Chapter Two Consolidatio n of Financial Information Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Chapter Two Consolidation of Financial Information Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter Two

Consolidation of Financial

Information

Copyright © 2015 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill Education.

Learning Objective 2-1

Discuss the motives for

business combinations.

2-2

Business Combinations

FASB Accounting Standards Codification (ASC) Business Combinations (Topic 805) and Consolidation (Topic 810) provide guidance using the “acquisition method”.

The acquisition method embraces the fair value measurement for measuring and assessing business activity.

2-3

Reasons Firms Combine

Vertical integration Cost savings Quick entry into new markets Economies of scale More attractive financing opportunities Diversification of business risk Business Expansion Increasingly competitive environment

2-4

Recent Notable Business Combinations

2-5

Learning Objective 2-2

Recognize when consolidation of financial information into a single set of statements is necessary.

2-6

The Consolidation Process

Consolidated financial statements provide more meaningful information than separate statements.

Consolidated financial statements more fairly present the activities of the consolidated companies.

Yet, consolidated companies may retain their legal identities as separate corporations.

2-7

“There is a presumption that consolidated statements are more meaningful.. and that they are usually necessary for a fair presentation when one of the companies in the group… has a controlling financial interest..” FASB ASC (810-10-10-1)

“There is a presumption that consolidated statements are more meaningful.. and that they are usually necessary for a fair presentation when one of the companies in the group… has a controlling financial interest..” FASB ASC (810-10-10-1)

Learning Objective 2-3

Define the term business combination and differentiate across various forms of business combinations.

2-8

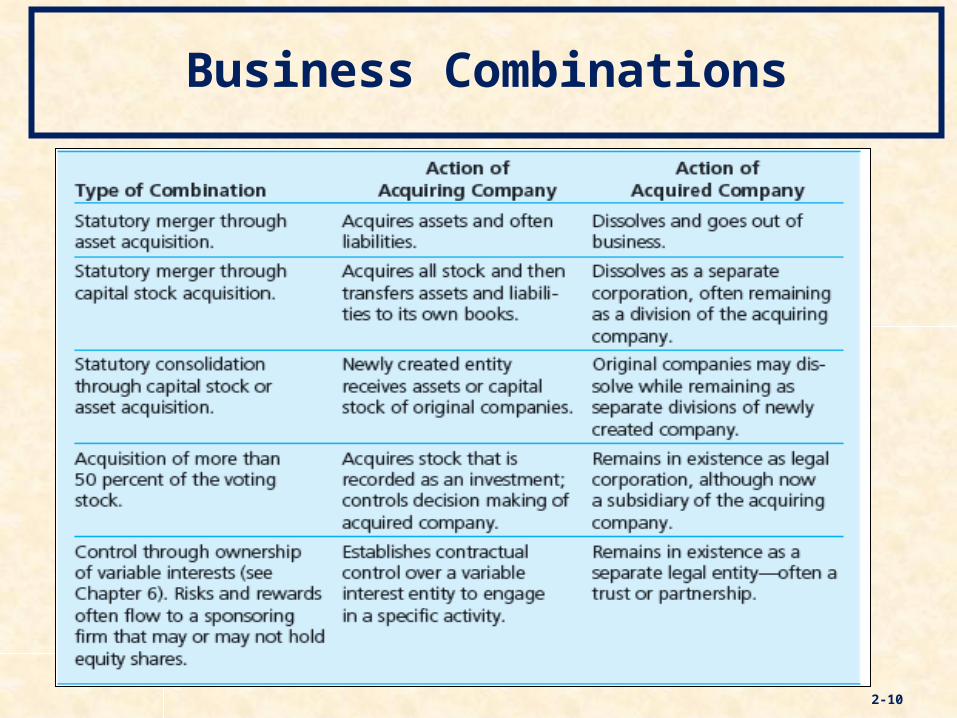

Business Combinations

2-9

A business combination . . . refers to a transaction or other event in which an

acquirer obtains control over one or more businesses. is formed by a wide variety of transactions or events

with various formats. can differ widely in legal form. unites two or more enterprises into a single economic

entity that require consolidated financial statements.

A business combination . . .

refers to a transaction or other event in which an acquirer obtains control over one or more businesses.

is formed by a wide variety of transactions or events with various formats.

can differ widely in legal form.

unites two or more enterprises into a single economic entity that require consolidated financial statements.

2-10

Business Combinations

FASB Control Model

The FASB provides guidance and defines control when accounting for business combinations with this control model: The FASB ASC Glossary, in addition to majority share

ownership, further describes control as the direct or indirect ability to determine the direction of management and policies through ownership, contract, or otherwise.

The FASB continues its effort to develop comprehensive guidance for consolidation of all entities, including entities controlled by voting interests.

2-11

Subsidiaries’ financial data

Prepare a single set of consolidated financial statements.

Parent’s financial data

Consolidation of Financial Information

2-12

To report the financial position, results of operations, and cash flows for the combined entity.

Reciprocal accounts and intra-entity transactions are adjusted or eliminated to. . .

brought together

What is to be consolidated?

If dissolution occurs: All appropriate account balances are physically consolidated in the financial records of the survivor.

If separate incorporation maintained: only the Financial statement information (on work papers, not the actual records) is consolidated.

2-13

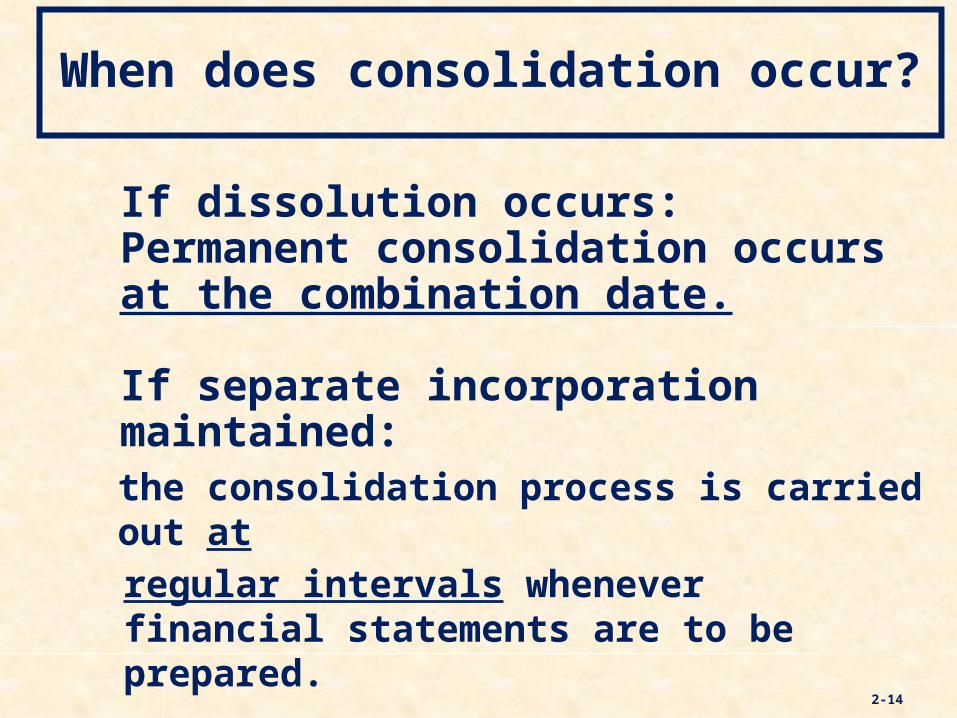

When does consolidation occur?

If dissolution occurs:Permanent consolidation occurs at the combination date.

If separate incorporation maintained:the consolidation process is carried out at

regular intervals whenever financial statements are to be prepared.

2-14

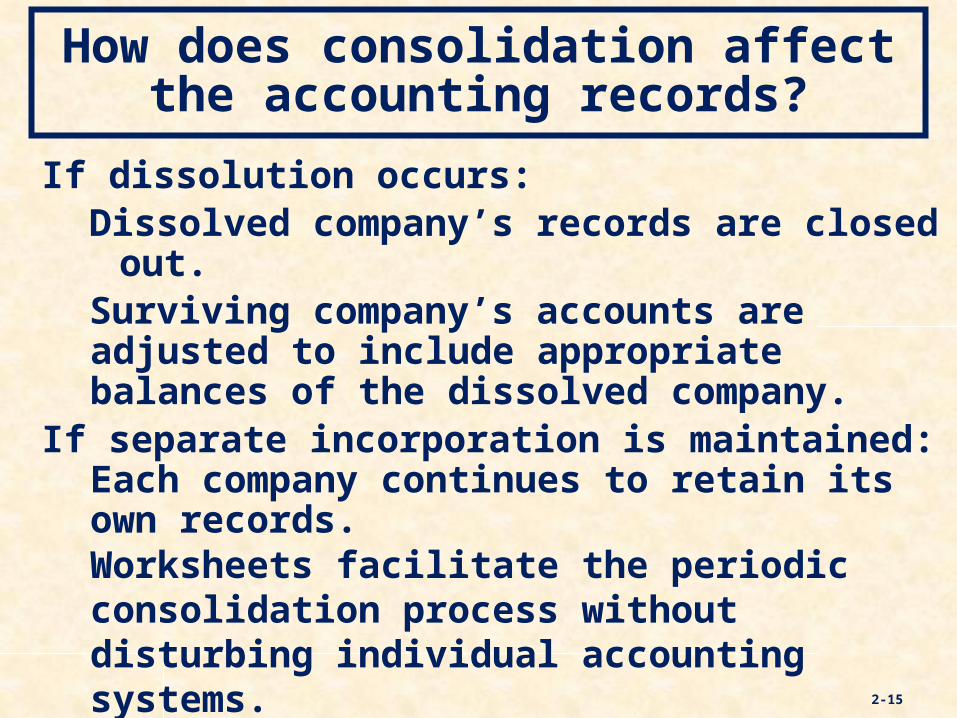

How does consolidation affect the accounting records?

If dissolution occurs:Dissolved company’s records are closed out.Surviving company’s accounts are adjusted to include appropriate balances of the dissolved company.

If separate incorporation is maintained:Each company continues to retain its own records. Worksheets facilitate the periodic consolidation process without disturbing individual accounting systems.

2-15

Learning Objective 2-4

Describe the valuation principles of the acquisition method.

2-16

The Acquisition Method

The acquisition method embraces the fair value in measuring the acquirer’s interest in the acquired business.

Applying the acquisition method involves recognizing and measuring: the consideration transferred for the acquired

business and any non-controlling interest. separately identified assets acquired and liabilities

assumed. goodwill, or a gain from a bargain purchase.

2-17

Fair Value

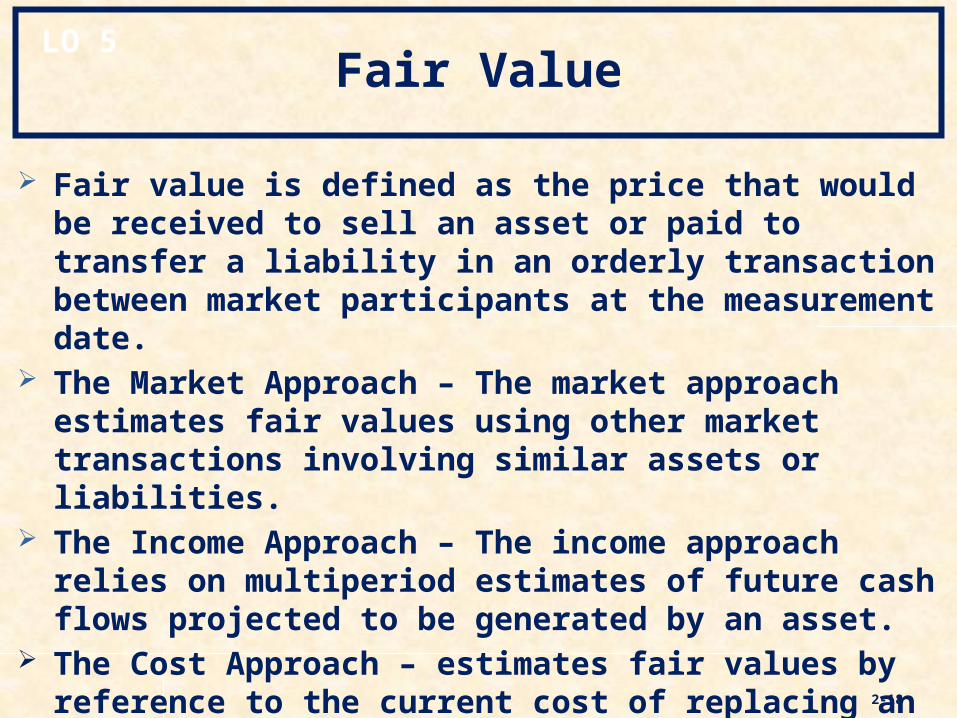

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

The Market Approach – The market approach estimates fair values using other market transactions involving similar assets or liabilities.

The Income Approach – The income approach relies on multiperiod estimates of future cash flows projected to be generated by an asset.

The Cost Approach – estimates fair values by reference to the current cost of replacing an asset with another of comparable economic utility.

2-18

LO 5

Acquisition Method

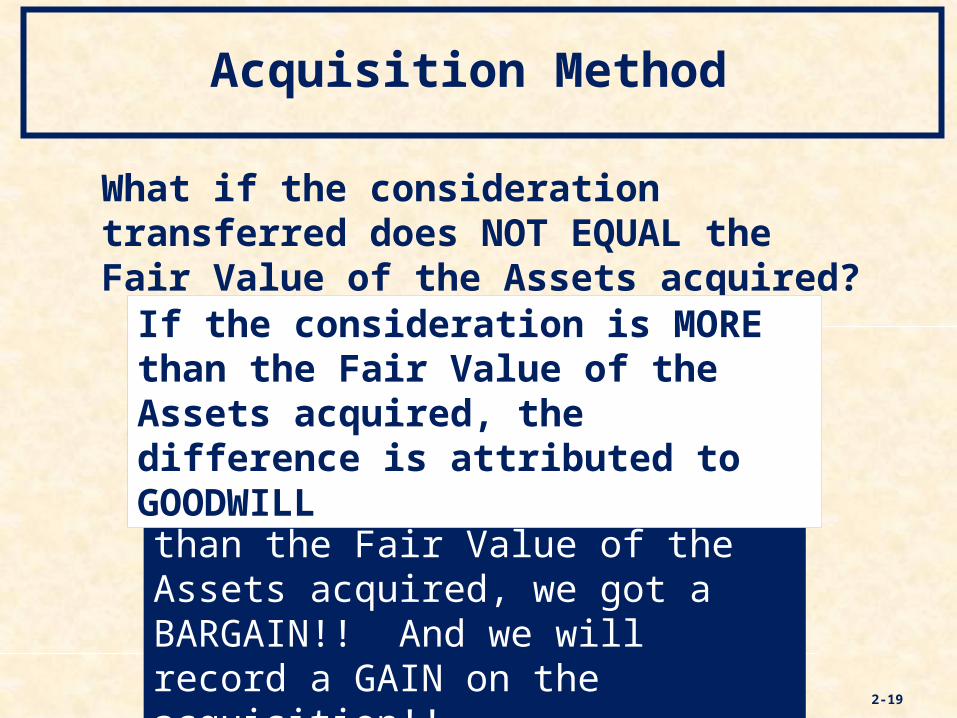

What if the consideration transferred does NOT EQUAL the Fair Value of the Assets acquired?

2-19

If the consideration is LESS than the Fair Value of the Assets acquired, we got a BARGAIN!! And we will record a GAIN on the acquisition!!

If the consideration is MORE than the Fair Value of the Assets acquired, the difference is attributed to GOODWILL

Learning Objective 2-5

Determine the total fair value of the consideration transferred for an acquisition and allocate that fair value to specific subsidiary assets acquired

(including goodwill) and liabilities assumed or to a gain on bargain purchase.

2-20

Procedures for Consolidating Financial Information

2-21

Legal and accounting distinctions divide business combinations into separate categories. Various procedures are utilized in this process according to the following sequence:

1. Acquisition method when dissolution takes place.

2. Acquisition method when separate incorporation is maintained.

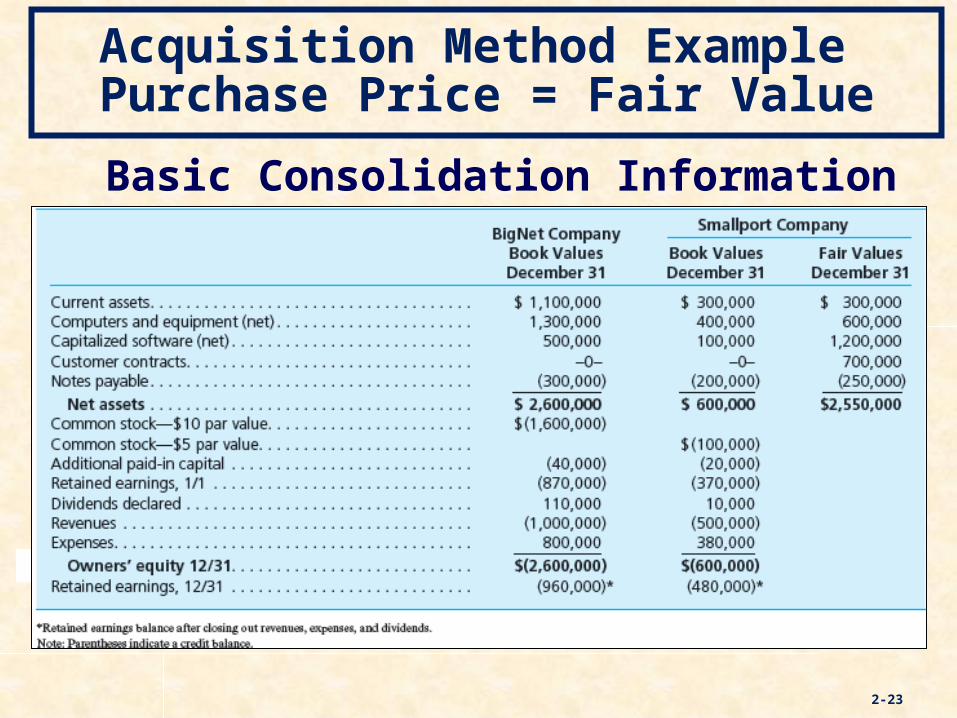

Acquisition Method Example Purchase Price = Fair Value

2-22

Assume BigNet Company owns Internet communications equipment and other business software applications. It seeks to expand its operations and plans to acquire Smallport on December 31. Smallport Company owns similar assets.

Smallport’s net assets have a book value of $600,000 and a fair value of $2,550,000. Fair values for assets and liabilities are appraised; capital stock, retained earnings, dividend, revenue, and expense accounts represent historical measurements. The equity and income accounts are not transferred in the combination.

Acquisition Method Example Purchase Price = Fair Value

2-23

Basic Consolidation Information

Learning Objective 2-6

Prepare the journal entry to consolidate the accounts of a subsidiary if dissolution

takes place.

2-24

Consideration Transferred = Net Identified Asset Fair Values

2-25

Dissolution of Subsidiary

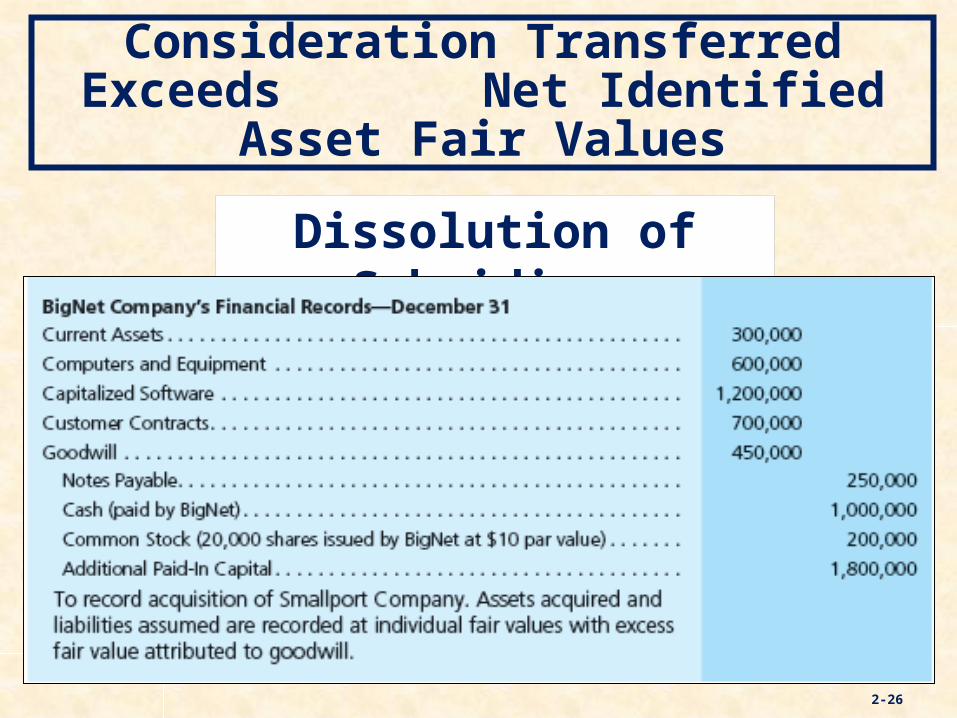

Consideration Transferred Exceeds Net Identified Asset Fair Values

2-26

Dissolution of Subsidiary

Consideration Transferred Is Less Than Net Identified Asset Fair Values

2-27

Dissolution of Subsidiary

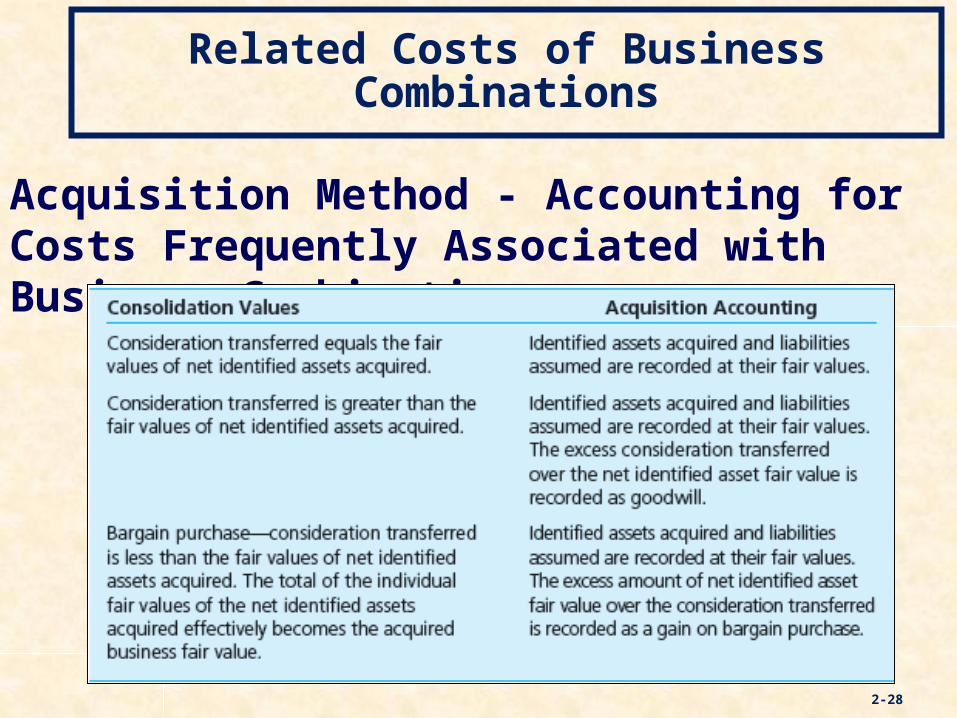

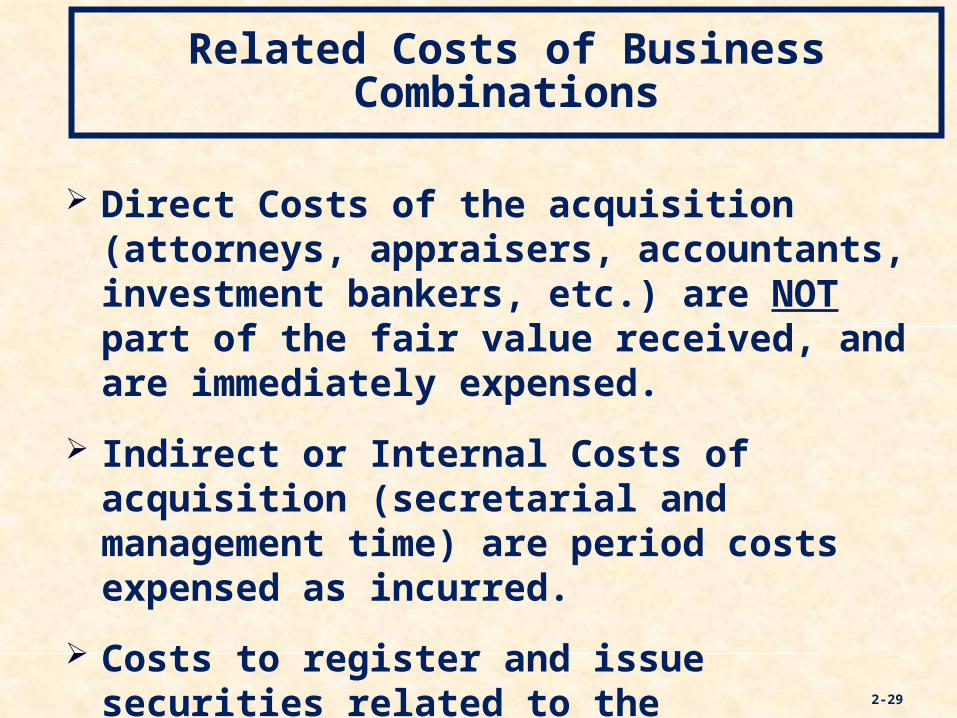

Related Costs of Business Combinations

2-28

Acquisition Method - Accounting for Costs Frequently Associated with Business Combinations

Related Costs of Business Combinations

Direct Costs of the acquisition (attorneys, appraisers, accountants, investment bankers, etc.) are NOT part of the fair value received, and are immediately expensed.

Indirect or Internal Costs of acquisition (secretarial and management time) are period costs expensed as incurred.

Costs to register and issue securities related to the acquisition reduce their fair value.

2-29

Acquisition Method - Subsidiary Is Not Dissolved

2-30

Separate Incorporation Maintained

Dissolution does not occur.Consolidation process is similar to previous example.Fair value is the basis for initial consolidation of

subsidiary’s net assets. Subsidiary is a legally incorporated separate entity.Each company maintains independent record-keepingConsolidation of financial information is simulated.Acquiring company does not physically record the

transaction.

Learning Objective 2-7

Prepare a worksheet to consolidate the accounts of two companies that form a business combination if dissolution doesnot take place.

2-31

The Consolidation Worksheet

2-32

Consolidation worksheet entries (adjustments and eliminations) are entered on the worksheet only.

Steps in the process:

1. Prior to constructing a worksheet, the parent prepares a formal allocation of the acquisition date fair value similar to the equity method procedures.

2. Financial information for Parent and Sub is recorded in the first two columns of the worksheet (with Sub’s prior revenue and expense already closed).

The Consolidation Worksheetcontinued. . .

2-33

3. Remove the Sub’s equity account balances.

4. Remove the Investment in Sub balance.

5. Allocate Sub’s Fair Values, including any excess of cost over Book Value to identifiable assets or goodwill.

6. Combine all account balances and extend into the Consolidated totals column.

7. Subtract consolidated expenses from revenues to arrive at net income.

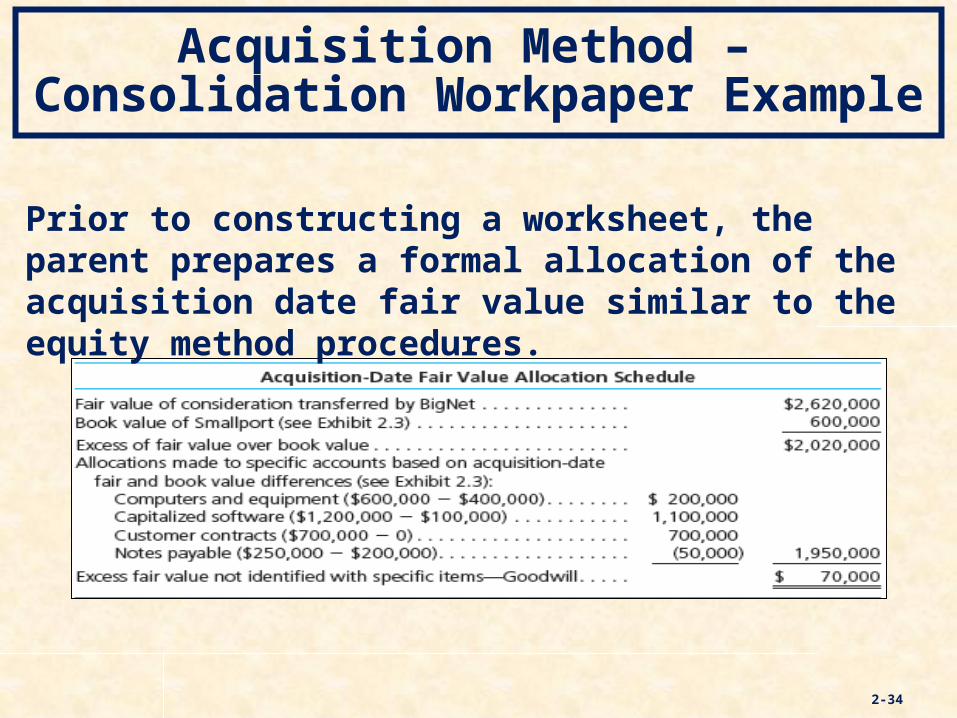

Acquisition Method – Consolidation Workpaper Example

2-34

Prior to constructing a worksheet, the parent prepares a formal allocation of the acquisition date fair value similar to the equity method procedures.

Acquisition Method – Consolidation Workpaper Example

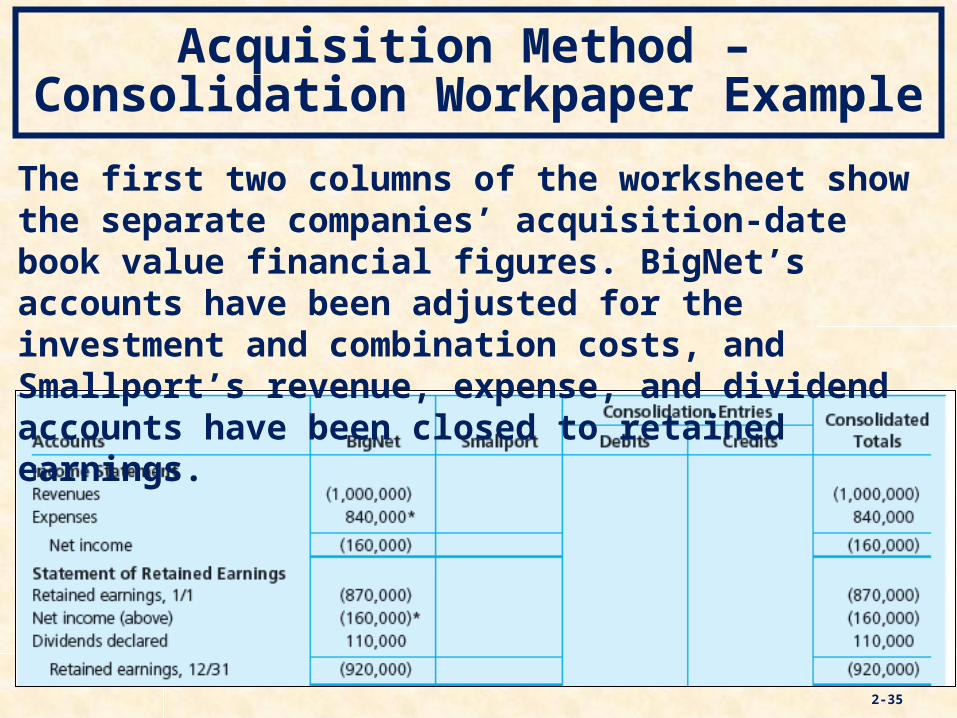

2-35

The first two columns of the worksheet show the separate companies’ acquisition-date book value financial figures. BigNet’s accounts have been adjusted for the investment and combination costs, and Smallport’s revenue, expense, and dividend accounts have been closed to retained earnings.

Acquisition Method – Consolidation Workpaper Example continued . . .

2-36

Acquisition Method – Consolidation Workpaper Journal Entries

2-37

Learning Objective 2-8

Describe the two criteria for recognizing intangible assets apart from goodwill in a business combination.

2-38

Acquisition Date Fair-Value Allocations – Additional Issues

In determining whether to recognize an intangibleasset in a business combination, two specific criteria are essential.

1. Does the intangible asset arise from contractual or other legal rights?

2. Is the intangible asset capable of being sold or otherwise separated from the acquired enterprise?

2-39

Acquisition Date Fair-Value Allocations – Additional Issues

Intangibles are assets that: Lack physical substance (excluding financial instruments) Arise from contractual or other legal rights (most intangibles

in business combinations meet the contractual-legal criterion). Is capable of being sold or otherwise separated from the

acquired enterprise

2-40

Preexisting goodwill recorded in the acquired company’s accounts is ignored in the allocation of the purchase price.

IPR&D that has reached technological feasibility is capitalized as an intangible asset at fair value with an indefinite life that is reviewed for impairment.

Ongoing R&D is expensed as incurred.

Intangible Assets That Meet the Criteria for Recognition Separately from Goodwill

2-41

Convergence between U. S. and International Standards

IASB International Financial Reporting Standard 3 (IFRS 3) Revised and FASB ASC topics 805, Business Combinations, and 810, Consolidation, effectively converged accounting for business combinations.

In 2011, the IASB issued IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities - effective beginning in 2013.

New definition of control focuses on the power to direct the activities of an entity, exposure to variable returns, and a linkage between power and returns.

2-42

Learning Objective 2-9

Identify the general characteristics of the legacy purchase and pooling of interest methods of accounting for past business combinations.

Understand the effects that persist today in financial statements from the use of these legacy methods.

2-43

Legacy Methods – Purchase and Pooling of Interests Methods

2002 to 2008: Purchase Method

Prior to 2002: Purchase Method Or The Pooling Of Interests Method

2-44

Since the ACQUISITION METHOD is applied to business combinations occurring in 2009 and after, the two prior methods are still in use.

Purchase Method – An Application of the Cost Method

How the cost-based purchase method differs from the fair value-based acquisition method. Acquisition date allocations (including bargain

purchases) Direct combination costs Contingent consideration In-Process R&D expensed under the Purchase

Method, unless it had reached technological feasibility

2-45

Purchase Method – An Application of the Cost Method

Valuation basis was “cost” The value of the consideration transferred, PLUS the direct costs of the acquisition, IGNORE any indirect costs of the acquisition, IGNORE any contingent payments.

The total cost of the acquisition was allocated proportionately to the net assets based on their fair values, with any excess going to goodwill.

2-46

Purchase Method – Purchase Price < Fair Value

Under the purchase method, a bargain purchase occurred when the sum of the individual fair values of the acquired net assets exceeded the purchase cost.

Current assets and liabilities were recorded at fair value, and some non-current assets were reduced proportionately. Long-term assets were reduced because their fair-value estimates were considered less reliable than current items and liabilities.

2-47

If the difference in purchase price and fair value was substantial enough to eliminate all the non-current asset account balances of the acquired company, the remainder was reported as an extraordinary gain.

Pooling of Interests Historical Review

Prior to 2002, under certain criteria, combinations could be accounted for as “Pooling of Interests” when one company acquired all of another company’s stock – using its own stock as consideration (no cash!)

These Pooling combinations are left intact going forward.

2-48

2-49

Book values of the assets and liabilities of both companies became the book values reported by the combined entity.

The revenue and expense accounts were combined both before and after the combination.

Reported income was typically higher than under the purchase accounting method. Not only did firms retrospectively combine incomes, there was less depreciation and amortization expense.

Pooling of Interests Historical Review

Related Documents