Chapter 8 Accounting for Long-Term Assets

Chapter 8 Accounting for Long-Term Assets. Called Property, Plant, & Equipment Plant Assets Expected to Benefit Future Periods Actively Used in Operations.

Dec 31, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 8

Accounting for

Long-Term Assets

Called Property, Plant, & EquipmentCalled Property, Plant, & Equipment

Plant Assets

Expected to Benefit Future PeriodsExpected to Benefit Future Periods

Actively Used in OperationsActively Used in Operations

Tangible in NatureTangible in Nature

C 1

Plant Assets

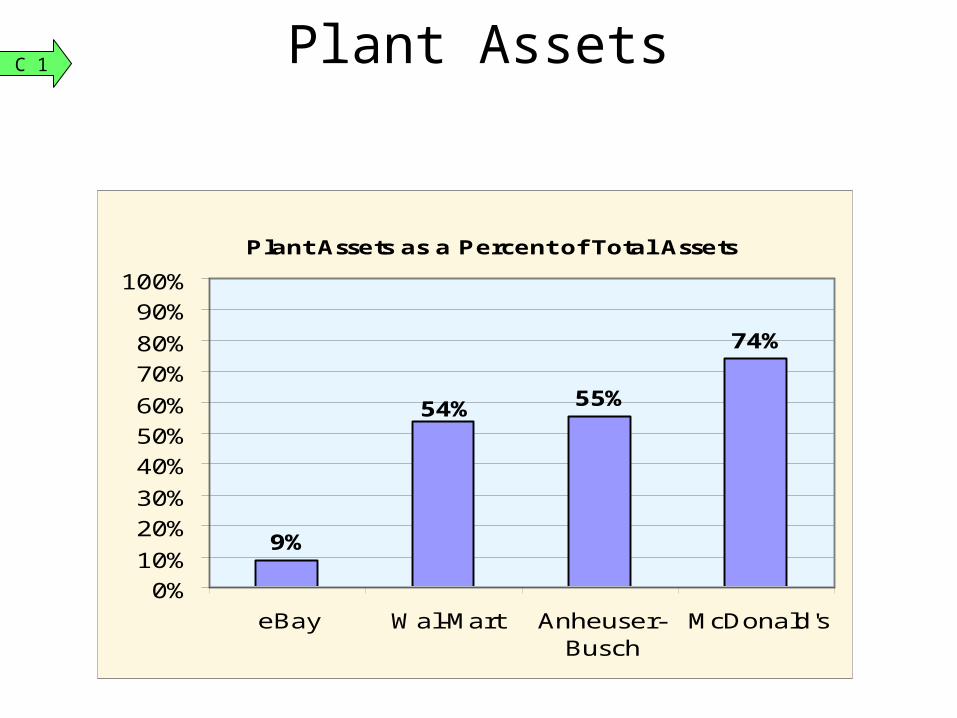

Plant Assets as a Percent of Total Assets

9%

54% 55%

74%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

eBay Wal-Mart Anheuser-Busch

McDonald's

C 1

Noncurrent assetswithout physicalsubstance.

Noncurrent assetswithout physicalsubstance.

Useful life isoften difficultto determine.

Useful life isoften difficultto determine.

Usually acquired for operational use.

Usually acquired for operational use.

IntangibleAssets

IntangibleAssets

Often provideexclusive rightsor privileges.

Often provideexclusive rightsor privileges.

Intangible AssetsP6

Decline in asset value over its useful life

Use2. Allocate cost to periods benefited.3. Account for subsequent expenditures.

Use2. Allocate cost to periods benefited.3. Account for subsequent expenditures.

Disposal 4. Record disposal. Disposal 4. Record disposal.

Plant Assets

Acquisition1. Compute cost. Acquisition1. Compute cost.

C 1

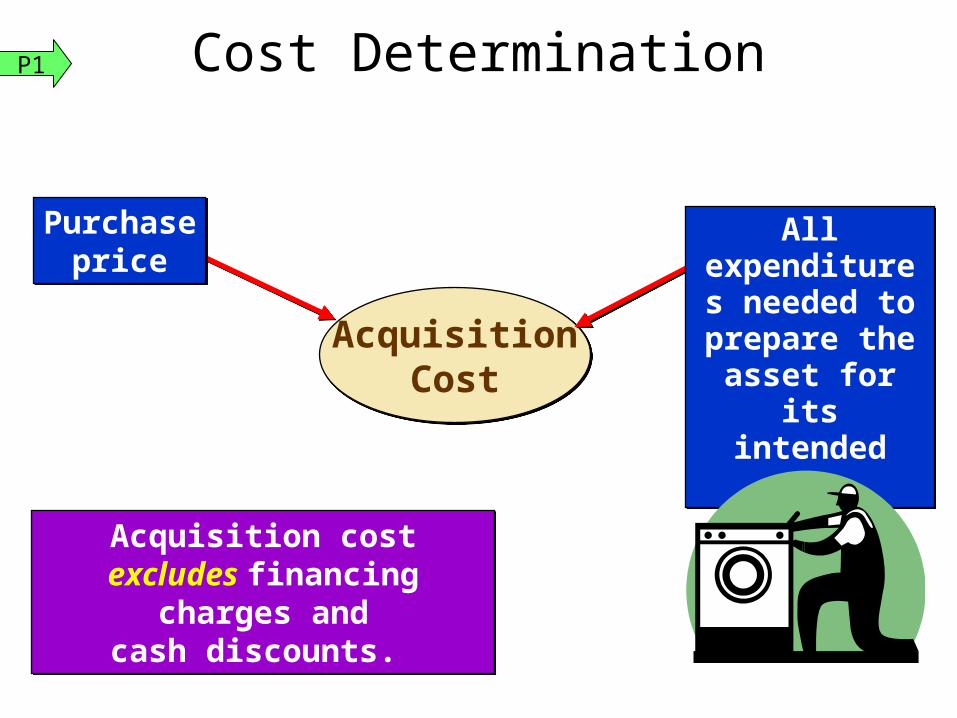

AcquisitionCost

AcquisitionCost

Acquisition cost excludes financing charges and

cash discounts.

Acquisition cost excludes financing charges and

cash discounts.

All expenditures

needed to prepare the asset for its intended use

All expenditures

needed to prepare the asset for its intended use

Purchaseprice

Purchaseprice

Cost DeterminationP1

Land is not depreciable.Land is not depreciable.

Purchaseprice

Purchaseprice

Real estatecommissionsReal estate

commissions

Title insurance premiumsTitle insurance premiums

Delinquenttaxes

Delinquenttaxes

Surveyingfees

Surveyingfees

Title search and transfer feesTitle search and transfer fees

LandP1

Land Improvements

Parking lots, driveways, fences, walks, shrubs, and lighting systems.

Parking lots, driveways, fences, walks, shrubs, and lighting systems.

Depreciate over useful life of

improvements.

P1

Cost of purchase or construction

Cost of purchase or construction

Brokeragefees

Brokeragefees

TaxesTaxes

Title feesTitle fees

Attorney feesAttorney fees

BuildingsP1

Purchaseprice

Purchaseprice

Installing,assembling, and

testing

Installing,assembling, and

testing

Insurance whilein transit

Insurance whilein transit

TaxesTaxes

Transportationcharges

Transportationcharges

Machinery and EquipmentP1

Depreciation is the process of allocating the cost of a plant asset to expense in the accounting periods benefiting from its use.

Depreciation is the process of allocating the cost of a plant asset to expense in the accounting periods benefiting from its use.

Cost

AllocationAcquisition

CostAcquisition

Cost

(Unused)

Balance Sheet

(Used)

Income Statement

ExpenseExpense

DepreciationC2

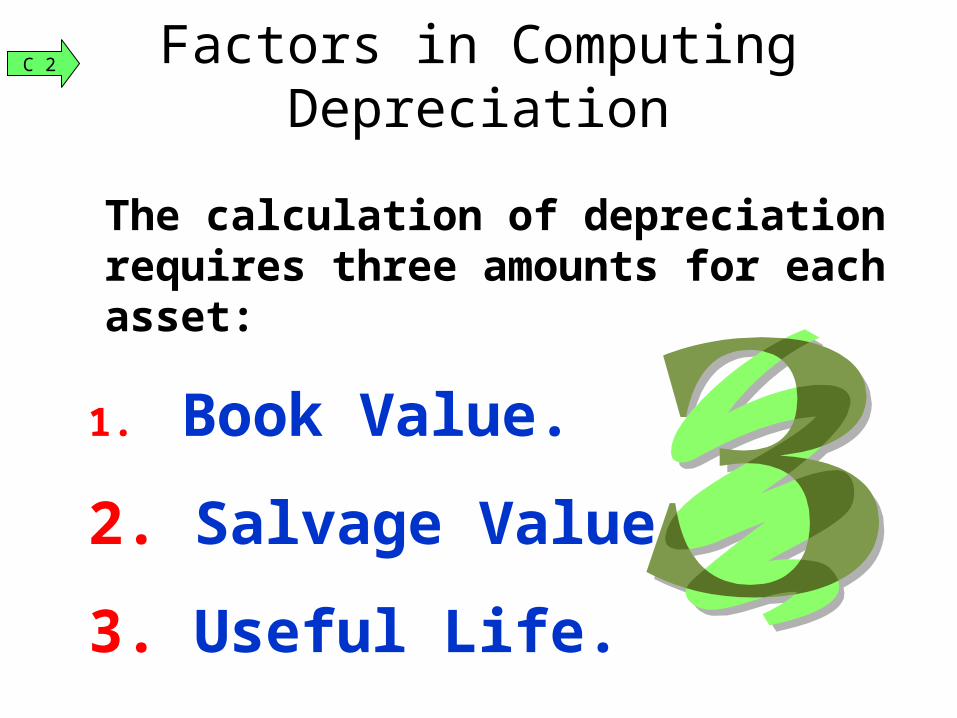

The calculation of depreciation requires three amounts for each asset:

1. Book Value.

2. Salvage Value.

3. Useful Life.

Factors in Computing Depreciation

C 2

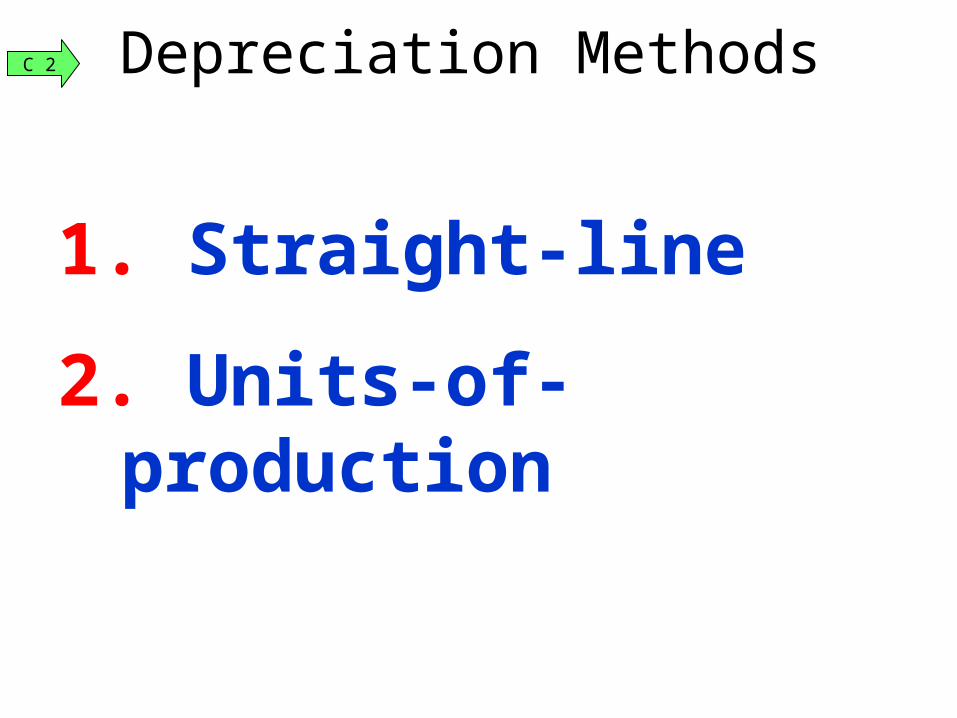

1. Straight-line

2. Units-of-production

Depreciation MethodsC 2

On January 1, 2007, equipment was purchased for $50,000 cash. The equipment has an estimated useful life of 5 years and an estimated residual value of $5,000.

Cost - Salvage Value

Useful life in periods

Depreciation

Expense for Period=

Straight-Line MethodP2

Straight-Line Method

Cost - Salvage Value

Useful life in periods

Depreciation

Expense for Period=

$9,000 Depreciation

Expense per Year=

$50,000 - $5,000

5 years=

Dr. Cr.Depreciation Expense 9,000

Accumulated Depreciation - Equipment 9,000 To record annual depreciation

P2

Depreciation AccumulatedExpense Depreciation Accumulated Book

Year (debit) (credit) Depreciation Value50,000$

2007 9,000$ 9,000$ 9,000$ 41,000 2008 9,000 9,000 18,000 32,000 2009 9,000 9,000 27,000 23,000 2010 9,000 9,000 36,000 14,000 2011 9,000 9,000 45,000 5,000

45,000$ 45,000$

Salvage ValueSalvage Value

Straight-Line Method

DepreciationRate

= (100% ÷ 5 years) = 20% per year

P2

Dep

reci

atio

n

Exp

ense Depreciation Expense

reported on theIncome Statement.

$0$1,000

$3,000

$5,000

$7,000

$9,000

2007 2008 2009 2010 2011

For the year ended December 31

Book Valuereported on theBalance Sheet.

$41,000

$32,000

$23,000

$14,000

$5,000

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

$45,000

2007 2008 2009 2010 2011

For the year ended December 31

Bo

ok

Val

ue

P2

Units-of-Production Method

Step 2:Depreciation Expense =

DepreciationPer Unit

×Number of

Units Producedin the Period

DepreciationPer Unit

= Cost - Salvage Value Total Units of Production

Step 1:

P2

On December 31, 2007, equipment was purchased for $50,000 cash. The equipment is expected to produce 100,000 units during its useful life and has an estimated salvage value of $5,000.

If 22,000 units were produced in 2008, whatis the amount of depreciation expense?

On December 31, 2007, equipment was purchased for $50,000 cash. The equipment is expected to produce 100,000 units during its useful life and has an estimated salvage value of $5,000.

If 22,000 units were produced in 2008, whatis the amount of depreciation expense?

Units-of-Production MethodP2

Step 2:Depreciation Expense = $.45 per unit × 22,000 units = $9,900

Step 1:Depreciation

Per Unit= $50,000 - $5,000

100,000 units = $.45 per unit

Units-of-Production MethodP2

Depreciation Accumulated BookYear Units Expense Depreciation Value

50,000$ 2008 22,000 9,900$ 9,900$ 40,100 2009 28,000 12,600 22,500 27,500 2010 - - 22,500 27,500 2011 32,000 14,400 36,900 13,100 2012 18,000 8,100 45,000 5,000

100,000 45,000$

No depreciation expense if the equipment is idle.

Units-of-Production MethodP2

Most corporations use the Modified Accelerated Cost Recovery System (MACRS) for tax purposes.

MACRS depreciation provides for rapid write-off of an asset’s cost in order to stimulate new investment.

Most corporations use the Modified Accelerated Cost Recovery System (MACRS) for tax purposes.

MACRS depreciation provides for rapid write-off of an asset’s cost in order to stimulate new investment.

Depreciation for Tax ReportingP2

Reporting Depreciation

Property, plant, and equipment: Land and buildings 150,000$ Machinery and equipment 200,000 Office furniture and equipment 175,000 Land improvements 50,000 Total 575,000$ Less Accumulated depreciation (122,000) Net property, plant, and equipment 453,000$

C 3

Additional Expenditures

If the amounts involved are not material, most companies expense the item.

If the amounts involved are not material, most companies expense the item.

Financial Statement EffectCurrent Current

Treatment Statement Expense Income Taxes

Capital Balance sheetExpenditure account debited Deferred Higher Higher

Revenue Income statement CurrentlyExpenditure account debited recognized Lower Lower

P3

Related Documents