Chapter 7 Costing and Pricing Strategies Check for updates on the w eb now! Click anywhere on the slide to view the next item on the slide or to advance to the next slide. Use the buttons below to navigate to another page, close the presentation or open the help page.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Chapter 7Costing and Pricing Strategies

Check for updates on the web now!

Click anywhere on the slide to view the next item on the slide or to

advance to the next slide. Use the buttons below to navigate to

another page, close the presentation or open the help page.

Chapter 7Costing and Pricing Strategies

2

Net Income

• Equals excess of revenues earned over related costs incurred for an accounting period

• Prime determinant of success• Total sales for a period determine revenue• Related costs determine profit or loss

Chapter 7Costing and Pricing Strategies

3

Mark Up and Margin

• Gross margin (GM)• Gross margin return on inventory (GMROI)• Adjusted gross margin (AGM)• Maintained (margin) markup• Required departmental markup

Chapter 7Costing and Pricing Strategies

4

Pricing

• Establish wholesale selling price for each garment• Responsibility of merchandiser• Requires accurate cost calculation

Chapter 7Costing and Pricing Strategies

5

Costing

• Calculate associated c osts for each style

• Responsibility of merchandiser

• P roduct costing is one of the most important

planning functions for garment company

Chapter 7Costing and Pricing Strategies

6

Financial Responsibility• Merchandiser Responsibilities

– Develop line– Adopt styles– Meet market objectives– Forecast sales– Sourcing– Control inventory– Mark downs– Dispose of excess inventory– Achieve target profit or gross margin

• Product Managers Responsibilities– Develop line– Adopt styles– Meet market objectives– Forecast sales– Control inventory– Achieve target profit or gross margin

Chapter 7Costing and Pricing Strategies

7

Pricing Formula

• Cost of goods + markup = W holesale selling pric

e• M aterials + direct labor

+ factory overhead = Co st of goods

• M arketing and selling co sts + product developm ent costs + distribution

costs + general and ad ministrative costs + prof

it = Markup (gross profit margin)

Chapter 7Costing and Pricing Strategies

8

Markup

• Can be represented as percent of wholesale sellin g price– Sales commission based upon % of selling price– Profit is planned as % of sales– Marketing, product development, distribution, and gener

al and administrative costs are budgeted items that can b e expressed as % of sales

Chapter 7Costing and Pricing Strategies

9

Wholesale Selling Price

• Price manufacturer charges the retailer or wholesaler for each garment style

• Wholesale “net” selling price includes discounts in payment terms (e.g., 8/10 net 30)

• Delay payment or “dating”

Chapter 7Costing and Pricing Strategies

10

Retail Selling Price

• Product managers establish retail selling price based on the needs of their consumers

• Product managers work backward to determine target materials and labor costs based on the established selling price and the required margin

Chapter 7Costing and Pricing Strategies

11

Shortcut

• Cost of goods divided by the reciprocal o f markup equals wholesale selling price

Chapter 7Costing and Pricing Strategies

12

Example

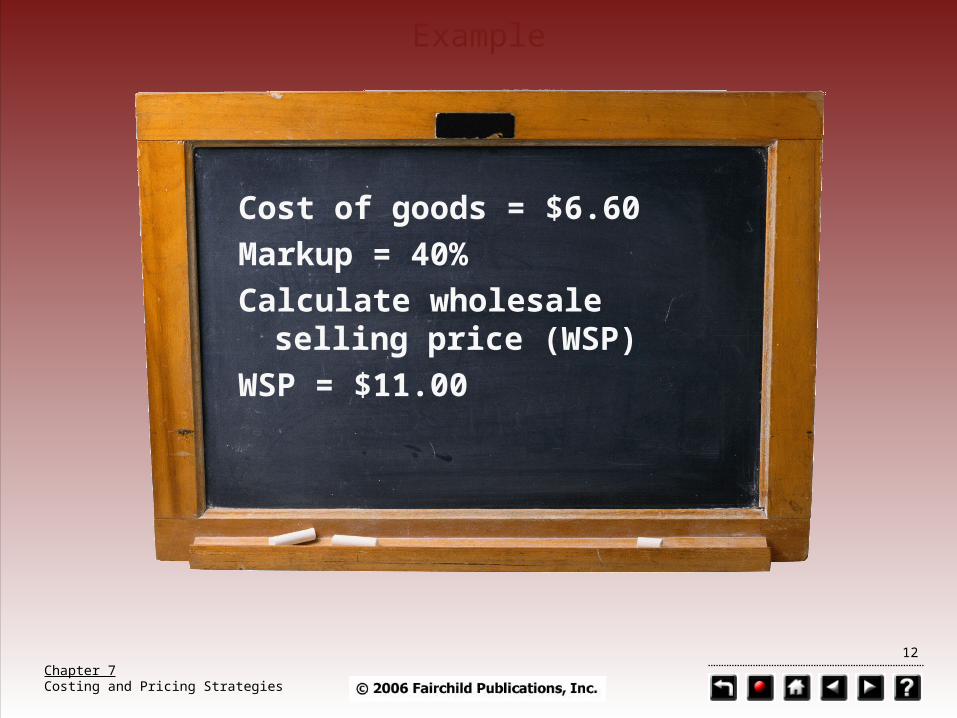

Cost of goods = $6.60Markup = 40%Calculate wholesale

selling price (WSP)WSP = $11.00

Chapter 7Costing and Pricing Strategies

13

Pricing Rule

• No matter how pricing formula is adjusted to accommodate different manufacturing methods, sales discounts, and company structures, it must ALWAYS cover all costs generated within company

• Costs not covered in formula result in reduced profit or financial loss

Chapter 7Costing and Pricing Strategies

14

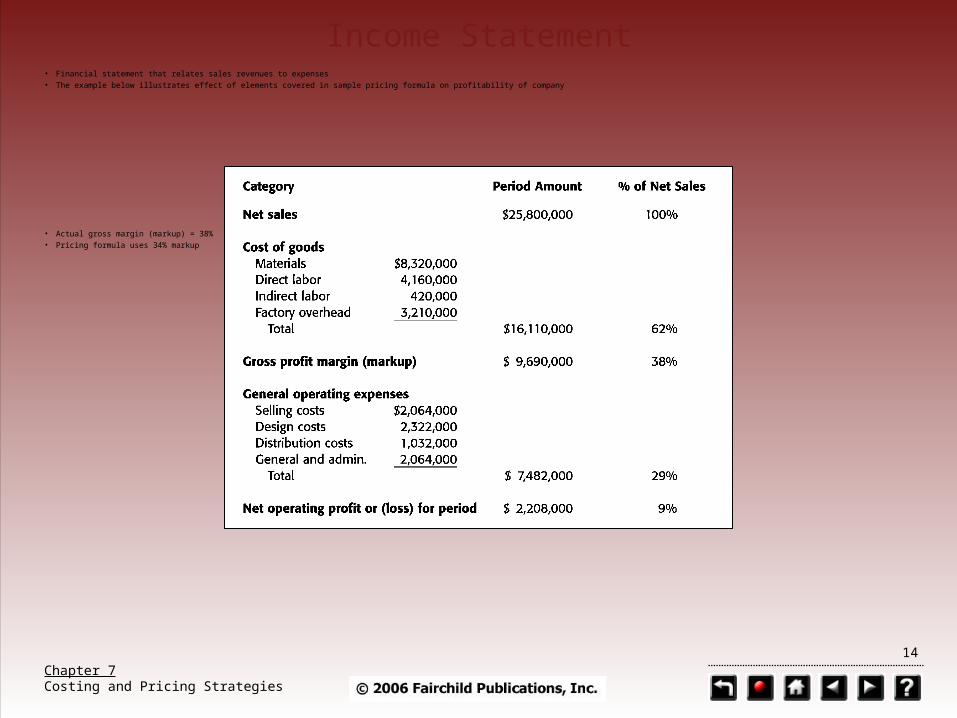

Income Statement• Financial statement that relates sales revenues to expenses• The example below illustrates effect of elements covered in sample pricing formula on profitability of company

• Actual gross margin (markup) = 38%• Pricing formula uses 34% markup

Chapter 7Costing and Pricing Strategies

15

Pricing Strategies

• Pricing is a calculation and determination of wholes ale selling prices

• Calculation is objective• Determination is subjective• Product managers must also consider these factors

Chapter 7Costing and Pricing Strategies

16

Rigid Calculation

• Price is based on rigid calculation similar to Figures 7.1 and 7.2

• Assumes all cost data and sales expectations will be consistent with estimates used to develop:– Variable direct labor and materials costs– Variable and fixed factory overhead– Variable and fixed costs included in markup

• Process adequate for basic styles

Chapter 7Costing and Pricing Strategies

17

Subjective Pricing

• Pricing according to what the market will bear• Allows merchandiser to evaluate:

– Current selling prices of similar competitive styles– Uniqueness of style– Current value of brand name– - Advertising plans (pull through marketing)– Effect of price on potential sales volume– Current market trends– Gross profit to sales volume

Chapter 7Costing and Pricing Strategies

18

Subjective Pricing cont.

• Calculate price using pricing formula• Adjust price up or down depending on market con

ditions– Adjusting price upward could increase earned markup an

d potential profits– Adjusting price downward could increase sales and absor

b more fixed costs and increase potential profits

Chapter 7Costing and Pricing Strategies

19

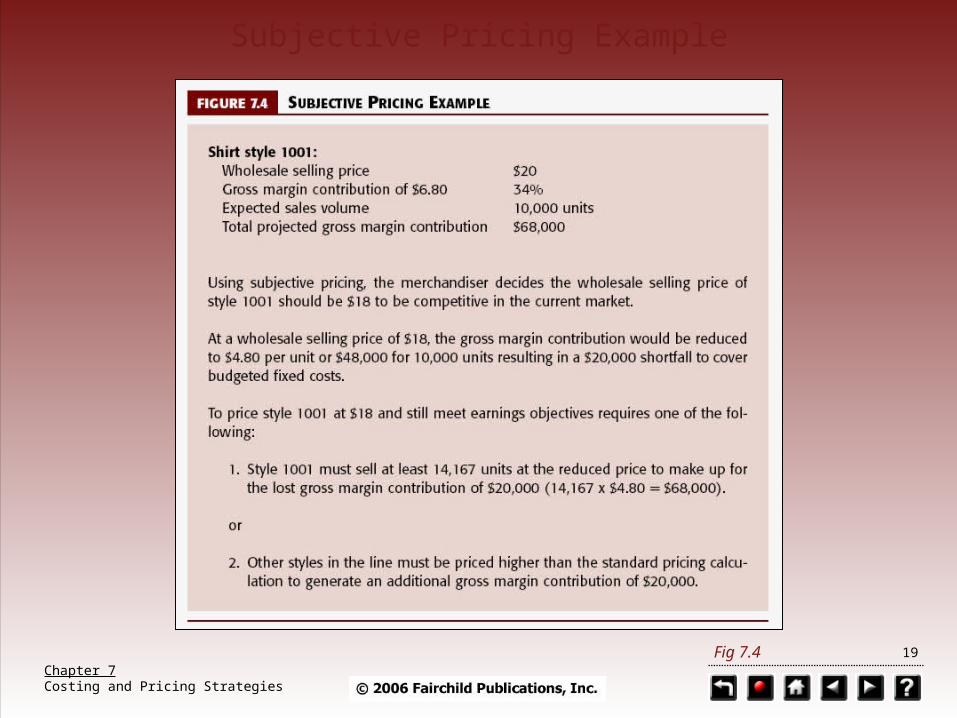

Subjective Pricing Example

Fig 7.4

Chapter 7Costing and Pricing Strategies

20

Subjective Pricing Errors

• Reduced sales if price higher than what market can bear• Decreased markup if lower price does not result in expected incr

ease in sales• Risky practice when used by inexperienced merchandisers• Product managers must consider these factors when

establishing retail prices

Chapter 7Costing and Pricing Strategies

21

Costing Principles

• Pricing strategies can only be effective if cost bases are accurate

• Requires precise accumulation and allocation of all c osts reported in company’s financial statements

Chapter 7Costing and Pricing Strategies

22

Cost of Goods

• Includes a ll expenses involved in the manufacture of an apparel product

– materials– direct labor– factory overhead

Chapter 7Costing and Pricing Strategies

23

Direct Materials

• Fabric, thread, trim, and findings• Quantities must be accurately measured• Prototyping• Cutting marker (company size scale)• All other materials measured in units, sets, or yards/

meters

Chapter 7Costing and Pricing Strategies

24

Direct Labor

• Those costs that involve change the condition or physical appearance of raw materials

• Examples: Cutting, bundling, folding, sewing, and finishing• Labor standards (SAMs)

Chapter 7Costing and Pricing Strategies

25

SAMs

• The time required for an average operator, fully qualified and trained and working at a normal pace, to perform the operation

• Include allowances for personal time, fatigue, and normally expected work delays (PF&D)

Chapter 7Costing and Pricing Strategies

26

Direct Labor Example

Operation calculated to take .86 SAMs per unit to complete

Earnings objective is $6.00 per hourDirect labor cost is $0.086/unit

($6/hr. ÷ 60min./hr. = $0.10/min. x .86 min./unit = $0.086/unit)

Chapter 7Costing and Pricing Strategies

27

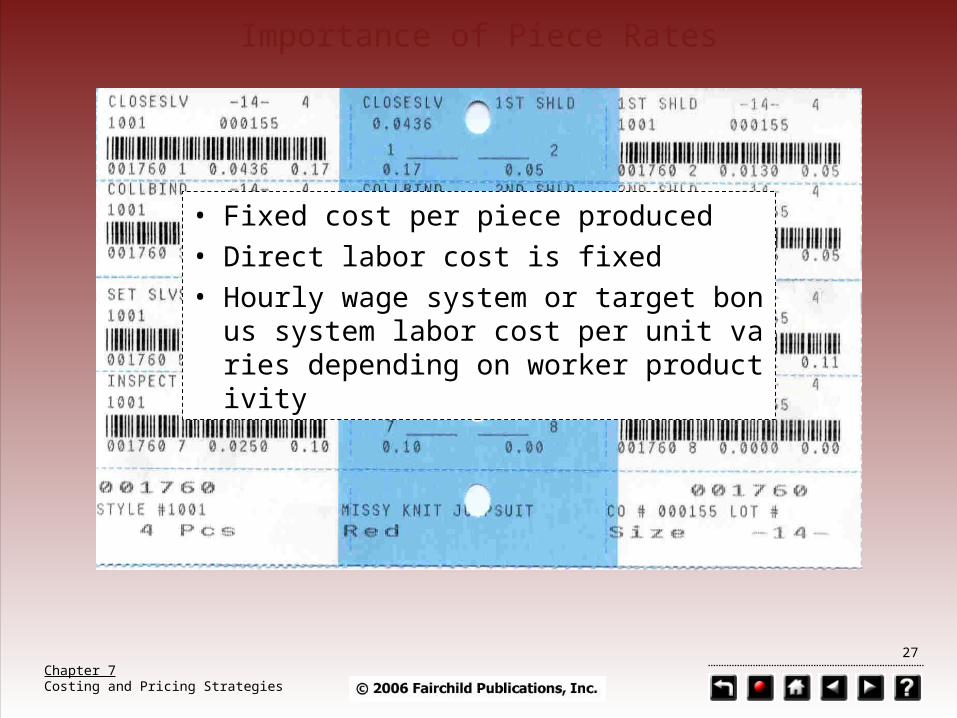

Importance of Piece Rates

• Fixed cost per piece produced• Direct labor cost is fixed• Hourly wage system or target bonu

s system labor cost per unit varies d epending on worker productivity

Chapter 7Costing and Pricing Strategies

28

- Off standard Costs

• - Adjustments must be made for off standard manufa cturing time

– Operator training– Machine down time– Waiting for work– Overtime premium

Chapter 7Costing and Pricing Strategies

29

Manufacturing Overhead

• A ll costs of manufacturing except direct materials and direct labor

• Variable costs– Machine oil– Sewing needles– Portion of power– Machine parts

• Fixed costs– Property Taxes– Depreciation of factory facilities– Building maintenance– Light– Heat– Indirect labor (supervision and bundle handlers)

Chapter 7Costing and Pricing Strategies

30

General Operating Expenses

• All costs over and above costs included in total cos t of goods

• Marketing and selling expenses• Product development expenses• Distribution expenses• Administrative expenses

Chapter 7Costing and Pricing Strategies

31

Costing Strategies

• Information to identify, measure, and allocate costs• Based on cost accounting policies

Chapter 7Costing and Pricing Strategies

32

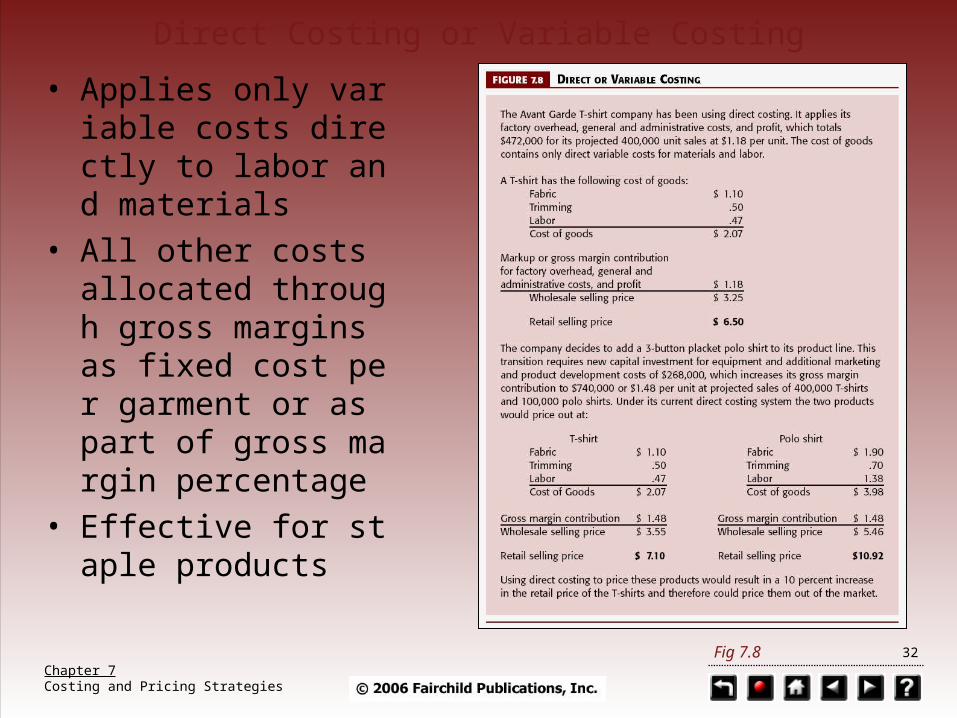

Direct Costing or Variable Costing

• Applies only variabl e costs directly to l

abor and materials• All other costs alloc

ated through gross margins as fixed co

st per garment or a s part of gross mar

gin percentage• Effective for staple

products

Fig 7.8

Chapter 7Costing and Pricing Strategies

33

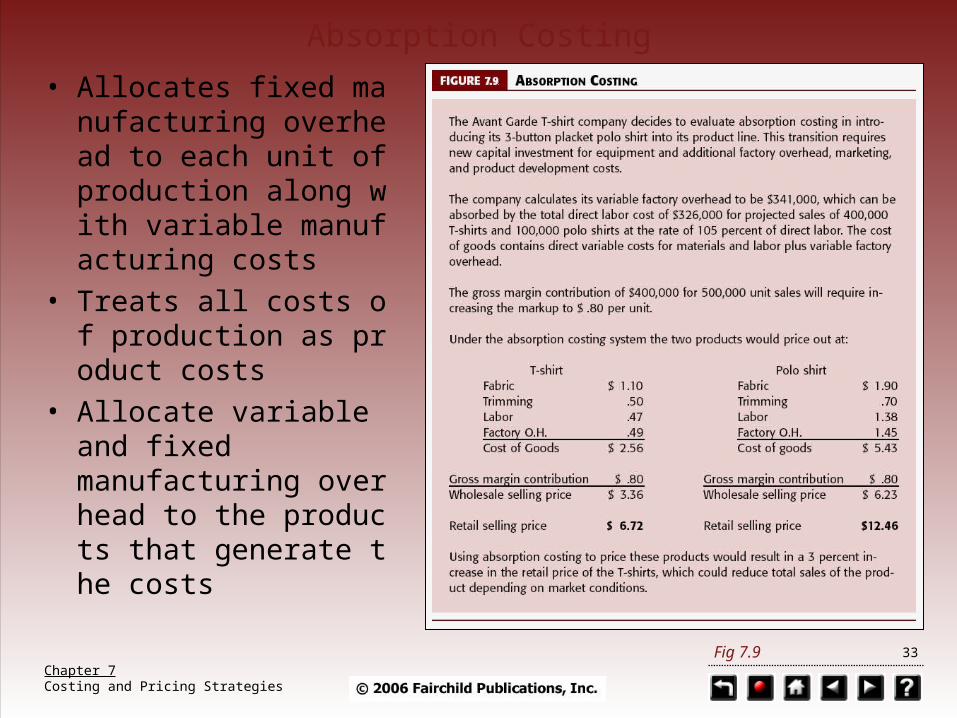

Absorption Costing

• Allocates fixed man ufacturing overhea

d to each unit of pro duction along with v

ariable manufacturi ng costs

• Treats all costs of pr oduction as product

costs• Allocate variable an

d fixedmanufacturing over

head to the product s that generate the

costsFig 7.9

Chapter 7Costing and Pricing Strategies

34

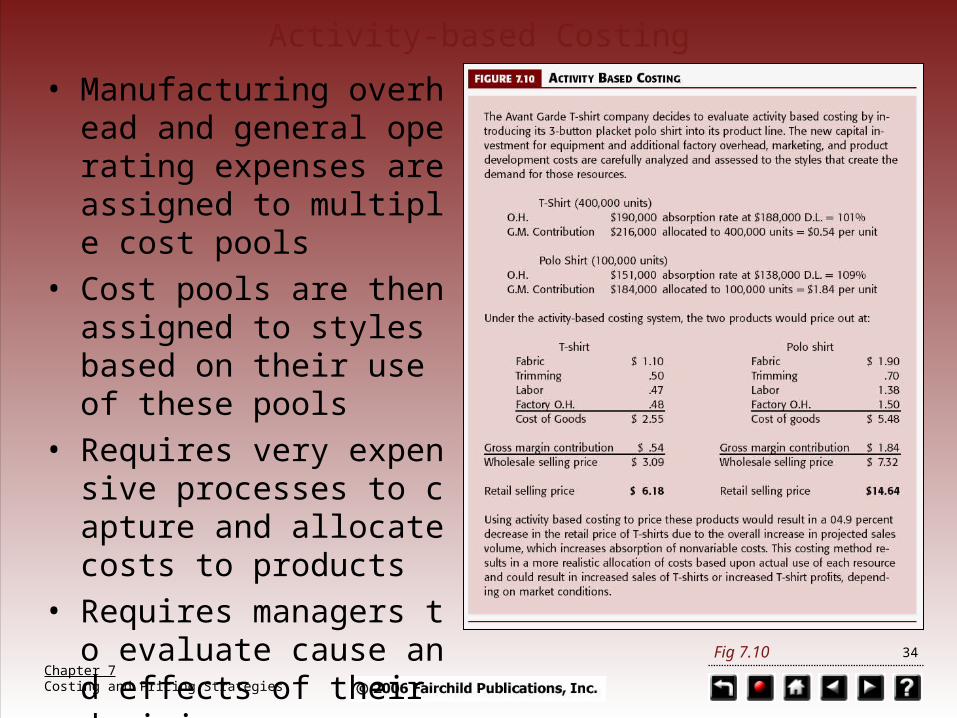

- Activity based Costing

• Manufacturing overhe ad and general operati ng expenses are assig

ned to multiple cost pools

• Cost pools are then as signed to styles based

on their use of these pools

• Requires very expensi ve processes to captur

e and allocate costs toproducts

• Requires manager s to evaluate cause and eff

ects of their decisionsFig 7.10

Chapter 7Costing and Pricing Strategies

35

Levels of Costing

• Quickie Costing (estimating)• Costing for Sale (calculating)• Production Costing (monitoring)• Accounting Costing (reporting)

Chapter 7Costing and Pricing Strategies

36

Quick Costing (Pre-Cost)

• Within +/- 10%• Used to evaluate style alternatives• Use standardized cost data, previous cost

sheets, approximate fabric requirements• Eliminates styles with little chance of

adoption because of pricing parameters

Chapter 7Costing and Pricing Strategies

37

Costing for Sale

• Accurate calculations for adoption and final pricing

• Based on actual sample• Fabric requirements based on test

marker of all sizes, actual fabric widths, completed pattern sets

• Labor costs from predetermined time standards or proven piece rates

• Product engineering might take place to lower costs

Chapter 7Costing and Pricing Strategies

38

Production Costing

• Actual variable manufacturing expenses for material and labor only

• Actual material used including waste, re-cuts, rejects, and transportation cost

• Adjusted piece rates are used from any calculated standards

• Off-standard manufacturing costs are used to adjust overhead rates

• Purpose is to validate and adjust current cost data

Chapter 7Costing and Pricing Strategies

39

Accounting Costing

• Used to create financial statements• Basis for evaluating profit and loss

statements• Measures CGS, variable and fixed

manufacturing overhead, fixed and variable general operating overhead

End Chapter 7

Chapter 7Costing and Pricing Strategies

41

System Requirements:

Windows® 98, SE, 2000, ME, XP, or NT 4.0 Service Pack 4 and up Microsoft PowerPoint® 97, 2000, 2002, XP, 2003 or PowerPoint®

Viewer 2003Pentium II Minimum, Pentium III Recommended 72 MB of hard disk space 64 MB of RAM minimum 128 MB of RAM recommendedSuper VGA (800 × 600) or higher resolution monitor

Macro Security:

The macros contained in this presentation will not run unless the security settings in PowerPoint are set to “Low”. To change security settings do the following:

1. Open PowerPoint2. From the top menu panel select “Tools”3. From the dropdown menu select “Macro”4. From the Macro menu select “Security”5. A tabbed dialog box appears, select the “Security Settings” tab6. Select “Low”7. Click “OK”

When you are finished viewing the presentation remember to reset your Macro Security Level.

Support:

Email: [email protected] Phone: 267-808-4816 9am–5pm Eastern Standard Time

Help and Support

Go to the Help Slide

Go to the Next Slide

Go to the Previous Slide

Go to the Table of Contents Slide

End Presentation

Go to Last Slide Viewed

Related Documents