Chapter Twelve Incentive Compensation

Chapter Twelve Incentive Compensation. Copyright © Houghton Mifflin Company. All rights reserved. 12–2 Chapter Outline Strategic Importance of Variable.

Dec 29, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter Twelve

Incentive Compensation

Copyright © Houghton Mifflin Company. All rights reserved. 12–2

Chapter Outline

• Strategic Importance of Variable Pay• Linking Pay to Performance• Individual Incentives• Group Incentives• Barriers to Pay-for-Performance Success• Summary: Making Variable Pay Successful• Executive Compensation

Copyright © Houghton Mifflin Company. All rights reserved. 12–3

Strategic Importance of Variable Pay

• Aim is for Employees Who Can:– Understand the Goals of the Organization– Know their Role in Accomplishing these

Goals– Become Appropriately Involved in

Decisions of the Organization– Accept that Their Rewards Are Related to

Their Contribution to the Goal Attainment of the Organization

Copyright © Houghton Mifflin Company. All rights reserved. 12–4

Alignment

• A major strategic goal is to align organizational and individual goals through pay

• Best understood through examples of misalignment

Copyright © Houghton Mifflin Company. All rights reserved. 12–5

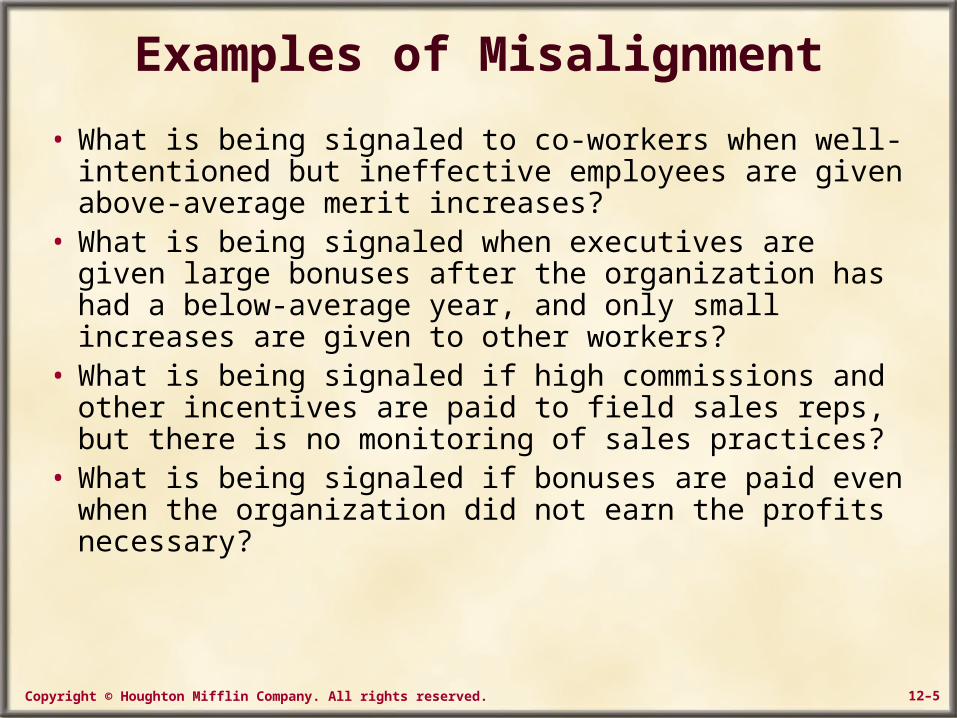

Examples of Misalignment

• What is being signaled to co-workers when well-intentioned but ineffective employees are given above-average merit increases?

• What is being signaled when executives are given large bonuses after the organization has had a below-average year, and only small increases are given to other workers?

• What is being signaled if high commissions and other incentives are paid to field sales reps, but there is no monitoring of sales practices?

• What is being signaled if bonuses are paid even when the organization did not earn the profits necessary?

Copyright © Houghton Mifflin Company. All rights reserved. 12–6

Table 12.1 Ratings of the Effectiveness of Various Incentive Pay Reward Programs

Source: HR Focus, Vol. 78 (4), April 2001, pp.3-4.

Copyright © Houghton Mifflin Company. All rights reserved. 12–7

Linking Pay to Performance

• Reasons to Link Pay to Performance– Motivation

• Expectancy• Instrumentality• Valence

Copyright © Houghton Mifflin Company. All rights reserved. 12–8

Figure 12.1 Major Elements of Expectancy Theory

Copyright © Houghton Mifflin Company. All rights reserved. 12–9

Table 12.2: Ratings of Pay Incentive Plans

Source: E.E. Lawler, Pay and Organization Development, 1981 Addison Wesley Longman, Inc. Reprinted by permission of Addison Wesley Longman.

Copyright © Houghton Mifflin Company. All rights reserved. 12–10

Linking Pay to Performance

• Reasons to Link Pay to Performance– Motivation– Retention– Productivity– Cost Savings– Organizational Objectives

• Reasons Not to Link Pay to Performance• Factors Affecting the Design of Incentive

Systems

Copyright © Houghton Mifflin Company. All rights reserved. 12–11

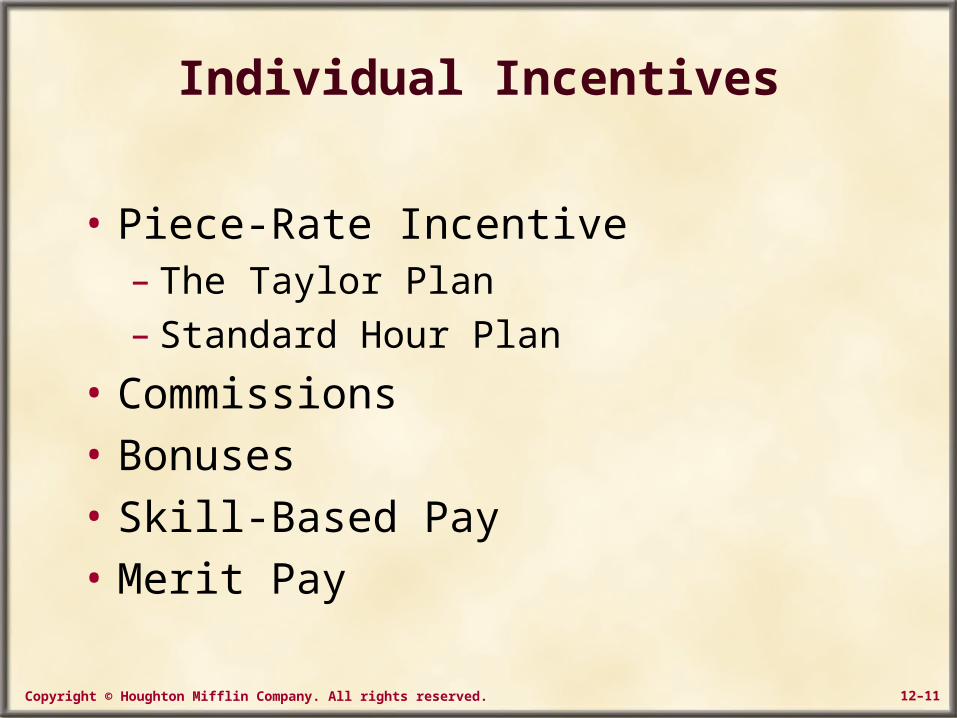

Individual Incentives

• Piece-Rate Incentive– The Taylor Plan– Standard Hour Plan

• Commissions

• Bonuses

• Skill-Based Pay

• Merit Pay

Copyright © Houghton Mifflin Company. All rights reserved. 12–12

Skill-Based Pay

• A reward system that pays employees on the basis of the work-related skills they possess rather than associated rewards with performance levels or seniority– Stair-step model– Job-point accrual model– Cross-department model

Copyright © Houghton Mifflin Company. All rights reserved. 12–13

Table 12.4 Merit Increase Guidelines

Copyright © Houghton Mifflin Company. All rights reserved. 12–14

Merit Pay

+A major motivational device

– Permanent commitment to an increased

salary

Copyright © Houghton Mifflin Company. All rights reserved. 12–15

Group Incentives

• Profit Sharing

• Gain-Sharing Plans– Scanlon Plan– Rucker Plan– Improshare– Winsharing– Summary

Copyright © Houghton Mifflin Company. All rights reserved. 12–16

Table 12.5 Principal Features of Gain-Sharing and Profit-Sharing Programs

Source: Robert Doyle, Gainsharing and Productivity: A Guide to Planning, Implementation, and Development. Copyright © 1983 by AMACOM, a division of American Management Association. Sections adapted from Jay R. Schuster and Patricia K. Zingheim, The New Pay: Linking Employees and

Organizational Performance (Lexington, Mass.: Lexington Books, 1992).

Copyright © Houghton Mifflin Company. All rights reserved. 12–17

Group Incentives

• Profit Sharing• Gain-Sharing Plans

– Scanlon Plan– Rucker Plan– Improshare– Winsharing– Summary

• Employee Stock Ownership Plans (ESOPs)

Copyright © Houghton Mifflin Company. All rights reserved. 12–18

Table 12.6 America’s Largest Companies Over 50% Employee Owned

Source: “The Employee Ownership 100,” National Center for Employee Ownership, July 2004. (Available at : http://www.nceo.org/library/eo100.html)

Copyright © Houghton Mifflin Company. All rights reserved. 12–19

Barriers to Pay-for-Performance Success

• Nature of the Task

• Performance Measurement

• Amount of Payout

• Frailty of the Linkage

Copyright © Houghton Mifflin Company. All rights reserved. 12–20

Summary: Making Variable Pay Successful

• Characteristics of Successful Incentive Systems:– Employee-Organization Partnerships– Employee Empowerment– Relevant, Simple Measures– Effective Communication – Balance Between Short- and Long-Term

Performance Factors– Line-of-Sight Considerations

Copyright © Houghton Mifflin Company. All rights reserved. 12–21

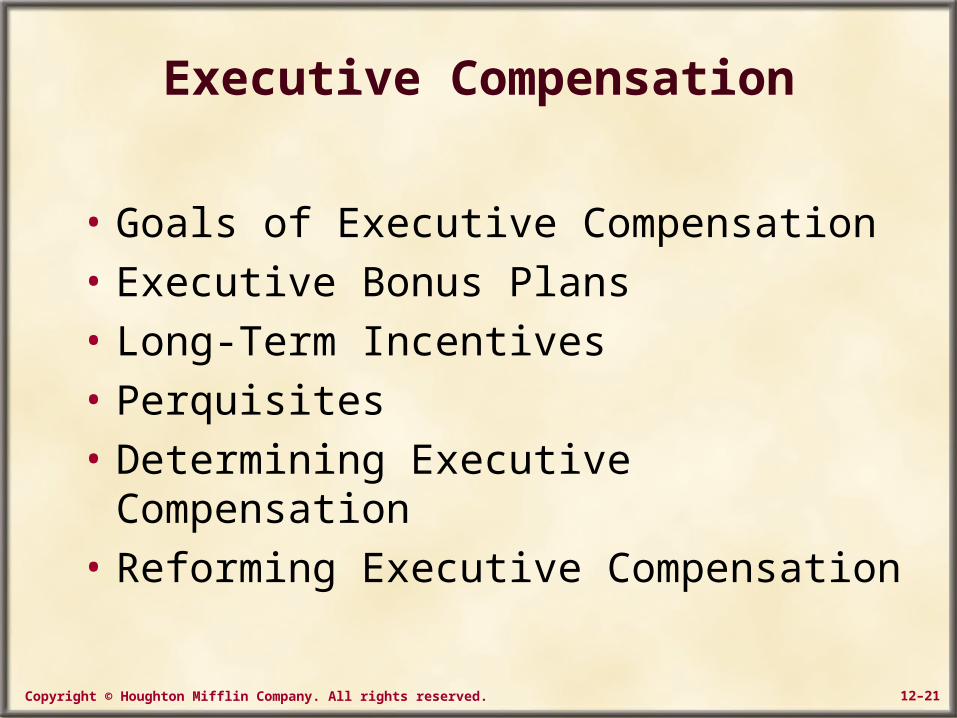

Executive Compensation

• Goals of Executive Compensation

• Executive Bonus Plans

• Long-Term Incentives

• Perquisites

• Determining Executive Compensation

• Reforming Executive Compensation

Copyright © Houghton Mifflin Company. All rights reserved. 12–22

Reasons for Interest in Executive Compensation

• In 1993, the average CEO earned $3,841,273. In 1997, just four years later, CEO pay more than doubled to an average $7.8 million.

• In 2000, U.S. CEOs earned on average a princely $13.1 million.

• The result of the weakening returns led to the first decreases in more than a decade in the early 2000s with the 2003 average of CEO salary, bonus, and long-term compensation at $8.1 million.

Copyright © Houghton Mifflin Company. All rights reserved. 12–23

Reasons for Interest in Executive Compensation (cont’d)

• Reuben Mark, CEO, Colgate-Palmolive, was the top-paid CEO with a total pay of $141.1 million. This at a time when Colgate-Palmolive saw a –19 percent return in the three year period ending in 2003

• In 1980, CEO pay was 42 times the pay of a factory worker; in 1997, the CEO earned 326 times as much.

Copyright © Houghton Mifflin Company. All rights reserved. 12–24

Reasons for Interest in Executive Compensation (cont’d)

• In 1980 CEO pay was 42 times the pay of the ordinary factory worker; by 1991 this ratio had increased to 104; by 1993 to 149; by 1997 to 326; and was 531 times the average worker in 2001. As a result of the collapsing stock market, this ratio fell to 282 in 2002

• In the period 1990 to 2003, CEO pay rose 313 percent. During that time the S&P 500 stock index rose 242 percent, corporate profits increased 128 percent, the average worker’s pay climbed 49 percent, and inflation rose 41 percent

Copyright © Houghton Mifflin Company. All rights reserved. 12–25

Reasons for Interest in Executive Compensation (cont’d)

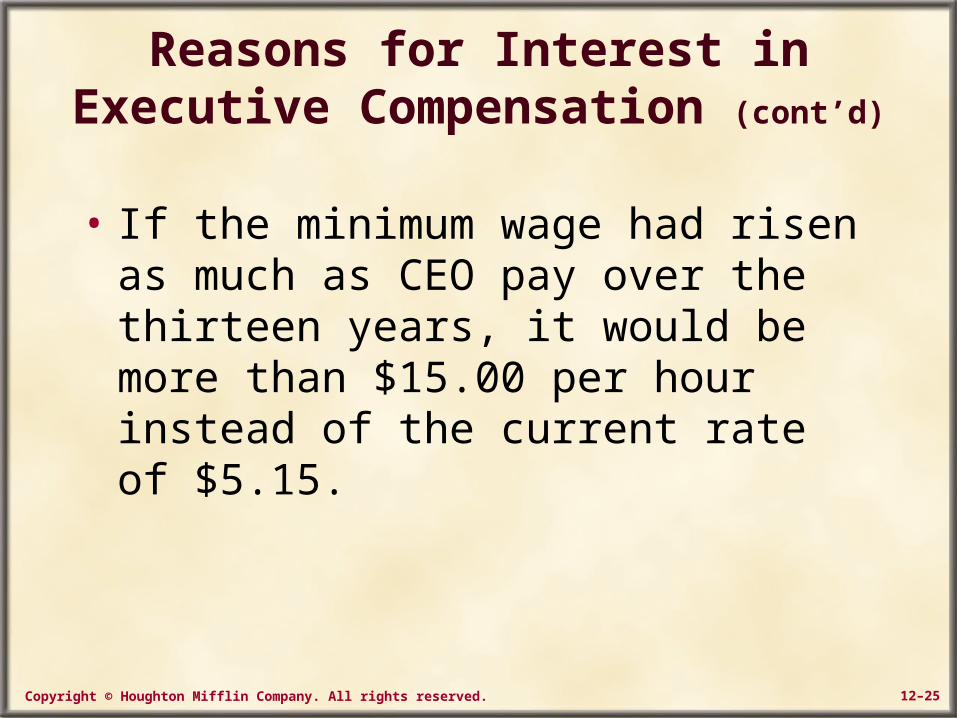

• If the minimum wage had risen as much as CEO pay over the thirteen years, it would be more than $15.00 per hour instead of the current rate of $5.15.

Copyright © Houghton Mifflin Company. All rights reserved. 12–26

Review

• Strategic Importance of Variable Pay• Linking Pay to Performance• Individual Incentives• Group Incentives• Barriers to Pay-for-Performance Success• Summary: Making Variable Pay Successful• Executive Compensation

Related Documents