RECEIVABLES AND INVENTORY CHAPTER 6 1

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

RECEIVABLES AND INVENTORY

CHAPTER 6

2

ICLICKER: BELL RINGER

CTE specializes in engine repair & reconditioning of yard machines. CTE overhauls the engine on a riding lawnmower for a client and bills them $1,600 on account. What is the effect of this transaction on CTE?

B. Accounts Receivable increases by $1,600

Sales Revenue (and Retained Earnings) increases by $1,600

★ What happens when the customer doesn’t pay?

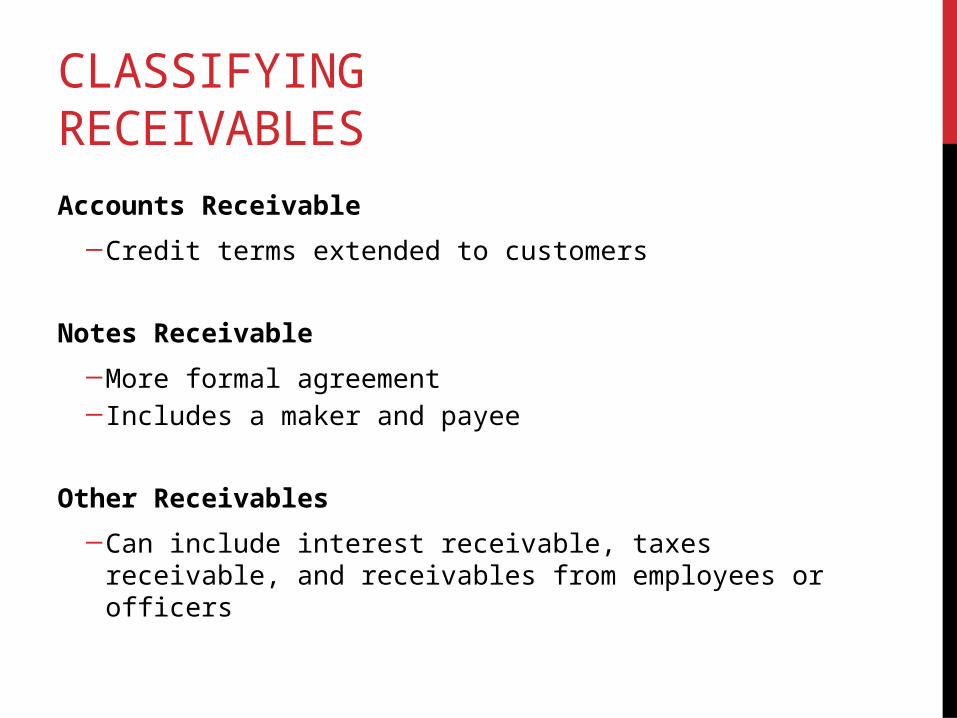

CLASSIFYING RECEIVABLES

Accounts Receivable

─Credit terms extended to customers

Notes Receivable

─More formal agreement─Includes a maker and payee

Other Receivables

─Can include interest receivable, taxes receivable, and receivables from employees or officers

ACCOUNTING FOR NOTES RECEIVABLE

5

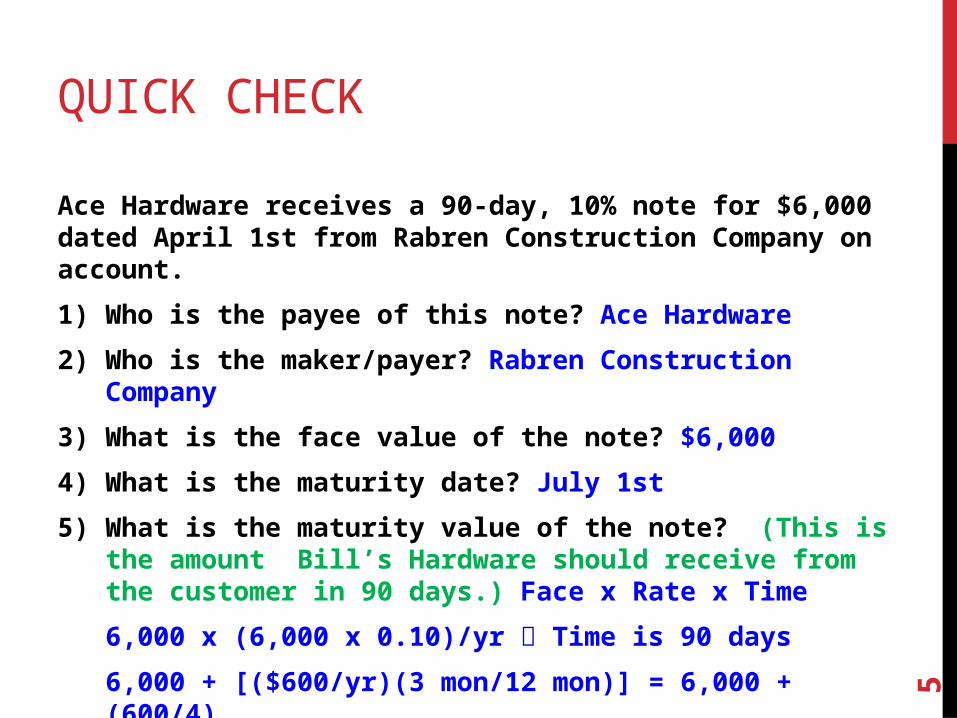

QUICK CHECK

Ace Hardware receives a 90-day, 10% note for $6,000 dated April 1st from Rabren Construction Company on account.

1) Who is the payee of this note? Ace Hardware

2) Who is the maker/payer? Rabren Construction Company

3) What is the face value of the note? $6,000

4) What is the maturity date? July 1st

5) What is the maturity value of the note? (This is the amount Bill’s Hardware should receive from the customer in 90 days.) Face x Rate x Time

6,000 x (6,000 x 0.10)/yr Time is 90 days

6,000 + [($600/yr)(3 mon/12 mon)] = 6,000 + (600/4)

= $6,150

6

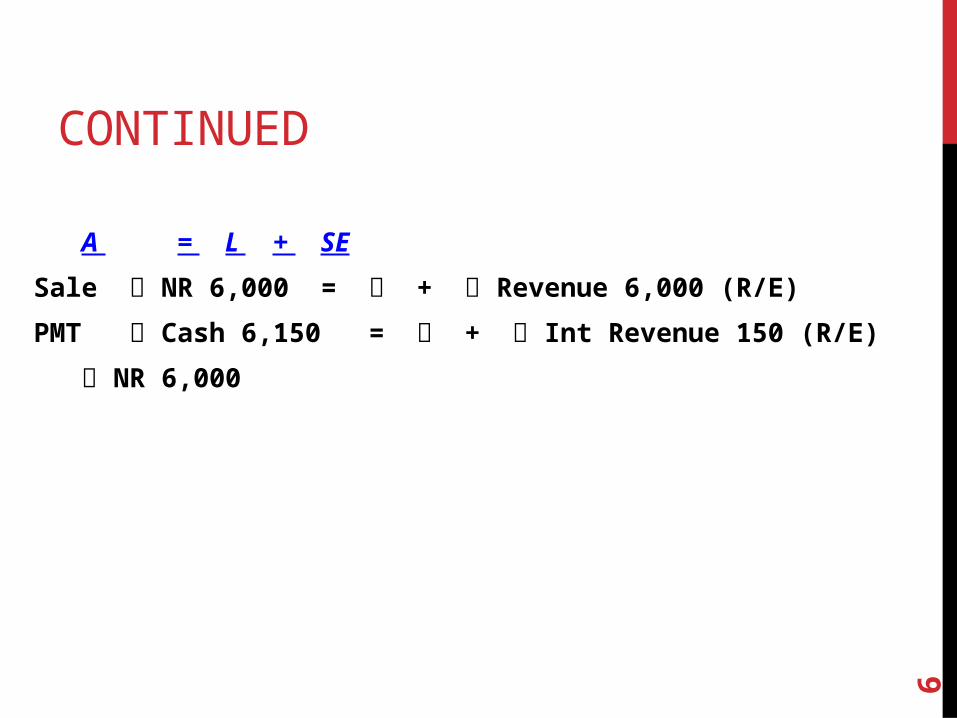

CONTINUED

A = L + SE

Sale NR 6,000 = + Revenue 6,000 (R/E)

PMT Cash 6,150 = + Int Revenue 150 (R/E)

NR 6,000

7

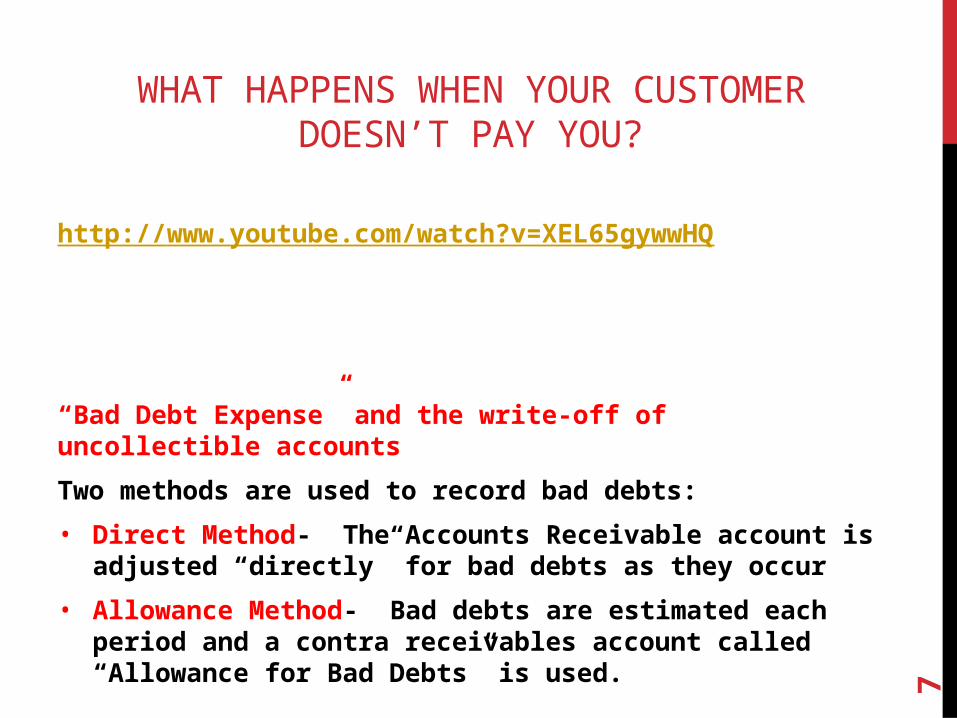

WHAT HAPPENS WHEN YOUR CUSTOMER DOESN’T PAY YOU?

http://www.youtube.com/watch?v=XEL65gywwHQ

“Bad Debt Expense” and the write-off of uncollectible accounts

Two methods are used to record bad debts:

• Direct Method- The Accounts Receivable account is adjusted “directly” for bad debts as they occur

• Allowance Method- Bad debts are estimated each period and a contra receivables account called “Allowance for Bad Debts” is used.

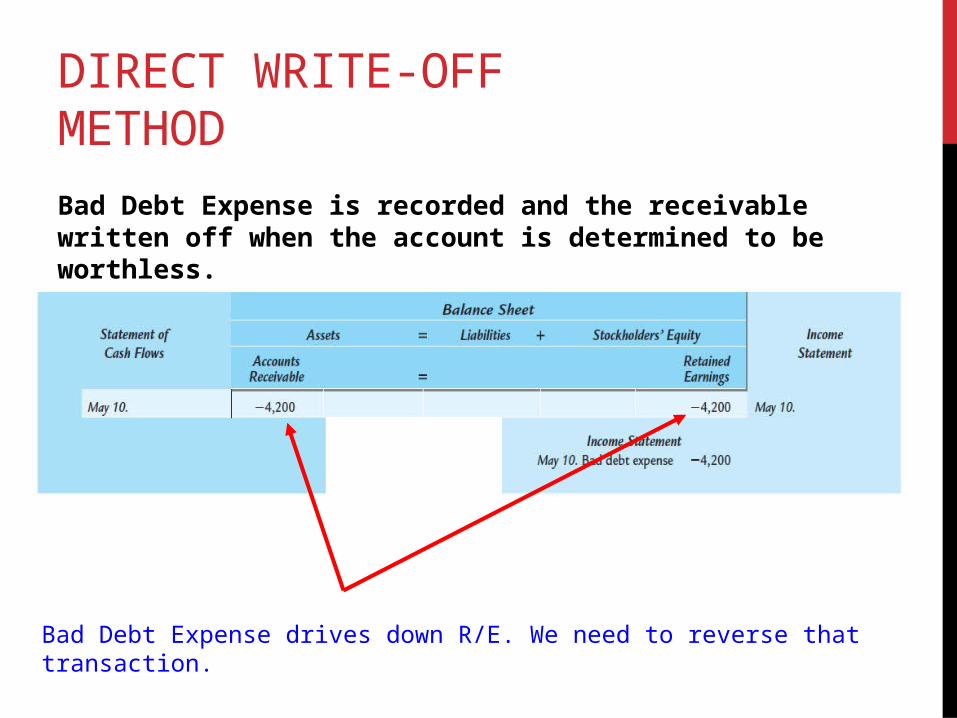

DIRECT WRITE-OFF METHOD

Bad Debt Expense is recorded and the receivable written off when the account is determined to be worthless.

Bad Debt Expense drives down R/E. We need to reverse that transaction.

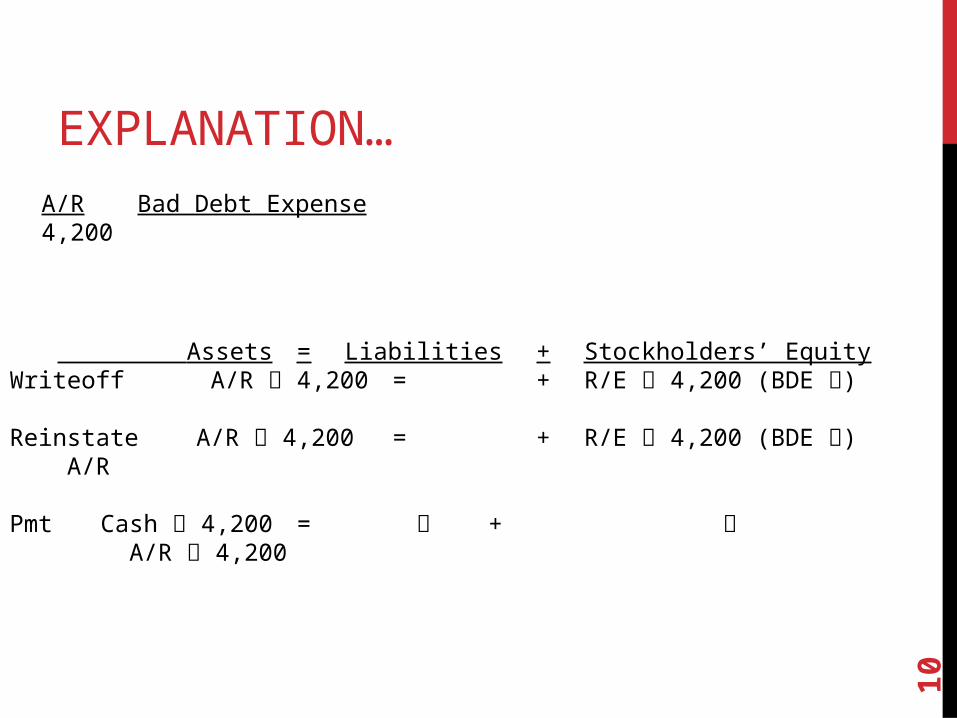

IF PAYMENT IS COLLECTED AFTER THE WRITE-OFF, THE WRITE-OFF ENTRY IS REVERSED AND THE CASH COLLECTION IS RECORDED

Undo transaction Reverse transaction to get our A/R back on the book

10

EXPLANATION…A/R Bad Debt Expense4,200

Assets = Liabilities + Stockholders’ EquityWriteoff A/R 4,200 = + R/E 4,200 (BDE )

Reinstate A/R 4,200 = + R/E 4,200 (BDE ) A/R

Pmt Cash 4,200 = + A/R 4,200

11

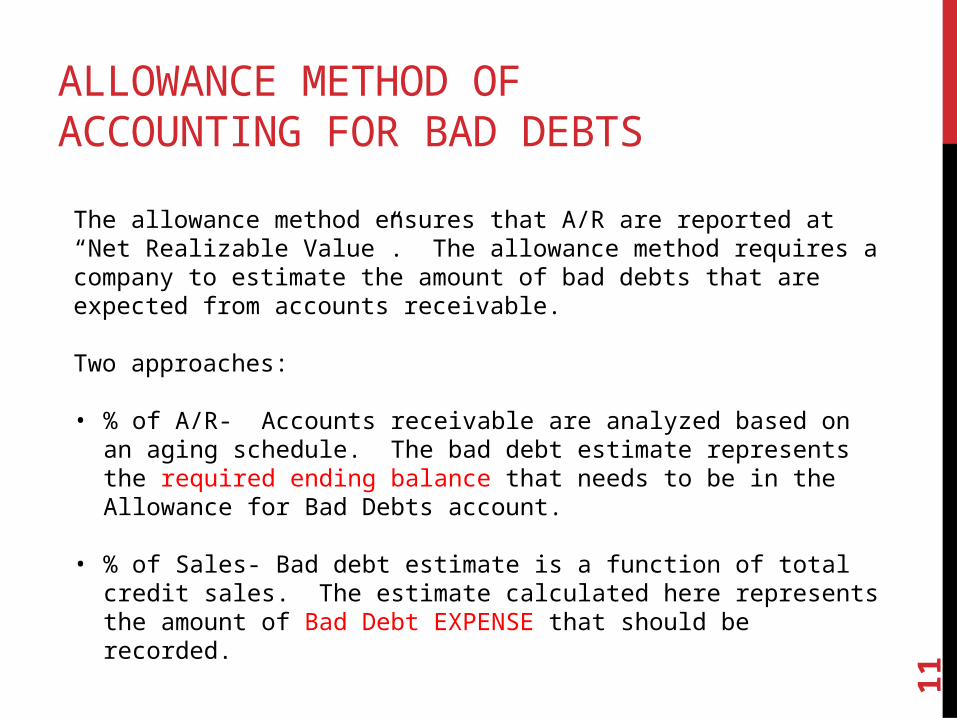

ALLOWANCE METHOD OF ACCOUNTING FOR BAD DEBTS

The allowance method ensures that A/R are reported at “Net Realizable Value”. The allowance method requires a company to estimate the amount of bad debts that are expected from accounts receivable.

Two approaches:

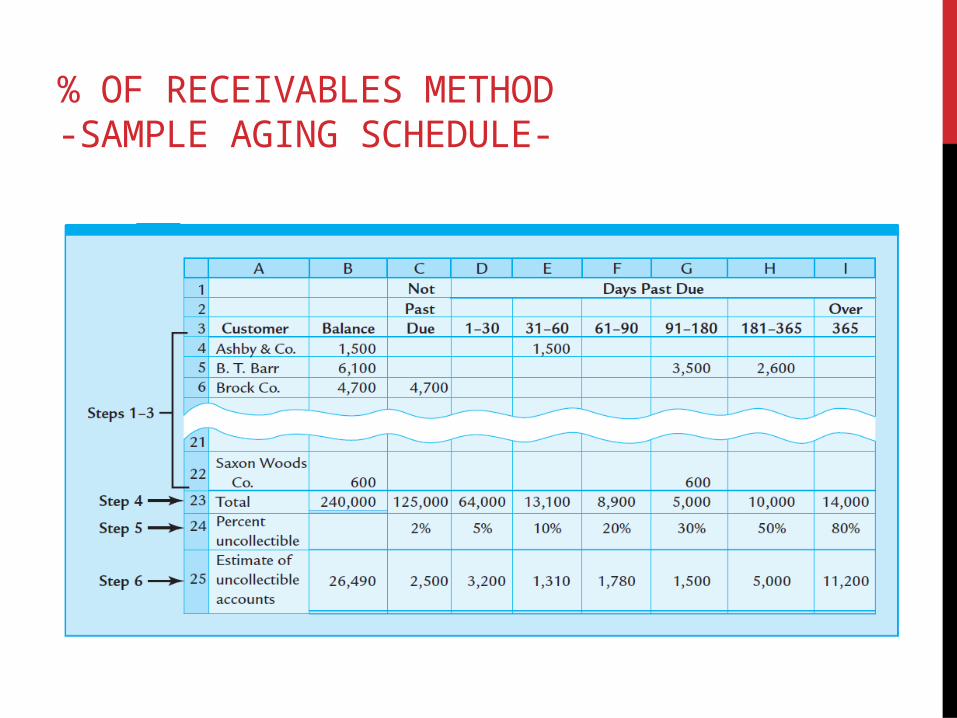

• % of A/R- Accounts receivable are analyzed based on an aging schedule. The bad debt estimate represents the required ending balance that needs to be in the Allowance for Bad Debts account.

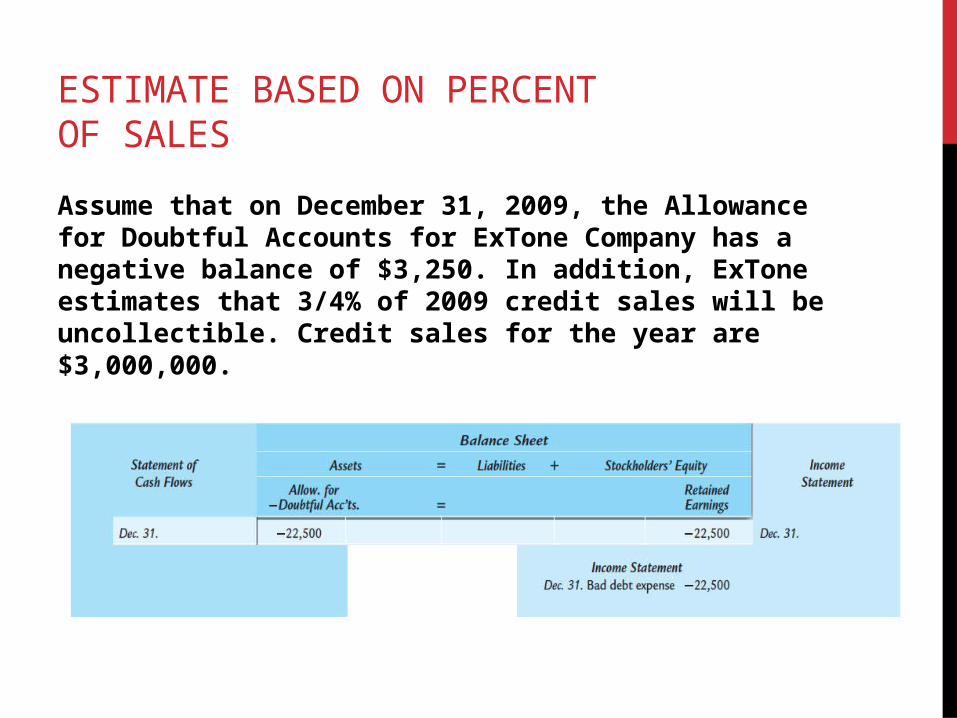

• % of Sales- Bad debt estimate is a function of total credit sales. The estimate calculated here represents the amount of Bad Debt EXPENSE that should be recorded.

12

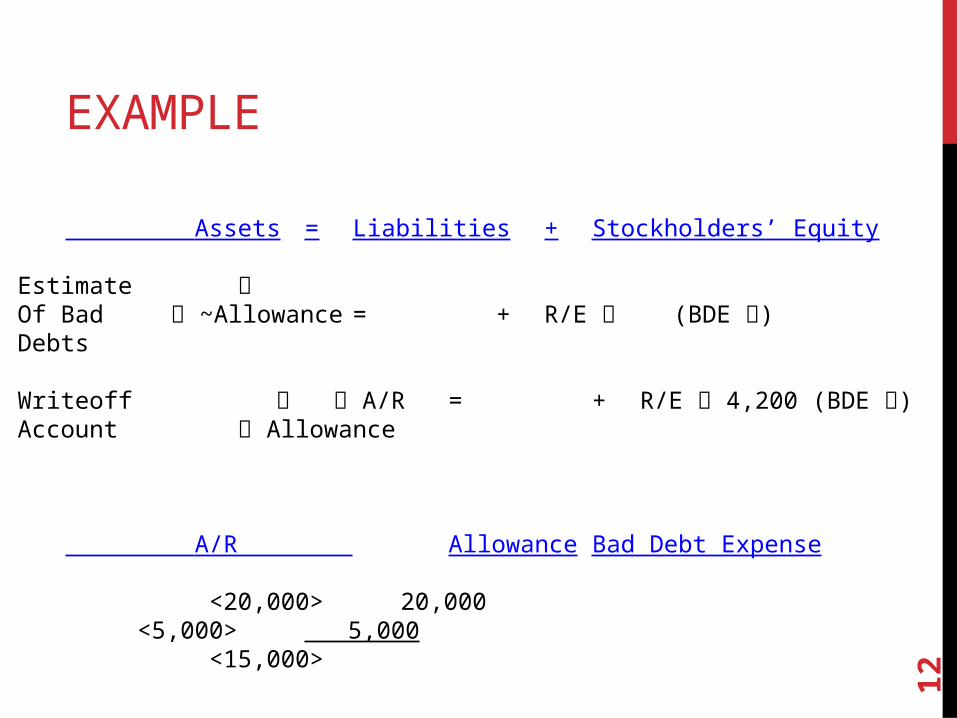

EXAMPLE

Assets = Liabilities + Stockholders’ Equity

Estimate Of Bad ~Allowance = + R/E (BDE )Debts

Writeoff A/R = + R/E 4,200 (BDE )Account Allowance

A/R Allowance Bad Debt Expense

<20,000> 20,000 <5,000> 5,000

<15,000>

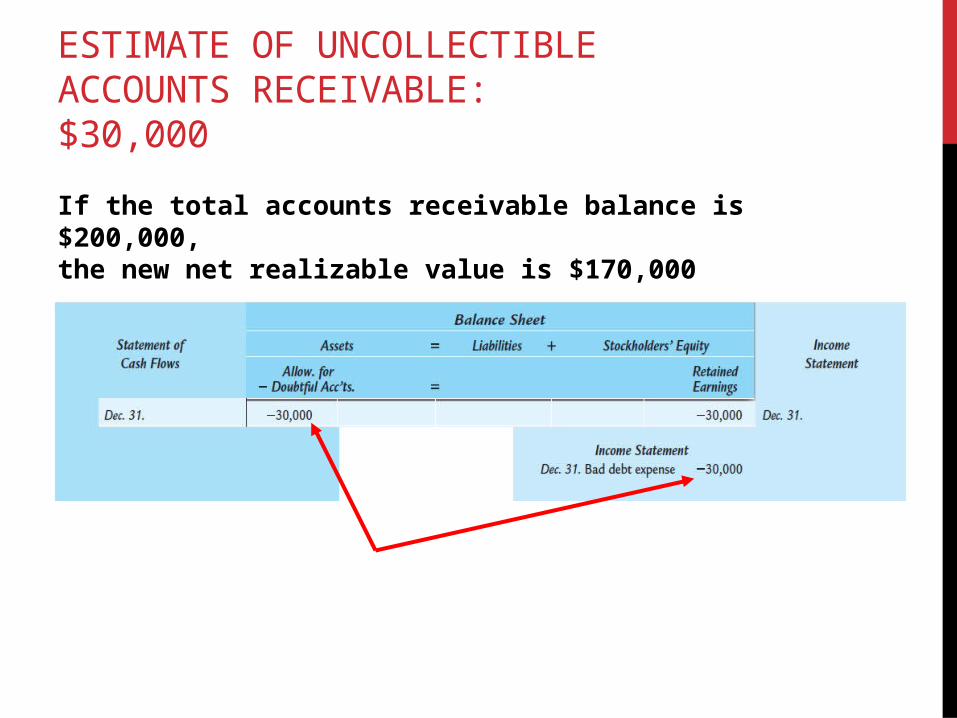

ESTIMATE OF UNCOLLECTIBLE ACCOUNTS RECEIVABLE: $30,000

If the total accounts receivable balance is $200,000, the new net realizable value is $170,000

WRITE-OFFS TO THE ALLOWANCE ACCOUNT

When a customer’s account is identified as uncollectible, it is written off against the allowance account

IF PAYMENT IS COLLECTED AFTER THE WRITE-OFF, THE WRITE-OFF ENTRY IS REVERSED AND THE CASH COLLECTION IS RECORDED.

Assume a $5,000 account had been previously written off.

% OF RECEIVABLES METHOD-SAMPLE AGING SCHEDULE-

ESTIMATE BASED ON ANALYSIS OF RECEIVABLES

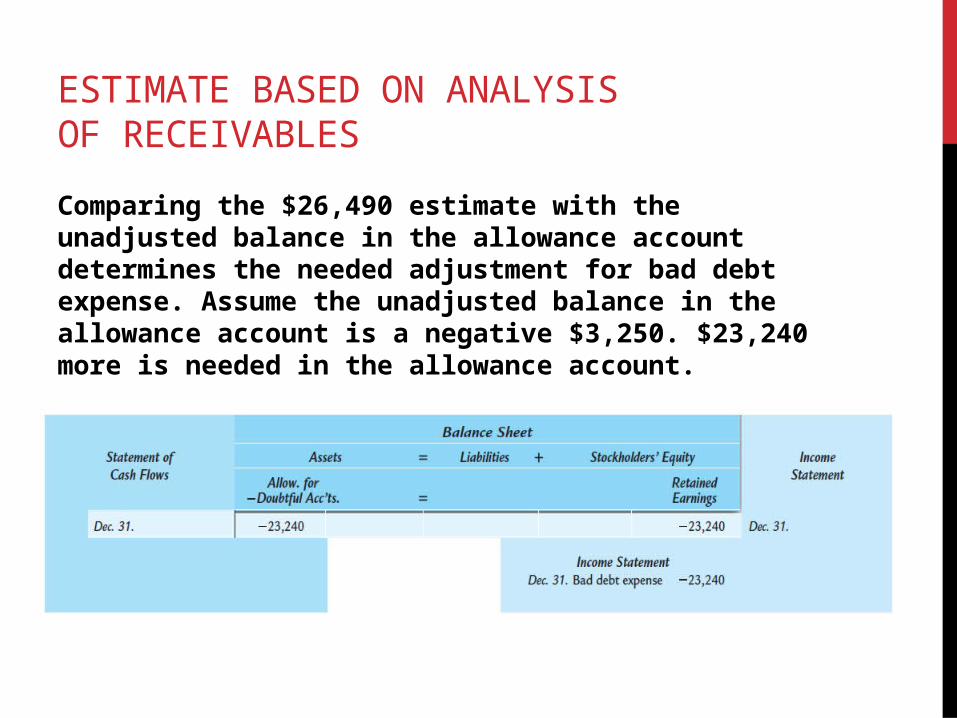

Comparing the $26,490 estimate with the unadjusted balance in the allowance account determines the needed adjustment for bad debt expense. Assume the unadjusted balance in the allowance account is a negative $3,250. $23,240 more is needed in the allowance account.

ESTIMATE BASED ON PERCENT OF SALES

Assume that on December 31, 2009, the Allowance for Doubtful Accounts for ExTone Company has a negative balance of $3,250. In addition, ExTone estimates that 3/4% of 2009 credit sales will be uncollectible. Credit sales for the year are $3,000,000.

19

ICLICKER: BELL RINGER

1. Allowance for Doubtful Accounts has an unadjusted balance of $1,100 at the end of the year, and an aging analysis of customers’ accounts indicates doubtful accounts of $12,900. Which of the following records the proper provision for doubtful accounts?

D. Increase Uncollectible Accounts Expense, $11,800; increases Allowance for Doubtful Accounts, $11,800

20

ICLICKER: BELL RINGER (CONT.)

2. Allowance for Doubtful Accounts has an unadjusted balance of $500 at the end of the year, and uncollectible accounts expense is estimated at 1% of net sales. If net sales are $950,000, the amount of the adjustment to record the provision for doubtful accounts is

A. $9,500

CLASSIFICATION OF INVENTORIESMerchandisers-• One classification - “Merchandise inventory”

• Cost of inventory includes all costs of ownership

• purchase price• transportation costs• insurance costs, etc.

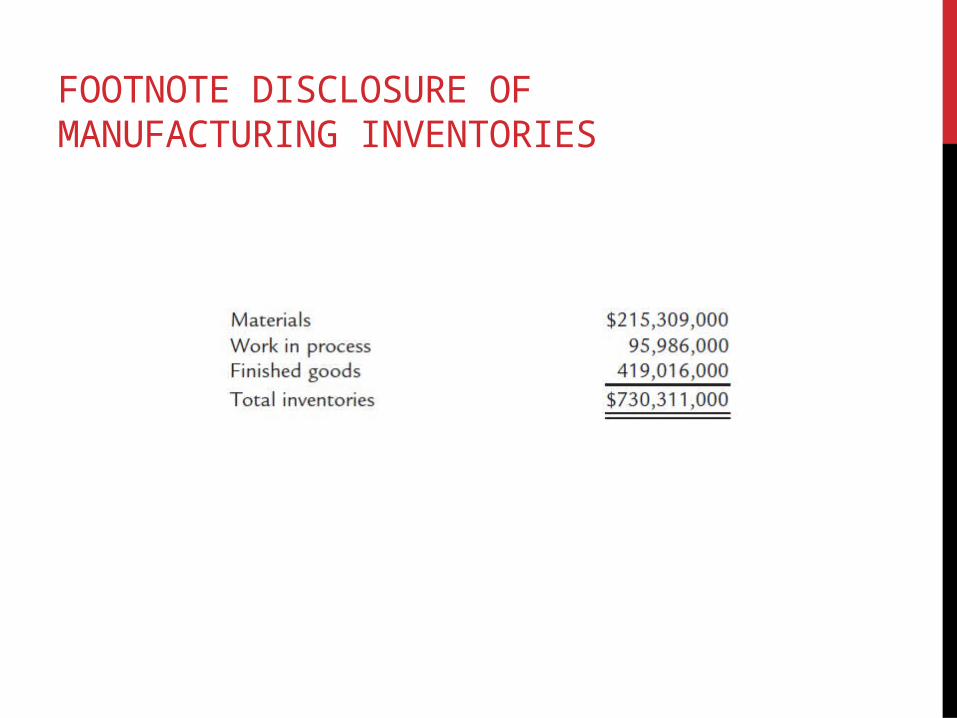

Manufacturers-• Every manufacturer has 3 classifications of Inventory

• Materials• Work in Progress• Finished Goods

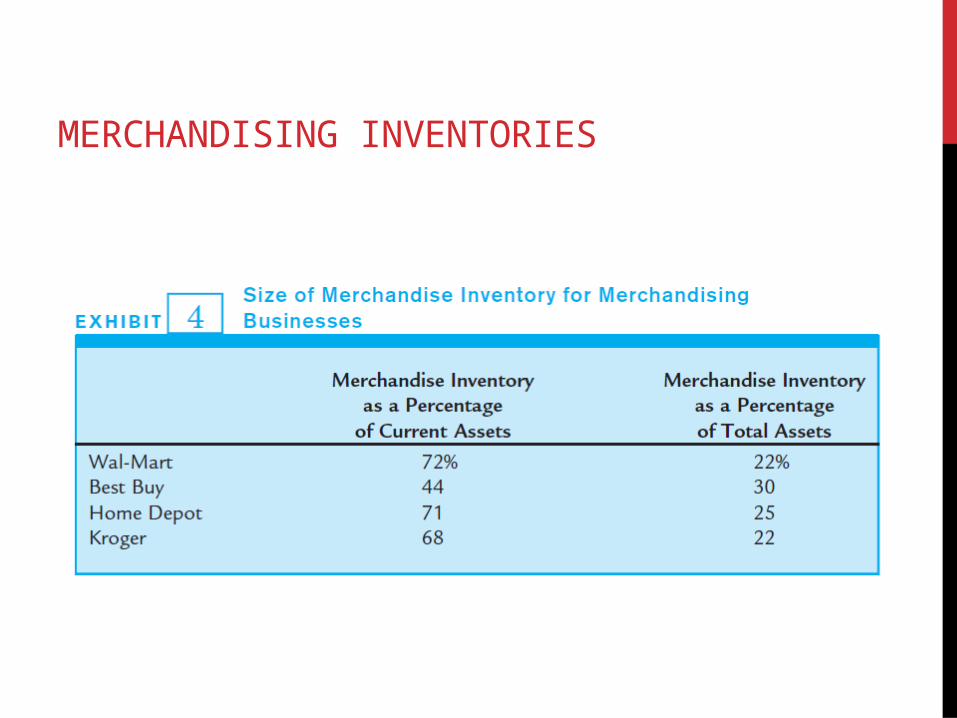

MERCHANDISING INVENTORIES

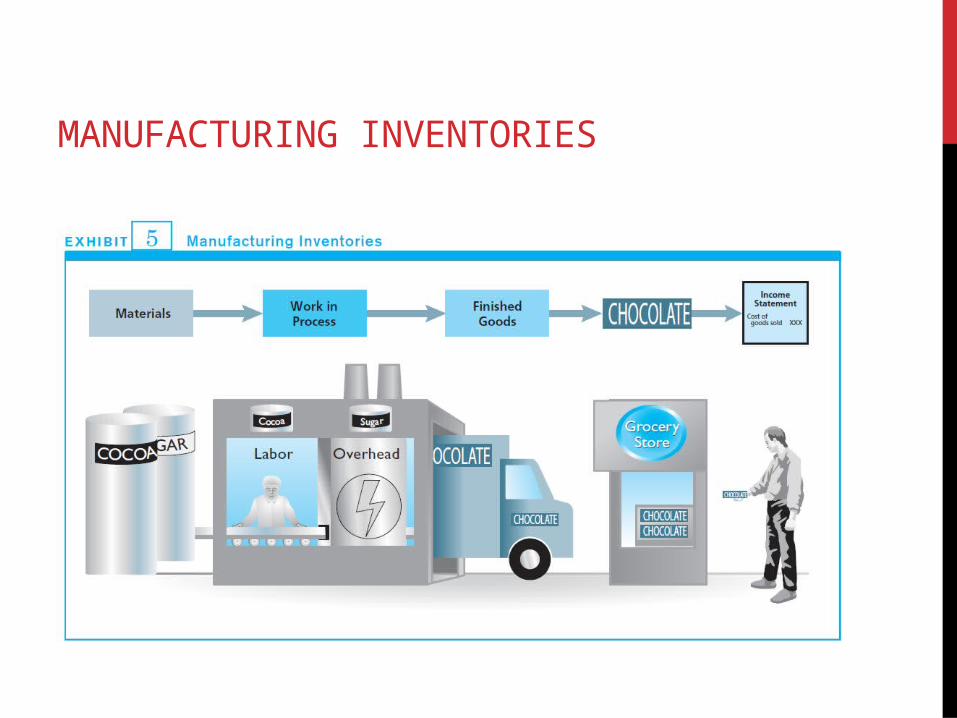

MANUFACTURING INVENTORIES

FOOTNOTE DISCLOSURE OF MANUFACTURING INVENTORIES

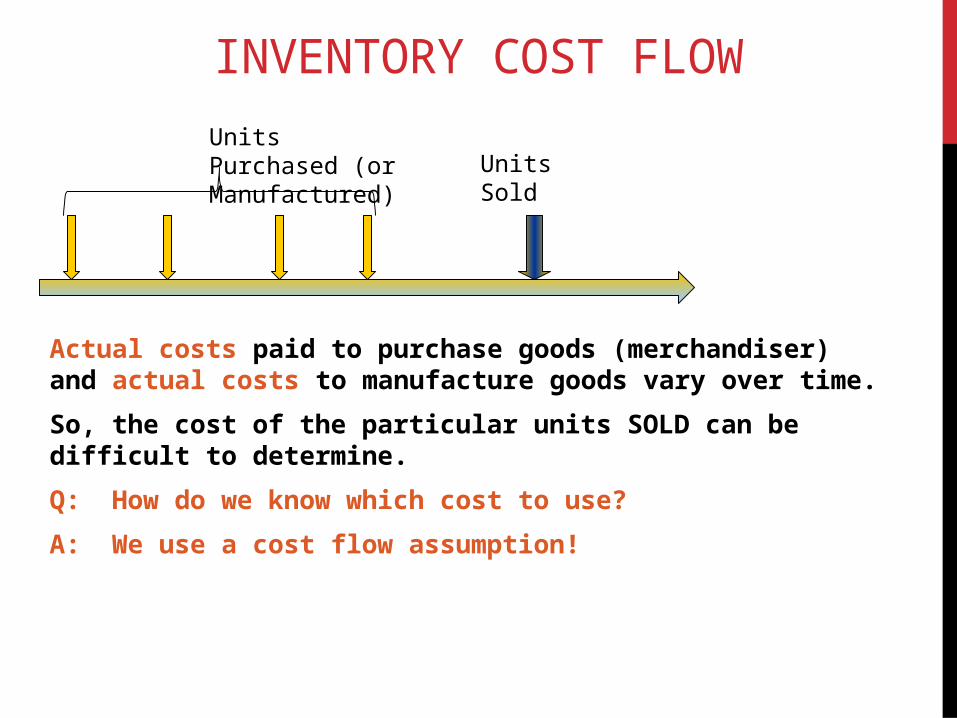

INVENTORY COST FLOW

Actual costs paid to purchase goods (merchandiser) and actual costs to manufacture goods vary over time.

So, the cost of the particular units SOLD can be difficult to determine.

Q: How do we know which cost to use?

A: We use a cost flow assumption!

Units Purchased (or Manufactured) Units Sold

SPECIFIC IDENTIFICATION

If the merchandise can be easily tied to a specific purchase, the specific identification method can be used.

Cost of each unit of merchandise is determined by looking at the purchase price of that particular unit.

Only works if there is a unique characteristic of each item that makes it identifiable

• Example: VIN for an automobile

Specific Identification is not a widely used method for valuing inventory!

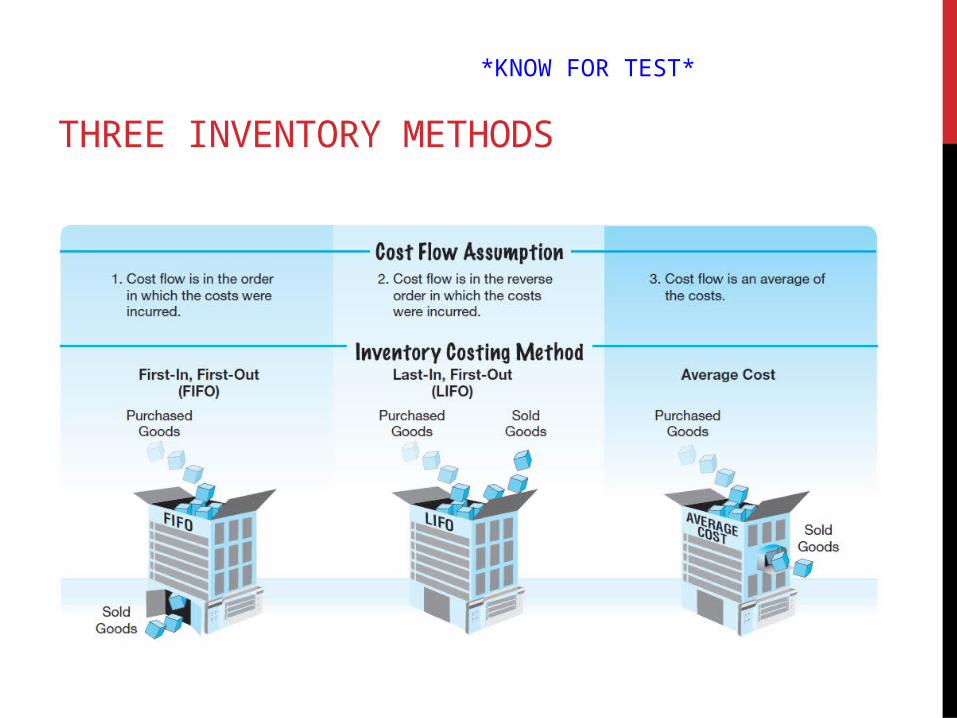

THREE INVENTORY METHODS

*KNOW FOR TEST*

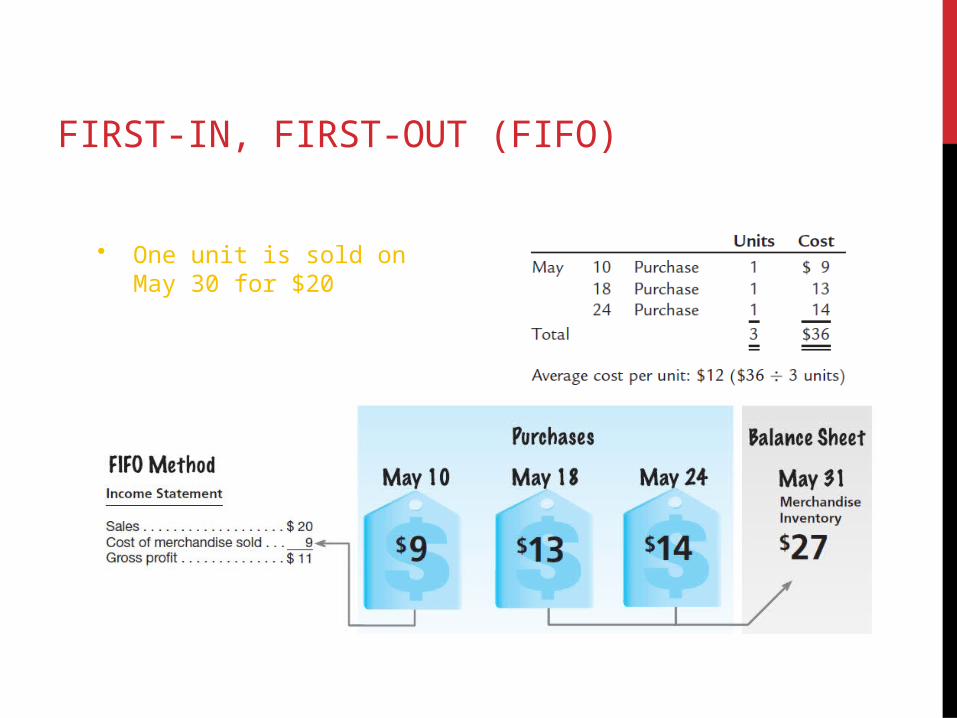

FIRST-IN, FIRST-OUT (FIFO)

• One unit is sold on May 30 for $20

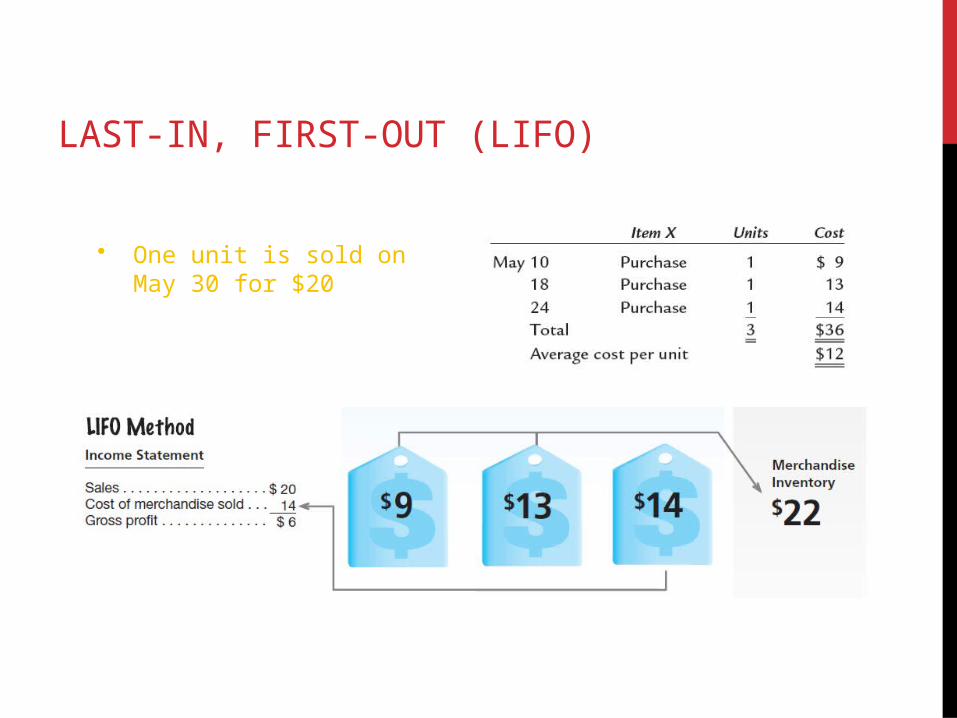

LAST-IN, FIRST-OUT (LIFO)

• One unit is sold on May 30 for $20

AVERAGE COST

• One unit is sold on May 30 for $20

31

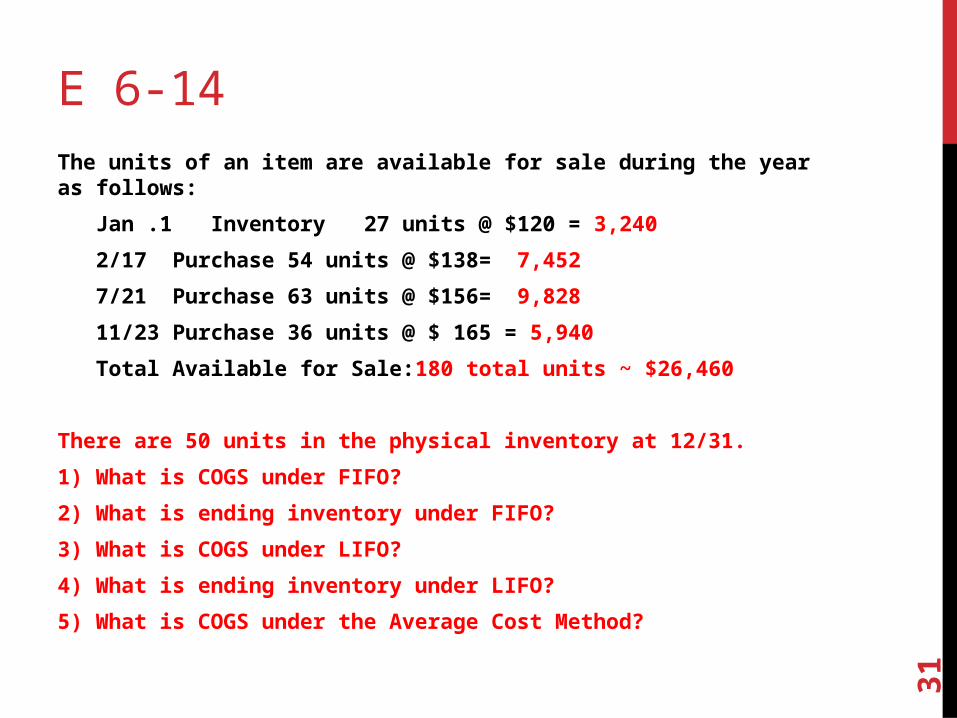

E 6-14The units of an item are available for sale during the year as follows:

Jan .1 Inventory 27 units @ $120 = 3,240

2/17 Purchase 54 units @ $138= 7,452

7/21 Purchase 63 units @ $156= 9,828

11/23 Purchase 36 units @ $ 165 = 5,940

Total Available for Sale:180 total units ~ $26,460

There are 50 units in the physical inventory at 12/31.

1) What is COGS under FIFO?

2) What is ending inventory under FIFO?

3) What is COGS under LIFO?

4) What is ending inventory under LIFO?

5) What is COGS under the Average Cost Method?

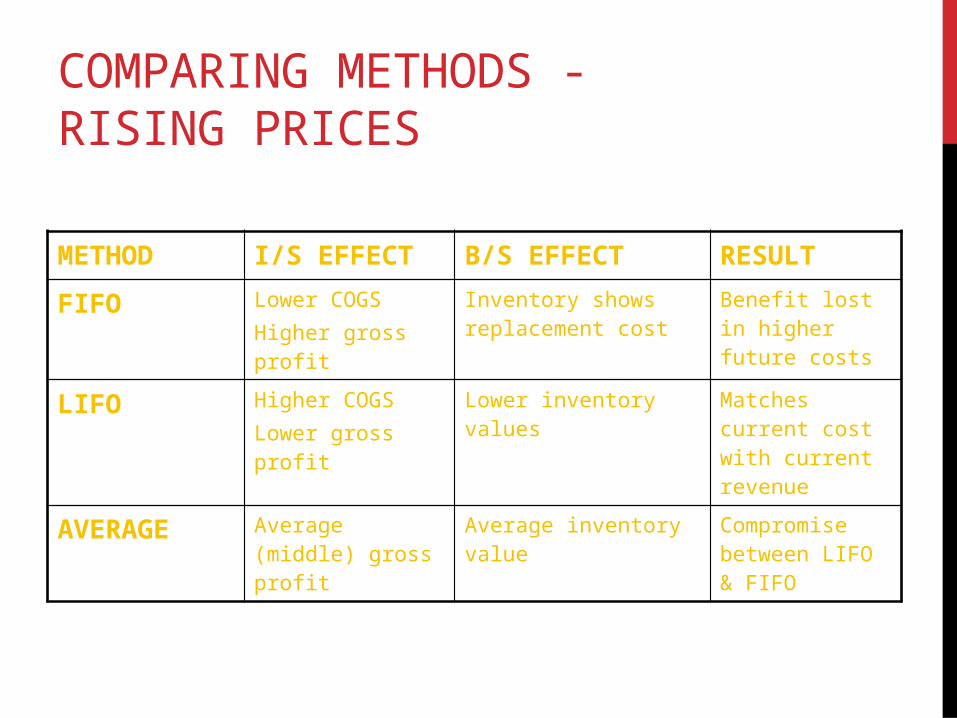

COMPARING METHODS - RISING PRICES

METHOD I/S EFFECT B/S EFFECT RESULT

FIFO Lower COGSHigher gross profit

Inventory shows replacement cost

Benefit lost in higher future costs

LIFO Higher COGSLower gross profit

Lower inventory values Matches current cost with current revenue

AVERAGE Average (middle) gross profit

Average inventory value Compromise between LIFO & FIFO

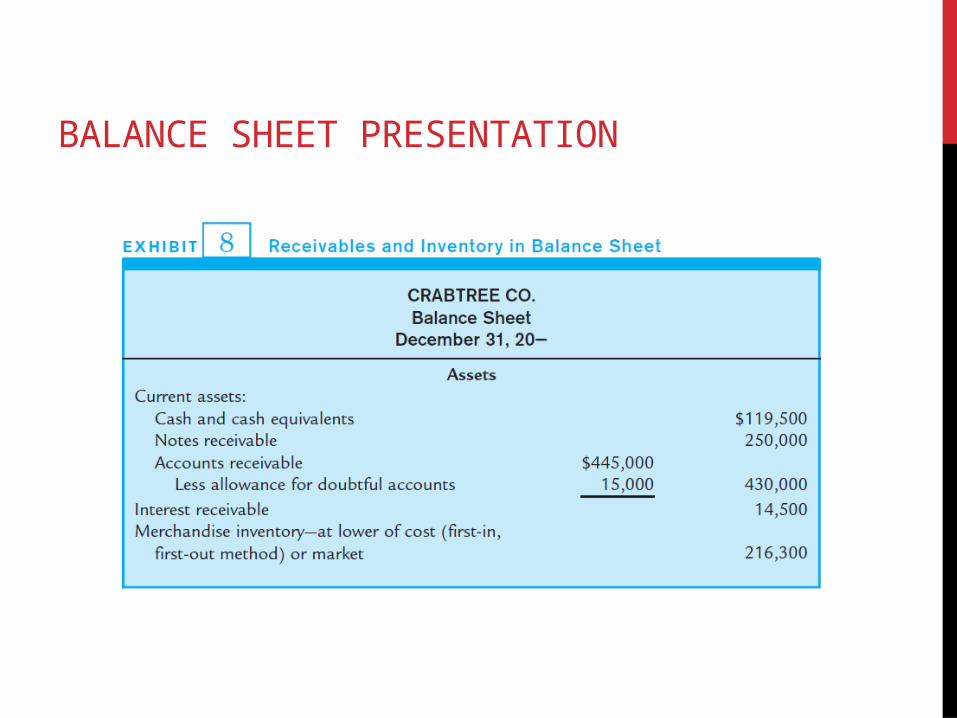

BALANCE SHEET PRESENTATION

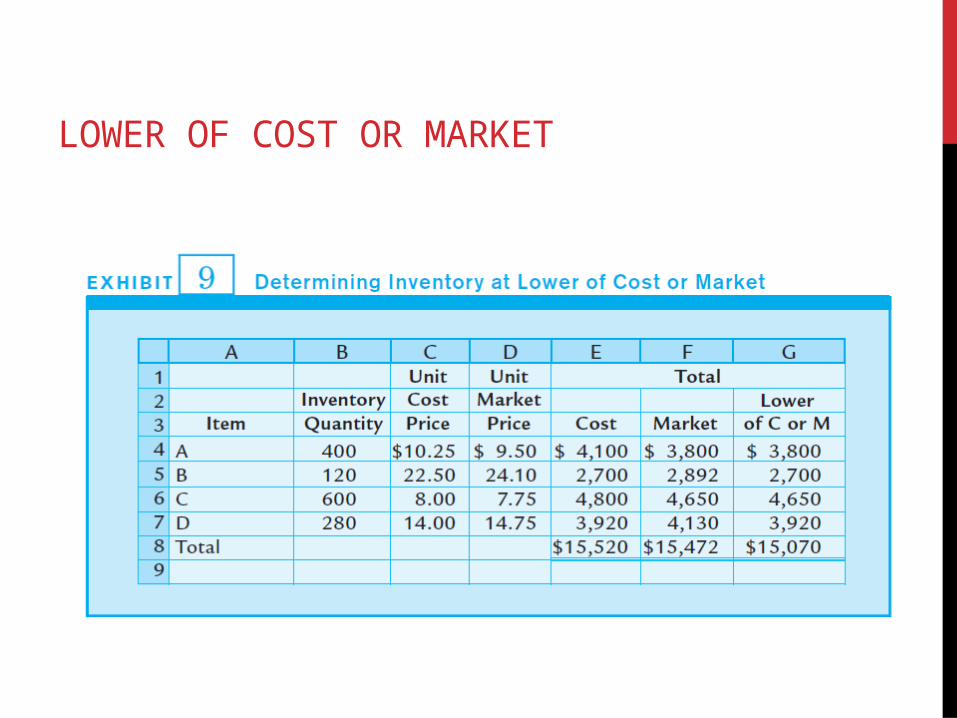

LOWER OF COST OR MARKET

REPORTING RECEIVABLES AND INVENTORY

Accounts Receivable

• Classified as a current asset if collection is expected within 1 year.

• Reported at net realizable value: A/R – Allowance for Doubtful Accounts

Inventory

• Reported at the net realizable value• Net realizable value = selling price – direct costs of disposal• Reported at Lower of Cost or Market (LCM)

Related Documents