3CADB61E-3CA8-CD64.doc Michel Gutsatz 1 Chapter 7: Five key success factors The consumers desire luxury brands and luxury goods. Luxury brands develop business strategies to satisfy these desires. But as Domenico De Sole himself said: “You can have the best strategy in the world, but the difference between the excellent and the incompetent is: execution, execution, execution”. Luxury brands’ history is filled of magnificent strategies, of hailed CEOs, of awesome transactions that now fill the graveyards of the industry and the casebooks of business schools. There are at least five key success factors that all relate to the implementation of the strategy, most of which are quite specific to luxury brands: 1. Being consistent in the brand image and strategy 2. Investing in retail and balancing distribution channels 3. Being innovative and developing new products 4. Managing the gross margin 5. Investing in communication and medias to develop brand awareness Each is critical. Each can be a stumbling stone. Managing all effectively can lead to a huge success. We will review them, highlighting the difficulties in their implementation.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

1

Chapter 7: Five key success factors

The consumers desire luxury brands and luxury goods. Luxury brands develop business strategies to

satisfy these desires. But as Domenico De Sole himself said: “You can have the best strategy in the world,

but the difference between the excellent and the incompetent is: execution, execution, execution”. Luxury

brands’ history is filled of magnificent strategies, of hailed CEOs, of awesome transactions that now

fill the graveyards of the industry and the casebooks of business schools.

There are at least five key success factors that all relate to the implementation of the strategy, most of

which are quite specific to luxury brands:

1. Being consistent in the brand image and strategy

2. Investing in retail and balancing distribution channels

3. Being innovative and developing new products

4. Managing the gross margin

5. Investing in communication and medias to develop brand awareness

Each is critical. Each can be a stumbling stone. Managing all effectively can lead to a huge success. We

will review them, highlighting the difficulties in their implementation.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

2

A. Consistency, consistency, consistency…

There are currently three basic situations in luxury brands –but history shows that all mixes of these

are possible:

1. The Creator –or a substitution creator- is present: that is the case in most apparel brands. Dior

with John Galliano, Thierry Mugler, Jean Paul Gaultier, Miuccia Prada are such cases.

2. The brand has a Creative Director, who may or may not be a designer himself, who overlooks

all the creative aspects of the brand presence: the template here is Tom Ford at Gucci.

3. The brand has designers that are not in the spotlights and who work under the supervision of

the brand’s CEO: this generally is the case in non-apparel brands like Bulgari or was the case

at Louis Vuitton before Marc Jacobs was hired.

In all three instances a CEO manages the brand and is in charge of the business per se. Amongst the

possible mixes you will have Hermès where Jean Louis Dumas is both CEO and de facto Creative

Director but has Martin Margiela to help him with RTW; Burberry with Rose Marie Bravo as CEO and

different designers for its different lines1 –although Roberto Manichetti who left in March 2001 was

officially Creative Director but in fact only oversaw the top-end Prorsum line. As Rose Marie Bravo

says: “Burberry has never been about a celebrity designer”2.

In reality cases 1 (the creator-designer) and cases 2 (the creative director) are quite close. The major

differences lie in the breadth of that person’s responsibilities: they are maximal in Tom Ford’s case and

can be minimal in Roberto Manichetti or John Galliano’s cases (see: The Dior case lower). In the

following sections creator and creative director can be used symmetrically.

A formula for success: a creator + a businessman

The paradox of a Luxury brand is that there should be both a strong emotional link between a brand

and its customers AND that it should be managed as a very complex business: the gross margins

should be right, the raw materials should be purchased at the right prices, the distribution channels

must be chosen carefully, the stores that must be opened in the major cities of the world will require

huge investments in top locations, outstanding designs and fixtures and heavy inventories. Not unlike

music where a Performer must give to his audience the feeling that he plays a Sonata without any

effort, the designer must give the feeling that he only worries about product design and quality…

Business must of course follow, but it is not so easy to have it run it smoothly…

1 For the “London line” –the one based on the Burberry check: Deborah Lloyd on momen’s wear; Michael McGrath on

men’s wear; Giovanni Morelli on women’s accessories – and now –replacing Manichetti- Christopher Baily.

2 WWD, May 4, 2001

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

3

For a business to be successful, one therefore needs a creator who is in the limelight AND a manager

who works at making it a business success. Who is the most important? This is where the issue is a

difficult one. The manager must run the show, but he must remain behind the scene… So between

creator and manager, there is a need for a very strong relationship based on mutual trust and the

understanding that the two parts must be played together.

The creators create the products, develop their vision of the world (or of what a woman is… of what

beauty is about…), but are creators business-wise? Can a creator develop a business by him/herself?

That was clearly the case up to the 60’s: Christian Dior, Coco Chanel, Charles Christofle, Charles

Lewis Tiffany, Louis Vuitton at different periods in time, managed their company directly. But going

global and developing a brand necessitates different competencies, different skills. The successful

brands have seen a new leadership model, that of the couple creator + businessman. This model is

transnational: you have it in the USA with Calvin Klein & Barry Schwartz, in France with Yves Saint

Laurent & Pierre Bergé, in Italy with Miuccia Prada & Patrizio Bertelli or Tom Ford & Domenico De

Sole. Clearly trust is critical between the two. As Michael Newman, former Vice Chairman of Polo

Ralph Lauren said: «My working relationship with Ralph Lauren is entirely based on trust”3. This is the sort

of trust that close personal links can favor: Miuccia Prada & Patrizio Bertelli are married, Yves Saint

Laurent & Pierre Bergé were lovers.

The Miuccia Prada- Patrizio Bertelli Case

“Designers who have worked at Prada like to describe the experience as «school.» The focus of their

studies is a double major in creativity and commerce, taught with authority and passion by professors

Miuccia Prada and Patrizio Bertelli, respectively.”4

Designers with a marketing edge, they have recently moved on to head Lanvin couture or Feraud

design, be women's design director for Yves Saint Laurent ready-to-wear, become women's ready-to-

wear designer at Ferragamo or Neil Barrett , designer of Samsonite's new and popular Travelwear

collection…. Yvan Mispelaere, the new head of design at Feraud, says he had «the great opportunity to

work in a very merchandising, marketing way, to think about the product and how the clothes will be received by

the customer and displayed in the store. The most important thing about Prada is thinking through at the

beginning what will happen at the end, controlling the whole process.»

Neil Barrett adds: «everything was thought out in depth because, down to the width of the stitches, Bertelli was

very keyed in with the technical aspects. What he didn't understand, he wanted to understand.»

P Personal communication.

4 “There’s something about Miuccia”, WWD, 10 July 2000

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

4

Lawrence Steele, who left Prada to launch his own collection in 1995 after working on the women's

collection for five years, agrees «it was great to work in the middle of two brilliant people. Miuccia is very

passionate about design. She is an expressive and poetic person. Bertelli, on the other hand, is always so excited

and driven. They have a great method of working, because even though they have different roles, there is a great,

common harmony. Bertelli has a particular way of structuring because he's involved with the color choices, the

clothes and the accessories. The greatest experience was seeking the big picture with the eyes of two different

people who are so in sync.»

To his wife’s designing skills Patrizio Bertelli adds the profile of the autocratic entrepreneur: “I trust no

one”, he says. One of his critical characteristics is that he is a control-freak. Tightly controlled image,

obsessive quality control, strict control of suppliers & sub-contractors, development of a network of

directly owned stores.. all contrive to this obsession with control. It goes a long way: if you walk into

the New York headquarters of I.P.I. USA (the Prada company), you will discover a uniform

environment of white offices, black ledgers, all the way from the CEO to the clerk. “Patrizio Bertelli

even oversaw the installation of the microwave oven in the kitchen, so as to have it where it is in the Milan

headquarters kitchen” says a Prada employee.

The Creative Director: a critical role

Consistency is also about building a brand around a Vision.

We have a creator, we have his/her vision, we have a brand, we have luxury products sold under the

name of the brand which is also the name of the creator, we have multiple channels of

communications between the brand and its customers, we have the employees working for the

brand…. All these must converge around the Vision, which is the essence of the brand. This is what

consistency is about.

When L’Oréal bought Lanvin, they found that that “Arpège”, its n°1 best selling perfume, had a

different formula in each country: each licensee had found it financially rewarding to replace certain

expensive components by cheaper scents. This is pure inconsistency. This is what customers, that are

now well traveled, will punish by discarding the brand.

When Gucci bought Yves Saint Laurent, the brand had 167 product licenses. Traveling from country

to country, the luxury brand customer found as many YSL images as countries (s)he was visiting.

Making the brand consistent is the primary role of the Creative Director.

“Christine Laroche is the guardian of dogma,» says Philippe de Beauvoir, the Le Bon Marché CEO of his

Creative Director.

“I am the keeper of the brand”, says Silvio Ursini, the Marketing Director of Bulgari.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

5

Nothing escapes the Creative Directors. They must apply their vision to all the components of the

aesthetics of the brand:

• The product presence (materials used, design of new products…)

• The spatial & retail environment (the store design, the shopping bags, the packaging, the

office design and furnishings, the music in the stores, the windows)

• The services (the sales method, the after sales service)

• The visual image (stationary and all the graphic identity of the brand –including internal

templates such as faxes, presentations, letters, memos, emails-, the logo, the shopping bags

and the packaging)

• The communication5 (the fashion shows, advertising, special events, annual reports,

website…)

• The people working for the brand (the uniforms, the attitudes, the grooming of salespersons,

the training of the employees)

What do all these have in common? They are “key experiential providers”6. They are what makes the

customer experience the brand, relate to the brand, feel the brand: when a customer enters the brand’s

store, the ambience, the layout, the quality of the salesperson’s approach, the service provided, the

products are unique opportunities for the brand and the customer to experience an emotional

relationship, for the brand to build a unique experience the customer will remember. When the

customer opens a magazine that depicts one of the brand’s ads, when (s)he reads about the designer in

some other magazine, when (s)he is invited by the brand to a special event or sees his-her favorite

music star sporting one of the brand’s products, this will enhance the emotion.

Now the CEO and the Creative Director have both their areas of expertise and their responsibilities

(listed in the next exhibit). All lie within the Brand Vision and should be consistent with it. Many of

these topics need concerted decisions: for instance the new products must be in line with market

needs and therefore closely integrate markets (which will give input on sizes, colors and other market

specificities), merchandisers (which will build the collection structure) and the Creative Director.

5 In 1997, Gucci had to fight a battle with their perfume licensee (Wella, now known as Cosmopolitan Cosmetics):

the Wella marketers had devised an ad campaign for Gucci Envy that Tom Ford rejected, thinking it was not

consistent with Gucci’s image. Gucci finally came up with their own campaign and had the final word: “The key issue

for us was creative control” said Domenico De Sole.

6 Bernd H.Schmitt: Experiential Marketing, The Free Press, 1999

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

6

Nevertheless if trust is not there boundary problems will arise soon: the Creative Director will want to

manage store locations and store refurbishments, while the CEO will consider that cost of store

concept is way too expensive! If a license is managed by a License Manager, (s)he may have a

tendency to work directly with the licensee and not include the Creative Director in the loop: as a

result time is lost in the choice of new products or in the organization of events for the launch.

• Distribution channels• Store locations• Choice of suppliers• Quality control• Hire of Store managers

and salespersons• Training of salespersons• Delivery on time of goods• Gross margin management• Pricing strategy• General collection structure

• Product presence (product lines, materials, design)• Spatial and retail environment (store design, windows, visual merchandising, store music, packaging, shopping bags)• Communication (advertising, events, fashion shows, annual reports, website)• Visual image of brand(logo, graphic image)• Services (after sales, selling attitude)• People (grooming, uniforms)

CEO Creative Director

The Vision

Figure 1: The respective roles of CEO and Creative Director

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

7

Exhibit: The Bally aesthetics

The logo

The mark

The packaging

The Berlin Store

A product:

An ad

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

8

The Tom Ford Case

Tom Ford, the Gucci Creative Director and since 2001 the Yves Saint Laurent Creative Director, and

the template for all Creative Directors, himself says:

“ I’m one of those people who has a vision. I always know instantly: yes, no, I like it, I hate it. My job is just that

all day long., expressing my vision in some way or another. … Gucci IS Tom Ford. Of course, Gucci is not all

me. It’s a part of me. But I have expressed myself…. The New York Studio 54 side of me is more Gucci… (For

YSL) it was hard at first. I had to tap into a different side of my personality, a different side of my taste level.

Growing up in New Mexico, a lot of what I was exposed to was Hispanic culture, which was lace and ruffles,

pattern, color. And that’s very much about what Yves Saint Laurent does, to a certain extent”7.

“I saw that Tom, like me, was a maniac”8, says Domenico DeSole, the Gucci Group CEO. Creative

Directors are maniacs, they are detail focused: Tom Ford is obsessive about details. “He moved a

white stool, he worried that the handrail would give shoppers splinters and he set little marks on the

stereo volume so the music would provide the proper ambience” before the opening of the new YSL

store in New York last December. Tom Ford knew the New York store would set the tone for all YSL

stores worldwide.

Tom Ford has also an acute sense of the business: “ I intellectualize to a point, but in a fitting or when I am

working on anything, I say okay, but does she look skinny in it? Is she going to feel good? If the answer is no

then who cares that’s it’s about the Russian revolution blah blah blah and the theme is blah blah blah.. who

CARES9? When the customer puts on those pants she doesn’t care what the original inspiration was. She cares

about whether her butt looks good… I worry too much about whether it would sell or if people would like it.”

Tom Ford adds “I have to give a huge amount of credit to Domenico; he has made it possible for me to work.

We are a great team. I completely trust Domenico with my life. Not everybody has that. And the fact of the

matter is that I am a business-minded designer. I cannot divorce the commercial from the creative., because my

goal is to create something beautiful that people will want more than anything in the world. When they find

something they want, they buy it, and if they buy it, it makes sales, and if it makes sales… It’s a tangible side of

a creative idea that works – money”10

7 Interview, I-D, July 2001

8 Lynn Hirschberg: “Tom Ford, Ensuring a Place for Gucci in Hard Times”, The New York Times, December 2, 2001

9 “Yves Saint Laurent doesn’t work like that. And he never will. The idea of him doing something just because he

thinks he’d be able to sell it is crazy” recalls Clara Saint. Quoted in Alice Rawsthorne (1996).

10 “Tom Pumps Up”, W, July 2000

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

9

As Carine Roitfeld, the editor of French Vogue and a stylist for Gucci from 1995 to 2000 says, “Tom is

artistic, but he has such a strong business side, and that is very rare. For most designers, it's the cut of

a jacket. With Tom, it's the cut of the jacket and all the accouterments. He thinks about the car the

woman drives, the kind of place she likes to live, how she likes to have sex. Tom considers all these

things when he thinks about Gucci or YSL”.

The Creative Director is the one person that personifies the vocabulary of the brand AND who knows

what will sell. This mix of a vision, creative instinct and business instinct is rare. Most designers lack

the business instinct and will favor a much more top down approach: this is good for the brand

because I have designed it. This is how it should be, irrelevant of business constraints: who cares if the

market wants men’s rubber-soled shoes, if I consider that this brand will only have leather soled

shoes? Why bother with functionalities if the design is great? Why bother with fit if the clothes are

made only for anorexics? This is the aristocratic attitude – the “Moi le Roi Soleil” syndrome - that most

French couturiers and some British designers exemplify. But ultimately in the 21st century luxury

brands are about creation AND business, and business always tells. Customers are the ultimate

deciders on what brand meets their desires, their needs, their expectations.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

10

The Yves Saint Laurent case: from consistency to inconsistency… and back

January 30, 1958: the Press and attendants of Yves Saint Laurent first show for Dior –where he

displayed the now famous “Trapeze line”- give him a standing ovation and find no words to say their

emotion11. He is shown to a small balcony overlooking the Avenue Montaigne (Exhibit 1) and

applauded by all that had not been able to enter.

January 11, 2002: three days after announcing his retirement, Yves Saint Laurent, in an interview given

to Paris Match admits his disdain for contemporary fashion: “I have nothing in common with this new

world of fashion, which has been reduced to mere window dressing. Elegance and beauty have been

banished. I utterly reject the fantasies of those who seek to satisfy their egos through fashion. I feel like

a dove that has been stabbed.”

What had happened over those 44 years that led to this bitterness? The rise and fall of a great brand,

which we shall now relate12 from a strict business perspective.

November 14, 1961: Yves Saint Laurent and his partner Pierre Bergé set up the Yves Saint Laurent

Company, funded by Jesse Mack Robinson, an American self-made businessman from Georgia, who

had made a fortune from second-hand car dealerships and motor-loan companies. He invests $700,000

in the company over three years, in return for 80% of the equity “and the firm promise that his

identity would be kept secret”. Cassandre, one of the major French graphic artists of the time designs

the now world-famous logo, entwining Yves’ three initials.

11 “My dear, France is saved. It’s Joan of Arc” said an attendant, as reported by Alice Rawsthorn: Yves Saint Laurent,

A Biography, Doubleday, 1996

12 Our major source here is Alice Rawthorn’s book. All quotes, unless otherwise specified, come from it.

Exhibit 1: The 1958 triumph

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

11

In 1962, Pierre Bergé, knowing that the Company’s success laid not in the fashionable celebrities that

bought the couture dresses but in the buyers from the Department Stores and the licenses Dior had so

successfully developed, hired a Sales Director and started signing contracts: in 1963 with Seibu for

Japan13; with Charles of the Ritz –and its president Richard Salomon, a future investor in YSL- for

perfumes in return for a royalty of 5% of its ales; for women’s stockings and men’s ties. All this led to

an annual turnover of around $1 million. The Seibu move was really innovative: it made YSL one of

the first luxury brands to develop its sales in Japan, seeing a huge potential market in it.

July 13, 1965: Lanvin-Charles of the Ritz buy back JM Robinson’s shares for a little less than $1 million.

1965 also sees the decision by Pierre Bergé to diversify into ready-to-wear. This was a revolutionary

step, as most couturiers were opposed to selling inexpensive “copies” of their couture dresses. But

Bergé had understood that this was where the future of the business laid. The radical innovation of

Yves Saint Laurent was that of designing a specific RTW collection and not a cheaper version of his

couture collection.

September 22, 1966: Opening of the first Rive Gauche boutique in Paris at 21, rue de Tournon a small

street on the Paris Left Bank. Manufacturing of this RTW line was contracted with C.Mendès, an

important French textile and clothing manufacturer. This family business14 was managed by Didier

Grumbach since 1964 – Didier Grumbach who now is (in 2002) President of the Chambre Syndicale de

la Couture, that is the French Association in charge of all the couture events in France, after having

been CEO of Thierry Mugler. The contract itself was in fact a joint venture (and not strictly a license): a

new company –Saint Laurent Rive Gauche- was set up, 25% of which were owned by Mendès, 25% by

Didier Grumbach and the remaining 50% by Pierre Bergé and Yves Saint Laurent. “A 12% royalty

would be payable on sales of Rive Gauche products, 5% of which would go to the Yves Saint Laurent

13 The licensing business was in its infancy as the following quote shows: “Each season they chose a selection of

outfits from the YSL collection and ordered two samples of each to be flown to Tokyo. Once the clients had placed

their orders, the Seibu team made up the garments, sending them back to rue Spontini to be checked at least three

times before being handed to the customers.”

14 The family included the former French Prime Minister Pierre Mendès France.

Exhibit 2: The Cassandre Logo

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

12

couture house” and the rest reinvested in Saint Laurent Rive Gauche. The store and the line were an

immediate huge success: “Everyone went to Rive Gauche, absolutely everyone... It was so exciting.

You could buy an entire wardrobe there: everything you needed… The clothes just walked out of the

shop”.

September 1968 saw the opening of the second Rive Gauche boutique in New York, on Madison

Avenue, between 70th and 71st Street. The success was as big as in Paris, selling $25,000 on the first

day. A boutique in London and one in Milan followed it in 1969. Urged by Richard Salomon, there

were 20 Rive Gauche boutiques open by the end of 1969.

1971: Yves Saint Laurent decides to use his own image –in the nude- to advertise his new perfume for

men and asks Jean Loup Sieff, one of France’s major photographers to take the picture. This reinforced

his reputation as “the most iconoclastic of the couturiers and enhanced his cult status” and shows him

to be a pioneer in what was known later as “designer marketing”.

“Realizing that the future of French fashion lay with prêt-à-porter, Pierre Bergé as anxious to distance

Yves Saint Laurent from the dying couture trade”. They decided to drop the couture shows and

replace them by RTW shows: another revolution. The first took place on October 28, 1971. Everything

was made to reinforce the RTW business: the new women’s perfume was named Rive Gauche.

1969 had seen a change in ownership for Charles of the Ritz, now part of Squibb-Beech Nut. A new

deal was struck concerning Yves Saint Laurent. Yves Saint Laurent and Pierre Bergé exchanged the

shares and royalty entitlements they had in the Company in return for full ownership of the fashion

company and a 5% royalty on wholesale sales of perfumes. Yves Saint Laurent had a right of veto over

the new fragrances to be developed –both the scents and the communication. They kept the right to

license any product except perfume and cosmetics.

In 1973, they decided to go back to couture: Yves Saint Laurent now created four collections a year.

Exhibit 3: The Jean Loup Sieff ad

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

13

In 1974, they signed an agreement with Maurice Bidermann, to manufacture Rive Gauche men’s wear

in the USA. This meant an immediate entry into the Department Stores: the men’s wear line made $50

million in sales in North America during its first year.

The 1970s were the years where Pierr Bergé grew the licensing business to huge proportions: he sold

the YSL name for eyewear, scarves, belts, ties ans even cigarettes. By the end of the decade, the YSL

name concerned 130 different products!

Couture definitely played its role in this: it was what built the brand ethos, what gave it its cult status.

The day following the “Ballets Russes” couture presentation in July 1976, the Madison Avenue store

made sales of $20 000, “ten times as much as the same day the previous year”. The $500,000 of the

couture show was bringing in the equivalent of millions in advertising. As Didier Grumbach says in

2002: “Creating haute couture costs a lot less than mounting an international ad campaign, but can have a lot

more impact”15.

By then Pierre Bergé, who was a visionary businessman and had learnt from Richard Salomon to take

a long-term view of the business, had taken the brand where no one else had really ventured, but

where all designers then went: the mix between couture, ready-to-wear and licenses. By 1977 the YSL

annual sales were reaching $250 million annually. Building on the iconoclastic image, YSL and Squibb

launched in 1975 (20 years before Calvin Klein’s “Ck One”) a genderless perfume “Eau Libre”, that

was intended to appeal to both men and women. Too far ahead of its times, it was a failure. However,

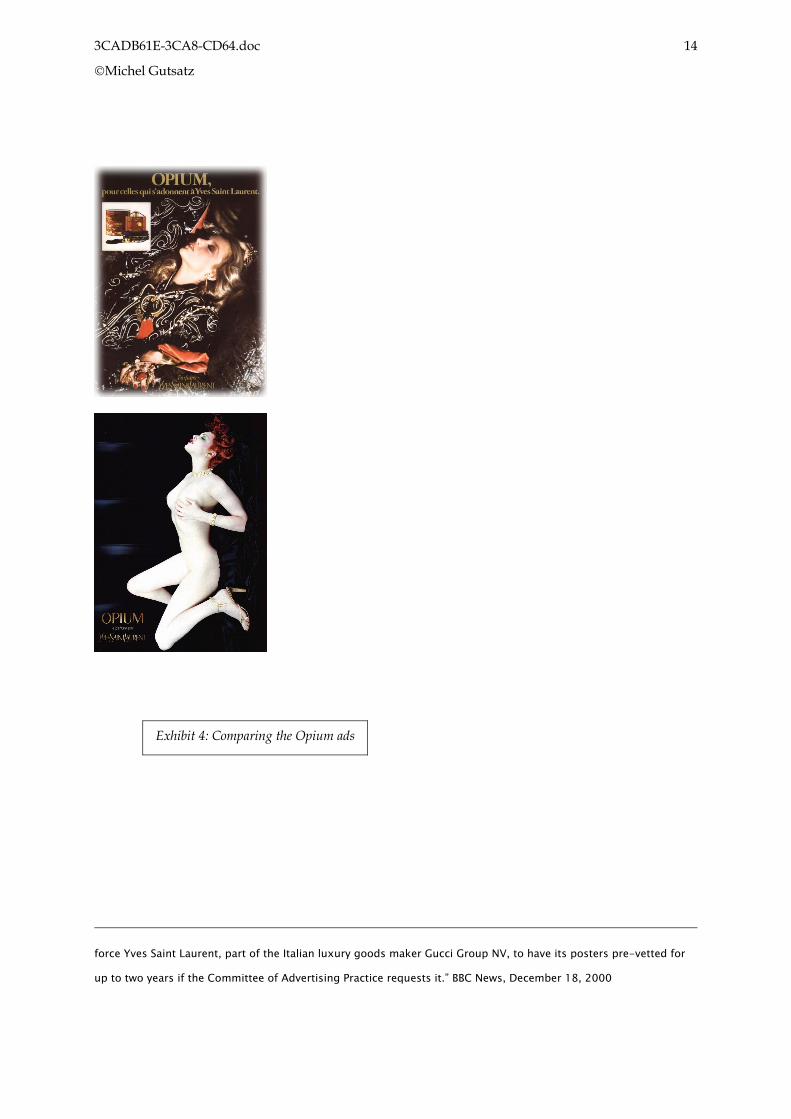

the next perfume was a huge success: “Opium” started as a scandal, both by the name16 and by the ad,

shot by Helmut Newton, that depicted model Jerry Hall “lying languidly on a lame sofa in the

Oriental Room at Rue de Babylone (Yves’ home), with the slogan ‘Opium, pour celles qui s’adonnent à

Yves Saint Laurent’; ‘Opium, for those that are addicted to Yves Saint Laurent’”. Yves Saint Laurent

himself was a major actor in the shooting of the picture, in the choice of the dress and in the slogan.

Isn’t it the same scandal that Tom Ford reinvents when his first gesture as YSL Creative Director is to

redesign the “Opium” ad in the summer of 2000 and have shoot model Sophie Dahl in a provocative

nude picture17?

15 http://www.fashionwindows.com/beauty/2002/ysl_save.asp

16 Yves Saint Laurent and squibb were accused of “glamorizing drug addiction”.

17 “A controversial billboard advert showing a naked female model in a suggestive pose has been banned by the

Advertising Standards Authority ruling. The Yves Saint Laurent Opium perfume advert featuring Sophie Dahl

attracted 730 complaints, making it one of the most complained about in the ASA's history. On Monday evening the

watchdog ordered all the posters to be withdrawn because they are "degrading" to women and offensive.

Christopher Graham, ASA director general, said the poster was sexually suggestive and likely to cause "serious or

widespread offence" thereby breaking the British Codes of Advertising and Sales Promotion. The ruling may also

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

14

force Yves Saint Laurent, part of the Italian luxury goods maker Gucci Group NV, to have its posters pre-vetted for

up to two years if the Committee of Advertising Practice requests it.” BBC News, December 18, 2000

Exhibit 4: Comparing the Opium ads

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

15

The resemblance is striking: Tom Ford obviously walks Yves Saint Laurent’s path here.

The US launch of Opium was a party on a junk that cost $300,000, a small part of the cost of the global

launch, of a perfume that made annual sales of $100 million with $2.5 million in royalties for Yves

Saint Laurent.

The end of the 70s saw Yves Saint Laurent himself retreating for RTW: the lines were now designed by

others, taking the themes he had defined and adapting them for the Rive Gauche line. That had a

catastrophic consequence: the discrepancies between the lines became soon evident. The Fall 1978

RTW collection was dismissed by Hebe Dorsey from the Herald Tribune as “terribly safe and classic”.

She added in the fall of 1979 “Yves Saint Laurent is on a fashion sabbatical”. Although this same

season’s couture was one of his greatest triumphs, the RTW collection was said to be a disaster “with

not a single new look”, “bourgeois and rather boring”.

1980: there are 140 Rive Gauche boutiques worldwide (but all of them save six were owned by

licensees and franchisees) and the annual royalties Yves Saint Laurent and Pierre Bergé draw from

their 190 licenses18 is approximately $18 million. They are very rich but the brand is getting to be

increasingly inconsistent. Alice Rawsthorn relates a significant anecdote that is the perfect example of

how a brand can be progressively killed by over stretching. Yves Saint Laurent was visiting China in

1985: “over on the other side of the store was an American tourist, one of those overweight Texans in a

plaid shirt, polyester trousers and a belt with a big buckle. The buckle might have had a cow on it, but

it didn’t, it said YSL. The Texan was smiling at Saint Laurent from the other side of the store, swaying

to and fro, pointing at the buckle.”

In 1985 Yves Saint Laurent had an annual turnover of $40 million and netted $8.4 million in profits –

but the brand name generated $1.2 billion in sales: this is where one sees the difference in scale

between the licensee business model and the fully controlled business model.

Pierre Bergé and Yves Saint Laurent made a step toward this alternative model when they bought

back the perfume & cosmetics business from Squibb in 1986, for $630 million, financed through a $465

million loan from Crédit Suisse First Boston. This was done with the help of Italian businessman Carlo

de Benedetti, who acquired a 25% stake in the company in November 1986. The new company, that

now included couture, perfume and cosmetics, made $432 million in annual sales. Pierre Bergé’s

objective was to gain as much control as possible over the brand, though he never seems to have

wanted to drop the other profitable license contracts and bring back into the company those products.

18 1983 saw the signature of the license with Cartier for watches, pens, leather goods and lighters.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

16

In order to finance its future development, and given the new model LVMH had set when it was

established in 1987, they decided to float the company in July 198919, Cartier taking a 6% stake in it

and Cerus, a Carlo de Benedetti company 14.9%. Eventually Pierre Bergé and Yves Saint Laurent

bought back in their name this stake when De Benedetti decided to sell it.

The 1990 results were great: $540 million in sales, which netted $45.4 million profits. But the Gulf War

was disastrous for the whole luxury industry. Two years later the situation deteriorated rapidly: some

boutiques were closed, the perfume sales were declining and the brand suffered both from its multiple

license system that flooded the market with inconsistent products and from the example of other

luxury companies that were considered as much more consistent than YSL. Moreover, YSL did not

benefit completely from the Rive Gauche distribution, as it did not own those stores: the largest part of

the profits went to the franchisees and licensees that operated them. Pierre Bergé had started closing

down certain licenses and imposed tighter control on the design of licensed products. But that was not

enough, and to achieve this the company needed much more important investments than it could

realize. The YSL shares had gone down from 1098 Francs in 1989 after flotation to 476 Francs in

December 1992. In 1993 Pierre Bergé and Yves Saint Laurent sold their shares of YSL to Sanofi, a major

French pharmaceutical company. The deal left both men in charge of the fashion house till 2001, Yves

Saint Laurent keeping right of veto over all beauty products to be developed as in the Squibb contract.

However they had to relinquish their rights to royalties on the sales of perfumes and cosmetics20.

Pierre Bergé was now a salaried manager and both him and Yves Saint Laurent were but minority

shareholders in a company they had owned.

The final act was played in 1999, when Gucci bought YSL from Sanofi (with the money of PPR). The

last deal Pierre Bergé closed for Yves Saint Laurent was to split couture from ready-to-wear, Yves and

himself keeping the couture house as a separate legal entity, Gucci managing all the other YSL

operations. The financial deal is, according to French daily Le Monde21, astonishing and most

profitable: first of all they will receive $70 million for the use of Yves Saint Laurent’s name and for

giving up all executive positions in the YSL company; they will be paid –through their common

consulting company – 0.4% of the annual sales of YSL Parfums till 200622; the couture company will

receive $40 million in intellectual property rights (halved if both men retire before December 31 2002 –

which is now the case).

The Gucci Group’s first decisions are in line with the Gucci business model.

19 “Yves Saint Laurent had become the first French fashion company ever quoted on the stock market”.

20 For which they received $65 million in shares of YSL, plus shares in Sanofi, plus annual salaries of $2 million.

21 November 19, 1999

22 With a maximum of $4 million per year. This part of the agreement can be renewed for a maximum of 10 years.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

17

«Gucci was more complicated with the family situation, and it was a process that went on for a long time», says

Domenico De Sole23. «The situation at YSL was more dramatic because of the timing. Most of the licenses have

already been terminated, and the others will have expired by the end of next year. In the end, we want to see YSL

running on the same business model as Gucci.»

Tom Ford the Creative Director of Gucci, was appointed Creative Director of Yves Saint Laurent and

he outlined what his strategy would be:

• Give a consistent vision to the brand: “My first job is to unify the entire company, give it a strong

point of view, from advertising to store concept, visual display, clothing, shoes, bags, it all has to relate”

• Open Company owned stores: “We have about 25 stores now, and will have between 50 and 60 in

two to three years.” The franchisees are progressively bought back: in November 2000 YSL took

over the rights to the Japanese market from its Japanese franchisee –including the 5 stores.

From 15 at the end of 2000, the number has grown to 40 at the end of 2001.

• Cutting down licenses: “When we took possession of the company in December, we had 167 licenses.

By January of 2001, we will have 64…. Our goal over the next two to three years is to get that number

down to a tiny handful of licenses, like we have at Gucci. We have licensed eyewear24, we have the

fragrance license, and that’s it. We have a complete control over the product”25. YSL acquired its

ready-to-wear licensee C. Mendes SA in February 2000 –who owned nine stores- , and has

since bought back licenses from Cartier for watches and Schwartz & Benjamin for footwear.

Sergio Rossi, part of the Gucci Group, will now manufacture Yves Saint Laurent shoes. In

February 2001, YSL discontinued the “Variation” line, the ready-to-wear sportswear line

Pierre Bergé had launched and which was competing with Rive Gauche at much lower price

points.

23 WWD, August 1 2000

24 YSL signed an eyewear license with Safilo (Gucci’s licensee) in January 2002.

25 “Tom Pumps Up”, W, July 2000

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

18

B. Investing in Retail and Balancing Distribution Channels

“We compete for everything. We compete for stores, for talents, for brands” Domenico De Sole

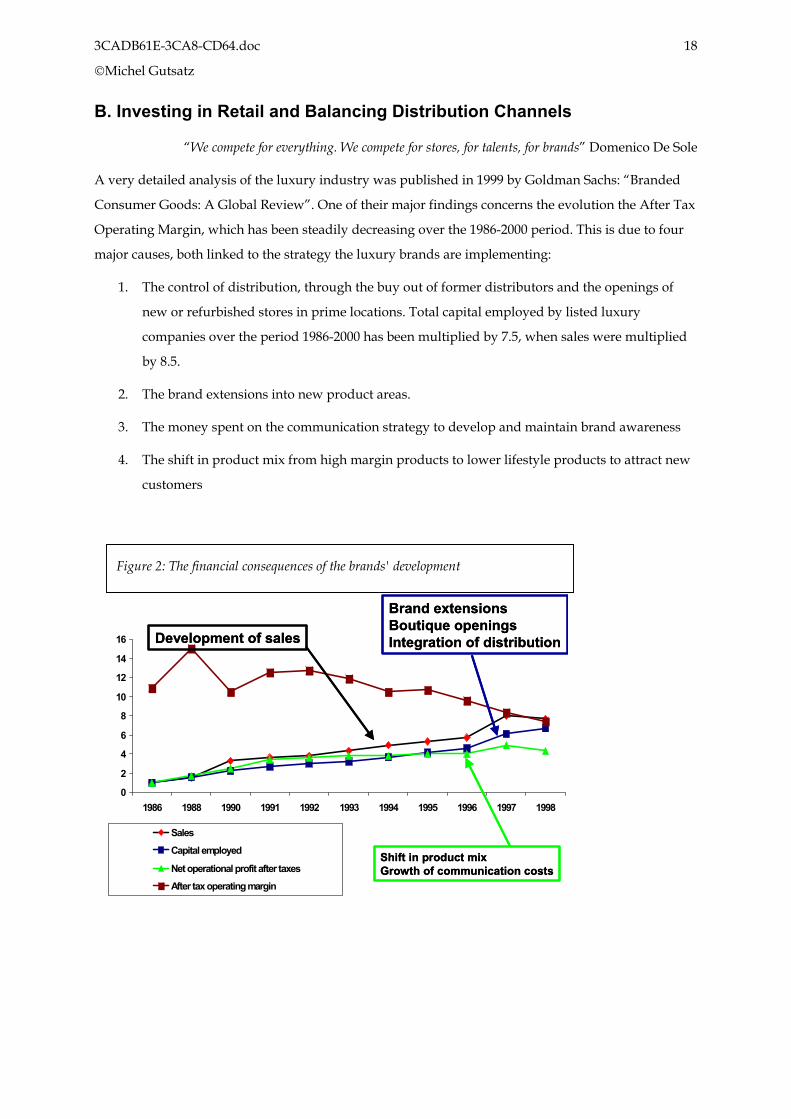

A very detailed analysis of the luxury industry was published in 1999 by Goldman Sachs: “Branded

Consumer Goods: A Global Review”. One of their major findings concerns the evolution the After Tax

Operating Margin, which has been steadily decreasing over the 1986-2000 period. This is due to four

major causes, both linked to the strategy the luxury brands are implementing:

1. The control of distribution, through the buy out of former distributors and the openings of

new or refurbished stores in prime locations. Total capital employed by listed luxury

companies over the period 1986-2000 has been multiplied by 7.5, when sales were multiplied

by 8.5.

2. The brand extensions into new product areas.

3. The money spent on the communication strategy to develop and maintain brand awareness

4. The shift in product mix from high margin products to lower lifestyle products to attract new

customers

Figure 2: The financial consequences of the brands' development

0

2

4

6

8

10

12

14

16

1986 1988 1990 1991 1992 1993 1994 1995 1996 1997 1998

SalesCapital employed

Net operational profit after taxesAfter tax operating margin

Brand extensionsBoutique openingsIntegration of distribution

Brand extensionsBoutique openingsIntegration of distribution

Shift in product mixGrowth of communication costsShift in product mixGrowth of communication costs

Development of salesDevelopment of sales

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

19

Controlling distribution, as we have seen, is critical for Luxury Brands. This means fighting for

window space to develop highly visible stores in fashionable areas. Brands must tackle a tricky

problem: simultaneously open new stores to develop awareness AND make sure that these operations

are profitable. As we shall see, this is no simple problem: it has led luxury brands to develop a

flagship plus satellite store network we shall analyze.

But directly operated retail is but one of the many distribution channels these brands use. There is

only ONE Luxury Brand that relies 100% on its own stores: Louis Vuitton. ALL other brands develop

multiple distribution channels. We shall look into it, with a strong focus on Travel Retail.

Retail locations: fighting for window space

A recent study by French marketing company Euromap26 shows that 80% of those that had recently

bought a luxury product (67% of interviewees) had pre-decided where they would go shopping for it.

Both the part of the city and the store they were initially targeting were also where they finally bought

the product. For the customers of luxury brands the city is segmented in zones where you will

systematically shop for the items you are looking for. Each major city in the world has its luxury retail

areas.

The traditional luxury shopping areas are the “luxury ghettos”, where all luxury brands aggregate

themselves, one next to the other. Avenue Montaigne, Rue du Faubourg Saint Honoré and Place

Vendôme (for jewelers) in Paris, Bond Street in London, Madison Avenue and 57th Street in New

York, Via Montenapoleone and Via Spiga in Milan. You will find a similar model in a shopping mall

like Lee Gardens in Hong Kong.

The last four or five years have seen an alternative model appear. Customers that will favor luxury

consumption as part of their normal daily consumption will want to be able to reach multiple levels of

distribution in a single vicinity. They will want to buy Versace or Hermès but also see a movie, buy a

newspaper, eat, buy at Gap or H&M. We have all seen the chauffeured limousine waiting for a very

well dressed lady who carries a Zara shopping bag. You will also have the hedonic consumer, that

will be a basketball fan, and who will shop at the NBA store on 5th Avenue and at nearby Prada. These

new luxury distribution areas you also will find in most large cities: Avenue des Champs Elysées in

Paris, 5th Avenue and Soho in New York, Pacific Place in Hong Kong, Ginza in Tokyo.

26 EUROMAP: Comment se decide et se réalise un achat dans le luxe, January 2002. 600 affluent women in France,

Germany and Italy were interviewed.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

20

LUXURY GHETTOS: THE LONDON BOND STREET CASE

The following map shows what a luxury ghetto is: a continuous line of luxury brand stores, with, here

and there, auctioneers, department stores, jewelers. The list of brands present speaks for itself.

• Hermès •Church’s •Lalique •Celine •Nicole Farhi •Max Mara •Fine Arts Society •Polo Ralph Lauren •Mallett Antiques •Zili •Philipps Silverware •YSL •Wempe •Thierry Mugler •Louis Vuitton •Donna karan •Burberry •Charles Jourdan •Longchamp •Alain Figaret •Sotheby’s •Zegna •Mulberry •Armani

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

21

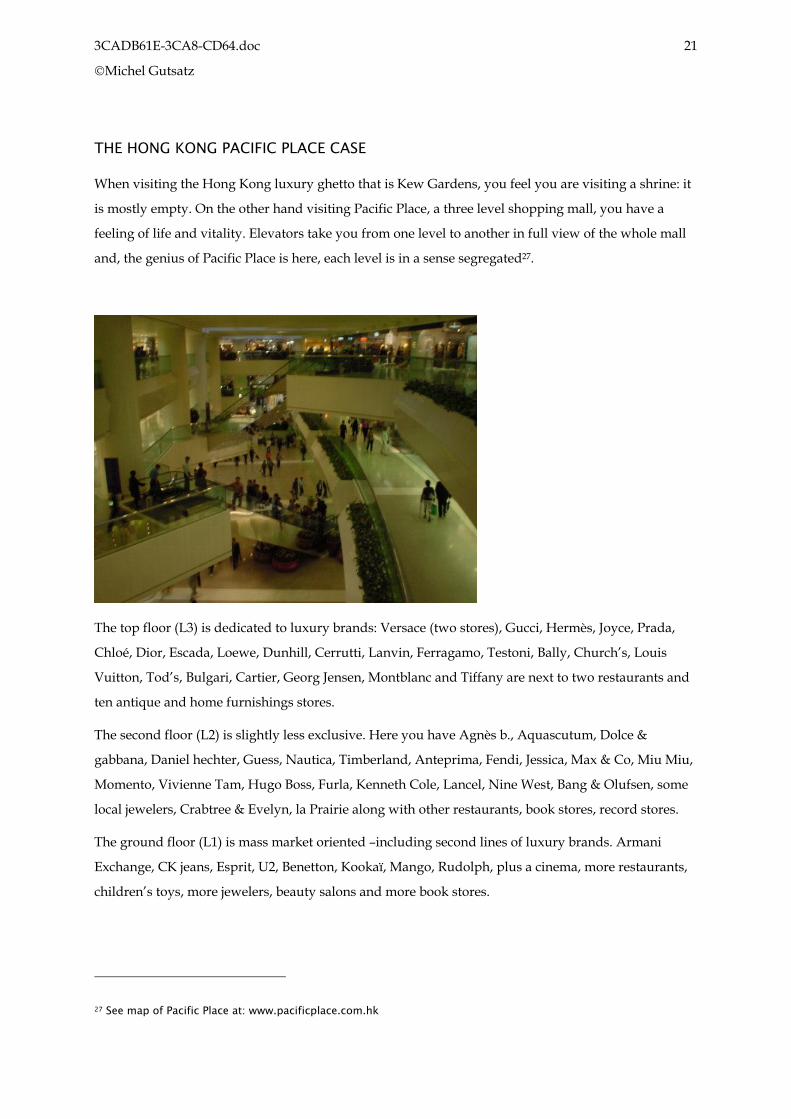

THE HONG KONG PACIFIC PLACE CASE

When visiting the Hong Kong luxury ghetto that is Kew Gardens, you feel you are visiting a shrine: it

is mostly empty. On the other hand visiting Pacific Place, a three level shopping mall, you have a

feeling of life and vitality. Elevators take you from one level to another in full view of the whole mall

and, the genius of Pacific Place is here, each level is in a sense segregated27.

The top floor (L3) is dedicated to luxury brands: Versace (two stores), Gucci, Hermès, Joyce, Prada,

Chloé, Dior, Escada, Loewe, Dunhill, Cerrutti, Lanvin, Ferragamo, Testoni, Bally, Church’s, Louis

Vuitton, Tod’s, Bulgari, Cartier, Georg Jensen, Montblanc and Tiffany are next to two restaurants and

ten antique and home furnishings stores.

The second floor (L2) is slightly less exclusive. Here you have Agnès b., Aquascutum, Dolce &

gabbana, Daniel hechter, Guess, Nautica, Timberland, Anteprima, Fendi, Jessica, Max & Co, Miu Miu,

Momento, Vivienne Tam, Hugo Boss, Furla, Kenneth Cole, Lancel, Nine West, Bang & Olufsen, some

local jewelers, Crabtree & Evelyn, la Prairie along with other restaurants, book stores, record stores.

The ground floor (L1) is mass market oriented –including second lines of luxury brands. Armani

Exchange, CK jeans, Esprit, U2, Benetton, Kookaï, Mango, Rudolph, plus a cinema, more restaurants,

children’s toys, more jewelers, beauty salons and more book stores.

27 See map of Pacific Place at: www.pacificplace.com.hk

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

22

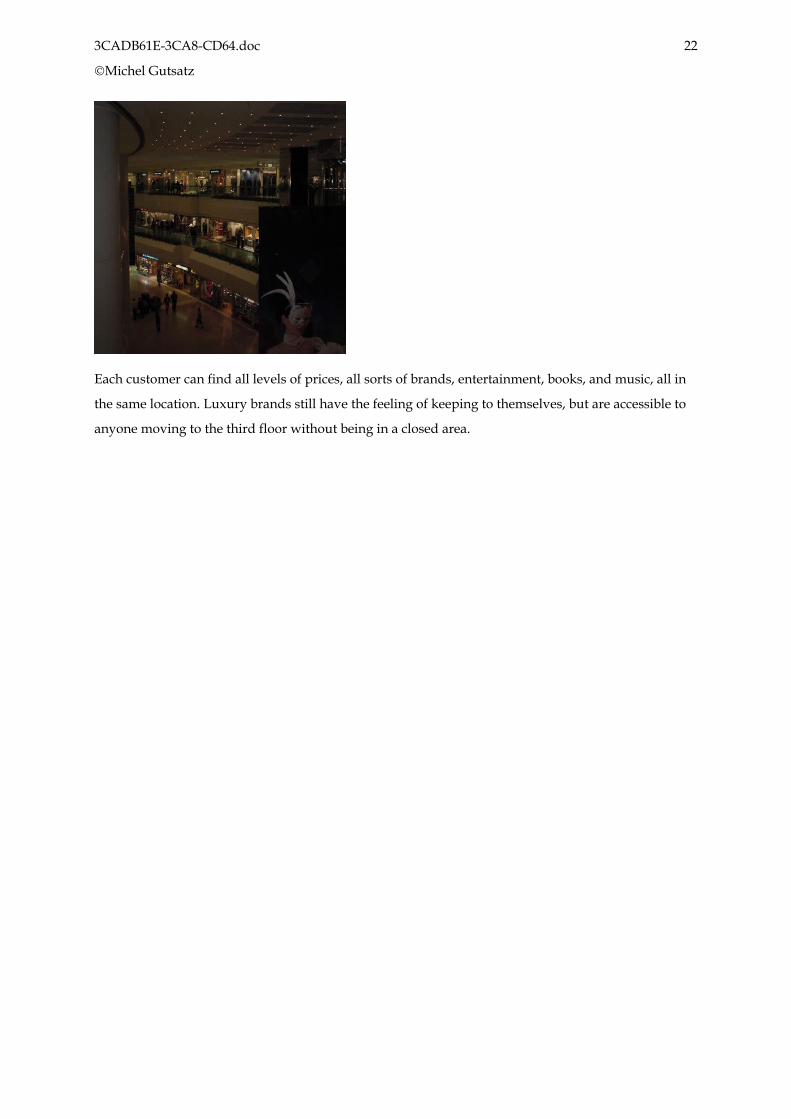

Each customer can find all levels of prices, all sorts of brands, entertainment, books, and music, all in

the same location. Luxury brands still have the feeling of keeping to themselves, but are accessible to

anyone moving to the third floor without being in a closed area.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

23

LOCATION, LOCATION, BREAK-EVEN: THE FLAGSHIP AND SATELLITES MODEL

Of course location is critical. Of course size and quality of the store are critical too. Recently each

brand has been focusing on having a dual store system, the “flagship and satellites” model:

• Big flagship stores in prime locations: they are supposed to display the whole range of

merchandise available, on surfaces that are over 800 sq.meters or approximately 8,000 sq.

feet. One of the most spectacular is the 1000 sq.meters Louis Vuitton flagship that opened in

February 1998 on the Paris Champs Elysées, and whose turnover was $95 million in 2000.

Recently these flagships have seen a further move towards integration of all available lines of

the brand, which may have been displayed in different stores. Armani is a perfect case here.

They are opening a new 29 000 sq. feet store in Hong Kong, within which all Armani lines will

be grouped: Giorgio Armani, Emporio Armani, Armani Jeans, Armani cosmetics, an Armani

Caffe’ and a flower store. This is the second such “lifestyle” store, following the 8 000 sq.

meters Milan one on Via Manzoni that opened in October 2000: Emporio Armani, Armani

Jeans, Armani Casa, a gallery Armani Arte, an Armani Caffe’, a book store, a restaurant and a

flower store are thus displayed together.

• Satellites, that is medium sized stores (100 to 400-500 sq. meters) in prime secondary locations

in important cities. A small part of the available lines and merchandise are displayed, usually

the best sellers. It can happen that these stores be specialized: a women’s store, a men’s store,

a shoe store…

The move to bigger flagship stores started in 1995-1996 and the trend has been to grow the size of all

stores –even medium-sized ones- when possible: Hermès has grown its New York store from 5000 to

20200 sq. feet in 2000, its Bal Harbour store from 720 to 4400 sq. feet in 2002 and its Beverly Hill’s store

from 1300 to 17000 sq. feet in 1997; when Gucci revamped its London Sloane Street store in 1997, it

went from 5000 to 15000 sq. feet; even Louis Vuitton –whose stores are not above the 10 000 sq. feet

mark- has refurbished its Bal Harbour store and has grown it from 1800 to 5400 sq. feet.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

24

Europe USA Japan + Asia

Flagship store Milan Via Sant’Andrea (760 sq. meters)

Paris

London (Club 21)

Beverly Hills (13,000 sq ft-Franchisee)

Chicago (8 000 sq ft)

Los Angeles

New York

San Francisco

Tokyo

Hong Kong (29,000 sq.ft grouping all Armani lines – Fall 2002)

Normal store Italy:

Bologna

Florence

Naples

Padova & Portofino (Franchisee)

Rome

Torino

Belgium:

Brussels

Germany:

Dusseldorf

Hamburg

Munich

Spain

Madrid & Barcelona (franchisee)

Switzerland:

Geneva (franchisee)

Saint Moritz

Zurich (Franchisee)

UK:

London Sloane Street (Club 21)

Bal Harbour

Boston

Las Vegas

Manhasset

Palm Beach

Kobe

Nagoya

Osaka

Exhibit 5: The Armani Stores

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

25

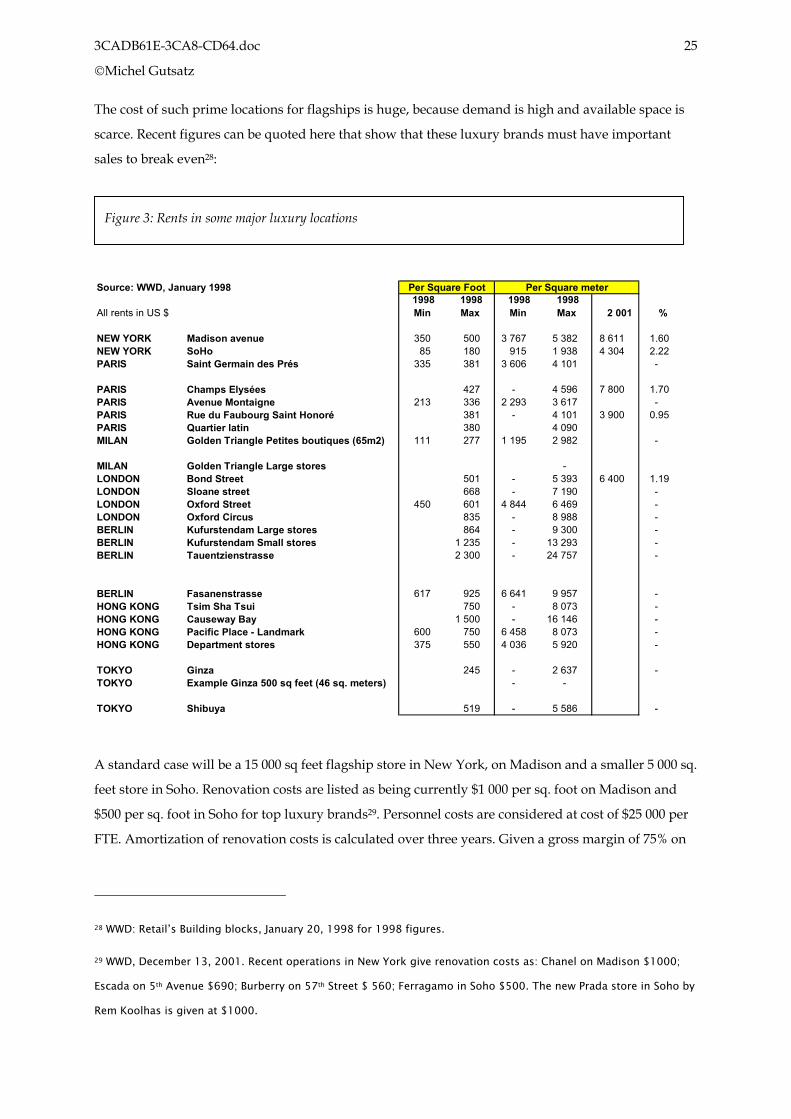

The cost of such prime locations for flagships is huge, because demand is high and available space is

scarce. Recent figures can be quoted here that show that these luxury brands must have important

sales to break even28:

A standard case will be a 15 000 sq feet flagship store in New York, on Madison and a smaller 5 000 sq.

feet store in Soho. Renovation costs are listed as being currently $1 000 per sq. foot on Madison and

$500 per sq. foot in Soho for top luxury brands29. Personnel costs are considered at cost of $25 000 per

FTE. Amortization of renovation costs is calculated over three years. Given a gross margin of 75% on

28 WWD: Retail’s Building blocks, January 20, 1998 for 1998 figures.

29 WWD, December 13, 2001. Recent operations in New York give renovation costs as: Chanel on Madison $1000;

Escada on 5th Avenue $690; Burberry on 57th Street $ 560; Ferragamo in Soho $500. The new Prada store in Soho by

Rem Koolhas is given at $1000.

Source: WWD, January 1998

All rents in US $1998Min

1998Max

1998Min

1998Max 2 001 %

NEW YORK Madison avenue 350 500 3 767 5 382 8 611 1.60 NEW YORK SoHo 85 180 915 1 938 4 304 2.22 PARIS Saint Germain des Prés 335 381 3 606 4 101 -

PARIS Champs Elysées 427 - 4 596 7 800 1.70 PARIS Avenue Montaigne 213 336 2 293 3 617 - PARIS Rue du Faubourg Saint Honoré 381 - 4 101 3 900 0.95 PARIS Quartier latin 380 4 090 MILAN Golden Triangle Petites boutiques (65m2) 111 277 1 195 2 982 -

MILAN Golden Triangle Large stores - LONDON Bond Street 501 - 5 393 6 400 1.19 LONDON Sloane street 668 - 7 190 - LONDON Oxford Street 450 601 4 844 6 469 - LONDON Oxford Circus 835 - 8 988 - BERLIN Kufurstendam Large stores 864 - 9 300 - BERLIN Kufurstendam Small stores 1 235 - 13 293 - BERLIN Tauentzienstrasse 2 300 - 24 757 -

BERLIN Fasanenstrasse 617 925 6 641 9 957 - HONG KONG Tsim Sha Tsui 750 - 8 073 - HONG KONG Causeway Bay 1 500 - 16 146 - HONG KONG Pacific Place - Landmark 600 750 6 458 8 073 - HONG KONG Department stores 375 550 4 036 5 920 -

TOKYO Ginza 245 - 2 637 - TOKYO Example Ginza 500 sq feet (46 sq. meters) - -

TOKYO Shibuya 519 - 5 586 -

Per Square Foot Per Square meter

Figure 3: Rents in some major luxury locations

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

26

the products sold in the stores (standard luxury brands USA figures30), these two stores would have to

sell $9 000 per sq. meter (Soho) and $ 17 000 per sq. meter (Madison) to break even.

MADISON SOHOSurface 15 000 5 000 Renovation costs 15 000 000 2 500 000 Rent per sq foot 800 400 Personnel FTE 20 12 Rent 12 000 000 2 000 000 Personnel 500 000 300 000 Others 5 000 000 800 000

Total 17 500 000 3 100 000 Gross margin 75%Annual sales to breakeven 23 333 333 4 133 333 Sales per sq. foot 1 556 827 Sales per sq. meter 16 744 8 898

These figures show that opening a store since 1997-1998 is a tough proposition: breakeven can be very

difficult to achieve in certain locations, unless you are a very well known brand. Neiman Marcus gives

their annual sales per sq. meter to be $4800 and a standard department store’s to be $2000. Galeries

Lafayette in Paris has sales of $11,000 per sq. meter. The only way to achieve the figures above is to

draw traffic and make sure the conversion rates are good!31

As store designer Kenne Shepherd says: “The luxury fashion store has become as important an identity

statement for the fashion designer as the collection itself. It is an extension of a unified worldwide fashion image,

in a world where image is the lifeblood of the industry”32.

Those flagships are image-builders. Profits come from all the satellite stores, those that either are in

cheaper areas or have been in prime locations with the brand for a long time –when rents were much

lower. For instance a 459 sq. meter store in New Bond Street whose lease ends in 2011 comes for a rent

30 It would be 60-65% in Europe and 80% in Japan.

31 If, on top of these direct costs, the brand has overheads of $ 1 million (cost of HQ, conception, marketing and

communication) it needs an additional $1.8 million in sales at full price to break even. Total sales in a small 150 sq.

meters store would then need to be around $3 million. On the other hand licensing production and distribution,

given a 6% licensing royalty, needs total sales (at retail level) of $ 17 million to cover the overheads!

32 Kenne Shepherd: Lifestyles as Destination: Retail Design Today, www.kenneshepherd.com/articles/qxd-

pdf/FGI.pdf. He works currently for Ferragamo, Escada, Lancôme, Calvin Klein.

Figure 4: Breakeven figures for New York Locations (2001)

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

27

of $800 per sq. meter. A 245 sq. meter store in Old Bond Street whose lease runs to 2015 has rent of

$1600 per sq. meter. Bond Street today is rated at $6400 per sq. meter! Break even in those stores will

be much lower: given a 65% gross margin (European standard figures), no renovation costs and other

direct costs equivalent to the personnel costs, this store reaches break even at $ 5000 per sq. meter sales

– against $15 000 per sq. meter if it was to be rented and renovated today.

Luxury brands are facing a very cyclical real estate market. When the demand is high (as in the period

1999-2001), real estate is priced at the level of the highest performers – those that are ready to offer top

prices for scarce prime locations- and include aggressive sales expectations over the coming 3 to 5

years. Renegotiating leases at that period of the business cycle will be tough, and stores that were very

profitable before may not be profitable anymore.

When there is a slowdown of the market (1991-1992 after the Gulf War; 1997-1998 in Asia) the real

estate market falls and brands will renegotiate their leases. This is what happened in Asia in 1997-

1998: instead of closing down operations, the major luxury brands renegotiated their contracts and

opened new stores with rock-bottom leases. These stores now are very profitable.

Last but not least, there is a Group factor: each Luxury Group will have a strong negotiation power

when opening stores for more than one of their brands.

BOND STREET NEW LEASE

BOND STREET OLD LEASE

Surface (sq.meters) 400 400 Renovation costs (per sq. meter) 5 000 Total renovation cost 2 000 000 Rent per sq meter 6 400 1 600 Personnel FTE 13 13 Rent 2 560 000 640 000 Personnel 500 000 500 000 Others 700 000 100 000

Total 3 760 000 1 240 000 Gross margin 65%Annual sales to breakeven 5 784 615 1 907 692 Sales per sq. meter 14 462 4 769

Figure 5: Breakeven figures in London

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

28

TURNING AROUND A BRAND: THE STORE URGENCY

When Domenico De Sole became COO of Gucci in May 1994, one of his very first moves was to

redesign the stores: “In December 94, within six weeks, all stores worldwide had been ‘milanized’ that is

redesigned on the model of the Milan store.. small changes, not expensive but which made major impact”33.

When Gucci bought Yves Saint Laurent in November 1999, the very first thing they did was develop

both the store network and redesign the standard store format. The model of the new YSL store,

designed by Tom Ford and architect William Sofield, was opened in December 2000 at the Bellagio in

Las Vegas, the seconb being the New York Madison Avenue flagship store in September 2001. The

number of stores, which was 15 when the brand was bought, grew to 30 a year later and to 40 two

years later.

When Gucci bought Bottega Venetta in February 2001, the brand owned 19 stores. The first new-look

flagship store was opened in December 2001 on Madison Avenue. Six more stores -in Paris, Milan,

London, San José, Costa Mesa, Chicago (a move to a more prestigious place in the Hyatt) - to which

will be added eight stores in Japan are planned in 2002. The existing stores will all be refurbished

within one year. This means that within two years of its take-over, Bottega Venetta will have renewed

all its stores and doubled their number!

Stores are where the brand meets the customer: this is where the vision and the style of the brand are

expressed. This is where a luxury brands has to invest in CAPEX if they want to increase their

visibility. Brands that do not have the money to ensure that this is the case, brands that do not

understand that it is in the stores that it all happens and just keep the old concepts up and running,

will face tough problems34.

33 Les Echos Conference, March 14 2000

34 This is the case for Bally, the Swiss brand that Texas Pacific Group bought in October 1999. Having decided to

turn it into a luxury brand they have not had this sense of urgency: after closing down most of the second rate

stores, they were left with 179 stores in July 2001, out of which TWO had the new concept (in Berlin and Singapore)

and 15 only had been refurbished along softer and much less luxurious lines!

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

29

STORE FORMATS: CLOSED OR OPEN?

The traditional luxury brand store is a closed store, which is to be entered through a glass door. There

are however different formats possible (which we will illustrate with the different Cartier stores),

ranging from closed to very closed format, all based on the window concept:

• A closed window, with no view on the inside of the store, and a door that opens only on

request: this is the traditional Jewelry format that Cartier displays in most of its stores (Exhibit

8)

• An open window, displaying products, with a removable back, which only gives a partial

view of the inside of the store. This is the new “slate” Cartier format displayed in the

Faubourg Saint Honoré in Paris (Exhibit 7)

• An open see through window, that allows the customer to envision the whole store when

standing outside: this is the case for the Cartier stores on Madison Avenue and 5th Avenue in

New York (Exhibit 6)

Exhibit 6: The Cartier New York store format

Exhibit 7: The new “slate” Cartier format

Exhibit 8: The traditional Cartier format

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

30

Each of these formats will generate a different relationship between the customer and the brand,

which will very much depend on the familiarity of the customer with the brand.

Familiar customers Non familiar customers

Format 1“Fort Knox” They will feel at ease and

sheltered from the rest of the

world in a very exclusive

environment

They will feel totally unwelcome

and will not even push the door

open

Format 2 They will still be rather

intimidated: this format is close

to Format 3

Format 3 « Open window » The will feel rather comfortable

and can anticipate what will

happen inside.

Democratization of luxury means also that potential customers, not familiar with the brand, must

be able to access it without feeling rejected or intimidated. The “Open Window” format is therefore

much more suited to these new customers. There exists a fourth store concept, the “Open store”,

which is the ultimate in welcoming unfamiliar customers: there is no door and no window to hinder

the entrance. There are two examples of such stores:

• Almost all the Travel Retail stores in the Airports have this format: people can come in

without having to push a door open. All studies made show that this facilitates the access of

luxury brands for non-traditional customers. Even jewelers like Cartier and Bulgari adopt

these open stores in their airport locations (Exhibits 9 & 10).

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

31

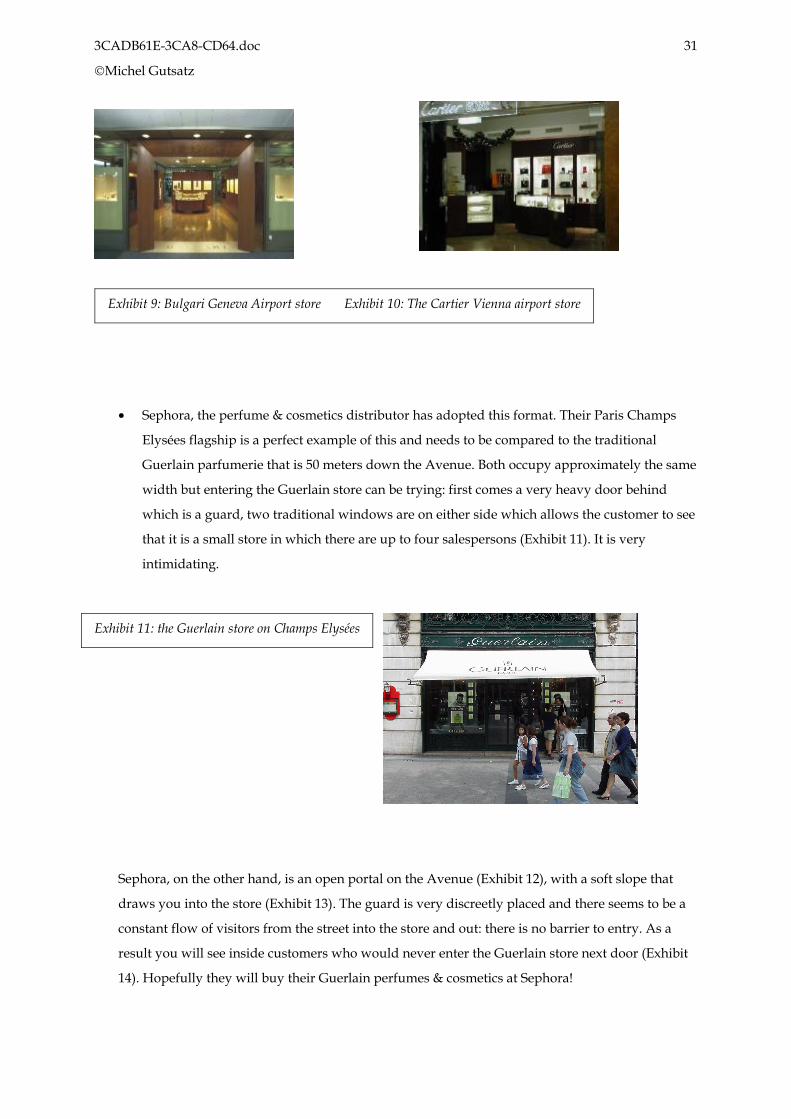

• Sephora, the perfume & cosmetics distributor has adopted this format. Their Paris Champs

Elysées flagship is a perfect example of this and needs to be compared to the traditional

Guerlain parfumerie that is 50 meters down the Avenue. Both occupy approximately the same

width but entering the Guerlain store can be trying: first comes a very heavy door behind

which is a guard, two traditional windows are on either side which allows the customer to see

that it is a small store in which there are up to four salespersons (Exhibit 11). It is very

intimidating.

Sephora, on the other hand, is an open portal on the Avenue (Exhibit 12), with a soft slope that

draws you into the store (Exhibit 13). The guard is very discreetly placed and there seems to be a

constant flow of visitors from the street into the store and out: there is no barrier to entry. As a

result you will see inside customers who would never enter the Guerlain store next door (Exhibit

14). Hopefully they will buy their Guerlain perfumes & cosmetics at Sephora!

Exhibit 9: Bulgari Geneva Airport store Exhibit 10: The Cartier Vienna airport store

Exhibit 11: the Guerlain store on Champs Elysées

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

32

Exhibit 12: the entrance of Sephora Exhibit 13: Customers at Sephora

Exhibit 14: The slope draws you inside…

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

33

GROWING A RETAIL NETWORK: THE SEPHORA CASE

In the summer of 1997 the whole luxury industry was shocked still by two news: LVMH had bought

DFS (Duty Free Shoppers) the world’s n°1 Duty Free chain and Sephora, Europe’s n°2 perfume &

cosmetics chain. Many stupid things were said at the time, most of them along the line: “LVMH will

favor their own brands in those stores; the other luxury brands will be cut out of these distribution

channels”. Many observers noted that LVMH was entering a new business –distribution- it had only

been familiar with through their brands’ company owned stores. Others hailed this move (I was one

of them at the time) as offering the possibility of capturing the retailer’s margin and making important

additional profits.

March 2002: given the poor results of its Selective Distribution Division, observers are laying bets on

when LVMH will divest itself of DFS and Sephora, concentrating on its core business, luxury brands.

Sephora had closed its operations in Japan, Germany and Turkey late 2001. Bernard Arnault, in an

interview, said: “Our objective is to make these companies profitable”35 –which analysts immediately

translated as “to sell them for a better price”.

Sephora is the story of a brilliant concept that lost its soul as it was grown much too fast in less than

three years. It is a story of overconfidence.

When LVMH bought Sephora in July 1997, it was a French chain of 57 stores with a radical concept,

highly visible in its flagship store on the Champs Elysées. This concept obeys seven basic rules:

• Rule 1: The customer is free to move and choose in the one-level store. Salespersons are there

“on demand”. This is a break from traditional French perfumeries with its ever-present sales

staff and is copied on modern distribution.

35 Le Monde, March 9 2002

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

34

• Rule 2: The store is organized in three areas, fragrances, cosmetics and skin-care. Within the

fragrances area, brands are organized by alphabetical order; by colors in the make-up area

and by function in the skin-care area. A given brand is therefore present in three different

locations, which breaks one of the basic rules of brand selling in perfumes & cosmetics:

present the complete brand offer. When discussing the topic with Estée Lauder executives in

1999, they were adamant: “This is contrary to our brand strategy”, but when asked their sales,

they had to admit that the Champs Elysées store was by far their best sales point in Paris.

• Rule 3: “Sephora is a sect” used to say former CEO Daniel Richard. A church of modern

perfumes & cosmetics consumption would be a better description: ''A bit religious, a bit

Egyptian, as if they were offering rites in a cathedral'' he added. Of course the black uniform

and the black glove on the left hand are important here, but the architecture of the flagship

stores is what is critical. It is the “Cathedral Concept”. Both the Paris Champs Elysées (2 500

sq meters) and the Barcelona (20 000 sq ft) stores are typical here: they are organized on a plan

that is similar to that of a (modern) church. A very long nave, round columns on either side, a

slope that draws you inside the store, the cash registers centered as an altar may be. Light is

used as a modern substitute for stained glass.

Exhibit 15: Plan of the Champs Elysées Sephora store

Exhibit 16: Lights in the Barcelona Store

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

35

• Rule 4: Develop an entertainment concept, all features relating to the business. The Top Ten

Fragrance Wall (to experience the bestsellers), the Fragrance Organ (to test and compare

fragrances), the Cultural Gallery (featuring exhibits on beauty, magazines, books), the Lipstick

Rainbow (365 shades displayed), the Fragrances Prices Wall (displaying worldwide prices of

chosen fragrances compared to the local Sephora price): all are there to make shopping an

experience. The use of colors, music, scents; the space available for customers to roam around

without bumping into each other, are all there to have people buy more.

• Rule 5: Mix flagship stores and satellite stores. Next to the Champs Elysées store, the standard

Sephora in France is approximately 400 to 500 square meters (# 5 000 sq. ft.) and has kept only

the merchandising of the “Cathedral Concept”. The new US stores are 4,000 to 5,000 sq. ft

(Disneyland, Pittsburgh, Sacramento, Pasadena…).

• Rule 6: Have the widest possible offer on the market, mixing luxury brands, some mass brands

and the Sephora brand. Standard company figures say that their stores hold 250 different

brands and 12000 products.36

• Rule 7: Introduce modern distribution methods in a world of tradition. Most brands were

accustomed to deal with independent retailers or department stores. Sephora changed that.

When the Paris flagship opened, the boards above the fragrances were the alphabetical order,

read A…For Aramis, B…For Boucheron, etc. A few months later, where some boards retained

brand names others read: A.. For Alchemy; B.. For Beauty. The difference was that now

Sephora asked the brands to pay to have their names displayed. As a further step they

introduced in 2001 Category Management that Wal-Mart and Carrefour have been using for

years. The Luxury Brands have a tough time adapting to this.

36 In The New York 5th Avenue store the Color Floor holds 40 brands, the Fragrance Floor 300 women’s and 200

men’s fragrances, the Well Being Floor, 100 collections.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

36

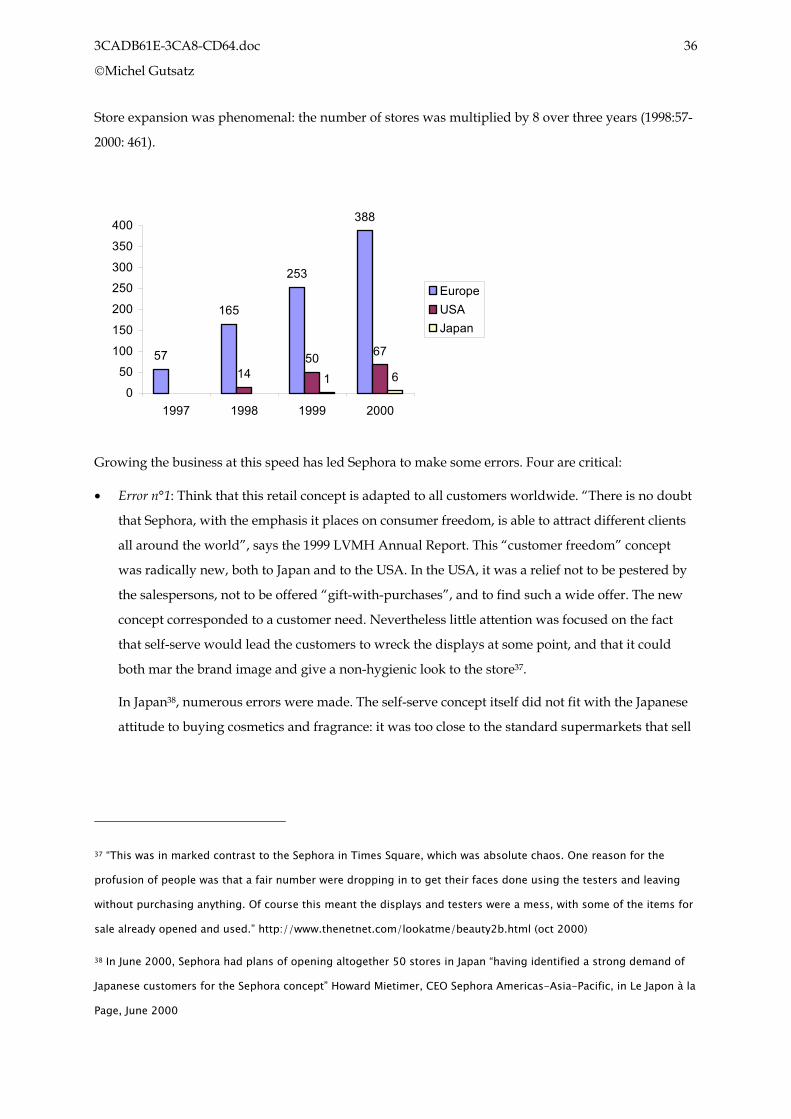

Store expansion was phenomenal: the number of stores was multiplied by 8 over three years (1998:57-

2000: 461).

57

165

253

388

1450 67

1 60

50100

150

200

250300

350

400

1997 1998 1999 2000

EuropeUSAJapan

Growing the business at this speed has led Sephora to make some errors. Four are critical:

• Error n°1: Think that this retail concept is adapted to all customers worldwide. “There is no doubt

that Sephora, with the emphasis it places on consumer freedom, is able to attract different clients

all around the world”, says the 1999 LVMH Annual Report. This “customer freedom” concept

was radically new, both to Japan and to the USA. In the USA, it was a relief not to be pestered by

the salespersons, not to be offered “gift-with-purchases”, and to find such a wide offer. The new

concept corresponded to a customer need. Nevertheless little attention was focused on the fact

that self-serve would lead the customers to wreck the displays at some point, and that it could

both mar the brand image and give a non-hygienic look to the store37.

In Japan38, numerous errors were made. The self-serve concept itself did not fit with the Japanese

attitude to buying cosmetics and fragrance: it was too close to the standard supermarkets that sell

37 “This was in marked contrast to the Sephora in Times Square, which was absolute chaos. One reason for the

profusion of people was that a fair number were dropping in to get their faces done using the testers and leaving

without purchasing anything. Of course this meant the displays and testers were a mess, with some of the items for

sale already opened and used.” http://www.thenetnet.com/lookatme/beauty2b.html (oct 2000)

38 In June 2000, Sephora had plans of opening altogether 50 stores in Japan “having identified a strong demand of

Japanese customers for the Sephora concept” Howard Mietimer, CEO Sephora Americas-Asia-Pacific, in Le Japon à la

Page, June 2000

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

37

mass products and gave none of the advice Japanese women are accustomed to39. Moreover its

Ginza flagship store was organized contrary to the Japanese market: fragrances –that represent a

very small market in Japan- were on the ground floor, cosmetics on the first floor and skin-care –a

very important Japanese market- were relegated on the second floor.

• Error n°2: Consider Sephora as a Luxury Brand, and therefore move into the same prime

locations. Sephora retails luxury brands among others: one of its focuses is innovative or niche

cosmetics brands for instance. Moreover fragrances & cosmetics are, as we have seen, an entry

point to luxury brands for customers that are not familiar with luxury. This would normally mean

that most stores should be where luxury brand stores are NOT.

Japan stores were opened in Ginza and Shibuya, the traditional Luxury Brands areas where rents

are phenomenal. Some US stores were opened in similar locations: 5th Avenue (21,000 sq.ft.), Soho

(9,000 sq.ft.), Flatiron (8,400 sq. ft.), San Francisco Union Square (16,500 sq.ft.), Chicago Michigan

Avenue, Miami Beach, Las Vegas (one 10,000 sq.ft. & one 6,000 sq. ft.), etc. This means very high

rents for very big stores and little chances to see profitability, given that Sephora is a retailer and

that it shares the margin with the brands40.

Bernard Arnault himself acknowledged: “In the US we have modified our approach: the stores that have

opened since December 2000, are smaller, have smaller rents and are already profitable. Growth in those

stores is above 20%”41.

• Error n°3: Forget the “Cathedral Concept” for its flagship stores. The 5th Avenue store, when it

opened in 1999, came as a shock: it had nothing to do with the original concept. First there was a

door to open; behind it was a person that helped you open it: the open access had been discarded.

Then you were forced to move along a given path, along conveyor beltways that led you through

three levels. There was no roaming around, no easy access throughout a unique level to products

in different areas: the cathedral had been replaced by a maze. The magic was gone and the store

39 Most major fragrance and cosmetics brands had preferred not to be sold at Sephora, because they thought the

open sell concept would be in contradiction with their luxury positioning.

40 “Q: What profit margins are you expecting in retailing?

A: We have set a target for our travel retail of 10% by 2002. Globally, we expect Sephora to be 7% to 10%. We're

looking for an operating profit in the third year [after each Sephora store opens].” Myron Ullmann, Business Week

Online, December 11 2000. This is far from the Luxury Brands margins. The New York stores are said to have sales

of $1000/sq.ft. and smaller stores of $500 per sq.ft.

41 Le Monde, March 9 2002. The 1999 LVMH Annual Report was already stating : « Sephora will improve its

profitability, its fast growth generating more and more economies of scale and its accumulated international

experience should make new openings more and more successful”. Profitability is now scheduled for 2003.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

38

was empty.

As a result another store was opened in 2001, in Times Square, which mirrors the Paris flagship

store in all details (even the architect, Gérard Barrau is the same).

The problem here is a classic one: how can we transfer a concept into a different format, i.e. a

single level Cathedral into a multi-level store? Sephora still has not found the answer.

• Error n°4: Selling cosmetics needs some assistance. Basically Sephora is a Fragrance retail concept

and they have made a huge success of it. Their approach to cosmetics and skin-care is not as

successful. They have not created a really innovative retail concept there and customers notice it:

“Thus my initial exposure to Sephora was through my local mall, and while the store was interesting to

visit, I did not consider it anything too special. The usually teenaged staff could not provide much help

regarding the profusion of products on sale. For actual purchases, I continued to traipse over to Nordstrom

and my favorite Prescriptives sales associate, who was always knowledgeable and helpful regarding various

cosmetics lines. But what's a girl to do when she is in an unfamiliar city with no favorite sales associates in

sight? Check out Sephora, of course”, says an American customer on her website42. The problem lies

also with the cosmetics brands that have not worked hand in hand with Sephora to deliver this

innovative concept that would have the customer buy, buy, buy.

42 http://www.thenetnet.com/lookatme/beauty2b.html. Check out alt.fashion for similar messages.

3CADB61E-3CA8-CD64.doc

Michel Gutsatz

39

Balancing Distribution Channels to achieve visibility

In all product categories multibrand retailers exist that once were the natural outlet for luxury brands.

At their beginnings these mostly had a handful of flagship stores in major cities and relied on two

channels to distribute their products: independent retailers and department stores. This is the

wholesale trade that is critical for brand development. Two cases are instructive, Gucci and Bulgari.

The differences seen here depend mostly on the different core businesses of these brands: there are

numerous luxury watch retailers –one of Bulgari’s core businesses- that the company can tap to

distribute their products. No equivalent distribution exists in other product lines (save eyewear and

fragrances).

• Bulgari’s strategy has been to grow primarily its wholesale business, which now represents

43% of its sales (vs. 54% for its stores –both company operated and franchisees): the number of

watch retailers was multiplied by 10 between 1993 and 2000 when the company operated

stores were only multiplied by 443. Interestingly the sales per Bulgari company operated store

are decreasing: they have gone down from $3 900 in 1993 to $2 700 in 2000. Of course opening

stores will drive your sales but there is a limit to store growth: store profitability.

• Gucci’s strategy is different: they had a very sound base of 64 stores in 1990 – to which had to

be added the “ the historical distribution network”, that is the department stores, duty-free

locations and franchisees. It was only in 1997 and 1998 that the network of company operated

stores was grown significantly to 83 and then 126 stores, both by buying back franchisees and

by opening new stores44. Since then openings and buying back franchisees has brought the