Chapter 7 International Bond Markets Management 3460 Institutions and Practices in International Finance Fall 2003 Greg Flanagan

Chapter 7 International Bond Markets Management 3460 Institutions and Practices in International Finance Fall 2003 Greg Flanagan.

Dec 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 7 International Bond Markets

Management 3460 Institutions and Practices in

International Finance

Fall 2003Greg Flanagan

November 4, 2003 2

Chapter Objectives The student will be able to:

explain the difference between domestic, foreign, and Euro bonds.

use present value in determining a bond’s price.

describe the world’s bond markets and explain their relative importance in international finance.

be aware of the currency distribution, nationality, type of Issuer.

November 4, 2003 3

Chapter Objectives The student will be able to:

explain the factors that affect the price and sales of different bonds.

list and describe the different types of bond instruments.

be aware of International bond market credit ratings

explain the Eurobond market structure & practices.

describe the J.P Morgan Domestic and other International Bond Market Indices

November 4, 2003 4

BondsDomestic bond—issued in the country by a

domestic firm, government, or institution, in local currency.

Foreign bond—issued in a country in local currency by a foreign agent (borrower).

Eurobond—issued in a particular currency and sold in countries other than the denominated currency.

International bonds—foreign and Euro bonds.Consul—perpetual bond a P = A/r

November 4, 2003 5

Present Value (basic) PV is what one would be willing to pay today for

the right to receive a certain value in the future.

Example: T-bills auctions determine the bank rate.

with annual interest rate r (assumed constant); time period T in years; and future payout R (no inflation)

PV = R Note: r PV and T PV a

(1+r)T

November 4, 2003 6

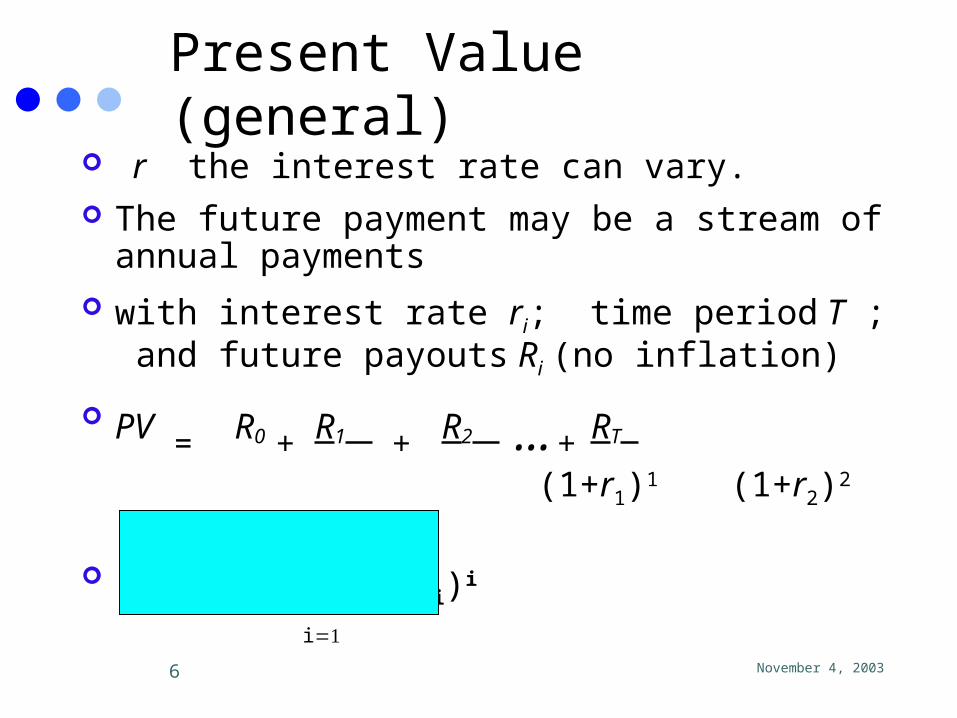

Present Value (general) r the interest rate can vary. The future payment may be a stream of

annual payments with interest rate ri; time period T ; and future

payouts Ri (no inflation)

PV = R0 + R1 + R2 … + RT a

(1+r1)1 (1+r2)2 (1+rT)T

PV = Ri / (1+ri)i

i

November 4, 2003 7

Present Value (inflation) The PV decreases because the interest rate r

includes inflation r + .

The PV increases with inflation in terms of future nominal payment

PV = R0 + (1+) R1 + (1+) R2 … + (1+) RT a

(1+)(1+r1)1 (1+) (1+r2)2 (1+) (1+rT)T

PV = R0 + (1+) R1 + (1+) R2 … + (1+) RT a

(1+)(1+r1)1 (1+) (1+r2)2 (1+) (1+rT)T

November 4, 2003 8

Present Value (inflation)

The PV is the same in nominal and real if calculated consistently.

PV = R0 + R1 + R2 … + RT a

(1+r1)1 (1+r2)2 (1+r)T

Use either Real or Nominal for both

but do not mix.

November 4, 2003 9

The World’s Bond Market The total market value of the world’s bond

markets are about 50% larger than the world’s equity markets.

Most issues are denominated in U.S. dollars (50%), Japanese Yen are second, followed by the Euro, and British pound sterling.

~82 percent of outstanding bonds are domestic.

November 4, 2003 10

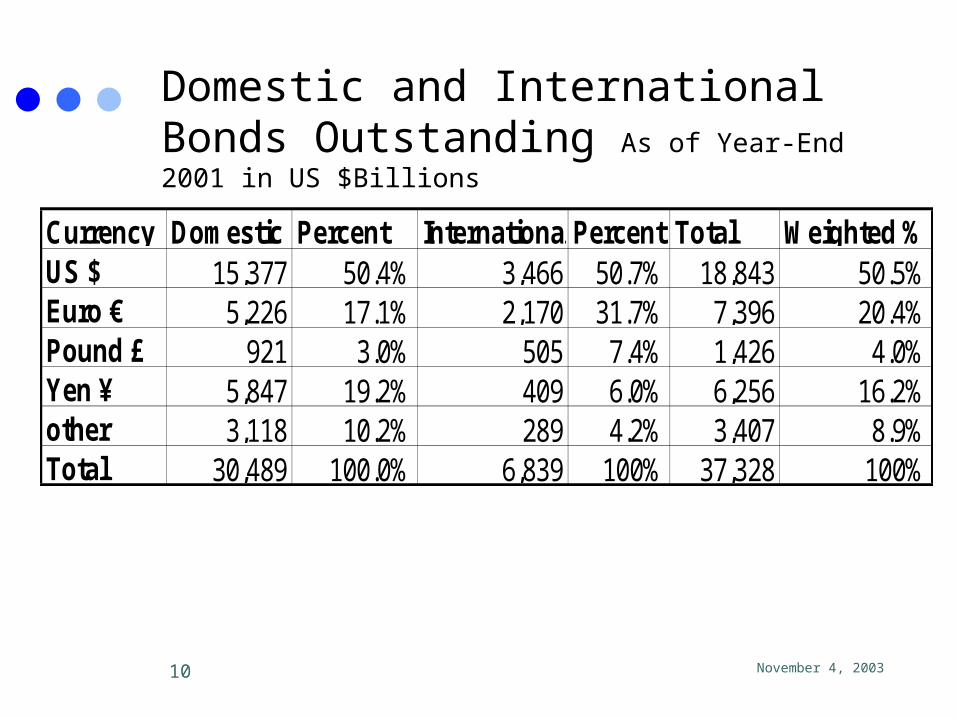

Currency Domestic Percent InternationalPercent Total Weighted %US $ 15,377 50.4% 3,466 50.7% 18,843 50.5%Euro € 5,226 17.1% 2,170 31.7% 7,396 20.4%Pound £ 921 3.0% 505 7.4% 1,426 4.0%Yen ¥ 5,847 19.2% 409 6.0% 6,256 16.2%other 3,118 10.2% 289 4.2% 3,407 8.9%Total 30,489 100.0% 6,839 100% 37,328 100%

Domestic and International Bonds Outstanding As of Year-End 2001 in US $Billions

November 4, 2003 11

Domestic and International Bonds Outstanding As of Year-End 2001 in U.S. $Billions

$-

$5,000.0

$10,000.0

$15,000.0

$20,000.0

$25,000.0

$30,000.0

$35,000.0

$40,000.0

Domestic

International

Total

November 4, 2003 12

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

U.S.dollar

Euro Pound Yen Other

Domestic

International

Total

Domestic and International Bonds Outstanding As of Year-End 2001 in U.S. $Billions

November 4, 2003 13

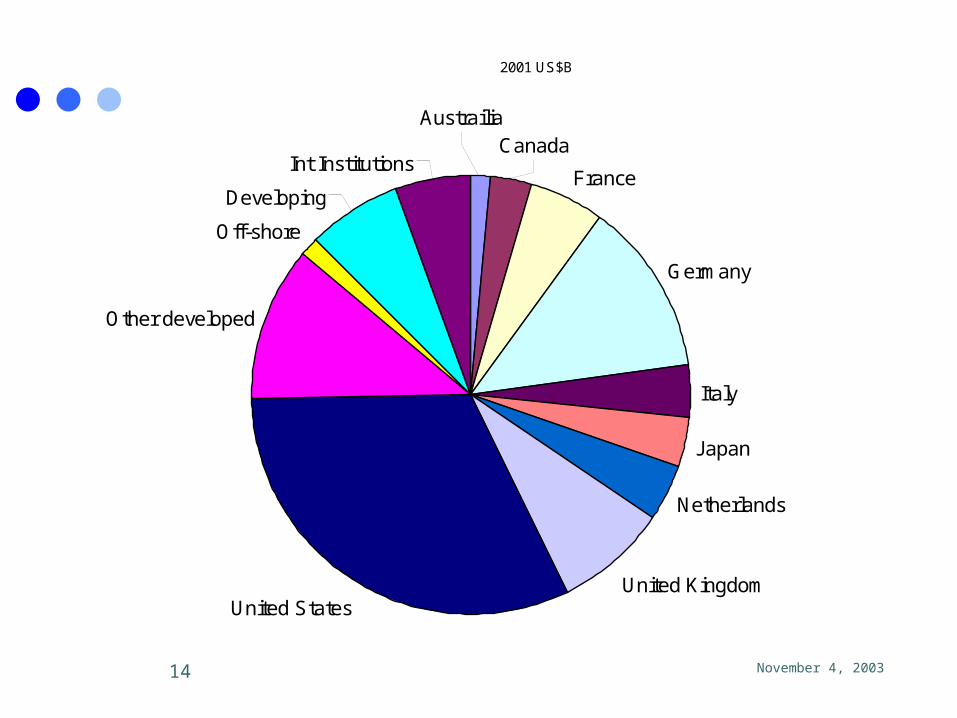

International BondsNationality 2001 US$B PercentAustrailia 99.8 1.5%Canada 208.3 3.0%France 366.7 5.4%Germany 889.4 13.0%Italy 259.3 3.8%Japan 245.6 3.6%Netherlands 293.9 4.3%United Kingdom 571.5 8.4%United States 2,170.3 31.7%Other developed 788.2 11.5%Off-shore 87.0 1.3%Developing 481.3 7.0%Int Institutions 377.1 5.5%Total 6,838.4 100.0%

Distribution of International Bond Offerings by Nationality

November 4, 2003 14

2001 US$B

France

Germany

Italy

Japan

Netherlands

United KingdomUnited States

Other developed

Off-shore

Developing

Int Institutions

AustrailiaCanada

November 4, 2003 15

Type 1997 1998 1999 2000 2001 2001%Financial Institutions 1,475.1 1,885.8 2,397.2 3,470.1 4,030.3 58.9%Governments 710.3 863.4 1,032.1 1,173.3 1,416.5 20.7%International Institutions 299.5 370.8 375.2 374.1 377.7 5.5%Corporations 837.9 983.4 1,301.0 861.8 1,014.6 14.8%Total 3,322.8 4,103.4 5,105.5 5,879.3 6,839.1 100.0%

International Bonds by Type of Issuer

November 4, 2003 16

International Bonds by Type of Issuer

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1997 1998 1999 2000 2001

Year

US

$ (B

illl

ion

s)

Financial InstitutionsGovernmentsInternational InstitutionsCorporationsTotal

November 4, 2003 17

International Bonds by Type of Issuer 2001 US$ (Billions)

Financial Institutions

International Institutions

Corporations

Governments

November 4, 2003 18

Bearer Bonds and Registered Bonds

Bearer Bonds are bonds with no registered owner. As such they offer anonymity but they also offer the same risk of loss as currency.

Registered Bonds: the owners name is registered with the issuer.

U.S. security laws require Yankee bonds sold to U.S. citizens to be registered.

November 4, 2003 19

National Security Registrations

Yankee bonds must meet the requirements of the SEC, just like U.S. domestic bonds.

Many borrowers find this level of regulation burdensome and prefer to raise U.S. dollars in the Euro bond market.

Eurobonds sold in the primary market in the United States may not be sold to U.S. citizens.

U.S. citizen can buy Euro bonds on the secondary market.

November 4, 2003 20

U.S. Withholding Taxes Prior to 1984, the United States required a 30

percent withholding tax on interest paid to nonresidents who held U.S. government or U.S. corporate bonds.

The repeal of this tax led to a substantial shift in the relative yields on U.S. government and Eurodollar bonds.

market participants react to tax code changes.

November 4, 2003 21

Recent US Regulatory Changes Shelf Registration (SEC Rule 415)

Allows the issuer to preregister a securities issue, and then offer the securities when the financing is actually needed.

SEC Rule 144A Allows qualified institutional investors to

trade private placements.These issues do not have to meet the strict

information disclosure requirements of publicly traded issues.

November 4, 2003 22

Global BondsA global bond is a very large international

bond offering by a single borrower that is simultaneously sold in North America, Europe and Asia.

Mostly institutional investors are the purchasers so far.

United States SEC Rule 415 and 144A have likely facilitated global bond offerings, and more can be expected in the future.

November 4, 2003 23

Types of InstrumentsStraight Fixed Rate Debt

Floating-Rate Notes

Equity-Related Bonds

Zero Coupon Bonds

Dual-Currency Bonds

Composite Currency Bonds

November 4, 2003 24

Straight Fixed Rate DebtThese are “plain vanilla” bonds with a

specified coupon rate and maturity and no options attached.

Since most Eurobonds are bearer bonds, coupon dates tend to be annual rather than semi-annual.

The vast majority of new international bond offerings are straight fixed-rate issues.

November 4, 2003 25

Floating-Rate NotesJust like an adjustable rate mortgage.Common reference rates are 3-month

and 6-month U.S. $ LIBORSince FRN reset every 6 or 12

months, the premium or discount is usually quite small…as long as there is no change in the default risk.

November 4, 2003 26

Equity-Related BondsConvertibles

Convertible bonds allow the holder to surrender his bond in exchange for a specified number of shares in the firm of the issuer.

Bonds with equity warrantsThese bonds allow the holder to keep his

bond but still buy a specified number of shares in the firm of the issuer at a specified price.

November 4, 2003 27

Zero Coupon BondsZeros are sold at a large discount from face

value because there is no cash flow until maturity.

In the U.S., investors in zeros owe taxes on the “imputed income” represented by the increase in present value each year, while in Japan, the gain is a tax-free capital gain.

Pricing is very straightforward:Tr

parvaluePV

)1(

November 4, 2003 28

Dual-Currency BondsA straight fixed-rate bond, with

interest paid in one currency, and

principal in another currency.Japanese firms have been big issuers

with coupons in yen and principal in dollars.

Good option for a MNC financing a foreign subsidiary.

November 4, 2003 29

Composite Currency BondsDenominated in a currency basket,

like the SDRs or ECUs instead of a single currency.

Often called currency cocktail bonds.

Typically straight fixed rate debt.

November 4, 2003 30

Instrument

Straight Fixed-Rate

Floating Rate Note

Convertible Bond Annual Fixed Currency of issue or conversion to equity shares.

Straight fixed rate with equity warrants

Annual Fixed Currency of issue plus conversion to equity shares.

Zero none zero Currency of issue

Dual Currency Bond

Annual Fixed Dual currency

Frequency of Payment

Annual

Size of Coupon

Payoff at Maturity

Characteristics of International Bond Market Instruments

Currency of issueFixed

Every 3 or 6 months Variable Currency of issue

November 4, 2003 31

Brady Bonds Convert ‘bad’ loans to marketable bonds

at 65% of face value with reduced interest rate

Extend maturities to 25-30 years Buy collateral zero coupon US treasury

bonds with $100 million converted covering 92% of

private

November 4, 2003 32

International Bond Market Credit Ratings

Fitch IBCA, Moody’s and Standard & Poor’s sell credit rating analysis.

Focus on default risk, not exchange rate risk.

Assessing sovereign debt focuses on political risk and economic risk.

See: Exhibit 7.7

November 4, 2003 33

Eurobond Market Structure Primary Market

Very similar to U.S. underwriting. Secondary Market

OTC market centered in London.• Comprised of market makers as well as brokers.• Market makers and brokers are members of the

International Securities Market Association (ISMA).

Clearing ProceduresEuroclear and Cedel handle most Eurobond

trades.

November 4, 2003 34

International Bond Market Indices

J.P. Morgan and CompanyDomestic Bond Indices International Government bond index

for 18 countries.Widely referenced and often used as

a benchmark.Appears daily in The Wall Street

Journal

November 4, 2003 35

International Bond Market Indices

Wall Street Journal publishes daily values of yields Government bonds.Compares interest rat s and term

structuresFinancial Times publishes

“Benchmark Government Bonds” table comparing coupon rates, prices, yields etc.

Related Documents