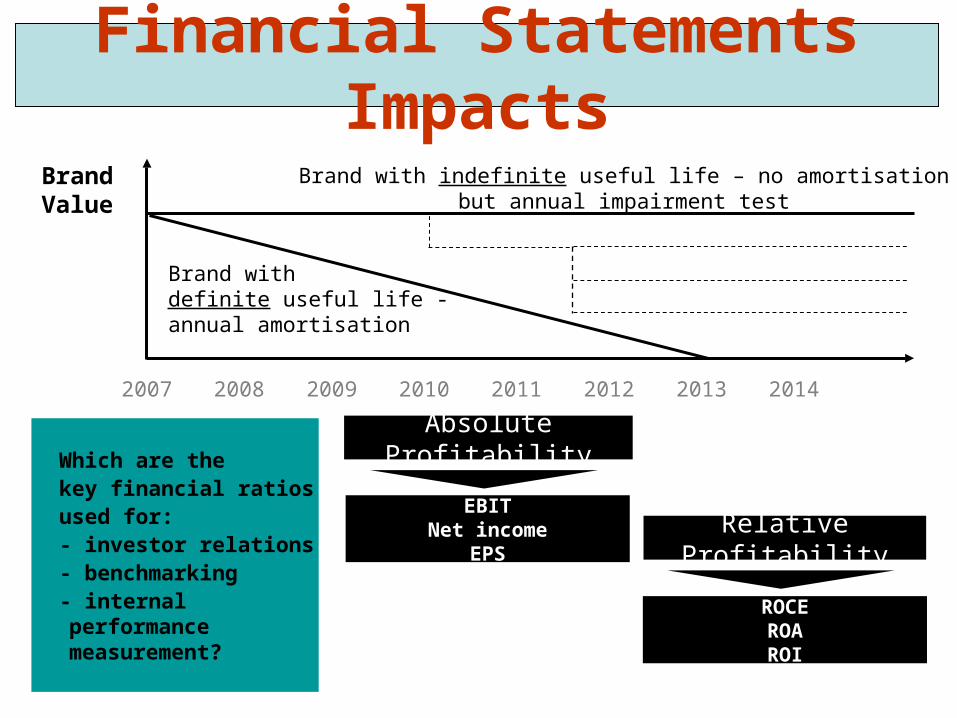

•. . . if no foreseeable limit: apply indefinite useful life

Brand with indefinite useful life – no amortisationbut annual impairment test

Brand Value

Financial Statements Impacts

2007 2008 2009 2010 2011 2012 2013 2014

Brand with definite useful life -annual amortisation

EBITNet income

EPS

ROCEROAROI

Absolute Profitability

Relative Profitability

Which are the key financial ratios used for:- investor relations- benchmarking- internal performance measurement?

Licensing Trademarks

• Twenty-five percent rule:– 25% of EBIT to licensor

– 75% of EBIT to licensee

• 25% EBIT/ Revenue = Royalty rate

Licensing Trademarks

• Commercial relationship:– Competitors

– Unrelated parties selling in different markets

– Franchisor / franchisee

– Manufacturer / distributor

Licensing Trademarks

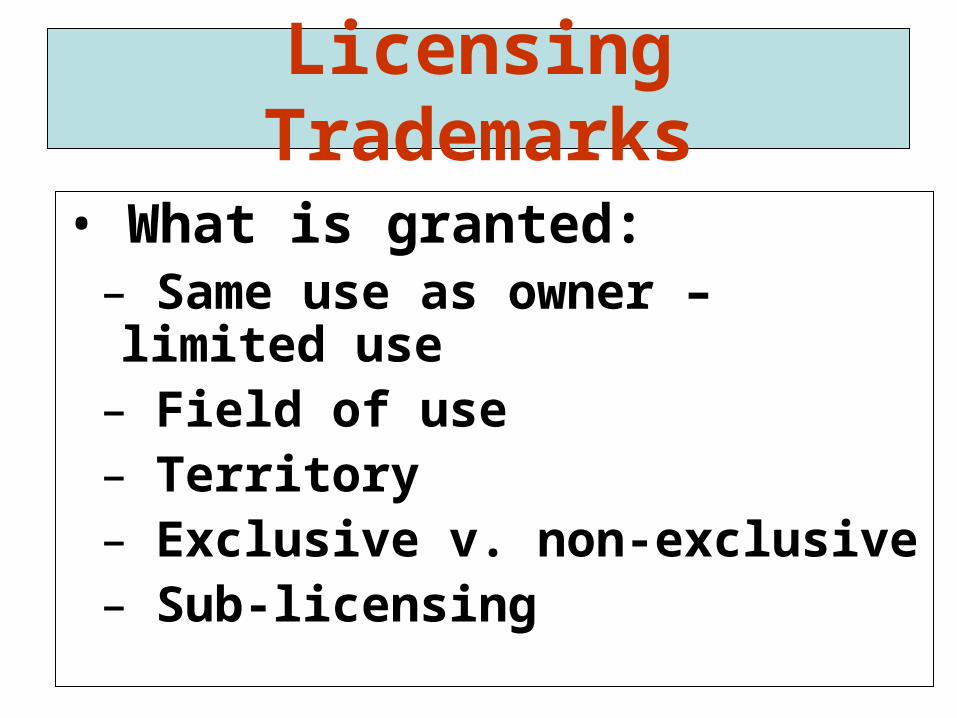

• What is granted:– Same use as owner – limited use

– Field of use – Territory– Exclusive v. non-exclusive– Sub-licensing

Licensing Trademarks

• Future profits derived from use of the trademark will determine the amount of the royalty– Method to use

• Income approach

• Market approach

Sport TrademarksTrademark Licensor Licensee

Royalty Rate (low)

Royalty Rate (high) Royalty Base

Exclusive or Nonexclusive

1 Gary Player Gary Player GroupAjay Leisure Products Inc. 3.00% 3.00%

Gross Wholesale Sales Exclusive

2 NautilusNautilus Wear International Bollinger Ind. Inc. 5.00% 5.00% Net Sales Non-exclusive

3 Kemper ImaginOn Inc Jaysport Int. Inc. 3.00% 3.00% Net SalesExclusive

sublicense

4 Victoriaville Warren Amendola, Sr.

Les Equipements Sportifs Davtec,

Inc. 2.00% 2.00% ? Exclusive

5 NFL NFL Properties Inc. Oxboro Outdoors

Inc. 11.00% 11.00% ? ?

6California Pro

Thunder California Pro Sports Playmaker 5.00% 5.00% All sales ?

7 LPGA LPGA S2 Golf Inc. 1.00% 5.00% Net Sales Non-exclusive

8 Nancy LopezNancy Lopez

Enterprises Inc S2 Golf Inc. 3.00% 3.50% ? Exclusive

9 Kemper ImaginOn Inc

United Merchandising

Corp. 7.50% 7.50% Cost to licensee Non-exclusive

10 Victoriaville Warren Amendola, Sr. USA Skate Co. 1.00% 1.00% ? Exclusive

4.15% 4.60%

3.00% 4.60%

Trademark Royalty Rates -- Sporting Goods Industry

Average Royalty Rate

Median Royalty Rate

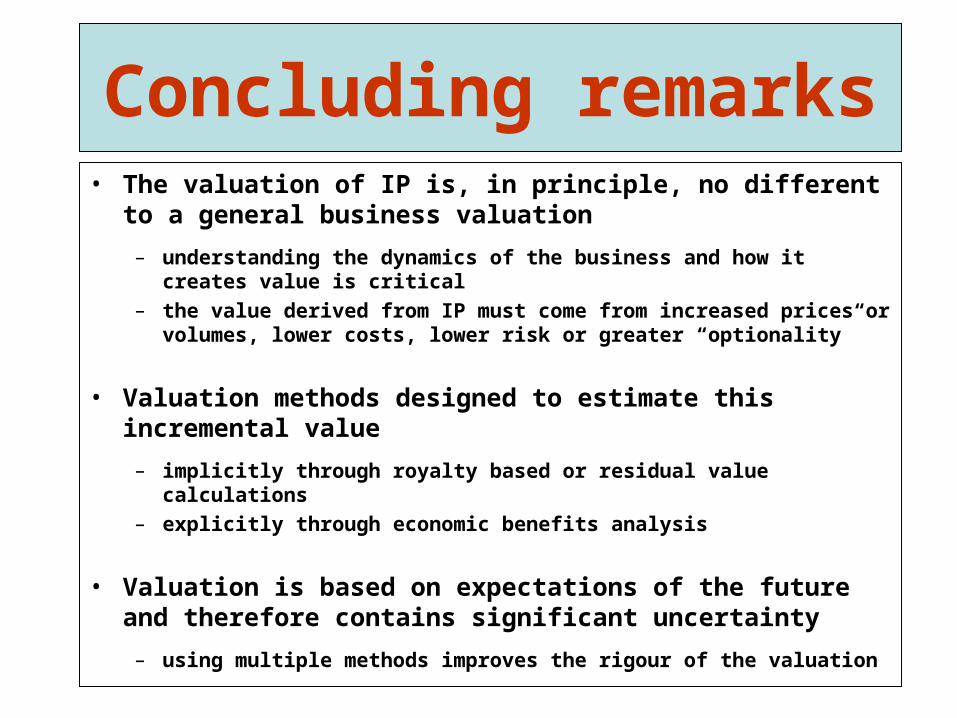

Concluding remarks• The valuation of IP is, in principle, no different to a general

business valuation

– understanding the dynamics of the business and how it creates value is critical

– the value derived from IP must come from increased prices or volumes, lower costs, lower risk or greater “optionality”

• Valuation methods designed to estimate this incremental value

– implicitly through royalty based or residual value calculations– explicitly through economic benefits analysis

• Valuation is based on expectations of the future and therefore contains significant uncertainty

– using multiple methods improves the rigour of the valuation

Related Documents