68 CHAPTER FOUR TECHNICAL EFFICIENCY OF ETHIOPIAN MICROFINANCE INSTITUTIONS 4.1 Introduction This chapter aims to measure the technical efficiency and its determinants of the MFIs. Methodologically, efficiency of the MFIs is estimated using the preferred DEA and then complimented the SFA for the robustness of the results. The remaining part of this chapter is structured as follows. Content wise, the chapter begins with discussion of prior empirical finding on efficiency of MFIs in the globe. The next section provides the methodology i.e., the DEA model specification, and input and output selection. Then section three presents results and discussions. Finally, section four presents the conclusion. 4.2 Prior empirical works on efficiency of MFIs Though the efficiency of the banking sector is adequately examined, researches related to the efficiency of MFIs in general are limited. This fact is substantiated by Berger and Humphrey (1997). Their survey shows that more than 130 studies have used the frontier techniques in analyzing efficiency of banks in different countries. On the other hand, a survey by Cummins and Weiss (2000), which focuses on efficiency in the insurance industry, has found 21 studies which applied frontier techniques. A more recent survey

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

68

CHAPTER FOUR

TECHNICAL EFFICIENCY OF ETHIOPIAN

MICROFINANCE INSTITUTIONS

4.1 Introduction

This chapter aims to measure the technical efficiency and its determinants of the MFIs.

Methodologically, efficiency of the MFIs is estimated using the preferred DEA and then

complimented the SFA for the robustness of the results. The remaining part of this

chapter is structured as follows. Content wise, the chapter begins with discussion of prior

empirical finding on efficiency of MFIs in the globe. The next section provides the

methodology i.e., the DEA model specification, and input and output selection. Then

section three presents results and discussions. Finally, section four presents the

conclusion.

4.2 Prior empirical works on efficiency of MFIs

Though the efficiency of the banking sector is adequately examined, researches related to

the efficiency of MFIs in general are limited. This fact is substantiated by Berger and

Humphrey (1997). Their survey shows that more than 130 studies have used the frontier

techniques in analyzing efficiency of banks in different countries. On the other hand, a

survey by Cummins and Weiss (2000), which focuses on efficiency in the insurance

industry, has found 21 studies which applied frontier techniques. A more recent survey

69

by Luhen (2009) found more than 93 studies using frontier efficiency measurement with

application to the insurance industry. However, only studies of (Nghiem,2004; Gutierrez-

Nieto et al., 2005; Gutierrez-Nieto et al., 2009; Hassan and Tuffe, 2001; Qayyum and

Ahmed, 2006; Haq et al., 2007; Sufian, 2006; Bassem, 2008; Hermes et al., 2009; Hassan

and Benito, 2009; Nawaz, 2009; Masood and Ahmed, 2010,Oteng-Abayie et al., 2011)

are found in microfinance institutions. The findings of these empirical studies are

thoroughly discussed below.

Guitierrez-Nieto et al. (2005) applied a DEA non-parametric approach to analyze the

efficiency of 30 Latin American MFIs. In their study, they tried to explore the

multivariate analysis of the DEA results by developing 21 specifications using two inputs

and three outputs. Their study found that an NGO and a non-bank financial institution are

the most efficient among the various group of MFIs.

Bassem (2008) estimated efficiency of 35 microfinance institutions in the Mediterranean

zone during the period 2004–2005 using DEA and found that eight institutions were

efficient. Further, the study revealed that size of the MFI has a negative effect on

efficiency.

Hassan and Sanchez (2009) applied DEA to investigate the technical and scale

efficiencies of microfinance institutions (MFIs) in three regions: Latin America countries,

Middle East and North Africa (MENA) countries, and South Asia countries, and

compares efficiencies across regions and across type of MFIs. They found that technical

efficiency is higher for formal MFIs (banks and credit unions) than non-formal MFIs

(nonprofit organizations and non-financial institutions). Furthermore, South Asian MFIs

70

have higher technical efficiency than Latin American and MENA MFIs. Finally they

concluded that the source of inefficiency was pure technical rather than scale, suggesting

that MFIs were either wasting resources or were not producing enough outputs (making

enough loans, raising funds, and getting more borrowers).

Masood and Ahmed (2010) applied a stochastic frontier model to estimate the efficiency

of 40 Indian microfinance institutions for the period 2005-2008. They found that mean

efficiency level of microfinance institutions is low (34%) but it increases over the period

of study. The study also estimated determinants of efficiency and the result showed that

age of microfinance institution is positive determinant of efficiency. Further, the study

found regulated microfinance institutions are less efficient.

Haq et al. (2009) investigates the efficiency of 39 MFIs in developing world (Africa,

Asia, and Latin America) using the data envelopment analysis (DEA) based

intermediation and production approaches. These diffident approaches tend to give them

conflicting results. Their findings show that non-governmental microfinance institutions

under production approach are the most efficient. On the other hand, the study shows

bank-microfinance institutions outperform and are more efficient under intermediation

approach.

Servin et al. (2012) using stochastic frontier analysis examines technical efficiency of

different types of microfinance institutions in Latin America. Their sample includes 315

MFIs operating in 18 Latin American countries for the period 2003-2009. Their

methodology permits them both the production frontier and error structures to differ

between four types of ownership types of MFIs (NGO, Cooperative/Credit Union, Non-

71

Bank Financial Intermediary and Bank). They differentiate between intra-firm and inter-

firm efficiency. Their results show that Non-Governmental Organizations and

Cooperatives/Credit Unions have much lower inter-firm and intra-firm technical

efficiencies than Non-Bank Financial Intermediaries and Banks, which indicates the

importance of ownership type for technical efficiency. According to the authors, the

finding that NGOs and Cooperative/Credit Unions now are, on average, less efficient

than mutual NBFIs and Banks seem to suggest that further increases in regulation and

competition will be needed to curtailing inefficiencies of non-share holder MFIs.

Abdul Qayyum and Ahmad (2006) tried to investigate the efficiency of 85 MFIs in South

Asia (consisting of 15 Pakistani, 25 Indian, and 45 Bangladeshi). The analysis revealed

that the inefficiency of the MFIs in Pakistan, India, and Bangladesh is mainly of technical

nature and to improve their efficiencies, they suggest that the MFIs need to enhance their

managerial expertise and improve technology.

Nghiem et al. (2004) investigates the efficiency of microfinance industry in Vietnam

through a survey of 46 schemes in the north and central regions by employing the Data

Envelopment Analysis (DEA). The result of the study reveals that the average technical

efficiency score of schemes is 80%. Further, the study found that age and location have

positive effect on efficiency of the schemes.

Hassan and Tufte (2001) examine cost inefficiency and determinants of the Grameen

Bank (GB) using branch level cost data over the 1988-1991 period. Using a stochastic

frontier analysis they found that Grameen Bank’s branches staffed by the female

72

employees operated more efficiently than their counterparts staffed by the male

employees.

Gregorio and Ramirez (2004) analyzed the efficiency of Microfinance Institutions (MFIs)

in Peru between 1999 and 2003 by estimating a stochastic cost frontier. They found

that MFIs with the largest assets tend to post the highest efficiency levels and

that MFIs operating in less concentrated market tend to be more efficient. Further their

study shows that cost efficiency of MFIs is affected by average loan size, proportion of

net assets, financial sufficiency, financial leverage, business experience and proportion of

farm loans.

Sufian (2006) also analyzed the efficiency of 80 Non Bank Financial Institutions (NBFI)

in Malaysia for the period 2000–2004 using DEA. His study revealed that only 28.75% of

80 observations are efficient. Moreover, his study revealed that the size and the part of

the market have a negative effect on efficiency.

Martinez-Gonzalez (2008) examined the relative technical efficiency of a sample of

microfinance institutions (MFIs) in Mexico using the data envelopment analysis (DEA).

The study found that most of the MFIs have been more successful in achieving the type

of efficiency related to sustainability rather than outreach. Further the study found that

average size of loan, proportion of assets used as performing portfolio, percentage of

FINAFIM funds, scale of operations, ratio of payroll to expenses, age, structure of

the board, and for-profit status of the MFI have significant impact on efficiency of

MFIs.

73

Hermes et al. (2008) used stochastic frontier analysis to examine a trade-off between

outreach to the poor and efficiency of microfinance institutions based on 435 MFIs and

found that outreach and efficiency of MFIs are negatively correlated. Their finding

further indicates that efficiency of MFIs is higher if they focus less on the poor and/or

reduce the percentage of female borrowers.

Nawaz (2010) attempts to measure the financial efficiency and productivity of

Microfinance Institutions (MFIs) worldwide taking into account the subsidies received by

MFIs by using the non-parametric Data Envelopment Analysis (DEA). The study carried

out a three-stage analysis. Firstly, technical and pure efficiency scores are calculated by

splitting subsidies into input and output and entered into the DEA framework

specifications depending on whether they are generating benefits (negative subsidies) or

cost (positive subsidies) to the society. Secondly DEA-based Malmquist indices are

calculated to analyze the intertemporal productivity change. Thirdly, Tobit Regression

analysis are carried out to test a series of hypotheses concerning the relationship between

financial efficiency and other indicators related to MFIs productivity, organization,

outreach, sustainability and social impact. The study concludes that overall subsidies

contribute to financial efficiency of MFIs albeit marginally. The study also provides

evidence on the tradeoff between outreach to the poor and financial efficiency. That is

MFIs which cater to the poor tend to be more inefficient than those with clients relatively

well off. Also evident is the fact that lending to women is efficient only in the presence of

subsidies MFIs in South Asia and Middle East & North Africa tend to be less efficient

than the others.

74

Ahmad (2011) has attempted to estimate the efficiency of microfinance institutions in

Pakistan. The non parametric Data Envelopment Analysis has been used to analyze the

efficiency of these institutions by using data for the year 2003 and 2009 respectively.

Both input oriented and output oriented methods have been considered under the

assumption of constant return to scale and variable returns to scale. He found that three

MFIs are on efficiency frontier in the year 2003 under both constant return to scale and

variable return to scale assumptions. Further, in year 2009, four microfinance institutions

are efficient under constant return to scale and nine are efficient under variable return to

scale assumption.

Oteng-Abayie et al. (2011) estimates economic efficiency of 137 microfinance units in

Ghana for 2007-2010 sample periods using a Cobb-Douglas stochastic frontier model.

They found that the MFIs are producing at constant cost to size with an overall average

economic efficiency for the group of MFIs to be 56.29%. Further their study reveals that

the main sources of inefficiencies in the microfinance sector in Ghana are due to the

variation in management practices and differences in technical capacities (both in training

and portfolio quality). Finally, the study reveals that age and savings indicators of

outreach and productivity, and cost per borrower are found to be significant determinants

of economic efficiency.

75

Source: Author’s survey

Table 4.1: Efficiency studies on MFIs

Author Data description Approach

Hassan and Sanchez(2009) 215 MFIs in the world DEA

Gutierrez-Nieto et al. (2007) 21 MFIs in Latin America DEA

Hamiza Haq et al. (2007) 39 MFIs from the world DEA

Abdul Qayyum and Munir Ahmed (2006) 85 MFIs from India, Pakistan and Bangladesh DEA

Nghiem (2004) 46 MFIs in Vietnam DEA and SFA

Ahmed Nawaz (2009) 204 MFIs around the world DEA

Bassem(2008) 35 MFIs in Mediterranean DEA

Hassan and Tufte (2001) Grameen Bank branch level over the 1988-1991 period SFA

Hermes et al. (2009) 435 MFIs in the world for the period 1997-2007 SFA

Oteng-Abayie et al. (2011) Ghana MFIs for the period from 2007-2010 SFA

Masood and Ahmed (2010) 40 Indian microfinance institutions for the period 2005-2008 SFA

Gregorio and Ramirez (2004) Peru MFIs for the period of 1999-2003 SFA

Martinez-Gonzalez (2008) Sample MFIs in Mexico DEA

Ahmed (2011) MFIs in Pakistan DEA

Servin et al. (2012) 315 MFIs from Latin America SFA

76

4.3 Methodology

In empirical works on the efficiency of financial institutions the parametric - SFA and the

non parametric – DEA are overwhelmingly dominating (Berger and Humphrey, 1997).

The DEA involves the use of linear programming whereas SFA involves the use of

econometric methods (Coelli et al., 1998). As the SFA impose functional and

distributional forms on the error term, the DEA does not require any functional form to

be specified. Further, while the former distinguishes the component of inefficiency in to

random and inefficiency effect, the later deems any deviation from the efficiency frontier

to the result of inefficiency. Studies acknowledged that both approaches have advantages

as well as limitations (Berger and Humphrey, 1997).The superiority of one approach over

the other has been a discussion and is still debatable in literature of financial institutions.

However, still others suggest that, for instance, Resti (1997); Ondrich and

Ruggiero(2000); and Leon(2001) both produce similar rankings, and conclude that both

approaches are complimentary to measure efficiency. Indeed, the nonparametric DEA is

more frequently used than parametric methods (Berger and Humphrey, 1997).

Parametric measurement includes specifying and estimating a stochastic production

frontier or stochastic cost frontier. In this method, the output (or cost) is assumed to be

function of inputs, inefficiency and random error. The main strength of the stochastic

frontier function approach (SFA) is its incorporation of stochastic error, and therefore

permitting hypothetical testing. An often quoted disadvantage of this approach, however,

is that it imposes an explicit functional form and distribution assumption on the data.

77

In contrast, the linear programming technique of data envelopment analysis (DEA) does

not impose any assumptions about functional form; hence it is less prone to mis-

specification. Further, DEA is a non-parametric approach so does not take into account

random error. Hence, it is subject to the problems of assuming an underlying distribution

about the error term. However, since DEA cannot take account of such statistical noise,

the efficiency estimates may be biased if the production process is largely characterized

by stochastic elements.

For the purpose of this study the non parametric DEA is preferred at least for three

reasons. First it considers multiple inputs and multiple outputs to assess the efficiency of

MFIs (i.e the dual objectives of social and financial).Second it does not require a prior

assumption about the analytical form of the production function. Third, DEA works well

with small number of observations as the case of Ethiopian MFIs.

4.3.1 Data envelopment analysis (DEA)

Originally, DEA was first introduced in the work of Farrell (1957) and then developed in

the work of Charnes et al. (1978) and is applied to non-profit organizations where the

objective of profit maximization and cost minimization may not be considered as the vital

factor. It has been extensively applied in performance evaluation and benchmarking of

schools, hospitals, bank branches, production plants, financial institutions (Charnes et al.,

1994; and Berger and Humphrey, 1997).

The DEA technique is essentially a linear programming technique that converts multiple

inputs and outputs into a measurement of efficiency. This conversion is conducted by

78

analyzing the resources (inputs) used and the results (outputs) achieved for each decision

making unit (DMU) or microfinance institution. The inputs and outputs of each DMU

(microfinance institution) are compared to the same quantities for all the remaining units.

The DEA identifies the most efficient units in a population and provides a measurement

of inefficiency for all the others. The method constructs a frontier based on actual data.

Firms on the frontier are efficient, while firms off the efficiency frontier are

inefficient.DEA is based on the concept of relative efficiency and is widely used in

efficiency and productivity analysis of financial institutions (see, Berger and Murphy,

1997). Moreover, DEA provides information about peers, which are the efficient schemes

that have similar input-output structure as some inefficient schemes.

In DEA, efficiency can be measured by an input-oriented process, which focuses on

reducing inputs to produce the same level of outputs, and an output-oriented process,

which aims to maximize outputs from a given set of inputs. The two measures provide

the same results under constant returns to scale but give different values under variable

returns to scale (Fare and Lovell 1978; Coeli et al., 1998). Furthermore, the choice of an

orientation will have only minor influences upon efficiency scores (Coelli et al., 1998).

However, this study is based on output oriented DEA which assumes the optimal output

that can be produced given a set of inputs. The output orientation seems more appropriate

to MFIs because such institutions are expected to reach many discriminated poor people

using a given level of inputs.

The DEA technical efficiency is calculated by assuming both Constant Returns to Scale

(CRS) and Variable Returns to Scale (VRS). The CRS assumption is only appropriate

79

when all DMUs are operating at an optimal scale. However, factors like imperfect

competition and constraints on finance may cause a DMU not to operate at optimal scale

(Coelli et al., 1996). Banker, Charnes and Cooper (1984) suggested an extension of the

CRS DEA model to account for variable returns to scale. The use of the CRS

specification when not all DMU’s are operating at the optimal scale will result in measure

of technical efficiencies which are confounded by scale efficiencies. The use of the VRS

specification will permit the calculation of pure technical efficiency devoid of these scale

efficiency effects. This study assumes the variable return to scale as it seems appropriate

for MFIs particularly operating in developing countries such as Ethiopia. However, for

comparison both assumptions are pursued to estimate the efficiency of the MFIs. By

running both CRS and VRS it is possible to decompose technical efficiency into pure

technical efficiency and scale efficiency and therefore to determine whether a DMU has

been operating at optimal returns to scale, increasing returns to scale, or decreasing

returns to scale ( Celli, 1996).

The study is based on Charnes, Cooper and Rhodes (1978) - CCR model and Banker,

Charnes and Cooper (1984)- BCC model. The basic difference between these two models

is the treatment of returns to scale. While the latter takes into account the effect of

variable returns to scale (VRS), the former restricts DMUs to operate with constant

returns to scale (CRS).

Assume that there are n Decision Making Units (DMUs), and each DMU has m inputs to

produce s outputs. This model measures the relative efficiency ratio of a given DMU (ho)

80

by the sum of its weighted outputs to the sum of its weighted inputs. It can be formulated

as follows as follows:

Max ho=∑ 𝑢𝑟 𝑦𝑟𝑜𝑠𝑟=1∑ 𝑣𝑖 𝑚𝑖=1 𝑥𝑖𝑜

Subject to

∑ 𝑢𝑟 𝑠𝑟=1 𝑦𝑟𝑗

∑ 𝑣𝑖𝑚𝑖=1 𝑥𝑖𝑗

≤ 1, (4.1)

𝑢𝑟 𝑣𝑖 ≥ 0, 𝑖 = 1, … ,𝑚, 𝑗 = 1, … ,𝑛, 𝑟 = 1, … , 𝑠,

where ℎ𝑜is the efficiency ratio of the DMU𝑜;𝑢𝑖 ,𝑢𝑟are virtual multipliers (weights) for the

i th input and the r th output, respectively; m is the number of inputs, s is the number of

outputs and n is the number of DMUs; 𝑥𝑖𝑜is the value of the input i for DMUo, 𝑦𝑟𝑜is the

value of the output r for DMUo.

The equation (1) is fractional programming and has an infinite number of solutions. It can

be solved by adding an additional constraint, ∑ 𝑣𝑖 𝑚𝑖=1 𝑥𝑖𝑜 = 1 . The form then converts to

the multiplier form of the DEA LP problem:

Maxℎ𝑜 = � 𝜇𝑟 𝑦𝑟𝑜𝑠

𝑟=1 (4.2)

Subject to

� 𝜇𝑟 𝑦𝑟𝑜 −� 𝑣𝑖 𝑥𝑖𝑗𝑚

𝑖=1

𝑠

𝑟=1≤ 0, 𝑗 = 1, … ,𝑛,

81

To reflect the transformation, the variables from (u, v) have been replaced by (μ, ν). ε is a

non‐Archimedean quantity defined to be smaller than any positive real number. The dual

form of equation (2) can be written as an equivalent envelopment form as follows:

minℎ𝑜 = 𝜃𝑜 − 𝜀(� 𝑠𝑖− + � 𝑠𝑖+𝑠

𝑟=1

𝑚

𝑖=1)

Subject to

� 𝑥𝑖𝑗

𝑛

𝑗=1𝜆𝑗 + 𝑠𝑖− = 𝜃𝑥𝑖𝑜, 𝑖

= 1, … ,𝑚, (4.3)

� 𝑦𝑟𝑗𝑛

𝑗=1𝜆𝑗 − 𝑠𝑟+ = 𝑦𝑟𝑜, 𝑟 = 1, …,

𝜆𝑗 ,𝑠𝑖−, 𝑠𝑟+ ≥ 0, 𝜀 > 0, 𝑗 = 1, … ,𝑛,

Where 𝜃𝑜 the proportion of DMUo′s inputs needed to produce a quantity of outputs

equivalent to its benchmarked DMUs identified and weighted by the𝜆𝑗 . 𝑠𝑖−. and 𝑠𝑟+are the

slack variables of input and output respectively. 𝜆𝑗is a (𝑛 × 1)column vector of constants

and can indicate benchmarked DMUs of DMUo. If ℎ0∗ = 1 is meant efficient and ℎ𝑜∗ < 1

is meant inefficient where the symbol “*” represents the optimal value.

However, the CCR model is calculated with the constant returns to scale (CRS)

assumption. This assumption is not supportable in imperfectly competitive markets. The

BCC model proposed by Banker, Charnes and Cooper (1984) modifies the CCR model

82

by allowing variable returns to scale (VRS). The CRS LP problem can be easily modified

to account for VRS by adding the convexity constraint

∑ 𝜆𝑗𝑛𝑗=1 = 1 to equation 4.3 to provide

minℎ𝑜 = 𝜃𝑜 − 𝜀(� 𝑠𝑖−𝑚

𝑖=1+ � 𝑠𝑟+

𝑠

𝑟=1)

Subject to

� 𝑥𝑖𝑗𝑛

𝑗=1𝜆𝑗 + 𝑠𝑖− = 𝜃𝑥𝑖𝑜, 𝑖 = 1, … ,𝑚, (4.4)

�𝑦𝑟𝑗

𝑛

𝑗=1

𝜆𝑗 − 𝑠𝑟+ = 𝑦𝑟𝑜, 𝑟 = 1, … , 𝑠,

� 𝜆𝑗𝑛

𝑗=1= 1,

𝜆𝑗,𝑠𝑖−, 𝑠𝑟+ ≥ 0, 𝜀 > 0, 𝑗 = 1, . . ,𝑛,

The Overall Technical Efficiency (OTE) from CCR model can be decomposed into Pure

Technical Efficiency (PTE) and Scale Efficiency (SE). The PTE can be obtained from

BCC model. We can measure the SE for a DMUo by using CCR and BCC model as

follow:

𝑆𝐸 = 𝑂𝑃𝐸𝑃𝑇𝐸� ( 4.5)

83

If the ratio is equal to 1 then a DMU𝑂is scale efficient, otherwise if the ratio is less than

one then a DMU𝑂is scale inefficient.

4.3.2 Tobit Model

The efficiency scores obtained from the DEA in the first stage may be regarded sufficient

to identify whether a particular microfinance is technically efficient or not. However,

there are institutional and environmental factors that are beyond the control of managerial

actions. More recently, in literatures of banking, education, hospitals and ports, among

others, apart from estimating the efficiency of various decisions making units (DMUS),

substantial number of studies have been tried to examine the determinants of efficiency

and productivity by employing a second stage DEA models(Aly et al., 1990; Miller and

Noulas, 1996; Rangan et al ,1988; Fethi, et al. 2000; Jackson and Fethi 2000; Stavarek,

2003; Casu and Molyneux, 2003; Chang and Chiu, 2006; Gupta et al, 2008; Delis and

Papanikolaou, 2009).

In the second stage, the efficiency scores from the first stage are (as dependent variable)

regressed upon institution’s specific and environmental variables to determine what

causes differences in efficiency levels across the DMUs under a given study. Generally,

in literatures the commonly used approaches are ordinary least square, Tobit regression

model, Tobit censored regression, Truncated regression and more recently double

bootstrap approach. An important issue, however, is that efficiency scores are censored at

the maximum value of the efficiency scores.

84

As Wooldridge (2000) noted, traditional methods of regression are not suitable for

censored data, since the variable to be explained is partly continuous and partly discrete

and thus, ordinary least squares analysis generates biased and inconsistent estimates of

model parameters. The empirical results using the Tobit regression model analysis is

more efficient and consistent than using the ordinary least squares model. According to

Hoff (2007), in most case the Tobit approach is sufficient in representing the second

stage DEA models. But McDonald (2009) argues that this approach might be

inappropriate because the efficiency scores are fractional data, not generated by a

censoring process. Based on the results of post-estimation regression analyses it has to be

decided as to which approach is more appropriate. Simar and Wilson (2007) however

recently criticized the Tobit model approach, and suggested instead a double bootstrap

approach in which it is possible to improve the accuracy of the regression estimates.

According to Afonso and Aubyn(2005),even if Tobit results are possibly biased, it is not

clear that bootstrap estimates are necessarily more reliable. In cross country efficiency

studies, Afonso and Aubyn(2005) apply both the usual Tobit procedure and two very

recently proposed bootstrap algorithms and the results are strikingly similar with these

three different estimation processes. Similarly, Borge and Haraldsvik (2009) performed

Tobit regressions and single and double bootstrap procedures in order to explain the

variation in efficiency scores across municipalities. It turns out that the bootstrapping

procedures yields similar results as Tobit in terms of sign and significance of the

coefficients except one variable that loses its significance with the single bootstrap

procedure. In terms of quantitative effects, however, the double bootstrap estimates are

substantially larger than the single bootstrap and Tobit estimates.

85

Based on the justification and given to limited nature of the dependent variable (the range

of efficiency estimated is limited to 0 and 1) a censored Tobit regression model is used

for the study, however, for robust analysis an alternative bootstrap approach suggested

by Simar and Wilson (2007) is also applied to estimate the determinants of Ethiopian

MFIs efficiency.

The Tobit model may be specified for observation (MFIs) i as follows

𝑦𝑖 ∗ = 𝛽′𝑥𝑖 + 𝜀𝑖

𝑦𝑖 = 𝑦𝑖∗𝑖𝑓𝑦𝑖∗ > 0, and (4.6)

𝑦𝑖 = 0, otherwise

Where 𝜀𝑖 ~ N(0, σ2), 𝑥𝑖and 𝛽 are vectors of explanatory variables and unknown

parameters respectively.The 𝑦𝑖∗is a latent variable and 𝑦𝑖 is the DEA score. The

likelihood function (L) is maximized to solve b and based on 19 observations (MFIs) of

xi and yi as

𝐿 = �(1 − 𝐹𝑖)�1

√2𝜋𝜎2𝑦>0𝑦𝑖

× 𝑒1(𝑦𝑖−𝛽𝑥𝑖)

2 𝜎2 (4.7)

Where

𝑭𝑖 = �1

√2𝜋

𝛽𝑥𝑖𝜎

−∞

𝑒𝑡2

2𝑑𝑡

86

The first product is over the observations for which the MFIs are 100% efficient (y = 0)

and the second product is over the observations for which MFIs are inefficient (y >0). Fi

is the distribution function of the standard normal evaluated at𝛽′ 𝑥𝑖 𝜎⁄

4.4 Inputs and output variables

In empirical studies on efficiency of financial institution an important and controversial

issue is choice of inputs and outputs. For banking there are two main approaches - the

production approach and the intermediation approach (Berger and Humphrey, 1997).

Both approaches differ in their view of the role of banks and neither fully captures the

dual roles of banks. Consequently, the outputs and inputs used have not been consistent

in empirical studies and the issue remains debatable in literature. Under the production

approach, banks or financial institutions in general are viewed as institutions making use

of various labor and capital resources to provide different products and services to

customers. Thus, the resources being consumed such as labor and operating cost are

deemed as inputs while the products and the services such as loans and deposits are

considered as outputs. Under the intermediation approach, financial institutions are

viewed as financial intermediaries which collect deposits and other loan able funds from

depositors and lend them as loans or other assets to others for profit. Microfinance

institutions are also financial institutions but their approach and motive differs from other

financial institutions. They are special banks that target mainly poor persons often

without any collateral requirements (Gutierrez-Neito et al., 2005; Tariq et al., 2008).

The selection of inputs and outputs for this study is based on the dual objectives of micro

finance institutions viz., outreach and sustainability framework which is in line with the

87

prior study of (Gutierrez-Neito et al., 2005). Specifically, outputs in this study are defined

to include gross loan portfolio, number of loans and interest and fee income. These items

represent the dual objectives of MFIs. To produce these outputs, the study assumes MFIs

use two main inputs: labor and operating expenses. The selected variables along with

definitions are given below (Table 4.2).The definition for inputs and outputs are based on

the MIXMARKET2.

Table 4.2: Selected inputs and outputs along with definitions

Variables Definition

Inpu

t

Total number of employees Total number of staff members or employees at end of period who were actively employed by the MFI. This number includes contract employees or advisors who dedicate the majority of their time to the MFI, even if they are not on the MFI’s roster of employees.

Operating expenses

Expenses related to operations, such as all personnel expenses, rent and utilities, transportation, office supplies, ,depreciation and amortization, and administrative expense

Out

put

interests and fee income All income on loans made to clients

Gross loan portfolio

All outstanding principal for all outstanding client loans including current, delinquent and restructure loans but not loans that have been written off. It excludes interest receivable and employee loans

Number of loans outstanding(number)

Number of loan accounts associated for any outstanding loan balance with the MFI and any portion of the loan portfolio.

2 is the most renowned and global web‐based microfinance information platform

88

Finally, the three outputs and the two inputs are specified as follows:

Out put Input

y1: Gross loan portfolio x1: Labor

y2: Interest and fee income x2: Operating expenses

y3: Number of loans

4.5 The Data

The study is based on annual data covering the period from 2004-2009 for the 19 micro

finance institutions operating in Ethiopia. In fact, there are 29 MFIs currently operating in

the country; however, data cannot be generated from all the MFIs as some lack sufficient

data while others are new to be included in the analysis. The study period is limited to

this period due the availability of the data. The data is extracted from the financial

statements provided by the Association of Ethiopian Microfinance Institutions (AEMFI),

National Bank of Ethiopia (NBE) and the Mix Market3.

4.6 Empirical Findings

In this section the study provides the efficiency results of for the industry as well as for

specific microfinance institutions under both the assumptions - Constant Returns to Scale

and Variable Returns to Scale. As discussed earlier, the DEA technical efficiency is

3is the most renowned and global web-based microfinance information platform. It yields information on micro finances institutions around the globe and provides information to sector actors and the public at large.

89

calculated by assuming both Constant Returns to Scale (CRS) and Variable Returns to

Scale (VRS). The Constant Returns to Scale assumption is only appropriate when all

MFIs are operating at an optimal scale. However, factors like imperfect competition and

constraints on finance may cause a microfinance not to operate at optimal scale. In order

to exploit the scale efficiency or inefficiency the study makes use of both assumptions.

Table 4.3 presents descriptive statistics of all input and output variables used in this

study.

90

Table 4.3: Descriptive statistics of variables (inputs and outputs) in US dollars

2004 2005 2006 2007 2008 2009

Output Gross loan portfolio Average 6328424.85 9744770.55 13766157.37 18844364.53 23339095.90 20927300.10

Std dev 12797557.82 20163130.28 25564762.22 36565166.93 46163287.85 38405984.36

Max 46365572 77918547 85266397 118766535 155668558 131184763

Min 103480 170229 263382 280132 427230 786650

Number of loans Average 58527.63 71582.16 85423.95 103368.3 113679.6 126817.8

Std dev 106247.5 132604.2 148559.6 174038.2 193172.8 201387.6

Max 351163 434814 536804 597723 710576 687586

Min 1153 1365 1917 1924 2984 2800

Interest & fee income Average 766112.75 1176197.55 1784483.84 1784483.84 3168793.15 3252691.95

Std dev 1531603.59 2394933.57 3333634.44 4602177.50 6408038.59 6325184.72

Max 5458600 8022074 11671356 16947735 25368310 25152802

Min 18806 32860 38236 74535 101127 152918

Input Operating expenses Average 338073.07 456196.20 661512.40 839407.10 1116844.00 1121145.55

Std dev 483416.053 677295.702 890280.763 1188215.847 1799420.306 1522281.266

Max 1865700 2687450 3216371 4336629 7394112 5422833

Min 25894 34499 51585 63465 72290 132600

No of employees Average 238.00 314.40 378.75 432.35 490.60 515.95

Std dev 408.790 529.080 604.587 684.013 754.046 802.781

Max 1670 1915 2065 2363 2590 2732

Min 17 18 27 28 38 37

Source: Author’s computation

91

As shown in Table 4.3, on an average all the outputs and inputs have increased over the

years. These statistics indicate that mean gross loan portfolio of microfinance institutions

has increased more than threefold (from 6.3 million USD to 20.9 USD in 2009) and

number of loans also increased more than two fold (from 58527 in 2004 to 126817 in

2009). Similarly mean interest and fee income has increased four- fold (i.e., from 766112

million in 2004 to 3252691) during the study period. Similar trend could be observed for

the input variables. Meanwhile, standard deviations for all the variables show that there

seem to exist variation among the sample MFIs in size as measured in output

produced(gross loan portfolio, number of loans and interest and fee income) and inputs

used (operating expense and number of staff). This implies that Ethiopian microfinance

industry comprises big, medium and small scale microfinance institution. Thus, the

observed differences in values of the outputs and inputs might result from this scale

differences. However, the methodology used allows assessment of efficiency and

productivity improvements of institutions (DMUs) ignoring their scale of operations

(Cooper et al., 2000).

4.6.1 Efficiency Estimates Using DEA

i. Efficiency Results under the Constant Returns to Scale (CCR Model)

The results of technical efficiency for the industry and specific institution are presented in

Table 4.4 and Table 4.5 respectively. It should be noted that the technical efficiency

estimates represent all optimal values based on the assumption of the constant returns to

scale model (CCR model) for the industry and as well as for specific microfinance

institution for the period of 2004-2009.

92

Table 4.4: Summary statistics of efficiency scores under the Constant Returns to Scale(CCR Model)

Source: Author’s estimates

Summary of the results of CCR-Model

2004 2005 2006 2007 2008 2009 Average

Number of DMU 19 19 19 19 19 19 19

Number of efficient DMU 2 1 1 2 4 5 3

Max efficiency score 1 1 1 1 1 1 1

Min efficiency score 0.115 0.275 0.241 0.279 0.219 0.407 0.256

Std. dev of efficiency .269 .171 .204 .244 .232 .218 0.223

Average of efficiency M 0.524 0.546 0.658 0.761 0.736 0.775 0.667

Average of inefficiency (1-M)/M 0.908 0.831 0.519 0.314 0.358 0.290 0.537

Percentage of the DMU in 1 10.53% 5.26% 5.26% 10.53% 21.05% 26.32% 13.16%

93

Results from the analysis reveal that average technical efficiency of the MFIs during the

study period ranges from 0.524(52.4%) in 2004 to 0.775(77.5%)in 2009 with an overall

mean efficiency of 0.667(66.7%).This means that Ethiopian MFIs could increase their

output by 33.3%using the exiting level of inputs. Besides that, the average computed

standard deviation of 0.223 shows that there is a large dispersion in terms of technical

efficiency among the MFIs.

Year wise, the MFIs could improve their output by 47.4%, 45.4%, 34.2%, 23.9%, 26.4%

and 22.5% in year 2004, 2005, 2006, 2007, 2008 and 2009 respectively without any

additional resources. More importantly, the yearly technical efficiency analysis reveals

that two MFIs (10%) in 2004, one (5%) in 2005, one (5%) in 2006,two (10%) in

2007four (21%) in 2008and five (21%) in 2009 are found to be efficient as indicated by

efficiency scores equal to 1(100%).On the other hand, seventeen (87%), eighteen (87%),

(61%), seventeen(12), fifteen (52%) and fourteen(35%) of the institutions have been

operating inefficiently in 2004, 2005, 2006, 2007, 2008 and2009 compared with the most

efficient MFIs in the sample.

It is evident from the results that efficiency of the industry appears to have increased

significantly over the period review. In other words, average inefficiency has been

decreasing significantly from 0.908[1-(0.524/0.524)] in 2004 to 0.290[1- (0.775/0.775)]

in 2009(see Table 4.1). However, the result implies that still on average MFIs could

possibly increase their output by about 33 % with the existing level of input through

efficient utilization of these inputs.

94

By pulling the data an attempt has been made to look at the distribution of efficiency

scores. Figure 4.1 shows the frequency distribution of technical efficiency score of the

MFIs. As it can be seen the distribution of efficiency scores is skewed towards the higher

efficiency scores (about 50 % MFIs score a relative efficiency between 70% and 100%

and nearly 25% of the sample MFIs with efficiency score above 90%).

Figure 4.1: Technical Efficiency Score distribution

Source: Author’s computation

1

6

10

13

21

7

17

11

28

0

5

10

15

20

25

30

<20 20‐30 30‐40 40‐50 50‐60 60‐70 70‐80 80‐90 90‐100

95

Table 4.5: Relative efficiency of Ethiopia MFIs in CCR model

No MFIs 2004 2005 2006 2007 2008 2009 Average

1 ACSI 0.804 0.659 0.917 0.998 1.000 1.000 0.896

2 ADCSI 0.989 0.611 0.536 0.695 0.760 1.000 0.765

3 AVFS 0.307 0.332 0.455 0.527 0.529 0.555 0.451

4 BGMFISC 0.288 0.445 0.775 1.000 0.982 1.000 0.748

5 Buusaa Gonofaa 0.387 0.382 0.527 0.736 0.739 0.810 0.596

6 DECSI 1.000 1.000 1.000 1.000 1.000 1.000 1.000

7 Eshet 0.738 0.702 0.714 0.814 0.661 0.599 0.705

8 Gasha 0.357 0.504 0.459 0.545 0.451 0.595 0.485

9 Metemamen 0.115 0.478 0.797 0.979 0.820 0.985 0.695

10 OCSSCO 0.553 0.569 0.541 0.969 0.861 0.855 0.724

11 OMO 0.329 0.723 0.833 0.803 1.000 1.000 0.781

12 PEACE 1.000 0.586 0.810 0.982 0.781 0.729 0.815

13 SFPI 0.585 0.555 0.735 0.858 0.722 0.754 0.701

14 Wasasa 0.507 0.406 0.684 0.950 0.930 0.921 0.733

15 Wisdom 0.493 0.370 0.461 0.491 0.467 0.479 0.460

16 Meklit 0.363 0.531 0.764 0.497 0.611 0.434 0.533

17 Sidama 0.283 0.714 0.865 0.997 1.000 0.998 0.809

18 SEYAMFI 0.271 0.275 0.241 0.342 0.445 0.607 0.363

19 Agar I 0.595 0.540 0.387 0.279 0.219 0.407 0.404

Mean 0.524 0.546 0.658 0.761 0.736 0.775 0.667

Source: Author’s computation

96

Turning to specific microfinance institution, the results show that there seem to be much

variation in efficiency level among the MFIs (see Table 4. 5 and Figure 4.2). For the year

2004, only 2(DECSI and PEASE) out of 19 MFIs are found fully efficient, with

efficiency score of 1(100%). However for the years 2005 and 2006 only one institution

(DECSI) turned to be efficient. In the following years two (DECSI and BGMFISC),

four(ACSI, DECSI, OMO and SIDAMA) and five(ACSI, ADCSI, BGMFISC DECSI,

and OMO MFIs) are found to be fully efficient in the years 2007, 2008 and 2009,

respectively. Overall, DECSI is the most efficient microfinance in all the six considered

years with efficiency score of 1(100%) followed by ACSI and PEASE with an average

technical efficiency 0.896 and 0.814 respectively. On the other hand SEYAMFI, Agar I

and AVFS are the most inefficient MFIs observed with an average technical efficiency of

0.363, 0.404 and 0.450 respectively during the study period.

97

Figure 4.2: Average Technical Efficiency score by Institution CCR-Model

Source: Author’s computation

00.10.20.30.40.50.60.70.80.9

1 0.896

0.765

0.451

0.748

0.596

1

0.705

0.485

0.695 0.724 0.781 0.815

0.701 0.733

0.46 0.533

0.809

0.363 0.404

Average Efficiency

98

Figures 4.3 and 4.4 provide the most efficient and least efficient of the sample MFIs

respectively. Accordingly, DECSI, ACSI, PEACE, SIDAMA, OMO ADCSI are found

to be most efficient institutions. On the other hand, Meklit, Ghasha, Wisdom,AVFS, Agar

and SEYAMFI are found to the least efficient MFIs during the study period.

Figure 4.3: MFIs with highest Efficiency Scores

Source: Author’s computation

Figure 4.4: MFIs with lowest Efficiency scores

Source: Author’s computation

0

0.2

0.4

0.6

0.8

1

1.2

DECSI ACSI PEACE Sidama OMO ADCSI

00.10.20.30.40.50.60.70.80.9

1

Meklit Gasha Wisdom AVFS Agar I SEYAMFI

99

Table 4.6 provides ranking of Ethiopian MFIs under the assumption of constant returns to

scale (CCR model). Accordingly, DECSI is the best practicing MFIs with technical

efficiency score of 1 and thus ranked first followed by ACSI with efficiency score of

0.896. PEACE (0.819), Sidama (0.810), and ADCSI (0.805) have occupied third, fourth

and fifth place respectively.

Table 4.6: Ranking of MFIs based on CRS(CCR Model)

MFIs Average efficiency score Rank

DECSI 1.000 1

ACSI 0.896 2

PEACE 0.819 3

sidama 0.810 4

ADCSI 0.805 5

OMO 0.781 6

OCSSCO 0.740 7

Wasasa 0.737 8

BGMFISC 0.724 9

Eshet 0.705 10

SFPI 0.704 11

Mettemenan 0.696 12

Bussa Guffa 0.600 13

Meklit 0.549 14

Gasha 0.492 15

Wisdom 0.464 16

AVFS 0.461 17

Agar I 0.413 18

Shashemene 0.386 19 Source: Author’s computation

100

ii. Efficiency Results under the Variable Returns to Scale (BCC Model)

Mean while the output oriented under the Variable Returns to Scale (BCC model) results

are provided in Table 4.6 for the industry and Table 4.7 for specific microfinance

institution. The results of the analysis show that Ethiopian MFIs experienced moderate

level of technical efficiency along with a substantial improvement over the study period

(see Table 4.7 and Figure 4.5). Annual average technical efficiency scores by the MFIs

ranges from 0.646(2004) to 0.890(2009) with an overall industry mean of 0.786.

However, the result suggests that still there is substantial scope for Ethiopian MFIs to

improve their efficiency performance without the need to use more resources, i.e, MFIs

could increase their output by 21.4% on average. More specifically, MFIs could improve

their efficiency by 35.4%, 28.70%, 19.6%, 16.6%, 16.9% and 11% in year 2004, 2005,

2006, 2007, 2008 and 2009 respectively.

Further, during the period on an average only about 14% of the MFIs are operating with

optimal scale operation while majority of the institutions (78.95%) are operating with

increasing returns to scale. Thus, it can be inferred that increasing returns to scale is

predominant in the Ethiopian MFIs. This suggests that majority of MFIs can increase

their operating scale to gain scale efficiency.

101

Table 4. 7: Summary statistics of efficiency scores under VRS (BCC model)

Summary of the results of BCC – model

2004 2005 2006 2007 2008 2009 Average

Number of DMU 19 19 19 19 19 19 19

Number of efficient DMU 6 4 6 6 7 8 6

Max efficiency score 1 1 1 1 1 1 1

Min efficiency score 0.153 0.391 0.467 0.496 0.376 0.495 0.396

Std. dev of efficiency .293 .201 .189 .178 .192 .133 0.197

Average of efficiency M 0.646 0.713 0.804 0.834 0.831 0.890 0.786

Average of inefficiency (1-M)/M 0.547 0.402 0.243 0.199 0.203 0.123 0.286

Percentage of the DMU in 1 31.51 21.05 31.58 31.58 36.84 42.10 32.46

Scale inefficiency[1-(CRS/VRS)] 0.189 0.234 0.182 0.0878 0.114 0.129 0.156

MFIs operating at IRS(%) 84.21 89.49 89.49 68.42 68.42 73.68 78.95

MFIs operating at RS(%) 5.26 5.26 10.53 15.79 5.26 5.26 7.89

MFIs operating at optimal scale 10.53 5.26 5.26 15.79 26.32 21.05 14.04

Source: Author’s computation

102

Figure 4.5: Efficiency trend of Ethiopian MFIs BCC Model

Source: Author’s computation

Considering specific microfinance results, for the first year of analysis (2004), six MFIs

out of nineteen are operating at the best practice frontier or are efficient and have scored

1(100%). These include ACSI, ADCSI, DECSI, PEASE, SEYAMFI and Agar I.

However, in the next year (2005) out of the efficient institutions only four MFIs (ACSI,

DECSI, SEYAMFI and Agar remained most efficient scoring 1(100%). In the year 2006

the number of efficient MFIs increased to six (ACSI, DECSI, Metemamen, PEASE,

SEYAMFI and Agar I), in the year 2007 still same number of MFIs operate efficiently

but include (ACSI, BGMFISC, DECSI, Metemamen, PEASE, and SEYAMFI), in the

year 2008, 36.84% or seven MFIs namely ACSI, BGMFISC, DECSI, Metemamen,

OMO, Sidama and SEYAMFI and in the year 2009, 42.10% or eight 8 MFIs in this case

ADCSI joined the efficient group of year 2008.

00.10.20.30.40.50.60.70.80.9

1

2003 2004 2005 2006 2007 2008 2009 2010

103

Table 4.8: Relative efficiency of Ethiopian MFIs under VRS(BCC model)

No MFIs 2004 2005 2006 2007 2008 2009 Average

1 ACSI 1.000 1.000 1.000 1.000 1.000 1.000 1

2 ADCSI 1.000 0.634 0.556 0.696 0.798 1.000 0.780

3 AVFS 0.481 0.520 0.650 0.630 0.717 0.918 0.653

4 BGMFISC 0.315 0.528 0.833 1.000 1.000 1.000 0.779

5 Buusaa Gonofa 0.468 0.461 0.565 0.738 0.774 0.810 0.636

6 DECSI 1.000 1.000 1.000 1.000 1.000 1.000 1

7 Eshet 0.898 0.810 0.781 0.856 0.731 0.835 0.818

8 Gasha 0.400 0.556 0.568 0.584 0.563 0.919 0.598

9 Metemamen 0.153 0.933 1.000 1.000 1.000 1.000 0.848

10 OCSSCO 0.555 0.572 0.581 0.970 0.905 0.869 0.742

11 OMO 0.335 0.746 0.840 0.819 1.000 1.000 0.790

12 PEACE 1.000 0.727 1.000 1.000 0.900 0.775 0.900

13 SFPI 0.649 0.673 0.786 0.861 0.770 0.756 0.749

14 Wasasa 0.662 0.518 0.747 0.955 0.969 0.923 0.795

15 Wisdom 0.525 0.391 0.467 0.496 0.475 0.495 0.475

16 Meklit 0.523 0.659 0.944 0.642 0.814 0.752 0.722

17 Sidama 0.303 0.810 0.963 1.000 1.000 1.000 0.846

18 SEYAMFI 1.000 1.000 1.000 1.000 1.000 1.000 1

19 Agar I 1.000 1.000 1.000 0.593 0.376 0.862 0.805

Mean 0.646 0.713 0.804 0.834 0.831 0.890 0.786

Source: Author’s computation

104

Figure 4.6: Average Technical Efficiency score by Institution-BCC model

Source: Author’s computation

0

0.2

0.4

0.6

0.8

11

0.78

0.653

0.779

0.636

1

0.818

0.598

0.848 0.742

0.79 0.9

0.749 0.795

0.475

0.722

0.846

1

0.805 0.786

Average Efficiency

105

In sum, the result of the analysis shows that during the study period, on an average ACSI,

DECSI, and SEYAMFI are the most efficient MFIs with an average efficiency score of 1

followed by PEACE (0.9), Metemamen(0.848), Sidama(0.486) and ESHET (0.818).On

the other hand, Ghasa and Wisdom are found to be the least efficient MFIs.

Table 4.9 provides ranking of Ethiopian MFIs under the assumption of variable returns to

scale (BCC model). Accordingly, ACSI, DECSI and Shashemene are the best practicing

MFIs with technical efficiency score of 1(100%) and thus are ranked first followed by

PEACE with efficiency score 0.930. Mettemamen(0.848), Sidama (0.846), Eshet (0.820)

and ADCSI(0.814) have occupied third, fourth fifth and sixth place respectively.

106

Table 4.9: Ranking of MFIs based on VRS (BCC Model)

MFIs Average efficiency score BCC model Ranking

ACSI 1.000 1

DECSI 1.000 1

Shashemene 1.000 1

PEACE 0.930 2

Mettemenan 0.848 3

sidama 0.846 4

Eshet 0.820 5

ADCSI 0.814 6

Agar I 0.808 7

Wasasa 0.805 8

OMO 0.790 9

BGMFISC 0.767 10

OCSSCO 0.758 11

SFPI 0.753 12

Meklit 0.733 13

AVFS 0.657 14

Bussa Guffa 0.640 15

Gasha 0.600 16

Wisdom 0.476 17 Source: Author’s computation

When estimating efficiency under the Variable Returns to Scale (BCC model), the

number of efficient MFIs and the average technical efficiency for the industry are

increased (i.e., higher than in the case of Constant Returns to Scale) (See Table 4.7).The

results suggest that the prevalence of pure technical inefficiency and scale inefficiencies

(See Figure 4.7). Here it is worth mentioning the case of SEYAMFI which is identified as

107

the most inefficient in CRS, but is found to be one of the most efficient under the VRS

assumption. This indicates that the inefficiency for SEYMFI is due to scale inefficiency

rather than management practice.

Figure 4.7: Efficiencies of MFIs CCR and BCC Model and Scale

Efficiency

Source: Author’s computation

Scale Efficiency

Technical efficiency can be further examined by decomposing it into pure technical

efficiency and scale efficiency. Decomposing technical efficiency into pure technical

efficiency and scale efficiency allows us to gain insight into the main sources of

inefficiencies. The annual average technical, pure technical and scale efficiencies of

Ethiopian MFIs are provided in Table 4.10.

0

0.2

0.4

0.6

0.8

1

1.2

BCC

CCR

Scale

108

Table 4.10: Annual average technical, pure technical and scale

efficiencies of the MFIs

Year Technical

efficiency

Pure technical

efficiency

Scale

efficiency

2004 0.524 0.646 0.811

2005 0.546 0.713 0.766

2006 0.658 0.804 0.818

2007 0.761 0.834 0.912

2008 0.736 0.831 0.886

2009 0.775 0.890 0.871

Overall average 0.667 0.786 0.849 Source: Author’s computation

The overall average technical efficiency of Ethiopian MFIs over the period 2004-2009 is

66.7 percent. The pure technical efficiency on average is 78.6 percent. Further the scale

efficiency is 84.9 percent on average. It can be seen in Table 4.10, after decomposing the

technical efficiency into pure technical and scale efficiency, Ethiopian MFIs pure

technical efficiency is lower than the scale efficiency for most of the years. This implies

that the Ethiopian microfinance institutions’ technical inefficiency is mainly due to the

pure technical inefficiency rather than the scale inefficiency. In other words, the

relatively lower pure technical efficiency in comparison to scale efficiency suggests that

inefficiencies are mostly due to inadequate management practices (pure technical

inefficiency), than to inappropriate size of institutions (scale inefficiencies).However, it

should be noted that scale inefficiency is as equally prevalent as pure technical

inefficiency in the industry.

109

Table 4.11 shows the decomposition of technical efficiency for the year 2009 only. That

is the discussion regarding to scale inefficiency and returns to scale is based on the year

2009. It should be noted that the decomposition of technical efficiency for the year 2004,

2005, 2006, 2007, and 2008 is provided in the annexure of the thesis.

110

Table 4.11: Decomposition of technical efficiency for the year 2009

No Institution Technical

Efficiency(CRS)

Pure Technical

efficiency(VRS)

Scale

efficiency

Return to

scale

1 ACSI 1.000 1.000 1.000 CRS

2 ADCSI 1.000 1.000 1.000 CRS

3 AVFS 0.555 0.918 0.605 IRS

4 BGMFISC 0.963 0.972 0.991 IRS

5 Buusaa Gonofaa 0.829 0.834 0.994 IRS

6 DECSI 1.000 1.000 1.000 CRS

7 Eshet 0.599 0.835 0.717 IRS

8 Gasha 0.599 0.919 0.652 IRS

9 Metemamen 0.985 1.000 0.985 IRS

10 OCSSCO 0.855 0.869 0.984 DRS

11 OMO 1.000 1.000 1.000 CRs

12 PEACE 0.756 0.851 0.888 IRS

13 SFPI 0.770 0.777 0.992 IRS

14 Wasasa 0.941 0.947 0.993 IRS

15 Wisdom 0.500 0.503 0.994 IRS

16 Meklit 0.434 0.752 0.577 IRS

17 Sidama 0.998 1.000 0.998 IRS

18 SEYAMFI 0.642 1.000 0.642 IRS

19 Agar I 0.407 0.862 0.472 IRS

Mean 0.781 0.897 0.868

Source: Author’s computation. Notes: CRS denotes constant returns to scale most productive scale size.; DRS denotes

decreasing returns to scale and IRS denotes increasing returns to scale.

111

As shown in Table 4.11, the overall average technical efficiency (under the assumption of

CRS) is 78.1 percent. Technical inefficiency score from CRS is made up of two

components, one due to technical inefficiency and one due to scale inefficiency. The

analysis reveals that scale inefficiency is as equally prevalent as pure technical

inefficiency as such pure technical inefficiency accounts for 10.3 percentage points and

scale inefficiency accounts for 13.2 percentage points.

As far as scale inefficiency is concerned, in the year 2009 four (21%) of the microfinance

institutions are scale efficient because they have a relative scale efficiency score of 100%.

Majority of the MFIs (69%) have scale efficiency of less than 100%, and as such they are

scale inefficient. Increasing returns to scale is the predominant form of scale inefficiency

observed.

Figure 4.8: Nature of Return to scale

Source: Author’s computation

CRS 21%

DRS 5%

IRS 74%

Return to scale year 2009

112

Figure 4.8 shows the nature of returns to scale for the sample MFIs graphically. These

results show that 21 percent of microfinance institutions in the sample in 2009 are

operating at their optimal scale. Further, the results of the analysis show that about 74 per

cent of the MFIs are operating below their optimal scale. This means that these

institutions could increase their technical efficiency by continuing to increase their size.

The results also indicate that 5 percent of the MFIs are above their optimal scale and

hence could increase their technical efficiency by decreasing their size.

4. 6.1.1 Efficiency by size

In order to get an insight whether size of microfinance matters in Ethiopian microfinance

industry, the study analyzes the efficiency differences among MFIs belonging to different

size classes and their efficiency scores. To classify the MFIs by size, number of active

borrowers which is a proxy of outreach is used as a criteria as per the definition of MIX

MARKET peer group. Accordingly, MFIs with number of borrowers less than 15,000 is

considered small, greater than 15,000 and less than 50,000 medium and MFIs with more

than 50,000 active borrowers as large. Table 4.10 summarizes average efficiency score of

the three group classifications, large, medium and small for the sample study period.

113

Table 4.12: Relative Efficiency of Ethiopian MFIs in BCC model by Size

Classification MFIS 2004 2005 2006 2007 2008 2009 Average

Large

ACSI 1 1 1 1 1 1 1

ADCSI 1 0.634 0.556 0.696 0.798 1 0.781

DECSI 1 1 1 1 1 1 1

OCSSCO 0.555 0.572 0.581 0.97 0.905 0.869 0.742

OMO 0.335 0.746 0.84 0.819 1 1 0.79

Average 0.778 0.790 0.795 0.897 0.941 0.974 0.863

Medium BGMFISC 0.315 0.528 0.833 1 1 1 0.779

B. Gonofaa 0.468 0.461 0.565 0.738 0.774 0.81 0.636

Eshet 0.898 0.81 0.781 0.856 0.731 0.835 0.819

PEACE 1 0.727 1 1 0.9 0.775 0.9

SFPI 0.649 0.673 0.786 0.861 0.77 0.756 0.749

Wasasa 0.662 0.518 0.747 0.955 0.969 0.923 0.796

Wisdom 0.525 0.391 0.467 0.496 0.475 0.495 0.475

Sidama 0.303 0.81 0.963 1 1 1 0.846

Average 0.603 0.615 0.768 0.863 0.827 0.824 0.75

Small Metemamen 0.153 0.933 1 1 1 1 0.848

Gasha 0.4 0.556 0.568 0.584 0.563 0.919 0.598

Meklit 0.523 0.659 0.944 0.642 0.814 0.752 0.722

AVFS 0.481 0.52 0.65 0.63 0.717 0.918 0.653

SEYAMFI 1 1 1 1 1 1 1

Agar I 1 1 1 0.593 0.376 0.862 0.805

Average 0.593 0.778 0.860 0.741 0.745 0.908 0.771 Source: Author’s computation

As shown the results from Table 4.12, the average technical efficiency scores are found

to be 0.8630.750, and 0.771for large, medium and small MFIs respectively. It is clear that

the large MFIs are performing better compared to medium and small MFIs. In other

114

words, large MFIs are relatively technically efficient and this is followed by the small

MFIs and finally the medium MFIs. This implies that large MFIs are taking advantage of

scale economies in the intermediation process. To test whether the observed efficiency

differences between MFIs belonging to different size classes are statistically significant

or not, the nonparametric Kruskal-Wallis test is performed for the efficiency scores. The

null hypothesis is that the rank of technical efficiency scores, based on the mean is the

same across the different microfinance sizes. Using the Kruskal-Wallis test, the null

hypothesis for microfinance sizes is rejected at the 1% significance level. This provides

evidence that microfinance size does matter when comparing microfinance technical

efficiency.

Figure 4.9: Efficiency trend of Ethiopian MFIs by Size

Source: Authors’ calculation

0

0.2

0.4

0.6

0.8

1

1.2

2003 2004 2005 2006 2007 2008 2009 2010

All

Large

Meduim

Small

115

Figure 4.9 shows the trend efficiency results by size and accordingly large MFIs are

performing better compared to medium and small institutions and appear to be the most

efficient over the period. Medium size MFIs demonstrated modest improvement and

stable efficiency; however, on an average, the small MFIs are more efficient than the

medium MFIs in the period.

4.6.1.2.Efficiency by Ownership Structure

In order to see whether ownership type of microfinance matters in Ethiopian

microfinance industry, the study analyzes the efficiency differences between the two

groups of MFIs (i.e., government affiliated versus non government affiliated). The

estimated average efficency of the MFIs in the period seems to vary by ownership

structure. Under both assumptions(models), on an average, government affilated MFIs

are found to be outperformed the non government affilated MFIs( Figure4.10 and 4.11).

Figure 4.10: Efficiency by Ownership CCR Model

Source: Author’s computation

2004 2005 2006 2007 2008 2009Gov't affilated 0.533 0.582 0.687 0.824 0.829 0.853Non_ Gov't 0.481 0.536 0.65 0.751 0.738 0.755

00.10.20.30.40.50.60.70.80.9

Aver

age

effi

cien

cy

Technical Efficiency- CRS, 2004-2009, by ownership

116

Figure 4.11: Efficiency by Ownership BCC Model

Source: Author’s computation

4.6.2 Efficiency Estimates Using SFA

In the previous section, the study focused on the preferred DEA for measuring the

technical efficiency of Ethiopian MFIs. However, it must be acknowledged that the DEA

approach also has some drawbacks compared to SFA as discussed in chapter 3 of the

thesis. In this section for the purpose of consistency and robustness of the results, the

study presents and discusses the empirical results of the SFA and then tries to compare

the results with the DEA estimates. The frequency distributions of technical efficiency

scores of the MFIs using the SFA are presented in Table 4.13.

2004 2005 2006 2007 2008 2009Gov’t affilated 0.6 0.705 0.76 0.845 0.89 0.941Non_Gov't 0.604 0.7 0.806 0.832 0.842 0.885

00.10.20.30.40.50.60.70.80.9

1

Aver

age

effic

ienc

y Technical efficiency -VRS,2004-2009, by ownership

117

Table 4.13: Frequency Distribution of Efficiency of MFIs under SFA Efficiency levels Frequency Percentage

TE ≤ 10 0 0

0 < TE≤ 20 0 0

20 < TE≤ 30 2 1.75

30 < TE≤ 40 1 0.88

40 < TE≤ 50 6 5.26

50 < TE≤ 60 18 15.79

60 < TE≤ 70 19 16.67

70 < TE≤ 80 31 27.19

80 < TE≤ 90 31 27.19

TE > 90 6 5.26

Total 114 100

Mean 0.717

Std. Dev. 0.139

Minimum 0.267

Maximum 0.912 Source: Author’s computation

The estimated result shows that mean technical efficiency of the MFIs during the period

2004 to 2009 is found to be 71.72% ranging from minimum 26.74% to maximum

91.23%. The MFIs thus show considerable differences in inefficiency from 8.77% to

73.28 %. The average efficiency indicates that Ethiopian MFIs have realized 71.72 % of

the potential output to be realized. In other words, on the whole, the average

118

microfinance institution can increase its output level by 28.28 % using the same amount

of inputs. However, if the average microfinance institution has to attain the level of the

most efficient MFI within the sampled institutions, then the average MFI may increase

output by 21.38% [1- (71.72/91.23)]. Similarly the most inefficient institution can

increase its output by 70.69%.

Table 4.14: Average efficiency year wise -SFA Year Mean efficiency

2004 0.634

2005 0.716

2006 0.733

2007 0.726

2008 0.753

2009 0.74 Source: Author’s computation

As it can be seen from the Table 4.14 in year 2004 Ethiopian MFIs resulted to show mean

efficiency score of 0.634 which is relatively low; however, in 2009 the mean efficiency

turned to be 0.74. During the period except slight efficiency decline from 2006 to 2007

and 2008 to 2009 they have shown interesting improvement in their efficiency

performance. Overall, over the period the mean efficiency increased by about 16.6

percent. The efficiency improvement in the period is more visible in Figure 4.12 below.

119

Figure 4.12: Efficiency Trend -SFA

Source: Author’s computation

From the figure above, it is interesting to observe a clear trend in time which suggests

that Ethiopian MFIs have experienced continuous improvement in their efficiency

performance over the period.

Table 4.15 provides the mean technical efficiency score of each MFI along with ranking

based on SFA. Accordingly, DECSI is the best practicing MFIs with technical efficiency

score of 0.87 and thus ranked first followed by PEACE with efficiency score 0.858.

ADCSI (0.808) Eshet (0.797) and SFPI (0.790) have occupied third, fourth and fifth

place respectively.

0.560.58

0.60.620.640.660.68

0.70.720.740.760.78

2004 2005 2006 2007 2008 2009

Average efficiency trends, 2004-2009

120

Table 4.15: Ranking of MFIs under SFA

MFIs Average efficiency scores Rank

DECSI 0.870 1

PEACE 0.858 2

ADCSI 0.808 3

Eshet 0.797 4

SFPI 0.790 5

Meklit 0.765 6

Wasasa 0.758 7

Shashemene 0.748 8

BGMFISC 0.741 9

Agar I 0.741 10

Gasha 0.729 11

Sidama 0.707 12

AVFS 0.704 13

OMO 0.679 14

ACSI 0.666 15

OCSSCO 0.630 16

Mettemenan 0.614 17

Wisdom 0.523 18

Bussa Guffa 0.523 19 Source: Author’s computation

4.6.3 Comparing Empirical Results

In this section the study tries to compare the empirical results obtained from the DEA and

SFA approaches. The two approaches measured the efficiency of microfinance

institutions relative to different frontiers. Hence, differences in efficiency scores could be

expected and yet, there is expectation that there would be an overall consistency between

121

the two approaches. Iraizoz et al. (2003) claims that the technical efficiency estimates

need to fulfill a certain level of consistency if they are to be of any use for regulatory

analysis or other purposes.

In order to compare the results obtained by the DEA (CRS and VRS) and SFA, the study

followed the recommendations of Bauer et al. (1998), who proposed a set of consistency

conditions. According to Bauer et al. (1998) there are three conditions to measure how far

the different approaches are mutually consistent. The first one is that the efficiency scores

obtained by the different approaches should have comparable means, standard deviations

and other distributional properties. The second condition is that the different approaches

should rank the MFIs in approximately the same order. The third condition stated that the

different approaches should identify largely the same MFIs as best-practice and as worst-

practice.

Table 4.16: Summary of efficiency estimates of different models

Variable Obs Mean Std. Dev. Min Max

Efficiency -CRS 114 .673 .242 .115 1

Efficiency-VRS 114 .792 .217 .153 1

Efficiency SFA 114 .718 .129 .267 .912

Source: Author’s computation

Table 4.16 provides summary of technical efficiency estimates under different

approaches. Accodingly, it can be noted that the three approaches seem to result

insimilar efficiency estimates. Indeed, the constant returns to scale efficiency(CRS) is

lower than variable returns to scale(VRS) due to the presence of scale efficiencies. Not

122

surprisingly, the technical efficiency estimated by DEA-CRS is lower than the one

estimated by SFA, as DEA attributes the entire distance from the frontier to inefficiency.

The standard deviation of efficiency estimates for SFA 0.129 is also less than the

standard deviation from the DEA VRS 0.217 and DEA-CRS 0.242.Most importanly, the

average efficiecny scores of 0.673, 0.792 and 0.718 under CRS,VRS and SFA estimates

respectivly imply that on an average nearly 33%, 21% and 28% inefficiecny appear to

exist. This means that with the given resources, microfinance could, on an average,

increase outputs by approximately 21% to 33%. An important implication of the analysis

is that regardless of the approaches used, there is substaintial room for the MFIs to

enhance their ouput with the extsing resources.

Figure 4.13: Efficiency trend by different approaches

Source: Author’s computation

Figure 4.13 presents the average efficiency scores of MFIs for the period based on

different estimation approaches. As can be seen, regardless of the approaches used,

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

2004 2005 2006 2007 2008 2009

DEA CRS

DEA VRS

SFA

123

Ethiopian MFIs have experienced continuous efficiency improvement in the period. Thus

it can be inferred the three approaches seem to give us similar efficiency estimates.

To give deep insight, the average efficiency scores over the period under the three

approaches for each institution are displayed in Figure 4.14.In fact in all the cases the

efficiency score under the DEA-CRS is found to be lower than the DEA-VRS and SFA.

Yet, the three approaches seem to show similar efficiency scores for the MFIs.

124

Figure 4.14: Efficiency estimates by different approaches

Source: Author’s computation

0.000

0.200

0.400

0.600

0.800

1.000

1.200

Average‐CRS

Avearage‐VRS

Average_SFA

125

4.17: Efficiency ranking of the MFIs under different approaches

Efficiency Rank

MFIs

CRS VRS SFA

Efficiency Rank Efficiency Rank Efficiency Rank

ACSI 0.896 2 1.000 1 0.766 6

ADCSI 0.805 5 0.814 8 0.808 3

Agar I 0.413 18 0.808 9 0.741 10

AVFS 0.461 17 0.657 16 0.704 14

BGMFISC 0.724 9 0.767 12 0.741 11

Bussa G. 0.600 13 0.640 17 0.523 19

DECSI 1.000 1 1.000 1 0.870 1

Eshet 0.705 10 0.820 7 0.797 4

Gasha 0.492 15 0.600 18 0.729 12

Meklit 0.549 14 0.733 15 0.765 7

Mettemenan 0.696 12 0.848 5 0.614 17

OCSSCO 0.740 7 0.758 13 0.630 16

OMO 0.781 6 0.790 11 0.679 15

PEACE 0.819 3 0.930 4 0.858 2

SFPI 0.704 11 0.753 14 0.790 5

Shashemene 0.386 19 1.000 3 0.748 9

sidama 0.810 4 0.846 6 0.707 13

Wasasa 0.737 8 0.805 10 0.758 8

Wisdom 0.464 16 0.476 19 0.523 18 Source: Author’s computation

The findings indicate that regardless of the approaches used, DECSI stands out as being

the most technically efficient microfinance in the sample. This is an important finding

given that DECSI has attained the dual objectives of reaching much larger scale than the

126

other institutions, is financially sustainable and viable, and may represent a best

practicing model of MFI in Ethiopia. Conversely, Wisdom seems to be the worst

practicing MFI in sample under all the approaches.

Table 4.18: Correlation coefficient DEA and SFA

TE-CRS TE-VRS TE-SFA

TE-CRS 1.000

TE-VRS 0.730 1.000

TE-SFA 0.579 0.614 1.000

Source: Author’s computation

Table 4.18 provides the correlation coefficients of efficiency estimates under different

approaches. As it can be seen the correlation of technical efficiency of the institutions in

the study years obtained from CRS versus VRS is high (0.73). Moreover, the correlation

coefficient of the SFA is found to be positive and moderate (0.57). In all cases the

coefficients are statistically significant at 1% level. This indicates that the three

approaches seem to have similar results.

127

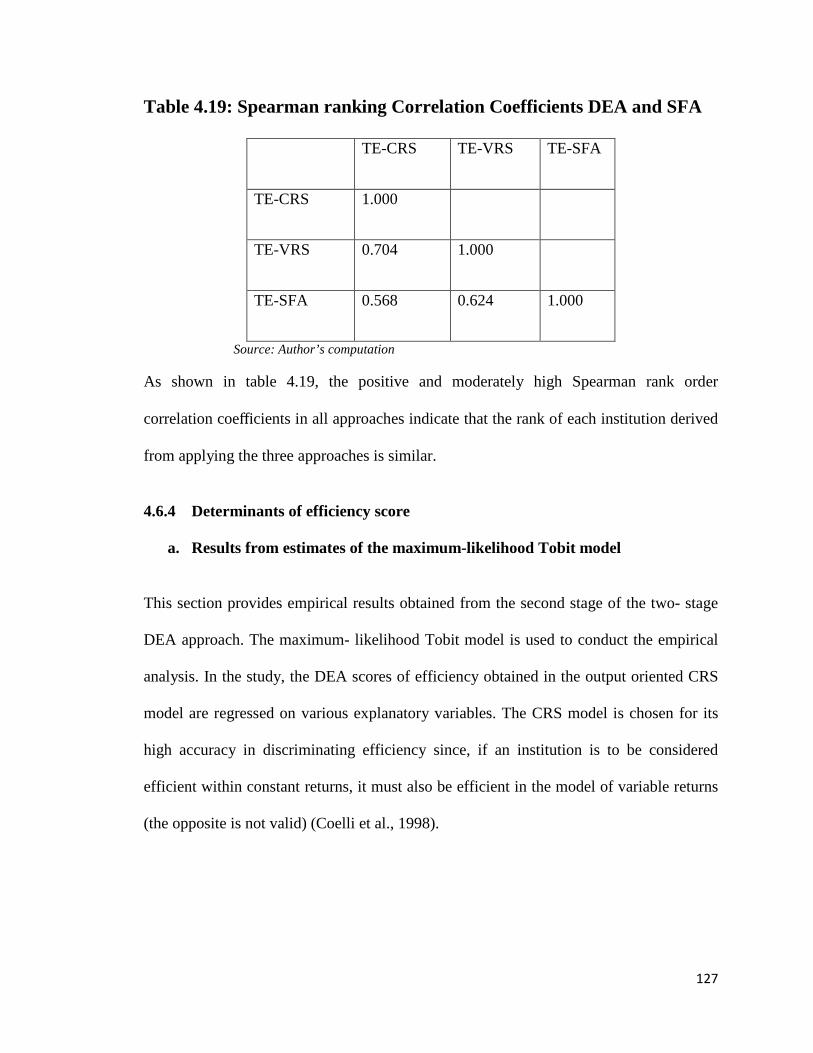

Table 4.19: Spearman ranking Correlation Coefficients DEA and SFA

TE-CRS TE-VRS TE-SFA

TE-CRS 1.000

TE-VRS 0.704 1.000

TE-SFA 0.568 0.624 1.000

Source: Author’s computation

As shown in table 4.19, the positive and moderately high Spearman rank order

correlation coefficients in all approaches indicate that the rank of each institution derived

from applying the three approaches is similar.

4.6.4 Determinants of efficiency score

a. Results from estimates of the maximum-likelihood Tobit model

This section provides empirical results obtained from the second stage of the two- stage

DEA approach. The maximum- likelihood Tobit model is used to conduct the empirical

analysis. In the study, the DEA scores of efficiency obtained in the output oriented CRS

model are regressed on various explanatory variables. The CRS model is chosen for its

high accuracy in discriminating efficiency since, if an institution is to be considered

efficient within constant returns, it must also be efficient in the model of variable returns

(the opposite is not valid) (Coelli et al., 1998).

128

The explanatory variables included in this study are: age (captures experience), size

(captures scale), and other indicators related to ownership, outreach, sustainability and

social performances (see Table 4.20). The institutions’ specific variables or factors

considered in the study are neither inputs nor outputs of the production process, but rather

circumstances faced by decision makers. Determining how these variables influence

efficiency is critical in designing appropriate performance improvement strategies.

Table 4.20: Description of variables along with expected sign

Variables Description Hypothesis

Age Age of MFIs is the number of years since

establishment +

Size Total of all net asset accounts +

Financial self sufficiency Adjusted revenue/Adjusted(Financial Expense

+Impairment Losses on Loans +Operating

Expense)

+

loan size Total value of loans/Number of credit clients -

Ownership 1 if a microfinance institution is government

affiliated4, 0 other wise +

Gender sensitive 1 if a microfinance with more than 50%

women borrowers, 0 other wise -

Debt equity ratio Ratio of total debt to total equity +/-

Capital Asset ratio Ratio of total equity to total assets +/-

4 A microfinance is considered as government affiliated institution if at least 25% its initial capital of ownership

129

The Tobit model used in this study may be specified as :

εα ββββββββ +++++++++=∗

DERCAROwnWomenALSFSSageAssetyi 87654321

(4.10)

Where Asset represents total of all net asset accounts of the i-th microfinance institutions

measured in dollar. In financial institutions asset is usually taken a proxy for size. Larger

size could result in scale efficiency and is expected to have positive effect on efficiency.

However, for institutions which are extremely large, the effect of size could be negative.

Age is age of the i-th microfinance institutions measured in number of years and shows

the experience of the MFI. Matured and experienced institutions are expected to be more

efficient than the young or new institutions. FSS measures microfinance sustainability is

achieved when the operating income of an MFI is sufficient enough to cover all

operational costs. The FSS is expected to have positive impact on efficiency as most

efficient MFIs generate higher returns and thereby are sustainable. Womenitisan

indicator of depth outreach and social orientation of MFIs. It is dummy variable 1 if

MFI has more than 50% women borrowers, 0 otherwise. Higher value for women

indicates more depth of outreach, since lending to women is associated with lending to

poor borrowers (Hermes et al., 2009). Ownership is a dummy variable reflecting 1 if MFI

is government affiliated,0 otherwise.

Table 4.21 provides the descriptive statistics of the explanatory variables included in the

analysis of technical efficiency including their mean, standard deviation, minimum and

maximum values for the sample of 19 MFIs during the period 2004-2009.

130

Table 4.21: Summary of Descriptive Statistics of Variables